G R E A T R I V E R E N E R G Y 2 0 1 3

59

GREAT RIVER ENERGY 2013 ANNUAL REPORT

Transcript of G R E A T R I V E R E N E R G Y 2 0 1 3

G R E A T R I V E R E N E R G Y 2 0 1 3

A N N U A L R E P O R T

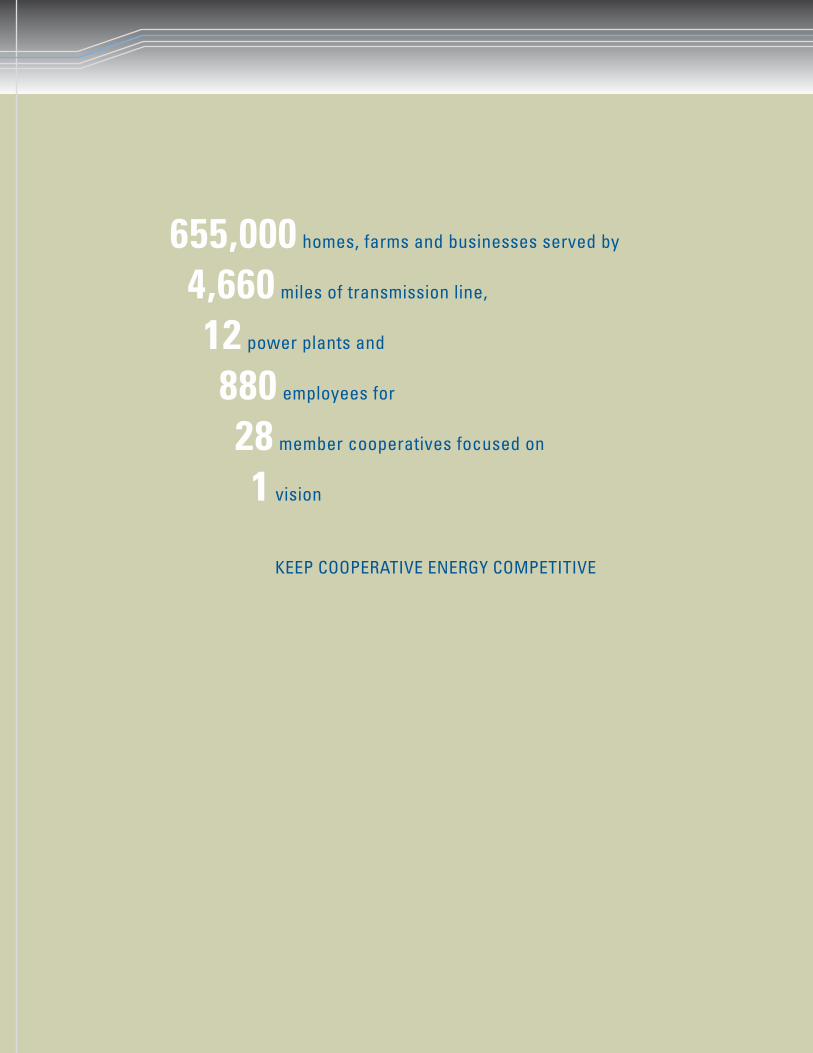

655,000 homes, farms and businesses served by

4,660 miles of transmission line,

12 power plants and

880 employees for

28 member cooperatives focused on

1 vision

KEEP COOPERATIVE ENERGY COMPETITIVE

C O N T E N T S

Letter to stakeholders . . . . . . . . . . . . . . . . . . . . . . . . . . 2

About Great River Energy . . . . . . . . . . . . . . . . . . . . . . 4

Reliable resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Generation: Energy that never stops . . . . . . . . . . . . 8

Transmission: Wired to serve . . . . . . . . . . . . . . . . . . 12

Members: Partners in power . . . . . . . . . . . . . . . . . . 16

2013 financial report . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Management and board of directors . . . . . . . . . . . 56

During periods of uncertainty, a company can choose to wait for clarity or take action.

Great River Energy has thrived in recent years because we have discovered opportunities within the challenges facing our industry. We are beginning to see returns from actions taken, and we continue to enact strategies to improve our position in the future.

The challenges facing our industry have not changed. But, together with our member

cooperatives, Great River Energy enters 2014 better prepared to face them.

In many ways, 2013 was among the best financial years in our history. Our margin exceeded budget by more than $10 million, and we were able to budget for no rate increase in 2014.

Our success was the result of the prudent strategies we adopted in response to a trend of flat energy sales over the previous five years. Among the most significant actions were our reduced capital spending plans and heightened focus on reducing

Michael Thorson

Great River Energy Board Chair

David Saggau

Great River Energy President and CEO

EFFICIENT POWER GENERATION

RELIABLE TRANSMISSION

STRONG FINANCES

L E T T E R T O S TA K E H O L D E R S

2

expenses in our daily operations. Those savings are reinforced through our business improvement program, which systematically encourages employees to pursue efficiencies in their work.

Great River Energy’s board of directors and company leaders understand that the strategies that helped us in recent years will not be enough to keep us competitive in the years ahead. That is why we have already taken actions to improve our position in the future.

Our board of directors passed a resolution in July to mitigate business risk associated with pending greenhouse gas regulations. That resolution resulted in immediate actions, including accelerating the depreciation of Great River Energy’s Coal Creek Station and Stanton Station. The resolution also charged Great River Energy with engaging in the development of the regulations to minimize rate impacts and ensure reliable electric service.

Although there are still uncertainties ahead of us, we are seeking clarity through engagement. This fall, we invited several of our external stakeholders to Great River Energy to discuss our business and the challenges we are facing, and to understand their views on pressing issues. By welcoming the perspectives of end-use consumers, financial institutions, low-income advocates and environmental nonprofit organizations, we gained valuable insight into the priorities of those with a vested interest in cooperative electricity in Minnesota.

We are determined to act strategically in the best interests of our members, and not

to wait for outside forces to dictate our decisions. As regulatory proposals are discussed, we are analyzing potential effects on our business and working with a variety of organizations to collaborate on solutions to further the position of Great River Energy and our member cooperatives. While we monitor and influence what lies ahead for our industry, we are also taking action to thrive in the current environment.

The positive results of the past year are not an end result. They are a signal of positive progress and a step toward our mission to continue providing members with reliable energy at affordable rates in harmony with a sustainable environment.

Fifteen years ago, two generation and transmission cooperatives looked far into the future and recognized that they could be better united than apart, so they formed Great River Energy. That same culture of long-term thinking continues to exist at Great River Energy to this day.

The men and women who care for our generation and transmission resources have the training and experience to maintain our system to exacting standards, while working safely. Our member cooperatives and board of directors have the confidence and motivation to improve our operations and financial performance.

Great River Energy exists because our two predecessor companies recognized a better way to achieve their goal of providing reliable, low-cost power to their member distribution cooperatives. Our success in 2013 is the result of a continued focus on that same goal.

Our margin exceeded budget by more than $10 million, and we were able to budget for no rate increase in 2014.

3

GREAT RIVER ENERGY IS A NOT-FOR-PROFIT COOPERATIVE

WHICH PROVIDES WHOLESALE ELECTRIC SERVICE TO

28 DISTRIBUTION COOPERATIVES IN MINNESOTA AND

WISCONSIN. THOSE MEMBER COOPERATIVES DISTRIBUTE

ELECTRICITY TO APPROXIMATELY 655,000 MEMBER

ACCOUNTS – OR ABOUT 1.7 MILLION PEOPLE. WITH

$3.7 BILLION IN ASSETS, GREAT RIVER ENERGY IS THE

SECOND LARGEST ELECTRIC POWER SUPPLIER IN

MINNESOTA AND ONE OF THE LARGEST GENERATION AND

TRANSMISSION COOPERATIVES IN THE UNITED

STATES. GREAT RIVER

ENERGY’S MEMBER

COOPERATIVES RANGE

FROM THOSE IN THE OUTER-

RING SUBURBS OF THE TWIN CITIES

TO THE ARROWHEAD REGION OF

MINNESOTA TO THE FARMLAND OF

SOUTHWESTERN MINNESOTA. GREAT

RIVER ENERGY’S LARGEST DISTRIBUTION

COOPERATIVE SERVES MORE THAN 125,000

MEMBER-CONSUMERS; THE SMALLEST

SERVES ABOUT 2,500. LEARN MORE AT

GREATRIVERENERGY.COM.

OUR MEMBER COOPERATIVES

A B O U T G R E AT R I V E R E N E R G Y

4

Member Cooperative Summary

Number of member accounts . . . . . . . . . 655,000

Sales to members . . . . . 12,105,295 megawatt hours

Total distribution line . . 88,000 miles

Average density 7.5 consumers/mile

Distribution substations . . . . . . . . 553

Combined annual revenue . . . . . . . . . . . . . . $1.35 billion

Electric plant in service (net) . . . . . . . . . . . $1.9 billion

Average kilowatt hours per account . . . . . . . . . 18,000/year

Distribution employees . . . . . . 1,575

Great River Energy 2013

Financial Highlights

Revenue . . . . . . . . . . . $980.4 million

Total assets . . . . . . . . . . . $3.7 billion

Utility plant investment (net) . . . . . . . . $2.7 billion

Long-term obligations, including current maturities . . . . . . $2.7 billion

Systemwide Load

Characteristics*

Residential . . . . . . . . . . . . . . . . . 55.6%

Seasonal . . . . . . . . . . . . . . . . . . . . 1.6%

Commercial, industrial and other . . . . . . . . . . . . . . . . . . 42.8%

*Based on energy sales

5

Coal Creek StationLocation: Underwood, N.D.Generating capability: 1,142 MWStart of operation: Unit 1, 1979; Unit 2, 1980Fuel: Lignite coal and DryFineTM

lignite coal

Elk River Energy Recovery StationLocation: Elk River, MinnesotaGenerating capability: 31 MWStart of operation: Units 1 & 2, 1951; Unit 3, 1959Fuel: Refuse-derived fuel

Stanton StationLocation: Stanton, N.D.Generating capability: 187 MWStart of operation: Unit 1, 1966; Unit 10, 1982Fuel: Powder River Basin coal

Lakefield Junction StationLocation: Martin County, MinnesotaGenerating capability: 522 MW (summer)Start of operation: 2001Fuel: Natural gas; backup, fuel oil

GENERATION

2

1 4

7

Spiritwood StationLocation: Jamestown, N.D.Generating capability: 99 MW Start of operation: November 2014Fuel: DryFine lignite coal

3

345 kV 75 mi500 kV 70 mi±400 kilovolt (kV) DC 436 mi

PROVIDING DEPENDABLE

WHOLESALE ELECTRICITY TO

GREAT RIVER ENERGY’S

MEMBER COOPERATIVES

REQUIRES A WELL

MAINTAINED AND FLEXIBLE

RESOURCE PORTFOLIO THAT

INCLUDES GENERATION

FACILITIES OF A VARIETY OF

SIZES AND FUEL TYPES AND A

WIDESPREAD NETWORK OF

TRANSMISSION LINES.

GREAT RIVER ENERGY

MAINTAINS 4,660 MILES OF

TRANSMISSION LINE AND

OWNS OR PARTIALLY OWNS 102

TRANSMISSION SUBSTATIONS.

R E L I A B L E R E S O U R C E S

TRANSMISSION

6

Arrowhead Emergency Generation StationLocation: Cook County, MinnesotaGenerating capability: 18 MWFuel: Fuel oil

Trimont WindPurchase: 100 MW (nameplate) Turbine: 67 General Electric 1.5-MW wind turbines

Elm Creek WindPurchase: 99 MW (nameplate) Turbine: 66 General Electric 1.5-MW wind turbines

Prairie Star WindPurchase: 101 MW (nameplate) Turbine: 61 Vestas 1.65-MW wind turbines

Ashtabula II WindPurchase: 51 MW (nameplate) Turbine: 34 General Electric 1.5-MW wind turbines

Endeavor I WindPurchase: 100 MW (nameplate) Turbine: 40 Clipper 2.5-MW wind turbines

St. Bonifacius StationLocation: St. Bonifacius, MinnesotaGenerating capability: 56 MW (summer) Fuel: Fuel oil

Rock Lake StationLocation: Pine City, Minnesota Generating capability: 19 MW (summer) Fuel: Fuel oil

Maple Lake StationLocation: Maple Lake, Minnesota Generating capability: 19 MW (summer)Fuel: Fuel oil

Elk River Peaking StationLocation: Elk River, MinnesotaGenerating capability: 185 MW* (summer)Start of operation: 2009Fuel: Natural gas; backup, fuel oil

Cambridge StationLocation: Cambridge, Minnesota Generating capability: 177 MW* (summer)Start of operation: 2007Fuel: Fuel oil (Unit 1), and natural gas (Unit 2)

Pleasant Valley StationLocation: Mower County, MinnesotaGenerating capability: 408 MW (summer)Start of operation: Units 11 & 12, 2001; Unit 13, 2002Fuel: Natural gas; backup, fuel oil

5 6

8

9

OTHER ASSETSBlue Flint EthanolBlue Flint Ethanol is a biorefinery that uses process steam from the nearby Coal Creek Station power plant to produce 65 million gallons of ethanol per year.

Elk River Resource Processing PlantMunicipal solid waste is processed to create refuse-derived fuel (RDF) for powering Great River Energy’s Elk River Energy Recovery Station. Up to 300,000 tons of waste is transformed into RDF each year.

Other wind energy purchases: 17 MW (nameplate) from four Minnesota wind farms.Location: Jackson, Dodge and Murray counties.

Generating capability based on Summer Net Dependable Capacity per NERC Generating Availability Data System for the 2014 - 2015 planning year.*Based on the 2013 - 2014 planning year.

69 kV or less 3,024 mi115 kV 468 mi161 kV 46 mi230 kV 523 mi

10

11

13

14

15

16

17

12

7

Great River Energy’s peaking plants are meticulously maintained so they are ready to produce electricity immediately when demand increases. Peaking Plant Operator Tech Kevin Beske performs maintenance checks at Pleasant Valley Station near Dexter, Minnesota.

Flexible generation resources, dependable fuel supplies, second-to-none maintenance and an ever-present focus on the safety of employees and members add up to the quality of service Great River Energy provides for its member cooperatives.

ENERGY THAT NEVER STOPS

8

uilt on a foundation of two workhorse coal-based power plants complemented by peaking stations and widespread renewable resources, Great River Energy’s generation portfolio has been crafted over decades for reliability, affordability and environmental performance. Each source is important to meet demand for electricity while producing revenue for Great River Energy and its member cooperatives.

Over the past five years, Great River Energy’s coal-based resources have been available to generate electricity nearly 93 percent of every year, which consistently exceeds the averages of other power plants in the region.

Such remarkable plant performance is due to the diligent maintenance performed by Great River Energy employees. In 2013, one of the two units at Great River Energy’s Coal Creek Station power plant successfully completed a major scheduled outage to perform preventive maintenance, inspections and repairs. Taking a plant offline at regular intervals to perform maintenance is vital to ensure that the plant continues to operate reliably.

Bright future for renewable resourcesThe Elk River Resource Recovery Project consists of two facilities: one that processes municipal solid waste to create a burnable fuel and a power plant that produces renewable energy from the resulting refuse-derived fuel. Great River

Energy renewed its contract with Hennepin County to receive up to 100,000 tons of solid waste for the next five and a half years to supply fuel to the facilities.

The contract ensures a dependable supply of waste, allowing the entire project to operate efficiently. The project generates revenue for Great River Energy by selling steel, aluminum and other valuable materials removed from the waste for recycling, and by selling electricity into the market.

Great River Energy signed a 200-megawatt seasonal diversity exchange with Manitoba Hydro of Winnipeg, extending a 150-megawatt arrangement that has been in place between the two utilities since 1995. The diversity exchange means Manitoba Hydro will provide 200 megawatts of renewable hydroelectric capacity to Great River Energy in the summer to meet its energy needs, while Great River Energy will provide Manitoba Hydro with 200 megawatts of capacity during the winter. Each utility receives the additional energy during its peak period of the year. The new agreement runs until 2030.

New solar panels will be installed next to the Great River Energy headquarters

B

9

Great River Energy’s power supply portfolio consists of a diverse mix of energy sources.

The Elk River Resource Processing Plant uses specialized equipment to pull steel and aluminum out of household garbage to be recycled. Each year, the facility removes 9,000 tons of steel – roughly as much as the Eiffel Tower – and 1,500 tons of aluminum – the equivalent of 100 million pop cans.

facility in Maple Grove, Minnesota, in 2014 and throughout the organization’s service area through 2015. The first construction project is a 250 kilowatt solar array slated for land south of Great River Energy’s headquarters facility and will include a mix of technologies to help determine how small solar energy installations can be integrated into cooperative systems.

Great River Energy is working with its member cooperatives to identify potential sites for 20 kilowatt solar installations in their communities.

Progress through researchAt any given time, Great River Energy is involved in several research projects at its generation facilities. The projects range from studies aimed at reducing emissions of mercury, nitrogen oxides and sulfur dioxide to tests for new maintenance practices. Research helps the cooperative

stay aware of innovations in a rapidly changing industry.

By collaborating with research organizations and other utilities, Great River Energy gains more from its research dollars than it ever could acting alone. These alliances give Great River Energy access to a larger body of knowledge and provide opportunities to develop key contacts. The benefits of research include the DryFining™ technology that was installed at Coal Creek Station in 2009.

Developed with financial assistance from the U.S. Department of Energy, DryFining technology is a lignite coal refining process that has yielded environmental, efficiency and maintenance benefits. In 2013, Great River Energy executed a DryFining License and Technology Transfer Agreement with Tangshan Shenzhou Manufacturing Company to make the technology available to utilities in China.

During the major scheduled maintenance outage at Great River Energy’s Coal Creek Station, welders repair power plant equipment.

10

New ventures keep energy competitiveAside from electricity, Great River Energy’s generation facilities produce a variety of other products and services, ranging from ethanol to corn drying, that increase revenue. In a cooperative business model, that revenue directly offsets plant costs. Revenue from steam, water, ash and other products and services marked 2013 as a record year in value created for the membership to benefit overall member rates.

Located adjacent to Coal Creek Station near Underwood, North Dakota, Blue Flint Ethanol is the first co-located, directly integrated biorefinery in North America – and one of the most cost-effective, energy efficient and environmentally friendly biorefineries in the country. By purchasing steam from Great River Energy, Blue Flint Ethanol saved initial capital by not building a gas-fired boiler. The flexible steam supply also contributes other annual operating benefits while Great River Energy enjoys the steam sales revenue.

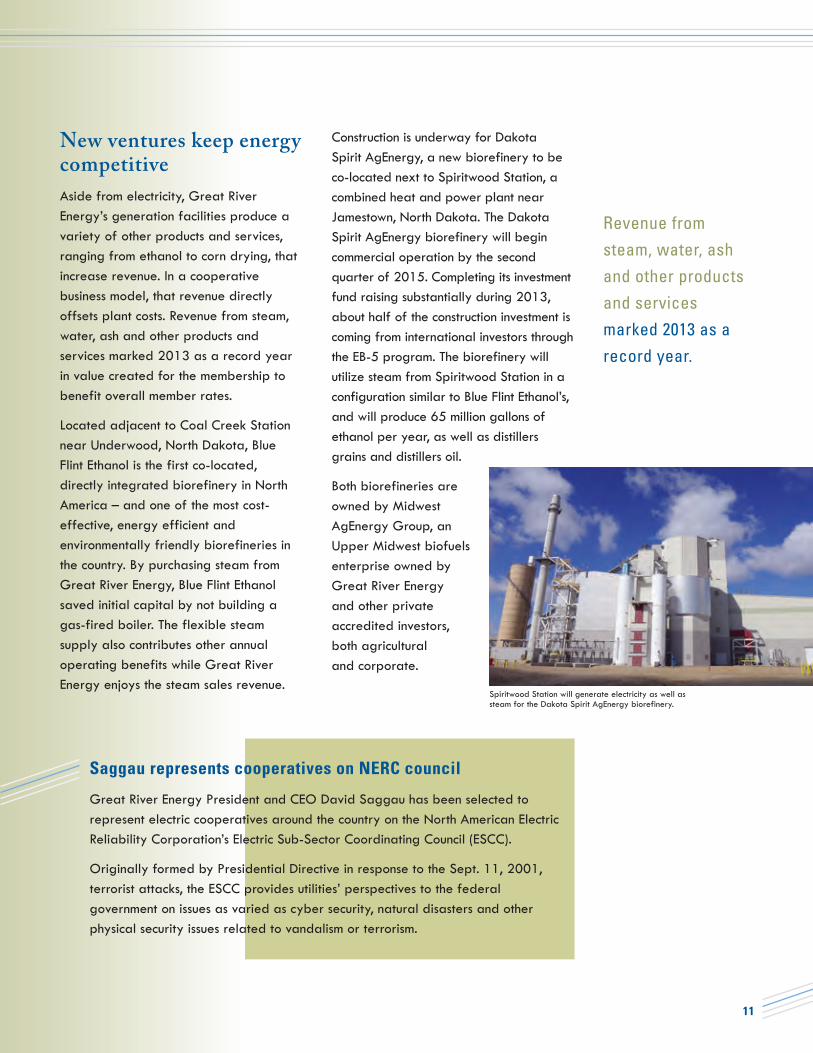

Construction is underway for Dakota Spirit AgEnergy, a new biorefinery to be co-located next to Spiritwood Station, a combined heat and power plant near Jamestown, North Dakota. The Dakota Spirit AgEnergy biorefinery will begin commercial operation by the second quarter of 2015. Completing its investment fund raising substantially during 2013, about half of the construction investment is coming from international investors through the EB-5 program. The biorefinery will utilize steam from Spiritwood Station in a configuration similar to Blue Flint Ethanol’s, and will produce 65 million gallons of ethanol per year, as well as distillers grains and distillers oil.

Both biorefineries are owned by Midwest AgEnergy Group, an Upper Midwest biofuels enterprise owned by Great River Energy and other private accredited investors, both agricultural and corporate.

Spiritwood Station will generate electricity as well as steam for the Dakota Spirit AgEnergy biorefinery.

11

Revenue from steam, water, ash and other products and services marked 2013 as a record year.

Saggau represents cooperatives on NERC council

Great River Energy President and CEO David Saggau has been selected to represent electric cooperatives around the country on the North American Electric Reliability Corporation’s Electric Sub-Sector Coordinating Council (ESCC).

Originally formed by Presidential Directive in response to the Sept. 11, 2001, terrorist attacks, the ESCC provides utilities’ perspectives to the federal government on issues as varied as cyber security, natural disasters and other physical security issues related to vandalism or terrorism.

Through carefully constructed and maintained transmission resources, Great River Energy and its member cooperatives consistently deliver exactly the right amount of power to farms, factories and families.

WIRED TO SERVE

Great River Energy Line Technician J.R. McGuire works to remove capacitors containing polychlorinated biphenyls, a potentially harmful material, from Dickinson Station near Buffalo, Minnesota.

12

roducing electricity is only the first step in providing reliable service. Great River Energy must also deliver power through its transmission system. Year after year, Great River Energy’s transmission system is highly reliable, and 2013 was no different.

Great River Energy tracks the reliability of its transmission system using industry-standard indices which measure how often outages occur and how long they last. In 2013, Great River Energy recorded about half of the typical number of momentary outages, ranking it among the best years in the cooperative’s history. Momentary outages are those lasting less than one minute.

Two bouts of extreme weather in the first half of the year significantly affected Great River Energy’s year-end results for total outage hours. A major ice storm April 9-11 and a thunderstorm outbreak June 21-22 accounted for about three-quarters of the total outage time in 2013. That said, Great River Energy’s system was extremely reliable.

New lines for new needsDue to northern Minnesota homeowners increasingly converting from propane to electricity for space heating, the electric transmission system in the region has become strained to its limit. The system must be built to handle the periods of highest electricity use, which now occur in the winter.

Two projects are underway to bring relief to the constrained region surrounding

Grand Rapids, Minnesota. A new transmission line will link a much-needed substation to the local grid, while a second enhancement will increase the capacity of approximately 38 miles of an existing 69-kilovolt transmission line.

Advancing grid technologyGreat River Energy and two of its member cooperatives, Lake Region Electric Cooperative of Pelican Rapids, Minnesota, and Minnesota Valley Electric Cooperative of Jordan, Minnesota, have collaborated on a demonstration project to pilot technologies designed to enable future utility programs and services.

After nearly 18 months of development, the completely new “smart grid” systems delivered the business and technical functionality ready for demonstration and testing. The project illustrates the potential business value that Great River Energy and its member cooperatives can gain from using technology to improve meter data management and demand response management.

The three cooperatives will continue working to improve the technology and establish business practices to uncover additional value from the new capabilities.

The project was coordinated by the National Rural Electric Cooperative Association’s Cooperative Research Network and is funded in part by a U.S. Department of Energy grant.

P

13

In 2013, Great River Energy recorded about half of the typical number of momentary transmission outages.

THE BENEFITS OF CapX2020

GENERATION

The new lines will open pathways to centers of high energy use from areas of power generation, including remote areas with strong wind resources. They will also make the energy market work more efficiently.

RELIABILITY

These high-voltage transmission links assure that wide area reliability will be maintained and make the system less susceptible to disturbances.

ECONOMIC DEVELOPMENT

CapX2020 is an approximately $2 billion investment that will create 8,000 jobs during peak construction and $3.9 billion in total economic impact.

Serving the region at largeFor decades, electric utilities built transmission lines to serve only their customers. That changed over the past decade as regional transmission operators were formed as independent, third-party bodies to oversee and grant access to the grid while creating real-time energy markets.

As this evolution occurred, transmission development was needed to foster a more efficient and effective electricity market. These projects are known as regional transmission, and Great River Energy has spent the past several years involved in an extensive buildout of this kind.

Known as CapX2020, these lengthy high-voltage projects are needed to expand electric transmission and ensure continued reliable and affordable service. CapX2020 is a joint initiative of 11 utilities, and Great River Energy is construction lead on the 345-kilovolt, 240-mile transmission line spanning from Brookings County, South Dakota, to Hampton, Minnesota.

Technology speeds up power restorationEvery moment matters when electric service is interrupted to a home or business. Great River Energy and its member cooperatives are testing ways to use technology to boost system reliability by sharing real-time electric grid information.

The cooperatives are piloting a real-time data interface that will allow cooperatives to automate distribution outage processes and reduce restoration time.

The Chub Lake Substation, located in Scott County, Minnesota, is one of two new substations that were needed on the CapX2020 project between Brookings County, South Dakota, and Hampton, Minnesota.

14

A major ice storm in April accounted for a significant portion of total transmission outage time in 2013. Pictured here, crews restore service to a downed transmission line.

As regulatory proposals are discussed, a Great River Energy task force is analyzing potential effects on the business.

15

During the first half of 2014, federal greenhouse gas regulations are being drafted that have the potential to impose new and significant costs on the operations of electric utilities. As a utility that will be affected by the resulting regulations, Great River Energy is determined to be an active participant in their creation.

Anticipating the likely adoption of greenhouse gas regulations, the Great River Energy board of directors passed a resolution enacting a plan to mitigate the risk of the regulations. That resolution resulted in immediate actions, including

accelerating the depreciation of Great River Energy’s Coal Creek Station and Stanton Station. Great River Energy will depreciate these coal-based resources by 2028, which is significantly sooner than previously planned. The resolution also charged Great River Energy with reducing its reliance on coal-based electricity and managing carbon dioxide emissions to 2005 levels.

Great River Energy is also working with a variety of organizations to shape the proposed regulations to minimize their financial impact on Great River Energy and its members.

Engagement during policy discussions

Great River Energy’s Coal Creek Station power plant is located near Underwood, North Dakota, and generates electricity using DryFineTM lignite coal.

Great River Energy remains in tune with the communities it serves, and that applies to the communities where its 28 member distribution cooperatives operate and where Great River Energy has facilities and employees. Cooperatives find ways to foster thriving communities.

PARTNERS IN POWER

16

Great River Energy’s business improvement program encourages employees to streamline practices to keep rates affordable. In 2013, employees discovered an innovative way to correct a deficiency in vital emission control equipment at Coal Creek Station. The solution will save approximately $66 million in future capital spending. The effort involved many employees, including (left to right) Brian Freed, Skip Oberg, Gary Sawicki, Tyler Kinn and Ethan Vaagene.

lectric cooperatives focus on the needs of the communities they serve, and that goes far beyond providing electricity. In fact, this promise is included in the principles that guide all cooperative businesses. The “concern for community” cooperative principle states that while focusing on member needs, cooperatives must work for the sustainable development of the communities they serve.

Healthy communities and strong economies go hand in hand. A 2013 study showed that Great River Energy’s operations to supply wholesale power throughout greater Minnesota have far reaching positive effects on the region’s economy.

In an analysis of the company’s core operations, the University of Minnesota-Duluth found that Great River Energy has an average annual economic impact of more than $1 billion and 4,000 jobs.

Great River Energy and its member cooperatives work closely with the businesses they serve to ensure they can remain competitive by helping them use energy wisely and by offering ways to invest in their operations. Great River Energy often helps cooperatives pursue funding through the U.S. Department of Agriculture’s Rural Economic Development Loan and Grant program as well as other programs.

Cooperatives commended for conservationGreat River Energy has long worked with its member distribution cooperatives to offer programs that encourage end-use members to manage electricity costs through conservation and energy efficiency improvements. Helping members use energy wisely not only reduces their costs, but also contributes toward more efficient, affordable and reliable electric service.

Great River Energy coordinates a portfolio of programs with its members to encourage homeowners and businesses to replace outdated, inefficient equipment with newer, efficient installations. Programs encourage members to pursue efficient alternatives ranging from small upgrades, such as compact fluorescent light bulbs and LED holiday lights, to large installations, such as ground-source heat pumps, variable frequency drives and manufacturing process improvements.

At the end of 2013, Great River Energy received a letter of commendation from the Minnesota Division of Energy Resources for its 28 member cooperatives’ efforts to achieve Minnesota’s Conservation Improvement Program goal. The law calls for every utility in the state to work toward an energy savings goal that is equivalent to 1.5 percent of annual retail energy sales.

E

17

Great River Energy has an average annual economic impact of more than $1 billion and 4,000 jobs.

Doing good in the communityEvery day for two weeks in April, employee groups volunteered their time to help Habitat for Humanity build a new home for a family in need. The home now shelters a single mother and her four children and is served by a Great River Energy member cooperative.

For the fifth consecutive year, Great River Energy was recognized as a member of the Keystone Program, an organization of the Minneapolis Regional Chamber of Commerce that recognizes companies that donate generously to the community.

New equipment at Bismarck State College in North Dakota will help college students while securing a valuable training tool for Great River Energy. In 2013, Great River Energy donated a new power plant training simulator to the college that is equipped with modern computer controls and graphics. The new simulator replaced an existing simulator that Great River Energy donated to the school in 1999. The simulator is used both for student education and to train Great River Energy employees preparing to become control room operators. Great River Energy funded the simulator’s development and installation, while the college houses it and provides training.

Sharing services with membersGreat River Energy and its member cooperatives continually find new ways to share services that save money and generate revenue. Every year, Great River Energy increases the information technology services it provides through agreements with interested member cooperatives and wholly owned subsidiaries.

Rather than hire vendors, Great River Energy and its member cooperatives collaborate on services ranging from ongoing support to short-term projects. These agreements save money and boost the collective knowledge and experience among the cooperatives.

Top honors for healthGreat River Energy’s wellness initiatives landed the cooperative on an elite list of employers: the 2014 Healthiest 100 Workplaces in America. Great River Energy ranked 31st among thousands of entries. This national award recognizes that Great River Energy has achieved remarkable and sustainable success through a broad range of corporate wellness programs and employee wellness initiatives.

18

Great River Energy volunteers spent a dreary April day roofing a Habitat for Humanity house. In all, more than 100 employees worked on the house, which is now home to a family of five.

The Falkirk Mine in central North Dakota provides almost eight million tons of coal to Great River Energy’s Coal Creek Station power plant each year. The machinery and effort required to move the earth above the coal, and the coal itself, is immense. But arguably even more immense is the work that comes after the land has been mined.

Falkirk must return mined land to a diverse productive landscape – at least as productive and diverse as it was before mining started. Before it starts removing dirt, Falkirk conducts extensive surveys of the land to create an accurate record of the original composition and topography.

After reclamation, Falkirk must manage the land for at least 10 years from the initial vegetation seeding. Farmers keep careful records of the yields of reclaimed cropland so that Falkirk is able to show that the land has been returned to an equal or greater state of productivity than it was originally. Only then can the land be released from bond, removed from the permit and turned completely over to private or public land management.

Almost two-thirds of Falkirk’s total permitted acres are used by local farmers for agricultural production or grazing. Falkirk has received numerous state and national awards for its reclamation projects.

Providing energy, respecting nature

19

A North Dakota farmer tends to reclaimed cropland as a Falkirk Mine dragline works in the distance.

Mined land must be returned to a diverse productive landscape – at least as productive and diverse as it was before mining started.

FINANCIAL HIGHLIGHTS . . . . . . . . . . . . . . . . . . . . . . 22

FINANCIAL DISCUSSION AND ANALYSIS . . . . . . 22

MANAGEMENT REPORT . . . . . . . . . . . . . . . . . . . . . . 26

INDEPENDENT AUDITORS’ REPORT . . . . . . . . . . . . 27

CONSOLIDATED BALANCE SHEETS . . . . . . . . . . . . 28

CONSOLIDATED STATEMENTS

OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

CONSOLIDATED STATEMENTS OF

COMPREHENSIVE INCOME . . . . . . . . . . . . . . . . . . . . 31

CONSOLIDATED STATEMENTS OF

CHANGES IN CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . 31

CONSOLIDATED STATEMENTS

OF CASH FLOWS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . 33

MANAGEMENT AND

BOARD OF DIRECTORS . . . . . . . . . . . . . . . . . . . . . . . . 56

C O N T E N T S

20

21

F I N A N C I A L R E P O R T 2 0 1 3

Great River Energy’s 2013 financial results were veryimpressive. Great River Energy exceeded its budgetedmargin of $32.0 million by $10.8 million, deferred memberrevenue of $13.8 million to offset future rates, returned apower cost adjustment (PCA) credit of $10.2 million to itsmembers, improved its equity to capitalization to 15.4percent, well on the way to Great River Energy’s targeted20 percent by 2020, maintained its investment gradecredit ratings, and sustained its strong liquidity. Theseimpressive results include unbudgeted additionaldepreciation related to Coal Creek Station and StantonStation of $10.0 million as the estimated service lives wereshortened to the year 2028. This decision affords GreatRiver Energy flexibility as future operating strategies aredeveloped in these changing times. The results of 2013continue to strengthen Great River Energy’s financialposition and prepare the cooperative for the future.

MARGINSNet margin attributable to Great River Energy for the yearended December 31, 2013, was $42.8 million and includesthe net income from Blue Flint Ethanol LLC (Blue Flint) of$10.0 million and Coal Creek Drying & Storage (CCD&S)of $0.6 million. This compares to a budget of $32.0 millionfor 2013 and actual results of $45.4 million for 2012.Great River Energy’s indenture requires the maintenance ofa margin-for-interest (MFI) ratio of 1.1x in order to issueadditional secured debt. In addition, Great River Energy’sboard of directors targeted a debt service coverage (DSC)ratio of 1.17x when setting member rates for 2013. GreatRiver Energy’s 2013 operations produced an MFI of 1.24xand a DSC of 1.22x.

ELECTRIC REVENUEElectric revenue increased $48.4 million or 5.6 percent to$918.0 million in 2013 from $869.6 million in 2012.Electric revenue from member cooperatives was $835.7million during 2013, an increase of $35.4 million or 4.4percent from $800.3 million in 2012. The member revenueincrease was due to increased member energy anddemand unit sales of 3.0 percent and 1.8 percent,respectively, compared to 2012, and a planned wholesalerate increase. Member revenue was reduced for a PCAcredit of $10.2 million and the deferral of memberrevenue of $13.8 million under regulatory accounting. ThePCA allows Great River Energy to bill or credit differencesbetween actual and budgeted results in MidcontinentIndependent System Operator (MISO) market activity,

22

2 013 2 012 Change

OPERATIONSRevenues $ 980.4 $ 921.2 $ 59.2Purchased Power $ 196.4 $ 167.8 $ 28.6Fuel $ 225.7 $ 217.9 $ 7.8Other Operating Expenses $ 279.9 $ 250.4 $ 29.5Depreciation and Amortization $ 115.6 $ 100.5 $ 15.1Interest Expense $ 134.1 $ 143.8 $ (9.7)Other Income $ 3.4 $ 4.5 $ (1.1)Nonutility Operations, Excluding Variable Interest Entity $ 10.7 $ 0.1 $ 10.6Net Margin Attributable to GRE $ 42.8 $ 45.4 $ (2.6)FINANCIAL POSITIONElectric Plant and Plant Held for Future Use $ 4,079.3 $ 3,994.8 $ 84.5Utility Plant - net $ 2,743.9 $ 2,683.6 $ 60.3Deferred Charges $ 215.9 $ 225.1 $ (9.2)Cash and Cash Equivalents $ 271.6 $ 323.1 $ (51.5)Total Assets $ 3,704.4 $ 3,689.8 $ 14.6Long-term Obligations $ 2,605.8 $ 2,712.1 $ (106.3)Members' Capital $ 487.7 $ 444.8 $ 42.9Equity to Capitalization Ratio 15.4% 13.7% 1.7%

Financial Discussion and Analysis

Financial Highlights(DOLLARS IN MILLIONS)

2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3

900

800

700

600

500

400

300

200

100

0

NON-MEMBERS

MEMBERS

Member Cooperatives/Others

(DOLLARS IN MILLIONS )

ELECTRIC REVENUES BILLED

62

705

76

743

60

768

69

801

82

836

purchased power, non-member revenue, and fuel. The2013 PCA credit was due to the strong performance of allof Great River Energy’s power plants, higher marketenergy prices, and strong member energy unit sales.Electric revenue from non-members increased $13.0 millionor 18.8 percent to $82.3 million in 2013 from $69.3 millionin 2012. This increase in revenue was the result of anincrease in megawatt hour (MWh) sales of 12.5 percentand an increase in average market energy prices for thesesales of 6.3 percent in 2013 compared to 2012.

OTHER OPERATING REVENUEOther operating revenue increased $10.8 million or 20.9percent to $62.4 million in 2013 from $51.6 million in2012 due to increased transmission revenue from both theMISO market and under inter-utility transmissionagreements of $9.1 million and increased revenue fromtipping fees and waste recovery at the Elk River ResourceProcessing Plant of $2.1 million.

OPERATING EXPENSESTotal operating expenses for 2013 were $817.6 million, anincrease of $81.0 million or 11.0 percent from $736.6million in 2012. Purchased power increased $28.6 million or 17.0 percent to$196.4 million in 2013 from $167.8 million in 2012. Theincrease is largely due to purchasing 17.2 percent moreMWhs from the MISO market and increased energypurchases under bilateral contracts, including Genoa 3,during 2013. The average energy price paid increased 7.8percent in 2013 compared to 2012. Great River Energy’sincreased power purchases were primarily the result ofincreased member and non-member MWh sales anddecreased generation from Coal Creek Station (CCS) andStanton Station (Stanton) due to scheduled majormaintenance outages during 2013. There were no scheduledmajor maintenance outages during 2012. These increaseswere partially offset by a decrease in capacity costs forGenoa 3 of $3.6 million in 2013 compared to 2012, dueprimarily to an extended maintenance outage in 2012.Fuel expense increased $7.8 million or 3.6 percent to$225.7 million in 2013 from $217.9 million in 2012. Fuelexpense at CCS increased $5.8 million or 3.6 percent dueto increased mining costs per mined ton and increasedrepairs and maintenance in the mining operation and coalhandling system. Fuel expense at the peaking plantsincreased $4.6 million or 23.4 percent in 2013 comparedto 2012. Peaking generation decreased 12.7 percent in2013 compared to 2012; however, the average naturalgas price paid for the year increased 34.1 percent to$3.70/MMBtu in 2013 compared to $2.76/MMBtu in2012. Fuel expense at Stanton decreased $3.9 million or16.0 percent in 2013 compared to 2012 due to Stantongenerating 18.2 percent fewer MWhs, primarily the resultof the 2013 scheduled major maintenance outage.Operation and maintenance expense increased $27.4million or 12.1 percent to $253.9 million in 2013 from$226.6 million in 2012. As Great River Energy’s

infrastructure continues to age, operation and maintenanceexpense will increase due to increased investment andinflationary increases. Great River Energy maintains itsassets to ensure continued reliability. Great River Energyexpensed $11.2 million in 2013 in outage costs related tothe CCS and Stanton 2013 scheduled major maintenanceoutages. Additionally, as regional transmission projectsowned by others are completed within the MISO territory,Great River Energy’s share of these costs will increase.Great River Energy incurred $3.7 million of additionaltransmission expense related to these projects in 2013compared to 2012. Great River Energy also incurred anadditional $5.8 million in transmission expense to servemember load under inter-utility transmission agreements in2013 compared to 2012.

23

Financial Discussion and AnalysisCONTINUED

Depreciation and amortization increased $15.1 million or15.0 percent to $115.6 million in 2013 from $100.5 millionin 2012. Great River Energy shortened the estimatedservice lives for CCS and Stanton to the year 2028,beginning in July 2013, resulting in additional depreciationof $10.0 million for 2013. Additionally, amortizationincreased $4.0 million in 2013 compared to 2012 due toregulatory accounting for CapX2020 projects as GreatRiver Energy received approval from the Federal EnergyRegulatory Commission (FERC) for incentive-based ratetreatment for these projects. Under incentive-based ratetreatment, Great River Energy expenses in the current yearthe equivalent amount of interest capitalized duringconstruction for these projects and records an offsettingregulatory liability that will be amortized over the usefullife of the related asset.

OTHER INCOME (EXPENSE)Interest expense – net of amounts capitalized decreased$9.7 million or 6.8 percent to $134.1 million in 2013 from$143.8 million in 2012. Interest incurred on Great RiverEnergy’s long-term obligations decreased $5.5 million in2013 compared to 2012 due to a lower averageoutstanding long-term obligations balance. Capitalizedinterest increased $4.2 million in 2013 as construction workin progress increased in 2013 compared to 2012.

Purchased Power 19.7%

Fuel 22.7%

Operation andMaintenance 25.6%

Depreciation andAmortization 11.6%

Property Tax 2.6%

Interest Expense 13.5%

Net Margin Attributable to Great

River Energy 4.3%

2 013 EXPENSES AND MARGINS

Other assets and investments decreased $6.8 million to$289.0 million in 2013 from $295.8 million in 2012. Thisdecrease is primarily the result of a decrease in deferredcharges-financing related of $20.5 million to $97.3 millionin 2013, which is due to annual amortization and adecrease in bond issuance costs of $13.1 million, and theimpact of a favorable market valuation of certainderivative instruments accounted for under regulatoryaccounting of $7.4 million. This decrease is offset by anincrease in deferred charges-other of $11.2 million to$118.6 million in 2013. The increase is due to the deferralof refined coal purchase costs associated with theDryFining lease transaction of $12.0 million and thedeferral of scheduled major outage maintenance costs of$27.1 million, offset by a decrease in the deferred chargesassociated with the postretirement defined benefit pensionand medical plans of $26.1 million. The deferred chargesrelated to the DryFining lease will be recognized intomember rates commensurate with the net benefits of thetransaction. The deferred charges related to the scheduledmajor outage maintenance are amortized over themaintenance cycle period, which is three years for CCS andfour years for Stanton. The deferred charges related to thepostretirement benefit plans adjust each year with theremeasurement of the associated benefit obligations. Current assets decreased $43.1 million to $608.6 million in2013 from $651.7 million in 2012. Cash and cashequivalents decreased $51.5 million to $271.6 million in2013 due to a planned strategy to reduce cash on hand.Other inventory, which consists of corn, ethanol, and relatedinventory at Blue Flint, decreased $11.6 million to $10.8million in 2013 due to Blue Flint holding fewer bushels ofcorn in inventory and at significantly lower prices in 2013compared to 2012. These decreases were offset by anincrease in accounts receivable from members of $19.5million to $146.0 million in 2013. This increase is due tomember energy and demand unit sales increases for themonths of December and November in 2013 compared to2012, and the impact of the PCA in those same months asthere were PCA charges for December and November in2013 compared to PCA credits in 2012.

NONUTILITY OPERATIONSNonutility operating revenue and expense represents theoperations of Blue Flint. Operating income increased$10.1 million to $10.0 million in 2013 from $(0.1) million in 2012 due to a record production year and strong crushmargins per gallon as a result of tight ethanol supplies inthe region in 2013.Income from equity method investments primarily representsGreat River Energy’s share of net income from CCD&S for2013 and 2012.In January 2011, Great River Energy closed on a transactionwith North Dakota Refined Coal LLC (NDRC), and itssubsidiaries for the lease and operation of Great RiverEnergy’s DryFining facility. NDRC represents a variableinterest entity of Great River Energy and is consolidated in thefinancial statements. Great River Energy included in nonutilityoperations in the financial statements the noncontrollinginterest net loss of $16.1 million and $14.5 million for theyears ended December 31, 2013 and 2012, respectively,which represents the net operating results of NDRC.

24

Financial Discussion and AnalysisCONTINUED

MEMBER RATEGreat River Energy’s 2013 member billed rate was 70.4mills/kilowatt hour (kWh) compared to 68.5 mills/kWh in 2012.The increase in member rate was due primarily to a plannedrate increase for 2013; however, the rate was favorablyimpacted by the PCA credit of $10.2 million in 2013.

BALANCE SHEET REVIEWGreat River Energy’s total consolidated assets increased$14.6 million to $3.7 billion in 2013. Utility plant - net increased $60.3 million to $2.7 billion in2013. Utility plant increased $190.4 million due toadditions related to Great River Energy’s investment intransmission projects, including CapX2020, of $140.4million and other generation, general plant, and Falkirkadditions of $50.0 million. Additions were offset by netretirements and depreciation of $130.1 million. Nonutility plant and equipment – net increased $4.2 millionto $62.9 million in 2013 from $58.7 million in 2012 dueprimarily to the commencement of construction activities atDakota Spirit AgEnergy, LLC (DSA).

Non-member 8.2%

Member 84.0%

Nonutility Operations, Excluding Variable Interest Entity 1.1%

Nonoperating 0.4%

Other 6.3%

2 013 REVENUES

2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3

70

60

50

40

30

20

10

0

Excluding WAPA (MILLS PER kWh)

MEMBER AVERAGE RATE PER kWh

60.3 64.0 66.3 68.5 70.4

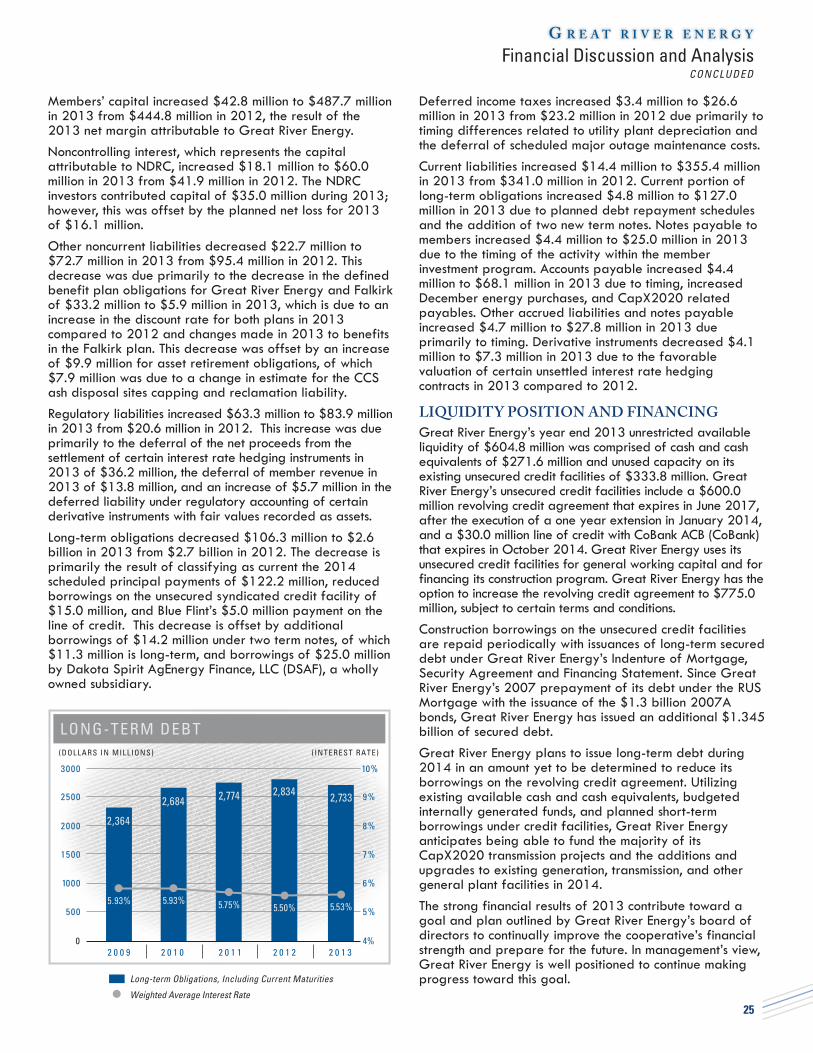

Members’ capital increased $42.8 million to $487.7 millionin 2013 from $444.8 million in 2012, the result of the2013 net margin attributable to Great River Energy.Noncontrolling interest, which represents the capitalattributable to NDRC, increased $18.1 million to $60.0million in 2013 from $41.9 million in 2012. The NDRCinvestors contributed capital of $35.0 million during 2013;however, this was offset by the planned net loss for 2013of $16.1 million.Other noncurrent liabilities decreased $22.7 million to$72.7 million in 2013 from $95.4 million in 2012. Thisdecrease was due primarily to the decrease in the definedbenefit plan obligations for Great River Energy and Falkirkof $33.2 million to $5.9 million in 2013, which is due to anincrease in the discount rate for both plans in 2013compared to 2012 and changes made in 2013 to benefitsin the Falkirk plan. This decrease was offset by an increaseof $9.9 million for asset retirement obligations, of which$7.9 million was due to a change in estimate for the CCSash disposal sites capping and reclamation liability. Regulatory liabilities increased $63.3 million to $83.9 millionin 2013 from $20.6 million in 2012. This increase was dueprimarily to the deferral of the net proceeds from thesettlement of certain interest rate hedging instruments in2013 of $36.2 million, the deferral of member revenue in2013 of $13.8 million, and an increase of $5.7 million in thedeferred liability under regulatory accounting of certainderivative instruments with fair values recorded as assets. Long-term obligations decreased $106.3 million to $2.6billion in 2013 from $2.7 billion in 2012. The decrease isprimarily the result of classifying as current the 2014scheduled principal payments of $122.2 million, reducedborrowings on the unsecured syndicated credit facility of$15.0 million, and Blue Flint’s $5.0 million payment on theline of credit. This decrease is offset by additionalborrowings of $14.2 million under two term notes, of which$11.3 million is long-term, and borrowings of $25.0 millionby Dakota Spirit AgEnergy Finance, LLC (DSAF), a whollyowned subsidiary.

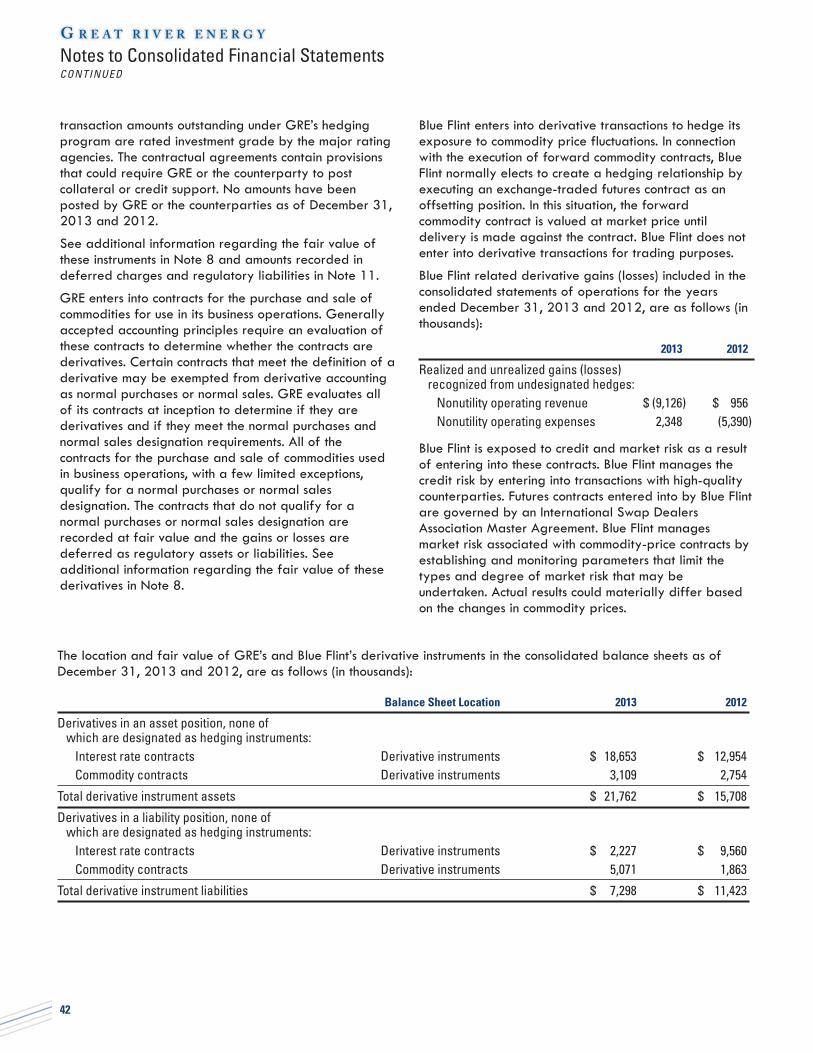

Deferred income taxes increased $3.4 million to $26.6million in 2013 from $23.2 million in 2012 due primarily totiming differences related to utility plant depreciation andthe deferral of scheduled major outage maintenance costs. Current liabilities increased $14.4 million to $355.4 millionin 2013 from $341.0 million in 2012. Current portion oflong-term obligations increased $4.8 million to $127.0million in 2013 due to planned debt repayment schedulesand the addition of two new term notes. Notes payable tomembers increased $4.4 million to $25.0 million in 2013due to the timing of the activity within the memberinvestment program. Accounts payable increased $4.4million to $68.1 million in 2013 due to timing, increasedDecember energy purchases, and CapX2020 relatedpayables. Other accrued liabilities and notes payableincreased $4.7 million to $27.8 million in 2013 dueprimarily to timing. Derivative instruments decreased $4.1million to $7.3 million in 2013 due to the favorablevaluation of certain unsettled interest rate hedgingcontracts in 2013 compared to 2012.

LIQUIDITY POSITION AND FINANCINGGreat River Energy’s year end 2013 unrestricted availableliquidity of $604.8 million was comprised of cash and cashequivalents of $271.6 million and unused capacity on itsexisting unsecured credit facilities of $333.8 million. GreatRiver Energy’s unsecured credit facilities include a $600.0million revolving credit agreement that expires in June 2017,after the execution of a one year extension in January 2014,and a $30.0 million line of credit with CoBank ACB (CoBank)that expires in October 2014. Great River Energy uses itsunsecured credit facilities for general working capital and forfinancing its construction program. Great River Energy has theoption to increase the revolving credit agreement to $775.0million, subject to certain terms and conditions. Construction borrowings on the unsecured credit facilitiesare repaid periodically with issuances of long-term secureddebt under Great River Energy’s Indenture of Mortgage,Security Agreement and Financing Statement. Since GreatRiver Energy’s 2007 prepayment of its debt under the RUSMortgage with the issuance of the $1.3 billion 2007Abonds, Great River Energy has issued an additional $1.345billion of secured debt. Great River Energy plans to issue long-term debt during2014 in an amount yet to be determined to reduce itsborrowings on the revolving credit agreement. Utilizingexisting available cash and cash equivalents, budgetedinternally generated funds, and planned short-termborrowings under credit facilities, Great River Energyanticipates being able to fund the majority of itsCapX2020 transmission projects and the additions andupgrades to existing generation, transmission, and othergeneral plant facilities in 2014.The strong financial results of 2013 contribute toward agoal and plan outlined by Great River Energy’s board ofdirectors to continually improve the cooperative’s financialstrength and prepare for the future. In management’s view,Great River Energy is well positioned to continue makingprogress toward this goal.

25

Financial Discussion and AnalysisCONCLUDED

2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3

3000

2500

2000

1500

1000

500

0

10%

9%

8%

7%

6%

5%

4%

Long-term Obligations, Including Current Maturities

Weighted Average Interest Rate

LONG -TERM DEBT

5.93%

2,364

5.93%

2,684

5.75%

2,774

5.50%

2,834

5.53%

2,733

(DOLLARS IN MILLIONS ) ( INTEREST RATE)

To the Board of Directors and Members of Great River Energy:

Management is responsible for the fairness and accuracy of the financial information presented in this annualreport. The accompanying financial statements have been prepared in accordance with generally acceptedaccounting principles, using management’s best estimates and judgments where appropriate. Great River Energymaintains an internal accounting control system that provides reasonable assurance of the integrity and reliabilityof the financial statements and the protection of assets from loss or unauthorized use or disposition. Directors, whoare not employees, make up the Finance and Audit Committee of the Board of Directors. The committee meetsregularly with management and independent public accountants to review and discuss Great River Energy’sinternal accounting controls and financial reports. The independent public accountants have free access to thecommittee and the Board of Directors, without management present, to discuss the findings of their audits.

David SaggauPresident and CEOGreat River EnergyMaple Grove, MinnesotaMarch 18, 2014

26

Management Report

To the Board of Directors of Great River Energy Maple Grove, Minnesota

We have audited the accompanying consolidated financial statements of Great River Energy (GRE), whichcomprise the consolidated balance sheets as of December 31, 2013 and 2012, and the related consolidatedstatements of operations, comprehensive income, changes in capital, and cash flows for each of the three years inthe period ended December 31, 2013, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements inaccordance with accounting principles generally accepted in the United States of America; this includes the design,implementation, and maintenance of internal control relevant to the preparation and fair presentation ofconsolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We didnot audit the financial statements of Blue Flint Ethanol LLC (Blue Flint), a wholly owned subsidiary, which statementsreflect total assets constituting 1% of consolidated total assets as of December 31, 2013 and 2012, and totalrevenues constituting 16% and 18%, respectively, of consolidated total revenues for the years then ended. Also,we did not audit the financial statements of Blue Flint, GRE’s investment which was accounted for by use of theequity method as of December 31, 2011. GRE’s equity method investment of $23,331,000 in Blue Flint’s net assetsas of December 31, 2011, and of $3,440,000 in Blue Flint’s net income for the year ended December 31, 2011, isincluded in the accompanying consolidated financial statements. Those statements were audited by other auditors,whose report has been furnished to us, and our opinion, in so far as it relates to the amounts included for Blue Flint,is based solely on the report of the other auditors. We conducted our audits in accordance with auditing standardsgenerally accepted in the United States of America. Those standards require that we plan and perform the auditto obtain reasonable assurance about whether the consolidated financial statements are free from materialmisstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in theconsolidated financial statements. The procedures selected depend on the auditor’s judgment, including theassessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to GRE’s preparation and fairpresentation of the consolidated financial statements in order to design audit procedures that are appropriate inthe circumstances, but not for the purpose of expressing an opinion on the effectiveness of GRE’s internal control.Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of significant accounting estimates made by management, as well asevaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinion.

Opinion

In our opinion, based on our audits and the report of the other auditors, the consolidated financial statementsreferred to above present fairly, in all material respects, the financial position of GRE as of December 31, 2013and 2012, and the results of its operations and its cash flows for each of the three years in the period endedDecember 31, 2013, in accordance with accounting principles generally accepted in the United States of America.

Minneapolis, MinnesotaMarch 18, 2014

27

Independent Auditors’ Report

A S S E T S 2 013 2 012

UTILITY PLANT:Electric plant $ 3,653,224 $ 3,569,607Plant held for future use 426,068 425,156Coal mine plant 351,486 352,789Construction work in progress 221,242 134,028Less accumulated depreciation and amortization (1,908,156) (1,798,030)

Utility plant — net 2,743,864 2,683,550

NONUTILITY PLANT AND EQUIPMENT — Net 62,893 58,679

OTHER ASSETS AND INVESTMENTS: Restricted investments — deferred compensation 12,285 10,762Other investments 28,223 27,716Deferred charges — financing related 97,259 117,756Deferred charges — other 118,632 107,393Other long-term assets 29,045 27,477Other long-term receivables:

Members 566 2,151Others — net of allowance for doubtful accounts of $100

for both 2013 and 2012 3,001 2,564

Total other assets and investments 289,011 295,819

CURRENT ASSETS: Cash and cash equivalents 271,610 323,108Accounts receivable:

Members 146,000 126,532Others — net of allowance for doubtful accounts of $535

and $0 for 2013 and 2012, respectively 17,968 18,005Inventories:

Materials and supplies 69,702 72,680Fuel 22,904 23,700Other 10,833 22,435

Prepaids and other current assets 20,672 25,558Derivative instruments 21,762 15,708Deferred income tax benefit 27,182 23,993

Total current assets 608,633 651,719

TOTAL $ 3,704,401 $ 3,689,767

28

Consolidated Balance SheetsAS OF DECEMBER 31 , 2013 AND 2012( IN THOUSANDS)

Continued

L I A B I L I T I E S A N D C A P I TA L 2 013 2 012

CAPITAL:Members:

Patronage capital $ 487,663 $ 444,827Memberships 3 3

Total members’ capital 487,666 444,830Noncontrolling interest 60,043 41,883

Total capital 547,709 486,713

OTHER NONCURRENT LIABILITIES 72,717 95,395

REGULATORY LIABILITIES 83,895 20,586

LONG-TERM OBLIGATIONS — Less current portion 2,605,797 2,712,106

DEFERRED COMPENSATION 12,285 10,762

DEFERRED INCOME TAXES 26,636 23,220

COMMITMENTS AND CONTINGENCIES (Notes 4, 5, and 10)CURRENT LIABILITIES:

Current portion of long-term obligations 126,950 122,141Notes payable to members 24,969 20,562Obligations under line of credit 10,000 10,000Accounts payable 68,057 63,636Property and other taxes 25,228 22,673Other accrued liabilities and notes payable 27,804 23,118Accrued interest payable 65,056 67,432Derivative instruments 7,298 11,423

Total current liabilities 355,362 340,985

TOTAL $ 3,704,401 $ 3,689,767

See notes to consolidated financial statements.

29

Consolidated Balance Sheets

Concluded

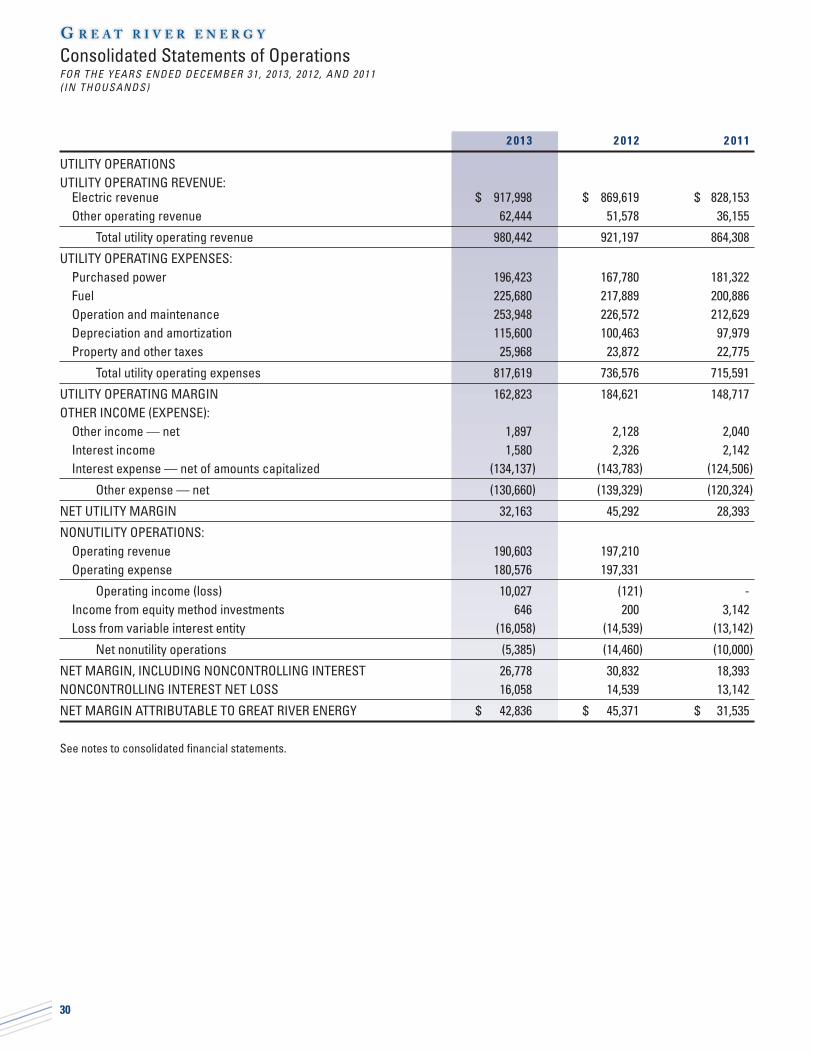

2 013 2 012 2 011

UTILITY OPERATIONSUTILITY OPERATING REVENUE:

Electric revenue $ 917,998 $ 869,619 $ 828,153Other operating revenue 62,444 51,578 36,155

Total utility operating revenue 980,442 921,197 864,308

UTILITY OPERATING EXPENSES:Purchased power 196,423 167,780 181,322Fuel 225,680 217,889 200,886Operation and maintenance 253,948 226,572 212,629Depreciation and amortization 115,600 100,463 97,979Property and other taxes 25,968 23,872 22,775

Total utility operating expenses 817,619 736,576 715,591

UTILITY OPERATING MARGIN 162,823 184,621 148,717OTHER INCOME (EXPENSE):

Other income — net 1,897 2,128 2,040Interest income 1,580 2,326 2,142Interest expense — net of amounts capitalized (134,137) (143,783) (124,506)

Other expense — net (130,660) (139,329) (120,324)

NET UTILITY MARGIN 32,163 45,292 28,393

NONUTILITY OPERATIONS:Operating revenue 190,603 197,210Operating expense 180,576 197,331

Operating income (loss) 10,027 (121) -Income from equity method investments 646 200 3,142Loss from variable interest entity (16,058) (14,539) (13,142)

Net nonutility operations (5,385) (14,460) (10,000)

NET MARGIN, INCLUDING NONCONTROLLING INTEREST 26,778 30,832 18,393NONCONTROLLING INTEREST NET LOSS 16,058 14,539 13,142

NET MARGIN ATTRIBUTABLE TO GREAT RIVER ENERGY $ 42,836 $ 45,371 $ 31,535

See notes to consolidated financial statements.

30

Consolidated Statements of OperationsFOR THE YEARS ENDED DECEMBER 31 , 2013 , 2012 , AND 2011( IN THOUSANDS)

AccumulatedOther

Patronage Comprehensive Noncontrolling TotalCapital Memberships Income (Loss) Interest Capital

BALANCE — January 1, 2011 $ 367,921 $ 3 $ (405) $ - $ 367,519Comprehensive income (loss):

Net margin (loss) 31,535 (13,142) 18,393Change in unrealized loss on interest rate swap —

equity method investment 405 405

Total comprehensive income (loss) 31,535 - 405 (13,142) 18,798Capital contributed by noncontrolling interest 105,930 105,930Capital distributed by noncontrolling interest (13,876) (13,876)

Dividends paid by noncontrolling interest (715) (715)

BALANCE — December 31, 2011 399,456 3 - 78,197 477,656

Net margin (loss) and comprehensive income (loss) 45,371 (14,539) 30,832Capital distributed by noncontrolling interest (21,016) (21,016)Dividends paid by noncontrolling interest (759) (759)

BALANCE — December 31, 2012 444,827 3 - 41,883 486,713Net margin (loss) and comprehensive income (loss) 42,836 (16,058) 26,778Capital contributed by noncontrolling interest 34,989 34,989Dividends paid by noncontrolling interest (771) (771)

BALANCE — December 31, 2013 $ 487,663 $ 3 $ - $ 60,043 $ 547,709

See notes to consolidated financial statements.

31

Consolidated Statements of Changes in CapitalFOR THE YEARS ENDED DECEMBER 31 , 2013 , 2012 , AND 2011

( IN THOUSANDS)

Consolidated Statements of Comprehensive IncomeFOR THE YEARS ENDED DECEMBER 31 , 2013 , 2012 , AND 2011

( IN THOUSANDS)

2 013 2 012 2 011

NET MARGIN, INCLUDING NONCONTROLLING INTEREST $ 26,778 $ 30,832 $ 18,393COMPREHENSIVE INCOME — Change in interest

rate swap valuation — equity method investment 405

COMPREHENSIVE INCOME, INCLUDING NONCONTROLLING INTEREST 26,778 30,832 18,798NONCONTROLLING INTEREST COMPREHENSIVE LOSS 16,058 14,539 13,142

COMPREHENSIVE INCOME ATTRIBUTABLE TO GREAT RIVER ENERGY $ 42,836 $ 45,371 $ 31,940

See notes to consolidated financial statements.

2 013 2 012 2 011

CASH FLOWS FROM OPERATING ACTIVITIES:Net margin, including noncontrolling interest $ 26,778 $ 30,832 $ 18,393Adjustments to reconcile net margin to net cash provided by operating activities:

Depreciation and amortization:Charged to operating expenses 115,600 100,463 97,979Charged to fuel expense and other accounts 30,251 16,958 18,468

Income from equity method investments (646) (200) (2,880)Patronage credits earned from investments (1,205) (906)Deferred charges (39,075) (12,000) (15,670)Regulatory liabilities 13,750Changes in working capital (excluding cash, investments, and borrowings):

Accounts and long-term receivables (17,538) (2,262) 4,401Inventory and other assets 8,737 (26,690) (7,530)Accounts payable, taxes, and other accrued expenses 4,183 (9,492) (11,680)Accrued interest (2,374) (2,355) 2,966Noncurrent liabilities (6,275) 7,772 (3,144)

Net cash provided by operating activities 132,186 102,120 101,303

CASH FLOWS FROM INVESTING ACTIVITIES:Property additions (164,275) (150,745) (144,982)Proceeds from sale of property 348 374 378Purchase transactions and investment in equity method

investments — net of cash acquired of $24,174 in 2012 5,660 (102)Redemption of patronage capital from investments 698 449Purchases of investments (61,230)Proceeds from maturity of investments 60,000 896

Net cash used in investing activities (163,229) (84,262) (205,040)

CASH FLOWS FROM FINANCING ACTIVITIES:Proceeds from issuance of long-term obligations 315,205 120,000 180,475Repayments of long-term obligations (416,726) (127,141) (98,201)Proceeds from interest rate hedging instruments settlement 42,915Costs of new debt issuances, leases, and interest rate hedging instruments (474) (6,445) (10,791)Borrowings on line of credit — net 10,000Notes received from (paid to) members — net 4,407 4,975 (5,258)Capital contributed by noncontrolling interest 34,989 105,930Capital distributed by noncontrolling interest (21,016) (13,876)Dividends paid by noncontrolling interest (771) (759) (715)

Net cash (used in) provided by financing activities (20,455) (20,386) 157,564

NET (DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS (51,498) (2,528) 53,827CASH AND CASH EQUIVALENTS — Beginning of year 323,108 325,636 271,809

CASH AND CASH EQUIVALENTS — End of year $ 271,610 $ 323,108 $ 325,636

See notes to consolidated financial statements.

32

Consolidated Statements of Cash FlowsFOR THE YEARS ENDED DECEMBER 31 , 2013 , 2012 , AND 2011( IN THOUSANDS)

1. ORGANIZATIONORGANIZATION — Great River Energy (GRE) is a Minnesota electric generation and transmission cooperativecorporation providing wholesale electric service to member distribution cooperatives engaged in the retail sale ofelectricity to member consumers in Minnesota and a small section of Wisconsin. This service is provided in accordancewith the terms of the power purchase and transmission service contracts between GRE and the members. These contractshave expiration dates of December 31, 2045, and December 31, 2050, respectively.

BASIS OF ACCOUNTING — The consolidated financial statements are prepared on the accrual basis of accountingand include the accounts of GRE, as well as the following entities:

33

Notes to Consolidated Financial StatementsAS OF DECEMBER 31 , 2013 AND 2012 , AND

FOR THE YEARS ENDED DECEMBER 31 , 2013 , 2012 , AND 2011

YearsEntity Relationship Consolidated

The Falkirk Mining Company (Falkirk) Variable interest entity 2013, 2012, 2011North Dakota Refined Coal LLC (NDRC) Variable interest entity 2013, 2012, 2011

Midwest AgEnergy Group, LLC (MAG) Wholly owned subsidiary 2013Blue Flint Ethanol LLC (Blue Flint) Wholly owned subsidiary 2013, 2012Dakota Spirit AgEnergy Finance, LLC (DSAF) Wholly owned subsidiary 2013Dakota Spirit AgEnergy, LLC (DSA) Wholly owned subsidiary 2013

FALKIRK — GRE has an agreement with Falkirk for thedevelopment and operation of a lignite coal mine. Falkirkis the coal supplier for the Coal Creek Station (CCS),GRE’s steam-generating facility located nearUnderwood, North Dakota. GRE is required to providefinancing for all costs associated with the minedevelopment and operation. Accounting principlesgenerally accepted in the United States of America(“generally accepted accounting principles”) require GREto consolidate its financial statements with Falkirk sinceFalkirk qualifies as a variable interest entity for whichGRE is the primary beneficiary. The coal purchase priceincludes all costs incurred by Falkirk for development andoperation of the mine, including Falkirk’s interest expenseof $3.5 million, $3.9 million, and $4.1 million in 2013,2012, and 2011, respectively; income tax expense of$2.7 million, $3.0 million, and $2.4 million in 2013,2012, and 2011, respectively; and net income of $12.0million, $11.6 million, and $11.3 million in 2013, 2012,and 2011, respectively, all of which are part of thecontract cost of coal purchased under the coal salesagreement. Accordingly, the net effect of consolidatingthe income statement of Falkirk had no impact on GRE’smargin for the years ended December 31, 2013, 2012,and 2011.

Assets and liabilities included in the consolidated balancesheets as of December 31, 2013 and 2012, afterintercompany eliminations, are as follows (in thousands):

2013 2012

Coal mine plant $ 297,855 $ 299,158Construction work in progress 1,582 1,303Accumulated depreciation

and amortization (158,152) (145,710)Deferred charges 10,838 31,680Other long-term assets 6,784 7,436Fuel inventory 5,175 5,404Materials and supplies inventory 21,037 19,284Deferred income tax benefit 546 772Other current assets 323 1,490Other noncurrent liabilities 26,150 47,671Long-term obligations 63,627 78,393Current liabilities 25,791 26,623

Falkirk is a wholly owned subsidiary of the North AmericanCoal Corporation (NACC), which is a wholly ownedsubsidiary of NACCO Industries, Inc. Falkirk is principallyengaged in lignite mining through the operation of asurface mine in North Dakota.

The consolidation of NDRC also includes NDRC’s wholly owned subsidiaries, North Dakota Refined Coal ProjectCompany A LLC and North Dakota Refined Coal Project Company B LLC.

All significant intercompany balances and transactions have been eliminated in consolidation, except for the steamsales between GRE and Blue Flint discussed within Note 1.

NDRC — Beginning on January 21, 2011, GRE has anagreement with NDRC, or its wholly owned subsidiaries, forthe lease and operation of the DryFining facility at CCS.NDRC purchases coal from GRE under fixed pricing,refines the coal in the DryFining facility, and sells therefined coal to GRE under fixed pricing. GRE providescertain other services to NDRC under fee arrangements.The lease and related agreements have a 16-year term;however, included in the participation agreement is apurchase option to buy out the remaining term of thetransaction on January 31, 2020. Generally acceptedaccounting principles require GRE to consolidate itsfinancial statements with NDRC, since NDRC qualifies as avariable interest entity for which GRE is the primarybeneficiary. NDRC entered into an operating andmaintenance agreement with NoDak Energy Services LLC(“NoDak”) to perform the day-to-day operation andmaintenance of the DryFining facility. NoDak qualifies as avariable interest entity for which NDRC is the primarybeneficiary. As a result, GRE is also consolidating NoDakas part of NDRC. The utility fuel operating expense in theconsolidated statements of operations includes a netbenefit to GRE of $11.4 million, $10.1 million and $9.4million for the years ended December 31, 2013, 2012,and 2011, respectively, related to this transaction. Thisincludes the revenue from the lease and other agreementspartially offset by the costs incurred for the purchase ofrefined coal from NDRC. The net loss incurred by NDRC of$16.1 million, $14.5 million, and $13.1 million for theyears ended December 31, 2013, 2012, and 2011,respectively, is reported as nonutility operations in theconsolidated statements of operations.

The agreements include various operational metrics, suchas minimum requirements on the tons of refined coalpurchased by GRE and the achievement of qualifiedemission reductions. In the event that the operationalmetrics are not met over the life of the transaction, GREmay be required to pay specified amounts to NDRC attransaction termination. No liability has been recorded byGRE in the consolidated financial statements related tothese operational metrics as of December 31, 2013 and2012.

Assets and liabilities included in the consolidated balancesheets as of December 31, 2013 and 2012, afterintercompany eliminations, are as follows (in thousands):

2013 2012

Cash $ 4,016 $ 680Prepaids 73 70Current liabilities 234 232

JPM Capital Corporation and WM Refined Coal, LLChold a 55% and 45% membership interest, respectively,in NDRC. NoDak is a wholly owned subsidiary of TRUGlobal Energy Services LLC, a wholly owned subsidiaryof NACC.

BLUE FLINT — Blue Flint operates an ethanol biorefineryfacility located in Underwood, North Dakota. Blue Flint hasa production capacity of approximately 65 million gallonsof undenatured ethanol per year. Blue Flint is a dry-millproduction facility that produces and sells ethanol, dry andmodified distillers grain, and distillers oil.

Prior to 2012, GRE owned 49% of Blue Flint andaccounted for Blue Flint as an equity method investment.On January 1, 2012, GRE purchased the remaining 51%ownership interest in Blue Flint from HES Ethanol Holdings,LLC for a cash purchase price of $18.3 million. As GRE issubject to regulatory accounting, the fair value of GRE’s49% equity interest in Blue Flint was determined to benet book value, as of January 1, 2012, of $23.9 million.The transaction price of $18.3 million was determined tobe fair value for the 51% ownership interest using boththe market and income approaches. GRE did notrecognize any gain or loss related to this transaction.

The recognized amounts of identifiable assets acquiredand liabilities assumed at January 1, 2012, are asfollows (in thousands):

Cash $ 24,174Accounts receivable — net of allowance for

doubtful accounts of $0 5,133Inventory 14,415Other financial assets 3,674Plant and equipment 61,722Financial liabilities (66,938)Total identifiable net assets $ 42,180

The pro forma net margin attributable to GRE wouldhave been $35.9 million for the year ended December31, 2011, had Blue Flint been wholly owned for all yearspresented. Blue Flint’s operating revenue was $187.3million for the year ended December 31, 2011, andwould have been reported as nonutility operations hadBlue Flint been wholly owned for all years presented.

Blue Flint purchases steam and water under a long-termcontract from CCS for use in the production of ethanoland related products. Steam and water purchases were$5.6 million and $5.5 million for the years endedDecember 31, 2013 and 2012, respectively. The sale ofsteam and water by CCS is recorded as utility otheroperating revenue and the purchase by Blue Flint isrecorded as nonutility operating expense. This transactionwas not eliminated in consolidation for 2013 and 2012.

34

Notes to Consolidated Financial StatementsCONTINUED

Notes to Consolidated Financial StatementsCONTINUED

Utility net margin and nonutility operating income (loss) as of December 31, 2013 and 2012, would be as follows hadthis transaction been eliminated (in thousands):

2013 2012

As With As WithPresented Elimination Presented Elimination

Net utility margin $ 32,163 $ 26,564 $ 45,292 $ 39,792

Nonutility operating income (loss) $ 10,027 $ 15,626 $ (121) $ 5,379

Total $ 42,190 $ 42,190 $ 45,171 $ 45,171

The equity method investment activity for Blue Flint for the year ended December 31, 2011, is as follows (in thousands):

2011

Beginning equity investment balance $ 19,486GRE’s share of Blue Flint’s income 3,440GRE’s share of Blue Flint’s other comprehensive income 405

Ending equity investment balance $ 23,331

GRE’s share of Blue Flint’s accumulated other comprehensive income relates to an interest rate swap agreementdesignated as a cash flow hedge, which Blue Flint recorded at fair value. GRE recognized $4.6 million in steam sales toBlue Flint and $1.2 million related to Blue Flint’s use of CCS infrastructure for the year ended December 31, 2011.

During 2013, GRE transferred its ownership interest in Blue Flint to another GRE wholly owned subsidiary, MAG.

MAG — MAG has two wholly owned subsidiaries, Blue Flint and DSAF, as of December 31, 2013. DSAF’s whollyowned subsidiary, DSA, began construction in 2013 of a biorefinery facility located near Jamestown, North Dakota.DSA will be a dry-mill production facility that produces and sells ethanol, dry and modified distillers grain, anddistillers oil, and it will have a production capacity of approximately 65 million gallons of undenatured ethanol per year.