FY2012 Annual Report on Food, Agriculture and … FY2012 Annual Report on food, agriculture and...

44

FY2012 Annual Report on Food, Agriculture and Rural Areas in Japan Summary Ministry of Agriculture, Forestry and Fisheries Japan, 2013

Transcript of FY2012 Annual Report on Food, Agriculture and … FY2012 Annual Report on food, agriculture and...

FY2012 Annual Report on Food, Agriculture and Rural Areas in Japan

Summary

Ministry of Agriculture, Forestry and Fisheries Japan, 2013

The FY2012 Annual Report on food, agriculture and rural areas in Japan is based on Items 1 and 2 of Article 14 of the Food, Agriculture and Rural Areas Basic Act (Law No. 106 for 1999).

Contents

○FY2012 Annual Report on Food, Agriculture and Rural Areas in Japan

Foreword ··············································································· 1

Chapter 1: Reconstruction from the Great East Japan Earthquake ············· 2

Chapter 2: Efforts for securing stable food supply ······························· 5

Chapter 3: Efforts for sustainable development of agriculture ··············· 13

Chapter 4: Utilizing local resources to promote and invigorate rural areas · 26

○Summary of FY2013 Measures for Food, Agriculture and Rural Areas ···· 31

Definitions ··········································································· 32

Acronyms and abbreviations

CAA Consumer Affairs Agency EU European Union GCC Cooperation Council for the Arab States of the Gulf ILO International Labour Organization JA Japan Agricultural Cooperatives JAS Japan Agricultural Standards JFC Japan Finance Corporation MAFF Ministry of Agriculture, Forestry and Fisheries METI Ministry of Economy, Trade and Industry MHLW Ministry of Health, Labour and Welfare MIC Ministry of Internal Affairs and Communications MOD Ministry of Defense MOF Ministry of Finance Japan US The United States

Symbols

ha Hectare kl Kilolitre a Are kg Kilogram t tons

Foreword

Two years have passed since the Great East Japan Earthquake that occurred in March 2011. Restoration and reconstruction from the Great East Japan Earthquake has become one of the government's top priorities. Relevant parties are going ahead with various efforts to reconstruct the Tohoku Region as Japan's food supply base. Therefore, this report includes a chapter on "Reconstruction from the Great East Japan Earthquake -- Reconstruction steps" to widely cover farmland restoration and other agricultural restoration and reconstruction measures in disaster-affected areas, measures for securing farm and livestock product safety and reconstruction support measures including sales of products from disaster-affected areas. In describing these measures, we detailed disaster-affected farm households' steps toward resuming farming as much as possible and tried to directly convey their firsthand opinions to readers. As well, this report specifies production trends, business management conditions and challenges for each of the major farm and livestock products including rice, wheat, soybeans, vegetables, fruits, flowers, sugar beets, sugar canes, tea, livestock products and feed and forage crops, while giving considerations to the balance between these products. In addition to their production trends, this report uses various statistical data to analyze and explain structural changes and characteristics of their consumption under the aging population and women's advance into society. This report also presents future food consumption prospects. This report also discusses global food supply and demand, Japan’s food self-sufficiency ratio, negotiations on EPA/FTA and the proposed TPP agreement, food industry trends, efforts for ensuring food safety and consumer confidence, and Shokuiku (food education) promotion measures from the viewpoint of securing stable food supply. From the viewpoint of sustainable development of agriculture, this report describes the promotion of structural agriculture reforms, measures for solving problems between farmers and farmlands, agricultural production infrastructure development and conservation, measures for raising value added for agriculture and promoting exports of agricultural, forest and fishery products, the latest research and technological development, agricultural production giving priority to environmental conservation, and agricultural organizations’ efforts. Furthermore, from the viewpoint of promoting and revitalizing rural areas, this report discusses the present conditions of rural areas, measures for eliminating abandoned cultivated lands, the present conditions of and measures against damage by wild animals, measures for demonstrating multifunctional roles of agriculture and rural areas, measures for harmonious coexistence and interactions between urban and rural areas, measures for agriculture’s cooperation with education, welfare and tourism, measures for utilizing renewable energy, and urban agriculture conservation and promotion measures. While this report covers a wide range of topics, we have tried to avoid any disproportionate emphasis on data analysis and comments and introduce various efforts taken throughout Japan as much as possible for specifying frontline conditions to make this report approachable and easy to understand. We hope that this report will help citizens deepen their interests in and understanding of Japan’s food, agriculture and rural areas.

1

Sendai city

Natori city

Program implementation area Enlarged farmland partitions

Orderly land utilization

Crop diversion area

Sendai Higashi District (Miyagi Prefecture) Farmland consolidation implementation area (draft)

A farmland filed after consolidation

A farmland filed before consolidation

Upstream HazamagawaRiver and Aratozawa Dam

Upstream Hazamagawa RiverSendai Higashi

Watari Yamamoto

Shirakawayabuki(Hatori Dam)

Upstream AbukumagawaRiver (Saigo Dam)

Haga Plateau

Miyagi Prefecture

Fukushima Prefecture

Tochigi Prefecture

Natorigawa River

Jokawa River

Watari Yamamoto Coastal Farmland

Kanan

Legend

Areas for implementing national specific disaster restoration programs (tsunami-affected areas)

Areas for implementing national specific disaster restoration programs

Areas for implementing national disaster restoration programs for coastal conservation facilities (deputize)

Minamisoma

Item

Farmlands

Tsunami-damaged farmlands in six prefectures→21,480 hectares

Area available for farming resumption under the Basic Guidelines

FarmsTsunami-damaged farms in six prefectures→10,100 farms

0 40 80 100(%)

5,070 farmsResumed farming 50%

20 60

FY2012 FY2013 FY2014 Others8,310 hectares 5,610 hectares 4,990 hectares 2,570 hectares

8,190 hectares Available for resuming farming 38%

5,280 hectares Restoration ongoing 63%

Overview of farmland compartment enlargement in Sendai Higashi District

Chapter 1 Reconstruction from the Great East Japan Earthquake – Reconstruction steps 1 Earthquake and tsunami damage and restoration/reconstruction efforts

The Great East Japan Earthquake inflicted damage worth 2,384.1 billion yen on the agriculture-forestry-fisheries sector (including 904.9 billion yen for agriculture sector).

As for the tsunami-affected farmlands totaling 21,480 hectares, restoration and salt removal have been being implemented to allow farming to be resumed in three years or by FY2014 under the Basic Guidelines for Reconstruction of Agriculture and Rural Communities.

By the FY2012 planting season, farming was allowed to resume for 8,190 hectares (38% of the tsunami-affected farmlands), almost attaining the target under the Basic Guidelines. In addition, restoration is going on for 5,280 hectares for farming resumption in FY2013.

MAFF launched its national specific disaster restoration programs for farmlands and farming facilities in FY2011. In FY2012, MAFF kicked off its national specific restoration program of farming facilities in Minamisoma city of Fukushima Prefecture.

In efforts to secure reconstruction after restoration, it is implemented to enlarge partitions for farmlands totaling 9,400 hectares in Iwate, Miyagi and Fukushima prefectures, using the Great East Japan Earthquake Reconstruction Grants and the like (including those still under planning for readjustment) (as of March 2013).

Source: MAFF

Districts for implementing MAFF’s national specific disaster restoration programs

Agriculture restoration conditions after the Great East Japan Earthquake (As of March 2013)

Source: MAFF Notes: 1) The six prefectures are Aomori, Iwate, Miyagi, Fukushima, Ibaraki and Chiba.

2) The 5,070 farms that resumed farming include those that resumed agricultural production operations or their preparations.

Source: MAFF

2

Rice farming technology

Vegetable and fruit horticulture technology

Livestock farming technology

Demonstration Area for Agricultural Research

Open laboratory

Disaster reduction and business diagnosis

technology

Greenhouse horticulture technology

(Strawberry, tomato)

Government Building research groups and cooperation arrangementsProduction corporations or

fisheries cooperatives

Prefectural and other public experimental laboratories in disaster-affected areas

Incorporated administrative agencies, universities and private enterprises

Contracting

Combination and optimization of highly advanced technologies

Demonstration of technologies

Promotion of technology extension

and commercialization

Number ofreportedsamples

Number ofsamples above the

maximum limit

Above themaximum limit

(%)

The items from which radioactive cesiumabove the maximum limit was detected

Rice 10.32 million 84 0.0008 Rice 2.2Wheat 1,818 0 0 4.8Beans 4,398 25 0.6 Soybean, Azuki bean 2.3

Vegetables 18,570 5 0.03Spinach*2, Angelica keiskei (Ashitaba),Lotus roots, Three leaf arrowhead, Japanesemustard spinach (Komatsuna)*2

3.0

Fruits 4,478 13 0.3Japanese apricot (Ume), Blueberry,Chestnut, Citrus fruit (Yuzu), Satsumamandarin

7.7

Tea infusion 867 13 1.5 Tea 8.6Other cultivated plants 3,094 14 0.5 Buckwheat 3.2Raw milk 2,421 0 0 0.4Meat and eggs(excluding wildlife meat)

154,866 4 0.003 Beef, Pork, Horse meat 1.3

Category

April 1, 2012, to March 31, 2013 Above the maximumlimit before FY2011-

end*1

(%)

A case for large-scale demonstration research on highly advanced agricultural technology

MAFF has implemented a large-scale research and demonstration project in the south coast area of Miyagi prefecture through industry-academia-government collaboration. This project applies and combines various highly advanced agriculture and fisheries technologies in the field of production and processing of rice farming, greenhouse horticulture, and fruit horticulture.

For example, in Yamamoto town, Miyagi Prefecture, a sunlight-using experimental plant for strawberry production was built in FY2011, and advanced technologies, such as optimizing the local temperature for strawberry growing points were demonstrated in FY2012, for faster growth while reducing total heating costs.

Strawberry shelves

To ensure distribution of safe foods, measures to reduce radioactive cesium and inspections of concentration of radioactive cesium in agricultural products have been implemented. As for rice safety, restriction on planting in certain areas, measures to prevent rice plants from absorbing radioactive cesium in planting paddies, and inspections of radioactive cesium before shipment are implemented. In Fukushima Prefecture, all rice bags are inspected. As for livestock products, it is important to promote measures for preventing grass from absorbing radioactive cesium. Such measures were completed by the end of FY2012 for 17,000 hectares out of the 38,000 hectares in grassland subjected to these measures. As a result of these measures, the frequency of exceeding the maximum limit of radio nuclides in farm and livestock products in FY2012 declined substantially from FY2011.

Source: Prepared by MAFF based on materials from MHLW and local public entities *1: The frequency of exceeding the maximum limit which was enforced in April 2012: 100 Bq/kg for general food products, 10 Bq/kg for

tea infusion and 50 Bq/kg for raw milk. 500 Bq/kg for crude or processed tea, which is equivalent to 10 Bq/kg for tea infusion, is used as the maximum limit for this calculation.

*2: Inappropriate storage and use of covering materials should cause these violations.

2 Impacts of the accident at the Fukushima Daiichi Nuclear Power Plant of the Tokyo Electric Power Company and restoration/reconstruction efforts

Image of large-scale demonstration research on highly advanced agricultural technology

Source: MAFF

Technology for optimizing temperatures at

strawberries’ growing point

Results of the inspections on radioactive cesium levels in farm and livestock products (17 prefectures)

3

Radioactive cesium levels inplow layers

Air dose rates at a height of1 meter above surface

Topsoil removal Reduce about 80-90% Reduce about 60-80%Inverting plowing Reduce about 60% Reduce about 30%

Results of farmland decontamination demonstration projects

Source: MAFF

MAFF published a farmland decontamination technical book (in August 2012) that compiled demonstrative farmland decontamination projects demonstrated at the local farmlands, which indicated notes on construction and construction management methods of farmland decontamination. Radioactive cesium levels in rice and vegetables that were test-cropped on decontaminated farmlands were reduced below the minimum radiation detection limit.

Under the catch-phrase “Eating for support” for disaster-affected areas, the government has promoted sales fairs for food products from disaster-affected areas and the proactive use of these products at companies’ in-house restaurants and used and sold these products at restaurants and shops at each government agency.

Many foreign countries and regions toughened import controls on Japanese agricultural, forest and fishery products including food due to the nuclear power plant accident. As the government has been united to ask foreign countries to ease such controls, 10 foreign countries including Canada lifted extra controls. Generally, foreign countries have been easing or lifting such controls.

With the needs for safety certificates being expected to grow in the future, the government developed its certificate issuance arrangements.

In order to recover exports, the government has supported disaster-affected areas’ export promotion efforts and send messages abroad about the attractiveness of Japanese food products.

Latest exports are recovering from the impact of the nuclear power plant accident.

Results of test-cropping on farmlands decontaminated under farmland decontamination demonstration projects

Test cropping Farmland decontamination (topsoil removal)

“Eating for support” campaign

MAFF restaurant and shop

METI restaurant MOD restaurant

Products from disaster-affected areas were promoted at the Hong Kong international Wine & Spirits fair.

Opening a foreign-language website

Easing import controls of major export destination

Sending messages abroad about attractiveness of Japanese food products

Demonstrative farmland decontamination project

Source: MAFF

2011 and 2012 exports (in value) comparing exports before and after the disaster

Source: Prepared by MAFF, based on MOF, “Trade Statistics”

(April-December)

Before the disaster After the disaster

In hundred millions of yen

In hundred millions of yen

Fishery products

Forest products

Agriculturalproducts

(January-March)

Municipality Crop acreage(Unit: a = 0.01 hectare)

Crop Results

57 Rice (Hitomebore, Akitakomachi,Maihime)

10 Vegetables (cucumbers, cabbages, etc.)Kawamata

town64 Rice (Akitakomachi, Hitomebore)

Iitatevillage

Belowminimumdetection

limit

Country /region Date Summary of easing import control

Thailand April 4, 2012Requirement for radioactive material test results9 prefectures 8 prefectures (excludingTokyo)

Vietnam July 2, 2012 Lifting controls on processed food productsApril 2 and October 30,

2012Easing controls on liquor imports

May 2013

Requirement for radioactive material testcertificates for all products from 9 prefectures

Limiting requirements to some specificproducts

Singapore April 8, 2013

Suspension of some specific exports from eightprefectures Exports allowed with requirementfor radioactive material test certificates (sevenprefectures)

EU

4

Country Product Weather conditions

U.S. Corn,soybeans

High temperatures and droughtfrom June 2012 in the corn belt

Russia,Ukraine,Kazakhstan

Wheat, etc.

Freezing damage in January-February 2012, and hightemperatures and drought fromspring

Wheat

Rainfall shortages and freezingdamage in January-February2012 in Germany and Spain,rainfall excess from August2012 in the United Kingdom

Corn Drought from July 2012 in theSoutheastern EU

Australia Wheat, etc.Low temperatures and droughtfrom July 2012 in WesternAustralia

EU

0

200

400

600

800

1,000

0

5

10

15

20

1819 20

2008

21200

9

22201

0

23201

1

24201

2

25201

3

Rice (right scale)

Soybeans

Corn

Wheat

2006 2007 2008 2009 2010 2011 2012 2013

dollars per bushel dollars per ton

53

86

88

93

98

47

14

12

7

2

0 20 40 60 80 100

FY2012

FY2011

FY2010

FY2009

FY2008

%

U.S. Others (South America, Eastern Europe, etc.)

1 Global food supply/demand and establishment of comprehensive food security (1) Global food supply/demand trends

Due to high temperatures and drought in the United States from June 2012, corn and soybean prices rose above their respective past record levels reached in 2008.

Wheat prices also rose along with corn prices but fell short of reaching the record level in 2008 because of wheat stocks in 2012 that exceeded those in 2008. Rice prices leveled off in 2012 as demand shifted to cheaper Indian rice on India’s resumption of rice exports after rice price hikes attributable to Thailand’s reintroduction of the government rice buyback system.

As feed grain (corn and others) buyers shifted rapidly from the United States to South America in response to U.S. corn price hikes from the summer of 2012, new risks emerged, including transportation delays arising from vulnerable infrastructure in South America.

Chapter 2 Efforts for securing stable food supply

Changes in International prices of grains and soybeans

Weather conditions affecting grain and soybean supply/demand (FY2012-2013)

Source: MAFF

Rice: $596 per ton

Record high: $1,038 per ton on May 21, 2008

Soybean: $14.6 per bushel Record high: $17.7 per bushel on September 4, 2012

Wheat: $7.1 per bushel Record high: $12.8 per bushel on February 27, 2008

Corn: $7.2 per bushel Record high: $8.3 per bushel on August 21, 2012

As of April 1, 2013

Sources: Prepared by MAFF based on data from the Chicago Board of Trade and the Rice Committee, Board of Trade of Thailand

Note: One bushel is equivalent to 27.2155 kg of soybeans and wheat, and 25.4012 kg of corn.

Feed corn procurement breakdown trends (in volume)

Source: Prepared by MAFF based on MOF, “Trade Statistics” Note: FY2012 data include preliminary data for March 2013.

5

Rice10.1 (34%)

Pork4.6 (15%)Beef

3.6 (12%)

Milk and milk products2.9 (10%)

Fisheries products2.5 (8%)

Sugar1.5 (5%)

Hen eggs1.1 (4%)

Forestry products0.5 (2%)

Chicken1.0 (3%)

Wheat0.8 (3%)

Other agricultural products1.1 (4%)

(Unit: 100 billion yen)

Und

er n

egot

iatio

n

: Negotiations : Signed : Effectuation : Revision protocols signed : Revision protocols effectuation

(Oct.)

EPA

/FTA

sign

ed

(Sep.)

2002 2003 2004 2005 2006 2007 2008 2009

Entire ASEANBrunei

Philippines

VietnamSwiss

IndonesiaThailand

ChileMalaysiaMexico

Singapore

South KoreaGCC

India

Australia

(from Nov. )

(from Jan.)

(from Feb.)

(from Feb.)

(from Jul. )

(from Jun.)

(from Apr.)

(from Feb.)

(form May)

(from Dec.)

(from Sep.)

(from Jan.)

(from Apr.)

(Sep.)

(Dec.)(Mar.)

(Apr.)

(Aug.)

(Jun.)

(Apr.)

(Sep.)

(Feb.)

(Sep.)

(Apr.)

(Nov.)(Jan.)

(Jul.)

(Nov.)

(Jul.)

(Jul.)

(Dec.)

(Dec.)

(from Jan.) (Dec.)

2010

Peru (from May)

2011

(Feb.)

(May)

2012

(Aug.)

(Mar.)

Mongolia (from Jun.)

Canada (from Nov.)

Colombia (from Dec.)

2013

Japan-China-South Korea

(from Mar.)

(Mar.)

(Sep.)(Sep.)

(Apr.)

Estimationtarget

Economic effects

Consumption + 0.61% (+ 3.0 trillion yen)

Exports + 0.55% (+ 2.6 trillion yen)

Investment + 0.09% (+ 0.5 trillion yen)

Imports - 0.60% (- 2.9 trillion yen)

Source: Cabinet Secretariat Notes: 3) The estimation shows the impacts on the Japanese economy and agriculture-forestry-fisheries production when Japan joins the TPP (11 countries). 4) Assumptions : <1> The estimation includes the impacts of tariff elimination, but not those of reduction of non-tariff barriers and liberalization of services and investment. <2> All tariffs are assumed to be eliminated upon entry into force. <3>The effects of additional domestic support measures are not taken into account. 5) MAFF estimated the output decrease in agriculture-forestry-fisheries considering details of each product such as production and distribution systems, and potential export capacities of exporting countries. The government incorporated MAFF’s estimate into the GTAP (Global Trade Analysis Project) model and estimated the impacts on the Japanese economy. Assumptions: <1> All domestic products are divided into two groups, “competing with imports” or “not competing with imports”, from the view point of price differentials, quality gaps and potential export capacities. <2> Competing goods are replaced by low price imports. <3> Prices of non-competing goods fall as low price imports spread among people.

(2) Trends in agriculture trade negotiations

Progress in Japan’s EPA/FTA negotiations

Source: MAFF Notes: 1) The Japan-ASEAN EPA took effect for Singapore, Laos, Vietnam and Myanmar in December 2008, for Brunei in January

2009, for Malaysia in February 2009, for Thailand in June 2009, for Cambodia in December 2009 and for the Philippines in July 2010.

2) On signed EPAs or FTAs, renegotiations have been conducted since their effectuation according to the respective agreements.

Economic effects (estimated) of tariff elimination under the TPP Effects on the entire Japanese economy (real GDP)

+ 0.66% (+ 3.2 trillion yen) Agriculture-forestry-fisheries output

decline: 3.0 trillion yen

By April 2013, Japan has signed economic partnership agreements with 12 countries and one region. Japan’s EPA negotiations are ongoing with Australia, Mongolia, Canada, Colombia, South Korea (negotiations suspended) and the GCC (negotiations delayed). In order to realize the Free Trade Area of the Asia-Pacific (FTAAP), Japan in November 2012 declared launching negotiations on the RCEP (Regional Comprehensive Economic Partnership: an EPA between ASEAN and six other countries – Japan, China, South Korea, India, Australia and New Zealand) and the Japan-China-South Korea free trade agreement. In March 2013, Japan announced its participation in the TPP (Trans-Pacific Partnership) negotiations. According to the government’s estimate, the impact of tariff elimination under the TPP on the Japanese economy is a 0.66% (3.2 trillion yen) increase in real GDP, while the TPP reduces domestic agriculture-forestry-fisheries output by approximately 3 trillion yen. (Since the government’s estimate is calculated under the assumptions given in Notes 4 and 5, the actual impacts on agriculture-forestry-fisheries output could be severer in the regions that depend more heavily on the agriculture-forestry-fisheries sector.)

6

4843 40 40 39 39

75 74 71 69 7066

0102030405060708090

FY1990 FY1995 FY2000 FY2005 FY2011

% Food self-sufficiency ratio(Production value basis)

Food self-sufficiency ratio(Calorie supply basis)

FY2010 FY2011

Food supply capacity

Domestic production capacity

Import capacity

Reserves

Food self-sufficiency potential

Farmlands, farming water and other agricultural resources

Farmers (business farmers)

Agricultural technologies

(Unit: 10,000 tons)

FY2008 FY2011FY2020targets

Rice 881 837 855Rice for flour 0.1 4.0 50.0Rice for feed 0.9 18.3 70.0Wheat 88 75 180Sweet potatoes 101 89 103Potatoes 274 239 290Soybeans 26 22 60Vegetables 1,265 1,182 1,308Fruits 341 297 340Raw milk 795 753 800Beef 52 51 52Pork 126 128 126Chicken 138 138 138Hen eggs 255 248 245Sugar beet 425 355 380Sugar canes 160 100 161Feed crops 435 408 527

Rice 100%

Wheat15%

Sugar 32%

Seafood 72%

Others28%Fruits

58%Soybeans25%

Vegetables90%

Livestock products

21% 56%

Per capita daily calorie supply: 2,640 kcal

48%2,436kcal

39%

FY2011

Others23%

Fruits33%Soybeans25%Vegetables76%

Seafood 64%

Sugar 26%

Wheat11%

Oils/fats 3%

16% 48%

Rice 97%

FY1990

562kcal

396kcal

341kcal

330kcal

198kcal109kcal

683kcal

366kcal

360kcal

320kcal

229kcal

143kcal

Imported-feed portion of production

Oils/fats16%

Japan’s food self-sufficiency ratio trends

Source: MAFF, “Food Balance Sheet”

2 Japan’s food self-sufficiency ratio trends The food self-sufficiency ratio on calorie supply basis in FY 2011 remained unchanged from 39% in the previous year as a wheat production recovery was coupled with a decline in rice demand following a temporary demand rise just after the Great East Japan Earthquake. (The feed self-sufficiency ratio rose by 1 percentage point to 26% on a TDN* basis.)

The food self-sufficiency ratio on production value basis in FY2011 fell by 4 percentage points to 66% as domestic production value decreased due to beef and vegetable price drops under the impact of the Great East Japan Earthquake.

* TDN stands for total digestible nutrients for livestock.

Trends of product-by-product food self-sufficiency ratios (on calorie supply basis)

Source: MAFF, “Food Balance Sheet”

The Basic Plan for Food, Agriculture and Rural Areas sets the food self-sufficiency ratio target for FY2020 at 50% on calorie supply basis and 70% on production value basis setting production targets for major products. At present, some increases have been seen in rice output for flour and feed. But wheat and soybean production has fallen on unfavorable weather conditions and a decline in their crop acreage. In addition to increase in the food self-sufficiency ratio, Japan should maintain and improve its food self-sufficiency potential that indicates domestic agricultural production’s potential food supply capacity covering farmlands, farming water and other agricultural resources, farmers (business farmers) and agricultural technologies.

Source: MAFF

Source: MAFF

Production targets and present conditions

Concept of food self-sufficiency potential

7

0

1,000

2,000

3,000

4,000

5,000

Ric

e

Bre

ad

Noo

dles

Fish

and

she

llfi

sh

Mea

t

Dai

ry p

rodu

cts/

eggs

Veg

etab

les/

seaw

eeds

Frui

ts

Oil

s/fa

ts/c

ondi

men

ts

Coo

ked

food

wit

h ri

ce, b

read

, no

odle

s

Oth

er c

ooke

d fo

od

Oth

er fo

od

Eat

ing

out

Yen/monthHouseholds including elderly people aged 65 or more

Households including no elderly people aged 65 or more

67.5

69.3

73.4

78.0

11.7

10.5

7.7

5.6

10.9

10.5

10.7

8.2

9.9

9.7

8.2

8.2

0 20 40 60 80 100

2010

2000

1990

1980

%

Fresh and processed food products

Cooked foodEating out

Alcoholic and other beverages

94.5

92.9

84.2

70

80

90

100

110

1990 1995 2000 2005 2012

Consumption expenditure level index (general) Real wage index

Consumption expenditure level index (food)

Indexes 29.0

23.7

23.5

10

15

20

25

30

05

101520253035

1980 1990 1995 2000 2005 2012

10,000 yen/month %Household consumption spending

Engel’s coefficient (right scale)Food expense

0

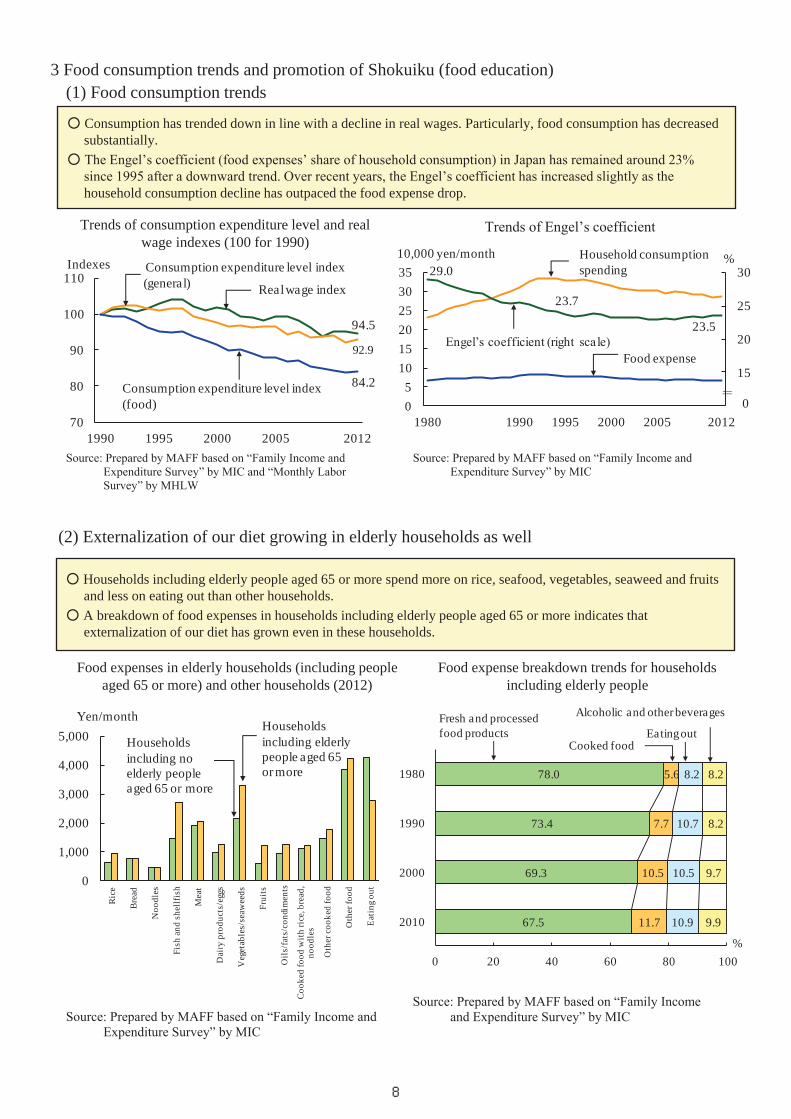

3 Food consumption trends and promotion of Shokuiku (food education) (1) Food consumption trends

Consumption has trended down in line with a decline in real wages. Particularly, food consumption has decreased substantially. The Engel’s coefficient (food expenses’ share of household consumption) in Japan has remained around 23% since 1995 after a downward trend. Over recent years, the Engel’s coefficient has increased slightly as the household consumption decline has outpaced the food expense drop.

Source: Prepared by MAFF based on “Family Income and Expenditure Survey” by MIC and “Monthly Labor Survey” by MHLW

Trends of Engel’s coefficient

Source: Prepared by MAFF based on “Family Income and Expenditure Survey” by MIC

Trends of consumption expenditure level and real wage indexes (100 for 1990)

(2) Externalization of our diet growing in elderly households as well

Households including elderly people aged 65 or more spend more on rice, seafood, vegetables, seaweed and fruits and less on eating out than other households.

A breakdown of food expenses in households including elderly people aged 65 or more indicates that externalization of our diet has grown even in these households.

Food expenses in elderly households (including people aged 65 or more) and other households (2012)

Food expense breakdown trends for households including elderly people

Source: Prepared by MAFF based on “Family Income and Expenditure Survey” by MIC

Source: Prepared by MAFF based on “Family Income and Expenditure Survey” by MIC

8

7.9

8.2

8.6

8.9

9.7

7.2

8.0

9.4

10.2

11.7

6.2

6.7

7.5

8.3

9.5

3.9

4.1

4.5

4.7

4.2

10.1

10.5

11.1

11.5

11.7

3.0

3.4

3.8

4.0

4.5

4.5

4.3

4.0

3.7

3.1

7.4

7.3

6.7

6.3

6.7

16.6

14.7

12.0

10.9

8.3

7.7

6.9

5.6

4.6

3.8

4.8

4.7

4.8

4.8

4.8

20.8

21.2

22.1

22.1

21.9

0 20 40 60 80 100

2025

2015

2005

2000

1990

%

Cereals Fish and shellfish Eating outMeat

Dairy products/eggs

Vegetables/seaweedsFruits

Oils/fats/condiments

Alcoholic beveragesBeverages

Cooked food

Cakes/candies

813 1,073

1,504 1,934

22.7 26.4

32.2 37.3

0

10

20

30

40

0

1,000

2,000

3,000

1980 1990 2000 2010

%10,000 households

Percentage share for households including elderly people aged 65 or more (right scale)

Number of households including elderly people aged 65 or more

0

1

2

3

20 30 40 50 60 70

1,000 yen

Rea

l spe

ndin

g on

coo

ked

food

1,000 yenReal income for spouses

19.8

32.437.2

12.5

19.821.2

42.1

27.9 23.3

5.7 8.711.4

19.9

11.1

6.90

10

20

30

40

50

1980 1990 2000 2010 2020 2035

Couple-and-child households Single-member households

Couple-only households

Others (including three-generation households)

Single-parent households

Two-

mem

ber o

r lar

ger h

ouse

hold

s

%

42.6 43.8

61.968.6

75.7

76.4

87.8 88.7

0

20

40

60

80

100

Aged 15-19

Aged 20-24

Aged 25-29

Aged 30-34

Aged 35-39

Aged 40-44

Aged 45-49

Aged 50-54

Aged 55-59

Aged 60-64

Aged 65 or more

Japan (1975)

Japan (2012)

Germany

Sweden

U.S.

%

Percentage shares have tended to increase for single-member households, couple-only households and households including elderly people aged 65 or more. Particularly, the percentage share for single-member households has been rising faster than for couple-only households. This tendency is expected to continue in the future.

The share of overall food expenditure has declined for meat and vegetables while increasing for cooked food and oils/fats/condiments. As the tendency is expected to continue, externalization of our diet is projected to further grow.

(4) Structural food consumption changes

Changes in shares for household categories Changes in the number of and percentage share for households including elderly peopled aged 65 or more

Sources: MIC, “Population Census,” the National Institute of Population and Social Security Research, “Household Projections for Japan”

Source: “Outlook on household food expenditure under the falling birthrate and aging population” (August 2010) by the MAFF Policy Research Institute Note: Data through 2005 are from “Family Income and Expenditure Survey,” “Consumption Survey” and others by MIC. Data in and after 2015 are estimates.

Changes in and projections of food categories’ shares of food expenditure

Source: MIC, “Population Census”

(3) Changes in women’s labor situation and their impacts on demand for cooked food Women’s labor participation rate by age group in Japan indicates a moderate M-shaped curve reflecting improvements in work conditions. Meanwhile, these rates in Western countries including Sweden, Germany and the United States indicate parabolic curves. In line with an increase in real income for spouses in workers’ households, real spending per household member on cooked food has trended upward. If women’s participation in society in Japan reaches the levels in Western countries, demand for cooked food will increase in line with income growth.

Women’s labor participation rate by age group (international comparison)

Source: Prepared by MAFF based on “Labor Force Survey” by MIC and “LABORSTA” by the ILO

Source: Prepared by MAFF based on “Family Income and Expenditure Survey” and “Consumer Price Index” by MIC

Real income for spouses of householders and real spending per household member on cooked food

9

78.9

94.2

78.62.3

5.8

01234567

60

70

80

90

100

1990 1995 2000 2005

Trillion yenHome-meal replacement industry

(right scale)

Food industry

Trillion yen

02010 2011

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2008 2009 2010 Estimate

2011 Projection

2015 Projection

100 million yen

16,382

19,225

22,70324,265

26,156

31,752

Confectionery

Seasoned food

Seasoning

Beverages and articles of tasteDry food

Chilled beverages and milk productsProcessed livestock products

Japanese and dry meals for daily delivery

Others

Frozen food products

Alcoholic beverages

(5) Promotion of Shokuiku (food education) The promotion of Shokuiku (food education) is important for fostering people who have knowledge about food and select foods to practice healthy eating habits.

MAFF has expanded advanced wide-area and region-specific Shokuiku activities to promote the implementation of Japanese eating habits.

[Specific cases] National Food Koshien Contest in Yamagata 2012 (Yamagata city, Yamagata Prefecture)

The association for delicious Yamagata food and culture, the Yamagata Shokuiku network, the prefectural federation of agricultural cooperatives and the Yamagata Prefecture government have sponsored the contest through cooperation between the public and private sectors to foster senior high school students’ consciousness about Shokuiku and promote the succession of local food cultures. Senior high school students who won regional preliminary contests raced to present new cooking ideas taking advantage of local food cultures and rich food materials as learned from local farmers and cooks.

Efforts using a Shokuiku and Hanaiku (flower education) center (Niigata city, Niigata Prefecture)

The Niigata municipal government launched a Shokuiku and Hanaiku center in FY2011as a Shokuiku promotion base to implement cooking practices using local food materials and elementary school students’ trial participation in farming. In the future, it plans to open agricultural parks including trial farming fields, livestock barns and accommodation facilities in a bid to allow all elementary school students in the city to experience trial farming. Retailer’s health promotion efforts (Sakado and Tsurugashima cities, Saitama Prefecture)

Under a partnership between Yaoko Co. and the Kagawa Education Institute of Nutrition, Saitama Prefecture has promoted campaigns at supermarket stores to increase vegetable intake under the slogan “Vegetables for health and longevity.” In efforts to increase the vegetable intake of the people in Saitama Prefecture, the prefecture calls for one additional vegetable dish everyday through posters and holds tasting events for broccoli produced in the prefecture.

4 Food industry trends

The domestic production value of the food industry has been falling due to food price drops since a peak was posted in the second half of the1990s.

Even amid the trend, the home-meal replacement market has been expanding due to structural family changes and the growth of externalization of our diet, indicating it is important for food companies to explore domestic markets from the viewpoint of consumers.

Regarding product planning and development, the private brand products market expanded from 1.6 trillion yen in 2007 to 2.4 trillion yen in 2010 and is projected to exceed 3 trillion yen in 2015.

Trends of domestic production value of the food industry and the home-meal replacement market

Source: MAFF, “Agriculture/Food Industry Economic Accounting,” Foodservice Industry Research Institute survey

Notes: 1) The home-meal replacement industry market represents delicatessen stores (excluding catering lunch boxes).

2) The food industry covers combined production in value by the food manufacturing industry, restaurants and relevant distributors.

Trends of the private brand products market

Source: Fuji Keizai Co., “PB Food Market Fact-finding Survey 2011”

Note: On a retail base

10

0

5,000

10,000

15,000

20,000

FY2006 FY2007 FY2008 FY2009 FY2010Estimate

FY2011Projection

FY2015Projection

100 million yen

14,35415,262 15,735 16,166 16,806 17,260

19,021

Home natural food delivery service

Home meal delivery

Home prepared-food

Home pizza delivery

Home sushi delivery

Home delivery by restaurant and fast food chains

Milk delivery

Coop delivery service

Home delivery by convenience stores and Internet supermarkets

329 327 357 379 387 404 401

41 48 46 53 57 62 68163 179 174 156 168 187 198

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011

Companies RestaurantsFood manufacturing

533 554653

577 588 612667

Distribution/trade (including logistics)

8

In food distribution, the food delivery service market expanded from 1.4 trillion yen in FY2006 to 1.7 trillion yen in FY2010 and is projected to increase to 1.9 trillion in FY2015.

Food companies operating in Asia account for 667 firms or two-thirds of Japanese food firms that have expanded into overseas markets, indicating these companies’ accelerating efforts to grab Asian and other overseas demand expected to increase in the future.

[Japanese restaurants opened as a symbol of Japanese culture in Thailand]

The Japanese restaurant chain Ootoya Co. has opened Japanese restaurants in Bangkok. It exports udon wheat noodles and soba buckwheat noodles as well as shoyu soy sauce and miso fermented soybean paste that determine the taste of Japanese food, while procuring pork, chicken and other food materials in Thailand. As Japanese restaurants have been expanded to spread Japan’s food culture in Bangkok, Japanese department stores in Bangkok have increased sales of shoyu and miso exported from Japan.

Changes in the number of Japanese food firms operating in Asia

Source: Prepared by MAFF based on “List of Overseas Operating Enterprises 2012” by Toyo Keizai, Inc.

Notes: 1) The total number of companies operating overseas was 977. 2) Data are for 2011. 3) Asian markets covered by the figure are China, Hong Kong,

Singapore, Taiwan, South Korea, Thailand, Malaysia, the Philippines, Indonesia, Vietnam and India.

Source: Yano Research Institute Ltd. ,“Food Delivery Market Survey 2011” Notes: 1) On a corporate sales basis

2) Effects of the March 2011 Great East Japan Earthquake are not taken into account.

Food delivery market value and breakdown trends

Ensuring food safety and consumer confidence (1) Efforts for improving food safety

MAFF implements the risk management process based on scientific principles to improve food safety. In FY2012, MAFF compiled a databook of analytical results from MAFF surveillance studies on hazardous

chemicals in agricultural, livestock, fishery and other food products conducted from FY2003 until FY2010 (a total of about 344,000 data) and distributed it widely to interested parties.

Using outcomes from MAFF surveillance studies on foodborne pathogens, MAFF published a handbook for egg farms, following the handbooks for beef and chicken farms issued in the previous year, that provided measures to prevent food poisoning bacteria from invading into or spreading in farms.

The number of data and the use of outcomes from MAFF surveillance studies shown in the databook

Source: MAFF

MAFF investigated the occurrence of contaminants (e.g. mycotoxins and heavy metals) and pesticide residues in fifty-four agricultural products, six livestock products, thirty fishery products and thirty-eight processed food products that Japanese people consumed abundantly, or that had contained previously or potentially contained those chemicals at high levels (the total number of data: approx. 344,000).

The studies confirmed that the safety of most agricultural, livestock, fishery and processed food products produced in Japan is highly ensured.

The data are used as a basis for domestic and international risk assessments and for evaluation of risk management measures.

11

Food labeling surveillance council (local level)

Relevant prefectural organizations Local branches of central government agencies

Local MAFFbranchLocal MHLWbranchLocal JFTC (Japan Fair Trade Commission) branchetc.

Division in charge of the Act against Unjustifiable

Premiums and Misleading Representations

Division in charge of the Food Sanitation

Act

Division in charge of the Act on Standardization and Proper

Quality Labeling of Agricultural and Forestry Products

Consumer center, etc.

Division in charge of the Rice Traceability Act

Prefectural police department

Punishing business operators as necessary

Relevant organizations share information and exchange opinions

Information on inappropriate food labeling

(2) Animal and plant epidemic prevention measures

Cases for thorough sanitary control to prevent infectious livestock diseases from breaking out

Source: MAFF

Putting up barricades to separate a sanitary control area

An orderly locker room for visitors

Cases for border measures for passengers at international airports

Shoe sole disinfection using a disinfection mat A baggage inspection with a quarantine detector dog

An animal quarantine questionnaire

Prepared in Japanese,

English, Korean, Chinese

(simplified and traditional) and

Russian

Source: MAFF

MAFF implements animal and plant epidemic prevention measures to prevent infectious livestock diseases and plant pests from entering Japan from abroad and breaking out or flourishing in Japan.

In order to prevent infectious livestock diseases from entering Japan at the border, MAFF implements shoe sole disinfection for all travelers entering Japan and baggage inspections with quarantine detector dogs at airports and seaports, and announcement-based questions to passengers on all direct flights from countries or regions where foot-and-mouth diseases and the like were reported, and questionnaire surveys on some of such flights.

MAFF conducts on-the-spot inspections under the Act on Standardization and Proper Quality Labeling of Agricultural and Forestry Products and the Law for Keeping Transaction Record and Relaying Place of Origin Information of Rice and Rice Products, and gives instructions on and publishes inappropriate product labeling and provide guidance against inappropriate information about the origins of rice and processed rice products. Local food labeling surveillance councils share information and exchange opinions on inappropriate food labeling.

The CAA has submitted to the Diet a food labeling bill to unify food labeling provisions in the three food labeling laws (the Food Sanitation Act, the Act on Standardization and Proper Quality Labeling of Agricultural and Forestry Products, and the Health Promotion Act) (On April 5, 2013, the bill was decided on by the Cabinet and submitted to the Diet).

(3) Efforts to secure consumers confidence

Cooperation between agencies involved in food labeling

Source: MAFF

12

2,9024,986 5,272

8,700

14,100

0.4 1.5 1.62.5

6.2

0

2

4

6

8

10

0

5,000

10,000

15,000

20,000

1990 1995 2000 2005 2012

Corporation farms %Corporation farms’ share of total farmlands (right scale)

Number of corporation farms

65 79 119

16

21

32

05101520253035

0

100

200

300

400

500

1990 2000 2010

398 380 368

10,000 hectares %

Area cultivated by farms having 20 hectares or more in farmland

Percentage share of land area cultivated by farms having 20 hectares or more in farmland(right scale)

Area cultivatedby farms havingless than 20hectares infarmland

0

2

4

6

8

10

12

14

1970 1975 1993 2005 2010

Lease hold rights transfers

Ownership transfers

Creation of the agricultural land use promotion project

Creation of the super L loan system for certified farmers

Creation of farm management stabilization programs

10,000 hectaresCreation of the certified farmer system

Less than20

hectares

20hectaresor more

Total

9,706 2,805 12,511

78% 22% 100%

3.8 15.4 19.2

20% 80% 100%

Number ofcorporation

farms

Farmland size(10,000 ha)

2831

3540

45

21 2326

3035

2226

0

10

20

30

40

50

1990 1995 2000 2005 2010

%

5 hectares or more

10 hectares or more20 hectares or more

Source: MAFF

Source: MAFF

Changes in farmland concentration rates by size of cultivated land under management

(family farms )

Number of corporation farms by size of cultivated land under

management and farmland size (2010)

Source: MAFF

Changes in the number of corporation farms

While the number of family farms has declined, family farms scales have expanded. Family farms cultivating 5 hectares or more in farmlands now account for 45% of overall farmlands held by family farms.

The number of corporation farms has increased and their share of overall farmlands has expanded. In 2010, corporation farms cultivating 20 hectares or more in farmlands accounted for 22% of the total number of

corporation farms and 80% of their farmlands.

Chapter 3 Efforts for sustainable development of agriculture 1 Promoting structural agriculture reforms (1) Agricultural structure changes

Percentage of land area cultivated for land-extensive farming by farms having 20 hectares or more in farmland

Changes in farmland size for rights transfers

Sources: Estimated based on MAFF’s “Census of Agriculture and Forestry” and “Statistics on Cultivated Area and Planted Area”

Source: MAFF Note: “Super L loan” is a low-interest loan for certified farmers.

Since the creation of the agricultural land use promotion project in 1975, MAFF has promoted the mobility of farmland using mainly the leasehold rights. The creation of the certified farmer system in 1993 and that of the super L loan system for certified farmers in 1994 have helped accelerate the mobilization.

As a result, the percentage share of land area cultivated for land-extensive farming by farms having 20 hectares or more in farmland rose to 32% in 2010.

13

9,417

11,539 12,311 12,14911,717

0

4,000

8,000

12,000

16,000

2005 2010 2011 2012 2013 (Estimate)

Community-based farm cooperatives

Corporations participating in

agriculture(1,071

corporations)

Vegetables: 492 corporations (46%)

Rice, wheat, barley, etc.: 183 corporations

(17%)

Mixed production: 199 corporations

(19%)

Fruits: 92 corporations (8%)

Industrial crops: 42 corporations (4%)

Flowers: 30 corporations (3%)

Livestock (including feed crop production): 25 corporations (2%)

Others: 8 corporations (1%)

235 435

671(63%)63

108

145

66

134

255(24%)

0

200

400

600

800

1,000

1,200

2010 2011 2012

Corporations

Stock corporations

Special limited liability companies

NPO corporations

677

364

1,071

(14%)

Voluntary organization Corporation organizationCorporate status Absent Present

Decision-makingsystem

Cooperative members'agreements, based on no law

Directors make decisionsbased on law

Internal reserves cannot beaccumulated

Internal reserves can beaccumulated

Loans to or investment in avoluntary organization cannotbe accepted

Loans to and investment in acorporation organization canbe accepted

Securingemployment

Difficult Possible

Securinginvestmentresources

(Unit: %)

Securing stablematerial supply

Reducingmaterialprocurementcosts

Securingtraceability

Increasing valueadded for anddifferentiatingmainstayproducts

Upgradingcorporate image

Diversifyingbusinessoperations

Securing profitContributing tolocaldevelopment

Promotingemploymentmeasures(effectiveutilization ofhuman resources)

Foodmanufacturers 51 22 37 59 45 31 29 57 41

Food wholesalers 67 28 28 56 39 44 39 50 22

Constructioncompanies 12 12 8 12 28 80 32 60 72

14

In three years after the Agricultural Land Act was revised in 2009, 1,071 corporations launched agricultural production. Stock corporations accounted for the largest share at 63% of the total, followed by 24% for NPO (nonprofit organization) corporations and 14% for special limited liability companies.

Of these corporations, the largest portion at 46% produce vegetables, followed by 19% for mixed production and 17% for rice, wheat, barley, etc.

More than 50% of food manufacturers and wholesalers have participated in agriculture for the purpose of securing stable material supply or increasing value added for and differentiating their mainstay products. More than 70% of construction companies have participated in agriculture for the purpose of business diversification and employment measures (effective utilization of human resources).

Differences between voluntary community-based farm cooperatives and corporation organizations

Trends of general corporations’ entry into agriculture (Increases after Agricultural Land Act revision)

Changes in the number of community-based farm cooperatives (voluntary organizations)

Source: MAFF surveys Source: MAFF, “Survey on Community-Based Farm Cooperatives”

Community-based farm cooperatives (voluntary organizations) have been in transition to corporation farms. Some new cooperatives have been created while some existing cooperatives have been transformed into corporation farms. As a result, the number of community-based farm cooperatives has remained around 12,000 over recent years.

For further stabilization of their management community-based farm cooperatives, if they are voluntary organizations, they should be encouraged to become corporation organizations.

Corporation farms by product (at the end of December 2012)

Purposes for participation in agriculture by type of industry (multiple answers allowed)

Source: MAFF Note: At the end of December for each year

Source: MAFF Note: “Mixed production” indicates producers of multiple products.

Source: JFC, “Survey on Enterprises’ Entry into Agriculture” (published in January 2012)

14

Conscious of being farm manager46.5%Not conscious of

being farm manager

No opinion

No response6.6%

15.3%

31.7% 41 74 84 91 91 89

59 26 16 9 9 11

0 20 40 60 80

100

Less than 3 m. yen

3-5 m. yen

5-10 m. yen

10-50 m. yen

50-100 m. yen

100 m. yen or more

With women%

Without women

55.1

41.5

28.2

20.8

11.3

11.0

0 10 20 30 40 50 60

Improving women's ambitions and consciousness

Other family members' understanding

Improving women's capabilities

Women's networks

Providing information and opportunities

Local communities' understanding %

23.0

9.4

0 10 20 30

With women directors or managers

Without women directors or managers

%

Gap of 13.6 percentage points

Engaged69.9%

Not engaged

No opinion

No response1.3%

15.8%

12.9%

Women farmers play a key role in agriculture and regional activities. Of women farmers, 70% are engaged in preparing farm management policies and 47% are recognized as farm managers.

Business operations with women directors or managers tend to feature higher sales and profitability than those without them.

Farms with core women farmers tend to feature higher sales than those without them. Required for allowing women farmers to work proactively are their improvement of ambitions and capabilities, other

family members’ understanding, women’s networks, and the provision of information and opportunities. In October 2012, a nationwide network (nicknamed “Hime Collabo (princess collaboration)” was launched for women

farmers to have links with non-agriculture industries.

Engaged in preparing farm management policies (women farmers)

Comparison of sales growth rates for cases with and without women directors or managers

Conscious of being farm manager (women farmers)

Source: MAFF, “Questionnaire Survey on Women’s Engagement in Agriculture” (conducted in January 2013)

Percentage shares for farming families with and without core women farmers by farm product sales size

Source: MAFF Note: Prepared based on MAFF’s “2010 World Agriculture-Forestry

Census” (custom-ordered tabulation)

Source: JFC, “Survey on Women’s Performance in Farm Management” (published in January 2013)

Launching a “nationwide network linking with women agriculture-forestry-fisheries workers”

(nicknamed “Hime Collabo”)

In October 2012, a nationwide network (nicknamed “Hime Collabo”) linking with women agriculture-forestry-fisheries workers was launched to form a network for women agriculture-forestry-fisheries workers, deepen their links with different industries and private enterprises, develop business partnerships and step up information and other exchanges and collaboration to further promote business operations of women agriculture-forestry-fisheries workers.

An exhibition booth at “Agriculture Frontier 2012”

A national seminar

Measures required for allowing women farmers to work proactively (multiple answers allowed)

Source: MAFF, “Questionnaire Survey on Women’s Engagement in Agriculture” (conducted in January 2013)

15

0.1 2.5 5.99.8

25.552.5

81.5

0 1 3 614

30

46

0

10

20

30

40

50

60

0

20

40

60

80

100

120

Aged 15-19

Aged 20-29

Aged 30-39

Aged 40-49

Aged 50-59

Aged 60-69

Aged 70 or more

10,000 persons %Number of core persons mainly

engaged in farming

Percentage shares of all core persons mainly engaged in farming (right scale)

Total number of core persons mainly engaged in farming at

1.78 million

1.06 million people aged 65 or more (60%)

180,000 persons aged less than 50 (10%)

0.7 0.6 0.6 0.6 0.6 0.8

10.3 9.68.3

9.37.7 7.6

3.7 4.15.5 5.1 4.9

5.9

02468

1012

2006 2007 2008 2009 2010 2011

1,000 persons New self-employed farmersNew employed farmers

New entries

72.464.4

49.657.4

44.847.1

6.5 7.3 8.4 7.6 8.0 8.9

0

20

40

60

801,000 persons New self-

employed farmers

New employed farmers

New entries

5 1 6 10 5 17 7 14 5 7 6 2 8 12 7 15

8 11 7 8 15

9 17

23 17

29 19

28 17 19 13

13 13

14 14

13

13 15

14 14

61 74 56 40 58 26

53 31

58 52

0 20 40 60 80

100

Tota

l

Ric

e fa

rmin

g

Out

door

veg

etab

le fa

rmin

g

Faci

lity

-bas

ed v

eget

able

fa

rmin

g

Orc

hard

farm

ing

Dai

ry fa

rmin

g

Cat

tle

farm

ing

Hog

farm

ing

Sem

i-m

ulti

ple

farm

ing

Mul

tipl

e fa

rmin

g

39 or less40-4950-59

60-64

65 or more

%

Single farming

(66) (70) (65) (60) (66) (55) (63) (57) (65) (63) Average age

81.073.5

60.066.8

54.6 58.166.3 59.1 45.6

51.8 41.4 43.9

14.7 14.3 14.4 15.0 13.2 14.2

0102030405060708090

2006 2007 2008 2009 2010 2011

1,000 personsNew farmers (Total)

New farmers (40 year-old or older)

New farmers (39-year-old or younger)

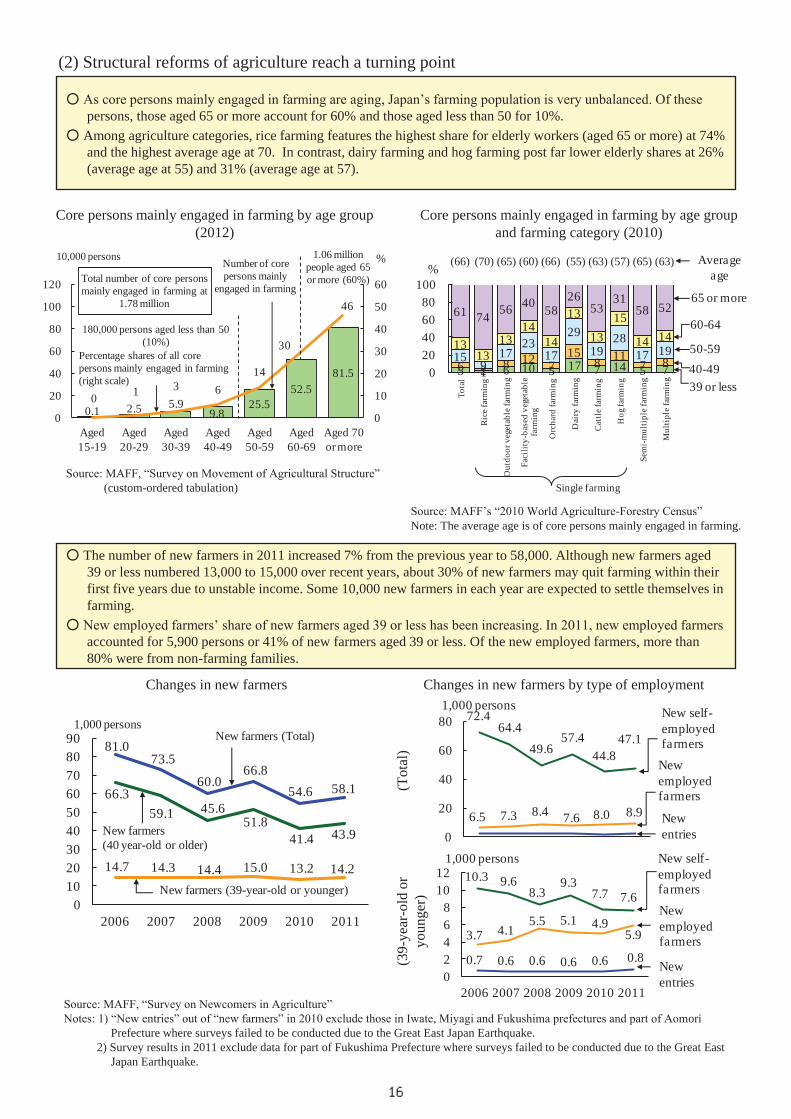

(2) Structural reforms of agriculture reach a turning point

Source: MAFF, “Survey on Movement of Agricultural Structure” (custom-ordered tabulation)

Core persons mainly engaged in farming by age group (2012)

Source: MAFF’s “2010 World Agriculture-Forestry Census” Note: The average age is of core persons mainly engaged in farming.

Core persons mainly engaged in farming by age group and farming category (2010)

As core persons mainly engaged in farming are aging, Japan’s farming population is very unbalanced. Of these persons, those aged 65 or more account for 60% and those aged less than 50 for 10%.

Among agriculture categories, rice farming features the highest share for elderly workers (aged 65 or more) at 74% and the highest average age at 70. In contrast, dairy farming and hog farming post far lower elderly shares at 26% (average age at 55) and 31% (average age at 57).

Source: MAFF, “Survey on Newcomers in Agriculture” Notes: 1) “New entries” out of “new farmers” in 2010 exclude those in Iwate, Miyagi and Fukushima prefectures and part of Aomori

Prefecture where surveys failed to be conducted due to the Great East Japan Earthquake. 2) Survey results in 2011 exclude data for part of Fukushima Prefecture where surveys failed to be conducted due to the Great East

Japan Earthquake.

The number of new farmers in 2011 increased 7% from the previous year to 58,000. Although new farmers aged 39 or less numbered 13,000 to 15,000 over recent years, about 30% of new farmers may quit farming within their first five years due to unstable income. Some 10,000 new farmers in each year are expected to settle themselves in farming.

New employed farmers’ share of new farmers aged 39 or less has been increasing. In 2011, new employed farmers accounted for 5,900 persons or 41% of new farmers aged 39 or less. Of the new employed farmers, more than 80% were from non-farming families.

Changes in new farmers Changes in new farmers by type of employment

(39-

year

-old

or

youn

ger)

(T

otal

)

16

3.2 3.1 3.8 6.6 8.3 13.3 16.2 18.2 9.9 9.2 9.7

1.3 2.0

5.4

14.412.4

0

5

10

15

20

25

30

35

40

1975 1980 1985 1990 1995 2000 2005 2010

10,000 hectares

Owned by land tenure non-farm households

Owned by noncommercial farm households

Owned by commercial farm households

3.84.1

5.6

7.99.0

39.638.6

34.3

24.421.7

13.512.313.1

Total owned by farm households

1.37 million households in 2010

900,000 households in 2010

1.63 million households in 2010

524483 461 459 456

535456 424 423 419

102.0

94.5 92.1 92.2 91.9

50

60

70

80

90

100

110

300

400

500

600

700

1990 2000 2009 2010 2011

%

Aggregate planted area of crop

Utilization rate of cultivated land (right scale)

00

Cultivated land area

10,000 hectares

0.4

1.2 0.9 0.8 0.7 0.7

1.01.0 0.8 0.8 0.7

-4

-3

-2

-1

0

1

2008 2009 2010 2011 2012

Damaged by natural disaster

Abandonment of cultivation

Transformation of farmlands into industrial or residential lands

Development for cultivation

Others

Recovery

1.71.7

0.60.2

10,000 hectaresExpansion

Reduction 3.3

462.8 460.9 459.3 456.1 454.9

440 450 460 470

10,000 hectares

Cultivated land area0

Japan’s cultivated land area has trended down due to the transformation of some farmlands into industrial lands and elimination through abandonment of cultivation. In 2011, the cultivated area declined by 17,000 hectares due primarily to the tsunami waves caused by the Great East Japan Earthquake. In 2012, however, farmlands totaling 4,000 hectares were recovered.

The utilization rate of cultivated land has remained around 92% over recent years. The rate in 2011 fell by 0.3 percentage point from the previous year as the rice planted area decreased in locations affected by the Great East Japan Earthquake and the Tokyo Electric Power Co. Fukushima Daiichi Nuclear Power Plant accident, despite an increase in the area for feed crop planting at paddy fields.

Source: MAFF, “Statistics on Cultivated Area and Planted Area” Note: Utilization rate of cultivated land: Total planted area/

cultivated land area x 100

Changes in utilization rate of cultivated land

The abandoned cultivated land area has increased rapidly due to elderly farmers’ retirement. Particularly, abandoned cultivated land lots owned by land tenure non-farm households have expanded rapidly,

accounting for half of the total.

Changes in abandoned cultivated land area by farm household category

Source: MAFF, “Census of Agriculture and Forestry” Notes: 1) Numbers in parentheses at the right end represent total numbers of farm households including those that have no

abandoned cultivated land. 2) In and before 1985, farm households had not been divided into commercial and noncommercial farm households.

Changes in cultivated land area and breakdown by cultivated land reduction or expansion factor

Source: MAFF, “Statistics on Cultivated Area and Planted Area”

17

18

Source: MAFF Notes:1)* These municipalities have communities that have already prepared “Farmers and Farmland Plans.”

2) In parentheses are the four categories’ percentage shares of the total number of municipalities about to prepare “Farmers and Farmland Plans.”

In order to solve regional problems between farmers and farmlands, “Farmers and Farmland Plans” have been being prepared since FY2012 to specify how to integrate farmlands for future leading farms and how to develop regional farming through thorough discussions among local and regional farmers.

As of March 2013, municipalities that had already prepared such plans had accounted for 84% (7,573 communities) of those willing to create such plans.

Progress in preparation of “Farmers and Farmland Plans” (at the end of March 2013)

2 Measures for solving problems between farmers and farmlands

3 Developing and conserving agricultural production infrastructure Agricultural irrigation facilities have been deteriorating on a nationwide basis. About 20% of major irrigation

facilities have already exceeded their respective standard durable years. In order to make the national land more resilient, Japan should promote measures to lengthen service lives and enhance resistance against earthquakes for deteriorated irrigation facilities and measures against torrential rains.

Of paddy fields totaling 2.5 million hectares in Japan, about 60% have been integrated into 30-ares or larger partitions. Only about 10% have been integrated into large (approximately 1-hectare or larger) partitions. About one-third of integrated paddy fields have unfavorable drainage conditions. Japan should promote the integration and improvement of paddy fields to accelerate farmland integration for business farmers and increase value added for agriculture.

Facilities that have already exceeded the standard

durable years: 3.1 trillion yen (17% of total)

Adding those that will exceed the

standard durable years in the next

decade to the above: 5.6 trillion yen (31% of total)

State of paddy fields improvement (2011)

Sources: MAFF, “Statistics on Cultivated Area and Planted Area” and “Basic Survey on Agriculture Infrastructure Information”

Notes: 1) Integration-completed paddy fields mean those that have been integrated into 30-ares or larger partitions (large-scale partitions are 1 hectare or larger).

2) Favorable drainage conditions represent a groundwater level of 70 centimeters depth or deeper and the removal of flooding within four hours.

State of outdated major irrigation facilities (2009)

Source: MAFF, “Basic Survey on Agriculture Infrastructure Information”

*: An asset value of major irrigation facilities (agricultural irrigation facilities benefitting from 100 hectares or more) (on a reconstruction cost basis)

[Resident participatory management] Farmers expand paddy partitions by removing ridges and conduct underdrainage construction on their own to expeditiously improve infrastructure at lower cost.

Expanding a paddy partitions by

removing ridges

Underdrainage construction

Favorable water drainage conditions

1.06 million hectares

Unfavorable drainage conditions

490,000 hectares

Paddy fields totaling 2.47 million hectares

Multipurpose paddy fields

Before-integration paddy fields: 920,000 hectares (37%)

Integration-completed paddy fields: 1.55 million hectares (63%)

Large-scale partitions:

210,000 hectares (8%)

State-run facilities

0.8 Prefecture-run and other

facilities 2.3

Prefecture-run and other

facilities 1.7

State-run facilities

0.8Total at

17.9 trillion yen*

(Unit: trillion yen)

(Unit: municipalities)

Hokkaido 171 167 (98%) 161 (94%) 158 (92%) 158 (92%)Tohoku 210 208 (99%) 185 (88%) 173 (82%) 173 (82%)Kanto 376 358 (95%) 302 (80%) 291 (77%) 289 (77%)Hokuriku 79 79 (100%) 77 (97%) 77 (97%) 77 (97%)Tokai 117 114 (97%) 103 (88%) 90 (77%) 89 (76%)Kinki 152 143 (94%) 125 (82%) 115 (76%) 113 (74%)Chugoku/Shikoku 195 195 (100%) 178 (91%) 171 (88%) 170 (87%)Kyushu/Okinawa 260 260 (100%) 250 (96%) 243 (93%) 243 (93%)Total for entire Japan 1,560 1,524 (98%) 1,381 (89%) 1,318 (84%) 1,312 (84%)Number of communities 17,481 communities 7,573 communities

Number of municipalitieswilling to create "Farmers

and Farmland Plans"

Progress in preparation

Number of municipalitiesthat have almost

completed explanationsto local communities

Number of municipalitieswhere farmers in local

communities havestarted talks

Number of municipalitiesthat have opened meetings to

consider "Farmers andFarmland Plans"

Number ofmunicipalities that haveprepared "Farmers and

Farmland Plans"*

18

0

2

4

6

8

10

12

1984 1990 2000 20082010

2011

1.8 (22%)

Vegetables

Fruits

Livestock products

Others

Rice

2.1 (26%)

0.7 (9%)

2.6 (31%)

1.0 (12%)

11.5

8.2

11.7Trillion yen

8.1

3.9(34%)

2.0(17%)

0.9(8%)

3.3(28%)

1.6(14%) 9.1 8.5

566

13,041

27,796

40,311

34,521

0

10,000

20,000

30,000

40,000

50,000

2008 crop

2009 2010 2011 2012

tons

122 113 97

116

22 11 5

6 5 3 127

119 123 130

108 105 103 104

19 14 20 26 0

20

40

60

80

100

120

140

2008 2009 2010 2011

1,000 yen/10 ares

Sales income, etc.Mutual relief indemnity, subsidies, etc.

(excluding income support direct payments)Income support direct paymentsAgricultural

expenditure

Agricultural income

Agr

icul

tura

l gro

ss in

com

e

(Unit: 10,000 yen)2009 2010 2011

Total 104 122 120Rice farming 35 48 51Upland fieldfarming

217 217 231

Outdoor vegetablefarming

177 195 177

Facility-basedvegetable farming

382 441 413

Orchard farming 145 172 171Dairy farming 768 720 656Cattle farming 122 206 168Hog farming 396 658 629

Japan’s total agricultural output has trended down since 1984, standing at 8.2 trillion yen in 2011. Rice’s share of the total output has trended down, while the shares for livestock products and vegetables have followed an upward trend.

Agricultural income of farms (individual farms) in 2011 decreased by 2% from the previous year to 1.2 million yen. Among farm categories, rice farming farms boosted income by 6% thanks to rice price hikes. Meanwhile, dairy farming farms saw an income decline due to feed and fuel cost hikes.

Changes in agricultural income by farming category (individual farms)

Source: MAFF, “Statistical Survey on Farm Management – Statistics by Farming Category (individual farms)”

Changes in total agricultural output

Source: MAFF, “Agricultural Production Income Statistics”

4 Agricultural output and income trends

5 Production trends for major farm and livestock products (1) Rice

Changes in planned rice production for flour

In 2012, the rice crop condition index stood at 102 (the index was as high as 107 for Hokkaido and 103 for Tohoku while being as low as 97 in Kyushu due to sunlight shortages in June and damage inflicted by Typhoon No. 16).

The rice farming division’s agricultural gross income in 2011 increased by 7,000 yen per 10 ares or 6% from the previous year due primarily to rice price hikes. In line with this rise, agricultural income expanded by 6,000 yen per 10 ares or 30%.

Rice production for flour increased to 40,000 tons in 2011 before falling 14% from the previous year to 35,000 tons in 2012 due to slower growth in demand for rice flour products.

Changes in rice farming division’s agricultural gross income and agricultural income

Source: MAFF, “Statistical Survey on Farm Management – Statistics by Farming Category”

Source: MAFF, “Certification of Plans for New-use Rice”

19

(Unit: hectares)

2009 crops 2012 Change( )

Entire Japan 145,400 131,100 -14,300 49,949Hokkaido 24,500 27,200 2,700 1,221Mie 3,360 4,120 760 664Shiga 5,430 5,700 270 825Gifu 2,690 2,780 90 684Hyogo 2,670 2,700 30 484Akita 10,100 7,620 -2,480 2,000Miyagi 11,500 9,040 -2,460 2,497Tochigi 4,830 2,710 -2,120 4,884Yamagata 7,250 5,640 -1,610 2,266Niigata 7,140 5,630 -1,510 3,753

Planted area for soybeans

Upp

erLo

wer

Change inplanted areafor rice for newuses(2009-2012)

548 1,128

463

933

300

538

331

457

1,441

2,930

0

500

1,000

1,500

2,000

2,500

3,000

FY2007 FY2009 FY2011

hectares

Other fruitsOther citrus fruits

Apples

"Satsuma" mandarins

(Units: hectares, %)2008crops

2009 2010 2011 2012

Planted area 208,800 208,300 206,900 211,500 209,200115,700 116,300 116,300 119,200 119,200

Hokushin 103,756 96,373 72,901 545 21Kitahonami - 6,888 29,636 106,948 104,628

16,882 17,726 20,210 21,550 25,949

(8.1) (8.5) (9.8) (10.2) (12.4)

Yumechikara - - 56 159 1,214Haruyokoi 6,760 6,500 7,098 7,774 9,539Yumekaori - 4 43 251 416Chikushi W2-go - 149 566 767 880

Hokkaido

Wheat for bread andChinese noodles(share)

(3) Vegetables, fruits

Trends of accumulated area for switching to higher-quality fruit species or varieties

Source: MAFF Note: The area for switching means the area for plans approved under

the orchard management support project.

As for outdoor vegetable farming, the development and diffusion of new agricultural machines have been promoted to save costs and labor according to demand for vegetables being used for processing and commercial uses. Recently, integrated mechanized systems have been developed and commercialized progressively for spinaches, cabbages and other vegetables.

In orchard farming, it is important to enhance local fruit producers’ competitiveness and profitability through production and supply of high-quality fruits. To this end, producers have been switching to excellent species or varieties according to consumer needs. In FY2011, the accumulated area for such switching came to 2,930 hectares.

Machine commercialized for harvesting spinaches for processing in 2011

The machine harvests only the above-ground part separated from roots that are not necessary for processing. Harvesting time has been reduced to one-tenth.

Machine to be commercialized for harvesting cabbages for processing and commercial uses in 2013 The machine uses a precision system to harvest, select and adjust massive

cabbages for direct accommodation into large containers, reducing adjustment and shipment labor.

Excellent brand case (Shiranuhi (Dekopon))

(2) Wheat, soybeans Japan’s wheat-planted area in 2012 came to 209,000 hectares, of which Hokkaido accounted for 60% (119,000

hectares). The main brand in Hokkaido has shifted from Hokushin to Kitahonami, a high-quality, high-yielding variety.

Wheat for bread and Chinese noodles increased to 26,000 hectares or 12% of the total wheat-planted area. As the soybean-planted area has followed a downward trend since 2009, prefectures posting large declines have

tended to increase the planted area for rice for new uses. Meanwhile, the planted area for soybeans has increased in prefectures like Mie where local communities have been united to promote organized aggregative farming of paddy fields.

Changes in planted area for wheat

Sources: MAFF, “Crop Statistics” and MAFF surveys

Changes in planted area for soybeans since 2009

Sources: MAFF, “Crop Statistics” and MAFF surveys

20

425

353 308

269 257 249 243 257

227 219 177 110

51 42 38

0 50

100 150 200 250 300 350 400 450

2004 2006 2008 2010 2011

1,000 yen/10 ares Agricultural expenditure

Agricultural income

Agricultural gross income