FY NPA MANAGEMENT POLICY - Kerala Financial … · Corporation’s Non Performing Assets Management...

32

NPA MANAGEMENT POLICY 2009-10 1 KERALA FINANCIAL CORPORATION Vellayambalam, Thiruvananthapuram -33 FY 2009 -10 NPA MANAGEMENT POLICY

Transcript of FY NPA MANAGEMENT POLICY - Kerala Financial … · Corporation’s Non Performing Assets Management...

NPA MANAGEMENT POLICY 2009-10

1

KERALA FINANCIAL CORPORATION Vellayambalam, Thiruvananthapuram -33

FY

2009 -10 NPA MANAGEMENT POLICY

NPA MANAGEMENT POLICY 2009-10

2

N.P.A. MANAGEMENT POLICY - FY 2009-10

1. Introduction:

Upto the F.Y. 2008-09 the Corporation was having a Recovery Policy

with special stress on One Time Settlement scheme. Now the Board of the

Corporation has decided to dispense with the same policy w.e.f. F.Y. 2009-10

onwards. However it is observed that a number of sticky loan cases are still

pending with the Corporation in the Loss Assets and D3 Categories which

deserve Special consideration for negotiated settlement. As such it has

become imperative to have a new scheme for amicable settlement. Hence

Corporation’s Non Performing Assets Management Policy (KFC NPAMP) has

been formulated. Our NPA Management Policy seeks to lay down emphasis on

settlement of Non-Performing Assets (NPAs), and proactive initiatives to

prevent slippages in asset portfolio. The aim of the policy is to improve the

quality of assets.

2. Objectives of the Policy:

(a) To lay down a system for management of NPAs and to develop the

system into an effective tool to contain NPAs within the prudential limits.

(b) To outline the strategies to meet the goals in tune with R.B.I./SIDBI

directives and put in place necessary procedures complimentary to

recovery procedures, loan policy of the Corporation and other instructions

on the subject.

(c) For improving recovery, quality of loan assets by reducing NPA and

increasing profitability of the Corporation by reducing provisioning and

increasing interest income.

(d) For proper monitoring of industrial units to address their problems and to

help them for their survival.

(e) Preventive and timely corrective actions assume prime importance in

management of NPAs. Therefore, the policy proposes to have special

thrust on loan review mechanism, which will give early warning signals to

ensure effective and expeditious corrective measures.

(f) To lay down a liberalised approach for compromise settlement of NPAs.

NPA MANAGEMENT POLICY 2009-10

3

(g) To lay down broad approach for transfer of NPAs to Asset Reconstruction

Companies / Other institutions for reduction of NPA level.

3.3.3.3. Identification of NPAs:

The primary guiding factor for recognizing a non-performing asset will

be the Asset classification norms prescribed by RBI.

As per the norms, among other conditions, if interest and / or principal

instalments remain unpaid in a loan account for a period of 90 days or more

on the relevant date, the loan account concerned will be classified as NPA.

4.4.4.4. Steps to be taken to reduce NPA:

Each Branch Office should take the following steps to reduce the level

of NPA.

5. Standardization of accounts

(i) Interest Reduction Scheme:-

The Corporation has been giving interest reduction facility to its

existing clients provided 50% of the interest arrears is cleared. This scheme

was in operation during the last financial year. Interest collection is the

income of the Corporation and hence it has to be boosted up through some

incentive scheme. In order to increase the interest collection Corporation

may continue the same by giving interest reduction to those who clear 50%

of the interest arrears. In case of default 2% penal interest will be charged.

The interest rate applicable will be limited to prime lending rate. The period of

operation of the scheme may be extended upto 31.03.2010.

(ii) Reschedulement / Restructuring

a) Eligibility criteria for restructuring of advances :

Corporation may restructure the accounts classified under 'standard',

'sub-standard' and doubtful' categories. No accounts should be rescheduled /

restructured / renegotiated with retrospective effect. While a restructuring

proposal is under consideration, the usual asset classification norms would

continue to apply. The process of re-classification of an asset should not stop

merely because restructuring proposal is under consideration. The asset

classification status as on the date of approval of the restructured package by

NPA MANAGEMENT POLICY 2009-10

4

the competent authority would be relevant to decide the asset classification

status of the account after restructuring / rescheduling / renegotiation. In

case there is undue delay in sanctioning a restructuring package and in the

meantime the asset classification status of the account undergoes

deterioration, the same should be monitored and corrective measures taken.

Normally, restructuring can not take place unless alteration / changes

in the original loan agreement is made with the formal consent / application

of the debtor. However, the process of restructuring can be initiated by the

Corporation in deserving cases subject to customer agreeing to the terms and

conditions. No account will be taken up for restructuring by the Corporation

unless the financial viability is established and there is a reasonable certainty

of repayment from the borrower, as per the terms of restructuring package.

This should be done only after inspection of the unit by concerned F.Os. to

assess the repaying capacity. The accounts not considered viable should not

be restructured and Corporation should accelerate the recovery measures in

respect of such accounts. Any restructuring done without looking into cash

flows of the borrower and assessing the viability of the projects / activity

financed by Corporation would be viewed seriously.

The restructuring of such cases may be done with MD’s approval. For

restructuring BIFR cases, it should be ensured that all the formalities in

seeking the approval from BIFR are completed before implementing the

package.

b) Asset classification norms:

Restructuring of advances could take place in the following stages :

i) Before commencement of commercial production/operation;

ii) After commencement of commercial production/operation but before

the asset has been classified as ‘sub-standard’;

iii) After commencement of commercial production/operation and the

asset has been classified as ‘sub-standard’ or ‘doubtful’.

The accounts classified as 'standard assets' should be immediately re-

classified as 'sub-standard assets' upon restructuring. The non-performing

assets, upon restructuring, would continue to have the same asset

classification as prior to restructuring and slip into further lower asset

NPA MANAGEMENT POLICY 2009-10

5

classification categories as per extant asset classification norms with

reference to the pre-restructuring repayment schedule.

All restructured accounts which have been classified as non-performing

assets upon restructuring, would be eligible for up-gradation to the ‘standard’

category after observation of ‘satisfactory performance’ during the ‘specified

period’. Specified period means a period of one year from the date when the

first payment of interest or instalment of principal falls due under the terms

and conditions.

In case, however, satisfactory performance after the specified period is

not evidenced, the asset classification of the restructured account would be

governed as per the applicable prudential norms with reference to the pre-

restructuring payment schedule.

Any additional finance may be treated as ‘standard asset’, up to a

period of one year after the first interest / principal payment, whichever is

earlier, falls due under the approved restructuring package. However, in the

case of accounts where the pre-restructuring facilities were classified as ‘sub-

standard’ and ‘doubtful’, interest income on the additional finance should be

recognized only on cash basis. If the restructured asset does not qualify for

upgradation at the end of the above specified one year period, the additional

finance shall be placed in the same asset classification category as the

restructured debt.

In case a restructured asset, which is a standard asset on

restructuring, is subjected to restructuring on a subsequent occasion, it

should be classified as substandard. If the restructured asset is a sub-

standard or a doubtful asset and is subjected to restructuring, on a

subsequent occasion, its asset classification will be reckoned from the date

when it became NPA on the first occasion. However, such advances

restructured on second or more occasion may be allowed to be upgraded to

standard category after one year from the date of first payment of interest or

repayment of principal whichever falls due earlier in terms of the current

restructuring package subject to satisfactory performance.

c) Income recognition norms:

In the case of accounts classified as 'standard ‘ the income, if any,

generated by these accounts may be recognized on accrual basis. In the

case of restructured accounts classified as 'non-performing assets' the

NPA MANAGEMENT POLICY 2009-10

6

income , if any, generated by these accounts may be recognized only on

cash basis.

(iii) Rehabilitation:

In deserving cases rehabilitation of sick units to be made after

conducting detailed inspection and study by teams consisting of Technical

Officers. Based on the recommendation of the teams suitable package of

assistance to be extended to the units. Close follow-up and monitoring of

these units to be made by F.Os. during their periodic visits.

F.Os. should prepare status of these rehabilitated / rescheduled units

and submit to C.Ms. / Z.Ms. and ZMs who in turn should evaluate this report

and send to GM-I every month. Separate Register is to be maintained. As

per Circular No.7 dt. 16.4.2008 the Branch level S.C. chaired by BM/CM can

sanction loan upto Rs.250 lakhs and Zonal Level Committee chaired by Z.M.

can sanction above Rs.250 lakhs upto Rs.500 lakhs. The rehabilitation,

revival, reschedulement packages within this delegation can also be exercised

by BMs/CMs/ZMs.

6. Waiver of Penal interest (D1 & D2 Category).

For all Term loans in D1 & D2 category waiver of penal interest can be

considered for remitting the interest arrears or for exiting loan when the

project is not viable or the promoter is no more and the legal heirs wants to

wind up the business, as per the following limits.

Upto Rs.25,000 - BMs / CMs

Above Rs.25,000 to Rs.50,000 - ZMs

Above Rs.50,000 up to 10,00,000 - MD

Above Rs.10,00,000/- - EC/Board

7. Compromise Settlement Scheme:-

Compromise Settlement will be allowed only in those cases where all

efforts have failed to recover the dues. Wherever the compromise settlement

is expected to serve the best interest of the Corporation, Branch Level

Committee can give permission to process such applications*. For such

cases, the eligibility is as follows.

*Amended on 01.10.2009 (Item No. 116)

(i) Eligibility

NPA MANAGEMENT POLICY 2009-10

7

Where asset classification is Doubtful III and loss assets as at the end

of the immediately preceding FY (March 31st).

(OR)

The unit is in the possession of the Corporation for more than 1 year

immediately preceding the date on which the Compromise Settlement

proposal is considered by the Branch level Compromise Settlement

Committee.

(OR)

Units in which the assets have been advertised 3 times but no

reasonable offer has been obtained.

(OR)

In cases where the loanee has remitted atleast 75% of the principal

amount during the loan period, the Compromise Settlement amount as per

NSR and yield method have to be compared with and can be considered for

settlement at the lower amount. All other guidelines applicable to

Compromise Settlement cases are applicable to these cases also.

(ii) Conditions to be followed:

α) All DIII cases as on 01.04.09 and continuing in the same category as

on date of approaching for Compromise Settlement and all loss assets

are eligible for Compromise Settlement.

β) The default shall not be willful.

χ) Borrowers who have involved in fraudulent practices will not be eligible

for Compromise Settlement. However the Co-obligants if any who

have mortgaged their properties to the Corporation will be able to

approach the Corporation for Compromise Settlement.

(iii) Compromise Settlement Formula:

Guidelines:

It was observed that though major portion of advances are secured by

collateral, but past experience of the Corporation shows that recovery of dues

through realisation of such collateral (mostly residential houses of low income

group) is very low. Hence a liberal Compromise Settlement scheme as below

is proposed.

NPA MANAGEMENT POLICY 2009-10

8

a) Loans upto Rs. 2/- lakhs: D3 Loans upto Rs.2/- lakhs (Rupees Two

lakhs only) disbursed can be settled for Principal outstanding plus other

expenses irrespective of the Security position of the assets.

b) D3 loans above Rs.2/- lakhs but below Rs.10/- lakhs:

i) D3 loans above Rs. 2 lakhs & upto Rs. 5 lakhs.

Table I

Sl.

No.

Amount Disbursed Value of primary + Collateral security as %

of P + I + OE + NSR is

Upto 100% Above 100%

1 Above Rs.2/- lacs to Rs.5/-

lacs

* P + I + OE +

20% NSR

* P + I + OE + 50%

NSR. (*) Principal Write Off only with permission of Board.

ii) D3 loans above Rs.5/- lacs and upto Rs.10/- lacs.

Table II

Sl.

No. Amount Disbursed

Value of primary + Collateral

security as % of P +I+ OE +

NSR is

One or more

Promoters/

Guarantors/ Co-

obligants to get

relieved of liability

Upto 100% Above 100%

1 Above Rs.5/- lacs

and upto Rs.10/-

lacs

P+I+OE+50%

NSR P+I+OE+ NSR P+I+OE

(iv) Definitions for NSR Calculation:

P = Principal outstanding on the date of Calculation of Compromise

Settlement.

I = Interest accrued as on NPA date.

OE = Other expenses outstanding on the date of calculation of

Compromise Settlement.

NSR = Net Simple Interest rate to be realized.

Net Simple Interest Rate amount is arrived by Calculating the Interest

at Simple rate at documented rate from the date of the account becoming

NPA and not from the date of first disbursement and till the date of

application for Compromise Settlement and deducting from this amount, the

amount of interest already paid after becoming NPA. This balance arrived

NPA MANAGEMENT POLICY 2009-10

9

shall be the Net Interest payable (NSR) to be added to the Principal and Over

head expenses.

However, if NSR is less or negative it shall not be credited to the

Principal. In such cases the settlement should be at Principal + other

expenses outstanding. There shall be no Principal Write off.

c) For loans above Rs. 10/- lakhs:

i) D3 loans above Rs. 10 lakhs having Primary or collateral

security:

Table III

Sl.

No

Amounts

Disbursed

Value of Primary and Collateral Security as percentage to the

Principal+I+ OE+NSR Interest amount is

More

than

150%

Bet-

ween

125% -

150%

Bet-

Ween

100%

-

125%

Between 75

– 100% and

Between 50-

75% and

Less than 50%

and

Repaying

Capacity

worth &

standing of

Promoters &

Guarantors is

Repaying

Capacity

worth &

standing of

Promoters &

Guarantors is

Repaying

Capacity worth

& standing of

Promoters &

Guarantors is

High Mod &

Low

High Mod &

Low

High Mod &

Low

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

1

Above

Rs.10/-lakhs

General

Package

P+I+

OE+

(NSR+

3%)

P+I+O

E+

(NSR+

2%)

P+OE

+

NSR

P+I+

OE+

90%

NSR

P+I+

OE+

80%

NSR

P+I+

OE+

75%

NSR

P+I+

OE+

65%

NSR

P+I+

OE+

60%

NSR

P+I+

OE+

50%

NSR

Note:

1) If units are abandoned and closed then the B.M and Field Officers shall

jointly certify the fact.

2) Current Valuation Certificate to be attached with the Compromise

Settlement Proposal.

3) For valuation primary and collateral security available is between 125%

and 150% of principal outstanding at the time of Compromise Settlement

NPA MANAGEMENT POLICY 2009-10

10

application + Interest accrued as on NPA date + other expenses + the

eligible NSR, add 2% of NSR amount to arrive at the minimum

Compromise Settlement amount.

4) For valuation primary and collateral security available is more than 150%

of principal outstanding at the time of Compromise Settlement application

+ Interest accrued as on NPA date + other expenses + the eligible

NSR, add 3% of NSR amount to arrive at the minimum Compromise

Settlement amount.

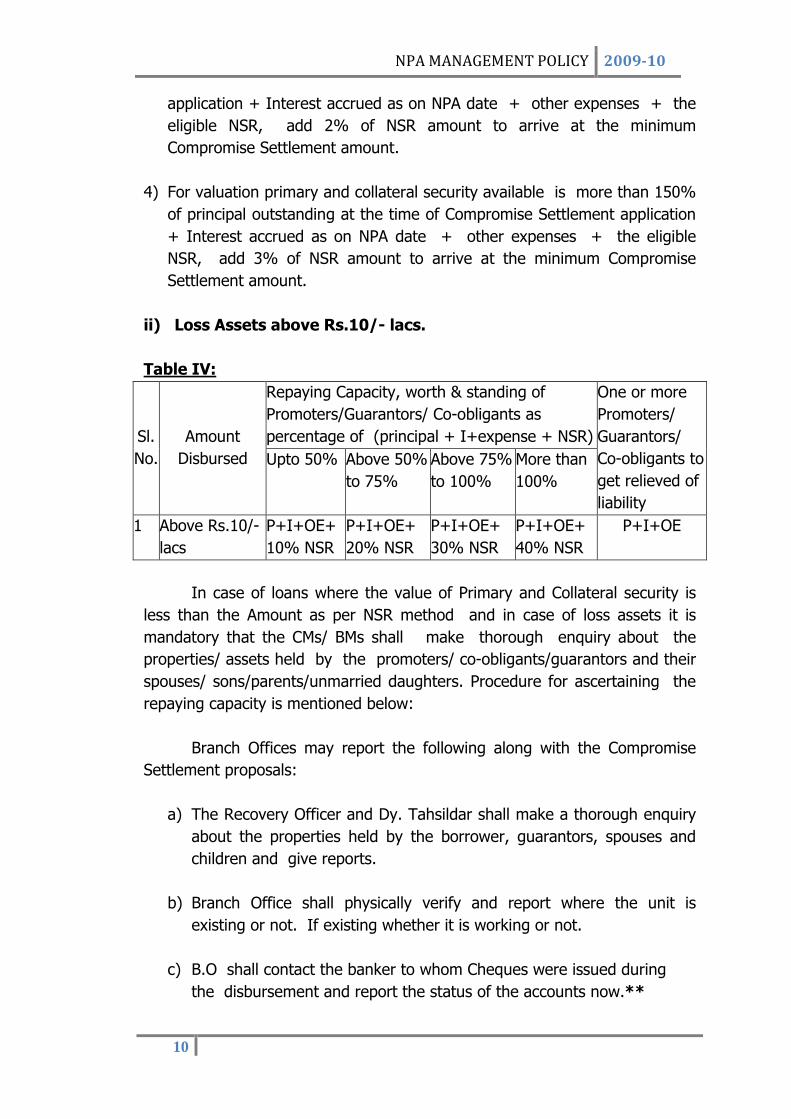

ii) Loss Assets above Rs.10/- lacs.

Table IV:

Sl.

No.

Amount

Disbursed

Repaying Capacity, worth & standing of

Promoters/Guarantors/ Co-obligants as

percentage of (principal + I+expense + NSR)

One or more

Promoters/

Guarantors/

Co-obligants to

get relieved of

liability

Upto 50% Above 50%

to 75%

Above 75%

to 100%

More than

100%

1 Above Rs.10/-

lacs

P+I+OE+

10% NSR

P+I+OE+

20% NSR

P+I+OE+

30% NSR

P+I+OE+

40% NSR

P+I+OE

In case of loans where the value of Primary and Collateral security is

less than the Amount as per NSR method and in case of loss assets it is

mandatory that the CMs/ BMs shall make thorough enquiry about the

properties/ assets held by the promoters/ co-obligants/guarantors and their

spouses/ sons/parents/unmarried daughters. Procedure for ascertaining the

repaying capacity is mentioned below:

Branch Offices may report the following along with the Compromise

Settlement proposals:

a) The Recovery Officer and Dy. Tahsildar shall make a thorough enquiry

about the properties held by the borrower, guarantors, spouses and

children and give reports.

b) Branch Office shall physically verify and report where the unit is

existing or not. If existing whether it is working or not.

c) B.O shall contact the banker to whom Cheques were issued during

the disbursement and report the status of the accounts now.**

NPA MANAGEMENT POLICY 2009-10

11

d) B.O to report if proceedings against the unit has been initiated by

authorities like Panchayat/ Revenue/ Sales Tax/ Income Tax/ Bankers/

KSEB/ other lenders.**

e) A notarized affidavit from the borrowers/ guarantors specifying the

financial status/ assets at the time of applying for Compromise

Settlement to be produced.

f) Where borrowers have filed cases in Courts/ DRT, if Court cases can

be withdrawn and then out of Court settlement can be preferred for

Compromise Settlement.

** Deleted on 01.10.2009(Item No. 116)

(v) Mode of Payment:

Application for Compromise Settlement need be registered only if

Compromise Settlement advance computed at 10% of balance outstanding

or 25% of principal outstanding(whichever is less) is remitted. In cases

where the mortgaged assets have been sold or proprietor expired, 50% of

the Compromise Settlement advance need only be paid i.e for this category

Compromise Settlement advance is 12.5% of principal outstanding or 5% of

balance outstanding which ever is less. The amount has to be kept in

Compromise Settlement appropriation account. No application should be

processed without Compromise Settlement advance as above. If there is any

court direction giving relaxation to the above condition the same shall be

brought to the notice of the Managing Director before processing the

Compromise Settlement application. Normally 3 months time from the

date of sanction by appropriate authority will be given for remittance. No

interest will be charged during this period.

A lot of work involving several man-hours of officers at all levels go

into a Compromise Settlement proposal. Further in most of the Compromise

Settlement cases the loanee will not be having the required liquidity and will

be raising resources through sale of assets which may not materialise within

the above period of 3 months due to circumstances beyond the control of the

loanee. Hence it is recommended that CM/BM may be empowered to allow

extension of the period allowed for Compromise Settlement, upto a further

period of 9 months with belated interest provided atleast 12% (Twelve

percent) of the balance Compromise Settlement amount to be paid is remitted

within the period of 3 months allowed. The above 12% is in addition to the

NPA MANAGEMENT POLICY 2009-10

12

Compromise Settlement advance remitted at the time of submitting the

proposal.

(vi) Date of processing Compromise Settlement Calculation:-

The calculation will be taken as on 1st of the month in which

Compromise Settlement proposal is finalised and should include interest not

due.

(vii) Delegation of Powers of sacrifice for Compromise Settlement:

The revised delegation will be as follows:-

Managing Director - Sacrifice up to Rs.10 lakhs

E.C. - Sacrifice of Rs.10 lakhs to Rs.25 lakhs

Board - Sacrifice more than Rs.25.00 lakhs.

(viii) Waiver of Belated Interests on Compromise Settlement

amount :-

i) Branch/Chief Managers – waiver of belated interest upto Rs.25,000/-

ii) Zonal Managers – waiver of belated interest upto Rs.50,000/-.

iii) Managing Director - waiver of belated interest subject to maximum of

Rs.10.00 lakhs.

iv) Above and over Rs.10.00 lakhs to be taken to the Board / E.C.

(ix) Waiver of Penal Interest on D III Cases:

i) Branch/Chief Managers – waiver of penal interest upto Rs.25,000/-.

ii) Zonal Managers – waiver of penal interest upto Rs.50,000/-.

iii) Managing Director - waiver of penal interest subject to maximum of

Rs.10.00 lakhs.

iv) Above and over Rs.10.00 lakhs to be taken to the Board / E.C. 8. Identification and review of potential NPA accounts:

NPA MANAGEMENT POLICY 2009-10

13

S1 accounts which are in arrears for more than 30 days may be

monitored closely. Such type of accounts are to be identified and corrective

action taken from the inception onwards to avoid deterioration in asset

quality.

i) Early warning signals like irregularity in accounts, default in repayment

obligations, operating losses, rejection of products, diversion of funds,

keeping machines idle, number of shifts/ workers decreasing etc.

should be watched. Problems arising out of regulatory changes may

also be watched to identify such accounts.

ii) Auditors report forms an essential source of information for

identification and management of NPAs. Audit reports such as Internal

Audit Report, Concurrent Audit Report, SIDBI Audit Report, Statutory

Auditors Report, AGs Audit Report, etc. are to studied and timely

action taken for the management of NPAs.

iii) A review and reporting system for the timely identification and

management of NPAs is introduced and report to be furnished on

a monthly basis as per format given at Annexure-VII.

Review and Reporting System at Branch Level Committee.

Our basic strategy is to initiate appropriate preventive/corrective action

at the right time to prevent slippages of accounts to NPAs. Once the problem

loans are identified, steps are to be taken immediately to analyse the

problems based on facts and circumstances by means of a review technique

at the Branch Level.

Functions:

The important functions of the Branch Level Review are as follows:

a. Diagnose the reasons for the deterioration in asset quality and put the

unit under close monitoring.

b. Review the assumptions made at the time of sanction of the credit

facilities and see that whether they are matching with the actuals.

c. Ascertain the cash generation in the business.

NPA MANAGEMENT POLICY 2009-10

14

d. Bring the deviation / situation to the notice of the borrower and co-

obligants. Call up on them to regularize the accounts or remedy the

situation and prescribe corrective steps.

e. Ascertain the availability of other source of repayments and make use

of situation.

f. Obtain realistic and time bound commitments from the borrower / co-

obligants to arrest the deterioration in the quality of the loan.

g. Discuss with the borrower and determine corrective course of action

required for the upgradation / recovery of the loan.

The aforesaid functions are to be carried out by the F.Os and reports

given to the BM/CM monthly and the reports should be consolidated by the

recovery head and place in the Branch Level Committee. The decision of the

BLC should be submitted to DGM/AMO/ZM monthly basis. Remedial action

should be initiated by a committee consisting of DGM/AMO and ZM. If the

matter cannot be sorted out at Branch Level/Zonal level, report the matter to

GM-I who will place the matter before the HPC. Cases which are to be

reported to the EC/Board will be placed after review by the HPC in the H.O.

9. General Guidelines:

The Branch Level and Zonal level officers will strive hard to settle the

cases under Compromise Settlement as per the policy approved now. If any

of the loans cannot be settled as per general rules of the policy it may be

placed before the HPC. After the HPC, sacrifice above Rs.10 lakhs may be put

up to EC/Board.

1) Time frame for Processing Compromise Settlement Applications:-

B.O - 15 days.

MD’s level - 10 days

HPC cases - 15 days

Board / EC - 1 month

2) Time frame for informing the Client for Compromise Settlement

sanction.

α) Within two days of receipt of MD’s order

β) Within 7 days of receipt of HPC/ Board minutes for action.

NPA MANAGEMENT POLICY 2009-10

15

3) For recommendation of waiver of belated interest of already sanctioned

Compromise Settlement cases any of the conditions (a to g) may be

satisfied. *

a) Borrowers / Co-obligants are financially poor (to be certified

by Branch Level Committee). *

b) Borrowers/ co-obligants have no other property other than

residential property.

c) Borrowers/ co-obligants are critically sick and being treated for

terminal diseases.

d) Borrower/ co-obligants have absconded/ abandoned the assets.

e) Borrowers/ co-obligants are dead and legal heirs are coming to

settle the debts.

f) Where primary or collateral assets have been seized and sold by

the Corporation/ Revenue Authorities before sanction of

Compromise Settlement.

g) If the Branch Level Committee is of the opinion that the

promoter has suffered heavy losses by venturing into the

project. (New clause added)*

*Amended on 01.10.2009 (Item No.116)

4) The RR Commission if charged by the RR authorities has to be paid by

the loanee. This should be communicated to the loanee.

5) Compromise Settlement cases already sanctioned will not be reopened.

6) Belated interest:-

Normally Compromise Settlement is allowed for 3 months only.

Coercive action has to be initiated / continued in case the remittance is not

made within 3 months. Some times the loanees are not able to pay the

Compromise Settlement amount due to various constraints like selling of

property which takes time, and mobilisation of resources from friends and

relatives, raising funds from other institutions, etc. In genuine cases the time

for payment of Compromise Settlement amount can be extended by 6

NPA MANAGEMENT POLICY 2009-10

16

months by CM/BM/ZM (ie. above 3 months and upto a period of 9

months) by payment of belated interest and above 9 months up to 12

months by M.D. by payment of belated interest. However, in the best

interest of the Corporation M.D. can revive the Compromise

Settlement even after the expiry of 12 months based on merits.

No interest will be charged if Compromise Settlement amount is remitted

within 3 months from the date of sanction of Compromise Settlement.

Interest at 12% simple interest will be charged for the period

exceeding three months and up to 12 months. Interest on delayed

belated interest amounts pending will also attract 12% Simple interest till

date of settlement.

(The condition that "12% of the Compromise Settlement

amount (excluding advance) be remitted within 1st three

months" is dispensed with in view of difficulty faced by the

loanees)*.

* Amended on 01.10.2009 (Item No.116)

7) For the purpose of waiver of penal interest the expiry of loan period will

be reckoned as per original schedule.

8) Under no circumstances shall Compromise Settlement result in reful of

remittances already received by the Corporation.

9) Principal Write Off shall be allowed only in exceptional cases with

approval of the Board.

10) If for any reason it is felt that the interests of the Corporation will be

best served by settling the account under Compromise Settlement by

allowing relaxation in norms, such cases have to be compulsorily

referred to the Board/Committee of the Board. The minutes of the

Branch/Zonal/H.O. level Committee recommending such cases should

clearly spell out the deviation from norms and justification/reasons for

recommending Compromise Settlement despite the deviations.

11) Any proposal for modification to the policy shall be placed before the

Board and if approved shall be circulated as substitution of/addition to

the existing chapter/paragraph.

NPA MANAGEMENT POLICY 2009-10

17

12) Compromise Settlement shall not be allowed for NEF portion of loans

and other loans for which Compromise Settlement is not being allowed

in the Corporation.*

*Amended on 01.10.2009 (Item No.116)

13) The Compromise Settlement scheme shall be kept open up to March 31,

2010.

14) The applications received during the above period along with the

required advance need only be considered for Compromise Settlement.

15) Time limit for cancellation of Compromise Settlement:

Compromise Settlement approved shall be cancelled if the default

exceeds 90 days from the approved schedule at any stage. However

in the best interest of the Corporation M.D. can revive the

Compromise Settlement. (New clause added). *

* Amended on 01.10.2009 (Item No. 116)

16) a) BIFR/ AAIFR Cases: In respect of BIFR/ AAIFR cases the

Compromise Settlement packages shall be awarded in the light of

decisions taken in the consortium meetings subject to final approval of

the Board of Directors.

b) Consortium: In respect of Consortium cases the Compromise

Settlement packages shall be awarded in the light of decision taken in

joint meetings and after the approval of the Board of Directors.

17) Compromise Settlement amount prescribed are minimum: It is reiterated

that amount prescribed for settlement in the tables are only the

minimum amounts. All concerned shall negotiate for higher amounts

depending on the value of available securities, solvency and repaying

capacity of the borrower / guarantors / co-obligants / legal heirs.

18) Withdrawal of earlier Office Orders & Circulars on Compromise

Settlement Scheme:

The revised Compromise Settlement Guideline above supersedes all

earlier guidelines on Compromise Settlement issued earlier.

NPA MANAGEMENT POLICY 2009-10

18

19) Clarifications and Interpretations: Clarifications if any, on the N.P.A. Management Policy shall be referred to Managing Director/GM for

interpretation and approval.

20) Further loans for Promoters involved in Compromise Settlement cases:

Anyone who has obtained Compromise Settlement shall not be eligible

for future loans from the Corporation. However, where the promoters

have settled their loan accounts eligible for further loan under

Compromise Settlement due to failure of units and reasons beyond their

control. approval from M.D. may be obtained before such applications

are accepted.

MANAGING DIRECTOR

NPA MANAGEMENT POLICY 2009-10

19

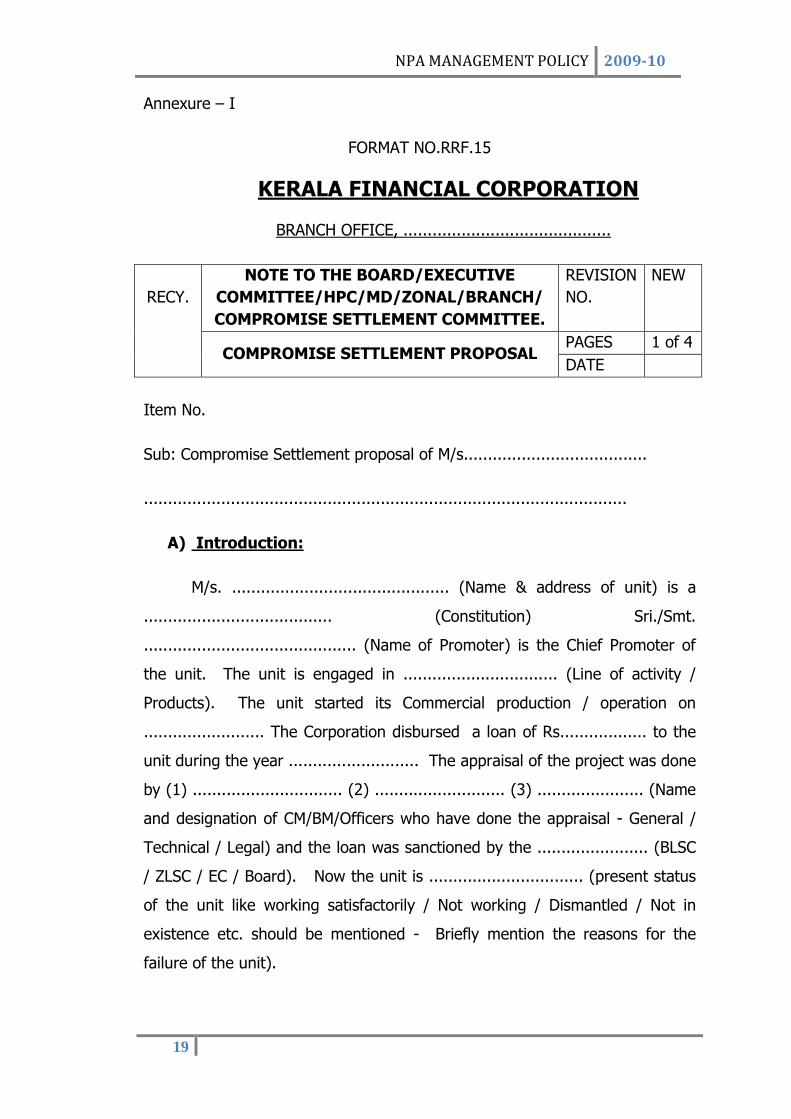

Annexure – I

FORMAT NO.RRF.15

KERALA FINANCIAL CORPORATION

BRANCH OFFICE, ...........................................

RECY.

NOTE TO THE BOARD/EXECUTIVE

COMMITTEE/HPC/MD/ZONAL/BRANCH/

COMPROMISE SETTLEMENT COMMITTEE.

REVISION

NO.

NEW

COMPROMISE SETTLEMENT PROPOSAL PAGES 1 of 4

DATE

Item No.

Sub: Compromise Settlement proposal of M/s......................................

....................................................................................................

A) Introduction:

M/s. ............................................. (Name & address of unit) is a

....................................... (Constitution) Sri./Smt.

............................................ (Name of Promoter) is the Chief Promoter of

the unit. The unit is engaged in ................................ (Line of activity /

Products). The unit started its Commercial production / operation on

......................... The Corporation disbursed a loan of Rs.................. to the

unit during the year ........................... The appraisal of the project was done

by (1) ............................... (2) ........................... (3) ...................... (Name

and designation of CM/BM/Officers who have done the appraisal - General /

Technical / Legal) and the loan was sanctioned by the ....................... (BLSC

/ ZLSC / EC / Board). Now the unit is ................................ (present status

of the unit like working satisfactorily / Not working / Dismantled / Not in

existence etc. should be mentioned - Briefly mention the reasons for the

failure of the unit).

NPA MANAGEMENT POLICY 2009-10

20

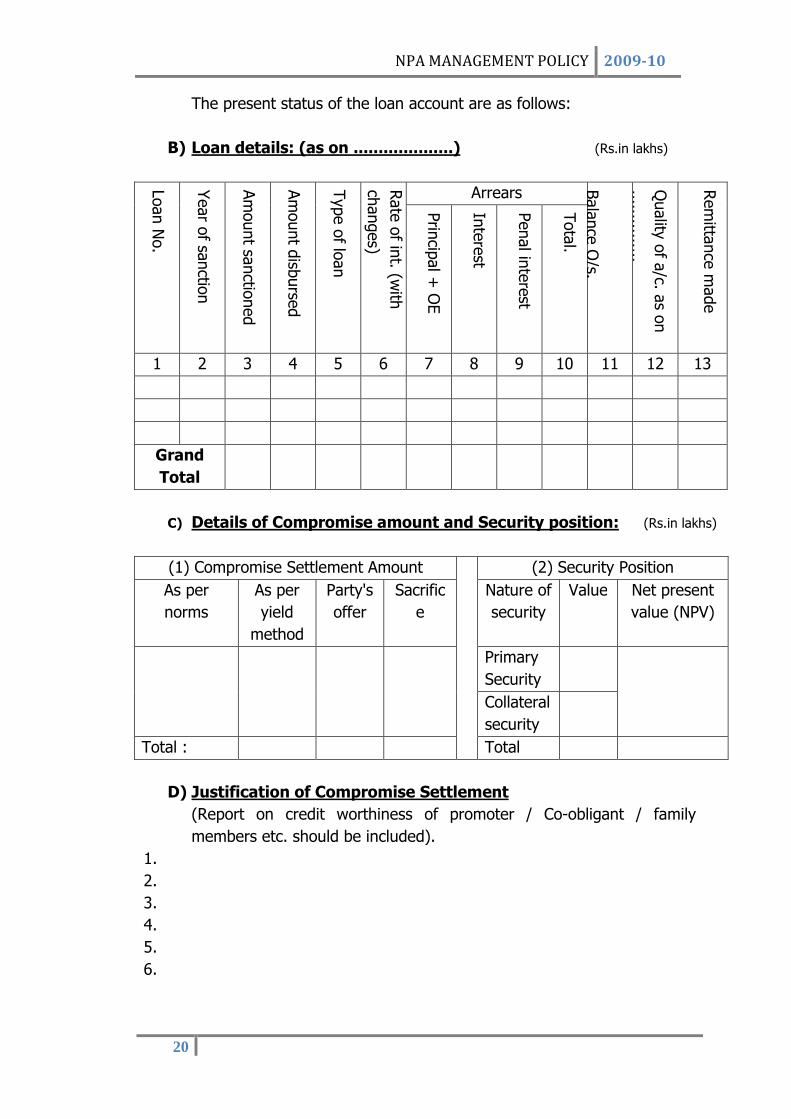

The present status of the loan account are as follows:

B) Loan details: (as on ....................) (Rs.in lakhs)

Loan N

o.

Year o

f sanctio

n

Amount sa

nctio

ned

Amount d

isburse

d

Type of lo

an

Rate of in

t. (with

changes)

Arrears Balance

O/s.

Quality

of a

/c. as o

n

...............

Remitta

nce

made

Prin

cipal +

OE

Interest

Penal in

terest

Total.

1 2 3 4 5 6 7 8 9 10 11 12 13

Grand

Total

C) Details of Compromise amount and Security position: (Rs.in lakhs)

(1) Compromise Settlement Amount (2) Security Position

As per

norms

As per

yield

method

Party's

offer

Sacrific

e

Nature of

security

Value Net present

value (NPV)

Primary

Security

Collateral

security

Total : Total

D) Justification of Compromise Settlement

(Report on credit worthiness of promoter / Co-obligant / family

members etc. should be included).

1.

2.

3.

4.

5.

6.

NPA MANAGEMENT POLICY 2009-10

21

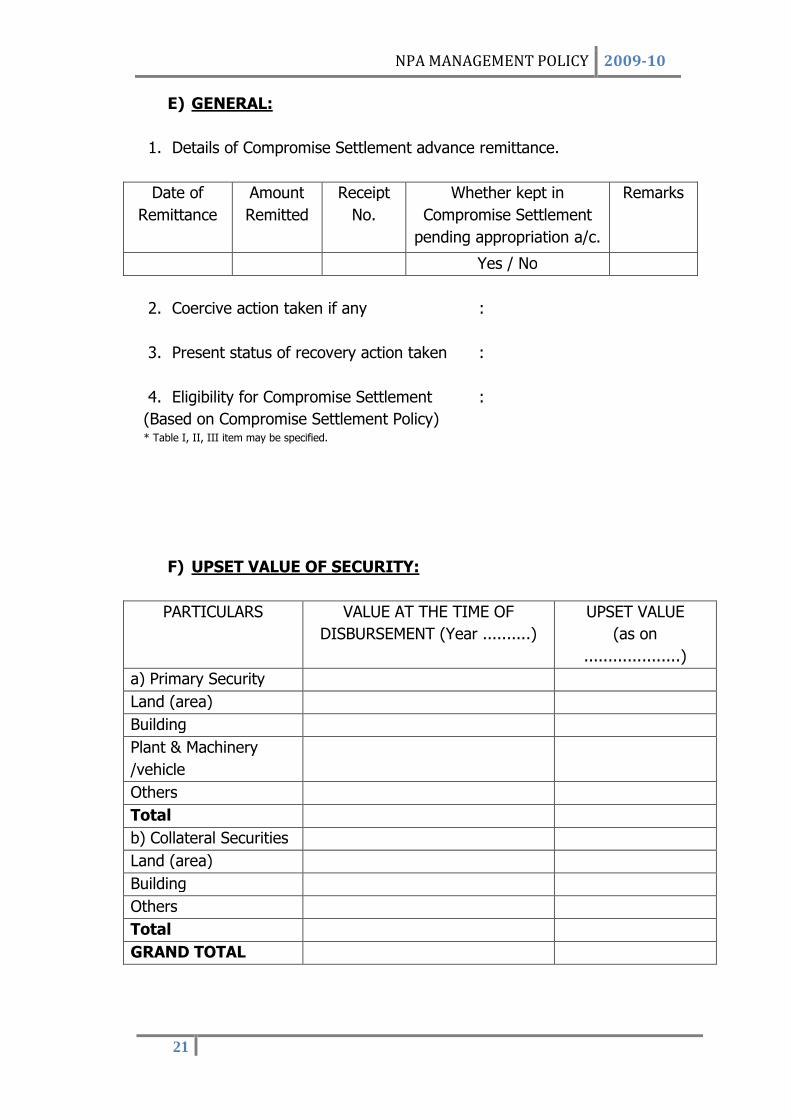

E) GENERAL:

1. Details of Compromise Settlement advance remittance.

Date of

Remittance

Amount

Remitted

Receipt

No.

Whether kept in

Compromise Settlement

pending appropriation a/c.

Remarks

Yes / No

2. Coercive action taken if any :

3. Present status of recovery action taken :

4. Eligibility for Compromise Settlement :

(Based on Compromise Settlement Policy) * Table I, II, III item may be specified.

F) UPSET VALUE OF SECURITY:

PARTICULARS VALUE AT THE TIME OF

DISBURSEMENT (Year ..........)

UPSET VALUE

(as on

....................)

a) Primary Security

Land (area)

Building

Plant & Machinery

/vehicle

Others

Total

b) Collateral Securities

Land (area)

Building

Others

Total

GRAND TOTAL

NPA MANAGEMENT POLICY 2009-10

22

G) COMPROMISE SETTLEMENT DETAILS: (Rs.in lakhs)

Balance Outstanding

Party

's offe

r

(Exclu

ding R

R C

harg

es)

Sacrifice

Pro

visio

ning

require

ment

Prin

cipal

Other e

xpense

s

Interest

Penal in

terest

Total

Prin

cipal

Other e

xpense

s

Interest

Penal in

terest

Tot.

H) REPORT OF FIELD OFFICER (Present status of the unit may be

reported). Loan details need not be repeated. Date of inspection

should be mentioned.

I) *RECOMMENDATION OF BO COMPROMISE SETTLEMENT COMMITTEE.

J) *RECOMMENDATION OF ZONAL COMPROMISE SETTLEMENT

COMMITTEE.

K) *RECOMMENDATION OF HO COMPROMISE SETTLEMENT COMMITTEE.

* For item No. I to K date of the meeting should be specified.

MANAGING DIRECTOR.

Encl:

1. Annexure-I - NSR Calculation

2. Annexure-II - Minutes of BO/ZO Compromise Settlement Committee.

3. N.P.V. Calculation.

NPA MANAGEMENT POLICY 2009-10

23

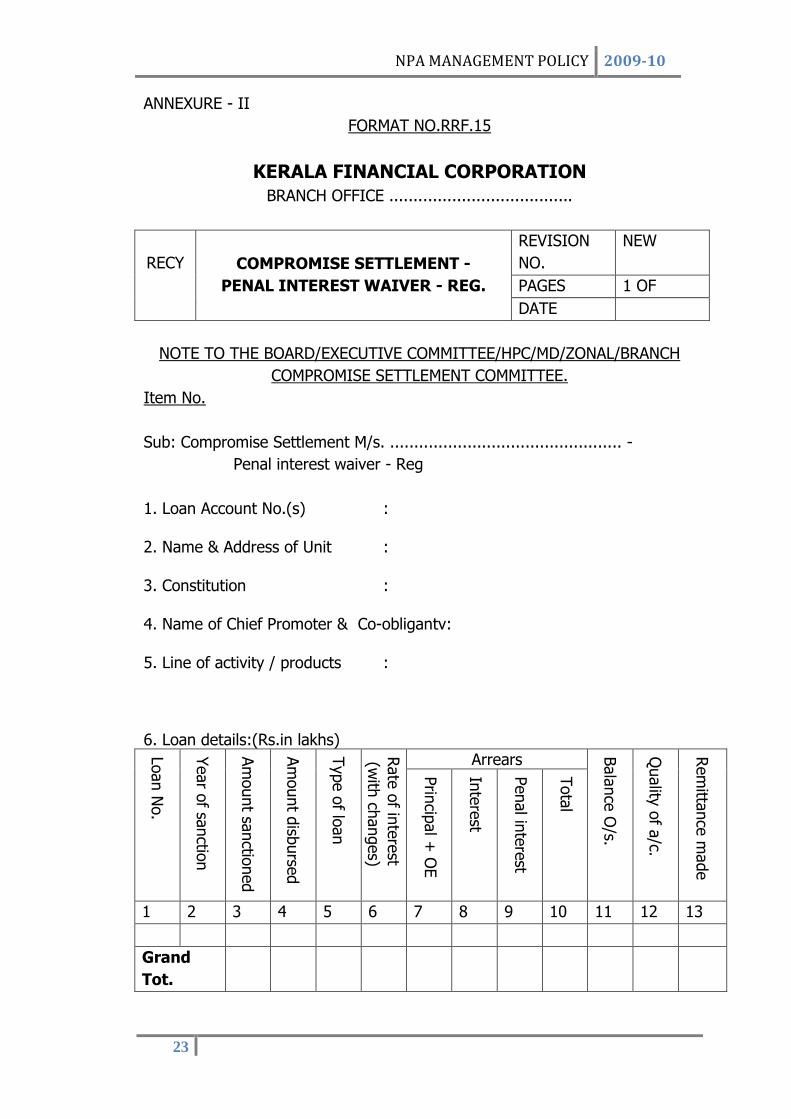

ANNEXURE - II

FORMAT NO.RRF.15

KERALA FINANCIAL CORPORATION

BRANCH OFFICE ......................................

RECY COMPROMISE SETTLEMENT -

PENAL INTEREST WAIVER - REG.

REVISION

NO.

NEW

PAGES 1 OF

DATE

NOTE TO THE BOARD/EXECUTIVE COMMITTEE/HPC/MD/ZONAL/BRANCH

COMPROMISE SETTLEMENT COMMITTEE.

Item No.

Sub: Compromise Settlement M/s. ................................................ -

Penal interest waiver - Reg

1. Loan Account No.(s) :

2. Name & Address of Unit :

3. Constitution :

4. Name of Chief Promoter & Co-obligantv:

5. Line of activity / products :

6. Loan details:(Rs.in lakhs)

Loan N

o.

Year o

f sanctio

n

Amount sa

nctio

ned

Amount d

isburse

d

Type of lo

an

Rate of in

terest

(with

changes)

Arrears

Balance

O/s.

Quality

of a

/c.

Remitta

nce

made

Prin

cipal +

OE

Interest

Penal in

terest

Total

1 2 3 4 5 6 7 8 9 10 11 12 13

Grand

Tot.

NPA MANAGEMENT POLICY 2009-10

24

7. Repayment Schedule:

Original Revised

8. Justification for waiver of Pental interest (Report on credit worthiness

of Promoter/Co-obligant/family members etc. should be included).

1.

2.

3.

4.

5.

6.

9. Coercive action taken if any and its Present Status:

10. Security position as on ............................

Industries : Rs. .....................

Non-industrial : Rs. .....................

--------------------------

Total : Rs.

=================

11. Quality of Asset : S1/S2/D1/D2/D3/Loss Assets.

12. Details of facilities if any,

sanctioned earlier :

(Please specify the nature of facility granted such as reschedulement /

interest funding, Moratorium etc. and its compliance).

13. Present status of the unit : Working satisfactorily/Workingmoderately/

Not working/Dismantled/Not in existence/

abandoned etc should be reported.

14. Penal interest charged in the account as on .....................: Rs.

15. Party's request and offer : Rs.

NPA MANAGEMENT POLICY 2009-10

25

16. Amount and % of Penal interest

recommended for waiver : Rs. ....................... (%)

17. Report of F.O. (Present status of the unit to be reported briefly). Date of

inspection should be mentioned.

18.* Recommendation of the B.O. Settlement Committee (Incorporate

decision)

19.* Recommendation of the Z.O. Settlement Committee (Incorporate

decision)

20.* Recommendation of the H.O. Settlement Committee (Incorporate

decision)

* For item No. 18 to 20 date of the meeting should be specified.

C.M. / B.M.

NPA MANAGEMENT POLICY 2009-10

26

ANNEXURE - III

FORMAT NO.RRF.15

KERALA FINANCIAL CORPORATION

BRANCH OFFICE ......................................

RECY COMPROMISE SETTLEMENT -

BELATED INTEREST WAIVER - REG.

REVISION NO. NEW

PAGES 1 OF

DATE

NOTE TO THE BOARD/EXECUTIVE COMMITTEE /HPC/MD/ ZONAL/BRANCH

COMPROMISE SETTLEMENT COMMITTEE.

Item No.

Sub: Compromise Settlement M/s. ................................................

Belated interest waiver - Reg. .................................

1. Loan Account No.(s) :

2. Name & Address of Unit :

3. Constitution :

4. Name of Chief Promoter &

Co-obligant :

5. Line of activity / products :

6. Loan details as on ..................: (Rs.in lakhs)

Loan N

o.

Year o

f sanctio

n

Amount

sanctio

ned

Amount d

isburse

d

Type of lo

an

Rate of in

terest

(with

changes)

Arrears

Balance

O/s.a

s on

……………………

Quality

of a

/c.

Remitta

nce

made

Prin

cipal +

OE

Interest

Penal in

terest

Total

1 2 3 4 5 6 7 8 9 10 11 12 13

Grand

Total

NPA MANAGEMENT POLICY 2009-10

27

7. Justification for waiver of Pental interest (Report on credit worthiness of

Promoter/Co-obligant/family members etc. should be included).

1.

2.

3.

4.

5.

6.

8. Coercive action taken if any and its Present Status:

9. Security position as on ............................

Industries : Rs. .....................

Non-industrial : Rs. .....................

--------------------------

Total : Rs.

=================

10. Quality of Asset : S1/S2/D1/D2/D3/Loss Assets.

11. Details of settlement facilities sanctioned earlier:

Date of

sanction

Settlement

Amount

Cut off

date

Sacrifice Settlement Amount

remitted, if any with

date of remittance.

12. Present status of the unit : Working satisfactorily/Working

moderately/

Not working/Dismantled/Not in existence /

abandoned etc should be mentioned.

13. Belated interest charged in the account as on ................: Rs.

14. Party's offer : Rs.

15. Amount and % of belated interest

recommended for waiver : Rs. ....................... (%)

16. Report of F.O. (Present status of the unit to be reported briefly). Date of

inspection should be mentioned.

NPA MANAGEMENT POLICY 2009-10

28

17. *Recommendation of the B.O.Settlement Committee (Incorporate

decision)

18. * Recommendation of the Z.O. Settlement Committee (Incorporate

decision)

19. *Recommendation of the H.O. Settlement Committee (Incorporate

decision).

* For item No. 17 to 19 date of the meeting should be specified.

C.M. / B.M.

NPA MANAGEMENT POLICY 2009-10

29

ANNEXURE -IV

NOTE TO COMPROMISE SETTLEMENT COMMITTEE

For loans below Rs.2.00 lakhs

1. Loan No. & Category

DI/DII/DIII

2. Name of unit

3. Name of Promoter & Address

4. Constitution

5. Date of Sanction

6. Amount sanctioned

7. Amount disbursed

8. Amount remitted so far

9. Date of NPA

10. Balance outstanding as on ..........

Principal Rs.

Interest Rs.

Others charges Rs.

Total

Rs.

11. Justification for Compromise Settlement.

12. Sacrifice required

13. Report of the F.O. Date of inspection

should be mentioned.

14. Recommendation of Branch Office

Compromise Settlement Committee

(Minutes to be enclosed, date of the

meeting should be specified).

15. Recommendation of Z.O. Compromise

Settlement Committee (Minutes to be

enclosed, date of the meeting should be

specified).

16. Decision

BRANCH MANAGER.

NPA MANAGEMENT POLICY 2009-10

30

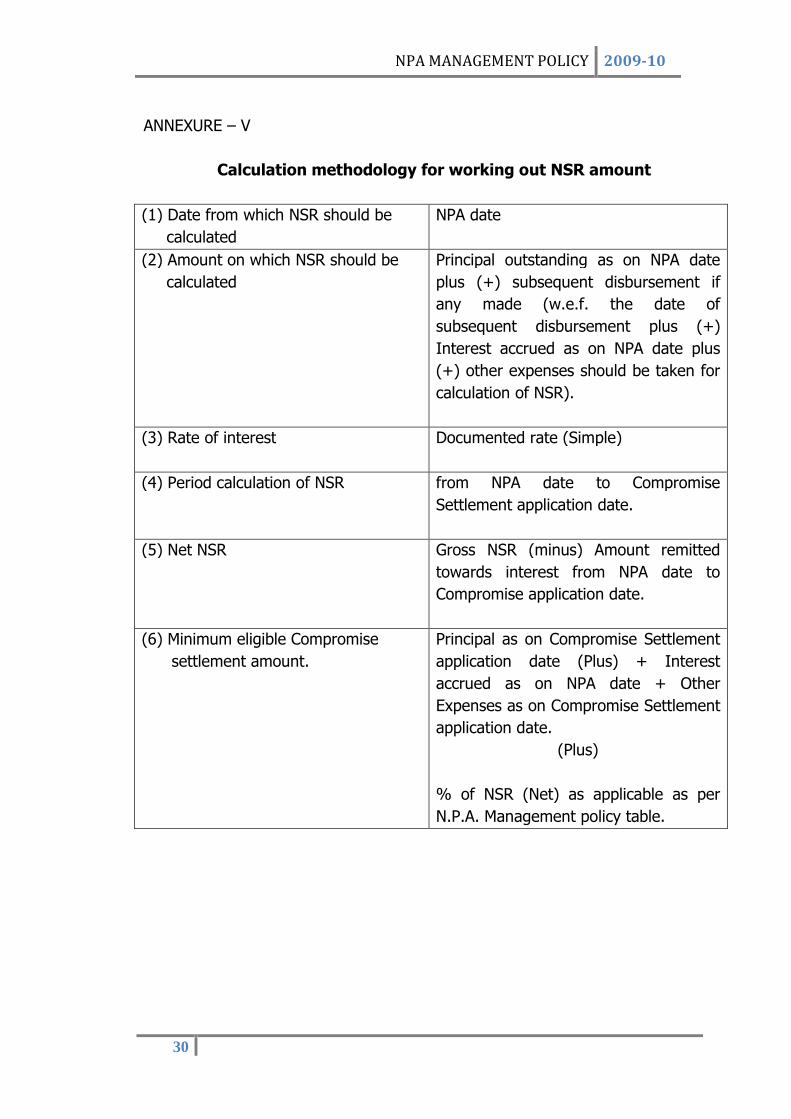

ANNEXURE – V

Calculation methodology for working out NSR amount

(1) Date from which NSR should be

calculated

NPA date

(2) Amount on which NSR should be

calculated

Principal outstanding as on NPA date

plus (+) subsequent disbursement if

any made (w.e.f. the date of

subsequent disbursement plus (+)

Interest accrued as on NPA date plus

(+) other expenses should be taken for

calculation of NSR).

(3) Rate of interest Documented rate (Simple)

(4) Period calculation of NSR from NPA date to Compromise

Settlement application date.

(5) Net NSR Gross NSR (minus) Amount remitted

towards interest from NPA date to

Compromise application date.

(6) Minimum eligible Compromise

settlement amount.

Principal as on Compromise Settlement

application date (Plus) + Interest

accrued as on NPA date + Other

Expenses as on Compromise Settlement

application date.

(Plus)

% of NSR (Net) as applicable as per

N.P.A. Management policy table.

NPA MANAGEMENT POLICY 2009-10

31

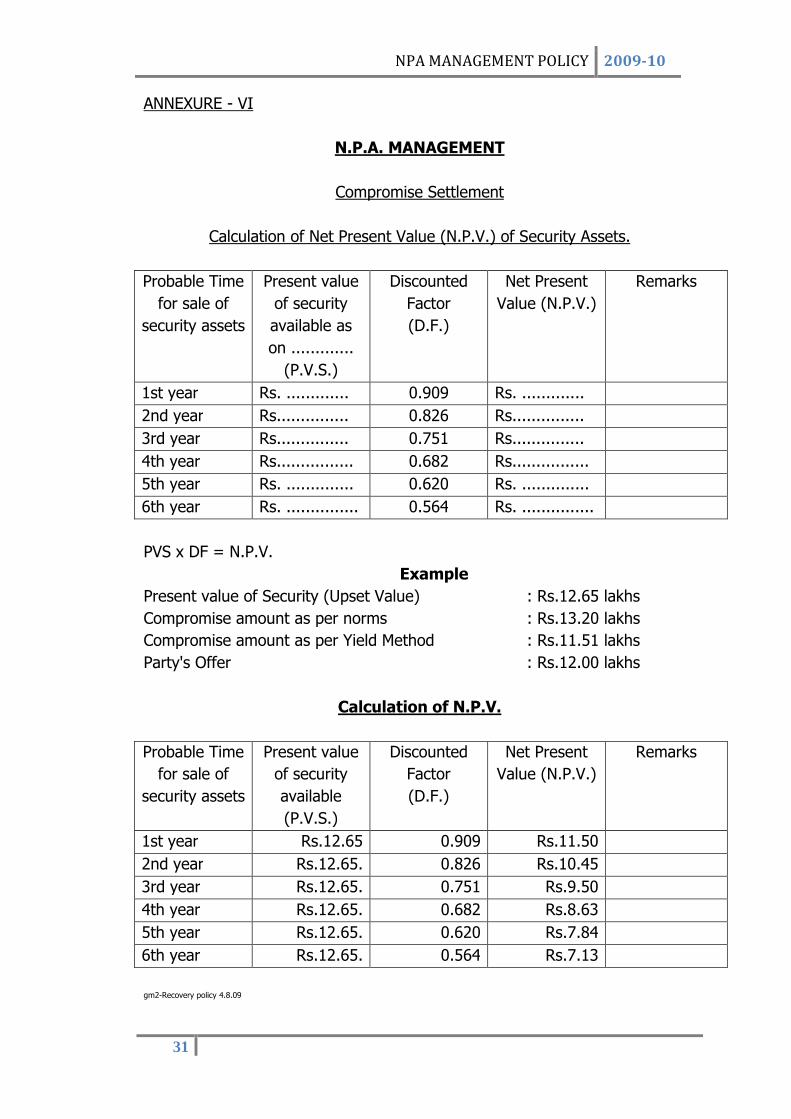

ANNEXURE - VI

N.P.A. MANAGEMENT

Compromise Settlement

Calculation of Net Present Value (N.P.V.) of Security Assets.

Probable Time

for sale of

security assets

Present value

of security

available as

on .............

(P.V.S.)

Discounted

Factor

(D.F.)

Net Present

Value (N.P.V.)

Remarks

1st year Rs. ............. 0.909 Rs. .............

2nd year Rs............... 0.826 Rs...............

3rd year Rs............... 0.751 Rs...............

4th year Rs................ 0.682 Rs................

5th year Rs. .............. 0.620 Rs. ..............

6th year Rs. ............... 0.564 Rs. ...............

PVS x DF = N.P.V.

Example

Present value of Security (Upset Value) : Rs.12.65 lakhs

Compromise amount as per norms : Rs.13.20 lakhs

Compromise amount as per Yield Method : Rs.11.51 lakhs

Party's Offer : Rs.12.00 lakhs

Calculation of N.P.V.

Probable Time

for sale of

security assets

Present value

of security

available

(P.V.S.)

Discounted

Factor

(D.F.)

Net Present

Value (N.P.V.)

Remarks

1st year Rs.12.65 0.909 Rs.11.50

2nd year Rs.12.65. 0.826 Rs.10.45

3rd year Rs.12.65. 0.751 Rs.9.50

4th year Rs.12.65. 0.682 Rs.8.63

5th year Rs.12.65. 0.620 Rs.7.84

6th year Rs.12.65. 0.564 Rs.7.13

gm2-Recovery policy 4.8.09

NPA MANAGEMENT POLICY 2009-10

32

ANNEXURE - VII

KERALA FINANCIAL CORPORATION BRANCH OFFICE :……………………………….

Report on Slippages loan cases. (As on .............................)

Sl. No.

Loan No. Name of unit Slippage from S1 Category to S2

Category

Arrears

B/O. Amount required

for upgradati

on

Action taken by B.O.

Remarks

Pl. Int. Total

gm2-report on slippage