Future of Mobility New Market Entrants in Mobility Integration

23

Future of Mobility Future of Mobility—New New Market Market Entrants in Entrants in Mobility Integration Mobility Integration Transport Operators, OEMs, Fleet Companies, and IT Organisations Transport Operators, OEMs, Fleet Companies, and IT Organisations Aggressively Competing to Become Mobility Integrators Aggressively Competing to Become Mobility Integrators Yeswant Abhimanyu, Research Associate Martyn Briggs, Program Manager, Mobility Research Associate Automotive & Transportation © 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan. Program Manager, Mobility Automotive & Transportation 17 th January 2013

-

Upload

frost-sullivan -

Category

Business

-

view

2.805 -

download

2

Transcript of Future of Mobility New Market Entrants in Mobility Integration

Future of MobilityFuture of Mobility——New New Market Market Entrants in Entrants in Mobility IntegrationMobility Integration

Transport Operators, OEMs, Fleet Companies, and IT Organisations Transport Operators, OEMs, Fleet Companies, and IT Organisations Aggressively Competing to Become Mobility IntegratorsAggressively Competing to Become Mobility Integrators

Yeswant Abhimanyu,

Research Associate

Martyn Briggs,

Program Manager, Mobility Research Associate

Automotive & Transportation

© 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Program Manager, Mobility

Automotive & Transportation

17th January 2013

Today’s Presenter

Experienced Automotive & Transportation consultant and Project Manager, working

Martyn Briggs, Program Manager – Mobility

Frost & Sullivan

2

Experienced Automotive & Transportation consultant and Project Manager, working with clients to implement growth strategies. My current working focus is related to Mobility networks and associated Mega Trends, considering the role of technology and forecasting new market opportunities.

Specialties: Urban Mobility, Smarter Transport, Intelligent Transport Services, Transport Economics

Particular expertise in: Transport Policy, Transport Planning, Behavioural Changeand Transport Economic Appraisal

Today’s Presenter

An Automotive Research and Consulting Professional with a keen interest in

Yeswant Abhimanyu, Research Associate

Frost & Sullivan

3

An Automotive Research and Consulting Professional with a keen interest in exploring next generation disruptive business models and market roadmaps, and to engage in knowledge sharing with visionary thinkers and thought leaders of the world.

Authored studies with core competences in:

• Automotive Powertrain

• Vehicle Fleet & Leasing

• Eco-Innovation, Mega Trends

• Future of Mobility (Mobility Integration, Multi-Modality)

Focus Points — Agenda for Today’s Presentation

• Mega Trends Influencing Rise of Mobility Integration

• Mobility Integrators—Definition and Key Findings

• Mobility Integrators—Ecosystem

• Types of Mobility Integrators

• Mobility Integrators and Existing Product Portfolio

• Mobility Integrators—Customer Types

4

• Case Examples

• Key Conclusions and Future Outlook

Poll Question

What do you think is the one big impact Mobility Integrators will have on Personal Mobility of the future ?

A.Flexibility—time and cost savings

B.One-stop-shop solution

C.Sustainable and responsible travel

5

D.Single ticket travel

Note: Figures used only for representation purposes. Source: Frost & Sullivan analysis.

Occasion for the Analyst Briefing

• Urgency: With an increasing number of smart cities emerging in Europe and North America by 2025,

new Mega Trends like urbanisation, connectivity and convergence, smartphone apps and the

technology boom are expected to drive the rise of interconnected mobility, leading to the creation of a

new class of market players called 'mobility integrators'.

• Noteworthiness: The mobility of the future will be flexible and integrated and will offer on-demand

services to serve customer demand. Car/bike/ride sharing coupled with advancements in high speed

rail, micro-mobility and the emergence of mega corridors are offering customers the ability to move

6

rail, micro-mobility and the emergence of mega corridors are offering customers the ability to move

more conveniently, comfortably, cost-effectively and quickly.

• How will this affect participants: Aided by new business models like car sharing and challenges in

terms of increased cost of vehicle ownership (parking charges, servicing and maintenance, congestion

charges, etc.), a new economic landscape provides stakeholders with an array of opportunities to

exploit, in the quest towards integrated mobility. Participants will benefit, as this briefing will introduce

them to the opportunities that are present in the market today.

Mega Trends Influencing Rise of Mobility IntegrationGlobal Mega Trends are changing the way humans live, move, and co-exist. Dependency on technology and need for operational ease and comfort are amongst key reasons for the evolution of new business models.

Car Sharing/Car Pooling

Geo-SocializationAnd Social Media

New Micro Mobility Products

Urbanization

Smart and Sustainable

Cities

New Business Models

7

Integrated Mobility Solutions

E-Mobility

Connected and Wireless Planet

Sustainable Public Transportation

and BRT

High Speed Rail

New Business Models (Value for Many)

Power to the Middle Class and Gen Y

Photo Credits: Dreamstime and Commons. Source: Frost & Sullivan Analysis

Mobility Integrators—New Market PlayerTravel today is more than just station to station; it is about door-to-door connectivity, thus giving rise to new market players offering integrated various modes to travel.

2020

City

Suburbs

Intercity

Tra

ve

l D

ista

nc

e

Private CarsIntercity Bus

Intercity

Train

Shared Mobility

CAR

Mobility Integrators Market: Future Approach towards Mobility Integration, Europe, 2011–2020

8

City

Tra

ve

l D

ista

nc

e

Travel DistanceDestination

Public

Transportation

Shared Mobility

Micro-mobility

CAR

OWNERSHIP

Note: Figures used only for representation purposes. Source: Frost & Sullivan analysis.

• Door-to-door integrated, multi-mobility a reality in future• Market will see new players in market termed 'mobility integrators‘

Mobility Integrators—DefinitionMobility is about seamless travel using all of the various modes of transportation available rather than relying solely on one transportation mode.

'Mobility integrator is an entity or a combination of entities in the value chain which provides the right combination of various modes of transportation to offer an integrated, multi-modal door-to-door mobility solution using a mobility platform by leveraging technological expertise, operational excellence, infrastructural advancements and innovative business propositions.'

Key Elements—Customer Perspective Urging Mobility Integration

9

CUSTOMER PERSPECTIVE URGING MOBILITY INTEGRATION Time and Cost

Saving

Multiple modes

of Transport

Technology Integration

Integrated Journey

Key Elements—Customer Perspective Urging Mobility Integration

Mobility Platform for

Real-time dynamics

Note: Figures used only for representation purposes. Source: Frost & Sullivan analysis.

Mobility Integrators—EcosystemCross interoperability and co-operation between the different entities in the ecosystem to be the crux that makes or breaks future of mobility integration

Public transport operators, carsharing, bike sharing, parking

operators, rentals, and leasing

• OEMS • Technology *

Mobility Integrators Market: Ecosystem, Europe, 2011

Key Responsibility:Providing the

technology and

technical support

required to realise

new innovations

Key Responsibility:Providing mobility

Key Responsibility:Providing mobility

from Point A to B

10

*Cross interoperability and co-operation, for example, between OEM and technology providers converging on infotainment

• OEMS• Supplier• Transport

companies

• Infrastructure providers

• Payments providers• Charging stations• Mobile infrastructure

• Technology providers

• IT supportMI*

*

**

Government laws, regulations, incentives, promotion, support, and

subsidies to the different entities

Source: Frost & Sullivan analysis.

Key Responsibility:Providing

infrastructure for

mobility

Providing mobility

vehicles (cars, trams,

EVs, and so on)

Mobility Integrators—Stakeholders making it possibleStakeholders in an ever expanding integrated value chain taking the role of mobility integrators in the quest for totally integrated multi-modal door-to-door connected travel.

Online Mobility

New Opportunities

Parking Operators

LBS and Telematics

OnStar, ATX,

Charging Point

ChargePoint,

Park-o-charge

Telecom Operators

Vodafone,

T-Mobile, O2,

Orange

PublicTransport

RailBus

Shared Mobility Bike/Car Pooling

TaxiNS, DB Bahn

Velib, ZipCar,

Greenwheels,

DriveNow,

Car2Go

Connexxions

Payment Engine

PayPal, AMEX,

Parkeon, Navx,

QPark, Vinci

MI

With

advancements in

technology and

continuous

innovation, new

opportunities are

believed to evolve

into new MI

participants in an

expanding

integrated value

chain.

Mobility Integrators Market: Mobility Integrators, Europe, 2011

11

Mobile Apps

App Store,

AppWorld,

Google Play,

ovi Store

Ever Expanding Integrated Value Chain

New Opportunities

Long Distance Mobility

Short Distance Urban Mobility

Online Mobility Booking Agency/ Journey Planners

Oyster,

OV-Chip Card,

Leap Card

Expedia, makemytrip, STA,

Travelocity

New Opportunities(office space

rental and so

on)

Park-o-charge PayPal, AMEX,

Visa,

MasterCard

Car Rental and Fleet Company

ALD, Hertz,

Alphabet,

Athlon

Tech Solutions Provider—IT

Bosch, Continental AG,

Amadeus, Nokia, IBM, NXP

Current EV OEMs

PSA, Renault,

Daimler,

SMART, BMW

MI

Technology Advancements

Mobile 2.0,

Web 2.0

Infrastructure and Transport

CompaniesVeolia Transdev,

Siemens

Source: Frost & Sullivan analysis.

Mobility Integrators and Existing Product PortfolioNS Business card is the only full-fledged MI, while Mobility Mixx uses the same platform to extend its offering; it will be easier for the transport companies to become the Mobility Integrators.

Company Name

Car Leasing and Carsharing Public TransportParking

Management

Long-Distance

TravelOthers

ServicePlatforms

Carsharing (Traditional)

Car Leasing (Long-term)

Car Rentals (Short-term)

Bike (Cycle) Renting

ScooterRenting

Intra-city Inter-city TaxiBike

ShedsCar

ParkingTrains Flight

Refuel/Tele-

confer-encing

Others (Hotels, accesso-ries and so on)

Infra-struc-

ture and Charg-

ing

Apps, JourneyPlanners,

Scheduling,Re-routing

Tra

nsp

ort

Op

era

tors NS Business

Card � � � � � � � � � � �

Connexxion � � �

Car

Co

mp

an

ies

µ by Peugeot � � � �

Multicity by

Citroën � � � � �

Mobility Integrators Market: Snapshot of Mobility Offerings by Mobility Integrators, Europe, 2011

12

Car

Co

mp

an

ies

Citroën � � � � �

BMW/

Daimler � � �

Leasin

g C

om

pan

ies

MobilityMixx

(LeasePlan) � � � � � � � � � �

ALD � � � �

Alphabet � � �

Athlon � �

Arval � �

Tra

nsp

ort

C

om

pan

y

Siemens � � � � �

Veolia-

Transdev � � � � � � � � �

Source: Frost & Sullivan analysis.

Type of Mobility Integrators A mobility integrator’s function varies depending on what it offers and how it wants to position itself in the market in line with market demands and the group vision.

Mobility Integrator

(MI)

Mobility Player(MP)

Mobility Aggregator

(MA)

Mobility Integrators Market: Types of Mobility Integrators, Europe, 2011 and 2020

• MI is an entity which enables the existence of mobility

• MA is an entity which offers a selection of mobility services

• MP is a member in the value chain who enables or owns approximately 50

13

Note: Figures used only for representation purposes. Image Source: railteam.co.uk, Peugeot Mu, and Alphabet.com. Source: Frost & Sullivan analysis.

of mobility programmes through its

current offering

mobility services as core businesseither as stand-alone providers or through partnerships

approximately 50 percent of the different modes of transport offered

• Offers a selection of 3 or 4 mobility solutions

Mobility Integrators—Snapshot of Existing Mobility Integrators ExamplesThe future focus is moving towards integrated mobility with a number of mobility concepts and disruptive business models.

Mobility Aggregators/Players • Oyster CardMobility Trend• Numerous carsharing programs• Barclays bike sharing programs

Mobility Aggregators/Players

Mobility Integrators• Mobility Mixx• NS Business CardMobility Trend• Integrated mobility trend evident

with the introduction of mobility budgets

Mobility Aggregators/Players • DB Bahn—Touch & Travel System

Mobility Aggregators/Players

• cOPENhagen Card

• Excellent bicycle infrastructure with specific lanes; a number of bicycle sharing programs

14

Note: Figures used only for representation purposes. Source: Frost & Sullivan analysis.

Mobility Aggregators/Players • NaviGo, Orange Card, Peugeot

Mu, Citroen MulticityMobility Trend• Mobility integration activities by

Veolia-Transdev such as Urban Pulse and City Way; close working with IBM for integrated real-time mobility.

• EV carsharing programs

• DB Bahn—Touch & Travel System• RMV Transport CardMobility Trend• Mobility trend: Towards multi-

modal integration and encouragement of carsharing

Mobility Aggregators/Players • ATM Itinero

Mobility Aggregators/Players • New Transit Card

Mobility Integrators—Customer TypesCustomers for mobility integration range from everyday general public to cities and countries looking to rebrand their positions.

BusinessB2B

Mobility Mobility

Mobility Integrators Market: Customer Types, Europe, 2011

Mobility Industry Mobility Industry

Transport/Infrastructure Companies

Transport/Infrastructure Companies

Other Company ClientsOther Company Clients

Another MIAnother MI

15

City as a Customer

Mobility Integration Customer

Types

Mobility Integration Customer

Types

Note: Figures used only for representation purposes. Source: Frost & Sullivan analysis.

Smarter and Sustainable Cities

Smarter and Sustainable Cities

Another MIAnother MI

General PublicGeneral Public

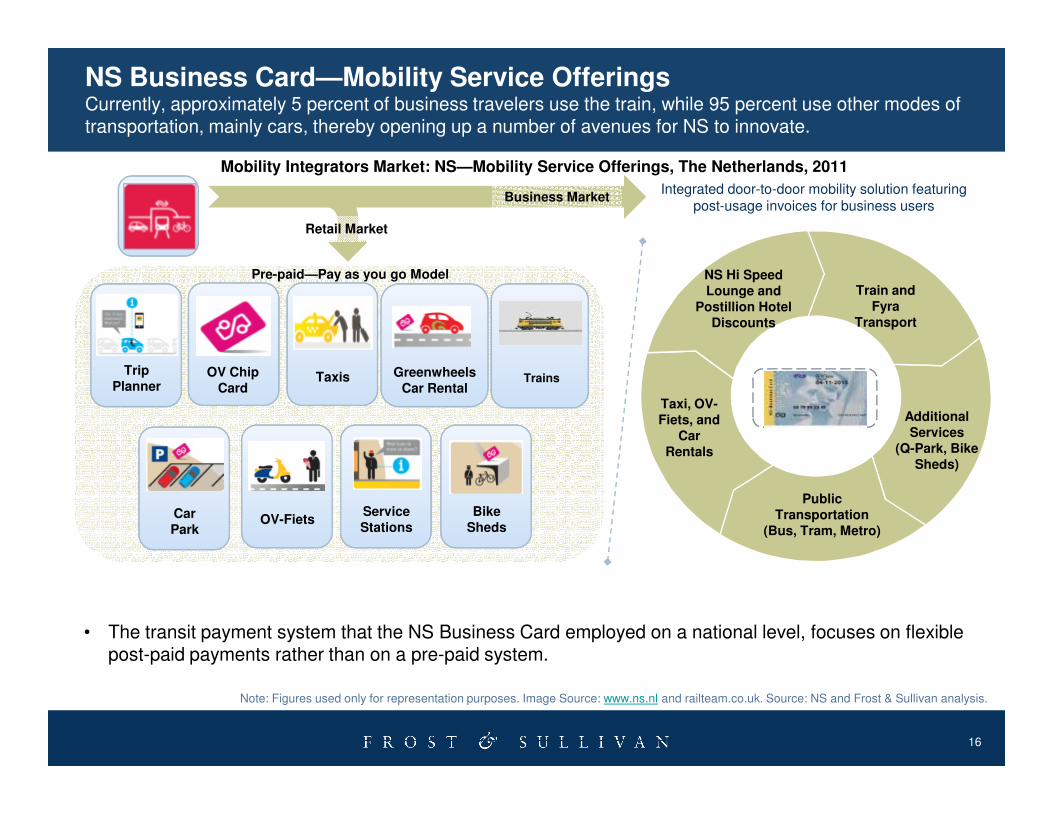

NS Business Card—Mobility Service OfferingsCurrently, approximately 5 percent of business travelers use the train, while 95 percent use other modes of transportation, mainly cars, thereby opening up a number of avenues for NS to innovate.

Business Market

Retail Market

Trip Planner

OV Chip Card

Taxis GreenwheelsCar Rental

Trains

Train and Fyra

Transport

Taxi, OV-

NS Hi Speed Lounge and

Postillion Hotel Discounts

Integrated door-to-door mobility solution featuring post-usage invoices for business users

Pre-paid—Pay as you go Model

Mobility Integrators Market: NS—Mobility Service Offerings, The Netherlands, 2011

16

Car Park

OV-FietsBike

ShedsService Stations

Additional Services

(Q-Park, Bike Sheds)

Public Transportation

(Bus, Tram, Metro)

Taxi, OV-Fiets, and

Car Rentals

• The transit payment system that the NS Business Card employed on a national level, focuses on flexible post-paid payments rather than on a pre-paid system.

Note: Figures used only for representation purposes. Image Source: www.ns.nl and railteam.co.uk. Source: NS and Frost & Sullivan analysis.

Daimler—Mobility Services, Moovel At the Heart of Moovel are intelligent mobility linkages with better use of available resources.

Bus and Rail• The different available bus and

rail connections are shown

Integrated Platform and Direct Comparison• Direct comparison of different

mobility modes based on user selection

Ride Sharing and Taxi Cabs• Search for available ride-

sharing possibilities for a specific route.

17

Note: Images used only for representation purposes. Image Source: Daimler.com. Source: Daimler.com and Frost & Sullivan analysis.

specific route. • A taxi can be ordered using the

app.

Decisions-making enabler• Prices, quickest time, and

comfort levels

Future of Mobility• Expansion opportunities for

Car2gether and Car2go

Mobility Integrators—Key Conclusions and Future OutlookThe future of integrated technology is connected, with networked products and services with technology advancements acting as the key enabler.

Real-time data sharing• Opening up of – key enabler that will make or break mobility integration.• Real-time data sharing and integration – shared costs and risks among – the way forward.

City versus country-wide MI• Infrastructure capabilities – governments and investments • Future smart and Mega Cities are expected to be attractive MI customers• Country-wide integration – co-existence of competitors in view of a unified goal.

1

2

18

Source: Frost & Sullivan analysis.

Future business models• Developing business models – p2p carsharing, renting personal parking spaces, and ride-sharing• Personal transport merging with public transport and utilizing wasted travel capacity.• Mobility budget handling –(TCO����TCM).

Technology advancements• Web sites and smartphone apps• NFC is a futuristic potential technology – payments, check-in/outs, security, safety, and telematics.• E-ticketing – with virtual tickets allowing for seamless customer-controlled travel.

3

4

Table of Content of Frost & Sullivan’s M8BF–18 StudyFuture of Mobility—New Business Models, Opportunities, and Market Entrants in Mobility Integration

Section Slide Numbers

Executive Summary 4

Research Scope, Objectives, Methodology and Background 25

Mobility Integrators—Mega Trends and Influencing factors 31

Mobility Integrators—Overview 49

Mobility Integrators—Definition and Ecosystem 67

Mobility Integrators—Customer Types 75

19

Source: Frost & Sullivan analysis.

Mobility Integrators—Technology Solutions 92

Mobility Budget 98

Mobility Integrators—Case Studies and Examples 105

Mobility Integrators—Potential Cities 177

Conclusions and Future Outlook—The Last Word 183

Appendix 188

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

20

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

21

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

22

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Katja FeickCorporate Communications

Automotive & Transportation

+49 (0) 69 [email protected]

Yeswant Abhimanyu

Research Associate

Automotive & Transportation

(0091) 44 6681 4163

23

Martyn Briggs

Program Manager – Mobility

Automotive & Transportation

0044 (0)207 915 7830

Cyril Cromier

VP Sales

Automotive & Transportation

+33 1 4281 2244