Exponenciális - Logaritmus függvények, Benford fura törvénye

Corporate PresentationFebruary 1, 2018

Fura Gems Inc

Opportunity to invest in an innovative and disruptive company

operating in a highly exclusive resource sector

This presentation contains, or incorporates by reference, “forward-looking information” within the meaning of applicable Canadian securities legislation. Forward-looking information may include, but

is not limited to, statements with respect to the future performance of Fura Gems Inc. (“Fura” or the “Company”), Fura’s mineral properties, the future price of emeralds, rubies and other gemstones,

the estimation of mineral resources and mineral reserves, results of exploration activities and studies, the realization of mineral resource estimates, exploration activities, costs and timing of the

development of new deposits, the acquisition of additional mineral resources, the results of future exploration and drilling, costs and timing of future exploration of the mineral projects, requirements

for additional capital, management’s skill and knowledge with respect to the exploration and development of mining properties, government regulation of mining operations and exploration

operations, timing and receipt of approvals and licences under mineral legislation, the Company’s local partners, and environmental risks and title disputes. In certain cases, forward-looking

statements can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “believes”, or variations

(including negative variations) of such words and phrases, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking

statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Fura to be materially different from any future results,

performance or achievements expressed or implied by the forward-looking statements. Such factors include, among others, risks associated with the Company’s dependence on the mineral projects;

general business, economic, competitive, political and social uncertainties; the actual results of current exploration activities; risks associated with dependence on key members of management;

conclusions of economic evaluations and studies; currency fluctuations; future prices of emeralds, rubies and other gemstones; uncertainty in the estimation of mineral resources, exploration and

development risks; infrastructure risks; inflation risks; defects and adverse claims in the title to the projects; accidents, political instability, insurrection or war; labour and employment risks; changes in

government regulations and policies, including laws governing development, production, taxes, royalty payments, labour standards and occupational health, safety, toxic substances, resource

exploitation and other matters; delays in obtaining governmental approvals or financing or in the completion of development or construction activities; insufficient insurance coverage; the risk that

dividends may never be declared; and liquidity and financing risks related to the global economic crisis. Such forward-looking statements are based on a number of material factors and

assumptions, including: that contracted parties provide goods and/or services on the agreed timeframes; that on-going contractual negotiations will be successful and progress and/or be completed

in a timely manner; that no unusual geological or technical problems occur; that plant and equipment work as anticipated and that there is no material adverse change in the price of emeralds and

rubies. Although Fura has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may

be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward looking statements contained herein are made as of the date of this presentation.

There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly,

readers should not place undue reliance on forward-looking statements due to the inherent uncertainty therein.

Ricardo A. Valls, M.Sc., P.Geo., of Valls Geoconsultant, Toronto, Ontario, a Qualified Person as defined by National Instrument 43-101, has reviewed the scientific and technical information disclosed

in this presentation.

2

Legal Disclaimer

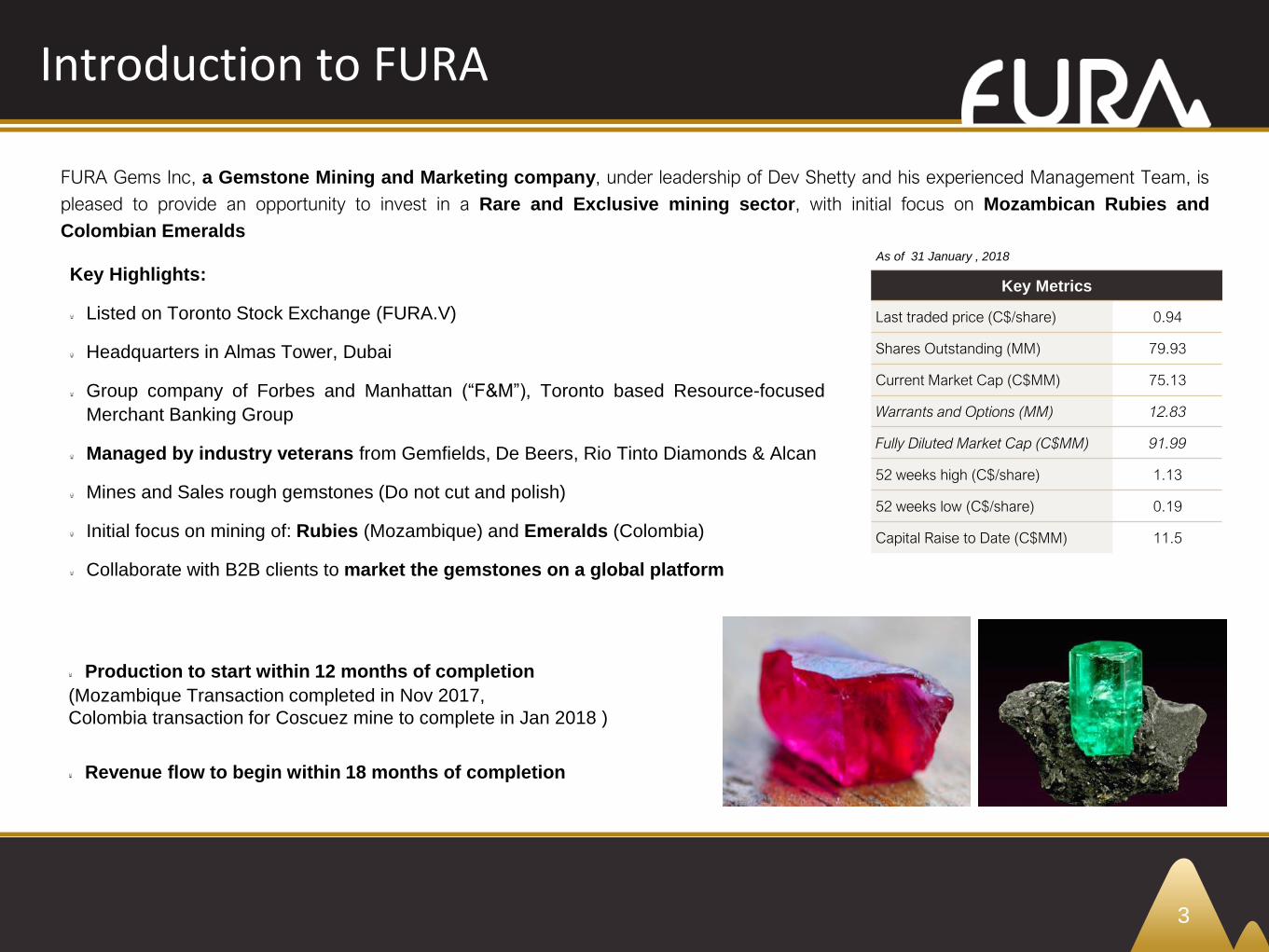

Introduction to FURA

3

Key Highlights:

Listed on Toronto Stock Exchange (FURA.V)

Headquarters in Almas Tower, Dubai

Group company of Forbes and Manhattan (“F&M”), Toronto based Resource-focused

Merchant Banking Group

Managed by industry veterans from Gemfields, De Beers, Rio Tinto Diamonds & Alcan

Mines and Sales rough gemstones (Do not cut and polish)

Initial focus on mining of: Rubies (Mozambique) and Emeralds (Colombia)

Collaborate with B2B clients to market the gemstones on a global platform

FURA Gems Inc, a Gemstone Mining and Marketing company, under leadership of Dev Shetty and his experienced Management Team, is

pleased to provide an opportunity to invest in a Rare and Exclusive mining sector, with initial focus on Mozambican Rubies and

Colombian Emeralds

Production to start within 12 months of completion

(Mozambique Transaction completed in Nov 2017,

Colombia transaction for Coscuez mine to complete in Jan 2018 )

Revenue flow to begin within 18 months of completion

Key Metrics

Last traded price (C$/share) 0.94

Shares Outstanding (MM) 79.93

Current Market Cap (C$MM) 75.13

Warrants and Options (MM) 12.83

Fully Diluted Market Cap (C$MM) 91.99

52 weeks high (C$/share) 1.13

52 weeks low (C$/share) 0.19

Capital Raise to Date (C$MM) 11.5

As of 31 January , 2018

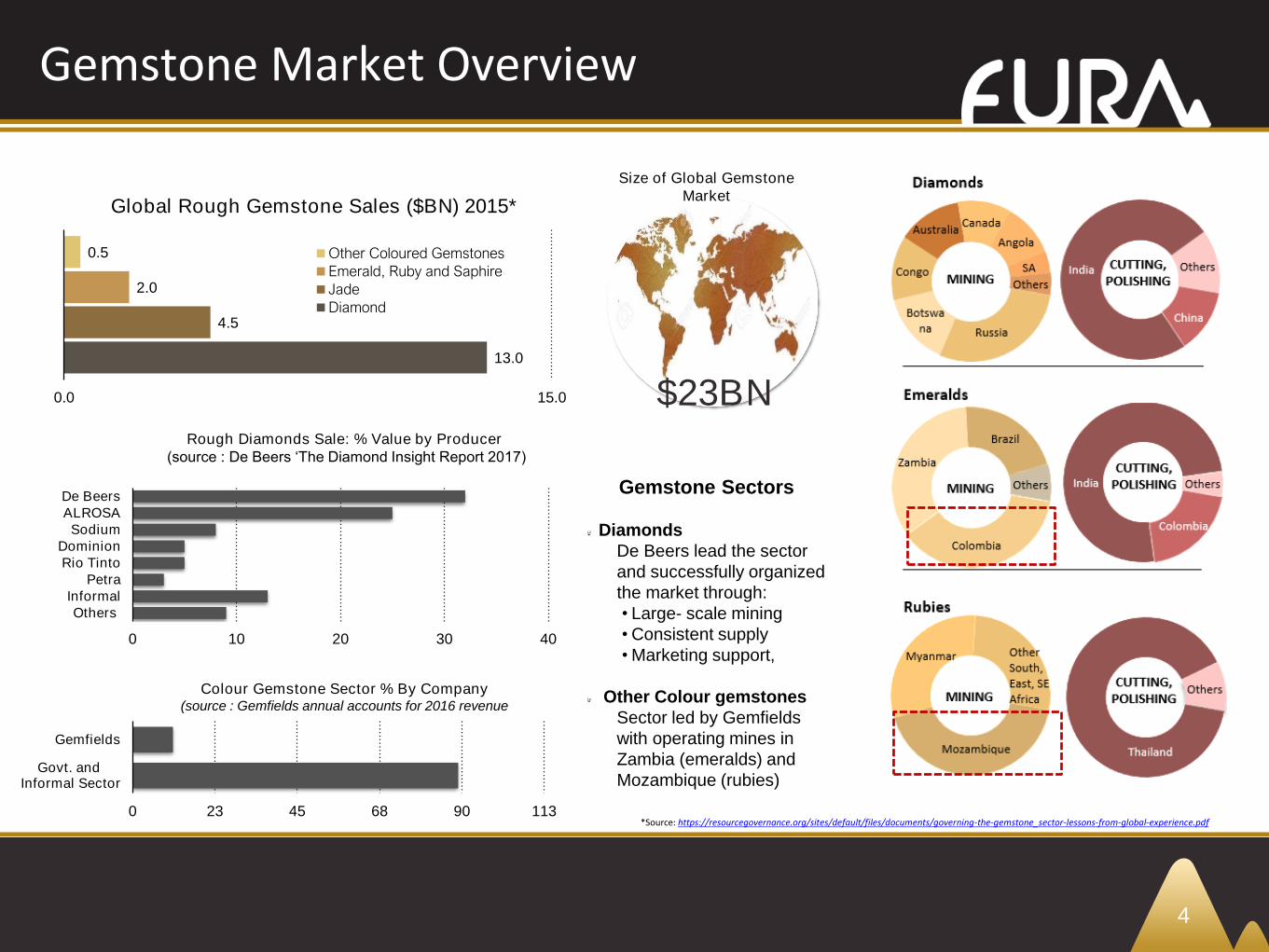

Gemstone Market Overview

0.5

2.0

4.5

13.0

0.0 15.0

Global Rough Gemstone Sales ($BN) 2015*

Other Coloured Gemstones

Emerald, Ruby and Saphire

Jade

Diamond

0 10 20 30 40

De Beers

ALROSA

Sodium

Dominion

Rio Tinto

Petra

Informal

Others

Gemstone Sectors

Diamonds

De Beers lead the sector

and successfully organized

the market through:

• Large- scale mining

• Consistent supply

• Marketing support,

Other Colour gemstones

Sector led by Gemfields

with operating mines in

Zambia (emeralds) and

Mozambique (rubies)

*Source: https://resourcegovernance.org/sites/default/files/documents/governing-the-gemstone_sector-lessons-from-global-experience.pdf

$23BN

Size of Global Gemstone

Market

0 23 45 68 90 113

Gemfields

Govt. and Informal Sector

Colour Gemstone Sector % By Company(source : Gemfields annual accounts for 2016 revenue

Rough Diamonds Sale: % Value by Producer

(source : De Beers ‘The Diamond Insight Report 2017)

4

Gemstones Market - Emeralds

5

Long Been Recognised as Status Symbol

Celebrated by Top Jewellery Houses

Legacy Remains Unprecedented

Diadem of the Duchess of Angoulême of FranceThe Moghul EmeraldThe Seringapatam Jewels The Guinness Emerald

Crystal

Cleopatra

Queen of Ancient EgyptBeyonce Knowles

Singer

Kim Kardashian

Socialite

Angelina Jolie

Hollywood StarElizabeth Taylor

British-American actress

The Chalk Emerald

Gemstones Market - Rubies

Top 5 Most Expensive Rubies Sold in the Last Decade

Ruby The Sunrise Ruby The Graff RubyA Ruby & Diamond Brooch, by Cartier

A Ruby & Diamond Ring, mounted by

CartierThe Patiño Ruby

Sale Date May 2015 Nov 2014 Nov 2014 Apr 2014 May 2012

Auction House Sotheby’s Geneva Sotheby’s Geneva Christie's Hong Kong Sotheby's Hong Kong Christie's Geneva

Price (USD $MM) 30.34 8.60 8.43 7.38 6.74

Price per Carat ($MM) 1.19 0.99 0.83 0.25 0.21

Baselworld 2015

Presented byAmrapali, London

Mozambique Ruby Ring

Dec 2016

Christie's Geneva

1.03

0.10

6

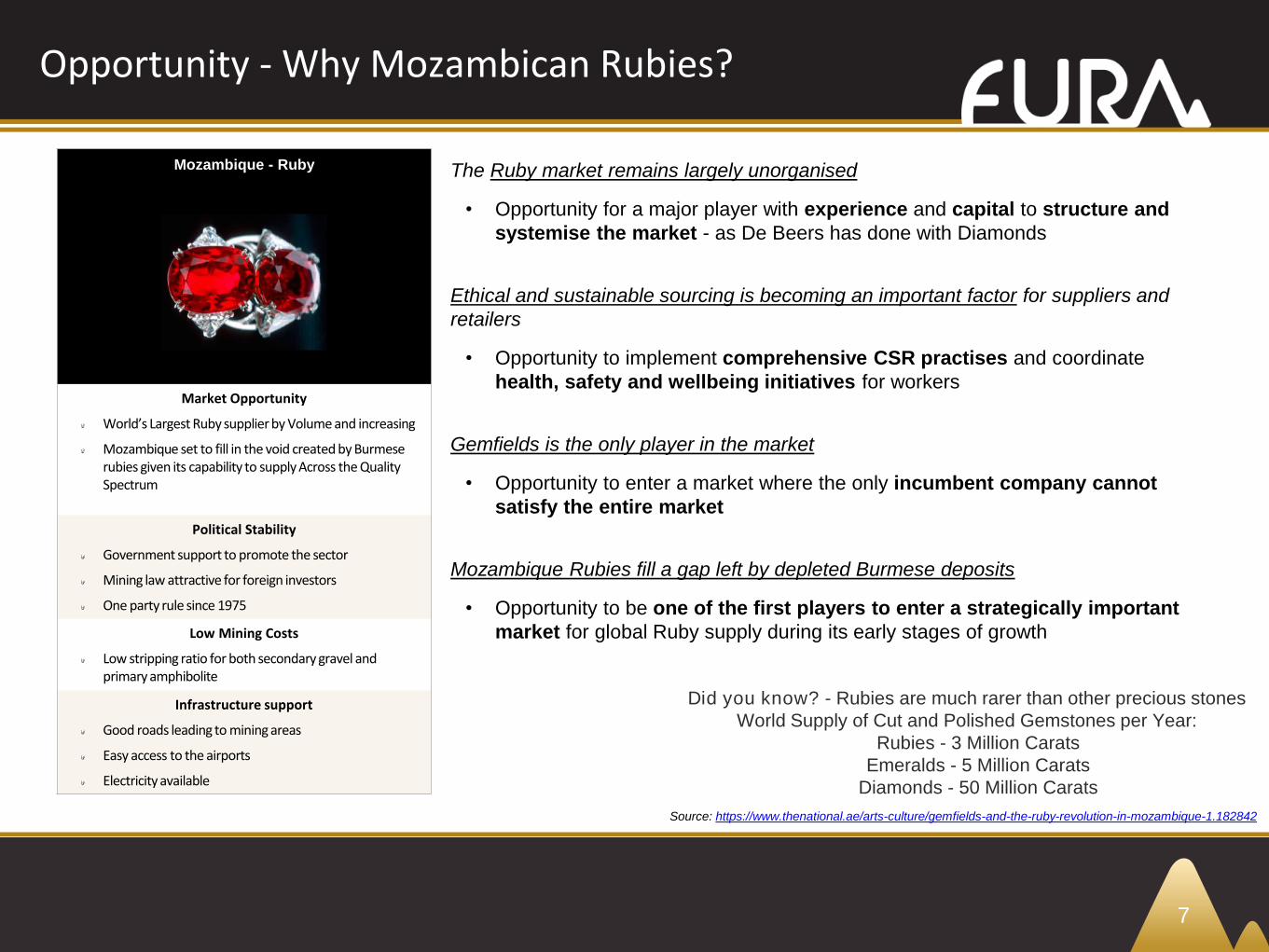

Opportunity - Why Mozambican Rubies?

7

Mozambique - Ruby

Market Opportunity

World’s Largest Ruby supplier by Volume and increasing

Mozambique set to fill in the void created by Burmese rubies given its capability to supply Across the Quality Spectrum

Political Stability

Government support to promote the sector

Mining law attractive for foreign investors

One party rule since 1975

Low Mining Costs

Low stripping ratio for both secondary gravel and primary amphibolite

Infrastructure support

Good roads leading to mining areas

Easy access to the airports

Electricity available

Did you know? - Rubies are much rarer than other precious stones

World Supply of Cut and Polished Gemstones per Year:

Rubies - 3 Million Carats

Emeralds - 5 Million Carats

Diamonds - 50 Million Carats

The Ruby market remains largely unorganised

• Opportunity for a major player with experience and capital to structure and

systemise the market - as De Beers has done with Diamonds

Ethical and sustainable sourcing is becoming an important factor for suppliers and

retailers

• Opportunity to implement comprehensive CSR practises and coordinate

health, safety and wellbeing initiatives for workers

Gemfields is the only player in the market

• Opportunity to enter a market where the only incumbent company cannot

satisfy the entire market

Mozambique Rubies fill a gap left by depleted Burmese deposits

• Opportunity to be one of the first players to enter a strategically important

market for global Ruby supply during its early stages of growth

Source: https://www.thenational.ae/arts-culture/gemfields-and-the-ruby-revolution-in-mozambique-1.182842

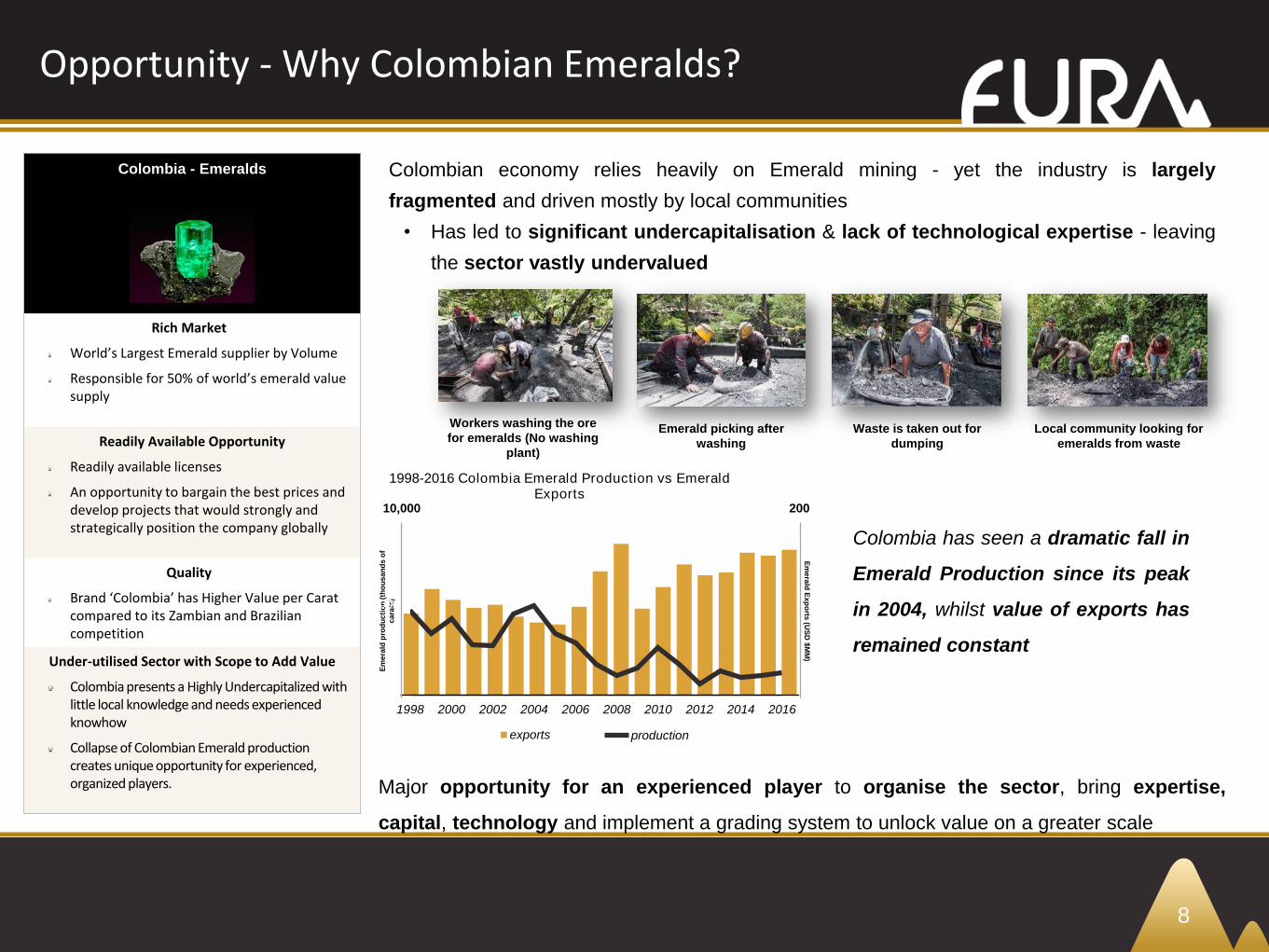

Opportunity - Why Colombian Emeralds?

8

Colombia - Emeralds

Rich Market

World’s Largest Emerald supplier by Volume

Responsible for 50% of world’s emerald value supply

Readily Available Opportunity

Readily available licenses

An opportunity to bargain the best prices and develop projects that would strongly and strategically position the company globally

Quality

Brand ‘Colombia’ has Higher Value per Carat compared to its Zambian and Brazilian competition

Under-utilised Sector with Scope to Add Value

Colombia presents a Highly Undercapitalized with little local knowledge and needs experienced knowhow

Collapse of Colombian Emerald production creates unique opportunity for experienced, organized players.

Local community looking for

emeralds from waste

Emerald picking after

washing

Workers washing the ore

for emeralds (No washing

plant)

Waste is taken out for

dumping

Colombian economy relies heavily on Emerald mining - yet the industry is largely

fragmented and driven mostly by local communities

• Has led to significant undercapitalisation & lack of technological expertise - leaving

the sector vastly undervalued

Colombia has seen a dramatic fall in

Emerald Production since its peak

in 2004, whilst value of exports has

remained constant

Em

era

ld p

rod

uc

tio

n (

tho

us

an

ds

of

ca

rats

)

0

20

40

60

80

100

120

140

160

180

exports

0

10000

20000

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

1998-2016 Colombia Emerald Production vs Emerald Exports

production

10,000 200

Em

era

ld E

xp

orts

(US

D $

MM

)

Major opportunity for an experienced player to organise the sector, bring expertise,

capital, technology and implement a grading system to unlock value on a greater scale

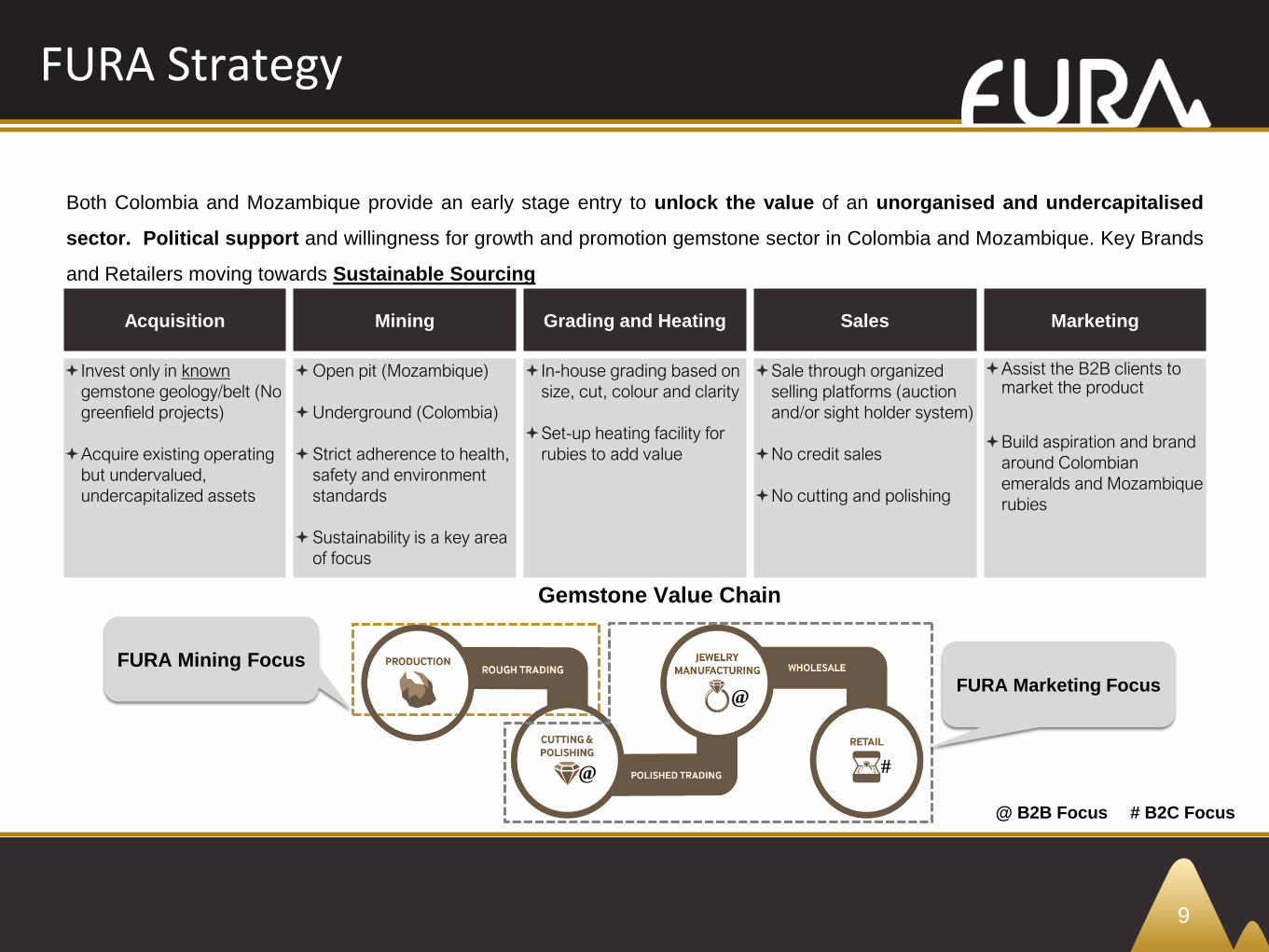

FURA Strategy

9

Gemstone Value Chain

Acquisition Mining Grading and Heating Sales Marketing

Invest only in known

gemstone geology/belt (No

greenfield projects)

Acquire existing operating

but undervalued,

undercapitalized assets

Open pit (Mozambique)

Underground (Colombia)

Strict adherence to health,

safety and environment

standards

Sustainability is a key area

of focus

In-house grading based on

size, cut, colour and clarity

Set-up heating facility for

rubies to add value

Sale through organized

selling platforms (auction

and/or sight holder system)

No credit sales

No cutting and polishing

Assist the B2B clients to market the product

Build aspiration and brand

around Colombian

emeralds and Mozambique

rubies

FURA Mining Focus

FURA Marketing Focus

@

@

@ B2B Focus # B2C Focus

#

Both Colombia and Mozambique provide an early stage entry to unlock the value of an unorganised and undercapitalised

sector. Political support and willingness for growth and promotion gemstone sector in Colombia and Mozambique. Key Brands

and Retailers moving towards Sustainable Sourcing

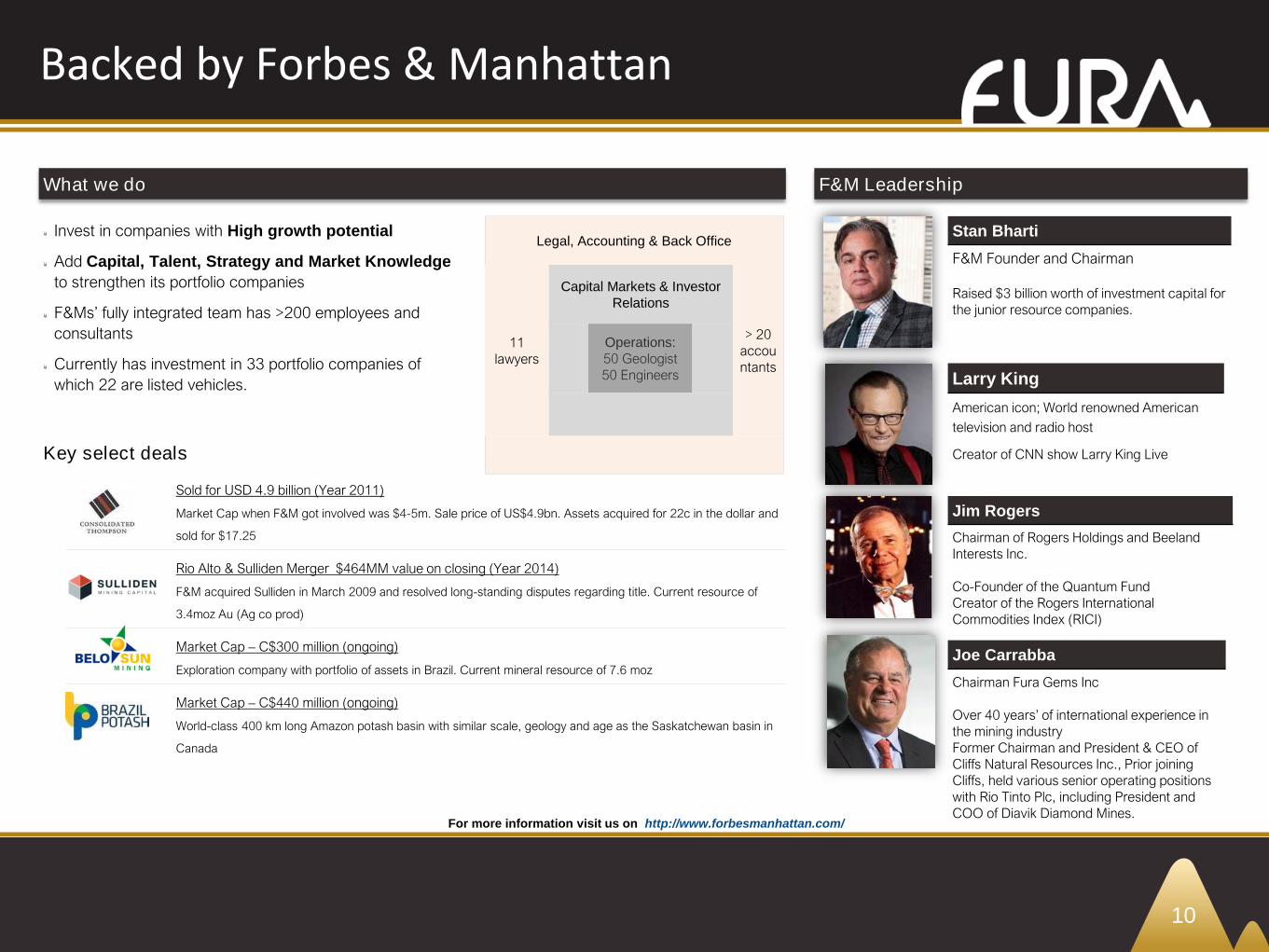

Backed by Forbes & Manhattan

Stan Bharti

F&M Founder and Chairman

Raised $3 billion worth of investment capital for

the junior resource companies.

Larry King

American icon; World renowned American

television and radio host

Creator of CNN show Larry King Live

Jim Rogers

Chairman of Rogers Holdings and Beeland

Interests Inc.

Co-Founder of the Quantum Fund

Creator of the Rogers International

Commodities Index (RICI)

Sold for USD 4.9 billion (Year 2011)

Market Cap when F&M got involved was $4-5m. Sale price of US$4.9bn. Assets acquired for 22c in the dollar and

sold for $17.25

Rio Alto & Sulliden Merger $464MM value on closing (Year 2014)

F&M acquired Sulliden in March 2009 and resolved long-standing disputes regarding title. Current resource of

3.4moz Au (Ag co prod)

Market Cap – C$300 million (ongoing)

Exploration company with portfolio of assets in Brazil. Current mineral resource of 7.6 moz

Market Cap – C$440 million (ongoing)

World-class 400 km long Amazon potash basin with similar scale, geology and age as the Saskatchewan basin in

Canada

Invest in companies with High growth potential

Add Capital, Talent, Strategy and Market Knowledge

to strengthen its portfolio companies

F&Ms’ fully integrated team has >200 employees and

consultants

Currently has investment in 33 portfolio companies of

which 22 are listed vehicles.

What we do

Key select deals

F&M Leadership

For more information visit us on http://www.forbesmanhattan.com/

Joe Carrabba

Chairman Fura Gems Inc

Over 40 years’ of international experience in

the mining industry

Former Chairman and President & CEO of

Cliffs Natural Resources Inc., Prior joining

Cliffs, held various senior operating positions

with Rio Tinto Plc, including President and

COO of Diavik Diamond Mines.

10

Legal, Accounting & Back Office

11

lawyers

Capital Markets & Investor

Relations

> 20

accou

ntants

Operations:

50 Geologist

50 Engineers

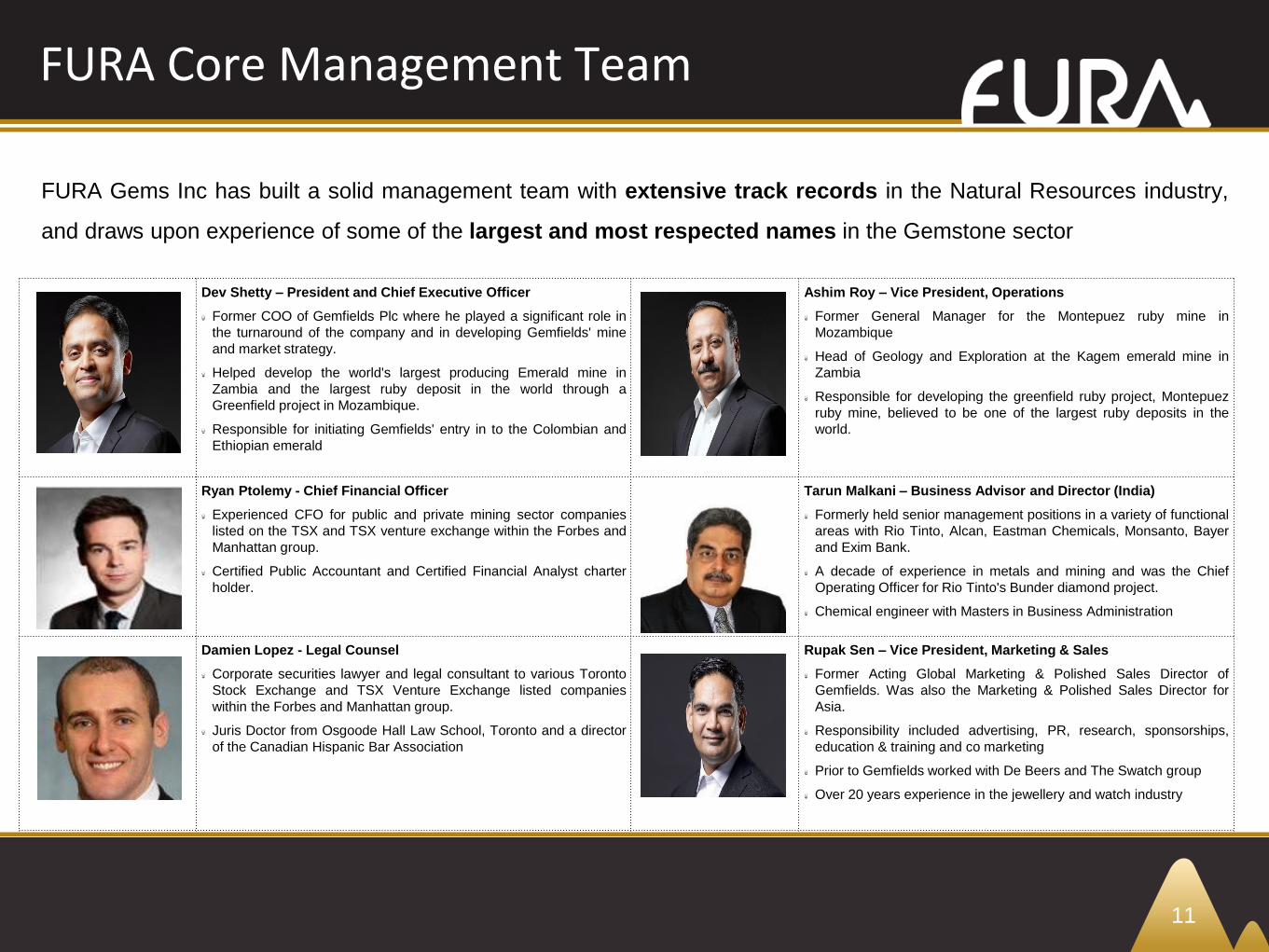

FURA Core Management Team

R

Dev Shetty – President and Chief Executive Officer

Former COO of Gemfields Plc where he played a significant role in

the turnaround of the company and in developing Gemfields' mine

and market strategy.

Helped develop the world's largest producing Emerald mine in

Zambia and the largest ruby deposit in the world through a

Greenfield project in Mozambique.

Responsible for initiating Gemfields' entry in to the Colombian and

Ethiopian emerald

Ashim Roy – Vice President, Operations

Former General Manager for the Montepuez ruby mine in

Mozambique

Head of Geology and Exploration at the Kagem emerald mine in

Zambia

Responsible for developing the greenfield ruby project, Montepuez

ruby mine, believed to be one of the largest ruby deposits in the

world.

Ryan Ptolemy - Chief Financial Officer

Experienced CFO for public and private mining sector companies

listed on the TSX and TSX venture exchange within the Forbes and

Manhattan group.

Certified Public Accountant and Certified Financial Analyst charter

holder.

Tarun Malkani – Business Advisor and Director (India)

Formerly held senior management positions in a variety of functional

areas with Rio Tinto, Alcan, Eastman Chemicals, Monsanto, Bayer

and Exim Bank.

A decade of experience in metals and mining and was the Chief

Operating Officer for Rio Tinto's Bunder diamond project.

Chemical engineer with Masters in Business Administration

Damien Lopez - Legal Counsel

Corporate securities lawyer and legal consultant to various Toronto

Stock Exchange and TSX Venture Exchange listed companies

within the Forbes and Manhattan group.

Juris Doctor from Osgoode Hall Law School, Toronto and a director

of the Canadian Hispanic Bar Association

Rupak Sen – Vice President, Marketing & Sales

Former Acting Global Marketing & Polished Sales Director of

Gemfields. Was also the Marketing & Polished Sales Director for

Asia.

Responsibility included advertising, PR, research, sponsorships,

education & training and co marketing

Prior to Gemfields worked with De Beers and The Swatch group

Over 20 years experience in the jewellery and watch industry

11

FURA Gems Inc has built a solid management team with extensive track records in the Natural Resources industry,

and draws upon experience of some of the largest and most respected names in the Gemstone sector

12

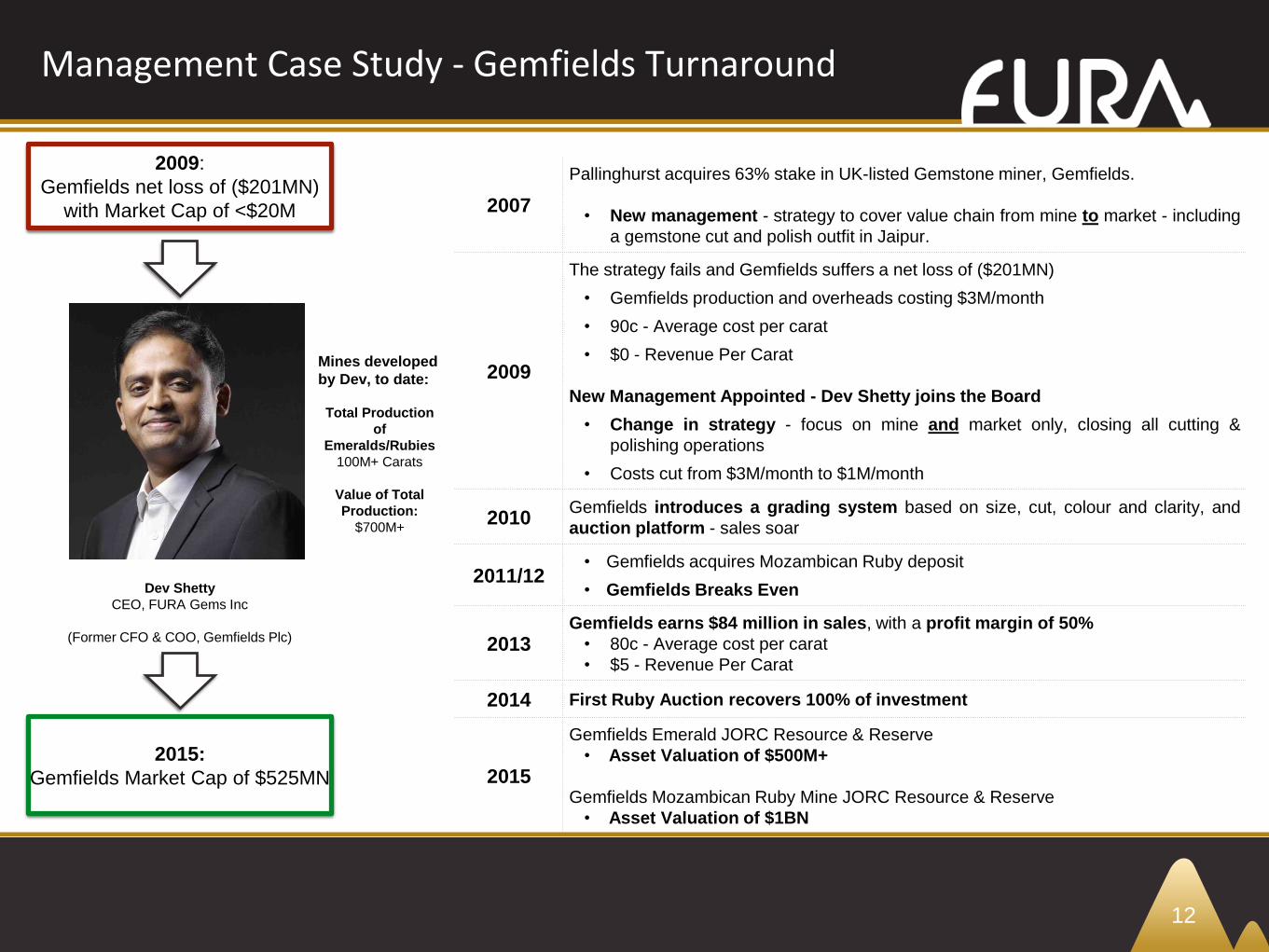

Management Case Study - Gemfields Turnaround

2009:

Gemfields net loss of ($201MN)

with Market Cap of <$20M 2007

Pallinghurst acquires 63% stake in UK-listed Gemstone miner, Gemfields.

• New management - strategy to cover value chain from mine to market - including

a gemstone cut and polish outfit in Jaipur.

2009

The strategy fails and Gemfields suffers a net loss of ($201MN)

• Gemfields production and overheads costing $3M/month

• 90c - Average cost per carat

• $0 - Revenue Per Carat

New Management Appointed - Dev Shetty joins the Board

• Change in strategy - focus on mine and market only, closing all cutting &

polishing operations

• Costs cut from $3M/month to $1M/month

2010Gemfields introduces a grading system based on size, cut, colour and clarity, and

auction platform - sales soar

2011/12• Gemfields acquires Mozambican Ruby deposit

• Gemfields Breaks Even

2013Gemfields earns $84 million in sales, with a profit margin of 50%

• 80c - Average cost per carat

• $5 - Revenue Per Carat

2014 First Ruby Auction recovers 100% of investment

2015

Gemfields Emerald JORC Resource & Reserve

• Asset Valuation of $500M+

Gemfields Mozambican Ruby Mine JORC Resource & Reserve

• Asset Valuation of $1BN

2015:

Gemfields Market Cap of $525MN

Dev Shetty

CEO, FURA Gems Inc

(Former CFO & COO, Gemfields Plc)

Mines developed

by Dev, to date:

Total Production

of

Emeralds/Rubies

100M+ Carats

Value of Total

Production:

$700M+

13

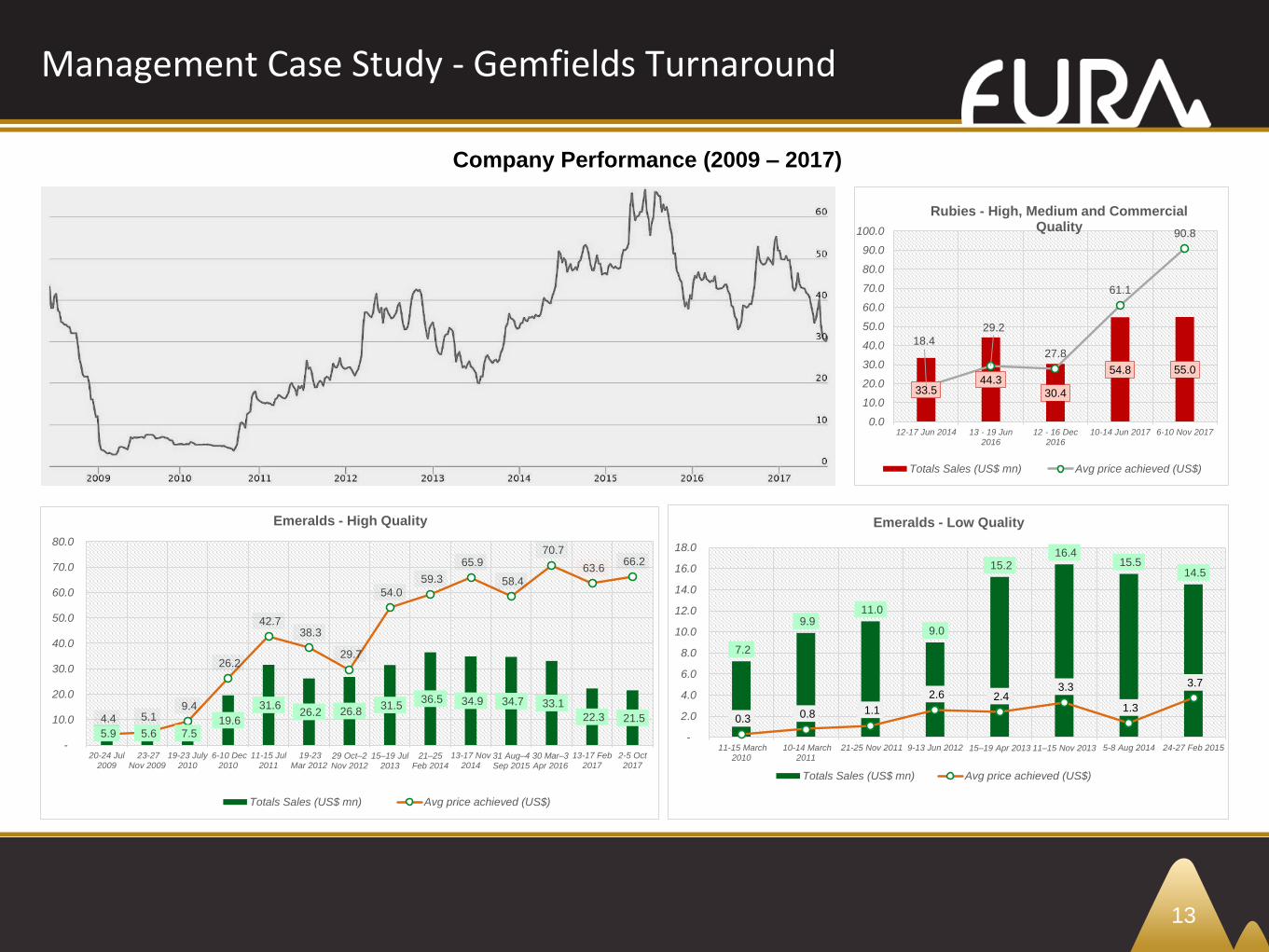

Management Case Study - Gemfields Turnaround

Company Performance (2009 – 2017)

5.9 5.6 7.5 19.6

31.6 26.2 26.8

31.5 36.5 34.9 34.7 33.1

22.3 21.5 4.4 5.1 9.4

26.2

42.7 38.3

29.7

54.0

59.3

65.9

58.4

70.7

63.6 66.2

20-24 Jul2009

23-27Nov 2009

19-23 July2010

6-10 Dec2010

11-15 Jul2011

19-23Mar 2012

29 Oct–2 Nov 2012

15–19 Jul 2013

21–25 Feb 2014

13-17 Nov2014

31 Aug–4 Sep 2015

30 Mar–3 Apr 2016

13-17 Feb2017

2-5 Oct2017

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Emeralds - High Quality

Totals Sales (US$ mn) Avg price achieved (US$)

7.2

9.9 11.0

9.0

15.2 16.4

15.5 14.5

0.3 0.8 1.1

2.6 2.4 3.3

1.3

3.7

11-15 March2010

10-14 March2011

21-25 Nov 2011 9-13 Jun 2012 15–19 Apr 2013 11–15 Nov 2013 5-8 Aug 2014 24-27 Feb 2015 -

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Emeralds - Low Quality

Totals Sales (US$ mn) Avg price achieved (US$)

33.544.3

30.4

54.8 55.0

18.4

29.2

27.8

61.1

90.8

12-17 Jun 2014 13 - 19 Jun2016

12 - 16 Dec2016

10-14 Jun 2017 6-10 Nov 20170.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Rubies - High, Medium and Commercial Quality

Totals Sales (US$ mn) Avg price achieved (US$)

14

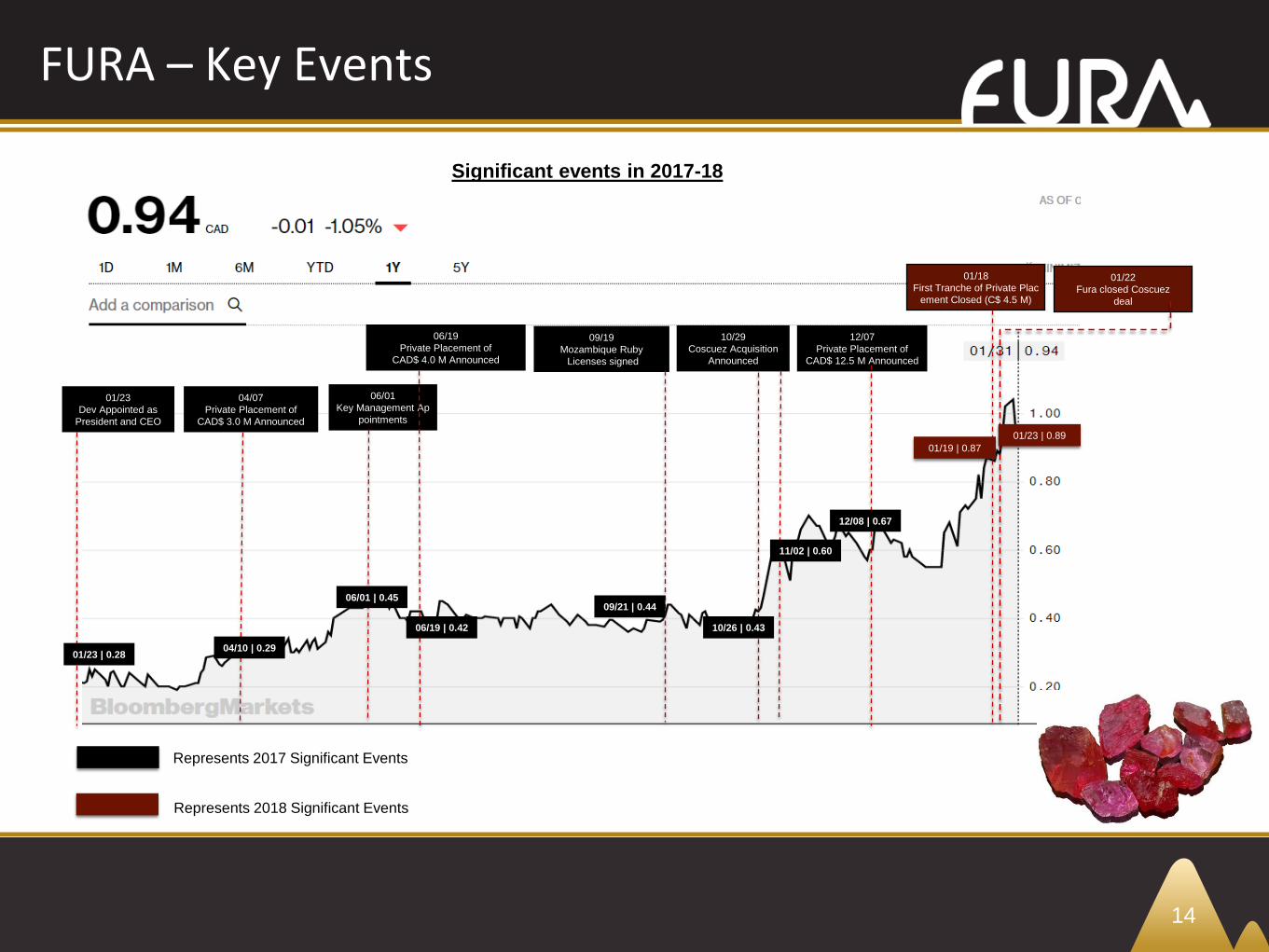

FURA – Key Events

Significant events in 2017-18

01/23 | 0.28

01/23

Dev Appointed as

President and CEO

04/07

Private Placement of

CAD$ 3.0 M Announced

04/10 | 0.29

06/01

Key Management Ap

pointments

06/01 | 0.45

06/19

Private Placement of

CAD$ 4.0 M Announced

06/19 | 0.42

09/19

Mozambique Ruby

Licenses signed

10/29

Coscuez Acquisition

Announced

12/07

Private Placement of

CAD$ 12.5 M Announced

09/21 | 0.44

10/26 | 0.43

11/02 | 0.60

12/08 | 0.67

01/18

First Tranche of Private Plac

ement Closed (C$ 4.5 M)

Represents 2017 Significant Events

Represents 2018 Significant Events

01/19 | 0.87

01/22

Fura closed Coscuez

deal

01/23 | 0.89

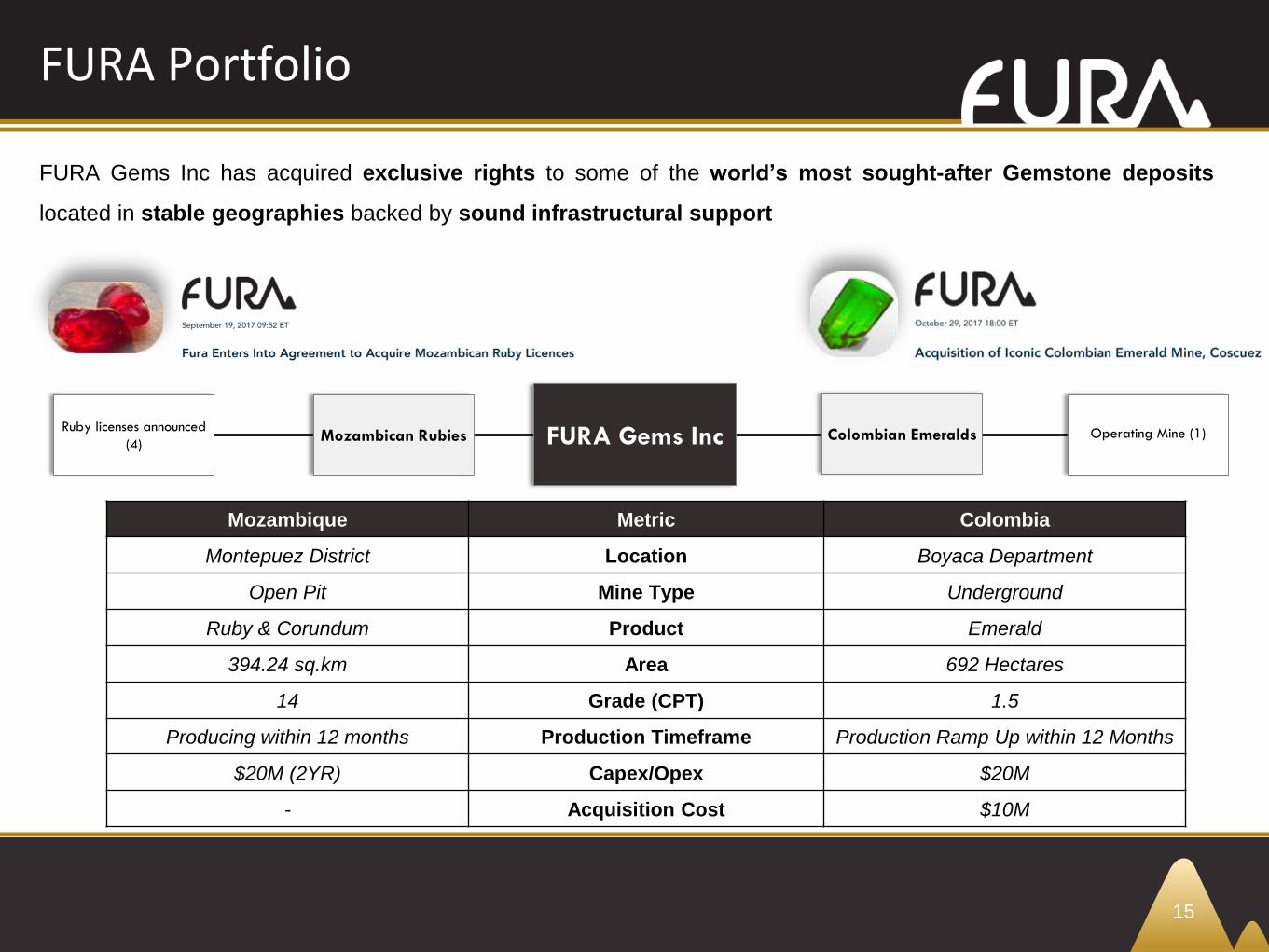

FURA Portfolio

15

Mozambican RubiesRuby licenses announced

(4)Operating Mine (1)

FURA Gems Inc has acquired exclusive rights to some of the world’s most sought-after Gemstone deposits

located in stable geographies backed by sound infrastructural support

FURA Gems Inc Colombian Emeralds

Mozambique Metric Colombia

Montepuez District Location Boyaca Department

Open Pit Mine Type Underground

Ruby & Corundum Product Emerald

394.24 sq.km Area 692 Hectares

14 Grade (CPT) 1.5

Producing within 12 months Production Timeframe Production Ramp Up within 12 Months

$20M (2YR) Capex/Opex $20M

- Acquisition Cost $10M

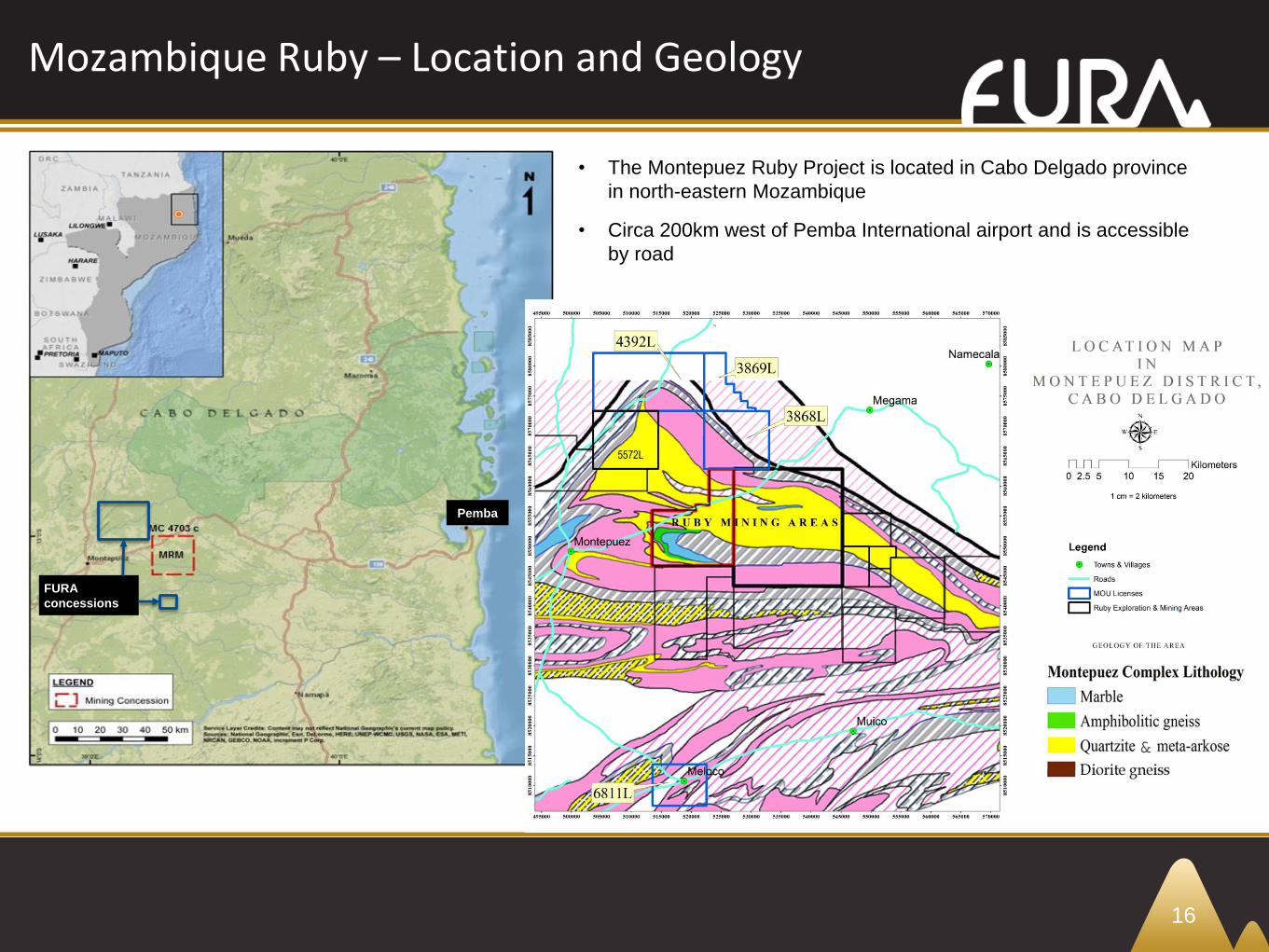

Mozambique Ruby – Location and Geology

16

• The Montepuez Ruby Project is located in Cabo Delgado province

in north-eastern Mozambique

• Circa 200km west of Pemba International airport and is accessible

by road

FURA

concessions

Pemba

Mozambique Ruby – Asset Mineralogy

Asset MineralogyClassification:

Red gem variety of Corundum (AL2O3)

Unique features:

Hardness: 9 on mohs scale (diamond 10)

Rarity: Large transparent rubies even rare than diamonds of same size and comparable

quality

Formation:

A corundum is formed when solutions rich in Alumina (AL2O3) intrudes a host rock rich

in chromium (Cr),iron (Fe) and vanadium (V)

Chromium is the colour agent and the amount of chromium present determines how

intense the red is

Primary deposits mining involves mining rubies from the host rocks (amphibolite) where

they are formed.

Secondary deposits are made up of gem crystals separated from host rocks. These are

classified by the way they been transported (e.g.. deposits carried by river are called

placers/alluvial) or the place of deposit.

Secondary ruby mineralization

Primary ruby mineralization

Low quality

High volume carat/ton)

High quality

Low volume carat/ton)

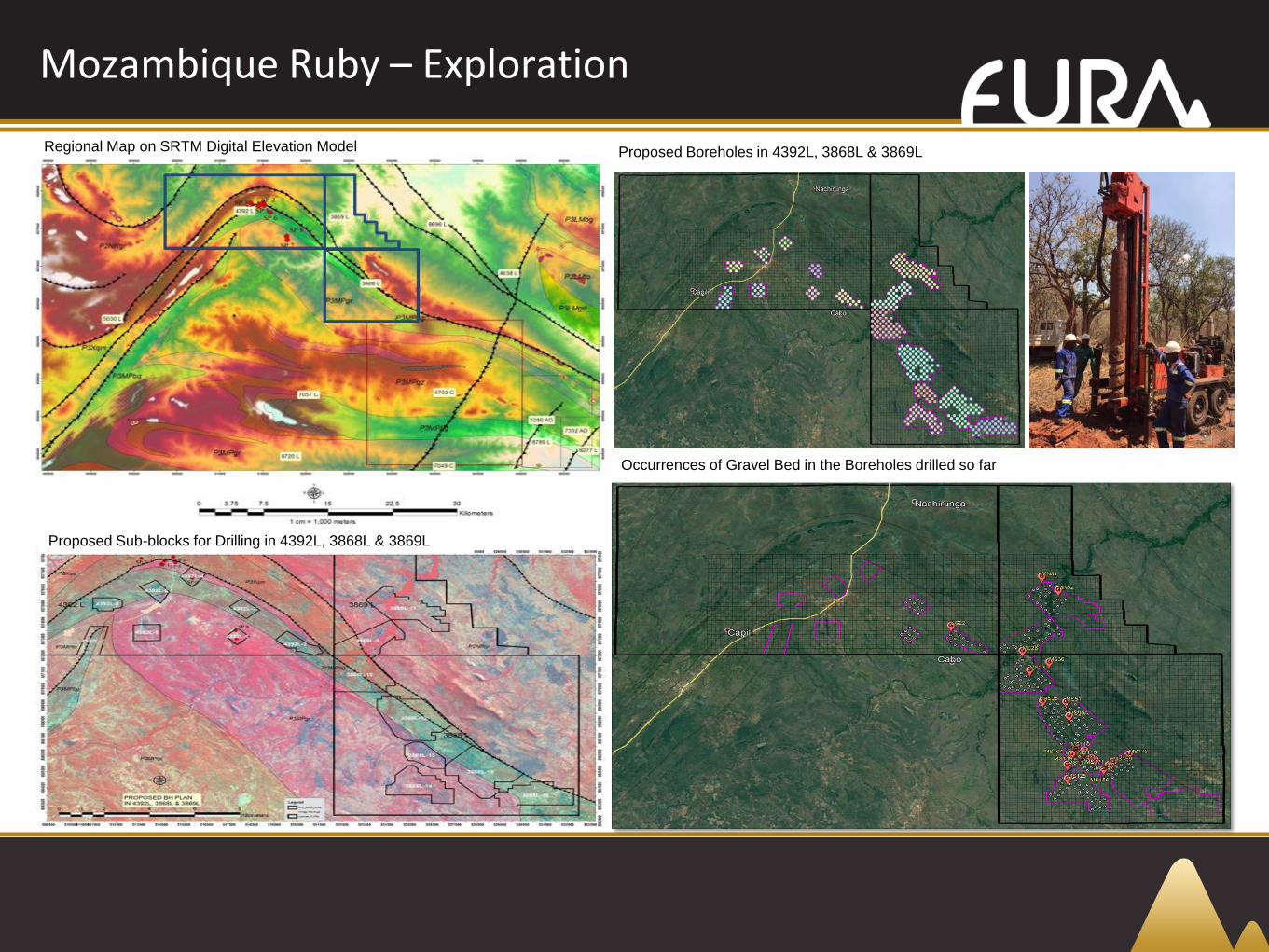

Mozambique Ruby – Exploration

Regional Map on SRTM Digital Elevation Model

Proposed Sub-blocks for Drilling in 4392L, 3868L & 3869L

Proposed Boreholes in 4392L, 3868L & 3869L

Occurrences of Gravel Bed in the Boreholes drilled so far

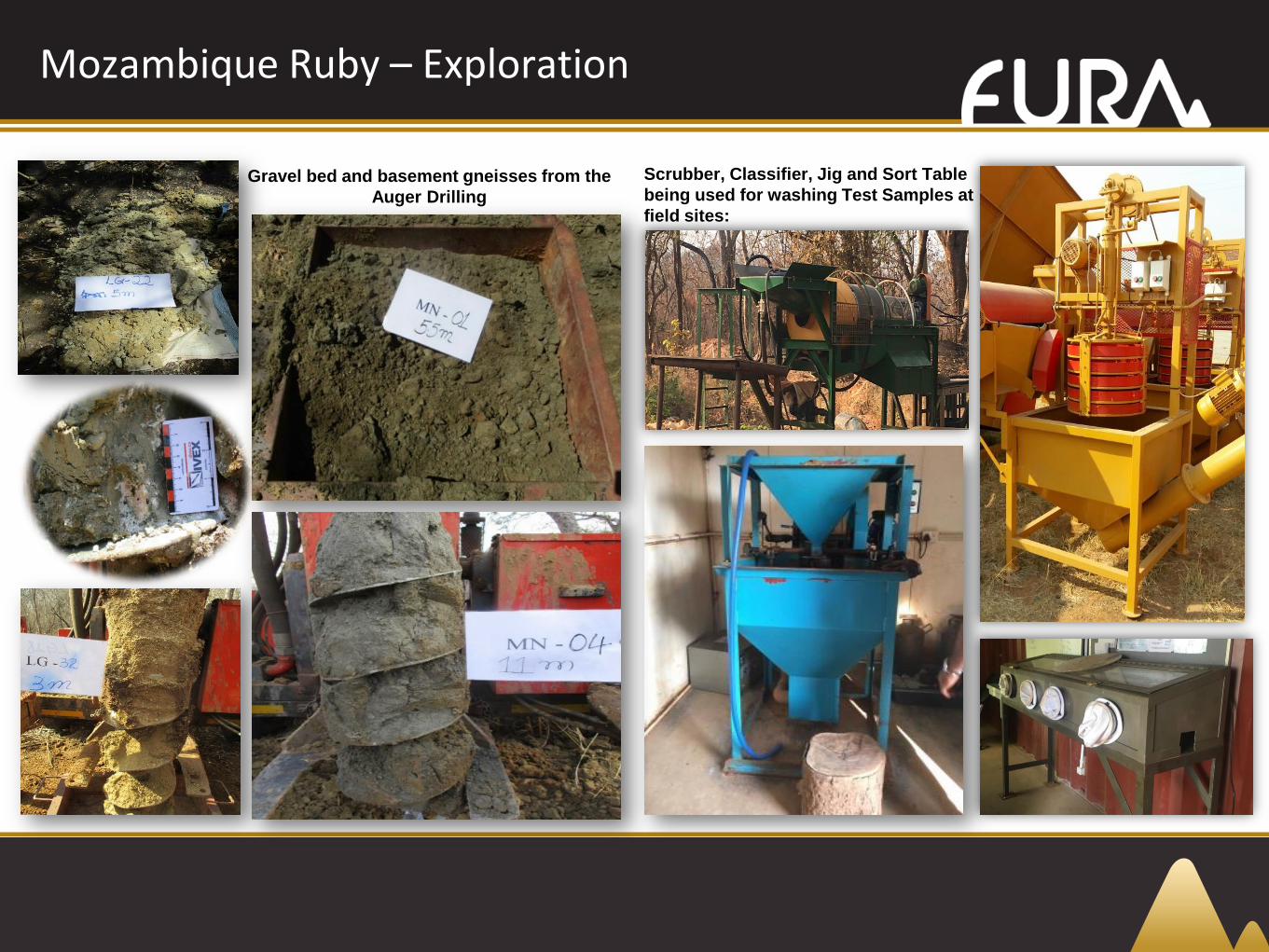

Mozambique Ruby – Exploration

Gravel bed and basement gneisses from the

Auger Drilling

Scrubber, Classifier, Jig and Sort Table

being used for washing Test Samples at

field sites:

Mozambique Ruby – Product

Colombia Emerald – Location and Geology

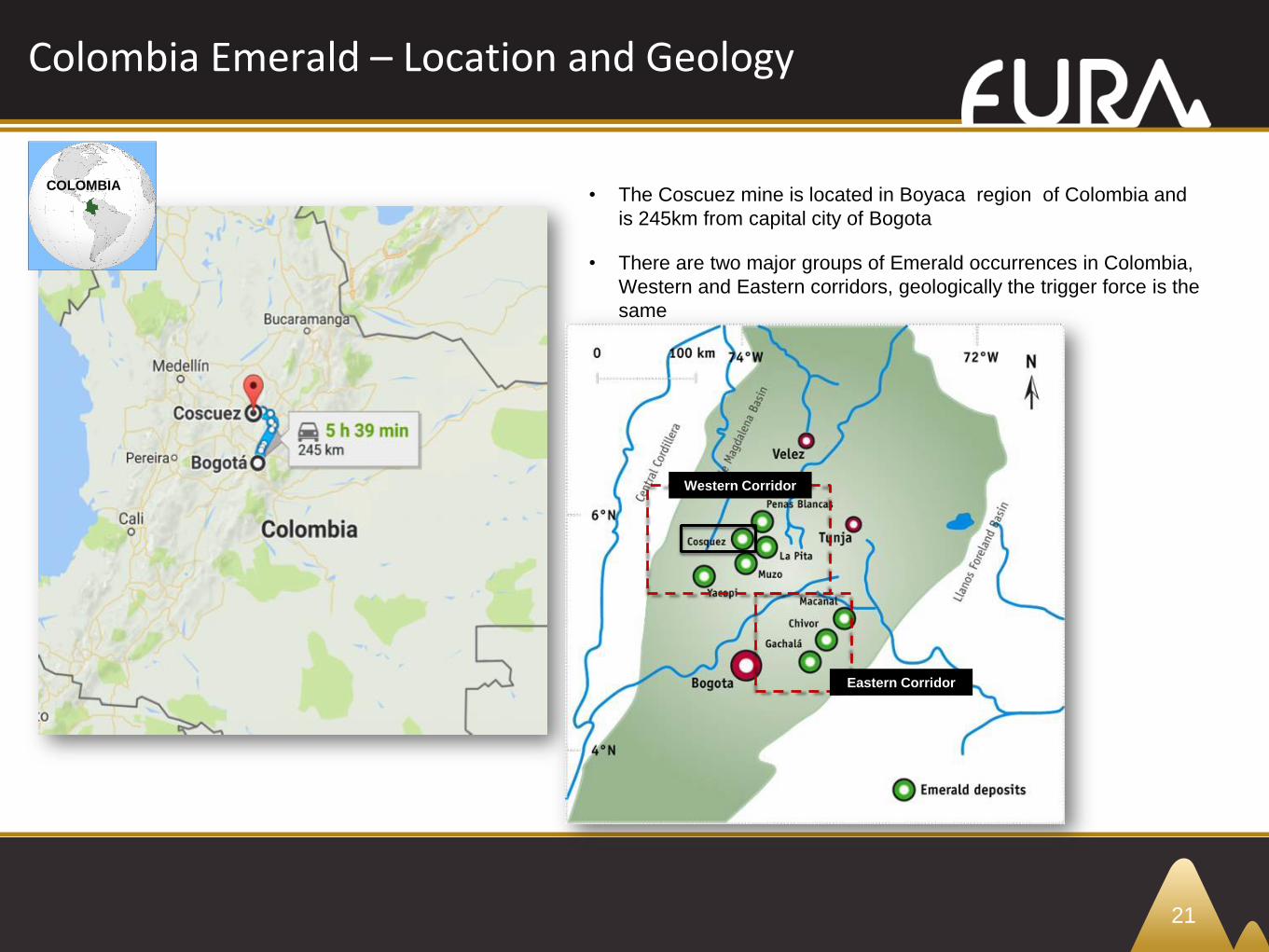

21

• The Coscuez mine is located in Boyaca region of Colombia and

is 245km from capital city of Bogota

COLOMBIA

• There are two major groups of Emerald occurrences in Colombia,

Western and Eastern corridors, geologically the trigger force is the

same

Western Corridor

Eastern Corridor

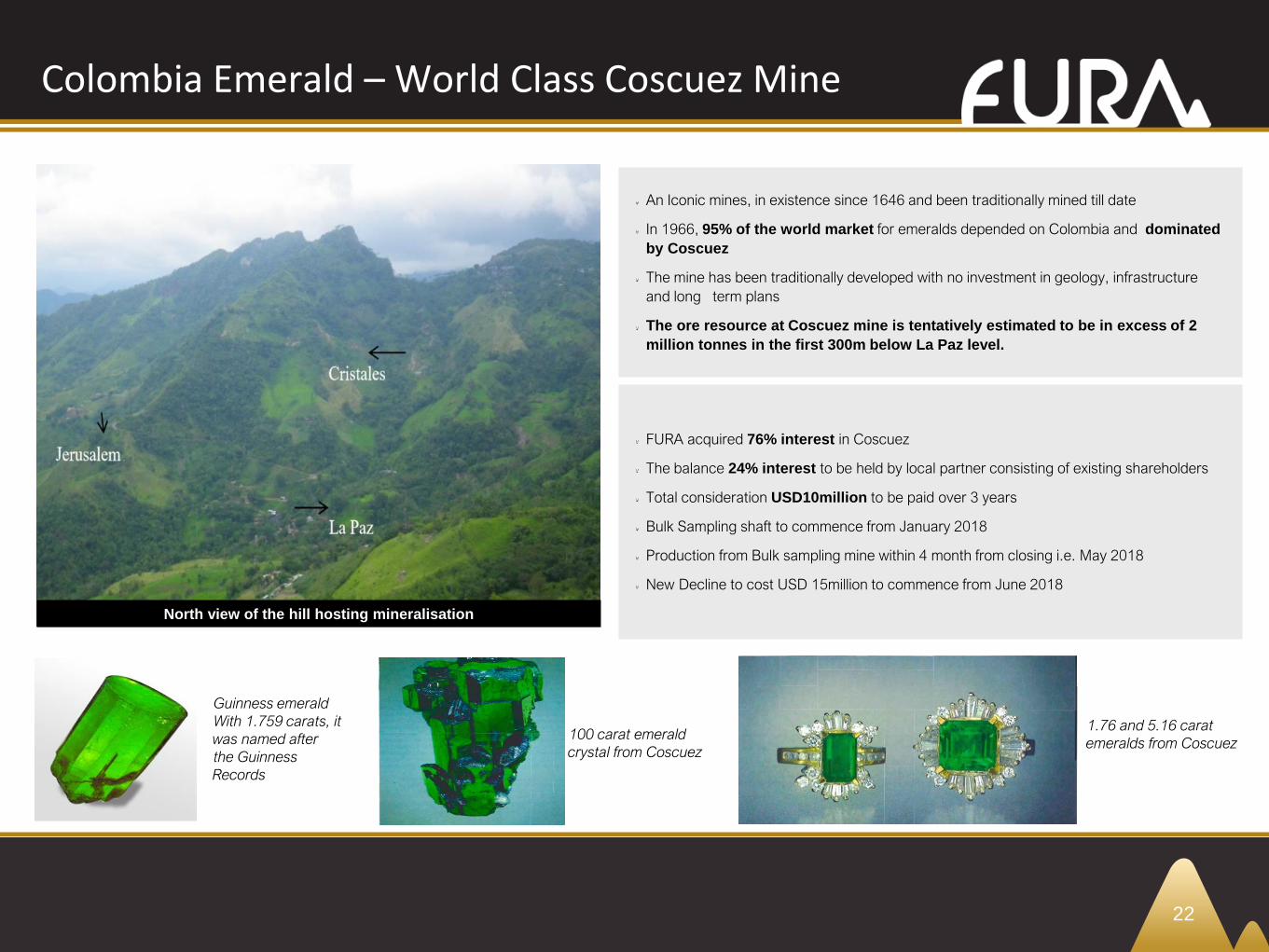

Guinness emerald

With 1.759 carats, it

was named after

the Guinness

Records

100 carat emerald

crystal from Coscuez

1.76 and 5.16 carat

emeralds from Coscuez

An Iconic mines, in existence since 1646 and been traditionally mined till date

In 1966, 95% of the world market for emeralds depended on Colombia and dominated

by Coscuez

The mine has been traditionally developed with no investment in geology, infrastructure

and long term plans

The ore resource at Coscuez mine is tentatively estimated to be in excess of 2

million tonnes in the first 300m below La Paz level.

FURA acquired 76% interest in Coscuez

The balance 24% interest to be held by local partner consisting of existing shareholders

Total consideration USD10million to be paid over 3 years

Bulk Sampling shaft to commence from January 2018

Production from Bulk sampling mine within 4 month from closing i.e. May 2018

New Decline to cost USD 15million to commence from June 2018

Colombia Emerald – World Class Coscuez Mine

22

North view of the hill hosting mineralisation

Colombia Emerald – Coscuez Current State

23

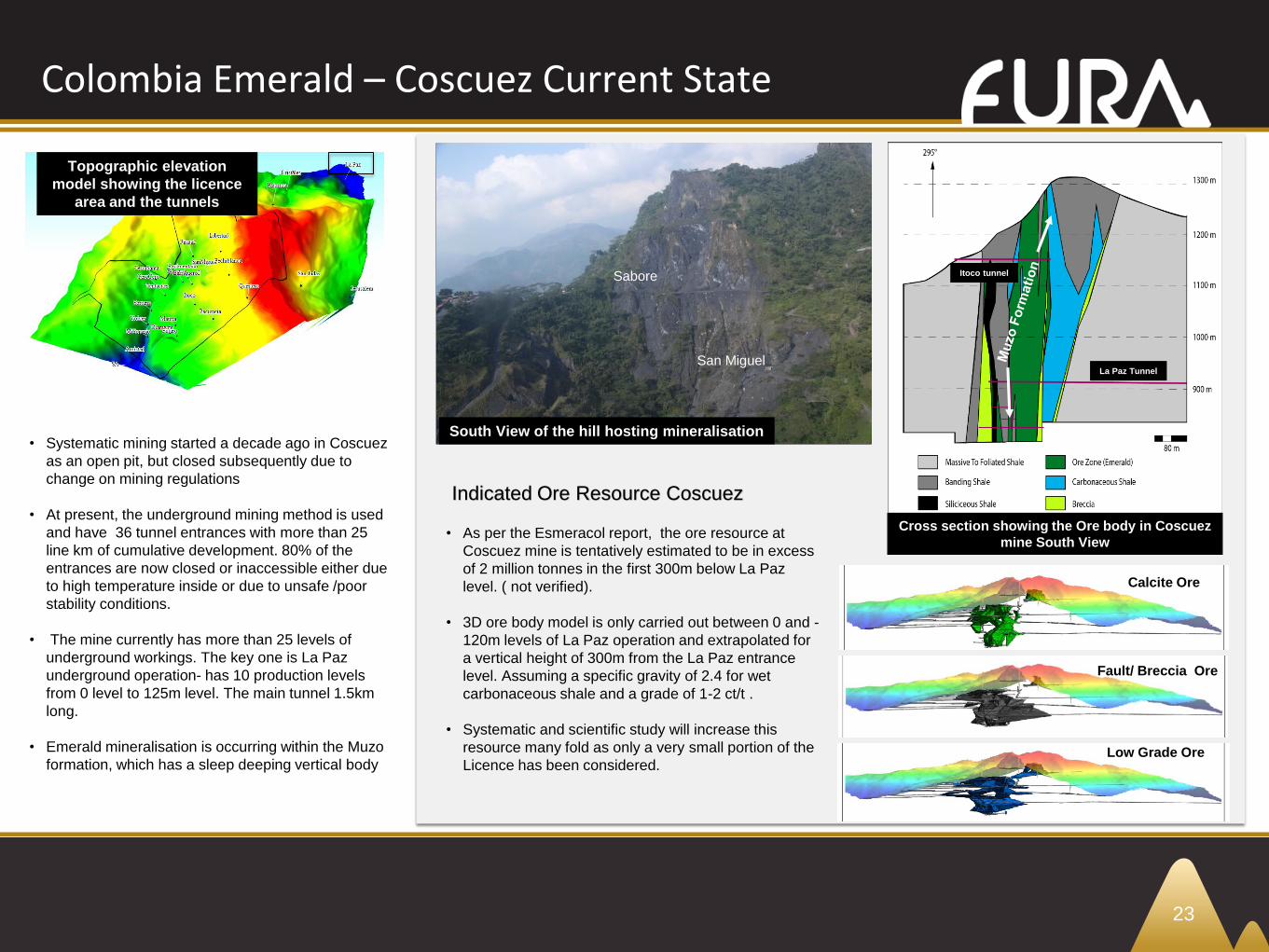

Topographic elevation

model showing the licence

area and the tunnels

Sabore

San Miguel

South View of the hill hosting mineralisation

Cross section showing the Ore body in Coscuez

mine South View

La Paz Tunnel

Itoco tunnel

Calcite Ore

Fault/ Breccia Ore

Low Grade Ore

Indicated Ore Resource Coscuez

• As per the Esmeracol report, the ore resource at

Coscuez mine is tentatively estimated to be in excess

of 2 million tonnes in the first 300m below La Paz

level. ( not verified).

• 3D ore body model is only carried out between 0 and -

120m levels of La Paz operation and extrapolated for

a vertical height of 300m from the La Paz entrance

level. Assuming a specific gravity of 2.4 for wet

carbonaceous shale and a grade of 1-2 ct/t .

• Systematic and scientific study will increase this

resource many fold as only a very small portion of the

Licence has been considered.

• Systematic mining started a decade ago in Coscuez

as an open pit, but closed subsequently due to

change on mining regulations

• At present, the underground mining method is used

and have 36 tunnel entrances with more than 25

line km of cumulative development. 80% of the

entrances are now closed or inaccessible either due

to high temperature inside or due to unsafe /poor

stability conditions.

• The mine currently has more than 25 levels of

underground workings. The key one is La Paz

underground operation- has 10 production levels

from 0 level to 125m level. The main tunnel 1.5km

long.

• Emerald mineralisation is occurring within the Muzo

formation, which has a sleep deeping vertical body

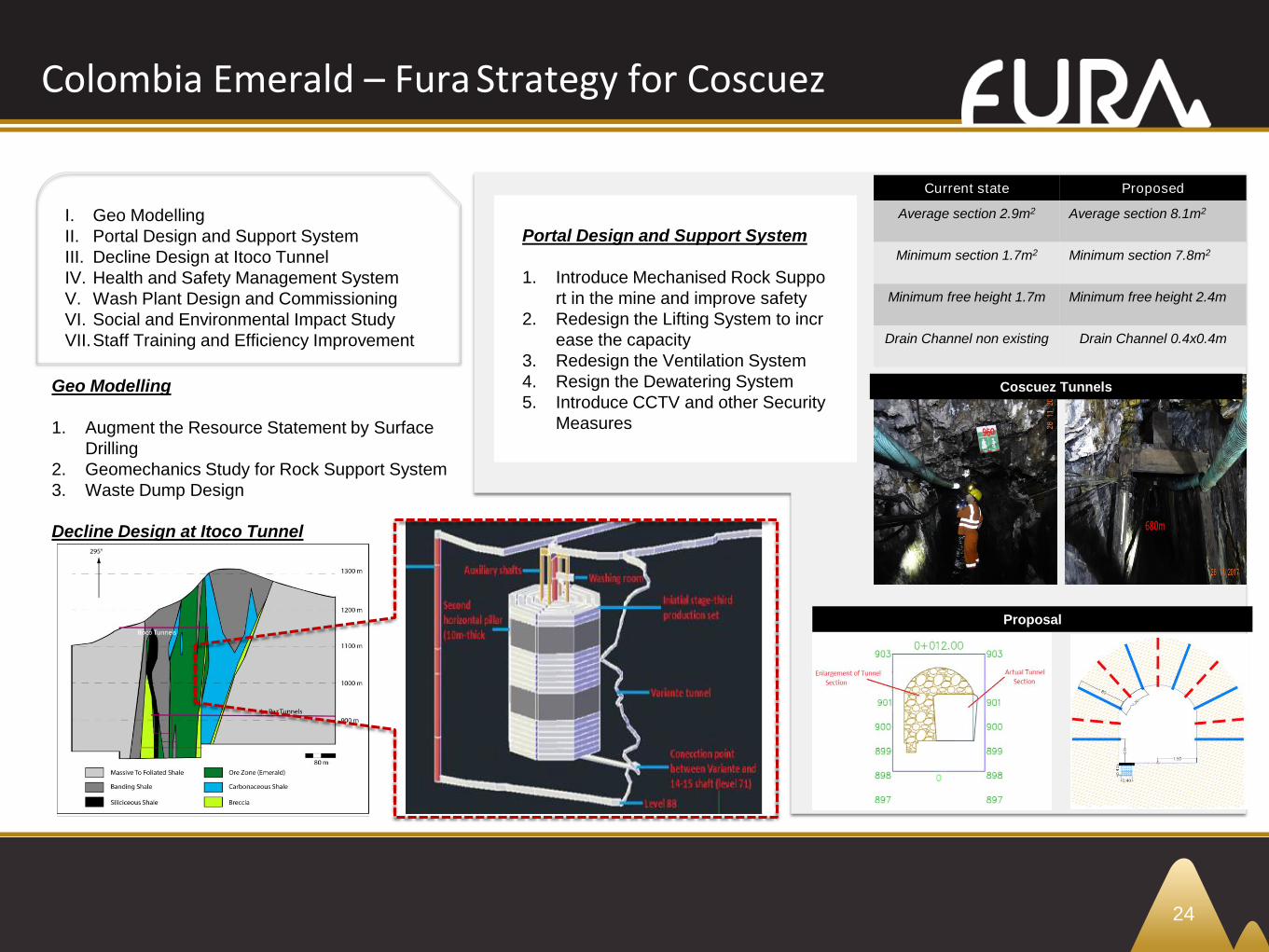

Colombia Emerald – Fura Strategy for Coscuez

24

I. Geo Modelling

II. Portal Design and Support System

III. Decline Design at Itoco Tunnel

IV. Health and Safety Management System

V. Wash Plant Design and Commissioning

VI. Social and Environmental Impact Study

VII.Staff Training and Efficiency Improvement

Geo Modelling

1. Augment the Resource Statement by Surface

Drilling

2. Geomechanics Study for Rock Support System

3. Waste Dump Design

Portal Design and Support System

1. Introduce Mechanised Rock Suppo

rt in the mine and improve safety

2. Redesign the Lifting System to incr

ease the capacity

3. Redesign the Ventilation System

4. Resign the Dewatering System

5. Introduce CCTV and other Security

Measures

Current state Proposed

Average section 2.9m2 Average section 8.1m2

Minimum section 1.7m2 Minimum section 7.8m2

Minimum free height 1.7m Minimum free height 2.4m

Drain Channel non existing Drain Channel 0.4x0.4m

Coscuez Tunnels

Proposal

Decline Design at Itoco Tunnel

4

5

6

7

CONTACT INFORMATION

Dev Shetty

President and Chief Executive Officer

+971- 50 187 2487

DubaiFura Services DMCC, 26J Almas Tower, Jumeirah Lake Towers, Dubai, UAE

Canada

Fura Gems Inc, 65 Queen Street West, Unit 800, Toronto, Ontario - M5H 2M5, Canada

www.furagems.com