Funny money may (double page spread)

14

Funny Money The weird and wonderful world of behavioural finance and economics Brought to you by… MAY

-

Upload

cowry-consulting -

Category

Economy & Finance

-

view

178 -

download

0

Transcript of Funny money may (double page spread)

Funny Money

The weird and wonderful world of behavioural

finance and economics

Brought to you by…

MAY

The weird and wonderful world of behavioural finance and economics

An Ode to Funny Money

ow customers make decisions is what we all strive to know

And Daniel Kahneman provided some of the answers in ‘Thinking

Fast and Slow’.

Sadly our brains are not as rational as we’d all like to think

In fact we often make choices a lot quicker than we can blink.

So when we are faced with a complex decision

We use instinct much more than we’d envision,

NEWSFLASH: We’re more like Homer Simpson than Mr Spock

Which for some of us can come as quite a shock!

But once we realise that survival and status are what drives us most

And that our reptilian brain is the real host,

We can help you communicate in a more natural way

Which will make customers happier and more likely to stay.

So here’s our ode to all things funny

About people’s behaviour, particularly when it comes to money,

We hope you enjoy our second edition

And make sure you take part in our competition!

“Overconfidence is a very serious problem. If you

don’t think it affects you, that’s probably because you’re overconfident.”

- Carl Richards, author of ‘Behaviour Gap’

(No need to explain the link between overconfidence and the recent financial crisis)

“Overconfidence is a very serious problem. If you

don’t think it affects you, that’s probably because you’re overconfident.”

- Carl Richards, author of ‘Behaviour Gap’

(No need to explain the link between overconfidence and the recent financial crisis)

4 MINREAD

2 MINREAD

3 MINREADCO

NTEN

TS

1 Premier MoneyHow can Leicester City help us to save more for retirement?

5 Emotional MoneyHow does your fund manager’s marriage affect your return on investment?

7 Desperate MoneyHow can your bladder help you make better financial decisions?

9 Virtual MoneyHow can artificial intelligence (AI) impact our understanding of behavioural finance and marketing?

11 The Financial Bias of the Month

15 Businesses BEhaving

17 An Interview withGerald Ashley

19 Nudges on the fly

3 Mobile MoneyHow do you give loans to a customer with no financial history?

We Love

3 MINREAD

2 MINREAD

3 MINREAD

2 MINREAD

1 MINREAD

1 MINREAD

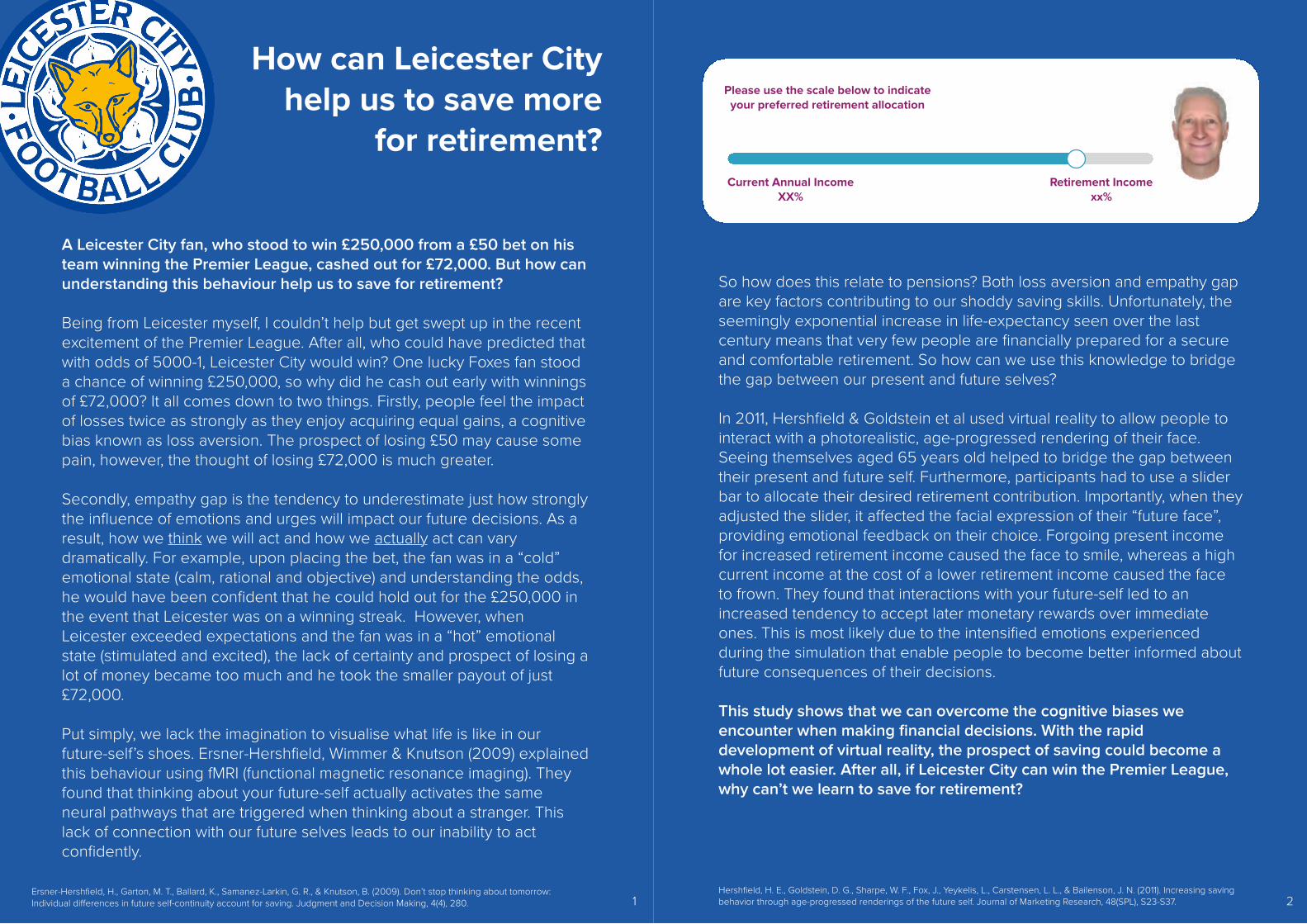

A Leicester City fan, who stood to win £250,000 from a £50 bet on his team winning the Premier League, cashed out for £72,000. But how can understanding this behaviour help us to save for retirement?

Being from Leicester myself, I couldn’t help but get swept up in the recent excitement of the Premier League. After all, who could have predicted that with odds of 5000-1, Leicester City would win? One lucky Foxes fan stood a chance of winning £250,000, so why did he cash out early with winnings of £72,000? It all comes down to two things. Firstly, people feel the impact of losses twice as strongly as they enjoy acquiring equal gains, a cognitive bias known as loss aversion. The prospect of losing £50 may cause some pain, however, the thought of losing £72,000 is much greater. Secondly, empathy gap is the tendency to underestimate just how strongly the influence of emotions and urges will impact our future decisions. As a result, how we think we will act and how we actually act can vary dramatically. For example, upon placing the bet, the fan was in a “cold” emotional state (calm, rational and objective) and understanding the odds, he would have been confident that he could hold out for the £250,000 in the event that Leicester was on a winning streak. However, when Leicester exceeded expectations and the fan was in a “hot” emotional state (stimulated and excited), the lack of certainty and prospect of losing a lot of money became too much and he took the smaller payout of just £72,000. Put simply, we lack the imagination to visualise what life is like in our future-self’s shoes. Ersner-Hershfield, Wimmer & Knutson (2009) explained this behaviour using fMRI (functional magnetic resonance imaging). They found that thinking about your future-self actually activates the same neural pathways that are triggered when thinking about a stranger. This lack of connection with our future selves leads to our inability to act confidently.

How can Leicester City help us to save more

for retirement?

Ersner-Hershfield, H., Garton, M. T., Ballard, K., Samanez-Larkin, G. R., & Knutson, B. (2009). Don’t stop thinking about tomorrow: Individual differences in future self-continuity account for saving. Judgment and Decision Making, 4(4), 280. 1

So how does this relate to pensions? Both loss aversion and empathy gap are key factors contributing to our shoddy saving skills. Unfortunately, the seemingly exponential increase in life-expectancy seen over the last century means that very few people are financially prepared for a secure and comfortable retirement. So how can we use this knowledge to bridge the gap between our present and future selves? In 2011, Hershfield & Goldstein et al used virtual reality to allow people to interact with a photorealistic, age-progressed rendering of their face. Seeing themselves aged 65 years old helped to bridge the gap between their present and future self. Furthermore, participants had to use a slider bar to allocate their desired retirement contribution. Importantly, when they adjusted the slider, it affected the facial expression of their “future face”, providing emotional feedback on their choice. Forgoing present income for increased retirement income caused the face to smile, whereas a high current income at the cost of a lower retirement income caused the face to frown. They found that interactions with your future-self led to an increased tendency to accept later monetary rewards over immediate ones. This is most likely due to the intensified emotions experienced during the simulation that enable people to become better informed about future consequences of their decisions.

This study shows that we can overcome the cognitive biases we encounter when making financial decisions. With the rapid development of virtual reality, the prospect of saving could become a whole lot easier. After all, if Leicester City can win the Premier League, why can’t we learn to save for retirement?

Hershfield, H. E., Goldstein, D. G., Sharpe, W. F., Fox, J., Yeykelis, L., Carstensen, L. L., & Bailenson, J. N. (2011). Increasing saving behavior through age-progressed renderings of the future self. Journal of Marketing Research, 48(SPL), S23-S37. 2

Please use the scale below to indicate your preferred retirement allocation

Current Annual IncomeXX%

Retirement Incomexx%

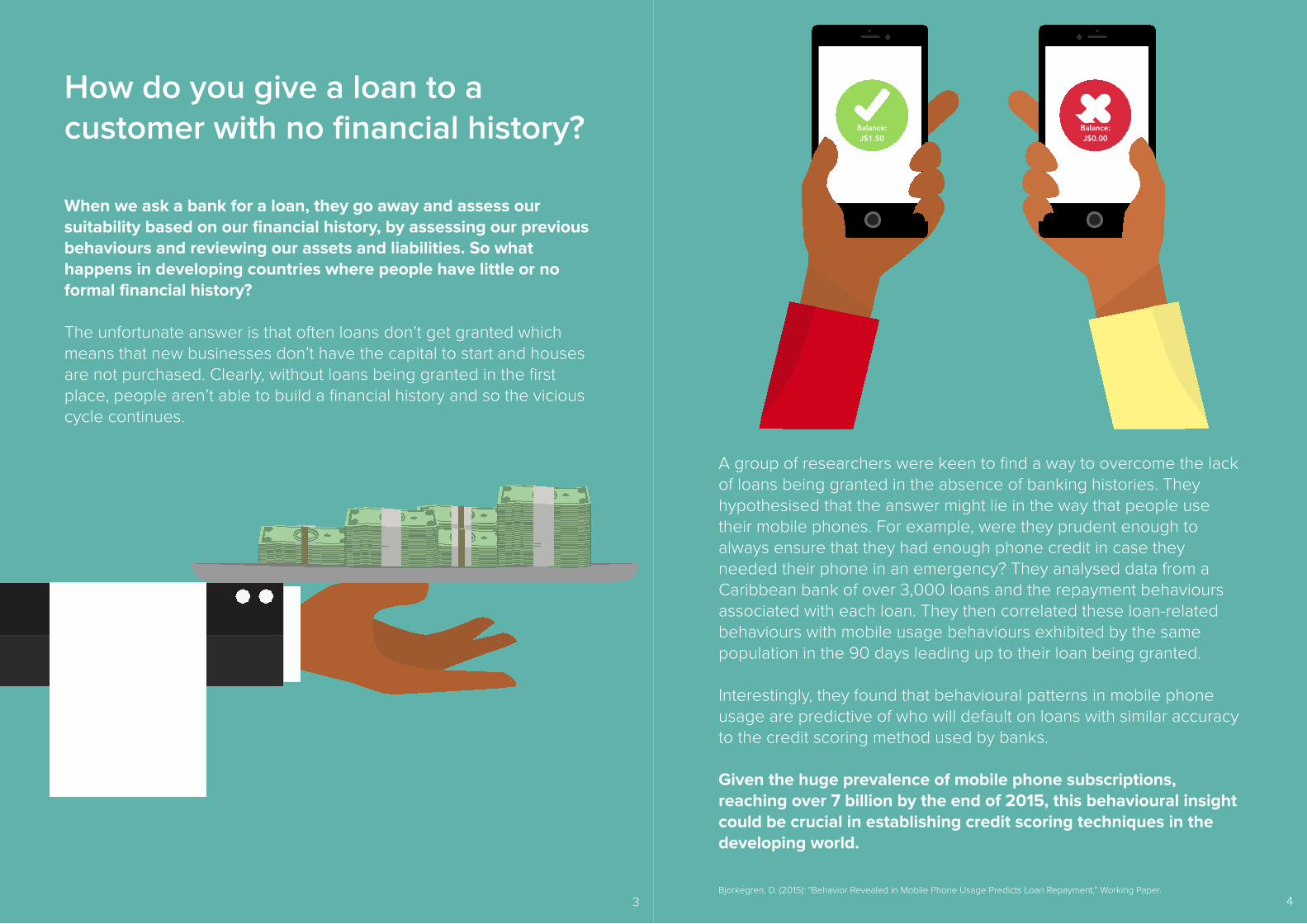

When we ask a bank for a loan, they go away and assess our suitability based on our financial history, by assessing our previous behaviours and reviewing our assets and liabilities. So what happens in developing countries where people have little or no formal financial history?

The unfortunate answer is that often loans don’t get granted which means that new businesses don’t have the capital to start and houses are not purchased. Clearly, without loans being granted in the first place, people aren’t able to build a financial history and so the vicious cycle continues.

How do you give a loan to a customer with no financial history?

3

A group of researchers were keen to find a way to overcome the lack of loans being granted in the absence of banking histories. They hypothesised that the answer might lie in the way that people use their mobile phones. For example, were they prudent enough to always ensure that they had enough phone credit in case they needed their phone in an emergency? They analysed data from a Caribbean bank of over 3,000 loans and the repayment behaviours associated with each loan. They then correlated these loan-related behaviours with mobile usage behaviours exhibited by the same population in the 90 days leading up to their loan being granted.

Interestingly, they found that behavioural patterns in mobile phone usage are predictive of who will default on loans with similar accuracy to the credit scoring method used by banks.

Given the huge prevalence of mobile phone subscriptions, reaching over 7 billion by the end of 2015, this behavioural insight could be crucial in establishing credit scoring techniques in the developing world.

Balance: J$1.50

Balance: J$0.00

Bjorkegren, D. (2015): “Behavior Revealed in Mobile Phone Usage Predicts Loan Repayment,” Working Paper. 4

It’s comforting to think that the people who manage our money are human calculators who are completely unaffected by the day to day emotional turmoil that affects the rest of us. However, a group of researchers have shown that this is not the case and that they too are capable of experiencing a whole spectrum of human emotions.

Researchers gathered data on fund managers’ divorces across 4 US States and correlated this with the performance of their respective funds. They found that when a fund manager gets divorced, they underperform by 7.4% that year. Interestingly, the event doesn’t have to be emotionally straining, as marriage has also been shown to lower performance, albeit by a slightly lower factor of 5.4% annually.

How does your fund manager’s marriage affect your return on investment?

5

The researchers attributed this drop in performance to an increased reliance on a bias known as the Disposition Effect. This relates to the tendency of investors to sell shares once the price has increased, whilst holding on to assets that have dropped in value. They argue that when fund mangers are emotionally distracted, they are less inclined to cut their losses and so hold on to underperforming stocks. This finding lends support to the growth of “robo-advice” platforms that use computer programmes and algorithms to make investment decisions in place of fund managers, such as the newly launched ‘Netwealth’. Headed up by Dr Gerard Lyons, Netwealth is a fund management platform which costs a third of the price of established money management firms and promises an emotionally vacuous (and hassle free) fund manager!

Lu, Y., Ray, S., & Teo, M. Till Death Do Us Part: Marital Events and Hedge Funds. 6

InvestmentDecisions

We all know the saying, “Never go shopping when you’re hungry”. When people are food deprived, they’re impulsive, and the chance of them purchasing a high-calorie “quick fix”, such as chocolate or crisps is much higher. Even when they know that in the long run, low calorie, healthier foods would satiate their hunger more effectively.

How often have you found yourself in the confectionary aisle, unable to stop yourself from filling your trolley with goodies that you just need? Frequently? Me too. However, hunger is not the only visceral state we need to consider when it comes to our ability to exercise self-control. Impulsive control is very important for human functioning. Without it, we would fall into overindulgence or financial mismanagement. Mirjam Tuk, a professor at the University of Twente in the Netherlands has found that bladder-control can be an important determinant of impulsive and reward seeking behaviour. In the study, disguised as a water-tasting test, 193 participants were split into 2 groups.

How can your bladder help you make better financial decisions?

7

Tal, A., & Wansink, B. (2013). Fattening fasting: hungry grocery shoppers buy more calories, not more food. JAMA internal medicine, 173(12), 1146-1148.

One group drank 50ml of water and the other drank 700ml. After 45 minutes, participants were asked a series of financial decision questions. They were offered either $16 tomorrow or $30 just over a month from now.

They found that those who had consumed less water had a desire for smaller but sooner rewards over later, larger rewards, whereas those with the urgency to urinate displayed increased impulse control in the behavioural domain.

Tuk, M. A., Trampe, D., & Warlop, L. (2011). Inhibitory spillover increased urination urgency facilitates impulse control in unrelated domains.Psychological Science, 22(5), 627-633. 8

Tuk also examined whether external cues could increase bladder control. Participants were primed with words related to urination – “bladder”, “toilet” – or unrelated words. They then had to perform the same financial decision task as before. They found that inhibitory effects triggered by cues in the environment can control urges in other domains. Put simply, even thinking about controlling our bladders can reduce the urge to act impulsively and help us to make more rational decisions. So next time you’re about to make a large purchase, drink a few glasses of water first and then think again.

In recent years, research in machine learning has made dramatic advances. Perhaps the most famous example is the AI Go player AlphaGo created at Google Deepmind. Although Go is overall a more popular game than Chess, it is not as well known here in the west owing to its Asian origins.

The scientific paper outlining Google’s approach, published in the journal Nature in January 2016 this year, leads with the sentence “the game of Go has long been viewed as the most challenging of classic games for artificial intelligence owing to its enormous search space and the difficulty of evaluating board positions and moves”.

The possibility of AI to beat the top human players was considered to be at least a decade away. The authors then describe the machine-learning algorithm that beat the European champion in five out of five professional games and later also beat the legendary South Korean player Lee Sedol, considered by many to be the top player over the past decade, in four out of five games. All games were broadcast on live TV across Asia and live streamed over the web to the rest of the world.

How can artificial intelligence (AI) impact our understanding of behavioural finance and marketing?

9Silver, D., Huang, A., Maddison, C. J., Guez, A., Sifre, L., Van Den Driessche, G.,& Dieleman, S. (2016). Mastering the game of Go with deep neural networks and tree search. Nature,529(7587), 484-489.

But it is not only in the area of games that machine learning has recently made significant progress. Another paper, also published in the journal Nature this year, shows how machine learning can be used to predict the synthesis of new inorganic-organic hybrid materials. The production of new materials is a complex process not fully understood and relies primarily on trial and error. A machine-learning algorithm trained on data from failed experiments was used to predict the successful synthesis of new materials. It greatly outperformed traditional human strategies. New hypotheses on the formation of materials, not previously understood, were revealed. These are only two out of many recent examples of where machine learning has supplemented human intelligence.

Practitioners in the areas of both behavioural finance and marketing are typically familiar with, now fairly standard, econometric techniques such as linear regression and controlled trials. These methods clearly have a firm place in the practitioner’s toolkit due to easy-to-understand properties and results that are easy to explain to clients.

But there is now scope for machine learning to make similar massive advances in our understanding of behavioural finance and marketing.

10

Dr Rickard Nyman, Cowry Consulting

Raccuglia, P., Elbert, K. C., Adler, P. D., Falk, C., Wenny, M. B., Mollo, A., ... & Norquist, A. J. (2016). Machine-learning-assisted materials discovery using failed experiments. Nature,533(7601), 73-76.

11

The

Of financial

biases

A -Z

12

And the financial bias of the month is…

We are herd animals and therefore we measure our behaviour in relation to each other to decide what is acceptable and appropriate in social settings.

Similarly, when we don’t have enough information about a given situation, we rely on the social default for guidance. For example, when English participants were asked to select a tea where the description was written in Korean, people were more than 3x as likely to mimic the choice of the person before them.

However, this effect was not observed when choosing between English teas. This is potentially because more information was available to help participants make an informed decision. Therefore they didn’t feel the need to follow others.

13

Social Norms

Huh, Y. E., Vosgerau, J., & Morewedge, C. K. (2014). Social defaults: Observed choices become choice defaults. Journal of Consumer Research,41(3), 746-760.

14

So what do Social Norms have to do with Donald Trump’s somewhat surprising success in the recent US presidential race?

In the US, each state takes it in turn to vote for their chosen presidential candidate. Therefore, due to the sequential nature of the voting system, winning one state can lead to voters in the subsequent states jumping on the bandwagon.

This often results in certain candidates picking up momentum as the primaries progress and, before you know it, Trump comes out on top #TopTrumps.

9

Have you ever had a free coffee from Pret a Manger?

Last year, Pret a Manger’s CEO, Clive Shlee, told his staff that they had a certain number of hot drinks and food to give away each week

for free, resulting in a huge 28% of customers walking away with something completely free that they had been prepared to pay for. The rumour quickly spread that these freebies were reserved for

particularly attractive customers. Clive Shlee seems to be employing some effective behavioural principles to get people buying Pret coffees, instead of employing the more common, expensive and

rational clubcard or loyalty systems.

Type something

When we are subject to a random act of kindness,

we are more likely to respond with an even

greater benefit in kind. In Pret a Manger’s case, this

would be repeat business.

Clive Shlee understands that if more people are

walking around drinking Pret coffees, it creates a

powerful social norm that that this is the thing to do.

The rumour that these freebies were only

handed out to attractive customers plays on and

confirms our innate superiority bias (the belief that we are all better than average at most things, a

statistically impossible phenomenon!).

Businesses BEhaving

Here’s why the Pret approach is a behaviourally insightful model:

15 10

Brain-friendly Breakfast Club

Keep an eye out for an invitation to our new breakfast club which promises

some serious food for thought!

See you at Nudgestock!Co-sponsored by Cowry Consulting

16

with thanks to our sponsors

18

Since humans build computers, is it true that there will always be cognitive bias “built into the machine"?

In truth - Yes and No! To date, much computing has been about trying to "find the answer" to a particular question or problem. Here our biases may well creep into the design process of any decision software. Typically we may filter potential inputs so influencing potential outputs. Some of the latest decision software tries to avoid this by avoiding any pre-filtering or definitive assumptions by humans.

We use heuristics and short cuts as we have limited processing power - but modern computing has staggering capacity these days so it makes sense to use it. In the future, computing will have self-learning programming elements (this worries some people) that will help

the computer to find emerging solutions based upon both all the potential inputs and the ability to test and retest endless combinations of those inputs. So I think machine learning techniques will even out human biases and help us make better decisions.

Two additional thoughts:

Although it is a truism, never forget that risk is dynamic. It flexes and twists in ways that can confuse and fool us. Never be too "certain" unless you are solving straightforward maths.

Sometimes the best answer is ‘don't know’ or perhaps a ‘maybe’. These can sometimes be more

valid answers than torturing data to death to get "the answer". Such results rarely stand the test of future dynamic changes.

Secondly remember the phrase “The Map is not the Territory”. However accurate and detailed your model is (The Map), real life conditions (The Territory) will throw up differences, gaps and overlaps and downright totally unexpected shocks and surprises.

The best decision makers and risk takers understand this intimately and try to account for variance by being flexible and having spare time/money built into their plans.

“…machine learning techniques will even out human biases and help us make better decisions”

Enjoyed this interview?Read more from Gerald Ashley in his new book “Two Speed World: the impact of explosive and gradual change – its effect on you and everything else” JUST CLICK HERE

17

“An interview with ...

Gerald Ashley”

This month we were lucky enough to get a couple of minutes with Gerald Ashley, to ask him some questions about the weird and

wonderful world of behavioural finance and economics.

So if brains can think so quickly, what’s the best rule of thumb for risk taking in your book?

I like the Venture Capital rule for business plans - always double the costs and halve the expected revenue projections!By their nature, entrepreneurs are confident and gutsy but they are not alone in tending to be overconfident. We can all suffer from overconfidence. Numerous studies show we overrate our driving skills, believe others are more likely to be hit by a bus than ourselves and that our neighbours are more likely to get burgled than us.

We are taught confidence is good - but decision makers and risk takers need to guard against misplaced "certainty”. One of the great lessons in risk is recognising that some situations are inherently uncertain and no amount of bluster or over-use of "models" will change that. Flexibility of thought and agility of action are the critical keys.

In one sentence could you share an example of how computers using Predictive Analytics have forecasted far better than humans?

Machine learning is transforming intelligent investment portfolio selection. We may think that the human fund manager will always be better but my money is increasingly on the smart asset allocation app.

“One of the great lessons in risk is recognising that some

situations are inherently uncertain…”

Think you’ve seen a notable nudge?

Tweet us a picture with the hashtag #NudgesOnTheFly for a chance to win a

spot in next month’s Funny Money!

@CowryConsulting19

Nudges on the fly

Thank you for all of the wonderful entries we’ve received this month!

We’ve narrowed it down and our favourite nudge this month was spotted by Ed Carr!

Why do we love it?

A saying is judged to be more accurate or truthful if it rhymes, this is known as the rhyme-as-reason effect.

Therefore this poster encouraging people not to litter on the tube is effective because of the way it rhymes.

A famous example was used in the O.J Simpson trial with the defense's use of the phrase "If the gloves don't fit, then you must acquit."

competition

20

Brought to you by…

Raphy MarchBehavioural Designer

Ziba GoddardChoice Architect

Dr Rickard NymanCognitive Auditor

See you in July!