Fundign Optiona for Fire Districts in Washington State

45

FUNDING OPTIONS FOR FIRE DISTRICTS IN WASHINGTON STATE STRATEGIC MANAGEMENT OF CHANGE By: Jerry E. Thorson Federal Way Fire Department Federal Way, Washington An applied research project submitted to the National Fire Academy as part of the Executive Fire Officer Program. October 2001

Transcript of Fundign Optiona for Fire Districts in Washington State

FUNDING OPTIONS FOR FIRE DISTRICTS IN WASHINGTON STATE

STRATEGIC MANAGEMENT OF CHANGE

By: Jerry E. Thorson Federal Way Fire Department

Federal Way, Washington

An applied research project submitted to the National Fire Academy as part of the Executive Fire Officer Program.

October 2001

2

ABSTRACT

Washington State has experienced repeated efforts to limit property taxes. The next attempt,

which would limit property taxes to an annual 1% increase, is expected to pass in November

2001. If passed this measure would have a dramatic impact on fire districts throughout the state.

The problem is that as the inflation rate increases at approximately 3.9%, limiting property

taxes to a 1% increase will force fire districts to reduce services.

The purpose of this research was to identify funding options that will allow the Federal Way

Fire Department to maintain it’s current level of service. Evaluative research methods were used

to answer the following questions:

1. What fees, levies or other charges are available to supplement property taxes?

2. What are the advantages/disadvantages or unintended consequences of each option?

3. Which option or options provide the most consistent funding that will allow Fire Districts to

maintain their level of service?

The procedures used included a literature review, an external fire district survey and a review

of Washington State laws. The research also included a review of studies conducted in Federal

Way evaluating all aspects of fees for patient transports, which are currently performed by

private ambulances.

The results indicate that options for fire districts include an EMS levy, excess levies, bond

issues, service benefit charges, and an EMS fee for services. Each of these have positive and

negative attributes which the research has identified.

It is recommended that the Federal Way Fire Department collect a fee for patient transports

and evaluate the political impacts of implementing the service benefit charges. This research

identified, and evaluated the funding options and did not consider the politics of going to the

3

voters with an issue. The politics of whether to adopt a funding source was not an objective of

this research.

4

TABLE OF CONTENTS

ABSTRACT………………………………………………………………………………………2

TABLE OF CONTENTS………………………………………………………………………..4

INTRODUCTION……………………………………………………………………………….5

BACKGROUND AND SIGNIFICANCE……………………………………………………....7

LITERATURE REVIEW…………………………………………………………………….…9

PROCEDURES…………………………………………………………………………………16

RESULTS……………………………………………………………………………………….19

DISCUSSION…………………………………………………………………………………...26

RECOMMENDATIONS……………………………………………………………………….30

REFERENCES………………………………………………………………………………….32

APPENDIX A (Roger Ferris Memo)…………………………………………………………..34

APPENDIX B (Survey Letter)...……………………………………………………………….35

APPENDIX C (Service Benefit Charge Survey Form)……….……………………….……..36

APPENDIX D (Survey Results Summary)..…………….…………………………………….39

5

INTRODUCTION

Fire districts in Washington State are primarily funded through property taxes. These

taxes are based on the assessed valuation of each property within the fire district’s boundaries.

The county assessor is required to reassess each property within the county on a regular basis.

As property values increase so do the taxes a property owner must pay. Over the years in

Washington State, the taxpayers have grown unhappy with the tax increases. There is an

ongoing citizen effort to limit the state from increasing taxes unless they are specifically

authorized by voters for every proposed increase. In the last three years there have been three

tax limitation initiatives on the state ballot to limit those taxes. Two of these initiatives have

passed however; both have been repealed by the State Supreme Court as a violation of state

constitution. In November 2001, Initiative 747 (I-747) is expected to pass both with the

electorate and the legal challenge that is sure to follow.

While many districts throughout the nation are facing various budget cuts, the latest effort

in Washington is predicted to deliver a severe blow to fire district budgets. If I-747 passes and is

upheld by the State Supreme Court, the effect will be dramatic. It will limit the taxes that a fire

district can collect in 2002 to no more than one percent above the amount collected in 2001. Fire

districts throughout the state will have to reduce spending or find some way to replace the lost

income. Some districts including Federal Way have placed measures on the ballot to allow the

collection of taxes above the 1% cap imposed by I-747. This however will have to be an annual

effort with the public voting on it each year. If the measure fails the district is forced to either

resubmit the item to the voters, or make drastic budgetary cuts. Rather than this short-term issue

many districts are looking for a long-term solution by adopting alternative funding sources.

6

The problem is that as the inflation rate (based on the Consumer Price Index-

Washington) increases at approximately 3.9%, the impact of limiting property taxes to a 1%

increase will force fire districts to reduce services. Fire districts are affected by inflation just as

homeowners are. The current initiative will impose a reduction of $500,000.00 on the Federal

Way Fire Department in the year 2002 if passed and no other relief is obtained. Federal Way’s

total budget for year 2001 is approximately ten million dollars. This equals a 4.2% reduction in

the districts total budget at a time when operational costs are increasing at an annual rate of

approximately 3.9%.

The purpose of this research is to identify funding options that will allow the Federal

Way Fire Department to maintain its current level of service and keep up with residential and

commercial growth. Evaluative research methods are used to answer the following questions:

1. What other fees, levies, or charges are available to supplement property taxes?

2. What are the advantages/disadvantages or unintended consequences of each option?

3. Which option or options provide the most consistent funding that will allow Fire

Districts to maintain their current level of service?

The research includes a survey of fire districts throughout the state that are using the service

benefit charge as an alternate source of funding, a review of state laws, and other reference

sources. The research also included a review of previous studies conducted in Federal Way

evaluating all aspects of adopting a fee for patient transports.

7

BACKGROUND AND SIGNIFICANCE

Funding options are a concern for all fire districts in Washington State. This research

will focus on the Federal Way Fire Department, however the outcomes and recommendations

can be applied to districts throughout the state, as the funding laws and options available will

apply statewide.

The Federal Way Fire Department is a medium size district covering 34 square miles

with a population of approximately 105,000 people. Fire department services are provided to the

entire city of Federal Way, part of the city of Des Moines and part of unincorporated King

County. The area protected by the fire district is primarily residential, with retail, business and

manufacturing occupancies.

When the city of Federal Way incorporated in 1990 the citizens elected to annex into the

local fire district. Federal Way Fire Department remained a separate agency not under the

control of the new city. The Fire Department is legally a separate special purpose district and is

bound by the state laws that affect those districts. It is important to note that while the name

implies that the Federal Way Fire Department is a city department, it is in fact legally a fire

district.

Six stations are staffed full time with career firefighters. Minimum staffing for the

districts is normally 20 but the minimum staffing is18 firefighters due to sick leave or other

factors. Federal Way Fire Department is a full service fire districts providing basic life support

(BLS) fire incident response, fire inspections and public education. The district also maintains

hazardous materials and technical rescue teams. All of these responsibilities require extensive

training and coordination in order to function properly.

8

During the seventies and eighties, the area experienced a rapid growth in population,

however due to existing tax limitations, growth in staff did not keep pace with the increased

population. The fire district Board of Commissioners has made it a high priority to adopt the

maximum tax increase each year until the staffing reaches the district's goal of three-person

engine companies. The maximum amount that a taxing district may raise the taxes paid by an

individual property is based on the assessed value of the property. If the value of the property

increase by four percent then the taxes may be increased by four percent. If the assessed

valuation is increased over six percent then a taxing district may still only increase property taxes

up to six percent over the amount collected in the preceding year.

If I-747 passes in the November general election it will limit the taxes the district can

collect to no more than one percent above the amount collected in the preceding year, without a

public vote. Currently fire districts are limited to a 6% increase, providing that property tax

values increased to at least that amount. I-747 would limit increases without voter approval to a

maximum 1% limit, even if the inflationary rate was higher. As a result of I-747 the fire district

will be forced to reduce services. In Federal Way’s case this would mean abandoning its long-

term goal of three-person engine companies. To mitigate this initiative the Federal Way Fire

Department placed a proposition in the September 2001 election to allow it to maintain services

at the current level. This measure passed giving the district one year to find alternative funding

sources that offer some long-term stability.

The research is relevant to the content and instruction of the National Fire Academy’s

(NFA) Strategic Management of Change course in several ways. By using the change

management model, the district has a much higher chance at succeeding with the new funding

sources. This research is the first step in the NFA’s change management model; analysis. By

9

analyzing the problem we have identified the situation and the steps needed to mitigate the

funding challenges. The process must include planning, implementation and

evaluation/institutionalism.

LITERATURE REVIEW

The literature review began at the National Fire Academy’s Learning Resource Center. It

continued in Federal Way with an analysis of documents, state laws, memos, committee reports

and a fire districts survey. Throughout the examination of the literature, it became apparent that

others have experienced the same problem that Federal Way is now facing. The research found

that there are many creative ways to obtain additional funding for fire districts programs.

The review shows that the funding concerns in Washington are similar to those affecting

fire districts throughout the nation. It is apparent from the literature that many districts are

facing a reduction of revenue, while at the same time the demand for services is continuing to

increase each year. In many cases tax limitations are forcing districts to either reduce services or

obtain alternative funding sources.

In a situation in California that is strikingly similar to Washington’s, Dennis Stouffer

(1993) writes,

Under Proposition 13, the county could increase tax assessment by no more than 2%

annually on existing properties, even if the actual property values had risen by 100% or

more in the past year. While a real boon to property owners, proposition 13 was a clear

threat to all government services (p. 36).

Stouffer (1993) further describes the impacts of the tax limitations, “It was clear that

deeper funding cuts would immediately lead to serious degradation in fire suppression and

10

related services. Public safety would invariably be endangered by existing cuts and the further

erosion of staffing was unacceptable from a life safety standpoint” (p. 37).

Christopher Cotter (1994) summarized the problem by writing “Clearly the issues of

reduced tax based revenue sources and the resultant increased competition for scarce dollars

have directed efforts toward alternative funding sources” (p. 6). Cotter focused his study on

what he termed the best-run fire departments and found that “83.3% of those departments used

alternative funding sources” (p. 6). It was interesting that the majority of the departments that

were considered best run were using alternatives to obtain the necessary funding.

The impact of the current I-747 would be dramatic to the Federal Way Fire Department.

According to an educational document prepared for the voters, the district states, “If

I-747 passes and Proposition 1 does not, the Fire Department’s tax revenue in 2002 will be up to

$500,000 less that we have been anticipating” (Fire District Letter to the Taxpayers, July 19,

2001). With an annual budget expected to be approximately $10,000,000 in 2002, it would be a

reduction of approximately 4.2% of the total fire district budget in the first year. Considering

that a large percentage of a fire districts budget is consumed by payroll it is understandable that

reductions to services or personnel would be necessary to account for the drop in funding.

The trend of tax revolts on the West Coast appears to be very strong. Randy Bruegman

(1998) writes, “I believe this latest tax reform movement in Oregon is a reflection of what will

occur across the United States in the next decade” (p. 28). Bruegman goes on to say “for many

department’s, it’s resulted in employee layoffs, station closings and company reductions. We’ve

had to reprioritize the services that we provide and in many cases, how if we will provide them”

(p. 28). It appears that the trend for tax limitation measures is real and will force districts to

either reduce services or look for additional funding sources.

11

Much of the current research in fire district funding advocates a creative approach,

evaluating sources not traditionally used by the fire service. “Innovative revenue sources must

be a priority for departments as we move toward the 21st century. The days of old when we had

a spending plan and no thought to revenue are over” (Davis and Macpherson, 1993, p.34). One

of the new approaches used by fire department’s is to adopt a user fee. “Just what does the term

user fee denote? Simply put, it is when goods and/or services are provided by government at a

charge to an individual user” (Nielsen, 1988, p. 49). According to Nielsen “the most prevalent

user fees within the fire service is the charge for ambulance usage”(p. 50). Nielsen described a

study conducted by the International City Management Association, “it was found that of

approximately 18,000 municipalities involved, approximately 17% of all fees come from user

fees. This group derives approximately 23% of all its revenue from user fees” (p. 49).

Another option found in the literature review is the fire suppression benefit assessment.

“This is a charge for service in a direct relationship to received benefits for that service. It is

legally not defined as a tax, it would be stabilizing and it does not require voter approval”

(Stouffer, 1993, p. 38). While this option can provide a substantial amount of alternate funding it

appears that it is not widely used or well known.

One of the most comprehensive documents on fire department funding is the booklet

produced by the United States Fire Administration (USFA) titled Funding Alternatives for Fire

and Emergency Services. This booklet states that, “funding alternatives range from small fees

for special services to major new sources of funds such as benefit assessments, which pay for as

much as 40 percent of the budget for some departments” (1999, p.1-1). The implications of

funding choices are great, an agency must carefully consider the political ramifications of those

choices. The USFA (1999) continues to drive this point home by stating, “The funding issue is

12

not one to be left solely to accountants and finance officers; it is a vital public policy issue that

can literally mean life or death in the community” (p. 1-2).

The USFA (1999) document describes two funding sources that are being utilized by

some departments in Washington State, benefit assessment charges and fees. A benefit

assessment charge is described as being,

Administered somewhat like property taxes, these charges factor in not only size and type

of property but also benefits from being close to fire stations, having reduced insurance,

having special services available, etc. These charges are a way to get around property

taxes and also can improve the equity of charges for fire protection (p. 1-3).

The USFA (1999) goes on to describe the fees in a wide range of concepts from fees for

our primary duties to the added on services such as service calls and special operations teams. It

does raise an issue that is not used by many fire districts in Washington, “Perhaps the most

lucrative new category of fees are those for emergency medical services transport and emergency

medical care” (p.1-3).

The literature review has revealed that there are many creative methods to obtain the

needed revenue, and that districts are not limited to simply using property taxes as the sole

source of income. The review to this point is general in nature and does not focus on the laws

and options in Washington State.

As the literature review focused more closely on Washington State the research revealed

many options for fire district funding. A very succinct list of the available options was found in

a memo from Roger Ferris (Executive Secretary of the Washington Fire Commissioners

Association) to Federal Way Fire Commissioner Jim Osborne. Ferris describes the options that

are available to fire districts. The memo is included as Appendix A and includes the sections of

13

the state law in which the complete text may be found. Ferris lists property taxes (with several

options) benefit charges and EMS charge for services. Other options listed in the Ferris memo

include a one-year excess levy and voter approved bonds. The EMS charge for service normally

includes payment for patient transport (R. Ferris, personal communication, July 27, 2001). The

next step in the literature review is to focus on the state laws that govern the fire district funding.

Once these options were identified, the research focused directly on the Washington State laws.

A review of the state laws titled Revised Code of Washington (RCW) verified the options

listed above and provided the details or legal requirements available for each option.

The regular property tax allows fire districts to tax up to one dollar per thousand dollars of

assessed valuation for each property within its district.

“To carry out the purpose for which fire protection districts are created, the Board of

Commissioners of a district may levy each year… an ad valorum tax on all taxable

property located in the district not to exceed fifty cents per thousand dollars of assessed

value: PROVIDED, that in no case may the total general levy for all purposes, except for

the levy for the retirement of general obligation bonds, exceed one dollar per thousand

dollars of assessed value. Levies in excess of one dollar per thousand dollars of assessed

value or in excess of the aggregate dollar rate limitations or both may be made for any

district purpose when so authorized at a special election under RCW 84.52.052” (Revised

Code of Washington, RCW 52.16.130, 1989; pg. 1).

The section above allows fire districts to collect up to one dollar per thousand dollars of

assessed valuation. In other words the owner of a house valued at $100,000.00 would pay

$100.00 annually in property taxes to the local fire district.

14

A further study of the RCW’s reveals additional money is available if other taxing

districts are not collecting their full amount. In this case districts commissioners may levy “an ad

valorem tax on all property located in the district of not to exceed fifty cents per thousand dollars

of assessed value and which will not cause the combined levies to exceed the constitutional or

statutory limitations” (RCW 52.16.140, 1984; pg. 1). When the two combined property tax

options are utilized it allows fire districts to collect up to $1.50 per thousand dollars of assessed

valuation on all properties within the district.

Another option found in the RCW’s is the Emergency Medical Care and Service levy.

“A taxing district may impose additional regular property tax levies in an amount equal to fifty

cents or less per thousand dollars of the assessed value of property in the taxing district” (RCW

84.52.069, 1999; pg. 1). The taxes for the EMS levy can be collected over six years, ten years or

on a permanent basis. There are some restrictions to the EMS levy however, “any tax imposed

under this section shall be used only for the provision of emergency medical care or emergency

medical services” (RCW 84.52.069, 1999; pg. 2). The law further requires that “if a county

levies a tax under this section, no taxing district within the county may levy a tax under this

section” (RCW 84.52.069, 1999; pg. 2). Thus if no other agency is collecting an EMS levy a fire

district may collect up to fifty cents per thousand dollars of assessed valuation.

The state laws do recognize that there are needs that may require collection of additional

taxes above the normal amounts. The law states that the limitations “shall not prevent the levy of

additional taxes by any taxing district except school districts in which a larger levy is necessary

in order to prevent the impairment of the obligation of contracts” (RCW 84.52.052, 1996; pg. 1).

This additional tax is commonly referred to as an excess levy and must be approved by the voters

of a district choosing this option on an annual basis.

15

Another option for fire districts are general obligation bonds. A limitation with these

bonds is that they must be used “for capital purposes” (RCW 52.16.080, 1984; pg.1). These

bonds must be voter approved and may not exceed a twenty-year term of payment. In essence

this is a loan taken out by the fire district with an extra amount collected from the taxpayer to

pay off the debt over a specified time period. There is also an option for the commissioners to

contract indebtedness for any purpose via bonds but the amount is lower than for the voter

approved bonds. These non-voter-approved bonds must be repaid from within the districts

operating budget.

The RCW’s allow another option that isn’t widely used but does have benefits to the fire

districts that adopt it. This code allows fire commissioners to,

Impose a benefit charge on personal property and improvements to real property which

are located within the fire protection district on the date specified and which have or will

receive the benefits provided by the fire protection district, to be paid by the owners of

the properties (RCW 52.18.10, 1998; pg. 1)

There are limitations of how much a district can charge via the service benefit charge

(SBC) however, “The aggregate amount of such benefit charges in any one year shall not exceed

an amount equal to sixty percent of the operating budget for the year in which the benefit charge

is to be collected” (RCW 52.18.10, 1998; pg.1). The benefit charge must be reasonably

proportioned to the measurable benefits to property resulting from the services afforded by the

district” (RCW 52.18.10, 1998; pg.1). In other words those properties that receive a greater

benefit from the fire district pay a larger amount to the fire district. The factors included in

measuring the benefits “may include but is not limited to the distance from regularly maintained

fire protection equipment, the level of fire protection services provided to the properties, or the

16

need of the properties for specialized services, may be specified in the resolution and shall be

subject to contest on the ground of unreasonable or capricious action” (RCW 52.18.10, 1998;

pg. 1). The RCW allows fire districts to collect up to 60% of their operating budget from service

benefit charges, and select parameters that encourage fire safety in order to keep taxes low.

Another option listed in the Ferris memo is an EMS charge for services. An evaluation

of the RCW finds that “Any fire protection district which provides emergency medical services,

may by resolution establish and collect reasonable charges for those services in order to

reimburse the district for its costs of providing emergency medical services” (RCW 52.12.131,

1984; pg. 1). This allows districts to establish fees for transports, supporting the budget with

substantial funding that is not affected by a voter initiatives.

PROCEDURES

Definition of Terms

Ad Valorem Tax- As used in the Revised Code of Washington, an Ad Valorem tax is a property

tax based on the value of that property. The value of the property in question is the value as

determined by the county assessor.

Fire District /Fire Department- For this research a fire district in Washington State is a

separate special purpose district. It has it’s own elected officials for budgetary and policy

oversight. A fire department is normally a city department under the direction of the city’s

elected officials. The function from an operational sense is the same, however funding

mechanisms are different.

RCW- The Revised Code of Washington (RCW) is the compilation of all permanent laws now

in force. It is a collection of session laws (enacted by the Legislature and signed by the

Governor, or enacted via the initiative process), arranged by topic, with amendments added and

17

repealed laws removed. The RCW is published by the Statute Law Committee and is the official

version of the code.

Research Methodology

Evaluative research methods were used to determine what options are currently in use by

other fire districts. The evaluative investigation included; other fire district funding plans, state

laws, and other documentation of the options available. Also included is a review of the Federal

Way Fire Department’s BLS Transport Task Force Summary that was completed in January

2001. It is intended that this research will be used by the Federal Way Fire Departments Board

of Commissioners to update the strategic plan in the first quarter of 2002.

Literature Review

The literature review began at the National Fire Academy’s Learning Research Center

(LRC) with an appraisal of applied research papers, trade journals, and student manuals. The

focus of the LRC research included searches for creative funding methods, alternative funding

sources and other information related to fire district funding. The review also includes a

systematic research of current Washington State laws. Local memos, reports and plans are also

reviewed. The literature review identified not only the anticipated options but also SBC that is

not as well known or utilized.

Survey Instrument

The research continued with an effort to determine how effective other funding options

were. The focus of this effort was the service benefit charge. This focus was selected because

many fire district administrators may not be fully aware of the details pertaining to the SBC.

While the benefit charge is authorized by the RCW’s, very few districts are currently using it as a

funding option. A survey instrument was created to determine the effectiveness of the service

18

benefit charge. The survey is included as Appendix B. This stage of the research was designed

to learn more about the practical aspects of the SBC. It examined how much time it takes, and

what percentage of the total budgets is derived from the SBC etc. It also asked about the benefits

and negatives of using the service benefit charge. The survey focused on the different formulas

that are utilized in an effort to identify potential starting points for districts that are considering

adopting the service benefit charge.

For this research the survey was sent out to nine fire districts that were identified as using

the SBC. These districts were identified by a private corporation that contracts with fire districts

to collect and maintain the service benefit charge.

A total of six districts returned the survey. Districts that participated in the survey

included King County Fire Districts 16, 36, 40; Mason County Fire Districts 2, 5; and Clark

County Fire District 6. The data was analyzed to identify how effective the SBC was. The

completed surveys were compiled into a survey summary and are included as Appendix C. The

summary reflects the handwritten or typed responses including, punctuation, grammar, and style

as accurately as possible.

Assumptions and Limitations

The SBC survey was sent out to nine fire districts in the state. While this isn’t a large

number to survey, there are very few fire districts in the state currently using service benefit

charges. This group was considered an adequate representative group to survey. The goal was

simply to identify the pros and cons of using the SBC. For this research the limited number of

respondents provided ample information to evaluate the benefits of adopting SBC as a funding

option.

19

Another limitation is that the research focused on funding options alone. It did not

attempt to measure or evaluate the political factors that may impact a fire commissioners’

decision on selecting funding options that are effective for funding a fire district. Before any

decision is made based on this research, a full evaluation of the political consequences must be

conducted.

An assumption of the research was that funding options were considered to be long-term

sources if they could be utilized over several years for programs and/or personnel; not simply

funding for one-time purchases such as a new fire station or apparatus.

RESULTS

Answers to Research Questions

1. What other fees, levies, or charges are available to supplement property taxes? In

addition to the regular property taxes, fire districts may collect money in the form of an:

• EMS levy

• Excess levy.

• Bonds may be issued by authority of either voters or the Board of Fire Commissioners.

(Bond funds must be used for capital purchases only.)

• Service benefit charge

• EMS fees for service; such as fees for transporting patients to the hospital.

2. What are the advantages/disadvantages and unintended consequences of each option?

The EMS levy is an option that can be approved by the voters for a six-year, ten-year or

permanent basis. An advantage of the EMS levy is that it can be a long-term levy that gets

20

approved once and remains in effect. It can fund either a regional system where the county

collects the money, shares the roles and money with the local fire departments, or it can be

targeted by individual fire districts.

Unfortunately for fire districts, the county has the first right to the EMS levy. If the

county doesn’t charge for an EMS levy or remains below the levy cap (fifty cents per

thousand dollars of assessed valuation) a district may choose to collect their own EMS levy.

A disadvantage to this system is that it is an additional tax for what many voters consider a

basic service, and feel it should be part of the general property taxes. Another disadvantage

is that the local providers are often at the mercy of a county administration that may choose

to collect an EMS levy and not share control with the local providers.

An excess levy may be used when the property taxes aren’t enough to fund the staff,

facilities, and equipment that the community feels are needed for a fire and life safety. If

property values aren’t sufficient to fund the fire district, the board may ask voters to exceed

the normal limits imposed by state law. The amount collected by an excess levy is set by the

board of commissioners and approved or rejected by the voters of the district. In most cases

the excess levy is authorized for one-year and requires an annual vote to maintain the levy.

The excess levy provides many options for fire districts without a strong tax base. The

biggest disadvantage is that this is an annual campaign that can be rejected by the voters.

While there is much flexibility with an excess levy it is not very predictable and is at the

desire of the voters. Perhaps an unintended consequence is that much time is spent educating

voters annually.

Voter approved bonds can only be used for capital purchases. The voters in essence

agree to raise their taxes to pay off the bonds. The advantages are that the use of bonds and

21

the message are very clear. Typically a fire district places a specific request on the ballot.

The ballot would ask for a specific amount of money for specific items. By passing a bond

issue, it frees up money that would otherwise have to be spent on purchasing equipment from

the general fund. The disadvantage is that it is usually a one-time purchase and can’t be used

for personnel. It can also be argued that it is a tax increase.

Commissioner approved bonds have additional limitations not used on voter approved

bonds. Non-voter approved bonds must be paid back from the general budget. In other

words, a district may take out a loan, which it must pay back from the existing property taxes

rather than collect additional money to pay off the bonds. An advantage is the district

doesn’t have to go to a public vote, and the district can react to an emergency faster than

waiting for the next election. The disadvantages are the money to repay the bonds comes

from the general budget and the amount a district can obtain is lower than voter approved

bonds.

Benefit charges have the ability to add significant money to the budget. The SBC

may provide up to 60% of a fire districts total budget, and it can be in effect for a six-year

period. A disadvantage of the benefit charge is that it isn’t well known by the taxpayers,

much education is required if a district chooses to use this funding option. The politics

required to implement and maintain the SBC must be considered as it may appear as an

additional tax to many taxpayers. Many districts have used this to maintain a stable source of

funding and haven’t used it to increase taxes above the rate that would have been charged

with property taxes alone.

Many fire districts are using the EMS charge for services in the form of transport

fees. The advantage of the transport fee is it charges the user for the service provided. It will

22

normally be very stable since the number of alarms in most districts is either very stable, or

in fact increasing. It is routinely being charged by private ambulance companies. If a fire

district chooses this mechanism of funding, it can be argued that the taxpayer was going to

receive a bill anyway, why not pay the public provider? The disadvantage is the additional

workload placed on the fire districts personnel and equipment. Another drawback is the

decreased public relations that may occur when the taxpayer receives an additional bill from

the fire department for a patient transport.

3. Which option or options provide the most consistent funding that will allow fire

districts to maintain their current level of service.

While property taxes are intended to provide consistent funding, they are under attack

from many sources. New limits are frequently debated and even placed on the ballot. It is this

history of limitation efforts that are causing possible budget cutbacks and concern for the long-

term ability of fire districts to plan for growth in the community. The combination of EMS

transport fees and service benefit charges appear to offer the best long-term stable funding

option. The service benefit charges may fund up to 60% of the district’s budget and those dollars

are more resistant to unanticipated limitations. Once the voters approve the service benefit

charges, they remain in place for an extended period of time. The EMS transport fees can be

based off actual costs to the district and have adjustments for inflation built into the system. The

money from transports is not likely to change significantly in the future as most of the area

departments have a history of slow increases in their alarm load. The money stream from

transports will be very predictable and will match alarm trends.

23

Survey Results

A survey was conducted to learn more about the successes and challenges of actually

implementing the service benefit charge. Fire Districts that were identified as having experience

with the state authorized service benefit charge were included in the survey. A complete

summary of the survey is included as Appendix D.

As the research focused on the survey for service benefit charge, it became apparent that

the number of districts using this option was limited to a small group and that there was no way

to identify all of those districts. Both the Washington State Association of Fire Chiefs and

Washington Fire Commissioners Association were asked for information on how many districts

may be using SBC, but neither had any data.

By utilizing some of the consultant firms associated with the SBC, 12 fire districts in

Washington State were identified as having experience with the service benefit charge. The

number of districts was reduced to nine as the research revealed some districts had merged

together. Of the nine that remained in the survey group, six districts chose to participate in the

survey. It is possible that more districts are using the service benefit option, however it is thought

to be a very limited number. This survey group is considered an adequate representation, as it is

approximately 66% of the districts that were identified as using this method for funding.

Of the districts in the survey group 50% are still using the SBC. The research shows a

strong polarity of experience. Those still using the SBC were very supportive of the funding

method and those that switched back to property taxes tended to view it in a much less favorable

light. The three districts still using the SBC felt that the current tax limitation initiative will not

impact the money gained via the SBC. They also felt that it was more stable and predictable

than relying on property taxes alone.

24

It was also revealed that no districts in the survey group had implemented this option in

recent years. The first district that identified using the SBC switched in 1988. The last to adopt

the SBC was in 1992.

The reasons listed for implementing the SBC were varied as well. Many respondents

listed threats to their funding from other taxing districts such as the hospitals or other public

works. In Washington there is competition for tax dollars by taxing districts. If a hospital

chooses to increase their tax rate, it can affect local fire district negatively. This concern was

listed by several of the survey respondents.

One of the items that was revealed in the research is that any attempt at using the SBC

will require a sustained educational effort. A district with a positive experience related that they

had an intensive internal education program so all employees understood the system. They then

provided presentations to area homeowner groups, and sent out newsletters with information for

the taxpayers. The district also included an independent political action committee to support the

political side. All survey respondents noted that they had to provide additional information for

their voters.

A full 50% of the survey respondents had experienced a rejection by the voters. Two of

the districts overcame that rejection at the next election. The failures appeared to be a result of

low voter turn out and the lack of a strong educational message. Two of the failures occurred in

the spring with less than the required 60% of the voters from the last general election voting on

the SBC issue. Both of these measures passed when resubmitted in the fall.

It was surprising in light of the 50% of the districts that experienced a failure at the ballot

box, only two of the six districts (33%) described any organized opposition to implementation of

the SBC. One district related that during a reauthorization effort in 2001 an organized group

25

went so far as to send out informational mailings and letters to the editors of the local

newspapers. Despite this effort the SBC passed at a rate of 75%.

The percentage of the district budget supported by the SBC was also varied, it ranged

from 33% to 46%. One of the districts no longer using the SBC had much as 50% of their

annual budget coming from the SBC prior to switching back to solely using property taxes.

All of the districts surveyed reported some funding in addition to property taxes. All but

one district uses the EMS levy as a funding source. One of the districts also collects money from

patient transport fees. Another district collects money via a fire prevention contract with a city

within their jurisdiction.

All of the districts surveyed hired a consultant to update and/or review the records rather

than assign that duty to fire district personnel. The amount of time fire district personnel are

involved in this process is limited to one or two meetings a year with the consultant to review

summary data. Most districts described some time spent on appeals by property owners. Most

of the appeals occurred in the early years after the SBC was implemented, however the number

of appeals declined as taxpayers became used to the system. The range of time described on the

completed survey returns was from one to two hours, up to several weeks experienced by one of

the districts no longer using SBC.

Since all of the districts utilized a consultant to administer the program, it is also

important to consider the cost for that consultant service. The consultant fees ranged from a low

of $13,012.00 to the highest at $34,125.00 per year.

The formulas used for implementing the SBC varied from district to district. Most were a

variation of utilizing distance to the nearest fire station, insurance benefit, and the required fire

flow. It became apparent during this phase of the research that this is one area that must be very

26

clear to the taxpayer. If the method for determining the rate is not clear it will likely meet with

opposition.

The research found that over 66% of the districts would implement the SBC again

knowing what they do now, if they could go back in time. One of the districts that is not

currently using the SBC stated that they had to implement it, but would not have attempted to

renew once they got out of their budget crisis. At this point in the survey one district stated that

they passed their last authorization attempt with an 88% vote in 2000.

When asked about the pros and cons of using the SBC, it rapidly become apparent that

the SBC does in fact provide a more stable, predictable, and more flexible source of funding.

One unanticipated benefit is that it allows a fire district to credit fire safety by allowing

reductions for monitored sprinkler systems. Some of the responses described it as

recession/initiative proof. It was also described as securing one third of the funding for the

budget. Other comments state that districts are able to collect additional revenue if approved by

the Board of Commissioners. The negatives are primarily associated with the confusing nature

of the benefit charge. Several comments on the survey described how their community struggled

to understand the rates, formulas, and the perception that the fire district can raise taxes without a

vote of the public. The descriptions go on to highlight that if the voters don’t understand an

issue, they tend to vote against it.

DISCUSSION

Many districts are facing a challenge that affects the ability to perform their missions.

The challenge is an increasing budget crisis, with not enough money to get all of our jobs done.

“Budget pressures have forced local governments across the country to seriously consider

27

reducing services, increasing efficiency, or finding new funding sources” (USFA, 1999, p. 1-7).

As a result of these pressures fire service administrators are forced to look for alternatives.

“Providers of fire protection and emergency medical service should consider the wide variety of

ways available to fund services and perhaps to improve the equity of paying for the service”

(USFA, 1999, p.1-5, 1-6). Fire districts in Washington State are facing a tax limitation initiative

that will force them to either reduce spending or increase revenue through sources other than

property taxes. This research simply focuses on the funding option and does not address the

option of reducing services.

Adopting alternative funding is a major decision for any fire district. The political

implications are almost as significant as the financial ones. Districts must evaluate not only their

financial needs but also consider the public relations issues and unintended consequences with

the public to ensure long term support of the fire district. “Prior to implementation of any

alternative funding program, the ramifications of initiating the funding source should be fully

explored to avoid any unintended, negative reaction” (Cotter, 1994, p.15). Cotter describes the

reasons for the increase in the use of alternative funding, “clearly the issues of reduced tax based

revenue sources and the resultant increased competition for scarce dollars have directed efforts

toward alternative funding sources” (1994, p.5).

“Taxes pay for the fire department to be available, to be ready like an insurance policy”

(Davis and MacPherson, 1993, p.34). In order for that insurance to be ready it must be

adequately funded from one year to the next. There are several options available that may be

legal but don’t meet the need for consistent and reliable funding. When discussing consistent

and reliable funding, the main goal is that the funding is predictable from one year to the next.

For long range or strategic planing it is important that revenue streams are reliable and the entire

28

plan isn’t postponed because of an unforeseen budget crisis. It is also desirable from a long term

planning standpoint that the revenue stream isn’t in danger of major cutbacks from one year to

the next. Most agencies would prefer to have revenue keep pace with inflation in order to keep

pace with the wages, benefits and supplies that a fire district must finance.

The excess levy is ruled out as an option because it must be voted on each year. Excess

levies force fire districts to commit considerable resources each year to running an educational

campaign so the voters are aware of the issue on the ballot. It is also a concern that the voters

must approve it on an annual basis. If a current event or some outside influence causes the

voters to reject the levy at the election, it removes a sizable part of the budget. In this case a

district must either resubmit the levy for a voter consideration, or reduce spending.

Bonds are also an option as alternative funding. “Fire protection districts additionally are

authorized to incur general indebtedness for capital purposes” (RCW 52.16.080, 1984, p.1).

Voter approved “bonds are essentially loans in which the principal is not paid until the end of a

period, typically 5-20 years. Interest is paid along the way” (USFA, 1999, 2-9). Bonds normally

provide funding for specific items such as apparatus, stations, or equipment. It is important to

keep in mind however that the bonds are passed for specific purchases, once the items are

purchased, the money is gone. Money from bonds does not provide a long-term source of

revenue that can be used for personnel or general operations. In Federal Way the Board of

Commissioners has decided to invest money each year into a capital replacement fund to reduce

the need for bonds. For the purposes of this research, bonds are not considered a viable option as

an alternative-funding source because they are short-term funds for specific items.

Benefit charges are a viable option for consistent funding for fire districts. They are

voted on for six-year periods making them more of a long-term solution. They are resistant to

29

the property tax backlash, as they are specifically voted on by the taxpayers and thus exempt

from the tax limitation efforts. They do however pose a challenge to educate the voters about the

specific details the first time they are imposed. An advantage of the benefit charge is that a

district can use it to encourage fire prevention efforts of the property owners. One district allows

a 50% reduction in the service benefit charge for monitored sprinkler systems.

Service fees for patient transports are another viable form of funding for fire districts.

Federal Way closely examined this option in January 2001. A comprehensive report delivered to

the fire district administrator on January 4, 2001 identified several recommendations.

A review of the summary reveals that there were “3,141 BLS transports by ambulance

companies in 1999” (BLS Task Force Summary, January 4, 2001). From the total of all of the

BLS transports; “2,419 BLS patients were transported by ambulance companies to St. Francis

hospital” (BLS Task Force Summary, January 4, 2001). St Francis is the local hospital and is

located within the fire district boundaries. The report goes on to describe the money that could

be earned for conducting those transports with fire district personnel for a fee. “Based on a

transport fee of $400, as utilized by several neighboring Pierce County Departments; a collection

rate of 60%; and an average of 2,500 BLS transports to St. Francis Hospital; the Federal Way

Fire Department would earn $600,000 for providing all transports to St. Francis” (BLS Task

Force Summary, January 4, 2001). One of the benefits of transport fees as an option is the trend

for increasing numbers of EMS responses. According to the Federal Way Fire Department’s

2000 Annual Report, EMS alarms increased “4.7% from 1999” (2001). This upward trend will

continue to provide stable and perhaps an increase of money each year as the number of patient

transports is directly related to the number of EMS alarms.

30

By charging a fee for patient transport the district could increase its revenue by an

additional 6%. This is money that taxpayers are already paying to ambulance companies and

therefore would not likely be opposed to the fire district implementing the patient transport fee.

The money would also be very stable, as the alarm load experienced over the last several years

has been slowly increasing.

RECOMMENDATIONS

The research has revealed two significant sources for alternative funding for fire districts

in Washington State; service benefit charges and patient transport fees. Transport fees are not

required to have voter approval, thus they may be implemented at any time and at a reasonable

rate as determined by the fire district. The transport fees are not susceptible to the current trend

of tax limitation and they charge only those that are actually using the service. Service benefit

charges are also a viable option, as they are valid for six-year periods and offer flexibility. They

can simply replace up to 60% of the district budget, or they can provide additional money over

the existing rate by going above what would be available with property taxes.

It is recommended that the Federal Way Fire Department fully implement the

recommendations of the BLS Task Force and commence BLS transports with the fee structure as

denoted in the summary. This will amount to a 6% increase, or an additional $600,000.00 in

revenue for the districts operational budget.

It is further recommended that the district evaluate the political impacts of implementing

the service benefit charge. If adopted, the SBC will reduce the threat from tax limitations by

protecting up to 60% of the districts funding. If the remaining 40% of revenue is attacked it will

be less of an impact to the operations of the district. The district has several options to consider

31

with regards to the SBC. The district can either replace part of the property tax or it could use

the SBC to bring additional money into the districts revenue stream.

This research was only intended to identify funding sources, not judge the political

impacts or the viability at the ballot box. Both the fee for transport and the SBC are viable

options for a more stable and consistent funding source. The decision at this point is whether the

Board of Commissioners feels the stability of SBC is worth the challenges of the educational

campaign.

32

REFERENCES

Bruegman, R. (January 1998). Tax revolt: A trend of the future. Fire Chief.

Pg. 26-29.

Cotter, C. (July 1994). The use of alternative funding sources, experiences of some of

America’s best run fire departments. (Applied Research Project). Emmitsburg, MD:

National Fire Academy, Executive Fire Officer Program. P. 5, 6, 15.

Davis, P., Macpherson, G. (January 1993). What you and your dentist have in common.

Fire Chief. p. 34, 35.

Federal Way Fire Department, (April 12, 2001), 2000 Annual Report, The Year in

Review, WA, Author, Pg. 5.

Federal Way Fire Department (January 4, 2001), BLS Transport Task Force Summary,

WA, Author, pg. 5,6.

Federal Way Fire Department Letter to the Taxpayers (July 19, 2001), Questions and

Answers about Federal Way Fire Department Proposition 1, pg. 1,2.

Nielsen, R.D. (January 1988). When budgets are cut, user fees can help. Fire Chief,

p. 49, 50.

Revised Code of Washington 52.12.131, Emergency Medical Services-Establishment and

Collection of Charges, (1984) pg. 1.

Revised Code of Washington 52.16.080 Bonds May be Issued for Capital Purposes-

Excess Property Tax Levies, (1984) pg. 1.

Revised Code of Washington 52.16.130 General Levy Authorized-Limit-Excess Levy at

Special Election, (1989) pg.1.

33

Revised Code of Washington 52.16.140 General Levy May Exceed Limit-When, (1984)

pg. 1.

Revised Code of Washington 52.18.10 Benefit Charges Authorized-Exception-Amount-

Limitations, (1998) pg. 1.

Revised Code of Washington 84.52.052 Excess Levies Authorized-When Procedure,

(1996) pg. 1.

Revised Code of Washington 84.52.069Emergency Medical Care and Service Levies,

(1999) pg. 1,2.

Stouffer, D. J. (January 1993), Budget Crisis in LA County. Fire Chief, Pg. 36-38.

United States Fire Administration. (December 1999). Funding Alternatives for fire and

emergency services. Emmitsburg, MA: Author. P. 1-1--1-7, 2-9.

34

Appendix A WASHINGTON FIRE COMMISSIONERS ASSOCIATION

July 27, 2001

TO: Jim Osborne, Commissioner King County FPD 39

FROM: Roger Ferris, Executive Secretary

RE: Fire District Funding Sources The following are fire district funding sources and appropriate RCW references. 1. Property Tax (RCW 84 Title) • Regular tax -RCW 52.16.160 • Emergency Medical Services 6-year, 10-year, permanent-RCW 84.52.069 • Excess Levy 1-year -RCW 84.52 • Voter approved bonds-RCW 52.16.080; non voter-

approved-RCW 52.16.061 2. Benefit Charges • Voter approval -RCW 52.18.050 3. EMS charge for services -RCW 52.12.131

*Collection for transport and reimbursement authorized. Please contact me if you have any questions. RF/ nr

LOCATION: Olympia Forum Bldg., 60511th Ave. S.E., Suite 205, Olympia, WA 98501 MAILING ADDRESS: P. O. Box 134, Olympia, WA 98507-0134 PHONE: (360) 943-38801-800-491-WFCA (9322) SCAN: 234-1552 FAX: (360) 664-0415

35

Appendix B SURVEY LETTER

September 5, 2001 INSERT CHIEF NAME Dear Chief INSERT NAME HERE, The Federal Way Fire Department is investigating a change in our fire department funding due to the increasing number of voter initiatives to reduce property taxes. Please assist us by completing this survey and returning it to me via fax or mail by September 28th. The continued efforts to reduce property taxes are very concerning to all of us in the public sector. We are looking for options that will ensure our funding is stable and not require annual voter campaigns for normal operating budget needs. The Federal Way Fire Department is considering all options that will make our budgeting less impacted by these limitation efforts. Your experience with the Service benefit Charge is important to us and we appreciate you taking the time to fill out the attached survey form. As a student in the National Fire Academy’s Executive Fire Officer Program, I am conducting this research as part of an applied research paper. The research paper is titled “Funding Options for Fire Districts in Washington State. My research includes identifying the state laws and the implications of new funding options. By completing this research I will also make recommendations to our Board of Commissioners as part of our strategic planning process. Your assistance will not only help the fire department but also help me as a student at the academy. Please fax the enclosed survey to: Or mail to B/C Jerry Thorson B/C Jerry Thorson (253) 529-7206 31617 1st Ave So. Federal Way, WA. 98003 Thank you for your assistance if you have any questions please feel free to call me at (253) 946-7240. Sincerely, Jerry E Thorson Fire Marshal

36

Appendix C

Service Benefit Charge Survey

Please answer the following questions to the best of your ability. The answers will be used to evaluate this option for the Federal Way Fire Department and in a National Fire Academy Applied Research Paper.

1. Are you currently using the Service Benefit Charge (SBC) as part of your fire district

funding?

Circle one: YES NO 2. When did you first implement the Service Benefit Charge?___________________________ 3. What were the original determining factors that encouraged you to implement the SBC?

(Revenue? Community growth? Operational ability?) 4. How did you educate the staff/voters about the changing from property taxes to a new system

that included the Service Benefit Charge? 5. Did you have any organized opposition to the Benefit Charge? If yes, what strategy did you

use to overcome that opposition? 6. Have your voters ever rejected the Benefit Charge proposal at an election?

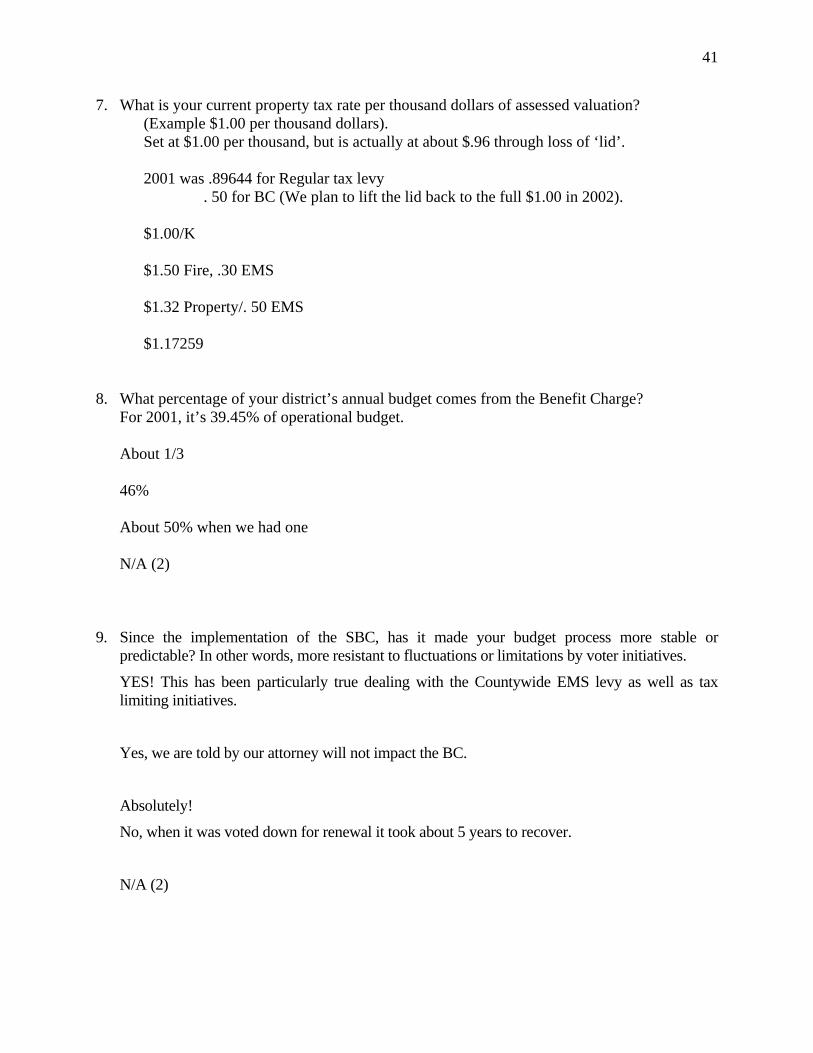

Circle one: YES NO 7. What is your current property tax rate per thousand dollars of assessed valuation?

(Example $1.00 per thousand dollars).

37

8. What percentage of your district’s annual budget comes from the Benefit Charge? 9. Since the implementation of the SBC, has it made your budget process more stable or

predictable? In other words, more resistant to fluctuations or limitations by voter initiatives.

10. Has the implementation of the SBC allowed you to hire more firefighters that you predicted

under property taxes alone? 11. Does your district currently utilize any other substantial funding such as an EMS Levy,

patient transport fees, etc? 12. If you use other levies or fees, please describe and include the approximate percentage of

your operational budget. 13. How much time does it take annually to update or review the records of the properties

included in the Service Benefit Charge?

38

14. How much time is spent reviewing appeals of the rates charged to property owners? 15. What percentage of the Service Benefit Charge collected district wide is needed for overhead

costs to maintain the program? 16. Describe or attach the formula used to calculate the Benefit Charge for each property. 17. If you could go back in time knowing what you know now, would you implement the Service

Benefit Charge again? If no, why not? 18. Briefly describe the pros and cons of using the Service Benefit Charge. 19. If you use a consultant to maintain your SBC, please list the company’s name. 20. If you would like to receive a summary of this survey when completed please list your

address or e-mail.

39

Appendix D Service Benefit Charge Survey Results Summary

Please answer the following questions to the best of your ability. The answers will be used to evaluate this option for the Federal Way Fire Department and in a National Fire Academy Applied Research Paper.

1. Are you currently using the Service Benefit Charge (SBC) as part of your fire district

funding?

Circle one: YES 3 NO 3 *We did from ‘92-95, went back to the $1.50 2. When did you first implement the Service Benefit Charge? ___________________________

1991 1988 1989 1992* 1990* • No longer using SBC • We tried a few years back when our property tax levy was being prorated.

*Switched back to property taxes 3. What were the original determining factors that encouraged you to implement the SBC?

(Revenue? Community growth? Operational ability?) Numerous, including threats of loss of funds from other junior taxing districts (i.e. hospitals, roads, etc). Ability to have a more ‘stable ‘ method of funding, and the ability to actually increase funding. The hospital district was considering increasing their tax authority that could have affected our 3rd 50 cents. The decision was made to go to the BC to maintain our third 50 cents now and in the future. Revenue, stability of funding All of the above (listed in survey) Revenue options, flexibility in FD establishing tax rate. Tax Proration

40

4. How did you educate the staff/voters about the changing from property taxes to a new system that included the Service Benefit Charge? First intensive internal education for all employees to understand. Second presentations to area homeowners associations. Third, district newsletter contained information. Additionally, an independent PAC was formed and supported on the political side. Informational meetings and flyers

Mailings Citizens groups, flyers, etc. Voter campaign, primary emphasis was on adding paramedics, the benefit was the means. We charted/graphed our declining tax levy

5. Did you have any organized opposition to the Benefit Charge? If yes, what strategy did you

use to overcome that opposition?

Yes, during a reauthorization vote in 2001. An organized group did a mailing and letters to the editor. As far as the district action, continued aggressive factual education through homeowners associations and district mailing. Note: even with organized opposition, ballot title passed at 75%. Yes, Education by speaking to public service groups. No opposition No (3)

6. Have your voters ever rejected the Benefit Charge proposal at an election?

Circle one: YES 3 NO 3 In spring of 1995, initial re-authorization vote failed. Was passed in the fall of 1995. May 1994 ballot failed at just less than 60% placed back on the ballot in Sept. and passed. We did a campaign in May, which proved to be a mistake. But they didn’t like it, it was confusing

41

7. What is your current property tax rate per thousand dollars of assessed valuation? (Example $1.00 per thousand dollars). Set at $1.00 per thousand, but is actually at about $.96 through loss of ‘lid’. 2001 was .89644 for Regular tax levy . 50 for BC (We plan to lift the lid back to the full $1.00 in 2002). $1.00/K $1.50 Fire, .30 EMS $1.32 Property/. 50 EMS $1.17259

8. What percentage of your district’s annual budget comes from the Benefit Charge?

For 2001, it’s 39.45% of operational budget. About 1/3 46% About 50% when we had one N/A (2)

9. Since the implementation of the SBC, has it made your budget process more stable or

predictable? In other words, more resistant to fluctuations or limitations by voter initiatives.

YES! This has been particularly true dealing with the Countywide EMS levy as well as tax limiting initiatives.

Yes, we are told by our attorney will not impact the BC.

Absolutely!

No, when it was voted down for renewal it took about 5 years to recover.

N/A (2)

42

10. Has the implementation of the SBC allowed you to hire more firefighters that you predicted

under property taxes alone? Yes, more than we would be able under the straight tax system for fire districts in the state. No, our board of commissioners has never collected more than the equivalent to 50 cents. No- it could if we wanted to raise the equivalent combination tax and benefit to above $1.50. No, it was a temporary budget boost. N/A (2)

11. Does your district currently utilize any other substantial funding such as an EMS Levy,

patient transport fees, etc? Yes, EMS levy as well as property taxes and benefit charge. Rough break down: Tax: 54% Misc.: 2% (school contracts, permits, etc) Benefit Charge: 39%

EMS: 5%

No we collect about $150,000-175,000 annually through our fire prevention contract with the city of Woodinville. Only the EMS levy Yes, EMS levy (2) Yes, EMS Levy $290,00 out of 2,450,000 and Patient Transport fees 363,000 out of 2,450,000.

12. If you use other levies or fees, please describe and include the approximate percentage of

your operational budget. See above (2)

N/A (2)

43

The benefit charge language (RCW) limits the other taxes you can charge. EMS levy 10%. Transport fees 15% 13. How much time does it take annually to update or review the records of the properties

included in the Service Benefit Charge? I’m not sure…we actually ‘out source this (and factor the amount of that into the benefit charge figure). Consultant handles this (2-3 hours with consultant reviewing the pervious year. We utilize a consultant who works with the county. This is the reason we discontinued We paid a consultant a fee. N/A

14. How much time is spent reviewing appeals of the rates charged to property owners?

During the first couple of years, quite a bit. The past two years we have only average about two (2) appeals, which take very little time. I believe that after 10 years, most citizens are aware. Approximately 40 hours We process fewer than 25 appeals per year. Very little time is required. Spent weeks of work One or two-two hour sessions. N/A

15. What percentage of the Service Benefit Charge collected district wide is needed for overhead

costs to maintain the program?

For 2001, it’s 2.3% (or $34,125 for a benefits Charge total of $1,422,604.00).

44

King County collected in 2001 $13,012 to collect BC for district Consultant cost in 2001 $14,375 Only other costs are staff time dealing with phone calls and appeals. Only the consultant fee and an annual mailing-less than ¾ of one percent. Consultant fees N/A (2)

16. Describe or attach the formula used to calculate the Benefit Charge for each property.

See attached (3) Not that easy- 1/3 to distance benefit 1/3 to insurance benefit 1/3 to fire flow benefit We used assessed value, distance to a fire station and water flow available. N/A

17. If you could go back in time knowing what you know now, would you implement the Service

Benefit Charge again? If no, why not?

YES (4) No (2) It was re-authorized by the voters of the district by 88% last year. No, The community didn’t understand the calculation and asked us to go back to the $1.50. Yes, we had to but we would not have tried to renew it.

18. Briefly describe the pros and cons of using the Service Benefit Charge.

Pro…stable, predictable, and more flexible. One of the BIGGEST pros is that it is a system that actually allows us to credit fire safety (we give 50% benefit charge reductions for monitored sprinkler systems!). It’s also locally set and controlled not done ‘downtown ‘ or downstate’.

45

Pro secures 1/3 of our funding, able to collect additional revenue if approved by the board. Recession/initiative proof The biggest con is that it is pretty (or can be) confusing. It is NOT value based, and everyone wants to know the $/1000 value (which can’t be done). The threat is that what people don’t understand, they tend to oppose. Collection is confusing to some taxpayers, some parts of BC collection are difficult to explain when asked questions The only “con” is the requirement to go back to the voters every six years. We have been able to stabilize funding, accomplish stability in our financial planning and all for less that we would have charge with the usual $1.50 limit.

The community didn’t understand the calculation and asked us to go back to the $1.50. Benefit complicated, not understood by voters, expensive to implement, voter anger, perception FD can raise tax without vote of the people. Taxpayers hated it. They did not understand it. They took it as a personal attack.

19. If you use a consultant to maintain your SBC, please list the company’s name.

Dakan & Associates (2) Interface Systems Management

20. If you would like to receive a summary of this survey when completed please list your

address or e-mail.

YES (3) No (1)