From the Retirement Plan Toolbox Selected Recent Developments and Planning Strategies Savings Simple...

41

From the Retirement From the Retirement Plan Toolbox Plan Toolbox Selected Recent Developments and Planning Strategies Savings Simple IRA Plan Design Recordkeepi ng Retiremen t 401K Cross Tested Employer Match Profit Sharing

-

Upload

gladys-pitts -

Category

Documents

-

view

217 -

download

0

Transcript of From the Retirement Plan Toolbox Selected Recent Developments and Planning Strategies Savings Simple...

From the Retirement From the Retirement Plan ToolboxPlan Toolbox

Selected Recent Developments and Planning Strategies

SavingsSavings

Simple IRA Plan Design

Recordkeeping RetirementRetirement401K

Cross TestedEmployer MatchProfit Sharing

I. Service Provider Fee I. Service Provider Fee Disclosure Regulations Under Disclosure Regulations Under

ERISA §408(b)(2)ERISA §408(b)(2)

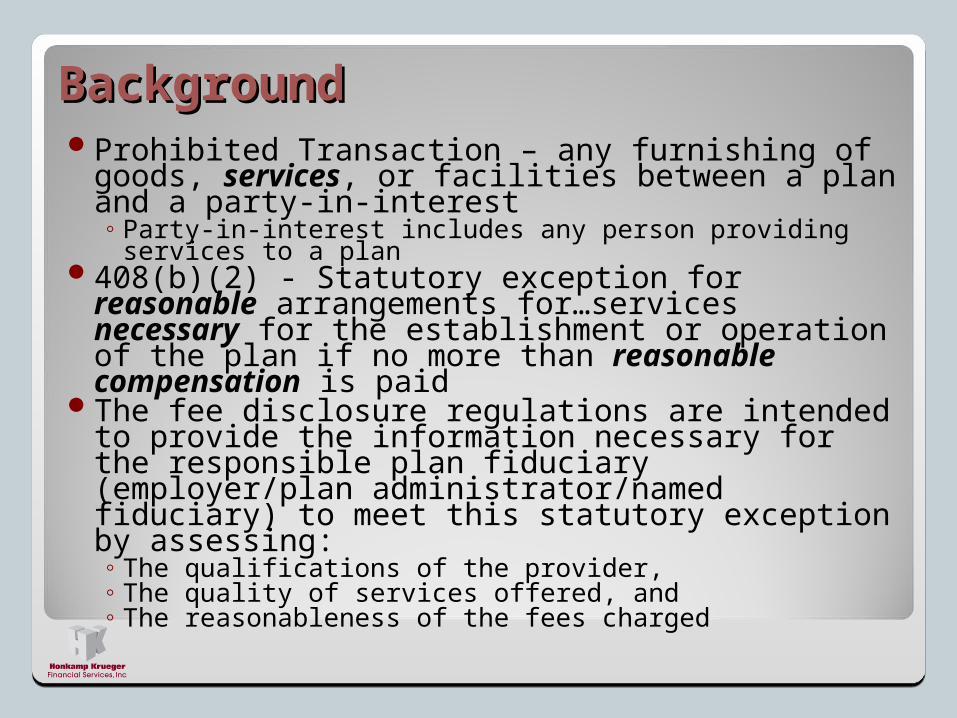

BackgroundBackgroundProhibited Transaction – any furnishing of goods,

services, or facilities between a plan and a party-in-interest◦ Party-in-interest includes any person providing services

to a plan408(b)(2) - Statutory exception for reasonable

arrangements for…services necessary for the establishment or operation of the plan if no more than reasonable compensation is paid

The fee disclosure regulations are intended to provide the information necessary for the responsible plan fiduciary (employer/plan administrator/named fiduciary) to meet this statutory exception by assessing:◦ The qualifications of the provider,◦ The quality of services offered, and◦ The reasonableness of the fees charged

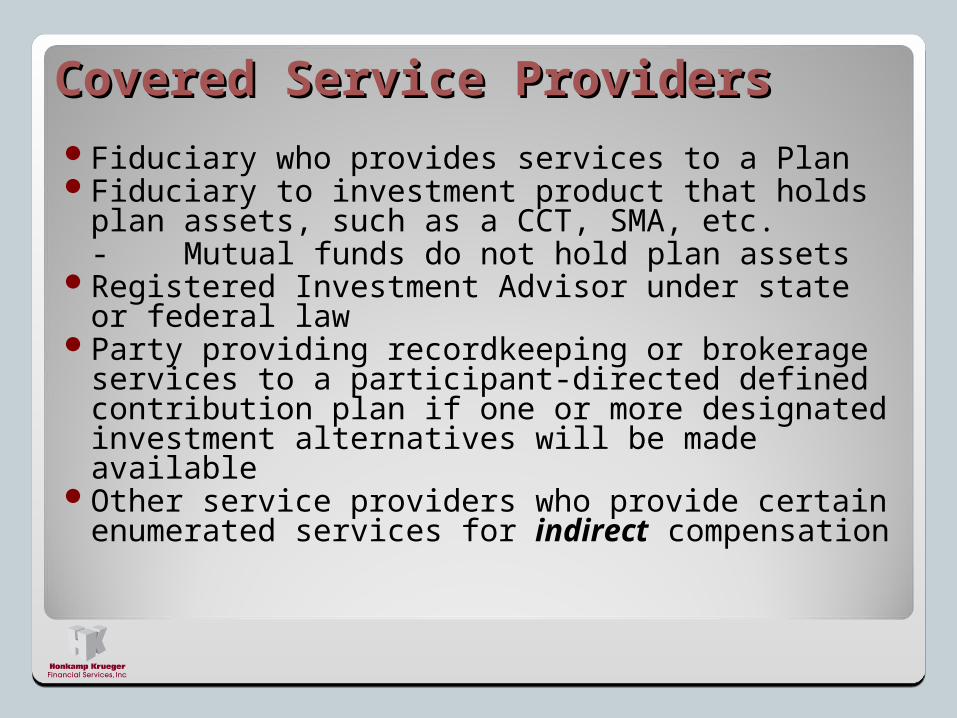

Covered Service Providers Covered Service Providers Fiduciary who provides services to a PlanFiduciary to investment product that holds plan

assets, such as a CCT, SMA, etc.- Mutual funds do not hold plan assets

Registered Investment Advisor under state or federal law

Party providing recordkeeping or brokerage services to a participant-directed defined contribution plan if one or more designated investment alternatives will be made available

Other service providers who provide certain enumerated services for indirect compensation

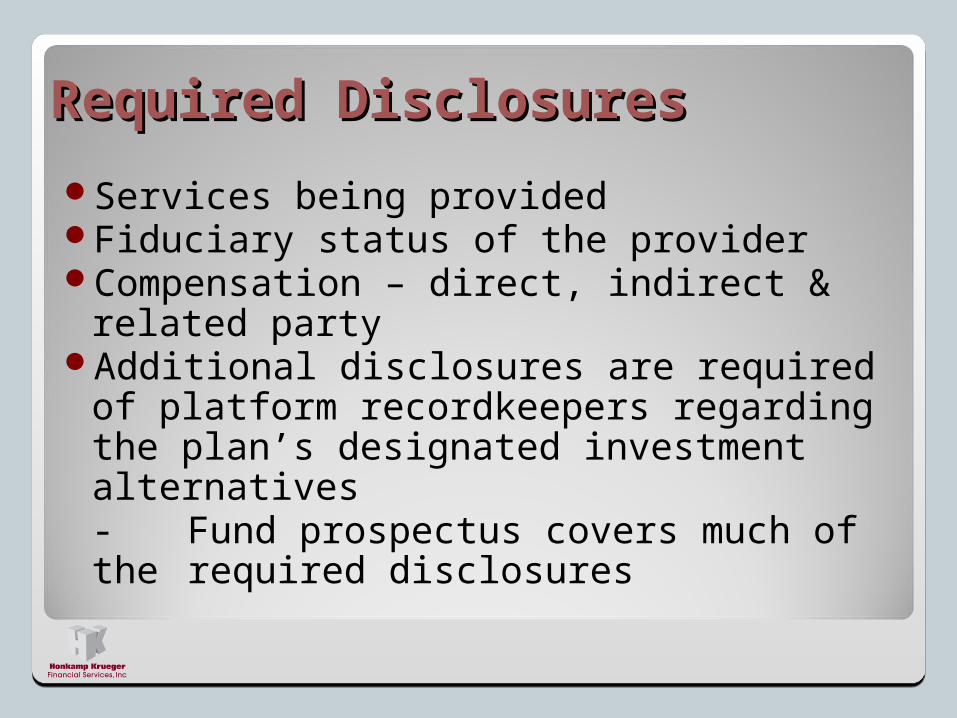

Required DisclosuresRequired Disclosures

Services being providedFiduciary status of the providerCompensation – direct, indirect & related

partyAdditional disclosures are required of

platform recordkeepers regarding the plan’s designated investment alternatives- Fund prospectus covers much of the

required disclosures

What if Disclosures Aren’t Made?What if Disclosures Aren’t Made?Prohibited Transaction has occurredCovered Service Provider is liable for penalty and

correction - Probably refund full compensation to plan

Fiduciary is not liable if ◦ requests the disclosures from the CSP◦ If none, notifies the DOL of failure

Disclosures must be in writing and made reasonably in advance of the date the contract (service agreement) is entered into

New disclosures required for changes to the contract

How Does This Compare With How Does This Compare With Schedule C of Form 5500?Schedule C of Form 5500?Issue Schedule C 408(b)(2) Disclosure

Who must comply: Large Plans Large & Small Plans

Pension/Welfare: Applies to both Pension only

Threshold: $5,000 per year $1,000 during contract

Service Providers: All Selected; many only if indirect compensation

Disclose indirect comp unless paid by:

Plan or sponsor Plan, sponsor, CSP, affiliate, subcontractor

Mutual fund advisors: Reported Not included

Penalty: Incomplete 5500 Prohibited transaction

Noncash de minimis: $10/$50/$100 $250

II. Participant Fee Disclosure II. Participant Fee Disclosure Regulations Under ERISA Regulations Under ERISA

§404(a)§404(a)

BackgroundBackgroundERISA requires that plan fiduciaries act prudently and

solely in the interest of plan participants

When a plan gives investment responsibility to participants, they must be made aware of their responsibilities and provided sufficient information to make informed decisions by the plan fiduciary

Compliance with the 404(a) regulations satisfies the plan fiduciary’s duty to sufficiently inform plan participants◦ The plan fiduciary is still responsible for prudently selecting

service providers and designated investment alternatives

Effective for plan years beginning after 10/31/2011

Required DisclosuresRequired Disclosures

Applies to participant-directed DC plans that are subject to ERISA:

1. Annual general plan disclosures2. Annual and quarterly disclosures of plan

administrative expenses3. Annual and quarterly disclosures of

individual expenses4. Annual investment disclosures and

information regarding “designated investment alternatives”• Using DOL-approved chart

Coordination with ERISA §404(c)Coordination with ERISA §404(c)

Most of 404(c) is superseded by 404(a)◦ Must still notify participants that plan is a 404(c) plan◦ If plan offers employer securities, must notify

participants of certain information◦ Must otherwise comply with 404(a)

The 404(c) regulatory scheme was voluntary – 404(a) is mandatory

404(a) requires more extensive disclosure of expenses and some 404(c) information that was available only if requested is now mandatory◦ But the 404(c) requirement that a participant receive a

copy of the fund prospectus upon initial investment is relaxed to only upon request

Effect of Failure to ComplyEffect of Failure to ComplyRegulations require the plan administrator

to comply with the disclosuresA PA that does not comply has breached

its fiduciary dutyDOL does not impose any penalty for non-

compliance with 404(a)◦The consequence of failure would be its use as

evidence of imprudence in a legal action by the DOL or a participant

◦The DOL or participant would still need to prove damages

III. In-Plan Roth RolloversIII. In-Plan Roth Rollovers

What is an In-Plan Roth Rollover What is an In-Plan Roth Rollover (IPRR)?(IPRR)?

An eligible rollover distributionFollowing a distributable eventFrom an individual’s plan accountRolled over to a designated Roth account

in the same plan◦Direct, or◦60-day

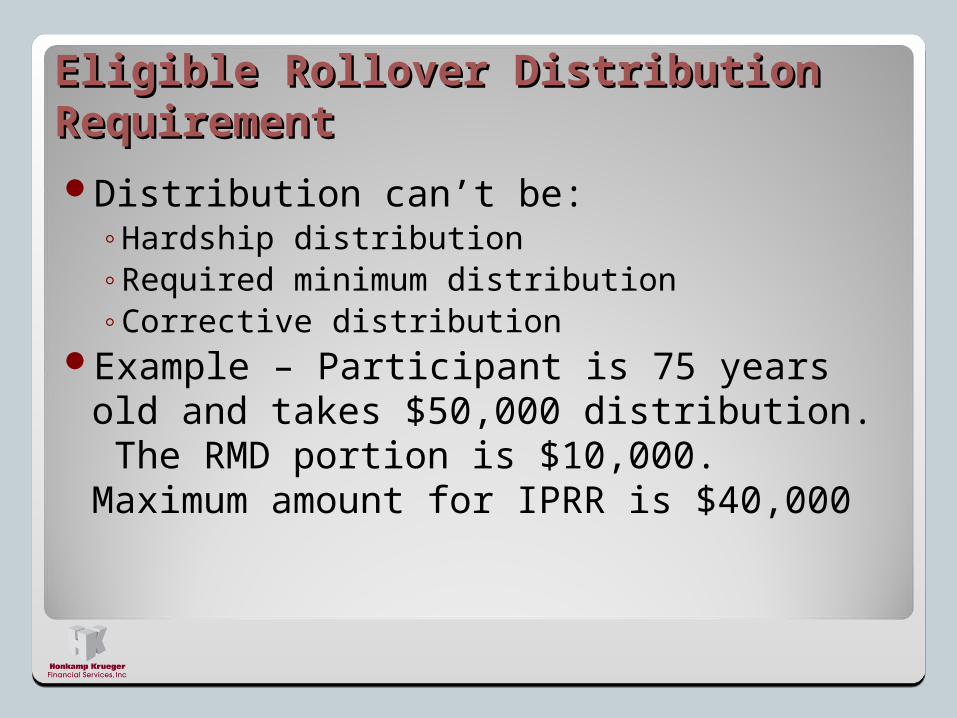

Eligible Rollover Distribution Eligible Rollover Distribution RequirementRequirement

Distribution can’t be:◦Hardship distribution◦Required minimum distribution◦Corrective distribution

Example – Participant is 75 years old and takes $50,000 distribution. The RMD portion is $10,000. Maximum amount for IPRR is $40,000

Distributable Event RequirementDistributable Event Requirement

Participant must be entitled to distribution:◦ Under Code and regulations◦ Under plan terms

Example 1 – Participant is 50 years old and still working. Participant can’t do IPRR of deferrals due to Code’s prohibition on distributions prior to age 59 ½

Example 2 – Participant is 60 years old and still working. Participant can’t do IPRR of deferrals unless the plan terms allow an in-service distribution after age 59 ½

IRS Notice 2010-84 allows plan to add in-service distribution option limited to IPRR

Tax Consequences of an IPRRTax Consequences of an IPRRParticipant is taxed as if there was a distribution from

the plan◦ But not subject to Code §72(t) 10% early distribution penalty◦ Mandatory 20% withholding does not apply, if direct IPRR

5-year Roth clock starts on January 1 of the year of the IPRR◦ Or, if earlier, on January 1 of the year of a prior Roth deferral

or direct rollover from another plan◦ There is only one Roth clock for a designated Roth account

IPRR account is subject to the 72(t) recapture rules if a subsequent distribution from the Roth account occurs within five years of the year of the IPRR

IPRR AccountingIPRR AccountingA designated Roth Account can contain

◦Roth elective deferrals◦Rollovers from Roth accounts in other plans◦In-Plan Roth Rollovers◦Earnings thereon

Different distribution requirements may apply to each◦So it makes sense to have separate

recordkeeping buckets for each contribution type

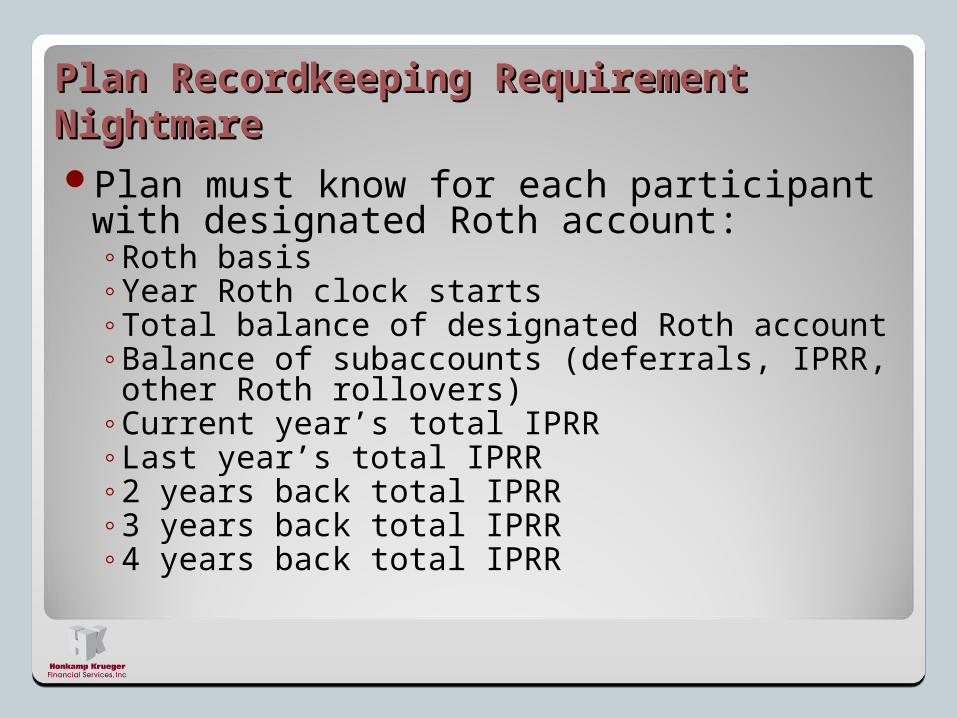

Plan Recordkeeping Requirement Plan Recordkeeping Requirement NightmareNightmarePlan must know for each participant with

designated Roth account:◦Roth basis◦Year Roth clock starts◦Total balance of designated Roth account◦Balance of subaccounts (deferrals, IPRR, other

Roth rollovers)◦Current year’s total IPRR◦Last year’s total IPRR◦2 years back total IPRR◦3 years back total IPRR◦4 years back total IPRR

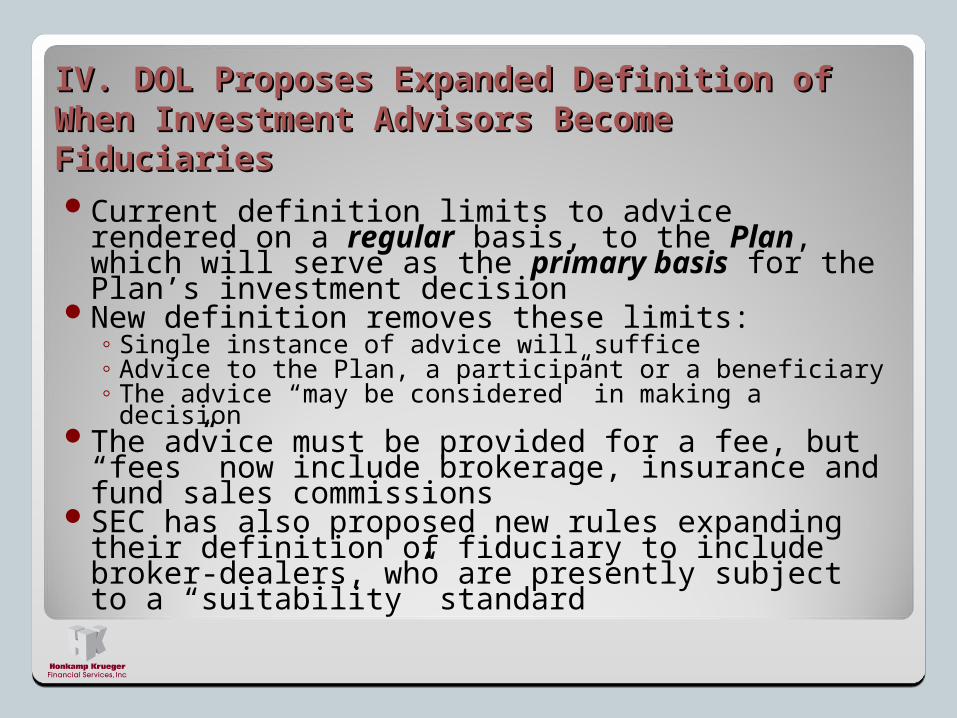

IV. DOL Proposes Expanded Definition of IV. DOL Proposes Expanded Definition of When Investment Advisors Become When Investment Advisors Become FiduciariesFiduciariesCurrent definition limits to advice rendered on a

regular basis, to the Plan, which will serve as the primary basis for the Plan’s investment decision

New definition removes these limits:◦ Single instance of advice will suffice◦ Advice to the Plan, a participant or a beneficiary◦ The advice “may be considered” in making a decision

The advice must be provided for a fee, but “fees” now include brokerage, insurance and fund sales commissions

SEC has also proposed new rules expanding their definition of fiduciary to include broker-dealers, who are presently subject to a “suitability” standard

V. Preparer Tax Identification V. Preparer Tax Identification Numbers and Form 5500Numbers and Form 5500 IRS Circular 230 requires a PTIN for all tax return preparers,

both signers and non-signers, and creates new designation – Registered Tax Return Preparer

Looked very likely that Form 5500 would be treated as a tax return- Many 5500 preparers would be required to become a RTRP and pass an exam in order to obtain a PTIN

IRS Notice 2011-6: The 5500 series returns, Forms 1099, W-2 and determination letter forms are NOT considered tax returns

The new Form 8955-SSA and Form 5558 do not require a PTIN

CAUTION - Many ERISA practitioners also prepare Forms 5330, 945 and 990-T. These are not exempted from the PTIN requirements

Planning StrategiesPlanning StrategiesEmployer Contribution Options

Contribution Analysis for Flesh & Bones Medical Group

SIMPLE IRA Plan

Full-Year Qualified Deferral Deferral Match Total

Employee Age Compensation Compensation % $ $1 for $1 on 3% Allocations

Dr. Flesh 52 350,000.00 245,000.00 5.71% 14,000.00 10,500.00 24,500.00

Dr. Bones 46 220,000.00 220,000.00 5.23% 11,500.00 6,600.00 18,100.00

Mr. Clamp 42 45,000.00 45,000.00 5.00% 2,250.00 1,350.00 3,600.00

Ms. Needle 50 35,000.00 35,000.00 3.00% 1,050.00 1,050.00 2,100.00

Ms. Suture 33 30,000.00 30,000.00 0.00% - - -

Ms. Xray 25 25,000.00 25,000.00 0.00% - - -

Grand Totals 705,000.00 600,000.00 28,800.00 19,500.00 48,300.00

Employer Dollars to Employees 2,400.00

% of Total Employer Dollars 12.31%

Contribution Analysis for Flesh & Bones Medical Group

Non-Safe Harbor 401(k) Plan With Fixed Match

Match Total

Employee Compensation Deferral % Deferral $ 50% on first 6% Allocations

Dr. Flesh 245,000.00 4.00% 9,800.00 4,900.00 14,700.00

Dr. Bones 220,000.00 4.00% 8,800.00 4,400.00 13,200.00

Mr. Clamp 45,000.00 5.00% 2,250.00 1,125.00 3,375.00

Ms. Needle 35,000.00 3.00% 1,050.00 525.00 1,575.00

Ms. Suture 30,000.00 0.00% - - -

Ms. Xray 25,000.00 0.00% - - -

Grand Totals 600,000.00 21,900.00 10,950.00 32,850.00

Employer Dollars to Employees 1,650.00

% of Total Employer Dollars 15.07%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic Match

Total

Employee Compensation Deferral Match Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 31,800.00

Dr. Bones 220,000.00 16,500.00 8,800.00 25,300.00

Mr. Clamp 45,000.00 2,250.00 1,800.00 3,375.00

Ms. Needle 35,000.00 1,050.00 1,050.00 1,575.00

Ms. Suture 30,000.00 - - -

Ms. Xray 25,000.00 - - -

Grand Totals 600,000.00 41,800.00 21,450.00 63,250.00

Employer Dollars to Employees 2,850.00

% of Total Employer Dollars 13.29%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic & Discretionary Match

67.00%Discretionary Total

Employee Compensation Deferral Basic Match Match Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 9,800.00 41,600.00

Dr. Bones 220,000.00 16,500.00 8,800.00 8,800.00 34,100.00

Mr. Clamp 45,000.00 2,250.00 1,800.00 1,507.50 5,557.50

Ms. Needle 35,000.00 1,050.00 1,050.00 703.50 2,803.50

Ms. Suture 30,000.00 - - - -

Ms. Xray 25,000.00 - - - -

Grand Totals 600,000.00 41,800.00 21,450.00 20,811.00 84,061.00

Employer Dollars to Employees 5,061.00

% of Total Employer Dollars 11.98%

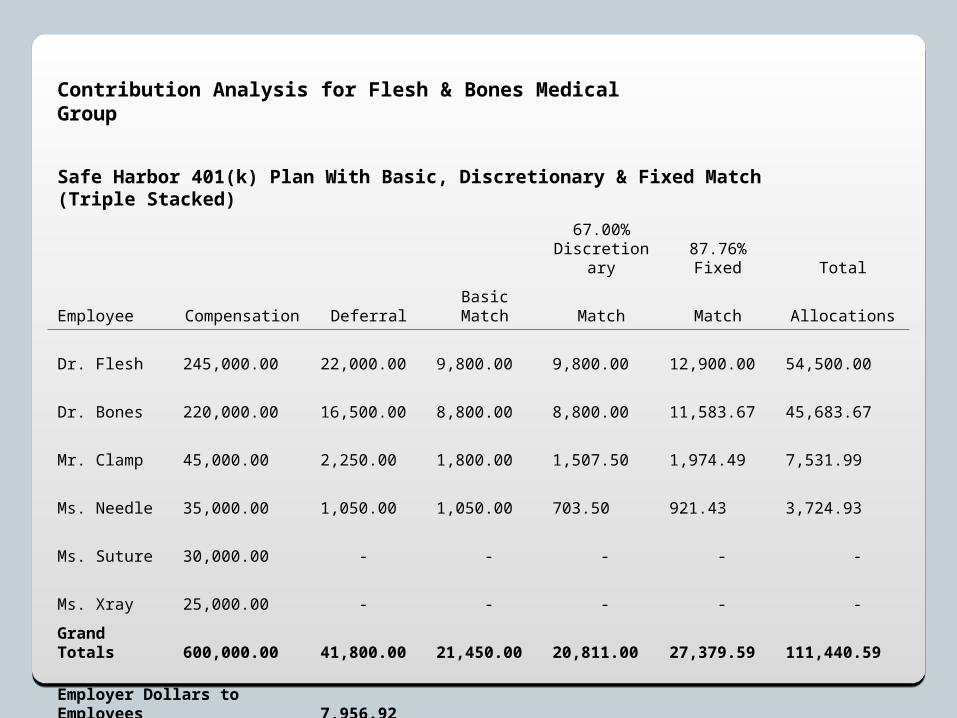

Contribution Analysis for Flesh & Bones Medical Group

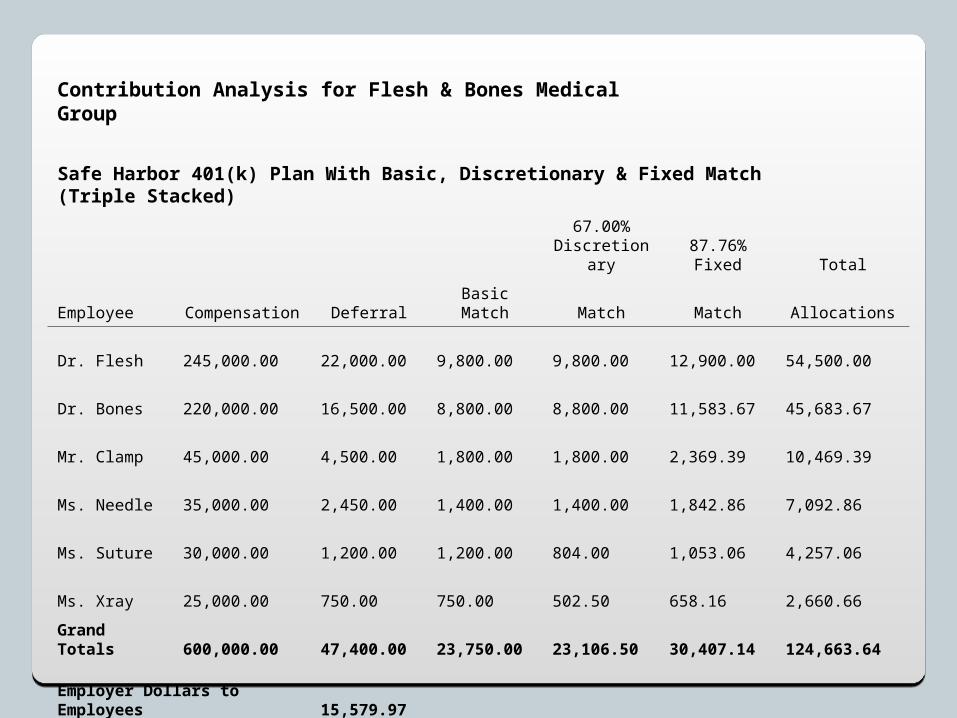

Safe Harbor 401(k) Plan With Basic, Discretionary & Fixed Match (Triple Stacked)

67.00%Discretionary

87.76%Fixed Total

Employee Compensation Deferral Basic Match Match Match Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 9,800.00 12,900.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 8,800.00 11,583.67 45,683.67

Mr. Clamp 45,000.00 2,250.00 1,800.00 1,507.50 1,974.49 7,531.99

Ms. Needle 35,000.00 1,050.00 1,050.00 703.50 921.43 3,724.93

Ms. Suture 30,000.00 - - - - -

Ms. Xray 25,000.00 - - - - -

Grand Totals 600,000.00 41,800.00 21,450.00 20,811.00 27,379.59 111,440.59

Employer Dollars to Employees 7,956.92

% of Total Employer Dollars 11.43%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic, Discretionary & Fixed Match (Triple Stacked)

67.00%Discretionary

87.76%Fixed Total

Employee Compensation Deferral Basic Match Match Match Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 9,800.00 12,900.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 8,800.00 11,583.67 45,683.67

Mr. Clamp 45,000.00 4,500.00 1,800.00 1,800.00 2,369.39 10,469.39

Ms. Needle 35,000.00 2,450.00 1,400.00 1,400.00 1,842.86 7,092.86

Ms. Suture 30,000.00 1,200.00 1,200.00 804.00 1,053.06 4,257.06

Ms. Xray 25,000.00 750.00 750.00 502.50 658.16 2,660.66

Grand Totals 600,000.00 47,400.00 23,750.00 23,106.50 30,407.14 124,663.64

Employer Dollars to Employees 15,579.97

% of Total Employer Dollars 20.16%

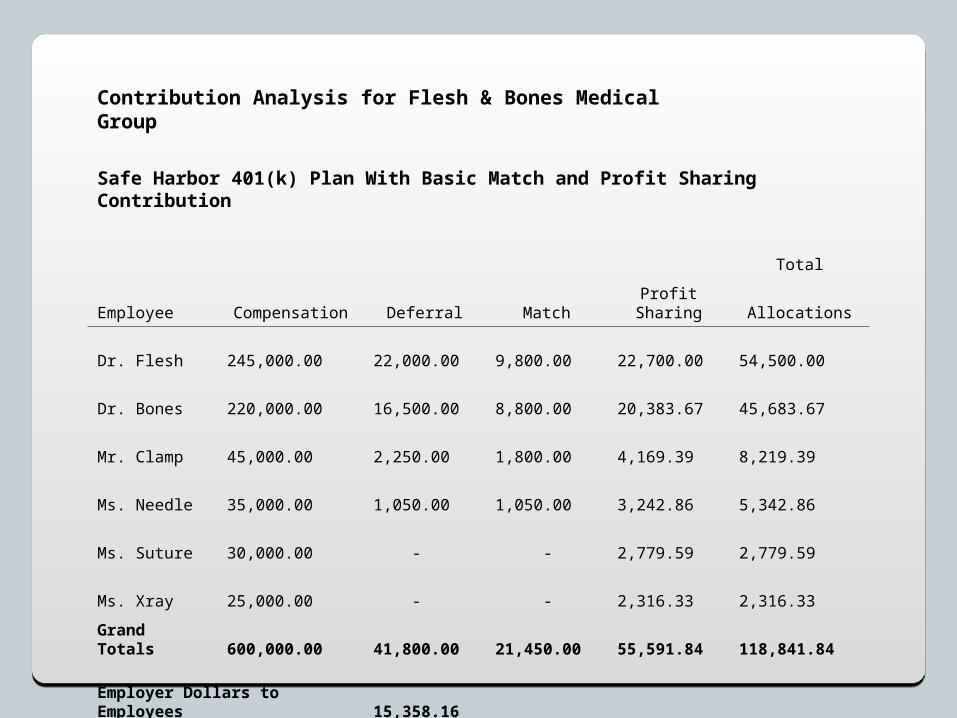

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic Match and Profit Sharing Contribution

Total

Employee Compensation Deferral Match Profit Sharing Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 22,700.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 20,383.67 45,683.67

Mr. Clamp 45,000.00 2,250.00 1,800.00 4,169.39 8,219.39

Ms. Needle 35,000.00 1,050.00 1,050.00 3,242.86 5,342.86

Ms. Suture 30,000.00 - - 2,779.59 2,779.59

Ms. Xray 25,000.00 - - 2,316.33 2,316.33

Grand Totals 600,000.00 41,800.00 21,450.00 55,591.84 118,841.84

Employer Dollars to Employees 15,358.16

% of Total Employer Dollars 19.93%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic Match and Permitted Disparity P/S Allocation

Total

Employee Compensation Deferral Match Profit Sharing Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 22,700.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 20,164.29 45,464.29

Mr. Clamp 45,000.00 2,250.00 1,800.00 2,629.29 6,679.29

Ms. Needle 35,000.00 1,050.00 1,050.00 2,045.00 4,145.00

Ms. Suture 30,000.00 - - 1,752.86 1,752.86

Ms. Xray 25,000.00 - - 1,460.71 1,460.71

Grand Totals 600,000.00 41,800.00 21,450.00 50,752.15 114,002.15

Employer Dollars to Employees 10,737.86

% of Total Employer Dollars 14.87%

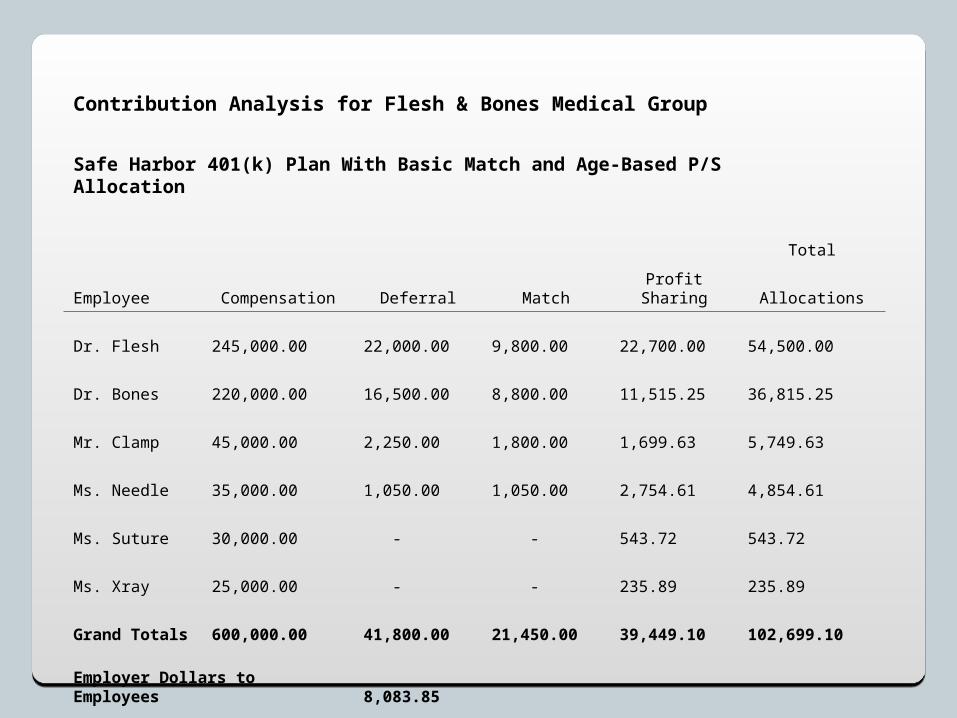

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic Match and Age-Based P/S Allocation

Total

Employee Compensation Deferral Match Profit Sharing Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 22,700.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 11,515.25 36,815.25

Mr. Clamp 45,000.00 2,250.00 1,800.00 1,699.63 5,749.63

Ms. Needle 35,000.00 1,050.00 1,050.00 2,754.61 4,854.61

Ms. Suture 30,000.00 - - 543.72 543.72

Ms. Xray 25,000.00 - - 235.89 235.89

Grand Totals 600,000.00 41,800.00 21,450.00 39,449.10 102,699.10

Employer Dollars to Employees 8,083.85

% of Total Employer Dollars 13.27%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With Basic Match and Cross-Tested P/S Allocation

Total

Employee Compensation Deferral Match Profit Sharing Allocations

Dr. Flesh 245,000.00 22,000.00 9,800.00 22,700.00 54,500.00

Dr. Bones 220,000.00 16,500.00 8,800.00 20,383.67 45,683.67

Mr. Clamp 45,000.00 2,250.00 1,800.00 1,390.50 5,440.50

Ms. Needle 35,000.00 1,050.00 1,050.00 1,081.50 3,181.50

Ms. Suture 30,000.00 - - 927.00 927.00

Ms. Xray 25,000.00 - - 772.50 772.50

Grand Totals 600,000.00 41,800.00 21,450.00 47,255.17 110,505.17

Employer Dollars to Employees 7,021.50

% of Total Employer Dollars 10.22%

Contribution Analysis for Flesh & Bones Medical Group

Safe Harbor 401(k) Plan With 3% Non-Elective and Cross-Tested P/S Allocation

Total

Employee Compensation Deferral3% Non-Elective Profit Sharing Allocations

Dr. Flesh 245,000.00 22,000.00 7,350.00 25,150.00 54,500.00

Dr. Bones 220,000.00 16,500.00 6,600.00 22,583.67 45,683.67

Mr. Clamp 45,000.00 2,250.00 1,350.00 639.00 4,239.00

Ms. Needle 35,000.00 1,050.00 1,050.00 497.00 2,597.00

Ms. Suture 30,000.00 - 900.00 426.00 1,326.00

Ms. Xray 25,000.00 - 750.00 355.00 1,105.00

Grand Totals 600,000.00 41,800.00 18,000.00 49,650.67 109,450.67

Employer Dollars to Employees 5,967.00

% of Total Employer Dollars 8.82%

Frequently Asked Frequently Asked QuestionsQuestions

Plan Adoption DeadlinesPlan Adoption Deadlines SEP-IRA Plan – A SEP must be established by the employer’s tax

return deadline (plus extensions) for the taxable year for which the employer wishes to make the SEP contribution

SIMPLE IRA Plan – A SIMPLE IRA must be maintained on a calendar year but a new SIMPLE IRA may have an effective date other than January 1. However, the effective date may not be later than October 1, unless the employer comes into existence after October 1◦ If this is not the employer’s first SIMPLE IRA, the effective date must be

Jan. 1 Other Qualified Plans – All other qualified plans must be

established by the last day of the taxable year for which a deduction is to be taken for contributions to the plan◦ Exception – Safe harbor 401(k) plans generally require a full 12- month

plan year, and so must be amended or adopted prior to January 1 if treated as a successor plan

◦ Exception to the Exception - The first plan year of a new safe harbor 401(k) plan can be less than 12 months but must be at least 3 months long, unless the employer is in existence less than 3 months

SEP and SIMPLE Plan Related Group SEP and SIMPLE Plan Related Group IssuesIssues Fact Situation 1 – An individual is 100% owner of two companies,

one of which he is the only employee. The owner-only company maintains a SEP for the owner. The other company with employees maintains a pension plan. Is this a problem?◦ Yes it is. A SEP is required to cover all members of a related group, as if

the related companies are one company. All employees who satisfy the participation requirements of the SEP must b eligible, regardless of which related group member they work for. It is not proper to establish a SEP for just one member of a related group, even if the coverage requirements would be satisfied, because the coverage rules are not applicable to SEPs.

Fact Situation 2 – A CPA participates in a SIMPLE IRA with her CPA firm, and also participates in a SEP as an employee of her husband’s 100%-owned business. Is this a problem?◦ That depends. Her husband’s ownership in his company is attributed to

her, and since she is an employee in the company, an exception to this attribution rule does not apply.

◦ However, if she owns less than 80% of the CPA firm it will not be treated as related to the husband’s company and the husband’s SEP is safe

How HKFS How HKFS Can HelpCan Help

The HKFS AdvantageThe HKFS Advantage Local Presence. As a local, independent organization, we’re very

responsive to customer needs. We don’t insist that you fit into our way of doing business – we adapt our practices to suit your needs and preferences. The people working on your account are right here in the upper Midwest.

Professional Experience. We have a rapidly expanding staff of retirement plan experts that includes an ERISA attorney, a Qualified Pension Administrator, a Qualified 401(k) Administrator and various securities and insurance licensed personnel. Our Retirement Plan Services director and operations supervisor alone boast over 45 years combined experience in retirement plan investment and administration. Your account administrator is an experienced professional.

Fiduciary Oversight. HKFS, as a registered investment advisor, will assume the status of an ERISA section 3(38) fiduciary. An ERISA 3(38) fiduciary has ERISA legally defined “discretion” that makes it a decision-maker. This means that a 3(38) fiduciary actually makes decisions for which it is legally culpable and for which the plan sponsor is no longer legally culpable.

The HKFS AdvantageThe HKFS Advantage Face-to-Face Relationships. HKFS prides itself on our network

of financial advisors. We will have a designated financial advisor available at reasonably short notice for sit-down meetings at the employer level or with individual plan participants. We also maintain an 800 number you can call with technical or service questions, and we will provide both a sponsor and participant website.

Impartial Advice. One of our great strengths is that we are not allied or associated with any one family of mutual funds. Virtually the entire universe of mutual funds is available to us, with operational practicalities being the only limiting factor. With the universe to choose from, we can generally offer you fund options that are broader than to any one family of funds or fund alliance.

Due Diligence. The investment funds and model portfolios that we select for use in retirement plans are screened and monitored by the HKFS Investment Advisory Committee. This Committee meets monthly, our Investment Management staff assesses the funds versus their peer group, using such tools as Morningstar®, Standard & Poors and Advisor Intelligence, a subscriber resource available only to registered investment advisors. The members of the Committee include an attorney, an MBA, two CFP designations, two CFA designations, and a PhD in Economics.

The HKFS AdvantageThe HKFS Advantage Reasonable Fees. We have no hidden loads or sales charges,

but quote our fees up-front and in writing. We can also provide you the flexibility of being billed for our charges or having them deducted from the plan assets. HKFS will periodically receive revenue sharing payments based on agreements between the mutual fund companies and our custodian, Fidelity. HKFS will normally NOT retain any revenue sharing payments and will not utilize the fees as soft dollar payments for other services. All revenue sharing payments will be applied to offset our contracted fees, and amounts in excess of our fees will be allocated on a non-discriminatory basis to plan participants. We will allow nothing to affect our independent judgment in selecting what we consider to be the best investment funds for plan participants.

Full Service. We bring to the table a complete bundle of financial services for your business. Our comprehensive retirement plan package covers every aspect of your company plan, from plan design to investment management, from recordkeeping to compliance testing, from government reporting to participant education. In addition, the Honkamp family can provide you with business consulting and tax planning, a seamlessly integrated payroll system, wealth and estate planning services and insurance planning and products.

Retirement Plan Services StaffRetirement Plan Services StaffRichard Howard, J.D., CRSPVice PresidentDirector, Retirement Services

Pam GoedkenSupervisor, Retirement Services

Joni DementSenior Document Specialist

Amy NeissSenior Retirement Services Rep

Kathy LentRetirement Services Rep

Chris MooreRetirement Services Rep

Tina DoughertyRetirement Services Rep II