Fringe Benefits

31

Fringe Benefits

-

Upload

clang-santiago -

Category

Documents

-

view

29 -

download

0

description

vvv

Transcript of Fringe Benefits

Fringe Benefits

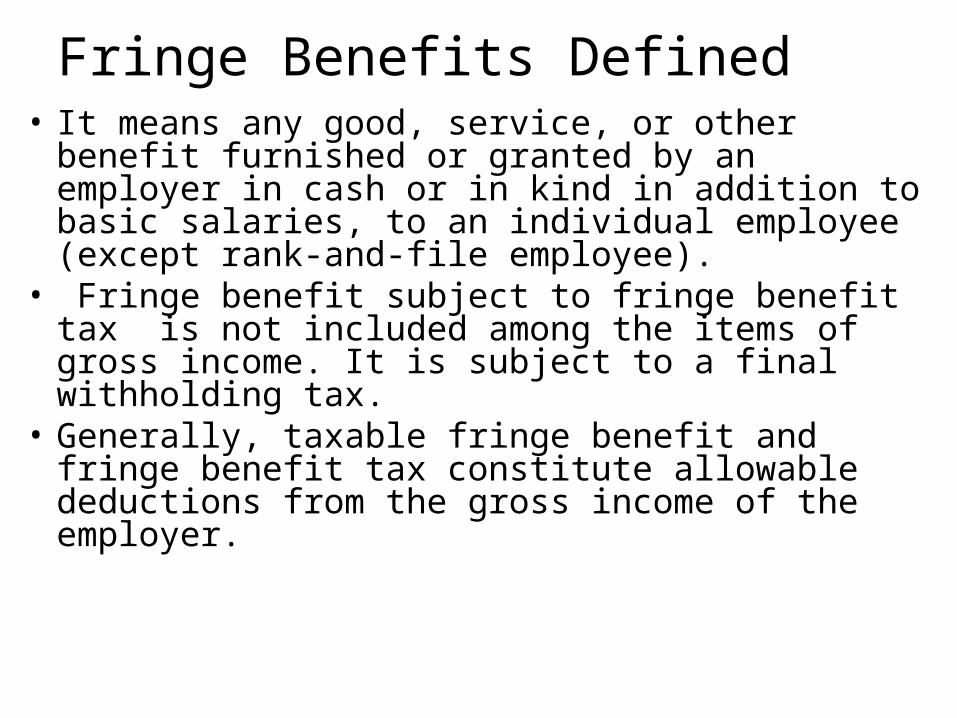

Fringe Benefits Defined• It means any good, service, or other benefit

furnished or granted by an employer in cash or in kind in addition to basic salaries, to an individual employee (except rank-and-file employee).

• Fringe benefit subject to fringe benefit tax is not included among the items of gross income. It is subject to a final withholding tax.

• Generally, taxable fringe benefit and fringe benefit tax constitute allowable deductions from the gross income of the employer.

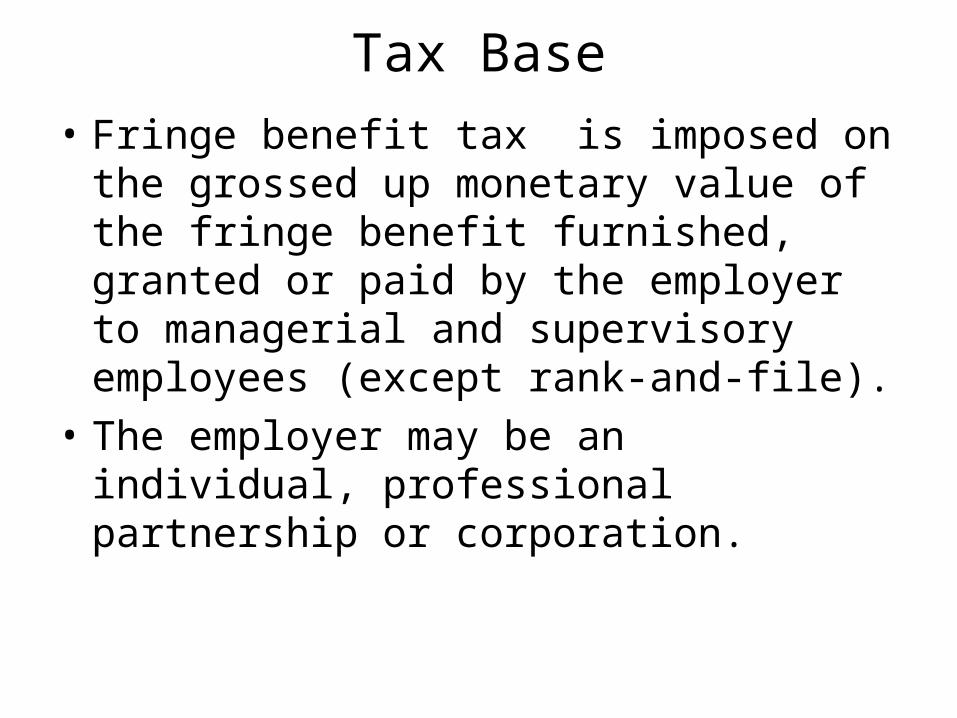

Tax Base

• Fringe benefit tax is imposed on the grossed up monetary value of the fringe benefit furnished, granted or paid by the employer to managerial and supervisory employees (except rank-and-file).

• The employer may be an individual, professional partnership or corporation.

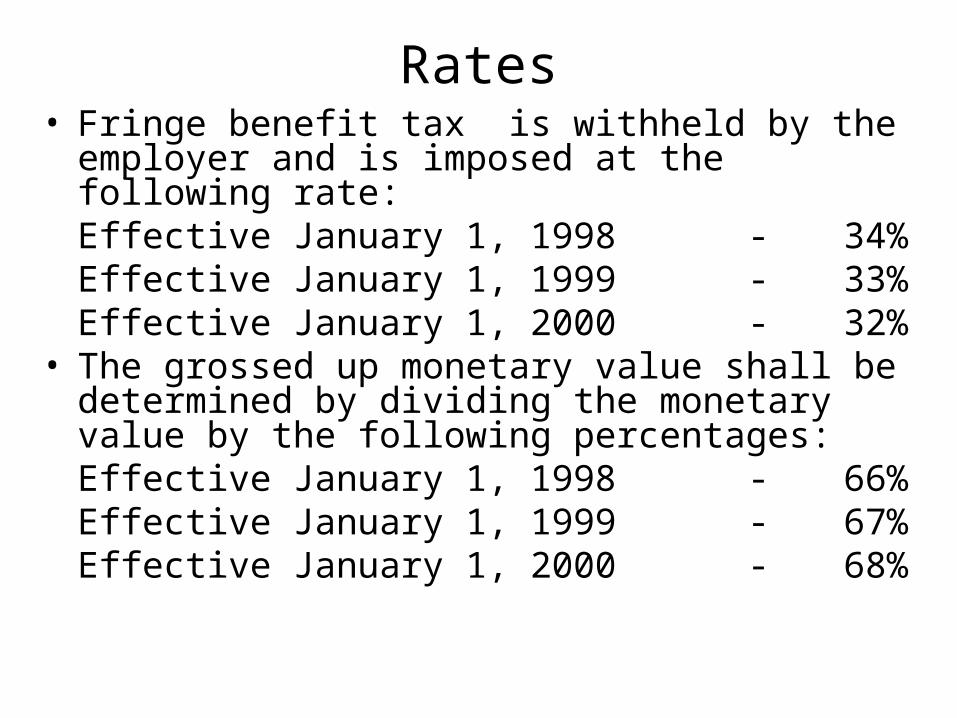

Rates

• Fringe benefit tax is withheld by the employer and is imposed at the following rate:Effective January 1, 1998 - 34%

Effective January 1, 1999 - 33%Effective January 1, 2000 - 32%

• The grossed up monetary value shall be determined by dividing the monetary value by the following percentages:Effective January 1, 1998 - 66%Effective January 1, 1999 - 67%Effective January 1, 2000 - 68%

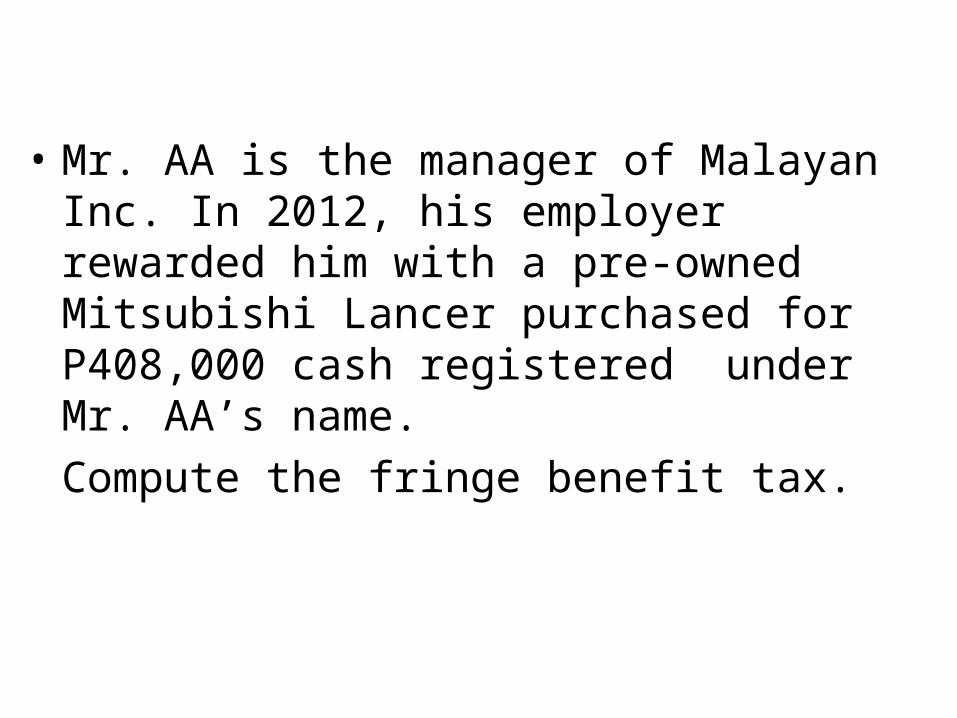

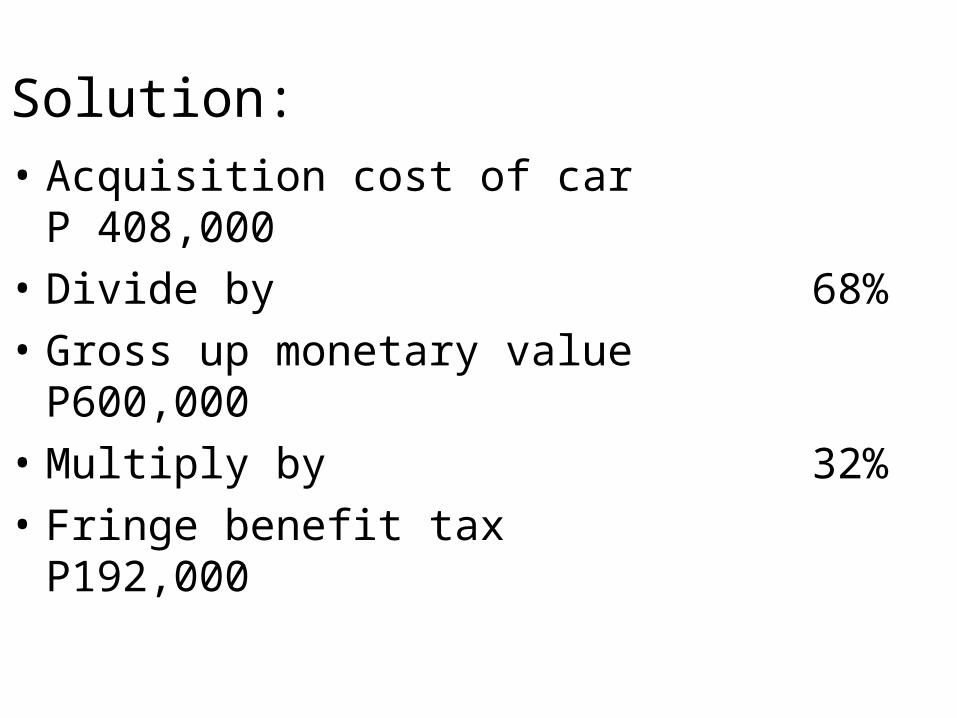

• Mr. AA is the manager of Malayan Inc. In 2012, his employer rewarded him with a pre-owned Mitsubishi Lancer purchased for P408,000 cash registered under Mr. AA’s name.Compute the fringe benefit tax.

Solution:• Acquisition cost of car P 408,000• Divide by 68%• Gross up monetary value P600,000• Multiply by 32%• Fringe benefit tax P192,000

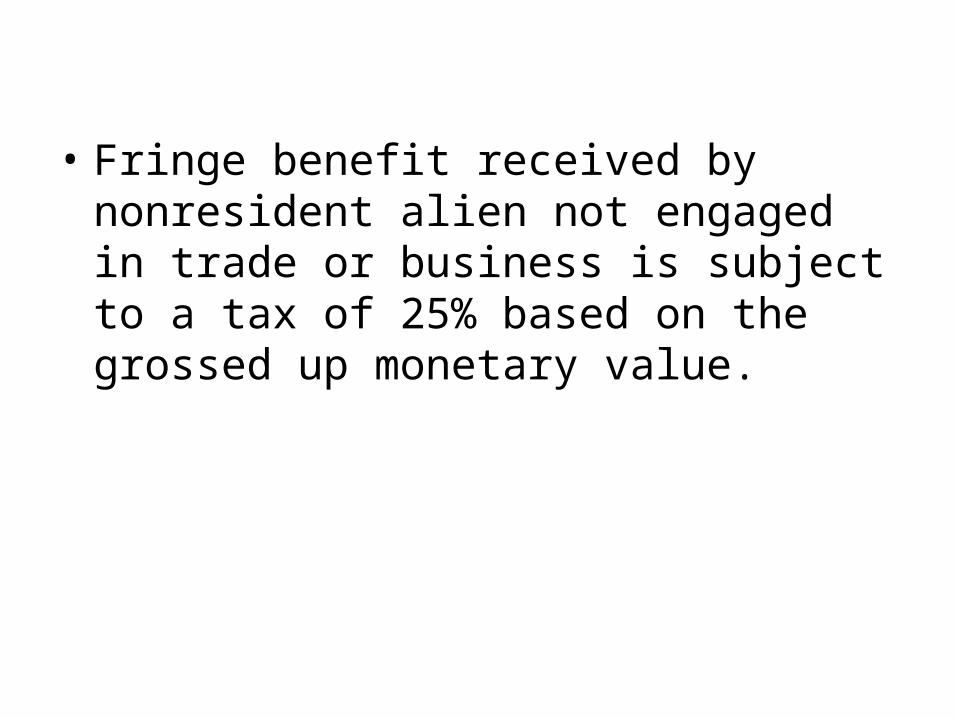

• Fringe benefit received by nonresident alien not engaged in trade or business is subject to a tax of 25% based on the grossed up monetary value.

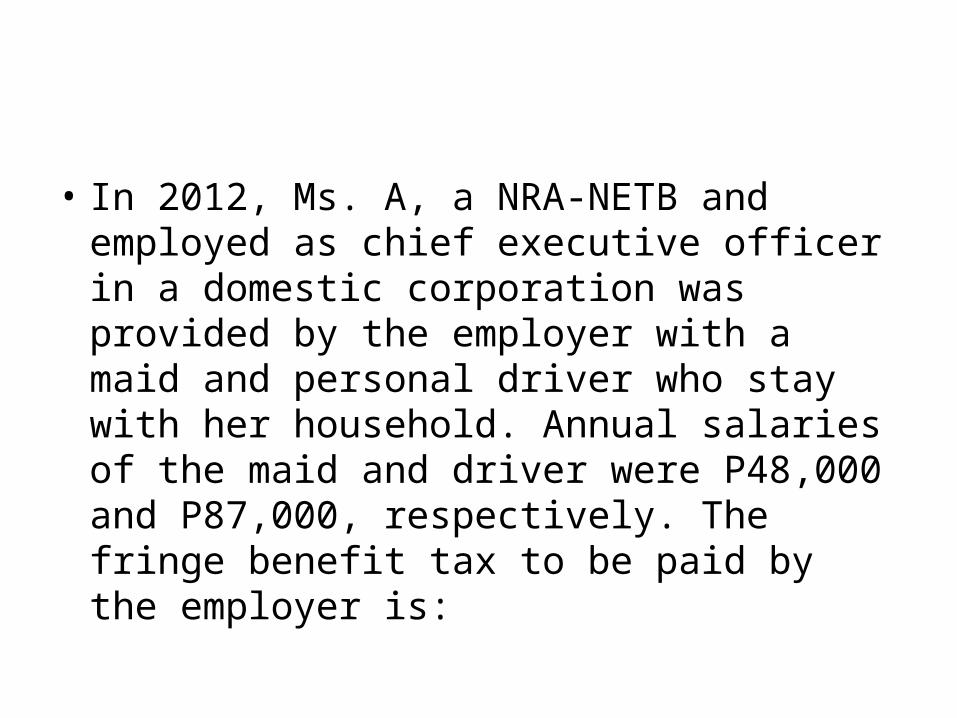

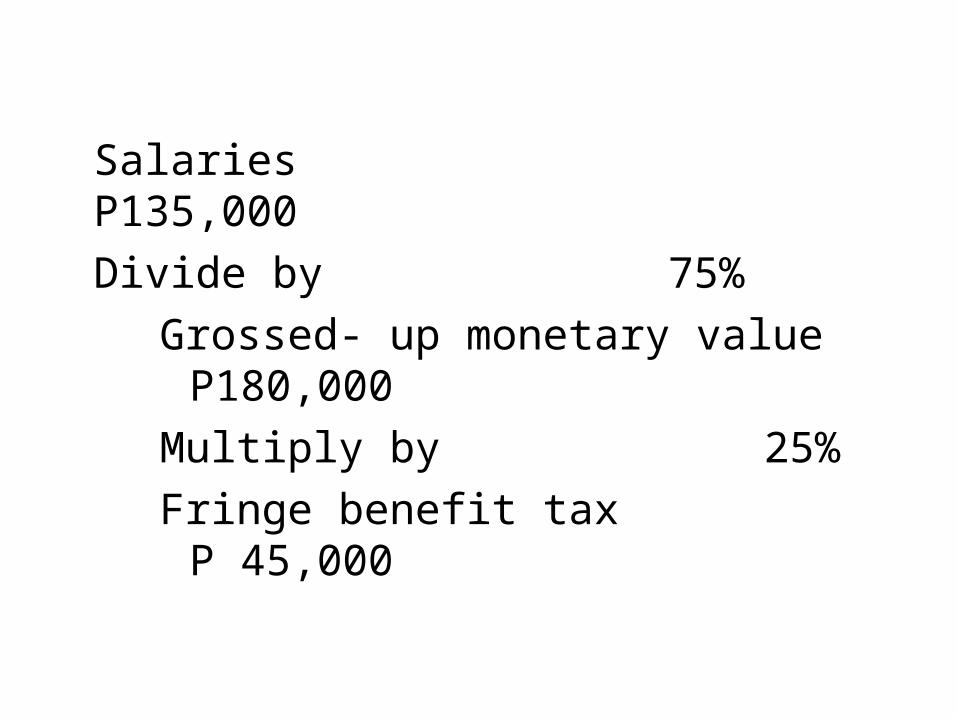

• In 2012, Ms. A, a NRA-NETB and employed as chief executive officer in a domestic corporation was provided by the employer with a maid and personal driver who stay with her household. Annual salaries of the maid and driver were P48,000 and P87,000, respectively. The fringe benefit tax to be paid by the employer is:

Salaries P135,000Divide by 75%

Grossed- up monetary value P180,000 Multiply by 25% Fringe benefit tax P 45,000

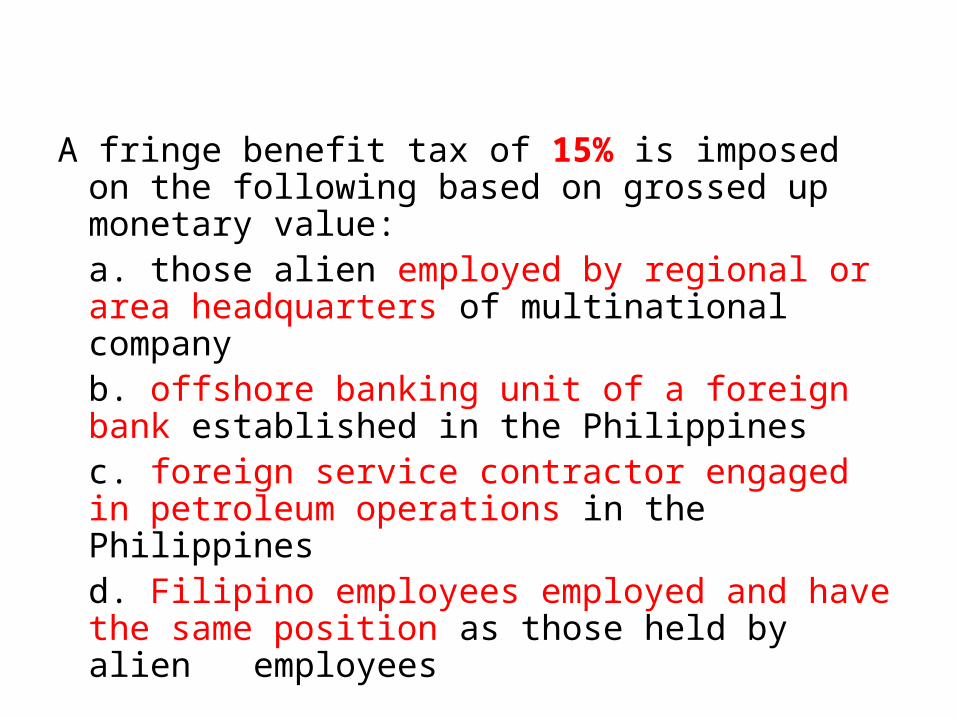

A fringe benefit tax of 15% is imposed on the following based on grossed up monetary value:a. those alien employed by regional or area headquarters of multinational companyb. offshore banking unit of a foreign bank established in the Philippinesc. foreign service contractor engaged in petroleum operations in the Philippinesd. Filipino employees employed and have the same position as those held by alien employees

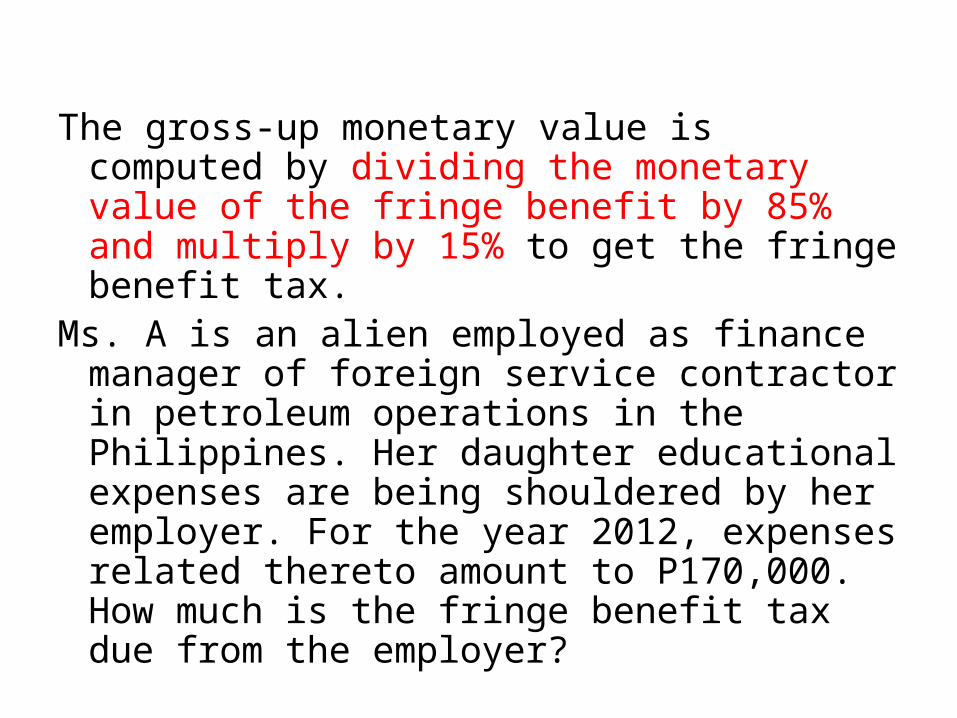

The gross-up monetary value is computed by dividing the monetary value of the fringe benefit by 85% and multiply by 15% to get the fringe benefit tax.

Ms. A is an alien employed as finance manager of foreign service contractor in petroleum operations in the Philippines. Her daughter educational expenses are being shouldered by her employer. For the year 2012, expenses related thereto amount to P170,000. How much is the fringe benefit tax due from the employer?

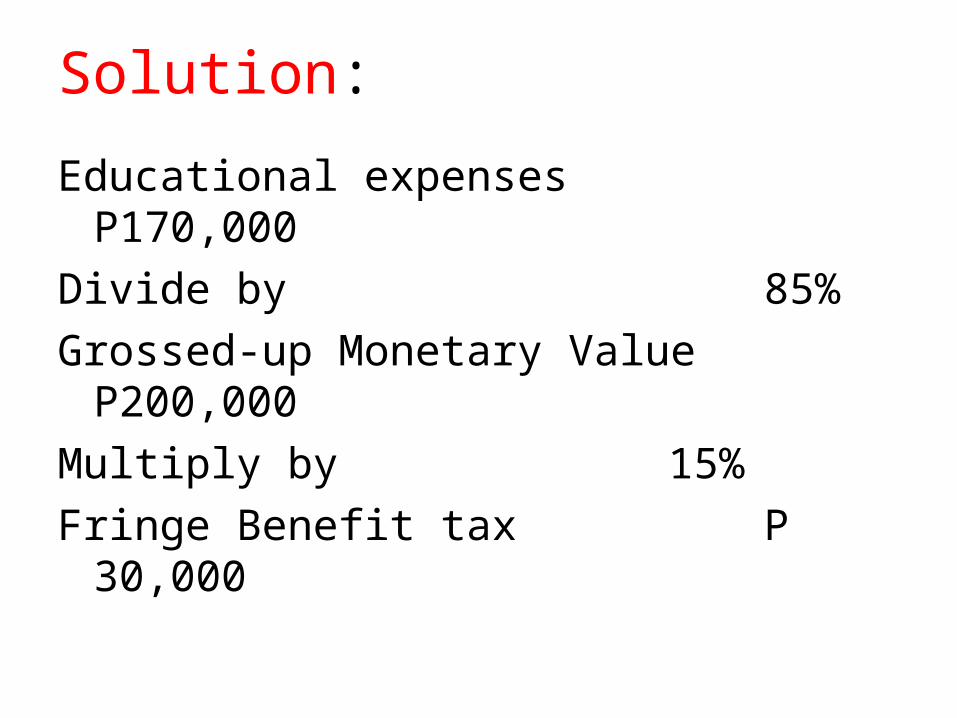

Solution:

Educational expenses P170,000Divide by 85%Grossed-up Monetary Value P200,000Multiply by 15%Fringe Benefit tax P 30,000

• Employees in special economic zones, including Clark Special Economic Zone and Subic Special Economic and Free Trade Zone are taxed at the normal rate (34%, 33%, 32%) or at special rates (25% and 15%), as the case may be.

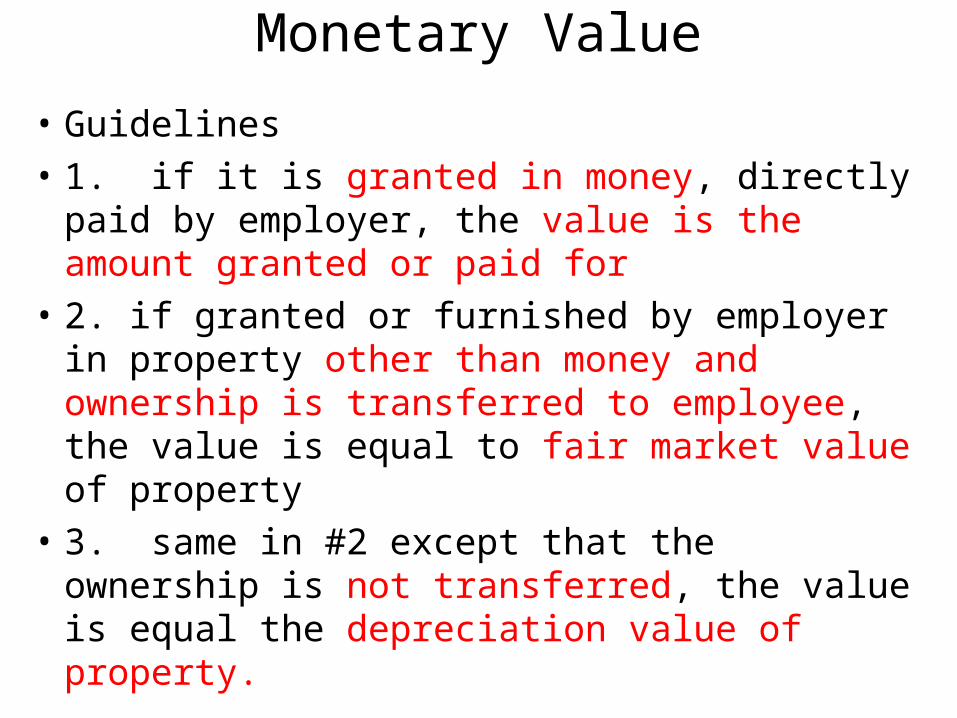

Monetary Value

• Guidelines• 1. if it is granted in money, directly paid by

employer, the value is the amount granted or paid for

• 2. if granted or furnished by employer in property other than money and ownership is transferred to employee, the value is equal to fair market value of property

• 3. same in #2 except that the ownership is not transferred, the value is equal the depreciation value of property.

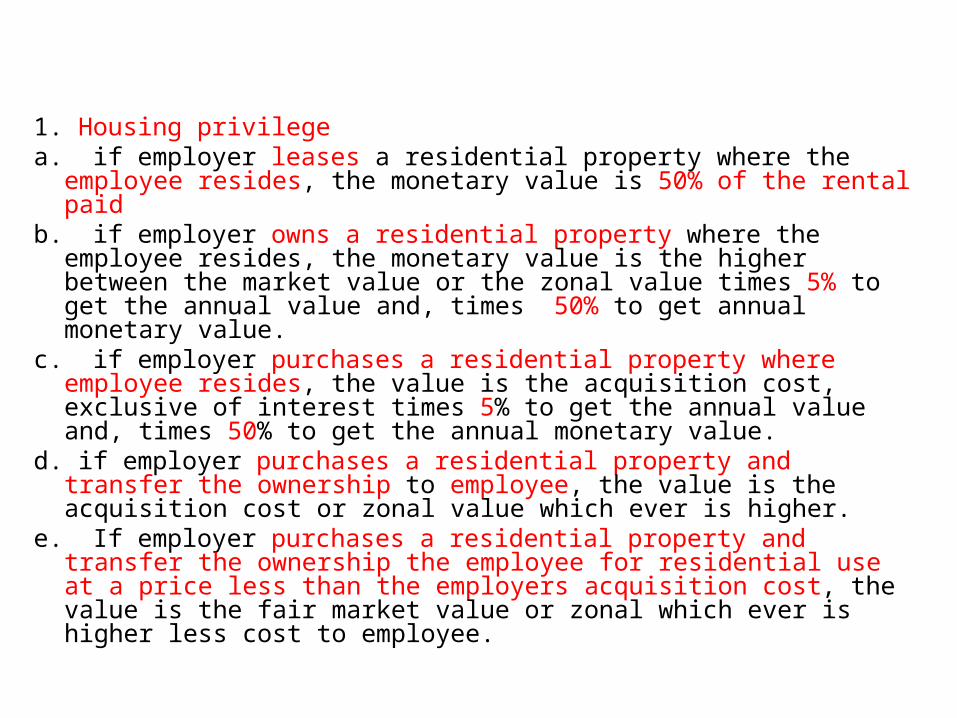

1. Housing privilegea. if employer leases a residential property where the employee resides,

the monetary value is 50% of the rental paidb. if employer owns a residential property where the employee resides,

the monetary value is the higher between the market value or the zonal value times 5% to get the annual value and, times 50% to get annual monetary value.

c. if employer purchases a residential property where employee resides, the value is the acquisition cost, exclusive of interest times 5% to get the annual value and, times 50% to get the annual monetary value.

d. if employer purchases a residential property and transfer the ownership to employee, the value is the acquisition cost or zonal value which ever is higher.

e. If employer purchases a residential property and transfer the ownership the employee for residential use at a price less than the employers acquisition cost, the value is the fair market value or zonal which ever is higher less cost to employee.

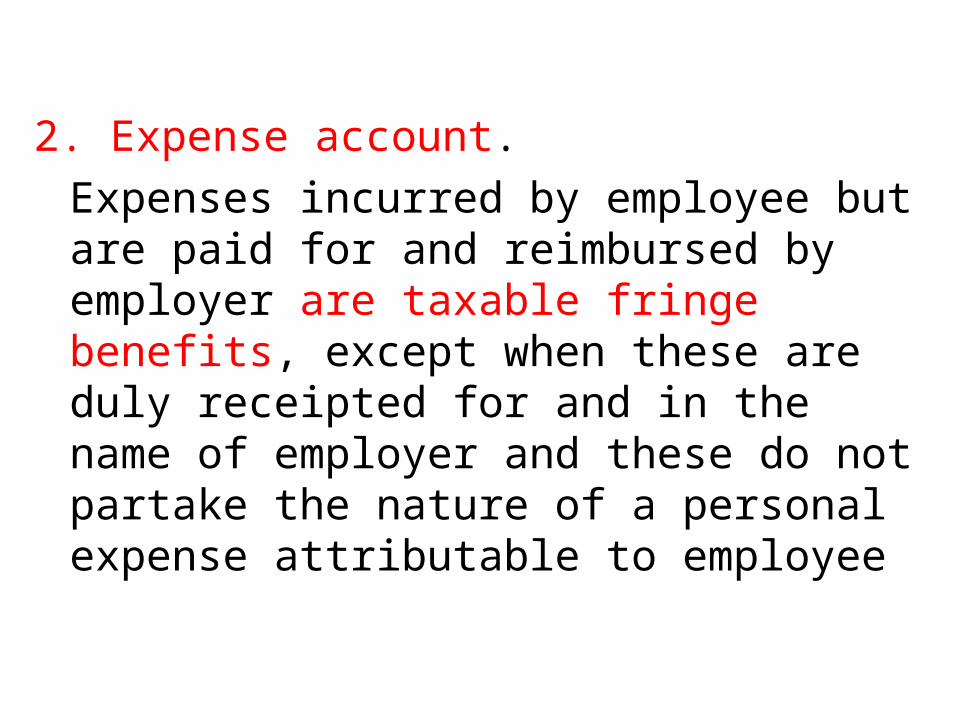

2. Expense account. Expenses incurred by employee but are paid for and reimbursed by employer are taxable fringe benefits, except when these are duly receipted for and in the name of employer and these do not partake the nature of a personal expense attributable to employee

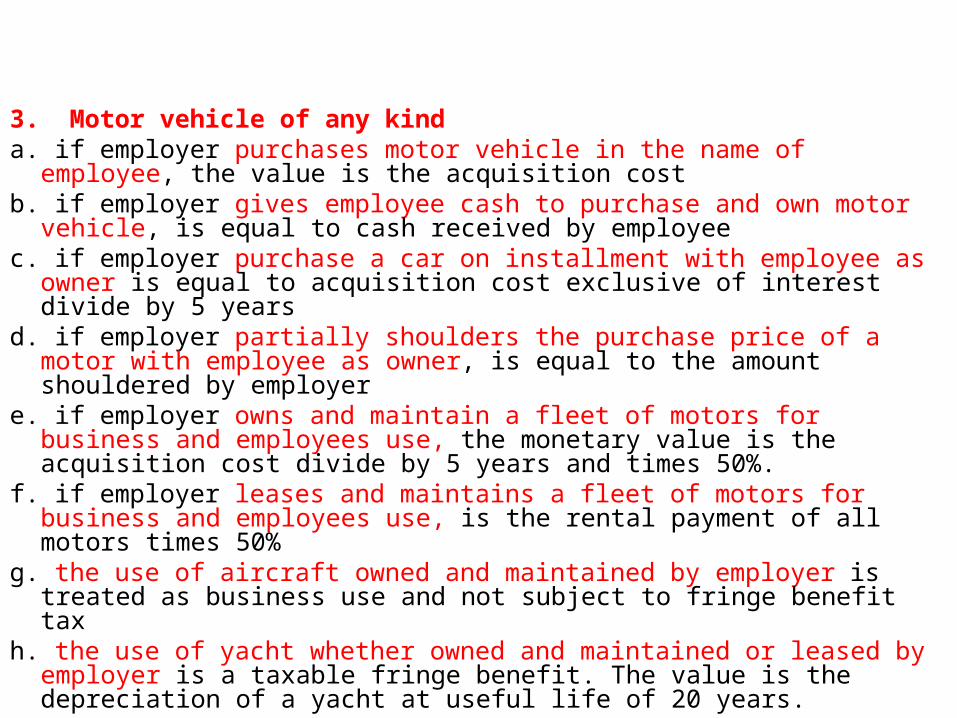

3. Motor vehicle of any kinda. if employer purchases motor vehicle in the name of employee, the value is

the acquisition costb. if employer gives employee cash to purchase and own motor vehicle, is

equal to cash received by employeec. if employer purchase a car on installment with employee as owner is equal

to acquisition cost exclusive of interest divide by 5 yearsd. if employer partially shoulders the purchase price of a motor with employee

as owner, is equal to the amount shouldered by employere. if employer owns and maintain a fleet of motors for business and employees

use, the monetary value is the acquisition cost divide by 5 years and times 50%.

f. if employer leases and maintains a fleet of motors for business and employees use, is the rental payment of all motors times 50%

g. the use of aircraft owned and maintained by employer is treated as business use and not subject to fringe benefit tax

h. the use of yacht whether owned and maintained or leased by employer is a taxable fringe benefit. The value is the depreciation of a yacht at useful life of 20 years.

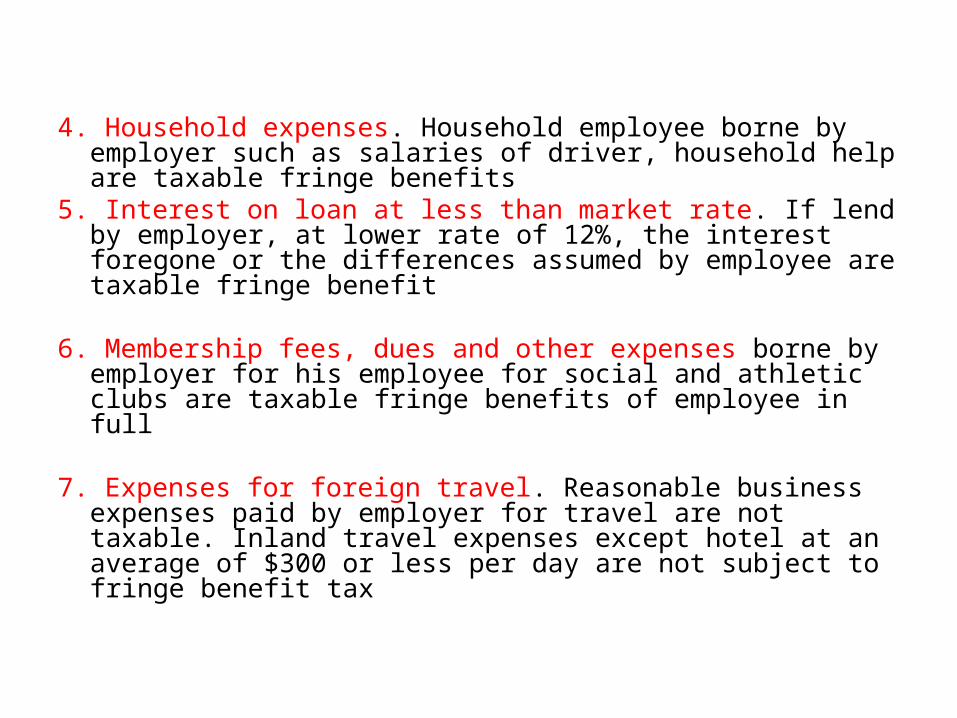

4. Household expenses. Household employee borne by employer such as salaries of driver, household help are taxable fringe benefits

5. Interest on loan at less than market rate. If lend by employer, at lower rate of 12%, the interest foregone or the differences assumed by employee are taxable fringe benefit

6. Membership fees, dues and other expenses borne by employer for

his employee for social and athletic clubs are taxable fringe benefits of employee in full

7. Expenses for foreign travel. Reasonable business expenses paid by

employer for travel are not taxable. Inland travel expenses except hotel at an average of $300 or less per day are not subject to fringe benefit tax

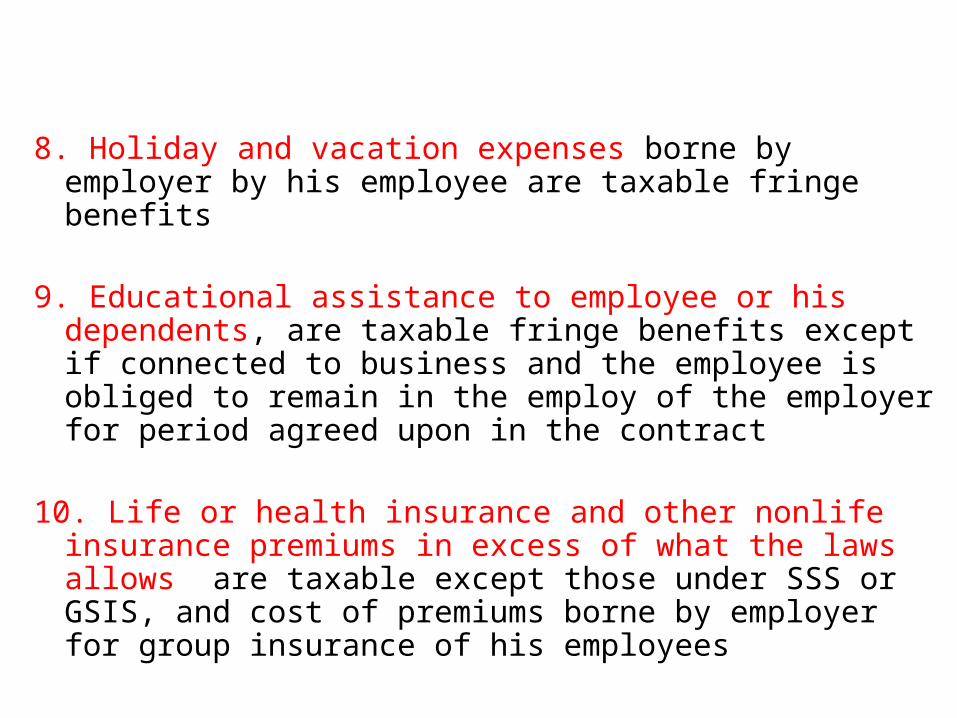

8. Holiday and vacation expenses borne by employer by his employee are taxable fringe benefits

9. Educational assistance to employee or his dependents, are

taxable fringe benefits except if connected to business and the employee is obliged to remain in the employ of the employer for period agreed upon in the contract

10. Life or health insurance and other nonlife insurance

premiums in excess of what the laws allows are taxable except those under SSS or GSIS, and cost of premiums borne by employer for group insurance of his employees

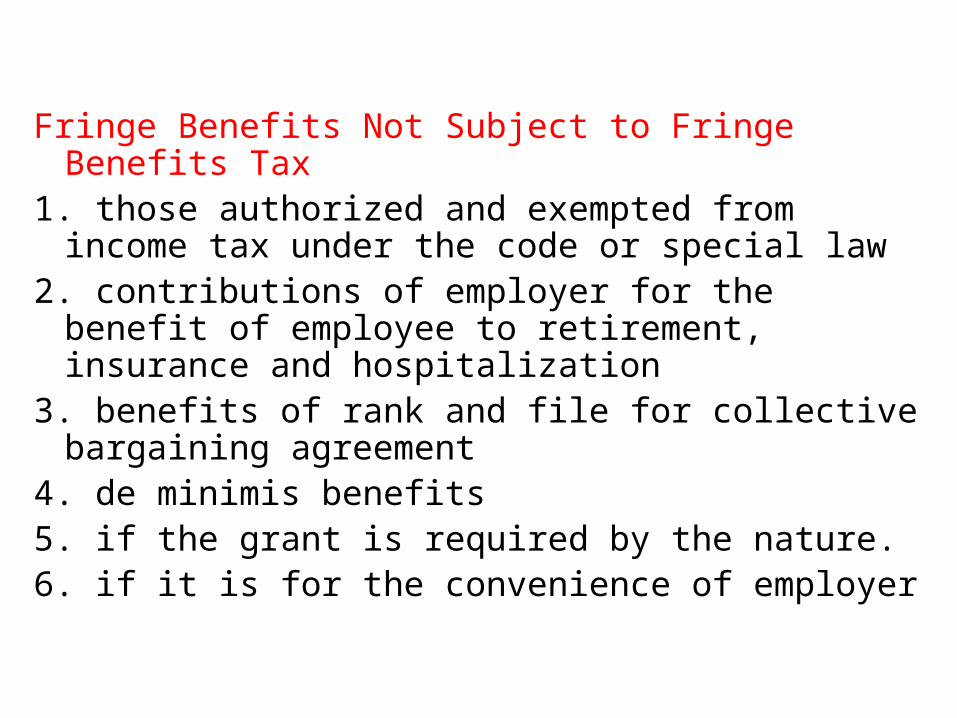

Fringe Benefits Not Subject to Fringe Benefits Tax1. those authorized and exempted from income tax

under the code or special law2. contributions of employer for the benefit of

employee to retirement, insurance and hospitalization

3. benefits of rank and file for collective bargaining agreement

4. de minimis benefits5. if the grant is required by the nature.6. if it is for the convenience of employer

Accounting for fringe benefits

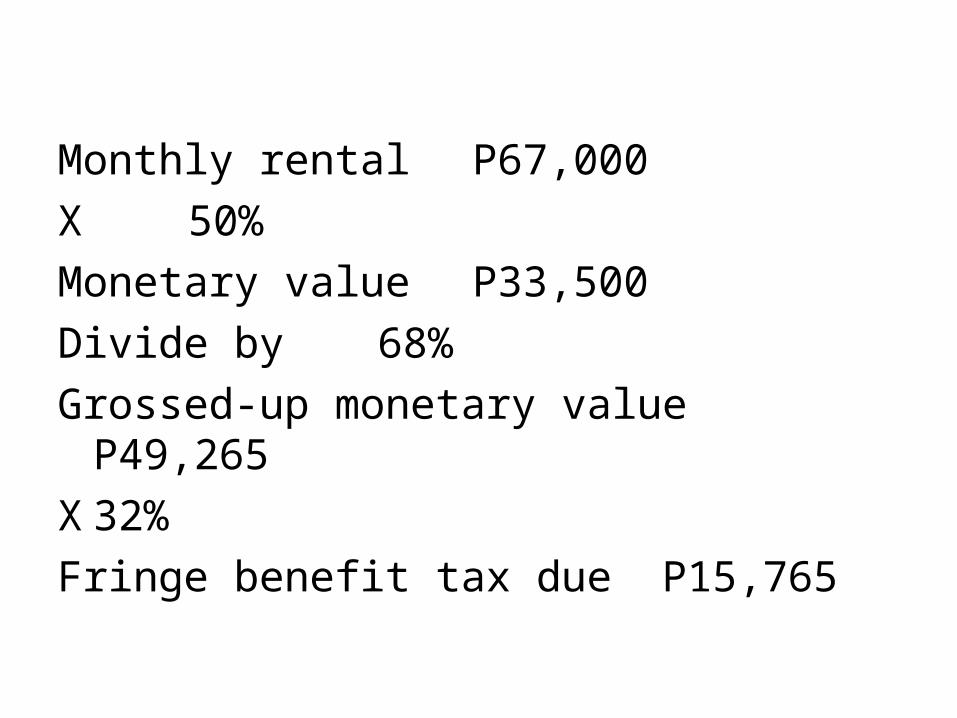

1. During the year 2012, Holiday Corp. paid month rental of a residential house of its branch manager, Mr. AA, amounting to P67,000.Compute the fringe benefit tax due

Monthly rental P67,000X 50%Monetary value P33,500Divide by 68%Grossed-up monetary value P49,265X 32%Fringe benefit tax due P15,765

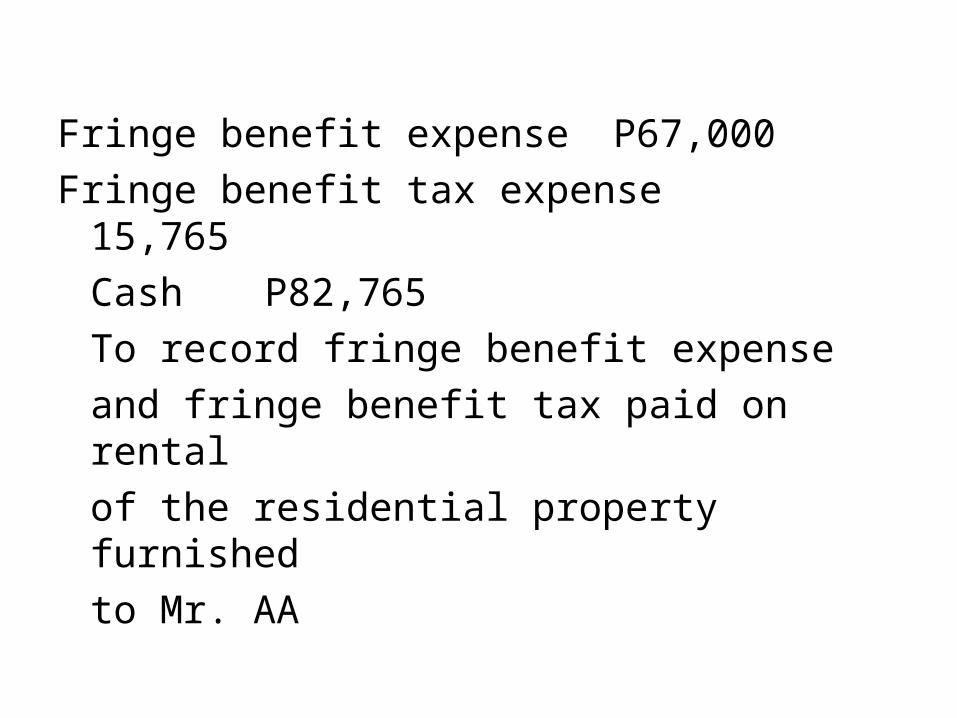

Fringe benefit expense P67,000Fringe benefit tax expense 15,765

Cash P82,765To record fringe benefit expenseand fringe benefit tax paid on rental of the residential property furnishedto Mr. AA

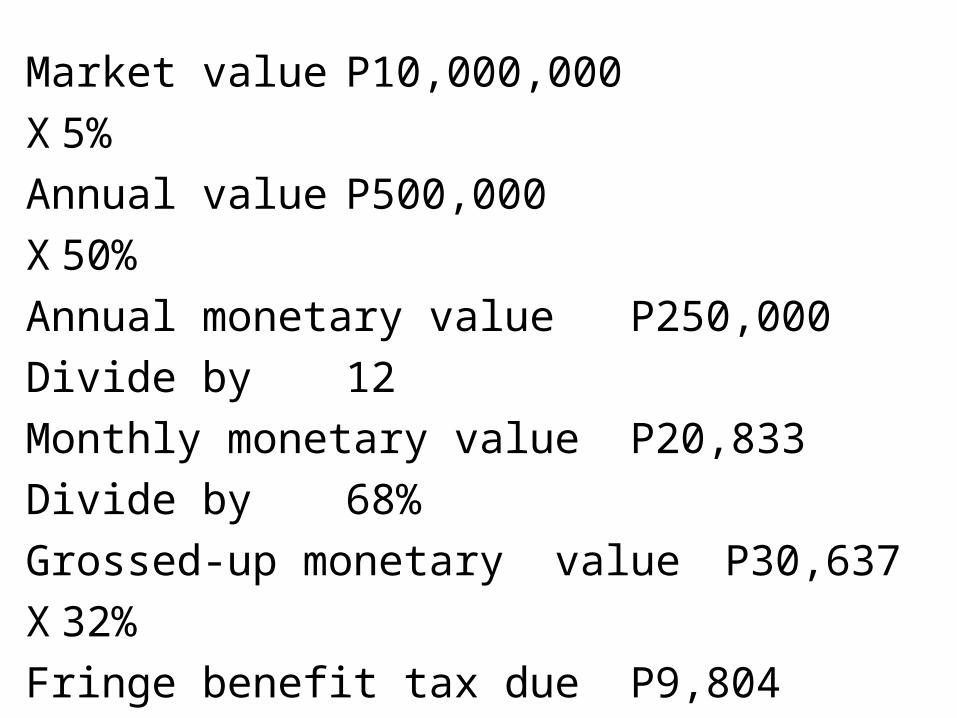

2. Plaza Corp. owns a condominium unit. During the year 2012, the said corporation furnished and granted the said property for residential use of its Senior Vice-President. The fair market value is P10m while its zonal value is P8m.Compute monthly fringe benefit tax due.

Market value P10,000,000X 5%Annual value P500,000X 50%Annual monetary value P250,000Divide by 12Monthly monetary value P20,833Divide by 68%Grossed-up monetary value P30,637X 32%Fringe benefit tax due P9,804

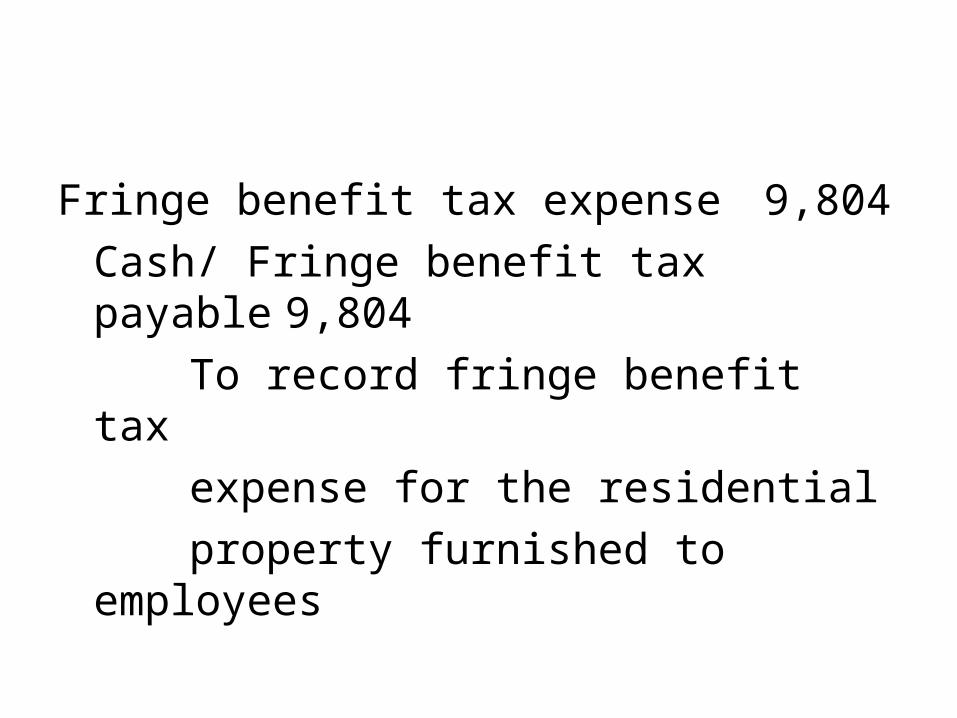

Fringe benefit tax expense 9,804Cash/ Fringe benefit tax payable 9,804

To record fringe benefit taxexpense for the residential property furnished to employees

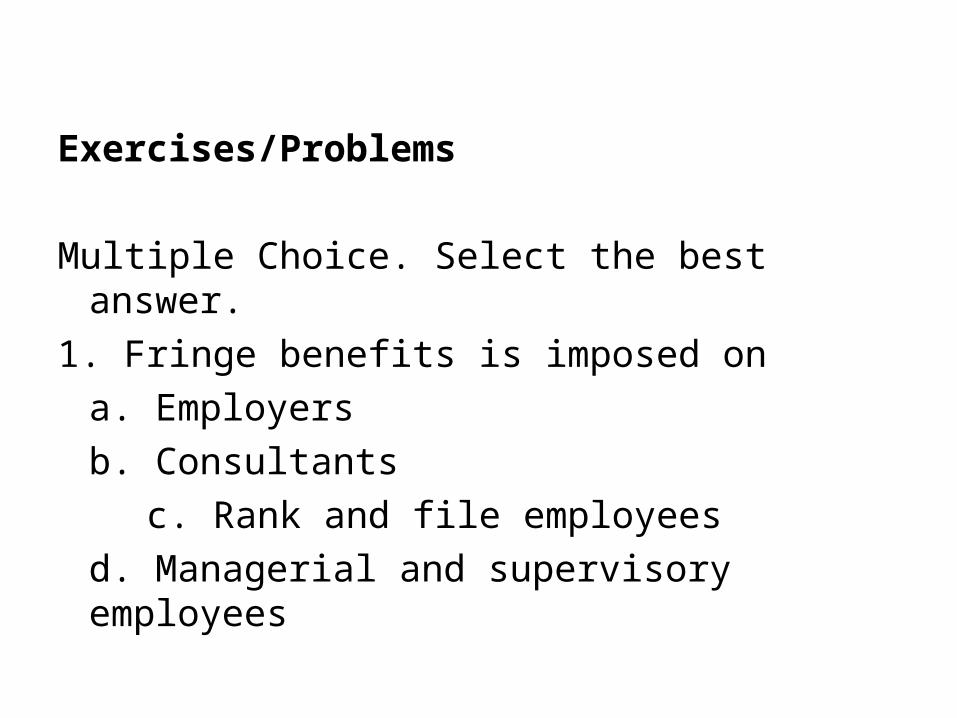

Exercises/Problems Multiple Choice. Select the best answer. 1. Fringe benefits is imposed on

a. Employersb. Consultants

c. Rank and file employeesd. Managerial and supervisory employees

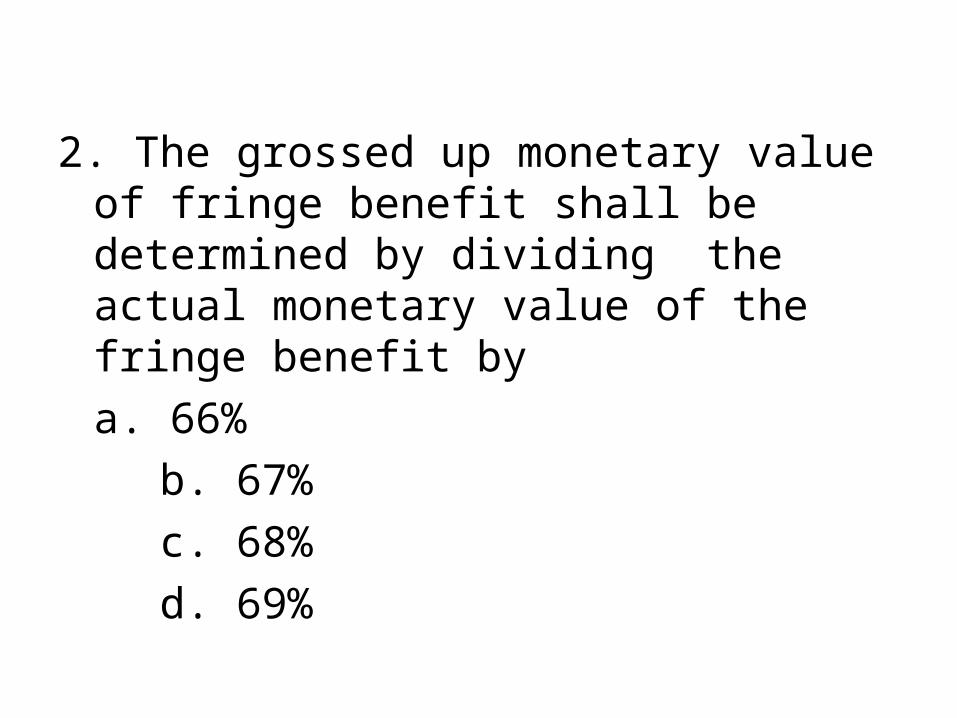

2. The grossed up monetary value of fringe benefit shall be determined by dividing the actual monetary value of the fringe benefit bya. 66%

b. 67% c. 68% d. 69%

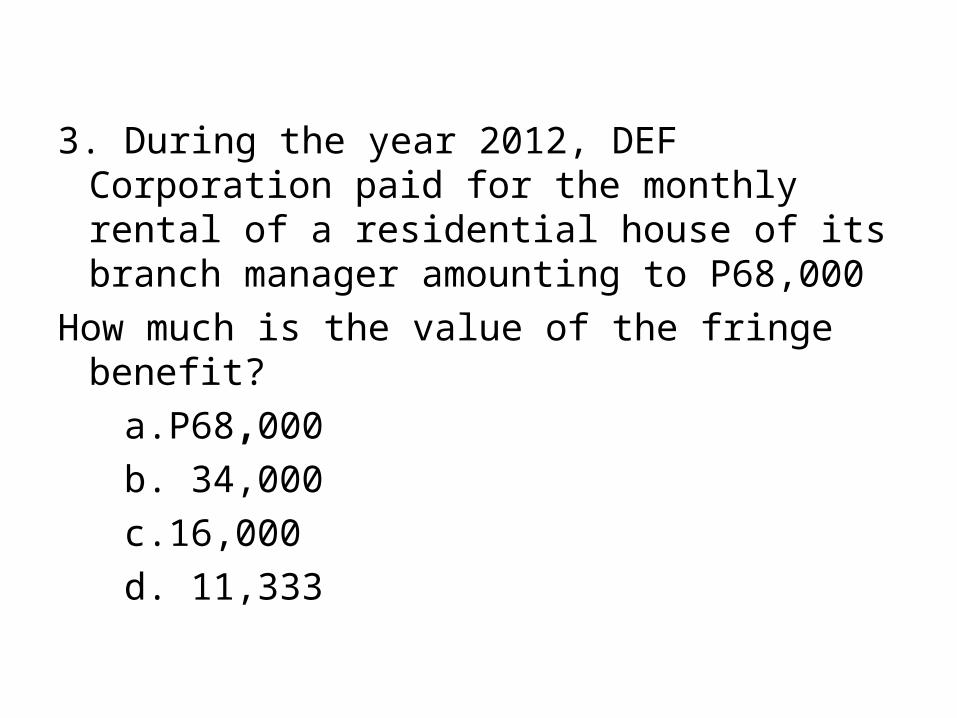

3. During the year 2012, DEF Corporation paid for the monthly rental of a residential house of its branch manager amounting to P68,000

How much is the value of the fringe benefit? a.P68,000 b. 34,000 c.16,000 d. 11,333

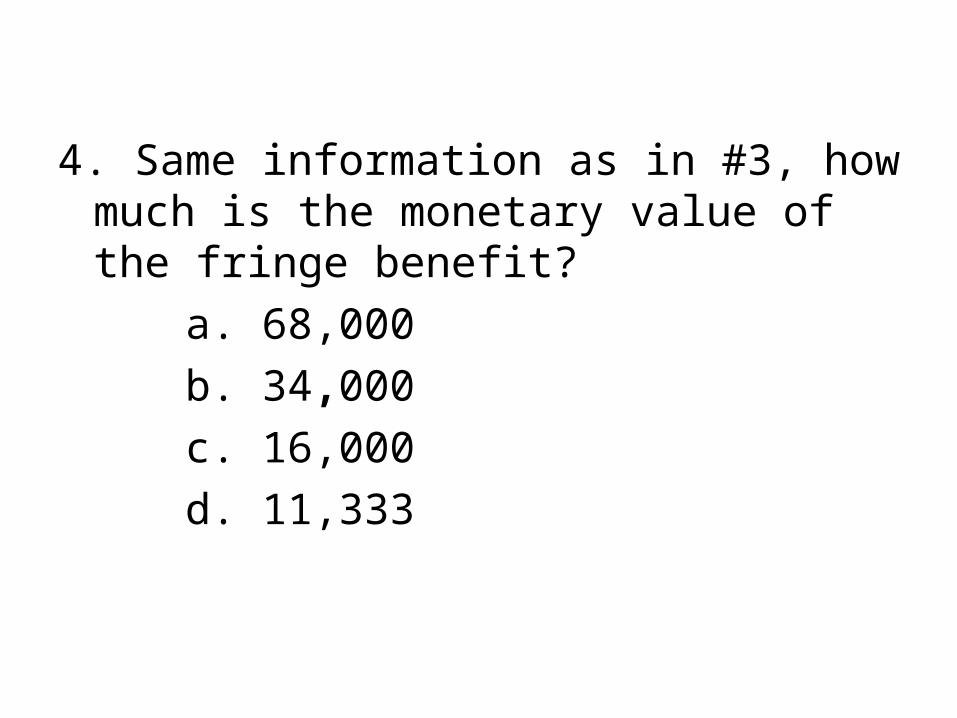

4. Same information as in #3, how much is the monetary value of the fringe benefit?

a. 68,000 b. 34,000 c. 16,000 d. 11,333

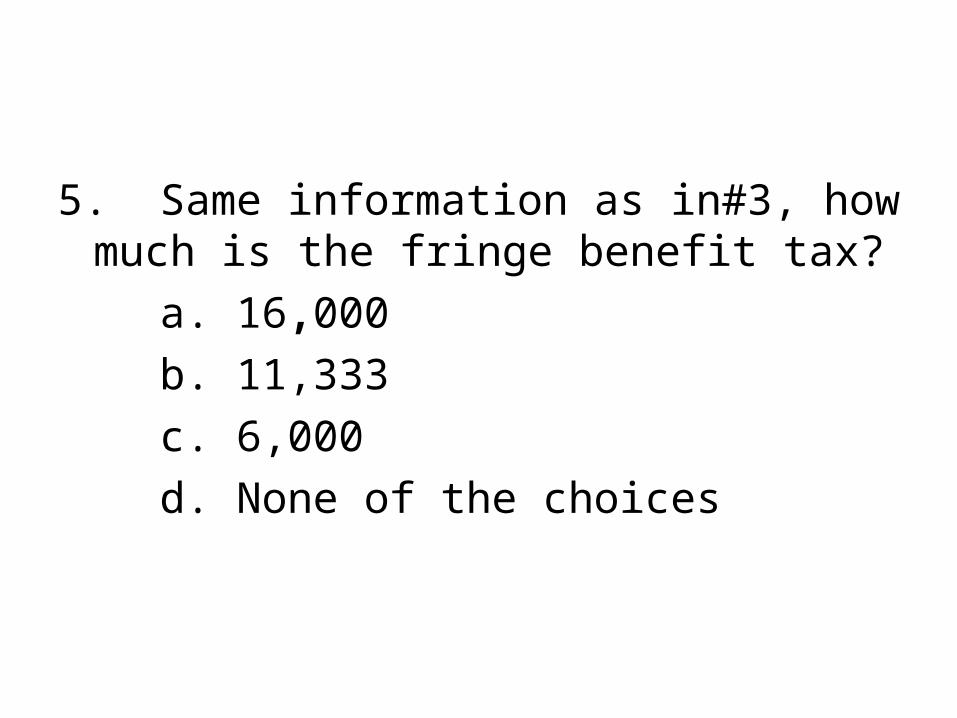

5. Same information as in#3, how much is the fringe benefit tax?

a. 16,000 b. 11,333 c. 6,000 d. None of the choices