Frictions & Macro

28

1 Frictions & Macro Introduction: 1 Frictions: Reasons why markets are not fully efficient 2 Some empirical documentation of frictions 3 Avoiding frictions Topics: 4 Banks 5 Implications of frictions and interaction with aggregate economy

Transcript of Frictions & Macro

1

Frictions & Macro

Introduction:

1 Frictions: Reasons why markets are not fully efficient

2 Some empirical documentation of frictions

3 Avoiding frictions

Topics:

4 Banks

5 Implications of frictions and interaction with aggregate economy

2

• Frictions exist

• Their importance varies over time

• Frictions affect economic performance but economic performance also affects frictions

Key Insights

The Invisible Hand Result

Famous result in economics:

IF

• markets (and associated prices) exist for all goods and services,

• no externalities exist

• nor information asymmetries or market power

• agents maximize their own well being,

THEN

• competitive markets allocate resources efficiently

3

Key Aspects of Credit Contracts

(such as debt & equity)

1. Products are not homogeneous

2. Delivery and payment don’t occur at the same time

Note that when we are talking about the market for equity in this lecture we do not mean the secondary market for equity shares

Wrong View on Firm Finance

Consumers Firms

Intermediaries

4

Better View on Firm Finance

Consumers FirmsIntermediaries

Terminology

Efficient Markets

In economics EM typically means: without frictions/externalities

In finance EM typically means that no returns in excess over a just compensation for risk are possible

⇒ no short-term predictability of stock prices

⇒ stock prices are only influenced by fundamentals

⇒ no irrational bubbles

5

Key Frictions

1. Transaction and search costs, bounded rationality

2. Imperfect information especially asymmetric information

• imperfect info about contract partner’s characteristics; adverse selection

3. Imperfect information about partner’s actions; moral hazard

4. Limits to enforcement; e.g., limited liability and debt finance

5. Controlling the manager and equity finance

Transaction Costs:

Efficient Market Impossibility

• Financial markets are efficient ⇒

• No benefits for anybody to do market research into individual stocks ⇒

• Nobody does research ⇒

• Markets are not efficient

6

Search Costs & Bargaining

• Lenders (banks, venture capitalists, private equity firms) specialize

• Lending capacity of lenders is likely to be constrained from time to time

• Costly for lenders and borrowers to find the right match and this search cost will affect real activity

Small Search Costs

Search costs not only make it costly for borrowers and lenders to find each other but also affect the contracting environment

Suppose:

• Venture capitalists have the bargaining power

• Cost of funds for venture capitalist is 5%

• Reservation interest rate for borrower is known to be 15%

• There is a small cost to contact another venture capitalist

7

Small Search Costs

It would be an equilibrium for each venture capitalists tocharge 15%

• Given that all venture capitalists charge 15% there is no incentive for borrower to pay the small search cost and find another venture capitalist

• The VC knows this and charges 15%

What would break this equilibrium?

Informational Asymmetry

• Entrepreneur has better information about

• Project’s expected return and risk characteristics

• Ways in which the lender can reduce informational asymmetries

• Specialisation (lending to a particular type of firm)

• Long-term relationships

• Punishments ex post: For example, deny future credit in case the borrower misbehaves (but informational problem here too)

• Ingenious set up (For example, Grameen Bank & Insurance Company)

8

Informational Asymmetry

Revelation?

• Suppose a lender faces a number of different borrowers with projects of different risk characteristics

• Everything else equal the bank would rather charge lower rates to the borrowers with the less risky projects

• Suppose the risk characteristics are private information. Will the lender charge everybody the same rate?

• No, not if borrowers can without costs convincingly reveal risk characteristics

Adverse Selection:

Hidden Information & participation decision

Adverse selection determines characteristics of those who want to trade with you; You get to transact with exactly those that are less desirable.

• Insurance is more attractive to those prone to sickness or accidents

• High credit card rates are not much of a problem for borrowers who expect to go bankrupt anyway

• One reason the seller wants to sell his car is that it is a lemon

9

Truth “telling” despite Adverse Selection

Smart contracts may help in revealing the true characteristics or your transaction partner

Suppose an insurance company would like to distinguish between customers that work out and those that don’t work out

Start new insurance program

• annual fee that is $100 more than old program

• free membership to health club worth $200 per year

Moral Hazard – “Hidden” actions

Moral hazard: behaviour changes after transaction

• Borrower may take the money and run

• Borrower may squander the money lent (e.g., buy luxurious corporate yet)

• Borrower may take on more risk

10

IMF & Moral Hazard

The existence of IMF is to some extent comparable to having insurance against default.

• Does this lead to irresponsible lending to emerging markets?

Moral Hazard or Adverse Selection

Volvo drivers are more likely to go through a red light

• Adverse selection interpretation

• Moral hazard interpretation

11

Limited LiabilityEquity = £5m

Debt = £95m (5% interest rate)

Two possible choices

1. Maintain the course; 6% return ⇒ equity increases with £1.25m

2. Change the risk of the operations

• With probability ½ return of -15% ⇒ equity decreases with £5m

• With probability ½ return of +15% ⇒ equity increases with £10.25m

Choice #2 has a much lower expected return (only 0%), but high expected return to shareholders so despite the risk might look attractive to some owners. Moreover, the smaller the amount of equity the more attractive risk becomes

Payoff with Limited LiabilityRisk shifting or asset-substitution

Last period equity + this period’s net profits

Next period

payoff

Negative equity

12

Effect of Risk Taking under Limited Liability

Suppose the following holds in an economy

• cost for the lender is 10%

• some projects have a safe return of 10%

• other projects either have a return of 0% or 15%

• lender cannot distinguish between the two

• low equity

• to break even a debt provider would have to charge more than 10% ⇒ safe projects will not be financed

Are Managers Making the World Efficient?

13

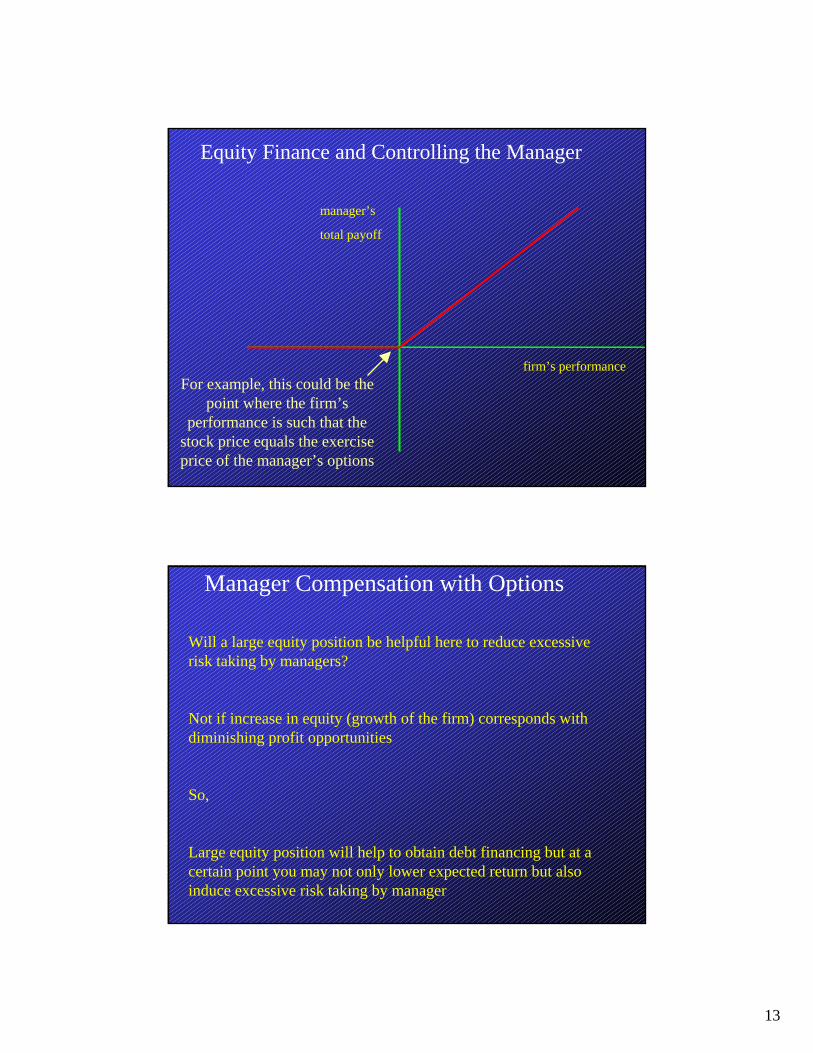

Equity Finance and Controlling the Manager

firm’s performance

manager’s

total payoff

For example, this could be the point where the firm’s

performance is such that the stock price equals the exercise price of the manager’s options

Manager Compensation with Options

Will a large equity position be helpful here to reduce excessiverisk taking by managers?

Not if increase in equity (growth of the firm) corresponds with diminishing profit opportunities

So,

Large equity position will help to obtain debt financing but at a certain point you may not only lower expected return but also induce excessive risk taking by manager

14

Options and Manager Incentives

Arguments why current options do not create right incentives

• No benchmarking, that is, options also pay out if all share prices increase

• Optimal contracting would suggest great variety but options are typically granted with an exercise price equal to current marketprice

• Resetting: Exercise prices are often reset if company’s share price fall

• Managers are allowed to hedge and cash out options as soon as they are vested

Shareholder control

• In Britain a little more than 50% of the shares in the biggest 350 companies are voted

•Why?

• Free rider problem

• In US it is 80% but resolutions are often ignored because they are not binding

• What about large Shareholders?

15

Large Shareholders

• Important to make a distinction between “transparent industries” and “opaque industries”

• Transparent: food processing, petroleum, retail stores, textiles

• Opaque: Aerospace, chemical manufacturing, drugs, semiconductors

Effect of Large Shareholders on E/P

12.812.6Opaque

11.610.1Transparent

without large

shareholder

with large shareholder

A large investor is defined as a single entity owning 15% or more of the outstanding voting stock of the corporation

16

Introduction

This lecture:

1 Frictions: Reasons why markets are not fully efficient

2 Some empirical documentation of frictions

3 Avoiding frictions

Retained Earnings and Investment

Theory

• perfect capital markets ⇒• external funds are a perfect substitute for

internal funds ⇒• investment should not depend on past

earnings, cash flows, or the firm’s financial structure

17

Retained Earnings and Investment

Empirical Evidence

• Fazzari, Hubbard, & Petersen (1988): the firm’s cash flow is an important determinant for future investment (US manufacturing)

• Hoshi, Kashyap, & Scharfstein (1990): the sensitivity of investment to liquidity is less for firms with close bank ties (Japanese data)

Bank Equity

Correlation between bank equity and real activity is positive but does this imply

if bank equity ↓ ⇒ real activity ↓, or

if real activity ↓ ⇒ bank equity ↓, or

both?

• That real activity affects bank equity is pretty obvious but the following empirical study shows that bank equity also affects real activity

18

Effects of the Japanese Banking Crises

during early ’90s on US Real Estate

• Second half of the 80’s: Japanese banks penetrated US market for mortgages especially in California, Illinois, and New York

• Early 90’s: Plunging real-estate prices in Japan caused Japanese banks to withdraw funds from the US

• In a perfect capital market real-estate construction in regions with heavy penetration should not behave differently than construction in the other regions

• Peek and Rosengren (2000): Real-estate construction in regions with a large degree of Japanese penetration was affected

Introduction

This lecture:

I.1 Frictions: Reasons why markets are not fully efficient

I.2 Some empirical documentation of frictions

I.3 Avoiding Frictions

- clever contracting

- relationships

- laws?

19

Ingenuity and Alleviating Frictions

• Problem for lenders in developing countries:

• bad information about quality of borrower

• hard to enforce contracts and motivate borrower

• borrowers don’t have collateral

Grameen Bank of Bangladesh

Micro lending

• Lends to about two million people

• No collateral (because the borrowers don’t have any)

• Rural projects (poultry, handloom weaving, dairy farming, tea shops)

• As in the example earlier there are safe and risky projects and rates charged by moneylenders are too high for many decent projects

20

Grameen Bank of Bangladesh

Properties of the Grameen bank’s loans

• Borrowers organize themselves into self-selected groups of about five people from the same village

• Joint liability

• If any member of the group defaults then all members are ineligible for future credit

• Regular payments

• Promise of repeat lending if borrowers perform well

Networking: Black Ties OnlyIn NYC African Americans own few businesses, not only relative to whites but also to other minorities such as Asians and Caribbean Americans

Fraction of firms that use debt capital at start up:

•69% for Korean-immigrant-owned firms

•40% for black-owned firms

Fraction of firms for whom friends were a major provider of debt funding:

• 25% for Korean-immigrant-owned firms

• 11% for black-owned firms

21

Networking: Black Ties Only

Caribbean Business Organization:

• > 1,300 members

• business resource centre

• seminars

• trade missions

• power breakfasts

• website: http://www.cacci.org/

No equivalent African American organization

VietnamMcMillan and Woodruff survey

• 259 firms in Hanoi (’95-’96) and Ho Chi Minh City (’97)

• 91% of survey respondents said courts could not enforce contract

Still booming private sector with trade credit

• Threat of cutting future supply helps; borrowers that lack alternative suppliers will receive more trade credit

• Suppliers belonging to a network with other suppliers extend more trade credit

• Firms run into problems when they get bigger and have to deal with suppliers from different cities

22

Laws and Regulations

Many laws to limit (the harmful effects of) frictions

Many laws increase frictions including some intended to limit frictions

Laws and Regulations

1720 Bubble Act

•in response to increase in stock price of South Sea Company

•required joint-stock companies to have royal charter

•Glass-Steagall Act

•in response to crash of 1929

•split of commercial banking and securities dealing

•Basle I (early 90’s)

•in response to decades of bank troubles

•restricts the amount of loans relative to bank equity

23

Credit and State Bankruptcy Laws in the U.S.

Berkowitz and White (2002)

• study small firms (< 500 employees)

• note that small firms were responsible for 76.5% of all new jobs over the period from ’90 to ’95.

• if the state allows a higher bankruptcy exemption ⇒

• a firm is more likely to be denied credit

• received loans are smaller

• interest rates are higher

Minimizing Frictions During CrisesImportance of Flexibility in Regulations

24

Importance of Flexibility in Regulations

October 1987 crash and the FED’s actions?

• Lowered the funds rate from 7.5% to 6.5%

• Liberalized the rules governing the lending of securities from the FED’s portfolio to make more collateral available

• Intense communication with banks to stress that banks had to ensure the liquidity of their clients

• Placed monitors in major banking institutions to gather real-time information and identify potential for bank runs

I would like to acknowledge the help of my friends at the Federal Reserve Bank of New York, Dino Kos, Spence Hilton and Peter Bakstansky, for explanations, data and photographs.

25

Summary

• Firm finance comes with frictions.

• Limited liability is key for debt financing

• Moral hazard is key for equity financing

• More net worth helps reduce frictions in obtaining debt financing but this may not be easy in times of distress and high leverage may help to reduce moral hazard problem with managers

• These frictions are more likely to be important during economic downturns and in industries with low surplus values

Extra Material

• Truth revelation in the presence of private information

26

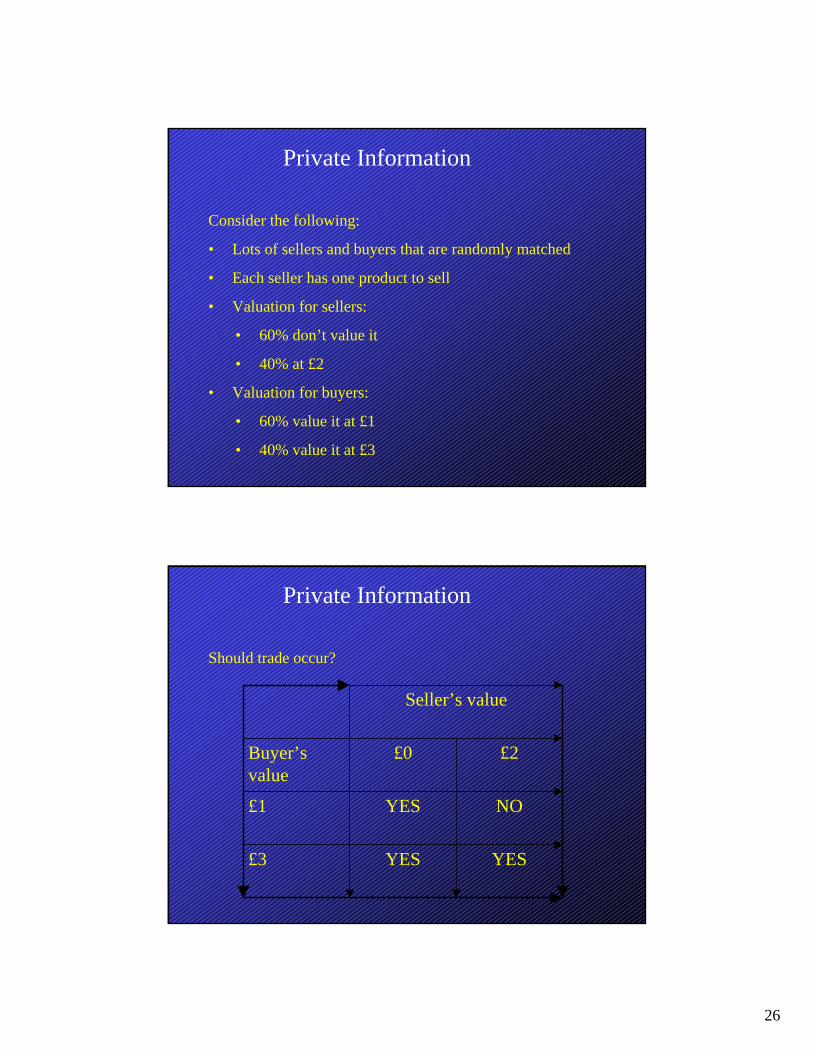

Private Information

Consider the following:

• Lots of sellers and buyers that are randomly matched

• Each seller has one product to sell

• Valuation for sellers:

• 60% don’t value it

• 40% at £2

• Valuation for buyers:

• 60% value it at £1

• 40% value it at £3

Private Information

Should trade occur?

YESYES£3

NOYES£1

£2£0Buyer’s value

Seller’s value

27

Private InformationAre prices possible that induce truth telling and efficient trading? Sometimes yes.

trade At £2

trade at p

£3

No tradetrade at £1

£1

£2£0Buyer reportedvalue

Value reported by seller

Private Information: Truth tellingAre prices possible that induce truth telling and efficient trading? Sometimes yes.

No overreporting by seller (£0 guy claiming to be £2 guy)

Honesty > Dishonesty

0.6*(£1-£0) + 0.4*(p-£0) > 0.6*0 + 0.4*(£2-£0)

No underreporting by buyer (£3 guy claiming to be £1 guy)

Honesty > Dishonesty

0.6*(£3-p) + 0.4*(£3-£2) > 0.6*(£3-£1) + 0.4*0

28

Private Information: Truth tellingAre prices possible that induce truth telling and efficient trading? Sometimes yes.

No overreporting by seller (£0 guy claiming to be £2 guy)

p > 0.5

No underreporting by buyer (£3 guy claiming to be £1 guy)

p < 1.6667

![Macroeconomics and financing frictions, [lectures 2 and 3]. Part 1: crisis narrative and the thieving banker model Lecture to MSc Advanced Macro Students,](https://static.fdocuments.net/doc/165x107/56649e855503460f94b87ec3/macroeconomics-and-financing-frictions-lectures-2-and-3-part-1-crisis.jpg)