Franchise and Excise Tax Manual - Tennessee

581

Franchise and Excise Tax Manual March 2021

Transcript of Franchise and Excise Tax Manual - Tennessee

Franchise and Excise Tax Manual

March 2021

2 | P a g e

Contents

Chapter 1: Introduction ............................................................................................................................18

History .....................................................................................................................................................18

Overview .................................................................................................................................................18

1. Entities Subject to Franchise & Excise Taxes .........................................................................19

2. Rates and Impositions ..............................................................................................................19

3. Credits ........................................................................................................................................20

4. Exemptions ................................................................................................................................20

Chapter 2: Persons Subject to Tax and Exemptions .............................................................................21

Entities Not Subject to Franchise and Excise Tax ..............................................................................21

1. Sole Proprietorships .................................................................................................................21

2. General Partnerships ...............................................................................................................21

3. Not-for-Profits ...........................................................................................................................21

4. SMLLC Owned by Pension Trust .............................................................................................22

Entity Exemptions..................................................................................................................................22

1. Franchise and Excise Tax Exemptions ...................................................................................22

2. Exemptions Requiring an Evaluation .....................................................................................23

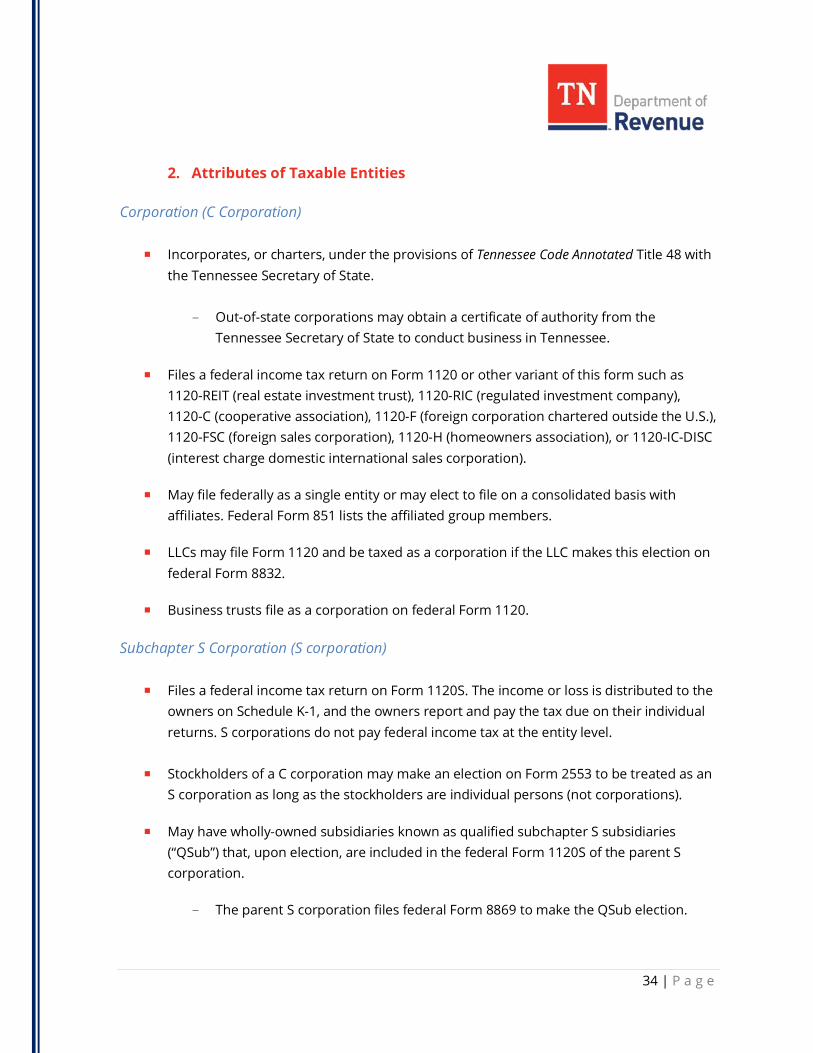

Taxable Entities ......................................................................................................................................32

1. Types of Taxable Entities .........................................................................................................32

2. Attributes of Taxable Entities ..................................................................................................34

Entity Formation ....................................................................................................................................37

Entity Classification ...............................................................................................................................39

1. Classification for Franchise and Excise Tax Purposes..........................................................39

2. Federal Default Classification ..................................................................................................39

3. State Classification of SMLLC ..................................................................................................40

4. Federal Election to be Treated as a Corporation ..................................................................40

Out-of-State Businesses Responding to State Declared Disaster or Emergency .........................41

Chapter 3: Nexus .......................................................................................................................................42

3 | P a g e

Overview .................................................................................................................................................42

1. Doing Business in Tennessee ..................................................................................................42

2. Substantial Nexus .....................................................................................................................44

Entity Specific Nexus .............................................................................................................................46

1. Trucking Companies .................................................................................................................46

2. Foreign Corporations ...............................................................................................................47

3. Financial Institutions ................................................................................................................48

Due Process and Commerce Clause ...................................................................................................50

Nexus-Related Issues ............................................................................................................................51

1. Ownership Interests Do Not Create Nexus ...........................................................................51

2. Standard for Nexus and Right to Apportion .........................................................................52

Public Law 86-272 ..................................................................................................................................53

1. Overview ....................................................................................................................................53

2. Unprotected vs. Protected Activities ......................................................................................55

Chapter 4: Identifying the Proper Franchise and Excise Taxpayer .....................................................60

Separate Single-Entity Reporting.........................................................................................................60

1. Exceptions to Separate Single-Entity Reporting ...................................................................61

2. Tax Implications of Single Filer Returns vs. Consolidated Return ......................................61

3. Direct Taxation of Pass-Through Entities ..............................................................................61

Disregarded Entities ..............................................................................................................................62

1. Corporations Formed Under State Law .................................................................................63

2. Default Classification ................................................................................................................63

3. Election to be Taxed as a Corporation ...................................................................................63

Organizational Structure – Role in an Audit ......................................................................................64

1. Pre-Audit Evaluation .................................................................................................................64

2. Organizational Chart Symbols ................................................................................................65

Special Circumstances ..........................................................................................................................66

1. Multimember LLC .....................................................................................................................66

2. Series LLCs .................................................................................................................................68

4 | P a g e

Disregarded Entities – Federal vs. State Rules ..................................................................................69

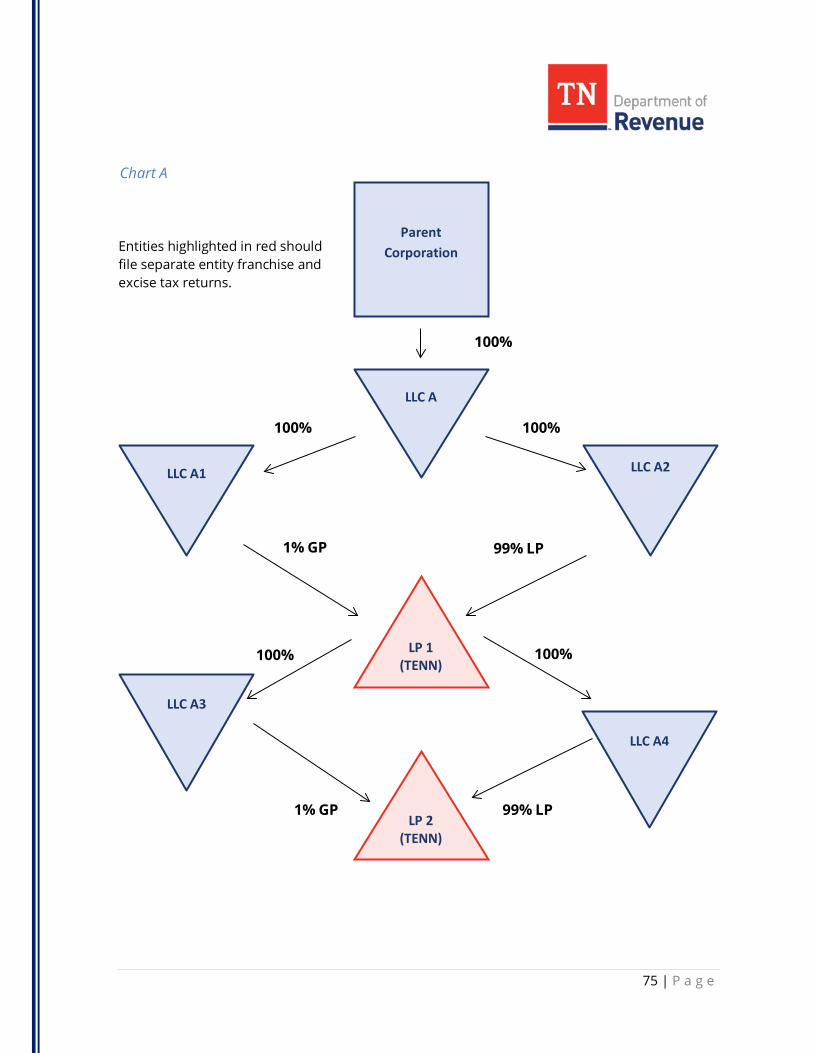

Additional Examples of Complex Disregarded Business Structures ..............................................72

1. Scenario One .............................................................................................................................72

2. Scenario Two .............................................................................................................................72

3. Revenue Ruling 11-46 – Disregarded Entities and Filing Requirements ...........................74

4. Revenue Ruling 11-53 - Disregarded Entities and Filing Requirements ............................77

Chapter 5: Filing Requirements ...............................................................................................................80

Registration ............................................................................................................................................80

Electronic Filing ......................................................................................................................................80

Filing Period............................................................................................................................................80

1. Annual Returns ..........................................................................................................................81

2. Short-Period Returns ................................................................................................................82

3. Foreign Entities Newly Subject to Franchise and Excise Tax ...............................................83

Filing Due Dates .....................................................................................................................................83

1. Calendar Year, Fiscal Year, and Short-Period Filers .............................................................83

2. 52-53 Week Filers ......................................................................................................................84

3. Filing Extension .........................................................................................................................84

4. Estimated Assessment .............................................................................................................85

Change in Ownership - Filing Periods and Due Dates ......................................................................86

Franchise Tax Proration and Annualizing Rents ...............................................................................87

1. Proration ....................................................................................................................................87

2. Annualizing Rents .....................................................................................................................87

Final Returns ..........................................................................................................................................89

1. “True” Final Return ....................................................................................................................89

2. Liquidation and Tax Base Calculation ....................................................................................90

3. Tax Clearance ............................................................................................................................93

4. Tax Collection ............................................................................................................................95

5. Events Not Resulting in a Final Return ...................................................................................95

6. Corporate Reorganizations......................................................................................................98

5 | P a g e

Estimated Tax Payments ................................................................................................................... 100

1. Estimated Payment Requirement........................................................................................ 100

2. Quarterly Estimated Payment Amount ............................................................................... 100

3. Remitting Payments .............................................................................................................. 101

4. Payment Due Dates ............................................................................................................... 102

Penalties .............................................................................................................................................. 102

1. Penalties and Penalty Rates ................................................................................................. 102

2. Penalty Waiver ........................................................................................................................ 105

Interest ................................................................................................................................................. 107

Delinquent Accounts .......................................................................................................................... 107

Statute of Limitations......................................................................................................................... 108

1. Assessments ........................................................................................................................... 108

2. Refunds ................................................................................................................................... 108

3. Statute Waivers ...................................................................................................................... 110

Records Maintenance ........................................................................................................................ 110

Assessment ......................................................................................................................................... 110

Chapter 6: Federal Income Tax Returns and Filings .......................................................................... 111

Corporations ....................................................................................................................................... 111

1. Consolidated Group Election, Form 851 & Subsidiary Statements ................................. 111

2. Capital Loss ............................................................................................................................. 113

3. Capital Gain Net Income ....................................................................................................... 113

4. Dividends and Inclusions ...................................................................................................... 114

5. Exempt Interest Income ........................................................................................................ 114

6. Other Income ......................................................................................................................... 114

7. Charitable Contributions ...................................................................................................... 114

8. Balance Sheet ......................................................................................................................... 114

9. Reconciliation of Income (Loss) per Books with Income per Return .............................. 115

S-corporations .................................................................................................................................... 115

Corporations Charted Outside the United States .......................................................................... 117

6 | P a g e

Partnerships ........................................................................................................................................ 117

Limited Liability Company (LLC) ....................................................................................................... 119

Single Member LLC ............................................................................................................................ 119

Other Federal Forms .......................................................................................................................... 119

1. Form 940 ................................................................................................................................. 119

2. Form 1125-A ........................................................................................................................... 120

3. Form 4562 ............................................................................................................................... 120

4. Form 4797 ............................................................................................................................... 121

5. Form 6252 ............................................................................................................................... 121

6. Form 7004 ............................................................................................................................... 121

7. Form 8594 ............................................................................................................................... 122

Chapter 7: Federal Income Revisions .................................................................................................. 123

General Discussion............................................................................................................................. 123

Statute of Limitations - FIR ................................................................................................................ 125

Audit Procedures ................................................................................................................................ 126

Chapter 8: Business and Nonbusiness Earnings ................................................................................ 128

Introduction ........................................................................................................................................ 128

1. Allocation Methodology for Nonbusiness Earnings .......................................................... 129

2. Audit Adjustments when Nonbusiness Earnings are Reclassified .................................. 131

Business Earnings .............................................................................................................................. 131

1. Transactional and Functional Tests ..................................................................................... 132

2. Rule 23 – Business and Nonbusiness Earnings ................................................................. 134

Nonbusiness Earnings ....................................................................................................................... 138

1. Nonbusiness Earnings Examples ......................................................................................... 138

2. Expenses Related to Nonbusiness Earnings ...................................................................... 139

Tax Impact of Earnings Classification .............................................................................................. 139

Unitary Earnings ................................................................................................................................. 140

1. Legal Analysis ......................................................................................................................... 141

2. Example – Nonunitary Business .......................................................................................... 143

7 | P a g e

Litigation – Unitary Business Principle ............................................................................................ 143

1. Finding: Nonunitary ............................................................................................................... 143

2. Finding: Unitary Business Earnings ..................................................................................... 144

Audit Procedures ................................................................................................................................ 146

Chapter 9: Franchise Tax ....................................................................................................................... 148

Overview .............................................................................................................................................. 148

1. Who Must File? ....................................................................................................................... 148

2. Minimum Franchise Tax ........................................................................................................ 148

3. Franchise Tax Base ................................................................................................................ 149

4. Minimum Measure (Schedule G) ......................................................................................... 149

5. Manufacturers’ Franchise Tax Base..................................................................................... 149

6. GAAP Books and Records ..................................................................................................... 150

Non-Consolidated Net Worth – Schedule F1 .................................................................................. 150

1. Net Worth................................................................................................................................ 150

2. Affiliated Indebtedness ......................................................................................................... 154

3. Net Worth Apportionment ................................................................................................... 160

Consolidated Net Worth – Schedule F2 ........................................................................................... 160

1. Overview ................................................................................................................................. 160

2. Affiliated Group Members .................................................................................................... 161

3. Consolidated Net Worth Computation ............................................................................... 164

4. Apportionment of Consolidated Net Worth ....................................................................... 167

5. Verifying Affiliated Group Members .................................................................................... 175

6. Other Issues ............................................................................................................................ 183

7. Audit Procedures ................................................................................................................... 184

Chapter 10: Property Valuation ............................................................................................................ 189

Overview .............................................................................................................................................. 189

1. Property Included .................................................................................................................. 189

2. Property Excluded.................................................................................................................. 190

3. Property Exempted ................................................................................................................ 191

8 | P a g e

Property Owned ................................................................................................................................. 191

1. Land and Buildings ................................................................................................................ 192

2. Leasehold Improvements ..................................................................................................... 192

3. Depreciable Property ............................................................................................................ 193

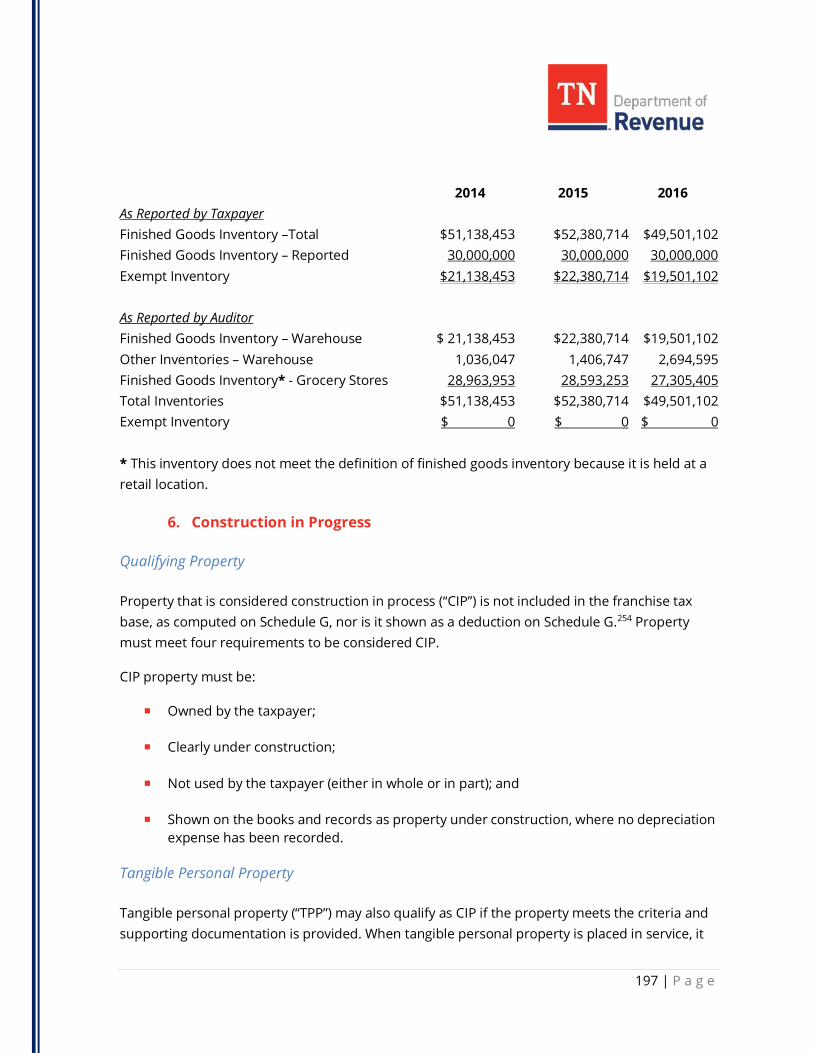

4. Prepaid Supplies .................................................................................................................... 195

5. Inventory ................................................................................................................................. 195

6. Construction in Progress ...................................................................................................... 197

7. Exempt Certified Pollution Control Equipment ................................................................. 203

8. Exempt Certified Green Energy Production Facility .......................................................... 203

9. Exempt Required Capital Investment ................................................................................. 203

10. Federal Repair Regulations .............................................................................................. 204

Property Rented or Leased ............................................................................................................... 206

1. Property Multiples ................................................................................................................. 207

2. Sub-Rents ................................................................................................................................ 208

3. “In Lieu” of Rents .................................................................................................................... 210

4. Rents that Include a Service ................................................................................................. 211

5. Distinguishing Between Leases and Licenses .................................................................... 214

6. Annualize Rent in Short Period ............................................................................................ 217

7. Termination Fees, Renewals, and Software Fees .............................................................. 218

8. Common Lease Terms .......................................................................................................... 218

9. Operating and Finance Leases ............................................................................................. 221

10. Industrial Development Corporation .............................................................................. 227

Ownership in a General Partnership ............................................................................................... 227

1. Owned Property Held by a General Partnership ............................................................... 228

2. Property Leased by a General Partnership ........................................................................ 229

3. Audit – Ownership of a General Partnership ..................................................................... 230

Ownership in a Pass-through Entity Not Subject to the Tax ........................................................ 231

Property Used and Neither Owned nor Rented............................................................................. 231

Chapter 11: Excise Tax ........................................................................................................................... 233

9 | P a g e

Overview .............................................................................................................................................. 233

Recent Form Changes ........................................................................................................................ 234

Partnerships - Schedule J1 ................................................................................................................ 235

1. Addition - Ordinary Income (Loss) from Form 1065 ......................................................... 235

2. Addition - Income Items Specifically Allocated to Partners, Including Guaranteed Payments ......................................................................................................................................... 235

3. Addition - Any Net Loss or Expense Distributed to a Publicly Traded REIT ................... 237

4. Deduction - Expense Items Specifically Allocated to Partners......................................... 238

5. Deduction - Amount Subject to Self-employment Taxes Distributable or Paid to Each Partner or Member ........................................................................................................................ 239

6. Deduction - Amount of Contribution, Not Previously Deducted, to Qualified Pension or Benefit Plans of any Partner or Member, Including all I.R.C. 401 Plans ................................. 241

7. Deduction - Any Loss on the Sale of an Asset Sold within 12 Months after the Date of Distribution ..................................................................................................................................... 242

Single-Member LLC Filing as Individual – Schedule J2 ................................................................... 243

1. Addition - Net Profit or Loss ................................................................................................. 244

2. Addition - Capital Gains or Losses ....................................................................................... 244

3. Addition - Rental Real Estate and Royalty Income or Loss ............................................... 244

4. Addition - Profit or Loss from Farming ............................................................................... 245

5. Addition - Ordinary Gain or Loss – Depreciable Property ................................................ 245

6. Deduction – Amount Subject to Self-Employment Taxes Distributable or Paid to the Single Member................................................................................................................................ 245

Subchapter S-Corporations – Schedule J3 ...................................................................................... 246

1. Addition/Deduction - Income and Expense Items as if no “S” Election .......................... 246

2. Deduction - Any Loss on the Sale of an Asset Sold within 12 Months after the Date of Distribution ..................................................................................................................................... 246

Schedule J4 – Corporations and Other Entities .............................................................................. 246

1. Addition - Domestic Production Activities Deduction (2017) ........................................... 247

2. Addition/Deduction - Contributions .................................................................................... 248

3. Addition - Capital Gains Offset by Capital Losses .............................................................. 249

10 | P a g e

4. Deduction - Capital Loss, Deduction ................................................................................... 249

Schedule J Computation of Net Earnings Subject to Excise Tax - All Entity Types ..................... 251

1. Schedule J, Line 1 – Federal Income (Loss) ......................................................................... 252

2. Addition – Intangible Expense .............................................................................................. 252

3. Addition - Bonus Depreciation ............................................................................................. 254

4. Addition - Gain on the Sale of a Distributed Asset & Repatriated and GILTI Adjustment (2018) ............................................................................................................................................... 261

5. Addition – Tennessee Excise Tax Deducted on Federal Return ...................................... 264

6. Addition - Gross Premiums Tax ........................................................................................... 264

7. Addition - Interest Income of States and Political Subdivisions ...................................... 265

8. Addition - Depletion............................................................................................................... 267

9. Addition – Excess Fair Market Value over Book Value of Property Donated ................. 268

10. Addition – Excess Rent to/from an Affiliate .................................................................... 270

11. Addition – Net Loss or Expense Received from a Pass-through Entity Subject to the Excise Tax ........................................................................................................................................ 272

12. Amount Equal to Five Percent of IRC Section 951A Global Intangible Low-Taxed Income ............................................................................................................................................. 275

13. Business Interest Expense ................................................................................................ 275

14. Total Additions ................................................................................................................... 275

15. Deduction – Depreciation ................................................................................................. 275

16. Deduction – Excess Gain/Loss on Asset with Bonus Depreciation ............................. 276

17. Deduction – Dividends Received ..................................................................................... 276

18. Deduction – Donations to Qualified Public School Support Groups and Nonprofit Organizations.................................................................................................................................. 277

19. Deduction – Federal Expense Reduction Related to Federal Credit ........................... 278

20. Deduction - Safe Harbor Lease ........................................................................................ 281

21. Deduction – Nonbusiness Earnings ................................................................................ 282

22. Deduction – Intangible Expense Paid to an Affiliate ..................................................... 282

23. Deduction – Intangible Income ........................................................................................ 283

11 | P a g e

24. Deduction – Net Gain or Income Received from a Pass-through Entity Subject to the Excise Tax ........................................................................................................................................ 283

25. Deduction – Grants (2018) ................................................................................................ 284

26. IRC Section 951A Global Intangible Low-Taxed Income ............................................... 284

27. Business Interest Expense ................................................................................................ 285

28. Calculated Amounts .......................................................................................................... 286

Ownership of a Pass-through Entity ................................................................................................ 286

Tax Cuts and Jobs Act of 2017 (TCJA) ............................................................................................... 288

1. Interest Expense Limitation .................................................................................................. 288

2. State Grants ............................................................................................................................ 289

3. Repatriated Earnings for 2017 ............................................................................................. 289

4. Repatriated Earnings and Global Intangible Low-Taxed Income, beginning in 2018 ... 290

M-3 and M-1 Federal Schedules ....................................................................................................... 292

1. Schedule M-3 .......................................................................................................................... 293

2. Chart of Schedule J4, J Adjustments .................................................................................... 295

Like-Kind Exchanges .......................................................................................................................... 297

1. Overview ................................................................................................................................. 297

2. Federal Tax Mechanics .......................................................................................................... 297

3. Excise Tax Implications ......................................................................................................... 303

4. Apportionment Implications ................................................................................................ 306

5. Franchise Tax Implications ................................................................................................... 307

6. Appendix (Like-Kind Exchanges) – Federal Forms and Schedules .................................. 308

Chapter 12: Net Operating Losses ....................................................................................................... 318

Schedule K – Loss Carryover ............................................................................................................. 318

Schedule U – Loss Carryover ............................................................................................................ 318

Audit Adjustments to Carryover Schedules .................................................................................... 319

Survivability of NOLs .......................................................................................................................... 321

1. Successors and “Shell” Entities ............................................................................................. 321

2. Unitary Groups of Financial Institutions ............................................................................. 322

12 | P a g e

3. Conversion from Corporation to SMLLC Owned by Non-Shell Parent Corporation .... 322

4. “F” Reorganization – U.S.C. §368(a)(1)(F) ............................................................................. 322

5. Dissolution of Affiliate ........................................................................................................... 323

6. Loss Generated by Taxpayer Making an Entity Election ................................................... 323

7. “338(h)(10)” Election Deemed Existence of Two Corporations ........................................ 323

Audit Procedures – Loss Carryovers ................................................................................................ 324

Chapter 13: Discharge of Indebtedness Income ................................................................................ 325

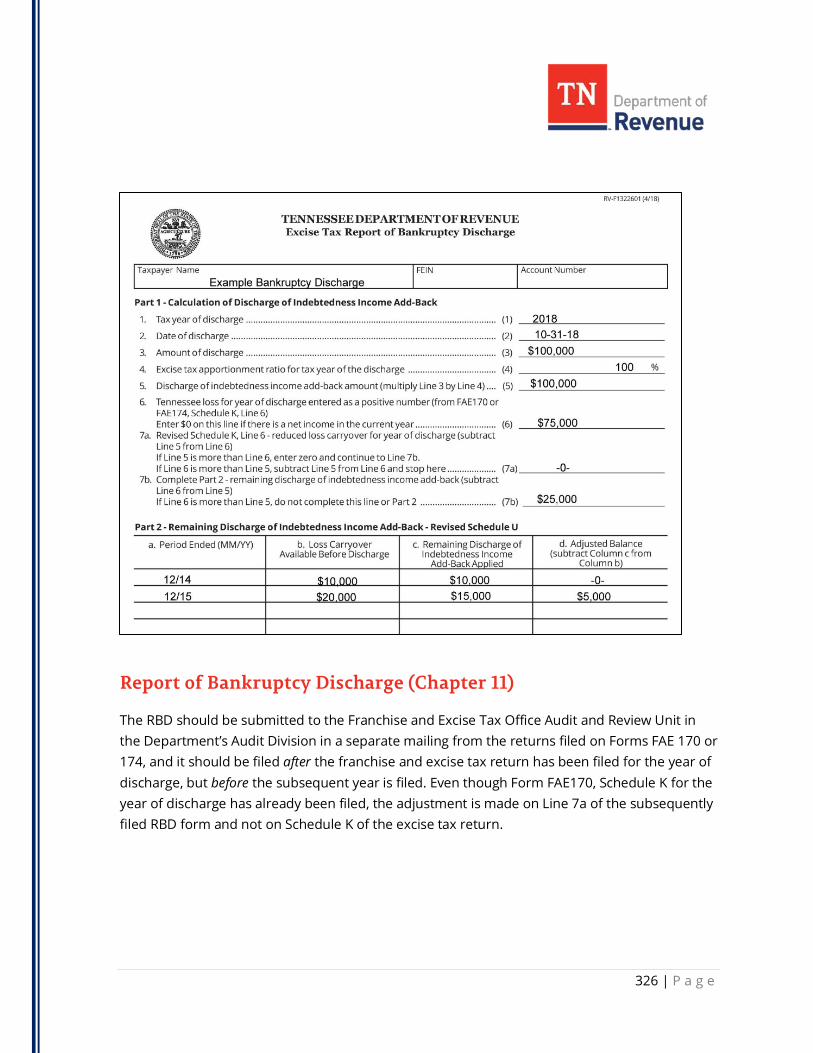

Summary ............................................................................................................................................. 325

Example – Discharge of Debt ............................................................................................................ 325

Report of Bankruptcy Discharge (Chapter 11) ............................................................................... 326

Federal Treatment (Chapter 11) ....................................................................................................... 327

GAAP Accounting Treatment (Chapter 11) ...................................................................................... 328

Audit Procedures – Discharge of Indebtedness ............................................................................. 329

Chapter 14: Apportionment .................................................................................................................. 330

Introduction to Tax Apportionment................................................................................................. 330

1. Allocation (Nonbusiness Earnings) Versus Apportionment (Business Earnings) .......... 330

2. Right to Apportion ................................................................................................................. 331

3. Public Law 86-272 .................................................................................................................. 332

Forms – Apportionment .................................................................................................................... 332

Apportionment Ratio Calculation ..................................................................................................... 333

1. Standard Apportionment – Schedule N .............................................................................. 333

2. Elective Apportionment for Certain Taxpayers.................................................................. 334

3. Consolidated Net Worth Apportionment ........................................................................... 337

Pass-through Entity Ownership ........................................................................................................ 338

Standard Apportionment Factors - Property, Payroll, and Sales ................................................. 340

1. Property Factor ...................................................................................................................... 340

2. Payroll Factor .......................................................................................................................... 346

3. Sales Factor ............................................................................................................................. 360

Variances from the Standard Apportionment Formula ................................................................ 412

13 | P a g e

Special Apportionment for Common Carriers ............................................................................... 413

1. Schedule O – Apportionment – Common Carriers ............................................................ 414

2. Schedule P – Apportionment – Air Carriers ........................................................................ 416

3. Schedule R – Apportionment – Air Express Carriers ......................................................... 416

Apportionment Examples ................................................................................................................. 416

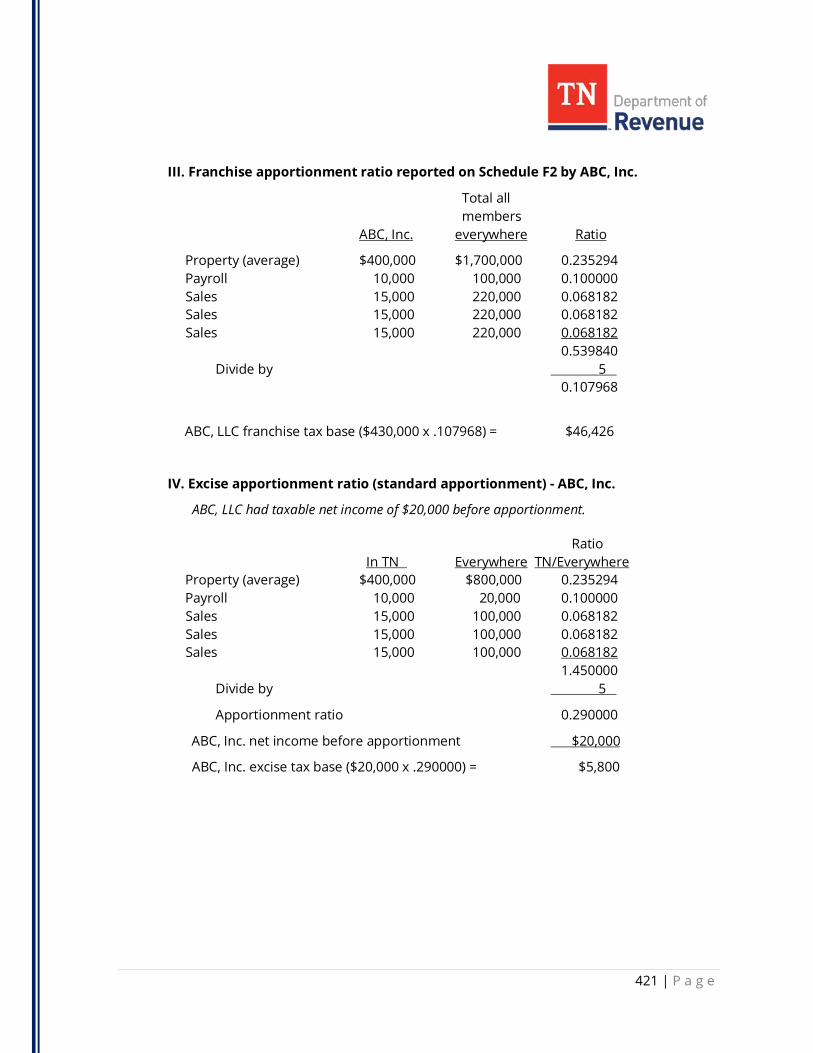

1. Example - Standard Apportionment - Franchise and Excise Tax for ABC, LLC .............. 417

2. Example – Franchise Tax Consolidated Net Worth Apportionment - ABC, Inc. ............. 419

3. Example – Consolidated Net Worth and Single Sales Factor Elections .......................... 422

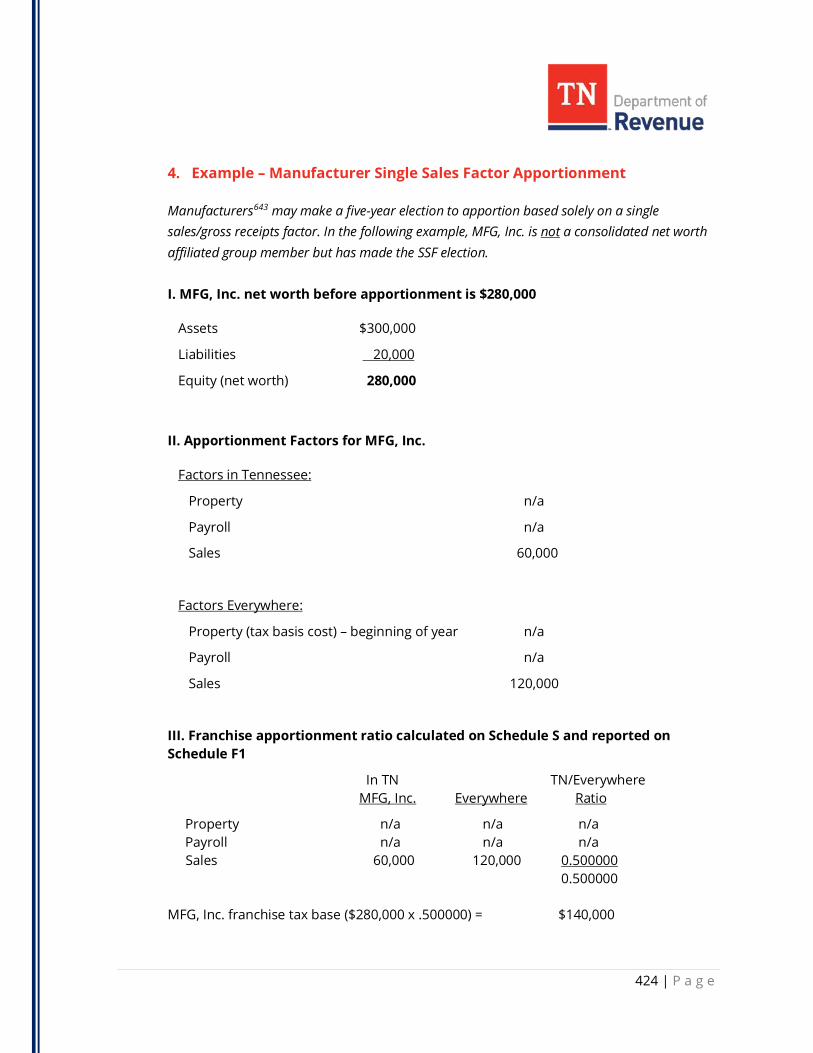

4. Example – Manufacturer Single Sales Factor Apportionment ......................................... 424

Chapter 15: Credits and Overpayments .............................................................................................. 426

Tax Credits ........................................................................................................................................... 426

1. Community Investment Tax Credit...................................................................................... 427

2. Gross Premiums Tax Credit .................................................................................................. 430

3. Income Tax Credit (Hall Tax) ................................................................................................. 431

4. Brownfield Tax Credit ............................................................................................................ 431

5. Broadband Internet Access Equipment [Repealed] .......................................................... 433

6. Industrial Machinery.............................................................................................................. 433

Overpayment Credits ......................................................................................................................... 440

Chapter 16: Job Tax Credit..................................................................................................................... 442

Job Tax Credit Overview .................................................................................................................... 442

Terms Defined by Statute ................................................................................................................. 443

1. Qualified Business Enterprise .............................................................................................. 443

2. Required Capital Investment ................................................................................................ 444

3. Enhancement County ............................................................................................................ 444

4. Qualified Job ........................................................................................................................... 445

5. Investment Period ................................................................................................................. 448

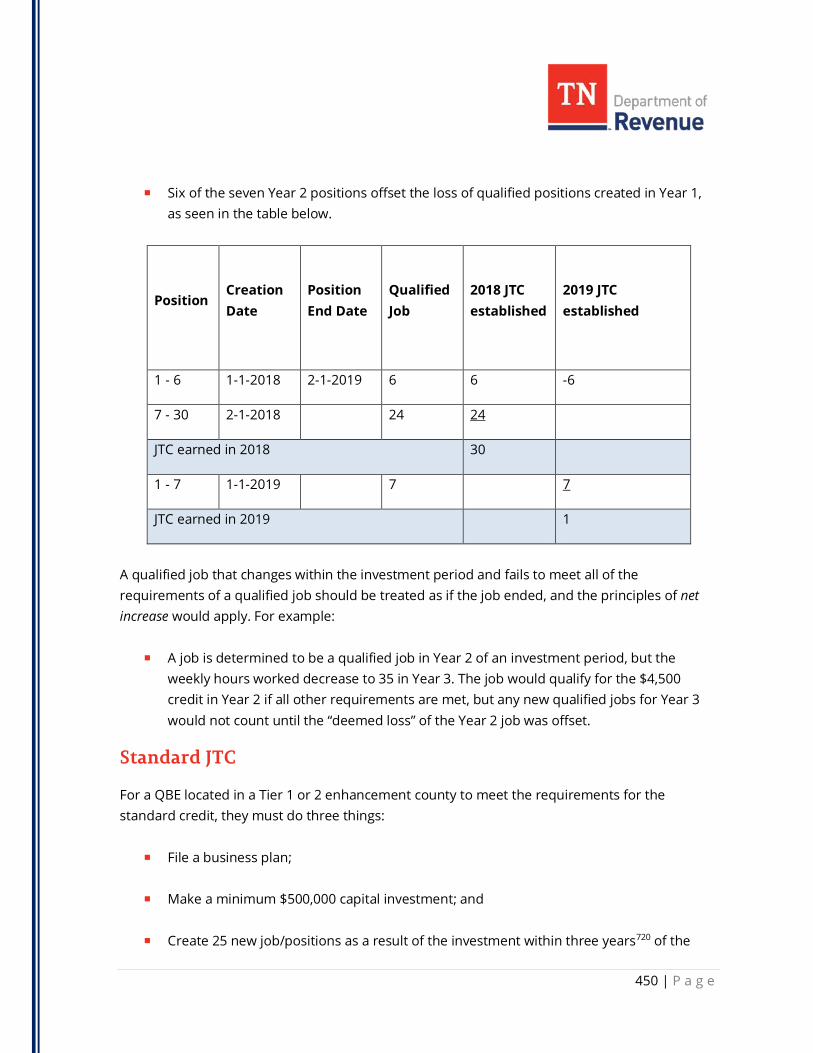

Net Increase in Qualified Jobs during the Investment Period ...................................................... 449

Standard JTC ........................................................................................................................................ 450

1. Table of Standard JTC - Jobs, Years & Tiers......................................................................... 451

14 | P a g e

2. Business Plan and Recommended Documentation.......................................................... 452

3. When Credit May Be Claimed, Offset Limits, and Carryover ........................................... 455

Additional Annual Job Tax Credits .................................................................................................... 456

1. Tier 2, Tier 3, or Tier 4 Enhancement Counties .................................................................. 456

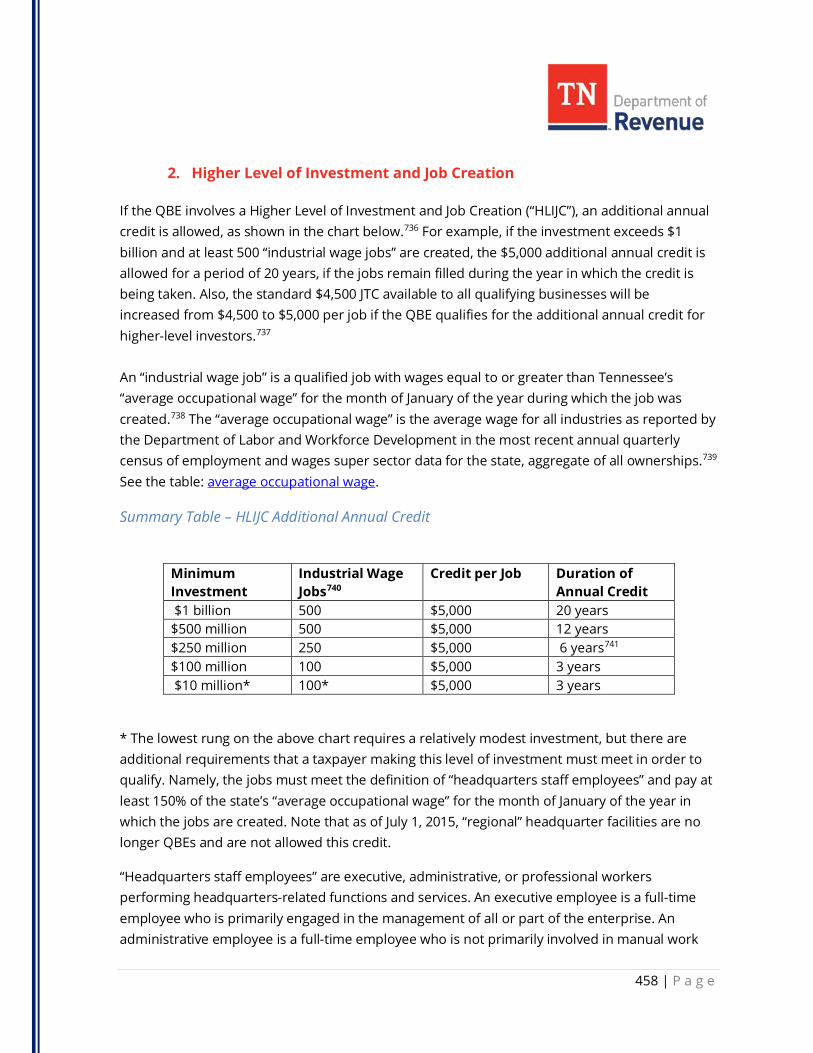

2. Higher Level of Investment and Job Creation .................................................................... 458

3. Adventure Tourism Zone ...................................................................................................... 460

Persons with Disabilities.................................................................................................................... 462

Community Resurgence JTC .............................................................................................................. 463

Wage Rate Requirements .................................................................................................................. 464

Common Law Employer .................................................................................................................... 465

Order of Use – One-time Credits and Credits with Carryovers .................................................... 466

Tax Planning ........................................................................................................................................ 466

1. Investment Period ................................................................................................................. 466

2. Credit Selection: Enhancement County or HLIJC Additional Annual Credit ................... 466

Survival of Credits in Reorganizations and Unitary Group Carryover Issues ............................. 467

1. Corporation Becomes SMLLC Disregarded to Parent....................................................... 467

2. Merger ..................................................................................................................................... 467

3. Taxpayer Sells its Disregarded SMLLC that Created the JTC ............................................ 467

4. Unitary Group of Financial Institutions ............................................................................... 467

Audit Documentation ........................................................................................................................ 468

1. Retained Documents and Workpaper Organization ......................................................... 469

2. Auditor’s Authority to Request Additional Information .................................................... 471

3. Audit Summary Report and Sample Language .................................................................. 472

Audit Procedures ................................................................................................................................ 476

1. Preliminary Audit Research .................................................................................................. 477

2. Business Plan Review ............................................................................................................ 477

3. Identifying the Common Law Employer ............................................................................. 478

4. Qualified Business Enterprise .............................................................................................. 478

5. Required Capital Investment ................................................................................................ 479

15 | P a g e

6. Position Increase .................................................................................................................... 482

7. JTC Credit Carryover .............................................................................................................. 487

8. Tier Minimums – Job Creation .............................................................................................. 488

9. Additional Annual Credits ..................................................................................................... 488

Chapter 17: Real Estate Investment Trusts ......................................................................................... 489

What is a Real Estate Investment Trust? ......................................................................................... 489

REIT Requirements ............................................................................................................................. 490

REIT Structure ..................................................................................................................................... 491

1. Qualified REIT Subsidiary ...................................................................................................... 491

2. Taxable REIT Subsidiary ........................................................................................................ 491

3. Lower-tier LPs and LLCs ........................................................................................................ 491

REIT Types ........................................................................................................................................... 491

1. Publicly-Traded REIT .............................................................................................................. 492

2. Private REIT ............................................................................................................................. 492

3. Captive REIT ............................................................................................................................ 492

4. Captive REIT Affiliated Group ............................................................................................... 493

5. Chart of REIT Types and F&E Implications .......................................................................... 493

REIT Audit ............................................................................................................................................ 494

1. REIT .......................................................................................................................................... 495

2. Captive REIT ............................................................................................................................ 496

3. Qualified REIT Subsidiary ...................................................................................................... 497

4. Taxable REIT Subsidiary ........................................................................................................ 498

5. LPs and LLCs ........................................................................................................................... 498

REIT Examples ..................................................................................................................................... 500

1. Publicly Traded REIT A ........................................................................................................... 500

2. Publicly Traded REIT B ........................................................................................................... 500

3. Non-Public REIT ...................................................................................................................... 501

Chapter 18: Financial Institutions ......................................................................................................... 502

Overview of Financial Institution Taxation...................................................................................... 502

16 | P a g e

Financial Institution Defined ............................................................................................................. 504

1. Holding Company .................................................................................................................. 504

2. Regulated Financial Corporation ......................................................................................... 505

3. Subsidiary of a Holding Company or Regulated Financial Corporation ......................... 507

4. An Investment Entity that is Indirectly More Than 50% Owned by A Holding Company or Regulated Financial Corporation.................................................................................................. 507

5. An Entity Carrying on the Business of a Financial Institution .......................................... 508

Doing Business ................................................................................................................................... 509

Unitary Group ..................................................................................................................................... 512

1. Captive Real Estate Investment Trust Affiliated Group .................................................... 513

2. Exempt Unitary Entities and Apportionment ..................................................................... 513

3. Disclosure Requirement for Financial Institutions ............................................................ 514

Combined Basis .................................................................................................................................. 515

1. Joint Liability ........................................................................................................................... 515

2. FI Unitary Group versus GAAP Consolidated Group ......................................................... 516

3. Unitary Group - Federal Form 851....................................................................................... 516

Franchise Tax Net Worth Tax Base .................................................................................................. 517

1. Schedule F – Non-Consolidated Net Worth ........................................................................ 518

2. Schedule F2 – Consolidated Net Worth .............................................................................. 524

3. Schedule F1 – Captive REIT Net Worth ................................................................................ 526

Franchise Tax Real and Tangible Property Tax Base ..................................................................... 528

Unitary Members with Short Periods .............................................................................................. 528

Excise Tax ............................................................................................................................................ 529

1. Captive REIT Affiliated Group ............................................................................................... 530

2. Excise Tax Apportionment – Schedule SE ........................................................................... 530

3. Loss Carryovers ...................................................................................................................... 533

Credits Available to Financial Institutions ....................................................................................... 534

1. Affordable Housing ................................................................................................................ 535

2. Community Development Financial Institutions ............................................................... 538

17 | P a g e

3. Rural Opportunity Fund and Small Business Opportunity Fund Credit ......................... 540

4. Job Tax Credit ......................................................................................................................... 540

Credit Carryover ................................................................................................................................. 540

Audit Procedures ................................................................................................................................ 541

1. Gather Data ............................................................................................................................ 541

2. Determine the Unitary Group and CNW Affiliated Group ................................................ 544

3. Filing Period ............................................................................................................................ 545

4. Verify Data .............................................................................................................................. 545

Examples of Common Audit Findings ............................................................................................. 546

18 | P a g e

Chapter 1: Introduction

History

Since the enactment of the Tennessee Corporate Excise Tax (“excise tax”) in 1923, and the Tennessee Franchise Tax (“franchise tax”) in 1937, businesses operating for-profit have been subject to tax for the privilege of doing business or exercising the corporate franchise in Tennessee. The imposition of the excise tax was first upheld by the Tennessee Supreme Court in 1924 in Bank of Commerce & Trust Co. v. Senter.1 The imposition of the franchise tax was first upheld by the Tennessee Supreme Court in the 1936 case of Corn v. Fort.2 Initially, franchise and excise tax was levied solely upon the privilege of engaging in business in the corporate form.3 In 1999, the Tennessee General Assembly passed the Tax Revision and Reform Act that broadened the scope of the franchise and excise tax to all “persons” doing business in Tennessee, including pass-through entities such as limited liability companies (“LLC”) and limited partnerships (“LP”).4 In 2015, the Tennessee General Assembly made another significant update to franchise and excise tax law when it passed the Revenue Modernization Act, which made significant changes to the state’s nexus provisions. Current excise tax laws are found in Tenn. Code Ann. §§ 67-4-2001 et seq., and franchise tax laws are found in Tenn. Code Ann. §§ 67-4-2101 et seq. Rules and regulations can be found at TENN. COMP. R. & REGS. 1320-06-01-.01 et seq. or online under the Tax Resources page on the Department’s website.5

Overview

Franchise and excise tax is imposed on entities that operate in Tennessee and offer their owners limited liability protection. In-state and out-of-state entities can both be subject to franchise and excise tax.6 These taxes are accrued taxes imposed on the privilege of doing business in this state or by exercising the corporate franchise.7 Both taxes are solely for state purposes and no county, municipality, or local taxing district has the power to levy similar taxes.8 Although the franchise and excise tax are two separate taxes and are computed separately, the Department of Revenue (the “Department”) administers both taxes together under a singular tax structure. Taxpayers must file both taxes on one return, Form FAE170.9 The return is filed on an annual basis, concurrent with each federal return filing period.

19 | P a g e

1. Entities Subject to Franchise & Excise Taxes

For franchise and excise tax purposes, each taxpayer is considered a separate and single business entity and must file individual tax returns. Entities other than unitary groups of financial institutions and captive real estate investment trust (“REIT”) affiliated groups are not permitted to file a consolidated or combined franchise and excise return.10 Unitary groups of financial institutions and captive REIT affiliated groups are required to file Form FAE174.

General partnerships and sole proprietors are not subject to franchise and excise tax because they do not offer their owners limited liability protection.11 Not-for-profit entities are not generally subject to franchise and excise tax.12

Businesses disregarded for federal income tax purposes are not disregarded for franchise and excise tax purposes except for LLCs whose single member is a corporation (“SMLLC”).13 Additionally, a taxable business that is inactive or has had its charter or other registration forfeited, revoked, or suspended, but has not been dissolved or otherwise properly terminated with the Tennessee Secretary of State, is not relieved from filing a return and paying the minimum franchise tax.14

2. Rates and Impositions

Franchise Tax

Franchise tax is based on the greater of the taxpayer’s net worth or the book value of real or tangible personal property owned or used in Tennessee, based upon values determined at the end of the taxable period.15

The franchise tax rate is 25 cents per $100, or .25% of a taxpayer’s net worth at the close of the tax year covered by the required return.

The minimum franchise tax payable each year is $100.16

Excise Tax Excise tax is based on the taxpayer’s net earnings or net loss for the taxable year.17 “Net earnings” or “net loss” is defined as a taxpayer’s federal taxable income or loss before the operating loss deduction and special deductions,18 with certain adjustments that are required under Tennessee excise tax law.19

20 | P a g e

Tennessee imposes a 6.5% corporate excise tax on the fiscal year net earnings of all persons engaged in business in Tennessee except nonprofit entities, entities otherwise specifically exempt, and businesses not subject to excise tax, such as sole proprietors.20 This rate was set in 2002 by the Tennessee General Assembly.2122

3. Credits

Credits offset tax liability. Depending on the type of credit and the year, a credit may offset both franchise and excise tax or it may offset just one of the taxes. Unused tax credit may or may not be allowed to offset future tax. While the tax code does not specify the order in which to apply credits, the Department applies credits that do not have a carryover provision first. Franchise and excise tax credits that are currently in effect are found in Tenn. Code. Ann. §§ 67-4-2009, 67-4-2109. (Please see Chapter 15 for more information on Credits.)

4. Exemptions

There are seventeen types of exemptions available to entities which will be explained in detail in this publication.23 Filing requirements differ based on the exemption type. Two of the most common exemptions are Family-Owned Non-Corporate Entities (“FONCE”) and Obligated Member Entities (“OME”). (Please see Chapter 2 for more information on Exempt Entities.)

21 | P a g e

Chapter 2: Persons Subject to Tax and Exemptions One of the most important steps in determining if a business is subject to franchise and excise tax is determining if the business operates as a taxable entity. Some businesses, such as those that operate as a sole proprietor, are not subject to franchise and excise tax. While other businesses, such as those that operate as a corporation, are generally subject to franchise and excise tax. This chapter provides an overview of the most common entity types and exemptions that apply to otherwise taxable entities.

Entities Not Subject to Franchise and Excise Tax

1. Sole Proprietorships

Sole proprietorships are not subject to franchise and excise tax because they do not provide their owners limited liability protection. Sole proprietorships report their business activity on federal Form 1040, Schedules C, E, or F.

2. General Partnerships

General partnership (“GP”) is defined by Tenn. Code Ann. § 67-4-2004(19) as a “partnership in which all partners, as defined by state law, are fully liable for the debts of, or the claims against, the partnership.” GPs are not subject to franchise and excise tax because they do not provide their owners limited liability protection. GPs files on federal Form 1065. A GP can usually be identified by its name (the GP’s name would not include “LP” or “LLC”) and it would identify as a GP on Form 1065, Schedule B. While GPs are not taxable entities, if a taxable entity is a partner in a GP, then the activities of the GP that pass through to that GP partner on federal Schedule K-1 are taxable to that GP partner for franchise and excise tax purposes.24

3. Not-for-Profits

Not-for-profit is defined in Tenn. Code Ann. § 67-4-2004(34) and refers to numerous federal classifications of exemptions, the most common being an entity described in Internal Revenue Code § 501. Not-for-profits are generally not subject to franchise and excise tax. They file an information return, Form 990, for federal income tax purposes. However, a not-for-profit entity that has earnings from activities outside the scope of the activities that give it its exempt status is subject to federal and franchise and excise taxes. The not-for-profit’s unrelated business taxable income is reported on federal Form 990-T25 and is subject to the excise tax. A not-for-

22 | P a g e

profit entity is also subject to the franchise tax on the greater of its net worth or real and tangible property owned or used in the state that is attributable to any activities that are unrelated to, and outside the scope of, the activities that give the not-for-profit its exempt status.

4. SMLLC Owned by Pension Trust

If a single-member limited liability company (“SMLLC”) is wholly-owned by a pension trust, which is a not-for-profit entity, the SMLLC is disregarded to the pension trust for federal income tax purposes. The SMLLC is also disregarded for franchise and excise tax purposes, and its earnings are considered to be net earnings of the pension trust. The combined net earnings of the pension trust and the SMLLC are not subject to franchise and excise tax unless the earnings constitute unrelated business taxable income.26

Entity Exemptions

1. Franchise and Excise Tax Exemptions

There are 17 types of exemptions available to entities that would otherwise be subject to franchise and excise tax. The following exemptions apply to both the franchise and excise taxes. If a taxpayer fails to meet the requirements for the exemption at any time during the taxable period, the taxpayer loses the exemption for the entire taxable period. The complete list of franchise and excise tax exemptions and requirements can be found in Tenn. Code Ann. § 67-4-2008. The exemptions are as follows:

Industrial development corporations

Masonic lodges and similar lodges

Regulated investment companies whose investments consist of at least 75% U.S., state or local bonds

Federal and state credit unions

Venture capital funds*

Farming or the holding of a personal residence*

LLCs, LLPs, LPs, or business trusts that acquire receivables from an affiliate which report the income in Tennessee*

23 | P a g e

LPs or LLCs that provide affordable housing and receive low-income housing credits27*

Obligated member entities*

Partnerships, trusts, REMICs, and FASITs that have asset-backed securities of debt obligations28*

Family-owned noncorporate entities*

Diversified investing funds*

Tennessee historic property preservation entities

Insurance companies

TNInvestco entities that receive investment credits under the Tennessee Small Business Investment Company Credit Act29

Any entity that is owned, in whole or in part, by the United States armed forces and derives more than 50% of its gross income from operating facilities which are located on property owned or leased by the federal government and operated primarily for the benefit of members of the United States armed forces*

Qualified low-income community historic structure owners or lessees*

* An entity claiming this exemption must file an Application for Exemption/Annual Exemption Renewal (Form FAE183) for the initial and subsequent taxable periods for which the entity is claiming the exemption. This form is due on or before the 15th day of the fourth month following the close of the entity’s taxable period. The Department will grant an extension of time of six months in which to file the form if the entity makes a valid extension request.30 While failure to timely file the form will not preclude the entity from qualifying for the exemption, the Department may assess the entity a penalty of $200, per occurrence, for late filing.

2. Exemptions Requiring an Evaluation

Of the 17 exemptions listed above, there are 6 that might require an evaluation by the Audit Division to verify the taxpayer’s eligibility. These exemptions include: 1) venture capital fund, 2) farming/holding a personal residence, 3) obligated member entity, 4) family-owned noncorporate entity, 5) diversified investing fund, and 6) entities created for asset-back securitization of debt obligations. The Department may request documents such as federal tax returns (including all forms and schedules), articles of organization, or partnership agreements

24 | P a g e

(to determine an entity’s business purpose) when evaluating an entity’s eligibility for exemption. An overview of the requirements for each of these exemptions is listed below.

Venture Capital Fund

Entity must be an LLC, LLP, LP, or a business trust.

Entity is operated for the exclusive purpose of buying, holding, and/or selling securities and greater than 50% of securities are in non-publicly traded companies.

Entity buys, holds, and/or sells securities on its own and not as a broker.

More than 50% of the entity’s capital is from investments neither related to nor affiliated with the fund.

Farming/Holding a Personal Residence31

Entity must be an LLC, LP, or LLP.

At least 66.67% of the entity’s activity is in farming and 66.67% of its assets are used by the owner or the owner’s lessee for farming, or at least 66.67% of the entity’s activity is the holding of one or more personal residences where one or more of the members/partners reside.

At least 95% of the voting rights, capital interests, or profits are owned by natural persons who are relatives or by trusts for their benefit.

Entity must complete a Disclosure of Activity form, which is due with its Application for Exemption and each Annual Exemption Renewal, to inform the Department of the entity’s activities relating to the exemption.

Obligated Member Entity (“OME”)

It is imperative that the taxpayer complete the Disclosure of Activity form in its entirety, including all pertinent addresses and the county in which the assets are located.

25 | P a g e

Entity must be an LP, LLP, or LLC (cannot be an LLC that has elected to be classified as a corporation for federal income tax purposes by filing federal Form 8832).32

All members or partners of the entity make an election to be fully liable for the debts, obligations, and liabilities of the entity.

- An “Obligated member” is a member or partner of an obligated member entity that is fully liable for the debts, obligations and liabilities of the entity, as provided in Tenn. Code Ann. § 67-4-2008(b)-(d), and that has filed appropriate documentation to that effect with the secretary of state;33

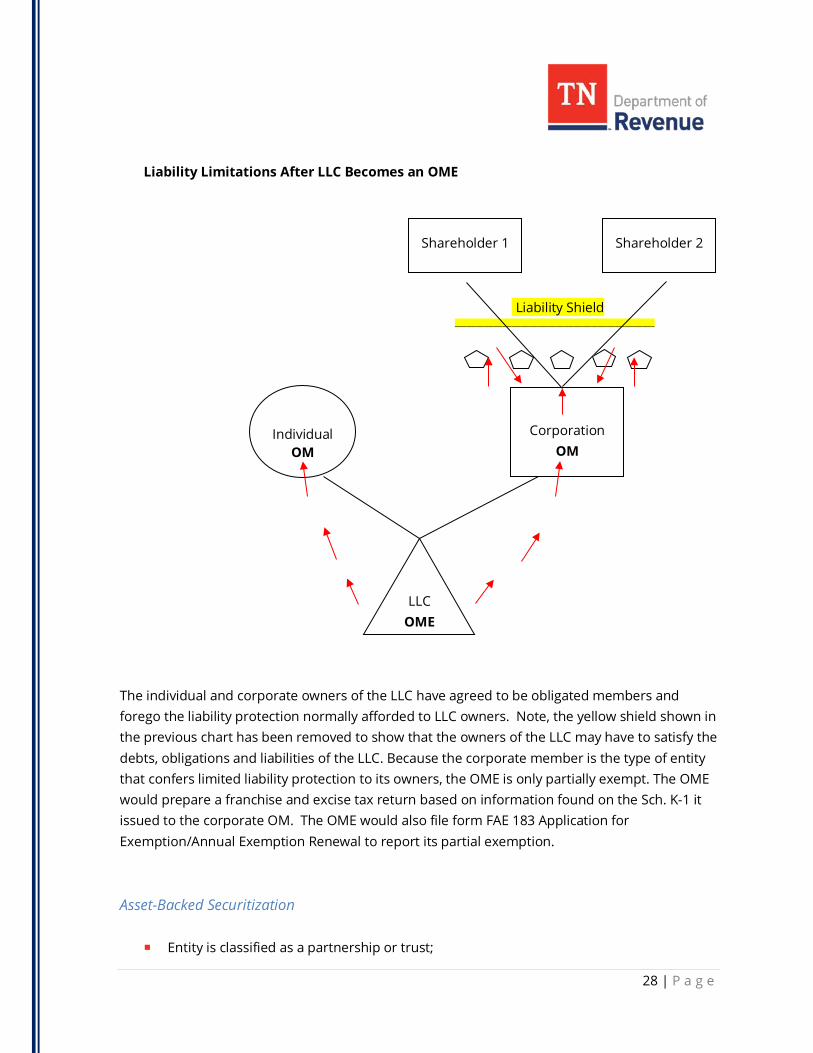

An OME is subject to franchise and excise tax to the extent any obligated member, or any owner of an obligated member, provides limited liability protection.34 The information needed to compute the tax is generally found on the OME’s federal Schedule(s) K-1. For example:

- XYZ, LLC (“XYZ”) has two members, A and B. XYZ qualifies as an obligated member entity because A and B have filed documentation with the secretary of state to make them fully liable for the debts, obligations and liabilities of XYZ. The corporate, LP and LLC forms of entity organization generally shield the entity’s owners from being subject to the entity’s debts, obligations and liabilities; however, in this example, A and B have given up this protection by becoming obligated members. As A and B are both individuals, there are no additional, indirect ownership interests to consider with respect to XYZ. OMEs that are directly and solely owned by individuals do not have indirect ownership interests to consider, and such OMEs will always be fully exempt from the franchise and excise tax.

- In this example, Member A is an individual and Member B is a corporation with shareholders of its own. As stated above, corporations provide their owners with limited liability protection and generally shield them from liabilities of the corporation. This remains true even though B has agreed to be an obligated member of XYZ. When one of the obligated members of an OME itself confers limited liability protection on its own owners, then the OME is partially exempt from the franchise and excise tax. The tax is computed on the information reported on B’s federal Schedule K-1 received from XYZ. More specifically, the values shown on B’s Sch. K-1, Part III, Lines 1-13, are reported on Schedule J1 of XYZ’s Tennessee excise tax return. Additionally, the equity of XYZ attributable to Member B is subject to the franchise tax. In this example, XYZ’s equity (net

26 | P a g e

worth), as reported under generally accepted accounting principles, is $100,000. Member B’s ending capital percentage reported on Sch. K-1, Part II, Item J is 50%. (This is the percentage share of the capital that Member B would receive if XYZ was liquidated by the distribution of undivided interests in XYZ’s assets and liabilities.) The net worth reported on the franchise tax return Sch. F1, Line 1 is $50,000 ($100,000 x 50%).

Estates, trusts that are not taxpayers, not-for-profit entities, or other entities exempt from franchise and excise tax, are not deemed to provide limited liability protection. They must, however, follow the same procedures renouncing liability protection with the Tennessee Secretary of State for XYZ to qualify as an obligated member entity.

- A partially exempt OME will file both an Annual Exemption Renewal (Form FAE183) and a franchise and excise tax return (Form FAE170) for the taxable period.

The entity must file the required documentation, as detailed at Tenn. Code Ann. § 67-4-2008(b)-(d), with the Tennessee Secretary of State to be eligible for this exemption and must provide a copy of such documentation to the Department when applying for this exemption.

- The OME must file the required documentation on or before the first day of the taxable period for which the exemption applies.

- If the OME files the required documentation after the first day of the taxable period, the exemption will not become effective until the following taxable period. The exemption may not be prorated.

The following charts show limited liability protection before and after an LLC becomes an OME.