FOURTH QUARTER 2014 FINANCIAL RESULTS .../media/Files/T/Thehartford...FOURTH QUARTER 2014 FINANCIAL...

23

FOURTH QUARTER 2014 FINANCIAL RESULTS PRESENTATION The Hartford Financial Services Group, Inc. Investor Presentation February 2, 2015

Transcript of FOURTH QUARTER 2014 FINANCIAL RESULTS .../media/Files/T/Thehartford...FOURTH QUARTER 2014 FINANCIAL...

FOURTH QUARTER 2014 FINANCIAL RESULTS PRESENTATION

The Hartford Financial Services Group, Inc.

Investor Presentation

February 2, 2015

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Safe Harbor Statement

Certain statements made in this presentation should be considered forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. These include statements about The Hartford’s future results of operations. We caution investors that these forward-looking statements are not guarantees of future performance, and actual results may differ materially. Investors should consider the important risks and uncertainties that may cause actual results to differ, including those discussed in The Hartford’s news release issued on February 2, 2015, our Quarterly Reports on Form 10-Q, our 2013 Annual Report on Form 10-K, and other filings we make with the Securities and Exchange Commission. We assume no obligation to update this presentation, which speaks as of today’s date. The discussion in this presentation of The Hartford’s financial performance includes financial measures that are not derived from generally accepted accounting principles (GAAP). Information regarding these non-GAAP financial measures, including reconciliations to the most directly comparable GAAP financial measures, is provided in the news release issued on February 2, 2015 and The Hartford’s Investor Financial Supplement for fourth quarter 2014 which is available at the Investor Relations section of The Hartford’s website at http://ir.thehartford.com.

From time to time, The Hartford may use its website to disseminate material company information. Financial and other important information regarding The Hartford is routinely accessible through and posted on our website at http://ir.thehartford.com. In addition, you may automatically receive email alerts and other information about The Hartford when you enroll your email address by visiting the “Email Alerts” section at http://ir.thehartford.com.

2

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Fourth Quarter 2014 Key Financial Highlights

3

• Core EPS1,2 up 22% to $0.96; core earnings1 up 12% to $426 million ˗ Core EPS $0.95 excluding CATs3 below outlook and unfavorable PYD4

˗ Growth driven by improved P&C5 and Corporate results

BVPS and ROE • BVPS, ex-AOCI1,6, up 4% over 4Q13 to $40.71

• Core earnings ROE1,7 8.4%, up 1 point over 2013

P&C Underwriting

• P&C (Combined) CAY8 combined ratio, before CATs1, improved 3.8

points to 92.0 driven by Commercial and Personal Lines

Core Earnings

Capital Management

Talcott Runoff • Variable and fixed annuity contract counts down 13% and 18%,

respectively, since 4Q13

• Weighted average diluted shares outstanding declined 9% from 4Q13 ˗ Repurchased 7.7 million shares in the quarter for $300 million

˗ Completed ASR9 program in the quarter, taking delivery of an additional 2.7 million shares

Commercial Lines Pricing

• Standard Commercial renewal written price increases averaged 3%,

in-line with loss cost trends

1. Denotes financial measure not calculated based on generally accepted accounting principles (GAAP) 2. Earnings per diluted share 3. Catastrophes 4. Prior year development 5. Property &

Casualty 6. Book value per diluted share, excluding accumulated other comprehensive income 7. Return on equity 8. Current accident year 9. Accelerated share repurchase

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

4Q14 core earnings per diluted share of $0.96, up 22% over 4Q13

Core Earnings (Loss) By Segment ($ in millions except per diluted share amounts) 4Q13 4Q14 Change 3

Commercial Lines $229 $251 10%

Personal Lines 49 65 33%

P&C Other Operations 22 - (100%)

Group Benefits 55 45 (18%)

Mutual Funds 20 27 35%

Sub-total $375 $388 3%

Talcott Resolution 99 98 (1%)

Corporate (92) (60) 35%

Core earnings1 $382 $426 12%

Net realized capital gains (losses) 1 11 (9) NM

Unlock charge, after-tax 1 13 NM

Restructuring and other (costs), after-tax (10) (17) (70%)

Income (loss) from disc. operations, after-tax (70) 37 NM

Pension settlement, after-tax - (83) NM

Net reinsurance gain on dispositions, after-tax - 15 NM

Net income $314 $382 22%

Core earnings per diluted share $0.79 $0.96 22%

Wtd. avg. diluted shares outstanding2 486.1 442.6 (9%)

• Core earnings increased 12%

from 4Q13 primarily due to

improved P&C and Corporate

results

• Core earnings per diluted share

were $0.96, up 22% over 4Q13

• Net income of $382 million

included an $83 million, after-tax,

pension settlement charge

• Weighted average diluted shares

outstanding decreased 9% due

to the company’s equity

repurchases

• 4Q14 last 12 months core

earnings ROE of 8.4%, up from

7.4% in 4Q13

4

1. Net realized capital gains (losses), after-tax and deferred acquisition

costs (DAC), excluded from core earnings

2. In millions

3. The Hartford defines increases or decreases greater than or equal to

200%, or changes from a net gain to a net loss position, or vice versa, as

“NM” or not meaningful

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

5

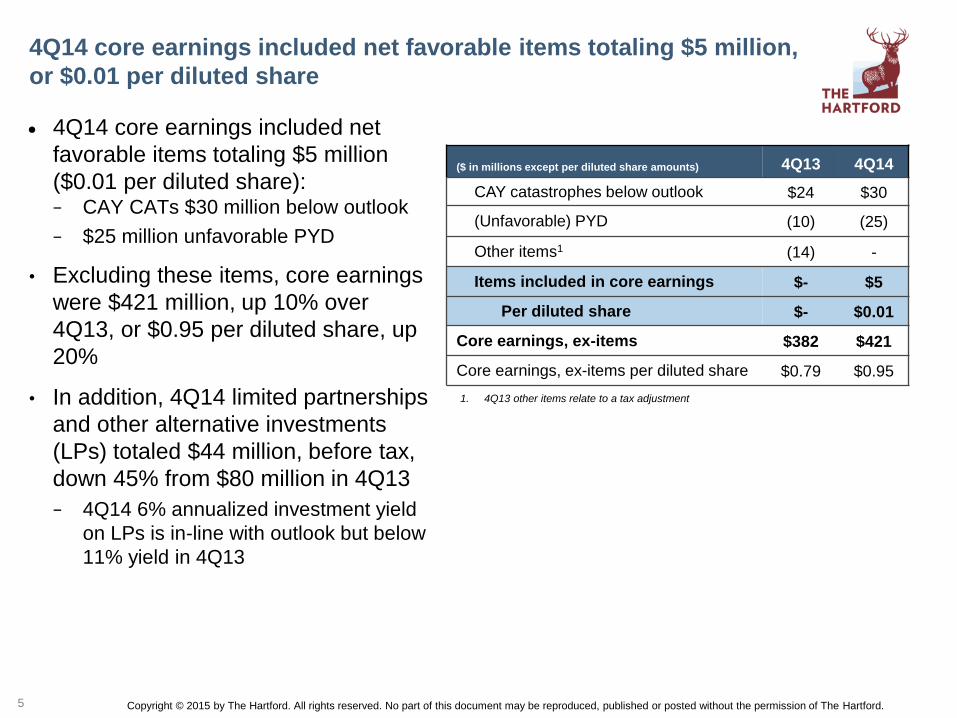

4Q14 core earnings included net favorable items totaling $5 million,

or $0.01 per diluted share

4Q14 core earnings included net

favorable items totaling $5 million

($0.01 per diluted share): − CAY CATs $30 million below outlook

− $25 million unfavorable PYD

• Excluding these items, core earnings

were $421 million, up 10% over

4Q13, or $0.95 per diluted share, up

20%

• In addition, 4Q14 limited partnerships

and other alternative investments

(LPs) totaled $44 million, before tax,

down 45% from $80 million in 4Q13

− 4Q14 6% annualized investment yield

on LPs is in-line with outlook but below

11% yield in 4Q13

($ in millions except per diluted share amounts) 4Q13 4Q14

CAY catastrophes below outlook $24 $30

(Unfavorable) PYD (10) (25)

Other items1 (14) -

Items included in core earnings $- $5

Per diluted share $- $0.01

Core earnings, ex-items $382 $421

Core earnings, ex-items per diluted share $0.79 $0.95

5

1. 4Q13 other items relate to a tax adjustment

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

P&C (Combined) Written Premiums

($ in millions)

4Q14 P&C (Combined)1 top line growth and margin improvement

continues

6

$1,463 $1,669 $1,571 $1,583 $1,558

$886 $927 $1,003 $1,019 $912

4Q13 1Q14 2Q14 3Q14 4Q14

Commercial Lines Personal Lines

$2,603 $2,349

$2,597 $2,574 $2,470

P&C (Combined) Combined Ratio Breakdown

64.7 61.7 62.4 61.8 61.0

31.1 27.9 30.2 30.1 31.0

1.7 1.9

17.7 1.2 1.8

4Q13 1Q14 2Q14 3Q14 4Q14Total Losses and LAE Before CATs and PYD Expenses CATs and PYD

91.4 97.5 110.4

93.0 93.8

• Written premiums rose 5% over 4Q13

− 6% growth in Commercial Lines

− 3% growth in Personal Lines

• P&C (Combined) core earnings rose 5%

to $316 million from $300 million in 4Q13

driven by improved CAY underwriting

results

• Combined ratio of 93.8 was 3.7 points

better than 4Q13 due to improved loss

and loss adjustment expense (LAE) ratio

• CAY combined ratio, before CATs, of 92.0

improved 3.8 points from 4Q13

− Both Commercial Lines and Personal Lines

CAY combined ratio, before CATs, improved

over 4Q13

1. P&C (Combined) consists of the Commercial Lines, Personal Lines and P&C Other segments

2. 1Q14 expense ratio includes 2.0 point benefit related to NY State Workers’ Compensation Board assessments (NY Assessments)

3. Expense ratio includes policyholder dividends

6

2

3

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

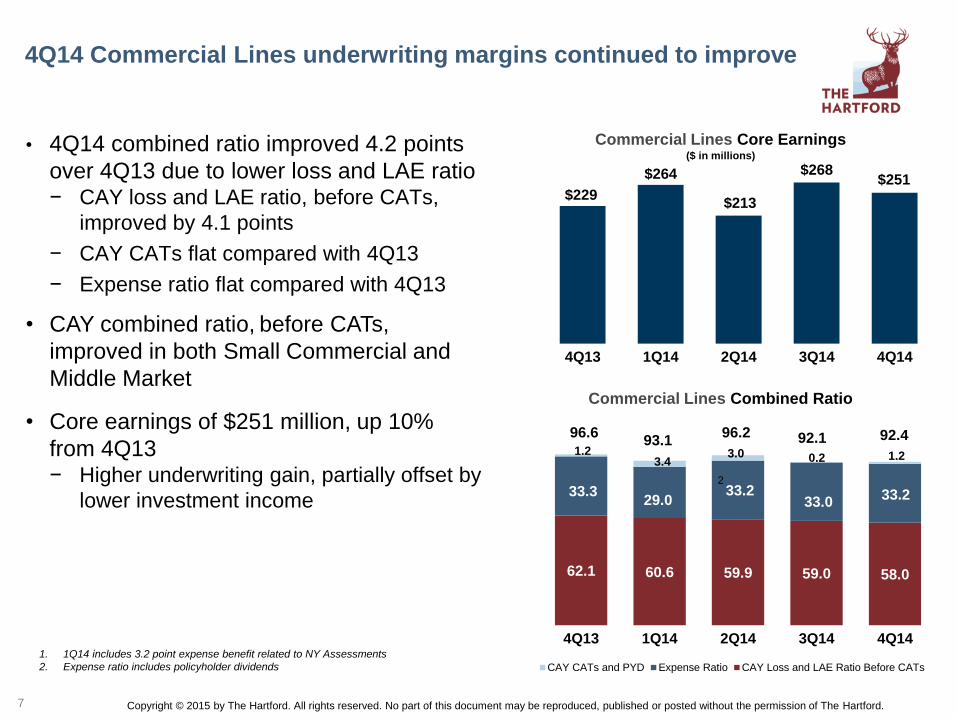

4Q14 Commercial Lines underwriting margins continued to improve

7

• 4Q14 combined ratio improved 4.2 points

over 4Q13 due to lower loss and LAE ratio − CAY loss and LAE ratio, before CATs,

improved by 4.1 points

− CAY CATs flat compared with 4Q13

− Expense ratio flat compared with 4Q13

• CAY combined ratio, before CATs,

improved in both Small Commercial and

Middle Market

• Core earnings of $251 million, up 10%

from 4Q13 − Higher underwriting gain, partially offset by

lower investment income

Commercial Lines Combined Ratio

62.1 60.6 59.9 59.0 58.0

33.3 29.0

33.2 33.0

33.2

1.2 3.4

3.0 0.2 1.2

4Q13 1Q14 2Q14 3Q14 4Q14

CAY CATs and PYD Expense Ratio CAY Loss and LAE Ratio Before CATs

96.6 93.1

96.2 92.1 92.4

1. 1Q14 includes 3.2 point expense benefit related to NY Assessments

2. Expense ratio includes policyholder dividends

1

2

$229

$264

$213

$268 $251

4Q13 1Q14 2Q14 3Q14 4Q14

Commercial Lines Core Earnings

($ in millions)

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Commercial Lines written premium grew 6% with strong

retention and new business

1. Programs written premiums were negatively impacted by underwriting actions to

reposition the business and the exit from unprofitable programs. The company ceased

writing all transportation programs effective Jan. 1, 2014

2. Standard Commercial is comprised of Small Commercial and certain Middle Market lines

of business

3. Renewal written price statistics are subject to change from period to period, based on a

number of factors, including changes in actuarial estimates and the effect of subsequent

cancellations and non-renewals on rate achieved, and modifications made to better reflect

ultimate pricing achieved

• Written premiums rose 6% over 4Q13; up

7% excluding programs1 − Small Commercial rose 5%

− Middle Market rose 6%, 7% excluding programs

− Specialty Commercial premiums increased 13%,

driven by 29% growth in National Accounts

• Renewal written price increases averaged

3% in Standard Commercial2, in line with

loss cost trends

− More competitive pressure in Middle Market

workers’ compensation

− Commercial auto remains highest in rate

increase

$715 $865 $833 $791 $754

$568 $572 $537 $583 $601

$173

$223 $192 $201 $195

4Q13 1Q14 2Q14 3Q14 4Q14

Small Commercial Middle Market Specialty Commercial

$1,583 $1,463

$1,669 $1,571 $1,558

Commercial Lines Written Premiums

($ in millions)

7%

6%

5% 5%

3%

4Q13 1Q14 2Q14 3Q14 4Q14

Standard Commercial1 Renewal Written Pricing3

8

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

• Written premiums increased 5% over

4Q13 − Renewal written price increases averaged

3%

− New business premium totaled $122

million, up 10% for the third consecutive

quarter of double-digit growth

− Policy count retention increased to 85%,

up 3 points

• Small Commercial delivered outstanding

underwriting results in 4Q14 − Combined ratio improved 1.6 points over

4Q13 to 86.1 due to improved CAY results

and lower PYD

− CAY combined ratio, before CATs, of 86.8

improved 1.1 points from 4Q13, reflecting

strong margins in workers’ compensation

Small Commercial: 4Q14 results driven by sustained pricing and

underwriting initiatives

9

9

1. 1Q14 expense ratio includes 3.3 point benefit related to NY Assessments

87.9 85.9 87.6 87.5 86.8

1.9

3.8 0.9

4Q13 1Q14 2Q14 3Q14 4Q14

CATs and PYD CAY Combined Ratio Before CATs

87.7 86.1 87.8

91.4 88.4

(0.2) (0.7)

Small Commercial Combined Ratio

$111

$131 $140

$128 $122

82% 83% 84% 84% 85%

4Q13 1Q14 2Q14 3Q14 4Q14New Business Retention

Small Commercial Written Premiums & Retention ($ in millions)

$754 $715

$865 $833 $791

1

1

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

• Written premiums rose 6% over 4Q13, 7%

excluding programs

− Renewal written price increases averaged 3%

− New business premium of $131 million, up

30% driven by strong growth in workers’

compensation, particularly in large accounts

− Policy count retention of 80%, up 1 point

• Margins continue to improve

− Combined ratio improved 4.8 points to 97.8

due to improved CAY underwriting results

− CAY combined ratio, before CATs, improved

5.0 points to 94.7, reflecting an improved

workers’ compensation loss and LAE ratio

• Facing increased competition in Middle

Markets, particularly in the workers’

compensation and property lines

• During 4Q14, realigned certain business

lines between Middle Market and Specialty

Commercial2

Middle Market: Strong top line growth and improved margins

10

10

1. 1Q14 expense ratio includes 2.6 point benefit related to NY Assessments 2. Underwriting results for programs and livestock business are now reported in

Middle Market instead of Specialty Commercial, and underwriting results for bond are now reported in Specialty Commercial instead of Middle Market

Middle Market Combined Ratio

99.7 92.2 97.6 93.5 94.7

2.9 6.6 2.2 0.2 3.1

4Q13 1Q14 2Q14 3Q14 4Q14

CATs and PYD CAY Combined Ratio Before CATs

102.6

$101 $110 $110

$107 $131

79% 81% 80% 80% 80%

4Q13 1Q14 2Q14 3Q14 4Q14New Business Retention

Middle Market Written Premiums & Retention ($ in millions)

$583 $568 $572 $537

$601

98.8

1

1 99.8 93.7 97.8

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

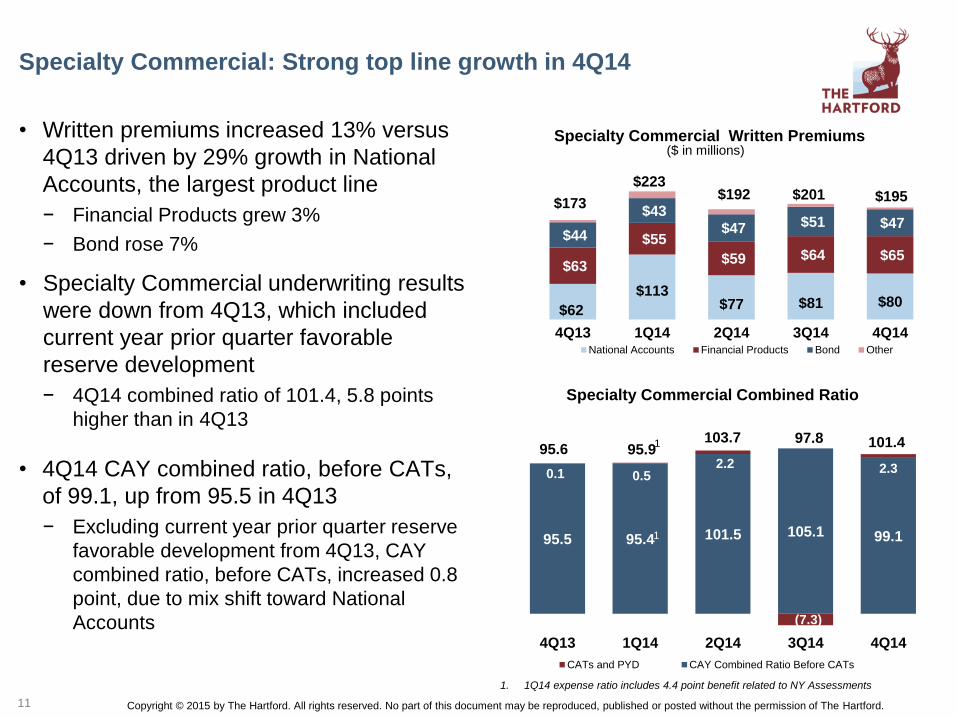

• Written premiums increased 13% versus

4Q13 driven by 29% growth in National

Accounts, the largest product line

− Financial Products grew 3%

− Bond rose 7%

• Specialty Commercial underwriting results

were down from 4Q13, which included

current year prior quarter favorable

reserve development

− 4Q14 combined ratio of 101.4, 5.8 points

higher than in 4Q13

• 4Q14 CAY combined ratio, before CATs,

of 99.1, up from 95.5 in 4Q13

− Excluding current year prior quarter reserve

favorable development from 4Q13, CAY

combined ratio, before CATs, increased 0.8

point, due to mix shift toward National

Accounts

11

$62

$113 $77 $81 $80

$63

$55

$59 $64 $65

$44

$43

$47 $51 $47

4Q13 1Q14 2Q14 3Q14 4Q14National Accounts Financial Products Bond Other

Specialty Commercial: Strong top line growth in 4Q14

11

Specialty Commercial Written Premiums

($ in millions)

Specialty Commercial Combined Ratio

95.5 95.4 101.5 105.1 99.1

0.1 0.5 2.2

(7.3)

2.3

4Q13 1Q14 2Q14 3Q14 4Q14

CATs and PYD CAY Combined Ratio Before CATs

95.6 95.9 103.7 97.8 101.4

$173

$223

1. 1Q14 expense ratio includes 4.4 point benefit related to NY Assessments

1

1

$192 $201 $195

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

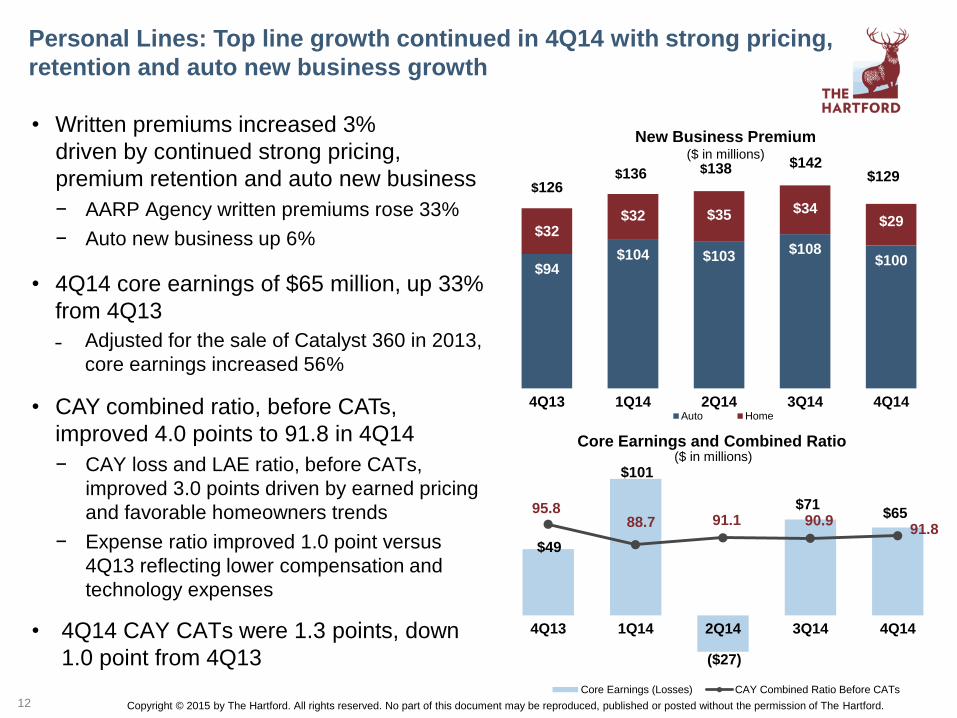

Personal Lines: Top line growth continued in 4Q14 with strong pricing,

retention and auto new business growth

• Written premiums increased 3%

driven by continued strong pricing,

premium retention and auto new business

− AARP Agency written premiums rose 33%

− Auto new business up 6%

• 4Q14 core earnings of $65 million, up 33%

from 4Q13

˗ Adjusted for the sale of Catalyst 360 in 2013,

core earnings increased 56%

• CAY combined ratio, before CATs,

improved 4.0 points to 91.8 in 4Q14

− CAY loss and LAE ratio, before CATs,

improved 3.0 points driven by earned pricing

and favorable homeowners trends

− Expense ratio improved 1.0 point versus

4Q13 reflecting lower compensation and

technology expenses

• 4Q14 CAY CATs were 1.3 points, down

1.0 point from 4Q13

12

Core Earnings and Combined Ratio

($ in millions)

$49

$101

($27)

$71 $65 95.8

88.7 91.1 90.9 91.8

4Q13 1Q14 2Q14 3Q14 4Q14

Core Earnings (Losses) CAY Combined Ratio Before CATs

$94 $104 $103

$108 $100

$32 $32 $35 $34

$29

4Q13 1Q14 2Q14 3Q14 4Q14Auto Home

New Business Premium ($ in millions)

$126 $136 $138 $142

$129

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Personal Lines: Auto written premiums up 3% in 4Q14

13

1. Before CATs and PYD

• Auto written premiums increased 3%

over 4Q13 due to new business, strong

retention and renewal written price

increases

− New business premium rose 6%

− Policy and premium retention of 84% and

87%, respectively

− Renewal written price increases averaged

6%, up from 5% in 3Q14 and 4Q13

• CAY auto combined ratio, before CATs,

improved 2.4 points to 102.4 in 4Q14

reflecting:

− Earned pricing and favorable liability

frequency trends offsetting moderate

severity trends

− Lower expense ratio

Auto Combined Ratio1

104.8

92.8 96.0 97.0

102.4

4Q13 1Q14 2Q14 3Q14 4Q14

5% 5% 5% 5%

6%

86% 87% 86% 85% 84%

4Q13 1Q14 2Q14 3Q14 4Q14Renewal Written Price Increases Policy Count Retention

Auto Renewal Written Price Increases and

Policy Count Retention

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

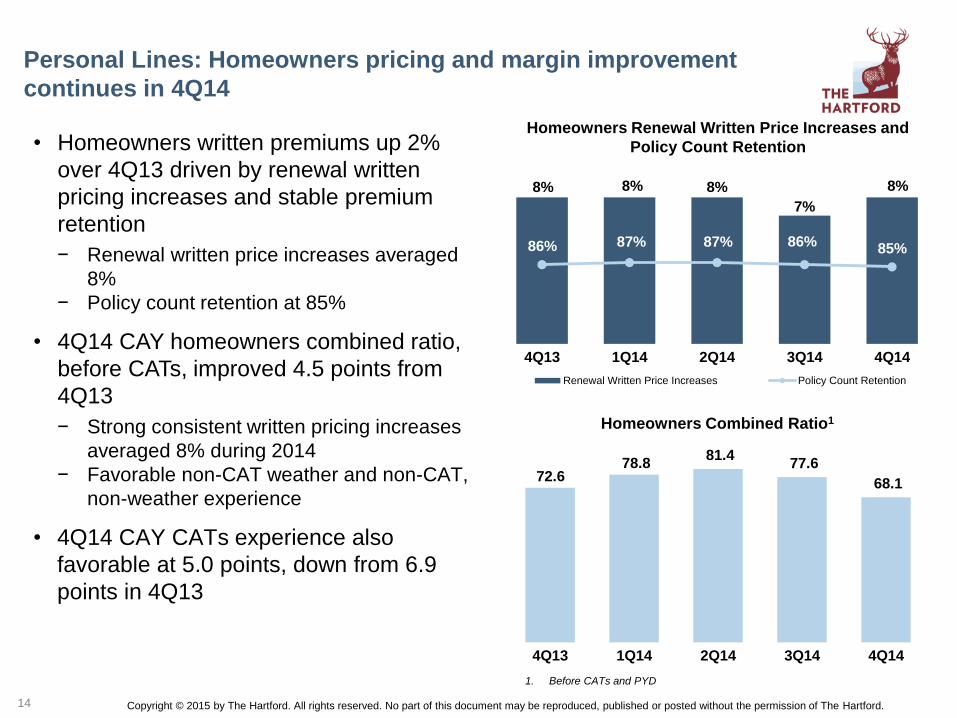

Personal Lines: Homeowners pricing and margin improvement

continues in 4Q14

1. Before CATs and PYD

8% 8% 8%

7%

8%

86% 87% 87% 86% 85%

4Q13 1Q14 2Q14 3Q14 4Q14

Renewal Written Price Increases Policy Count Retention

Homeowners Renewal Written Price Increases and

Policy Count Retention

72.6 78.8

81.4 77.6

68.1

4Q13 1Q14 2Q14 3Q14 4Q14

Homeowners Combined Ratio1

• Homeowners written premiums up 2%

over 4Q13 driven by renewal written

pricing increases and stable premium

retention

− Renewal written price increases averaged

8%

− Policy count retention at 85%

• 4Q14 CAY homeowners combined ratio,

before CATs, improved 4.5 points from

4Q13

− Strong consistent written pricing increases

averaged 8% during 2014

− Favorable non-CAT weather and non-CAT,

non-weather experience

• 4Q14 CAY CATs experience also

favorable at 5.0 points, down from 6.9

points in 4Q13

14

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

$756 $732 $742 $731 $737

74.7% 77.6% 77.5% 78.3% 76.0%

4Q13 1Q14 2Q14 3Q14 4Q14Premiums Loss Ratio

Group Benefits: After-tax core earnings margin 5.3% in 4Q14

Core Earnings & After-Tax Margin1 ($ in millions)

1. Denotes a financial measure not calculated based on GAAP

2. Excludes A-FI and buyout premiums

Fully Insured Ongoing Premiums2 & Loss Ratio2 ($ in millions)

15

• Core earnings declined from 4Q13 due to lower

disability results and LP income, partially offset

by favorable life results

- 5.3% after-tax core earnings margin versus 5.9%

in 4Q13

• 4Q14 loss ratio, excluding A-FI, increased 1.3

points from 4Q13 to 76.0% due to less

favorable group disability results

• Group life loss ratio, excluding A-FI, improved

2.8 points to 71.8% on favorable mortality

• Group disability loss ratio increased 6.2 points

to 81.9% - 4Q13 results benefited from improved recovery

rates on claims incurred in prior policy years

- Disability recovery rates remained strong in 4Q14

• Fully insured ongoing premiums declined 3%

from 4Q13, excluding A-FI

15

$55

$45

$52

$38

$45

5.9%

5.1%

6.0%

4.5%

5.3%

4Q13 1Q14 2Q14 3Q14 4Q14Core earnings After-Tax Margin

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Mutual Fund Sales & Net Flows

($ in millions)

Mutual Funds: Continued strong sales

and fund performance

16

• Core earnings of $27 million, up 35% from 4Q13

driven by a state income tax benefit as well as by

higher fee income due to an increase in Mutual

Fund AUM

• Mutual Fund2 assets under management (AUM),

which excludes Talcott Resolution AUM3,

increased 3% from 4Q13 to $73.0 billion − Talcott Resolution AUM declined 20%

• Mutual Fund sales remained strong at $3.9

billion, up 10% compared with 4Q13

• Mutual Fund net outflows of $0.4 billion,

excluding a planned $0.7 billion AUM transfer

within the company, versus net outflows of $0.4

billion in 4Q13

• Solid overall fund performance as 43%, 63% and

64% of funds beat peers on a 1-, 3- and 5-year basis4,

respectively

1. Core earnings $ in millions and AUM $ in billions. AUM as of end of period.

2. Mutual funds sold through retail, bank trust, registered investment advisor and 529 plan channels

3. Consists of mutual fund assets held in separate accounts supporting variable insurance and investment products

4. Hartford Mutual Funds (HMF) only on Morningstar net of fees basis

$3,555 $3,692 $3,910 $3,753 $3,894

($3,997) ($3,674) ($4,348)

($3,660)

($4,954)

($442) $18

($438) $93

($1,060)

Sales Redemptions Net Flows

$25.8 $25.0 $24.5 $22.9 $20.6

$70.9 $73.3

$74.3 $73.3 $73.0

$20 $21 $21 $22

$27

4Q13 1Q14 2Q14 3Q14 4Q14

Talcott Resolution AUM Mutual Funds AUM

Mutual Funds Segment Core Earnings & AUM1

4Q13 2Q14 1Q14 4Q14 3Q14

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Talcott Resolution: Variable and fixed annuity contract counts declined

13% and 18%, respectively, since Dec. 31, 2013

17

• Core earnings of $98 million, almost flat with

4Q13

− Lower fee income due to variable annuity (VA) run-

off partially offset by lower expenses, including lower

expenses related to contract holder initiatives

• VA contract counts decreased 3% during 4Q14

and 13% since Dec. 31, 2013

• Fixed annuity contract counts decreased 3%

during 4Q14 and 18% since Dec. 31, 2013

• Institutional covered lives declined 1% during

4Q14 and 3% since Dec. 31, 2013

• Guaranteed minimum withdrawal benefit

(GMWB) moneyness remained favorable

− 94% of GMWB contracts out-of-the-money; for those

contracts in-the-money, average moneyness of 11%

in 4Q14

• 91% of VA block beyond surrender charge period at

Dec. 31, 2014

1. Individual Annuity consists of U.S. annuity products for individuals, including variable, fixed and payout

2. Other consists of PPLI, residual income or tax benefits associated with the reinsurance of the policyholder and separate account liabilities of the Retirement Plans, Individual Life

businesses and International discontinued operations.

774 747 721 694 674

170 163

151 143

139

4Q13 1Q14 2Q14 3Q14 4Q14Variable Annuity Fixed Annuity and Payout

944 910

872 837

Individual Annuity Contract Counts (in thousands)

813

(14%)

$81 $89 $84 $83 $80

$18 $23

$17 $39

$18

4Q13 1Q14 2Q14 3Q14 4Q14Individual Annuity Institutional and Other

$98 $99

$112 $101

$122

Talcott Resolution Core Earnings

($ in millions)

1 2

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

U.S. government/government agencies

13%AAA12%

AA17%

A28%

BBB24%

BB & below6%

36%

17% 15%

12%

7%

4%

4% 3% 2%

$76.3 billion

High quality and well-diversified investment portfolio

18

• Fixed maturities portfolio weighted

average credit rating of “A+” as of

Dec. 31, 2014, up from “A” at Dec.

31, 2013 – 5.7% rated below investment grade as

of Dec. 31, 2014, down from 6.3% as

of Dec. 31, 2013

• Duration of 5.3 years as of Dec. 31,

2014 versus 5.2 as of Dec. 31,

2013

• Energy exposure4 totals $3.5 billion

in book value

˗ Generally high quality and well-

diversified

˗ Have reduced exposure selectively

and will continue to manage it

proactively

1. Includes high yield, emerging market and private placement securities

2. Includes commercial mortgage backed securities, collateralized debt obligations, and residential mortgage backed securities

3. Includes emerging market securities

4. Includes direct investments in energy companies, as well as direct investments in entities that have meaningful exposure to the energy sector, including sovereigns and government

agencies

5. Average credit ratings are based on availability, and are the midpoint of the applicable ratings among Moody’s, S&P, Fitch and Morningstar. If no rating is available from a rating

agency, then an internally developed rating is used

Investment Portfolio Composition (Excluding equity securities, trading)

As of Dec. 31, 2014

Fixed Maturities by Credit Rating5

$59.4 Billion – Weighted Average Rating A+

Corporate 1

Municipal

Real estate backed securities 2

US government/government agency & short-term

Mortgage loans

Limited partnerships

Policy loans, equity and other

Asset-backed securities

Foreign government/government agency 3

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

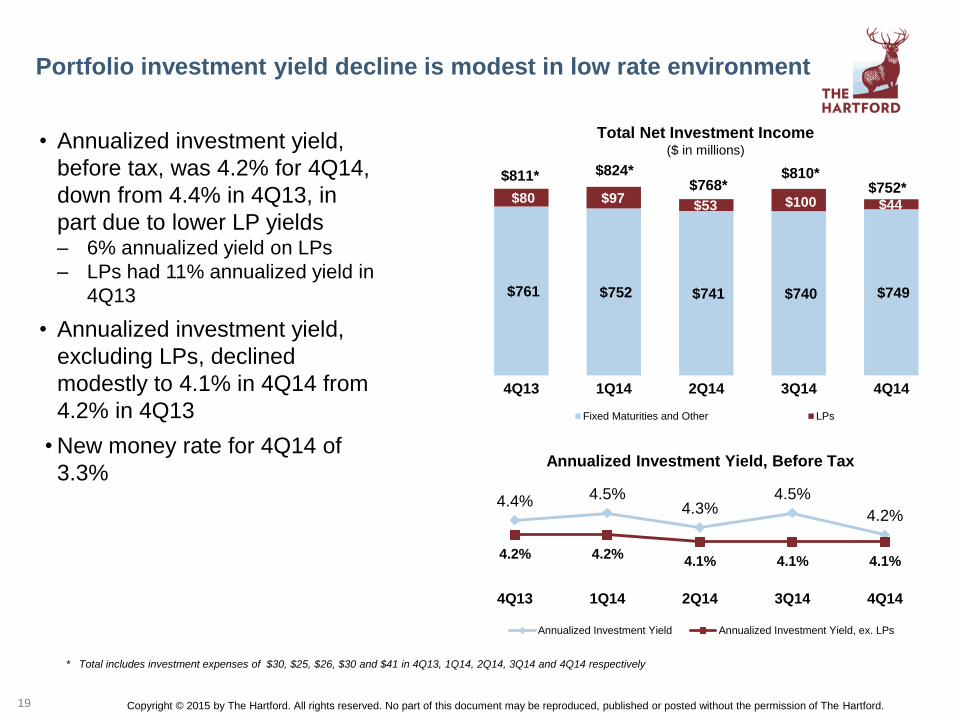

Portfolio investment yield decline is modest in low rate environment

19

* Total includes investment expenses of $30, $25, $26, $30 and $41 in 4Q13, 1Q14, 2Q14, 3Q14 and 4Q14 respectively

• Annualized investment yield,

before tax, was 4.2% for 4Q14,

down from 4.4% in 4Q13, in

part due to lower LP yields – 6% annualized yield on LPs

– LPs had 11% annualized yield in

4Q13

• Annualized investment yield,

excluding LPs, declined

modestly to 4.1% in 4Q14 from

4.2% in 4Q13

• New money rate for 4Q14 of

3.3%

$761 $752 $741 $740 $749

$80 $97 $53 $100 $44

4Q13 1Q14 2Q14 3Q14 4Q14

Fixed Maturities and Other LPs

Total Net Investment Income

($ in millions)

$811* $824* $768*

$810* $752*

4.4% 4.5% 4.3%

4.5%

4.2%

4.2% 4.2% 4.1% 4.1% 4.1%

4Q13 1Q14 2Q14 3Q14 4Q14

Annualized Investment Yield Annualized Investment Yield, ex. LPs

Annualized Investment Yield, Before Tax

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

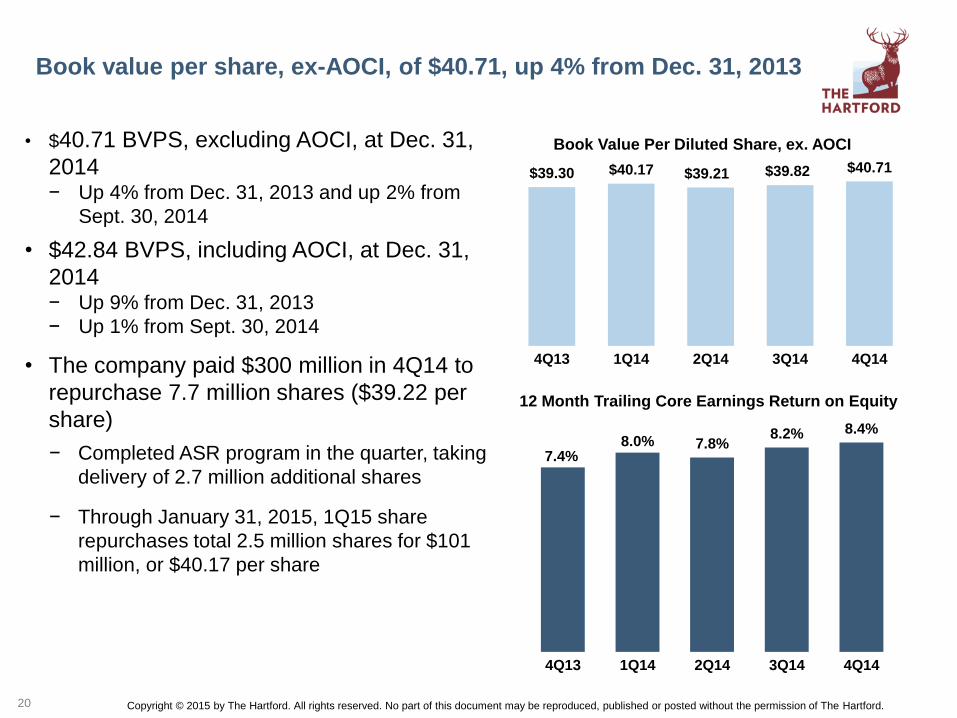

Book value per share, ex-AOCI, of $40.71, up 4% from Dec. 31, 2013

20

• $40.71 BVPS, excluding AOCI, at Dec. 31,

2014 − Up 4% from Dec. 31, 2013 and up 2% from

Sept. 30, 2014

• $42.84 BVPS, including AOCI, at Dec. 31,

2014 − Up 9% from Dec. 31, 2013

− Up 1% from Sept. 30, 2014

• The company paid $300 million in 4Q14 to

repurchase 7.7 million shares ($39.22 per

share)

− Completed ASR program in the quarter, taking

delivery of 2.7 million additional shares

− Through January 31, 2015, 1Q15 share

repurchases total 2.5 million shares for $101

million, or $40.17 per share

Book Value Per Diluted Share, ex. AOCI

$39.30 $40.17 $39.21 $39.82 $40.71

4Q13 1Q14 2Q14 3Q14 4Q14

7.4% 8.0% 7.8%

8.2% 8.4%

4Q13 1Q14 2Q14 3Q14 4Q14

12 Month Trailing Core Earnings Return on Equity

APPENDIX

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

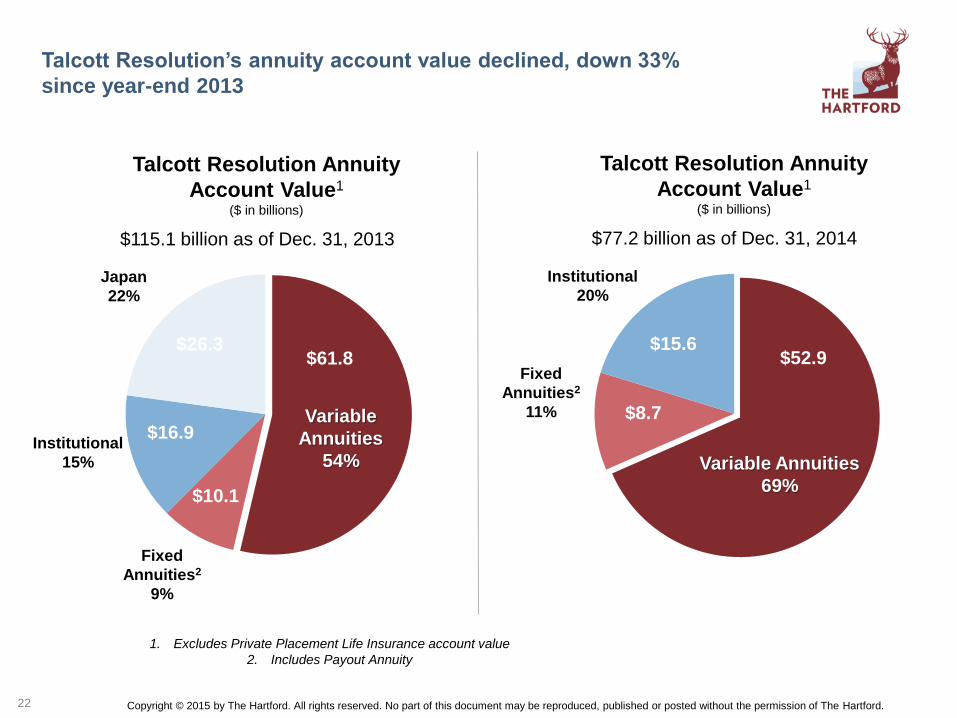

Talcott Resolution’s annuity account value declined, down 33%

since year-end 2013

22

Talcott Resolution Annuity

Account Value1

($ in billions)

$115.1 billion as of Dec. 31, 2013

Fixed

Annuities2

9%

Japan

22%

Variable

Annuities

54%

1. Excludes Private Placement Life Insurance account value

2. Includes Payout Annuity

$77.2 billion as of Dec. 31, 2014

Fixed

Annuities2

11%

Institutional

20%

Variable Annuities

69%

Institutional

15%

$26.3

Talcott Resolution Annuity

Account Value1

($ in billions)

$16.9

$10.1

$61.8 $15.6

$8.7

$52.9

Copyright © 2015 by The Hartford. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 23

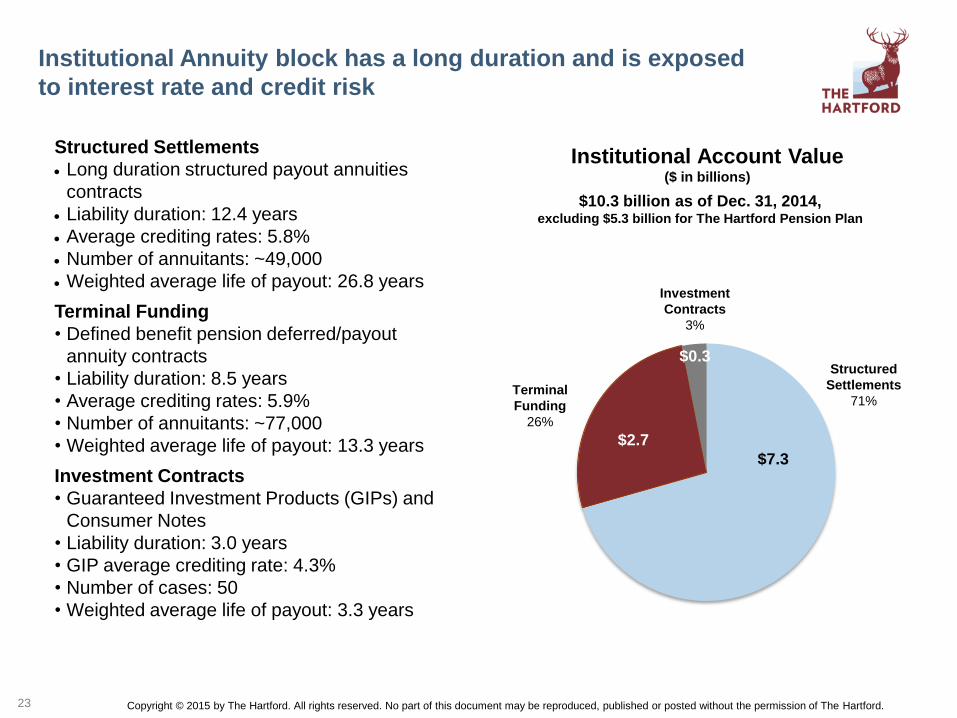

Institutional Annuity block has a long duration and is exposed

to interest rate and credit risk

$7.3

$2.7

$0.3

Institutional Account Value ($ in billions)

$10.3 billion as of Dec. 31, 2014, excluding $5.3 billion for The Hartford Pension Plan

Investment

Contracts

3%

Terminal

Funding

26%

Structured

Settlements

71%

Structured Settlements

Long duration structured payout annuities

contracts

Liability duration: 12.4 years

Average crediting rates: 5.8%

Number of annuitants: ~49,000

Weighted average life of payout: 26.8 years

Terminal Funding

• Defined benefit pension deferred/payout

annuity contracts

• Liability duration: 8.5 years

• Average crediting rates: 5.9%

• Number of annuitants: ~77,000

• Weighted average life of payout: 13.3 years

Investment Contracts

• Guaranteed Investment Products (GIPs) and

Consumer Notes

• Liability duration: 3.0 years

• GIP average crediting rate: 4.3%

• Number of cases: 50

• Weighted average life of payout: 3.3 years