Fourth Quarter 2013 CFPB – International Remittance Transfers CFPB – Credit Access Rule NCUA...

28

Compliance Outlook 2013 Fourth Quarter - 2014 First Quarter

-

Upload

dorthy-mcgee -

Category

Documents

-

view

217 -

download

2

Transcript of Fourth Quarter 2013 CFPB – International Remittance Transfers CFPB – Credit Access Rule NCUA...

Compliance Outlook

2013 Fourth Quarter -

2014 First Quarter

Program OverviewFourth Quarter 2013

• CFPB – International Remittance Transfers

• CFPB – Credit Access Rule

• NCUA Liquidity & Contingency Funding Plans

• NCUA Electronic Filing

• NCUA Charitable Donation Accounts

• FFIEC Social Media Guidance

Program OverviewFirst Quarter 2014

CFPB

• Ability to Repay / Qualified Mortgages

• Loan Originator Compensation

• Valuations and Appraisal Requirements

• HOEPA Rules

• Mortgage Servicing

CFPB – International Remittance Transfers 10/28/2013

• 100 IRT Exemption

• Disclosures

• Temporary Exceptions

CFPB – Credit Access Rule

The credit access rule allows:

• Joint-account income as an asset on credit applications.

11/4/2013

NCUA – Liquidity & Contingency Funding

3/31/2014

• FICUs with assets less than $50 million must maintain a basic written policy for managing liquidity and a list of contingent liquidity sources.

• FICUs with assets over $50 million must have a contingency funding plan that sets out strategies for liquidity shortfalls in emergency situations.

• FICUs with assets of $250 million or more must have access to a backup federal liquidity source for emergency situations.

NCUA – Electronic Filing

1/1/2014

NCUA – Charitable Donation Accounts

12/19/2013

• FCUs are now permitted to create and fund charitable donation accounts (CDAs), which may contain otherwise “impermissible” investments.

• CDAs are a hybrid charitable and investment vehicle, satisfying certain conditions. (721.3)

• Funding is limited to 5% of the FCU’s net worth at all times for the duration of the CDAs, measured quarterly during the Call Report cycle.

FFIEC Social Media Guidance

IMMEDIATE

Addresses the applicability of consumer protection and compliance laws, regulations, and policies to activities conducted via social media……

CFPB – Dealer Mark-ups

Indirect Auto Lending

o Credit unions that allow dealer mark-ups in their indirect lending program should be aware of details from a consent order to Ally Financial Inc. and Ally Bank.

CFPB – Ability to Repay (ATR)Must establish a consumer’s ability to repay:

At a minimum creditors must consider 8 underwriting factors:(1) Current or reasonably expected income or assets;

(2) Current employment status;

(3) Monthly payment on the covered transaction;

(4) Monthly payment on any simultaneous loan secured by same property;

(5) Monthly payment for mortgage-related obligations;

(6) Current debt obligations, alimony, and child support;

(7) Monthly debt-to-income ratio or residual income; and

(8) Credit history

Must use reasonably reliable third-party records to verify the information they use to

evaluate the factors.

CFPB – Qualified Mortgage (QM)Must establish a consumer’s ability to repay:

There are qualified mortgage standards that if met provide the presumption that the credit union has established the ability to repay – consider it a “Safe Harbor”.

CFPB – Loan Originator Compensation• MLO cannot receive compensation on any of the

mortgage loans’ terms or conditions.

• No Dual Compensation – if the MLO receives compensation from the borrower in connection with a mortgage loan, s/he cannot receive compensation from their organization or another person for the same transaction.

CFPB – Loan Originator Compensation MLO’s must be registered according to the SAFE Act. MLO’s AND CREDIT UNIONS must include their name and

NMLS ID on the following loan documents:– Credit application– Note or loan contract– Security instrument

Generally include on documents that require a member’s signature.

CFPB – Valuation & AppraisalTILA

– Applies to first lien or subordinate lien closed end loans secured by a member’s principal dwelling.

– Higher Priced Mortgage Loan (HPML):• First lien with an APR that exceeds the APOR by 1.5% or more• First lien jumbo loan with an APR that exceeds the APOR by 2.5% or

more.• Subordinate lien with an APR that exceeds the APOR by 3.5% or

morehttp://www.ffiec.gov/ratespread/newcalc.aspx

CFPB – Valuation & AppraisalTILA - Appraisal Requirements:• Disclose within three business days after receiving the

members’ applications that they are entitled to a free copy of their appraisal and can hire their own appraiser at their own expense for their own use.

• Disclosure Requirement (Appendix C – Form C-9)

“We may order an appraisal to determine the property’s value and charge you for this appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. You can pay for an additional appraisal for your own use at your own cost.”

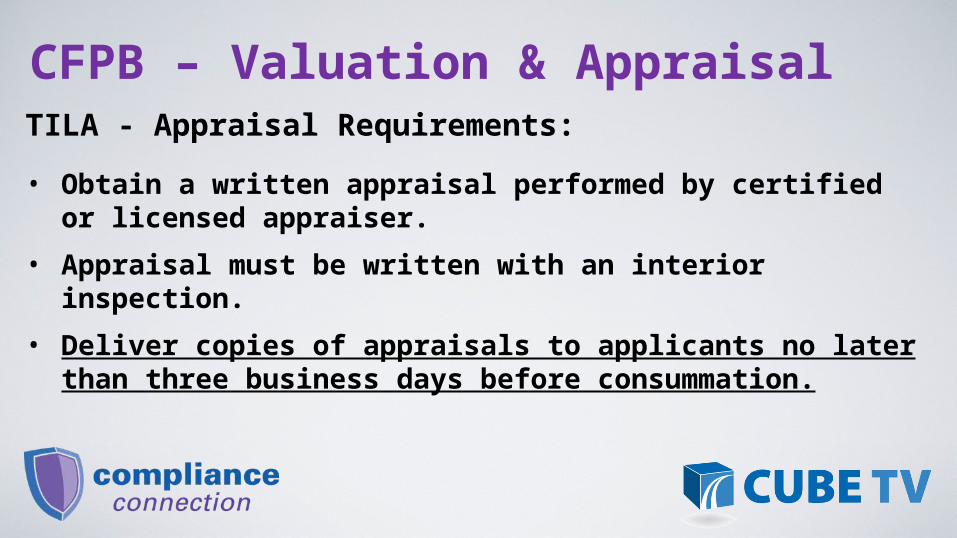

CFPB – Valuation & AppraisalTILA - Appraisal Requirements:

• Obtain a written appraisal performed by certified or licensed appraiser.

• Appraisal must be written with an interior inspection.

• Deliver copies of appraisals to applicants no later than three business days before consummation.

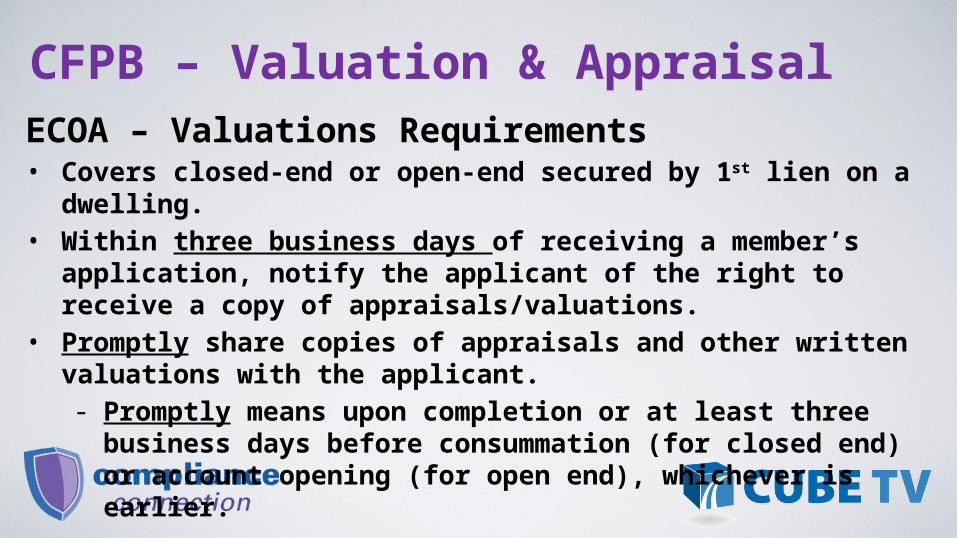

CFPB – Valuation & AppraisalECOA – Valuations Requirements• Covers closed-end or open-end secured by 1st lien on a

dwelling.• Within three business days of receiving a member’s

application, notify the applicant of the right to receive a copy of appraisals/valuations.

• Promptly share copies of appraisals and other written valuations with the applicant.- Promptly means upon completion or at least three

business days before consummation (for closed end) or account opening (for open end), whichever is earlier.

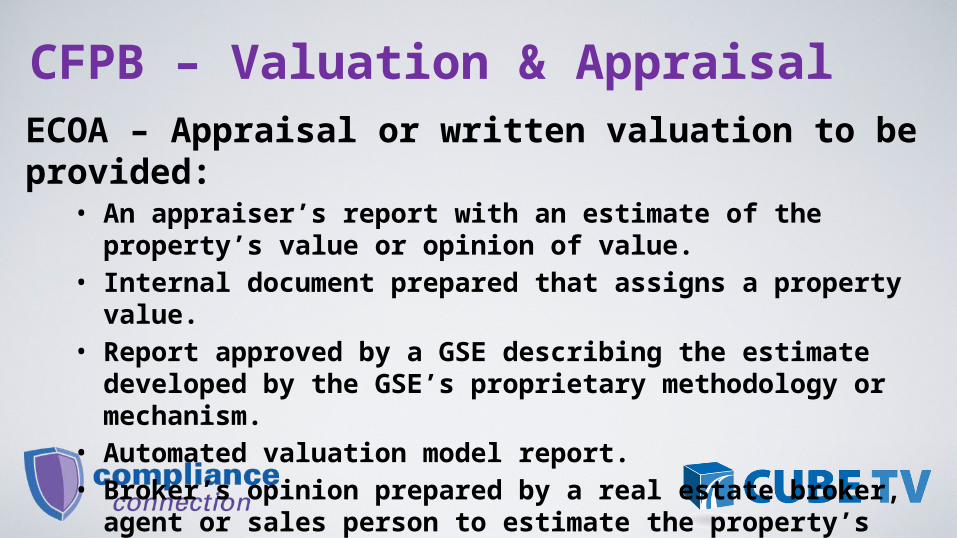

CFPB – Valuation & AppraisalECOA – Appraisal or written valuation to be provided:

• An appraiser’s report with an estimate of the property’s value or opinion of value.

• Internal document prepared that assigns a property value.

• Report approved by a GSE describing the estimate developed by the GSE’s proprietary methodology or mechanism.

• Automated valuation model report.• Broker’s opinion prepared by a real estate broker,

agent or sales person to estimate the property’s value.

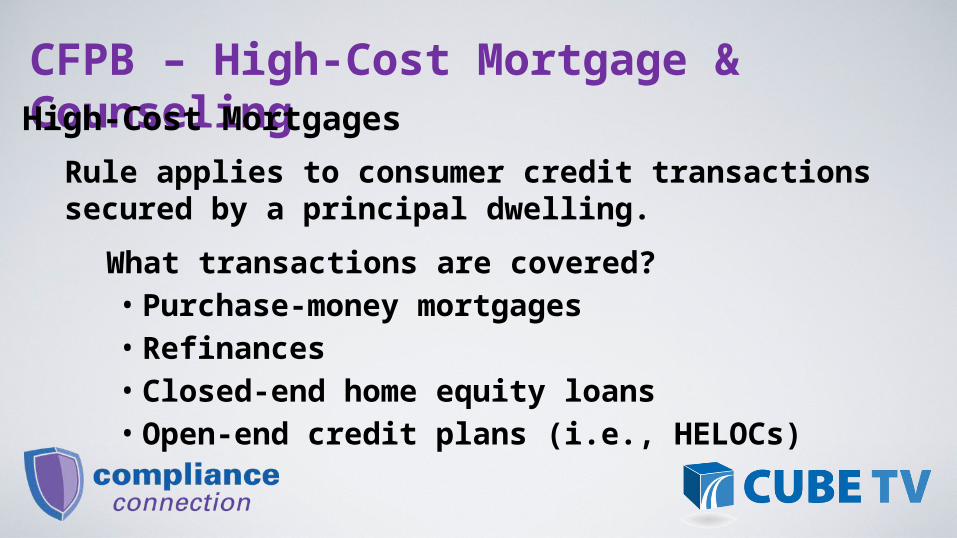

CFPB – High-Cost Mortgage & CounselingHigh-Cost Mortgages

Rule applies to consumer credit transactions secured by a principal dwelling.

What transactions are covered?• Purchase-money mortgages• Refinances• Closed-end home equity loans• Open-end credit plans (i.e., HELOCs)

CFPB – High-Cost Mortgage & CounselingHigh-Cost Mortgages - Special disclosures– Provided 3 days prior to consummation or account opening.

• Loan will not be effective until consummation or account opening occurs.

• Explain consequences of default.• Disclose loan terms such as APR, amount borrowed and monthly

payment.• Variable rate – explain maximum monthly payment that may be

required.Regulation Z – Appendix H (Sample H-16)

CFPB – High-Cost Mortgage & CounselingHigh-Cost Mortgages – Restriction on Terms

The rule bans certain loan features:– Balloon payments – except in 3 circumstances:

• Payment schedule is adjusted to accommodate member’s seasonal or irregular income.

• Short term bridge loan to finance new home purchase for member selling existing home.

• Credit union serving predominately rural or underserved areas and meets the ATR/QM rule.

– Prepayment Penalties– Due on Demand Features

CFPB – High-Cost Mortgage & CounselingHomeownership Counseling– Prior to making a high-cost mortgage, the credit union must

receive written certification that the member has received homeownership counseling on the advisability of the mortgage from a HUD approved counselor or state housing finance authority.

– The counselor must confirm that the member received ALL of the high-cost mortgage / RESPA disclosures before they can issue the certificate.

CFPB – High-Cost Mortgage & CounselingHomeownership Counseling

Credit unions must give applicants for federally related mortgages (whether or not it is high-cost) a written list of homeownership counseling organizations within 3 business days of receiving the application.

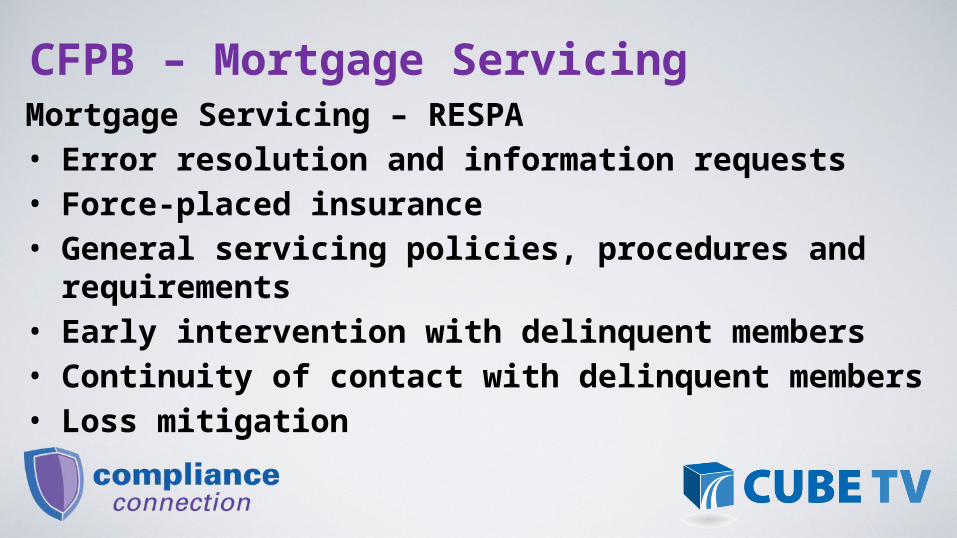

CFPB – Mortgage ServicingMortgage Servicing – RESPA• Error resolution and information requests• Force-placed insurance• General servicing policies, procedures and

requirements• Early intervention with delinquent members• Continuity of contact with delinquent members• Loss mitigation

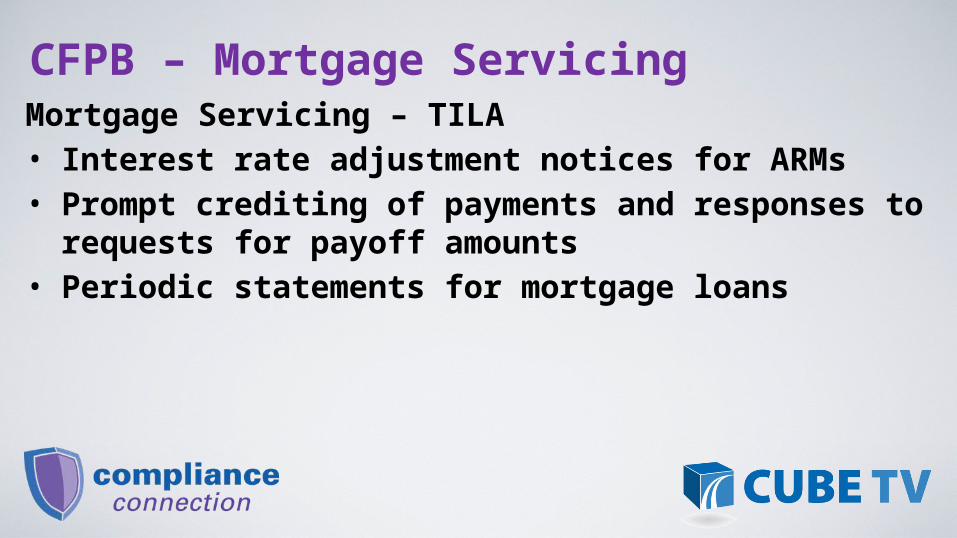

CFPB – Mortgage ServicingMortgage Servicing – TILA• Interest rate adjustment notices for ARMs• Prompt crediting of payments and responses to

requests for payoff amounts• Periodic statements for mortgage loans

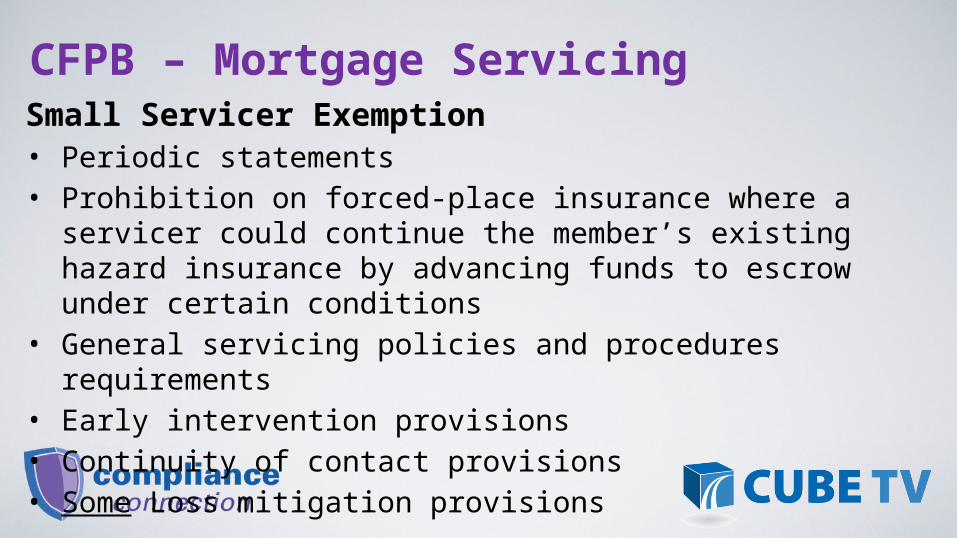

CFPB – Mortgage ServicingSmall Servicer Exemption• Periodic statements• Prohibition on forced-place insurance where a servicer

could continue the member’s existing hazard insurance by advancing funds to escrow under certain conditions

• General servicing policies and procedures requirements• Early intervention provisions• Continuity of contact provisions• Some Loss mitigation provisions

Thank you for joining us for this overview of the Credit Union Compliance Connection. Stay

Tuned……..