FortisBC Energy Inc. - British Columbia Utilities … in British Columbia, ... (December 2011) and...

1

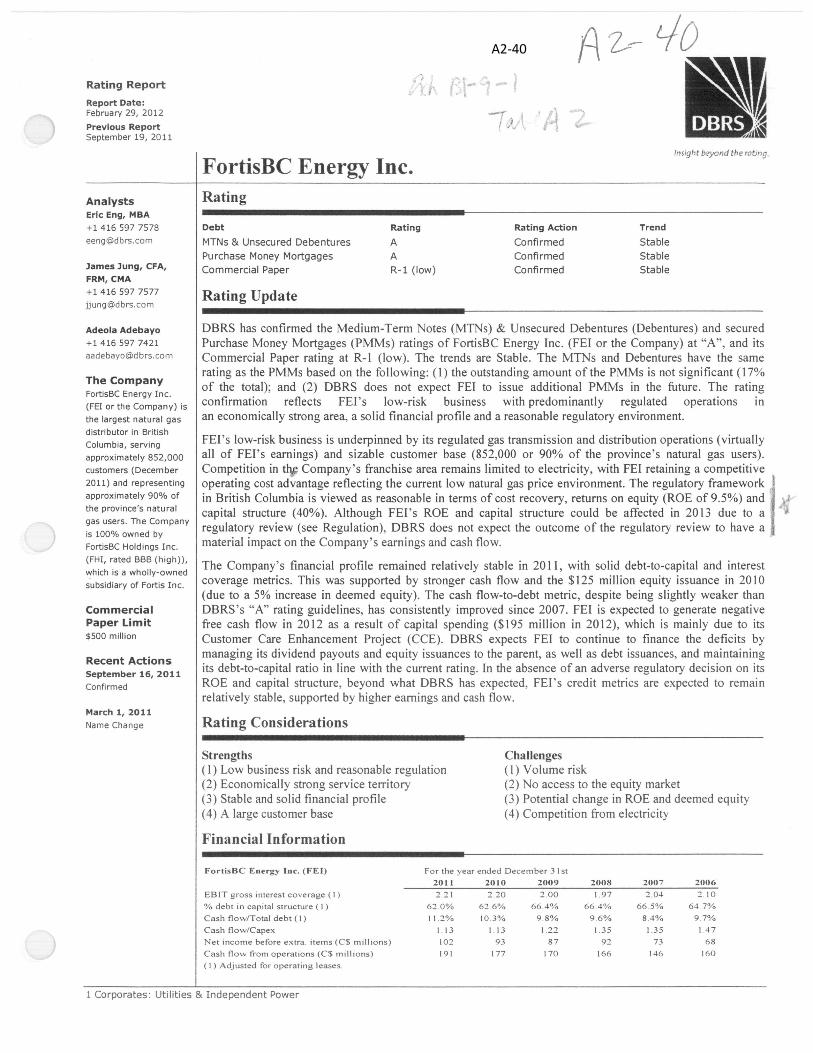

Rating Report Report Date: February 29, 2012 Previous Report September 19, 2011 Insight beyond ti>erati'19_ FortisBC Energy Inc. Analysts Eric Eng, MBA +14165977578 [email protected] James Jung, CFA, FRM, CMA +14165977577 [email protected] Adeola Adebayo +14165977421 [email protected] The Company FortisBC Energy Inc. (FEI or the Company) is the largest natural gas distributor in British Columbia, serving approximately 852,000 customers (December 2011) and representing approximately 90% of the province's natural gas users. The Company is 100% owned by FortisBC Hold ings Inc. (FHI, rated BBB (high)), which is a wholly-owned subsidiary of Fortis Inc. Commercial Paper Limit $500 million Recent Actions September 16, 2011 Confirmed March 1, 2011 Name Change Rating Debt MTNs & Unsecured Debentures Purchase Money Mortgages Commercial Paper Rating Action Confirmed Confirmed Confirmed Trend Stable Stable Stable Rating A A R-l (low) Rating Update DBRS has confirmed the Medium-Term Notes (MTNs) & Unsecured Debentures (Debentures) and secured Purchase Money Mortgages (PMMs) ratings of FortisBC Energy Inc. (FE I or the Company) at "A", and its Commercial Paper rating at R-l (low). The trends are Stable. The MTNs and Debentures have the same rating as the PMMs based on the following: (I) the outstanding amount of the PMMs is not significant (17% of the total); and (2) DBRS does not expect FEI to issue additional PMMs in the future. The rating confirmation reflects FEl's low-risk business with predominantly regulated operations in an economically strong area, a solid financial profile and a reasonable regulatory environment. FEI's low-risk business is underpinned by its regulated gas transmission and distribution operations (virtually all of FEI's earnings) and sizable customer base (852,000 or 90% of the province's natural gas users). Competition in t~ Company's franchise area remains limited to electricity, with FEI retaining a competitive operating cost advantage reflecting the current low natural gas price environment. The regulatory framework in British Columbia is viewed as reasonable in terms of cost recovery, returns on equity (ROE of 9.5%) and capital structure (40%). Although FEI's ROE and capital structure could be affected in 2013 due to a regulatory review (see Regulation), DBRS does not expect the outcome of the regulatory review to have a material impact on the Company's earnings and cash flow. The Company's financial profile remained relatively stable in 2011, with solid debt-to-capital and interest coverage metrics. This was supported by stronger cash flow and the $125 million equity issuance in 20 I0 (due to a 5% increase in deemed equity). The cash flow-to-debt metric, despite being slightly weaker than DBRS's "A" rating guidelines, has consistently improved since 2007. FEI is expected to generate negative free cash flow in 2012 as a result of capital spending ($195 million in 2012), which is mainly due to its Customer Care Enhancement Project (CCE). DBRS expects FEI to continue to finance the deficits by managing its dividend payouts and equity issuances to the parent, as well as debt issuances, and maintaining its debt-to-capital ratio in line with the current rating. In the absence of an adverse regulatory decision on its ROE and capital structure, beyond what DBRS has expected, FEI's credit metrics are expected to remain relatively stable, supported by higher earnings and cash flow. Rating Considerations Strengths ( I) Low business risk and reasonable regulation (2) Economically strong service territory (3) Stable and solid financial profile (4) A large customer base Challenges (1) Volume risk (2) No access to the equity market (3) Potential change in ROE and deemed equity (4) Competition from electricity Financial Information Forti.Be Energy Inc. (FEI) For the year ended December 3 t st 2011 2010 2009 2008 2007 2006 2.21 2.20 2.00 1.97 2.04 2.10 62.0% 62.6% 66.4% 66.4% 66.5% 64 70/0 I 1.20/0 10.30/0 9.80/0 9.6% 8.4% 9.70/0 1.13 I 13 1.22 1.35 1.35 147 102 93 87 92 73 68 191 177 170 166 146 160 EBIT gross interest coverage (I) 0/0 debt in capital structure (I) Cash flow/Total debt (I) Cash Flow/Capex Net income before extra. items (C$ millions) Cash flow from operations (C$ millions) (I) Adjusted for operating leases. 1 Corporates: Utilities & Independent Power A2-40

Transcript of FortisBC Energy Inc. - British Columbia Utilities … in British Columbia, ... (December 2011) and...

Rating ReportReport Date:February 29, 2012

Previous ReportSeptember 19, 2011

Insight beyond ti>erati'19_

FortisBC Energy Inc.AnalystsEric Eng, [email protected]

James Jung, CFA,FRM, [email protected]

Adeola [email protected]

The CompanyFortisBC Energy Inc.(FEI or the Company) isthe largest natural gasdistributor in BritishColumbia, servingapproximately 852,000customers (December2011) and representingapproximately 90% ofthe province's naturalgas users. The Companyis 100% owned byFortisBC Hold ings Inc.(FHI, rated BBB (high)),which is a wholly-ownedsubsidiary of Fortis Inc.

CommercialPaper Limit$500 million

Recent ActionsSeptember 16, 2011Confirmed

March 1, 2011Name Change

Rating

Debt

MTNs & Unsecured DebenturesPurchase Money MortgagesCommercial Paper

Rating Action

ConfirmedConfirmedConfirmed

Trend

StableStableStable

Rating

AAR-l (low)

Rating Update

DBRS has confirmed the Medium-Term Notes (MTNs) & Unsecured Debentures (Debentures) and securedPurchase Money Mortgages (PMMs) ratings of FortisBC Energy Inc. (FE I or the Company) at "A", and itsCommercial Paper rating at R-l (low). The trends are Stable. The MTNs and Debentures have the samerating as the PMMs based on the following: (I) the outstanding amount of the PMMs is not significant (17%of the total); and (2) DBRS does not expect FEI to issue additional PMMs in the future. The ratingconfirmation reflects FEl's low-risk business with predominantly regulated operations inan economically strong area, a solid financial profile and a reasonable regulatory environment.

FEI's low-risk business is underpinned by its regulated gas transmission and distribution operations (virtuallyall of FEI's earnings) and sizable customer base (852,000 or 90% of the province's natural gas users).Competition in t~ Company's franchise area remains limited to electricity, with FEI retaining a competitiveoperating cost advantage reflecting the current low natural gas price environment. The regulatory frameworkin British Columbia is viewed as reasonable in terms of cost recovery, returns on equity (ROE of 9.5%) andcapital structure (40%). Although FEI's ROE and capital structure could be affected in 2013 due to aregulatory review (see Regulation), DBRS does not expect the outcome of the regulatory review to have amaterial impact on the Company's earnings and cash flow.

The Company's financial profile remained relatively stable in 2011, with solid debt-to-capital and interestcoverage metrics. This was supported by stronger cash flow and the $125 million equity issuance in 20 I0(due to a 5% increase in deemed equity). The cash flow-to-debt metric, despite being slightly weaker thanDBRS's "A" rating guidelines, has consistently improved since 2007. FEI is expected to generate negativefree cash flow in 2012 as a result of capital spending ($195 million in 2012), which is mainly due to itsCustomer Care Enhancement Project (CCE). DBRS expects FEI to continue to finance the deficits bymanaging its dividend payouts and equity issuances to the parent, as well as debt issuances, and maintainingits debt-to-capital ratio in line with the current rating. In the absence of an adverse regulatory decision on itsROE and capital structure, beyond what DBRS has expected, FEI's credit metrics are expected to remainrelatively stable, supported by higher earnings and cash flow.

Rating Considerations

Strengths( I) Low business risk and reasonable regulation(2) Economically strong service territory(3) Stable and solid financial profile(4) A large customer base

Challenges(1) Volume risk(2) No access to the equity market(3) Potential change in ROE and deemed equity(4) Competition from electricity

Financial Information

Forti.Be Energy Inc. (FEI) For the year ended December 3 t st2011 2010 2009 2008 2007 2006

2.21 2.20 2.00 1.97 2.04 2.1062.0% 62.6% 66.4% 66.4% 66.5% 64 70/0

I 1.20/0 10.30/0 9.80/0 9.6% 8.4% 9.70/0

1.13 I 13 1.22 1.35 1.35 147102 93 87 92 73 68191 177 170 166 146 160

EBIT gross interest coverage (I)

0/0 debt in capital structure (I)Cash flow/Total debt (I)Cash Flow/CapexNet income before extra. items (C$ millions)Cash flow from operations (C$ millions)(I) Adjusted for operating leases.

1 Corporates: Utilities & Independent Power

A2-40

markhuds

Generec Cost Capitol