Forte oil annual report 2014

95

-

Upload

michael-olafusi -

Category

Investor Relations

-

view

120 -

download

59

Transcript of Forte oil annual report 2014

1964A.D

1979A.D

2010A.D

www.forteoilplc.com

MISSION

Building a long-term successful company and making Forte Oil Plc the investment of choice through positive actions that boost investor confidence at all times.

VISION

To be the Foremost Integrated Energy Solutions Provider in Nigeria.

COMMITTED: We are passionate about everything we do; committed to our values; our mission; to customer satisfaction and to flawless execution of our individual roles and responsibilities at all times.

OPEN: We operate open and transparent communications with ourselves and every stakeholder. We are transparent in our dealings and open in our engagements at all times. Open and honest communications give us a platform that creates a feedback mechanism for individuals and our system.

RESPECT: We believe that respect for stakeholders and fellow employees is sacrosanct and critical to actualizing the vision of the company.

RESPONSIVE: We are proud of our abilities to do things in a quick and efficient manner to generate results as speed is of the essence in our industry. We move at break-neck speed (without violating policies and guidelines) in getting things done so as to win market share and continue to create value for our shareholders.

We are passionate about our core values; the fulcrum and essence of our corporate existence. These guide our corporate actions and they are as follows:

Our Core Values

Contents

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4

Corporate Information

Results at a Glance

Notice of Annual General Meeting

Chairman’s Statement

Group CEO’s Statement

Subsidiaries Reviews

Internal Control & Risk Management

Company’s Secretariat’s Report

Profile of Directors

Reports of Directors

Report of the Audit Committee

Report of Independent Auditors

Consolidated Statement of Financial Position

Consolidated Statement of Comprehensive Income

Consolidated Statement of Cash Flows

Consolidated Statement of Changes in Equity

Notes to the Consolidated Financial Statements

Consolidated Statement of Value Added

Financial Summary

Proxy Form

Admission Card

Postage

E-Dividend Mandate

Authority to Electronically Receive Corporate Information

2

3

4

5

7

9

12

13

19

23

29

32

33

34

35

36

38

86

87

89

90

91

92

93

01

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 402

FEMI OTEDOLA, CON - Chairman

AKIN AKINFEMIWA - Group Chief Executive Officer

JULIUS B. OMODAYO-OWOTUGA, CFA - Group Chief Financial Officer

LAYIWOLA BOLODEOKU - Director

GRACE C. EKPEYONG - Director

CHRISTOPHER ADEYEMI - Director (Independent)

PHILIP M. AKINOLA - Director

KOREDE OMOLOJA - Director

AKINLEYE OLAGBENDE - Company Secretary

UKPAI OKWARAMANAGING DIRECTORAP OIL AND GAS GHANA LIMITED

KENNETH OLISA MANAGING DIRECTOR FORTE UPSTREAM SERVICES LTD

ADEYEMI ADENUGA (FNSE)MANAGING DIRECTORGEREGU POWER PLC

Board of Directors

ECOBANK NIGERIA PLCHERITAGE BANKING COMPANY LTD

Corporate Information

GUARANTY TRUST BANK PLCFIRST BANK OF NIGERIA LTD

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 03

2014 Group Financial Result at a Glancefor the year ended 31 December, 2014

N'000 N'000

2014 2013

N170bnRevenue

N6bn N18.5bnGross ProfitProfit Before Tax

Revenue 128,027,744

Cost of sales (115,766,506)

Gross profit 12,261,238

Profit before income tax 6,524,550

Income tax expense (1,520,153)

Profit after tax for the year 5,004,397

Other comprehensive loss net of taxes (108,263)

Total comprehensive income for the year 4,896,134

Total comprehensive income attibutable to:

Owners of the company 4,549,323

Non controlling interests 346,811

4,896,134

Earnings per share

Basic/dilluted earnings per share in (N) 4.32

170,127,978

(151,663,049)

18,464,929

6,006,298

(1,549,681)

4,456,617

(78,018)

4,378,599

2,322,246

2,056,353

4,378,599

2.20

NOTICE IS HEREBY GIVEN that the Thirty Sixth Annual General Meeting of the Members of FORTE OIL PLC will hold at the Bespoke Event Centre, Lekki-Ajah Expressway, Lagos on April 15, 2015 at 10:00 a.m. to transact the following business: ORDINARY BUSINESS

1. To present the Report of the Directors, the Consolidated Statement of Financial Position with the Statement of Comprehensive Income at 31st December, 2014 and the report of the Auditors and Audit Committee thereon.

2. To re-elect Directors under Articles 89 of the Company's Articles of Association

3. To declare a dividend

4. To authorize the Directors to fix the remuneration of the Auditors.

5. To elect/re-elect the members of the Audit Committee.

SPECIAL BUSINESS

1. To re-appoint Ven Layi Bolodeoku who has attained Seventy(70) years of age pursuant to Section 256 of the Companies and Allied Matters Act of 2004

2. To issue a bonus share of one (1) ordinary share for every five(5) fully paid ordinary shares of 50 kobo each held by each shareholder as at the closure of the Company's register on March 31, 2015. The Bonus shares will rank parripassu for all purposes and in all respects with the existing shares of the Company and the Board of Directors be and are hereby also authorized generally to do and effect all acts and things required to give effect to this Resolution except that such bonus shares shall not qualify for dividend recommended by the Directors in respect of the year ended December 31, 2014.

PROXY

A member entitled to attend and vote at the Annual General Meeting is entitled to appoint a proxy to attend and vote in his stead. A proxy need not be a member of the Company. For the appointment to be valid, a completed and duly stamped proxy form by the Commissioner of Stamp Duties must be deposited at the office of the Registrar, Veritas Registrars Limited, Plot 89A Ajose Adeogun Street, Victoria Island, Lagos not less than 48 hours before the time fixed for the meeting.

CLOSURE OF REGISTER

The Register of Members will be closed on April 01 to April 07, 2015 to enable the Registrars prepare for the payment of dividend.

DIVIDEND WARRANTIf the dividend recommended is approved, dividend warrants will be posted on April 22, 2015 to shareholders whose names appear on the Company's Share Register at the close of business on March 31, 2015.

AUDIT COMMITTEEIn accordance with Section 359(5) of the Companies and Allied Matters Act of 2004, any member may nominate a shareholder as a member of the Audit Committee by giving in writing of such nomination to the Secretary of the Company at least 21 days before the Annual General Meeting.

Dated March 16, 2015. BY ORDER OF THE BOARD

AKIN OLAGBENDECompany SecretaryFRC/2013/NBA00000003160FO House, 13 Walter Carrington CrescentVictoria Island,Lagos.

F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4

Notice of Annual General Meeting

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C 04

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 05

istinguished shareholders, members of

Dthe Board of Directors, gentlemen of

the press, invited guests, ladies and

gentlemen. I am honoured to present an

overview of the major developments that took

place in our operating environment as well as

the summary of the company's performance for

the financial year ended 31st December, 2014.

The Operating Environment

The country’s GDP grew by 6.23% in 2014 with

2015 forecast put at 5.54%. The economy slowed

in Q4 2014 as it advanced 5.94% year on year.

The Non-oil Sector continues to drive growth

through agriculture, services and real estate

activities.

Our operating environment remains very

challenging with enormous economic and

security issues. Economic issues bothering on the

strength of the local currency in the era of falling

crude prices and tight liquidity in the Nigerian

Money Market resulting in high interest rates.

Also the reduced revenue accruing to the

Federal Government of Nigeria affected the

reimbursement of our fuel subsidies under the

PSF scheme; this non payments coupled with the

illiquid money market caused a 124% increase in

our finance cost.

Security challenges in some areas within the

northern region also negatively impacted our

activities. Retail outlets in the affected area

were closed and rendered inoperative for the

most part of the year.

Despite these challenges, the business

demonstrated resilience and grew through

strategic partnerships that yielded the desired

results.

The 2014 Financial Results

2014 financial year was the third and final year of

our 3- year strategic transformation initiatives

and we are pleased with our 2014 performance

amid the challenging environment highlighted

above.

We closed the year with a 33% growth in revenue

to post N170bn compared to N128bn same

period in 2013. Likewise, operating profit

increased by 30% to N8.14bn compared to

N6.27bn recorded in 2013. Profit before income

tax declined by 7.94% to N6bn from N6.5bn of

same period in 2013 while profit after tax

dropped by 11% to N4.46bn from N5bn of 2013.

The growth in revenue is attributable to the

significant increase recorded in the sales of our

fuel products segment, comprising Premium

Motor Spirit (PMS), Automotive Gas Oil (AGO),

Aviation Turbine Kerosene (ATK); as well as

Production Chemicals; Lubricants and Greases.

The power entity, Geregu Power Plc also

contributed significantly to the revenue streams.

The 7.94% drop in the Group's Profit before Tax is

largely attributable to the 10% devaluation of

the Naira in November 2014 and increased

finance costs caused by huge subsidy

Chairman’s Statement

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 406

receivables from the Federal Government of

Nigeria. These receivables were outstanding for

an average of 270 days compared to the 45

days provided for in the PSF scheme. Also in

2013, we had non-recurring income of N2.11

billion from sale of properties and interest

received from PPPRA relating to late payment of

subsidies in 2010 and 2011. We believe the

business is resilient, stronger, sustainable and

better positioned for the challenges ahead.

The earnings from our power subsidiary is a clear

indication that our diversification strategies are

yielding the desired results, having contributed

12% to the Group profit before taxes. We

recently awarded a contract for the major

overhaul of the Plant to Siemens AG and expect

this to be completed within the next twelve

months. We strongly believe that, this segment of

our business will drive growth going forward.

Awards

During the year 2014, your company received

various awards including but not limited to:

1. Top 100 business in Nigeria by His Excellency

Dr. Ebele Goodluck Jonathan, GCFR,

President of the Federal Republic of Nigeria.

2. Top 100 Most respected companies in

Nigeria by BusinessDay Newspaper.

3. Brand excellence in Oil and Gas by

Marketing World Awards.

Changes in the Structure of the Board.

There were no changes to the board

composition during the year. We however now

have a Board Finance and Strategy Committee

with a view to further strengthening our

corporate governance practices in line with

world-class standards. This committee shall

have oversight responsibility over capital

optimisation, budgets, strategic planning,

investments and projects. Its recommendations

shall be prepared and sent to the Board of

Directors for approval.

The committee has five members; two non-

executive directors, two executive directors and

our independent director as the Chairman.

Dividend

The Board proposes a 250 kobo per share

(N2.7bn) dividend to be distributed for the year

ended December 2014 subject to the

deduction of appropriate taxes.

Bonus

The Board also proposes an additional bonus

share for every five shares held in line with our

mission of making Forte Oil Plc the investment of

choice.

The Future

We remain committed to our vision of being the

foremost integrated energy solutions provider in

Nigeria with strong presence in downstream

operations, power and upstream services. We

will be expanding our reach in the near term to

the upstream sector and other related high

margin businesses that will continue to maximize

shareholders' wealth.

We thank our shareholders for their firm belief in

us in the course of our business transformation

and also use this opportunity to assure them of

better performance in the future.

I thank you for continually investing in Forte Oil

PLC.

Femi Otedola, CON

Chairman

FRC/2013/IODN/00000002426

March 2015

Chairman’s Statement (Cont’d)

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 07

e successfully concluded our 3-year

Wbusiness transformation in the year

2014 and I am pleased to inform you

that this transformation was unprecedented

having witnessed a complete turnaround of

our company from a loss making entity of

NGN19 Billion loss in 2011to a profit and

sustainable business entity within the last 3 years

and also delivering annual group profit of

NGN1.1Billion in 2012, NGN 6.5 Billion in 2013

and NGN 6.01 Billion in 2014. Our objective of

creating a lean, talent based and technology-

driven business resulted in increased market

share and revenues from all product lines that

has seen us come from the bottom position to

the league of the top three petroleum products

marketing companies in the industry in the

period under review. We resumed the payment

of dividend after four years of huge losses and

negative retained earnings having successfully

executed a capital reorganisation exercise in

line with our mission of building a long term

successful company and making Forte Oil Plc.

the investment of choice through positive

actions that boost investor confidence at all

times. Our drive to operate a high performing

organisation on the bedrock of solid corporate

governance practices and transparency

ranked us not only as a consistent early filer on

the NSE but also as the first Nigerian company in

50 years to submit its 2013 audited financials on

January 31 2014 and of course our subsequent

inclusion into the Morgan Stanley Capital

I n t e r n a t i o n a l F r o n t i e r M a r k e t s . O u r

transformation initiatives did not also go

unrecognised. Forte Oil Plc. was adjudged one

of Nigeria's Top 100 companies by the Federal

Government of Nigeria in addition to receiving

the award for the best CEO in Corporate

Nigeria among the Top 25 CEOs of quoted

companies award in Nigeria organized by the

Business Day research and intelligence unit.

Forte Oil Plc., was also admitted into British

Safety council as a result of its zero lost time to

Injury (LTI) and fatalities during the year under

the review.

Overview of our Financial Performance in 2014

Forte Oil Plc's revenue increased by 33% to

N170.13 billion compared to N128.03 billion

recorded same period in 2013 largely due to

ongoing strategic retail network expansion,

growth of our commercial customer base and

gains from our recent diversification into the

power sector- Geregu Power Plc. which

contributed 5.33% at the Revenue level.

Gross profit increased by 51% to N18.46 billion

compared to N12.26 billion recorded same

period in 2013 as a result of improved sourcing

of petroleum products, raw materials,

aggressive marketing of our lubricants and

specialties products and sales of petroleum

products through more profitable channels.

Operating profit increased by 30% to 8.14 billion

compared to N6.27 billion recorded same

period in 2013 due to gains from operational

Akin Akinfemiwa Group Chief Executive Officer

The Group CEO's Report

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 408

efficiencies and improved logistics with the

injection of 100 brand new company-owned

trucks to support the uninterrupted supplies of

petroleum products across the country and

exceptional customer service delivery.

Profit before tax of N6.01billion recording a 7.94%

decrease compared to N6.52 billion same

period in 2013 as a result of the huge finance cost

incurred, 10% devaluation of the naira in 2014

and poor performance from APOG due to

recent economic meltdown and the harsh

business environment in Ghana.

2015 and Beyond:

We are confident that we are on the right path in

our pursuit to become Nigeria's Foremost

Integrated Energy Solutions Provider as we unveil

our 5-year Growth and Consolidation Strategy

for all our strategic business units.

Our quest to dominate the downstream

petroleum sector in Nigeria and by extension

Africa, remains a key aspect of our consolidation

strategy. We are currently pursuing opportunities

for mergers and acquisition in a bid to drive

volume, revenues and ultimately maximize

profits for our shareholders. The Organic growth

of our downstream business through the

acquisition of strategically positioned outlets to

create an optimized network and drive revenues

and profits remain on course. Expanding our

retail presence supports our drive to boost our

Non-Fuel Revenue income through strategic

alliances that will sustain superior customer

experience.

Our aggressive drive to compete effectively in

the upstream sector led to a major restructuring

exercise of our upstream services subsidiary -

African Petroleum Oilfield Services (APOS)

wherein the company's name changed to Forte

Upstream Services. Our priorities in this regard

are; focus on higher margin related businesses,

position the renewed entity to take full

advantage of the Nigerian Local Content,

part ic ipate in the proposed Federa l

Government Nigeria sale of marginal oil fields

and divestment of International Oil Companies

investments in local oil blocks.

We remain committed to making our Power

business a key driver of our growth initiatives by

ensuring that it contributes 40% to our Group PBT

in the near future. To this end, we have

contracted and commenced a Major Overhaul

of our 414-MW Geregu Power Plant at a cost of

USD 83 Million Naira to Siemens AG.

As part of our efforts to further boost investor

confidence, Forte Oil Plc is aiming for the listing of

its shares on the newly established NSE premium

board by submitting itself for evaluation under

the Corporate Governance Rating System

(CGRS) developed by the NSE and the

Convention for Business Integrity (CBI) in the very

near future.

Our commitment to continually invest in a highly

skilled, vibrant and motivated workforce remains

unflinching. We have and will continue to review

our employee compensation and benefits

system and our manpower development needs

in tune with the dynamics of our business

operating environment. We are also creating a

platform that will serve as an umbrella for all our

CSR initiatives in our bid to ensuring that they

yield their intended objectives.

Akin Akinfemiwa,

Group Chief Executive Officer

FRC/2013/IODN/00000001994

The Group CEO's Report (Cont’d)

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 09

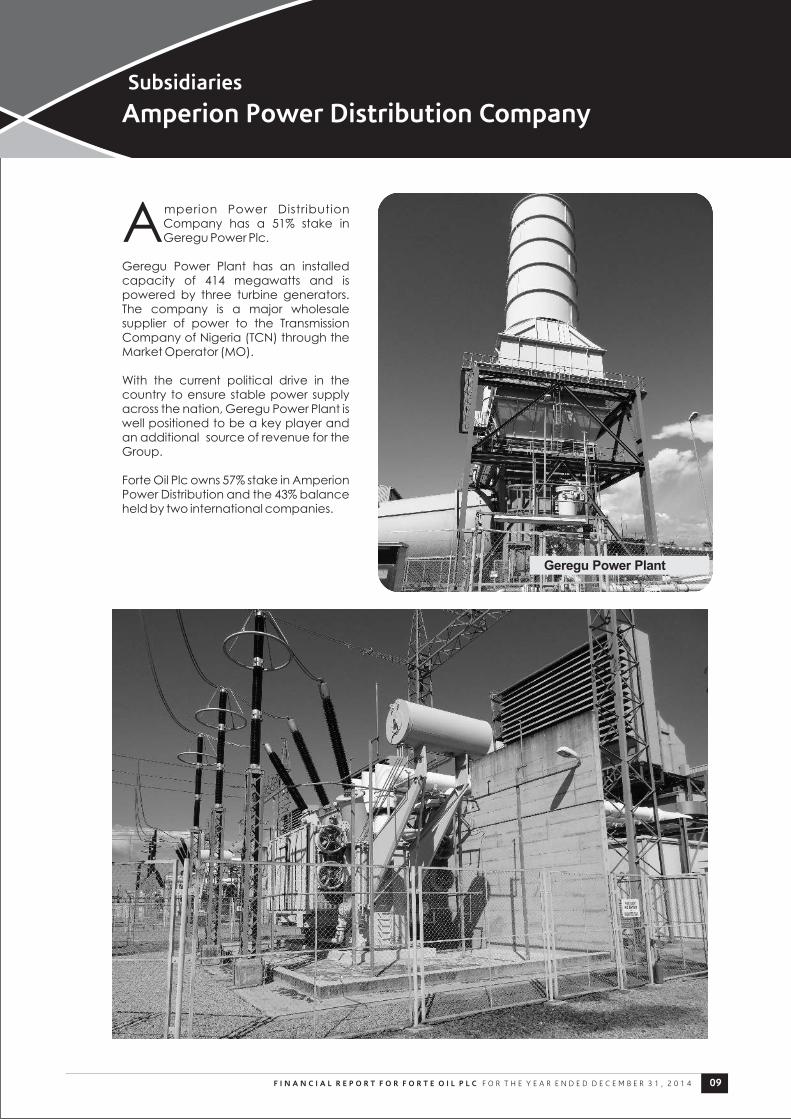

mperion Power Distribution

ACompany has a 51% stake in Geregu Power Plc.

Geregu Power Plant has an installed capacity of 414 megawatts and is powered by three turbine generators. The company is a major wholesale supplier of power to the Transmission Company of Nigeria (TCN) through the Market Operator (MO).

With the current political drive in the country to ensure stable power supply across the nation, Geregu Power Plant is well positioned to be a key player and an additional source of revenue for the Group.

Forte Oil Plc owns 57% stake in Amperion Power Distribution and the 43% balance held by two international companies.

Geregu Power Plant

Subsidiaries

Amperion Power Distribution Company

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 410

However, the Company was able to achieve a profit before tax of NGN 363,743,000 as against NGN 485,190,000 in the year 2013 (a decrease of 25%). This decrease was due to the delay in the implementation of our drilling contracts, these contracts have been re-scheduled for 2015.

As part of our continued business strategy for sustained growth and profitability going forward in 2015, the Company is poised to increase its proportion of the provision of production chemicals and the completion fluids contract with SNEPCO through optimization of existing contracts. The LMP, Onne is being refurbished to meet current standards to increase capacity in carrying out our obligations for the existing contracts and our optimization strategy.

FUS is still operating its contracts with ADDAX valued over 2m million for the supply of production chemicals, Laboratory Services and Wellbore c l e a n u p f l u i d s a n d h o p e f u l o f t h e commencement of supplying drilling fluids and services in 2015.

In addition, the Company was successful on its submission of both technical and commercial tenders/bids to various International Oil Companies (IOCs) and Indigenous Exploration & Production Companies with the hope of breaking new grounds for improved performance taking into consideration our indigenous status and the opportunities offered by the Nigerian Content Act to support our operations.

We are poised to partner with one of the most successful drilling companies in the world as they re-establish their presence in Nigeria and hopeful that this arrangement will further reposition FUS to be one of the leading upstream services company in Nigeria and beyond ultimately.

It is expected that these various business decisions will aid the Company in its aspiration to attain leadership position in the supply of oilfield production, drilling fluids chemicals and other oilfield services.

INTRODUCTIONForte Upstream Services Limited formerly known as African Petroleum Oilfield Services Limited (APOS) is a fully owned subsidiary of Forte Oil Plc. The Company is engaged in the sale of production and drilling fluids chemicals and other engineering services to both local emerging & major international oil exploration and production companies in Nigeria.

FUS 2014 BUS INESS OUTLOOK AND PERFORMANCE REVIEWIn 2014, the Company continued its supply of production chemicals, drilling fluids and completion fluids to local and international oil exploration and production companies such as the Shell, Addax, Afren, e.t.c. During the period under review, the Company operated under a challenging environment.

Subsidiaries Cont’d

Forte Upstream Services Limited (FUS)

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 11

AP Oil and Gas Ghana Limited a wholly owned subsidiary of Forte Oil Plc is a marketer of refined petroleum products and lubricants. It is one of the 122 Oil Marketing Companies (OMCs) trading in Ghana oil and gas industry. The downstream business in Ghana segmented into two: Oil Marketing Companies (OMCs) and Bulk Distribution Companies (BDCs) has over the years witnessed a continuous proliferation of both BDCs and OMCs. Four dominant OMCs (GOIL, Shell, Total Plc and Star Oil) accounted for about 44% of the market share while the rest of other 120 OMCs struggle with the remaining 56% with none having more than 3%. The competition no doubt has remained intense as in the previous years leading to market share shifts and buyers market.

The general business environment is stil l characterized by cedi devaluation, unpaid fuel subsidies by government, huge credit transactions due to buyer market scenarios with the attendant Trade Accounts Receivables (TAR) challenges,

difficulties in securing finance from the banks etc. In the year under review BDCs experienced difficulties in accessing Letter of Credits from Banks due to huge debts owed the banks by the later. This situation for some months adversely affected products supply and availability and as well changed industry trade terms to cash and carry thereby increasing increased finance cost.

However, despite all these challenges, the company’s ongoing restructuring exercise has continued to focus on retail network expansion, sound and efficient service delivery, increased commercial customer base, strong credit control and TAR management, among others. Fortunately the company is steadily inching towards the desired sales volume target as evidenced by the significant leap in sales volume during the last quarter of the year 2014 and shall strive to consolidate and improve on this last quarter performance in the year 2015 .

PERFORMANCE REVIEW

Subsidiaries Cont’d

AP Oil and Gas Ghana Ltd

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 412

Internal Control Systemhe Board is responsible for maintaining a

Tsound system of internal control to safeguard shareholders’ investment and

the assets of the Company. The system of internal control is to provide reasonable assurance against material misstatement, prevent and detect fraud and other irregularities.

There is an effective internal control function within the Company which gives reasonable assurance against any material misstatement or loss. The Board and Management will continue to review the effectiveness and the adequacy of the company's internal control systems and update such as may be necessary.

The Directors are responsible for the overall management of risk as well as expressing their opinion on the effectiveness of the process. The risk management framework is integrated into the day-to-day operations of the business and provides guidelines and standards for administering the acceptance and on-going management of key risks such as financial,

compliance/legal/regulatory, reputational, strategic and operational risk. The Directors are of the view that effective internal audit function exists in the company and that r i sk management controls and compliance system are operating efficiently and effectively in all respects.

Risk Management

Internal Control & Risk Management

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 13

The Chairman is responsible for the leadership and management of the Board and for ensuring that the Board and its committees function effectively according to their various charters. One way in which this is achieved is by ensuring Directors receive accurate, timely and clear information. He is also responsible for agreeing and regularly reviewing the training and development needs of each Director which he does with the assistance of the Company Secretary.

The Chief Executive Officer bears overall responsibility for the implementation of the strategy agreed by the Board, the operational management of the Company and the subsidiaries. He is supported in this by the Executive Committee, which he chairs.

The Board of Forte Oil Plc is made up of executive and non-executive directors based on integrity, professionalism, recognition and the ability to add value to the organization. The membership of the Board comprises of Directors with a broad range of expertise, skills and experience from different industries and businesses.

The Company currently has eight (8) members which include the Chairman, four (4) Non-Executive Directors, one (1) Independent Director and two (2) Executive Directors to ensure the stability and accountability of the organization at all times.

The Non-executive Directors bring a wide range and balance of skills and international business experience to Forte Oil Plc. Through their contribution to Board meetings and to Board committee meetings, they are expected to challenge constructively and help develop proposals on strategy and bring independent judgment on issues of performance and risk. Generally, prior to each meeting of the Board, the Chairman and the Non-executive Directors meet

Board of Directorswithout the Executive Directors to discuss, among other things, the performance of individual Executive Directors.

The Board as the focal point of the Company's corporate governance system is ultimately accountable and respons ib le for the performance and affairs of the Company with a commitment to uphold and discharge its legal, financial and regulatory responsibilities to all at all times. The Board is also responsible for the strong financial performance of the Company and approves the design of the Company's annual strategy and monitors the implementation of the set objectives.

The governance structure of the Company is designed to ensure that the board performs its functions as provided for in the charters and in accordance with all legislative and regulatory developments and trends in governance. Annually, the board of directors attend bespoke Board trainings/sessions, with the aim of ensuring that they are updated on international best governance practices, industry and global trends. Throughout the year, regular updates on developments in legal matters, governance and accounting are provided to Directors. Additional training is available so that Directors can update their skills and knowledge as appropriate. The performance of the Board is reviewed annually by an independent consultancy firm whose report is published in the yearly financial report of the company.

Furthermore, all Directors may seek independent professional advice in connection with their role as a Director. All Directors have access to the advice and services of the Company Secretary. The Company has provided both indemnities and directors' and officers' insurance to the Directors in connection with the performance of their responsibilities.

The Board CommitteesThe Board during the period under review, increased its Board Committees to five with the establishment of the Board Finance and Strategy Committee to assist the Board of Directors in fulfilling its oversight responsibilities to the Company. This Committee is in addition to the Corporate Governance and Remuneration Committee, the Risk Management Committee and the Statutory Audit Committee.

Each Committee comprises of non- executive directors; (except the Finance and Strategy Committee and the Risk Management Committee which has the two Executive directors as members) with a written charter. Each Committee meets on a quarterly basis to discuss matters pertaining to its terms of reference in addition to regular reports provided through the Company Secretariat on any significant issues to

Company Secretariat’s Report For 2014 Annual Report

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 414

be addressed by the Committee.

Outside of these Board Committees, there are other several management committees namely the Executive Management Committee, Management Committee, Risk Committee, Credit Risk Committee, Crystalized Assets Committee, Branding Committee and Inventory Management Tenders and Contracts Committee charged to ensure that the activities of the Company are at all times done with high standards of professionalism, accountability and integrity .

A Risk Management structure is also in place to assist the Board in fulfill ing its oversight

responsibilities in the identification, assessment, management of risk and adherence to internal risk management policies and procedures. This process ensures that the Company is aware of changes in the economic and business environment and compliance with regulations that impact on the company. Recently, the Firm of KPMG was engaged to update our enterprise risk management framework to align with best practice standards and to guide on any development needs or required improvements in our risk processes.

During the period under review, there was no change to the existing Board structure.

Director Amount

(N)

Mr. Femi Otedola, CON 750,000.00

Dr. Mrs. Grace Ekpenyong 500,000.00

Mrs. Korede Omoloja 500,000.00

Mr. Philip Akinola 500,000.00

Mr. Christopher Adeyemi 500,000.00

Ven. Layi Bolodeoku 500,000.00

Mr. Akin Akinfemiwa NIL

Mr. Julius B. Omodayo-Owotuga, CFA NIL

Directors Remuneration

Statement of Compliance with the Corporate Governance Code

Forte Oil Plc affirms its commitment and desire to continue to adhere to the principles of excellent corporate governance practices. The Company strives to carry out its business operations on the principles of integrity and professionalism through transparent conduct at all times.

The Company during the period under review in relation to its code of conduct developed a Company –wide securities trading policy to guide

its Directors, Executive Management and Officers on the rules regulating the trading of the Company's shares and insider trading. As a public quoted company, the Company was fully compliant in its corporate governance practices and operations with new amended listing rules by t h e N i g e r i a n S t o c k E x c h a n g e , t h e recommendations of the Securities and Exchange Commission (SEC) and in line with other international best practices.

The appointment and remuneration of directors is governed by the Company Policy on Directors. During the period under review, the Non- Executive Directors and Chairman received an annual remuneration fee as stated below.

2014 Board and Board Committees Meeting Attendance

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 15

In line with the best practice, the Board is expected to hold a minimum of four (4) meetings annually; this requirement was achieved during the year under review.The Director's attendances at the Board meetings are as follow:

1

2

3

4

5

6

7

8

S/N NAME

Mr. Femi Otedola (CON)

Mr. Akin Akinfemiwa

Mr. Julius B. Omodayo -Owotuga, CFA

Ven. Canon Layi Bolodeoku

Rev. Dr. (Mrs)Grace Ekpenyong

Deacon Philip Akinola

Mrs. Korede Omoloja

Mr. Christopher Adeyemi

POSITION

Chairman

Director

Director

Director

Director

Director

Director

Director

31JANUARY2014

21OCTOBER2014

27MARCH 2014,

06AUGUST2014

23DECEMBER2014

Symbol Meaning

Present

Absent

2014 Board and Board Committees Meeting Attendance

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 416

The Corporate Governance and Remuneration Committee's role is to assist the Board in fulfilling its responsibilities in relation to Corporate Governance and Remuneration matters, to satisfy legal and regulatory requirements so as to protect the Company from liability, improve organizational effectiveness and assist in the attainment of business goals.

The Committee comprises of only non – executive directors who oversee the nomination and board appointment process and the board remuneration process. The Committee is also responsible for the review of the company`s organizational structure and ensures compliance with the Code of Corporate governance. It also oversees the succession planning process of the board.

The Committee held four (4) meetings in year 2014.

Corporate Governance and Remuneration Committee

1

2

3

4

S/N Name

Ven. Layi Bolodeoku

Mr. Christopher Adeyemi

Deacon Philip Akinola

Rev. Dr. (Mrs)Grace Ekpenyong

Position

Chairman

Member

Member

Member

25 Mar

2014

05 Aug

2014

15 Oct

2014

22 Dec

2014

Risk Management Committee

The Risk Management Committee assists the Board in fulfilling its oversight responsibilities in the identification, assessment, management of risk and adherence to internal risk management policies and procedures. The Committee is further responsible for development of effective risk governance framework and disclosure process, reviewing of changes in the economic and business environment and reviewing of company`s compliance level with regulations that impact on the company.

The Committee held four (4) meetings in the year 2014.

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 17

S/N Name Position 25 Mar

2014

15 Oct

2014

05 Aug

2014

1

2

3

4

5

Ven. Layi Bolodeoku

Mr. Christopher Adeyemi

Mr. Julius B. Omodayo-Owotuga, CFA

Mr. Akin Akinfemiwa

Chairman

Member

Member

Member

Member

Rev. Dr. (Mrs) Grace Ekpenyong

22 Dec

2014

Statutory Audit CommitteeThe Audit Committee is composed of six (6) members, three shareholders representatives and three Directors. One of the shareholders representative seats as the Chairman of the Committee.

The functions of the committee are set out in section 359(6) of the Company and Allied Matters Act. The Committee reviews the company's Control Policies, Management accounting and reporting systems, internal control and overall standard of business conduct.

The Audit Committee held four (4) meetings in the year 2014.

1

2

3

4

5

S/N Name

Tokunbo Shofolawe Bakare (Shareholder)

Emmanuel Okoro (Shareholder)

Suleman Ahmed (Shareholder)

Philip Akinola(Non Executive Director)

Korede Omoloja(Non Executive Director)

Position

Chairman

Member

Member

Member

Member

31 Jan

2014

25 Mar

2014

15 Oct

2014

6

Christopher Adeyemi(Independent Director)

Member

22 Dec

2014

05 Aug

2014

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 418

The Board Finance & Strategy Committee

The Board Finance and Strategy Committee is composed of five(5) members constituted to assist the Board of Directors in fulfilling its oversight responsibilities of the financial management of the Company. In addition, the Committee is charged with the oversight of the Company's strategic and transactional planning activities, global financing and capital structure objectives and plans, insurance program, tax structure and investment policies and dividend management policies.

The Committee will play a central role in determining strategic goals of the Company, development of priority directions of the Company’s activities, elaboration of recommendations on the dividend policy of the Company, assessment of the effectiveness of the Company’s performance in the long run and amplification of recommendations to the Board of Directors on adjustments of the existing strategy of the Company's development.

This Committee was constituted in December 2014 and the membership are as follows;

1

2

3

4

S/N Name

Mr. Christopher Adeyemi

Mrs. Korede Omoloja

Mr. Phillip Akinola

Position

Chairman

Member

Member

Member

5 MemberMr. Julius B. Omodayo-Owotuga, CFA

Mr. Akin Akinfemiwa

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 19

Akin Akinfemiwa Group Chief Executive Officer

Mr. Femi Otedola, CON Chairman

Board of Directors

e was appointed the

HChairman of the Board of Directors of Forte Oil Plc

(formerly known as African Petroleum Plc) on May 25, 2007.

Mr. Otedola attended the famous London College of Printing from where he bagged a degree in Printing Technology in 1985. He then took over as the Managing Director of Impact Press Limited in 1988, growing the company into one of the foremost printing presses in Nigeria at that time.

In 1999, he ventured into the Oil and Gas sector by incorporating Zenon Petroleum & Gas Limited, a n i n d i g e n o u s c o m p a n y engaged in the procurement, s t o r a g e , m a r k e t i n g a n d d i s t r i b u t i o n o f p e t r o l e u m p r o d u c t s . I n 2 0 0 1 , h e incorporated Seaforce Shipping Company Limited which currently owns and manages modern tanker fleet of vessels that transport petroleum products.

Mr. Otedola is today the President and Chief Executive Officer of Zenon Petroleum & Gas Limited;

Chairman, Seaforce Shipping Company Limited, Atlas Shipping Agency Company Limited, F. O. Transport Limited, F.O. Properties Limited, Swift Insurance Brokers Limited and Garment Care Limited.

Mr. Otedola, a former President of the N iger ian Chamber of Shipping was appointed member of the governing council of the Nigerian Investment Promotion Council (NIPC) in January 2004, and in December of the same year, he was appointed a member of the committee saddled with the task of fostering business relationship between the Nigerian and the South African Private sectors.

Mr. Femi Otedola was further recognized for his immense contributions to the growth of the Nigerian economy when in May,2010 he was awarded the prestigious National Honours of “Commander, Order of the Niger - CON” by President Goodluck Jonathan.

r. Akin Akinfemiwa as the

MGroup Chief Executive Officer of the Company

is responsible for the overall strategic direction for the business and the subs id ia r ie s . Mr . Ak infemiwa was a former Director, Trading and Business development of Fineshade Energy Limited.

Mr. Akin Akinfemiwa is a seasoned and experienced International Petroleum Products Trader with focus on oil and oil products futures, swaps and derivatives trading responsibilities. He was influential in developing strategic trading and supply relationships for Oando in the West African Sub Region.Prior to this, Akin had worked with

FSB International Bank plc as a Business Process Analyst and a s u b - t e a m l e a d e r o n t h e C o m p a n y ' s B u s i n e s s Transformation project in 2001.Mr. Akinfemiwa is an alumnus of the Sa id Bus iness School , University of Oxford, United Kingdom. He also holds a B.sc Honours degree in Mechanical Engineering from the University of Ibadan and a Master of Business Administrat ion ( information Technology) from the University of Lincolnshire and Humberside, United Kingdom. Akin has also a t t e n d e d v a r i o u s g l o b a l leadership courses including that of the Wharton Business School, University of Pennsylvania.

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 420

Layi Bolodeoku Director

Profile of Directors

Julius B. Omodayo- Owotuga, CFA - Group Chief Financial Officer

r. Julius B. Omodayo-

MOwotuga is the Group Chief Financial Officer

of Forte Oil Plc. He is a CFA Charter Holder, a KPMG trained Chartered Accountant and an e x p e r i e n c e d f i n a n c e professional. Before he joined Forte Oil Group, he was at Africa Finance Corporation (AFC) where he had responsibilities for the Corporation's Assets and Liabilities Management function and also doubled as the Assistant Treasurer. AFC is a US$1bn private sector led Development Finance and Investment Bank. Prior to this, he had held the role of Finance M a n a g e r i n t h e s a m e Corporation. In this role, Mr. Omodayo-Owotuga set up the Financial Control function of the ins t i tut ion. He was a l so responsible for Human Resources and Administration at the Corporation's start up stage in 2007.

en. Bankole Olayiwola

VBo lodeoku i s a non Executive Director of Forte

Oil Plc. He obtained a Bachelor's Degree in History and Political Science from the University of Ibadan in 1965 and a Masters' Degree in Public Administration from the University of Ife in 1972. He worked with the old Western Region Civil Service in different capacities and was seconded to the newly founded Ibadan Polytechnic as the first Registrar in 1971.

Subsequently, he was appointed Registrar Examinations in the Public Service from where he became Training Officer in charge of the old Civil Service Training School. In 1973, he joined Evans Brothers Limited as a General Manager and later

Mr. Omodayo-Owotuga joined the AFC from Standard Chartered Bank Nigeria Limited where he was a Finance Manager with responsibilities for the finance aspect of the Bank's expansion project. Before this, he was at KPMG Professional Services where he led assurance engagements within the Nigerian financial se rv ices indus t ry . He a l so consulted for a number of Institutions on IFRS and Risk Management while at KPMG Professional Services. Prior to KPMG, Mr. Omodayo-Owotuga worked in the Foreign Operations Group of MBC International Bank (now First Bank Nigeria Limited).He holds a B.Sc in Accounting from the University of Lagos. He is also a Chartered Management Accountant, Chartered Tax Practitioner and a Certified Treasury and Financial Manager. H e h a s a l s o a t t e n d e d management courses at Harvard Business School and other renowned management schools.

b e c a m e t h e M a n a g i n g Director/Chief Executive Officer in 1976, and was also Director of Evans Brothers London and Evans East Africa, before he voluntarily retired in May, 2000.

Rev Bolodeoku is a member of the prestigious society of Young Publishers in Brighton England and the United Kingdom Society of Scientific Technical and Mechanical Publishers. Between 1980 and 1981, he served on the executive committee of the publisher's association based in Geneva. In 1979, he was appointed Vice President of the Nigerian Publishers' Association and became the President in 1980, and has remained on the Board of the University Bookshop as Chairman.

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 21

Profile of Directors (Cont’d)

Grace C. Ekpenyong Director

r a c e C h r i s t o p h e r

GEkpenyong holds a first Degree in Zoology from

the University of Ibadan in 1979 and a Post Graduate Diploma in Education from the University of Lagos. She is vastly experienced in different fields such as manufacturing, social welfare, educat ion , fa rm ing , and humanitarian activities - having worked in various capacities within the sectors.

From 1980 to 1985, she was a Senior Lecturer/Vice Principal, Cross River State Schools Board; Lecturer at Vivian Fowler Tutorial College from 1986-1989. From 1989 to date, she has been the Deputy Managing Director, Gestric Group of Companies; Managing Director, Amazing Quality Limited and President, W i d o w s M i t e I n t e g r a t e d

r. Adeyemi attended

MObafemi Awolowo University Ile Ife where

he obtained his LL.B (Hons) degree in 1989. He became a Barrister and Solicitor of the Supreme Court of Nigeria in 1991.

Mr. Adeyemi began his legal career as Head of Green Form Advice and Assistance Team in The Legal Aid Board of England and Wales. During his stint at the Legal Aid Board, he was responsible for setting up the Green Fo rm Adv ice and Assistance phone extensions team and also the Immigration Project Team. After leaving the public sector, Mr. Adeyemi, in partnership with others, set up Agape Consulting, a Legal Practice and Management Consultancy which assists in

Deve lopment Assoc iat ion . Currently, she also functions as Execut ive Di rector , Eemjm Investment.

Mrs. Grace Ekpenyong is a member of many associations, such as the Manufacturers Association of Nigeria, National A s s o c i a t i o n o f W o m e n Entrepreneurs (NAWE), Nigeria Institute of Management (NIM), etc.

She holds various awards such as Certificate of Honour, Federal UNESCO Club of Nigeria (FUCN); Leadership Award, Afr ican E d u c a t i o n a n d C u l t u r e Organisation, Miami, Florida, USA, and Honorary Degree of Doctor of Divinity. She has been on the Board of Forte Oil Plc since 1999.

setting up and advising over 100 Law firms in the United Kingdom.

Christopher Adeyemi is currently the Head of the Corporate and Media Law Department of an I n t e r n a t i o n a l L a w a n d Management Firm. He has advised multinational companies on setting up businesses in the African and European markets. Mr. Adeyemi has most recently advised the Nollywood Industry on how to make international profits.

He is a member of the Nigerian Bar Association, member of the Black Solicitors Network (UK), and member of Immigration Law Practitioners Association (UK). Mr Chris Adeyemi is an independent director on the Board of Forte Oil Plc.

Christopher AdeyemiDirector

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 422

Profile of Directors (Cont’d)

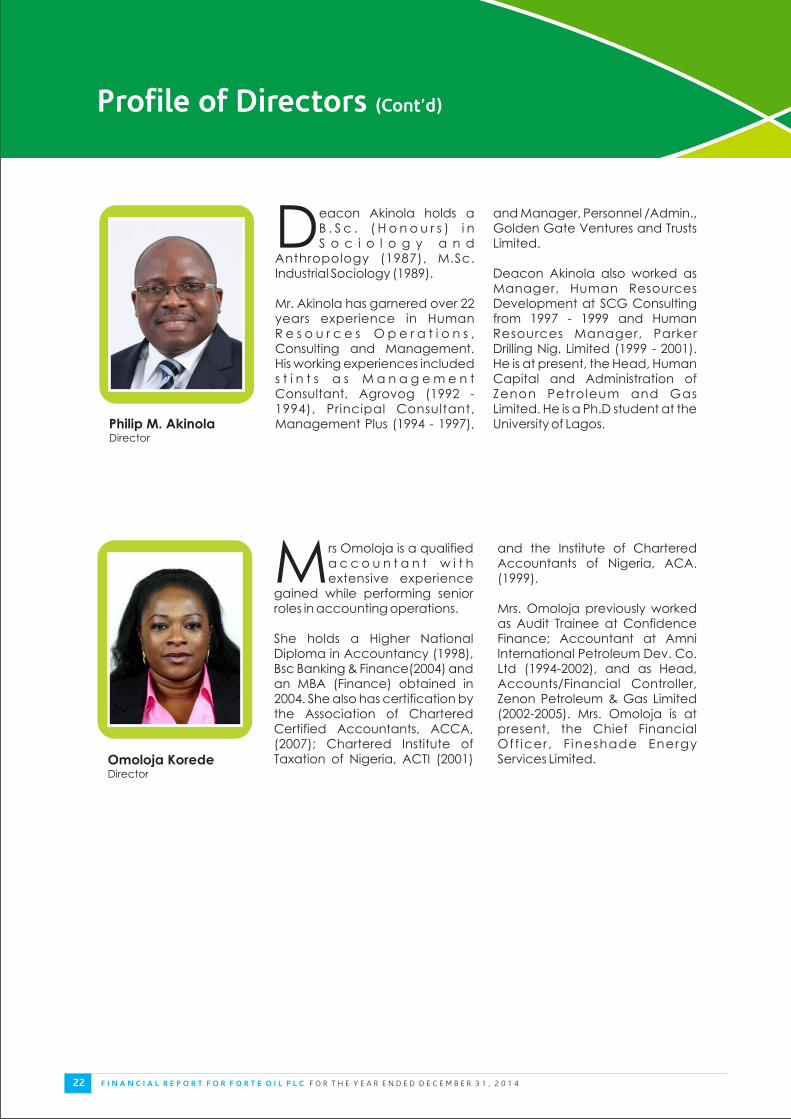

Philip M. Akinola Director

eacon Akinola holds a

DB . S c . ( H o n o u r s ) i n S o c i o l o g y a n d

Anthropology (1987), M.Sc. Industrial Sociology (1989).

Mr. Akinola has garnered over 22 years experience in Human R e s o u r c e s O p e r a t i o n s , Consulting and Management. His working experiences included s t i n t s a s M a n a g e m e n t Consultant, Agrovog (1992 - 1994), Principal Consultant, Management Plus (1994 - 1997),

and Manager, Personnel /Admin., Golden Gate Ventures and Trusts Limited.

Deacon Akinola also worked as Manager, Human Resources Development at SCG Consulting from 1997 - 1999 and Human Resources Manager, Parker Drilling Nig. Limited (1999 - 2001). He is at present, the Head, Human Capital and Administration of Zenon Petroleum and Gas Limited. He is a Ph.D student at the University of Lagos.

Omoloja Korede Director

rs Omoloja is a qualified

Ma c c o u n t a n t w i t h extensive experience

gained while performing senior roles in accounting operations.

She holds a Higher National Diploma in Accountancy (1998), Bsc Banking & Finance(2004) and an MBA (Finance) obtained in 2004. She also has certification by the Association of Chartered Certified Accountants, ACCA, (2007); Chartered Institute of Taxation of Nigeria, ACTI (2001)

and the Institute of Chartered Accountants of Nigeria, ACA. (1999).

Mrs. Omoloja previously worked as Audit Trainee at Confidence Finance; Accountant at Amni International Petroleum Dev. Co. Ltd (1994-2002), and as Head, Accounts/Financial Controller, Zenon Petroleum & Gas Limited (2002-2005). Mrs. Omoloja is at present, the Chief Financial Off icer, F ineshade Energy Services Limited.

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 424

Directors' ReportFor the year ended 31 December 2014

n accordance with the provisions of the

ICompanies and Allied Matters Act of 2004, the Directors are pleased to present their

report on the affairs of Forte Oil Plc (“the Company”) and subsidiary companies (“the Group”), together with the Group audited financial statements and the auditor's report for the year ended 31 December 2014. LEGAL FORM The Company was incorporated in 1964 as British Petroleum (BP) Nigeria Limited with the marketing of BP Petroleum Products as the main focus. The Company changed from a private to public company in 1978 when 40% of the shares were sold to Nigerian Citizens in compliance with the provisions of the Nigerian Enterprises Promotion Decree of 1977. On July 31, 1979, the Federal Government of Nigeria (FGN) acquired 60% share capital held originally by BP, through the Nigerian National Petroleum Corporation (NNPC). This step transformed the company in to an ent i re ly N iger ian concern necessitating the subsequent change of name to African Petroleum .

In March 1989, FGN sold 20% of its share holding to the Nigerian public, thus making AP the first public company privatized under the Privatization and Commercialization Policy. The Federal Government, under its privatization programme in 2000 divested its remaining 40% shareholding in AP thus making AP a privately owned Company, with over 153,000 shareholders.

In 2010, the Company was acquired by Zenon Petroleum and Gas Ltd which saw the change of name and corporate identity of the Company to Forte Oil Plc. In addition to this transformation, was the restructuring of the Company's operations and the incorporation of sustainable growth strategies and policies to continuously improve on its operations and deliver prompt quality and effective services to customers and all stakeholders.

PRINCIPAL ACTIVITY

The Company is a major marketer of refined petroleum products with a strong presence in the 36 States of Nigeria and the Federal Capital Territory - Abuja. It procures and markets Premium Motor Spirit (PMS), Automotive Motor Oil (Diesel), Dual Purpose Kero (DPK), Fuel Oils and Jet A-1 fuel amongst others. Forte Oil plc also manufactures and distributes a wide range of lubricants foremost amongst them is the SYNTH 10000 and newly repackaged SUPER V and VISCO 2000.

The company sources high quality chemical products, classed under industrial, organic and petro-chemicals, which it sells to local industries. The chemical Products include: D O P , P o l y o l , A c e t o n e , C a l c i u m Hydrochloride, Isopropyl Alcohol etc.

STRUCTURE

The Company has two wholly owned subsidiaries: Forte Upstream Services Limited and AP Oil & Gas, Ghana (APOG). In addition, the Company has 57% stake in Amperion Power Distribution Company. Amperion Power Distribution Company owns 51% of Geregu Power Plc. OPERATING RESULTS: The following is a summary of the Group's and Company's operating results:

Retained earnings at the end of the year

Earnings per share - basic & diluted

6,006,298

(1,549,681)

4,456,617

4,378,599

5,726,144

3,958,962

N2.20

4,207,443

(1,568,530)

2,638,913

2,638,913

4,854,671

3,346,139

N2.42

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 25

FIXED ASSETS Information relating to changes in fixed assets during the year is given in Note 14 to the financial statements. DIRECTORSThe names of the Directors as at the date of this report and those who held office during the year are as follows:

FEMI OTEDOLA, C.O.N. (Chairman) Appointed on May 25, 2007VEN. LAYI BOLODEOKU Re-elected on Sept 14, 2012GRACE C. EKPENYONG (MRS.) Re-elected on July 26, 2013CHRISTOPHER ADEYEMI Re-elected on March 28, 2014DEACON PHILIP M. AKINOLA Re-elected on Sept. 14, 2012OMOLOJA KOREDE (MRS) Re-elected on Sept. 14, 2012AKINWUNMI AKINFEMIWA Appointed December 28, 2011JULIUS OMODAYO-OWOTUGA, CFA Appointed December 28, 2011

In accordance with Article 89 of the Company's Articles of Association, Ven. Layi Bolodeoku, Mrs. Korede Omoloja and Decon Phillip Akinola will retire by rotation from the Board of Directors at this Annual General Meeting and being eligible have offered themselves for re-election at this meeting.

CHANGES ON THE BOARDSince the conclusion of the last Annual General Meeting, there have been no changes with the Board Members.

DIRECTORS INTERESTS The Directors of the Company who held office during the year together with their direct and indirect interest in the share capital of the Company were as follows: Number of Ordinary Shares 31/12/13 31/12/14 Mr. Femi Otedola - Chairman 115,878,398 128,706,299 499,323,557 (Indirect) 661,475,800(Indirect) Mr. Akin Akinfemiwa 20,000 20,000Mr. Julius Omodayo-Owotuga NIL NILRev. Mrs. Grace Ekpeyong 43,496 43,496 Ven. Layi Bolodeoku NIL NILMr. Christopher Adeyemi 80,485 80,485Deacon Phillip Akinola NIL NILMrs. Korede Omojola 49,187 49,187

CONTRACTS None of the Directors has notified the company for the purpose of Section 277 of the Company and Allied Matters Act of 2004 of any declarable interest in contracts which the Director is involved.

ACQUISITION OF SHARESThe Company did not purchase any of its own shares during the year.

Directors' Report (Cont’d)

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 426

Directors' Report (Cont’d)

SHARE OPTIONS SCHEMEThe Directors did not partake in any share option schemes during the period under review

MAJOR SHAREHOLDING According to the Register of Members, the shareholder under-mentioned held more than 5% of the issued share capital of the Company as at 31 December 2014:

No. of Shares % Holding ZENON PETROLEUM & GAS LIMITED 250,222,794 22.91%THAMES INVESTMENT INCORPORATED 160,783,449 14.72% ZRL NOMINEES 127,942,154 11.71%ZSL A/C FOZ 122,527,403 11.34%FEMI OTEDOLA 128,706,299 11.78%

SHARE CAPITAL HISTORY

Authorised Capital Issued and Fully Paid Capital

Date From To

22/06/7817/07/8028/08/8204/08/8406/08/8612/07/8829/06/9029/07/9328/11/9719/02/9915/11/02

26/11/13

N N

Date From To

N N

Consideration

ANALYSIS OF SHAREHOLDINGThe analysis of the distribution of the shares of the Company at the end of the 2014 financial year is as follows:

-Bonus (1:2)Bonus (1:1)Bonus (1:3)Bonus (1:5)Bonus (2:3)Rights IssueBonus (1:4)Rights IssueRights Issue

-Bonus (1:5)PlacementRights Issue

Public Offer-

Underwriting of 2008/2009

Hybrid Offer

7,500,000 11,250,000 22,500,000 30,000,000 36,000,000 43,200,000 86,400,000 86,400,000

108,000,000 216,000,000

234,263,450.50 281,116,141 394,393,919 443,271,555543,535,383543,535,383546,095,528

6,000,000 7,500,000

11,250,000 22,500,000 30,000,000 36,000,000 43,200,000 72,000,000 86,400,000

108,000,000 216,000,000

234,263,450.50 281,116,141 394,393,919 443,271,555543,535,383543,535,383

28/02/7917/07/8024/08/8210/08/8416/09/8603/08/8824/09/9010/01/9428/11/9913/09/0425/11/0430/09/0528/10/0620/04/0920/04/09

6/12/1311/07/2014

7,500,000 11,250,000 22,500,000 30,000,000 36,000,000 43,200,000 72,000,000 86,400,000

108,000,000 144,000,000

5,000,000,000

2,000,000,000

6,000,000 7,500,000

11,250,00022,500,00030,000,00036,000,000 43,200,000 72,000,000 86,400,000

108,000,000144,000,000

5,000,000,000

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 27

The Company identifies with the aspirations of the community as well as the environment within which it operates and made charitable donations to the under-listed organizations amounting to N10,135,500.00 during the year under review as follows:

Donations and Charitable Gifts

EMPLOYMENT OF DISABLED PERSONSThe Company operates a non-discriminatory policy in the consideration of applications for employment, including those received from disabled persons. The Company's policy is that the most qualified and experienced persons are recruited for appropriate job levels irrespective of the applicant's state of origin, ethnicity, religion or physical condition. In the event of any employee becoming disabled in the course of employment, the Company is in a position to arrange appropriate training to ensure the continuous employment of such a person without subjecting him/her to any disadvantage in his/her career development. As at 31 December 2014, the Company had no disabled persons in its employment. HEALTH, SAFETY AND WELFARE OF EMPLOYEESIt is the policy of Forte Oil Plc to carry out its activities in a manner that guarantees the health and safety of its workers and other stakeholders, the protection of the company's facilities and the environment and compliance with all regulatory and industry requirements.

We consider health, safety and environmental issues as important as our core businesses and assume the responsibility of providing healthy, safe and secure work environment for our workers as required by law. Our objective is to minimize the number of cases of occupational accidents, illnesses, damage to property and environmental degradation.

Our vision is to achieve leadership role in sustainable HSE practices through the establishment and implementation of effective business management principles that are consistent with local and

international regulations and standards.EMPLOYEE INVOLVEMENT AND TRAININGThe Company encourages participation of employees in arriving at decisions in respect of matters affecting their well being. Towards this end, the Company provides opportunities for employees to deliberate on issues affecting the Company and employees' interests, with a view to making inputs to decisions thereon. The Company places a high premium on the development of its manpower. Consequently, the Company sponsored its employees for various training courses both in Nigeria and abroad in the year under review. POST BALANCE SHEET EVENTSThere was no material event subsequent to year end that could impact on the financial statements. Please refer to note 31 of the consolidated financial statement for disclosure with respect to post balance sheet event. AUDITORSMessrs PKF Professional Services have indicated their willingness to continue in office in accordance with Section 357(2) of the Companies and Allied Act of Nigeria. BY ORDER OF THE BOARD

AKIN OLAGBENDECOMPANY SECRETARYFRC/2013/NBA00000003160

S/N ORGANIZATION/BODY AMOUNT

1.

2.

3.

4.

5.

Nigerian Stock Exchange Corporate Challenge N250,000.00

N1,000,000.00

ESQ Legal Practice Magazine, Esq Nigerian Legal Awards 2014 N2,000,000.00

N250,000.00

Save the Children Charity Organization Sponsorship N1,000,000.00

Partnership with the Nigerian Stock Exchange 13th Annual Essay Competition

National Association of Energy Correspondents (NAEC) Conference

TOTAL N10,135,500.00

6. The Abolarin College, Oke Ila N4,635,500.00

7. Women in Business (WIMBIZ) N500,000.00

8. Nigerian Union of Journalist, Ogun State Council N500,000.00

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 427

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 29

Report of the Audit Committeeto the members of Forte Oil Plc

In accordance with the provision of Section 359(6) of the Companies and Allied Matters Act of 2004, we confirm that:

1. We reviewed the scope and planning of the audit requirements.2. We reviewed the external auditors’ management reports for the

year ended 31st December, 2014 as well as the management response thereon; and

3. We ascertained that the accounting and reporting policies of the Company are in accordance with legal requirement and agreed ethical practices.

In our opinion, the scope and planning of the audit for the year ended 31st December, 2014 were adequate and we have reviewed the external auditor's findings on management matters and are satisfied with the responses to the findings.

In addition, the scope, planning and reporting of the consolidated financial statements are compliant with the requirements of the International Financial Reporting Standards (IFRSs) as adopted by the Company.

Dated this 18th Day of February 2015.

CHRIS ADEYEMI

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 430

CONSOLIDATEDFINANCIAL STATEMENTS3 1 D E C E M B E R 2 0 1 4

CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2014

Report of the Independent Auditors 34

Consolidated Statement of Financial Position 35

Consolidated Statement of Comprehensive Income 36

Consolidated Statement of Cash Flows 37

Consolidated Statement of Changes in Equity 38

Notes to the Consolidated Financial Statements 40

Consolidated Statement of Value Added 88

Financial Summary 89

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 31

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 432

Report of the Independent Auditorsto the members of Forte Oil Plc

We have audited the accompanying consolidated financial statements of Forte Oil Plc (“the Company”) and its subsidiaries (together, “the Group”), which comprise the consolidated financial position at 31 December 2014 and the consolidated statement of comprehensive income, consolidated statement of cash flows and statement of changes in equity for the year then ended and a summary of significant account ing pol ic ies and other explanatory information.

Directors' Responsibility for the Consolidated Financial Statements

The Directors are responsible for the preparation and fair presentation of these consolidated financial statements in accordance with the Companies and Allied Matters Act, Cap C20, LFN 2004 and with the requirements of the International Financial Reporting Standards in compliance with the Financial Reporting Council of Nigeria Act, No 6, 2011, and for such internal controls as the Directors determine are necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Nigerian and International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor consider internal control relevant to the entity's preparation and

fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by Directors, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Forte Oil Plc and its subsidiaries at 31 December 2014, and of their financial performance and its cash flows for the year then ended; in accordance with the Companies and Allied Matters Act, CAP C20, LFN 2004 and in the manner required by the International Financial Reporting Standards in compliance with the Financial Reporting Council of Nigeria Act, No 6, 2011.

The company and its subsidiaries have kept proper books of accounts, which are in agreement with the consolidated financial position and statement of comprehensive income as it appears from our examination of their records.

Tajudeen A. Akande, FCA, FRC/2013/ICAN/01780For: PKF Professional Services Chartered AccountantsLagos, NigeriaDate: 18 February 2015

Accountants &business advisers

Tel: +234(01) 8042074 | 7734940 | 7748366Web: www.pkf-ng.comEmail: [email protected] | [email protected] House | 205A Ikorodu Road, Obanikoro | Lagos | G.P.O. Box 2047 | Marina | Lagos, Nigeria

Partners: Isa Yusufu, Geoffrey C. Orah, Omede P.S. Adaji, Tajudeen A. Akande, Samuel I. Ochimena, Najeeb A. Abdus-salaam, Olatunji O. Ogundeyin, Benson O. AdejayanOfces in: Abuja, Bauchi, Jos, Kaduna, KanoPKF Professional Services is a member of PKF International Limited, a network of legally Independent Firms. PKF International does not accept any responsibility or liability for the actions or inactions on the part of any other individual member Firm or Firms

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 33

Consolidated Statement of Financial Position at 31 December 2014

Chairman FRC/2013/IODN/00000001994

FRC/2013/IODN/00000002426 Directors

FRC/2013/ICAN/00000001995

Note 31-Dec-14 31-Dec-13 31-Dec-14 31-Dec-13N’000 N’000 N’000 N’000

AssetsNon-current assetsProperty, plant and equipment 14 54,253,330

51,843,552

9,851,156

7,442,192

Investment property 15 1,934,928

2,021,526

1,934,928

2,021,526

Intangible assets 16 475,849

606,913

462,724

583,660

Investment in subsidiaries 17 -

-

11,032,291

11,141,547

Deferred tax assets 18 120,990

920,949

-

920,949

Long term employee benets 24 16,364

-

18,581

2,948

Total non-current assets 56,801,461

55,392,940

23,299,680

22,112,822

Current assetInventories 19 12,201,950

10,583,317

11,250,222

9,801,830

Other assets 20 572,565

426,462

127,415

107,511

Trade and other receivables 21 53,600,153

31,485,663

45,242,378

28,012,325

Cash and cash equivalent 22 16,062,169

6,789,618

13,758,711

5,281,601

Total current assets 82,436,837

49,285,060

70,378,726

43,203,267

Total assets 139,238,298

104,678,000

93,678,406

65,316,089

EquityShare capital 23 546,095

539,368

546,095

539,368

Share premium 23 8,181,162

6,947,887

8,181,162

6,947,887

Other reserves 23 (248,099)

(170,082)

(2,255)

(2,255)

Retained earnings 23 3,958,962

5,726,144

3,346,139

4,854,671

Total equity attributable to equity

holders of the Company 12,438,120

13,043,317

12,071,141

12,339,671

Non controlling interests 23 31,896,549

29,305,990

-

-

Total equity 44,334,669

42,349,307

12,071,141

12,339,671

LiabilitiesNon-current liabilitiesLong term employee benets 24 -

9,604

-

-

Deferred tax liabilities 18 82,373

86,332

-

-

Loans and borrowings 25 12,253,829

14,901,078

4,302,768

7,916,178

Non-current payables 26 421,839

680,711

421,839

680,711

Total non-current liabilities 12,758,041

15,677,725

4,724,607

8,596,889

Current liabilitiesLoans and borrowings 25 12,288,927

4,983,659

12,288,927

4,908,688

Bank overdrafts 22 16,496,305

4,906,018

16,496,305

4,906,018

Current income tax liabilities 12 845,611

570,523

639,847

468,148

Trade and other payables 26 52,514,745

36,190,768

47,457,579

34,096,675

Total current liabilities 82,145,588

46,650,968

76,882,658

44,379,529

Total liabilities 94,903,629

62,328,693

81,607,265

52,976,418

Total equity and liabilities 139,238,298

104,678,000

93,678,406

65,316,089

The accompanying notes and signicant accounting policies form an integral part of these consolidated nancial statements.

Group Company

The consolidated nancial statements were approved by the Board of Directors on 18 February 2015 and signed on its behalf by:

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 434

RevenueCost of sales

Gross protOther incomeDistribution expensesAdministrative expenses

Operating protNet nance cost

Prot before income taxIncome tax expense

Prot for the year

Other Comprehensive Income:Items that will not be reclassied

subsequently to prot or lossForeign exchange translation loss

Items that may be reclassied

subsequently to prot or lossDened benet plan actuarial loss

Total other comprehensive loss net of taxes

Total comprehensive income for the year

Total comprehensive income attibutable to:Owners of the companyNon controlling interests

Earnings per shareBasic/Dilluted earnings per share in (N)

CompanyGroup

The accompanying notes and signicant accounting policies form an integral part of these consolidated nancial statements.

Consolidated Statement of Comprehensive Incomefor the year ended 31 December 2014

F I N A N C I A L R E P O R T F O R F O R T E O I L P L C F O R T H E Y E A R E N D E D D E C E M B E R 3 1 , 2 0 1 4 35

for the year ended 31 December 2014Consolidated Statement of Cash Flows

31-Dec-14 31-Dec-13 31-Dec-14 31-Dec-13Notes N’000 N’000 N’000 N’000

Cash flows from operating activitiesProfit for the year 4,378,599

4,896,134

2,638,913

4,580,977

Adjustment for:Foreign exchange translation gain/loss on consolidation 77,796

106,008

-

-

Depreciation of property, plant and equipment 14 1,880,009

1,004,412

793,396

543,774

Property, plant and equipment written off 1,776

-

750

-

Amortization of intangible asset 16 191,024

180,164

180,684

173,069

Depreciation of investment property 15 86,598

89,919

86,598

89,919

Profit on disposal of property, plant and equipment (2,541)

(448,790)

(2,541)

(448,790)

Profit on disposal of investment property -

(790,785)

-

(790,785)

Impairment loss on property,plant and equipment -

754,817

-

7,241

Nominal value of shares issued in 2008 but not recognised in the books 4,167

-

4,167

-

Finance income 11 (2,077,351)

(2,132,804)

(1,971,304)

(2,099,077)

Interest expense 11 4,207,792

1,878,310

3,102,519

1,446,586

Increase/decrease in impairment allowance for trade receivables 8,20 46,600

(866,803)

(76,992)

(866,803)

Current service cost 24 71,578

56,646

58,402

52,771

Interest costs on defined benefit plan 15,584

14,306

Defined benefit plan actuarial loss 222

2,255

-

2,255

Deccrease in provision for employee benefit -

(26,428)

-

-

Expected return on gratuity planned asset 24 (23,031)

(15,809)

(23,031)

(15,809)

Capital gains tax expense 12 -

154,038

-

154,038

Income tax expense 12 1,549,681

1,366,115

1,568,530

1,374,060

Other non cash-items - translation losses (28,480)

(71,450)

-

-

10,380,023

6,135,949

6,374,397

4,203,426

Changes in:Inventories 19 (1,618,633)

(2,839,224)

(1,448,392)

(2,967,769)

Consumables 21 (146,103)

(278,173)

(19,904)

40,778

Trade and other receivables 20 (22,161,090)

(17,660,314)

(17,153,060)

(17,349,958)

Trade and other payables 26 16,919,160

19,839,421

14,946,956

20,657,044

Non trade payables and other creditors 26 402,137

(4,880,111)

(588,733)

(3,982,763)

Employee benefits paid 24 (20,562)

-

(9,403)

-

Cash generated from operating activities 3,754,932

317,548

2,101,861

600,758

Income taxes paid 12 (1,589,633)

(249,880)

(1,558,397)

(205,728)

Net cash from operating activities 2,165,299

67,668

543,464

395,030

Cash flows from investing activitiesProceeds from sale of property, plant and equipment 14,8 6,318

674,886

5,501

674,900