FORM 5 QUARTERLY LISTING STATEMENT MACCABI VENTURES …

37

FORM 5 – QUARTERLY LISTING STATEMENT January 2015 Page 1 Form 5 - Quarterly Listing Stmt_2016Q1.docx FORM 5 QUARTERLY LISTING STATEMENT Name of Listed Issuer: MACCABI VENTURES INC. (the “Issuer”). Trading Symbol: MBE This Quarterly Listing Statement must be posted on or before the day on which the Issuer’s unaudited interim financial statements are to be filed under the Securities Act, or, if no interim statements are required to be filed for the quarter, within 60 days of the end of the Issuer’s first, second and third fiscal quarters. This statement is not intended to replace the Issuer’s obligation to separately report material information forthwith upon the information becoming known to management or to post the forms required by the Exchange Policies. If material information became known and was reported during the preceding quarter to which this statement relates, management is encouraged to also make reference in this statement to the material information, the news release date and the posting date on the Exchange website. General Instructions (a) Prepare this Quarterly Listing Statement using the format set out below. The sequence of questions must not be altered nor should questions be omitted or left unanswered. The answers to the following items must be in narrative form. When the answer to any item is negative or not applicable to the Issuer, state it in a sentence. The title to each item must precede the answer. (b) The term “Issuer” includes the Listed Issuer and any of its subsidiaries. (c) Terms used and not defined in this form are defined or interpreted in Policy 1 – Interpretation and General Provisions. There are three schedules which must be attached to this report as follows: SCHEDULE A: FINANCIAL STATEMENTS Please see attached Schedule A. SCHEDULE B: SUPPLEMENTARY INFORMATION The supplementary information set out below must be provided when not included in Schedule A.

Transcript of FORM 5 QUARTERLY LISTING STATEMENT MACCABI VENTURES …

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 1

Form 5 - Quarterly Listing Stmt_2016Q1.docx

FORM 5

QUARTERLY LISTING STATEMENT

Name of Listed Issuer: MACCABI VENTURES INC. (the “Issuer”).

Trading Symbol: MBE

This Quarterly Listing Statement must be posted on or before the day on which the Issuer’s unaudited interim financial statements are to be filed under the Securities Act, or, if no interim statements are required to be filed for the quarter, within 60 days of the end of the Issuer’s first, second and third fiscal quarters. This statement is not intended to replace the Issuer’s obligation to separately report material information forthwith upon the information becoming known to management or to post the forms required by the Exchange Policies. If material information became known and was reported during the preceding quarter to which this statement relates, management is encouraged to also make reference in this statement to the material information, the news release date and the posting date on the Exchange website.

General Instructions

(a) Prepare this Quarterly Listing Statement using the format set out below. The sequence of questions must not be altered nor should questions be omitted or left unanswered. The answers to the following items must be in narrative form. When the answer to any item is negative or not applicable to the Issuer, state it in a sentence. The title to each item must precede the answer.

(b) The term “Issuer” includes the Listed Issuer and any of its subsidiaries.

(c) Terms used and not defined in this form are defined or interpreted in Policy 1 – Interpretation and General Provisions.

There are three schedules which must be attached to this report as follows: SCHEDULE A: FINANCIAL STATEMENTS Please see attached Schedule A. SCHEDULE B: SUPPLEMENTARY INFORMATION

The supplementary information set out below must be provided when not included in Schedule A.

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 2

Form 5 - Quarterly Listing Stmt_2016Q1.docx

1. Related party transactions

Provide disclosure of all transactions with a Related Person, including those previously disclosed on Form 10. Include in the disclosure the following information about the transactions with Related Persons: (a) A description of the relationship between the transacting parties. Be as

precise as possible in this description of the relationship. Terms such as affiliate, associate or related company without further clarifying details are not sufficient.

(b) A description of the transaction(s), including those for which no amount has been recorded.

(c) The recorded amount of the transactions classified by financial statement category.

(d) The amounts due to or from Related Persons and the terms and conditions relating thereto.

(e) Contractual obligations with Related Persons, separate from other contractual obligations.

(f) Contingencies involving Related Persons, separate from other contingencies.

Please see the section titled “Transactions with Related Parties” in the Issuer’s condensed interim consolidated financial statements attached.

Please see the section titled “Transactions with Related Parties” in the Issuer’s interim management’s discussion and analysis attached.

2. Summary of securities issued and options granted during the period.

Provide the following information for the period beginning on the date of the last Listing Statement (Form 2A): (a) summary of securities issued during the period,

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 3

Form 5 - Quarterly Listing Stmt_2016Q1.docx

Date of Issue

Type of Security

(common shares,

convertible debentures,

etc.)

Type of Issue

(private placement,

public offering,

exercise of warrants,

etc.)

Number

Price

Total Proceeds

Type of Consideration

(cash, property, etc.)

Describe

relationship of Person

with Issuer (indicate if

Related Person)

Commission Paid

None.

(b) summary of options granted during the period,

Date

Number

Name of Optionee if Related Person and relationship

Generic description of other Optionees

Exercise Price

Expiry Date

Market

Price on date of Grant

None.

3. Summary of securities as at the end of the reporting period.

Provide the following information in tabular format as at the end of the reporting period:

(a) Description of authorized share capital including number of shares for each class, dividend rates on preferred shares and whether or not cumulative, redemption and conversion provisions. The Issuer is authorized to issue an unlimited number of Common Shares without par value. The holders of the Common Shares, subject to the prior rights, if any, of any other class of shares of the Issuer, are entitled to receive such dividends in any financial year as the board of directors of the Issuer may by resolution determine. In the event of the liquidation, dissolution or winding-up of the Issuer, whether voluntary or involuntary, the holders of the Common Shares are entitled to receive, subject to the prior rights, if any, of the holders of any other class of shares of the Issuer, the remaining property and assets of the Issuer. The Common Shares do not carry any pre-emptive, subscription, redemption or conversion rights, nor do they contain any sinking or purchase fund provisions.

(b) Number and recorded value for shares issued and outstanding.

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 4

Form 5 - Quarterly Listing Stmt_2016Q1.docx

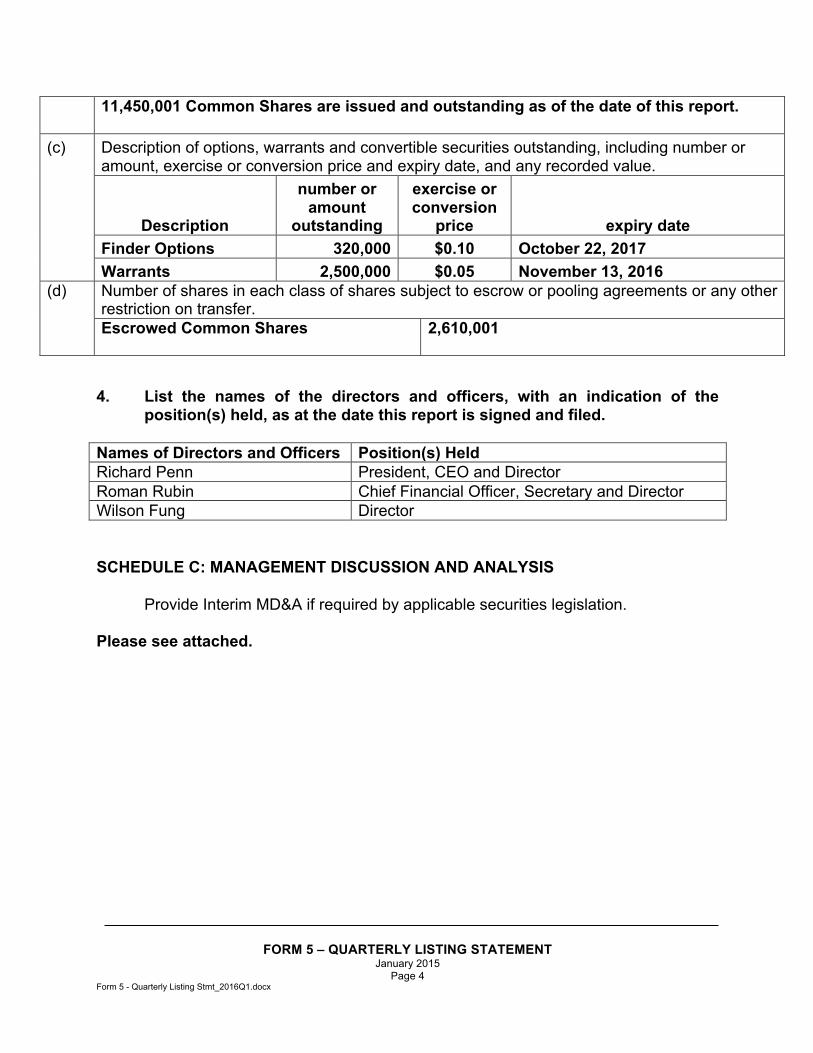

11,450,001 Common Shares are issued and outstanding as of the date of this report.

(c) Description of options, warrants and convertible securities outstanding, including number or amount, exercise or conversion price and expiry date, and any recorded value.

Description

number or amount

outstanding

exercise or conversion

price expiry date Finder Options 320,000 $0.10 October 22, 2017 Warrants 2,500,000 $0.05 November 13, 2016

(d) Number of shares in each class of shares subject to escrow or pooling agreements or any other restriction on transfer. Escrowed Common Shares

2,610,001

4. List the names of the directors and officers, with an indication of the

position(s) held, as at the date this report is signed and filed. Names of Directors and Officers Position(s) Held Richard Penn President, CEO and Director Roman Rubin Chief Financial Officer, Secretary and Director Wilson Fung Director SCHEDULE C: MANAGEMENT DISCUSSION AND ANALYSIS

Provide Interim MD&A if required by applicable securities legislation.

Please see attached.

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 5

Form 5 - Quarterly Listing Stmt_2016Q1.docx

Certificate Of Compliance

The undersigned hereby certifies that:

1. The undersigned is a director and/or senior officer of the Issuer and has been duly authorized by a resolution of the board of directors of the Issuer to sign this Quarterly Listing Statement.

2. As of the date hereof there is no material information concerning the Issuer which has not been publicly disclosed.

3. The undersigned hereby certifies to the Exchange that the Issuer is in compliance with the requirements of applicable securities legislation (as such term is defined in National Instrument 14-101) and all Exchange Requirements (as defined in CNSX Policy 1).

4. All of the information in this Form 5 Quarterly Listing Statement is true.

Dated April 26, 2016

RICHARD PENN Name of Director or Senior Officer

“Richard Penn” (signed) Signature

President and CEO Official Capacity

FORM 5 – QUARTERLY LISTING STATEMENT

January 2015 Page 6

Form 5 - Quarterly Listing Stmt_2016Q1.docx

Issuer Details Name of Issuer

For Quarter End

Date of Report YY/MM/D

MACCABI VENTURES INC. March 31, 2016

16/04/26

Issuer Address 2503 - 1455 Howe Street City/Province/Postal Code Issuer Fax No. Issuer Telephone No. Vancouver, BC V6Z 1C2 ( ) (604) 681-1220 Contact Name

Contact Position

Contact Telephone No.

Richard Penn CEO (604) 681-1220 Contact Email Address Web Site Address [email protected] www.maccabi.ca

NOTICE OF NO AUDITOR REVIEW OF THE CONDENSED INTERIM FINANCIAL STATEMENTS

FOR THE THREE MONTHS ENDED MARCH 31, 2016

The accompanying unaudited condensed interim financial statements of Maccabi Ventures Inc. (the “Company”) for the period ended March 31, 2016, have been prepared by, and are the responsibility of, the Company’s management. The Company’s independent auditor has not performed a review of these condensed interim financial statements in accordance with the standards established by the Canadian Institute of Chartered Accountants for a review of the condensed interim statements by an entity’s auditor.

MACCABI VENTURES INC.

CONDENSED INTERIM FINANCIAL STATEMENTS

FOR THE THREE MONTHS ENDED

MARCH 31, 2016 AND 2015

1

MACCABI VENTURES INC. CONDENSED INTERIM STATEMENTS OF FINANCIAL POSITION (Expressed in Canadian dollars)

NOTES March 31, 2016 December 31, 2015

ASSETS CURRENT

Cash $ 142,767 $ 174,276 Amounts receivable 2,320 6,243 Prepaid expenses - 7,125

TOTAL CURRENT ASSETS 145,087 187,644 EXPLORATION AND EVALUATION ASSET 5 27,706 22,866 TOTAL ASSETS $ 172,793 $ 210,510

LIABILITIES

CURRENT

Accounts payable and accrued liabilities $ 6,120 $ 12,035

SHAREHOLDERS’ EQUITY Share capital 6 415,866 411,366 Contributed surplus 6 63,644 63,644 Deficit (312,837) (276,535) TOTAL SHAREHOLDERS’ EQUITY 166,673 198,475 TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY $ 172,793 $ 210,510

Nature of business and continuing operations (Note 1) Approved and authorized for issue on behalf of the Board on April 20, 2016

Richard Penn Director Roman Rubin Director

The accompanying notes are an integral part of these condensed interim financial statements

2

MACCABI VENTURES INC. CONDENSED INTERIM STATEMENTS OF COMPREHENSIVE LOSS (Expressed in Canadian dollars) (UNAUDITED)

NOTES Three months ended

March 31, 2016Three months ended

March 31, 2015

EXPENSES

Advertising $ - $ 2,819

Consulting 7,125 -

Exploration expense 11,207 -

Filing fees 2,586 2,500

Management fees 7 21,000

Office and miscellaneous 9,287 5,787

Professional fees 7 6,097 24,248

Rent 7 - 9,000

Travel - 3,222

Operating expenses (36,302)

(68,576)

NET LOSS AND COMPREHENSIVE LOSS $ (36,302) $ (68,576)

LOSS PER SHARE – Basic and diluted $ (0.00) $ (0.01)

WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING 11,431,869 7,400,001

The accompanying notes are an integral part of these condensed interim financial statements

3

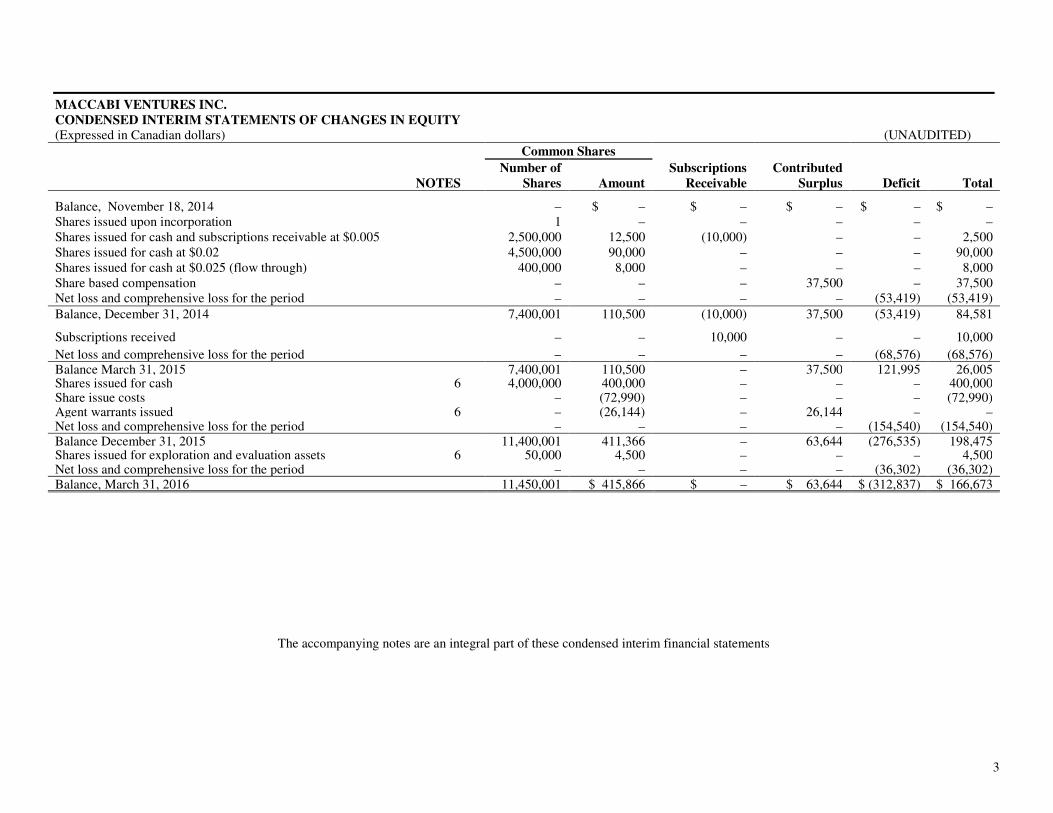

MACCABI VENTURES INC. CONDENSED INTERIM STATEMENTS OF CHANGES IN EQUITY (Expressed in Canadian dollars) (UNAUDITED) Common Shares

NOTES

Number of Shares Amount

Subscriptions Receivable

Contributed Surplus Deficit Total

Balance, November 18, 2014 – $ – $ – $ – $ – $ – Shares issued upon incorporation 1 – – – – – Shares issued for cash and subscriptions receivable at $0.005 2,500,000 12,500 (10,000) – – 2,500 Shares issued for cash at $0.02 4,500,000 90,000 – – – 90,000 Shares issued for cash at $0.025 (flow through) 400,000 8,000 – – – 8,000 Share based compensation – – – 37,500 – 37,500 Net loss and comprehensive loss for the period – – – – (53,419) (53,419) Balance, December 31, 2014 7,400,001 110,500 (10,000) 37,500 (53,419) 84,581 Subscriptions received – – 10,000 – – 10,000

Net loss and comprehensive loss for the period – – – – (68,576) (68,576) Balance March 31, 2015 7,400,001 110,500 – 37,500 121,995 26,005 Shares issued for cash 6 4,000,000 400,000 – – – 400,000 Share issue costs – (72,990) – – – (72,990) Agent warrants issued 6 – (26,144) – 26,144 – – Net loss and comprehensive loss for the period – – – – (154,540) (154,540) Balance December 31, 2015 11,400,001 411,366 – 63,644 (276,535) 198,475 Shares issued for exploration and evaluation assets 6 50,000 4,500 – – – 4,500 Net loss and comprehensive loss for the period – – – – (36,302) (36,302) Balance, March 31, 2016 11,450,001 $ 415,866 $ – $ 63,644 $ (312,837) $ 166,673

The accompanying notes are an integral part of these condensed interim financial statements

4

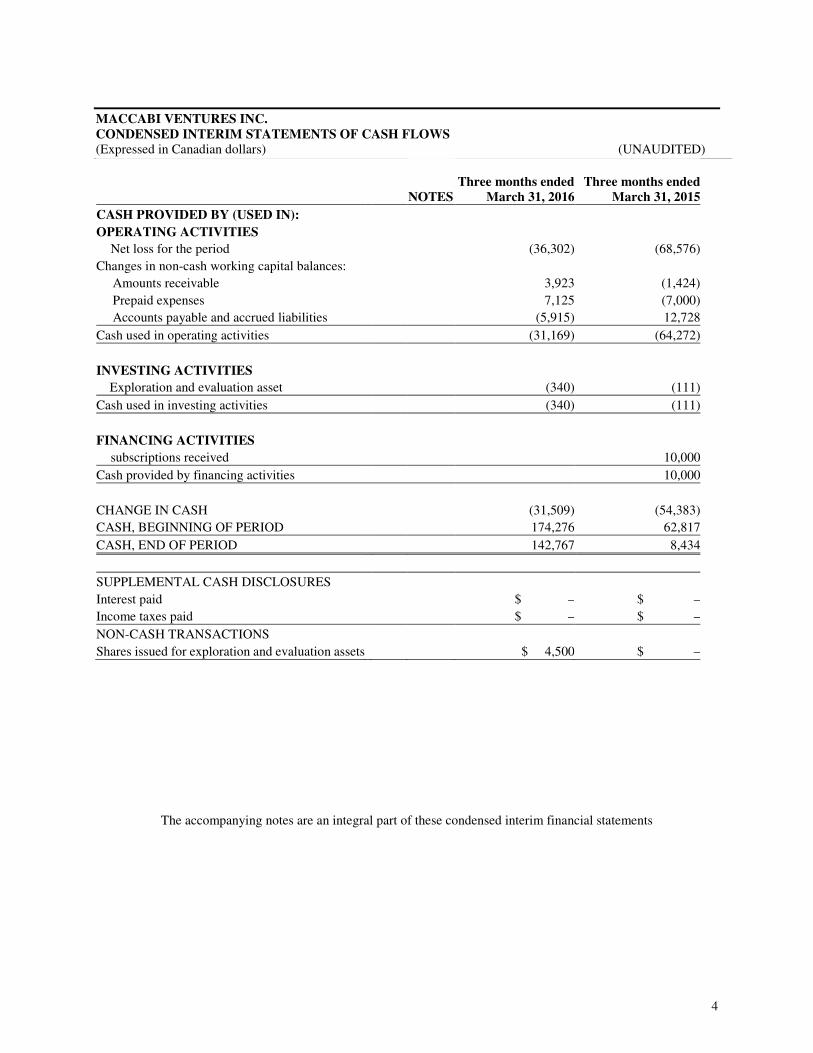

MACCABI VENTURES INC. CONDENSED INTERIM STATEMENTS OF CASH FLOWS (Expressed in Canadian dollars) (UNAUDITED)

NOTES Three months ended

March 31, 2016Three months ended

March 31, 2015

CASH PROVIDED BY (USED IN):

OPERATING ACTIVITIES

Net loss for the period (36,302) (68,576)

Changes in non-cash working capital balances:

Amounts receivable 3,923 (1,424)

Prepaid expenses 7,125 (7,000)

Accounts payable and accrued liabilities (5,915) 12,728

Cash used in operating activities (31,169) (64,272)

INVESTING ACTIVITIES

Exploration and evaluation asset (340) (111)

Cash used in investing activities (340) (111)

FINANCING ACTIVITIES

subscriptions received 10,000

Cash provided by financing activities 10,000

CHANGE IN CASH (31,509) (54,383)

CASH, BEGINNING OF PERIOD 174,276 62,817

CASH, END OF PERIOD 142,767 8,434

SUPPLEMENTAL CASH DISCLOSURES

Interest paid $ – $ –

Income taxes paid $ – $ –

NON-CASH TRANSACTIONS

Shares issued for exploration and evaluation assets $ 4,500 $ –

The accompanying notes are an integral part of these condensed interim financial statements

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

5

1. NATURE OF OPERATIONS Maccabi Ventures Inc. (“the Company”) was incorporated on November 13, 2014 under the laws of British Columbia. The address of the Company’s corporate office and its principal place of business is 704 – 595 Howe Street Vancouver, British Columbia, Canada. The Company’s principal business activities include the acquisition and exploration of mineral property assets. As at March 31, 2016, the Company had not yet determined whether the Company’s mineral property contains ore reserves that are economically recoverable. The recoverability of amounts shown for exploration and evaluation asset is dependent upon the discovery of economically recoverable reserves, confirmation of the Company’s interest in the underlying mineral claims, the ability of the Company to obtain the necessary financing to complete the development of and the future profitable production from the property or realizing proceeds from their disposition. The outcome of these matters cannot be predicted at this time and the uncertainties cast significant doubt upon the Company’s ability to continue as a going concern. The Company had a deficit of $312,837 as at March 31, 2016, which has been funded by the issuance of equity. The Company’s ability to continue its operations and to realize its assets at their carrying values is dependent upon obtaining additional financing and generating revenues sufficient to cover its operating costs. These condensed interim financial statements do not give affect to any adjustments which would be necessary should the Company be unable to continue as a going concern and therefore be required to realize its assets and discharge its liabilities in other than the normal course of business and at amounts different from those reflected in these condensed interim financial statements.

2. SIGNIFICANT ACCOUNTING POLICIES

a) Statement of compliance

The condensed interim financial statements (the “Financial Statements”) of the Company have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and Interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). Therefore, these Financial Statements comply with International Accounting Standard (“IAS”) 34, Interim Financial Statements.

These condensed interim financial statements do not include all of the information required of a full annual financial report and are intended to provide users with an update in relation to events and transactions that are significant to an understanding of the changes in financial position and performance of the Company since the end of the last annual reporting period. These condensed interim financial statements follow the same accounting policies and methods of application as the Company’s most recent annual financial statements. It is therefore recommended that this financial report be read in conjunction with the annual financial statements of the Company for the year ended December 31,, 2015.

These condensed interim financial statements were authorized for issuance in accordance with a resolution from the Board of Directors on April 5, 2016.

b) Basis of presentation

The condensed interim financial statements have been prepared on the historical cost basis, with the exception of financial instruments which are measured at fair value, as explained in the accounting policies set out below. In addition, these condensed interim financial statements have been prepared using the accrual basis of accounting, except for cash flow information.

The accounting policies set out below have been applied consistently for the periods presented in these condensed interim financial statements.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

6

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

c) Cash and cash equivalents

Cash in the statement of financial position is comprised of cash in banks and on hand, and short term deposits with an original maturity of three months or less, which are readily convertible into a known amount of cash.

d) Exploration and evaluation assets

Pre-exploration costs are expensed in the period in which they are incurred.

Once the legal right to explore a property has been acquired, all costs related to the acquisition, exploration and evaluation of mineral properties are capitalized by property. Upon commencement of commercial production, the related accumulated costs are amortized against projected income using the units-of-production method over estimated recoverable reserves.

Management annually assesses carrying values of non-producing properties and properties for which events and circumstances may indicate possible impairment. Impairment of a property is generally considered to have occurred if the property has been abandoned, there are unfavourable changes in the property economics, there are restrictions on development, or when there has been an undue delay in development, which exceeds three years. In the event that estimated discounted cash flows expected from its use or eventual disposition is determined by management to be insufficient to recover the carrying value of the property, the carrying value is written-down to the estimated recoverable amount.

The recoverability of mineral properties and exploration and development costs is dependent on the existence of economically recoverable reserves, the ability to obtain the necessary financing to complete the development of the property, and the profitability of future operations. The Company has not yet determined whether or not its mineral property contains economically recoverable reserves. Amounts capitalized to mineral properties as exploration and development costs do not necessarily reflect present or future values.

When options are granted on mineral properties or properties are sold, proceeds are credited to the cost of the property. If no future capital expenditure is required and proceeds exceed costs, the excess proceeds are reported as a gain on the statement of comprehensive loss.

e) Share-based compensation Share-based payments to employees and others providing similar services are measured at the estimated fair value of the instruments issued on the grant date and amortized over the vesting periods. Share-based payments to non-employees are measured at the fair value of the goods or services received or the fair value of the equity instruments issued if it is determined the fair value of the goods or services cannot be reliably measured, and are recorded at the date the goods or services are received. The amount recognized as an expense is adjusted to reflect the number of awards expected to vest. The offset to the recorded cost is to equity settled share-based payments reserve. Consideration received on the exercise of stock options is recorded as share capital and the related equity settled share-based payments reserve is transferred to share capital. Charges for options that are forfeited before vesting are reversed from equity settled share-based payment reserve.

Share-based compensation expense relating to deferred share units is accrued over the vesting period of the units based on the quoted market price. As these awards can be settled in cash, the expense and liability are adjusted each reporting period for changes in the underlying share price.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

7

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

f) Flow-through shares

The resource expenditure deductions for income tax purposes related to exploration and development activities funded by flow-through share arrangements are renounced to investors in accordance with Canadian tax legislation. On issuance, the premium recorded on the flow-through share, being the difference in price over a common share with no tax attributes, is recognized as a liability. As expenditures are incurred, the liability associated with the renounced tax deductions is recognized through profit and loss with a pro-rata portion of the deferred premium.

To the extent that the Company has deferred tax assets in the form of tax loss carry-forwards and other unused tax credits as at the reporting date, the Company may use them to reduce its deferred tax liability relating to tax benefits transferred through flow-through shares.

g) Foreign currency

Transactions and balances in currencies other than the Canadian dollar, the currency of the primary economic environment in which the Company operates (“the functional currency”), are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation of monetary assets and liabilities denominated in foreign currencies at exchange prevailing on the statement of financial position date are recognized in the statement of comprehensive loss.

h) Decommissioning, restoration and similar liabilities

An obligation to incur restoration, rehabilitation and environmental costs arise when environmental disturbance is caused by the exploration or development of a mineral property interest. Such costs arising from the decommissioning of plant and other site preparation work, discounted to their net present value, are provided for and capitalized at the start of each project to the carrying amount of the asset, along with a corresponding liability as soon as the obligation to incur such costs arises. The timing of the actual rehabilitation expenditure is dependent on a number of factors such as the life and nature of the asset, the operating license conditions and, when applicable, the environment in which the mine operates. Discount rates using a pre-tax rate that reflects the time value of money are used to calculate the net present value. These costs are charged against profit or loss over the economic life of the related asset, through amortization using either the units-of-production or the straight-line method. The corresponding liability is progressively increased as the effect of discounting unwinds creating an expense recognized in profit or loss Decommissioning costs are also adjusted for changes in estimates. Those adjustments are accounted for as a change in the corresponding capitalized cost, except where a reduction in costs is greater than the unamortized capitalized cost of the related assets, in which case the capitalized cost is reduced to nil and the remaining adjustment is recognized in profit or loss. The operations of the Company have been, and may in the future be, affected from time to time in varying degree by changes in environmental regulations, including those for site restoration costs. Both the likelihood of new regulations and their overall effect upon the Company are not predictable. The Company has no material restoration, rehabilitation and environmental obligations as the disturbance to date is immaterial.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

8

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

i) Loss per share

The Company presents basic and diluted loss per share data for its common shares, calculated by dividing the loss attributable to common shareholders of the Company by the weighted average number of common shares outstanding during the year. Diluted loss per share does not adjust the loss attributable to common shareholders or the weighted average number of common shares outstanding when the effect is anti-dilutive.

j) Income taxes

Current tax is the expected tax payable or receivable on the taxable income or loss for the year, using tax rates enacted or substantively enacted at the financial statements date, and includes any adjustments to tax payable or receivable in respect of previous years.

Deferred income taxes are recorded using the liability method whereby deferred tax is recognized in respect of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes.

Deferred tax is measured at the tax rates that are expected to be applied to temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the statement of financial position date. Deferred tax is not recognized for temporary differences which arise on the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting, nor taxable profit or loss.

A deferred tax asset is recognized for unused tax losses, tax credits and deductible temporary differences, to the extent that it is probable that future taxable profits will be available against which they can be utilized. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realized.

k) Financial assets

All financial assets are initially recorded at fair value and designated upon inception into one of the following four categories: held to maturity, available for sale, loans and receivables or at fair value through profit or loss (“FVTPL”).

Financial assets classified as FVTPL are measured at fair value with unrealized gains and losses recognized through earnings. The Company’s cash is classified as FVTPL.

Financial assets classified as loans and receivables and held to maturity assets are measured at amortized cost. As at March 31, 2016, the Company has not classified any financial assets as loans and receivables.

Financial assets classified as available for sale are measured at fair value with unrealized gains and losses recognized in other comprehensive income and loss except for losses in value that are considered other than temporary which are recognized in earnings. At March 31, 2016, the Company has not classified any financial assets as available for sale.

Transactions costs associated with FVTPL financial assets are expensed as incurred, while transaction costs associated with all other financial assets are included in the initial carrying amount of the asset.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

9

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

l) Financial liabilities

All financial liabilities are initially recorded at fair value and designated upon inception as FVTPL or other financial liabilities.

Financial liabilities classified as other financial liabilities are initially recognized at fair value less directly attributable transaction costs. After initial recognition, other financial liabilities are subsequently measured at amortized costs using the effective interest rate method. The effective interest rate method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period. The Company’s accounts payable are classified as other financial liabilities.

m) Financial liabilities

Financial liabilities classified as FVTPL include financial liabilities held for trading and financial liabilities designated upon initial recognition as FVTPL. Derivatives, including separated embedded derivatives are also classified as held for trading and recognized at fair value with changes in fair value recognized in earnings unless they are designated as effective hedging instruments. Fair value changes on financial liabilities classified as FVTPL are recognized in earnings. At March 31, 2016, the Company has not classified any financial liabilities as FVTPL.

A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expires.

3. SIGNIFICANT ACCOUNTING ESTIMATES AND JUDGMENTS

The preparation of these condensed interim financial statements requires management to make certain estimates, judgments and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and reported amounts of expenses during the reporting period. Actual outcomes could differ from these estimates. These condensed interim financial statements include estimates which, by their nature, are uncertain. The impacts of such estimates are pervasive throughout the condensed interim financial statements, and may require accounting adjustments based on future occurrences. Revisions to accounting estimates are recognized in the period in which the estimate is revised and future periods if the revision affects both current and future periods. These estimates are based on historical experience, current and future economic conditions and other factors, including expectations of future events that are believed to be reasonable under the circumstances. Significant assumptions about the future and other sources of estimation uncertainty that management has made at the financial position reporting date, that could result in a material adjustment to the carrying amounts of assets and liabilities, in the event that actual results differ from assumptions made, relate to, but are not limited to, the following:

Significant accounting estimates

i. the assessment of indications of impairment of the mineral property and related determination of the net realizable value and write-down of the mineral property where applicable;

ii. the estimated value of the acquisition costs which are recorded in the statement of financial position;

iii. the measurement of deferred income tax assets and liabilities; and

iv. the inputs used in accounting for share-based payments in profit or loss.

Significant accounting judgments

i. the evaluation of the Company’s ability to continue as a going concern.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

10

4. NEW ACCOUNTING STANDARDS ISSUED BUT NOT YET EFFECTIVE

Standards issued, but not yet effective, up to the date of issuance of the Company’s condensed interim financial statements are listed below. This listing of standards and interpretations issued are those that the Company reasonably expects to have an impact on disclosures, financial position or performance when applied at a future date. The Company intends to adopt these standards when they become effective. The following accounting standards were issued but not yet effective as of March 31, 2016:

New accounting standards effective for annual periods on or after January 1, 2017: IAS 1 – Presentation of Financial Statements In December 2014, the IASB issued an amendment to address perceived impediments to preparers exercising their judgment in presenting their financial reports. The changes clarify that materiality considerations apply to all parts of the financial statements and the aggregation and disaggregation of line items within the financial statements.

New accounting standards effective for annual periods on or after July 1, 2018:

IFRS 9 – Financial Instruments

The IASB intends to replace IAS 39 – Financial Instruments: Recognition and Measurement in its entirety with IFRS 9 – Financial Instruments (“IFRS 9”) which is intended to reduce the complexity in the classification and measurement of financial instruments. In February 2014, the IASB tentatively determined that the revised effective date for IFRS 9 would be January 1, 2018. The Company is currently evaluating the impact the final standard is expected to have on its financial statements. IFRS 7 Financial instruments: Disclosure IFRS 7 was amended to require additional disclosures on transition from IAS 39 to IFRS 9. The standard is effective on adoption of IFRS 9, which is effective for annual periods commencing on or after January 1, 2018. The extent of the impact of adoption of these standards and interpretations on the financial statements of the Company has not been determined.

5. EXPLORATION AND EVALUATION ASSET

Copper King Project

Pursuant to an option agreement dated November 28, 2014, with Rich River Exploration Ltd. (the “Optionor”), the Company was granted an option to acquire a 100% undivided interest in the Copper King Project property (the “Property”) located near the Olsen Lake north of Powel River, British Columbia.

Acquisition

Costs Exploration

Costs Total

Balance, November 13, 2014 (inception) $ – $ – $ – Acquisition costs 5,000 – 5,000 Other exploration costs – 5,850 5,850 Balance, December 31, 2014 5,000 5,850 10,850 Other exploration costs – 12,016 12,016

Balance, December 31, 2015 5,000 17,866 22,866 Acquisition costs (50,000 shares @ $0.05 per share issued to the optionor of the Copper King property) 4,500 – 4,500

Other exploration costs – 340 340

$ 9,500 $ 18,206 $ 27,706

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

11

5. EXPLORATION AND EVALUATION ASSET (continued)

To earn the 100% interest, the Company agreed to issue 625,000 common shares to the Optionor, make cash payments totalling $50,000, and incur a total of $400,000 in exploration expenditures as follows:

Common Shares

Cash

Exploration Expenditures

Upon execution of the agreement (paid) - $ 5,000 $ - Upon listing of the Company’s common shares on the Canadian Securities Exchange (the “Listing”) (issued) 50,000 - - On or before the first anniversary of the Listing 75,000 - - On or before the second anniversary of the Listing 100,000 - - On or before the third anniversary of the Listing 200,000 10,000 100,000 On or before the fourth anniversary of the Listing 200,000 15,000 100,000 On or before the fifth anniversary of the Listing - 20,000 200,000

Total 625,000 $ 50,000 $ 400,000

On February 2, 2016, 50,000 common shares of the Company were issued to the Optionor in accordance with the option agreement. (Note 6)

The Optionor will retain a 3% Net Smelter Returns royalty on the Property. The first 1% of the royalty may be purchased by the Company at $750,000 and the 2% remaining can be purchased for $900,000.

6. SHARE CAPITAL

a) Authorized The Company is authorized to issue an unlimited number of common and preferred shares without par value.

b) Escrow Shares Pursuant to the escrow agreements, 2,900,000 common shares issued and outstanding were escrowed and are scheduled for release at 10% on the listing date and at 15% on every six months from date of listing. At March 31, 2016 2,610,000 (December 31, 2015: 2,610,000) common shares remained in escrow.

c) Issued and Outstanding as at March 31, 2016 11,450,001 common shares (December 31, 2015: 11,400,001

common shares).

(i) During the year ended December 31, 2014, the Company issued 2,500,000 units at a price of $0.005 per unit, raising gross proceeds of $12,500. Each unit consisted of one common share and one share purchase warrant, with each share purchase warrant exercisable for one common share of the Company at a price of $0.02 per share for a period of two years. The fair value of the 2,500,000 units issued was estimated to be $50,000. Accordingly, the Company recorded share-based compensation expense of $37,500, and a corresponding increase to contributed surplus.

During the year ended December 31, 2015, the Company modified the exercise price of the share purchase warrants issued in connection with these units to $0.05 per common share.

(ii) During the year ended December 31, 2014, the Company issued 4,500,000 common shares at a price of

$0.02 per share, raising gross proceeds of $90,000.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

12

6) SHARE CAPITAL (continued)

(iii) During the year ended December 31, 2014, the Company issued 400,000 common shares at a price of $0.025 per share, raising gross proceeds of $10,000. The common shares were issued on a flow-through basis. As of March 31, 2016, $10,000 in eligible exploration expenditures related to the flow-through shares had been incurred.

For the purposes of the calculating the tax effect of any premium related to the issuances of the flow-through shares, the Company reviewed recent financings and compared it to determine if there was a premium paid on the shares. As at December 31, 2014, the Company had a flow-through premium liability of $830 in connection to these shares. During the year ended December 31, 2015, the Company recognized $830 as other income for a reduction in the flow-through premium liability for eligible expenditures incurred during the year.

(iv) During the year ended December 31, 2015, the Company issued 4,000,000 common shares at a price of

$0.10 per share, raising gross proceeds of $400,000. The Company incurred cash share issuance costs of $72,990 in connection with the financing and non cash share issuance costs of $26,144.

(v) On February 2, 2016, 50,000 common shares of the Company were issued at a price of $0.09 as payment to the optionors of the Copper King property. (Note 6)

d) Warrants

A summary of the Company’s share purchase warrants are as follows:

Number of

Warrants Weighted Average

Exercise Price

Expiry Date Balance at date of incorporation - - Issued 2,500,000 $ 0.05 November 13, 2016 Balance, December 31, 2014 2,500,000 Issued 320,000 $ 0.10 October 21, 2017

Balance, December 31, 2015 and March 31, 2016 2,820,000 $ 0.06

For the year ended December 31, 2014, no value was allocated to the warrants issued with the units as the Company uses the residual value method to allocate the value of the units. Accordingly, the value of the common shares is determined first and any residual value is allocated to the warrant. For the year ended December 31, 2015, no additional value was recognized as a result of modification of warrants as discussed in Note 6 (c) (i). On October 21, 2015, 320,000 Agent Warrants were issued as payment of finders fees in the initial public offering. Each warrant is exercisable into one common share of the Company at an exercise price of $0.10 and expire October 21, 2017. The Company recognized $26,144 representing the fair value of the warrants which was determined using the Black-Scholes option pricing model at the issue date using the following assumptions:

March 31, 2016 Expected option life (in years) 1.75 Risk-free interest rate .40% Expected dividend yield Nil Expected stock price volatility 188% Expected forfeiture rate 0%

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

13

6) SHARE CAPITAL (continued) e) Options to purchase shares

The Directors of the Company adopted a stock option plan on February 23, 2015 (the “Stock Option Plan”). The Stock Option Plan provides that, subject to the requirements of the Exchange, the aggregate number of securities reserved for issuance will be 10% of the number of the Company’s Common Shares issued and outstanding at the time such options are granted. The Stock Option Plan will be administered by the Company’s Board of Directors, which will have full and final authority with respect to the granting of all options thereunder. Options may be granted under the Stock Option Plan to such the directors, officers, employees, management or consultants of the Company and its affiliates, if any, as the Board of Directors may from time to time designate. The exercise price of option grants will be determined by the Board of Directors, but will not be less than the closing market price of the Common Shares on the Exchange less allowable discounts at the time of grant. The Stock Option Plan provides that the number of Common Shares that may be reserved for issuance to any one individual upon exercise of all stock options held by such individual may not exceed 5% of the issued Common Shares, if the individual is a director, officer, employee or consultant, or 1% of the issued Common Shares, if the individual is engaged in providing investor relations services, on a yearly basis. All options granted under the Stock Option Plan will expire not later than the date that is ten years from the date that such options are granted. Options terminate earlier as follows: (i) immediately in the event of dismissal with cause; (ii) 90 days from date of termination other than for cause; or (iii) one year from the date of death or disability. Options granted under the Stock Option Plan are not transferable or assignable other than by will or other testamentary instrument or pursuant to the laws of succession. Options Granted As of the date hereof, the Company has not granted any options.

7. RELATED PARTY BALANCES AND TRANSACTIONS

Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Related parties may be individuals or corporate entities. A transaction is considered to be a related party transaction when there is a transfer of resources or obligations between related parties.

At March 31, 2016 and December 31, 2015 there are no balances due to Related Parties Key management personnel receive compensation in the form of short-term employee benefits. Key management personnel include the directors of the Company. The remuneration of key management for the three month periods ended March 31, 2016 and 2015 is as follows:

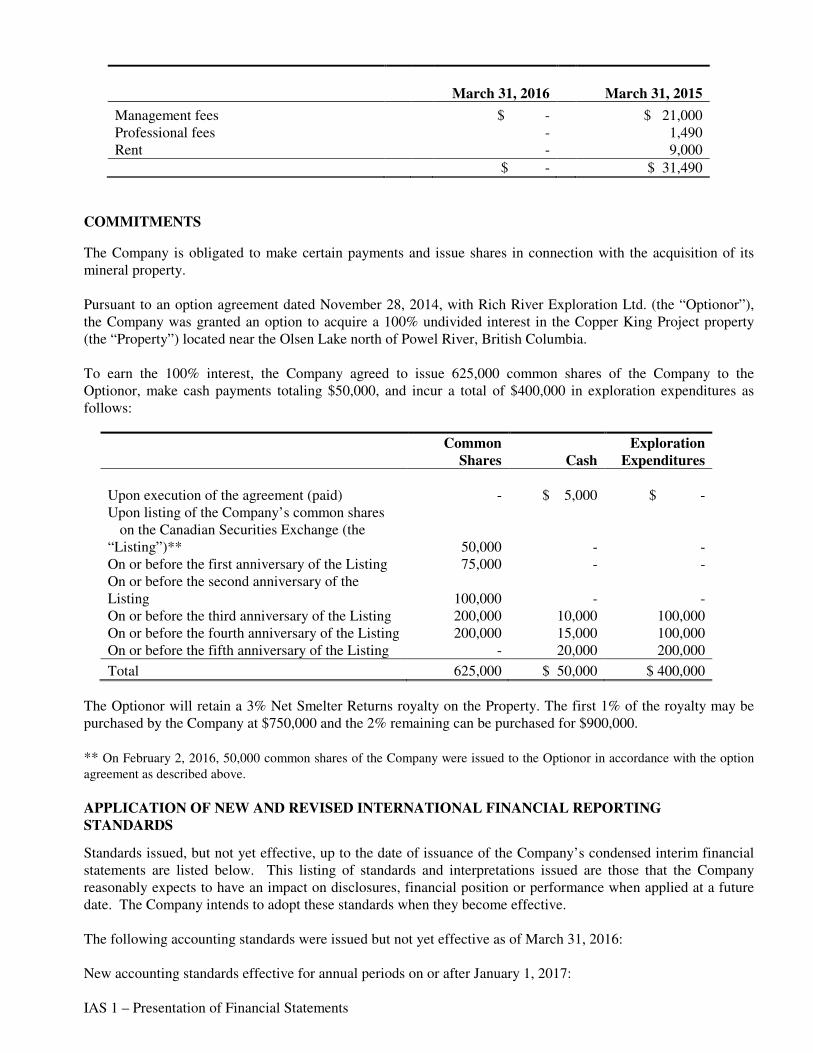

March 31, 2016 March 31, 2015

Management fees $ - $ 21,000 Professional fees - 1,490 Rent - 9,000 $ - $ 31,490

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

14

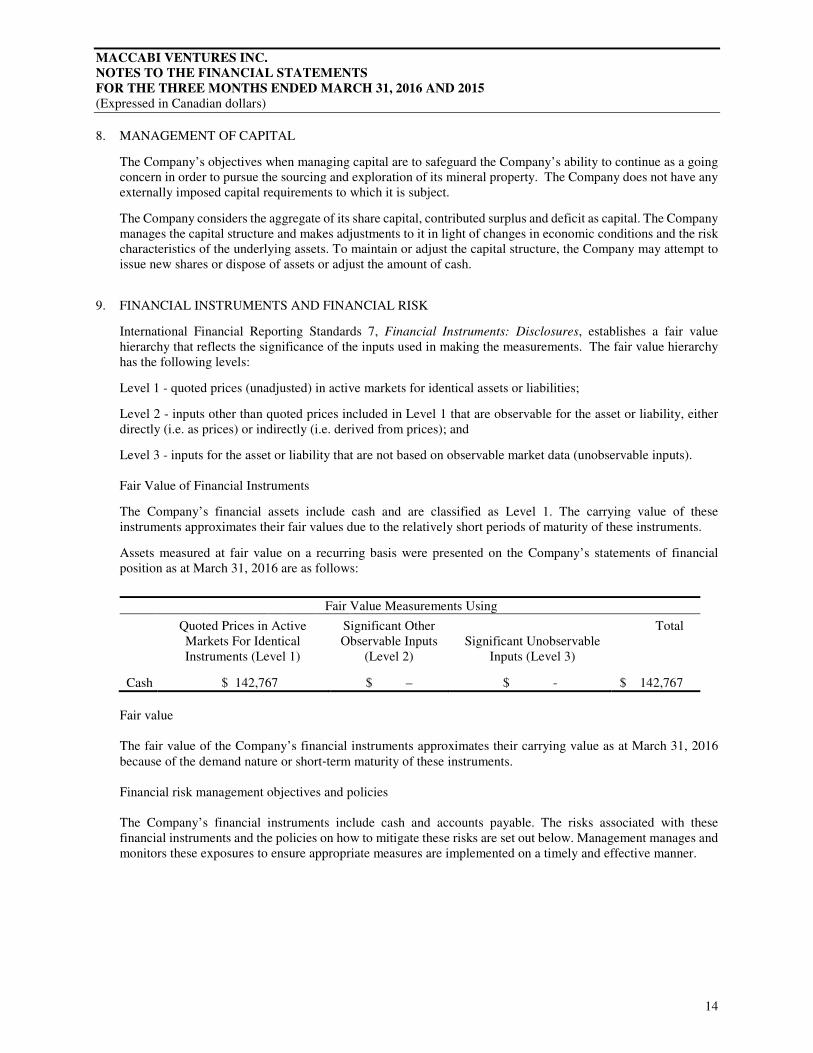

8. MANAGEMENT OF CAPITAL

The Company’s objectives when managing capital are to safeguard the Company’s ability to continue as a going concern in order to pursue the sourcing and exploration of its mineral property. The Company does not have any externally imposed capital requirements to which it is subject.

The Company considers the aggregate of its share capital, contributed surplus and deficit as capital. The Company manages the capital structure and makes adjustments to it in light of changes in economic conditions and the risk characteristics of the underlying assets. To maintain or adjust the capital structure, the Company may attempt to issue new shares or dispose of assets or adjust the amount of cash.

9. FINANCIAL INSTRUMENTS AND FINANCIAL RISK

International Financial Reporting Standards 7, Financial Instruments: Disclosures, establishes a fair value hierarchy that reflects the significance of the inputs used in making the measurements. The fair value hierarchy has the following levels:

Level 1 - quoted prices (unadjusted) in active markets for identical assets or liabilities;

Level 2 - inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

Level 3 - inputs for the asset or liability that are not based on observable market data (unobservable inputs). Fair Value of Financial Instruments

The Company’s financial assets include cash and are classified as Level 1. The carrying value of these instruments approximates their fair values due to the relatively short periods of maturity of these instruments.

Assets measured at fair value on a recurring basis were presented on the Company’s statements of financial position as at March 31, 2016 are as follows:

Fair Value Measurements Using Quoted Prices in Active

Markets For Identical Instruments (Level 1)

Significant Other Observable Inputs

(Level 2) Significant Unobservable

Inputs (Level 3)

Total

Cash $ 142,767 $ – $ - $ 142,767

Fair value

The fair value of the Company’s financial instruments approximates their carrying value as at March 31, 2016 because of the demand nature or short‐term maturity of these instruments.

Financial risk management objectives and policies The Company’s financial instruments include cash and accounts payable. The risks associated with these financial instruments and the policies on how to mitigate these risks are set out below. Management manages and monitors these exposures to ensure appropriate measures are implemented on a timely and effective manner.

MACCABI VENTURES INC. NOTES TO THE FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2016 AND 2015 (Expressed in Canadian dollars)

15

9. FINANCIAL INSTRUMENTS AND FINANCIAL RISK (continued)

(i) Currency risk The Company’s expenses are denominated in Canadian dollars. The Company’s corporate office is based in Canada and current exposure to exchange rate fluctuations is minimal. The Company does not have any significant foreign currency denominated monetary liabilities. The principal business of the Company is the identification and evaluation of assets or a business and once identified or evaluated, to negotiate an acquisition or participation in a business subject to receipt of shareholder approval and acceptance by regulatory authorities.

(ii) Interest rate risk The Company is exposed to interest rate risk on the variable rate of interest earned on bank deposits. The fair value interest rate risk on bank deposits is insignificant as the deposits are short‐term.

The Company has not entered into any derivative instruments to manage interest rate fluctuations. (iii) Credit risk

Credit risk is the risk of loss associated with the counterparty’s inability to fulfill its payment obligations. Financial instruments that potentially subject the Company to concentrations of credit risks consist principally of cash. To minimize the credit risk the Company places these instruments with a high quality financial institution. (iv) Liquidity risk In the management of liquidity risk of the Company, the Company maintains a balance between continuity of funding and the flexibility through the use of borrowings. Management closely monitors the liquidity position and expects to have adequate sources of funding to finance the Company’s projects and operations.

MACCABI VENTURES INC. Management Discussion and Analysis For the three months ended March 31, 2016

The following discussion and analysis should be read in conjunction with the audited financial statements of Maccabi Ventures Inc. (the “Company”) for the three months ended March 31, 2016 and related notes thereto, which are prepared in accordance with International Financial Reporting Standards. All amounts are stated in Canadian dollars unless otherwise noted.

Forward-Looking Information This management discussion and analysis contains “forward-looking information” which may include, but are not limited to, statements with respect to the future financial or operating performance of the Company. Often, but not always, forward-looking statements can be identified by the use of words such as “plans,” “expects,” “is expected,” “budget,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” or “believes” or variations (including negative variations) of such words and phrases, or statements that certain actions, events or results “may,” “could,” “would,” “might” or “will” be taken, occur or be achieved. Forward-looking information involves known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors include, among others, general business, economic, competitive, political and social uncertainties; the actual results of current exploration activities; changes in project parameters as plans continue to be refined; changes in labour costs; future mineral prices; failure of equipment or processes to operate as anticipated; accidents, labour disputes and other risks of the mining industry, including but not limited to environmental hazards, cave-ins, pit-wall failures, flooding, rock bursts and other acts of God or unfavourable operating conditions and losses; delays in obtaining governmental approvals or financing or in the completion of development or construction activities. See “Risk Factors”. Forward looking information is based on a number of material factors and assumptions, including the determination of mineral reserves or resources, if any, the results of exploration and drilling activities, the availability and final receipt of required approvals, licenses and permits, that sufficient working capital is available to complete proposed exploration and drilling activities, that contracted parties provide goods and/or services on the agreed time frames, the equipment necessary for exploration is available as scheduled and does not incur unforeseen break downs, that no labour shortages or delays are incurred and that no unusual geological or technical problems occur. While the Company considers these assumptions may be reasonable based on information currently available to it, they may prove to be incorrect. Actual results may vary from such forward-looking information for a variety of reasons, including but not limited to risks and uncertainties discussed above. The Company intends to discuss in its quarterly and annual reports any events and circumstances that occurred during the period to which such document relates that are reasonably likely to cause actual events or circumstances to differ materially from those disclosed in this management discussion and analysis. New factors emerge from time to time, and it is not possible for management to predict all of such factors and to assess in advance the impact of each such factor on the Company’s business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement. Date This management discussion and analysis is dated April 20, 2016 and is in respect of the three months ended March 31, 2016.

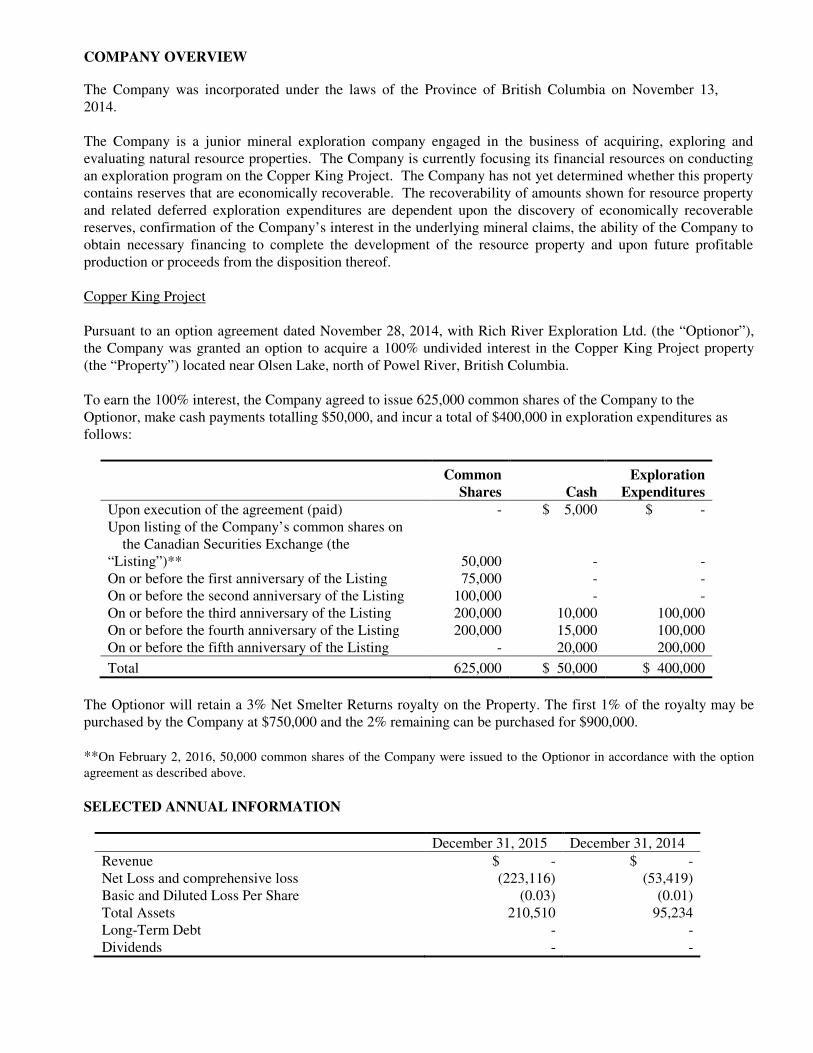

COMPANY OVERVIEW

The Company was incorporated under the laws of the Province of British Columbia on November 13, 2014. The Company is a junior mineral exploration company engaged in the business of acquiring, exploring and evaluating natural resource properties. The Company is currently focusing its financial resources on conducting an exploration program on the Copper King Project. The Company has not yet determined whether this property contains reserves that are economically recoverable. The recoverability of amounts shown for resource property and related deferred exploration expenditures are dependent upon the discovery of economically recoverable reserves, confirmation of the Company’s interest in the underlying mineral claims, the ability of the Company to obtain necessary financing to complete the development of the resource property and upon future profitable production or proceeds from the disposition thereof.

Copper King Project Pursuant to an option agreement dated November 28, 2014, with Rich River Exploration Ltd. (the “Optionor”), the Company was granted an option to acquire a 100% undivided interest in the Copper King Project property (the “Property”) located near Olsen Lake, north of Powel River, British Columbia. To earn the 100% interest, the Company agreed to issue 625,000 common shares of the Company to the Optionor, make cash payments totalling $50,000, and incur a total of $400,000 in exploration expenditures as follows:

Common Shares

Cash

Exploration Expenditures

Upon execution of the agreement (paid) - $ 5,000 $ - Upon listing of the Company’s common shares on the Canadian Securities Exchange (the “Listing”)** 50,000 - - On or before the first anniversary of the Listing 75,000 - - On or before the second anniversary of the Listing 100,000 - - On or before the third anniversary of the Listing 200,000 10,000 100,000 On or before the fourth anniversary of the Listing 200,000 15,000 100,000 On or before the fifth anniversary of the Listing - 20,000 200,000

Total 625,000 $ 50,000 $ 400,000

The Optionor will retain a 3% Net Smelter Returns royalty on the Property. The first 1% of the royalty may be purchased by the Company at $750,000 and the 2% remaining can be purchased for $900,000. **On February 2, 2016, 50,000 common shares of the Company were issued to the Optionor in accordance with the option agreement as described above.

SELECTED ANNUAL INFORMATION

December 31, 2015 December 31, 2014 Revenue $ - $ - Net Loss and comprehensive loss (223,116) (53,419) Basic and Diluted Loss Per Share (0.03) (0.01) Total Assets 210,510 95,234 Long-Term Debt - - Dividends - -

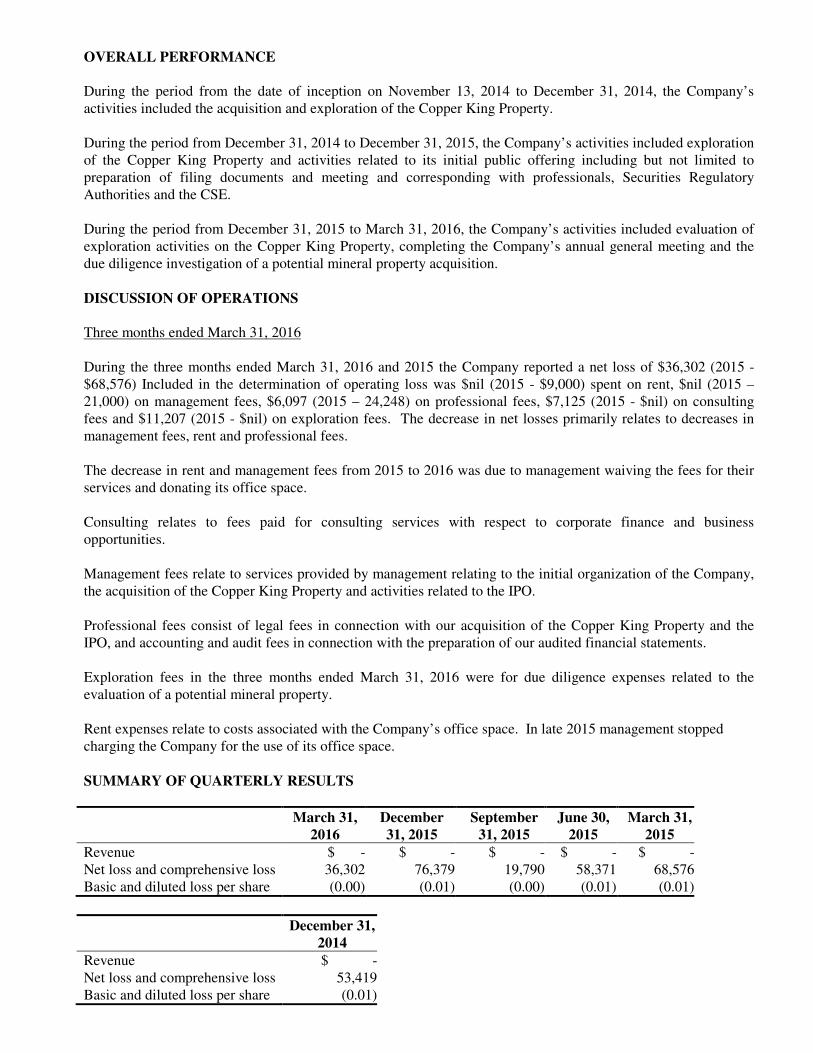

OVERALL PERFORMANCE During the period from the date of inception on November 13, 2014 to December 31, 2014, the Company’s activities included the acquisition and exploration of the Copper King Property. During the period from December 31, 2014 to December 31, 2015, the Company’s activities included exploration of the Copper King Property and activities related to its initial public offering including but not limited to preparation of filing documents and meeting and corresponding with professionals, Securities Regulatory Authorities and the CSE. During the period from December 31, 2015 to March 31, 2016, the Company’s activities included evaluation of exploration activities on the Copper King Property, completing the Company’s annual general meeting and the due diligence investigation of a potential mineral property acquisition. DISCUSSION OF OPERATIONS Three months ended March 31, 2016 During the three months ended March 31, 2016 and 2015 the Company reported a net loss of $36,302 (2015 - $68,576) Included in the determination of operating loss was $nil (2015 - $9,000) spent on rent, $nil (2015 – 21,000) on management fees, $6,097 (2015 – 24,248) on professional fees, $7,125 (2015 - $nil) on consulting fees and $11,207 (2015 - $nil) on exploration fees. The decrease in net losses primarily relates to decreases in management fees, rent and professional fees. The decrease in rent and management fees from 2015 to 2016 was due to management waiving the fees for their services and donating its office space. Consulting relates to fees paid for consulting services with respect to corporate finance and business opportunities. Management fees relate to services provided by management relating to the initial organization of the Company, the acquisition of the Copper King Property and activities related to the IPO. Professional fees consist of legal fees in connection with our acquisition of the Copper King Property and the IPO, and accounting and audit fees in connection with the preparation of our audited financial statements. Exploration fees in the three months ended March 31, 2016 were for due diligence expenses related to the evaluation of a potential mineral property. Rent expenses relate to costs associated with the Company’s office space. In late 2015 management stopped charging the Company for the use of its office space. SUMMARY OF QUARTERLY RESULTS

March 31, 2016

December 31, 2015

September 31, 2015

June 30, 2015

March 31, 2015

Revenue $ - $ - $ - $ - $ -Net loss and comprehensive loss 36,302 76,379 19,790 58,371 68,576Basic and diluted loss per share (0.00) (0.01) (0.00) (0.01) (0.01)

December 31, 2014

Revenue $ -Net loss and comprehensive loss 53,419Basic and diluted loss per share (0.01)

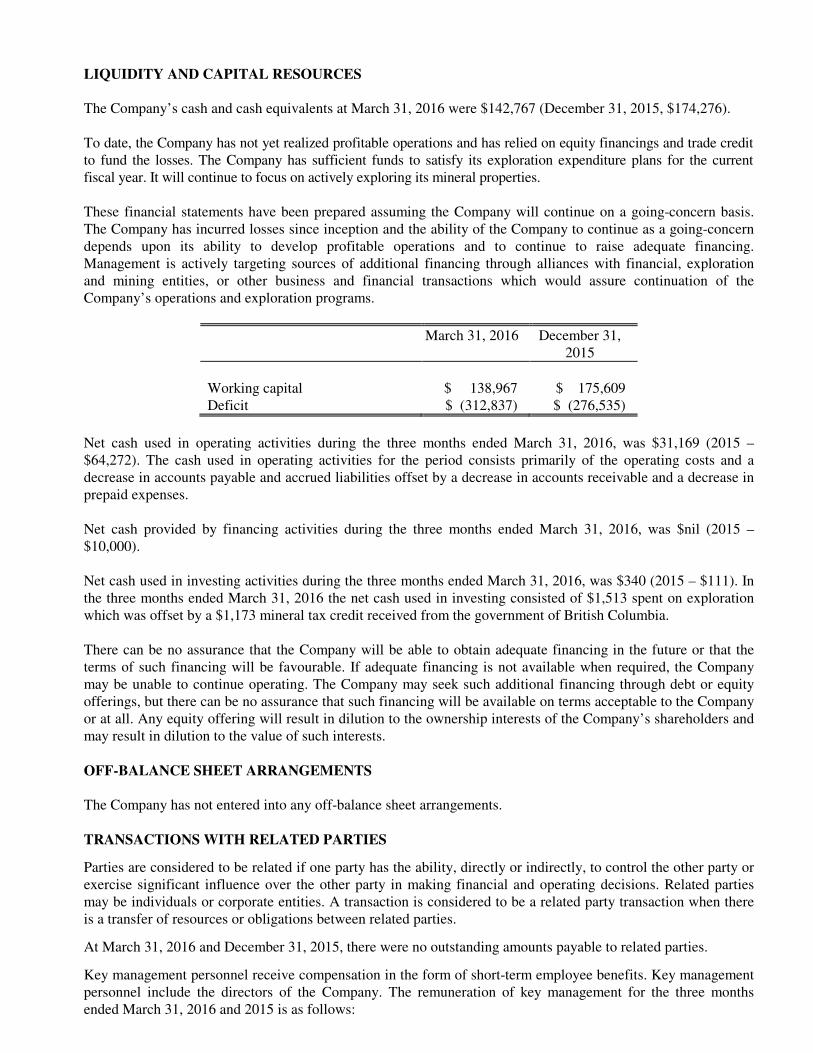

LIQUIDITY AND CAPITAL RESOURCES The Company’s cash and cash equivalents at March 31, 2016 were $142,767 (December 31, 2015, $174,276). To date, the Company has not yet realized profitable operations and has relied on equity financings and trade credit to fund the losses. The Company has sufficient funds to satisfy its exploration expenditure plans for the current fiscal year. It will continue to focus on actively exploring its mineral properties. These financial statements have been prepared assuming the Company will continue on a going-concern basis. The Company has incurred losses since inception and the ability of the Company to continue as a going-concern depends upon its ability to develop profitable operations and to continue to raise adequate financing. Management is actively targeting sources of additional financing through alliances with financial, exploration and mining entities, or other business and financial transactions which would assure continuation of the Company’s operations and exploration programs.

March 31, 2016 December 31, 2015

Working capital $ 138,967 $ 175,609 Deficit $ (312,837) $ (276,535)

Net cash used in operating activities during the three months ended March 31, 2016, was $31,169 (2015 – $64,272). The cash used in operating activities for the period consists primarily of the operating costs and a decrease in accounts payable and accrued liabilities offset by a decrease in accounts receivable and a decrease in prepaid expenses. Net cash provided by financing activities during the three months ended March 31, 2016, was $nil (2015 – $10,000). Net cash used in investing activities during the three months ended March 31, 2016, was $340 (2015 – $111). In the three months ended March 31, 2016 the net cash used in investing consisted of $1,513 spent on exploration which was offset by a $1,173 mineral tax credit received from the government of British Columbia. There can be no assurance that the Company will be able to obtain adequate financing in the future or that the terms of such financing will be favourable. If adequate financing is not available when required, the Company may be unable to continue operating. The Company may seek such additional financing through debt or equity offerings, but there can be no assurance that such financing will be available on terms acceptable to the Company or at all. Any equity offering will result in dilution to the ownership interests of the Company’s shareholders and may result in dilution to the value of such interests. OFF-BALANCE SHEET ARRANGEMENTS The Company has not entered into any off-balance sheet arrangements. TRANSACTIONS WITH RELATED PARTIES

Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Related parties may be individuals or corporate entities. A transaction is considered to be a related party transaction when there is a transfer of resources or obligations between related parties.

At March 31, 2016 and December 31, 2015, there were no outstanding amounts payable to related parties.

Key management personnel receive compensation in the form of short-term employee benefits. Key management personnel include the directors of the Company. The remuneration of key management for the three months ended March 31, 2016 and 2015 is as follows:

March 31, 2016 March 31, 2015

Management fees $ - $ 21,000 Professional fees - 1,490 Rent - 9,000 $ - $ 31,490

COMMITMENTS

The Company is obligated to make certain payments and issue shares in connection with the acquisition of its mineral property. Pursuant to an option agreement dated November 28, 2014, with Rich River Exploration Ltd. (the “Optionor”), the Company was granted an option to acquire a 100% undivided interest in the Copper King Project property (the “Property”) located near the Olsen Lake north of Powel River, British Columbia. To earn the 100% interest, the Company agreed to issue 625,000 common shares of the Company to the Optionor, make cash payments totaling $50,000, and incur a total of $400,000 in exploration expenditures as follows:

Common Shares

Cash

Exploration Expenditures

Upon execution of the agreement (paid) - $ 5,000 $ - Upon listing of the Company’s common shares on the Canadian Securities Exchange (the “Listing”)** 50,000 - - On or before the first anniversary of the Listing 75,000 - - On or before the second anniversary of the Listing 100,000 - - On or before the third anniversary of the Listing 200,000 10,000 100,000 On or before the fourth anniversary of the Listing 200,000 15,000 100,000 On or before the fifth anniversary of the Listing - 20,000 200,000

Total 625,000 $ 50,000 $ 400,000

The Optionor will retain a 3% Net Smelter Returns royalty on the Property. The first 1% of the royalty may be purchased by the Company at $750,000 and the 2% remaining can be purchased for $900,000. ** On February 2, 2016, 50,000 common shares of the Company were issued to the Optionor in accordance with the option agreement as described above. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS

Standards issued, but not yet effective, up to the date of issuance of the Company’s condensed interim financial statements are listed below. This listing of standards and interpretations issued are those that the Company reasonably expects to have an impact on disclosures, financial position or performance when applied at a future date. The Company intends to adopt these standards when they become effective. The following accounting standards were issued but not yet effective as of March 31, 2016:

New accounting standards effective for annual periods on or after January 1, 2017:

IAS 1 – Presentation of Financial Statements

In December 2014, the IASB issued an amendment to address perceived impediments to preparers exercising their judgment in presenting their financial reports. The changes clarify that materiality considerations apply to all parts of the financial statements and the aggregation and disaggregation of line items within the financial statements.

New accounting standards effective for annual periods on or after July 1, 2018:

IFRS 9 – Financial Instruments

The IASB intends to replace IAS 39 – Financial Instruments: Recognition and Measurement in its entirety with IFRS 9 – Financial Instruments (“IFRS 9”) which is intended to reduce the complexity in the classification and measurement of financial instruments. In February 2014, the IASB tentatively determined that the revised effective date for IFRS 9 would be January 1, 2018. The Company is currently evaluating the impact the final standard is expected to have on its financial statements.

IFRS 7 Financial instruments: Disclosure IFRS 7 was amended to require additional disclosures on transition from IAS 39 to IFRS 9. The standard is effective on adoption of IFRS 9, which is effective for annual periods commencing on or after January 1, 2018.

The extent of the impact of adoption of these standards and interpretations on the financial statements of the Company has not been determined. CRITICAL ACCOUNTING POLICIES Stock-based Compensation The Company has a stock option plan, which is described in the financial statements. The Company applies the fair value method to all stock-based payments and to all grants that are direct awards of stock that call for settlement in cash or other assets. Compensation expense is recognized over the applicable vesting period with a corresponding increase in contributed surplus. When the options are exercised, share capital is credited for the consideration received and the related contributed surplus is decreased. The Company uses the Black Scholes option pricing model to estimate the fair value of stock based compensation. Financial Instruments

Financial assets are classified into one of four categories:

• Fair value through profit or loss;

• Held-to-maturity;

• Available for sale and;

• Loans and receivables

The classification is determined at initial recognition and depends on the nature and purpose of the financial asset.

Financial assets at fair value through profit or loss (“FVTPL”)

A financial asset is classified at fair value through profit or loss if it is classified as held for trading or is designated as such upon initial recognition. Financial assets are designated as at FVTPL if

• It has been acquired principally for the purpose of selling in the near future;

• It is a part of an identified portfolio of financial instruments that the Company manages and has an actual pattern of short-term profit-taking or;

• It is a derivative that is not designated and effective as a hedging instrument.

The Company does not have any assets classified as FVTPL assets.

Held-to-maturity (“HTM”)

HTM investments are recognized on a trade-date basis and are initially measured at fair value, including transaction costs. The Company does not have any assets classified as HTM investments.

Available-for-sale financial assets (“AFS”)

AFS financial assets are non-derivatives that are either designated as AFS or are not classified as (i) loans and receivables, (ii) held-to-maturity investments or (iii) financial assets as at FVTPL. Subsequent to initial recognition, they are measured at fair value and changes therein, other than impairment losses and foreign currency differences on AFS monetary items, are recognized in other comprehensive income or loss. When an investment is derecognized, the cumulative gain or loss in the investment revaluation reserve is transferred to profit or loss. The Company classifies cash as AFS.

Loans and receivables

Loans and receivables are financial assets with fixed or determinable payments that are not quoted in an active market. Such assets are initially recognized at fair value plus any directly attributable transaction costs. Subsequent to initial recognition loans and receivables are measured at amortized cost using the effective interest method, less and impairment losses.

Derecognition of financial assets

A financial asset is derecognized when:

• The contractual right to the asset’s cash flows expire; or

• If the Company transfer the financial assets and substantially all risks and rewards of ownership to another entity.

Impairment of financial assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at each period end. Financial assets are impaired when there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investment have been impacted.

Objective evidence of impairment could include the following:

• Significant financial difficulty of the issuer or counterparty;

• Default or delinquency in interest or principal payments; or

• It has become probable that the borrower will enter bankruptcy or financial reorganization.

For financial assets carried at amortized cost, the amount of the impairment is the difference between the asset’s carrying amount and the present value of the estimated future cash flows, discounted at the financial asset’s original effective interest rate.

The carrying amount of all financial assets is directly reduced by the impairment loss. With the exception of AFS equity instruments, if, in a subsequent period, the amount of the impairment loss decreases and the decrease relates to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed through profit or loss. On the date of impairment reversal, the carrying amount of the financial asset cannot exceed its amortized cost had impairment not been recognized.

International Financial Reporting Standards 7, Financial Instruments: Disclosures, establishes a fair value hierarchy that reflects the significance of the inputs used in making the measurements. The fair value hierarchy has the following levels:

Level 1 – quoted prices (unadjusted) in active markets for identical assets or liabilities;

Level 2 - inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

Level 3 - inputs for the asset or liability that are not based on observable market data (unobservable inputs).

Fair Value of Financial Instruments

The Company’s financial assets include cash and are classified as Level 1. The carrying value of these instruments approximates their fair values due to the relatively short periods of maturity of these instruments.

Assets measured at fair value on a recurring basis were presented on the Company’s statements of financial position as at March 31, 2016 are as follows:

Fair Value Measurements Using Quoted Prices in Active

Markets For Identical Instruments (Level 1)

Significant Other Observable Inputs

(Level 2) Significant Unobservable

Inputs (Level 3)

Total

Cash $ 142,767 $ – $ - $ 142,767

FINANCIAL INSTRUMENTS

The Company’s financial instruments consist of cash. Unless otherwise noted, it is management’s opinion that the Company is not exposed to significant interest, currency or credit risks arising from these financial instruments. The fair values of these financial instruments approximate their carrying values unless otherwise stated.

ADDITIONAL DISCLOSURE FOR VENTURE ISSUERS Mineral Properties – Exploration and Evaluation The following tables set out the total deferred exploration costs recorded by the Company for the Copper King Property as at December 31, 2015 and March 31, 2016:

Acquisition

Costs Exploration

Costs Total

Balance, November 13, 2014 (inception) $ – $ – $ – Acquisition costs 5,000 – 5,000 Other exploration costs – 5,850 5,850 Balance, December 31, 2014 $ 5,000 $ 5,850 $ 10,850 Other exploration costs – 12,016 12,016

Balance, December 31, 2015 $ 5,000 $ 17,866 $ 22,866 Acquisition costs 4,500 – 4,500 Other exploration costs – 340 340 Balance, December 31, 2014 $ 9,500 $ 18,206 $ 27,706

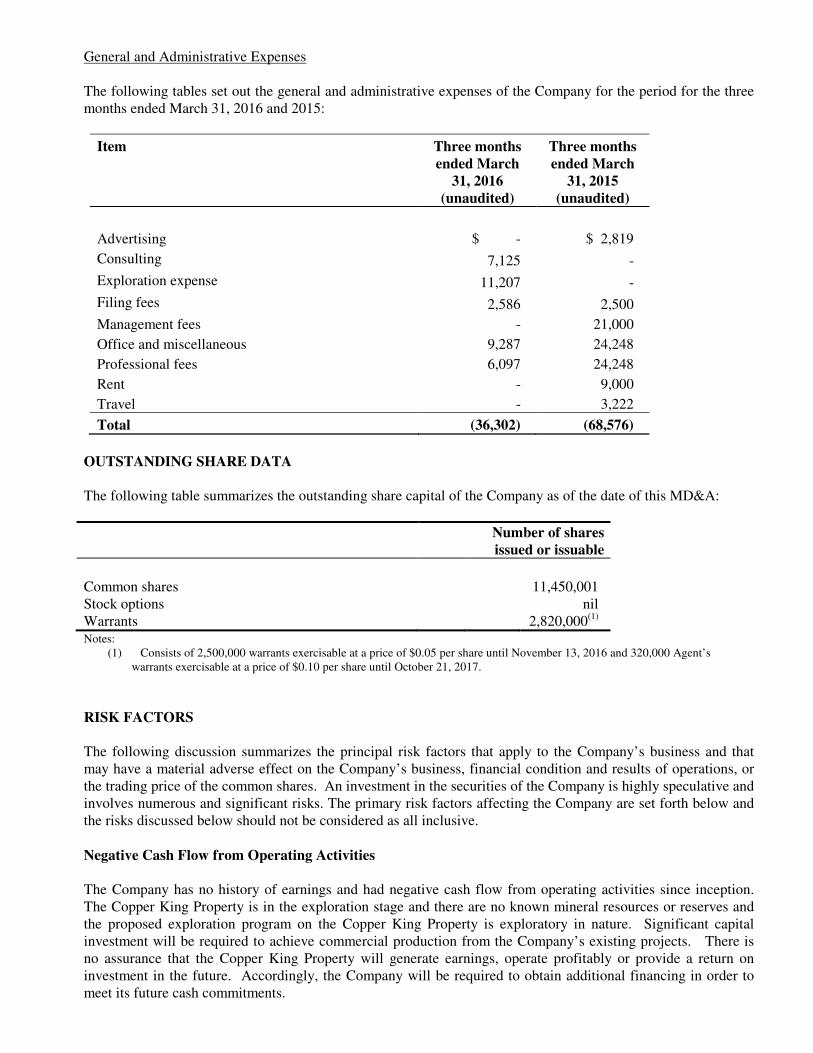

General and Administrative Expenses The following tables set out the general and administrative expenses of the Company for the period for the three months ended March 31, 2016 and 2015:

Item Three months ended March

31, 2016 (unaudited)

Three months ended March

31, 2015 (unaudited)

Advertising $ - $ 2,819

Consulting 7,125 -

Exploration expense 11,207 -

Filing fees 2,586 2,500

Management fees - 21,000

Office and miscellaneous 9,287 24,248

Professional fees 6,097 24,248

Rent - 9,000

Travel - 3,222

Total (36,302) (68,576)

OUTSTANDING SHARE DATA The following table summarizes the outstanding share capital of the Company as of the date of this MD&A:

Number of shares issued or issuable

Common shares 11,450,001 Stock options nil Warrants 2,820,000(1) Notes:

(1) Consists of 2,500,000 warrants exercisable at a price of $0.05 per share until November 13, 2016 and 320,000 Agent’s warrants exercisable at a price of $0.10 per share until October 21, 2017.

RISK FACTORS The following discussion summarizes the principal risk factors that apply to the Company’s business and that may have a material adverse effect on the Company’s business, financial condition and results of operations, or the trading price of the common shares. An investment in the securities of the Company is highly speculative and involves numerous and significant risks. The primary risk factors affecting the Company are set forth below and the risks discussed below should not be considered as all inclusive. Negative Cash Flow from Operating Activities The Company has no history of earnings and had negative cash flow from operating activities since inception. The Copper King Property is in the exploration stage and there are no known mineral resources or reserves and the proposed exploration program on the Copper King Property is exploratory in nature. Significant capital investment will be required to achieve commercial production from the Company’s existing projects. There is no assurance that the Copper King Property will generate earnings, operate profitably or provide a return on investment in the future. Accordingly, the Company will be required to obtain additional financing in order to meet its future cash commitments.