Form 1116 Foreign Tax Credits for Individuals: Mastering...

71

WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations: -Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN. IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: • Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa, MasterCard, Discover. • Listen on-line via your computer speakers. • Respond to five prompts during the program plus a single verification code. You will have to write down only the final verification code on the attestation form, which will be emailed to registered attendees. • To earn full credit, you must remain connected for the entire program. Form 1116 Foreign Tax Credits for Individuals: Mastering Calculations, Using Carryovers and Maximizing Benefits WEDNESDAY, AUGUST 17, 2016, 1:00-2:50 pm Eastern FOR LIVE PROGRAM ONLY

Transcript of Form 1116 Foreign Tax Credits for Individuals: Mastering...

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code. You will have to write down

only the final verification code on the attestation form, which will be emailed to registered attendees.

• To earn full credit, you must remain connected for the entire program.

Form 1116 Foreign Tax Credits for Individuals: Mastering

Calculations, Using Carryovers and Maximizing Benefits

WEDNESDAY, AUGUST 17, 2016, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

Aug. 17, 2016

Form 1116 Foreign Tax Credits for Individuals

William R. Skinner, Partner

Fenwick & West, Mountain View, Calif.

Neel Modha

Holthouse Carlin & Van Trigt, Costa Mesa, Calif.

Kevin M. Hall

Holland & Knight, Ft. Lauderdale, Fla.

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Form 1116 Foreign Tax Credits for Individuals: Mastering Calculations, Using Carryovers and

Maximizing Benefits

Presented by: William Skinner, Fenwick & West

Kevin Hall, Holland & Knight Neel Modha, Holthouse, Carlin & Van Trigt LLP

Wednesday, August 17, 2016

The Foreign Tax Credit, Overview

» U.S. persons generally are allowed a credit for foreign taxes paid

˗ Detailed statutory and regulatory guidance regarding eligibility and limitations

˗ Must be:

(1) person entitled to claim the credit; and

(2) creditable foreign tax

» Alternatives Territorial System

Deduction Only

6

Eligible Taxpayers

» U.S. Citizens/Resident Aliens and U.S. Corporations

˗ Allowed to credit income taxes paid to a foreign country or U.S. possession

» Partnerships

˗ Transparent under foreign law – foreign tax liability of partnership is creditable by U.S. partners

˗ Corporation under foreign law – foreign partners are entitled to a foreign tax credit for proportionate share of taxes paid by the partnership

» Foreign Persons

˗ General rule – no foreign tax credit

˗ Narrow exception – section 906 allows foreign person earning ECI a credit for

1) foreign source ECI and

2) U.S. source ECI if the foreign country deems the income to be sourced within its territory (source rather than residence based foreign tax)

7

Eligible Taxpayers (cont’d)

» Technical Taxpayer Rule ˗ Credit is allowed to the person who “paid or accrued” the

tax during the taxable year

˗ Regulations provide that payor of the foreign tax is “the person on whom foreign law imposes legal liability for such tax, even if another person (e.g., a withholding agent) remits such tax” and even if the economic burden of the tax is borne by another party to the transaction

» Nissho Iwai Corp. v. Comm’r, 89 T.C. 765 (1987) ˗ “Net loan” to Brazilian borrower – borrower pays

specified rate of interest after withholding tax

Even though borrower bears burden of withholding tax, U.S. lender is the technical taxpayer

8

Creditable Foreign Taxes

» 2 Requirements

˗ 1) Tax

˗ 2) On income (or section 903 in lieu of tax)

» Other foreign taxes

˗ Deduction only

9

Creditable Foreign Taxes (cont’d)

» Tax Defined ˗ Regulations define a “tax” as “a compulsory payment pursuant

to the authority of a foreign country to levy taxes”

» U.S. Legal Principles Apply ˗ Biddle v. Commissioner, 302 U.S. 573 (1938)

Whether a foreign levy is an income tax is determined by looking to U.S. tax law

Must be an income tax “in the U.S. sense”

Bearing burden of the foreign levy is not sufficient

10

Creditable Foreign Taxes (cont’d)

» Specific Economic Benefit ˗ Not a tax if payor receives “an economic benefit that is not

made available on substantially the same terms to substantially all persons”

» Dual Capacity Taxpayer ˗ Part Tax / Part Subsidy

˗ Levy imposed on the dual capacity taxpayer differs from the levy imposed on other taxpayers

˗ Result Credit allowed for tax portion

Deduction generally allowed for the subsidy portion

11

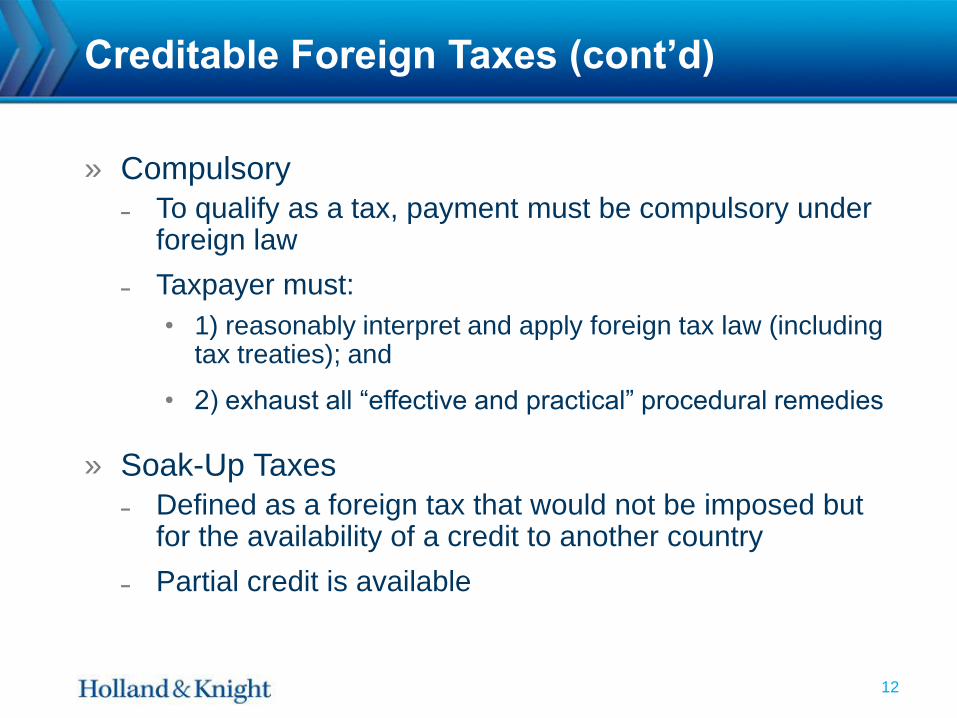

Creditable Foreign Taxes (cont’d)

» Compulsory

˗ To qualify as a tax, payment must be compulsory under foreign law

˗ Taxpayer must:

• 1) reasonably interpret and apply foreign tax law (including tax treaties); and

• 2) exhaust all “effective and practical” procedural remedies

» Soak-Up Taxes

˗ Defined as a foreign tax that would not be imposed but for the availability of a credit to another country

˗ Partial credit is available

12

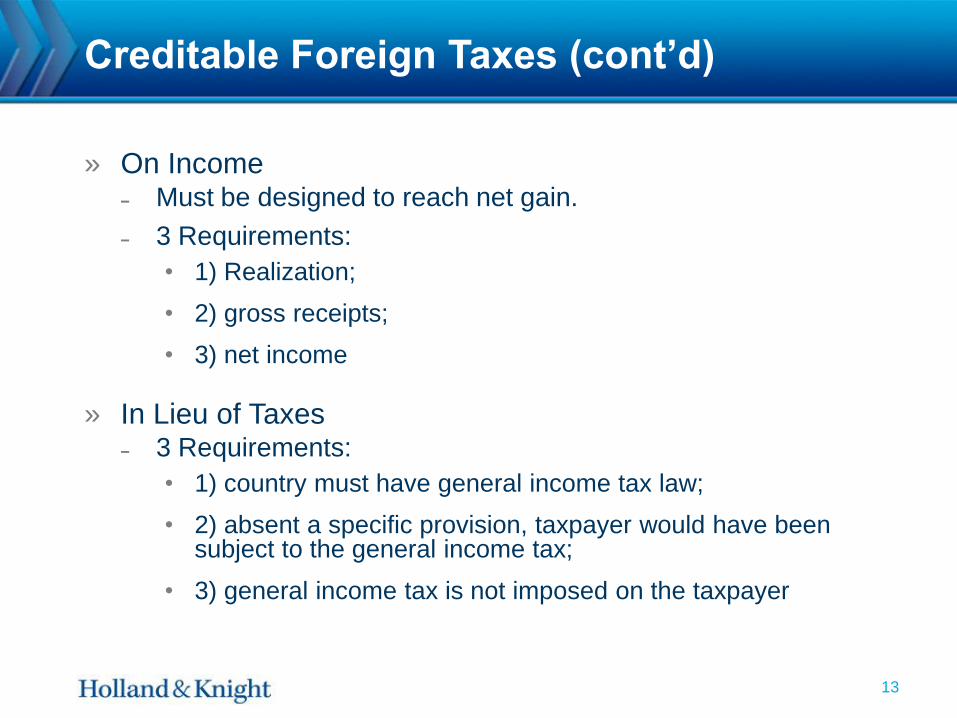

Creditable Foreign Taxes (cont’d)

» On Income ˗ Must be designed to reach net gain.

˗ 3 Requirements:

• 1) Realization;

• 2) gross receipts;

• 3) net income

» In Lieu of Taxes ˗ 3 Requirements:

• 1) country must have general income tax law;

• 2) absent a specific provision, taxpayer would have been subject to the general income tax;

• 3) general income tax is not imposed on the taxpayer

13

Tax Treaties

» Tax Treaties

˗ Typically incorporate otherwise allowable foreign tax

credits

˗ Generally do not provide for credits not otherwise

available under the Code

» But may:

˗ Specifically provide that a tax is creditable; or

˗ Treat income (e.g., gain from sale of stock) as

foreign source

14

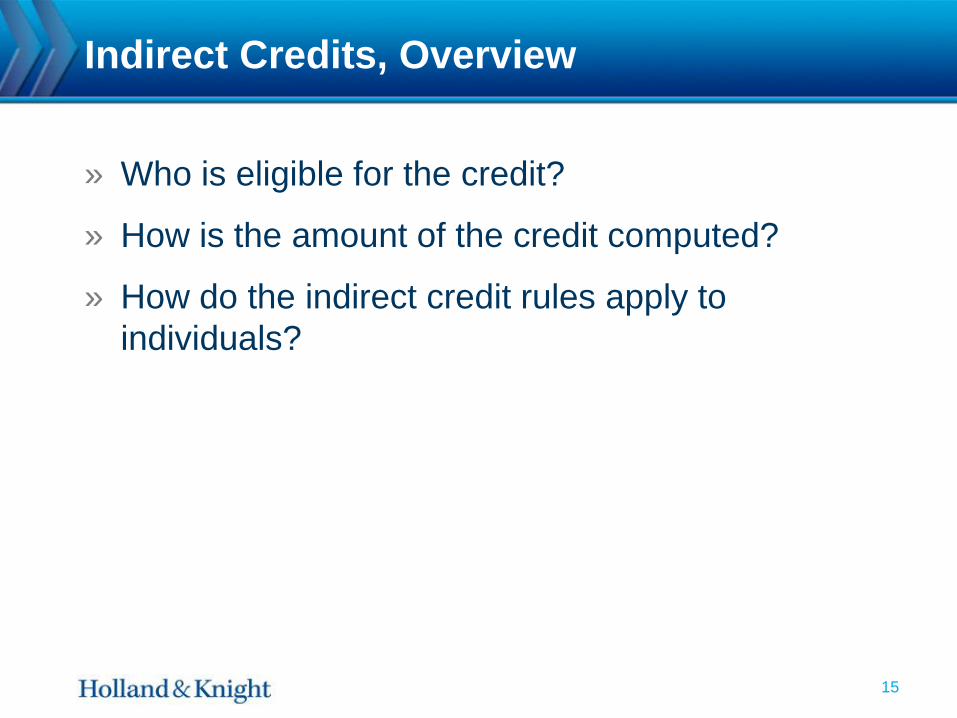

Indirect Credits, Overview

» Who is eligible for the credit?

» How is the amount of the credit computed?

» How do the indirect credit rules apply to

individuals?

15

Indirect Credits, Eligibility

» Indirect Credits ˗ Section 902 provides that a domestic corporation is

deemed to have paid its share of foreign taxes paid by a foreign corporation when:

1) it receives a dividend from the foreign corporation;

2) it includes income of the foreign corporation under section 951; and

3) it recognizes gain on the sale of the stock of a CFC

» Domestic Corporations Only ˗ Ownership Requirement:

1) at least 10% of voting stock of first-tier subsidiary; or

2) at least 5% of the indirect voting interest in a lower-tier subsidiary

16

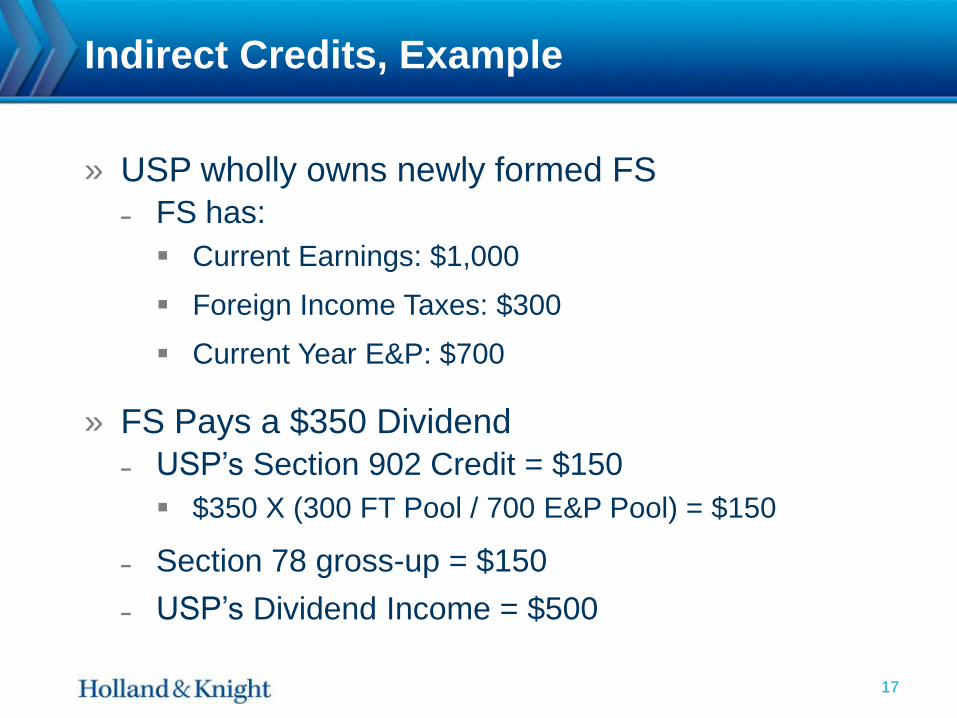

Indirect Credits, Example

» USP wholly owns newly formed FS

˗ FS has:

Current Earnings: $1,000

Foreign Income Taxes: $300

Current Year E&P: $700

» FS Pays a $350 Dividend

˗ USP’s Section 902 Credit = $150

$350 X (300 FT Pool / 700 E&P Pool) = $150

˗ Section 78 gross-up = $150

˗ USP’s Dividend Income = $500

17

Indirect Credits, Individuals

» Section 962 Election

˗ A U.S. individual, trust, or estate may elect to be taxed as a domestic corporation with respect to income included under section 951

» Consequences

˗ U.S. shareholder is taxed at corporate income tax rates and is eligible for indirect credits under the section 960 rules; and

˗ Subsequent distribution of the earnings is taxable to the shareholder at ordinary income tax rates

» Planning

˗ Reduces tax liability in year of section 951 inclusion

˗ Adds second level of tax upon distribution

˗ May be beneficial if second tax is deferred for significant period of time

18

Foreign Tax Credit

for Individuals:

Documentation and

Calculation

Neel Modha

August 17, 2016

Credit vs Deduction - Documentation 1. How to elect to take credit versus deduction

a. Itemize deduction (Form 1040, Schedule A) b. Foreign Tax Credit (Form 1116 – Attach to Form 1040) c. Annual choice

2. Claiming FTC Without Filing Form 1116 - Requirements a. All foreign source income is passive income; b. Reported on a qualified payee statement (e.g., Form 1099, Sch K-1); c. Total of qualified foreign taxes does not exceed a limit;

i. Limit for tax year 2015 = $300 (or $600 if MFJ) d. Asset giving rise to interest and dividends held for at least 16 days; e. Not filing Form 4563 or excluding income from sources within Puerto Rico;

and f. All foreign taxes were (i) legally owed and (ii) paid to countries recognized

by the US and do not support terrorism

3. If you claim the credit directly on Form 1040 without filing Form 1116, you cannot carry back or carry forward any unused foreign tax to or from this year.

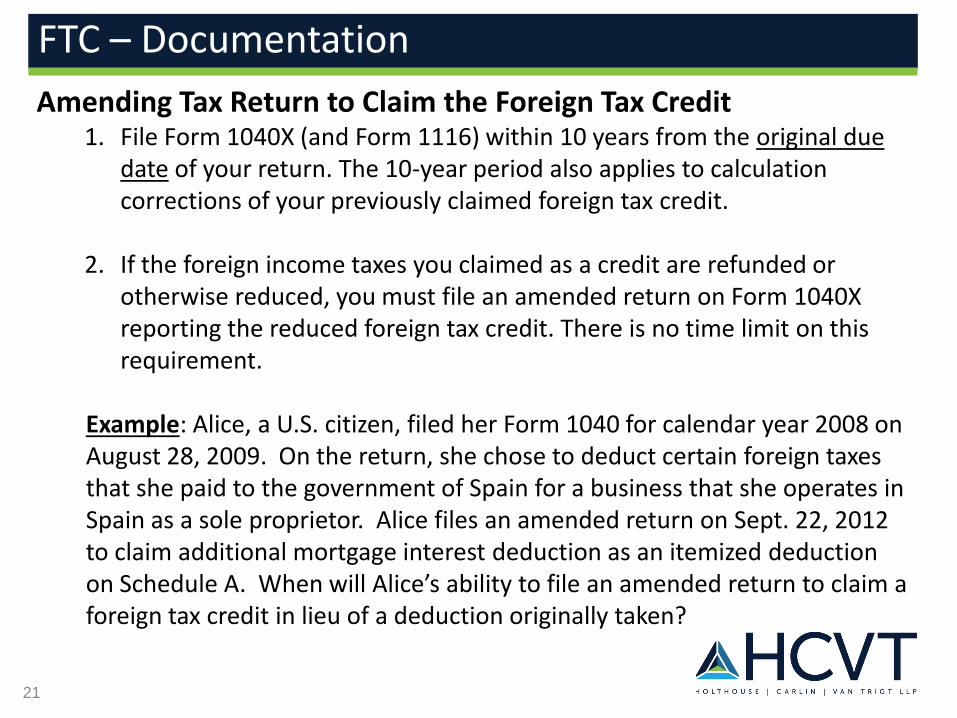

FTC – Documentation

20

Amending Tax Return to Claim the Foreign Tax Credit 1. File Form 1040X (and Form 1116) within 10 years from the original due

date of your return. The 10-year period also applies to calculation corrections of your previously claimed foreign tax credit.

2. If the foreign income taxes you claimed as a credit are refunded or otherwise reduced, you must file an amended return on Form 1040X reporting the reduced foreign tax credit. There is no time limit on this requirement.

Example: Alice, a U.S. citizen, filed her Form 1040 for calendar year 2008 on August 28, 2009. On the return, she chose to deduct certain foreign taxes that she paid to the government of Spain for a business that she operates in Spain as a sole proprietor. Alice files an amended return on Sept. 22, 2012 to claim additional mortgage interest deduction as an itemized deduction on Schedule A. When will Alice’s ability to file an amended return to claim a foreign tax credit in lieu of a deduction originally taken?

FTC – Documentation

21

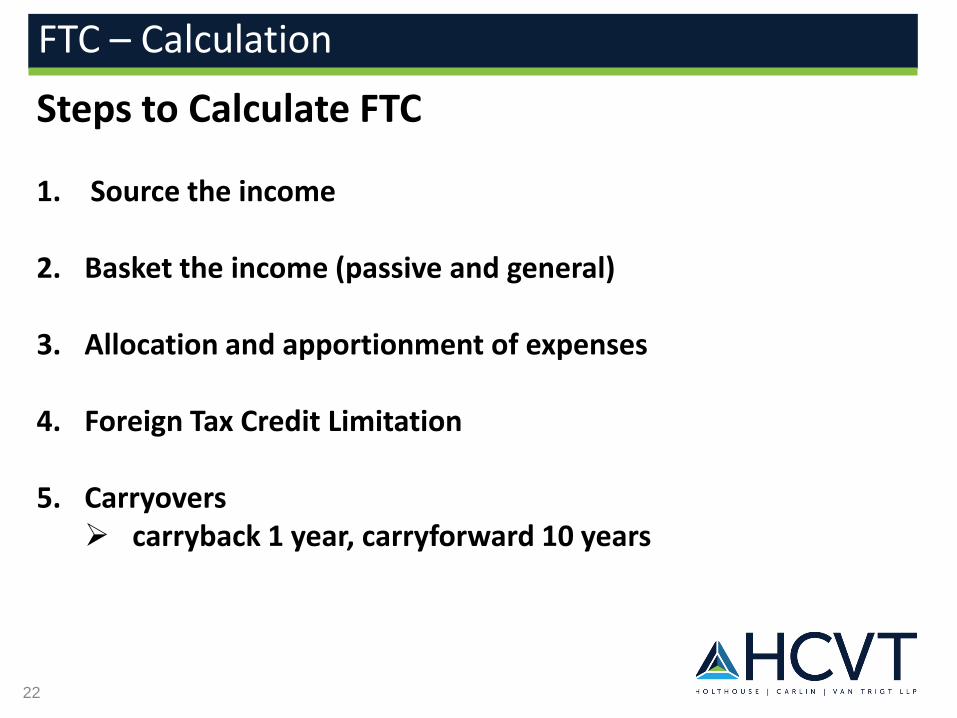

Steps to Calculate FTC

1. Source the income

2. Basket the income (passive and general)

3. Allocation and apportionment of expenses

4. Foreign Tax Credit Limitation

5. Carryovers carryback 1 year, carryforward 10 years

FTC – Calculation

22

Income Source Rules

FTC – Calculation

23

Type of income Source rule (in general)

Dividend Residence of payor Exception for foreign corp with >=25% US ECI

Interest Residence of payor Exception for US corp with 80% active business income from foreign sources over prior 3 years

Rent Location property used

Royalties Location IP is used

Gain from sale of personal property

Residence of seller US citizen with foreign tax home is foreign source

Gain from sale of inventory Location of sale Special rules if inventory is manufactured

Services Location where services are performed Commercial traveler exception

Income Source Rules – Examples Example #1 Adam receives $2,000 of interest income from domestic corporation ABC Co, and $10,000 of interest income from US corporation DEF Co. All of ABC Co’s income from inception has been US source income. For the past three years, 90% of DEF Co’s gross income has been active foreign business income. What is the source of the interest income that Adam receives for the current tax year from ABC Co and DEF Co?

FTC – Calculation

24

Income Source Rules – Examples Example #2 Barbara receives dividends from the following corporations for the current tax year. Calculate the amount of US source income:

FTC – Calculation

25

Amount Corporation % ECI for past 3 years US source income

$1,000 GHI Co (domestic) ?

$2,000 JKL Co (foreign) 20% ?

$3,000 MNO Co (foreign) 90% ?

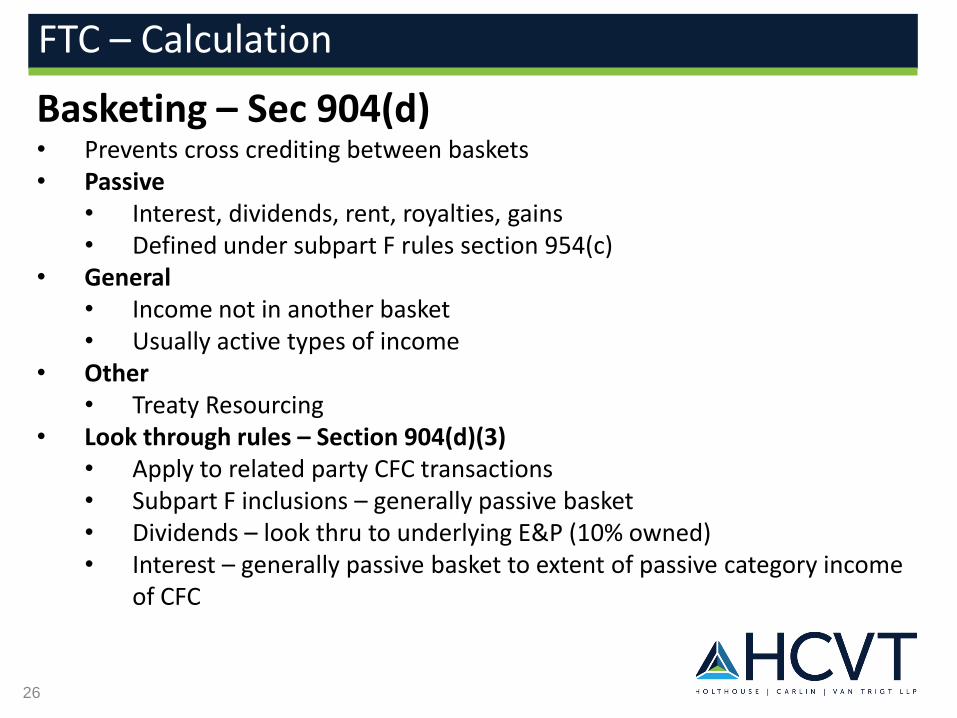

Basketing – Sec 904(d) • Prevents cross crediting between baskets • Passive

• Interest, dividends, rent, royalties, gains • Defined under subpart F rules section 954(c)

• General • Income not in another basket • Usually active types of income

• Other • Treaty Resourcing

• Look through rules – Section 904(d)(3) • Apply to related party CFC transactions • Subpart F inclusions – generally passive basket • Dividends – look thru to underlying E&P (10% owned) • Interest – generally passive basket to extent of passive category income

of CFC

FTC – Calculation

26

Three Types of Apportionment Rules 1. “Factual Relationship” Method Used for deductions definitely related to a class of

gross income, including all gross income. Temp. Reg. § 1.861-8T(c)(1).

2. Gross Income Method Required for deductions not definitely related to any

gross income. Treas. Reg. § 1.861-8(c)(3). 3. Specifically Prescribed Methods. Treas. Reg. § 1.861-

8(e) and Temp. Reg. § 1.861-8T(e).

FTC – Calculation

27

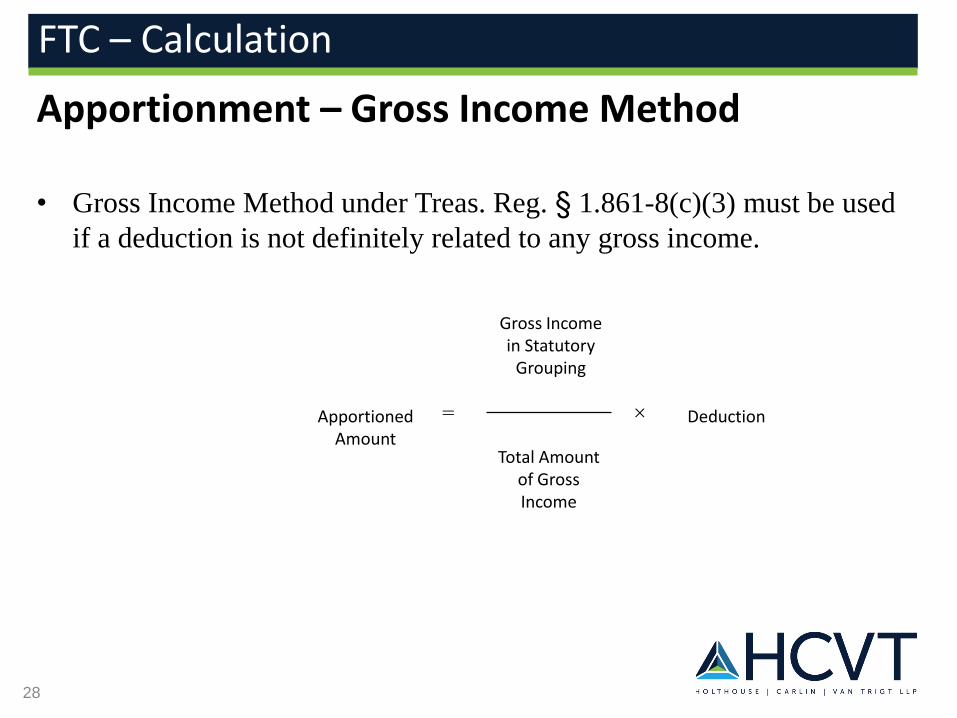

Apportionment – Gross Income Method

• Gross Income Method under Treas. Reg. § 1.861-8(c)(3) must be used

if a deduction is not definitely related to any gross income.

FTC – Calculation

28

Gross Income in Statutory

Grouping

Apportioned

Amount

=

Deduction

Total Amount of Gross Income

Expense Allocation for Individuals • Some deductions do not definitely relate to either your foreign source income or

your US source income. These expenses (except for interest expense) are allocated pro rata using the gross income method.

• Charitable contribution are definitely related and allocable to all of taxpayer’s gross income. The deduction is ratably apportioned between statutory grouping of gross income and the residual grouping on the basis of the relative amounts of U.S. source gross income in each grouping. It cannot offset foreign source income. Effectively, it cannot impair the foreign tax credit limitation.

• Mortgage interest is allocated using the gross income method unless the taxpayer’s FSI (including income excluded on Form 2555) does not exceed $5,000. Then the taxpayer can allocate all mortgage expense to US source income.

• Other interest (investment interest, passive activity interest, interest incurred in a trade or business) is allocated using the “asset method” unless the taxpayer’s FSI (including income excluded on Form 2555) does not exceed $5,000. Then the taxpayer can allocate all other interest expense to US source income.

FTC – Calculation

29

Foreign Tax Credit - IRC Section 904(d)

• Purpose = to prevent taxpayers from crediting foreign taxes against U.S.

taxes levied on U.S. source income

• Rule: FTC cannot exceed the lesser of two amounts: 1. Actual foreign taxes paid or accrued; or 2. U.S. tax on foreign source income

FTC – Calculation

30

Foreign-source taxable income

FTC

Limitation =

U.S. tax

before FTC Total taxable

income

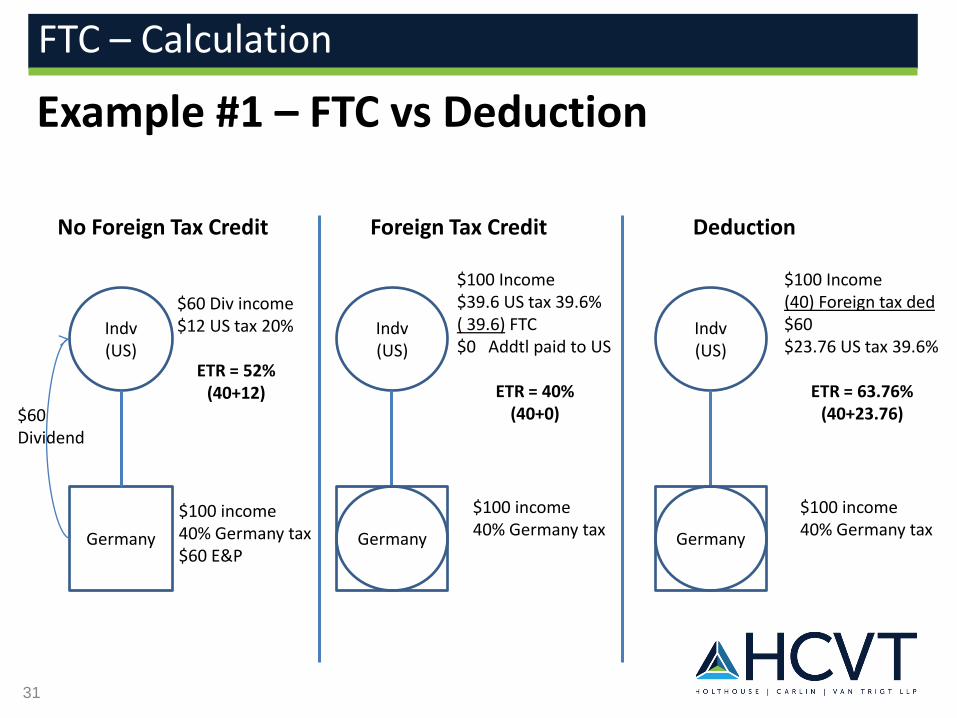

Example #1 – FTC vs Deduction

FTC – Calculation

31

Indv (US)

Germany

$100 income 40% Germany tax $60 E&P

No Foreign Tax Credit

$60 Div income $12 US tax 20%

ETR = 52% (40+12)

$60 Dividend

Foreign Tax Credit

Indv (US)

Germany

$100 income 40% Germany tax

$100 Income $39.6 US tax 39.6% ( 39.6) FTC $0 Addtl paid to US

ETR = 40% (40+0)

Deduction

Indv (US)

Germany

$100 income 40% Germany tax

$100 Income (40) Foreign tax ded $60 $23.76 US tax 39.6%

ETR = 63.76% (40+23.76)

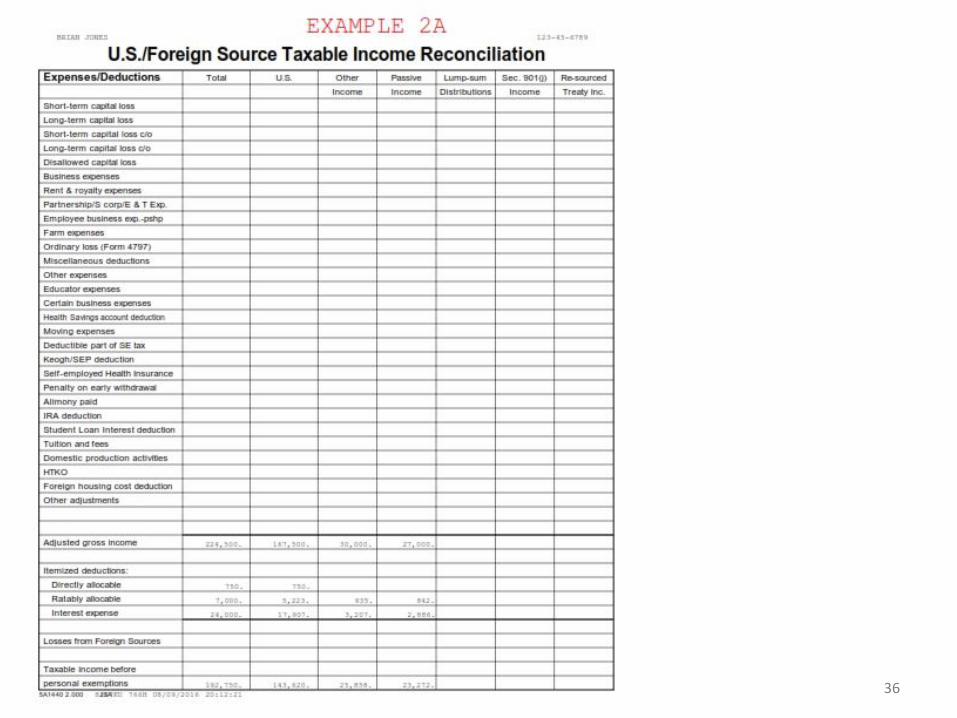

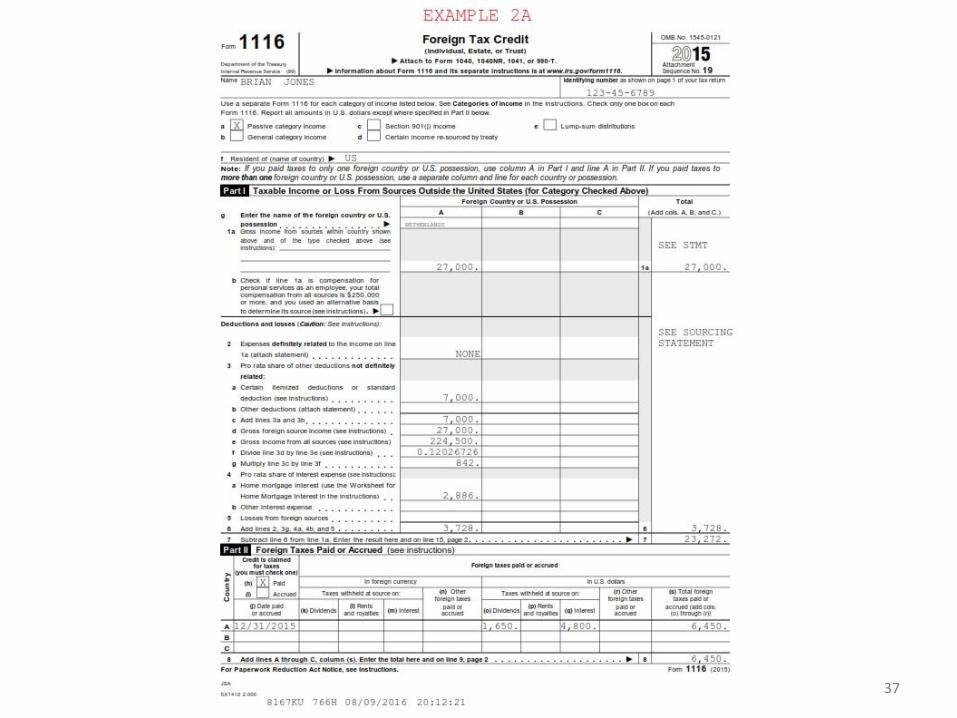

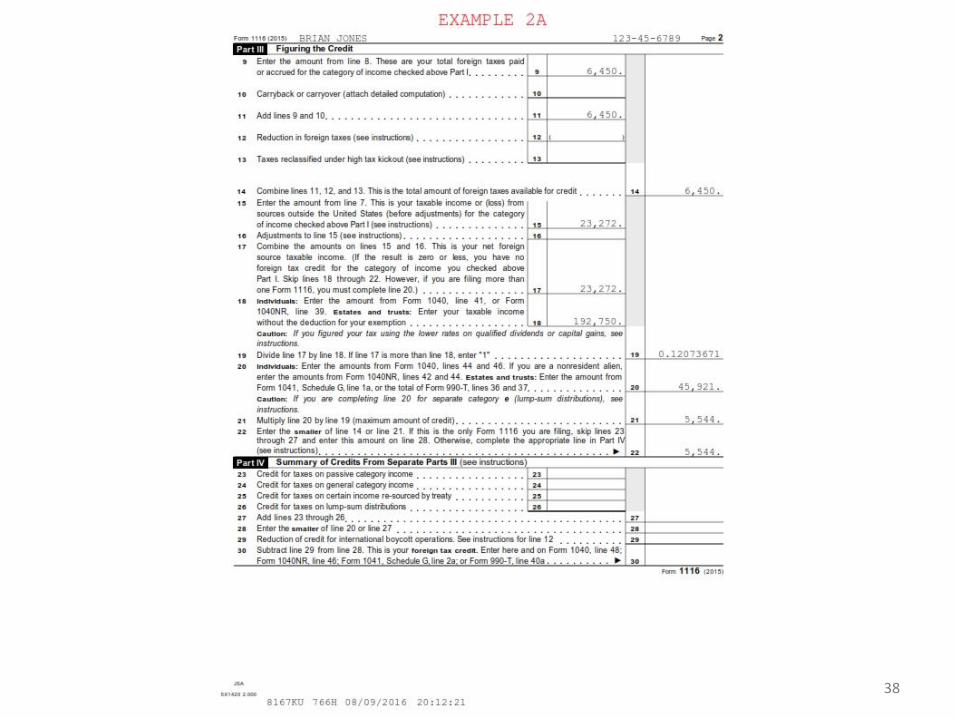

Example #2a Brian Jones is a US citizen living in Texas and has the following types of income and expenses for tax year 2015: 1. What is the source of Brian’s income items? 2. Calculate his foreign tax credit for 2015 and calculate any

excess foreign tax credits

FTC – Calculation

32

Income Tax Withheld

Wage income from US employer (services performed in the US) $ 150,000.00 $ 35,000.00

Partnership K-1

Nonqualified Dividend income from US-based corporation $ 7,500.00

Interest income from US government bond $ 10,000.00

Nonqualified Dividend from Dutch corporation (less than 10% owned) $ 11,000.00 $ 1,650.00

Interest income from Dutch government bond $ 16,000.00 $ 4,800.00

Consulting services performed in the Netherlands $ 30,000.00 $ 9,000.00

Total $ 224,500.00 $ 50,450.00

Mortgage Interest $ (24,000.00)

Charitable contributions $ (750.00)

Property taxes $ (7,000.00)

Total itemized deductions $ (31,750.00)

33

34

35

36

37

38

39

40

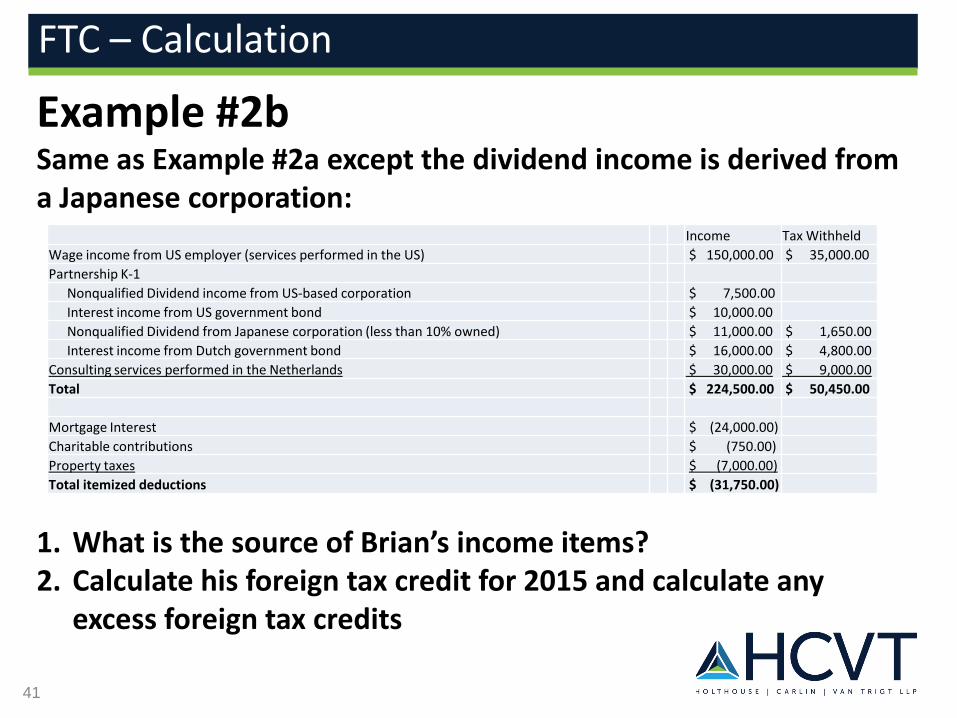

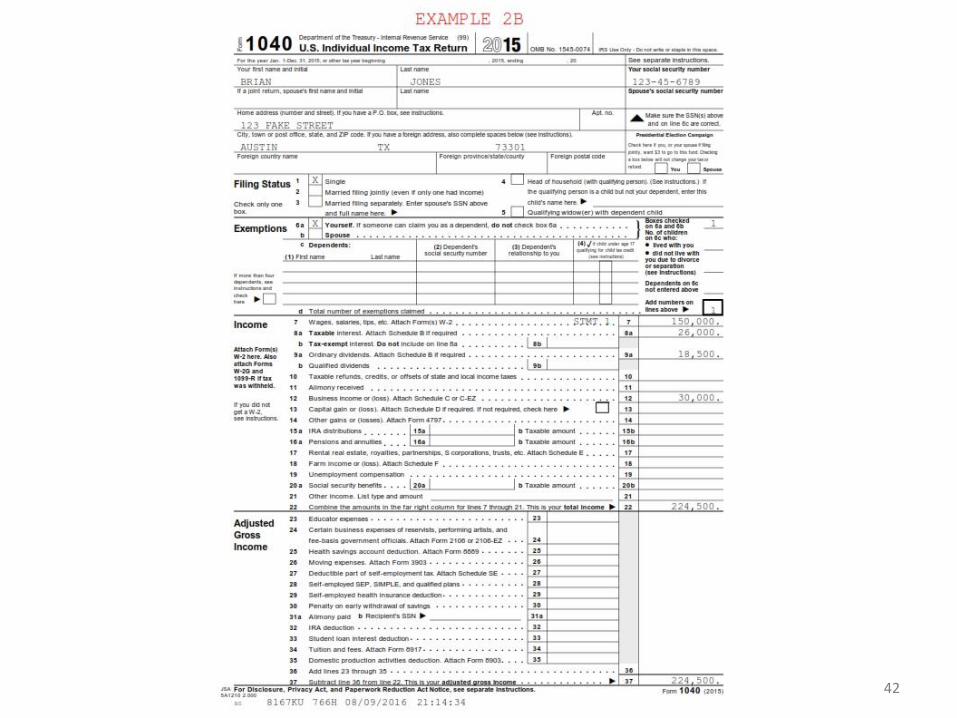

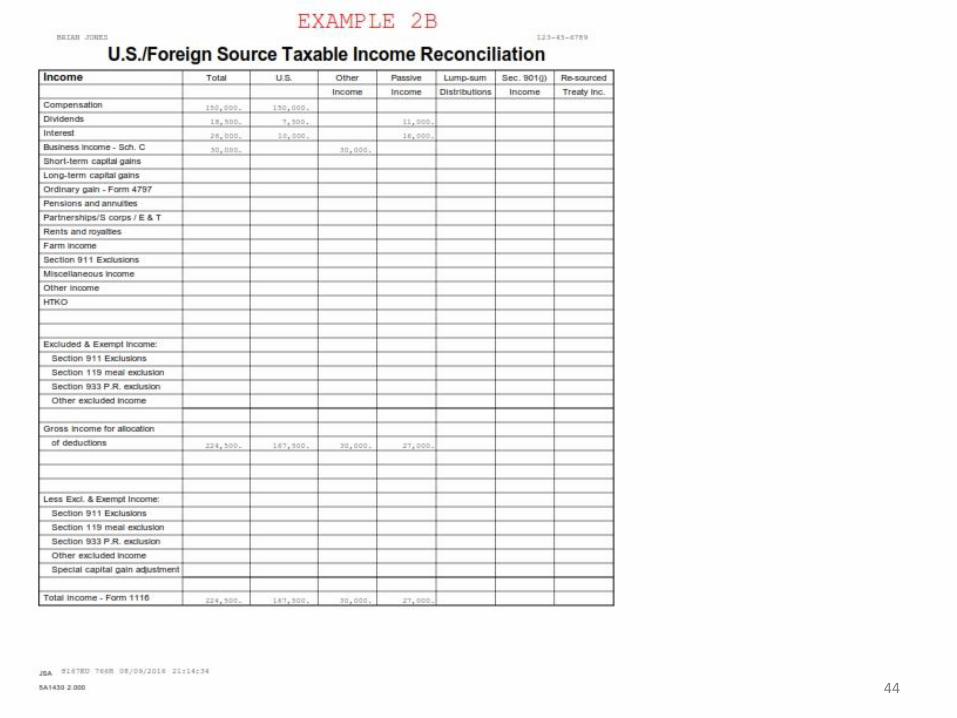

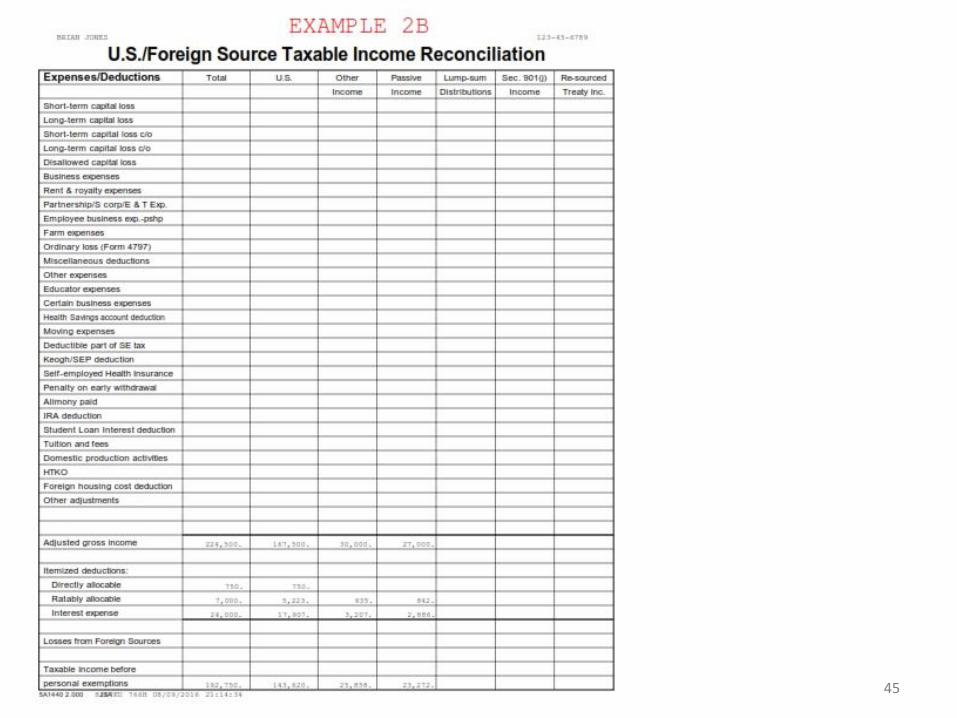

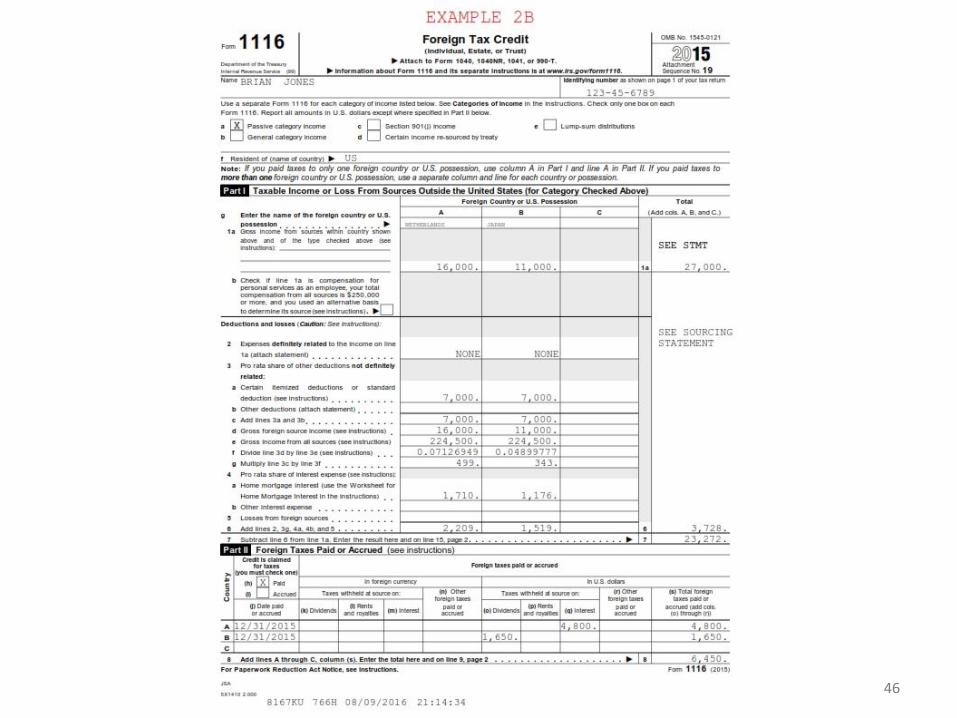

Example #2b Same as Example #2a except the dividend income is derived from a Japanese corporation: 1. What is the source of Brian’s income items? 2. Calculate his foreign tax credit for 2015 and calculate any

excess foreign tax credits

FTC – Calculation

41

Income Tax Withheld

Wage income from US employer (services performed in the US) $ 150,000.00 $ 35,000.00

Partnership K-1

Nonqualified Dividend income from US-based corporation $ 7,500.00

Interest income from US government bond $ 10,000.00

Nonqualified Dividend from Japanese corporation (less than 10% owned) $ 11,000.00 $ 1,650.00

Interest income from Dutch government bond $ 16,000.00 $ 4,800.00

Consulting services performed in the Netherlands $ 30,000.00 $ 9,000.00

Total $ 224,500.00 $ 50,450.00

Mortgage Interest $ (24,000.00)

Charitable contributions $ (750.00)

Property taxes $ (7,000.00)

Total itemized deductions $ (31,750.00)

42

43

44

45

46

47

48

49

Foreign Tax Credit (“FTC”) for Individuals –

The FTC Limitation &

Other Important FTC Rules and Pitfalls

50

51

William R. Skinner, Esq. is a tax partner

with Fenwick & West LLP, in Mountain

View, CA. He graduated from Stanford

Law School and was recognized as a

Rising Star in Tax by California Super

Lawyers. He focuses his practice on U.S.

international and corporate taxation,

including the full range of international

tax issues such as subpart F and deferral

structures, foreign tax credits, transfer

pricing, IP migration and structuring IP

ownership within a corporate group,

internal restructurings and cross-border

M&A, and tax treaties and inbound tax

planning. More information about his

practice is available at

www.fenwick.com.

William R. Skinner

Partner, Tax Group

Phone: 650.335.7669

Fax: 650.938.5200

E-mail:

Emphasis:

International Tax

Tax Planning

Tax Controversy

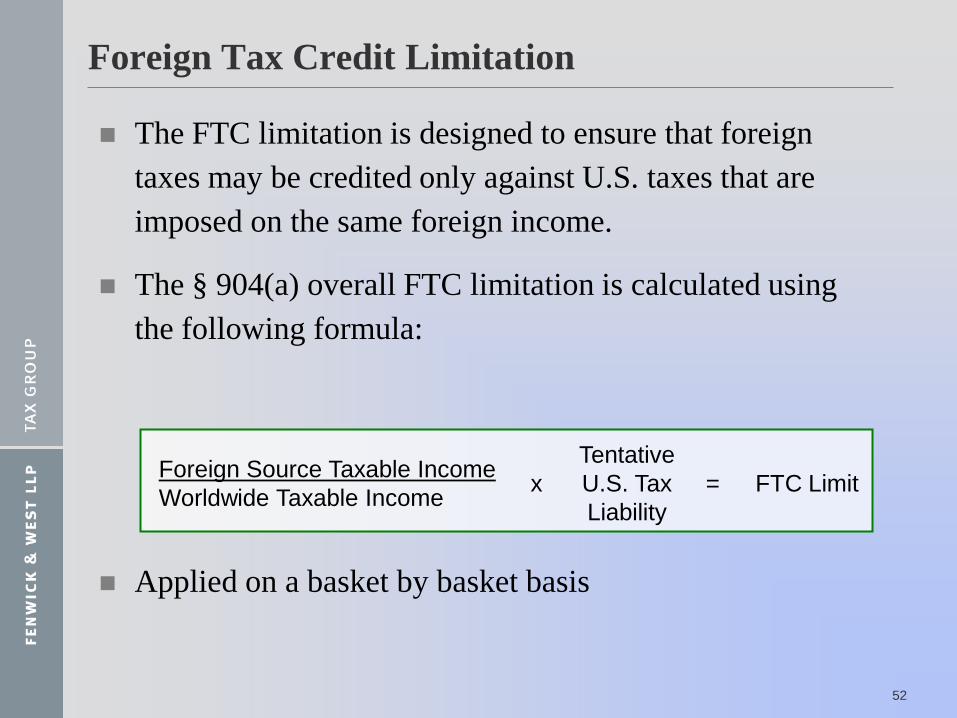

Foreign Tax Credit Limitation

The FTC limitation is designed to ensure that foreign

taxes may be credited only against U.S. taxes that are

imposed on the same foreign income.

The § 904(a) overall FTC limitation is calculated using

the following formula:

Applied on a basket by basket basis

Foreign Source Taxable Income

Worldwide Taxable Income

Tentative

U.S. Tax

Liability

x = FTC Limit

52

Foreign Tax Credit Limitation

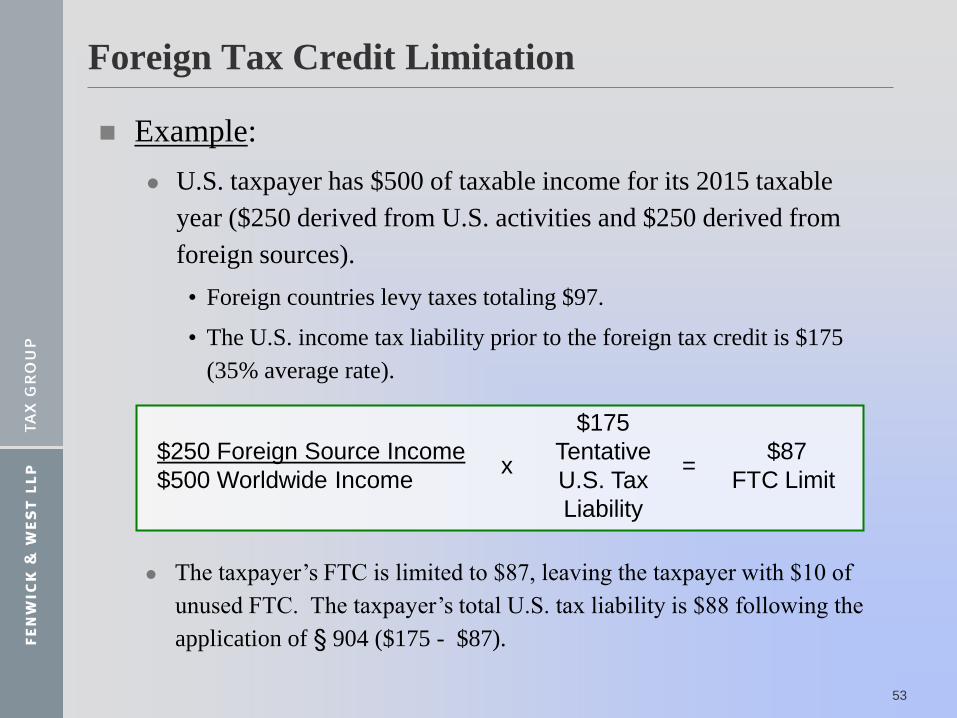

Example:

U.S. taxpayer has $500 of taxable income for its 2015 taxable

year ($250 derived from U.S. activities and $250 derived from

foreign sources).

• Foreign countries levy taxes totaling $97.

• The U.S. income tax liability prior to the foreign tax credit is $175

(35% average rate).

$250 Foreign Source Income

$500 Worldwide Income

$175

Tentative

U.S. Tax

Liability

x = $87

FTC Limit

The taxpayer’s FTC is limited to $87, leaving the taxpayer with $10 of

unused FTC. The taxpayer’s total U.S. tax liability is $88 following the

application of § 904 ($175 - $87).

53

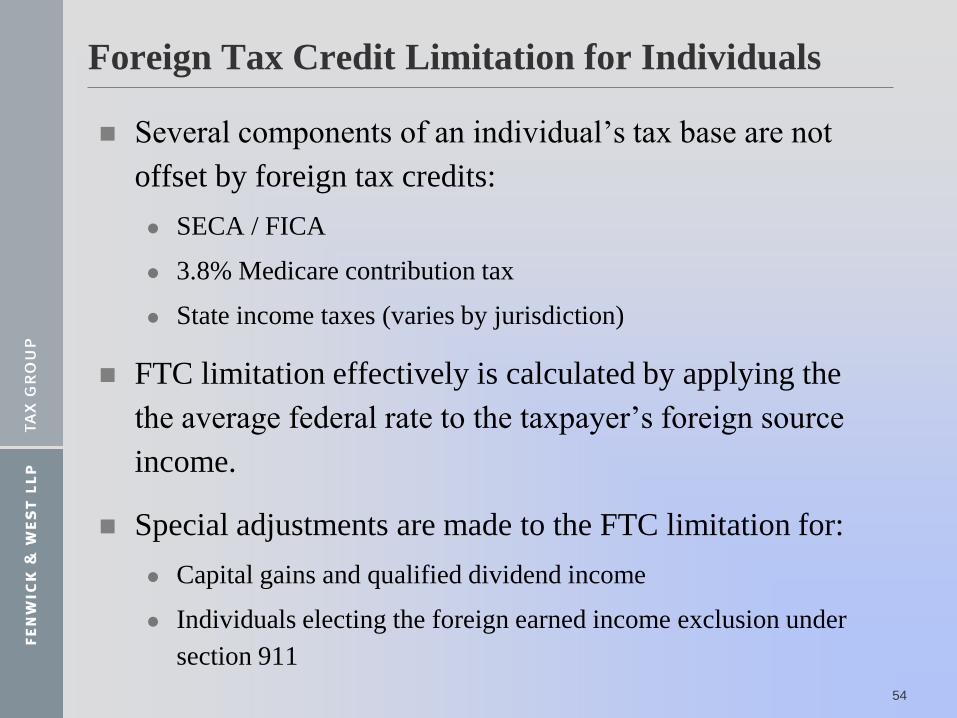

Foreign Tax Credit Limitation for Individuals

Several components of an individual’s tax base are not

offset by foreign tax credits:

SECA / FICA

3.8% Medicare contribution tax

State income taxes (varies by jurisdiction)

FTC limitation effectively is calculated by applying the

the average federal rate to the taxpayer’s foreign source

income.

Special adjustments are made to the FTC limitation for:

Capital gains and qualified dividend income

Individuals electing the foreign earned income exclusion under

section 911

54

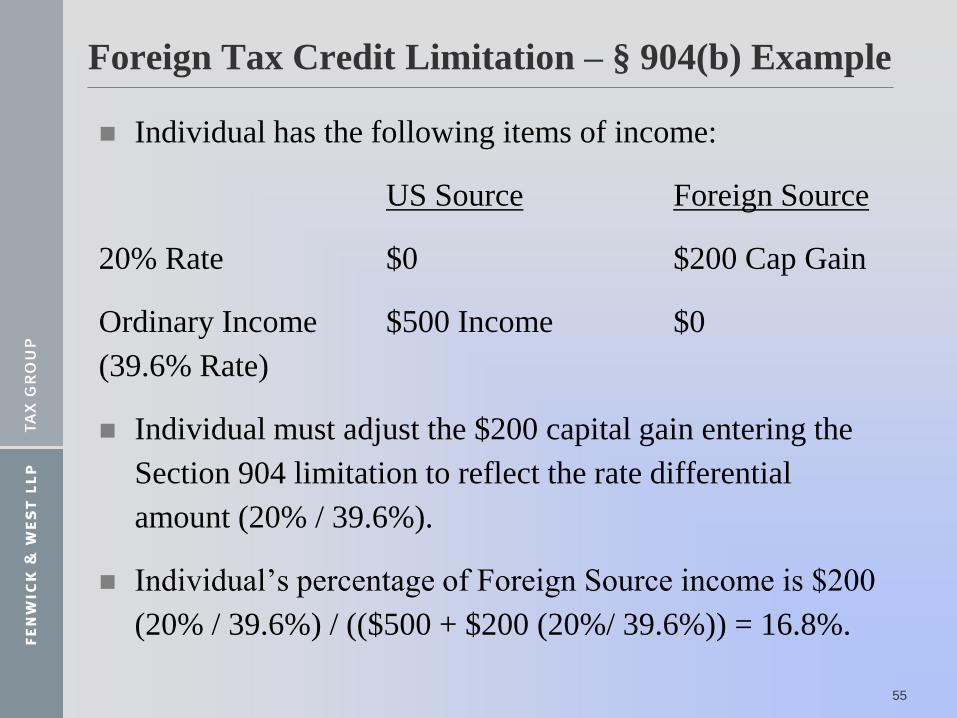

Foreign Tax Credit Limitation – § 904(b) Example

Individual has the following items of income:

US Source Foreign Source

20% Rate $0 $200 Cap Gain

Ordinary Income $500 Income $0

(39.6% Rate)

Individual must adjust the $200 capital gain entering the

Section 904 limitation to reflect the rate differential

amount (20% / 39.6%).

Individual’s percentage of Foreign Source income is $200

(20% / 39.6%) / (($500 + $200 (20%/ 39.6%)) = 16.8%.

55

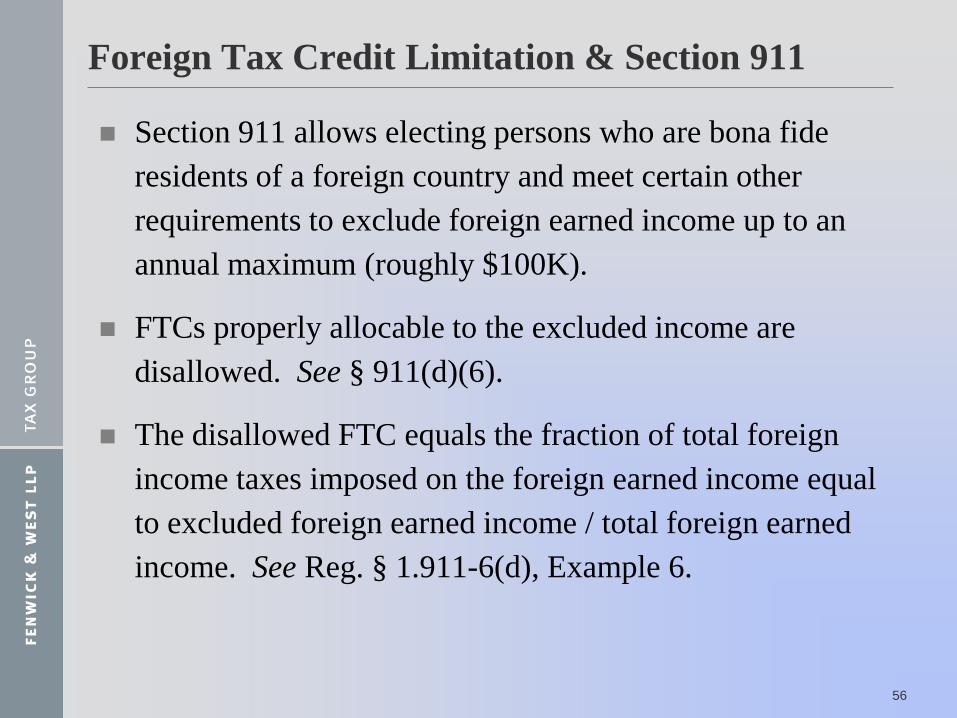

Foreign Tax Credit Limitation & Section 911

Section 911 allows electing persons who are bona fide

residents of a foreign country and meet certain other

requirements to exclude foreign earned income up to an

annual maximum (roughly $100K).

FTCs properly allocable to the excluded income are

disallowed. See § 911(d)(6).

The disallowed FTC equals the fraction of total foreign

income taxes imposed on the foreign earned income equal

to excluded foreign earned income / total foreign earned

income. See Reg. § 1.911-6(d), Example 6.

56

Foreign Tax Credit Limitation & Section 911

Example: X, a single individual earns $200,000 of

foreign salary on which $50,000 of foreign income tax is

imposed. X has no other income and assume, for

simplicity, that X has no deductions. X elects to exclude

$100,000 from gross income under Section 911(a).

X’s allowable foreign tax credit is reduced to $25,000

($50,000 * $100,000 / $200,000).

X’s Section 904 limitation is $27,955 (Total Fed tax *

$100,000 of FSI / $100,000 of total WWTI)). X fully

utilizes the $25,000 of FTCs.

*$27,995 = incremental tax on an individual from $100,000

to $200,000 under the Section 911(f)“Stacking Rule”. 57

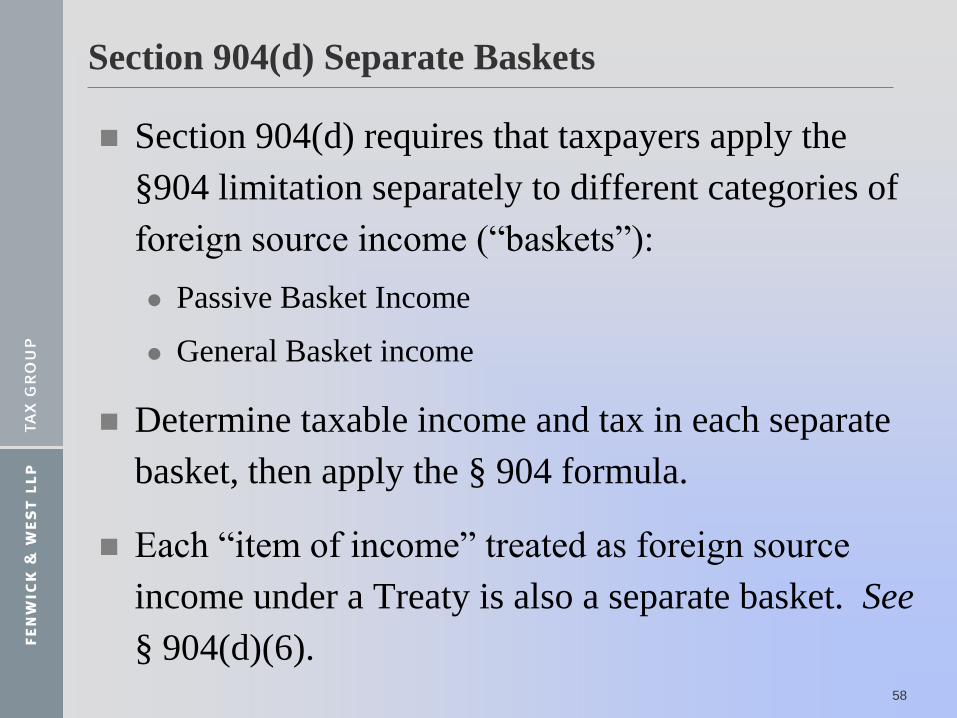

Section 904(d) Separate Baskets

Section 904(d) requires that taxpayers apply the

§904 limitation separately to different categories of

foreign source income (“baskets”):

Passive Basket Income

General Basket income

Determine taxable income and tax in each separate

basket, then apply the § 904 formula.

Each “item of income” treated as foreign source

income under a Treaty is also a separate basket. See

§ 904(d)(6). 58

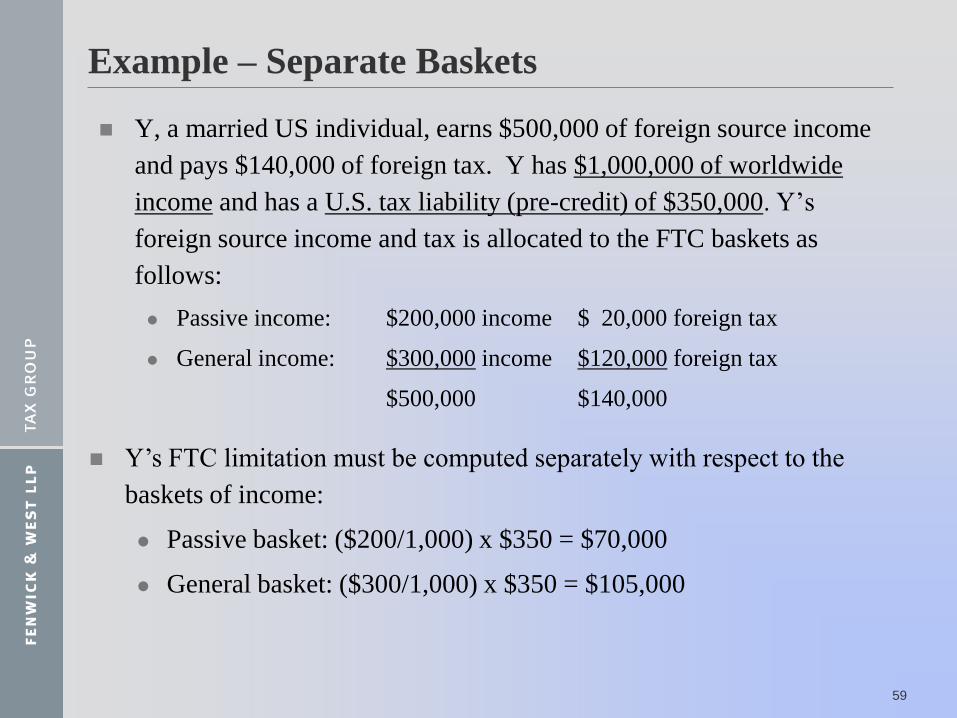

Y, a married US individual, earns $500,000 of foreign source income

and pays $140,000 of foreign tax. Y has $1,000,000 of worldwide

income and has a U.S. tax liability (pre-credit) of $350,000. Y’s

foreign source income and tax is allocated to the FTC baskets as

follows:

Passive income: $200,000 income $ 20,000 foreign tax

General income: $300,000 income $120,000 foreign tax

$500,000 $140,000

Example – Separate Baskets

Y’s FTC limitation must be computed separately with respect to the

baskets of income:

Passive basket: ($200/1,000) x $350 = $70,000

General basket: ($300/1,000) x $350 = $105,000

59

Section 904(c) Carryover / Carryback

Section 904(c) allows foreign income taxes in excess of

the Section 904 limitation for the year to be carried back

to the one (1) preceding taxable year, and then carried

forward to the following ten (10) taxable years.

Carryforward / carryback occurs on a basket-by-basket

basis.

Taxes paid or accrued in a year may be carried forward or

back from that year even if the taxpayer has no foreign

income in the year when the taxes were paid or accrued.

See Chief Counsel Advice 201438027.

60

Sourcing Rules – Compensation for Services

Place of performance sourcing rule also applies to multi-

year compensation arrangements (e.g., stock options,

RSUs).

Reg. § 1.861-4(b)(2)(ii)(F) - Attribution of compensation

to services during a multi-year period depends on the facts

and circumstances of the case. In some cases, time-based

analysis throughout the vesting period may be the best

measure.

US and foreign countries may not have same rules for

source and timing of such income, complicating FTC.

61

Sourcing Rules – Capital Gains

General rule is “residence of the seller.” § 865(a).

Several Code-based exceptions may provide foreign

source treatment to a US citizen / resident alien, including

the following:

Sale of real estate with a foreign situs. § 862(a)(5).

Deemed dividend on sale of CFC stock. § 1248.

Certain foreign IP sales with a royalty component. § 865(d)(1)(B).

Certain foreign-connected sales subject to at least 10% foreign tax

in the relevant country.

• US citizen or resident alien with “tax home” in a foreign country.

§865(g).

• US person with a foreign office to which the sale is attributable.

§865(e).

62

Sourcing Rules – Treaty Relief

Depending on applicable treaty terms, foreign source

treatment may be available under a tax treaty to avoid

double taxation.

2006 US Model Treaty Article 23(3). Where income of a

US resident is taxable in foreign country under treaty, the

income shall be sourced to that country.

2006 US Model Treaty Article 23(4) – alternative

resourcing under so-called “Three Bites rule” for an US

expatriate subject to tax as a Treaty country resident on

US source income.

Note: Form 8833 compliance obligations generally apply to reliance on

resourcing provisions of a tax treaty. 63

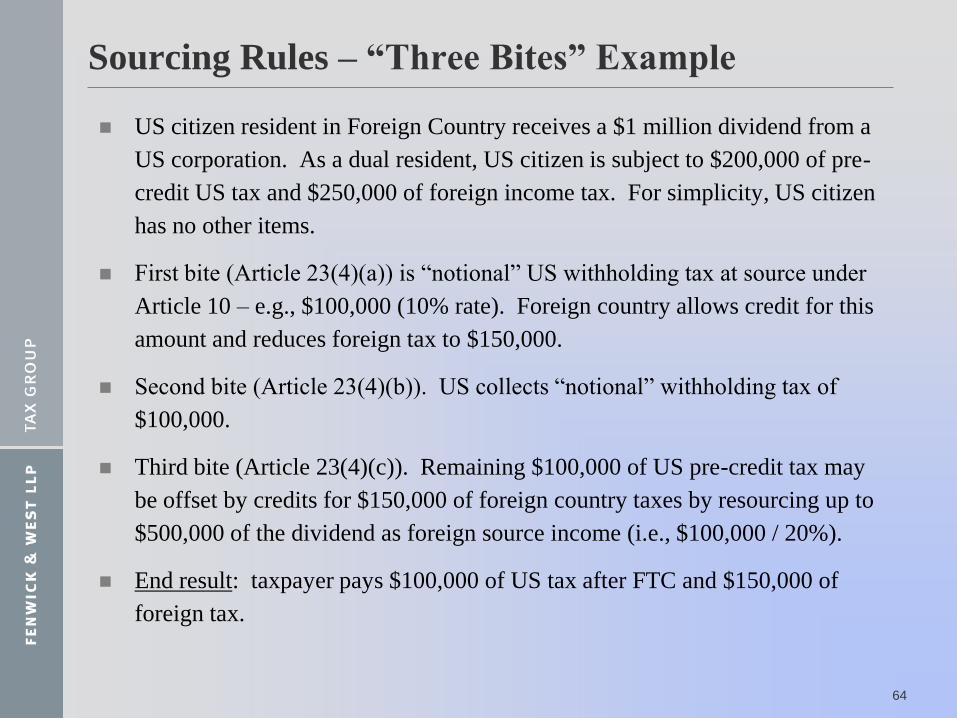

Sourcing Rules – “Three Bites” Example

US citizen resident in Foreign Country receives a $1 million dividend from a

US corporation. As a dual resident, US citizen is subject to $200,000 of pre-

credit US tax and $250,000 of foreign income tax. For simplicity, US citizen

has no other items.

First bite (Article 23(4)(a)) is “notional” US withholding tax at source under

Article 10 – e.g., $100,000 (10% rate). Foreign country allows credit for this

amount and reduces foreign tax to $150,000.

Second bite (Article 23(4)(b)). US collects “notional” withholding tax of

$100,000.

Third bite (Article 23(4)(c)). Remaining $100,000 of US pre-credit tax may

be offset by credits for $150,000 of foreign country taxes by resourcing up to

$500,000 of the dividend as foreign source income (i.e., $100,000 / 20%).

End result: taxpayer pays $100,000 of US tax after FTC and $150,000 of

foreign tax.

64

Sourcing Rules – Characterization Questions

Source of income depends on how income is characterized

for U.S. federal income tax purposes. In some areas,

substance of transaction may be different from its form:

Service fee vs. royalty income

Sale of entire asset vs. license or lease of limited rights

Sale of products with embedded IP vs. license of IP rights

and separate sale of products

Joint venture / profit sharing payment vs. service fee,

product sales or other guaranteed payment.

65

Timing Issues – Section 905

Foreign taxes generally are taken into account when paid

or accrued under the taxpayer’s normal method of

accounting. However, regardless of the taxpayer’s normal

method of accounting, a taxpayer may elect to take into

account foreign income taxes when accrued. See §905(a).

The election is binding for all future years.

Under the accrual method, foreign income taxes are taken

into account in the US year with which or in which the

foreign taxable year ends. See AM 2008-005, Situation

No. 2 (discussing Rev. Rul. 61-93)).

66

Timing Issues – Section 905

When foreign taxes claimed as a credit are re-determined,

the taxpayer must adjust the foreign tax credit

accordingly. See § 905(c).

For example, refunds of foreign taxes that were paid and

claimed as a credit require reversal of the previously

claimed FTC. See, e.g., Sotiropoulos v. Commissioner,

142 TC 269 (2014).

Whether an individual uses the cash or accrual method

may affect whether additional assessment taxes relate

back to prior years or are “bunched” in the current year.

See CCA 201534013 (and authorities discussed therein).

67

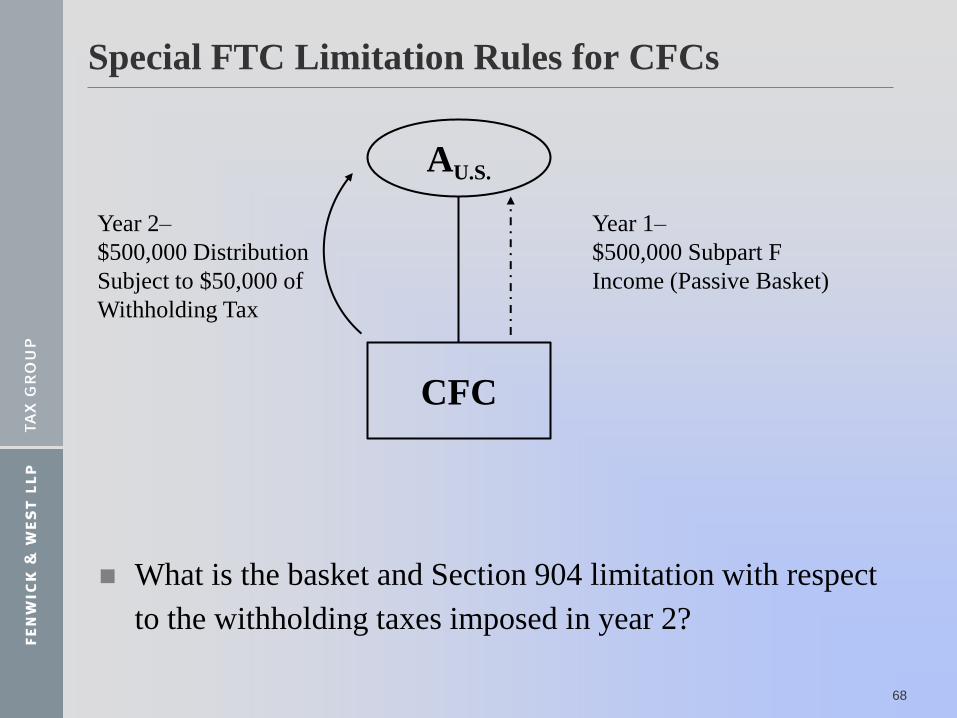

Special FTC Limitation Rules for CFCs

What is the basket and Section 904 limitation with respect

to the withholding taxes imposed in year 2?

68

AU.S.

CFC

Year 2–

$500,000 Distribution

Subject to $50,000 of

Withholding Tax

Year 1–

$500,000 Subpart F

Income (Passive Basket)

Special FTC Limitation Rules for CFCs

Section 960(b)(1) provides for an increase in the Section

904 limitation on taxes imposed on a distribution of a

CFC’s previously taxed income (“PTI”), where the

shareholder elected to credit foreign income taxes for both

the year of the inclusion and the year of the distribution.

The shareholder creates and draws down “excess

limitation accounts” with respect to the prior year subpart

F inclusions to allow use of credits on the distribution of

PTI. See § 960(b)(2).

69

Special FTC Limitation Rules for CFCs - Example

In facts of previous slide, in year 1, if shareholder elects to

credit foreign income taxes, it would create an excess

limitation account equal to the excess Section 904

limitation created by the Subpart F inclusion (e.g.,

$150,000, if average rate were 35% and no Section 962

credits were claimed).

In year 2, distribution of PTI would utilize $50,000 of

excess limitation to absorb withholding taxes.

Remaining excess limitation in the passive basket of

$100,000 would carry forward to future years.

With respect to the Section 904(d) basket of the taxes

imposed on the distribution, see Reg. 1.904-4(c)(6)(iii). 70

Any Questions?

William R. Skinner

Partner, Tax Group

Phone: 650.335.7669

E-mail: [email protected]

71