Foreign Account Tax Compliance Act FATCA -...

52

Foreign Account Tax Compliance Act FATCA Paul DePasquale – Baker & McKenzie, Zurich [email protected] Greg Lamont – PwC, Bangkok [email protected]

Transcript of Foreign Account Tax Compliance Act FATCA -...

Foreign Account Tax Compliance Act

FATCA

Paul DePasquale – Baker & McKenzie, Zurich

Greg Lamont – PwC, Bangkok

2

AGENDA

I. FATCA Overview

II. What We Know – Guidelines Issued So Far

III. What are the Consequences of Not Complying

with FATCA

IV. How to Avoid the FATCA Withholding

V. Other Points

VI. Exemptions from FATCA

VII. Time Line & Effective Dates

VIII. Current Withholding & Tax Treaties

IX. Key Points

X. What FFIs Should Do Now

I. FATCA OVERVIEW

3

FATCA OVERVIEW - BACKGROUND

• U.S. taxes it citizens and residents on

worldwide income

• Perceived inadequacy of current regimes

• UBS affair

• Swiss (and other countries) bank secrecy

laws

• U.S. Congress reacts with FATCA

4

WHAT FATCA IS ATTEMPTING TO DO

• Enlist Foreign Financial Institutions (FFIs)

in the U.S. efforts to catch U.S. citizens and

residents evading U.S. tax

• By getting FFI’s to report to the U.S. IRS

information about U.S. account holders

• U.S. cannot force FFIs to report to IRS

• So FATCA creates a “voluntary” reporting

scheme for FFIs

• If a FFI fails to “volunteer”, the FFI will

suffer a U.S. tax

5

FATCA OVERVIEW

• U.S. tax law that applies to non-U.S. “Foreign

Financial Institutions” (FFIs)

• Subjects FFIs to U.S. tax information reporting

requirements

• If FFI does not comply, it will suffer an additional

30% U.S. withholding tax on its U.S. income (and

possibly some non-U.S. income)

• The information reporting requirements are

burdensome and will require systems, process

and control modifications

• Effective Jan 1, 2013 – but delay announced on

July 14 6

FFI – WHAT IS IT?

Any non-U.S.:

• Bank

• Securities Broker/ Dealer

• Asset manager

• Funds – Mutual, Hedge, VC, Private Equity

• Some insurance companies

• Other?

7

COMMNLY USED TERMS

• FFI – “Foreign Financial Institution” – is any non- U.S. bank, broker, mutual fund or other financial institution

• PFFI – “Participating Foreign Financial Institution” – is any FFI which has entered into written agreement with the IRS to report and withhold under FATCA. A PFFI will not suffer FATCA withholding on its U.S. source withholdable payments

• NPFFI – “Non Participating Foreign Financial Institution” – is any FFI which has not entered into an FFI agreement with the IRS. NPFFI’s will be subject to 30% withholding on their U.S. (and possibly some non U.S.) withholdable payments

8

II. WHAT WE KNOW – GUIDELINES ISSUED

SO FAR

9

GUIDANCE ISSUED

• Under FATCA, Congress has granted wide authority to the

Treasury Department to issue regulations to implement and

enforce FATCA

• Treasury Dept issued a 62 page “Notice and Request for

Comments Regarding Implementation” in August 2010.

(Notice 2010-60)

• Issued Notice 2011-34 (46 pages) in April 2011 with additional

guidance

• Notice 2011-53 on July 14,2011 announcing delayed and

phased-in implementation timeline

• Comprehensive proposed regulations expected by end of 2011

• There is a lot we do not know and many unanswered

questions

• But with the 3 Notices there is enough information for FFIs to

begin evaluating their response to FATCA

10

III. WHAT ARE THE CONSEQUENCES OF NO T

COMPLYING WITH FATCA?

11

WHAT IS THE U.S. WITHHOLDING TAX

IMPOSED ON? • If a FFI fails to comply, there is 30% withholding

on the FFI’s :

• Interest income from U.S. sources

• Dividend income from U.S. sources

• Gross proceeds (not the gain, if any) from the

disposition of U.S. assets producing interest or

dividends

• Certain other U.S. source income – (Derivatives,

Hedges, Swaps, etc.?)

• Certain non-U.S. source income may also be

subject to withholding under “Passthru

Payment” rules

12

IMPACT ON FFI IF NOT FATCA COMPLIANT:

DIRECT US IMVESTMENT

13

Interest Income

of US$ 10M

US Withholding

Tax of US$ 3M

Loss Realized on

the Sale ; Gross

Proceeds from the

Sale of US$ 200M

US Withholding

Tax of US$ 60M

FFI

US

Treasuries*

• FFI makes an investment in U.S. Treasuries that generates U.S. source

interest income and eventually realizes loss on the sale of such U.S.

Treasuries.

• If FFI does not enter into an FFI agreement with the IRS, 30% tax would

be withheld on payments of interest income and sale or redemption

proceeds.

* Not limited to U.S. Treasury securities, same result if U.S. company

bonds or stock

WITTHOLDING ON PASSTHRU PAYMENTS

• In addition to 30% withholding on direct

payments of interest, dividends, and gross

proceeds there can be withholding on

indirect payments – “Passthru Payments”

• Each PFFI must compute and publish its

Passthru Payment Percentage (“PPP”)

• PPP is total U.S. assets / total worldwide

assets

• A PFFI must withhold 30% tax on Passthru

Payments it makes to NPFFIs based on its

PPP

14

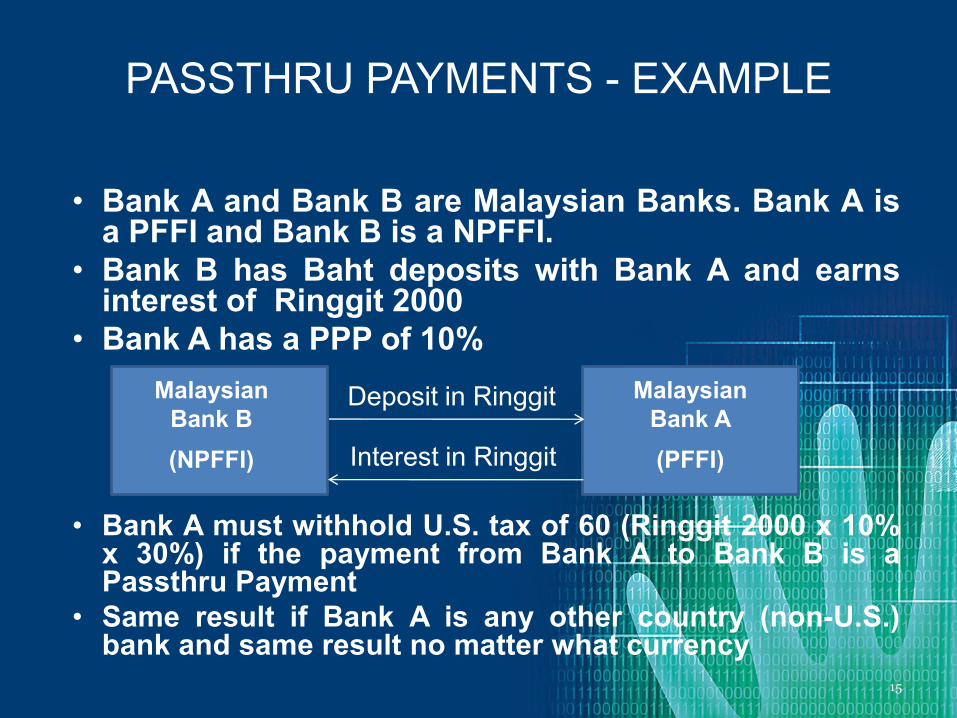

PASSTHRU PAYMENTS - EXAMPLE

• Bank A and Bank B are Malaysian Banks. Bank A is a PFFI and Bank B is a NPFFI.

• Bank B has Baht deposits with Bank A and earns interest of Ringgit 2000

• Bank A has a PPP of 10%

• Bank A must withhold U.S. tax of 60 (Ringgit 2000 x 10% x 30%) if the payment from Bank A to Bank B is a Passthru Payment

• Same result if Bank A is any other country (non-U.S.) bank and same result no matter what currency

15

Malaysian

Bank B

(NPFFI)

Malaysian

Bank A

(PFFI)

Deposit in Ringgit

Interest in Ringgit

PASSTHRU PAYMENTS – QUERY?

16

• Can Bank A legally withhold U.S. tax on the

interest payment to Bank B?

• Will Bank A have to “gross up” the payment

to cover the withholding thus essentially

suffering the withholding cost itself?

• Will PFFIs lose business to NPFFIs as a

result of the Passthru Payment rules?

IV. HOW TO AVOID FATCA WITHHOLDING

17

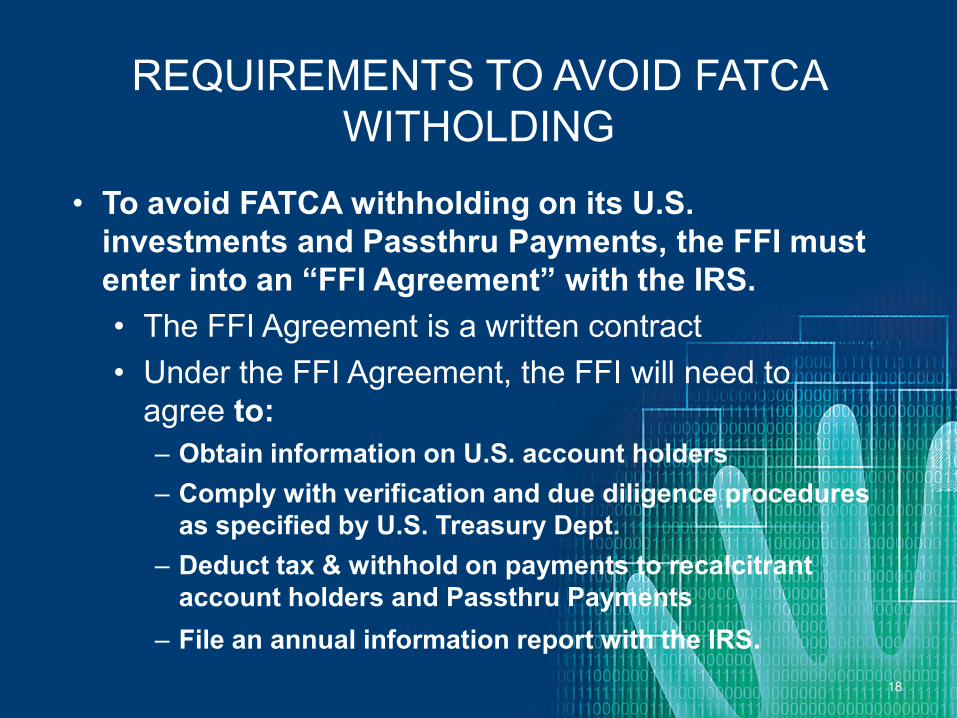

REQUIREMENTS TO AVOID FATCA

WITHOLDING

• To avoid FATCA withholding on its U.S.

investments and Passthru Payments, the FFI must

enter into an “FFI Agreement” with the IRS.

• The FFI Agreement is a written contract

• Under the FFI Agreement, the FFI will need to

agree to:

‒ Obtain information on U.S. account holders

‒ Comply with verification and due diligence procedures

as specified by U.S. Treasury Dept.

‒ Deduct tax & withhold on payments to recalcitrant

account holders and Passthru Payments

‒ File an annual information report with the IRS.

18

PFFI IS A WITHHOLDING AGENT UNDER A FFI

AGREEMENT

• If the FFI chooses to comply and become a

PFFI it will be required to withhold U.S. tax

on:

‒ Direct U.S. source payments to NPFFIs

‒ Passthru Payments to NPFFIs

‒ Payments to “recalcitrant” account holders

• “recalcitrant” account holders are those who

refuse to provide information to the PFFI

such as U.S. TIN or other required

information

19

ANNUAL INFORMATION REPORT

• Must contain :

1. The name, address, and U.S. Tax Identification Number

(“TIN”) of each account holder that is a specified U.S.

person;

2. The name, address, and TIN of each substantial U.S.

owner of any account holder that is a U.S. owned

foreign entity;

3. The account number;

4. The year end account balance or value; and

5. Gross interest, dividends, other income and gross

proceeds paid or credited to the account

• Must be filed electronically in a format specified by

U.S. Treasury

20

“SPECIFIED U.S. PERSON” and “U.S. OWENED

FOREIGN ENTITY”

• If the FFI enters into an FFI Agreement it must track

and report on accounts of “Specified U.S. Persons”

and “U.S. Owned Foreign Entities”

‒ A “Specified U.S. Person” includes:

• Individuals

• Corporations, companies, partnerships, trusts and other

entities

‒ A “U.S. Owned Foreign Entity” is any Malaysian (or

other country) company, corporation, etc. with a

“Substantial U.S. Owner”

‒ Substantial U.S. Owner is any Specified U.S. Person

owning directly or indirectly more than 10%

21

IDENTIFICATION OF U.S. ACCOUNT HOLDERS

• Key requirement is that the PFFI must have policies

and procedures in place to identify U.S. account

holders

• Accounts are segregated into 4 categories:

1. Pre-existing Individual Accounts

2. New Individual Accounts

3. Pre-existing Entity (company) Accounts

4. New Entity (company) Accounts

• The procedures that a PFFI must follow for each of

the 4 categories will vary.

• Detailed preliminary guidance has been issued only

for category 1

22

PRE–EXISTING* INDIVIDUAL ACCOUNTS

• A 6 step process must be followed to identify pre-existing individual

accounts

‒ What is required is a search of the FFI’s electronically searchable

information for indications of U.S. ownership

‒ Indications of U.S. ownership to search for:

• Any identification as U.S. citizen or resident

• U.S. place of birth

• Standing instructions to transfer funds to the U.S.

• U.S. address

• An “ in care of” or “ hold mail” address

• Power of attorney or signature authority for person with U.S.

address

‒ Special and additional procedures for:

• High value accounts ($500,000 or more)

• Private Banking Accounts

* Pre-existing means an account opened prior to January 1,2013

23

NON–INDIVIDUAL (COMPANY) ACCOUNTS

• The PFFI must have a process and

procedure to identify company accounts

with substantial (more than 10%) U.S.

Owners

• Guidance not yet issued on how to do this

24

V. OTHER POINTS

25

LOCAL PRIVACY OR BANK SECRECY LAWS

• What if local country privacy laws (or other

such laws) prohibit a FFI from disclosing

information to a third party such as the U.S.

IRS?

• The FFI must seek a waiver from the account

holder

• If the account holder refuses to provide the

waiver the FFI must treat the account as a

recalcitrant account

26

AFFILIATED GROUP RULES

• For a FFI Agreement to be effective all

members of an affiliated group must enter

into a FFI Agreement

• Cannot “Cherry Pick” and house all U.S.

investments in one compliant entity

• Affiliated group is more than 50% common

direct or indirect ownership

27

ANNUAL CERTIFICATION BY CHIEF

COMPLIANCE OFFICER

• The Chief Compliance Officer (or equivalent title)

of every PFFI must annually personally certify

(under penalty of perjury) that the FFI has adhered

to all aspects of the FFI agreement

28

VI. EXEMPTIONS FROM FATCA

29

EXEMPT FROM FATCA REPORTING &

WITHHOLDING

• Any foreign government, political

subdivisions and wholly owned foreign

government agencies

• Any “Foreign Central Bank of Issue” – e.g.

Bank Negara

• U.S. branches of a FFI

30

EXEMPTION FOR U.S. ACCOUNT HOLDERS -

$50,000

• A FFI need not report on U.S. account

holders if the account is $50,000 or less

• $50,000 threshold is based on average

monthly balances

• Must aggregate all of holder’s accounts

31

DEEMED COMPLIANT– CERTAIN LOCAL

BANKS

Local banks will be deemed compliant if all of the following

conditions are met by the bank and every FFI in its affiliated

group:

1. Each FFI is licensed as a bank in its country of

organization and does not engage primarily in trading

securities, commodities or financial products;

2. Each FFI is organized in the same country;

3. Each FFI does not maintain operations outside its

country of organization

4. Each FFI does not solicit account holders outside its

country of organization; and

5. Each FFI implements policies and procedures to ensure

it does not open or maintain accounts that could contain

U.S. holders 32

• If all tests are met then the deemed

compliant local bank is exempt from

withholding and reporting

• But must still register with IRS to obtain

deemed compliant status

33

DEEMED COMPLIANT– CERTAIN LOCAL

BANKS

VII. TIME LINE & EFFECYIVES DATES

34

TIME LINE & EFFECTIVE DATES

• Original effective date for all aspects of

FATCA was January 1, 2013

• Notice 2011-53 issued July 14, 2011 provides

a delay and a new timeline

35

KEY EFFECTIVE DATES IN NOTICE 2011-53

• January 1, 2014 – Withholding on interest,

dividends and other income paid to NPFFIs

• January 1, 2015 – Withholding on gross

proceeds & Passthru Payments

• June 30, 2013 – FFI Agreement must be

filed to avoid withholding on January 1,

2014

• Due diligence on new & certain existing

accounts must still begin in 2013

• Additional time for private banking and

high value accounts

36

FATCA TIMELINE – FOR FFIs As OF AUGUST

2011

VIII. CURRENT WITHHOLDING & TAX

TREATIES

38

CURRENT WITHHOLDING UNDER EXISTING

U.S. LAW

• U.S. payers must withhold 30% U.S. tax on

“Passive Income” (interest, dividends,

royalties, rents)

• 30% withholding may be reduced under a tax

treaty

• There is no current withholding on “Gross

Proceeds” or capital gains

• Interest – most interest is exempt today from

withholding under rule known as “Portfolio

Interest Exemption”

39

U.S. INCOME TAX TREATY MONETARY

NETWORK IN S.E. ASIA

• FFIs in the following countries will suffer

the full FATCA 30% withholding which will

be a final tax:

Malaysia, Singapore, Hong Kong, Vietnam,

Laos, Cambodia

40

U.S TREATIES WITH OTHER S.E. COUNTRIES

• NPFFI’s will initially suffer the full 30% FATCA withholding

• NPFFIs in India, Indonesia, Philippines and Thailand will be

able to seek partial refunds

• For example, Thai FFIs can seek refunds of 30% withholding

down to treaty rate:

‒ Interest 10%

‒ Dividends 10%

‒ Proceeds 0%

• But must file U.S. tax return and refund process could be as

long as 24 months and must maintain detailed records to claim

refunds

• The “Portfolio Interest Exemption” is effectively repealed, the

U.S. so the treaty withholding rate will be a new cost

41

IX. KEY POINTS

42

FATCA IS AN OPERATIONAL/COMPLIANCE

ISSUE – NOT JUST A TAX ISSUE

• FFIs that treat FATCA as a “Tax Issue” are making a mistake

• FATCA is an operational and compliance issue caused by U.S.

tax law

• FATCA will impact multiple business and operational areas

- Customer on boarding - Internal treasury & cash management

- KYC & AML processes - Legal

- Products & services offered - Compliance

- Systems & controls - Operations

- IT - Private Banking departments

- Insurance affiliates - Trust company affiliates

43

FATCA IS NOT AIMED AT RAISING U.S. TAX

REVENUE THROUGH WITHHOLDING TAX

• The U.S. Treasury has stated they hope

there would be no withholding tax

collected from FFIs

• The goal of FATCA is to identify

unreported income by U.S. persons

• The U.S. simply wants FFIs to sign up and

report their U.S. account holders

44

KEY POINTS

• Not having any U.S. account holders does

NOT exempt the FFI from FACTA

• It is the FFI itself who suffers the withholding

• Only those FFIs with no U.S. source income

that can possibly dismiss FATCA (but be

careful of affiliated group and Passthru

Payment rules)

45

X. WHAT FFIs SHOULD DO NOW

46

FFIs MUST DECIDE WHETHER TO COMPLY

• The U.S. cannot force compliance, but will

withhold 30% on the FFI’s U.S. income if it

chooses not to comply

• Even FFIs with no U.S. account holders must

enter into an “FFI Agreement”

• Decision factors:

‒ Compliance costs

‒ Amount of U.S. source income potentially

subject to withholding

‒ Passthru Payments?

47

IF FFI CHOOSES TO COMPLY

• Will need to make systems and controls

modifications to capture necessary

information and to have the ability to verify

• The systems and controls need to be in

place and operating before the various

effective dates

• The original Jan. 1, 2013 effective date and

announced additional delay was chosen

knowing there would be a long lead time for

FFIs to implement

48

SYSTEMS & PROCESSES NEEDED TO

COMPLY

• A Partial list

1. Systems to search electronic records for existing

U.S. accounts

2. Process for new accounts to identify U.S. persons

and collect needed information (including

substantial U.S. owners of entities with accounts)

3. System to track and identify counter party FFIs as

participating or non-participating

4. System to withhold U.S. tax on Passthru Payments

5. System to capture information needed for annual

electronic report to U.S. Treasury

49

SUGGESTED ACTIONS

1. Determine all touch points with U.S. that

generate U.S. source income and proceeds

across all business lines

2. Evaluate what information currently exists

to possibly identify existing U.S. account

holders

3. Consider implementing new identification

procedures for new account holders

4. Prepare preliminary estimate of costs of

compliance versus withholding costs

50

QUESTIONS?

CIRCULAR 230 DISCLOSURE

Pursuant to requirements relating to practice

before the Internal Revenue Service, any tax

advice in this communication (including any

attachments) is not intended to be used, and

cannot be used, for the purpose of (i)

avoiding penalties imposed under the United

States Internal Revenue Code, or (ii)

promoting, marketing, or recommending to

another person any tax-related matter.