For the six months ended 30 June 2017 Analysis of ...

41

For the six months ended 30 June 2017 Analysis of financial results Your progress is woven into the fabric of Nigeria

Transcript of For the six months ended 30 June 2017 Analysis of ...

For the six months ended 30 June 2017

Analysis of financial resultsYour progress is woven into the fabric of Nigeria

424446484951

5355576264

727273

7576

2729303539

Analysis of financial results for the six months ended 30 June 2017

Overview of group income

Net interest income and margin analysis

Non-interest revenue

Credit impairment charges

Operating expenses

Taxation

Overview of group consolidated assets

Loans and advances

Loans and advances performance

Deposits and current accounts

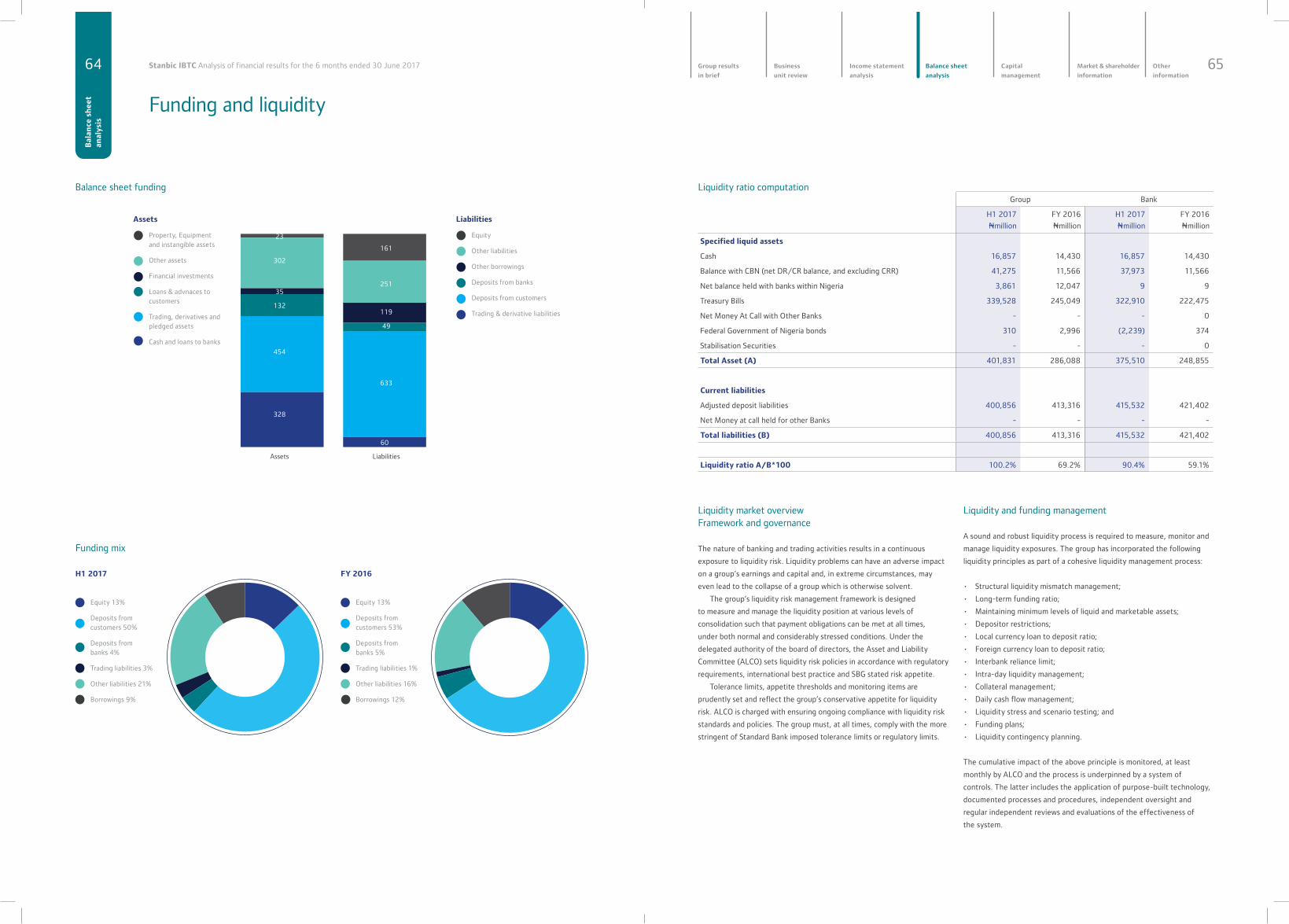

Funding and liquidity

Market capitalisation and price-to-book ratioDividend payment historyEquity and range analysis

Financial and other definitions

Contact details

Segmental structure for key business units

Segmental income statement

Personal & Business Banking

Corporate & Investment Banking

Wealth

6970

Return on ordinary equity

Risk weighted assets

Group results in brief 2

Business unit review

41Income statement analysis

Balance sheet analysis

67Capital management

Market & shareholder information

74Other information

26

52

71

347811121314151617181920222425

Performance highlights

Financial results, ratios and statistics

Economic and capital market statistics

Half year performance

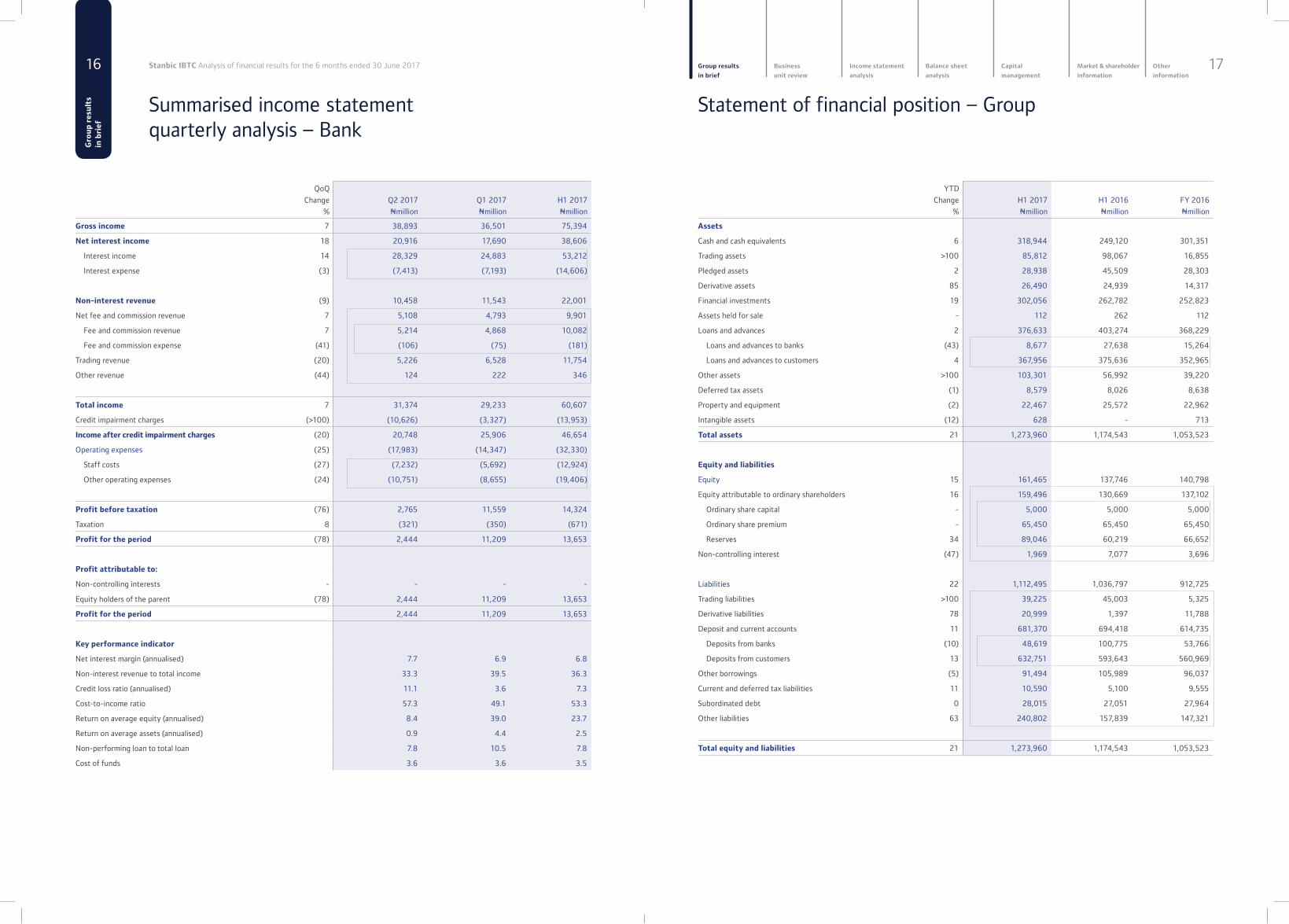

Summarised income statement – Group

Statement of comprehensive income – Group

Summarized income statement quarterly analysis – Group

Summarised income statement – Bank

Statement of comprehensive income – Bank

Summarized income statement quarterly analysis – Bank

Statement of financial position – Group

Group financial position quarterly analysis

Statement of financial position – Bank

Statement of changes in equity – Group

Statement of changes in equity – Bank

Statement of cashflows – Group

Statement of cashflows – Bank

Performance higlights

Gross earnings

N97.2 billion36% up

Profit after tax

N24.1 billion113% up

Cost-to-income ratio

47.0% (H1 2016: 57.7%)

Fitch rating

AAA(nga) (2016: AAA(nga))

Liquidity ratio (Bank)

90.4% (statutory minimum: 30%)

Total income

N81.3 billion43% up

Net loans & advances

N368 billion(FY 2016: N353 billion) up 4%

Capital adequacy ratio (Bank)

20.2% (H1 2016: 18.9%)

Annualized Return on average equity

31.3% (H1 2016: 15.0%)

NPL/total loan ratio

7.8% (FY 2016: 5.0%)

Profit before tax

N29.2 billion86% up

Deposit liabilities

N632.8 billion(FY 2016: N561 billion) up 13%

Credit loss ratio

7.3% (H1 2016: 4.3%)

Price to book

2.1 times (2016: 1.1 times)

Total assets

N1.274 trillion (FY 2016: N1,053 trillion) up 21%

Interest based revene

Non-interest based revene

Gross loans and advances

Deposits from customers

Interest based and non-interest based revenueCAGR (2013-2017): Interest based: 17%

Non-interest based: 14%

Gross loans and customer depositsCAGR (2013-2017): Gross loans: (2)%

Customer deposits: 1%10

0H1 2013 H1 2014 H1 2015 H1 2016 H1 2017

10,000

20,000

30,000

40,000

50,000

60,000

Nmillion

40,470

24,127

56,728

32,316

36,713

26,577

41,718

30,382 27,718

33,997

10

0H1 2015 FY 2015 H1 2016 FY 2016 H1 2017

10

200

300

400

500

700

600

Nbillion

632.8601.7

393.7

561.0

375.3

593.6

407.1431.5

493.5

379.4

2 3Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Title (continued)

Group results

in brief

347811121314151617181920222425

Performance highlightsFinancial results, ratios and statisticsEconomic and capital market statisticsHalf year performanceSummarised income statement – Group Statement of comprehensive income – GroupSummarized income statement quarterly analysis – Group Summarised income statement – Bank Statement of comprehensive income – BankSummarized income statement quarterly analysis – Bank Statement of financial position – GroupGroup financial position quarterly analysisStatement of financial position – BankStatement of changes in equity – GroupStatement of changes in equity – Bank Statement of cashflows – GroupStatement of cashflows – Bank

Group results in brief

Stanbic IBTC Group Change % H1 2017 H1 2016 FY 2016

Business unit contribution to profit before tax

Profit before tax Nmillion 86 29,169 15,682 37,209

Banking business >100 14,324 5,500 14,907

Personal & Business Banking Nmillion (>100) (5,179) 1,371 (1,684)

Corporate & Transactional Banking Nmillion >100 19,503 4,129 16,591

Investment Banking and other subsidiaries Nmillion >100 1,664 (233) 128

Wealth Nmillion 27 13,181 10,415 22,174

Balance sheet

Total assets Nmillion 21 1,273,960 1,174,543 1,053,523

Loans and advances (net of credit impairments) Nmillion 4 367,956 375,636 352,965

Deposits liabilities Nmillion 13 632,751 593,643 560,969

Key performance indicators

Net interest margin % 7.2 4.4 5.9

Non-interest revenue to total income % 49.5 60.0 54.1

Cost-to-income ratio % 47.0 57.7 54.8

Return on average equity % 31.3 15.0 18.9

Return on average assets % 4.3 2.2 2.5

Basic earnings per share kobo >100 230 95 246

Net asset value per share kobo 22 1,595 1,307 1,371

Shareholders' equity Nmillion 159,496 130,669 137,102

Other indicators

Price-to-book (P/B ratio) times 89 2.1 1.2 1.1

Effective tax rate % 17.3 27.8 23.4

Banking activities Change % H1 2017 H1 2016 FY 2016

Balance sheet

Total assets Nmillion 24 1,229,804 1,127,875 993,757

Loans and advances (net of credit impairments) Nmillion 4 367,956 375,636 352,965

Deposits from customers Nmillion 14 647,108 601,198 568,673

Selected returns and ratios

Return on average equity % 23.7 10.8 14.7

Return on average assets % 2.5 1.0 1.6

Loan to deposit ratio % 62.2 68.6 61.7

Net interest margin % 6.8 4.3 5.7

Non-performing loan to total loan % 7.8 6.9 5.0

Non-interest revenue to total income % 36.3 48.8 41.4

Credit impairment charges Nmillion >100 13,953 8,450 19,803

Credit loss ratio % 7.3 4.3 5.2

Cost-to-income ratio % 53.3 66.3 61.9

Tier 1 capital adequacy % 16.1 14.2 16.3

Total capital adequacy % 20.2 18.9 21.0

Effective taxation rate % 4.7 6.3 (0.8)

4 5Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Financial results, ratios and statistics

Stanbic share price NSE all share index Banking index

Economic and capital market statistics

Change % H1 2017 H1 2016 FY 2016

Economic indicators

Headline inflation % 16.1 16.5 15.7

GDP growth % (0.5) (2.1) (1.3)

External reserves $billion 15 30.3 26.4 25.8

Average official exchange rate N/$ 44 305.0 212.5 264.2

Market Indicators

NSE All Share Index 12 33,117.5 29,597.8 26,874.6

NSE turnover Nbillion 29 375 291.7 549.7

Average daily activity million 6 348.3 329.5 291.2

Aggregate market capitalisation Ntrillion 10 19 17.3 16.2

Equity market capitalisation Ntrillion 13 11.5 10.2 9.2

Stanbic share statistics

Share price

High for the period kobo 86 3,300 1,776 1,776

Low for the period kobo 23 1,500 1,223 1,223

Closing kobo >100 3,300 1,620 1,500

Shares traded

Number of shares thousands 61 300,355 185,988 348,093

Value of shares Nmillion >100 6,480 2,769 5,203

Market capitalisation Nbillon >100 330 162 150

6 7Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Financial results, ratios and statistics (continued)

In H1 2017, the group experienced:

Globally

• The global economy continued to be characterised by substantial

appetite for risk assets as a result of ample global flows, despite

an increase in political risk globally;

• Global markets remained on edge with respect to substantial increase

in political risk events which included scheduled elections in the

Netherland and France as well as an unscheduled election in the

United Kingdom, coupled with still uncertain policy outlook from

the United States;

• After initially rallying towards USD55 per barrel, oil prices declined

substantially towards the end of H1:2017 as fundamentals remain

unfavorable with global production potentially rising due to

rising output from Nigeria and Libya. The freezes engineered by

OPEC did little to stem the decline in oil prices;

• Going by growth data in H1:2017, an uptick in Africa’s economic

growth seems well underway. This will likely prompt forecasters

like the IMF to upgrade their growth forecasts for 2017 and 2018.

The laggards are likely to be those commodity exporters that are

not allowing their economies to adjust to a low commodity price

environment;

Nigeria

• Anecdotal evidence in H1:2017 suggests that some macroeconomic

rebalancing is underway in the Nigerian economy and should continue

over the next year. A combination of contracting credit demand and

stunted investment spending will allow economic growth recover

slowly in the near term.

• The introduction of the Investors’ and Exporters’ Foreign Exchange

(IEFX) window has signaled yet another step taken by the Central

Bank of Nigeria (CBN) to improve the functioning of the FX market.

• Although the Central Bank left the formal policy rate unchanged

through the course of the first half of the year, it has engineered

tight NGN liquidity conditions which resulted in private sector

credit contracting by an average of 2.0% y/y between January

and April, after taking account of the revaluation of FX loans due

to the depreciation of the NGN.

• The depressed oil price and production meant that government

revenue remained under pressure. As a result, government had to

ramp up its borrowing both domestically and externally with the

issuance of USD1.5billion Eurobond and a USD300million Diaspora

bond.

• The capital market performance returned into positive territory

in H1 2017 as a result of improved economic conditions.

Share price performance: H1 2017 (rebased)

Stanbic’s share price outperformed both the Banking Index (BI) and The NSE ASI. Stanbic’s share price closed at N33.00 representing a 120% increase

from N15.00 at the end of 2016 while the BI and NSE ASI appreciated by 45.1% and 23.2% respectively.

0

0.5

1.0

1.5

2.0

2.5

3-J

an-1

7

16

-Jan

-17

29

-Jan

-17

11

-Feb

-17

24

-Feb

-17

9-M

ar-1

7

22

-Mar

-17

4-A

pr-1

7

17

-Apr

-17

30

-Apr

-17

26

-May

-17

21

-Jun

-17

8-J

un-1

7

%

8 9Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Half year performance

Operating environmentWith the improved economic activities as a

result of increased foreign exchange liquidity

and rising oil price, we expect the nation to

be on its way out of recession by the end of

this year. The Stanbic IBTC Bank Purchasing

Manager Index and declining inflation rate

are signals to Nigeria’s economic recovery.

Real GDP growth is forecasted to reach 1.0%

year-on-year in 2017 and 2.5% year-on-year

in 2018 according to Standard Bank Research

from a 1.5% contraction in 2016. It is expected

that with oil prices and production levels rising,

banks’ dollar liquidity pressures would gradually

ease. As such, the Nigerian economy contracted

by 0.52% in real terms in the first quarter of

2017, the lowest level of contraction recorded

in the last five quarters reflecting the gradual

recovery of the macro-economic environment.

The nation’s external reserves reached

$30.3 billion in June 2017, increasing by 17.4%

from $25.8 billion recorded in December

2016. The increase in crude oil output and

price accounted for the accretion in external

reserves. According to OPEC, Nigerian crude

production rose to 1.68 million b/d in June,

the highest level in more than one year. This

followed the restart of Forcados loadings for

the first time since October 2016.

Headline inflation which had been on the

rise through out 2016 has begun to inch lower

with five consecutive month decreases to June

2017. From 18.6 per cent in December 2016,

headline inflation rose to 18.7 per cent in

January 2017, but subsided to 17.8 per cent in

February, 17.3 per cent in March, 17.2 per cent

in April, 16.3 per cent in May and decelerated

further, reaching 16.1 per cent in June 2017

thus representing the stabilization of general

prices, although food inflation continues to rise.

Food inflation reached the 19 per cent handle

in June, representing a historical high.

The Nigerian Stock Exchange All Share Index

(“The NSE ASI”) closed in positive territory

at 33,117.5 at the end of June 2017, crossing

the 30,000.0 points mark for the first time in

about a year. The positivity witnessed in the

Non-interest revenue

Non-interest revenue, which comprises revenue

from commissions, fees, trading and other

non-interest bearing revenue, was up by 18% to

N40.3 billion (H1 2016: N34.2 billion).

Net fees and commissions revenue

remained flat to N27.9 billion from previous

year, though we continue to face transaction

fee reduction from various stakeholders.

With the introduction of the IEFX market

and improved foreign exchange liquidity, we

expect investment banking deal pipelines will

be converted and growth in the stock market is

expected to impact revenue of our custody and

stockbroking businesses positively.

Trading revenue increased by 81% to N12

billion (H1 2016: N6.6 billion) on the back of

improved foreign exchange liquidity and high

interest rate on government securities.

Credit impairments

Credit impairment charges increased by 65%

to N13.95 billion (H1 2016: N8.5billion) as

we continued our clean-up of the risk asset

portfolio. With Nigeria falling into recession,

economic activites were impacted significantly

and we witnessed business activities decline. In

line with economic realities, the group had to

increase provisioning on its loan portfolio. The

increase in credit impairment charges led to a

higher cost of risk which increased to 7.3% from

5.2% in FY 2016.

Operating expenses

The group maintained cost discipline with cost

to income ratio declining to 47.0% from 57.7%

in H1 2016 as we continue on cost efficiency

drive. Operating expenses increased by 16% to

N38.2 billion (H1 2016: N32.9 billion). Staff

costs grew by 15% on the back of inflation

adjustment to staff salaries and net movement

in headcount of staff.

Other operating expenses increased by 17%

driven by increase in information technology,

AMCON sinking fund contribution expenses,

premises maintenance related expenses and

deposit insurance.

first half of the year may be attributed to major

interventions in the foreign exchange market

by the Central Bank which has boosted investor

confidence. The major intervention being the

introduction of the Investors’ and Exporters’

Foreign Exchange (“IEFX”) window which led to

significant improvement in the capital market

performance thereby impacting Assets Under

Management (“AUM”) positively.

The Federal Government introduced a

number of reforms aimed at revamping the

economy, one of which includes the publishing

of Economic Recovery and Growth Plan

(“ERGP”), a Medium Term Plan for 2017 –

2020 which was developed for the purpose of

restoring economic growth while leveraging

the ingenuity and resilience of the Nigerian

people. Furthermore, the signing of executive

orders aimed at improving the ease of doing

business in the country is a positive sign. That

said, implementation of reforms outlined in the

ERGP is key to ensuring sustainable growth and

development.

The financial sector has experienced

some regulatory changes since December

2016. The most significant has to do with the

foreign exchange market framework which the

introduction of the IEFX window has improved

dollar liquidity as we witnessed increased inflow

of funds from both foreign portfolio and direct

investors. While the monetary policy rate has

remained unchanged at 14.0%, the central bank

continues to implement a tight monetary policy

environment in order to curb inflation, limit

pressure on the exchange rate and engineer

positive real returns that will be attractive to

investors.

Available data from the CBN as at April 2017

suggests that average Capital Adequacy Ratio

(CAR) of Deposit Money Banks deteriorated to

12.8 per cent from 13.6 per cent in February,

which is below the prudential requirement

of 15.0 per cent for banks with international

authorization. Furthermore, Non-Performing

Loans (NPLs) rose to 15.2 per cent from 13.6

per cent in February 2017, which is above the

prudential guide of 5.0 per cent. The industry

Overall, the group’s profit before tax

increased by 86% to N29.2 billion (H1 2016:

N15.7 billion), while profit after tax also

increased by 113% to N24.1 billion (H1 2016:

N11.3 billion), attributable to increased interest

income and trading revenue.

Balance sheet analysisThe group’s total assets close at N1.27 trillion

at the end of June 2017, growing by 21% over

the N1.05 trillion recorded in FY 2016. The

growth in total assets is majorly from the 13%

growth in deposit from customers which funded

50% of total assets. Our eco-system and work

place banking team have been mining the

available opportunities as much as possible.

Loans and advances

Net loans and advances grew by 4% to N368

billion in the first six months of 2017 (FY 2016:

N353 billion), on the back of our growing

customer relationships. We will continue to

grow our loan book responsibly in line with

economic realities.

Non-performing loans increased by 65% to

N30.9 billion in H1 2017 from N18.7 billion in

FY 2016. The increase is largely on the back of

some newly classified loans in oil & gas sector.

The non-performing loans to total loans ratio

consequently deteriorated to 7.8% from 5.0%

recorded in FY 2016.

Funding and liquidity

Customer deposits closed at N632.8 billion

in H1 2017 increasing by 13% from N561

billion recorded in FY 2016. The increase in

deposit from customers is supported by our

growing customer base, enlarged delivery

channels, digitalization, ecosystem and work

place banking strategy. Customer acquisition

initiatives continued to yield positive results

as current and savings account balances grew

by 19% from FY 2016.

The ratio of current and savings deposits

to total deposits increased from 57% to 60%

at the end of H1 2017.

The group maintained a liquidity position

above minimum requirement throughout the

period ended 30 June 2017. The liquidity ratio

closed at 100.2% (Bank: 90.4%) in H1 2017

higher than the regulatory minimum of 30%.

liquidity ratio also recorded a decline from 46.6

per cent to 44.6 per cent.

We cautiously anticipate some improvement

in asset quality in the latter part of the year as

the economy gradually recovers from recession.

The manufacturing and agricultural sectors

are expected to drive lending in the near term

driven by government’s resolve to increase

domestic production and reduce dependence

on imports. In addition, it is expected that

AUM will continue to rise as higher oil revenues

should result in state and local governments

making good on salary payments to government

workers and the capital markets continue to

outperform.

Our resultsOur performance in the first half of 2017 was

characterised by steady growth in balance

sheet with conscious effort of deposit liability

growth via current and savings account thereby

reducing our interest expense in line with our

strong focus on cost containment to mitigate

the impact of rising cost of funds and credit

impairments on our operating performance.

Income statement analysisThe group’s gross revenue grew by 36% to

N97.2 billion (H1 2016: N71.3 billion) on the

back of a 80% increase in net interest income.

Net interest income

Interest income grew by 55% to N56.7 billion

in H1 2017 from N36.7 billion achieved in H1

2016. This growth is supported by increase

in yields from investment securities. Interest

expense was up 13% much lower than the

income growth rate largely due to growth in less

expensive to total deposit ratio. This resulted

in an 80% increase in net interest income and

consequently a growth in net interest margin to

7.2% (FY 2016: 5.9%).

The central bank’s strategies to mop up

liquidity has continued to keep interest rate and

yield up amidst declining inflation. We expect

interest and inflation rate to converge at some

point.

Summarised income statement – Group

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Gross earnings 36 97,198 71,320 156,425

Net interest income 80 41,035 22,849 57,859

Interest income 55 56,728 36,713 87,467

Interest expense (13) (15,693) (13,864) (29,608)

Non-interest revenue 18 40,289 34,218 68,194

Net fees and commission revenue 2 27,893 27,406 52,154

Fees and commission revenue 1 28,074 27,795 52,918

Fees and commission expense 53 (181) (389) (764)

Trading revenue 81 11,966 6,607 15,326

Other revenue >100 430 205 714

Total income 43 81,324 57,067 126,053

Credit impairment charges (65) (13,953) (8,450) (19,803)

Income after credit impairment charges 39 67,371 48,617 106,250

Operating expenses (16) (38,202) (32,935) (69,041)

Staff costs (15) (16,492) (14,378) (30,173)

Other operating expenses (17) (21,710) (18,557) (38,868)

Profit before taxation 86 29,169 15,682 37,209

Direct taxation (16) (5,057) (4,365) (8,689)

Profit for the period >100 24,112 11,317 28,520

Profit attributable to:

Non-controlling interests (42) 1,067 1,853 3,878

Equity holders of the parent >100 23,045 9,464 24,642

Profit for the period >100 24,112 11,317 28,520

Group H1 2017

Nmillion

Bank H1 2017

Nmillion

Group FY 2016

Nmillion

Bank FY 2016

Nmillion

Tier I capital 150,421 112,533 129,480 99,144

Tier II capital 28,827 28,070 28,906 28,099

Total qualifying capital 179,248 140,603 158,386 127,243

Credit risk 561,681 534,642 486,430 458,266

Operational risk 207,092 146,986 207,092 146,986

Market risk 15,425 15,425 1,917 1,917

Risk weighted assets 784,198 697,053 695,439 607,169

Capital adequacy

Tier I 19.2% 16.1% 18.6% 16.3%

Tier II 3.7% 4.0% 4.2% 4.6%

Total 22.9% 20.2% 22.8% 21.0%

Capital adequacyThe group’s capital base remained adequate with ratios above the regulatory requirement.

The group currently has no immediate plan to raise additional capital.

10 11Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Half year performance (continued)

Summarised group income statement quarterly analysisStatement of other comprehensive income – Group

QoQ

Change

%

Q2 2017

Nmillion

Q1 2017

Nmillion

H1 2017

Nmillion

Gross income 7 50,176 47,022 97,198

Net interest income 17 22,155 18,880 41,035

Interest income 11 29,887 26,841 56,728

Interest expense 3 (7,732) (7,961) (15,693)

Non-interest revenue 0.38 20,183 20,106 40,289

Net fee and commission revenue 11 14,699 13,194 27,893

Fee and commission revenue 12 14,805 13,269 28,074

Fee and commission expense (41) (106) (75) (181)

Trading revenue (20) 5,315 6,651 11,966

Other revenue (35) 169 261 430

Total income 9 42,338 38,986 81,324

Credit impairment charges (>100) (10,626) (3,327) (13,953)

Income after credit impairment charges (11) 31,712 35,659 67,371

Operating expenses 24 (21,169) (17,033) (38,202)

Staff costs (28) (9,258) (7,234) (16,492)

Other operating expenses (22) (11,911) (9,799) (21,710)

Profit before taxation (43) 10,543 18,626 29,169

Taxation 2 (2,505) (2,552) (5,057)

Profit for the period (50) 8,038 16,074 24,112

Profit attributable to:

Non-controlling interests (5) 520 547 1,067

Equity holders of the parent (52) 7,518 15,527 23,045

Profit for the period 8,038 16,074 24,112

Key performance indicator

Net interest margin (annualised) 7.8 7.0 7.2

Non-interest revenue to total income 47.7 51.6 49.5

Credit loss ratio (annualised) 11.1 3.6 7.3

Cost-to-income ratio 50.0 43.7 47.0

Return on average equity (annualised) 20.3 42.9 31.3

Return on average assets (annualised) 2.8 5.9 4.3

Non-performing loan to total loan 7.8 10.5 7.8

Cost of funds (annualised) 3.8 4.0 3.9

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Profit for the period 24,112 11,317 28,520

Other comprehensive income

Items that will never be reclassified to profit or loss - - -

Items that are or may be reclassified subsequently to profit or loss:

Net change in fair value of available-for-sale financial assets (50) (1,618) (409)

Realised fair value adjustments on available-for-sale financial assets

reclassified to income statement

(86) 96 76

Income tax on other comprehensive income - - -

Other comprehensive income for the period net of tax (136) (1,522) (333)

Total comprehensive income for the period 23,976 9,795 28,187

Total comprehensive income attributable to:

Non-controlling interests 1,061 1,836 3,829

Equity holders of the parent 22,915 7,959 24,358

23,976 9,795 28,187

12 13Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Statement of other comprehensive income – Bank

YoY

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Gross earnings 35 75,394 55,697 121,755

Net interest income 82 38,606 21,178 53,340

Interest income 51 53,212 35,150 83,267

Interest expense (5) (14,606) (13,972) (29,927)

Non-interest revenue 9 22,001 20,158 37,724

Net fees and commission revenue (26) 9,901 13,384 22,557

Fees and commission revenue (27) 10,082 13,773 23,321

Fees and commission expense 53 (181) (389) (764)

Trading revenue 78 11,754 6,610 14,504

Other revenue >100 346 164 663

Total income 47 60,607 41,336 91,064

Credit impairment charges (65) (13,953) (8,450) (19,803)

Income after credit impairment charges 42 46,654 32,886 71,261

Operating expenses (18) (32,330) (27,386) (56,354)

Staff costs (13) (12,924) (11,404) (24,104)

Other operating expenses (28) (19,406) (15,982) (32,250)

Profit before taxation >100 14,324 5,500 14,907

Direct taxation (94) (671) (347) 123

Profit for the period >100 13,653 5,153 15,030

Profit attributable to:

Non-controlling interests - - - -

Equity holders of the parent >100 13,653 5,153 15,030

Profit for the period >100 13,653 5,153 15,030

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Profit for the period 13,653 5,153 15,030

Other comprehensive income

Items that will never be reclassified to profit or loss - - -

Items that are or may be reclassified subsequently to profit or loss:

Net change in fair value of available-for-sale financial assets (167) (1,642) (474)

Realised fair value adjustments on available-for-sale financial assets

reclassified to income statement

87 96 (162)

Income tax on other comprehensive income - - -

Other comprehensive income for the period net of tax (80) (1,546) (636)

Total comprehensive income for the period 13,573 3,607 14,394

Total comprehensive income attributable to:

Non-controlling interests - - -

Equity holders of the parent 13,573 3,607 14,394

13,573 3,607 14,394

14 15Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Summarised income statement – Bank

Summarised income statement quarterly analysis – Bank

YTD

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Assets

Cash and cash equivalents 6 318,944 249,120 301,351

Trading assets >100 85,812 98,067 16,855

Pledged assets 2 28,938 45,509 28,303

Derivative assets 85 26,490 24,939 14,317

Financial investments 19 302,056 262,782 252,823

Assets held for sale - 112 262 112

Loans and advances 2 376,633 403,274 368,229

Loans and advances to banks (43) 8,677 27,638 15,264

Loans and advances to customers 4 367,956 375,636 352,965

Other assets >100 103,301 56,992 39,220

Deferred tax assets (1) 8,579 8,026 8,638

Property and equipment (2) 22,467 25,572 22,962

Intangible assets (12) 628 - 713

Total assets 21 1,273,960 1,174,543 1,053,523

Equity and liabilities

Equity 15 161,465 137,746 140,798

Equity attributable to ordinary shareholders 16 159,496 130,669 137,102

Ordinary share capital - 5,000 5,000 5,000

Ordinary share premium - 65,450 65,450 65,450

Reserves 34 89,046 60,219 66,652

Non-controlling interest (47) 1,969 7,077 3,696

Liabilities 22 1,112,495 1,036,797 912,725

Trading liabilities >100 39,225 45,003 5,325

Derivative liabilities 78 20,999 1,397 11,788

Deposit and current accounts 11 681,370 694,418 614,735

Deposits from banks (10) 48,619 100,775 53,766

Deposits from customers 13 632,751 593,643 560,969

Other borrowings (5) 91,494 105,989 96,037

Current and deferred tax liabilities 11 10,590 5,100 9,555

Subordinated debt 0 28,015 27,051 27,964

Other liabilities 63 240,802 157,839 147,321

Total equity and liabilities 21 1,273,960 1,174,543 1,053,523

QoQ

Change

%

Q2 2017

Nmillion

Q1 2017

Nmillion

H1 2017

Nmillion

Gross income 7 38,893 36,501 75,394

Net interest income 18 20,916 17,690 38,606

Interest income 14 28,329 24,883 53,212

Interest expense (3) (7,413) (7,193) (14,606)

Non-interest revenue (9) 10,458 11,543 22,001

Net fee and commission revenue 7 5,108 4,793 9,901

Fee and commission revenue 7 5,214 4,868 10,082

Fee and commission expense (41) (106) (75) (181)

Trading revenue (20) 5,226 6,528 11,754

Other revenue (44) 124 222 346

Total income 7 31,374 29,233 60,607

Credit impairment charges (>100) (10,626) (3,327) (13,953)

Income after credit impairment charges (20) 20,748 25,906 46,654

Operating expenses (25) (17,983) (14,347) (32,330)

Staff costs (27) (7,232) (5,692) (12,924)

Other operating expenses (24) (10,751) (8,655) (19,406)

Profit before taxation (76) 2,765 11,559 14,324

Taxation 8 (321) (350) (671)

Profit for the period (78) 2,444 11,209 13,653

Profit attributable to:

Non-controlling interests - - - -

Equity holders of the parent (78) 2,444 11,209 13,653

Profit for the period 2,444 11,209 13,653

Key performance indicator

Net interest margin (annualised) 7.7 6.9 6.8

Non-interest revenue to total income 33.3 39.5 36.3

Credit loss ratio (annualised) 11.1 3.6 7.3

Cost-to-income ratio 57.3 49.1 53.3

Return on average equity (annualised) 8.4 39.0 23.7

Return on average assets (annualised) 0.9 4.4 2.5

Non-performing loan to total loan 7.8 10.5 7.8

Cost of funds 3.6 3.6 3.5

16 17Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Statement of financial position – Group

Group financial position quarterly analysis

QOQ

Change %

2Q 2017

Nmillion

1Q 2017

Nmillion

FY 2016

Nmillion

Assets

Cash and cash equivalents 6 318,944 302,272 301,351

Trading assets (12) 85,812 98,039 16,855

Pledged assets (25) 28,938 38,493 28,303

Derivative assets 2 26,490 25,960 14,317

Financial investments 7 302,056 281,130 252,823

Assets held for sale - 112 112 112

Loans and advances 8 376,633 347,443 368,229

Loans and advances to banks 6 8,677 8,184 15,264

Loans and advances to customers 8 367,956 339,259 352,965

Other assets >100 103,301 40,189 39,220

Deferred tax assets 2 8,579 8,449 8,638

Property and equipment (1) 22,467 22,702 22,962

Intangible assets (2) 628 638 713

Total assets 9 1,273,960 1,165,427 1,053,523

Equity and liabilities

Equity 3 161,465 156,048 140,798

Equity attributable to ordinary shareholders 4 159,496 152,986 137,102

Ordinary share capital - 5,000 5,000 5,000

Ordinary share premium - 65,450 65,450 65,450

Reserves 8 89,046 82,536 66,652

Non-controlling interest (36) 1,970 3,062 3,696

Liabilities 10 1,112,495 1,009,379 912,725

Trading liabilities (15) 39,225 46,003 5,325

Derivative liabilities 17 21,000 17,995 11,788

Deposit and current accounts 0 681,370 678,322 614,735

Deposits from banks (43) 48,619 85,035 53,766

Deposits from customers 7 632,751 593,287 560,969

Other borrowings 10 91,494 83,147 96,037

Current and deferred tax liabilities (10) 10,590 11,797 9,555

Subordinated debt 1 28,015 27,651 27,964

Provisions and other liabilities 67 240,802 144,464 147,321

Total equity and liabilities 9 1,273,960 1,165,427 1,053,523

Statement of financial position – Bank

YTD

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Assets

Cash and cash equivalents 9 315,092 233,732 289,312

Trading assets >100 84,569 96,786 15,657

Pledged assets 2 28,938 45,509 28,303

Derivative assets 85 26,490 24,939 14,317

Financial investments 26 275,444 243,331 217,917

Assets held for sale - - 262 -

Loans and advances 2 376,633 403,234 368,229

Loans and advances to banks (43) 8,677 27,598 15,264

Loans and advances to customers 4 367,956 375,636 352,965

Other assets >100 94,574 50,581 31,307

Deferred tax assets 0 8,337 7,332 8,334

Property and equipment (3) 19,099 22,169 19,668

Intangible assets (12) 628 - 713

Total assets 24 1,229,804 1,127,875 993,757

Equity and liabilities

Equity 12 122,874 97,472 109,317

Equity attributable to ordinary shareholders 12 122,874 97,472 109,317

Ordinary share capital - 1,875 1,875 1,875

Ordinary share premium - 42,469 42,469 42,469

Reserves 19 78,530 53,128 64,973

Non-controlling interest - - - -

Liabilities 25 1,106,930 1,030,403 884,440

Trading liabilities >100 39,225 45,003 5,325

Derivative liabilities 78 20,999 1,397 11,788

Deposit and current accounts 12 695,727 701,973 622,439

Deposits from banks (10) 48,619 100,775 53,766

Deposits from customers 14 647,108 601,198 568,673

Other borrowings 15 91,494 105,989 79,633

Current tax liabilities 3 1,928 1,338 1,865

Subordinated debt 0 28,015 27,051 27,964

Provisions and other liabilities 69 229,542 147,652 135,426

Total equity and liabilities 24 1,229,804 1,127,875 993,757

18 19Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Statement of changes in equity – Group

Ordinary

share capital

Nmillion

Share

premium

Nmillion

Merger

reserve

Nmillion

Statutory

credit risk

reserve

Nmillion

Available-for-

sale revaluation

reserve

Nmillion

Share-based

payment reserve

Nmillion

AGSMEIS

reserve

Nmillion

Other

regulatory

reserves

Nmillion

Retained

earnings

Nmillion

Ordinary

shareholders’

equity

Nmillion

Non-controlling

interest

Nmillion

Total

equity

Nmillion

Balance at 1 January 2017 5,000 65,450 (19,123) 1,025 942 36 - 33,615 50,157 137,102 3,696 140,798

Total comprehensive(loss)/income for the period (130) - - 23,045 22,915 1,061 23,976

Profit for the period - - - - - - - 23,045 23,045 1,067 24,112

Other comprehensive (loss)/income after tax for the period (130) - - - - (130) (6) (136)

Net change in fair value on available-for-sale financial assets - - - - (44) - - - (44) (6) (50)

Realised fair value adjustments on available-for-sale financial assets - - - - (86) - - - (86) - (86)

Statutory credit risk reserve - - - - - - - - - - -

Transfer to statutory reserves - - - - - - 749 (749) - - -

Transactions with shareholders, recorded directly in equity - - - - - (21) - - (500) (521) (2,788) (3,309)

Equity-settled share-based payment transactions - - - - - (21) - - - (21) (21)

Dividends paid to equity holders - - - - - - - - (500) (500) (2,788) (3,288)

Balance at 30 June 2017 5,000 65,450 (19,123) 1,025 812 15 749 33,615 71,953 159,496 1,969 161,465

Balance at 1 January 2016 5,000 65,450 (19,123) 6,684 1,226 56 - 26,218 38,215 123,726 5,241 128,967

Total comprehensive income/(loss) for the period - - - - (1,505) - - - 8,407 6,902 1,836 8,738

Profit for the period - - - - - - - - 8,407 8,407 1,853 10,260

Other comprehensive income/(loss) after tax for the period - - - - (1,505) - - - - (1,505) (17) (1,522)

Net change in fair value on available-for-sale financial assets - - - - (1,601) - - - - (1,601) (17) (1,618)

Realised fair value adjustments on available-for-sale financial assets - - - - 96 - - - - 96 - 96

Statutory credit risk reserve - - - - - - - - - - -

Transfer to statutory reserves - - - - - - - - - - -

Transactions with shareholders, recorded directly in equity - - - - 40 - - 40 - 40

Equity-settled share-based payment transactions - - - - 40 - - 40 - 40

Transfer of vested portion of equity settled share based payment to

retained earnings

- - - - - - - - - -

Dividends paid to equity holders - - - - - - - - - -

Balance at 30 June 2016 5,000 65,450 (19,123) 6,684 (279) 96 26,218 46,622 130,668 7,077 137,745

20 21Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Statement of changes in equity – Bank

Group

Ordinary

share capital

Nmillion

Share

premium

Nmillion

Statutory credit

risk reserve

Nmillion

Available-for-

sale revaluation

reserve

Nmillion

Share-based

payment reserve

Nmillion

SMIEIS

reserves

Nmillion

AGSMIEIS

reserves

Nmillion

Statutory

reserves

Nmillion

Retained

earnings

Nmillion

Ordinary

shareholders’

equity

Nmillion

Balance at 1 January 2017 1,875 42,469 789 184 28 1,039 - 22,153 40,780 109,317

Total comprehensive income for the period - - (80) - - - - 13,653 13,573

Profit for the period - - - - - - - - 13,653 13,653

Other comprehensive income after tax for the year - - - (80) - - - - - (80)

Net change in fair value on available-for-sale financial assets - - - (167) - - - - - (167)

Realised fair value adjustments on available-for-sale financial assets - - - 87 - - - - - 87

Income tax on other comprehensive income - - - - - - - - - -

Statutory credit risk reserve - - - - - - - - - -

Transfer to statutory reserves - - - - - - 749 - (749) -

Transactions with shareholders, recorded directly in equity - - - - (16) - - - - (16)

Equity-settled share-based payment transactions - - - - (16) - - - - (16)

Transfer of vested share options to retained earnings - - - - - - - - - -

Dividends paid to equity holders - - - - - - - - - -

Balance at 30 June 2017 1,875 42,469 789 104 12 1,039 749 22,153 53,684 122,874

Balance at 1 January 2016 1,875 42,469 6,684 820 32 1,039 - 19,907 22,091 94,917

Total comprehensive income for the period - - (1,546) - - 5,153 3,607

Profit for the period - - - - - - - - 5,153 5,153

Other comprehensive income after tax for the period - - (1,546) - - - - (1,546)

Net change in fair value on available-for-sale financial assets - - - (1,642) - - - - - (1,642)

Realised fair value adjustments on available-for-sale financial assets - - - 96 - - - - - 96

Income tax on other comprehensive income - - - - - - - - - -

Statutory credit risk reserve - - - - - - - - - -

Transfer to statutory reserves

Transactions with shareholders, recorded directly in equity - - - - - - - - - -

Equity-settled share-based payment transactions - - - - - - - - - -

Transfer of vested share options to retained earnings - - - - - - - - - -

Dividends paid to equity holders - - - - - - - - - -

Balance at 30 June 2016 1,875 42,469 6,684 (726) 32 1,039 - 19,907 27,244 98,524

22 23Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Statement of cashflows – Group Statement of cashflows – Bank

H1 2017

Nmillion

H1 2016

Nmillion

Unaudited

Net cash flows from operating activities 56,227 77,659

Cash flows used in operations 20,581 62,165

Profit before tax 29,169 15,682

Adjusted for: (26,597) (9,295)

Credit impairment charges on loans and advances 13,953 8,450

Depreciation of property and equipment 2,010 1,830

Amortisation of intangible asset 23 -

Dividend income (50) (121)

Equity-settled share-based payments (21) 40

Non-cash flow movements in other borrowings (1,546) -

Non-cash flow movements in subordinated debt 51 3,352

Impairment of intangible asset 62

Interest expense 15,693 13,864

Interest income (56,728) (36,713)

Loss/(gain) on sale of property and equipment (44) 3

Increase/(decrease) in income-earning assets (175,449) (126,535)

Increase/(decrease) in deposits and other liabilities 193,458 182,313

Dividends received 45 109

Interest paid (15,541) (13,864)

Interest received 55,145 36,713

Direct taxation paid (4,003) (7,464)

Net cash flows from/(used in) investing activities (50,841) (103,435)

Capital expenditure on:

- property (36) (131)

- equipment, furniture and vehicles (1,499) (1,731)

Proceeds from sale of property, equipment, furniture and vehicles 63 35

(Purchase)/sale of financial investments (49,369) (101,608)

Net cash flows (used in)/from financing activities (6,285) 24,882

Proceeds from addition to other borrowings 24,803 24,882

Repayment of other borrowings (27,800) -

Dividends paid (3,288) -

Net increase/(decrease) in cash and cash equivalents (899) (894)

Effect of exchange rate changes on cash and cash equivalents 451 19,338

Cash and cash equivalents at beginning of the period 191,761 107,398

Cash and cash equivalents at end of the period 191,313 125,842

H1 2017

Nmillion

H1 2016

Nmillion

Unaudited

Net cash flows from operating activities 52,619 79,613

Cash flows used in operations 15,775 60,391

Profit before tax 14,324 5,500

Adjusted for: (24,486) (7,930)

Credit impairment charges on loans and advances 13,953 8,450

Depreciation of property and equipment 1,645 1,566

Amortisation of intangible assets 23 -

Dividend income (50) (121)

Items of intangible assets written off/expensed 62 0

Equity-settled share-based payments (16) 4

Non-cash flow movements in other borrowings (1,492) 0

Non-cash flow movements in subordinated debt 37 3,352

Interest expense 14,606 13,972

Interest income (53,212) (35,150)

Gains on disposal of property and equipment (42) (3)

Increase in loans and other assets (174,710) (123,401)

Increase in deposits and other liabilities 200,647 186,222

Dividends received 45 109

Interest paid (14,343) (13,957)

Interest received 51,748 33,891

Direct taxation paid (606) (821)

Net cash flows from/(used in) investing activities (58,643) (101,133)

Capital expenditure on:

- property (35) (131)

- equipment, furniture and vehicles (1,058) (1,646)

Proceeds from sale of property, equipment, furniture and vehicles 57 36

(Purchase)/sale of financial investments (57,607) (99,392)

Net cash flows (used in)/from financing activities 13,353 24,882

Proceeds from addition to other borrowings 24,803 24,882

Repayment of other borrowings (11,450) -

Proceed from issue of subordinated debt - -

Dividends paid - -

Net increase/(decrease) in cash and cash equivalents 7,329 3,362

Effect of exchange rate changes on cash and cash equivalents 410 19,338

Cash and cash equivalents at beginning of the period 179,722 89,862

Cash and cash equivalents at end of the period 187,461 112,562

24 25Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Gro

up

res

ult

s

in b

rief

Segmental structure for key business units

Stanbic IBTC Group

Personal and Business Banking Banking and other financial services

to individual customers and small-to-

medium-sized enterprises.

What we offer:

Mortgage lending

• Residential accomodation loans to

mainly personal market customers.

Instalmental sale and finance leases

• Finance of vehicles for personal

market customers.

• Finance of vehicles and equipment

in the business market.

Card Products

• Credit card facilities to individuals

and businesses (credit card issuing).

• Merchant transaction acquiring

services (card acquiring).

Transactional products

• Comprehensive suite of transactional,

savings and investment products.

This includes deposit taking activities

and electronic banking facilities.

Lending products

• Lending products offered to both

personal and business markets.

• Business lending offerings constitute

a comprehensive suite of lending

product offerings, structured

working capital finance solutions

and commercial property finance

solutions.

Corporate and Investment Banking Corporate and investment banking

services to government parastatals,

larger corporates, financial institutions

and international counterparties.

What we offer:

Global markets

• Fixed income instruments.

• Money market.

• Equities.

• Foreign exchange.

• Research.

Investment banking

• Equity capital market.

• Debt capital market.

• Financial advisory.

• Real Estate Finance.

• Mining, Energy and Infrastructure.

• Diversified Lending and Leverage.

Transactional products and services

• Investor services (asset custody).

• Transactional banking.

• Trade finance.

Coverage and distribution

• Client facing sales activities within

CIB division covering conglomerate

& diversified industries; consumer,

financial institutions; oil & gas, power &

infrastructure and telecommunications,

media & technology sector.

WealthInvestment management in form

of non-pension asset management,

pension asset management, trusteeship

and estate management.

What we offer:

Pension fund administration

• Retirement savings accounts.

• Gratuity schemes for companies.

Asset management

• Mutual funds.

• Portfolio management for High Net

worth individuals.

Trustee services

• Private trust.

• Corporate trust.

Insurance brokerage

• Life assurance.

• Group life assurance.

• Travel health insurance.

• General insurance.

27Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

2729303539

Segmental structure for key business unitsSegmental income statementPersonal & Business BankingCorporate & Investment BankingWealth

Business unit review

Business unit

review

H1 2017 H1 2016

Total income (Nmillion) 22,743 21,487

Total income (% change) 6 47.2

Total income contribution (%) 28.0 37.7

Cost-to-income ratio (%) 85.7 78.0

Credit loss ratio (%) 12.2 4.2

Gross loan growth (%) (8.7) (1.2)

Deposit growth (%) 9.1 14.2

H1 2017 H1 2016

Total income (Nmillion) 40,326 20,719

Total income (% change) 94.6 (1.7)

Total income contribution (%) 49.6 36.3

Cost-to-income ratio (%) 33.8 56.6

Credit loss ratio (%) 4.4 4.2

Gross loan growth (%) 14.2 13.7

Deposit growth (%) 19.1 26.7

H1 2017 H1 2016

Total income (Nmillion) 18,255 14,861

Total income (% change) 23 16.1

Total income contribution (%) 22.4 26

Cost-to-income ratio (%) 27.8 29.9

Assets under management growth (%) 16.4 8.2

Retirement savings accounts growth (%) 3.3 2.7

Personal & Business Banking% of group gross income

Corporate & Investment Banking% of group gross income

Wealth% of group gross income

Segmental income statement

Personal & Business Banking Corporate & Investment Banking Wealth

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

Gross income 21 29,495 24,432 52 48,172 31,638 30 19,350 14,861

Interest income 40 22,886 16,314 63 30,975 18,989 >100 2,867 1,410

Interest expense >100 (6,752) (2,945) (28) (7,846) (10,919) 0 (1,095) -

Net interest income 21 16,134 13,369 >100 23,129 8,070 26 1,772 1,410

Non-interest revenue (19) 6,609 8,118 36 17,197 12,649 23 16,483 13,451

Net fee and commission revenue (22) 6,285 8,074 (13) 5,145 5,891 22 16,463 13,441

Trading revenue 0 - - 81 11,950 6,607 16 -

Other revenue >100 324 44 (32) 102 151 (60) 4 10

Total income 6 22,743 21,487 95 40,326 20,719 23 18,255 14,861

Credit impairment charges >100 (8,421) (3,362) 9 (5,532) (5,088) 0 - -

Income after credit impairment charges (21) 14,322 18,125 >100 34,794 15,631 23 18,255 14,861

Operating expenses 16 (19,501) (16,754) 16 (13,627) (11,735) 14 (5,074) (4,446)

Staff costs 9 (9,284) (8,481) 28 (4,729) (3,703) 13 (2,479) (2,194)

Other operating expenses 23 (10,217) (8,273) 11 (8,898) (8,032) 15 (2,595) (2,252)

Profit before tax >(100) (5,179) 1,371 >100 21,167 3,896 27 13,181 10,415

Tax (83) (61) (357) 21 (737) (607) 25 (4,259) (3,401)

Profit after tax >(100) (5,240) 1,014 >100 20,430 3,289 27 8,922 7,014

28 29Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Bu

sin

ess

u

nit

rev

iew

Segmental structure for key business units (continued)

Personal & Business Banking (PBB)

Personal and Business Banking (PBB) deals with

the retail arm of group’s business. PBB provides

services to individual customers, high networth

individuals (HNIs) and the commercial and small

and medium scale enterprises (SME) business

segments. Personal and Business Banking

supports everyday banking needs of individuals

and businesses – receiving, saving and making

payments through our network of branches and

self-service digital channels. Overlaying these

horizontals is a strong relationship management

focus to ensure differentiated customer

experience for our customer segments.

The focus of PBB is to provide appropriate,

affordable, convenient and accessible financial

solutions to customers, through passionate and

customer focused employees nationwide. It

offers the following products; vehicle and asset

finance, unsecured and secured personal and

business loans, mortgage loans, a range of trade

finance products and various current, savings

and investment offerings.

PBB is divided into two business lines for

efficient service delivery - Personal Banking

and Business Banking. Personal Banking

focuses on banking services to individuals

through lifecycle management and offering

bespoke services to high networth individuals

by handling their wealth portfolio needs both

locally and abroad. It provides solutions that

meet individual need as these needs change.

Business Banking focuses on two segments

- small and medium scale enterprises and

commercial, providing them business solutions

to support their growing business needs.

Financial performance

PBB’s gross income grew by 21% to N29.5

billion (H1 2016: N24.4 billion), on the back

of 40% growth in interest income.

Interest income grew by 40% to N22.9

billion (H1 2016: N16.3 billion) on the back of

increase in investments and returns. Interest

expense increased by 129% to N6.8 billion

from N2.9 billion in H1 2016. The increase is

as a result of the increased deposits acquired

during the period. Consequently, Net interest

income increased by 21% to N16.1 billion from

N13.4billion.

Non-interest revenue, earned majorly

from fees and commission, declined by 19%

to N6.6 billion (H1 2016: N8.1 billion) on the

back of regulatory induced reduction in fees

and commission and the decline in economic

transactions. Total income however increased

by 6% to N22.7 billion from N21.5 billion in

H1 2016.

Credit impairment charges grew by over

100% to N8.4 billion in H1 2017 (H1 2016:

N3.4 billion) as a result of the challenging macro

environment and attendant second order risks

including the knock on effects of the prolonged

FX scarcity, high inflation levels, salary

arrears, job losses and low purchasing power,

which have reduced clients’ capacity to meet

existing obligations. The declining oil prices

and vandalization of oil pipelines also impacted

businesses negatively. The increase in credit

impairment also resulted in higher credit loss

ratio of 12.2% from 4.2% in H1 2016.

Operating expenses increased by 16% to

N19.5 billion (H1 2016: N16.8 billion). Staff

cost grew by 9% lower than inflation, while

other operating expenses increased by 23%

as a result of branch maintenance expenses,

marketing expenses to increase brand

awareness and insurance cost on securing

customer deposits. PBB’s cost-to-income ratio

deteriorated to 85.7% from 78.0% in H1 2016

due to increased operating expenses.

PBB recorded loss after tax of N5.2 billion

declining by over 100% from profit of N1.0

billion in H1 2016.

PBB’s gross loans declined by 9% to close

at N139 billion (FY 2016: N152 billion).

The slow growth is on the back of tightened

lending conditions and low customer appetite

for loans due to current economic situation.

Non-performing loans in PBB declined by 16%

to N15.7 billion following the write-off of fully

provisioned NPLs.

Customer deposits grew by 9% to N385

billion from N353 billion in FY 2016 on the

back of continued growth in customer numbers

and need to increase our cheap deposit base.

Deposit mix improved to 69% from 63% in FY

2016, as the ratio lower priced deposit to total

deposits.

Performance highlightsChange % H1 2017 H1 2016 FY 2016

Net interest income Nmillion 21 16,134 13,369 29,964

Non-interest revenue Nmillion (19) 6,609 8,118 14,512

Credit impairment charges Nmillion >100 (8,421) (3,362) (9,504)

Operating expenses Nmillion (16) (19,501) (16,754) (36,656)

(Loss)/profit before tax Nmillion >(100) (5,179) 1,371 (1,684)

(Loss)/profit after tax Nmillion >(100) (5,240) 1,014 (1,613)

Gross loans & advances Nmillion (9) 139,092 162,027 152,360

Deposit liabilities Nmillion 9 385,349 289,020 353,189

Cost-to-income % 85.7 78.0 82.4

Non-interest revenue to total income % 29.1 37.8 32.6

Credit loss ratio % 12.2 4.2 6.0

Loan to deposit % 36.1 56.1 43.1

Non-performing loans to total loans & advances % 11.3 11.5 12.3

Other key business statistics

Business infrastructure

Branch network Number 0 178 178 178

ATMs Number (1) 553 543 561

Net interest income

Non-interest revenue

Net interest income and net interest revenue

H1 2013 H1 2014 H1 2015 H1 2016 H1 2017

2,000

0

4,000

6,000

8,000

10,000

18,000

16,000

12,000

14,000

Nmillion

13,369

8,118

16,134

6,609

11,052

3,547

11,045

4,230

8,229

3,338

30 31Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Bu

sin

ess

u

nit

rev

iew

Quarterly analysis of performance

Q2 2017 Q1 2017 H1 2017

Net interest income Nmillion 7,757 8,377 16,134

Non-interest revenue Nmillion 3,240 3,369 6,609

Credit impairment charges Nmillion (6,912) (1,509) (8,421)

Operating expenses Nmillion (10,063) (9,438) (19,501)

Profit/(loss) before tax Nmillion (5,978) 799 (5,179)

Gross loans & advances Nmillion 139,092 147,321 139,092

Deposit liabilities Nmillion 385,349 378,477 385,349

Cost-to-income % 91.5 80.4 85.7

Non-interest revenue to total income % 29.5 28.7 29.1

Credit loss ratio % 19.9 4.1 12.1

Loan to deposit % 36.1 38.9 36.1

Non-performing loans to total loans & advances % 11.3 15.6 11.3

Factors impacting the results

Favourable

• Growth in net interest income is on the back of favourable yield on

assets and impact of current and savings deposits growth.

• Continued growth in customer deposits, supported by growth

in number of customers.

Transactional and lending products

• Decline in overdrafts to small and medium

scale businesses to support their working

capital requirements

• Term loans declined as some customers

paid down on their facilities.

• Impairment charges increased on both

performing and non-performing loans

due to economic realities

Adverse

• Increase in operating expenses as a result of growth in marketing

and advertising expenses, deposit and other insurance expenses and

AMCON sinking fund contribution.

• Reduction in transaction fees as directed by Central Bank of Nigeria.

• Increase in credit impairment charges.

Instalment sale and finance leases

• Asset quality deteriorated as non-

performing loans increased to N2.97

billion and non-performing loans ratio

increased to 17% (FY 2016: 11%). This

is due to classification of loans in haulage

and logistics business. This is linked to the

general economic slowdown evidenced in

the consumer sector.

Mortgage lending

• We witnessed decline in loan book which

can be attributed to the macro-economic

challenges the country is facing.

• Non-performing loans increased by over

12% to close at N325 million due to

increase in interest rate. Consequently, the

mortgage loan book’s non-performing loans

to total loans ratio worsened to 4% from

3% in FY 2016.

Breakdown of loans and advances to customers

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Gross loans and advances (9) 139,092 162,027 152,360

Mortgage (6) 8,370 8,918 8,924

Instalment sale & finance leases 8 17,418 20,775 16,123

Overdrafts (25) 21,128 21,542 28,086

Term loans (7) 92,176 110,793 99,226

Provisions (15) (12,637) (16,258) (14,839)

Specific credit impairment (19) (9,146) (12,808) (11,329)

Portfolio credit impairment (1) (3,491) (3,449) (3,510)

Net loans and advances (8) 126,455 145,770 137,521

Breakdown of non-performing loans

Overdrafts (24) 3,191 2,462 4,183

Term loans (27) 9,195 11,069 12,537

Instalment sale and finance leases 75 2,970 4,674 1,697

Mortgage loans 26 325 487 258

Total (16) 15,681 18,691 18,675

Loans and advances

32 33Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Bu

sin

ess

u

nit

rev

iew

Personal & Business Banking (continued)

Deposit breakdown

Change

%

H1 2017

Nmillion

H1 2016

Nmillion

FY 2016

Nmillion

Current deposits 17 221,411 143,849 188,877

Savings deposits 12 43,167 34,532 38,630

Call deposits (56) 4,250 2,935 9,687

Term deposits 0 116,521 107,703 115,996

Total deposits and current accounts 9 385,349 289,020 353,189

Deposit liabilities

• Growth in deposit book driven by growth customer numbers and need

to get cheaper funding

• Increase in current and savings accounts on the back of continued

execution of customer acquisition initiatives focused at individuals

and businesses with stable income.

• Lower priced deposits accounted for 69% of total deposits and

cushioned the impact of increased cost of funds due to expensive

term deposits acquired.

Corporate & Investment Banking (CIB)

Corporate and Investment Banking (CIB)

comprises four segment/units: Investment

Banking (IB), Global Markets (GM),

Transactional Products and Services (TPS) and

Client Coverage (CC).

Our Investment Banking team provides,

through Stanbic IBTC Capital Limited,

corporate finance and debt advisory services to

corporate and government entities.

The Global Markets team comprises

traders, sales managers and analysts of varying

specialisation in equities, fixed income, foreign

exchange, and money markets. Within GM,

Stanbic IBTC Stockbrokers Limited provides

world-class stockbroking services to local as

well as foreign investors in the Nigerian capital

markets and is the largest stockbroking house

in Nigeria. Also within GM, our highly respected

team of macroeconomic and equity research

analysts provide insights on the domestic

and international markets of our portfolio

investment clients.

Transactional Product and Services offers

standardised and tailored transactional

products and services including trade

finance solutions, working capital and cash

management solutions.

Our Client Coverage team manages

corporate relationships and is the main point

of contact with our clients. The team members

are skilled at identifying client needs and

requirements, and at aligning these with the

appropriate product houses for execution.

Financial performance

CIB’s total income was up 95% to N40.3billion

in H1 2017 (H1 2016: N20.7 billion), on the

back of a 63% growth in interest income.

Interest income increased by 63% to N31.0

billion (H1 2016:N19.0 billion). Interest income

growth is supported by increase in income from

investment securities due to favourable yields,

increase in income from loans and advances

on the back of loan growth and income from

interbank placement. Interest expense declined

by 28% to N7.8 billion from N10.9 billion

recorded in H1 2016. This is as a result of

high volume of cheap deposits recorded in the

deposit book. This led to an increase of over

100% in net interest income to N23.1 billion

(H1 2016: N8.07 billion).

Non-interest revenue increased by 36% to

N17.2 billion from N12.6 billion recorded in H1

2016. The increase was largely on the back of

trading revenue increase which came on the

back of the introduction of IEFX window. Net

fee and commission closed at N5.1 billion (H1

2016: N5.9 billion) as a result of regulatory

induced reduction in transaction fees and

conversion of deal pipeline in the investment

banking business.

Trading revenue was up 81% to N11.95

billion in H1 2017 (H1 2016: N6.6 billion).

The introduction of the IEFX window has

improved foreign exchange liquidity which in

turn impacted other product markets and the

macro-economy positively.

Credit impairment charge increased by 9%

to N5.5 billion from N5.1 billion in H1 2016.

The increase in credit impairments applied to

both performing and non-performing loans.

The decline in economic activities has resulted

in strain on some sectors of the economy

especially the oil and gas and telecoms. In line

with these economic realities, the group had to

increase its provisioning on loans and advances.

CIB maintained cost discipline in H1 2017

though operating expenses increased by 16%

to N13.6 billion from N11.7 billion in H1 2016.

Staff cost increased by 28% to N4.7 billion

from N3.7 billion in first half of 2017 due to

inflation related salary adjustment, while other

operating expenses increased by 11% to N8.9

billion (H1 2016: N8.0 billion) as a result of

growth in information technology expense to

drive efficient service delivery and increase

deposit insurance expenses. Profit before tax

was up by over a 100% to N21.2 billion, while

profit after tax also increased by over a 100%

to N20.4 billion.

Gross loans and advances grew by 14%

y-o-y to N255 billion in H1 2017 (FY 2016:

N223 billion). The growth was driven by 48%

and 11% growth in overdraft and term loans

to support customer’s working capital. CIB’s

asset quality deteriorated as non-performing

loans increased significantly to N15.2 billion

(FY 2016: Nil). Consequently, non-performing

loans to total loans ratio worsened to 6.0%

from nil position in FY 2016. The decline in

asset quality is primarily due to classification

of a client in the Oil & Gas sector whose

operations had been disrupted by militancy

action resulting in closure of the Trans

Forcados Pipeline.

Deposit liabilities grew to N247 billion,

representing a 19% increase over N207.8

billion achieved in FY 2016. The increase in

deposits is as a result of growing customer

relations.

34 35Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Bu

sin

ess

u

nit

rev

iew

Personal & Business Banking (continued)

10

0

50,000

H1 2015 FY 2015 H1 2016 FY 2016 H1 2017

150,000

100,000

200,000

250,000

400,000

350,000

300,000

Nmillion

0

20

40

60

80

120

100

%

262,640

215,451240,390

207,780222,956

254,597247,402245,060

304,623

80

107 103354,106

90

74

Gross loans & advances Net interest income

Deposit liabilities Non-interest revenue

Loan to deposit ratio

Performance highlightsChange % H1 2017 H1 2016 FY 2016

Net interest income Nmillion >100 23,129 8,070 24,202

Non-interest revenue Nmillion 36 17,197 12,649 25,308

Credit impairment charges Nmillion 9 (5,532) (5,088) (10,299)

Operating expenses Nmillion 16 (13,627) (11,735) (22,492)

Profit before tax Nmillion >100 21,167 3,896 16,719

Gross loans and advances Nmillion 14 254,597 245,060 222,956

Deposit liabilities Nmillion 19 247,402 304,623 207,780

Cost-to-income % 33.8 56.6 45.4

Non-interest revenue to total income % 42.6 61.1 51.1

Credit loss ratio % 4.4 4.2 3.4

Loan to deposit % 102.9 80.4 4.7

Other key business statistics

Investor services

Assets under custody Nbillion 26 3,648 1,916 2,900

Quarterly analysis of performance

Q2 2017 Q1 2017 H1 2017

Net interest income Nmillion 13,505 9,624 23,129

Non-interest revenue Nmillion 8,347 8,850 17,197

Credit impairment charges Nmillion (3,714) (1,818) (5,532)

Operating expenses Nmillion (8,216) (5,411) (13,627)

Profit before tax Nmillion 9,922 11,245 21,167

Gross loans & advances Nmillion 254,597 218,148 254,597

Deposit liabilities Nmillion 247,402 214,810 247,402

Cost-to-income % 37.6 29.3 33.8

Non-interest revenue to total income % 38.2 47.9 42.6

Credit loss ratio % 2.9 1.7 4.4

Loan to deposit % 102.9 101.6 102.9

Other key business statistics

Investor services

Assets under custody Nmillion 3,648 3,049 3,648

Factors impacting the results

Favourable

• Growth in loan book resulting in increase in interest income.

• Favourable yields on investment securities impacting positively on

interest income.

• Increase in rates impacting favourably on interbank placements.

• Decline in interest expense as a result of improved CASA mix.

• Improved FX liquidity has aided capital market activities which has

impacted our custody and capital market business.

Adverse

• Increase in credit impairment charges impacted negatively on profits.

• Strong competition for good quality credits.

• Reduction in transaction fees by Central Bank.

11

0H1 2013 H1 2014 H1 2015 H1 2016 H1 2017

5,000

10,000

15,000

25,000

20,000

Nmillion

17,197

13,497

23,129

12,649

8,070

11,517

9,562

13,551

8,749

10,921

Gross loans and customer deposits

CAGR (H1 2015-H1 2017): Gross loans: (1%)

Customer deposits: (9%)

Net interest income and non-interest revenue

CAGR (H1 2013-H1 2017): Net interest income: 28%

Non-interest revenue: 6%

36 37Group results

in brief

Business

unit review

Balance sheet

analysis

Market & shareholder

information

Income statement

analysis

Capital

management

Other

information

Stanbic IBTC Analysis of financial results for the 6 months ended 30 June 2017

Bu

sin

ess

u

nit

rev

iew

Corporate & Investment Banking (continued)

• Growth in deposits is as a result of growing customer relations.

Breakdown of deposits to customers

Change