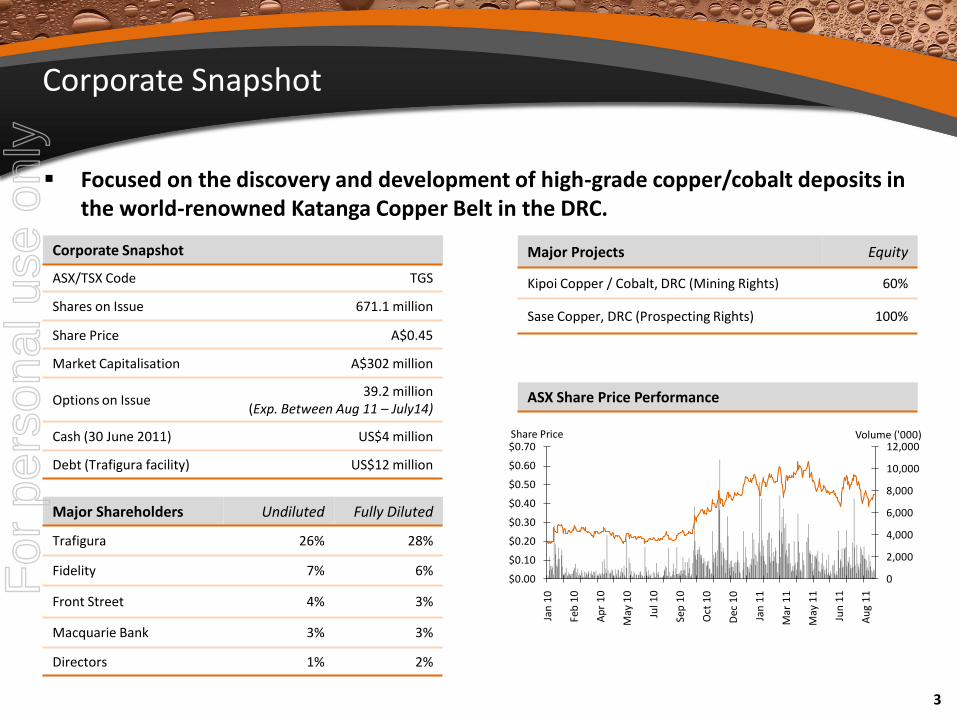

For personal use only - ASX · Corporate Snapshot ASX/TSX Code TGS Shares on Issue 671.1 million...

23

1 For personal use only

Transcript of For personal use only - ASX · Corporate Snapshot ASX/TSX Code TGS Shares on Issue 671.1 million...

1

For

per

sona

l use

onl

y

Disclaimer

Forward Looking Statements

This presentation contains forward looking information, which is based on assumptions and judgments of management regarding future events and

results. Such forward looking information, including but not limited to information with respect to the potential expansion of resources at Kipoi,

production and expected recoveries from the Stage 1 mining, HMS and spiral system operation, and development of a Stage 2 SX-EW plant at Kipoi,

involves known and unknown risks, uncertainties, and other factors which may cause the actual results, performance or achievements of the

Company to be materially different from any anticipated future results, performance or achievements expressed or implied by such forward looking

information. Such factors include, among others, the actual market prices of copper and cobalt, the actual results of current exploration, the

availability of equity and debt financing, the volatility currently being experienced in global financial markets, the actual results of future mining,

processing and development activities, changes in project parameters as plans continue to be evaluated, as well as those factors disclosed in the

Company's filings, is available under the Company’s profile on SEDAR at www.sedar.com.

Competent Person Statement

The information in this presentation that relates to exploration results, mineral resources or ore reserves is based on information compiled by Mr.

Brad Marwood, Managing Director and a full-time employee of the Company and a Member of the AusIMM (101610).

Mr. Marwood has sufficient experience, which is relevant to the style of mineralisation and type of deposit under consideration and to the activity

which he is undertaking, to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration

Results, Mineral Resources and Ore Reserves’ (JORC Code) and to qualify as a “Qualified Person” under National Instrument 43-101 –Standards of

Disclosure for Mineral Projects (“NI 43-101”). Mr. Marwood has verified the data disclosed in this presentation, including sampling, analytical and test

data underlying the information or opinions contained therein. Mr. Marwood consents to the inclusion in this presentation of the matters based on

his information in the form and context in which it appears.

2

For

per

sona

l use

onl

y

0

2,000

4,000

6,000

8,000

10,000

12,000

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

Jan

10

Feb

10

Ap

r 1

0

May

10

Jul 1

0

Sep

10

Oct

10

Dec

10

Jan

11

Mar

11

May

11

Jun

11

Au

g 1

1

Volume ('000)Share Price

3

Focused on the discovery and development of high-grade copper/cobalt deposits in the world-renowned Katanga Copper Belt in the DRC.

Corporate Snapshot

ASX/TSX Code TGS

Shares on Issue 671.1 million

Share Price A$0.45

Market Capitalisation A$302 million

Options on Issue39.2 million

(Exp. Between Aug 11 – July14)

Cash (30 June 2011) US$4 million

Debt (Trafigura facility) US$12 million

Major Projects Equity

Kipoi Copper / Cobalt, DRC (Mining Rights) 60%

Sase Copper, DRC (Prospecting Rights) 100%

Major Shareholders Undiluted Fully Diluted

Trafigura 26% 28%

Fidelity 7% 6%

Front Street 4% 3%

Macquarie Bank 3% 3%

Directors 1% 2%

ASX Share Price Performance

Corporate Snapshot

For

per

sona

l use

onl

y

Rhett BransNon Executive DirectorCivil engineer for 30 years involved in the development of numerous gold and base metal projects, including projects in Africa and more particularly the Democratic Republic of Congo, including copper SX/EW processing facilities.

Deon GarbersNon Executive DirectorMetallurgical Engineer with a MBA and 20 years experience in the mining industry in Africa. Occupied various high-level positions of mining companies and served on many boards in executive andnon-executive roles.

Jesus Fernandez LopezNon Executive DirectorCurrently Head of M&A Mining and CFO of Trafigura's mining division. More than nine years of experience in the corporate finance market and leads acquisitions and financings where Trafigura has an interest.

Neil FearisNon Executive Chairman29 years experience as a commercial lawyer in the UK and Australia. Practices principally in the areas of mergers and acquisitions, takeovers, public flotation, and other forms of capital raising. Non-executive director of Carnarvon Petroleum Limited, Perseus Mining Limited and Magma Metals Limited.

Brad MarwoodManaging DirectorMining engineer with over 26 years experience, including 16 years in development and operational roles across Africa. Project highlights include the Akim Yamfo-Sefwi Project in Ghana, now operated by Newmont Mining Ltd.

David ConstableNon Executive DirectorExtensive experience as an exploration geologist, investor relations professional and company director.

Experienced Board of Directors

4

For

per

sona

l use

onl

y

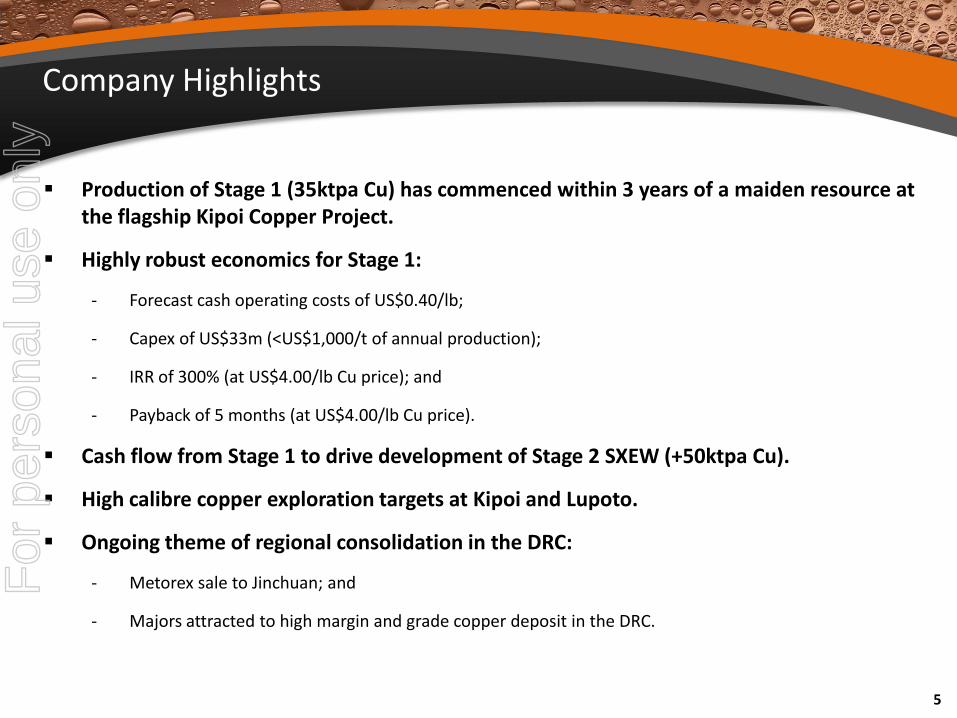

Production of Stage 1 (35ktpa Cu) has commenced within 3 years of a maiden resource at the flagship Kipoi Copper Project.

Highly robust economics for Stage 1:

- Forecast cash operating costs of US$0.40/lb;

- Capex of US$33m (<US$1,000/t of annual production);

- IRR of 300% (at US$4.00/lb Cu price); and

- Payback of 5 months (at US$4.00/lb Cu price).

Cash flow from Stage 1 to drive development of Stage 2 SXEW (+50ktpa Cu).

High calibre copper exploration targets at Kipoi and Lupoto.

Ongoing theme of regional consolidation in the DRC:

- Metorex sale to Jinchuan; and

- Majors attracted to high margin and grade copper deposit in the DRC.

Company Highlights

5

For

per

sona

l use

onl

y

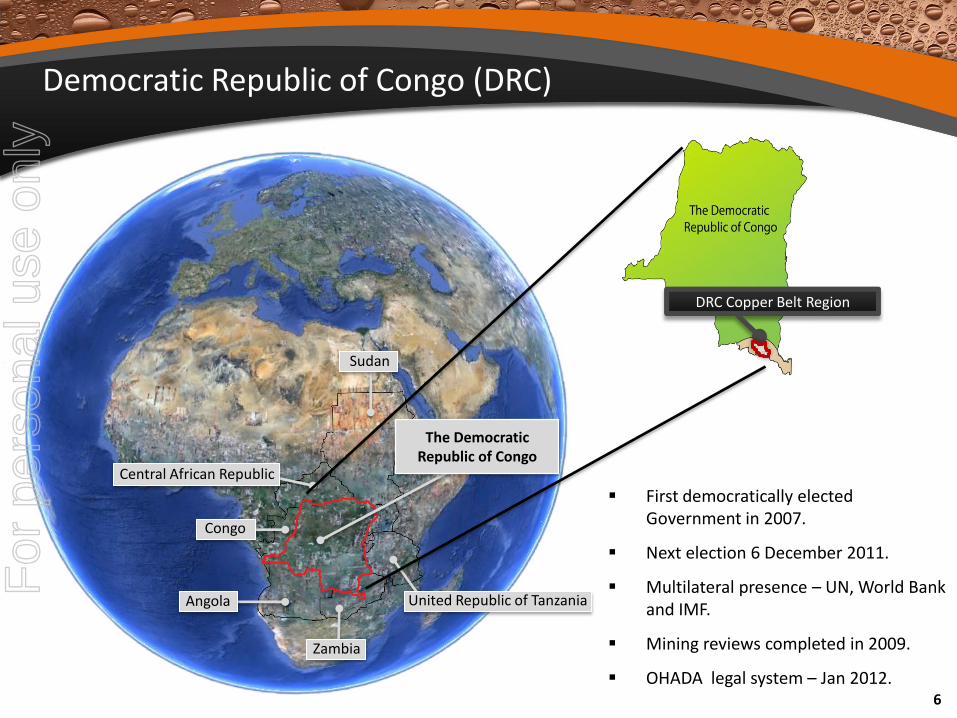

Sudan

Central African Republic

United Republic of Tanzania

Zambia

Angola

Congo

The Democratic Republic of Congo

DRC Copper Belt Region

6

Democratic Republic of Congo (DRC)

First democratically elected Government in 2007.

Next election 6 December 2011.

Multilateral presence – UN, World Bank and IMF.

Mining reviews completed in 2009.

OHADA legal system – Jan 2012.

For

per

sona

l use

onl

y

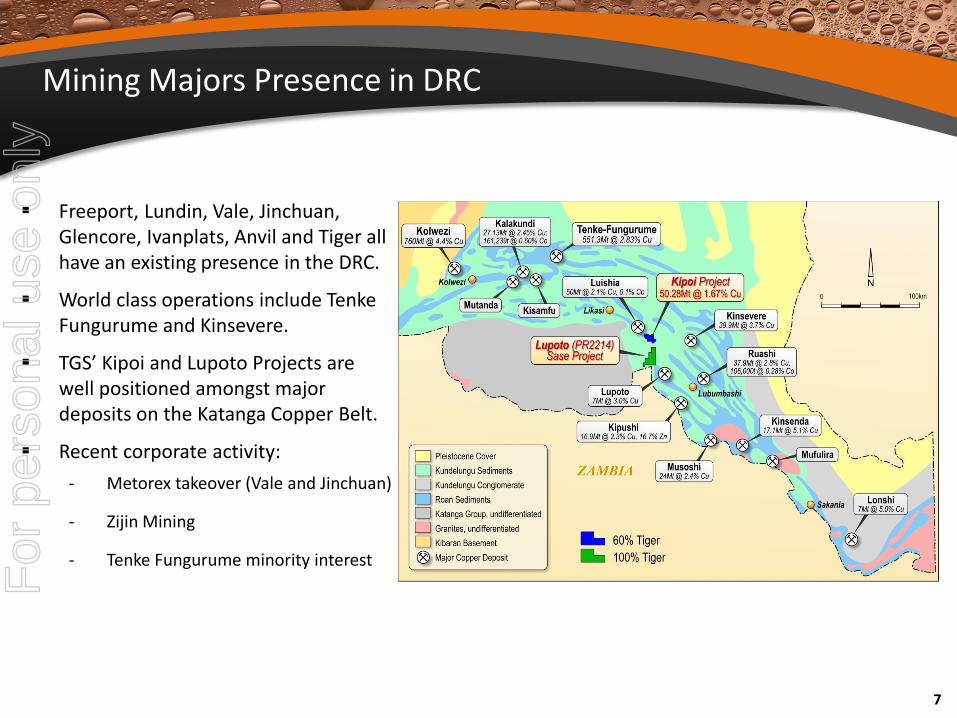

Mining Majors Presence in DRC

Freeport, Lundin, Vale, Jinchuan, Glencore, Ivanplats, Anvil and Tiger all have an existing presence in the DRC.

World class operations include Tenke Fungurume and Kinsevere.

TGS’ Kipoi and Lupoto Projects are well positioned amongst major deposits on the Katanga Copper Belt.

Recent corporate activity:

- Metorex takeover (Vale and Jinchuan)

- Zijin Mining

- Tenke Fungurume minority interest

7

For

per

sona

l use

onl

y

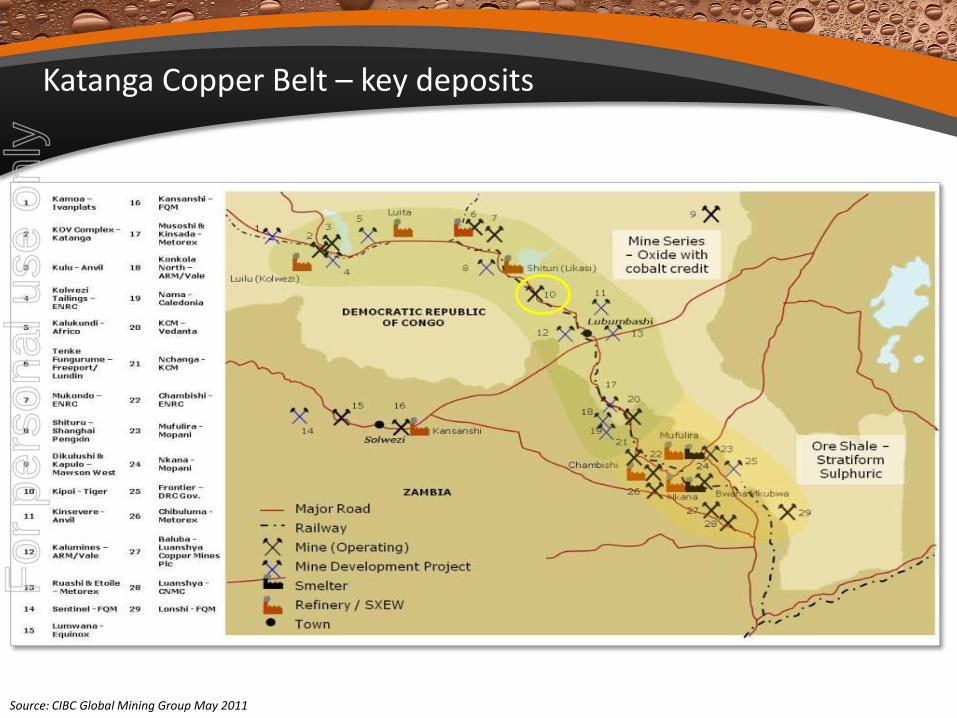

Source: CIBC Global Mining Group May 2011 8

Katanga Copper Belt – key deposits

For

per

sona

l use

onl

y

Roan SedimentsKundelungu Formation

Lubumbashi75km

Kipoi North71,600t Cu, (Inferred)

Kipoi Central23.5Mt @ 2.3% Cu for 535,000t Cu (M&I)

12.0 Mt @ 0.9% Cu for 102,000t Cu (Inferred)Incl. 2.9Mt @ 8.1% Cu for 232,000t Cu (M&I)

Kaminafitwe

[email protected]%[email protected]%Cu

Kileba South133,000t Cu

(Inferred)

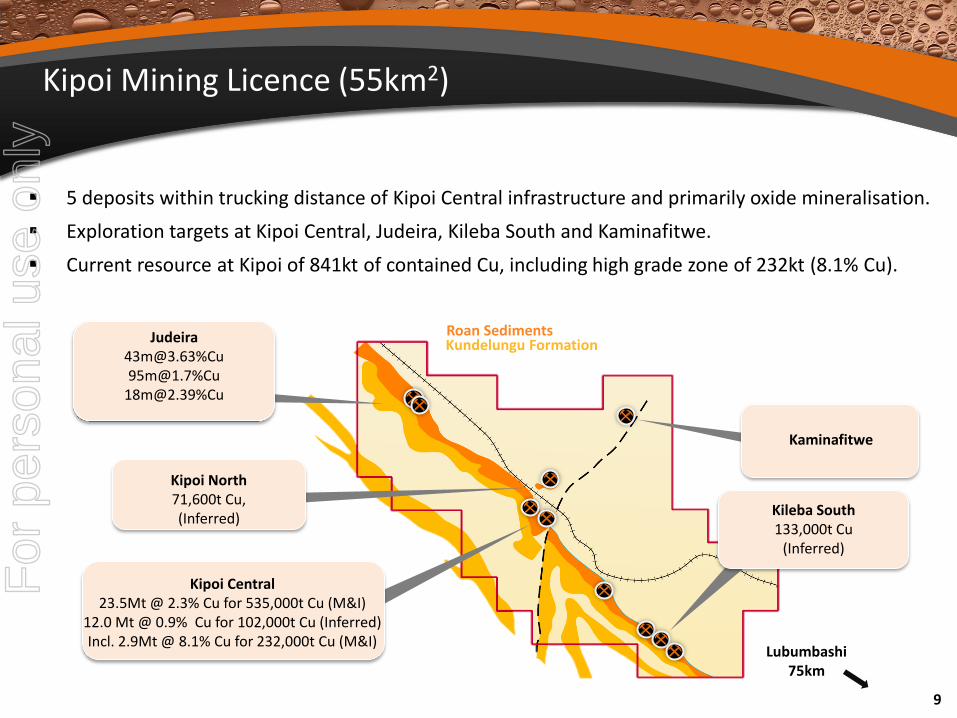

5 deposits within trucking distance of Kipoi Central infrastructure and primarily oxide mineralisation.

Exploration targets at Kipoi Central, Judeira, Kileba South and Kaminafitwe.

Current resource at Kipoi of 841kt of contained Cu, including high grade zone of 232kt (8.1% Cu).

Kipoi Mining Licence (55km2)

9

For

per

sona

l use

onl

y

Kipoi - Staged Operation

Staged development at Kipoi to minimise external funding requirements

Stage 1 – Heavy Media Separation (HMS)

High grade zone at Kipoi Central mined to produce 35ktpa of Cu in concentrate (25%) for 3 years.

During the Stage 1 operation 4.8Mt of lower grade ore (3% Cu) will be stockpiled for Stage 2.

Highly attractive economics (cash cost US$0.40/lb, capex US$33m, NPV US$258m and IRR of 300%) will result on significant cash flow to fund capex for Stage 2 development.

Production commenced April 2011.

Stage 2 – Solvent Extraction Electro Winning (SX-EW)

Initially process the 4.8Mt stockpile using heap leach to produce 25ktpa. C1 costs estimated at US$0.40/lb (no mining required).

Construction of a 50ktpa SX-EW plant to produce LME Grade A copper cathode.

Target of 75-100ktpa production subject to future exploration success. Plant expandable given ‘modular’ nature.

Scoping Study for Stage 2 due for completion in Q3 2011. DFS completion early 2012. First production 2014.

10

For

per

sona

l use

onl

y

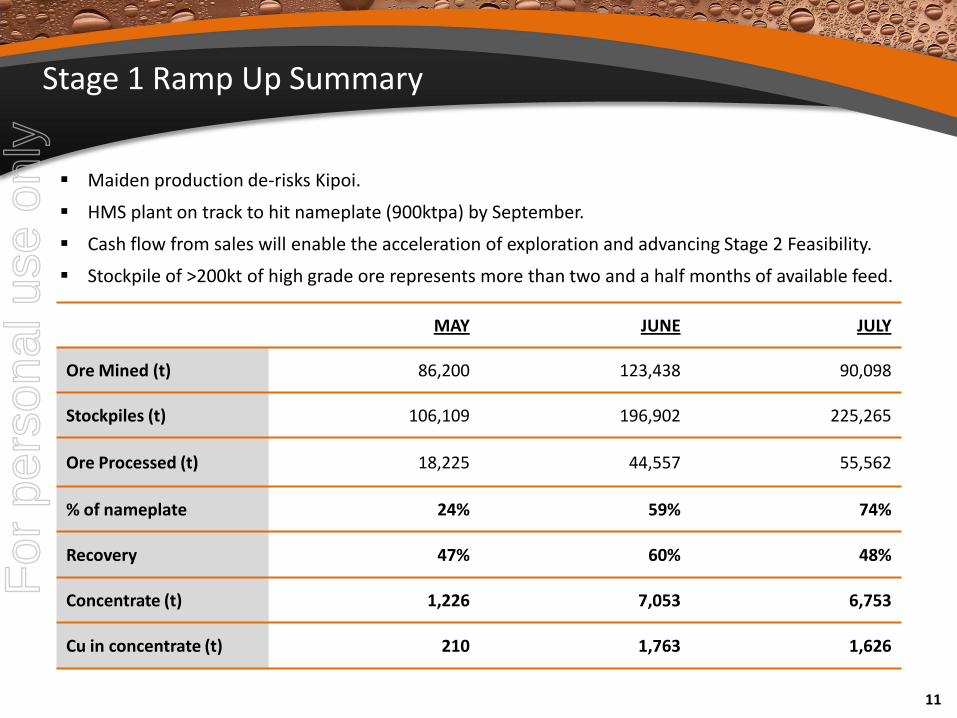

Stage 1 Ramp Up Summary

11

MAY JUNE JULY

Ore Mined (t) 86,200 123,438 90,098

Stockpiles (t) 106,109 196,902 225,265

Ore Processed (t) 18,225 44,557 55,562

% of nameplate 24% 59% 74%

Recovery 47% 60% 48%

Concentrate (t) 1,226 7,053 6,753

Cu in concentrate (t) 210 1,763 1,626

Maiden production de-risks Kipoi.

HMS plant on track to hit nameplate (900ktpa) by September.

Cash flow from sales will enable the acceleration of exploration and advancing Stage 2 Feasibility.

Stockpile of >200kt of high grade ore represents more than two and a half months of available feed.

For

per

sona

l use

onl

y

Stage 1 - On time and on budget

12

For

per

sona

l use

onl

y

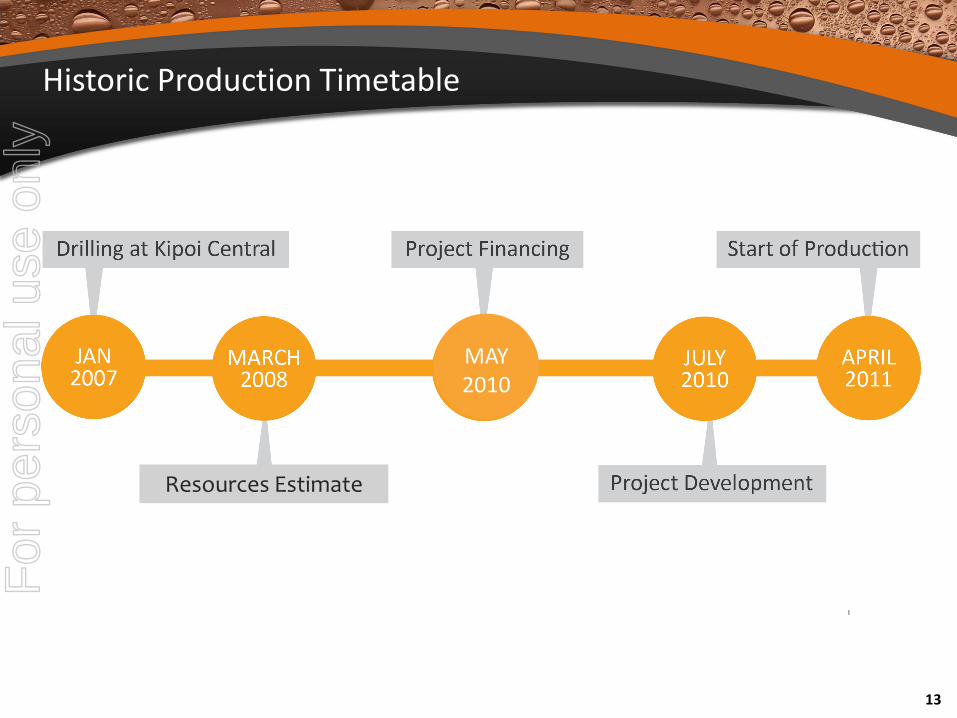

Historic Production Timetable

13

Resources Estimate

MAY2010

For

per

sona

l use

onl

y

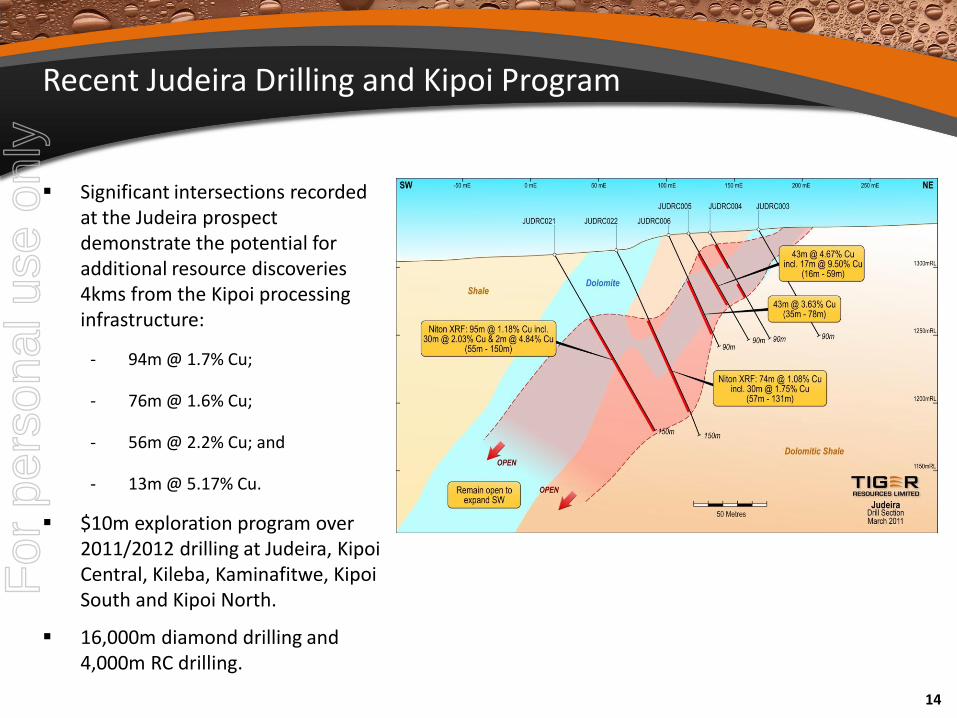

Significant intersections recorded at the Judeira prospect demonstrate the potential for additional resource discoveries 4kms from the Kipoi processing infrastructure:

- 94m @ 1.7% Cu;

- 76m @ 1.6% Cu;

- 56m @ 2.2% Cu; and

- 13m @ 5.17% Cu.

$10m exploration program over 2011/2012 drilling at Judeira, Kipoi Central, Kileba, Kaminafitwe, Kipoi South and Kipoi North.

16,000m diamond drilling and 4,000m RC drilling.

Recent Judeira Drilling and Kipoi Program

14

For

per

sona

l use

onl

y

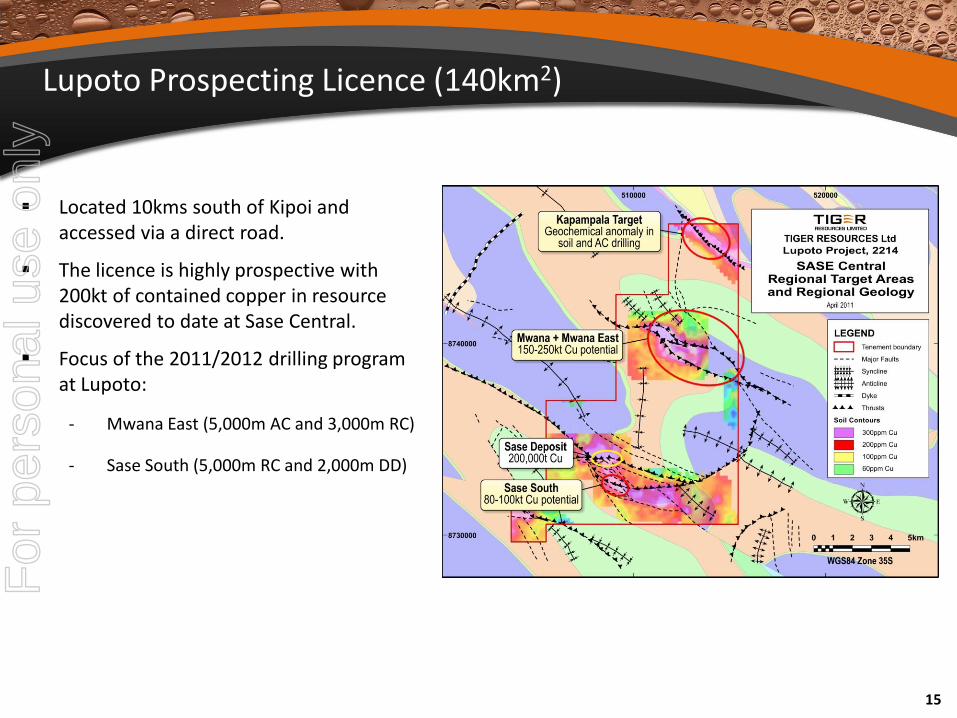

Lupoto Prospecting Licence (140km2)

Located 10kms south of Kipoi and accessed via a direct road.

The licence is highly prospective with 200kt of contained copper in resource discovered to date at Sase Central.

Focus of the 2011/2012 drilling program at Lupoto:

- Mwana East (5,000m AC and 3,000m RC)

- Sase South (5,000m RC and 2,000m DD)

15

For

per

sona

l use

onl

y

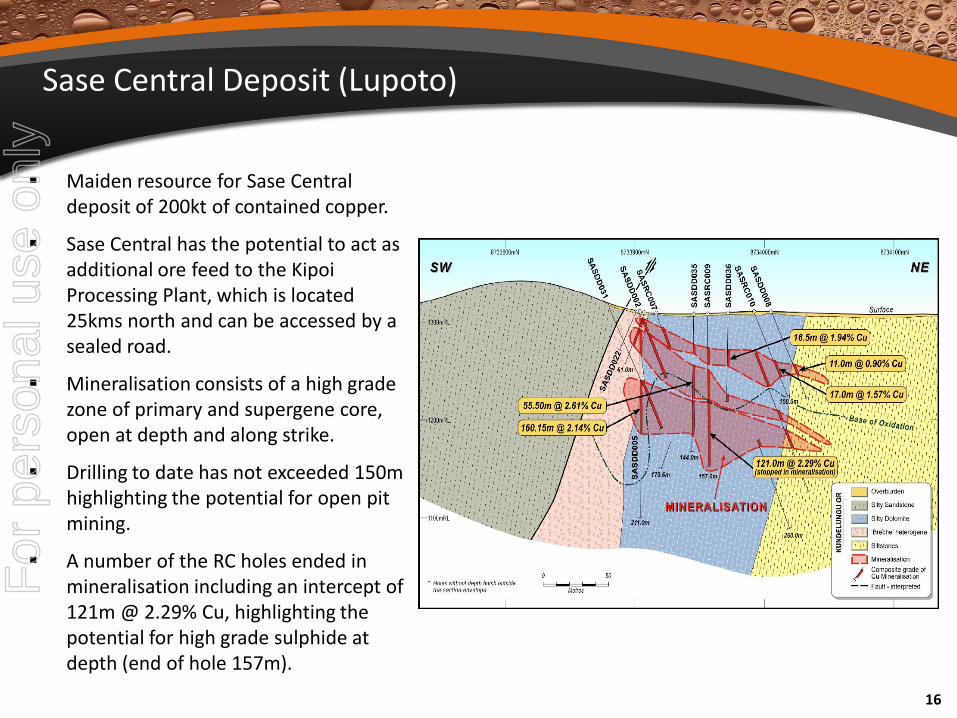

Maiden resource for Sase Central deposit of 200kt of contained copper.

Sase Central has the potential to act as additional ore feed to the Kipoi Processing Plant, which is located 25kms north and can be accessed by a sealed road.

Mineralisation consists of a high grade zone of primary and supergene core, open at depth and along strike.

Drilling to date has not exceeded 150m highlighting the potential for open pit mining.

A number of the RC holes ended in mineralisation including an intercept of 121m @ 2.29% Cu, highlighting the potential for high grade sulphide at depth (end of hole 157m).

Sase Central Deposit (Lupoto)

16

For

per

sona

l use

onl

y

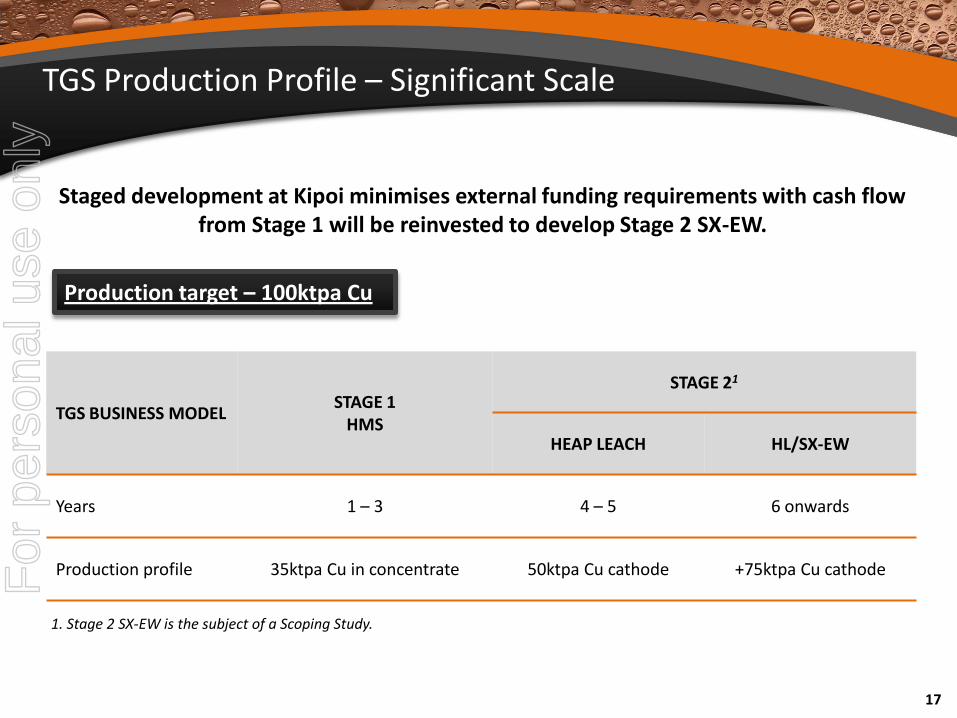

TGS Production Profile – Significant Scale

Production target – 100ktpa Cu

TGS BUSINESS MODELSTAGE 1

HMS

STAGE 21

HEAP LEACH HL/SX-EW

Years 1 – 3 4 – 5 6 onwards

Production profile 35ktpa Cu in concentrate 50ktpa Cu cathode +75ktpa Cu cathode

1. Stage 2 SX-EW is the subject of a Scoping Study.

Staged development at Kipoi minimises external funding requirements with cash flow from Stage 1 will be reinvested to develop Stage 2 SX-EW.

17

For

per

sona

l use

onl

y

Project Timeline

Ongoing news flow includes operational updates, drilling results, Stage 2 Scoping Study, Stage 2 DFS and regional initiatives.

18

Timeline 2011 2012 2013 2014 20152016

to 2024

Stage 1 (HMS 35ktpa Cu)

Stage 2

Scoping

DFS

Development

Production (50ktpa Cu) – HMS tail and LG stockpile

Production (50-100ktpa Cu) - SXEWFor

per

sona

l use

onl

y

-

20,000

40,000

60,000

80,000

100,000

120,000

$0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 $1.80 $2.00

Fore

cast

An

nu

al P

rod

uct

ion

(kt

pa)

Forecast C1 Cash Costs (US$/lb)

OZL

RXM (St 1)

RXM (St 2)

DML

PNA

AOH

SFR

TGS(St 1)

AVM

FND HGO

TGS(St 3) - 2016

TGS(St 2)

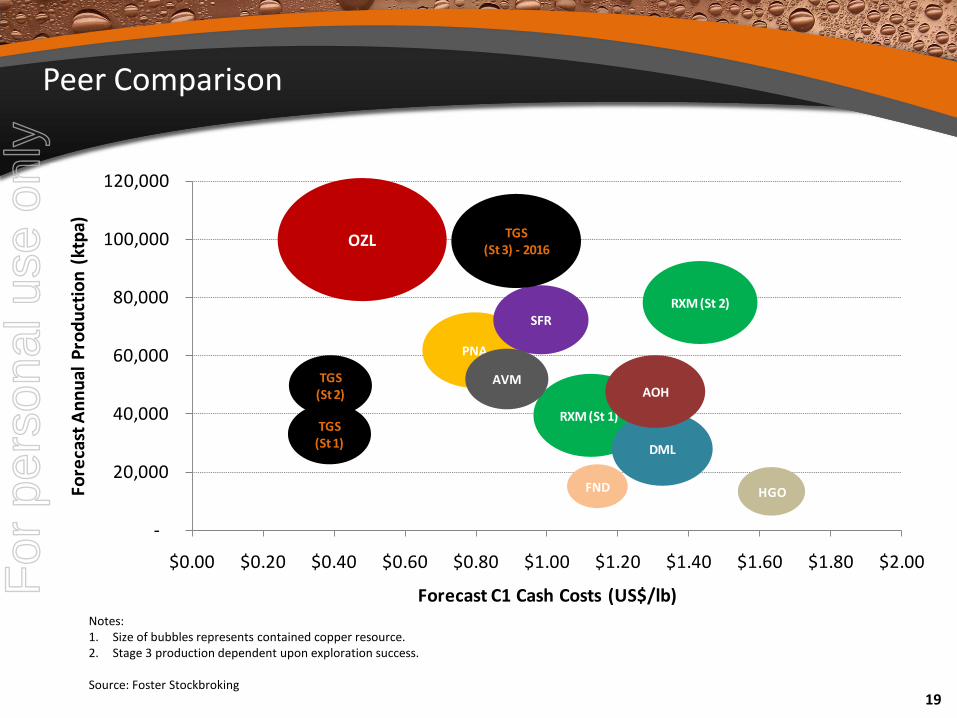

Peer Comparison

Notes:1. Size of bubbles represents contained copper resource.2. Stage 3 production dependent upon exploration success.

Source: Foster Stockbroking19

For

per

sona

l use

onl

y

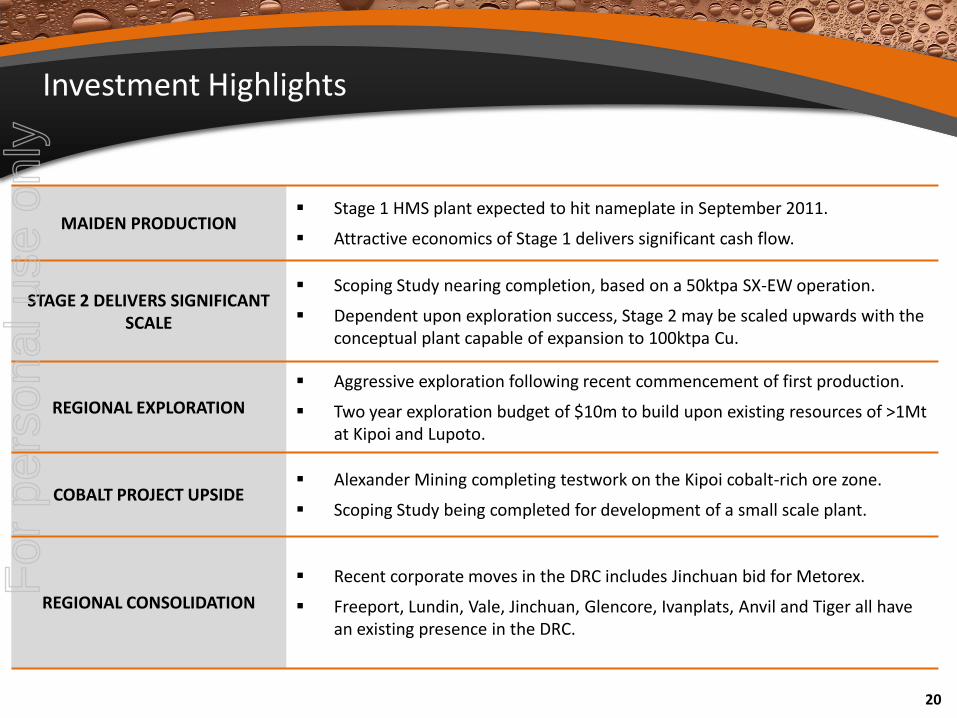

Investment Highlights

Fully Funded

MAIDEN PRODUCTION Stage 1 HMS plant expected to hit nameplate in September 2011.

Attractive economics of Stage 1 delivers significant cash flow.

STAGE 2 DELIVERS SIGNIFICANT SCALE

Scoping Study nearing completion, based on a 50ktpa SX-EW operation.

Dependent upon exploration success, Stage 2 may be scaled upwards with the conceptual plant capable of expansion to 100ktpa Cu.

REGIONAL EXPLORATION

Aggressive exploration following recent commencement of first production.

Two year exploration budget of $10m to build upon existing resources of >1Mt at Kipoi and Lupoto.

COBALT PROJECT UPSIDE Alexander Mining completing testwork on the Kipoi cobalt-rich ore zone.

Scoping Study being completed for development of a small scale plant.

REGIONAL CONSOLIDATION

Recent corporate moves in the DRC includes Jinchuan bid for Metorex.

Freeport, Lundin, Vale, Jinchuan, Glencore, Ivanplats, Anvil and Tiger all have an existing presence in the DRC.

20

For

per

sona

l use

onl

y

Contact details:

Stephen Hills – CFOOffice +61 (0)8 6188 2002Email: [email protected]

Brad Marwood - Managing DirectorOffice: +61 (0)8 6188 2001

Email: [email protected]

Nathan Ryan – Investor RelationsMobile: +61 3 96222 159

Further Information

21

For

per

sona

l use

onl

y

Kipoi Resource Type Mt Cu Grade Co Grade Cu (kt) Co (kt)

Kipoi Central Measured 9.2 3.8% 0.14% 347 13

Kipoi Central Indicated 14.3 1.3% 0.07% 187 9

Total Measured and Indicated 23.5 2.3% 0.09% 535 22

Kipoi Central Inferred 12.0 0.9% 0.05% 102 6

Kipoi North Inferred 5.3 1.4% 0.05% 72 3

Kileba South Inferred 9.5 1.4% - 133 -

Total Inferred 26.8 1.14% 0.05% 307 9

Kipoi High Grade Zone (included in Kipoi Central above)

Type Mt Cu Grade Co Grade Cu (kt) Co (kt)

Kipoi Central Measured 1.9 8.5% 0.2% 164 3

Kipoi Central Indicated 0.9 7.4% 0.1% 69 1

TOTAL 2.9 8.1% 0.1% 232 4

Global resources represent the equivalent of 841kt of contained Cu, including high grade resource component of 232kt Cu which forms the basis of Stage 1 operations.

Appendix 1: Detailed Kipoi Resource

22

For

per

sona

l use

onl

y

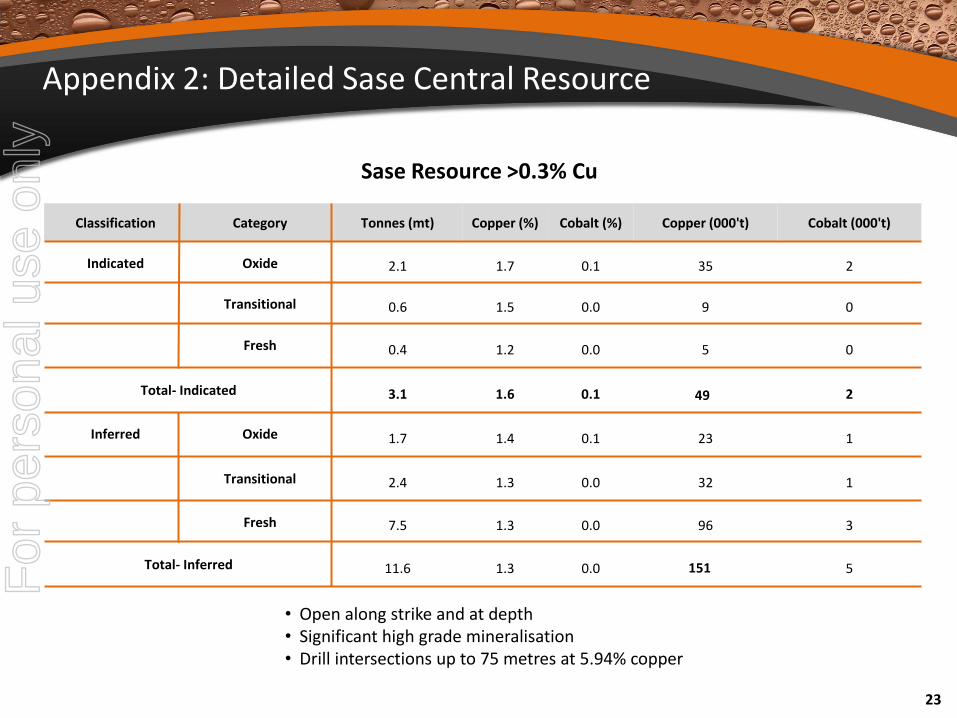

Appendix 2: Detailed Sase Central Resource

• Open along strike and at depth• Significant high grade mineralisation• Drill intersections up to 75 metres at 5.94% copper

Classification Category Tonnes (mt) Copper (%) Cobalt (%) Copper (000't) Cobalt (000't)

Indicated Oxide 2.1 1.7 0.1 35 2

Transitional 0.6 1.5 0.0 9 0

Fresh 0.4 1.2 0.0 5 0

Total- Indicated 3.1 1.6 0.1 2

Inferred Oxide 1.7 1.4 0.1 23 1

Transitional 2.4 1.3 0.0 32 1

Fresh 7.5 1.3 0.0 96 3

Total- Inferred 11.6 1.3 0.0 5

Sase Resource >0.3% Cu

151

49

23

For

per

sona

l use

onl

y

![[Positioning for Growth] - ASX · A financial snapshot Solid equity base (ASX & AIM: BSE ) o. A$224 million . market capitalisation @ A$0.30 Rapidly reducing debt. o. US$86 million](https://static.fdocuments.net/doc/165x107/5f0323f27e708231d407bcf6/positioning-for-growth-a-financial-snapshot-solid-equity-base-asx-aim.jpg)