FOR OFFICIAL USE ONLY - World Bank · FOR OFFICIAL USE ONLY INTERNATIONAL MONETARY FUND ... SICOES...

34

FOR OFFICIAL USE ONLY INTERNATIONAL MONETARY FUND WORLD BANK BOLIVIA HEAVILY INDEBTED POOR COUNTRIES INITIATIVE ASSESSMENT August, 2004

Transcript of FOR OFFICIAL USE ONLY - World Bank · FOR OFFICIAL USE ONLY INTERNATIONAL MONETARY FUND ... SICOES...

FOR OFFICIAL USE ONLY

INTERNATIONAL MONETARY FUND

WORLD BANK

BOLIVIA

HEAVILY INDEBTED POOR COUNTRIES INITIATIVE ASSESSMENT

August, 2004

List of Abbreviations AAP = Assessment and Action Plan CENCAP = Centro Nacional de Capacitación, Training National Center CFAA = Country Financial Accountability Assessment CGR = Controller General Office COSO = Committee of Sponsoring Organizations CUT = Treasury Single Account CV = Vigilance Committee DGC = Accounting Office DGMP = General Directorate for Public Procurement FAD = IMF Fiscal Affairs Department FNDR = National Regional Development Fund FPS = Fondo de Inversion Productiva y Social, Social Investment Fund GDP = Gross Domestic Product GFSM = IMF Government Finance Statistics Manual HIPC = Heavily Indebted Poor Country IMF = International Monetary Found INPS = National Social Security Institute INTOSAI = International Organization of Supreme Audit Institutions MOF = Ministry of Finance MTEF = Medium-Term Expenditure Framework NGO = NonGovernmental Organization PFM = Public Financial Management PEM = Public Expenditure Management PER = Public Expenditure Review POA = Plan Operativo Anual, Annual Operation Plan PRSP = Poverty Reduction Strategy Paper SAFCO = Financial Administration and Control System SAYCO = Administration and Control Systems SCCS = Accounts Section of the Supreme Court SICOES = Sistema de Información de Compras Estatales, Public Procurement Information System SIGMA = Financial Management Information System SINCOM = Sistema Integrado de Contabilidad Municipal, Municipal Integrated Accounting System SNC = Servicio Nacional de Caminos, National Road Service SNA = Servicio Nacional de Aduanas, Customs Agency SNII = Servicio Nacional de Impuestos Internos, National Tax Service TGN = National Treasury UPF = Fiscal Programming Unit VIPFE = Vice-Ministry of Public Investment and External Financing

2

TABLE OF CONTENTS

EXECUTIVE SUMMARY................................................................................................................4

I. ASSESSMENT OF THE CAPACITY TO TRACK POVERTY-REDUCING PUBLIC SPENDING…..……7

A. Assessment Coverage……………………..............................................................7

B. Budget Formulation..................................................................................................8

C. Budget Execution....................................................................................................16

D. Budget Reporting...................................................................................................20

E. Public Procurement.................................................................................................25

II. ACTION PLAN TO UPGRADE PUBLIC EXPENDITURE MANAGEMENT.....................................27

Tables 1. Public Expenditure Management AAP Indicators in Bolivia................................................6

2. HIPC II: Balance Distribution (2003) under the National Dialogue Law.............................8

3. Government Estimations for the Budget (in percent)….………….....................................11

4. Budget appropriations and execution by line-Ministries.....................................................12

5. Budget arrears by selected line-Ministries and local Governments.....................................17 6. SIGMA Coverage, 2003......................................................................................................23

3

EXECUTIVE SUMMARY

From May 10th to May 19th, 2004, an IMF/Bank mission conducted a HIPC assessment and action plan (AAP) on the monitoring of poverty-reducing expenditures. The team comprised Carlos Mollinedo-Trujillo (LCSPE, Team leader), Helio Tollini (IMF/FAD), Julio Velasco (LCCBO). Lurdes Linares (LCCBO) provided advice on the internal and external control and ensured coordination with the CFAA team. Simon Cueva, IMF Resident Representative, joined the mission at the first meeting with the Bolivian Authorities. The mission built up on CFAA, PER and IMF/WHD work and coordinated closely with their respective teams. It held discussions with a wide range of senior and technical Government officials (at national and sub-national levels) as well as with donors. The mission met senior and technical staff in MOF’s three Vice-Ministries (Budget, Public Investment and Treasury), the Fiscal Programming Unit, the Accountant General’s Office, the General Controller Office, the SIGMA/ILACO project, the Department of Public Procurement, the Prefecture of La Paz, the municipalities of La Paz and El Alto, and the donor community. The mission discussed extensively the draft AAP with the authorities and agreed an action plan with them. The AAP was discussed in a final meeting chaired by Mr. Luis Arnal (Vice-Minister of Public Investment and Foreign Financing, Ministry of Finance), with representatives from all Government units involved. The authorities stressed the importance of taking into account the extremely fragile political and economic situation while designing an action plan for PEM improvements in the short-term. After detailed discussions, agreement was reached on each and all AAP recommendations. Based on this frank and open discussion, it is the mission’s opinion that the authorities are likely to agree to publish the AAP following the review process. ASSESSMENT

In spite of the difficult political, economic and social situation, the draft assessment indicates that Bolivia’s PEM system has shown some improvement. Bolivia achieves the benchmark in 4 out of the 16 public expenditure management (PEM) indicators, compared to 5 out of 15 in the assessment carried out in 2001. The assessment shows that Bolivia has improved on 2 out of the 15 PEM indicators assessed in 2001, mainly due to more specific AAP guidelines related to the budgetary coverage. Despite the benchmark being reached, the coverage of the Central Government remains incomplete: public universities expenditures and revenues are poorly covered. The poverty reducing expenditures are clearly defined, although neither a proper functional classification nor a budget tagging mechanism exists. Improvement has been made in the areas of routine accounting and reconciliation since the progressive implementation of an integrated financial management system (SIGMA). Nowadays, the system covers all the Central Government – except for the Judiciary –, some decentralized agencies, one prefecture and two municipalities. Despite these improvements, the assessment shows that there are still some weaknesses in the PEM system. In total, Bolivia received lower ratings on 6 indicators compared to 2001. Local

4

Governments, which are responsible for more than 50 percent of total poverty related public expenditure, often tend to have weak PEM systems. Significant shortcomings identified in the assessment include: (1) a systematic over budgeting of current and capital items, both at central and local levels; (2) internal and external audit being only partially effective, resulting in weak oversight and a major absence of regular, timely and audited reports and financial statements; (3) the procurement system suffering from a weak legal framework and weak enforcement of rules. The achievement of actions agreed in the 2001 Action Plan has been hampered by the political instability and the difficult economic and social situation. Frequent changes in Administration combined with social unrest and severe fiscal crisis have delayed and hindered the Government efforts to improve PEM in Bolivia; in February 2003 the announcement of the national budget (in which projected fiscal adjustment measures were implicitly included) made by the Minister of Finance triggered a major social unrest. PEM in Bolivia has shown some progress in spite of these difficulties. Out of nineteen actions agreed in 2001, only 6 have been fully implemented, the implementation of another 6 has been initiated and the implementation of further 7 has not started. Most of the 2001 AAP recommendations that have not been completed have been postponed in light of the current social, economic and political difficult context. Additionally, two new actions have been introduced as the new Government decided that more effort is further needed. Table 3 presents the implementation status of the 2001 Action Plan in detail. ACTION PLAN

The mission formulated a new action plan, fully agreed upon with the Government, taking into consideration the present reality and needs of Bolivia. In the budget formulation process, the mission recommended the adoption of realistic macroeconomic assumptions, compatible with the fiscal program; the introduction of a true functional classification; the strengthening of technical expertise in Congress on budget formulation issues; and the assessment of the delicate issue of how to better budget public universities. The mission stressed that authorities should have a strategy to develop a Medium-Term Expenditure Framework (MTEF). A former Government priority, the idea was abandoned due to the recent high level of political uncertainty. The mission underlined the importance of maintaining the existing achievements on PEM, while longer-term initiatives continue to be gradually implemented. The mission stressed the importance of maintaining SIGMA and SIIF systems, as there are concerns among Government officials about their financial costs. The action plan presents a number of specific key recommendations on reporting, internal control, and external audit, in order to strengthen these capacities. Regarding procurement, the mission suggested to the Government to build on the good experience of the recent decree, and to later promulgate a law consistent with international practices.

5

Table 1: Public Expenditure Management AAP Indicators in Bolivia

Standard Desk 2001 2003-04Benchmark Assessment Assessment Assessment

FORMULATIONCOMPREHENSIVENESS

1 Fiscal reporting adequately covers the Government Finance Statistics definition of the general government sector A B B A2 Government activities are not funded through inadequately reported extrabudgetary sources to a significant degree A A B A3 Budget outturn data are quite close to the original budget B C C C4 Fiscal reports include grants projected to be provided by donors A A A A

CLASSIFICATION5 Budget expenditures are classified on an administrative, economic, and detailed functional or programmatic basis B C B B6 Poverty-reducing expenditures are clearly defined A B B B

PROJECTION7 Multi-year expenditure projections are integrated into the budget formulation process A C B B

EXECUTIONINTERNAL CONTROL

8 There exists a small stock of expenditure arrears, with little accumulation of arrears over the previous year A B B C9 Internal control is effective A C B B

10 Tracking surveys are in use, or are unnecessary B C B C

RECONCILIATION11 Satisfactory reconciliation of fiscal and banking records is undertaken routinely A B B B

REPORTINGIN-YEAR REPORTING

12 Internal fiscal repots are received within four weeks of the end of the relevant period B C B C13 Good-quality classification of poverty reducing spending is reflected in the in-year budget reports A C C C

FINAL AUDITED ACCOUNTS14 Routine transactions are entered into the main accounting system (s) within two months of the end of the fiscal year A A B C15 An audited record of the financial outturn is presented to the legislature within twelve months of the end of the fiscal year B C B C

NEWPROCUREMENT

16 The procurement system supports efficiency and effectiveness in the expenditure of public funds through clear A Band enforceable rules that promote competition, transparency and value for money.

3 5 4

Notes: Please shade cells in cases where the assessed indicator meets or exceeds the standard benchmark level

ASSESSMENT

TOTAL NUMBER OF BENCHMARKS MET

I. ASSESSMENT OF THE CAPACITY TO TRACK POVERTY-REDUCING PUBLIC SPENDING

A. Assessment Coverage

Bolivia’s General Government is constituted of a Central Administration, 9 Departments and 314 Municipalities (13 new ones will be created by December 2004), besides other decentralized institutions and the social security sector. Each Department has a Prefecture, which corresponds to a deconcentrated Central Government agency at the regional level. The Central Government appoints the prefecture governors, and their budget is included in the Central Government’s budget sent to the National Congress. Municipality majors are elected by direct vote every 5 years. The deconcentrated administrations are closely tied to the Central Government structure. For the education and health sectors, the corresponding ministry takes the decisions on formulation and execution of prefectures budget. The same laws and regulations govern both administration levels, and they use the same budget and accounting classifications as well as control mechanisms. The prefectures receive 20 percent of the significant hydrocarbons tax, specific royalties, and budget transfers from the Central Government. Municipal Governments are autonomous; their budgets are not included in the National Budget. However, the (consolidated) Government public investment program is somewhat disaggregated and reports projects executed by the municipalities. The role of municipal Government financial operations is significant: under the law, 20 percent of national tax collections are distributed to subnational Governments; a tributary co-participation is allocated from the central budget and automatically transferred by the National Treasury (TGN). Locally elected officials are empowered to define local Governments’ development and spending programs. The municipalities can levy additional taxes on real estate and vehicle property. Currently, approximately 55 percent of poverty related public spending is undertaken at subnational levels of Government, and about half of the total public investment is channeled through municipalities. The National Dialogue Law (Ley del Diálogo Nacional, N° 2235/2001), establishes the allocation of the HIPC II resources for a period of 15 years (Table 1). The municipalities receive the major share (56.5 percent). Additional amounts of poverty-reducing spending executed by sub-national levels are not expected in the near future, due to political difficulties in further decentralization. Hence, a significant share of the poverty reduction effort as well as from the HIPC II resources will remain with the Central Government, at least in the short to medium term.

7

Table 2. HIPC II: Balance Distribution (2003) under the National Dialogue Law CONCEPTS PERCENTAGE

HIPC II Resources 100.0 percent Bank charges (commissions, cost of checkbooks, etc) 1.2 percent Balance transferred to Central Government 42.3 percent National Solidarity Fund for Education 22.1 percent National Solidarity Fund for Health 10.2 percent National Solidarity Fund for SUMI benefits (mother and child) Max. 10.0 percent Balance transferred to Municipalities 56.5 percent Resources for productive infrastructure (70 percent) 39.6 percent Resources for education services (20 percent) 11.3 percent Resources for health services (10 percent) 5.6 percent Note: estimates from the European Commission in Bolivia. Unless otherwise advertised, the remainder of this assessment will discuss, under the various indicators, local, regional, and Central Government budget management and its capacity to track poverty related spending. The report’s findings on prefectures and municipality are based on meetings with officers from major prefectures, municipalities and their association, as well as on previous information available from the PER and CFAA.

B. Budget Formulation

Indicator 1: Coverage of the budget or fiscal reporting entity Benchmark 1: The budget covers the Government Finance Statistics Manual’s (GFSM) definition of the General Government sector, i.e., the central, regional, and local Governments, and all Government operations, whether funded through the budget or not. General Assessment: (A) - Benchmark is met. Overall, the fiscal data match the definition of the General Government sector set out in the GFSM. The central and local Government budgets are quite comprehensive. The financial operations of all these structures are tracked in the existing accounting systems. The budgetary coverage is comprehensive, fitting closely the consolidated General Government as defined in the IMF’s Manual of Government Finance Statistics (GFSM). The Central Government’s budget includes the deconcentrated Government agencies, including prefectures, and is submitted for approval to the National Congress. Coverage of expenditures and revenues from the 10 universities is limited to inter-Governmental transfers, classified as recurrent expenditures (even if actually spent on capital items), from the Central Government. Universities own-source revenues, estimated to be equivalent to 15 percent of their total expenditures and to approximately 1 percent of the Central Government’s budget, are not registered at all. Moreover, although supposed to send monthly execution information to the Accounting Office (DGC), in practice universities usually provide incomplete and delayed information, claiming they have financial autonomy.

8

Information on the Central Government’s recurrent expenditure execution is obtained through DGC, and on capital expenditures execution through the Vice-Ministry of Public Investment and External Financing (VIPFE). In both cases, as the financial management information system (SIGMA) still does not cover most prefectures and universities (Table 2), the Fiscal Programming Unit (UPF), which consolidates the General Government numbers, only receives the information after a 5 months lag. Municipalities have their own budget, submitted to their respective Representative Counsel. The central budget only records municipalities operations in respect to the amount of transfers conducted. As SIGMA has only been implemented in two municipalities (La Paz and Cochabamba, off-line), information on their budget execution is still a problem. The UPF, which consolidates the General Government numbers, follows closely 111 municipalities’ spending, which represent between 75 to 80 percent of local Governments expenditures, and estimates the rest. Other decentralized agencies, including social security institutes (cajas de salud), register all their operations in the Central Government’s budget and are required to periodically submit reports. Yet, expenditure allocations are not effectively monitored (in average there is a one-month lag in the submission of information). After the recent implementation of SIGMA, all transactions of these institutions are registered and the information on their activity is made readily available. At the municipal level, the Ministry of Popular Participation has developed a simplified PFM system (SINCOM) for small and medium sized municipalities. Indicator 2: Degree of spending being funded by inadequately reported extra budgetary sources Benchmark 2: Government activities are not funded to a significant extent through inadequately reported extra budgetary sources (less than 3 percent of total expenditures). General Assessment: (A) - Benchmark is met. Extra budgetary operations do exist, but are not significant. The budget incorporates own revenues generated by hospitals and by embassies since the formulation process. During execution, if collection of these revenues shows to be higher than initially estimated, the budget has to identify them, and authorization from the National Congress is needed before they can be spent. The Central Bank budget is also included within the Central Government’s budget. Extra budgetary expenditures are not permitted. However, until the end of 2002, due to the inherent weakness in budget planning, a great number of off-budget transactions were still executed outside of the system. This resulted in an overspending of certain budget and

9

treasury accounts, a practice that is in contradiction with the Budget Law, which prohibits this manner of public expenditure management. While SIGMA does not permit off-budget transactions, by subverting the system through manually recording accounting transactions, institutions are able to justify the expenditures ex post through the issuance of an Executive Decree. At the end of the fiscal year, the Government issues a Supreme Decree that regularizes pending cases. During this process, appropriations are transferred from budget categories with positive balances to those that have negative balances and additional spending carried out by agencies with their own resources are finally registered. In this way, public information on the executed budget does not show overdrafts. In 2002 this off-budget transactions amounted to about 1.2 percent of GDP or 3.8 percent of total public expenditure (approximately US$ 100 million). Starting 2003 off-budget transactions will be reduced significantly because this ex-post regularization practice has been explicitly forbidden and enforced. Moreover, although only for emergency adjustments, debt notes (Notas de Débito), an extraordinary fast payment mechanism, can still be used. This prevalent practice last happened during the political and social crisis of October 2003. These notes enabled the payment of the costs of social unrest, and were subsequently registered into the system. For 2004, the Financial Law has explicitly prohibited overspending through the mechanism described above. Additionally, as discussed in Indicator 1, universities do raise non-registered administrative fees and service charges. According to UPF, the known revenues of the universities outside the General Government budget amounted to about B$ 320 million in 2003, or 1 percent of total Government spending. Indicator 3: Reliability of the budget as a guide to future Benchmark 3: Budget outturn data are very close to the original budget General Assessment: (C) The benchmark is not met. There is a systematic over budgeting of current and capital items, both at central and local levels. Budget reallocations are significant, particularly at the institutional level. The Central Government budget is not a reliable guide overall to the Government’s fiscal policy. Although the average execution rate of the Central Government shown on Table 4 is highly acceptable (1.9 percent), the original budget tends to over-estimate revenues and overstate capital expenditures. This is part of the bargaining strategy used by Government entities, and gets worst when the formulation process goes to the National Congress, which usually artificially inflates revenues in order to incorporate new expenditures (especially pork-barrel amendments). To estimate revenues, the Government takes into account two variables, the potential nominal growth of the economy and the

10

efficiency gains of the collecting agencies, i.e. Impuestos Internos and Aduanas. Both are typically overestimated. Table 3 presents the real growth estimates used for the revenue forecasts, compared to actual growth rates, and the actual versus predicted deficits for the period 1999–2002 (inflation and exchange rate have been pretty stable in recent years in Bolivia). Growth estimates have been overestimated, on average, by more than 2 percentage points each year. However, most of the revenue overestimation has been linked to unrealistic predicted efficiency gains in revenue collection, which although they have diminished in the last two years are still high; over the 1999–2001 period they averaged nearly 10 percent per year for Impuestos Internos, and more than 16 percent per year for Aduanas. Interviews with participants in the budgetary process suggest that actual efficiency gains have been closer to 3 percent per year. Back of the envelope calculations, based on the evolution of revenues as a share of GDP, suggest that “efficiency” has increased by about 2.5 percent per year since 1995. Table 3. Government Estimations for the Budget (in percent)

Growth Deficit Predicted Efficiency Gains

Year Predicted Actual Predicted Actual SNII SNA 1999 5.2 0.6 3.6 3.7 9.0 17.0 2000 4.0 2.3 3.7 4.2 9.9 21.8 2001 4.5 1.5 3.7 7.0 10.0 10.0 2002 3.0 2.7 5.7 8.6 3.0 3.0 2003 2.9 2.4 6.5 7.9 5.0 5.0 As a result, during the year there is an acute shortage of resources to cover budgeted expenditures. Given the fiscal targets, Treasury manages to meet them through establishing monthly commitment and payment limits to line-ministries, which makes cash rationing an important feature of the system. The uncertainties concerning budget ceilings ensuing from this system produce operative inefficiencies over commitments and short-term planning horizons. Thus the budget is not being used as an effective tool for reflecting development plans and policies, but rather for defining budget envelopes for each agency. In general, the political bargaining power of each agency determines the allocations. The TGN decides re-allocations of current expenditures, whereas public investment decisions are competence of VIPFE. The budget is modified once over the year, to formalize the situations in which prior authorization by Congress is required. These situations include additional “appropriations” for the overall budget, for agencies that have underestimated their revenues, for any increase in payroll, and when reallocating from investments to recurrent expenditures. Other in-year expenditure reallocations within line agencies, called reversion, are authorized and can be done at any time during the year. Under this procedure, the agency changes the information introduced into the system after having used the funds for purposes different from those originally intended. Operations related to projects financed by external loans or grants are often introduced during execution and are reflected in the budget execution statement.

11

The information available on municipal budget realism in Bolivia does not show satisfactory results (Table 4). The analysis of selected municipalities shows that in 2 of the last 3 years the executed budget was more than 3 times bigger than the original one - the other year it was almost 2.5 times bigger. The credibility of municipal budgets largely depends on revenue projections, the quality of which is highly variable. Further allocation of funds for investment projects is somewhat less variable and is based on transfers from co-financing institutions such as FPS and FNDR as well as sources of external funding. Although there are incomplete fiscal transfers under revenue sharing and HIPC II arrangements, these are less variable than revenue estimations/collections. Table 4. Budget appropriations and execution by line-Ministries

2001 2002 2003

Approved Executed % Approved Executed % Approved Executed %

Total /1 34933 36937 105.7 37794 38343 101.5 34428 33918 98.5

Central Administration 21146 19249 91.0 23880 22746 95.3 25418 25075 98.7

Treasury 16693 14744 88.3 19012 18002 94.7 20258 20415 100.8

Ministry of Government 735 799 108.7 845 824 97.5 921 867 94.2

Ministry of Education 270 336 124.2 313 297 95.1 332 229 68.9

Ministry of Defense 918 1066 116.1 976 1045 107.0 1018 1178 115.7

Ministry of Finance 309 300 97.0 249 193 77.6 239 193 80.7

Ministry of Health 256 221 86.6 266 241 90.6 361 279 77.2

Ministry of Agriculture 366 256 70.0 430 344 80.0 544 384 70.6

Legislative Branch 200 207 103.5 212 222 104.9 203 214 105.3

Judicial Branch 409 316 77.5 435 333 76.5 402 357 88.7

Rest of Central Adm. 992 1004 101.2 1143 1246 109.0 1140 960 84.2

Deconcentrated agencies /1 2531 3716 146.8 3313 4115 124.2 3191 3043 95.4

Public finance sector /1 1338 960 71.8 1693 908 53.7 995 598 60.0

Social security agencies /1 1169 1180 100.9 1334 1420 106.5 239 261 109.3

Public enterprises /1 2893 2776 96.0 1360 1263 92.8 786 947 120.5

Prefectures /1 4375 4525 103.4 4576 4050 88.5 3052 1678 55.0

Municipalities /1 1481 4531 305.9 1638 3841 234.6 747 2316 309.9

1/ Note: Some decentralized institutions, prefectures and municipalities have not reported their financial statements to DGC; thus their information is not available.

12

Indicator 4: Inclusion of donor funds. Benchmark 4: Budgets and/or fiscal reports at all levels of Government include, without exception, grants expected to be provided by donors, and the capital and current expenditure of all multilateral or bilateral on Government activities. General Assessment: (A) The benchmark is met. All activities financed by donors are disclosed on the budget. In general, all grants and donations are included in the budget and in the actual outturn data. During the formulation of the budget law, there are sometimes lags between the approval of financing by donors and the preparation of the beneficiaries’ budget. In these cases, the beneficiary agency can increase its appropriations and get national resources as counterpart from the Treasury without requiring congressional approval, simply through budget modification. Whenever a credit/donation benefits several public entities, VIPFE records it and distributes the resources. The Government keeps a good track of external inflows. A standard approach to the handling of donor funds seems to be used in the large majority of cases, even at local level. Procedures seem to be simplified, conditionality from donors reduced, and only exceptionally, in small municipalities, deviations from these procedures occur. Sometimes cooperation agencies try to impose their own procedures for resource disbursement, and grants may not be included in the investment budget. In these cases, almost insignificant in terms of value according to the information obtained, donors and beneficiaries carry out the corresponding operations directly with each other, without a budgetary register. In bigger municipalities, according to our meetings with them and information from Government officers, previous register in the budget is required. Indicator 5: Classification Benchmark 5: Budget expenditures are classified on an administrative, economic, and detailed functional or programmatic basis. General Assessment: (B) - Benchmark is met. The budget classification system includes administrative, economic, and programmatic classification. A functional classification is not available.

13

The Central Government’s and the rest of the public sector entities’ budget operations are classified in conformity with international standards. They comprises administrative, economic sector, source of financing, and programmatic classifications. The institutional and economic classifications seem to be properly defined and implemented. Although current and capital budget are not formulated under the supervision of the same entity, they share the same institutional, economic and programmatic classifications (within different levels of Government). Within the programmatic classification, the specific activities and projects are budgeted. Notwithstanding, under the Financial Administration and Control System (SAFCO) norms, all agencies are required to present annual work programs using the program concept – Planes Operativos Anuales (POA) – which together form the budget submitted to Congress. Although there is a weak link between programs and outputs, the programmatic classification provides sufficient delineation of activities, enough to enable poverty-reducing spending to be identified. Neither the Central Government nor local Governments use functional classification to relate the uses of funds to the ends sought by the public sector. DGC uses a tentative functional classification to produce ex-post reports on budget execution. However, this functional classification is based on manual calculations “amalgamating” the institutional classifications and does not represent the coding of individual transactions, as acceptable by international standards. Indicator 6: Identification of poverty-reducing spending Benchmark 6: Poverty-reducing expenditures are clearly identified. General Assessment: (B) The benchmark is not met. Although the usage of HIPC II resources are well documented at both central and local level and the poverty-reducing expenditures are well defined, a proper functional classification or a budget tagging mechanism does not exist. Poverty reducing expenditures are defined in the Poverty Reduction Strategy Paper (PRSP), as follows: (i) the Ministry of Education’s budget (spending on universities not included); (ii) the Ministry of Health’s budget (spending on veterans’ pensions not included); (iii) expenditure on basic sanitation; (iv) urban and rural development expenditure; (v) other social spending by prefectures. However, there is no tagging of poverty-related expenditures in the budget, neither is it possible to identify expenditure by function, program or project. The poverty-reducing spending forecasts can not be obtained promptly by type of expenditure through a computer application. The process of estimating poverty-related expenditures is based on data from different sources, with the required aggregations being done manually, through a bridging-mechanism. DGC provides information on the Central Government’s recurrent poverty

14

reducing expenditures during budget execution, based mostly on SIGMA’s registers. Similarly, VIPFE provides information on public investments execution for the Central Government, singling out poverty reducing expenditures. UPF assesses 111 out of 314 municipalities’ spending, representing 75 to 80 percent of total expenditures—a limited but significant coverage—providing estimates on poverty reducing expenditure in the municipalities. UPF is also responsible for the final consolidation of this information. However, this is not done routinely nor produced on a timely basis—there is at least a 5 to 6 months lag. HIPC II resources are monitored by placing them into different accounts in the Central Bank. The amount transferred to each municipality is available, and expenditures are monitored by relying on quarterly municipal reports. These resources are also identified in the central and municipalities budgets—and budget execution reporting—by the source of financing classification. Reports are done on each project that is financed in whole or in part by HIPC II resources. Indicator 7: Integration of medium-term forecasts Benchmark 7: Multiyear expenditure projections are integrated into the budget formulation process. General Assessment: (B) - Benchmark not met. No multiyear expenditure projections are integrated into the budget formulation process, neither at the central nor the local level. There is no Medium-Term Expenditure Framework (MTEF) in Bolivia, neither in the Central Government nor in local Government administrations. Multi-year projections are currently being done for the period 2004-2008 as part of the exercise for producing the medium-term framework for the PRSP. There are no tools to integrate these projections into the preparation of the budget law, to assess the long-term costs of current policies, or to forecast poverty-reducing spending. The Central Government budget formulation process is not based on a realistic macroeconomic framework. Fiscal restrictions are not incorporated; macroeconomic parameters have usually been proven to be excessively optimistic. The National Congress always increases the revenues estimations that come in the draft budget law, without technical support, in order to incorporate new expenditures to regions. To achieve the fiscal results intended for the year, MOF has to impose strict commitment and payment monthly limits to line-ministries during budget execution. The Government intends to improve this arrangement, probably by establishing in an earlier regulation the fiscal target and restrictions for the upcoming budget. Moreover, discrepancies between the national budget and the fiscal program agreed with the IMF are significant.

15

C. Budget Execution Indicator 8: Arrears Benchmark 8: Small stock of expenditure arrears, little accumulation of arrears over the past year. General Assessment: (C) This benchmark is not met. Although at Central level the amount of arrears is reasonable, at local Governments’ level, especially in the large municipalities, arrears constitutes an important problem. Arrears defined as the difference between accrued and paid expenditures are common at all administration levels. In the Central Government and Prefectures, arrears represented in each of the last three years less than 5 percent of paid expenditures, varying within a range of US$ (+/-) 10 million. At deconcentrated (including social security agencies) and sub-national levels, arrears are much more significant, with values usually attaining far above 20 percent of paid expenditures. For the consolidated Government, in average, arrears represent slightly less than 10 percent of paid expenditures (Table 5). This is partly due to limitations in data recollection and processing. Recollection delays (approximately a 2-month lag) affect revenues as well as expenditures. Non recorded revenues are lost for the present administration and assigned to finance following year’s expenditures. Floating debt defined as the difference between committed and paid expenditures is a problem at all Government levels. In the Central Administration only, floating debt reached about US $ 100 million (over 1 percent of GDP) in 2000. It is estimated that for the Central Government the current share of the floating debt to the total budget reaches about 2.5 percent. At the municipal level, the degree of severity of the problem varies considerably. Even among the municipalities that do not have arrears to the private sector, several have arrears to the National Regional Development Fund (FNDR) and other parts of Government. Some small municipalities have already reached significant amounts of floating debt. And yet for big municipalities, estimations are even higher: an external audit reports that payments in arrears (floating debt) of the three largest Municipal Governments only – La Paz, Cochabamba and Santa Cruz – reached Bs. 137 million in 1999. This situation has spawned concern among the Government, which is trying to provide solutions through the PRFs (municipal rationalization program).

16

Table 5. Budget arrears by selected line-Ministries and local Governments 2001 2002 2003

Paid Arrears % Paid Arrears % Paid Arrears %

Total /1 33984 2950 8.7 34937 3407 9.8 31636 2282 7.2

Central Administration 18792 456 2.4 22085 661 3.0 24286 789 3.2

Treasury 14475 269 1.9 17559 443 2.5 19861 554 2.8

Ministry of Government 755 44 5.8 782 42 5.4 824 44 5.3

Ministry of Education 297 39 13.1 282 15 5.4 221 7 3.4

Ministry of Defense 1066 0 0.0 976 69 7.0 1111 66 6.0

Ministry of Finance 283 16 5.7 183 10 5.6 181 12 6.6

Ministry of Health 213 8 4.0 236 5 2.0 262 17 6.6

Ministry of Agriculture 254 2 0.9 339 5 1.4 378 7 1.7

Legislative Branch 193 14 7.3 205 17 8.2 201 14 6.7

Judicial Branch 290 26 9.1 318 15 4.6 344 13 3.9

Rest of Central Adm. 967 37 3.8 1205 41 3.4 905 55 6.1

Deconcentrated agencies /1 2950 766 26.0 3018 1098 36.4 2667 376 14.1

Public finance sector /1 904 56 6.2 867 41 4.8 554 43 7.8

Social security agencies /1 975 204 20.9 1066 354 33.2 146 116 79.5

Public enterprises /1 2684 91 3.4 1154 109 9.4 902 45 5.0

Prefectures /1 4458 67 1.5 3922 128 3.3 1634 44 2.7

Municipalities /1 3221 1310 40.7 2825 1016 36.0 1447 869 60.1

1/ Note: Some decentralized institutions, prefectures and municipalities have not reported their financial statements to DGC; thus their information is not available. Indicator 9: Effectiveness of the internal control system Benchmark 9: Internal control is effective. General Assessment: (B) This benchmark is not met. Internal control is only partially effective. There is a uniform framework for internal controls, but it is unsatisfactory in terms of compliance, quality control of fiscal and financial reports, as well as of its influence on the improvement of efficiency and effectiveness of expenditures. The Internal Control System has a uniform framework of regulations and procedures. The internal control is managed by the Bolivian Regulations for Internal Control, promulgated by the Controller General Office (CGR). In 2001, CGR updated these regulations with the incorporation of the principles set forth in the guidelines of the Committee of Sponsoring Organizations (COSO). The internal control system covers almost all administrative units. Internal control of the compliance of expenditures with laws and regulations remains insufficient. An adequate internal control environment is lacking and there is a strong

17

resistance against changing the situation. The internal control environment is highly dependent on the understanding that regulations are meant to improve transparency and governance regarding expenditure management. In general, the degree of compliance is low, especially within Governmental institutions, where personnel turnover and instability as well as political intervention are high. Quality control of fiscal and financial reports remains insufficient. According to the SAFCO Law, the role of internal audit is to check the functioning of internal controls ex post. There are approximately 207 internal audit units with more than 700 auditors executing annually between 2,500 and 3,000 internal audits. The internal audit units report directly to the head of each agency, but not to the MOF. This is one factor that seriously hampers the effectiveness of internal audit. On the other hand, the implementation of recommendations is solely dependent on the head of each agency; there is no incentive to improve controls and implement recommendations. CGR periodically supervises and assesses the internal audit units (CGR carried out 45 assessments and 71 follow-up reviews in 2002. In 2003, 37 assessments and 49 follow-up reviews were completed). These assessments have shown that internal audit is weak; high levels of turnover and staff instability, low wages and lack of technical competency are all contributing factors to the ineffectiveness of internal audit. According to CGR reports, in 2001 and 2002, only about 25 percent of the recommendations have been implemented. Monitoring of the efficiency and effectiveness of expenditures is insufficient. The weaknesses observed in the management of public expenditures undermine control activities; it is not possible to assess, due to the high degree of budget variation, whether resources are being used for the intended ends, nor whether the resources are being used effectively. Other important instruments for an effective internal control are information and management systems. The implementation of SIGMA along with the implementation of the treasury single account (CUT) and the standardization of the chart of accounts for Central Government entities contributed to improving the system of internal controls. However, besides a few exceptions, no system wide error rates neither material error rates in routine financial documents are monitored. At the local level, the implementation of the internal control system is just being developed. An adequate legal framework for municipal accounts and their auditing is in place. The law requires municipalities and prefectures to report budget executions to the Central Government. In recent years those reports have improved, even though they are not always timely. Moreover, Bolivia has created an alternative form of social oversight to monitor the implementation of municipal investment projects, the Vigilance Committees (Comités de Vigilancia, CVs). Complaints made by these social vigilance committees can be used to stop transfers for a project that is not being handled correctly. The role and performance of those Committees have improved; however, they still need to be strengthened in terms of technical and institutional capacity. CGR, in coordination with the Ministry of Popular Participation, is now working On the legal instruments to allow CENCAP to provide training to the CVs.

18

While all large and a few medium sized municipalities have established internal audit units, internal audit capacity is generally lacking in small municipalities. According to CGR, only 38 of 314 municipalities have an internal audit unit. As in the Central Government, the implementation of internal audit recommendations is solely dependant on the executive (in this case, the mayor). Indicator 10: Tracking surveys are in use. Benchmark 10: Tracking surveys, where necessary, are in use to supplement internal control, but may not be a regular feature of the public expenditure management (PEM) system. General Assessment: (C) This benchmark is not met. Tracking surveys have not been used and the underlying PEM system cannot reliably track spending. For the time being, concrete actions which seek to estimate the amount of public money that is actually delivered through the budget system to front-line service delivery units are still in their infancy. At present there is no tracking of Central Government expenditure through surveys, although their introduction is planned at municipal level. At the local level, tracking surveys are sporadically conducted through Vigilance Committees. However, those are not qualified for this assignment. In particular, CVs do not audit budgetary execution accounts to verify the reliability of budgetary information. They only ensure that the Mayor is carrying out his previous commitments. This limited role is mainly due to lack of resources for financing their main activities; however, a Social Control Fund (Fondo de Control Social) has been established for the specific purpose of financing the CVs’ expenses related to their functions. The European Commission is planning to conduct a compliance test exercise, which will mainly focus on verifying compliance with procedures and internal control systems to guarantee that funds are being used for the intended purposes. Indicator 11: Quality of fiscal information. Benchmark 11: Frequent reconciliation of all Government bank accounts (those held at the central bank and the commercial banks) with the Government’s accounting records. General Assessment: (B) This benchmark is not met. Although the central Government’s bank accounts are reconciled regularly and in a timely manner with the Government’s accounting records, the same does not happen in most municipalities.

19

For all Government bank accounts held at the central bank and at commercial banks a daily reconciliation is undertaken. This includes resources automatically transferred to municipalities. Bank accounts are reconciled daily both from balances of the above and below the line fiscal accounts. Executive reconciliation reports are available every day; complete reconciliation reports are available monthly. At the municipal level, reconciliation of all bank accounts including own revenues occurs satisfactorily and timely only in a number of municipalities. Bigger municipalities usually perform monthly reconciliation, which is informed a week later to DGC. In the smaller municipalities, reconciliation is not done in a satisfactorily and timely way; however the total amount transferred to small municipalities accounts is small.

D. Budget Reporting Indicator 12: Regularity of internal fiscal reporting Benchmark 12: Fiscal reports of spending units are received by the central agency between two and four weeks after the end of the relevant period. General Assessment: (C) This benchmark is not met. Adequate financial information is not timely available. Monthly and annual public financial statements are prepared in a timely fashion by the Central Agency; however, monthly reports are incomplete and are not published. Monthly information is available only of the Central Government and institutions that manage their budget and accounting via SIGMA (of those institutions, financial reporting is available in real time). Under the national accounting framework, obligatory accounting financial reports include: Balance Sheet, Income Statement, Statement of Cash Flow, Statement of Changes in Equity, Budget reports on Execution of Revenues and Expenditures, and the report on Account Savings for Public Investment Financing. However, in 2002 these financial statements covered only a small percentage of the sub-national administration: only 17 percent of the sub-national Government units were in compliance with reporting requirements. In 2003 compliance has improved. The lack of standardization of accounting and reporting requirements for all levels of Government and the fact that Government accounts remain unconsolidated weaken the ability of the Government to use financial statements to inform of public policy decisions.

Annually published financial reports contain only statistical information. The reports are not produced in accordance with recognized accounting standards, nor are prior year results presented, which does not allow for comparability of financial activity of the Government. In practice, DGC usually produces financial statements (unpublished) for the Central Government with a considerable delay—after June 30. Consolidated annual financial statements for the public sector are not produced, in part due to the lack of financial reports

20

from municipalities and the decentralized sector. As such, there are considerable gaps in the annual financial statements of the Government, and, if let unresolved, they will not result in the publication of meaningful Governmental financial information. In practice, according to the authorities, now that several agencies have been computerized, this time lag has been reduced to less than 30 days. Based on a sample of reports sent by the Ministries of Education, Health, and Agriculture, a transfer period of between three and ten days has been estimated.

Municipal accounting systems are weak; therefore reporting to Central Government is not always accurate. The only timely and reliable information on municipalities is prepared by the UPF which collects data of the 111 largest municipalities. Quarterly information is required to monitor the public sector deficit, but the UPF cannot provide municipal Government budget execution data—it is too difficult for the UPF to put together and reconcile this information. Indicator 13: Fiscal reports track poverty-reducing spending. Benchmark 13: Good-quality classification of poverty reducing spending is reflected in the in-year budget reports. General Assessment: (C ) This benchmark is not met. Social expenditures are being monitored, but the monitoring is not entirely based on a functional classification of expenditures. Rough poverty reduction spending items estimates are obtained from the programmatic budget structure to identify poverty objectives and policies. Current information systems are not equipped for providing functional classification of the budgetary execution. SIGMA (implemented essentially at Central Government level) as well as the systems currently used in the majority of municipal Government and prefectures does not enable to obtain a functional classification of expenditures. Ad hoc functional classification reports are projected when requested; these reports are not published. The information on budgetary execution is only displayed and published with an institutional or economic classification. There is no tagging of poverty-related expenditures in the budget both at the national and sub-national levels of Government. Social expenditures for the overall public sector are estimated annually outside of any information system. The UPF monitors social expenditures with annual frequency. To do that, it employs information from DGC on current expenditures of the various institutions of the Central Administration, public investment data of the MOF as well as data about 111 municipalities and various decentralized institutions collected by the UPF itself. Estimates of current social expenditures are available only by institutional classification of expenditures. Estimates of capital social expenditures are available by functional and institutional classification. The estimation of current social expenditures include current

21

expenditures of the Ministry of Health, Health Insurances, the Ministry of Education, public universities, expenditures of municipalities and prefectures in health and education, payments to pensioners and employers’ contributions. A functional classification of public investment is employed to estimate capital social expenditures, analyzing investments made in health, education, basic sanitation, urbanism and housing as well as rural development. Indicator 14: Operations are recorded in the accounts within the required periods. Benchmark 14: Routine transactions are entered into the main accounting system within two months of the end of the fiscal year. General Assessment: (C) This benchmark is not met. There is an official three month deadline for agencies to present their financial statements; most institutions do not submit their information on time. The Government has three month to close the accounts after the end of the fiscal year but some technical problems delay this process. According to the Budget Administration Law, accounts have to be closed and be submitted to DGC within three months after the end of the fiscal year (March 31st). As the majority of the institutions of the central administration are operating with SIGMA, they are able to present their financial states within the legal deadline; the majority of municipalities and prefectures nonetheless are unable to do so, precisely because they are not operating with SIGMA. Therefore, the delays in submitting financial information does not allow the closing of accounting books so as to respect the established deadline for closing the books. (March of the following year). Specifically the majority of prefectures are indeed able to present their financial statements within the legal deadline, while many municipalities do not present budget execution on time and fail to prepare financial statements due to a lack of capacity to generate financial information, lack of knowledge of statutory requirements and political conflicts. This lack of information is the reason why the report submitted to the Parliament by DGC six months after the end of the fiscal year only contains information provided by the Central Administration. SIGMA has a limited coverage at local and regional level (Table 6). SIGMA has achieved its implementation in almost all agencies of the Central Government (except for the Juridical Power) as well as in Governmental decentralized institutions like Development Funds, Custom and Tax Services, SNC and state universities. Yet, it is scarcely used in prefectures and municipalities. Out of the nine prefectures of Bolivia, the first one to adopt SIGMA was La Paz, in August 2003. Similarly of the 314 municipalities of the country, the only two that switched to SIGMA were those of La Paz and Cochabamba.

22

Table 6. SIGMA Coverage, 2003

Institutions

Budget in B$ millions

(no. of entities)

Budget execution

SIGMA on-line (no. of entities)

Budget execution

SIGMA off-line (no. of entities)

Budget execution

without SIGMA (no. of entities)

% Coverage Budget

Execution (no. entities)

Central Administration(a) 12,509 (25)

10,990 (24)

- (0)

1,519 (1)

88% (96%)

Decentralized Entities 4,241 (79)

95 (27)

- (1)

3,284 (51)

23% (35%)

Prefectures 4,821 (9)

- (0)

1,079 (1)

3,742 (8)

22% (11%)

Municipalities 2,315 (314)

- (0)

- (2)

2,315 (312)

0 % (0.6%)

Non-Financial Public Enterprises

1,212 (22)

630 (2)

- (0)

581 (20)

52% (9%)

Non-Banking Public Entities

690 (6)

618 (3)

- (0)

72 (3)

90% (50%)

Banks (b) 466 (1)

- (1)

- (0)

466 (0)

0 % (100%)

TOTAL 26,254 (456)

13,195 (57)

1,079 (4)

11,979 (395)

54% (13%)

(a) The Judicial Branch has not implemented SIGMA (b) The Central Bank uses SIGMA for Public Investment/Credit operations. Sources: Budget execution: Viceministerio de Presupuesto y Contaduría. No. of entities: Program (Programa de Modernización de la Administración Financiera Pública) The Ministry of Finance is unable to penalize the missing of the deadline. In principle, the Accountant General can suspend transfers from the Treasury to agencies that do not respect the deadline established by law, yet this practice is uncommon because of the political opposition it generates. The Congress is the other entity that could in theory reprimand the disregarding of the deadline, but again this practice is unusual. The UPF is the only Governmental institution that effectuates the timely follow-up of municipal expenditures. Currently the UPF collects information from 111 municipalities (that represent 84 percent of the population and 75 percent of HIPC II municipal transfers), which enables it to effectuate the follow-up of the program agreed with the IMF. Nevertheless the collection of information is realized manually, which delays the availability of information on municipal spending and does not allow to obtain the necessary information to assess the budgetary execution. Indicator 15: Timeliness of audited financial information. Benchmark 15: An audited record of the financial outturn should be presented to the national legislature within twelve months from the end of the fiscal year. General Assessment: (C) This benchmark is not met. Although the Controller General presents the findings of the external auditing six months after the end of the fiscal year, conditions are not met to effectuate an auditing of Financial Statements of the Central Administration.

23

CGR does not express any opinion of the Financial Statements of the Central Administration. CGR is in charge of realizing ex-post external auditing at all levels of Government, still the Congress receives the budgetary execution data from DGC six months after the end of the fiscal year without the auditing report of the CGR. In 2001 and 2002, CGR assessed the financial statements of the Central Administration establishing that they did not meet conditions to be audited, and therefore it was unable to express an evaluation of these financial states. Thus, in 2003, CGR took upon itself the task to realize follow-up auditing that enables to improve the financial statements of the Central Administration. CGR realizes external auditing of local and regional Governments. The 2001 financial statements of all prefectures and municipalities of the capital cities have been audited in 2002. The results of those auditing processes showed, however, that CGR usually cannot voice an opinion. Thus, in 2003, similarly to what was done with the Central Administration, CGR took upon itself the task to effectuate follow-up auditing in order for municipalities to improve their financial statements. In small and medium sized municipalities, CGR chooses among special, financial or SAYCO audits, thereby ensuring that each municipality will be visited at least once per year. CGR submits annually a report to the President. CGR presents an annual report to the President indicating the findings of the various auditing processes realized over the year.1 The report is informally distributed to other Governmental entities, including Congress –although it is never formally submitted to Congress. The CGR’s report to the President is published on its webpage, similarly to the executive summaries of the various auditing processes realized by this entity. The audited units are in charge of realizing the legal follow-up of the responsibility findings established by CGR. The (civil or penal) responsibility findings established by CGR are submitted to the audited expenditures units for them to start the corresponding legal actions. Nevertheless, the expenditures units rarely take the needed legal actions. At any rate the slowness of the legal system delays or even impedes the conclusion of the legal actions that have been started.

1 The Controller General is designed for a ten year mandate by the President, out of three candidates proposed by Congress with 2/3 of votes. Nevertheless he cannot be substituted by any of these authorities before the end of his mandate, except in case of a responsibility trial. For the past year and a half, the Government has been unable to name a Controller General, and an interim Controller has been appointed.

24

E. Public Procurement Indicator 16 – Efficiency and effectiveness of the public procurement system Benchmark 16: The public procurement system aims at providing efficiency and effectiveness in the expenditure of public funds through clear and enforceable rules that promote competition, transparency, and value for money. General Assessment: (B) This benchmark is not met. The acquisition norm is not yet formally a law. Consequently, juridical insecurity harms private sector participation, and jeopardizes efforts to eventually penalize irregularities found in the procurement process. Overall procurement risk assessment of Bolivia has been rated as high (see Bolivia CAS 2004), although significant improvement has been achieved in the CDF context by a majority of project-implementing agencies. Assigned risk assessment level is due mainly to a limited institutional capacity for implementing projects at all levels, particularly at the local Government level; lack of qualified procurement staff in a number of agencies to carry out procurement functions and tasks in an efficient manner; and the need to introduce modern and streamlined country procurement policies and procedures. The follow-up capacity and transparency of the procurement system has increased with the introduction in 2003 of the Public Procurement System (SICOES). The SICOES offers an improved transparency because it contains all Government procurements, planned and ongoing, with all the information being accessible through a webpage (www.sicoes.gob.bo), which enables the monitoring of the procurement processes at every level of Government. SICOES was complemented with the introduction of the Supreme Decree No. 27.328, of Jan/2004, agreed with the private sector, which enhanced competition by simplifying requirements for small firm participation, ensuring that a minimum acceptable deadline is respected during the procurement processes, and assuring full access to information by providers. Public procurement made outside of the formal system is reduced. Exception acquisitions represent less that 10 percent of public purchases (222 cases over 2.737 since it is in place); minor acquisitions represent less than 20 percent of the total public acquisitions of the Central Government. For municipalities, which usually cannot effectuate large amount acquisition because of their small revenues, 85 percent of procedures are done outside of the system. The SICOES does not effectuate a follow-up of these minor acquisitions, but it takes them into account in its statistics. The procurement system in Bolivia still faces some problems. The juridical insecurity due to the absence of a law is widely pointed out as a system weakness. Before the promulgation of a new law, it is important to initiate the process of harmonization, to ensure that the legislation will be consistent with internationally accepted practices. Recently a new

25

legislation has been approved by the Executive and contains measures against international standards. Too much preference is given too domestic firms in bidding contracts.

26

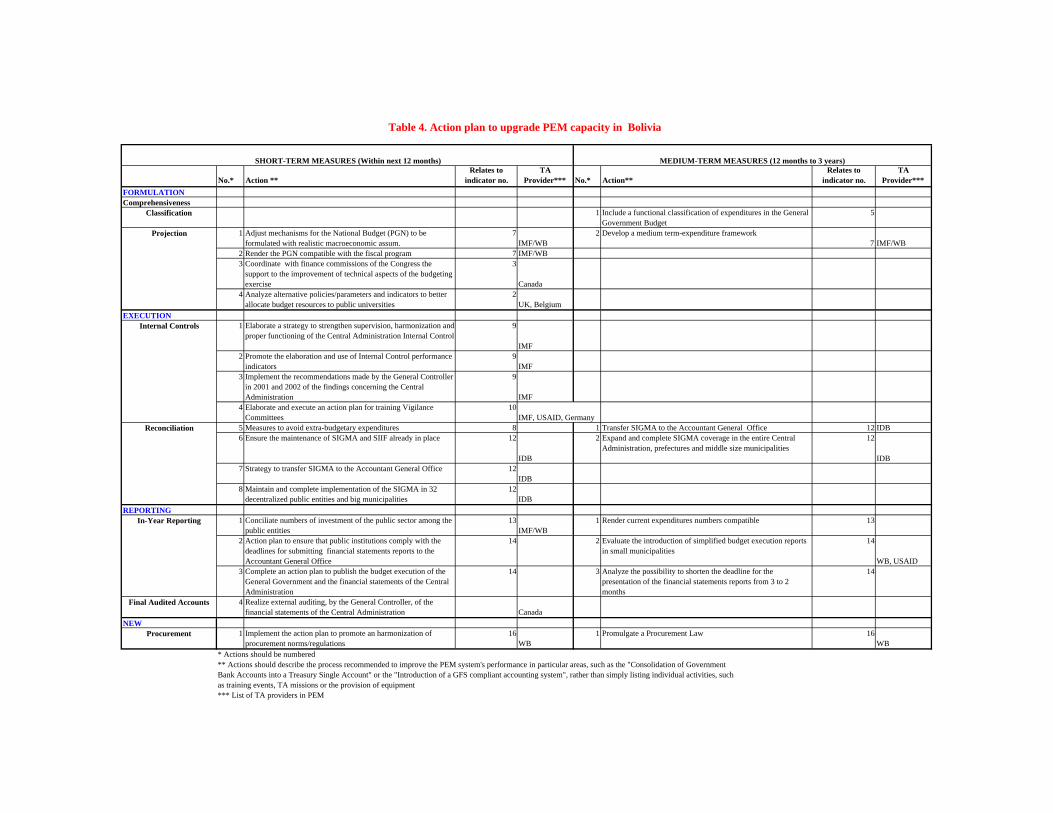

II. ACTION PLAN TO IMPROVE PUBLIC EXPENDITURE MANAGEMENT CAPACITY TO TRACK POVERTY RELATED EXPENDITURE

The Government’s authorities in conjunction with the mission have prepared a three-year action plan to improve the public expenditure management capacity at the national and sub-national levels of Government. The following short and medium-term objectives have been defined as high priority: 1. Budget Formulation

1.1. Adjust mechanisms in order for the National Budget (PGN) to be formulated with realistic macroeconomic assumptions that are compatibles with the market’s forecasts (short-term, starting in 2005).

1.2. Render the PGN compatible with the fiscal program taking into account the financial program agreed with the International Monetary Fund (short/medium-term, during 2004-2005).

1.3. Coordinate with the two finance commissions of the Congress the support to the improvement of technical aspects of the budgeting exercise (short-term, starting with the PGN 2005).

1.4. Analyze alternative policies/parameters and indicators to better allocate budget resources to public universities (short-term, starting with the PGN 2005).

1.5. Include a functional classification of expenditures in the General Government budget formulation and execution, compatible with internationally accepted patterns, which enables the identification of pro-poor expenditures (medium-term, during 2006).

1.6. Develop a medium term-expenditure framework (MTEF). The MTEF needs to include initial medium-term estimations of available resources and projected expenditures (medium-term, starting in 2006).

2. Budget Execution

2.1. Elaborate a strategy to strengthen supervision, harmonization and proper functioning of the Central Administration Internal Control (short-term, during 2004).

2.2. Promote the elaboration and use of Internal Control performance indicators for monitoring performance of administrative and operative systems, to improve the efficiency of Internal Control (short-term, starting in 2005).

2.3. Implement the recommendations made by the General Controller in 2001 and 2002 of the findings concerning the Central Administration and within the frame of competence of the Accountant General. (short/medium-term, during 2004-2005).

27

2.4. Elaborate and execute an action plan for training Vigilance Committees on social control, budget process and foundations of administration systems – with emphasis on budget (short/medium-term, during 2004-2005).

2.5. Assess whether it would be useful to incorporate adequate contingency reserves in the PGN with the aim to avoid extra-budgetary expenditures (short-term, during 2004).

2.6. Ensure the maintenance of SIGMA and SIIF already implemented within the public sector, providing them with adequate financial resources, with the objective to enable their proper functioning and their improvement in the medium term (short-term, during 2004).

2.7. Elaborate a strategy to transfer full responsibility of SIGMA to the Accountant General (short-term, during 2004).

2.8. Maintain and complete implementation of the SIGMA in 32 decentralized public entities, in the prefectures of Cochabamba and Santa Cruz and in the municipalities of Cochabamba, Santa Cruz, Tarija, Oruro, Potosí, Sucre and El Alto (short-term, until mid-2005)

2.9. Transfer full responsibility of SIGMA to the Accountant General (medium-term, from 2005 onwards).

2.10. Expand and complete SIGMA coverage (including the unique account system) in the entire Central Administration, 9 prefectures and in 4 middle size municipalities (medium-term, until the end of 2005).

3. Information and Budget Reporting

3.1. Conciliate numbers of investment of the public sector among the various entities of the public sector (short-term, during 2004).

3.2. Establish an action plan to ensure that public institutions comply with the deadlines for submitting financial statements reports to the Accountant General (short-term, during 2004).

3.3. Complete an action plan to publish the budget execution of the General Government and the financial statements of the Central Administration (short-term, during 2004; aiming at publishing the budget execution of the General Government and the financial statements of the Central Administration from the 2005-financial-year onwards).

3.4. Realize external auditing, by the General Controller, of the financial statements of the Central Administration (short-term, beginning from the closing of the 2005 financial exercise).

3.5. Render current expenditures numbers compatible among the various entities of the public sector (medium-term, during 2005).

3.6. Evaluate the possibility to introduce the use of simplified budget execution reports in the small municipalities to obtain basic information in a timely manner (medium-term, during 2005).

3.7. Analyze the possibility to shorten the deadline for the presentation of the financial statements reports from 3 to 2 months of public institutions to the Accountant General (medium-term, starting on 2005).

28

4. Public Procurement

4.1. Implement the action plan to promote a harmonization of procurement norms/regulations of the international cooperation (short/medium-term, during 2004-2005).

4.2. Promulgate a Procurement Law consistent with international practices as commonly accepted and building on the experience of the public procurement decree, through the (medium-term).

29

Standard Desk 2001 2003-04Benchmark Assessment Assessment Assessment

FORMULATIONCOMPREHENSIVENESS

1 Fiscal reporting adequately covers the Government Finance Statistics definition of the general government sector A B B A2 Government activities are not funded through inadequately reported extrabudgetary sources to a significant degree A A B A3 Budget outturn data are quite close to the original budget B C C C4 Fiscal reports include grants projected to be provided by donors A A A A

CLASSIFICATION5 Budget expenditures are classified on an administrative, economic, and detailed functional or programmatic basis B C B B6 Poverty-reducing expenditures are clearly defined A B B B

PROJECTION7 Multi-year expenditure projections are integrated into the budget formulation process A C B B

EXECUTIONINTERNAL CONTROL

8 There exists a small stock of expenditure arrears, with little accumulation of arrears over the previous year A B B C9 Internal control is effective A C B B

10 Tracking surveys are in use, or are unnecessary B C B C

RECONCILIATION11 Satisfactory reconciliation of fiscal and banking records is undertaken routinely A B B B

REPORTINGIN-YEAR REPORTING

12 Internal fiscal repots are received within four weeks of the end of the relevant period B C B C13 Good-quality classification of poverty reducing spending is reflected in the in-year budget reports A C C C

FINAL AUDITED ACCOUNTS14 Routine transactions are entered into the main accounting system (s) within two months of the end of the fiscal year A A B C15 An audited record of the financial outturn is presented to the legislature within twelve months of the end of the fiscal year B C B C

NEWPROCUREMENT

16 The procurement system supports efficiency and effectiveness in the expenditure of public funds through clear A Band enforceable rules that promote competition, transparency and value for money.

3 5 4

Notes: Please shade cells in cases where the assessed indicator meets or exceeds the standard benchmark level

Table 1: Public Expenditure Management AAP Indicators in Bolivia

ASSESSMENT

TOTAL NUMBER OF BENCHMARKS MET

Dates DatesWORLD BANK 2004 2005

2004 200520042004200320032004

IMF 200420042005

IDB 200420032003

CAF Support to the Economic Government Plan (Tax Administration Reform) 2003 20052003

CANADA 2003 200520032003

USAID 2003 200420032003

Others 20052005

* Within the last 12 months**List of TA providers in PEM

Support to the CGR

Civil Service Public Administration

Social Sectors Programmatic Credit (support to SIGMA)

Support to the Economic Government Plan (Hydrocarbon Tax Administration)

Strengthening of Municipal Administration II Strengthening of Municipal Administration IIIAnti-corruption National Office

DescriptionPublic Expenditure Review - Joint with IDB

Social Sectors Programmatic CreditSocial Safety Net Structural Adjustment Credit

Country Financial Accountability Assessment

Table 2: Overview of Technical and Donor Assistance in Public Expenditure Management in Bolivia

Fiscal Decentralization (Germany)

DescriptionDonor/ Provider**RECENT*/ONGOING assistance by major project PLANNED assistance by major project

Support to the Decentralization Committee of the Congress

Institutional Reform Project (Denmark, Sweden, Netherlands, WB)

Fiscal Sustainability Sectoral Project (support to SIGMA)

Subnational Government Reform

Public Expenditure Management ModernizationImplementation of Recent Tax Reform MeasuresCommittee of Sponsoring Organizations, COSO Mission

Study on Determinants of the Fiscal Structural Balance

PRSP Monitoring and Dissemination (UK)Budget Formulation (Belgium)

Anticorruption National Office

Transparency National Program (UK, Netherlands, Sweden, Denmark)

Social Protection FrameworkPoverty Social Impact Analysis

Public Expenditure Review - Joint with WBFiscal Sustainability Sectoral Program

Second Programmatic Structural Adjustment Credit

Relates to Timing Status DateIndicator² (S/M)³ (FI/II/NS)* Achieved**

1 Development of a medium-term expenditure framework. 7 M NS4 Not implemented due to the critical fiscal situation 2 Facilitate systematic incorporation of PDMs and POAs into budget allocation decisions. 1 M II Most of municipalities are using PDMs and POAs to

formulate their budgets.3 Introduce reforms on budget formulation 3 M NS4 Not implemented due to the critical fiscal situation

and the political/economic and social crisis.

4 Publication of the Government's Inter.-sectoral and sectoral policy priorities in advance of preparing the annual budget.

3 M NS4 Not implemented due to the critical fiscal situation and the political/economic and social crisis.

5 Development of effective institutional mechanism . 3 M NS4 Timid advances in few public institutions (IRS and Road National Service).

6 Budgeting, (and subsequent) execution of expenses at all levels of the Government following the classification of poverty-related expenses established in the PRSP.

6 S FI 2003

7 Implementing a systematic procedure for budgeting, execution of expenses at all levels of thGovernment following the classification of poverty-related expenses established in the PRSP.

6 M II Few advances in introducing poverty-related classification of expenditures.

N

1 Cashed management based on quarterly quotas with a simultaneous introduction of an obligations-based accounting practice at first to those agencies that meet the IRP criteria for operational decentralization.

8 M FI 2003

2 Introduction of cuotas de pago. 8 M FI 2003 3 Improvement in the inter-governmental transfers system. 8 M II The implementation of reforms has been delayed due

to political problems.4 Strengthen internal and external audit developing a traditional financial control system and

non-traditional measures for performance evaluation. 9 M NS4 Not implemented, reforms are pending

5 Introduce reforms on budget execution. 8 M NS4 Not implemented due to the critical fiscal situation N

1 Enhance of social oversight groups. 12 M II Partially implemented reform efforts continue2 SIGMA implementation throughout 91 municipal Governments (12 large, 39 medium and 4

small).12 M II Implementation delays due to political instability,

changes in personnel and restrictions of financing sources.

3 Budgeting reporting of expenses at all levels of the government following the classification of poverty-related expenses established in the PRSP.

13 S FI 2003

4 Full implementation of SIGMA system in the Central Government, Prefecturas including all decentralized institutions of the Government (e.g., superintendencias, Customs, Roads Service)

12 S II Delays in the Central Government implementation program SIGMA implementation just started in prefectures.

5 Raise of municipal accounting and reporting standards. 12 S II Partially implemented reform efforts continue6 Establish bridging mechanism for tracking poverty-related expenditures. 13 S FI 20037 Publication of historical series of budget outturns, with functional classification. 13 M FI 2003

8 Development of effective institutional mechanism . 15 M NS Not implemented due to the critical fiscal situation and the political/economic and social crisis.

9 Implementing a systematic procedure for budgeting reporting of expenses at all levels of the government following the classification of poverty-related expenses established in the PRSP.

13 M II The GOB has manually produced a classification of public expenditure related with poverty reduction

N

12N

team should update the status for all other actions)**Date achieved for FI reflects the action status in the March 2003 Board Paper.

Table 3: Implementation Status of Actions to Strengthen Tracking of Poverty-Reducing Public Spending: Bolivia

# Actions¹ Comments***

Actions to strengthen budget formulation

Actions to strengthen budget execution

Actions to strengthen financial reporting

Actions to strengthen public procurement

*** Comments may explain any changes in the nature of proposed actions or changes to the timing of their implementation.

¹Actions reflect the descriptions held by FAD-PREM in the March 2003 Board Paper and should relate to the earlier action plans developed in prior AAPs.² Show to which of the 16 indicators from the AAP the action chiefly relates.³ S=Short term action (within 12 months of action); M=medium term action.

* FI=fully implemented, II=Implementation initiated, NS=Not started (FI in blue reflects status as FI at the time of March 2003 board paper. Mission

4 The implementation of this actions was initiated at the time of the last AAP (March 2003), however they have been indefinitely postponed due the new GOB is much more realisticin terms of future actions in a context with strong social and political constrains

No.* Action **Relates to

indicator no.TA

Provider*** No.* Action**Relates to