FOR OFFICIAL USE ONLY Report No. 11096-TR...

83

Document of The World Bank Group FOR OFFICIAL USE ONLY Report No. 11096-TR INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL FINANCE CORPORATION MULTILATERAL INVESTMENT GUARANTEE AGENCY COUNTRY PARTNERSHIP FRAMEWORK FOR THE REPUBLIC OF TURKEY FOR THE PERIOD FY18-FY21 July 28, 2017 Turkey Country Management Unit Europe and Central Asia The International Finance Corporation Europe and Central Asia The Multilateral Investment Guarantee Agency This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank Group authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of FOR OFFICIAL USE ONLY Report No. 11096-TR...

Document of The World Bank Group

FOR OFFICIAL USE ONLY

Report No. 11096-TR

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL FINANCE CORPORATION

MULTILATERAL INVESTMENT GUARANTEE AGENCY

COUNTRY PARTNERSHIP FRAMEWORK

FOR

THE REPUBLIC OF TURKEY

FOR THE PERIOD FY18-FY21

July 28, 2017 Turkey Country Management Unit Europe and Central Asia The International Finance Corporation Europe and Central Asia The Multilateral Investment Guarantee Agency

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank Group authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

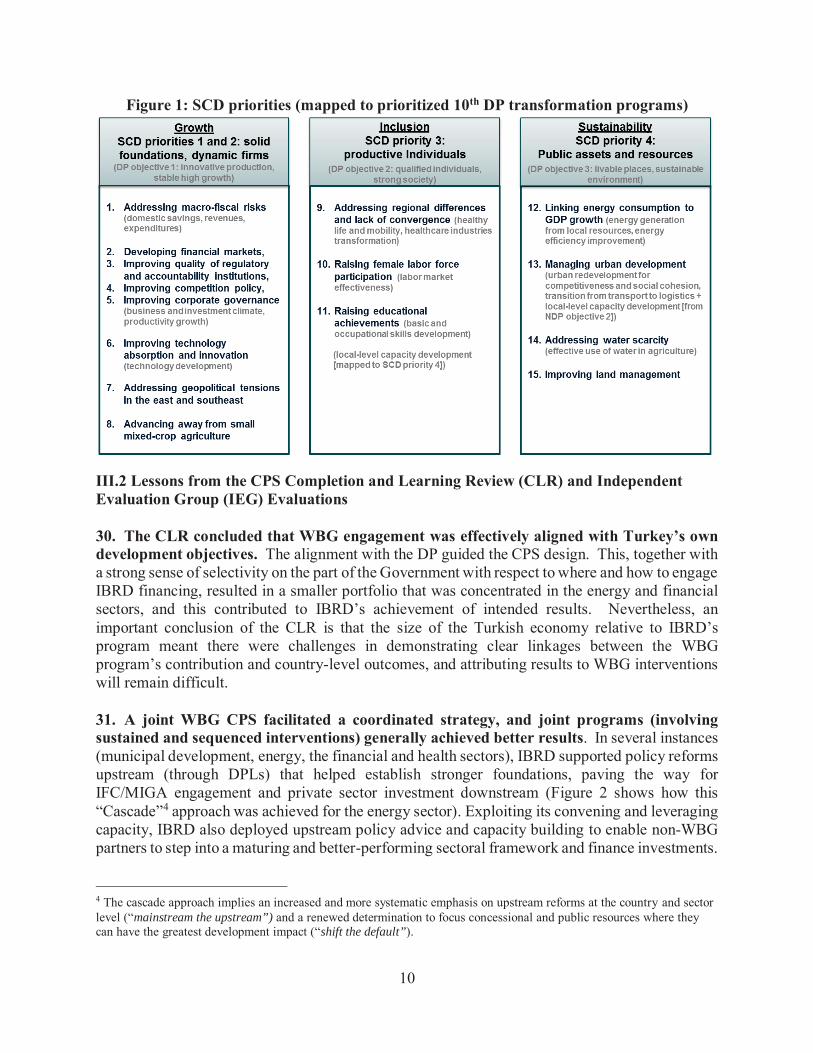

e A

utho

rized

Pub

lic D

iscl

osur

e A

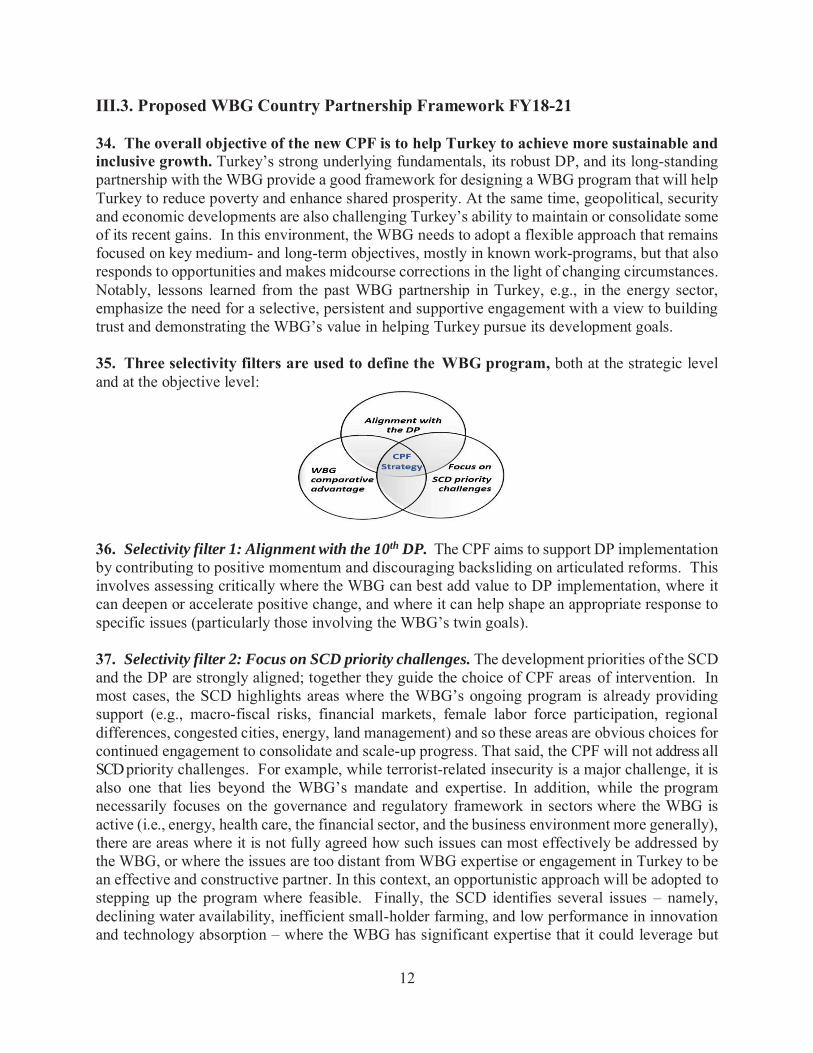

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

CURRENCY EQUIVALENTS Exchange Rate Effective July 28, 2017

Currency Unit 1 TL = 3.56 US$

FISCAL YEAR January 1 – December 31

ABBREVIATIONS AND ACRONYMS

ASA Advisory Services and Analytics IFC International Finance Corporation B40 Bottom 40 percent of the population IFI International Financial Institution

BOTAS Boru Hatlari ile Petro Tasima A.S. IMF International Monetary Fund CEM Country Economic Memorandum IPA Instrument for Pre-Accession CLR Completion and Learning Review IPARD Instrument for Pre-Accession in Rural Development CPF Country Partnership Framework MIGA Multilateral Investment Guarantee Agency CPS Country Partnership Strategy MSME Micro, Small, and Medium Enterprises CTF Clean Technology Fund NBFI Non-Bank Financial Institution DP Development Program NCD Non-Communicable Disease

DPL Development Policy Loan NPL Non-Preforming Loan DPO Development Policy Operation OECD Organization for Economic Co-operation and

Development EBRD European Bank for Reconstruction and Development OIZ Organized Industrial Zones

EC European Commission PforR Program for Results ECA Europe and Central Asia PISA Program for International Student Assessment

ESMAP Energy Sector Management Assistance Program PLR Performance and Learning Review EU European Union PPP Public-Private Partnership

EUR Euro RAS Reimbursable Advisory Services FDI Foreign Direct Investment SCD Systematic Country Diagnostic FSA Financial Sector Assessment SIDA Swedish International Development Agency FRiT Facility for Refugees in Turkey SOE State-Owned Enterprise FY Fiscal Year SORT Systematic Operations Risk-rating Tool

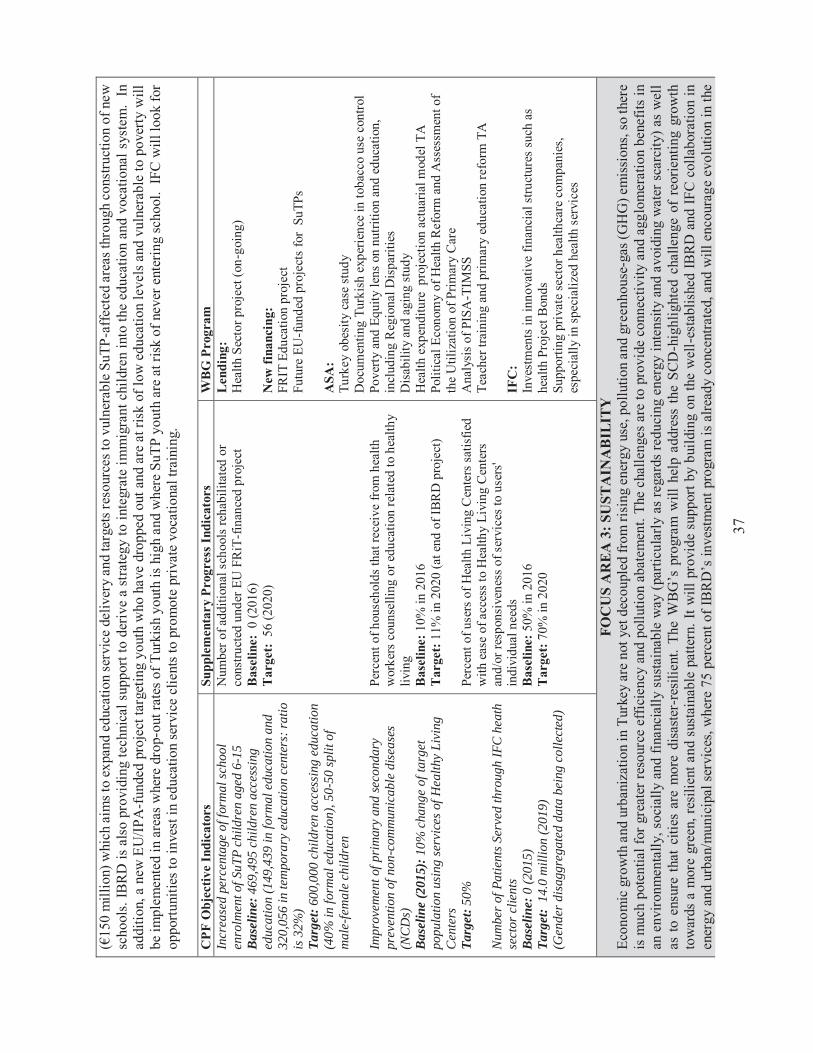

FSRU Floating Storage and Regasification Unit SuTP Syrians under Temporary Protection GDP Gross Domestic Product TA Technical Assistance GEF Global Environment Facility TANAP Trans-Anatolian Pipeline

GFDRR Global Facility for Disaster Reduction and Recovery TIMSS Trends in International Mathematics and Science Studies GHG Greenhouse Gas WB The World Bank IBRD International Bank for Reconstruction and Development WBG The World Bank Group ICT Information and Communication Technology

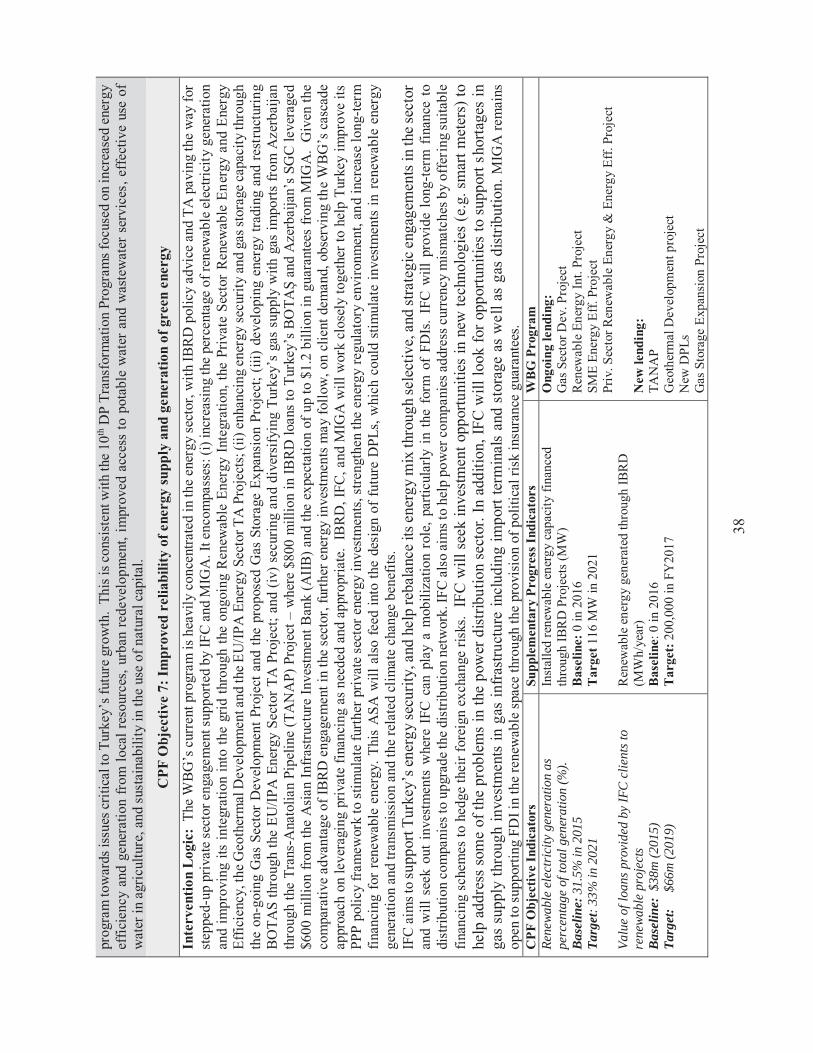

IBRD IFC MIGA Vice President: Director: Task Team Leader: Core Team Members:

Cyril E. Muller Johannes Zutt Eavan O’Halloran Ximena Del Carpio, Tamara Sulukhia, Alper Ahmet Oguz, P. Facundo Cuevas, Tunya Celasin, Donato de Rosa, Pinar Yasar

Dimitris Tsitsiragos Tomasz Telma George Konda, Aisha Williams, Enrique Lora

Keiko Honda Merli Baroudi Gianfilippo Carboni

iii

TURKEY COUNTRY PARTNERSHIP FRAMEWORK

Table of Contents I. INTRODUCTION .................................................................................................................. 1

II. COUNTRY CONTEXT AND DEVELOPMENT AGENDA ................................................... 1

II.1 Social and Political Context ................................................................................................. 1

II.2 Recent Economic Developments and Prospects .................................................................. 3

II.3 Poverty and Shared Prosperity ............................................................................................. 6

II.4 Development Challenges...................................................................................................... 7

III. WORLD BANK GROUP PARTNERSHIP FRAMEWORK .................................................. 9

III.1. Government’s Program and Medium-term Strategy .......................................................... 9

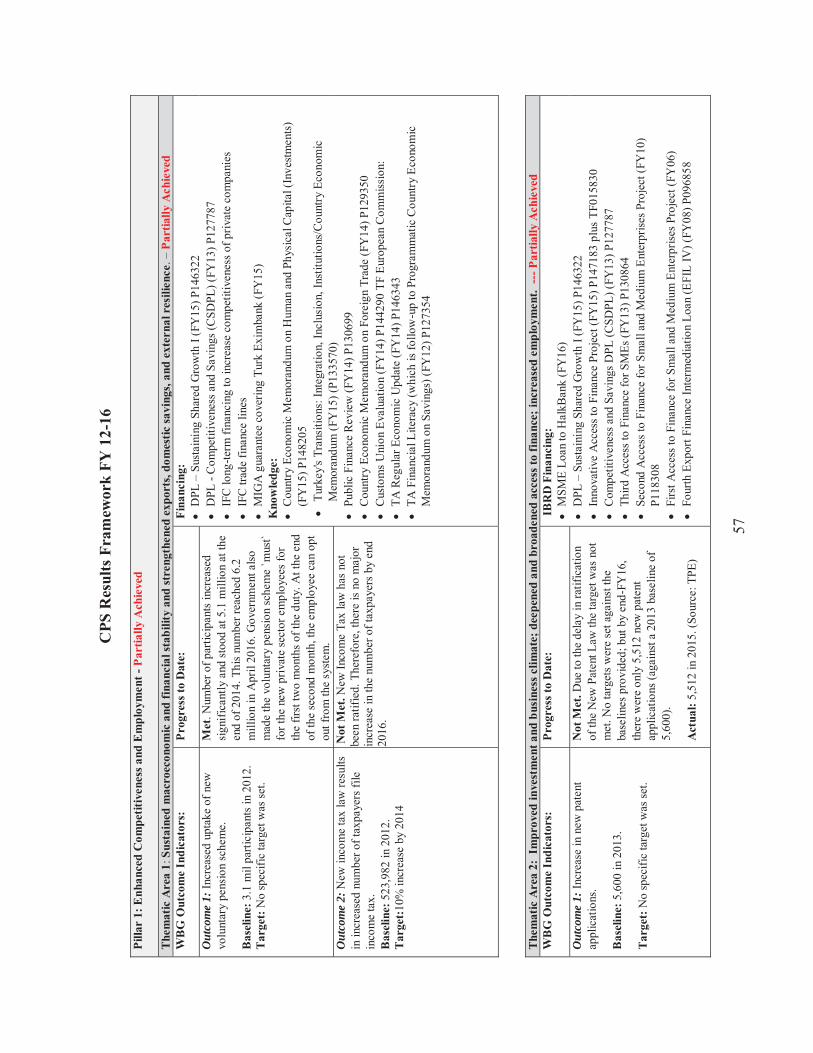

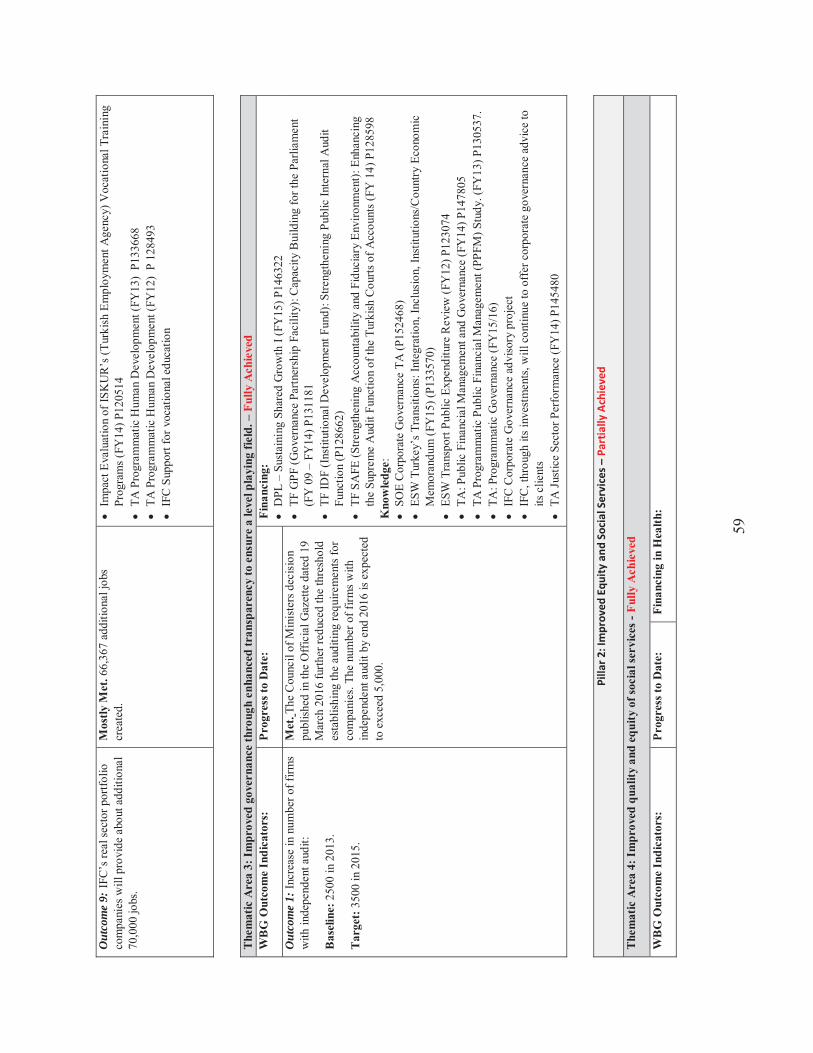

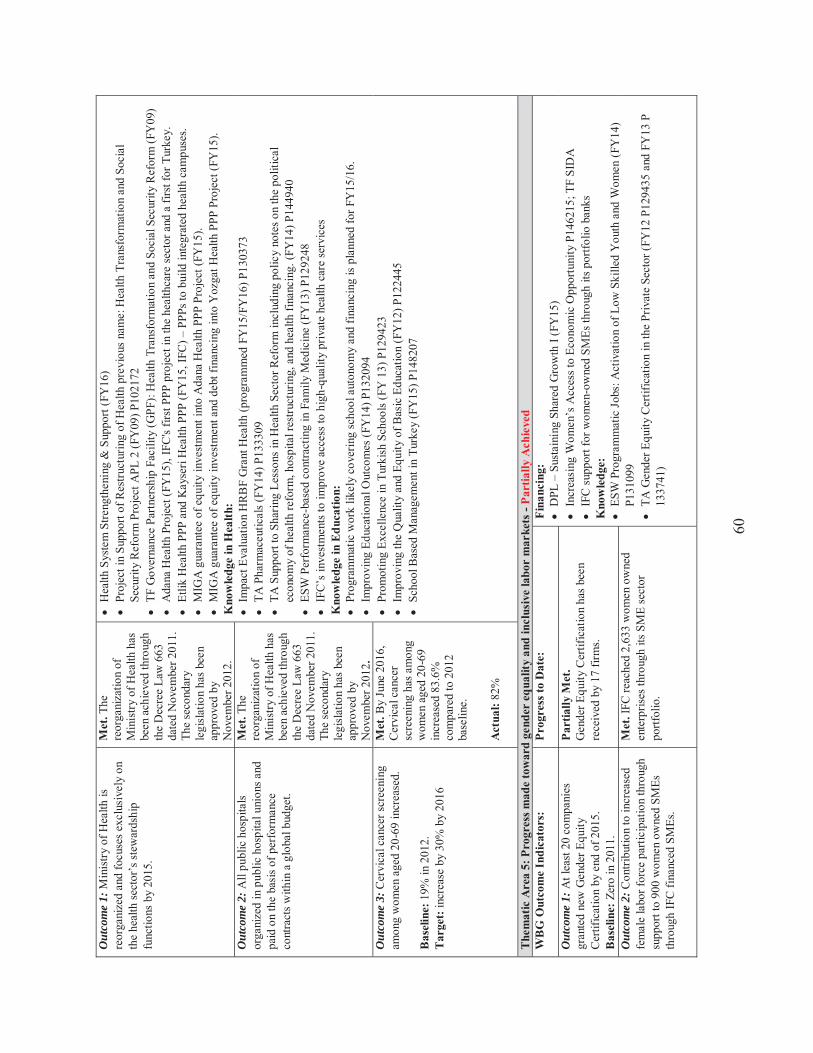

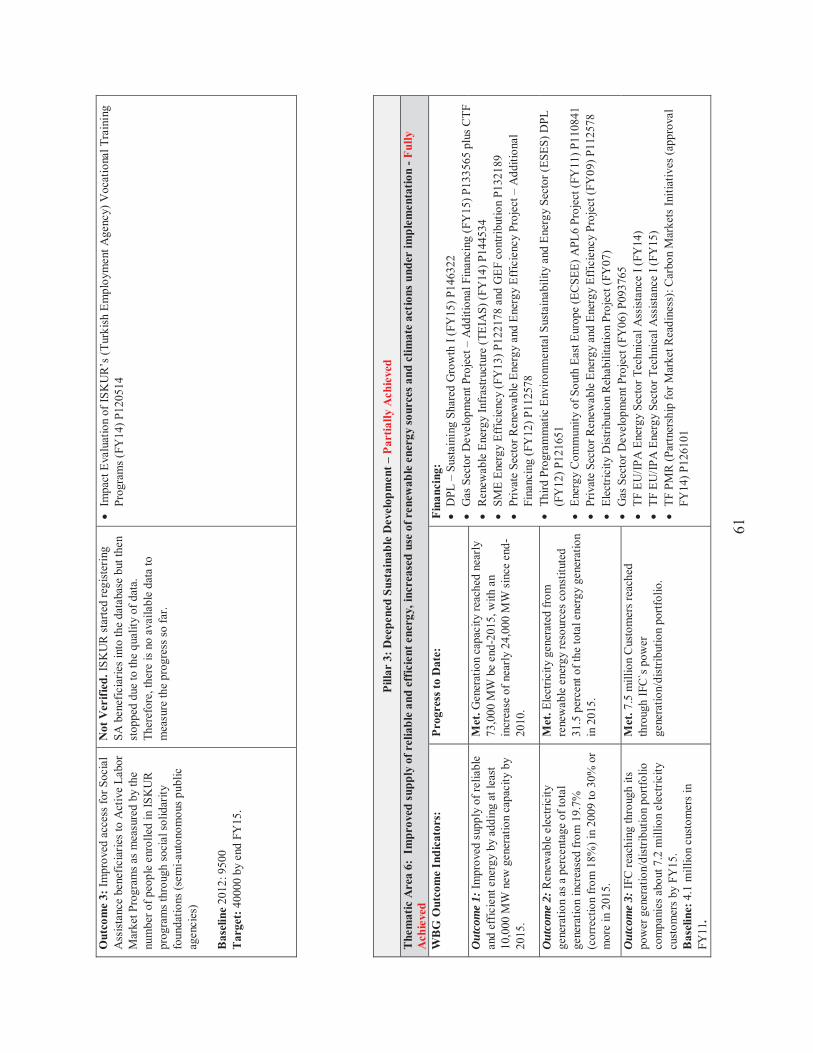

III.2 Lessons from the CPS Completion and Learning Review (CLR) and Independent Evaluation Group (IEG) Evaluations ........................................................................................ 10

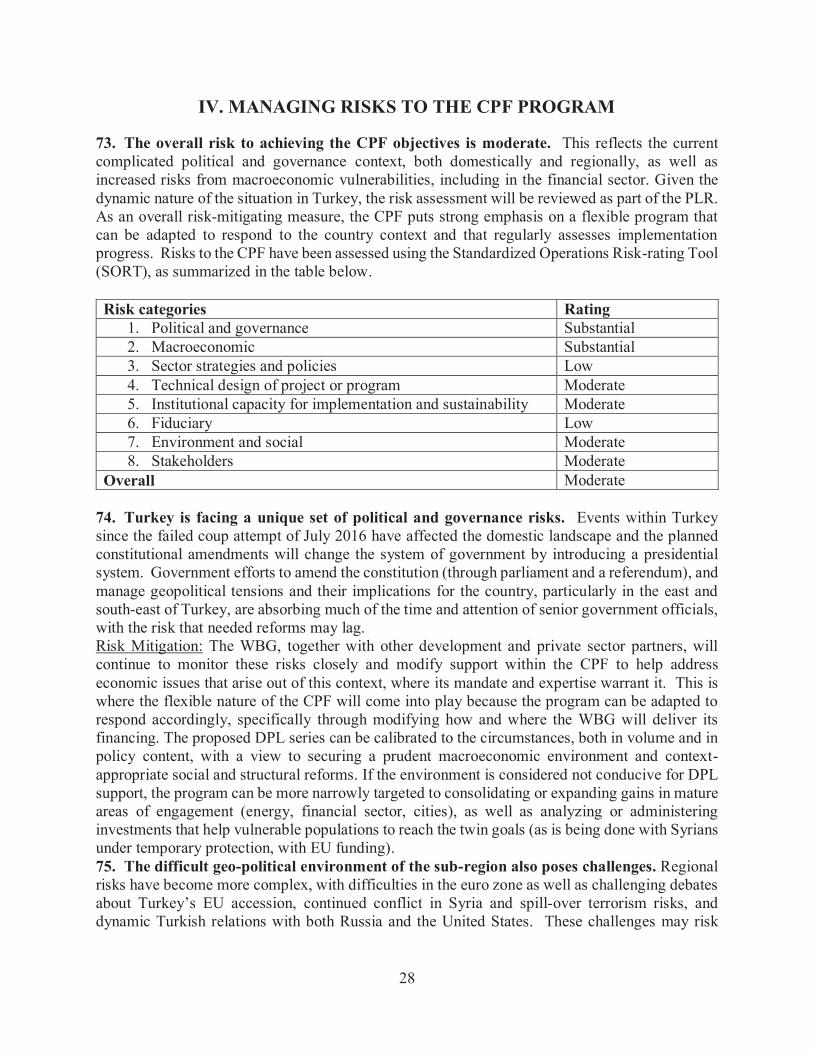

III.3. Proposed WBG Country Partnership Framework FY18-21 ............................................ 12

III.4 Implementing the FY18-21 Country Partnership Framework .......................................... 25

IV. MANAGING RISKS TO THE CPF PROGRAM .................................................................. 28

Annex 1. CPF Results Matrix ...................................................................................................... 31

Annex 2. CPS (FY12-FY16) Completion and Learning Review Report ..................................... 43

Annex 3. Selected Indicators of Bank Portfolio Performance and Management ........................ 70

Annex 4. Operations Portfolio (IBRD/IDA and Grants) .............................................................. 71

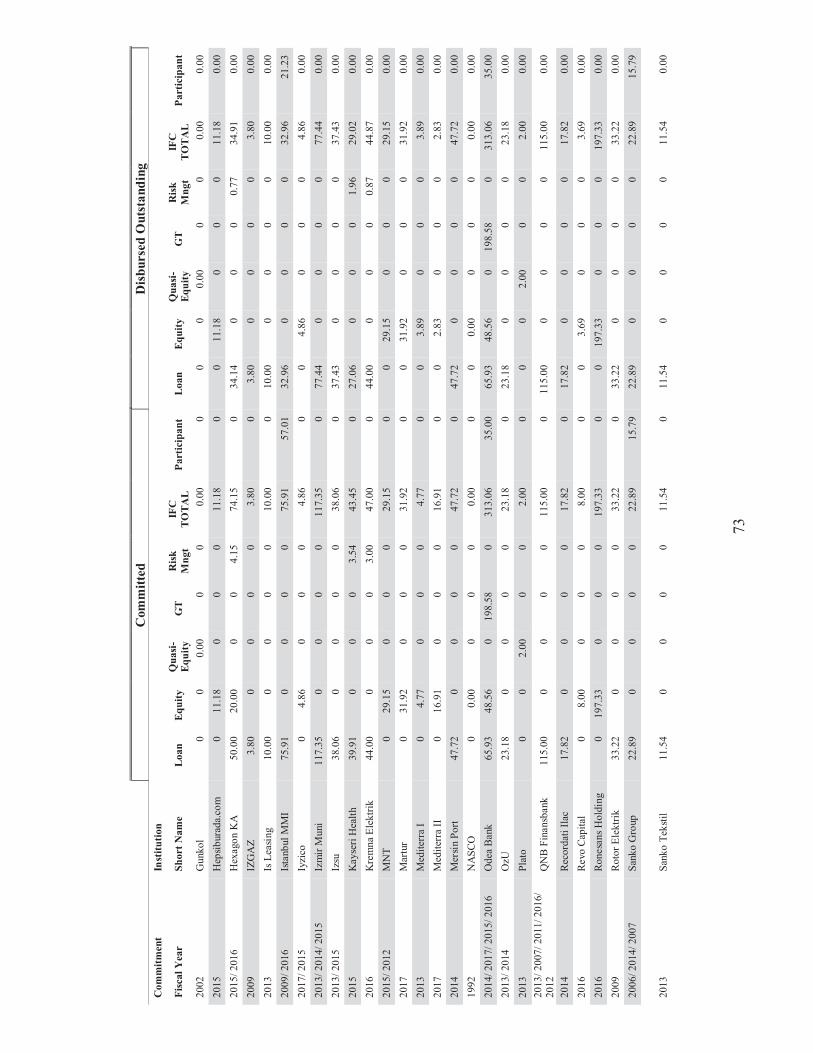

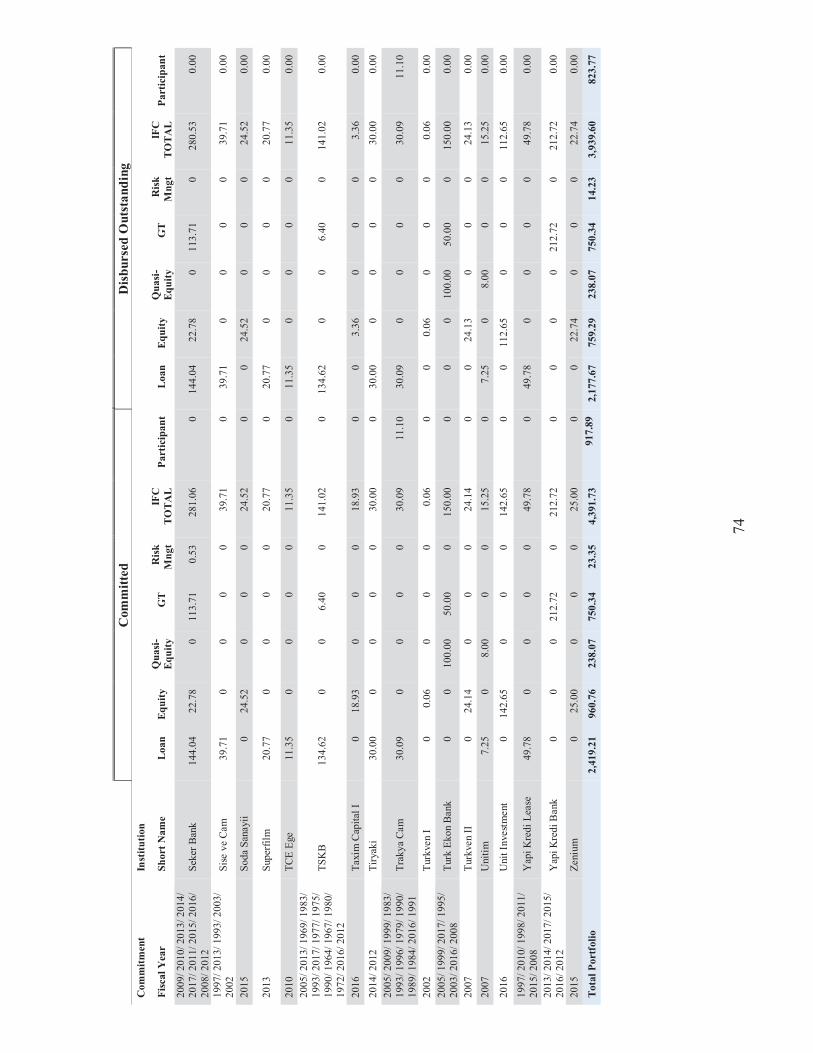

Annex 5. Statement of IFC’s Held and Disbursed Portfolio ........................................................ 72

Annex 6. MIGA Active Guarantees.............................................................................................. 75

Annex 7. Summary note of Country Gender Assessment 2016 ................................................... 76

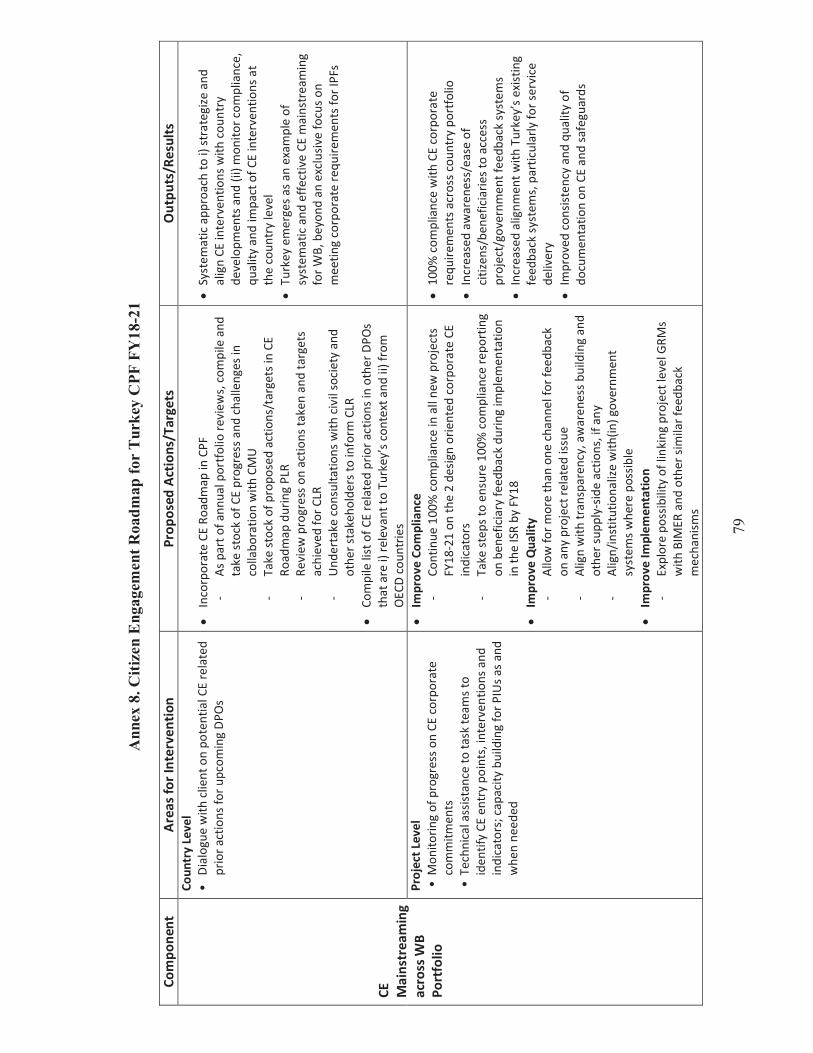

Annex 8. Citizen Engagement Roadmap for Turkey CPF FY18-21 ............................................ 79

1

COUNTRY PARTNERSHIP FRAMEWORK FOR TURKEY (FY18-21)

I. INTRODUCTION

1. This Country Partnership Framework (CPF) for Turkey covers the period FY18-21. It is aligned with the objectives of Turkey’s 10th Development Plan and is based on the findings of a World Bank Group (WBG) Systematic Country Diagnostic (SCD) that was finalized in February 2017. The CPF aims to help Turkey to achieve its development objectives through building on the foundations of the existing program and consolidating gains in key areas where the WBG is already active, as well as developing the program further in areas which target the WBG twin goals of reducing extreme poverty and boosting shared prosperity. The CPF puts forward a flexible approach for the WBG’s program that is appropriate for a middle-income country of Turkey’s size and takes account of the evolving country and regional situation. 2. The choice of CPF priorities and objectives was informed by a broad consultative approach undertaken both in the preparation of the SCD and of the CPF. The SCD was prepared following several rounds of discussions with Turkey experts, academia, private sector, investors, and civil society actors. The CPF benefited from strategic consultations with Government on the role of the WBG in Turkey for the CPF period that allowed for alignment of the program with client demand. It also benefited from discussions with a variety of stakeholders, private sector representatives and development partners whose feedback was incorporated into the design of the CPF.

II. COUNTRY CONTEXT AND DEVELOPMENT AGENDA

II.1 Social and Political Context 3. Turkey has achieved commendable economic and social development results since the early 2000s, raising it to the world’s 17th largest economy and establishing it as a global presence. Macroeconomic stability, financial sector reform, closer economic ties with the European Union (EU), and a transformation of a significant part of the economy away from agriculture into manufacturing and services were core contributors to Turkey’s growth. Broad reforms supported a dynamic private sector, opened the country to foreign trade, incentivized significant infrastructure investments and resulted in higher incomes as well as increasing convergence of social indicators to OECD norms. Turkey’s GNI per capita rose from $3,115 in 2001 to $11,000 in 2015: poverty incidence more than halved and extreme poverty fell even more dramatically. Turkey’s development successes have been justifiably lauded, with many countries looking to its development model for inspiration. 4. Going forward, Turkey is facing political, security and economic challenges. In recent years, various commonly-accepted indicators of the quality of a country’s institutions (including Doing Business, the Corruption Perceptions Index, and the World Economic Forum’s Competitiveness Index) have shown that Turkey remains below the levels obtained in high-income countries, and that the distance from the frontier has been widening. Since early 2015, the country

2

has also experienced a series of political challenges, including a long election cycle (with parliamentary elections in both June and November 2015), a Cabinet reshuffle in May 2016, and a failed coup attempt in July 2016. Following the failed coup attempt, the government decreed a state of emergency to undertake what it has described as counter-terrorism measures, including the dismissal of civil servants and the transfer of assets of some entities that it has found to be linked with terrorist organizations. In April 2017, voters approved a set of constitutional reforms that will create an executive presidency and bring about important changes in the relations between Government branches.

5. Regional dynamics and impacts from the Syrian conflict are also imposing significant challenges. The government of Turkey is hosting about three million Syrians who have the status of Syrians under Temporary Protection (SuTPs). Turkey is providing for the SuTPs under its own laws and mostly at its own expense, including registration, freedom of movement, housing, health and education services and prospects for legal employment (less than ten percent of SuTPs are hosted in camps). Despite this commendable approach, the presence of such a large number of SuTPs is creating pressures on services and the labor market. At the same time, the geopolitical turmoil in the Middle East region and its implications for the east and south-east of Turkey have affected local economies in some regions, depressed tourism and discouraged investment.

6. Turkey’s relationship with the EU is characterized by peaks and troughs. It has benefited significantly from EU economic ties since the 1995 customs union agreement. In 2005, it initiated EU accession negotiations, which provided an anchor for its reform path and a strong positive indicator of its long-term aspirations. Although the EU negotiations have slowed down since the early 2010s, two new chapters in the accession process were opened in 2015/16. In late 2015, the crisis resulting from high numbers of SuTPs crossing from Turkey into Europe appeared to provide an incentive for quicker progress. Turkey agreed to work further with the EU to stem the transit of irregular migration to Europe, while the EU agreed to admit SuTPs from Turkey via a humanitarian admission scheme, accelerate the updating of the Customs Union, the EU negotiation process and the possibility of Turkish visa-free access to the EU. The EU also pledged €6 billion in assistance to host SuTPs in Turkey. While the irregular crossings from Turkey to Greece have greatly decreased and €3 billion in EU support was committed, progress on visa-free access to the EU Schengen Area for Turkish citizens and developing the Voluntary Humanitarian Admission Scheme for resettlement of SuTPs to the EU has remained slow. Even so, because the EU remains Turkey’s largest trading and development partner, taking about half of exports, harmonization to EU trade and investment standards will continue to dominate Turkey’s reform agenda. 7. Even within this challenging environment, Turkey’s development foundations remain sound. Sitting at the crossroads of Asia and Europe, with a dynamic private sector and young population, and access to the EU, Turkey continues to attract global investors. Strong macro-economic management enabled Turkey to weather the global financial crisis relatively well. But past achievements are no guarantee of future success. How well it copes with its current political, social and economic challenges will determine how much foreign and domestic investment it continues to attract, and when it will achieve its aspiration to become a high-income country.

3

II.2 Recent Economic Developments and Prospects

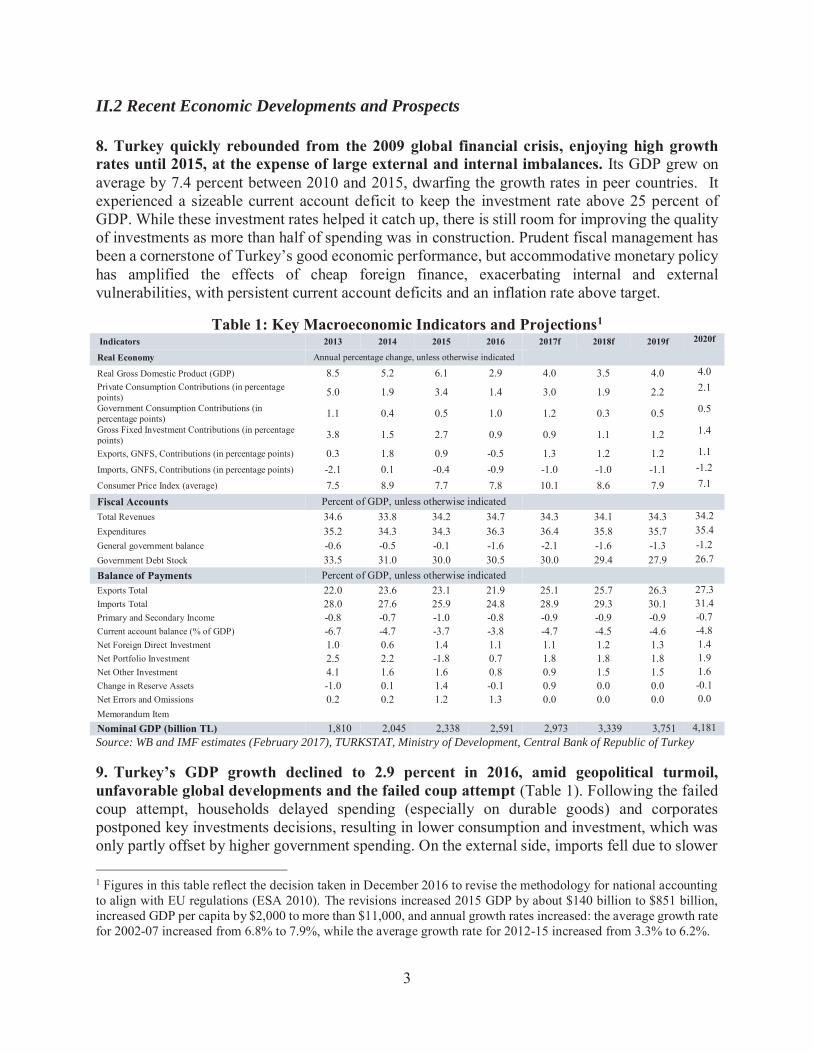

8. Turkey quickly rebounded from the 2009 global financial crisis, enjoying high growth rates until 2015, at the expense of large external and internal imbalances. Its GDP grew on average by 7.4 percent between 2010 and 2015, dwarfing the growth rates in peer countries. It experienced a sizeable current account deficit to keep the investment rate above 25 percent of GDP. While these investment rates helped it catch up, there is still room for improving the quality of investments as more than half of spending was in construction. Prudent fiscal management has been a cornerstone of Turkey’s good economic performance, but accommodative monetary policy has amplified the effects of cheap foreign finance, exacerbating internal and external vulnerabilities, with persistent current account deficits and an inflation rate above target.

Table 1: Key Macroeconomic Indicators and Projections1 Indicators 2013 2014 2015 2016 2017f 2018f 2019f 2020f

Real Economy Annual percentage change, unless otherwise indicated

Real Gross Domestic Product (GDP) 8.5 5.2 6.1 2.9 4.0 3.5 4.0 4.0 Private Consumption Contributions (in percentage points) 5.0 1.9 3.4 1.4 3.0 1.9 2.2 2.1

Government Consumption Contributions (in percentage points) 1.1 0.4 0.5 1.0 1.2 0.3 0.5 0.5

Gross Fixed Investment Contributions (in percentage points) 3.8 1.5 2.7 0.9 0.9 1.1 1.2 1.4

Exports, GNFS, Contributions (in percentage points) 0.3 1.8 0.9 -0.5 1.3 1.2 1.2 1.1

Imports, GNFS, Contributions (in percentage points) -2.1 0.1 -0.4 -0.9 -1.0 -1.0 -1.1 -1.2

Consumer Price Index (average) 7.5 8.9 7.7 7.8 10.1 8.6 7.9 7.1

Fiscal Accounts Percent of GDP, unless otherwise indicated Total Revenues 34.6 33.8 34.2 34.7 34.3 34.1 34.3 34.2 Expenditures 35.2 34.3 34.3 36.3 36.4 35.8 35.7 35.4 General government balance -0.6 -0.5 -0.1 -1.6 -2.1 -1.6 -1.3 -1.2 Government Debt Stock 33.5 31.0 30.0 30.5 30.0 29.4 27.9 26.7 Balance of Payments Percent of GDP, unless otherwise indicated Exports Total 22.0 23.6 23.1 21.9 25.1 25.7 26.3 27.3 Imports Total 28.0 27.6 25.9 24.8 28.9 29.3 30.1 31.4 Primary and Secondary Income -0.8 -0.7 -1.0 -0.8 -0.9 -0.9 -0.9 -0.7 Current account balance (% of GDP) -6.7 -4.7 -3.7 -3.8 -4.7 -4.5 -4.6 -4.8 Net Foreign Direct Investment 1.0 0.6 1.4 1.1 1.1 1.2 1.3 1.4 Net Portfolio Investment 2.5 2.2 -1.8 0.7 1.8 1.8 1.8 1.9 Net Other Investment 4.1 1.6 1.6 0.8 0.9 1.5 1.5 1.6 Change in Reserve Assets -1.0 0.1 1.4 -0.1 0.9 0.0 0.0 -0.1 Net Errors and Omissions 0.2 0.2 1.2 1.3 0.0 0.0 0.0 0.0 Memorandum Item Nominal GDP (billion TL) 1,810 2,045 2,338 2,591 2,973 3,339 3,751 4,181 Source: WB and IMF estimates (February 2017), TURKSTAT, Ministry of Development, Central Bank of Republic of Turkey 9. Turkey’s GDP growth declined to 2.9 percent in 2016, amid geopolitical turmoil, unfavorable global developments and the failed coup attempt (Table 1). Following the failed coup attempt, households delayed spending (especially on durable goods) and corporates postponed key investments decisions, resulting in lower consumption and investment, which was only partly offset by higher government spending. On the external side, imports fell due to slower 1 Figures in this table reflect the decision taken in December 2016 to revise the methodology for national accounting to align with EU regulations (ESA 2010). The revisions increased 2015 GDP by about $140 billion to $851 billion, increased GDP per capita by $2,000 to more than $11,000, and annual growth rates increased: the average growth rate for 2002-07 increased from 6.8% to 7.9%, while the average growth rate for 2012-15 increased from 3.3% to 6.2%.

4

domestic demand, and exports contracted due to weaker external demand and volatility in economic ties with some trading partners. The non-agricultural unemployment rate rose from 12.1 percent in January 2016 to 14.3 percent in December 2016. 10. The current account deficit slightly increased to 3.8 percent of GDP in 2016, mostly due to falling tourism revenues and has started to widen in 2017 along with the rebound in global oil prices. The current account deficit declined from 6.7 percent of GDP in 2013 to 3.7 percent of GDP in 2015, thanks to cyclical factors, such as an increased gold balance and a smaller energy bill owing to the collapse of global oil prices. While the core balance remained mostly flat due to weaknesses in Turkey’s main trading partners, the services balance deteriorated due to substantially lower tourism revenues resulting from security concerns and Russian sanctions. This offset the improvement in the energy bill, increasing the current account deficit to 3.8 percent of GDP in 2016. In 2017, the energy and gold excluded trade deficit has started to narrow, thanks to strengthening growth in the EU. Going forward, possible rising energy prices are expected to lead to a larger current account deficit in the medium-term. 11. Portfolio outflows from the bond market accelerated in late 2016, due to domestic and external factors but recovering modestly in 2017. The result of the United States (US) presidential election and anticipation that the Federal Reserve will increase interest rates faster than originally expected decreased global risk appetite, triggering outflows from most developing countries. In Turkey, slowing GDP growth, rising inflation, a widening current account deficit and the unorthodox response of the Central Bank to a depreciating lira triggered investor concerns. Against this backdrop, outflows (non-residents) from the bond market amounted to $3.2 billion in Q4, while the equity market witnessed marginal inflows. The outflows increased the benchmark 2-year government bond yield by more than two percentage points, to 11.15 percent, while the lira depreciated by more than 25 percent between the end of Q3 and the end of January 2017. Improvements in global risk appetite have triggered capital inflows to developing economies in 2017, with inflows into the Turkish bond market amounting to $1.7 billion in January-April. 12. Monetary policy decisions in the past three years have allowed inflation consistently to exceed the central bank’s 5 percent target. A-sharp increase in food prices, persistent depreciation of the lira, and accommodative monetary policy kept inflation well above the target in 2014 and 2015. In 2016, inflation reached 8.5 percent, with lower food inflation offset by tax increases on cars and tobacco products and higher transport and energy prices. The foreign-exchange pass-through associated with rapid lira depreciation, higher global energy prices and unfavorable weather conditions fed into prices and pushed headline inflation to 11.9 percent and core inflation to 9.4 percent by April 2017. In May, headline inflation slightly declined to 11.7 percent. Inflation is likely to hover in low double-digit levels throughout the year 2017.

13. Rapid depreciation of the lira prompted the central bank to increase interest rates in 2016-17. The central bank started simplifying its complex unorthodox monetary policy framework in March 2016 and narrowed the width of its interest rate corridor by cutting the overnight lending rate by 250 bps through September, but it followed an expansionary rather than neutral approach. Following rapid depreciation of the lira in late 2016, it reversed course and increased the 1-week repo and overnight lending rates by 50 bps and 100 bps, respectively, over November to January, and also returned to its previous policy framework. In January 2017, avoiding an outright hike in

5

the policy rate, it ceased 1-week repo auctions and provided funding at the overnight lending rate at 9.25 percent and a late liquidity window rate at 11 percent in order to support the lira. The Central Bank further increased the late liquidity window rate to 11.75 percent in March and to 12.25 percent in April, taking into account the upward trend in inflation. Market watchers continue to seek a more orthodox policy framework to restore confidence, stem lira depreciation, and maintain price and financial stability. 14. Fiscal policy provided a considerable stimulus to growth in 2016 and 2017. While the Government maintained fiscal discipline in 2012-2015, with the central government budget deficit averaging 1.0 percent of GDP and the primary surplus averaging 1.5 percent, central government expenditures grew by 15.4 percent in 2016, due to increases in wages, transfers, and purchases of goods and services. A fall in capital spending and interest expenditures as a share of GDP helped to contain the increase in total expenditures. Despite lower economic activity, revenues grew by 14.8 percent because of tax restructuring and amnesties. As a result, the central government budget posted a moderate deficit of 1.1 percent of GDP in 2016, in line with fiscal targets. Expansionary fiscal policy will likely lead budget balances to exceed fiscal targets in 2017, while the growing PPP portfolio will warrant closer monitoring. 15. GDP growth is projected to increase to 4 percent in 2017 and remain at 4 percent in the medium term. In 2017, growth is expected to be driven by consumption (triggered by fiscal measures) and by net exports. As the fiscal stimulus is assumed to be temporary, GDP growth is expected to slow to 3.5 percent in 2018, before reverting to 4 percent in 2019 and 2020 on the back of reduced economic and political uncertainty.

16. Turkey’s growth model faces challenges that are likely to keep growth subdued in the medium-term. With an expected tightening in global liquidity in the medium-term, Turkey`s large external financing requirements pose downside risks to growth. The 2016 current account deficit of 3.8 percent is expected to rise to 4.7 percent of GDP in 2017, and external debt equivalent to almost 20.3 percent of GDP is coming due by early 2018. Turkey has lost its investment grade status from all three major ratings agencies, which is likely to impact financing costs, worsen investment and consumer sentiment, and curtail investment and consumption. In an adverse scenario of tightening global liquidity, a new round of lira depreciation would put more strain on corporate balance sheets, depressing private investment and lowering GDP growth. Although banks are not allowed to hold net open currency positions, defaults in the corporate sector could also have an adverse impact on the banking sector through credit risk channels. Despite trending upward, non-performing loans (NPLs) currently are low at 3.2 percent and well-provisioned, providing comfort in case of an additional deterioration in credit quality. That said, banks have limited resources to support further loan growth, since the deposit base grows slowly, uncertainty concerning global liquidity constrains foreign borrowing, and low profitability prospects might entail additional capital injection to prevent erosion in banks’ capital adequacy. Fiscal prudency will be important in reducing internal and external imbalances in the medium term.

6

II.3 Poverty and Shared Prosperity 17. Turkey has made significant progress in reducing poverty and boosting shared prosperity. Over 2002 to 2014, the poverty rate fell from 44 percent to 18 percent (under the regional poverty line of US$5/day) and extreme poverty (US$2.50/day) fell even more rapidly, from 13 to 3.1 percent.2 Despite macroeconomic volatility and productivity differences, both moderate and extreme poverty decreased in rural and urban settings. Rural poverty went down from 54 to 33 percent, and urban poverty from 37 to 11 percent in this period. The major driver for poverty reduction was economic growth, as opposed to redistribution, with growth accompanied by more and better income generation opportunities for the low income population. 18. Turkey’s prosperity has been shared, improving the wellbeing of those at the bottom of the distribution. Shared prosperity, measured by the growth in consumption per capita of the poorest 40 percent of the population (B40), has been significant in Turkey. The annualized growth of consumption per capita of the B40 attained 4.3 percent between 2007 and 2012, close to the growth rate in consumption of the entire population. This represents a good performance compared to peer countries – better than OECD peers Mexico and Chile but lower than Russia and Brazil. 19. Despite this progress, wide differences persist between regions. Most regions have seen a reduction in poverty over time, with a general convergence trend occurring: however, the pace of progress has varied depending on the region, with some falling increasingly behind others, resulting in regions that are becoming more heterogeneous over time. The gap in GDP and poverty remains large between the prosperous West and the more challenged Southeast Anatolia. The poorest regions of the south-east now host large numbers of SuTPs and other refugees from the conflicts in neighboring Syria and Iraq. Moreover, the poorest regions have also seen significant under-investment in their abundant natural capital which, through degradation, is eroding potential pathways out of poverty and delaying economic convergence. Several incentive programs were launched to stimulate investment in these regions and the impact is expected to be seen in the near future.

20. In addition, there are large inequalities across socio-economic groups and gender. Though growth has been progressive and prosperity shared, the average income of the richest 10 percent is 13.5 times higher than the average income of the poorest 10 percent of the income distribution. This ratio is among the highest in the OECD. Inequality fell significantly for most of the 2000s, but the trend was reversed after the 2008/09 financial crisis. Moreover, women’s participation in the economy is still severely limited. While it has increased steadily in the past few years, female labor force participation remains just 33 percent, the lowest in the OECD and ECA. Turkey ranks 130th among 145 countries in the Global Gender Gap.

2 Poverty and extreme poverty are measured using the thresholds that the World Bank adopts for countries in the Europe and Central Asia (ECA) region. The poverty line is set at US$5.00 per day, and the extreme poverty line at US$2.50 per day, both in terms of 2005 purchasing power parity (2005 PPP). An individual is considered (extreme) poor if his/her expenditure per capita per day is below the (extreme) poverty line. For Turkey, expenditure data comes from the Household Budget Survey (HBS), collected by Turkey’s National Statistics Office (TUIK).

7

Summary of 2016 Country Gender Assessment (Further details in Annex 7) Turkey has substantially narrowed gender gaps in access to productive endowments and thus to economic opportunity. Between 2008 and 2013 maternal mortality rates were cut by half, secondary and tertiary education enrolment rates among women and men moved further towards convergence, and female labor force participation increased steadily. These outcomes have been partly the consequence of improvements to the legal and institutional framework for gender equality. However, despite these commendable advances, women still show systematically poorer outcomes than men across significant dimensions, and Turkey lags behind countries with similar income levels and its neighbors in this regard. Turkey ranks 130th among 145 countries according to the World Economic Forum’s “Global Gender Gap Report 2016”. Aggregate figures mask substantial socioeconomic and regional disparities, with women from vulnerable backgrounds bearing the brunt of the existing gender gaps in access to endowments and opportunity. Turkey has one of the lowest female labor force participation rates among countries with similar income levels, with only 33 percent of Turkish women economically active, compared to 62 percent on average in upper-middle-income countries. Women are also under-represented in entrepreneurship and business ownership and management, a situation related to significant socio-cultural as well as economic barriers to enter and remain in those activities. In particular, the gap in financial inclusion between men and women remains comparatively large. As an example, in 2014, 70 percent of men had formal accounts compared to only 44 percent for women. Women´s agency remains comparatively weak. At 14.9 percent in 2015, the share of female Parliamentary representatives remains well below the ECA average of 25.7 percent. The proportion of women in ministerial positions is even lower, at 4 percent, and compares poorly with the average 21.8 percent registered in ECA for 2015. At the local level the picture does not change much: a mere 4 percent of the representatives in local governing bodies are women.

II.4 Development Challenges

21. A recently-completed Systematic Country Diagnostic (SCD) identifies the key binding constraints to completing Turkey’s transition to a high income country, creating more and better jobs, reducing poverty and boosting shared prosperity sustainably. The analytical framework is structured along four main areas: (a) Solid Foundations, which looks into institutions, markets, economic and social stability; (b) Productive Individuals, which examines people’s access to skills, education, health, and economic opportunities across regions; (c) Dynamic Firms, which assesses firms’ access to financing, innovation, and investment opportunities; and (d) Public Assets and Resources, which analyzes connectivity, infrastructure, and protection of natural resources. . 22. The main challenges in the area of Solid Foundations are related to enhancing the quality of regulatory and accountability institutions; addressing the impact of geopolitical turmoil in the Middle East; developing capital markets; and mitigating macro-fiscal risks. Improving the quality of institutions will increase the ability to attract capital, promote innovation, and safeguard natural resources. A second key bottleneck is the geopolitical turmoil in the Middle East and its spillover impacts on southeast Turkey: a stable and safe environment is crucial to expand services, attract investment, create jobs and incentivize human capital accumulation. Capital markets that need deepening are a third bottleneck, contributing to gaps in formal saving and borrowing patterns, financial literacy and women’s access to financial services, and constraining the ability of small firms to expand and innovate. Fourth, Turkey faces external vulnerabilities stemming from macro-fiscal risks, including particularly a dependence on foreign savings and roll-over needs for its large stock of short-term debt; in this context, increased global risk aversion may expose Turkey to accelerating capital outflows.

8

23. In the area of Productive Individuals, the main challenges are low educational achievements, limited female economic participation, and economic and social exclusion in lagging regions. Firms can move up the value chain more effectively when they can hire tertiary education graduates and when those graduates have benefited from good-quality lower levels of education (including preschool) that provide the right cognitive and behavioural foundations. Low female labor force participation constrains economic growth and inclusion, and presents a challenge where Turkey finds more room for improvement vis-a-vis high income countries. Limited supply of affordable care for children and the elderly, and cultural norms reinforcing the patriarchal structure of the family prevailing in some regions have been constraining more active participation of women. Finally, regional economic and social inequalities persist and outcomes in lagging regions remain slow to converge to more advanced regions.

24. In the area of Dynamic Firms, a transition away from low-tech products is underway, but high-tech products currently provide only a small share of overall value-addition, and the share has been declining in recent years. Turkey has a number of well-funded programs to encourage private sector innovation. In 2016, the government adopted new legislation to provide further support, including a new R&D law, an investment climate law and an industrial property law. Nevertheless, there is room for improvement: Turkey’s low performance in technology absorption and innovation is especially visible in R&D and innovation indicators collected by the OECD. This constraint is linked with low educational achievement: poor human capital reduces the scope for innovation. It is also linked to the quality of regulatory and accountability institutions which should be improved to provide better incentives for private investment, innovation and entrepreneurship. Corporate governance as well as competition policy and its enforcement are additional crucial constraints that need to be strengthened for supporting the dynamism of Turkey’s firms. The Government has taken important steps by enacting a series of laws over the past year to incentivize R&D investment, improve the investment climate and align the industrial property framework with international standards. However, strengthening the regulatory and accountability institutions will be key to achieve success in effective implementation of these measures.

25. In the area of Public Assets and Resources, constraints relate to land, water, energy and congestion. Some cities (Istanbul and Kocaeli) are suffering from congestion, thus endangering the benefits of agglomeration which have contributed to growth and poverty reduction in the past. Financing and capital investment planning, consistent with territorial plans, is essential for sustaining urban growth. Connecting people and jobs efficiently at low environmental cost is essential for safeguarding competitiveness and sustainability. While water availability is generally sufficient now, projections for growth in water use may surpass availability by 20303 and this could put a brake on growth in agriculture and industry, while gravely affecting well-being. Improving the efficiency of energy consumption and reducing dependence on imported energy is also critical for competitiveness and sustainable economic growth. Inefficient land management affects city planning and financing of municipal infrastructure, as well as rural well-being.

3 Ministry of Forestry and Water Affairs, 2016: “Assessment of Climate Change Impact on Water Resources”, General Directorate of Water Management, Turkey.

9

III. WORLD BANK GROUP PARTNERSHIP FRAMEWORK

III.1. Government’s Program and Medium-term Strategy 26. Turkey’s overarching development goals are outlined in its 10th Development Plan (DP 2014-2018), which was launched in 2014. The 10th DP follows many of the same priorities that were pursued under the 9th DP, underscoring Turkey’s sustained commitment to a broad set of reforms and development programs. Implementation of successive DPs has been commendable. Respective DPs have traditionally formed the basis of the partnership between Turkey and the WBG, with the previous Country Partnership Strategy (CPS) (FY12-16) aligning its objectives with those of the 9th DP (covering 2007-13) and the CPS Progress Report (2014) allowing for alignment with the 10th DP objectives. 27. The DP diagnoses the key challenges that Turkey needs to overcome to escape the “middle income trap” and succeed in becoming a high-income country. It has four High Level Objectives (1) Innovative Production, Stable and High Growth (this targets macroeconomic measures, productivity improvements, energy, logistics, infrastructure and greater innovation and technological capacity); (2) Qualified Individuals and Strong Society (this focuses on social welfare, health, education, public services, and employment); (3) Livable Places and Sustainable Environment (this focuses on reducing regional disparities, promoting sustainable cities and services, and using natural resources responsibly); and (4) International Cooperation for Development (this focuses on sharing Turkey’s positive development experiences with other countries). Under the first three of these objectives is a set of 25 Transformation Programs that outline in more detail the reforms to be pursued and the types of investments to be made. Turkey also produces EU Pre-Accession Economic Reform Programs (ERP) that detail short- and medium-term policy actions and structural reform priorities related to EU accession. The last ERP covering 2017-2019 was issued in January 2017.

28. The Government remains committed to the 10th DP and its Transformation Programs. The reform path and investment priorities for these programs have been detailed and implementation is underway, with various degrees of progress depending on the program. At the same time, the WBG’s SCD shows a prioritization of development challenges that is closely aligned with DP objectives, even though the SCD is a fully independent diagnostic that did not seek alignment (see Figure 1). This confirms that the DP provides a solid foundation on which to build and, therefore, that the focus going forward should be on accelerating implementation.

29. Within the DP framework, the Government carefully considers which development partners it engages for which Transformation Programs and how that engagement is designed and delivered. With a large range of potential partners and access to financing on international markets, Turkey has traditionally engaged partners, including the WBG, in a deliberate manner, both for financing and advisory services. In preparing the DP, the government solicited the WBG’s advice generally, but requests for WBG financial support and investments have been much more selective (as noted in the Completion Learning Review -). This demand-driven approach will continue in Turkey.

10

Figure 1: SCD priorities (mapped to prioritized 10th DP transformation programs)

III.2 Lessons from the CPS Completion and Learning Review (CLR) and Independent Evaluation Group (IEG) Evaluations 30. The CLR concluded that WBG engagement was effectively aligned with Turkey’s own development objectives. The alignment with the DP guided the CPS design. This, together with a strong sense of selectivity on the part of the Government with respect to where and how to engage IBRD financing, resulted in a smaller portfolio that was concentrated in the energy and financial sectors, and this contributed to IBRD’s achievement of intended results. Nevertheless, an important conclusion of the CLR is that the size of the Turkish economy relative to IBRD’s program meant there were challenges in demonstrating clear linkages between the WBG program’s contribution and country-level outcomes, and attributing results to WBG interventions will remain difficult. 31. A joint WBG CPS facilitated a coordinated strategy, and joint programs (involving sustained and sequenced interventions) generally achieved better results. In several instances (municipal development, energy, the financial and health sectors), IBRD supported policy reforms upstream (through DPLs) that helped establish stronger foundations, paving the way for IFC/MIGA engagement and private sector investment downstream (Figure 2 shows how this “Cascade”4 approach was achieved for the energy sector). Exploiting its convening and leveraging capacity, IBRD also deployed upstream policy advice and capacity building to enable non-WBG partners to step into a maturing and better-performing sectoral framework and finance investments.

4 The cascade approach implies an increased and more systematic emphasis on upstream reforms at the country and sector level (“mainstream the upstream”) and a renewed determination to focus concessional and public resources where they can have the greatest development impact (“shift the default”).

11

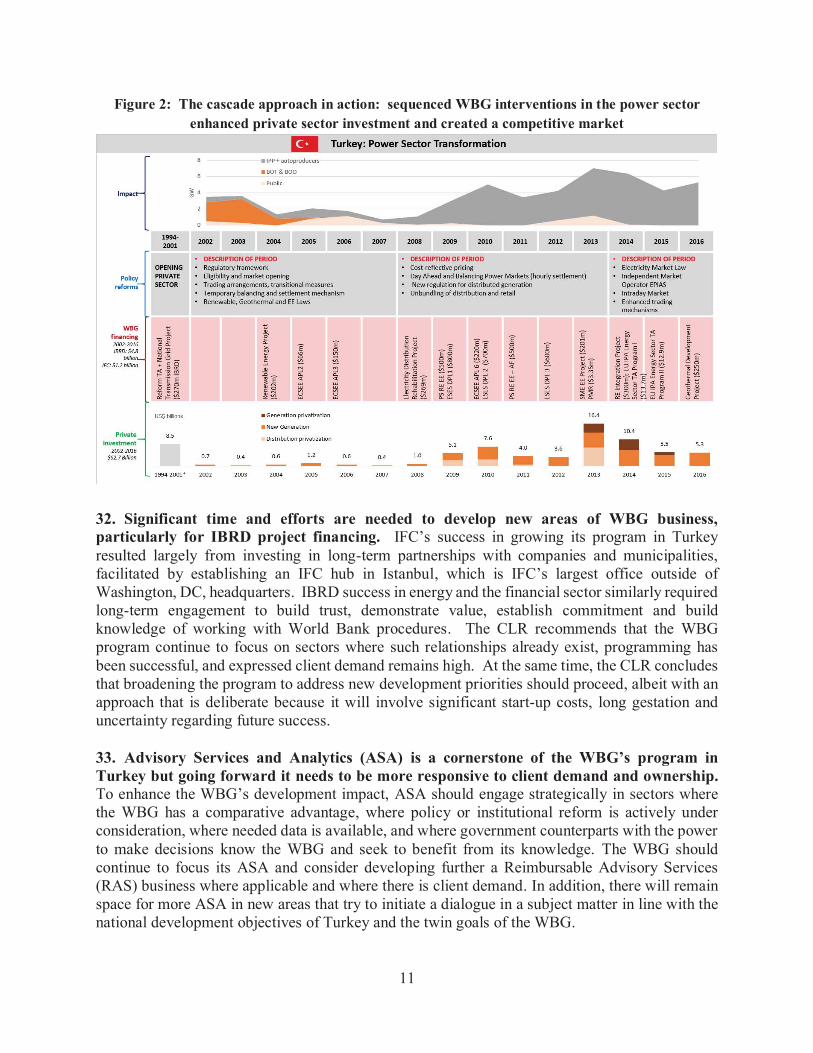

Figure 2: The cascade approach in action: sequenced WBG interventions in the power sector enhanced private sector investment and created a competitive market

32. Significant time and efforts are needed to develop new areas of WBG business, particularly for IBRD project financing. IFC’s success in growing its program in Turkey resulted largely from investing in long-term partnerships with companies and municipalities, facilitated by establishing an IFC hub in Istanbul, which is IFC’s largest office outside of Washington, DC, headquarters. IBRD success in energy and the financial sector similarly required long-term engagement to build trust, demonstrate value, establish commitment and build knowledge of working with World Bank procedures. The CLR recommends that the WBG program continue to focus on sectors where such relationships already exist, programming has been successful, and expressed client demand remains high. At the same time, the CLR concludes that broadening the program to address new development priorities should proceed, albeit with an approach that is deliberate because it will involve significant start-up costs, long gestation and uncertainty regarding future success. 33. Advisory Services and Analytics (ASA) is a cornerstone of the WBG’s program in Turkey but going forward it needs to be more responsive to client demand and ownership. To enhance the WBG’s development impact, ASA should engage strategically in sectors where the WBG has a comparative advantage, where policy or institutional reform is actively under consideration, where needed data is available, and where government counterparts with the power to make decisions know the WBG and seek to benefit from its knowledge. The WBG should continue to focus its ASA and consider developing further a Reimbursable Advisory Services (RAS) business where applicable and where there is client demand. In addition, there will remain space for more ASA in new areas that try to initiate a dialogue in a subject matter in line with the national development objectives of Turkey and the twin goals of the WBG.

12

III.3. Proposed WBG Country Partnership Framework FY18-21 34. The overall objective of the new CPF is to help Turkey to achieve more sustainable and inclusive growth. Turkey’s strong underlying fundamentals, its robust DP, and its long-standing partnership with the WBG provide a good framework for designing a WBG program that will help Turkey to reduce poverty and enhance shared prosperity. At the same time, geopolitical, security and economic developments are also challenging Turkey’s ability to maintain or consolidate some of its recent gains. In this environment, the WBG needs to adopt a flexible approach that remains focused on key medium- and long-term objectives, mostly in known work-programs, but that also responds to opportunities and makes midcourse corrections in the light of changing circumstances. Notably, lessons learned from the past WBG partnership in Turkey, e.g., in the energy sector, emphasize the need for a selective, persistent and supportive engagement with a view to building trust and demonstrating the WBG’s value in helping Turkey pursue its development goals. 35. Three selectivity filters are used to define the WBG program, both at the strategic level and at the objective level:

36. Selectivity filter 1: Alignment with the 10th DP. The CPF aims to support DP implementation by contributing to positive momentum and discouraging backsliding on articulated reforms. This involves assessing critically where the WBG can best add value to DP implementation, where it can deepen or accelerate positive change, and where it can help shape an appropriate response to specific issues (particularly those involving the WBG’s twin goals). 37. Selectivity filter 2: Focus on SCD priority challenges. The development priorities of the SCD and the DP are strongly aligned; together they guide the choice of CPF areas of intervention. In most cases, the SCD highlights areas where the WBG’s ongoing program is already providing support (e.g., macro-fiscal risks, financial markets, female labor force participation, regional differences, congested cities, energy, land management) and so these areas are obvious choices for continued engagement to consolidate and scale-up progress. That said, the CPF will not address all SCD priority challenges. For example, while terrorist-related insecurity is a major challenge, it is also one that lies beyond the WBG’s mandate and expertise. In addition, while the program necessarily focuses on the governance and regulatory framework in sectors where the WBG is active (i.e., energy, health care, the financial sector, and the business environment more generally), there are areas where it is not fully agreed how such issues can most effectively be addressed by the WBG, or where the issues are too distant from WBG expertise or engagement in Turkey to be an effective and constructive partner. In this context, an opportunistic approach will be adopted to stepping up the program where feasible. Finally, the SCD identifies several issues – namely, declining water availability, inefficient small-holder farming, and low performance in innovation and technology absorption – where the WBG has significant expertise that it could leverage but

13

where the future program is not yet clearly elaborated; hence WBG work in these areas will depend on an ability to achieve a common understanding and define an agreed work-program over the CPF period. 38. Selectivity filter 3: WBG comparative advantage: The CPF builds on strengths in the ongoing program where the WBG has a comparative advantage in four distinct ways through: (i) building on the already-fruitful relationships with government and the private sector in areas

where partnerships are mature and which present obvious choices for continued engagement to consolidate and scale up progress. These strong partnerships, together with the fully-joint WBG nature of the CPF, allow for the cascade approach to be deployed effectively. Efforts will a lso continue to encourage the client to make broader use of all WBG instruments while recognizing that agreed areas will likely present opportunities for follow-up lending and consolidate results over a longer term. Capitalizing on its significant and long presence through its office in Istanbul and well established relationships with different stakeholders, IFC will continue to focus on areas where its interventions will contribute to create new markets and help boost Turkey’s private sector-led growth;

(ii) exploration of other opportunities by selectively advocating for new engagement in areas that the SCD highlighted for accelerating poverty reduction and enhancing shared prosperity;

(iii) continued coordination and collaboration with other development partners, notably the EU and other IFIs, to maximize the leverage of WBG support; and

(iv) relationship building at central and municipal levels, with NGOs, academia and civil society to ensure the program has as broad a perspective as possible on country developments and events.

39. The CPF objectives are grouped into three focus areas with nine CPF objectives.

Figure 3: CPF areas of engagement (mapped to SCD priorities)

14

40. Gender concerns are central to the program through being embedded in the CPF objectives. The CPF draws on the recent Country Gender Assessment for Turkey (Annex 7) and places gender issues squarely in four of the nine CPF objectives. The CPF objective on women’s increased labor force participation puts Turkey’s gender development challenge at center-stage. Two other CPF objectives, focused on access to finance and on education and health services, directly target interventions on women. In addition, the CPF objective on improving the sustainability and resilience of cities aims to ensure that service delivery in supported cities targets and monitors impact on female beneficiaries. 41. The results framework reflects the flexible approach of the CPF. The program design and expected results are more certain in the early years of the CPF, where client demand is already expressed and where the contribution of the WBG’s program can be more clearly defined. In the outer years of the CPF, the engagement will evolve in response to country circumstances and government requests for support; hence the definition of expected results for this later period will be provided in the PLR. Given the large start-up costs and long timeframe related to new areas of IBRD engagement, flexibility will be manifested in choosing areas of engagement, instruments, and timeframes, both of financing and knowledge work. Focus Area 1: Growth

42. The WBG will continue to support government efforts to address challenges with respect to fiscal management, the financial sector, competitiveness, and private investment. Turkey rebounded quickly from the 2009 global financial crisis, enjoying strong growth until 2015. Prudent macroeconomic and fiscal management has been a cornerstone of Turkey’s good performance, but resilience to external shocks has weakened and vulnerabilities have increased. At the same time, the changes in the political context, geopolitical tensions, rising oil prices and an anticipated rise in US interest rates have dampened investor and consumer confidence and impacted growth prospects. Turkey’s bank-centric financial sector is also under stress, constraining credit to households and firms. To return to a higher growth path and convergence to high-income economies, the Government needs to continue to strengthen fiscal management, deepen institutional reforms to strengthen the rule of law and arm’s-length market regulation, and create the environment for a more effective and inclusive financial sector. Turkish firms need to increase productivity by boosting innovation and technology to add more value and create more and better jobs. Several of the DP’s Transformation Programs target these issues: Productivity Growth, Increasing Domestic Savings, Rationalization of Public Expenditures, Technology Development, and Business and Investment Climate. The SCD also identified these challenges under its pillars of Solid Foundations and Dynamic Firms. These challenges form the basis for the choice of CPF objectives under this first Focus Area: (i) increased fiscal space; (ii) enhanced access to finance to underserved segments; and (iii) enhanced competitiveness and employment in select industries.

CPF Objective 1: Increased Fiscal Space

Results indicators for Objective 1 Share of direct tax revenues in total tax revenues Establishment of a monitoring system for internal controls in public administration

15

43. The WBG’s program aims to help the government to preserve fiscal space. This will involve a Public Finance Review (benchmarked against EU standards) that will focus on fiscal management, possibly including areas such as income tax law, risk management, internal audit and the analysis of the distributional impacts of fiscal policy. The policy recommendations from this ASA will underpin a proposed DPL series which will be a core part of the IBRD program and which would begin in FY18. The series will have a crosscutting focus in support of key economic reform priorities and the size and frequency will depend on the country situation, the strength of the reform program and financing needs. Further details on the scope of the reform program supported by the DPL series will only become known during its preparation and will thus be provided in the future CPF Program and Learning Review (PLR).

CPF Objective 2: Enhanced Access to Finance to Underserved Segments

Results indicators for Objective 2 People, micro, small and medium enterprises (MSMEs) and exporters reached with financial services Increase in portfolio size of private pension investors/members

44. Turkey’s growth depends critically on a well-functioning and inclusive financial sector. This requires enhancing access to finance (especially for small and medium enterprises (SMEs), which account for 73.5% of jobs but receive only 24% of bank loans), expanding financial inclusion (40% of the population, mostly women, are unbanked), and deepening and diversifying financial and capital markets (e.g., developing long-term finance, increasing the size of institutional investors, diversifying corporate debt instruments, and expanding liquidity in the secondary market for corporate bonds). The banking sector overcame the recent global financial crisis without any state intervention, and exhibits good financial metrics; capital adequacy ratio at 15.6, non-performing loans at 3.2, return on assets at 1.50 and return on equity at 14.3 percent by the end of 2016. However, capital buffers, liquidity and profitability of the banks have been in a downward trend since the global crisis (although still remaining comfortably above the regulatory thresholds and there has been an increase in profitability recently) while there has been an upward trend in non-performing loans in recent years. The loan to deposit ratio has breached 123 percent, and banks have limited sources to support further loan growth due to: (i) low savings rates significantly limiting banks’ ability to attract new deposit, (ii) the uncertainty on global liquidity limiting foreign borrowing, and (iii) low profitability discouraging shareholders’ increase of capital. Going forward, Turkey needs to address concerns about financial sector risks and potential spillovers to the economy as a whole. The sector is vulnerable due to structural factors (high dependence on cross-border financing, high debt and savings held in foreign currency at short maturities) as well as cyclical factors (growing corporate leverage, rising corporate-bank and (contingent) corporate-sovereign exposures). While a recent IMF-WB financial sector assessment shows that banks’ capital buffers are resilient in the face of a short-term shock, a longer recession could force some to seek additional capital, which may be difficult in a context of possible future global liquidity constraints. 45. The WBG has a long engagement in many aspects of the financial sector and currently IFC, IBRD and MIGA deliver coordinated support through a portfolio of projects, investments and ASA. For the CPF period, this coordinated support will continue with a particular focus on stepping up finance to MSMEs and under-served segments and through robust ASA that will help inform government policy and underpin the DPL series. The ASA program

16

will be coordinated to cover critical issues such as financial sector diversification, pensions, capital market development (including WB-IFC support to develop municipal bond markets and to develop the Islamic finance market) and analysis of sector headwinds and how to respond to them. The ASA will inform any potential new financial sector investment operations as well as reforms to be supported through the DPL series (such as reforms on pensions). IBRD will continue to work with the state banks, development banks and other financial institutions to support their countercyclical and market-gap-filling functions, especially through providing long-term financial sources. New financial sector line-of-credit operations may be provided where they extend access to finance (e.g., to MSMEs, to female- or refugee-owned businesses), incentivize investors in key sectors (e.g., energy or technology innovators), and deepen and diversify applicable and client demand-driven instruments (e.g., leasing and factoring, corporate bonds, infrastructure bonds, Islamic finance, and risk-sharing facilities). In this context, a new operation – Long Term Export Finance – was delivered in early FY17 to help address lack of long-term finance: this operation targets support specifically to exporters and MSMEs. During the course of the CPF, should the financial sector show greater vulnerability to down-side risks, the program can be adapted accordingly. 46. Enhanced access to finance is a key IFC priority. IFC will continue to work with financial institutions and intermediaries to expand the availability of funding to MSMEs, with a focus on rural areas, women-owned enterprises, and agribusinesses. It will continue to support banks and non-bank financial institutions (NBFIs) with longer-term funds to help them scale-up support to the underserved and unbanked. To deepen and diversify financial markets and reach underserved segments, IFC aims to leverage diverse instruments and means of funding, including supply chain finance, digital financial services, NBFIs (leasing companies, insurance companies, and pension funds), and distressed asset resolution platforms. IFC will also support alternatives to bank finance by investing in capital market instruments such as covered bonds, diversified payment rights (DPRs), green bonds, municipal bonds, and PPP project bonds (both in euros and lira). In order to address currency risks facing Turkish borrowers, IFC will seek to maximize lira financing and offer currency hedging instruments for real sector clients, PPP investments and municipalities with large external exposures. Recognizing increased risks of capital erosion, IFC may also help banks to strengthen their regulatory capital. Finally, IFC will closely coordinate with MIGA to respond to commercial lenders’ increasing demand for risk guarantees to enhance municipalities’ creditworthiness. 47. MIGA will continue its support to Turkey’s Eximbank. Given the Eximbank’s strategic role, MIGA provided it with guarantees covering the non-honoring of the financial obligation of state-owned enterprises in 2015 and 2016, thus helping to strengthen the financial sector as a whole and to support lending activities to MSMEs and export-oriented companies.

CPF Objective 3: Enhanced Competitiveness and Employment in Selected Industries

Results indicators for Objective 3 Employment supported by IFC clients Employment supported by IFC-supported equity funds

48. To create the jobs needed to employ the rapidly growing labor force and raise it to a higher income level, Turkish businesses need to improve their competitiveness through

17

innovating, boosting productivity and moving up the value chain. The WBG program to date has focused its ASA on trade liberalization, competitiveness, the quality of exports, value chain progression in specified industries, the ability to attract foreign direct investment (FDI), and regional investment climates. This program is expected to be strengthened through analyzing past, and shaping future, efforts to improve the business environment, innovation and technology absorption (including through the links between FDI and local firms), subnational competitiveness, and trade in services, as well as to understand the drivers of competitiveness and productivity (as part of the upcoming Country Economic Memorandum (CEM)). Technical assistance (TA) is also planned to improve the regulatory environment and increase job opportunities in communities affected by SuTPs. TA on competitiveness, resource efficiency and cleaner production with a focus on Organized Industrial Zones (OIZs) will be delivered. Taken together, this ASA serves as a centerpiece of WBG dialogue in Turkey, feeding into the design of reforms, underpinning any relevant reforms that may be captured in the future DPL series, and helping target potential high-growth or innovative SMEs (which in turn could be targeted through the financial sector support pursued under CPF Objective 2 above). This stronger framework is expected to lead to enhanced private sector investment which IFC and MIGA could support. In later stages of the CPF period, IBRD may build on the ASA to step up lending in support of innovation, technology absorption, cleaner production and an improved business environment, should the client demand. 49. Boosting employment growth through support to entrepreneurship and innovation is IFC’s priority under this objective. Through financial intermediaries and direct engagements with real sector companies, IFC will help strengthen Turkish firms’ competitiveness (with new technology, innovation and improved governance) and support their regional and international expansion. IFC will continue investing in equity funds that promote local entrepreneurship, competitiveness and innovation, while also fostering employment in high-growth and high-value-added sectors (e.g., manufacturing, telecommunications, technology, agribusiness). It will continue with its Global Trade Finance program mitigating risks through guarantees to banks that deliver trade financing. IFC will also provide advisory services focused on corporate governance, and skills development that enable better linkages of SMEs with high growth value chains. IFC AS will contribute to improved competitiveness, productivity, and sustainability of Turkish manufacturers through (i) a set of greener manufacturing interventions in OIZs including resource efficiency, cleaner production, industrial symbioses, and green infrastructure, (ii) building business cases (cost-benefit analysis) at firm and OIZ levels to enable better detection of bankable projects, and (iii) helping develop a comprehensive national framework on Green OIZs for Turkey. Focus Area 2: Inclusion

50. WBG support in this area aims to consolidate Turkey’s success towards achieving the twin goals while also supporting efforts to reach those who are left behind. This implies realizing the demographic dividend by creating good jobs for increasing numbers of workers, which involves better integration of women, youth and SuTPs into the labor force, reducing persistent gender inequalities (particularly in access to economic opportunities), reducing regional labor-market disparities, and raising learning levels (including at the youngest ages, when development of the cognitive and behavioral skills required in the workplace is optimal). The WBG’s program to date in this focus area had a concentration on ASA which informs government-financed programming (and DPLs) and which the government wishes to remain at the core of the

18

engagement because of its role in providing knowledge for many of the reforms undertaken in this area. Broad issues of equity, vulnerability and regional disparities – that cut across the whole of the WBG program and not just this Focus Area – will continue to be the focus of in-depth ASA, possibly through a future CEM or other deep-dive diagnostic. An important evolution of the WBG program in this area has been the introduction in FY17 of new investment operations financed by the EU’s Facility for Refugees in Turkey (FRiT), which is the framework for the EU’s pledged assistance to Turkey for continuing to support hosting SuTPs; the FRiT funding has allowed the WBG to complement its ASA with more in-depth support through investment projects while strengthening cooperation between WBG and the EU.

CPF Objective 4: Increased Effectiveness of Social Assistance

Results indicators for Objective 4 Increased impact of social assistance on the poverty gap Increased availability of monetary and non-monetary indicators of welfare and inclusion.

51. This CPF objective has the goal of improving efficiency and effectiveness in social assistance and strengthening the evidence-base for policies aiming to narrow gaps between regions and ensure greater inclusion of vulnerable groups. The ASA program will continue to produce and disseminate monetary and non-monetary indicators of welfare and inclusion, including equality of opportunity and multi-dimensional poverty. The WBG will continue its support to the Poverty Reduction Strategy and Social Assistance Reform initiative of the Ministry of Family and Social Policies (MoFSP) for making the social assistance system more effective and efficient, especially towards vulnerable groups such as the disabled. The WBG’s Europe and Central Asia regional agenda on support to the Roma people will encompass Turkey through the framework of providing support to the recently-adopted policy of the Strategy for Roma in Turkey (2016-2021).

CPF Objective 5: Increased Labor Force Participation of Women & Vulnerable Groups

Results indicators for Objective 5 Increased female labor force participation Increased youth participation in the labor force Increased SuTP employability in the labor force (gender disaggregated) Direct employment supported by IFC manufacturing clients in south east regions

52. WBG support under this objective aims to bring more people – especially women and youth – into the formal labor market. This is critical for Turkey to reap the benefits of its demographic window and so to grow rich before it grows old. The importance of this challenge is recognized and reforms in the past have focused on different interventions. The Bank intends to continue its role of providing a comprehensive package of ASA that analyses the labor market’s supply and demand constraints (including jobs diagnostics, evaluations of labor policies such as minimum wage, pre-school and child-care policies, and social norm constraints) as well as assessments of individuals who are not in school, education, employment or training (NEET). The aim of these ASAs is to propose reform recommendations (e.g., on flexible work arrangements, tax incentives for pre-schools, maternity/paternity leave, and active labor market programs (ALMPs) incentivizing training and jobs for women and youth) which can guide Government

19

decision-making and could in turn be supported through DPLs. As part of the support to jobseekers, the WB will continue supporting the public employment services (ISKUR) institution to strengthen its capacity as well as its effectiveness helping jobseekers. 53. This objective seeks to improve the employability of other vulnerable groups. The influx of SuTPs has created new challenges among the labor force, particularly for those in the south-east which is hosting the concentration of SuTPs. This is exacerbating an already challenging environment for the people in southeast Turkey who have lower incomes, make less use of public services, and have less access to finance (for farmers, agribusinesses, and SMEs, particularly for women-owned enterprises). The WBG will help to address these issues through policy advice (supported by EU and SIDA trust funds) and project interventions. A FRiT-funded labor market inclusion project (€50 million, FY17) targets increased SuTP participation in the labor market through providing access to ALMPs. This is complemented by FRiT funding of €5 million for IBRD advisory work to support facilitation of employment and entrepreneurship opportunities in SuTP-affected regions. Further IBRD and/or EU investments will be considered where there is client demand and a link to the twin goals. The WBG is also providing support on migration issues more broadly as part of its global knowledge role in this subject. 54. IFC aims to invest in projects that promote greater equity in the access of vulnerable and underserved groups to services, jobs, and finance. IFC will scale up its SME financing targeted to women entrepreneurs and farmers and will leverage NBFIs to broaden access to finance of these groups. It will also invest in key manufacturing companies with presence in the south-east of Turkey with a view to support employment in the lagging regions. Aiming to help underserved populations access better urban services, IFC will pursue investment opportunities in commercially-viable urban infrastructure projects in second-tier, less developed regions. In addition, it will offer advisory services to Turkish corporates to help them develop gender programs that support women’s employment and entrepreneurship.

CPF Objective 6: Strengthened performance of the education and health sectors

Results indicators for Objective 6 Increased percentage of formal school enrollment of SuTP children between the ages of 6-18 Improvement of primary and secondary prevention of non-communicable diseases Number of patients served through IFC health sector clients

55. The focus in the health sector is on promoting healthy lifestyles. Turkey has already made enormous progress in reducing mortality and increasing life expectancy; now the challenge with the greatest potential impact is promoting healthy lifestyles through attacking behavioral risks. An ongoing IBRD-financed health project aims to enhance the capacity of the Ministry of Health (MoH) for evidence-based policy making, increase hospital management capacity, and improve the prevention of selected non-communicable diseases (NCDs). The project mainly aims to raise awareness about NCD risk factors (such as smoking, obesity and physical inactivity) and to promote behavior change; among other things, Turkey will be included in a global obesity study and its experience in tobacco control will be documented. In addition, IBRD will continue to support the second phase of the health transformation program through activities focusing on providing appropriate high-quality care by results-based interventions and payment reforms. This includes documenting the successes and challenges faced, and the political economy of the

20

transformation. IFC and MIGA will continue to support Turkey’s health sector through investments in specialized health service providers, and through financial innovation to help create alternative capital market solutions for health infrastructure financing. For example, IFC financed Turkey’s first PPP bond issuance under Elazig health PPP project, which was structured and supported by MIGA and EBRD through credit-enhancement products. IFC will invest in specialized services (e.g., bio-pharmaceuticals manufacturing), where it can play a role in bringing in strategic investors and building partnerships, which it can then support with financing. MIGA will remain open to support investments into Turkey’s health PPP program by providing political risk insurance guarantees for the construction and operation of new health facilities. Similarly to IFC, financial innovation in Turkey’s health sector will remain a focus area to leverage the use of MIGA’s credit enhancement products, as utilized on the recently closed Elazig bond transaction. 56. In the education sector, the CPF will step up ASA in response to the recent fall in PISA and TIMSS scores for Turkey. This ASA will support primary education and teacher training reform efforts, help inform and influence policies affecting the quality of education and the monitoring of education services. Given the time required to impact learning, results are likely to be modest and achieved beyond the CPF period. There are discussions underway with the Ministry of National Education (MONE) to support areas including life-long learning and distance education approaches where the WBG has global experience. IBRD will implement a FRiT-financed education project (€150 million) which aims to expand education service delivery and targets resources where SuTPs as well as host communities face capacity constraints. IBRD is also providing technical support to derive a strategy to integrate immigrant children into the education and vocational system. In addition, a new EU Instrument for Pre-Accession (IPA) -funded project targeting youth who are out of school is being prepared in areas where drop-out rates of Turkish youth is high and where SuTP youth are at risk of never entering school. Lastly, IFC will look for opportunities to invest in education service clients to promote private vocational training. Focus Area 3: Sustainability 57. The WBG’s program will help address the SCD-highlighted challenge of reorienting growth towards a more green, resilient and sustainable pattern. Economic growth and urbanization in Turkey are not yet decoupled from rising energy use, pollution and greenhouse-gas (GHG) emissions, so there is much potential for greater resource efficiency and pollution abatement. The challenges are to provide connectivity and agglomeration benefits in an environmentally, socially and financially sustainable way (particularly as regards reducing energy intensity and avoiding water scarcity). The program will build on the well-established IBRD and IFC collaboration in energy and urban/municipal services, where 75 percent of IBRD’s investment program and a sizeable proportion of IFC’s engagements are already concentrated: this provides an excellent opportunity for operationalizing the cascade approach to financing. The CPF proposes both to build on the on-going program and to encourage its evolution towards issues critical to Turkey’s future growth. It is consistent with the 10th DP Transformation Programs focused on increased energy efficiency and generation from local resources, urban redevelopment, improved access to potable water and wastewater services, effective use of water in agriculture, and sustainability in the use of natural capital. Within this focus area, the CPF objectives include (i) improved reliability of energy supply and generation of green energy; (ii) improved sustainability and resilience of cities; and (iii) increased sustainability of infrastructure assets and natural capital.

21

CPF Objective 7: Improved reliability of energy supply and generation of green energy

Results indicators for Objective 7 Renewable electricity generation as percentage of total generation Value of loans provided by IFC clients to renewable projects Total power generation and distribution clients reached Increased capacity of gas storage Gas imports through Trans-Anatolian Pipeline (TANAP)

58. The WBG’s current program is heavily concentrated in the energy sector, with a cascade approach underway whereby IBRD policy advice and TA are paving the way for stepped-up private sector engagement supported by IFC and MIGA. The program aims to help Turkey to reduce its energy dependence (it imports 92 percent of its oil and 98 percent of its gas), support the energy reform agenda, diversify its energy generation (inter alia to include more renewables), and upgrade regional transmission and distribution networks. Harmonization with EU standards is also a key objective. ASA – supported by EU/IPA, ESMAP and CTF grants on rooftop solar programs, generation planning, gas sector restructuring, smart grid applications and distribution companies – will continue to deliver policy advice and just-in-time analysis of sector issues under government debate. IBRD, IFC, and MIGA will work closely together to help Turkey improve its PPP policy framework to stimulate further private sector energy investments, strengthen the energy regulatory environment, and increase long-term financing for renewable energy5. This ASA will also feed into the design of future DPLs, which could stimulate investments in renewable energy generation and transmission and the related climate change benefits. 59. The IBRD investment portfolio will continue to focus on improving Turkey’s energy security and mix, including by increasing the use of renewable resources (wind, solar, and geo-thermal). The CPF program encompasses: (i) increasing the percentage of renewable electricity generation and improving its integration into the grid through the ongoing Renewable Energy Integration, the Private Sector Renewable Energy and Energy Efficiency, the Geothermal Development and the EU/IPA Energy Sector TA Projects; (ii) enhancing energy security infrastructure and gas storage capacity through the on-going Gas Sector Development Project and the proposed Gas Storage Expansion Project; (iii) developing energy trading and restructuring of BOTAŞ through the EU/IPA Energy Sector TA Project; (iv) securing and diversifying Turkey’s gas supply, including gas imports from Azerbaijan through the TANAP Project – where $800 million in IBRD loans to Turkey’s BOTAŞ and Azerbaijan’s Southern Gas Corridor (SGC) leveraged $600 million from the Asian Infrastructure Investment Bank (AIIB) and the expectation of up to $1.2 billion in guarantees from MIGA; (iv) development of interconnections to ensure cross-border electricity and natural gas trading; and (vi) other areas to support sustainable energy sector development as agreed between the Government and the WBG, including increasing the grid capacity and smart grid technologies, distribution and transmission networks and systems. Given the comparative advantage of IBRD in the sector, further energy investments may follow, on client demand, observing the WBG’s cascade approach on leveraging private financing.

5 Support for the regulatory environment for renewable energy, for example, is being provided under the ongoing EU-IPA Energy Sector TA and the Rooftop Solar PV Assessment. Further work to improve the investment climate for the energy sector will be coordinated with the PPP RAS.

22