FOR NON-PROFIT ORGANIZATIONS Presented by Henrietta Jordan.

26

FINANCIAL RECORDS AND REPORTING FOR NON-PROFIT ORGANIZATIONS Presented by Henrietta Jordan

-

Upload

asher-timmins -

Category

Documents

-

view

217 -

download

3

Transcript of FOR NON-PROFIT ORGANIZATIONS Presented by Henrietta Jordan.

FINANCIAL RECORDS AND REPORTING

FOR NON-PROFIT ORGANIZATIONS

Presented by Henrietta Jordan

Why Financial Statements MatterInternal management and decision

makingAccountability and transparencyDonor confidence and informationReporting to fundersInternal Revenue ServiceState regulatory agencies

PURPOSE OF FINANCIAL REPORTS

Snapshot of where you areStory of what happened – financiallyHelp you understand what you need to do

to achieve your goals

Financial StatementsStatement of Financial Position (aka

Balance Sheet)Statement of Activities (aka Profit and

Loss Statement)Statement of Cash FlowBudget Comparison

Relationships between StatementsStatement of Financial Position – assets

and liabilities at a single point in timeStatement of Activities – financial activity

over a period of timeBudget Comparison – performance vs.

expectationsCash flows – sources and uses of cash over

a period of time

Statement of Financial PositionSnapshot – single point in timeAssets of the organization – what it

ownsLiabilities of the organization – what it

owes to othersNet assets – what is left over

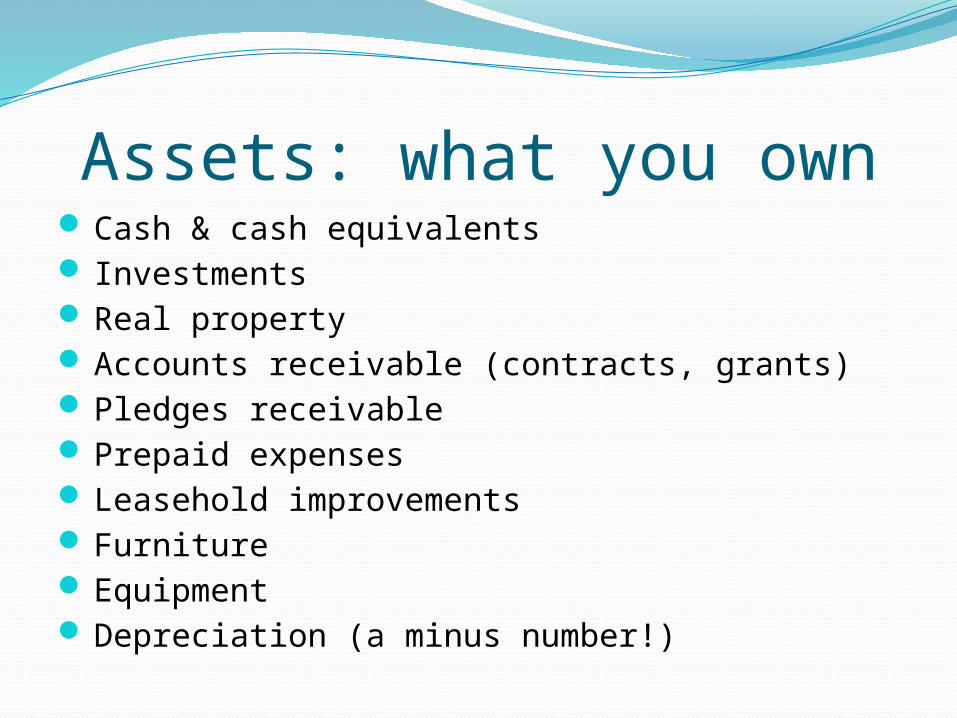

Assets: what you own Cash & cash equivalents Investments Real property Accounts receivable (contracts, grants) Pledges receivable Prepaid expenses Leasehold improvements Furniture Equipment Depreciation (a minus number!)

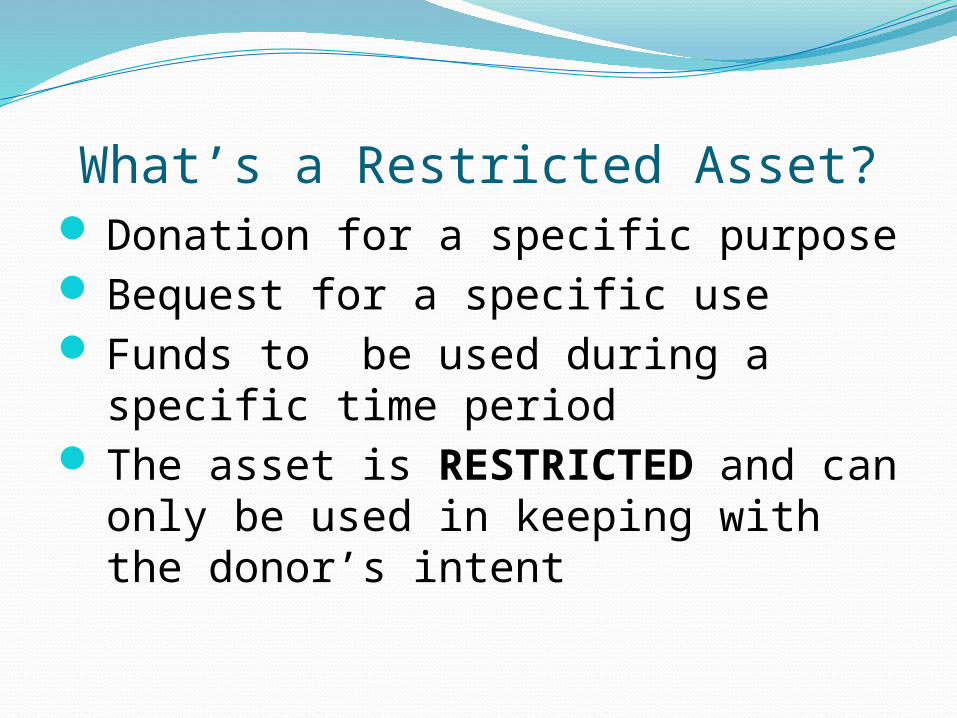

What’s a Restricted Asset? Donation for a specific purpose Bequest for a specific use Funds to be used during a specific time

period The asset is RESTRICTED and can only be used

in keeping with the donor’s intent

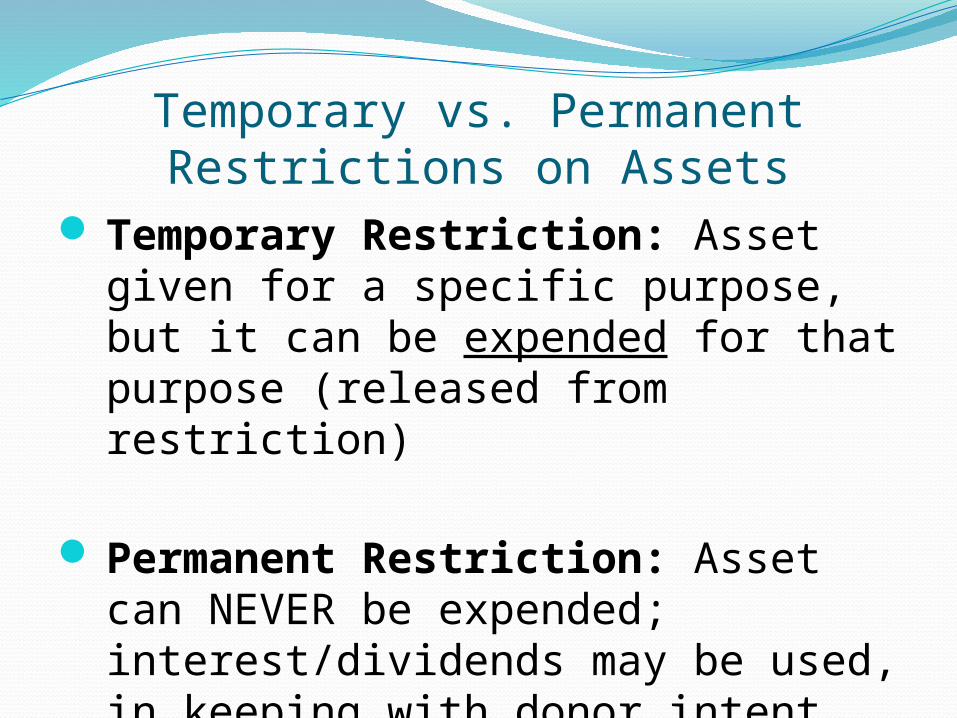

Temporary vs. Permanent Restrictions on Assets

Temporary Restriction: Asset given for a specific purpose, but it can be expended for that purpose (released from restriction)

Permanent Restriction: Asset can NEVER be expended; interest/dividends may be used, in keeping with donor intent (endowment)

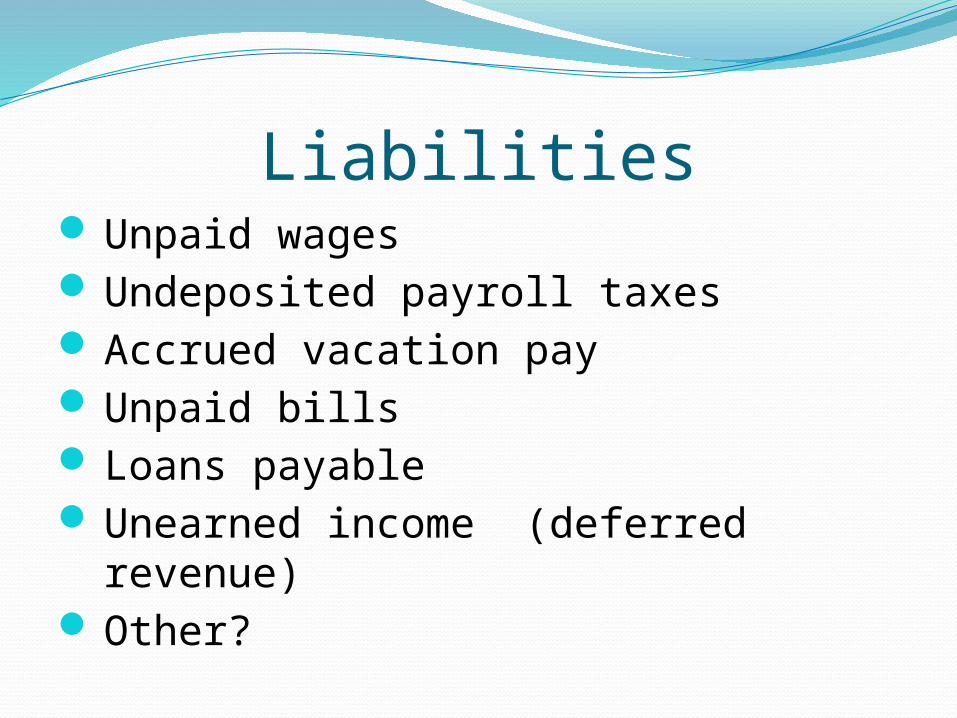

Liabilities Unpaid wages Undeposited payroll taxes Accrued vacation pay Unpaid bills Loans payable Unearned income (deferred revenue) Other?

Chart of Accounts The heart of your accounting system Method of classifying assets, liabilities,

income and expenses Should reflect the programs and activities of

the organization More accounts = more information but also

more work! Develop with professional advice

Why is it called a balance sheet?The Accounting Equation

Assets = net assets plus liabilities Or, more logically,Assets minus liabilities = net assets

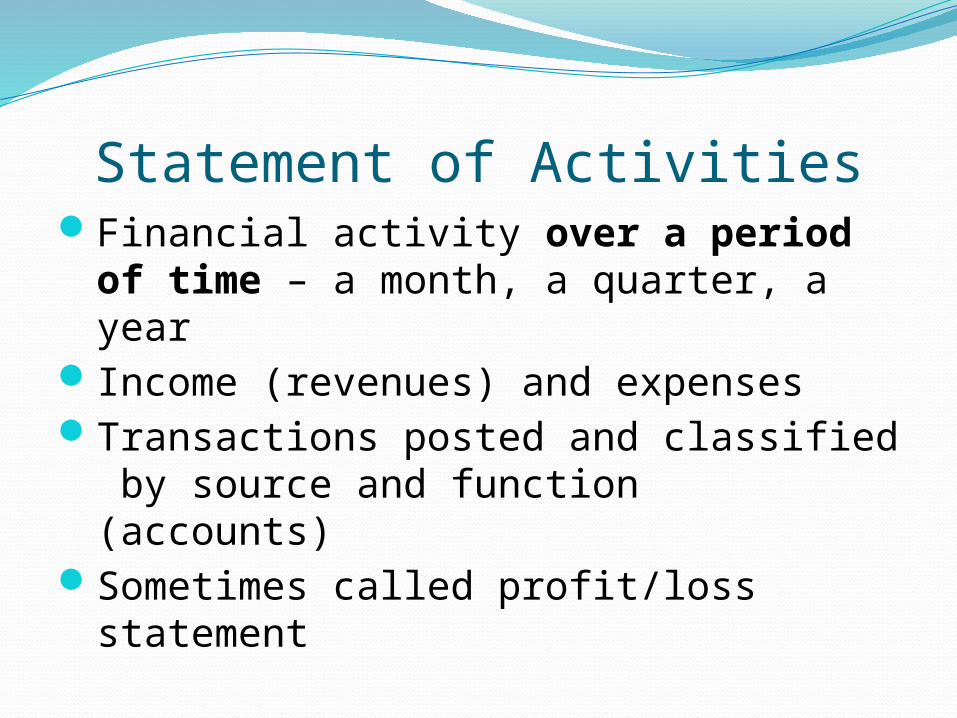

Statement of ActivitiesFinancial activity over a period of time –

a month, a quarter, a yearIncome (revenues) and expensesTransactions posted and classified by

source and function (accounts)Sometimes called profit/loss statement

Functional Classification of Expenses Program – expenses related to carrying out the work of the

organization (salaries/benefits of program staff, program supplies, portion of occupancy)

Fundraising – expenses related to soliciting contributions for the organization (portion of salary & benefits of staff participating in grantwriting, special events, donor cultivation, portion of occupancy)

Administration – expenses not related to program or fundraising but that are essential to the organization’s operation (salaries, benefits of finance staff, portion of ED’s salary and benefits, board-related costs, portion of occupancy)

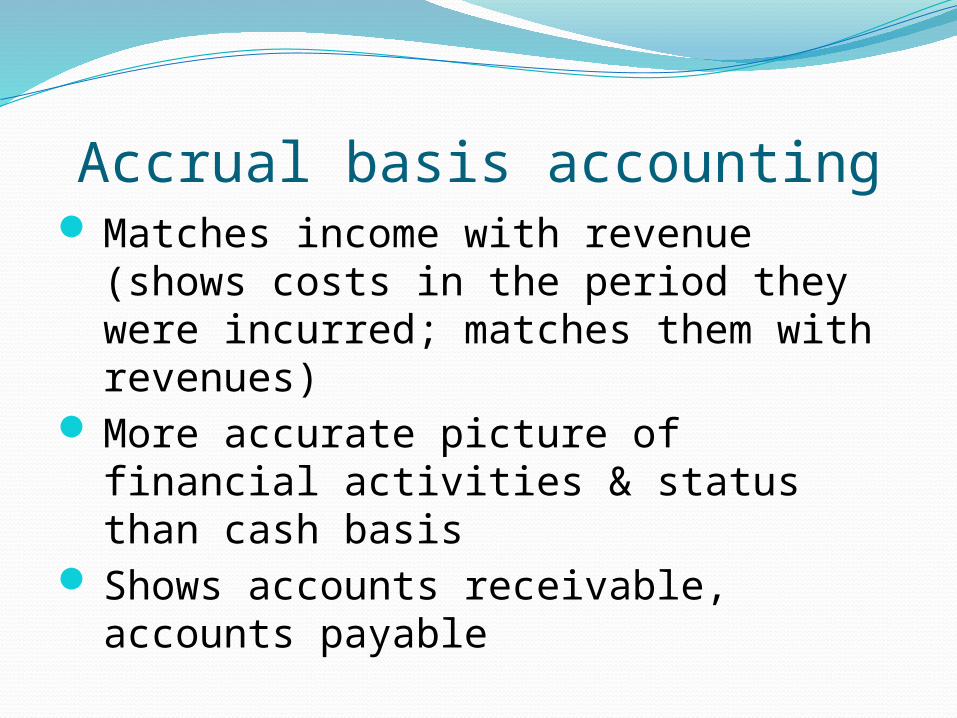

Accrual basis accounting Matches income with revenue (shows costs in

the period they were incurred; matches them with revenues)

More accurate picture of financial activities & status than cash basis

Shows accounts receivable, accounts payable

Capitalization and Depreciation Spreads the cost of major equipment over its useful life Computer system costing $3,000 with a 3-year depreciation

scheduleo Initially listed as an asseto Depreciation (cost) = $1,000/yro Annual cost listed as expense on Statement of Activitieso Accumulated depreciation subtracted from asset’s value

on balance sheeto At end of 3 years?

You decide: what is it?Asset, liability, income or expense?

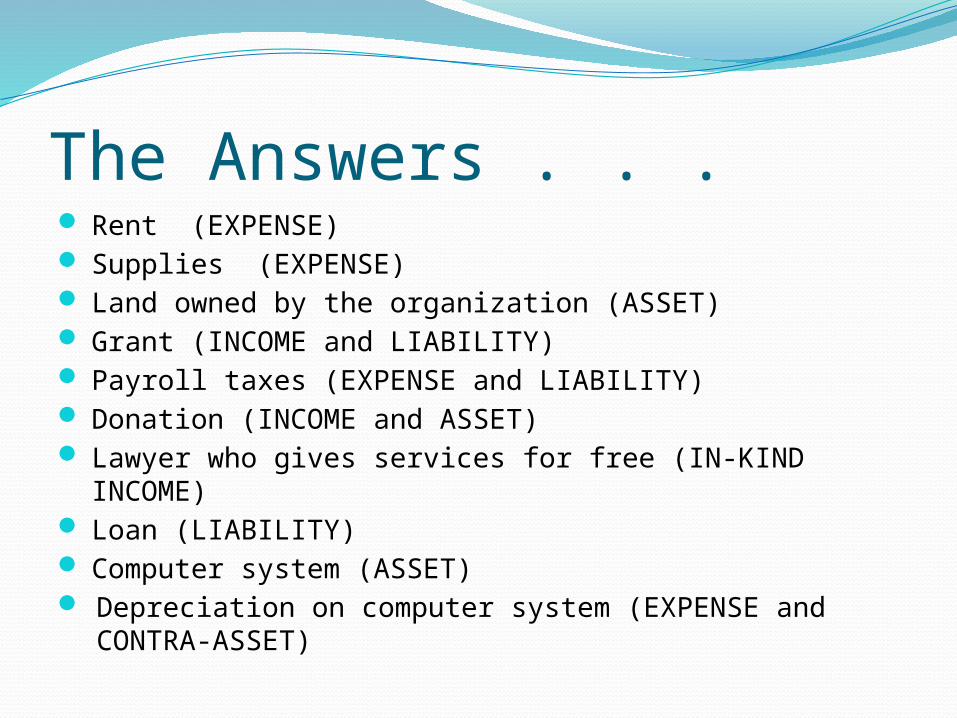

RentSuppliesLand owned by the organizationGrantPayroll taxesDonationLawyer who gives services for freeLoanComputer systemDepreciation on computer system

The Answers . . . Rent (EXPENSE) Supplies (EXPENSE) Land owned by the organization (ASSET) Grant (INCOME and LIABILITY) Payroll taxes (EXPENSE and LIABILITY) Donation (INCOME and ASSET) Lawyer who gives services for free (IN-KIND INCOME) Loan (LIABILITY) Computer system (ASSET) Depreciation on computer system (EXPENSE and CONTRA-

ASSET)

Budgeting Critical document for management Sources of information (prior year’s income &

expenses, anticipated increases/decreases, new programs)

What’s the plan? Process: who develops the first draft? How is

it marked up? Contingency Final approval by the board

Budget Comparison Side by side: Budgeted vs. Actual Percentage of anticipated revenues and

expenses to date Annotate to explain why income & expenses

happening unusually quickly or slowly Reviewed by board or finance committee at

least quarterly

Financial ReservesYour rainy-day fundEnough to cover 3-6 months of operating

expensesLiquidity?(Net unrestricted assets)

Internal Controls First line of defense against misuse of

organization’s funds Documented in accounting procedures Based on segregation of duties among several

different people in: Receiving donations Preparing deposits Authorizing expenditures Reconciling the bank statement

More important safeguardsAccount for staff time through

timesheetsLock it up!Secure recordkeeping systems

Independent Financial Review(by a CPA)

Compilation of Financial Statements Review of Financial Statements Audit

What is financial leadership?Decision makers . . . . Have timely and accurate financial data Periodically assess the financial condition of

activities and the organization as a whole Plan around a set of meaningful financial

goals Effectively communicate progress internally

and to stakeholders

Board Responsibilities Overall fiduciary responsibility for the

organization Hiring top management Approve budget Monitor results (reports) Take corrective action, if necessary Hire independent auditor