FOOD SAFETY AUDITING PROJECT REPORT - … · FOOD SAFETY AUDITING PROJECT REPORT September 2015...

26

FOOD SAFETY AUDITING PROJECT REPORT September 2015 Authors: Geoffrey Annison and Fiona Fleming Australian Trade Commission

Transcript of FOOD SAFETY AUDITING PROJECT REPORT - … · FOOD SAFETY AUDITING PROJECT REPORT September 2015...

FOOD SAFETY AUDITING PROJECT REPORTSeptember 2015

Authors: Geoffrey Annison and Fiona Fleming

Australian Trade Commission

Background. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Food safety auditing scoping project. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Industry survey. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Cost of food safety management and food safety audits. . . . . . . . . . . . . . . . . 6

Industry round table. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Conclusion and recommendations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Next steps. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Acknowledgements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Appendix: Food Safety Auditing Project – Food Industry Survey Report. . . . . 11

1. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2. Methodology. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.1 Survey design and development. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.2 Method of delivery. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3. Results. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3.1 Response rate. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3.2 Company information. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.3 Food safety programs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.4 Food safety auditing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.5 Food safety auditing - suppliers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4. Discussion and conclusion. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Contents

2

3

BackgroundThe Australian food production, manufacture and retail supply chain comprises a complex network of suppliers and customers. Products and manufacturing systems must meet regulatory requirements and customer specifications described in regulation, general industry standards, and/or bespoke company standards.

Compliance with regulations and other standards is demonstrated through the auditing of company operations. In essence, the audits seek to confirm adherence to food safety and quality procedures, and that those procedures are adequate to assure the safety and quality of food products.

Auditing may be conducted by certification bodies1 (CBs) i.e. a third party audit, or alternatively a customer may audit a supplier directly i.e. a second party audit. CBs can also be engaged to conduct second party audits.

In Australia, the major retailers, quick service restaurants, food service companies and major manufacturers commission a large number of audits of suppliers of fresh products, ingredients and finished retail ready products. Regulatory agencies (Commonwealth, State and Territory and local government) also conduct food safety audits. Industry surveys indicate that there is appreciable overlap between audits – that is individual companies may be audited multiple times over short time periods on behalf on different customers. A substantial commonality of elements between audits, particularly for food safety matters and a lack of cross-recognition of audit reports represent a significant, and in many case unnecessary, cost burden on the companies, which in aggregate across the supply chain is substantial, running to many millions of dollars.

To address this issue the AFGC has been consulting with all the stakeholders in the food value chain to explore options for alleviating some of the cost burden. Discussions with stakeholders indicate that better outcomes can be achieved through:

• identifying the critical food safety elements of regulatory requirements and industry standards and ensuring they are common to all of those used;

• standardising audit reporting documentation enabling use across a range of industry standards;

• establishing principles and agreements for cross-recognition of food safety elements of audit reports;

• promoting consistency and confidence in audit outcomes through establishing audit and auditor competency standards and skill sets appropriate for harmonised and aligned product categories; and

• promoting product safety across the food industry through highlighting the key behaviours of companies successfully managing food safety.

Notwithstanding this, there is still a degree of uncertainty regarding the overall cost-burden of auditing on the industry and the factors which drive these costs. This has hindered the development of a coordinated industry approach to addressing the problem, despite agreement among major stakeholders along the supply chain that costs of maintaining food safety systems are climbing, that the threats to food safety are increasing due greater supply chain complexity, and concerns regarding food safety in the community appear to be rising.

In order to gain a better understanding of the state of food safety auditing across the industry the AFGC was contracted by Food Innovation Australia Ltd. and AusIndustry to conduct a Scoping Project to gather further detailed information on the costs of auditing and their drivers, the value of auditing to the food industry, inefficiencies in the current auditing approaches and to canvas ideas for better ways of managing auditing across the sector.

The intent is that the results of the Scoping Study will inform the preparation of a Business Case for a larger body of work by the food industry with the ultimate aim of ensuring food safety auditing is a value-add across the food sector for the good of the industry and the consumers it serves.

This report provides an overview of the outcomes and findings of the scoping study which was conducted by the AFGC from June to August 2015.

1 Certification Bodies are independent companies accredited by government agencies in the jurisdictions in which they operate.

4

Food safety auditing scoping projectThe AFGC was contracted by Food Innovation Australia Ltd (FIAL) and AusIndustry to conduct a Scoping Project to gather information on food safety auditing of industry and its costs on businesses.

For the study the AFGC engaged with stakeholders by:

• establishing a project management committee;

• collating an extensive stakeholder email list of over 6,500 individuals; and

• conducting a stakeholder round table and a number of briefings.

The Project Management committee was established as a reference group for the scoping project. The members of the project management committee were drawn from a range of stakeholders all of whom had previously engaged with the AFGC on the topic of food safety auditing. All major post-farm gate2 food supply chain sectors were represented.

With the assistance of other organisations a stakeholder mailing list was established for the project. This served as a comprehensive list of stakeholders. The AFGC was able to engage with over 6,500 individuals across the food industry through this list.

Industry surveyTo provide qualitative and quantitative data on the impact of food safety auditing on the food industry the AFGC conducted industry survey in July 2015.

The Food Safety Auditing Project online industry survey was finalised and sent out on July 8th and closed on Monday August 3rd.

The purpose of the survey was to collect information on:

• the auditing standards which are currently being used across industry sectors for food safety;

• the cost and frequency of audits on food businesses; and to

• identify key attributes of effective food safety management.

The survey was distributed to over 6,500 email addresses via the mailing lists identified by the AFGC. A total of 225 company responses were received for the survey representing 659 manufacturing facilities in Australia and New Zealand. The survey represented a broad range of business types and sizes (small, medium and large), food product categories and distribution across Australia and New Zealand. Customers represented included other food manufactures; retailers; food service and quick service restaurants.

Key findings from the survey

When asked their view of food safety audits conducted on their business, 74% of respondents (n=163) considered that food safety audits are an integral part of managing food safety within their business. This is despite the cost and burden of food safety audits. 71% of respondents considered that food safety audits are a cost of doing business and 55% considered that food safety audits provide value to my business.

The number of audits commissioned by the business on the business (i.e. a company auditing its own systems) compared with the number commissioned to meet customer requirements supports the concern with respect to audit burden. Responses (n=95)3 indicated that an average of 14.9 audits are conducted per company with 4.3 commissioned by the business and a further 10.6 commissioned to meet customer requirements.

A total of 36 auditing standards were identified by companies in addition to audits conducted by government agencies.

2 The AFGC is aware of a similar project is being conducted in the horticultural sector.

3 N=95 represents the number of respondents that provided the full information for this question in the survey.

5

The Standards can be categorised as follows:

• ISO (International Organization for Standards) /AS (Standards Australia);

• GFSI (Global Food Safety Initiative) recognised standards;

• Retailer vendor standards;

• QSR (Quick Service Restaurants) vendor standards;

• Food Service vendor standards;

• Other Industry standards; and

• Food regulations.

The cost of food safety management and food safety audits is discussed in a following section.

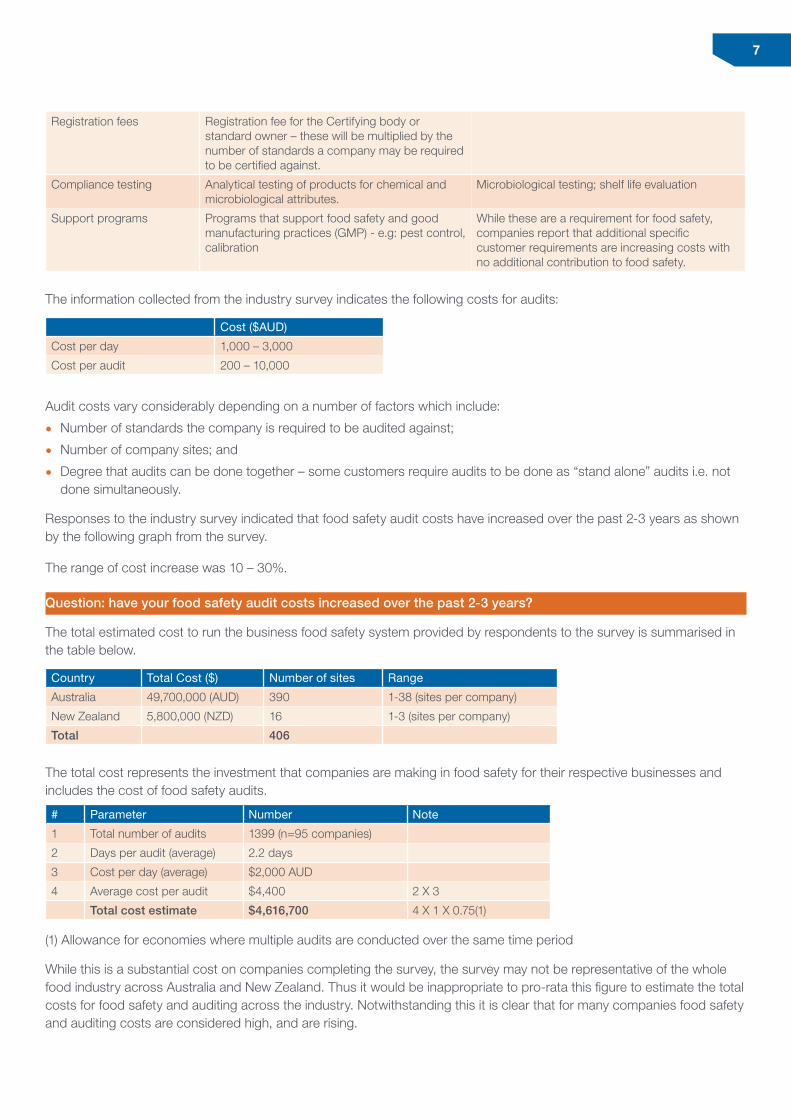

Cost of food safety management and food safety auditsThe scoping study has confirmed that food safety auditing in Australia and New Zealand places a substantial burden on the food industry as a result of the proliferation of a large number of proprietary and private standards. The industry survey, which was by far the most comprehensive survey of its type yet conducted in Australia revealed that food safety management costs of responding companies are AUD$49,700,000 p.a. The cost for New Zealand was NZD$5,800,000. These estimates include AUD$4,600,000 of food safety audits costs.

Specific issues identified in the survey and in one on one interviews included:

• the number of food safety audits conducted is higher than necessary to provide for safe foods;

• there is duplication of food safety requirements across these audits imposing unnecessary costs on food companies;

• the level of prescriptive requirements in standards is increasing counter to the established principle of standards being outcomes-based, as the best means of assuring food safety;

• auditor availability and competencies across all food categories is creating difficulties for companies trying to schedule audits; and

• the overall costs of food safety audits on businesses is increasing.

The information collected from the activities described in this section provided an insight into the costs for business of food safety management and food safety audits.

The food industry survey asked companies to estimate the total cost to their business to run the food safety system. The types of costs included varied across respondents, some of the cost types are set out below:

Cost type Description Examples

Staff Cost for permanent, part time staff or consultants/contractors to develop and maintain the food safety system.

Training of staff on standard and audit requirements

Salary and wages, on costs such as superannuation, insurance.

Consultant/contractor fees.

Preparation and follow up time for audits

Time for staff to prepare for audits and manage close out of any non-conformances (sometimes in duplicate).

Conduct mock recalls – generally each customer requires a mock recall to be conducted on their product meaning that multiple mock recall exercises may be conducted.

Audit Cost for auditor to conduct the audit and write up the audit report. May include travel and accommodation costs.

Cost of staff time

Where a company is audited against a number of standards this cost will reflect the time to write up multiple reports.

6

Registration fees Registration fee for the Certifying body or standard owner – these will be multiplied by the number of standards a company may be required to be certified against.

Compliance testing Analytical testing of products for chemical and microbiological attributes.

Microbiological testing; shelf life evaluation

Support programs Programs that support food safety and good manufacturing practices (GMP) - e.g: pest control, calibration

While these are a requirement for food safety, companies report that additional specific customer requirements are increasing costs with no additional contribution to food safety.

The information collected from the industry survey indicates the following costs for audits:

Cost ($AUD)

Cost per day 1,000 – 3,000

Cost per audit 200 – 10,000

Audit costs vary considerably depending on a number of factors which include:

• Number of standards the company is required to be audited against;

• Number of company sites; and

• Degree that audits can be done together – some customers require audits to be done as “stand alone” audits i.e. not done simultaneously.

Responses to the industry survey indicated that food safety audit costs have increased over the past 2-3 years as shown by the following graph from the survey.

The range of cost increase was 10 – 30%.

Question: have your food safety audit costs increased over the past 2-3 years?

The total estimated cost to run the business food safety system provided by respondents to the survey is summarised in the table below.

Country Total Cost ($) Number of sites Range

Australia 49,700,000 (AUD) 390 1-38 (sites per company)

New Zealand 5,800,000 (NZD) 16 1-3 (sites per company)

Total 406

The total cost represents the investment that companies are making in food safety for their respective businesses and includes the cost of food safety audits.

# Parameter Number Note

1 Total number of audits 1399 (n=95 companies)

2 Days per audit (average) 2.2 days

3 Cost per day (average) $2,000 AUD

4 Average cost per audit $4,400 2 X 3

Total cost estimate $4,616,700 4 X 1 X 0.75(1)

(1) Allowance for economies where multiple audits are conducted over the same time period

While this is a substantial cost on companies completing the survey, the survey may not be representative of the whole food industry across Australia and New Zealand. Thus it would be inappropriate to pro-rata this figure to estimate the total costs for food safety and auditing across the industry. Notwithstanding this it is clear that for many companies food safety and auditing costs are considered high, and are rising.

7

Industry round tableAn industry round table was held in Sydney on August 6th. The event was attended by a range of stakeholders from Industry, Government, Certifying Bodies, Retailers, and Food Service.

Following presentations of the results of the industry survey and an industry case study extensive group discussion of the key outcomes from the round table were as follows:

1. Food safety auditing places a substantial resource demand on the food industry. At the same time there are concerns current that auditing practices are not always providing the assurance of food safety required. As such it is an area that demands further work and attention.

2. Industry would benefit from a streamlining of food safety audits through reducing the number of standards used by the industry, identifying the critical common elements of food standards, and agreeing on a standard reporting format.

3. Any work undertaken to better coordinate food safety auditing across the food industry must not compromise food safety outcomes.

4. Cross recognition of food safety standards and audit outcomes would benefit the industry but this requires greater levels of confidence in audit and auditor competencies.

5. Key attributes for safe food production by food companies identified through the industry survey were agreed by the roundtable participants.

8

Conclusion and recommendationsFor the first time reliable, detailed information of the costs of food safety systems and auditing has been obtained and those costs are large. This will provide the impetus further work in this area as the potential rewards are substantial for all stakeholders.

This scoping study has confirmed that food safety auditing in Australia and New Zealand does place a substantial burden on the food industry as a result of the proliferation of a large number of proprietary and private standards. The industry survey, which was by far the most comprehensive survey of its type yet conducted in Australia revealed that food safety management costs of responding companies are AUD$49,700,000 p.a. The cost for New Zealand was NZD$5,800,000 (NZD). These estimates include $4,600,000 of food safety audits costs.

Substantial resources are required by industry in managing the different audit requirements as well as paying for audits of their food production operations. Cross-recognition of standards does occur, but it is at a low level. This represents inefficiency and therefore an unnecessary cost burden on industry.

The industry survey and follow-up interviews indicated that the situation is worsening providing impetus for greater coordination of food safety auditing across the sector.

To a large extent the Scoping Study has confirmed what has already been known i.e. that food safety auditing is imposing substantial cost on industry, at least a portion of which could be avoided through greater coordination. Its real value however has been in two areas:

1. for the first time reliable, detailed information of the costs of food safety systems and auditing , and the driver of those costs has been obtained; and

2. engagement with stakeholders across the industry as identified firstly, agreement that the industry would benefit from greater coordination of food safety auditing, and secondly, that there is now a willingness amongst stakeholders to work cooperatively across the industry to streamline food safety auditing practices.

The major conclusion is that further work in this area is warranted as the potential rewards are substantial for all stakeholders.

Next stepsThe AFGC proposes that the next steps will include:

1. Further work on the Food Safety Attributes for the FISCI. Whilst the key Food Safety Attributes have been identified and reported as part of the Scoping Study the AFGC will provide support to AusIndustry as they are adopted within the FISCI.

2. Seeking agreement from stakeholders to continue to work on food safety auditing. The AFGC will coordinate discussions through the AFGC Secretariat.

3. Further develop the Business Case for the rationalisation of auditing in the Baked Goods category. This will include refinement of the cost/benefit analysis with the information gathered in this Scoping Project.

4. Seek funding to continue to the Food Safety Auditing project (Baked Goods) from industry and government, as a public private partnership. This reflects the direct benefits to industry, to government, and the wider community of improving the efficiency and effectiveness of food safety auditing in Australia.

ContactFurther information on the Food Safety Auditing Project and this report can be obtained from the AFGC as follows:

Fiona Fleming, Advisor Policy and Regulation: [email protected]

9

AcknowledgementsThe AFGC wishes to acknowledge the funding and support provided by Food Innovation Australia Limited (FIAL) and AusIndustry for this scoping study.

The AFGC also wishes to acknowledge the input and contribution of the Food Safety Auditing Project Management Committee, their industry expertise and experience as key stakeholders has been invaluable in achieving the outcomes of this project. Organisations represented on the management committee and contributing their expertise were ALDI, Coles Supermarkets, Metcash Limited, Woolworths Supermarkets, Exemplar Global, Goodman Fielder, Compass Group Australia, McDonalds Australia, SAI Global, Sanitarium Health and Wellbeing Australia, Quick Service Restaurant (QSR) Holdings and General Mills Australia.

In addition we acknowledge the input of Foodlink Management Services representing the Global Food Safety Initiative (GFSI) for their input to the project and specifically the food safety attributes work.

The AFGC also thanks the companies which agreed to provide case studies detailing the impact of auditing and how it is managed within their businesses.

The AFGC is also grateful for the support it received from other industry associations and organisations which agreed to forward a survey to members and contacts on their mailing this. They were:

• New Zealand Food and Grocery Council

• Food and Beverage Importers Association

• Food Innovation Australia Limited

• Australian Institute of Food Science and Technology

• Grains & Legumes Nutrition Council

• Allergen Bureau

• Hamilton Grant

• Infant Nutrition Council

• Department of Agriculture

• FoodSA

• Food Industries Association of Queensland (FIAQ)

• Path4Find

• Dairy Food Safety Victoria

• Department of Agriculture and Food (WA)

10

Appendix: Food Safety Auditing Project – Food Industry Survey Report

11

1. IntroductionThis survey was conducted as part of wider AFGC project supported by Food Innovation Australia Ltd (FIAL) and AusIndustry.

An introduction and background to this Industry Survey is provided in the main body of this report.

2. Methodology2.1 Survey design and developmentThe survey questions were prepared by the AFGC Secretariat in consultation with the Food Safety Auditing Project Management Committee.

The survey was developed and conducted using SurveyMonkey® (https://www.surveymonkey.net/home/).

Survey structure

The survey consisted of 32 questions which were a mix of multiple choice and yes/no responses. The option to provide free text comments was provided for most questions to give participants the opportunity to elaborate on their responses or provide further details.

The questions in the survey did not include mandatory responses - participants were able to skip questions they did not wish to answer or which were not applicable to their business. To reduce the chance of more than one response being received from companies the survey requested participants to check that others in their business were not also responding to the survey.

A copy of the survey questions is provided with this Appendix.

2.2 Method of deliveryAn invitation to participate in the survey was distributed via email to over 6,500 email addresses via the mailing lists identified by the AFGC as part of the food safety auditing project. The survey was conducted in both Australia and New Zealand. The invitation contained a link to the survey in SurveyMonkey®. Participants were not provided with an opportunity to complete a paper copy of the survey. The survey was sent out on Wednesday July 8th and was open until Monday August 3rd.

3. Results3.1 Response rate

Survey invitations sent 6,504

Responses received 230

Response rate 3.5%

Duplicate responses

A total of 123 respondents provided their name and 115 provided the Company name. This information was used to identify any duplicate responses – two sets of duplicate responses were identified. The duplicate responses were followed up by the AFGC with the companies concerned who subsequently confirmed the response to be recorded.

12

The balance of respondents did not provide company details and it was not possible to determine if there were duplicate responses recorded for these businesses. It is assumed that, after removing duplicates each response represents a company.

Response rate

The overall response rate was 3.5%. The responses received represented 225 companies and 659 manufacturing facilities across Australia and New Zealand.

The following graphs and information provide a summary of the feedback received via the survey.

The results are based on the 225 company responses received after resolving identified duplicate responses from companies that provided contact information. The remaining unidentified responses were treated as unique responses for the purpose of this survey.

The response counts will vary by question - questions were not set up requiring a mandatory response and some questions allowed more than one response to be selected.

The full data for each question in the survey is provided with this report.

3.2 Company information

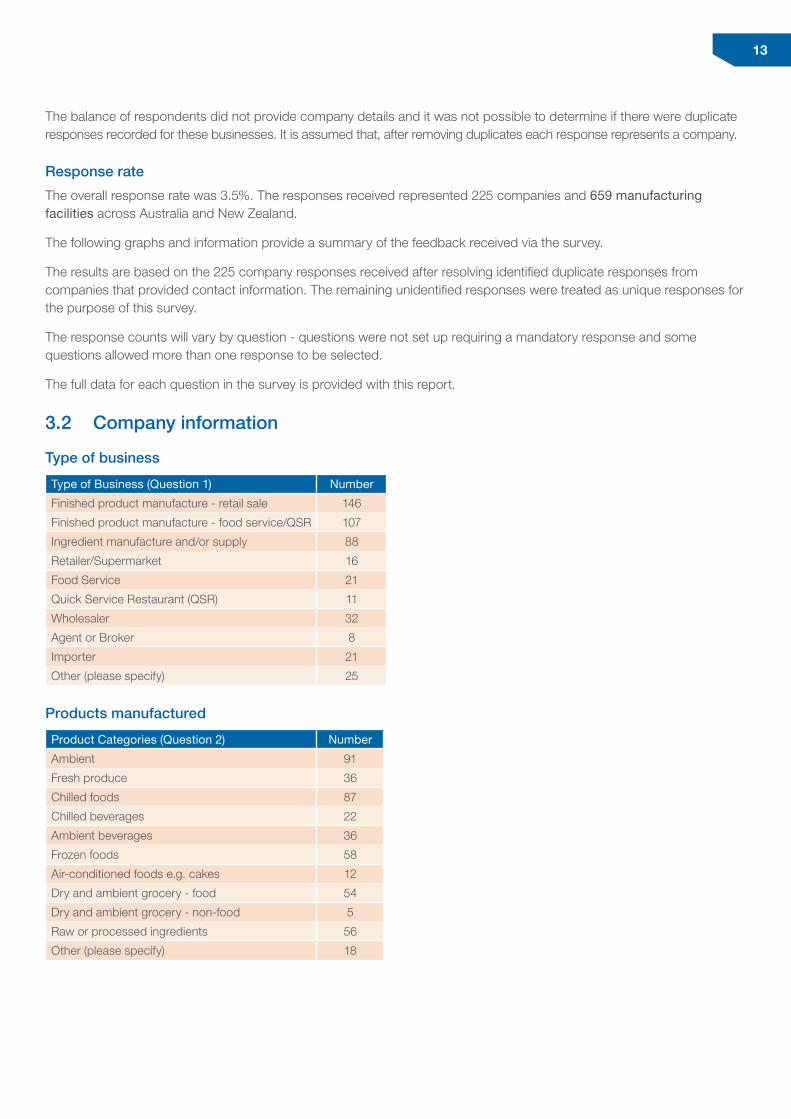

Type of business

Type of Business (Question 1) Number

Finished product manufacture - retail sale 146

Finished product manufacture - food service/QSR 107

Ingredient manufacture and/or supply 88

Retailer/Supermarket 16

Food Service 21

Quick Service Restaurant (QSR) 11

Wholesaler 32

Agent or Broker 8

Importer 21

Other (please specify) 25

Products manufactured

Product Categories (Question 2) Number

Ambient 91

Fresh produce 36

Chilled foods 87

Chilled beverages 22

Ambient beverages 36

Frozen foods 58

Air-conditioned foods e.g. cakes 12

Dry and ambient grocery - food 54

Dry and ambient grocery - non-food 5

Raw or processed ingredients 56

Other (please specify) 18

13

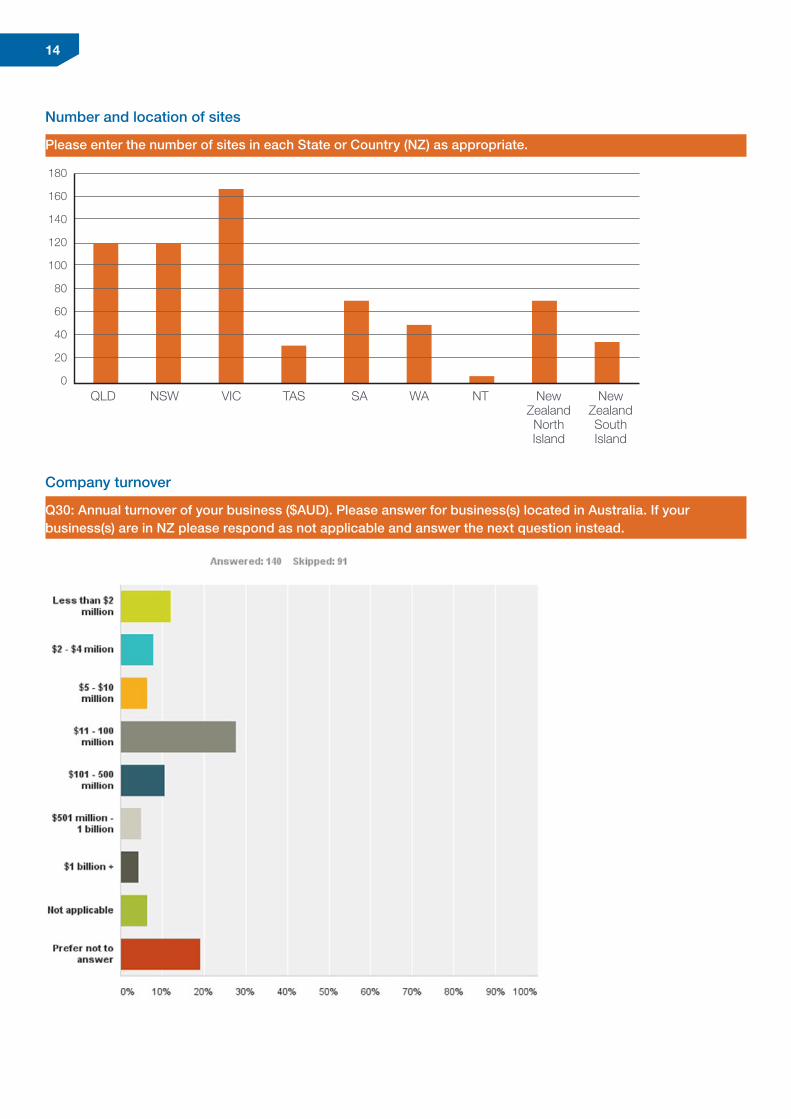

Number and location of sites

Please enter the number of sites in each State or Country (NZ) as appropriate.

QLD NSW VIC TAS SA WA NT NewZealandNorthIsland

NewZealandSouthIsland

180

160

140

120

100

80

60

40

20

0

Company turnover

Q30: Annual turnover of your business ($AUD). Please answer for business(s) located in Australia. If your business(s) are in NZ please respond as not applicable and answer the next question instead.

14

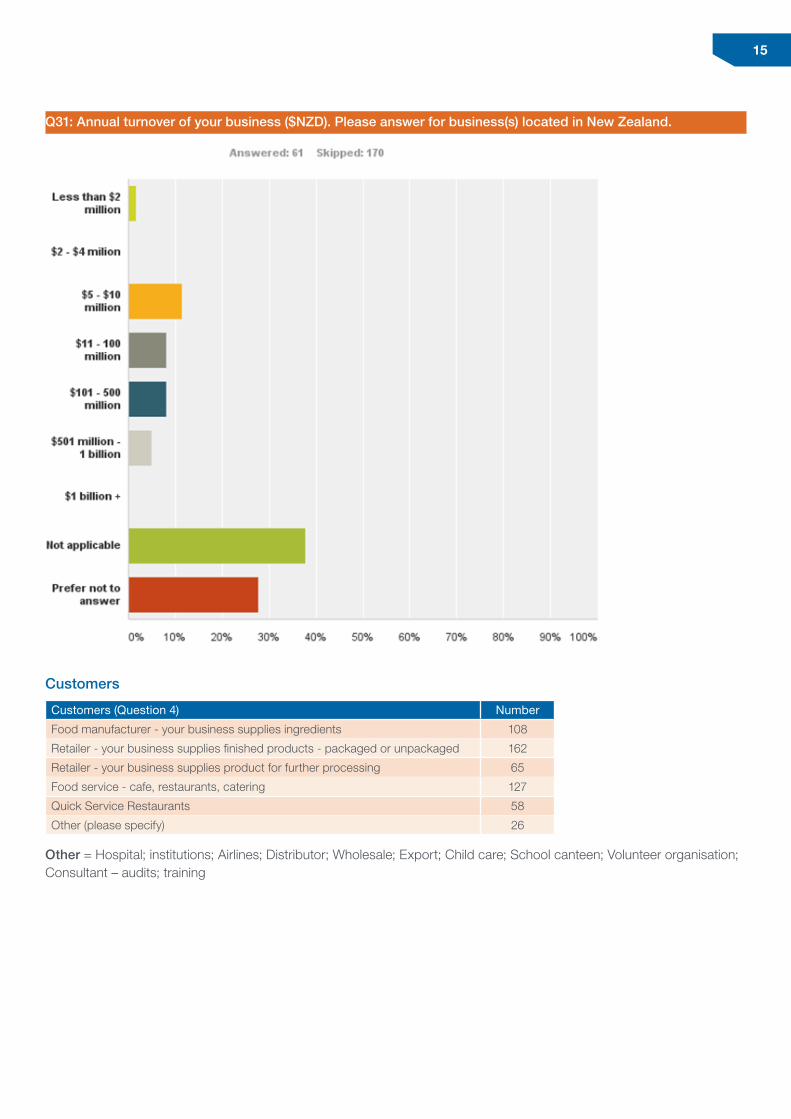

Q31: Annual turnover of your business ($NZD). Please answer for business(s) located in New Zealand.

Customers

Customers (Question 4) Number

Food manufacturer - your business supplies ingredients 108

Retailer - your business supplies finished products - packaged or unpackaged 162

Retailer - your business supplies product for further processing 65

Food service - cafe, restaurants, catering 127

Quick Service Restaurants 58

Other (please specify) 26

Other = Hospital; institutions; Airlines; Distributor; Wholesale; Export; Child care; School canteen; Volunteer organisation; Consultant – audits; training

15

3.3 Food safety programs

Food safety standards

What food safety standards does your business comply with or is audited against? Some examples are listed below.

Codex HACCP SQF (Safe FSSC (Food IFS BRC (British Quality Food) Safety System (International Retail Certification) Featured Consortium) Standards) Global Food Standard Standard for Food Safety

90%80%70%60%50%40%30%20%10%0%

Other standards

Standard Retailers QSR Food Service Industry Government

Global GAP BRC McDonalds Spotless Kraft MPI

Freshcare WQA YUM Compass Unilever Dept of Ag

Coles Subway Sodexo Nestlé DFSV

ALDI Gloria Jeans Q Catering Mars Primesafe

Metcash Hungry Jacks Heinz State Govt

Costco Burger King Pepsico Local Govt

Walmart Goodman Fielder

GWF

Food safety management – resources

How many full time equivalent (FTE) staff does your business employ to implement and maintain the food safety system?

Measure Number

Full time equivalents (FTE’s) across all sites 839

Number of sites 474

Range 0.1 - 47

Number of responses 161

Not all respondents answered this question

Food safety program – cost

What is the estimated cost to your business to run the food safety system?

Country Total Cost ($) Number of sites Range

Australia 49,700,000 (AUD) 390 1-38 Sites per company

New Zealand 5,800,000 (NZD) 16 1-3 Sites per Company

Total 406

16

3.4 Food safety auditing

Audit value

When you consider food safety audits conducted on your business, is it your view that:

Food Safety Audits Food Safety audits Food Safety audits Other (please are a cost of doing provide value to my are an integral part specify) business business of managing food safety within our business

80%

70%

60%

50%

40%

30%

20%

10%

0%

Who conducts audits?

Audits conducted by (Question 8) Response Count

SAI Global 40

BSI Group 46

SGS Auditing Services 54

HACCP Australia 5

AsureQuality 25

Silliker 21

AusQual/Aus Meat 16

Coles 52

Woolworths 56

ALDI 34

Metcash 7

Costco 11

Countdown 4

Foodstuffs 2

Commonwealth Government 20

State or Territory Health Department 63

NZ MPI 21

Other (please specify) 73

Other = Spotless; YUM; PIRSA; Walmart; Tesco; Sainsbury; ASDA; DAFF; Lite n Easy; McCains; Vesco; US Army; Wendy’s; SciQual; AIB; Fonterra; Inghams; Caltex; National Food Safety Consulting; Lion

17

Number of audits

Number of food safety audits overall

Number commissioned by your business on your

business

Number commissioned to meet customer supply

requirements

Number 1424 415 1009

Range 1 - 192 0 - 47 0 – 145

Average 14.9 4.3 10.6

n = 94

Audit time

How many days does it take (on average) to complete a food safety audit on your business?

Days

Range 0.5 - 10

Average 2.2

n = 151

What is the estimated time for a food safety audit - overall time per year?

Days

Range 0.5 - 240

Average 22.8

n = 122 (some multiple site companies)

Audit cost

What is the estimated cost of a food safety audit?

Cost per audit $AUD

Range 200 – 10,000

Cost per day $AUD

Range 1,000 – 3,000

18

Audit burden

Has the number of food safety audits increased for your business over the past 2-3 years?

2015

2013

19

Have your food safety audit costs increased over the past 2-3 years?

Has the complexity and associated time for food safety audits increased over the past 2-3 years?

Mutual recognition

Q26: Does your company accept food safety audits and/or audit reports commissioned by other companies?

20

What are the pre-conditions for your company to accept food safety audits and audit reports commissioned by other parties (i.e. provide cross-recognition). You may select more than one option below.

Answer OptionsResponse Percent

Response Count

Standardised provisions of common elements for food safety audits 49.6% 62

Standardised report format 12.8% 16

Agreed category specific auditor competencies 14.4% 18

Audit conducted by an accredited auditing/certifying body 84.8% 106

Other(s) 10.4% 13

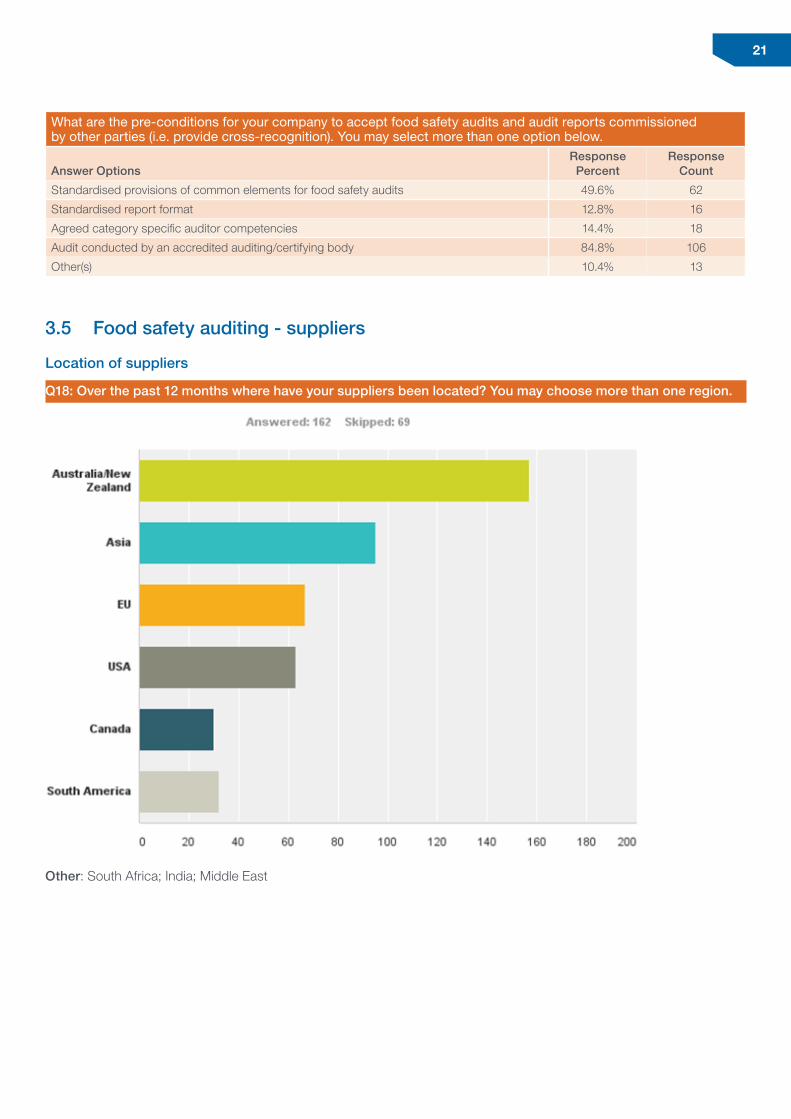

3.5 Food safety auditing - suppliers

Location of suppliers

Q18: Over the past 12 months where have your suppliers been located? You may choose more than one region.

Other: South Africa; India; Middle East

21

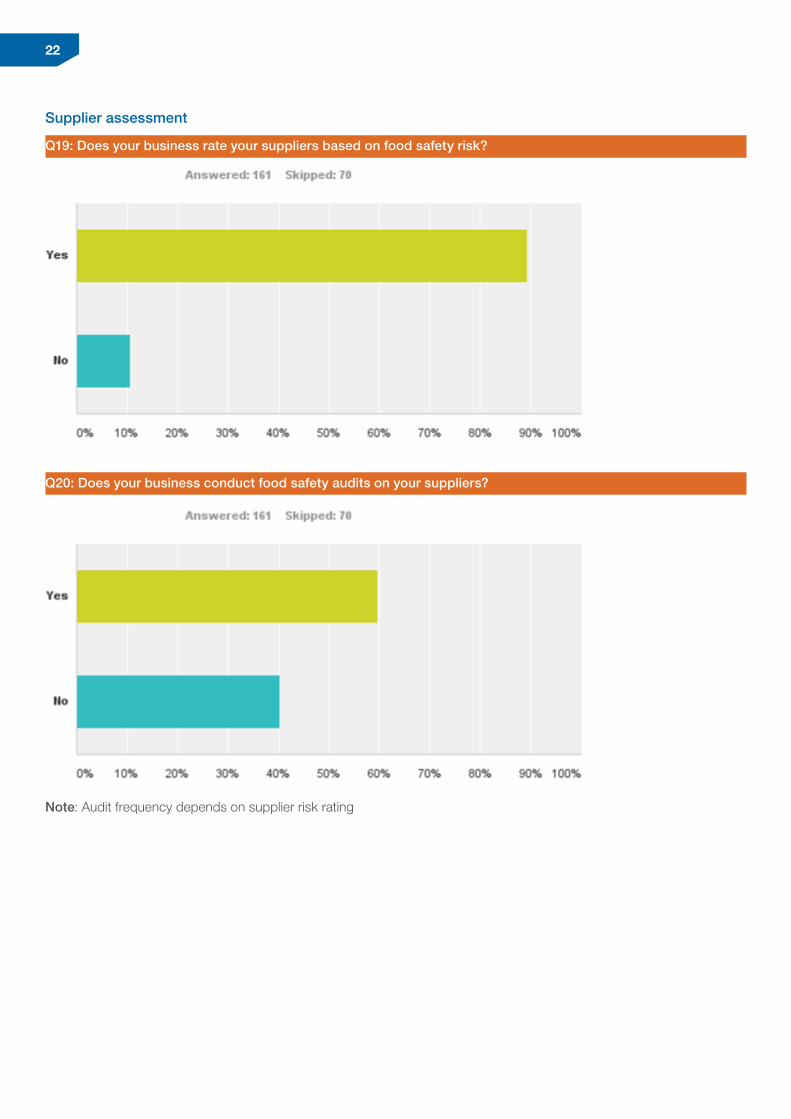

Supplier assessment

Q19: Does your business rate your suppliers based on food safety risk?

Q20: Does your business conduct food safety audits on your suppliers?

Note: Audit frequency depends on supplier risk rating

22

Q21: How often do you audit your suppliers?

Note: Company auditors – company staff

Q22: Who conducts these audits on your suppliers? You may choose more than one response.

23

Q22: Does your business use a questionnaire to evaluate suppliers?

Supplier audit standards

Q23: What food safety standards does your business audit your suppliers against? You may choose more than one.

Other: Internal company standard; ISO 22000; In house; YUM; Global GAP; Freshcare

What are the pre-conditions for your company to accept food safety audits and audit reports commissioned by other parties (i.e. provide cross-recognition). You may select more than one option below.

Answer OptionsResponse Percent

Response Count

Standardised provisions of common elements for food safety audits 49.6% 62

Standardised report format 12.8% 16

Agreed category specific auditor competencies 14.4% 18

Audit conducted by an accredited auditing/certifying body 84.8% 106

Other(s) 10.4% 13

24

4. Discussion and conclusionAlthough the response rate was low (3.5%) the very large of number of industry people contacted through the extensive email lists of other organisations resulted in a relatively large number of survey participants with 225 companies and 659 manufacturing sites represented.

The survey also recorded responses from many different types of business with all major food categories represented, from large, medium and small businesses and from companies operating all across Australia and New Zealand, with all states and territories represented, except the ACT.

It is valuable having data from New Zealand as many Australian companies operate in both markets and many New Zealand companies export to Australia.

Notwithstanding this, the data should not be considered as completely representative of the food industry across Australia and New Zealand. Thus quantitative data from the survey should not be adjusted on a pro-rata basis to provide estimates across the whole industry, or indeed subsectors of it.

The survey does, however, represent the most robust body of information yet collected and collated by the food industry on the issue of food safety auditing. It provides a number of insights into the issues faced by the industry in this area. These are discussed in greater detail in the main body of the report.

25

For further information on the Food Safety Auditing Project and this report please contact:

Fiona Fleming Advisor Policy and Regulation

Australian Food & Grocery Council

Australian Trade Commission