Food and Beverages Sector - EMIS Insight - Brazil Food a… · Brazil's food and beverages sector...

64

- 1 - Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Produced by: Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Food and Beverages Sector Brazil December 2014

Transcript of Food and Beverages Sector - EMIS Insight - Brazil Food a… · Brazil's food and beverages sector...

- 1 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Produced by:

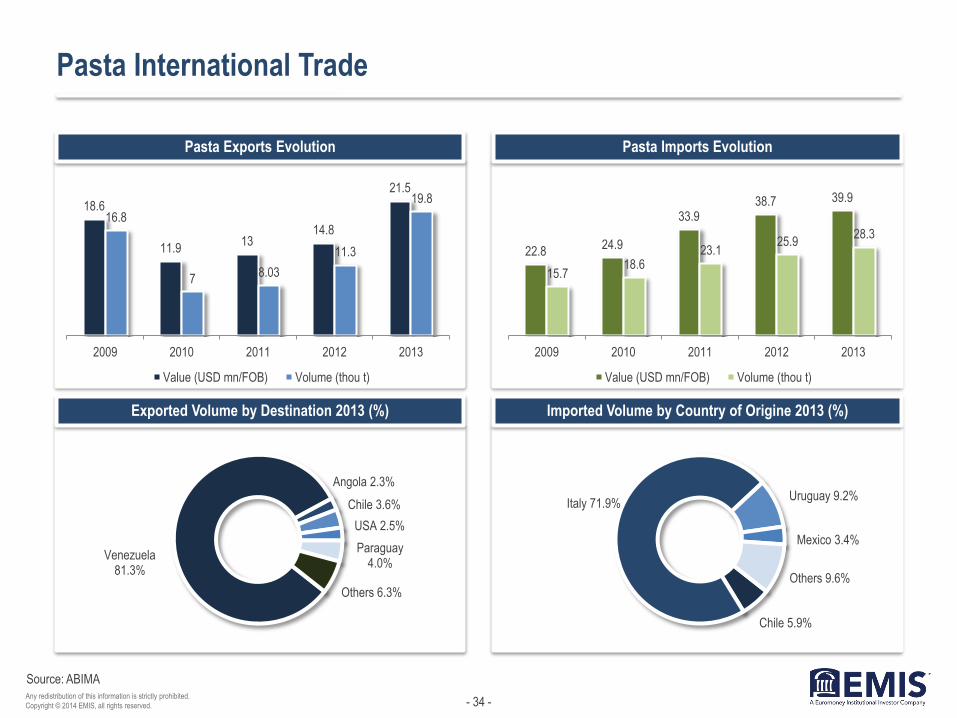

Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Food and Beverages

Sector Brazil

December 2014

- 2 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

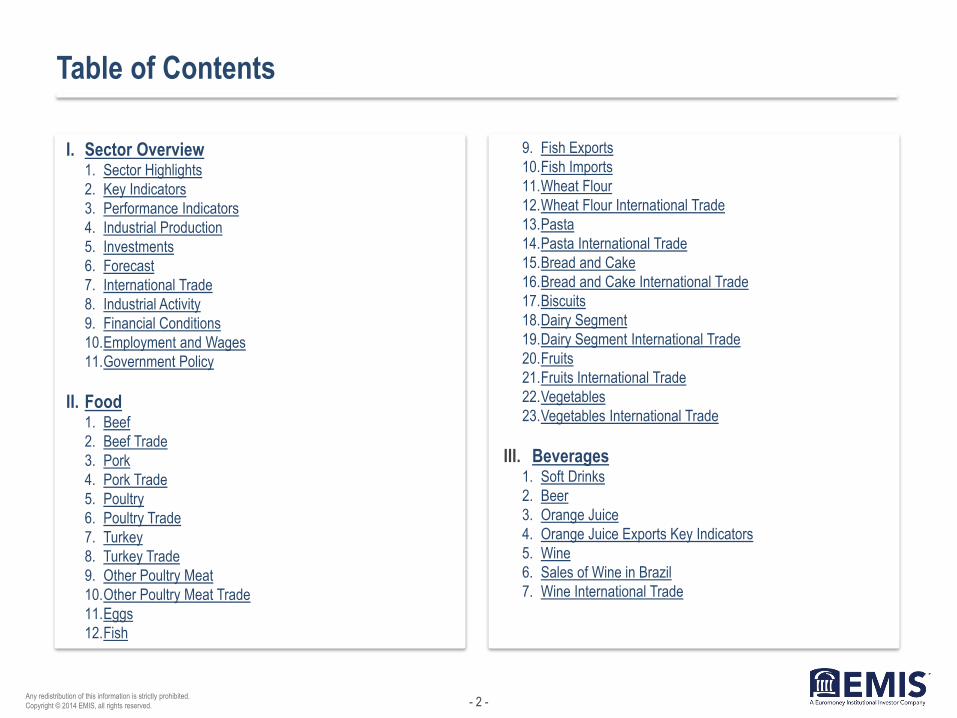

Table of Contents

I. Sector Overview 1. Sector Highlights

2. Key Indicators

3. Performance Indicators

4. Industrial Production

5. Investments

6. Forecast

7. International Trade

8. Industrial Activity

9. Financial Conditions

10.Employment and Wages

11.Government Policy

II. Food 1. Beef

2. Beef Trade

3. Pork

4. Pork Trade

5. Poultry

6. Poultry Trade

7. Turkey

8. Turkey Trade

9. Other Poultry Meat

10.Other Poultry Meat Trade

11.Eggs

12.Fish

9. Fish Exports

10.Fish Imports

11.Wheat Flour

12.Wheat Flour International Trade

13.Pasta

14.Pasta International Trade

15.Bread and Cake

16.Bread and Cake International Trade

17.Biscuits

18.Dairy Segment

19.Dairy Segment International Trade

20.Fruits

21.Fruits International Trade

22.Vegetables

23.Vegetables International Trade

III. Beverages 1. Soft Drinks

2. Beer

3. Orange Juice

4. Orange Juice Exports Key Indicators

5. Wine

6. Sales of Wine in Brazil

7. Wine International Trade

- 3 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Table of Contents

IV. Main Players 1. BRF

2. BRF (cont’d)

3. BRF (cont’d)

4. JBS

5. JBS (cont’d)

6. Marfrig Global Foods

7. Marfrig Global Foods (cont’d)

8. Ambev

9. Ambev (cont’d)

10.Vigor Alimentos

11.Vigor Alimentos (cont’d)

- 4 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

I. Sector Overview

- 5 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Sector Highlights

Brazil's beverages sector experienced strong growth in the past few years. The cumulative growth of physical production of beverages reached 50%

between 2004 and 2013. Notably, the average annual growth rate of beverages production in the last decade stood at 4.2%, while the average

annual growth rate of the country's GDP over the same period was 3.7%. The sector is dominated by the soft drinks and beer segments. Currently,

Brazil is the third-largest producer and consumer of soft drinks and beer in the world. Interestingly, despite the almost non-existent imports of soft

drinks and beer in Brazil, the segment's share in the country's overall imports is constantly growing due to the rise in imported raw materials,

especially the imports of malt.

The food sector is among the most dynamic in the Brazilian economy. The country is home to the largest players in the global meat market and

leading exporter of sugar, soybean and other raw materials for the food industry. The growth of the sector is strongly supported by the large and fast

growing consumer market. In addition, some local companies have strongly expanded abroad by acquiring international brands. Almost 100% of the

local demand is met by local companies or foreign entities operating in Brazil. The sector's imports are predominantly of some products in the

premium segment and also raw materials like wheat and wheat flour, milk powder and cocoa. The food sector in Brazil is highly concentrated, less

than 1% of the companies account for more than half of the production gross value.

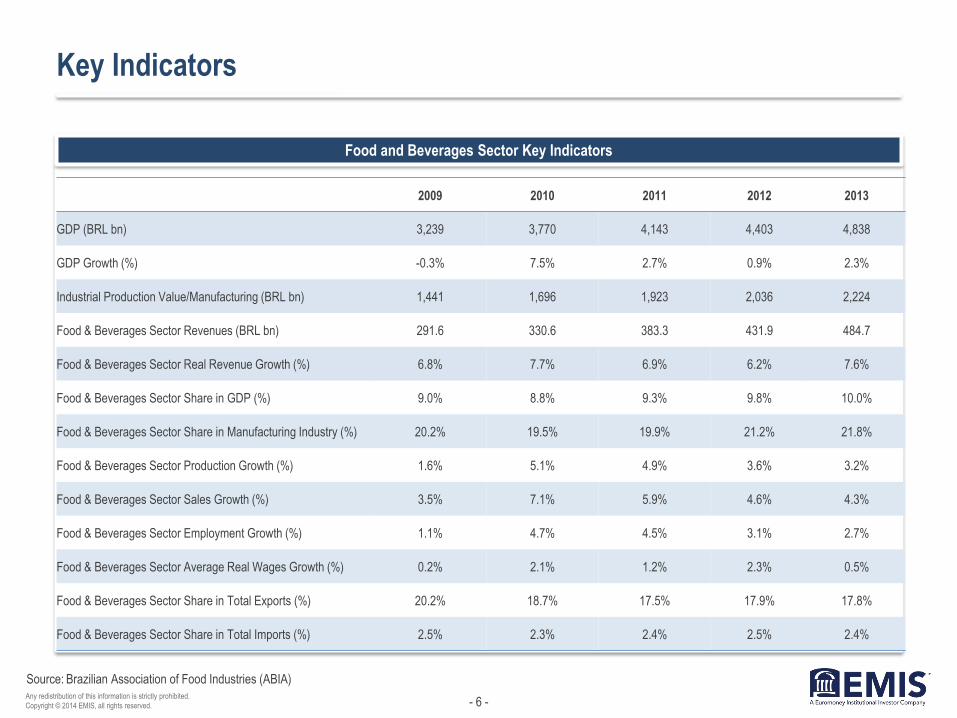

Brazil's food and beverages sector accounts for 10% of the country's GDP and is its largest exporter. In 2013, the revenues of the sector reached

BRL 485bn, an 11% increase from 2012. Currently, the food and beverages manufacturing industry is the second-largest segment of the

manufacturing industry in terms of gross output, behind only the petrochemical industry. Underpinned by rising domestic and foreign demand, the

sales in the sector are constantly growing despite the current slowdown of Brazil's economy.

There are about 32,000 companies operating in the food and beverages sector and they employ about 19% of the working population in the country.

Overview

Food

Beverages

- 6 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Key Indicators

Food and Beverages Sector Key Indicators

Brazilian Association of Food Industries (ABIA)

2009 2010 2011 2012 2013

GDP (BRL bn) 3,239 3,770 4,143 4,403 4,838

GDP Growth (%) -0.3% 7.5% 2.7% 0.9% 2.3%

Industrial Production Value/Manufacturing (BRL bn) 1,441 1,696 1,923 2,036 2,224

Food & Beverages Sector Revenues (BRL bn) 291.6 330.6 383.3 431.9 484.7

Food & Beverages Sector Real Revenue Growth (%) 6.8% 7.7% 6.9% 6.2% 7.6%

Food & Beverages Sector Share in GDP (%) 9.0% 8.8% 9.3% 9.8% 10.0%

Food & Beverages Sector Share in Manufacturing Industry (%) 20.2% 19.5% 19.9% 21.2% 21.8%

Food & Beverages Sector Production Growth (%) 1.6% 5.1% 4.9% 3.6% 3.2%

Food & Beverages Sector Sales Growth (%) 3.5% 7.1% 5.9% 4.6% 4.3%

Food & Beverages Sector Employment Growth (%) 1.1% 4.7% 4.5% 3.1% 2.7%

Food & Beverages Sector Average Real Wages Growth (%) 0.2% 2.1% 1.2% 2.3% 0.5%

Food & Beverages Sector Share in Total Exports (%) 20.2% 18.7% 17.5% 17.9% 17.8%

Food & Beverages Sector Share in Total Imports (%) 2.5% 2.3% 2.4% 2.5% 2.4%

- 7 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Performance Indicators

Financial Performance (BRL bn)

Domestic Sales Segmentation (BRL bn)

Main Segments Revenue Evolution (BRL bn)

ABIA

246.7 274.6 316.5 353.9 394.6

45.0 56.0

66.8 78.0

90.1

291.7 330.6

383.3 431.9

484.7

2009 2010 2011 2012 2013

Food Subsector Revenues Beverages Subsector Revenues

159.1 179.5 203.5 227.9 255.6

65.0 75.7

87.9 100.9

116.6

224.1 255.1

291.5 328.7

372.2

2009 2010 2011 2012 2013

Retail Food Service

17.7

15.6

19.9

37.7

29.3

33.1

35.9

66.0

20.5

18.2

21.4

42.2

34.5

38.1

40.6

79.1

24.2

20.4

23.5

41.9

40.9

42.2

46.9

88.7

28.7

23.7

26.8

40.9

42.3

50.1

52.8

100.8

Spices, Slat Deserts & IceCream,

Fruit & Vegetables

Corn & Corn Derivatives

Sweets

Oils & Fats

Dairy Segment

Coffee, Tea and Cereal

Meat & Processed Meat

2013

2012

2011

2010

- 8 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

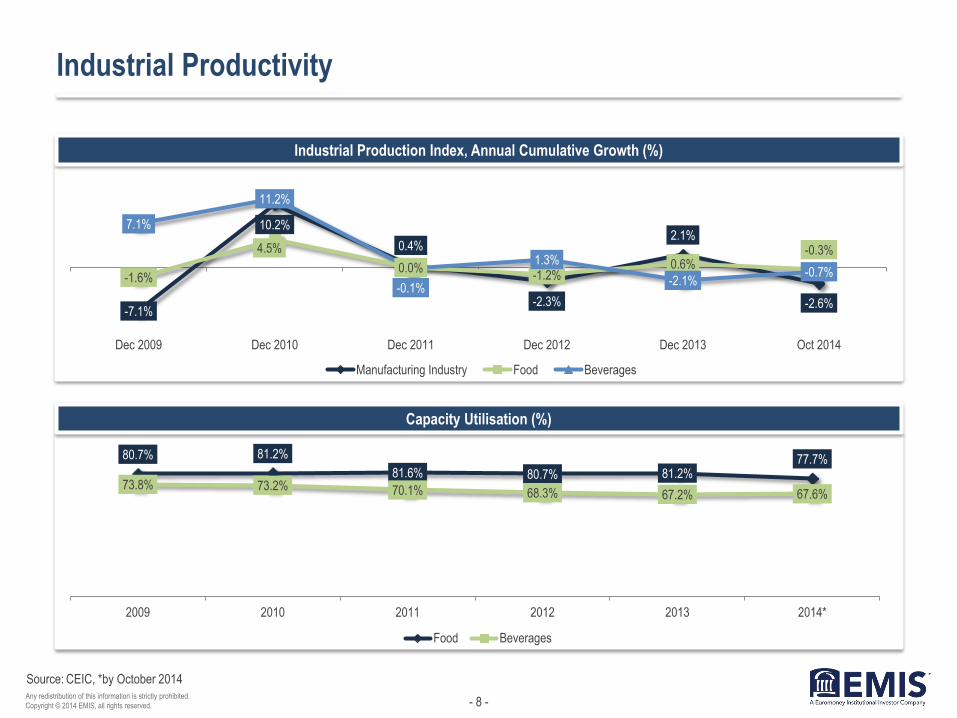

Industrial Productivity

Industrial Production Index, Annual Cumulative Growth (%)

Capacity Utilisation (%)

CEIC, *by October 2014

80.7% 81.2%

81.6% 80.7% 81.2% 77.7%

73.8% 73.2% 70.1% 68.3% 67.2% 67.6%

2009 2010 2011 2012 2013 2014*

Food Beverages

-7.1%

10.2%

0.4%

-2.3%

2.1%

-2.6%

-1.6%

4.5%

0.0% -1.2%

0.6% -0.3%

7.1%

11.2%

-0.1%

1.3%

-2.1% -0.7%

Dec 2009 Dec 2010 Dec 2011 Dec 2012 Dec 2013 Oct 2014

Manufacturing Industry Food Beverages

- 9 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Investments

The overall investments in the food and beverages sector in 2013 reached BRL 15bn, a 26% increase from the previous year. The funds were mainly used

for capacity upgrade and expansion.

The future investments announced by food sector players are predominantly focused on the purchase of new machinery and equipment as well as the

diversification of their product portfolio, which focuses on processed foods rather than on fresh ones. In the case of beverages, the companies earmark

considerable investments for marketing campaigns in order to increase their market share. According to estimates by Brazil's state development bank

BNDES, investments in the segment will reach BRL 32bn by 2018.

FDI, Equity Capital Inflow (USD mn) BNDES Investments (BRL bn)

EMIS Insight, CEIC, BNDES

58

49

32

2010 - 2013 2015 - 2018

Foods Beverages

451.0

1,716.1

3,063.3

5,076.0

1,486.7

115.8 366.4

4,265.0

511.0 598.1

2009 2010 2011 2012 2013

Food Beverages

- 10 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

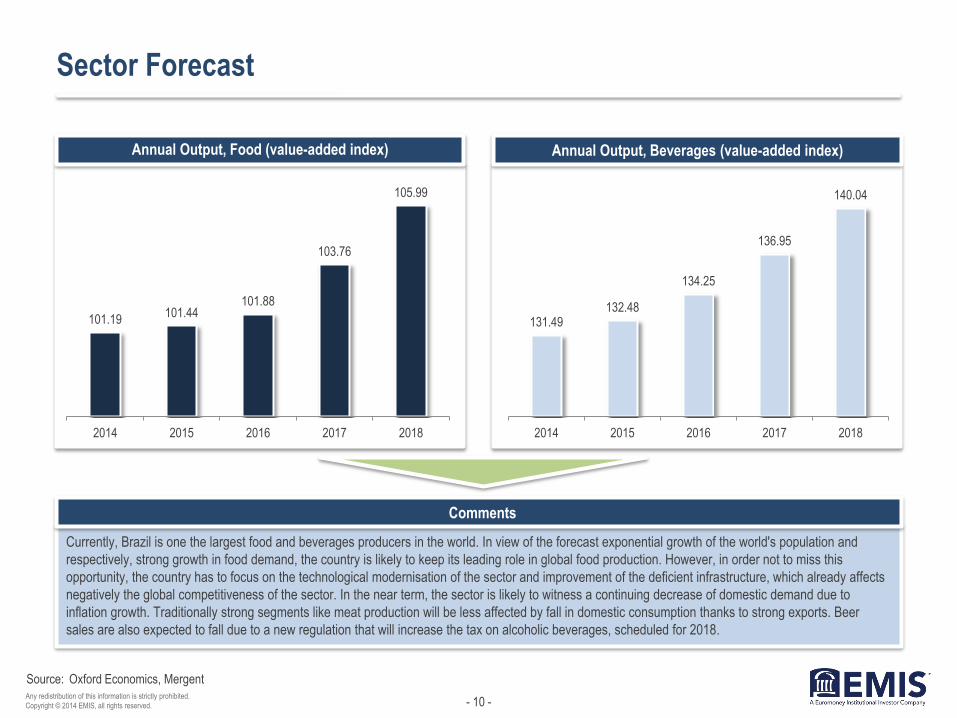

Sector Forecast

Currently, Brazil is one the largest food and beverages producers in the world. In view of the forecast exponential growth of the world's population and

respectively, strong growth in food demand, the country is likely to keep its leading role in global food production. However, in order not to miss this

opportunity, the country has to focus on the technological modernisation of the sector and improvement of the deficient infrastructure, which already affects

negatively the global competitiveness of the sector. In the near term, the sector is likely to witness a continuing decrease of domestic demand due to

inflation growth. Traditionally strong segments like meat production will be less affected by fall in domestic consumption thanks to strong exports. Beer

sales are also expected to fall due to a new regulation that will increase the tax on alcoholic beverages, scheduled for 2018.

Annual Output, Food (value-added index) Annual Output, Beverages (value-added index)

Oxford Economics, Mergent

101.19 101.44

101.88

103.76

105.99

2014 2015 2016 2017 2018

131.49 132.48

134.25

136.95

140.04

2014 2015 2016 2017 2018

- 11 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

International Trade

Food & Beverages Exports Evolution (USD bn)

Food & Beverages Trade Balance Evolution (USD bn)

Food & Beverages Imports Evolution (USD bn)

Comments

ABIA

Exports have a significant share in the sector's income, especially for

the food segment due to the leading role of Brazil as an exporter of

meat, orange juice, sugar and soybean products.

Imports have a small share on the domestic food market, restricted to

some segments, depending on the validity period and imports tariffs,

which are reflected on the final price of the products. Those are

predominantly foods in the premium segment like some fish species

and cheese. In the cheaper food segment, Brazil mainly imports

frozen fish and milk powder. In the case of beverages, the sector

mainly imports malt. However, in view of the increased production

capacity of domestic malt producers in the last few years, brewers

believe that their dependence on imports will shrink in the near future.

17.8 19.8

29.6 30.9 35.8

30.9

37.9

44.8 43.4 43

2009 2010 2011 2012 2013

Raw Foods Processed Food & Beverages

3.6

4.3 4.9 5.1

6.1

3.2

4.1

5.5 5.6 5.8

2009 2010 2011 2012 2013

Raw Foods Processed Food & Beverages

14.2 15.5

24.7 25.8 29.7

27.7

33.8

39.3 37.8 37.2

2009 2010 2011 2012 2013

Raw Foods Processed Food & Beverages

- 12 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

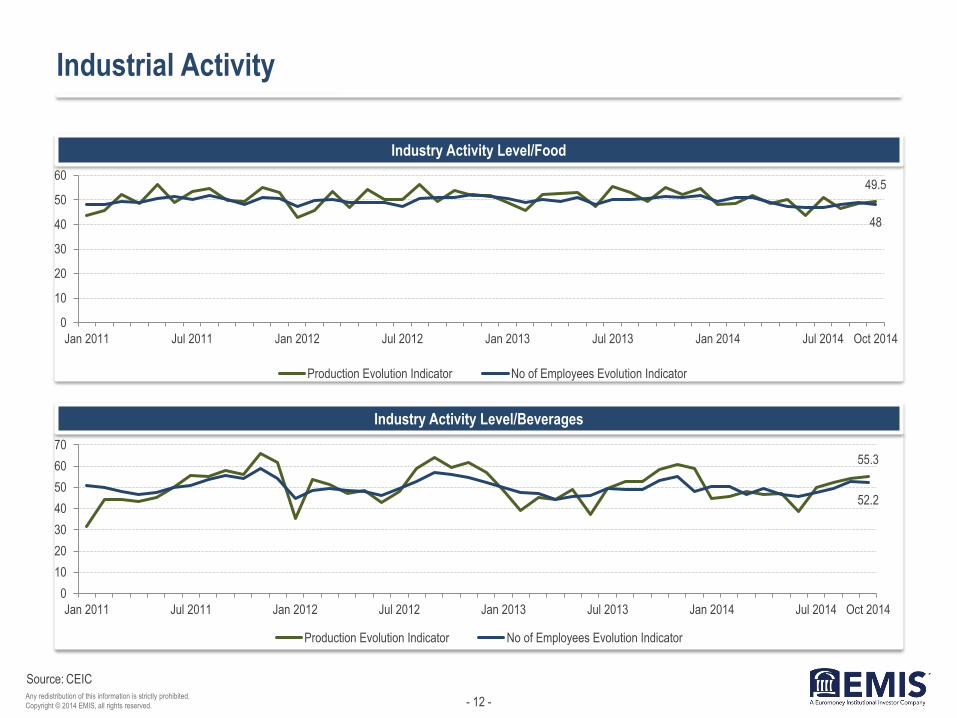

Industrial Activity

Industry Activity Level/Food

Industry Activity Level/Beverages

CEIC

49.5

48

0

10

20

30

40

50

60

Jan 2011 Jul 2011 Jan 2012 Jul 2012 Jan 2013 Jul 2013 Jan 2014 Jul 2014 Oct 2014

Production Evolution Indicator No of Employees Evolution Indicator

55.3

52.2

0

10

20

30

40

50

60

70

Jan 2011 Jul 2011 Jan 2012 Jul 2012 Jan 2013 Jul 2013 Jan 2014 Jul 2014 Oct 2014

Production Evolution Indicator No of Employees Evolution Indicator

- 13 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

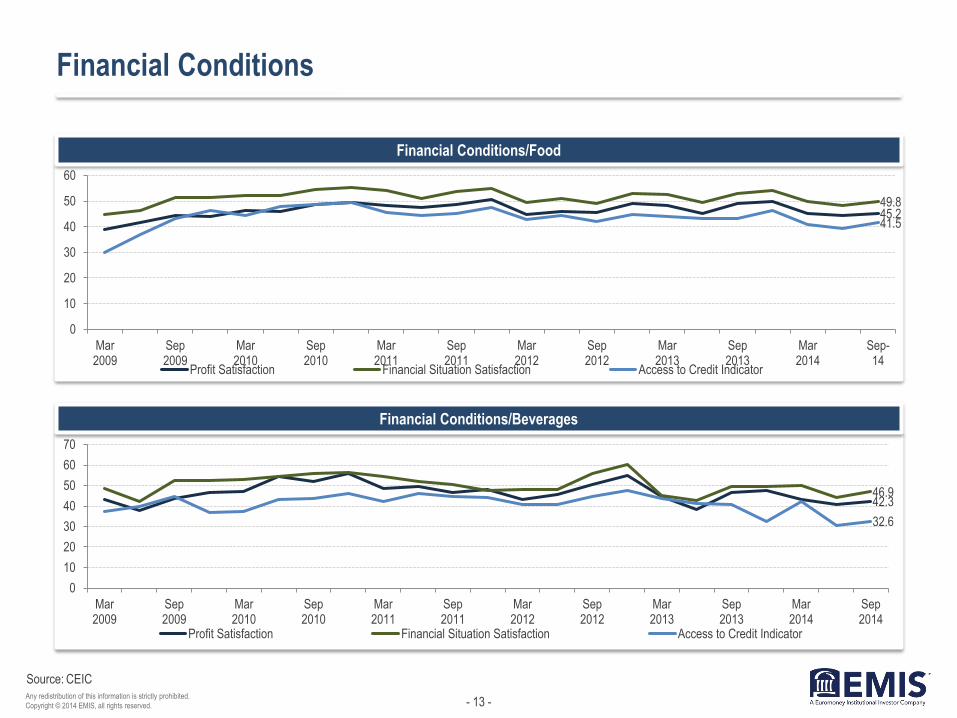

Financial Conditions

Financial Conditions/Food

Financial Conditions/Beverages

CEIC

45.2 49.8

41.5

0

10

20

30

40

50

60

Mar2009

Sep2009

Mar2010

Sep2010

Mar2011

Sep2011

Mar2012

Sep2012

Mar2013

Sep2013

Mar2014

Sep-14

Profit Satisfaction Financial Situation Satisfaction Access to Credit Indicator

42.3 46.9

32.6

0

10

20

30

40

50

60

70

Mar2009

Sep2009

Mar2010

Sep2010

Mar2011

Sep2011

Mar2012

Sep2012

Mar2013

Sep2013

Mar2014

Sep2014

Profit Satisfaction Financial Situation Satisfaction Access to Credit Indicator

- 14 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Employment and Wages

Employment (thou)

Wages and Productivity Evolution (%)

Sector's Share in Overall Manufacturing Industry (%)

Comments

ABIA, BNDES

The largest share of workers in the overall food and beverages sector

are employed in the food industry. The sector is among the biggest

employers in the country. The companies in the sector are often

located in the interior of the country and generate jobs and income in

smaller towns where the unemployment rates are traditionally higher.

The beverage segment is characterised as capital intensive, thus it

tends to have a lower importance as employer. However, it is

responsible for about 2.2% of the jobs in the overall manufacturing

industry of the country. The segment directly employs about 144,000

people, and more than 110,000 indirectly, predominantly engaged in

beverage retail sales.

1,437.8

1,527.3

1,583.7 1,585.6

1,626.1

2009 2010 2011 2012 2013

19.5% 19.4% 19.5% 19.5% 19.5%

1.1%

4.7% 4.5% 3.1% 2.7%

2009 2010 2011 2012 2013

Contribution to Employment in Man. Industry

Food & Beverages Employment Growth

5.3%

7.3% 7.9% 8.0%

7.1% 6.5% 6.8%

11.8% 12.6%

9.4%

2009 2010 2011 2012 2013

Nominal Average Wage Growth Revenue per Employee Growth

- 15 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

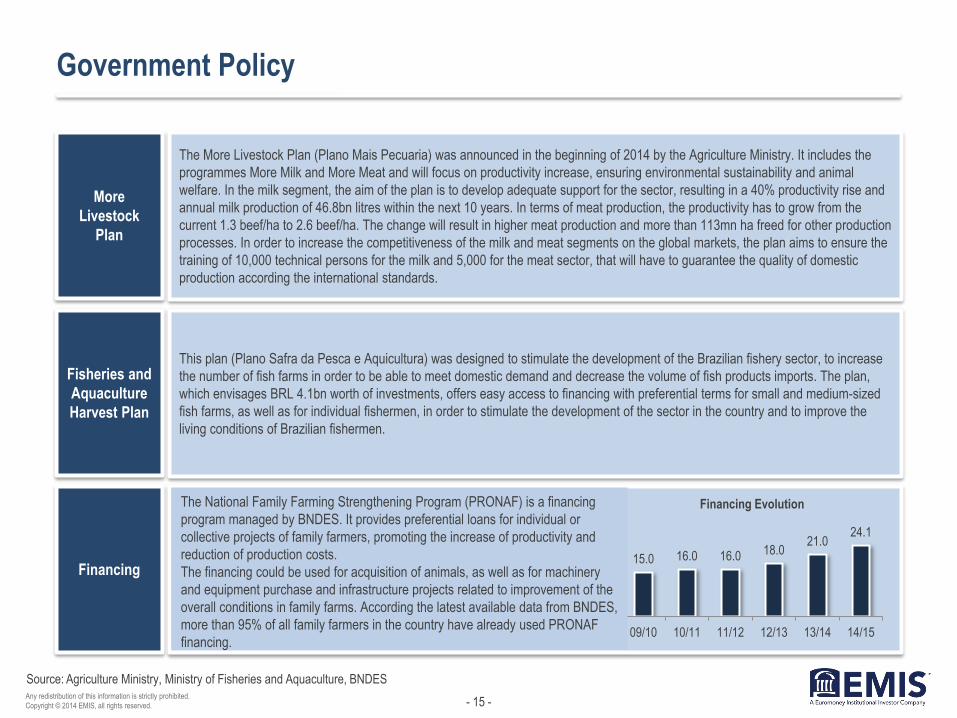

Government Policy

More

Livestock

Plan

The More Livestock Plan (Plano Mais Pecuaria) was announced in the beginning of 2014 by the Agriculture Ministry. It includes the

programmes More Milk and More Meat and will focus on productivity increase, ensuring environmental sustainability and animal

welfare. In the milk segment, the aim of the plan is to develop adequate support for the sector, resulting in a 40% productivity rise and

annual milk production of 46.8bn litres within the next 10 years. In terms of meat production, the productivity has to grow from the

current 1.3 beef/ha to 2.6 beef/ha. The change will result in higher meat production and more than 113mn ha freed for other production

processes. In order to increase the competitiveness of the milk and meat segments on the global markets, the plan aims to ensure the

training of 10,000 technical persons for the milk and 5,000 for the meat sector, that will have to guarantee the quality of domestic

production according the international standards.

Fisheries and

Aquaculture

Harvest Plan

This plan (Plano Safra da Pesca e Aquicultura) was designed to stimulate the development of the Brazilian fishery sector, to increase

the number of fish farms in order to be able to meet domestic demand and decrease the volume of fish products imports. The plan,

which envisages BRL 4.1bn worth of investments, offers easy access to financing with preferential terms for small and medium-sized

fish farms, as well as for individual fishermen, in order to stimulate the development of the sector in the country and to improve the

living conditions of Brazilian fishermen.

Financing

Agriculture Ministry, Ministry of Fisheries and Aquaculture, BNDES

15.0 16.0 16.0 18.0 21.0

24.1

09/10 10/11 11/12 12/13 13/14 14/15

Financing Evolution The National Family Farming Strengthening Program (PRONAF) is a financing

program managed by BNDES. It provides preferential loans for individual or

collective projects of family farmers, promoting the increase of productivity and

reduction of production costs.

The financing could be used for acquisition of animals, as well as for machinery

and equipment purchase and infrastructure projects related to improvement of the

overall conditions in family farms. According the latest available data from BNDES,

more than 95% of all family farmers in the country have already used PRONAF

financing.

- 16 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

II. Food

- 17 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

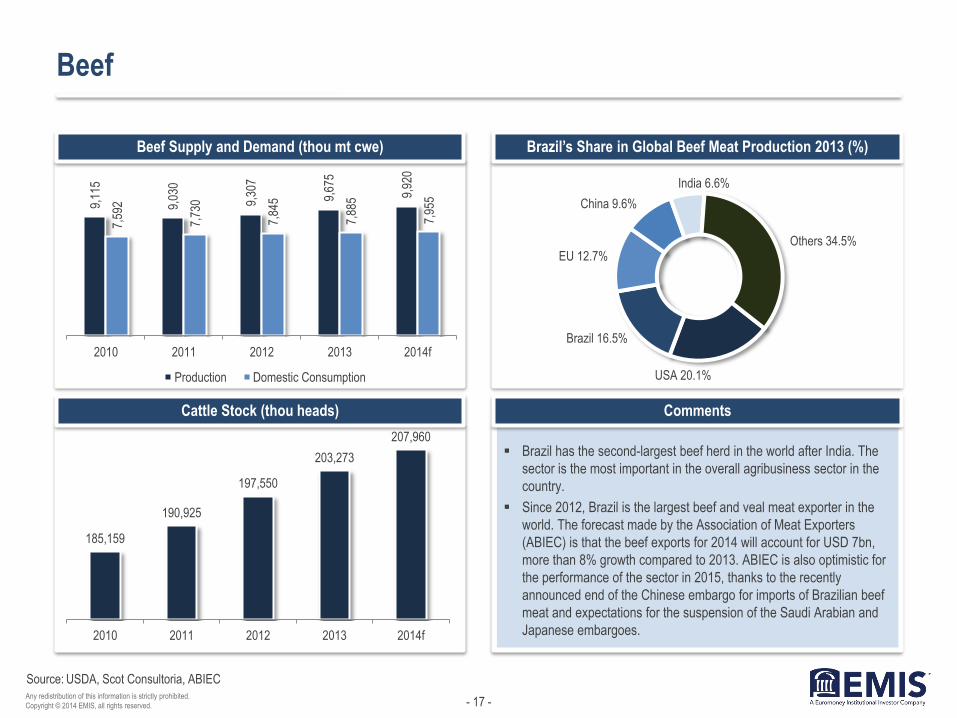

Beef

Beef Supply and Demand (thou mt cwe)

Cattle Stock (thou heads)

Brazil’s Share in Global Beef Meat Production 2013 (%)

Comments

USDA, Scot Consultoria, ABIEC

Brazil has the second-largest beef herd in the world after India. The

sector is the most important in the overall agribusiness sector in the

country.

Since 2012, Brazil is the largest beef and veal meat exporter in the

world. The forecast made by the Association of Meat Exporters

(ABIEC) is that the beef exports for 2014 will account for USD 7bn,

more than 8% growth compared to 2013. ABIEC is also optimistic for

the performance of the sector in 2015, thanks to the recently

announced end of the Chinese embargo for imports of Brazilian beef

meat and expectations for the suspension of the Saudi Arabian and

Japanese embargoes.

9,11

5

9,03

0

9,30

7

9,67

5

9,92

0

7,59

2

7,73

0

7,84

5

7,88

5

7,95

5

2010 2011 2012 2013 2014f

Production Domestic Consumption USA 20.1%

Brazil 16.5%

EU 12.7%

China 9.6%

India 6.6%

Others 34.5%

185,159

190,925

197,550

203,273

207,960

2010 2011 2012 2013 2014f

- 18 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

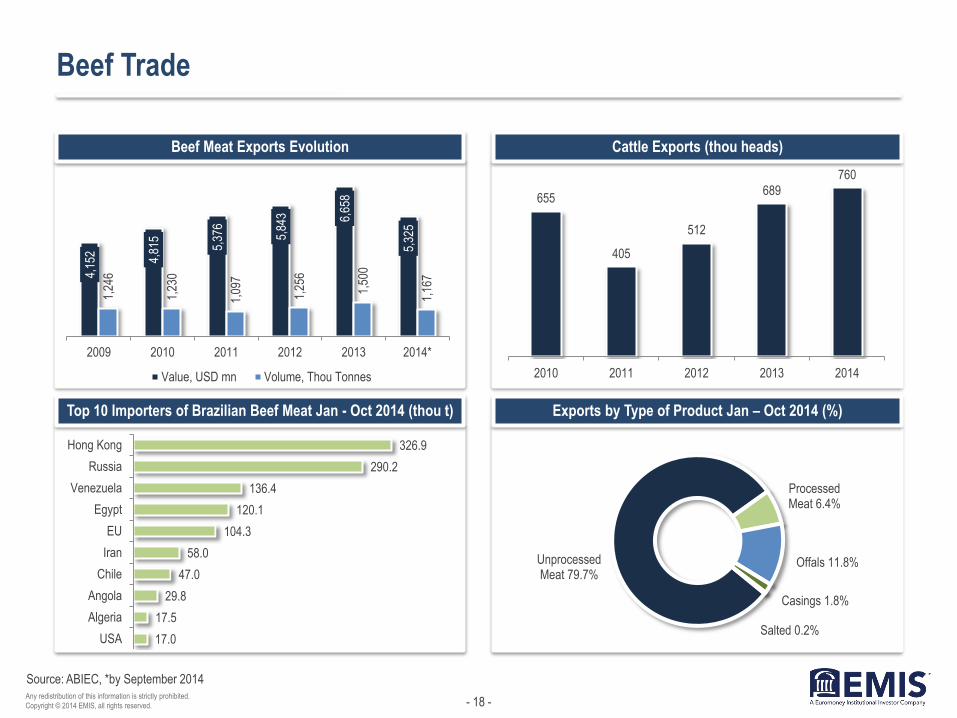

Beef Trade

Beef Meat Exports Evolution

Top 10 Importers of Brazilian Beef Meat Jan - Oct 2014 (thou t)

Cattle Exports (thou heads)

Exports by Type of Product Jan – Oct 2014 (%)

ABIEC, *by September 2014

4,15

2

4,81

5

5,37

6

5,84

3 6,65

8

5,32

5

1,24

6

1,23

0

1,09

7

1,25

6

1,50

0

1,16

7

2009 2010 2011 2012 2013 2014*

Value, USD mn Volume, Thou Tonnes

655

405

512

689

760

2010 2011 2012 2013 2014

17.0

17.5

29.8

47.0

58.0

104.3

120.1

136.4

290.2

326.9

USA

Algeria

Angola

Chile

Iran

EU

Egypt

Venezuela

Russia

Hong Kong

Unprocessed Meat 79.7%

Processed Meat 6.4%

Offals 11.8%

Casings 1.8%

Salted 0.2%

- 19 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Pork

Pork Meat Supply and Demand (thou t)

Swine Stock (thou heads)

Pork Meat Consumption per Capita (kg)

Comments

ABIPECS, USDA

Brazil has the third-largest swine herd in the world after China and

the European Union. However, it accounts for only 5% of the global

swine stock and for about 3% of the world's pork meat production.

The production and consumption of pork meat in Brazil have

remained almost flat in the last 2-3 years, predominantly due to high

end prices leading to a fall in the per capita consumption.

The pork meat production in the country is concentrated in a few

states – Santa Catarina (25%), Rio Grande do Sul (20%) and Parana

(16%).

3,91

0

3,23

8

3,39

8

3,48

8

3,42

9

2,58

3

2,69

8

2,88

2

2,90

7

2,91

2

2009 2010 2011 2012 2013

Production Consumption

13.7

14.1

14.9 14.9

14.6

2009 2010 2011 2012 2013

35,122

36,652

38,336 38,577 38,844

2010 2011 2012 2013 2014f

- 20 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Pork Trade

Brazil is the third-largest pork meat exporter in the world, after the European Union and Canada. However, the country's share in global exports was

relatively low at 8% in 2014. The main market for Brazilian pork meat is Russia. The country's imports of Brazilian pork meat increased by about 24% in

2014, pushed up predominantly by the Russian embargo on U.S., Canadian and European imports.

The main importers of Brazilian pork meat in South America are Uruguay and Argentina. Recently, the country received authorisation to exports pork meat

to the United States, the first shipments occurred in November 2014. By now, only two plants have the right to manufacture meat for the U.S. market -

Aurora Chapecó and BRF in Herval do Oeste in the Santa Catarina state.

Pork Meat Exports Pork Meat Exports by Country of Destination 2014* (%)

ABIPECS, *by September 2014

607 540 516

581 517

362

1,226 1,341

1,435 1,495

1,359

1,137

2009 2010 2011 2012 2013 2014*

Volume, thou tonnes Value, USD mnRussia 35.8%

Hong Kong 22.8%

Angola 10.7% Singapore

7.1%

Uruguay 4.4%

Georgia 2.1%

Others 17.2%

- 21 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

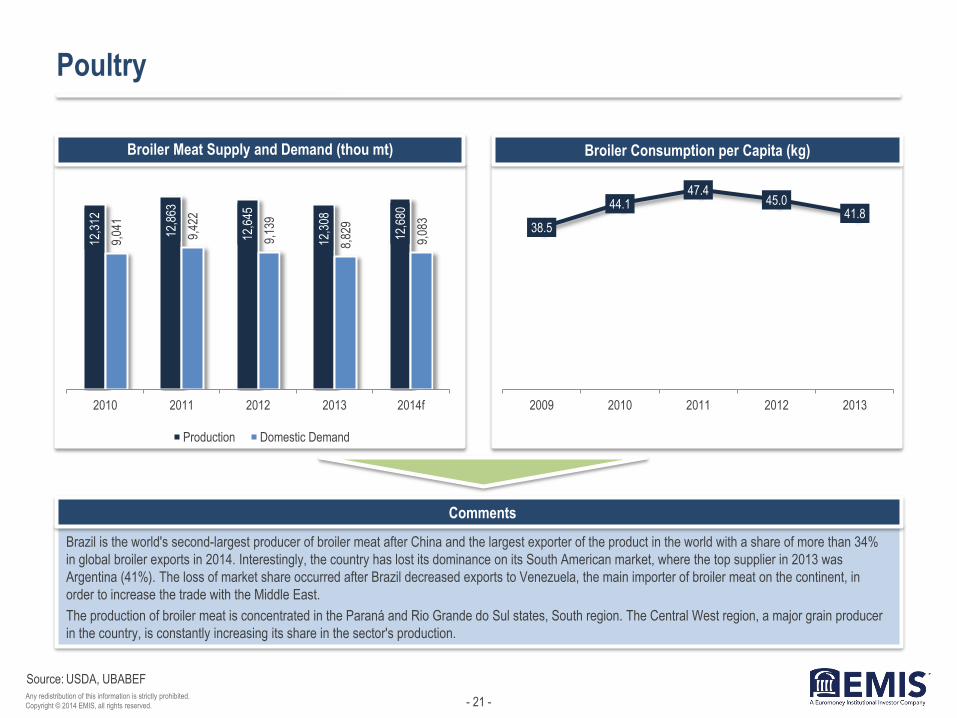

Poultry

Brazil is the world's second-largest producer of broiler meat after China and the largest exporter of the product in the world with a share of more than 34%

in global broiler exports in 2014. Interestingly, the country has lost its dominance on its South American market, where the top supplier in 2013 was

Argentina (41%). The loss of market share occurred after Brazil decreased exports to Venezuela, the main importer of broiler meat on the continent, in

order to increase the trade with the Middle East.

The production of broiler meat is concentrated in the Paraná and Rio Grande do Sul states, South region. The Central West region, a major grain producer

in the country, is constantly increasing its share in the sector's production.

Broiler Meat Supply and Demand (thou mt) Broiler Consumption per Capita (kg)

USDA, UBABEF

12,3

12

12,8

63

12,6

45

12,3

08

12,6

80

9,04

1

9,42

2

9,13

9

8,82

9

9,08

3

2010 2011 2012 2013 2014f

Production Domestic Demand

38.5

44.1 47.4

45.0 41.8

2009 2010 2011 2012 2013

- 22 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

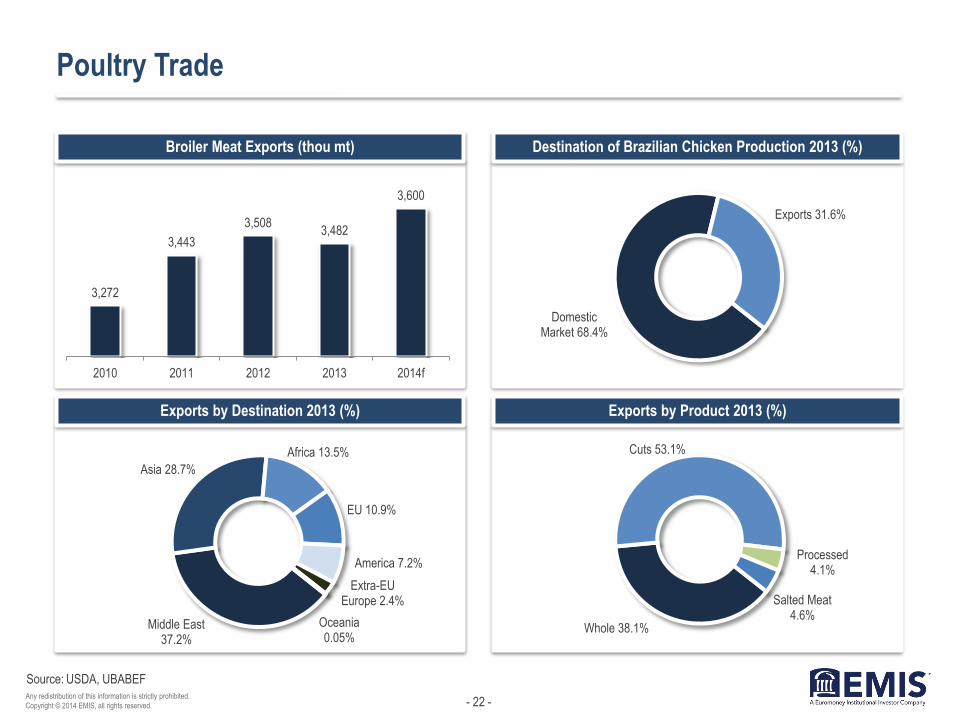

Poultry Trade

Broiler Meat Exports (thou mt)

Exports by Destination 2013 (%)

Destination of Brazilian Chicken Production 2013 (%)

Exports by Product 2013 (%)

USDA, UBABEF

3,272

3,443

3,508 3,482

3,600

2010 2011 2012 2013 2014f

Domestic Market 68.4%

Exports 31.6%

Middle East 37.2%

Asia 28.7%

Africa 13.5%

EU 10.9%

America 7.2%

Extra-EU Europe 2.4%

Oceania 0.05%

Whole 38.1%

Cuts 53.1%

Processed 4.1%

Salted Meat 4.6%

- 23 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Turkey

Turkey Meat Production (thou t)

Destination of Production 2013 (%)

Turkey Slaughtering by State 2013 (%)

Comments

UBABEF, Folha de Sao Paulo

Brazil is the world's second-largest exporter and third-largest

producer of turkey. However, the domestic consumption of turkey

meat is much lower than broiler and beef consumption, with sales

surging predominantly during festive periods like Christmas.

Nevertheless, the consumption of turkey meat is enjoying robust

growth. The increase registered in November 2014 was 6%

compared to the same period in 2013. However, the per capita

consumption of turkey meat in Brazil (1.7kg/year) is still much lower

than the consumption in developed markets like the United States

(7.4kg/year) and the EU (3.4%).

337 305

442

364

2010 2011 2012 2013 Paraná 26.6%

Santa Catarina 24.2%

Minas Gerais 17.6%

Goiás 19.4%

Rio Grande do Sul 14.3%

Domestic Market 56%

Exports 44%

- 24 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

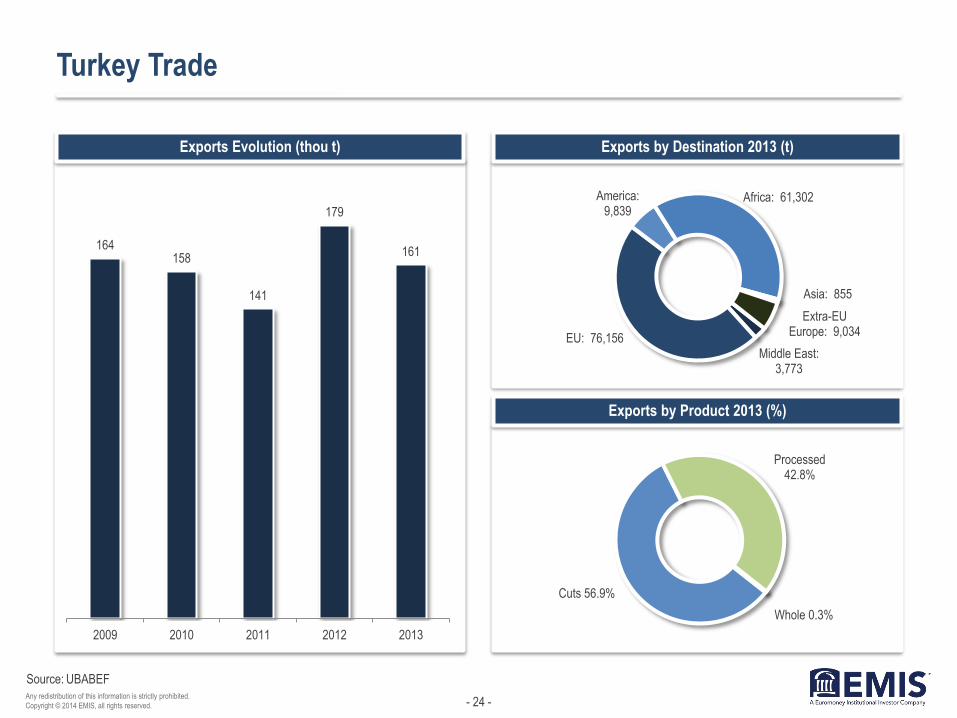

Turkey Trade

Exports by Destination 2013 (t)

Exports by Product 2013 (%)

Exports Evolution (thou t)

UBABEF

164 158

141

179

161

2009 2010 2011 2012 2013

Middle East: 3,773

EU: 76,156

America: 9,839

Africa: 61,302

Asia: 855

Extra-EU Europe: 9,034

Whole 0.3%

Cuts 56.9%

Processed 42.8%

- 25 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

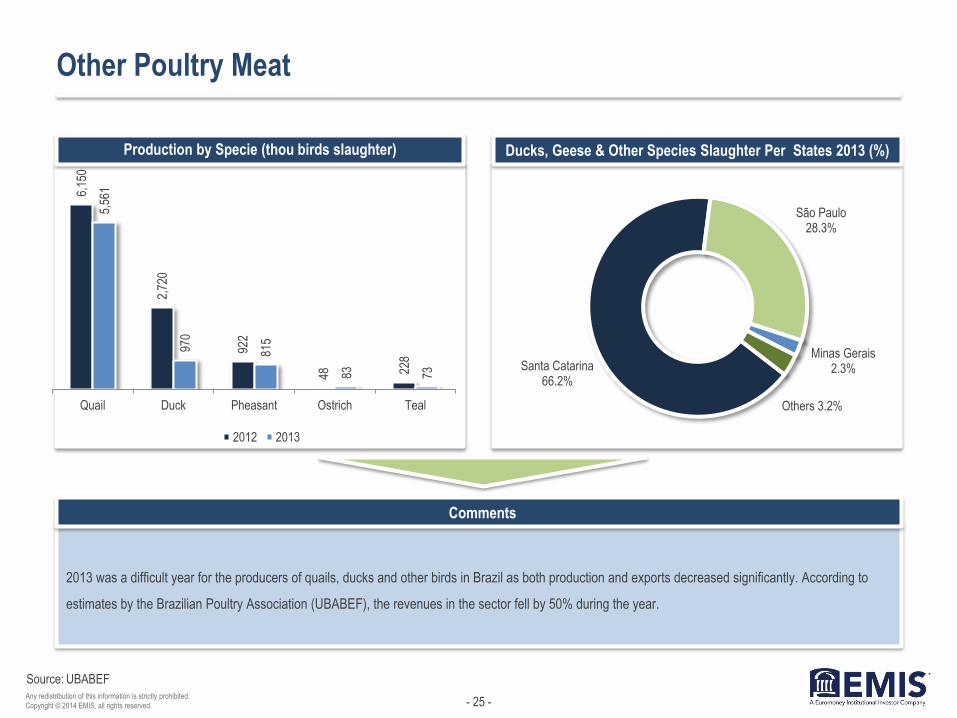

Other Poultry Meat

2013 was a difficult year for the producers of quails, ducks and other birds in Brazil as both production and exports decreased significantly. According to

estimates by the Brazilian Poultry Association (UBABEF), the revenues in the sector fell by 50% during the year.

Production by Specie (thou birds slaughter) Ducks, Geese & Other Species Slaughter Per States 2013 (%)

UBABEF

6,15

0

2,72

0

922

48

228

5,56

1

970

815

83

73

Quail Duck Pheasant Ostrich Teal

2012 2013

Santa Catarina 66.2%

São Paulo 28.3%

Minas Gerais 2.3%

Others 3.2%

- 26 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

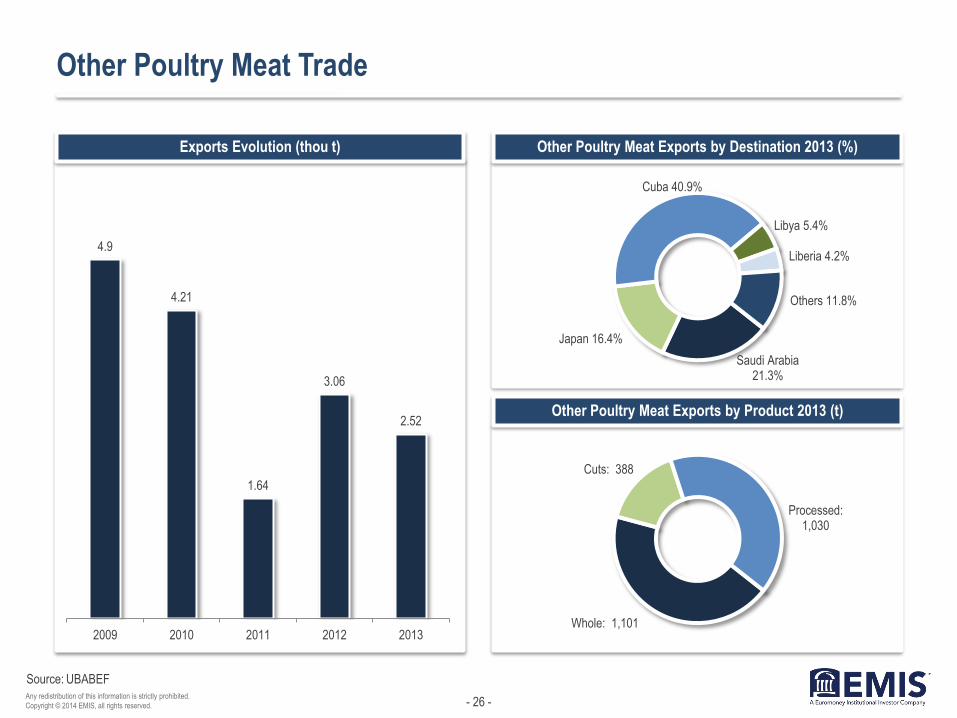

Other Poultry Meat Trade

Other Poultry Meat Exports by Destination 2013 (%)

Other Poultry Meat Exports by Product 2013 (t)

Exports Evolution (thou t)

UBABEF

4.9

4.21

1.64

3.06

2.52

2009 2010 2011 2012 2013

Saudi Arabia 21.3%

Japan 16.4%

Cuba 40.9%

Libya 5.4%

Liberia 4.2%

Others 11.8%

Whole: 1,101

Cuts: 388

Processed: 1,030

- 27 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Eggs

Eggs Supply and Demand

Exports Evolution (thou t)

Production by State 2013 (%)

Exports by Destination 2013 (%)

UBABEF

28.8 31.6 31.8 34.1

148.85 162.57 161.53 168.72

2010 2011 2012 2013

Production (bg units) Consumption per Capita (units/year)

São Paulo 34.3%

Minas Gerais 12.4%

Espírito Santo 8.7%

Mato Grosso 6.6%

Paraná 6.1% Pernambuco

6.4%

Rio Grande do Sul 5.9%

Others 19.7%

37.01

27.72

16.66

26.85

12.39

2009 2010 2011 2012 2013Angola 36.1%

Congo 4.3%

UAE 42.6%

Bolivia 7.2%

Uruguay 2.6%

Others 7.3%

- 28 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

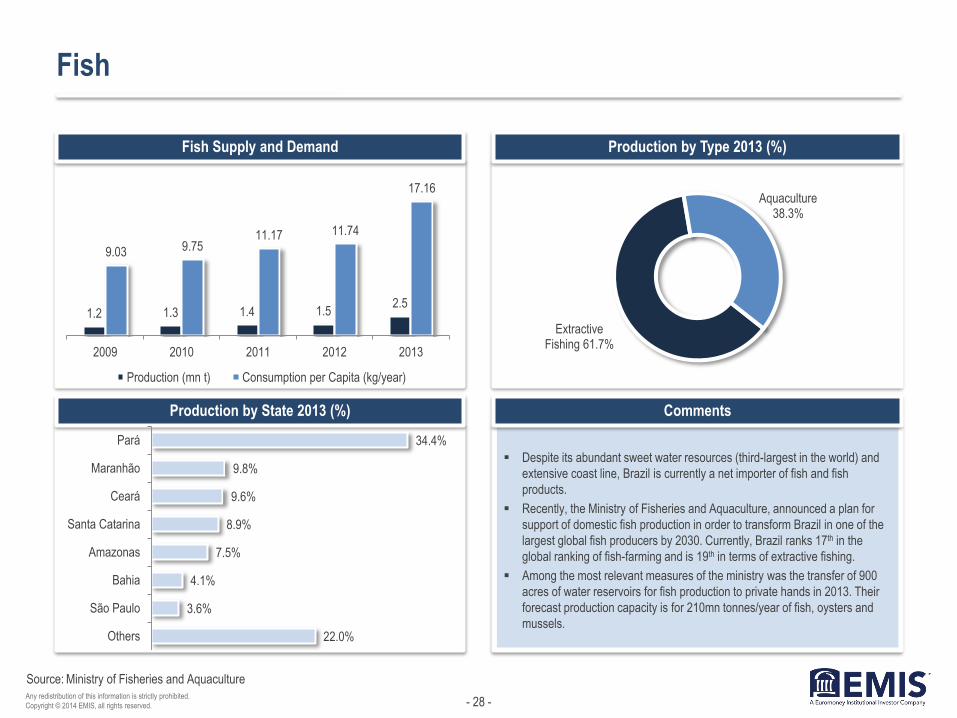

Fish

Fish Supply and Demand

Production by State 2013 (%)

Production by Type 2013 (%)

Comments

Ministry of Fisheries and Aquaculture

Despite its abundant sweet water resources (third-largest in the world) and

extensive coast line, Brazil is currently a net importer of fish and fish

products.

Recently, the Ministry of Fisheries and Aquaculture, announced a plan for

support of domestic fish production in order to transform Brazil in one of the

largest global fish producers by 2030. Currently, Brazil ranks 17th in the

global ranking of fish-farming and is 19th in terms of extractive fishing.

Among the most relevant measures of the ministry was the transfer of 900

acres of water reservoirs for fish production to private hands in 2013. Their

forecast production capacity is for 210mn tonnes/year of fish, oysters and

mussels.

1.2 1.3 1.4 1.5 2.5

9.03 9.75 11.17 11.74

17.16

2009 2010 2011 2012 2013

Production (mn t) Consumption per Capita (kg/year)

Extractive Fishing 61.7%

Aquaculture 38.3%

22.0%

3.6%

4.1%

7.5%

8.9%

9.6%

9.8%

34.4%

Others

São Paulo

Bahia

Amazonas

Santa Catarina

Ceará

Maranhão

Pará

- 29 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

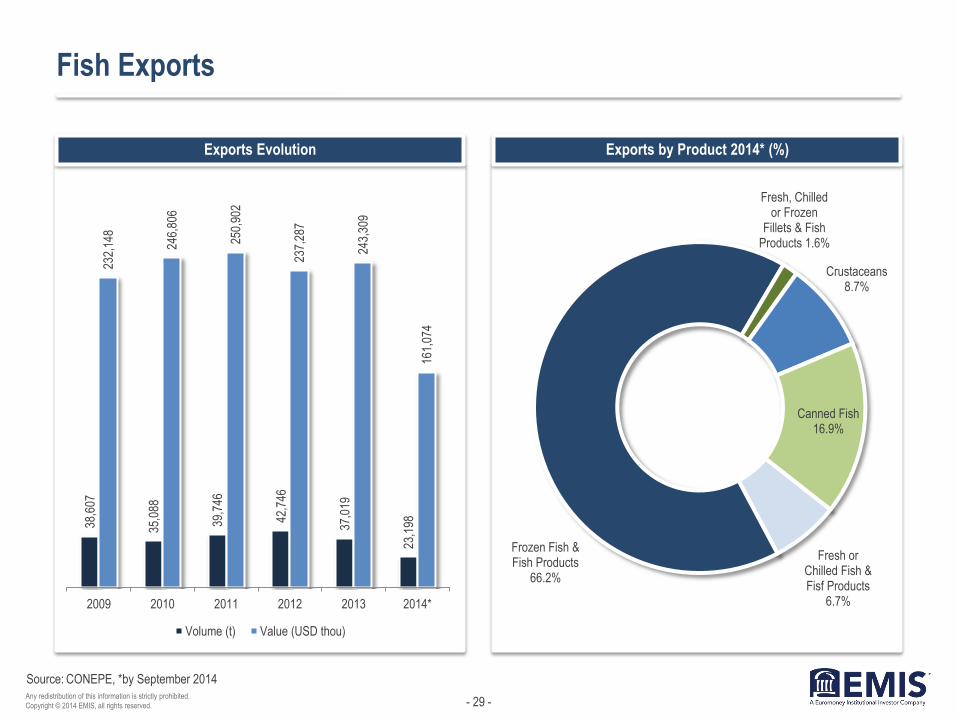

Fish Exports

Exports Evolution Exports by Product 2014* (%)

CONEPE, *by September 2014

38,6

07

35,0

88

39,7

46

42,7

46

37,0

19

23,1

98

232,

148

246,

806

250,

902

237,

287

243,

309

161,

074

2009 2010 2011 2012 2013 2014*

Volume (t) Value (USD thou)

Fresh or Chilled Fish & Fisf Products

6.7%

Frozen Fish & Fish Products

66.2%

Fresh, Chilled or Frozen

Fillets & Fish Products 1.6%

Crustaceans 8.7%

Canned Fish 16.9%

- 30 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Fish Imports

Imports by Country of Origine 2014* (%)

Imports by Product 2014* (%)

Imports Evolution

CONEPE, *by September 2014

Chile 22.0%

China 17.7%

Vietnam 16.6%

Argentina 9.4%

Norway 6.3%

Morocco 6.3%

Others 21.5%

Fresh or Chilled Fish & Fisf Products

20.2%

Frozen Fish & Fish Products

23.4%

Fresh, Chilled or Frozen

Fillets & Fish Products

47.4%

Canned Fish 9.0%

240 28

0 345

363 41

9

296

715

1,00

1

1,25

3

1,23

1

1,45

3

1,25

6

2009 2010 2011 2012 2013 2014*

Volume (thou t) Value (USD mn)

- 31 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Wheat Flour

The production of wheat and wheat flour in Brazil is much below the volume of domestic consumption. In fact, much of the wheat used in the production of

flour, pasta, bread, cakes and biscuits comes from imports. Actually, Brazil is one of the world's largest wheat importers and it is the second most imported

item in the country, after oil derivatives. In 2013, Brazil's wheat production decreased significantly as it was affected by the drought in the country. In 2014,

the wheat acreage increased by more than 14% to 2.524 million ha, and analysts had forecast a record wheat production of 7mn tonnes, a record high for

the country. However, in December 2014, the National Supply Company (Conab) announced much lower wheat production of 5.95 mn tonnes, explained

by unfavorable weather conditions.

Wheat Flour Supply and Demand by Harvest Period (mn t) Wheat Flour & Mixtures Consumption per Capita (kg/year)

ABIMA

3.75

4.5 4.24

3.18

4.07

7.58 7.65 7.69 7.73 7.8

2009/2010 2010/2011 2011/2012 2012/2013 2013/2014

Production Consumption

38.90 39.57

42.31

44.21 44.51 45.01

2008 2009 2010 2011 2012 2013

- 32 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

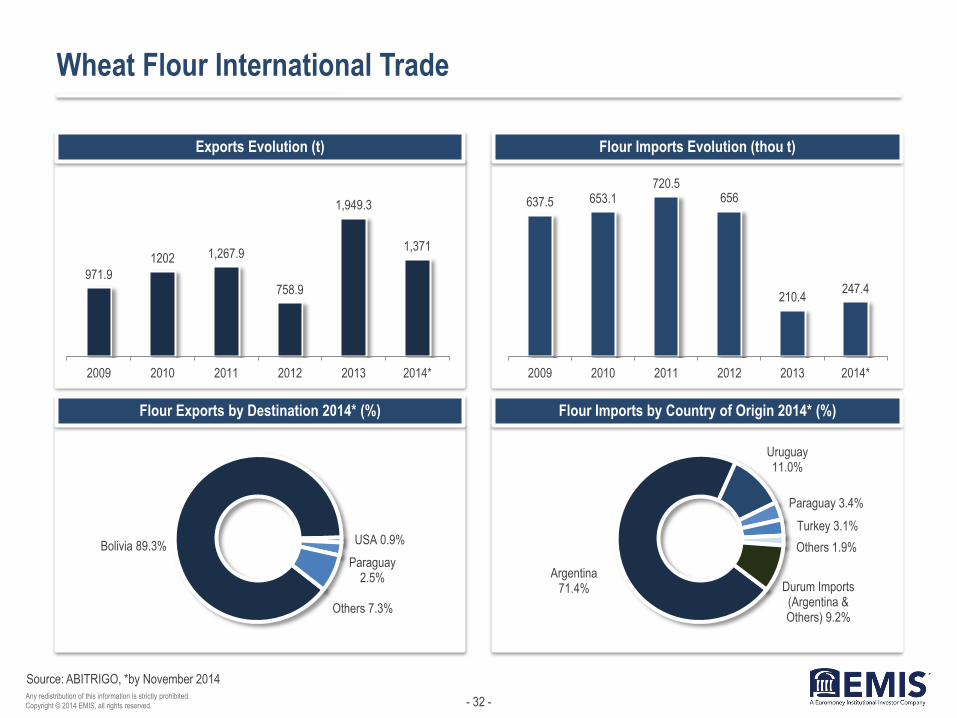

Wheat Flour International Trade

Exports Evolution (t)

Flour Exports by Destination 2014* (%)

Flour Imports Evolution (thou t)

Flour Imports by Country of Origin 2014* (%)

ABITRIGO, *by November 2014

971.9

1202 1,267.9

758.9

1,949.3

1,371

2009 2010 2011 2012 2013 2014*

Bolivia 89.3% USA 0.9%

Paraguay 2.5%

Others 7.3%

637.5 653.1 720.5

656

210.4 247.4

2009 2010 2011 2012 2013 2014*

Argentina 71.4%

Uruguay 11.0%

Paraguay 3.4%

Turkey 3.1%

Others 1.9%

Durum Imports (Argentina & Others) 9.2%

- 33 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Pasta

The consumption of pasta in Brazil is the third-largest in the world, after the United States and Italy. The most popular type is the spaghetti (57%), followed

by fusilli (15%) and lasagne. In 2013, the revenue of the segment reached BRL 7bn, or a 11.5% increase compared to 2012. Brazilian pasta enjoys very

high penetration on the domestic market – above 99%, according the latest research from the Brazilian Association of Pasta and Industrialised Bread &

Cake Producers (ABIMA).

Pasta Sales by Type (thou t) Consumption per Capita (kg/year)

ABIMA, O Globo

6.3 6.3

6.1

6.0 6.0

2009 2010 2011 2012 2013

1,015 1,007 961 953 967

170.8 180.8 183.5 187.8 186.7

40.8 45.2 51.1 50.5 51.5

1,226 1,233 1,196 1,191 1,205

2009 2010 2011 2012 2013

Dry Instant Fresh

- 34 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Pasta International Trade

Pasta Exports Evolution

Exported Volume by Destination 2013 (%)

Pasta Imports Evolution

Imported Volume by Country of Origine 2013 (%)

ABIMA

18.6

11.9 13

14.8

21.5

16.8

7 8.03

11.3

19.8

2009 2010 2011 2012 2013

Value (USD mn/FOB) Volume (thou t)

22.8 24.9

33.9 38.7 39.9

15.7 18.6

23.1 25.9

28.3

2009 2010 2011 2012 2013

Value (USD mn/FOB) Volume (thou t)

Venezuela 81.3%

Angola 2.3%

Chile 3.6%

USA 2.5%

Paraguay 4.0%

Others 6.3%

Chile 5.9%

Italy 71.9% Uruguay 9.2%

Mexico 3.4%

Others 9.6%

- 35 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

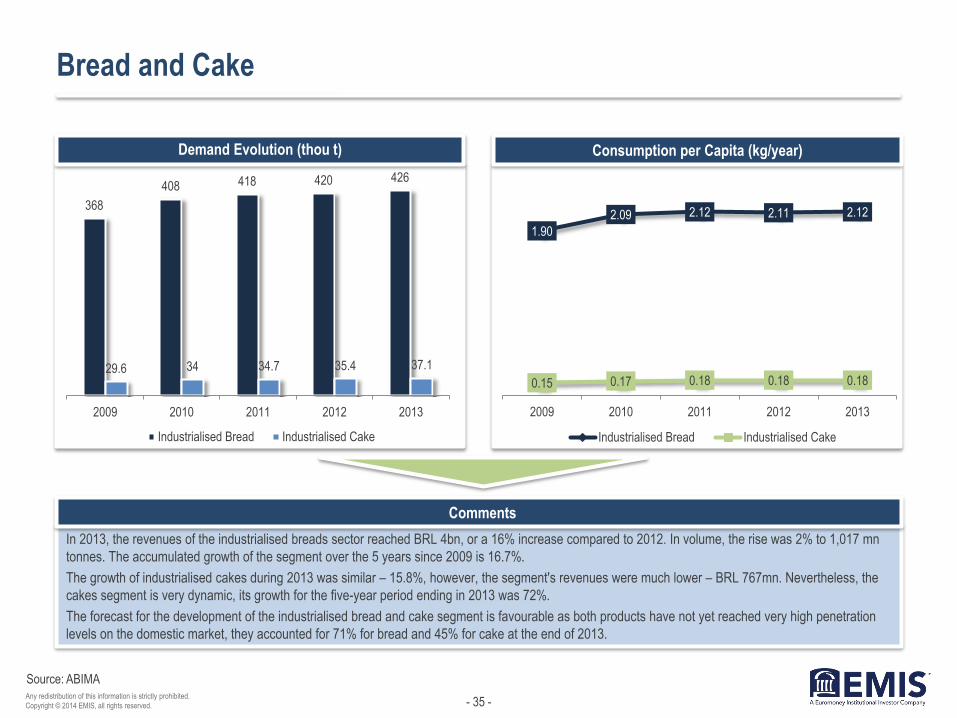

Bread and Cake

In 2013, the revenues of the industrialised breads sector reached BRL 4bn, or a 16% increase compared to 2012. In volume, the rise was 2% to 1,017 mn

tonnes. The accumulated growth of the segment over the 5 years since 2009 is 16.7%.

The growth of industrialised cakes during 2013 was similar – 15.8%, however, the segment's revenues were much lower – BRL 767mn. Nevertheless, the

cakes segment is very dynamic, its growth for the five-year period ending in 2013 was 72%.

The forecast for the development of the industrialised bread and cake segment is favourable as both products have not yet reached very high penetration

levels on the domestic market, they accounted for 71% for bread and 45% for cake at the end of 2013.

Demand Evolution (thou t) Consumption per Capita (kg/year)

ABIMA

368

408 418 420 426

29.6 34 34.7 35.4 37.1

2009 2010 2011 2012 2013

Industrialised Bread Industrialised Cake

1.90

2.09 2.12 2.11 2.12

0.15 0.17 0.18 0.18 0.18

2009 2010 2011 2012 2013

Industrialised Bread Industrialised Cake

- 36 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

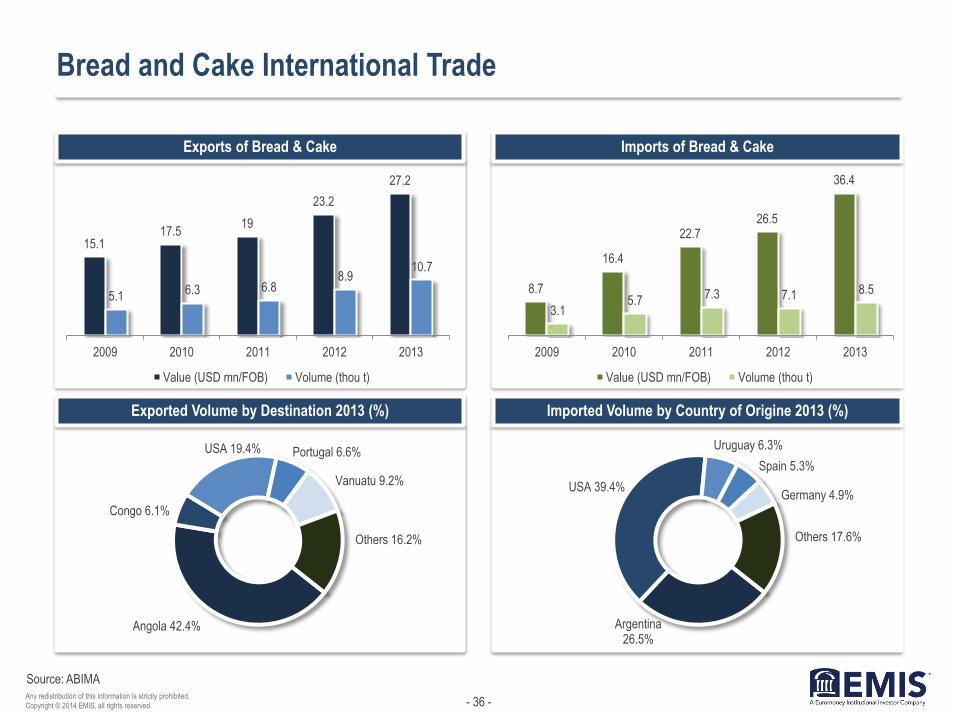

Bread and Cake International Trade

Exports of Bread & Cake

Exported Volume by Destination 2013 (%)

Imports of Bread & Cake

Imported Volume by Country of Origine 2013 (%)

ABIMA

15.1 17.5

19

23.2

27.2

5.1 6.3 6.8

8.9 10.7

2009 2010 2011 2012 2013

Value (USD mn/FOB) Volume (thou t)

8.7

16.4

22.7 26.5

36.4

3.1 5.7

7.3 7.1 8.5

2009 2010 2011 2012 2013

Value (USD mn/FOB) Volume (thou t)

Angola 42.4%

Congo 6.1%

USA 19.4% Portugal 6.6%

Vanuatu 9.2%

Others 16.2%

Argentina 26.5%

USA 39.4%

Uruguay 6.3%

Spain 5.3%

Germany 4.9%

Others 17.6%

- 37 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Biscuits

Production and Revenues

Production by Type 2013 (%)

Production by Region 2013 (%)

Comments

ANIB

Brazil is the second-largest producer of biscuits in the world, after the

United States. In 2013, the production reached 1.27 million tonnes, or

a 2% increase compared to 2012.

The sector's production is mainly used to meet domestic demand.

Despite the fact that the industry occupies the 36th place among

Brazilian exporters, it more than doubled its exported volumes in the

last decade. In 2013, the biscuits exports accounted for USD

155.8mn, 11% increase compared to 2012. The country exports

predominantly to Angola, the United States, Paraguay, Uruguay and

Argentina.

In 2013, the National Association of Biscuit Industry (ANIB) launched

a new brand in order to boost the image of Brazilian biscuits.

1.2 1.24 1.22 1.25 1.27

5.96 6.47 6.8 7.02

7.91

2009 2010 2011 2012 2013

Production (bn t) Reveneu (BRL bn)

North 1.5% Northeast 30.7%

Southeast 45.0%

South 15.0%

Central West 7.8%

Cracker 21.4%

Sandwich Cookies 26.8%

Dry Sweet Biscuits 15.4%

Salted 8.5%

Wafer 8.1%

Donuts 5.9%

Cornflour Biscuits 11.3%

Others 2.6%

- 38 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

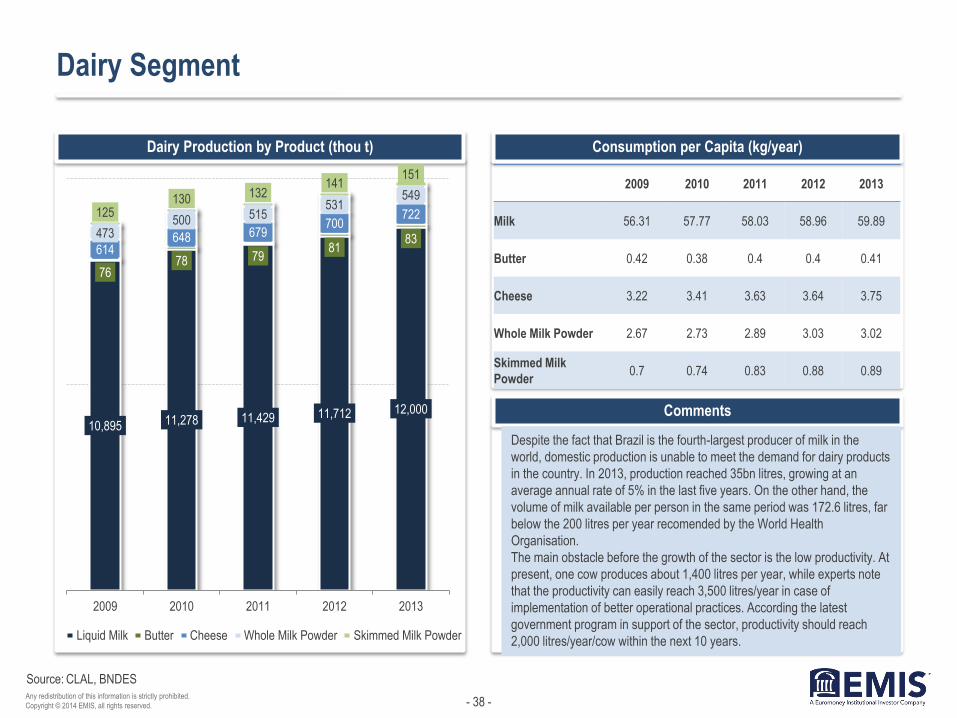

Dairy Segment

Consumption per Capita (kg/year)

Comments

Dairy Production by Product (thou t)

CLAL, BNDES

10,895 11,278 11,429 11,712 12,000

76 78 79

81 83

614 648 679

700 722

473 500 515

531 549

125 130 132

141 151

2009 2010 2011 2012 2013

Liquid Milk Butter Cheese Whole Milk Powder Skimmed Milk Powder

2009 2010 2011 2012 2013

Milk 56.31 57.77 58.03 58.96 59.89

Butter 0.42 0.38 0.4 0.4 0.41

Cheese 3.22 3.41 3.63 3.64 3.75

Whole Milk Powder 2.67 2.73 2.89 3.03 3.02

Skimmed Milk

Powder 0.7 0.74 0.83 0.88 0.89

Despite the fact that Brazil is the fourth-largest producer of milk in the

world, domestic production is unable to meet the demand for dairy products

in the country. In 2013, production reached 35bn litres, growing at an

average annual rate of 5% in the last five years. On the other hand, the

volume of milk available per person in the same period was 172.6 litres, far

below the 200 litres per year recomended by the World Health

Organisation.

The main obstacle before the growth of the sector is the low productivity. At

present, one cow produces about 1,400 litres per year, while experts note

that the productivity can easily reach 3,500 litres/year in case of

implementation of better operational practices. According the latest

government program in support of the sector, productivity should reach

2,000 litres/year/cow within the next 10 years.

- 39 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Dairy Segment International Trade

Exports by Product (thou t) Imports by Product (thou t)

CLAL

5.8 4.3 3.2 2.6 2.8

35

28

24 26 24

13.0

5.1

1.2 0.2 2.8

2009 2010 2011 2012 2013

Cheese Condensed Milk Whole Milk Powder

16 22

39 27 31

11

14

31

33 24

57 38

55 71

54

29

30

25 27

21 7

13

14

21

15

2009 2010 2011 2012 2013

Cheese Skimmed Milk Powder Whole Milk Powder

Whey Powder Lactose Edible

- 40 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

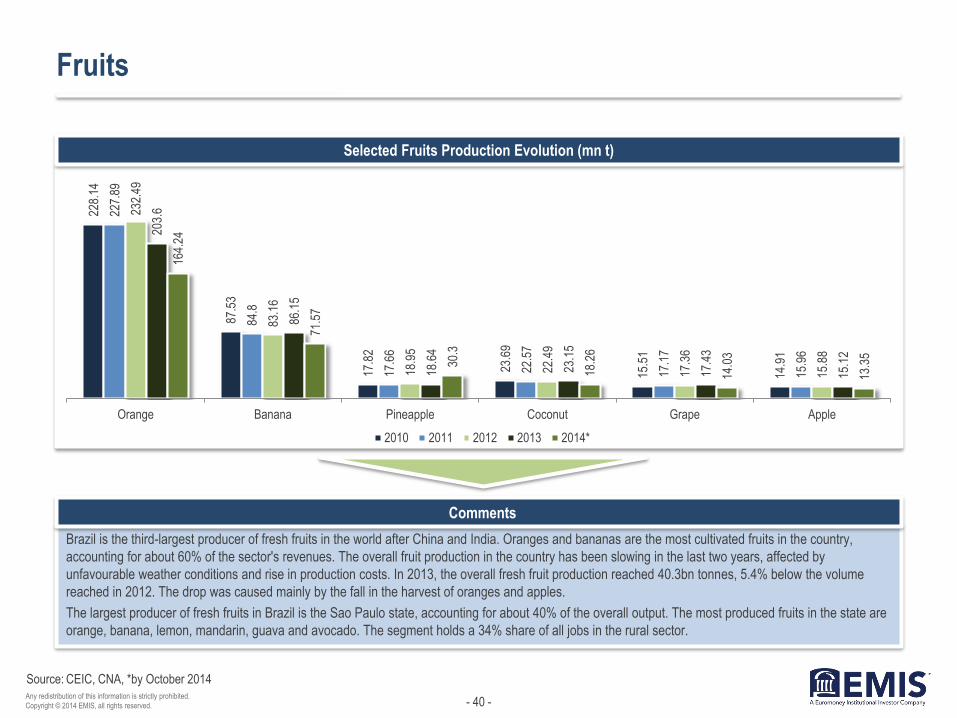

Fruits

Brazil is the third-largest producer of fresh fruits in the world after China and India. Oranges and bananas are the most cultivated fruits in the country,

accounting for about 60% of the sector's revenues. The overall fruit production in the country has been slowing in the last two years, affected by

unfavourable weather conditions and rise in production costs. In 2013, the overall fresh fruit production reached 40.3bn tonnes, 5.4% below the volume

reached in 2012. The drop was caused mainly by the fall in the harvest of oranges and apples.

The largest producer of fresh fruits in Brazil is the Sao Paulo state, accounting for about 40% of the overall output. The most produced fruits in the state are

orange, banana, lemon, mandarin, guava and avocado. The segment holds a 34% share of all jobs in the rural sector.

Selected Fruits Production Evolution (mn t)

CEIC, CNA, *by October 2014

228.

14

87.5

3

17.8

2

23.6

9

15.5

1

14.9

1

227.

89

84.8

17.6

6

22.5

7

17.1

7

15.9

6

232.

49

83.1

6

18.9

5

22.4

9

17.3

6

15.8

8

203.

6

86.1

5

18.6

4

23.1

5

17.4

3

15.1

2

164.

24

71.5

7

30.3

18.2

6

14.0

3

13.3

5

Orange Banana Pineapple Coconut Grape Apple

2010 2011 2012 2013 2014*

- 41 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Fruits International Trade

Fruit Exports by Product 2013 (thou t)

Fruit Exports by Destination 2013 (%)

Fruit Imports by Product 2013 (thou t)

Fruit Imports by Country of Origine 2013 (%)

ITC

1.4

1.0

1.4

4.2

35.9

43.2

85.4

99.2

102.5

129.0

252.0

Others

Citrus fruit & Melon peel

Provisionally preserved fruits & nuts

Frozen fruits & nuts

Brazil nuts, Cashew nuts & Coconuts

Grapes, fresh or dried

Apples, Pears & Quinces

Bananas & Plantains, fresh or dried

Citrus Fruit, fresh or dried

Dates, Figs, Pineapples, Mangoes,…

Melons, Watermelons & Papayas

Netherlands 36.6%

UK 16.3%

USA 12.6% Spain 8.7%

Germany 3.7%

Canada 2.7%

Portugal 2.6%

France 2.1%

Others 14.8%

0.7

1.1

9.9

12.6

19.4

26.7

29.6

55.3

57.5

58.0

283.7

Others

Dates, Figs, Pineapples, Mangoes,…

Frozen fruits & nuts

Nuts nes

Dried fruit

Citrus fruit, fresh or dried

Fruits nes, fresh

Brazil nuts, Cashew nuts & Coconuts

Grapes, fresh or dried

Apricots, Cherries, Peaches,…

Apples, Pears & Quinces

Argentina 37.9%

Chile 25.9%

Spain 9.0% Turkey 4.8%

Portugal 4.8%

USA 3.2%

Italy 3.2%

Others 11.2%

- 42 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Vegetables

Selected Vegetables Production Evolution (mn t)

Comments

Selected Seed Production (mn t)

CEIC, CNA, *by October 2014

45.4

42.7

5

17.5

6

47.2

7

46.2

9

7.39

47.2

7

42.8

7

16.6

6

46.6

1

42.1

3

16.2

9

40.4

8

36.9

9

15.6

2

Tomatoes Potatoes Onion

2010 2011 2012 2013 2014*

137

317

648

816

8,471

160

316

673

879

8,037

138

301

828

879

8,037

142

268

941

979

8,769

124

233

763

872

7,378

Rice

Cassava

Corn

Soybean

Sugarcane

2014*

2013

2012

2011

2010

Production of vegetables in Brazil has been stagnant in the last five

years, with an annual output around 18mn tonnes. Business

representatives explain the lack of dynamism in the segment with the

high production costs, inadequate infrastructure and logistics conditions,

absence of consumption incentives and poor rural expansion policy,

which is focused only in the development of selected cultures.

The production is very fragmented and is mainly in the hands of small

and medium-sized entities, of the type of family farms with an annual

turnover of BRL 60,000. The state of Sao Paulo is the largest vegetables

producer in the country with a share of more than 21% in overall

vegetables production in 2013.

- 43 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Vegetables International Trade

Vegetables Exports by Product 2013 (thou t)

Vegetables Exports by Destination 2013 (%)

Vegetables Imports by Product 2013 (thou t)

Vegetables Imports by Country of Origin 2013 (%)

ITC

0.6

1.5

2.0

3.0

3.6

5.0

35.4

Others

Tomatoes

Potatoes

Vegetables nes, fresh or chilled

Onions, Garlic & Leeks, fresh or chilled

Manioc, Arrowroot Salem (yams)

Dried Vegetables, shelled

Egypt 30.4%

India 17.5%

Uruguay 8.4%

USA 7.5% UK 5.2%

Pakistan 4.6%

Germany 4.4%

Argentina 3.4%

Others 18.6%

1.0

1.5

11.3

16.6

18.9

21.4

29.2

373.2

444.2

Others

Vegetables nes, fresh or chilled

Manioc, Arrowroot Salem (yams)

Vegetables, provisionally preserved…

Frozen Vegetables

Dried Vegetables

Potatoes

Dried Vegetables, shelled

Onions, Garlic & Leeks, fresh or chilled

China 47.8%

Argentina 34.0%

Bolivia 3.5%

Canada 2.9%

Netherlands 2.4%

Spain 1.5%

France 1.3%

Others 6.5%

- 44 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

III. Beverages

- 45 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

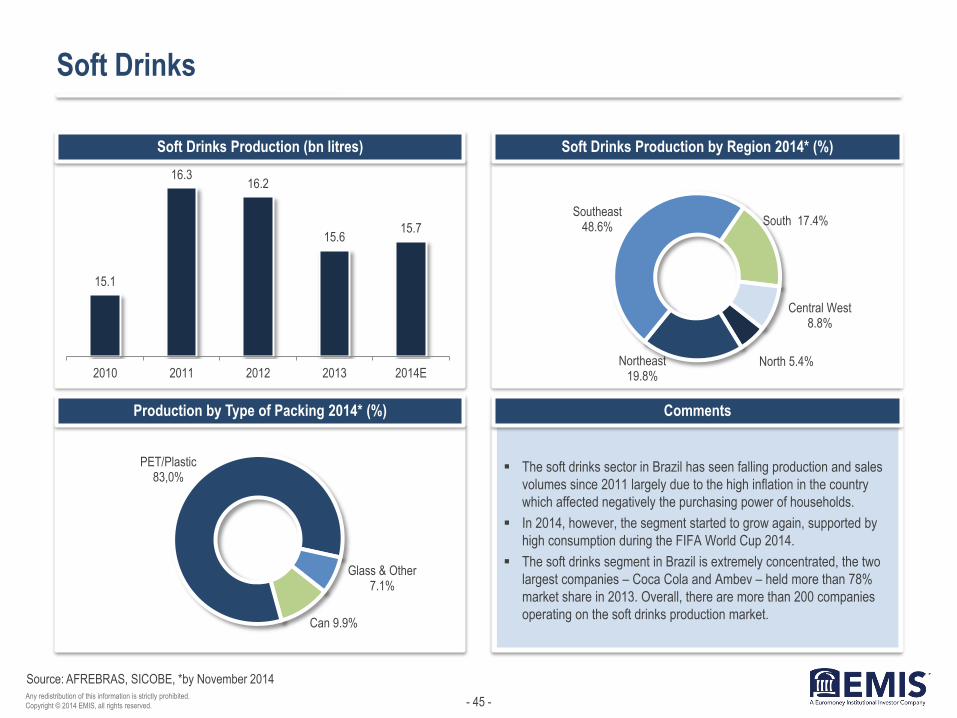

Soft Drinks

Soft Drinks Production (bn litres)

Production by Type of Packing 2014* (%)

Soft Drinks Production by Region 2014* (%)

Comments

AFREBRAS, SICOBE, *by November 2014

The soft drinks sector in Brazil has seen falling production and sales

volumes since 2011 largely due to the high inflation in the country

which affected negatively the purchasing power of households.

In 2014, however, the segment started to grow again, supported by

high consumption during the FIFA World Cup 2014.

The soft drinks segment in Brazil is extremely concentrated, the two

largest companies – Coca Cola and Ambev – held more than 78%

market share in 2013. Overall, there are more than 200 companies

operating on the soft drinks production market.

15.1

16.3 16.2

15.6 15.7

2010 2011 2012 2013 2014ENorth 5.4% Northeast

19.8%

Southeast 48.6% South 17.4%

Central West 8.8%

Can 9.9%

PET/Plastic 83,0%

Glass & Other 7.1%

- 46 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

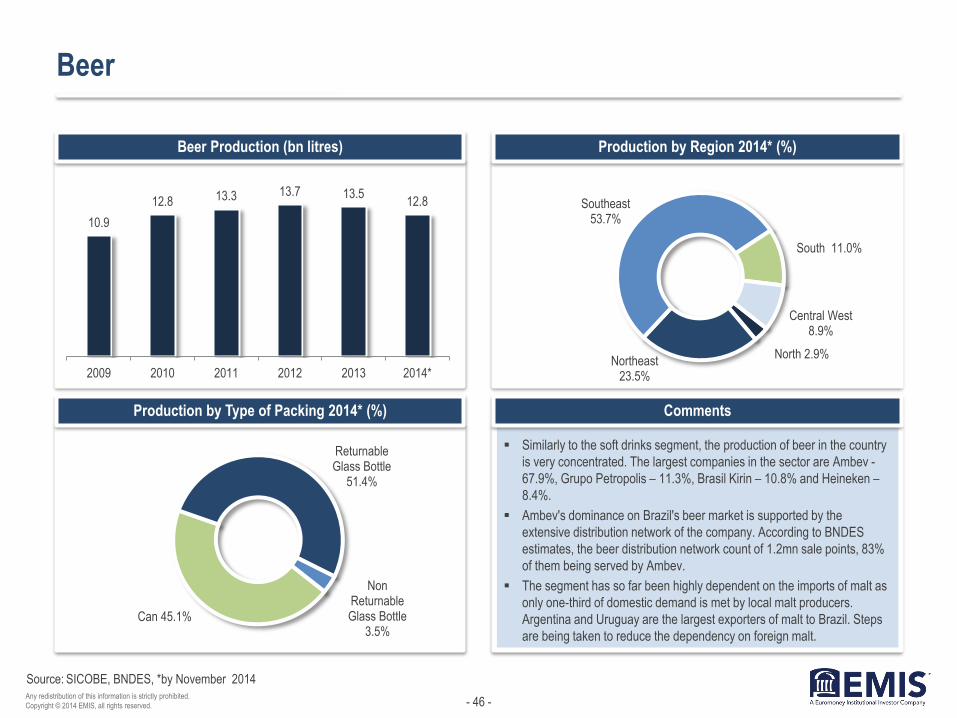

Beer

Beer Production (bn litres)

Production by Type of Packing 2014* (%)

Production by Region 2014* (%)

Comments

SICOBE, BNDES, *by November 2014

Similarly to the soft drinks segment, the production of beer in the country

is very concentrated. The largest companies in the sector are Ambev -

67.9%, Grupo Petropolis – 11.3%, Brasil Kirin – 10.8% and Heineken –

8.4%.

Ambev's dominance on Brazil's beer market is supported by the

extensive distribution network of the company. According to BNDES

estimates, the beer distribution network count of 1.2mn sale points, 83%

of them being served by Ambev.

The segment has so far been highly dependent on the imports of malt as

only one-third of domestic demand is met by local malt producers.

Argentina and Uruguay are the largest exporters of malt to Brazil. Steps

are being taken to reduce the dependency on foreign malt.

10.9

12.8 13.3 13.7 13.5 12.8

2009 2010 2011 2012 2013 2014*

North 2.9% Northeast

23.5%

Southeast 53.7%

South 11.0%

Central West 8.9%

Can 45.1%

Returnable Glass Bottle

51.4%

Non Returnable Glass Bottle

3.5%

- 47 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Orange Juice

Processed Volumes of Oranges per Season (mn bxs)

Oranges Production (mn bxs)

Centro de Citricultura, CEPEA, 1 box ≈ 40.8kg

264.86 251.11

398.03

301.69

240 258

2009/2010 2010/2011 2011/2012 2012/2013 2013/2014 2014/2015

355.4

297.5

428 385.4

289.9 308.8

2009/2010 2010/2011 2011/2012 2012/2013 2013/2014 2014/2015

Brazil is the world's largest producer and exporter of

orange juice, accounting for more than half of the global

output. The country exports more than 90% of the juice it

produces.

However, since 2011, the sector has been facing falling

production and exports volumes, which contributes

significantly to the overall slowdown of Brazilian economy.

For instance, the sector's exports have fallen by more

than 15% in the last 10 years since 2003, and the forecast

for 2014 is also not positive.

There are two main reasons behind the slowdown. The

first one is the decrease of global consumption,

predominantly in the leading markets – the United States

and Europe. In addition, the production costs in Brazil

have increased significantly in the last few years, mainly

the costs of labour, land lease, pesticides and fertilisers.

As a consequence, only for the two-year period between

2012 and 2013, in the state of Sao Paulo, the largest

producer of oranges in the country, 4,200 orange

producers left the sector, 80% of whom were small-sized

producers.

Additional challenge for the small and medium-sized

independent orange producers in the country is the

increasing share of fully integrated orange juice producers

on the market.

- 48 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Orange Juice Exports Key Indicators

Orange Juice Exports Evolution (USD mn/FOB)

Exports by Destination 2014* (%)

Exports Segmentation, January - December (thou t)

CitrusBR, *by October 2014, **by November 2014

170.0

172.3

188.7

177.0

200.0

159.8

553.5

558.5

522.3

436.1

445.5

304.9

524.2

424.3

387.3

405.1

520.6

430.9

934.8

947.4

1038

973.8

1099.8

878.7

1,247.7

1,155.1

1,098.4

1,018.3

1,166.0

895.6

2009

2010

2011

2012

2013

2014**

FCOJ Equivalent NFC FCOJ

Other Orange Juice NFC converted in FCOJ

1,619.2 1,774.8

2,376.2 2,276.4 2,295.4

1,542.8

2009 2010 2011 2012 2013 2014*

EU 62.6%

USA 19.5%

Japan 5.9%

China 3.9%

Switzerland 2.0%

Others 6.0%

- 49 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

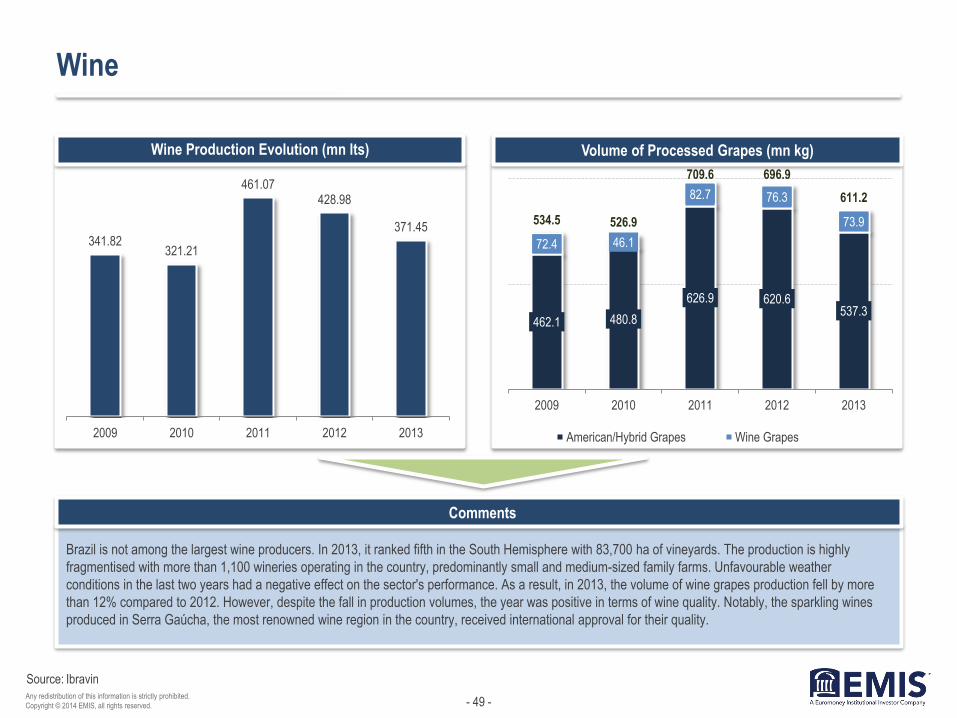

Wine

Brazil is not among the largest wine producers. In 2013, it ranked fifth in the South Hemisphere with 83,700 ha of vineyards. The production is highly

fragmentised with more than 1,100 wineries operating in the country, predominantly small and medium-sized family farms. Unfavourable weather

conditions in the last two years had a negative effect on the sector's performance. As a result, in 2013, the volume of wine grapes production fell by more

than 12% compared to 2012. However, despite the fall in production volumes, the year was positive in terms of wine quality. Notably, the sparkling wines

produced in Serra Gaúcha, the most renowned wine region in the country, received international approval for their quality.

Wine Production Evolution (mn lts) Volume of Processed Grapes (mn kg)

Ibravin

341.82 321.21

461.07 428.98

371.45

2009 2010 2011 2012 2013

462.1 480.8

626.9 620.6 537.3

72.4 46.1

82.7 76.3

73.9 534.5 526.9

709.6 696.9

611.2

2009 2010 2011 2012 2013

American/Hybrid Grapes Wine Grapes

- 50 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Wine Sales in Brazil

Fine Wines Sales Evolution (mn lts) Table Wine Sales Evolution (mn lts)

Ibravin

4.8 4.5 4.7 4.4 4.6

0.2 0.2 0.2 0.1 0.2

13.0 13.6 14.7

14.2 15.3

18.0 18.3

19.6 18.7

20.1

2009 2010 2011 2012 2013

White Rose Red

29.4 29.6 32.1 30.1 29.3

2.3 2.0 1.7 1.7 1.8

190.4 183.4 196.3

173.6 181.0

222.1 215.0

230.1

205.4 212.1

2009 2010 2011 2012 2013

White Rose Red

- 51 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Wine International Trade

Exports of Wine and Sparkling Wine (USD thou/FOB)

Imports of Wine and Sparkling Wine (mn lts)

Exports by Country of Destination 1H2013 (%)

Imports by Country of Origine 2013 (%)

Ibravin, * - estimates

2,571.6

4,117.9 4,453.5 4,383.5

4,014.4

2009 2010 2011 2012 2013* USA 23%

Paraguay 27%

Colombia 14% Germany 6%

UK 4%

China 2%

Netherlands 4%

Others 20%

59.1

75.3 77.6 79.5 72.2

2009 2010 2011 2012 2013 Chile 39.3%

Argentina 18.6%

Italy 12.7% France 6.5%

Portugal 12.9%

Others 10.0%

- 52 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

IV. Major Players

- 53 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

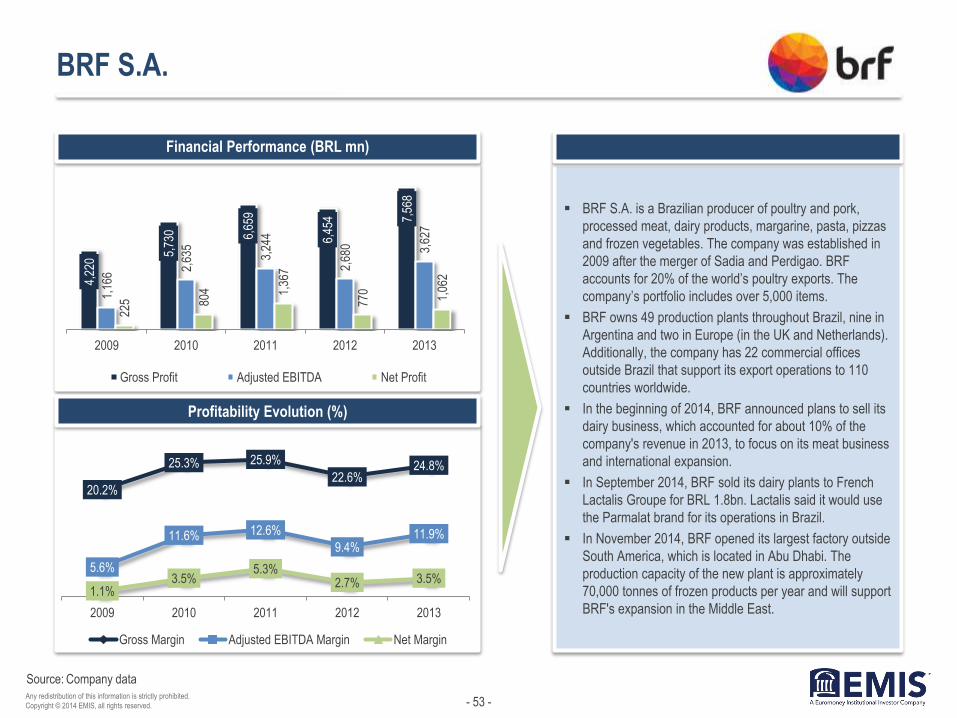

BRF S.A.

Financial Performance (BRL mn)

BRF S.A. is a Brazilian producer of poultry and pork,

processed meat, dairy products, margarine, pasta, pizzas

and frozen vegetables. The company was established in

2009 after the merger of Sadia and Perdigao. BRF

accounts for 20% of the world’s poultry exports. The

company’s portfolio includes over 5,000 items.

BRF owns 49 production plants throughout Brazil, nine in

Argentina and two in Europe (in the UK and Netherlands).

Additionally, the company has 22 commercial offices

outside Brazil that support its export operations to 110

countries worldwide.

In the beginning of 2014, BRF announced plans to sell its

dairy business, which accounted for about 10% of the

company's revenue in 2013, to focus on its meat business

and international expansion.

In September 2014, BRF sold its dairy plants to French

Lactalis Groupe for BRL 1.8bn. Lactalis said it would use

the Parmalat brand for its operations in Brazil.

In November 2014, BRF opened its largest factory outside

South America, which is located in Abu Dhabi. The

production capacity of the new plant is approximately

70,000 tonnes of frozen products per year and will support

BRF's expansion in the Middle East.

Profitability Evolution (%)

Company data

4,22

0

5,73

0 6,65

9

6,45

4 7,56

8

1,16

6

2,63

5

3,24

4

2,68

0 3,62

7

225 80

4 1,36

7

770

1,06

2

2009 2010 2011 2012 2013

Gross Profit Adjusted EBITDA Net Profit

20.2%

25.3% 25.9%

22.6% 24.8%

5.6%

11.6% 12.6%

9.4% 11.9%

1.1% 3.5%

5.3% 2.7% 3.5%

2009 2010 2011 2012 2013

Gross Margin Adjusted EBITDA Margin Net Margin

- 54 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

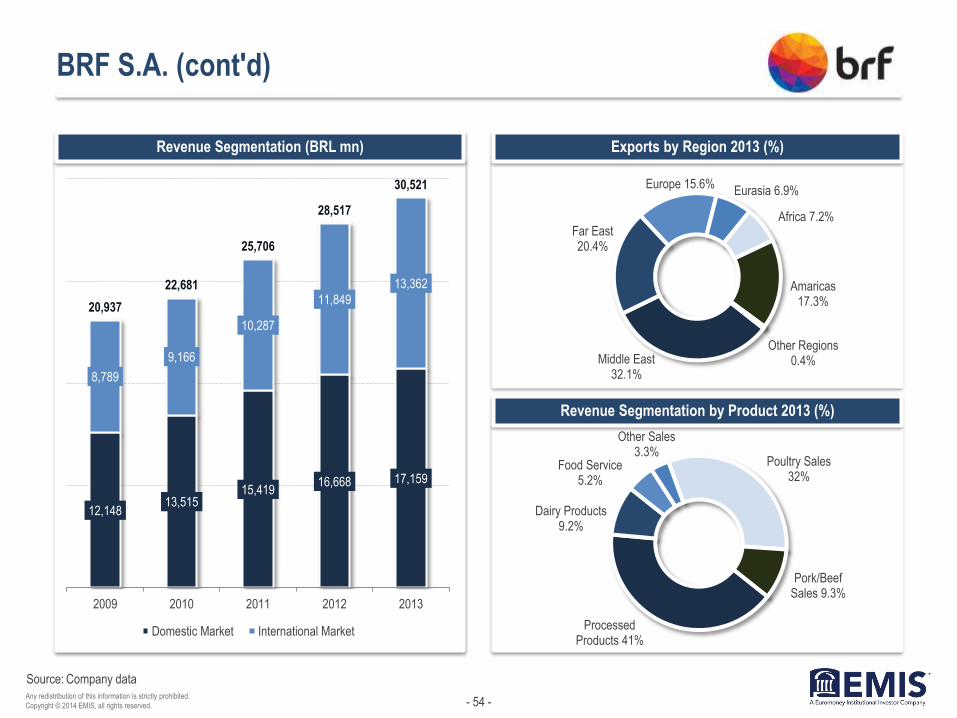

BRF S.A. (cont'd)

Exports by Region 2013 (%)

Revenue Segmentation by Product 2013 (%)

Revenue Segmentation (BRL mn)

Company data

12,148 13,515

15,419 16,668 17,159

8,789

9,166

10,287

11,849

13,362

20,937

22,681

25,706

28,517

30,521

2009 2010 2011 2012 2013

Domestic Market International Market

Middle East 32.1%

Far East 20.4%

Europe 15.6% Eurasia 6.9%

Africa 7.2%

Amaricas 17.3%

Other Regions 0.4%

Processed Products 41%

Dairy Products 9.2%

Food Service 5.2%

Other Sales 3.3%

Poultry Sales 32%

Pork/Beef Sales 9.3%

- 55 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

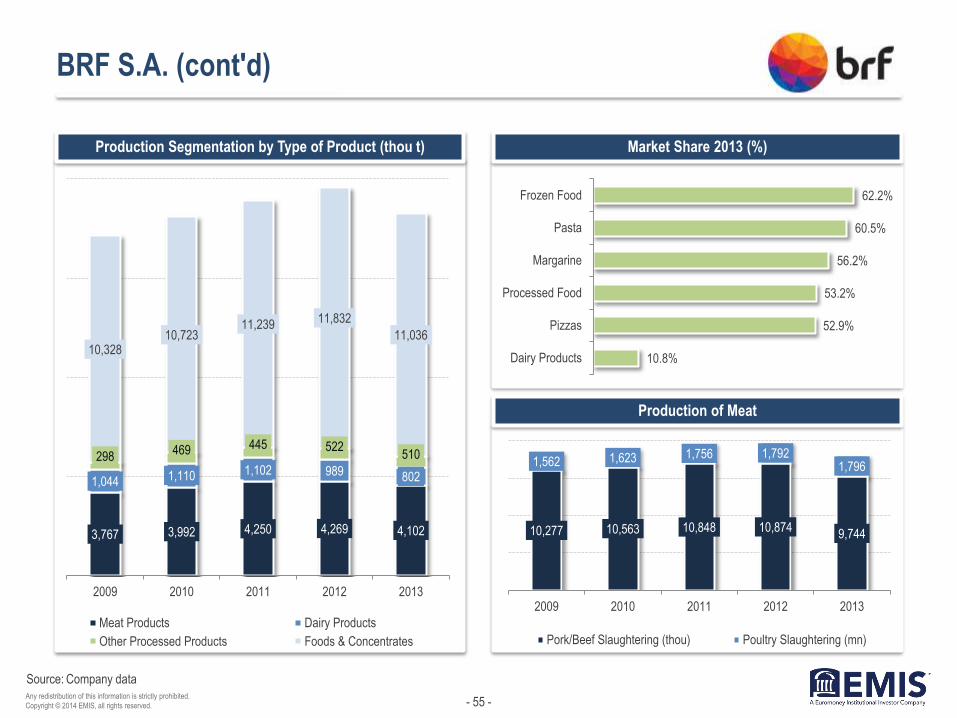

BRF S.A. (cont'd)

Market Share 2013 (%)

Production of Meat

Production Segmentation by Type of Product (thou t)

Company data

3,767 3,992 4,250 4,269 4,102

1,044 1,110 1,102 989 802

298 469 445 522

510

10,328 10,723

11,239 11,832

11,036

2009 2010 2011 2012 2013

Meat Products Dairy Products

Other Processed Products Foods & Concentrates

10.8%

52.9%

53.2%

56.2%

60.5%

62.2%

Dairy Products

Pizzas

Processed Food

Margarine

Pasta

Frozen Food

10,277 10,563 10,848 10,874 9,744

1,562 1,623 1,756 1,792 1,796

2009 2010 2011 2012 2013

Pork/Beef Slaughtering (thou) Poultry Slaughtering (mn)

- 56 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

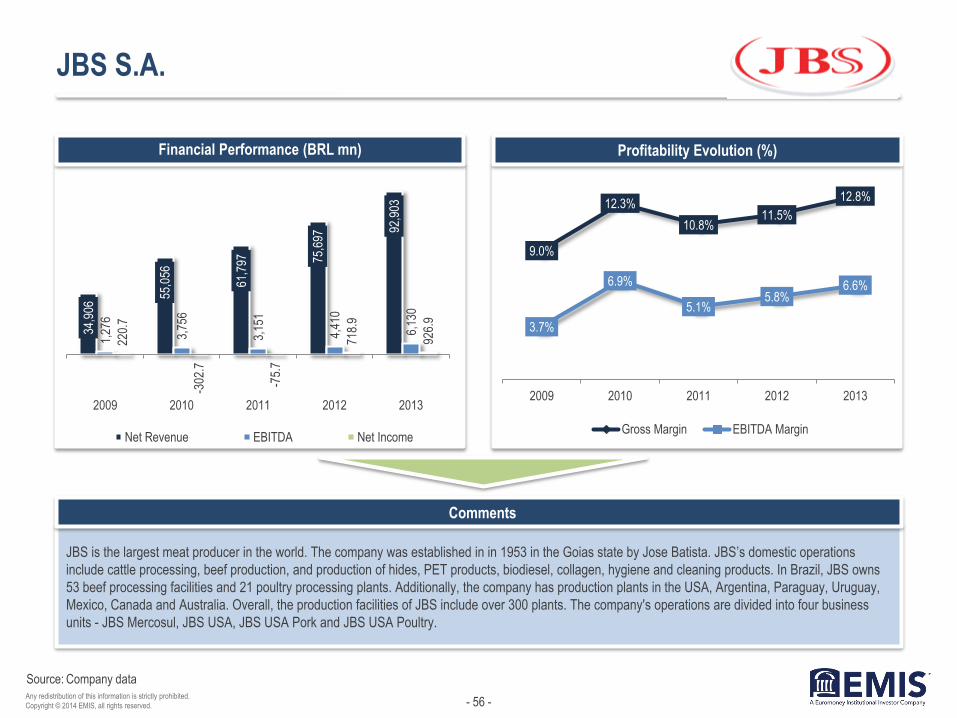

JBS S.A.

JBS is the largest meat producer in the world. The company was established in in 1953 in the Goias state by Jose Batista. JBS’s domestic operations

include cattle processing, beef production, and production of hides, PET products, biodiesel, collagen, hygiene and cleaning products. In Brazil, JBS owns

53 beef processing facilities and 21 poultry processing plants. Additionally, the company has production plants in the USA, Argentina, Paraguay, Uruguay,

Mexico, Canada and Australia. Overall, the production facilities of JBS include over 300 plants. The company's operations are divided into four business

units - JBS Mercosul, JBS USA, JBS USA Pork and JBS USA Poultry.

Financial Performance (BRL mn) Profitability Evolution (%)

Company data

34,9

06 55

,056

61,7

97

75,6

97 92

,903

1,27

6

3,75

6

3,15

1

4,41

0

6,13

0

220.

7

-302

.7

-75.

7

718.

9

926.

9

2009 2010 2011 2012 2013

Net Revenue EBITDA Net Income

9.0%

12.3%

10.8% 11.5%

12.8%

3.7%

6.9%

5.1% 5.8%

6.6%

2009 2010 2011 2012 2013

Gross Margin EBITDA Margin

- 57 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

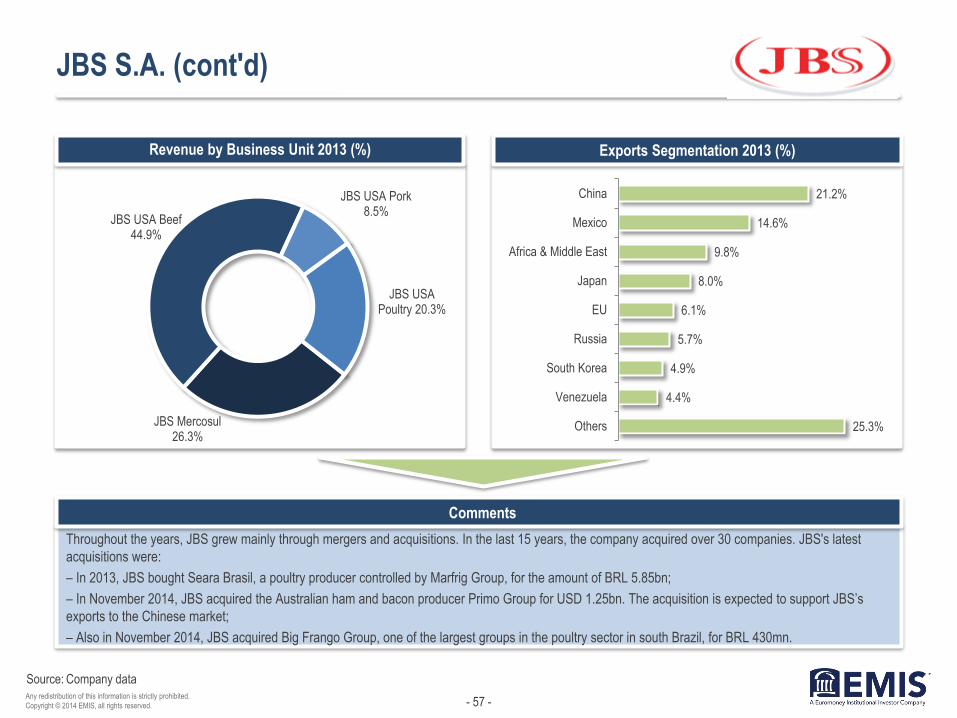

JBS S.A. (cont'd)

Throughout the years, JBS grew mainly through mergers and acquisitions. In the last 15 years, the company acquired over 30 companies. JBS's latest

acquisitions were:

– In 2013, JBS bought Seara Brasil, a poultry producer controlled by Marfrig Group, for the amount of BRL 5.85bn;

– In November 2014, JBS acquired the Australian ham and bacon producer Primo Group for USD 1.25bn. The acquisition is expected to support JBS’s

exports to the Chinese market;

– Also in November 2014, JBS acquired Big Frango Group, one of the largest groups in the poultry sector in south Brazil, for BRL 430mn.

Revenue by Business Unit 2013 (%) Exports Segmentation 2013 (%)

Company data

JBS Mercosul 26.3%

JBS USA Beef 44.9%

JBS USA Pork 8.5%

JBS USA Poultry 20.3%

25.3%

4.4%

4.9%

5.7%

6.1%

8.0%

9.8%

14.6%

21.2%

Others

Venezuela

South Korea

Russia

EU

Japan

Africa & Middle East

Mexico

China

- 58 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

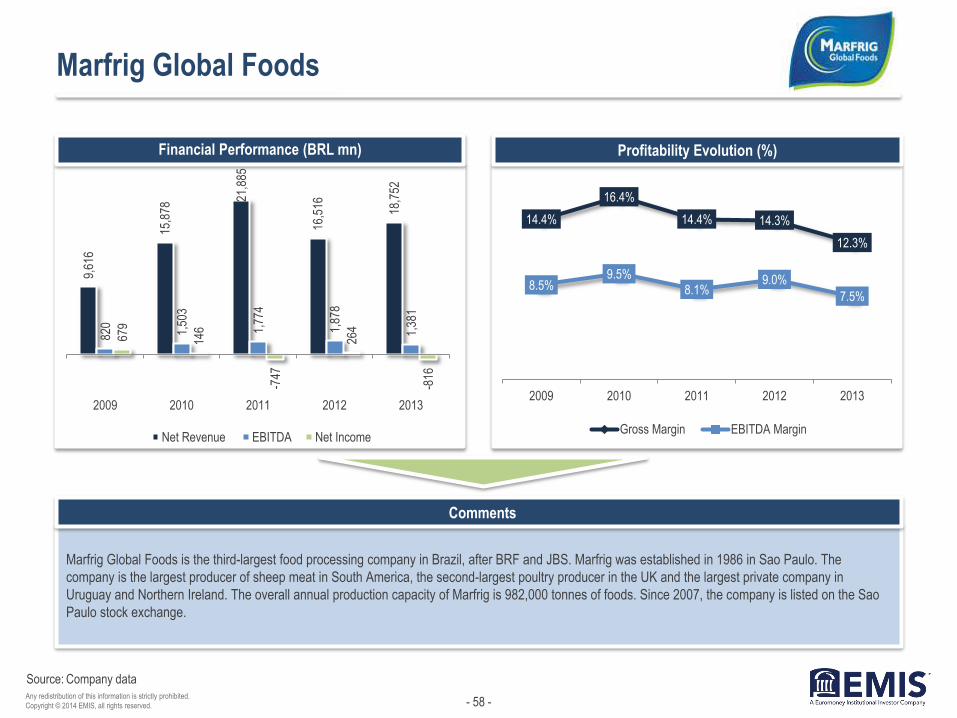

Marfrig Global Foods

Marfrig Global Foods is the third-largest food processing company in Brazil, after BRF and JBS. Marfrig was established in 1986 in Sao Paulo. The

company is the largest producer of sheep meat in South America, the second-largest poultry producer in the UK and the largest private company in

Uruguay and Northern Ireland. The overall annual production capacity of Marfrig is 982,000 tonnes of foods. Since 2007, the company is listed on the Sao

Paulo stock exchange.

Financial Performance (BRL mn) Profitability Evolution (%)

Company data

9,61

6

15,8

78 21

,885

16,5

16

18,7

52

820

1,50

3

1,77

4

1,87

8

1,38

1

679

146

-747

264

-816

2009 2010 2011 2012 2013

Net Revenue EBITDA Net Income

14.4%

16.4%

14.4% 14.3%

12.3%

8.5% 9.5%

8.1% 9.0%

7.5%

2009 2010 2011 2012 2013

Gross Margin EBITDA Margin

- 59 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Marfrig Global Foods (cont'd)

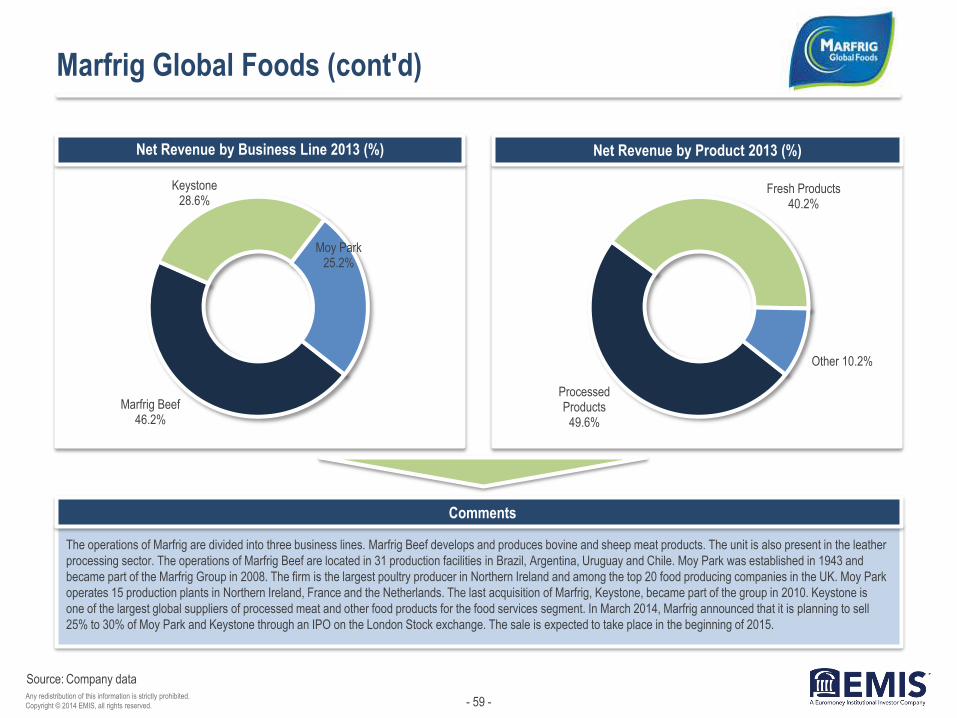

The operations of Marfrig are divided into three business lines. Marfrig Beef develops and produces bovine and sheep meat products. The unit is also present in the leather

processing sector. The operations of Marfrig Beef are located in 31 production facilities in Brazil, Argentina, Uruguay and Chile. Moy Park was established in 1943 and

became part of the Marfrig Group in 2008. The firm is the largest poultry producer in Northern Ireland and among the top 20 food producing companies in the UK. Moy Park

operates 15 production plants in Northern Ireland, France and the Netherlands. The last acquisition of Marfrig, Keystone, became part of the group in 2010. Keystone is

one of the largest global suppliers of processed meat and other food products for the food services segment. In March 2014, Marfrig announced that it is planning to sell

25% to 30% of Moy Park and Keystone through an IPO on the London Stock exchange. The sale is expected to take place in the beginning of 2015.

Net Revenue by Business Line 2013 (%) Net Revenue by Product 2013 (%)

Company data

Processed Products

49.6%

Fresh Products 40.2%

Other 10.2%

Marfrig Beef 46.2%

Keystone 28.6%

Moy Park 25.2%

- 60 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Ambev S.A.

Financial Performance (BRL mn)

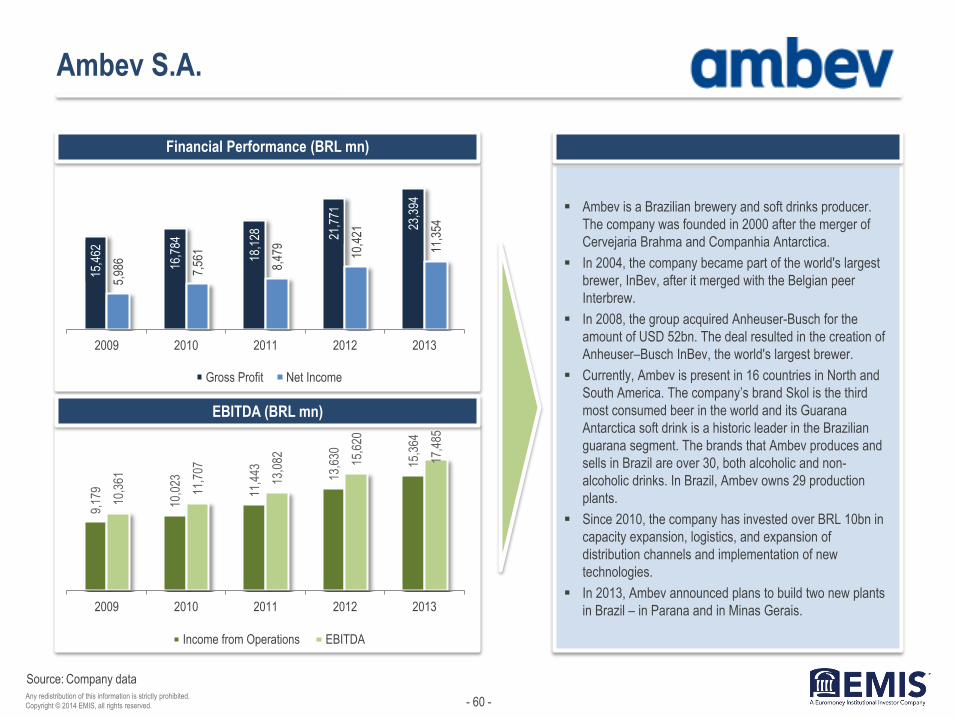

Ambev is a Brazilian brewery and soft drinks producer.

The company was founded in 2000 after the merger of

Cervejaria Brahma and Companhia Antarctica.

In 2004, the company became part of the world's largest

brewer, InBev, after it merged with the Belgian peer

Interbrew.

In 2008, the group acquired Anheuser-Busch for the

amount of USD 52bn. The deal resulted in the creation of

Anheuser–Busch InBev, the world's largest brewer.

Currently, Ambev is present in 16 countries in North and

South America. The company’s brand Skol is the third

most consumed beer in the world and its Guarana

Antarctica soft drink is a historic leader in the Brazilian

guarana segment. The brands that Ambev produces and

sells in Brazil are over 30, both alcoholic and non-

alcoholic drinks. In Brazil, Ambev owns 29 production

plants.

Since 2010, the company has invested over BRL 10bn in

capacity expansion, logistics, and expansion of

distribution channels and implementation of new

technologies.

In 2013, Ambev announced plans to build two new plants

in Brazil – in Parana and in Minas Gerais.

EBITDA (BRL mn)

Company data

15,4

62

16,7

84

18,1

28

21,7

71

23,3

94

5,98

6

7,56

1

8,47

9

10,4

21

11,3

54

2009 2010 2011 2012 2013

Gross Profit Net Income

9,17

9

10,0

23

11,4

43

13,6

30

15,3

64

10,3

61

11,7

07

13,0

82

15,6

20

17,4

85

2009 2010 2011 2012 2013

Income from Operations EBITDA

- 61 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Ambev S.A. (cont'd)

Sales by Region (BRL mn) Domestic Sales (BRL mn)

Company data

15,414 17,711

18,844

21,950 23,480

3,827

3,857

4,778

6,251

7,052

3,953

3,666

3,505

4,031

4,260

23,194

25,234

27,127

32,232

34,792

2009 2010 2011 2012 2013

Latin America/North Latin America/South Canada

12,065

14,279 15,668

17,598 18,407

2,567

2,867

2,949

3,380

3,634

14,632

17,146

18,617

20,978 22,041

2009 2010 2011 2012 2013

Beer Soft Drinks

- 62 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Vigor Alimentos S.A.

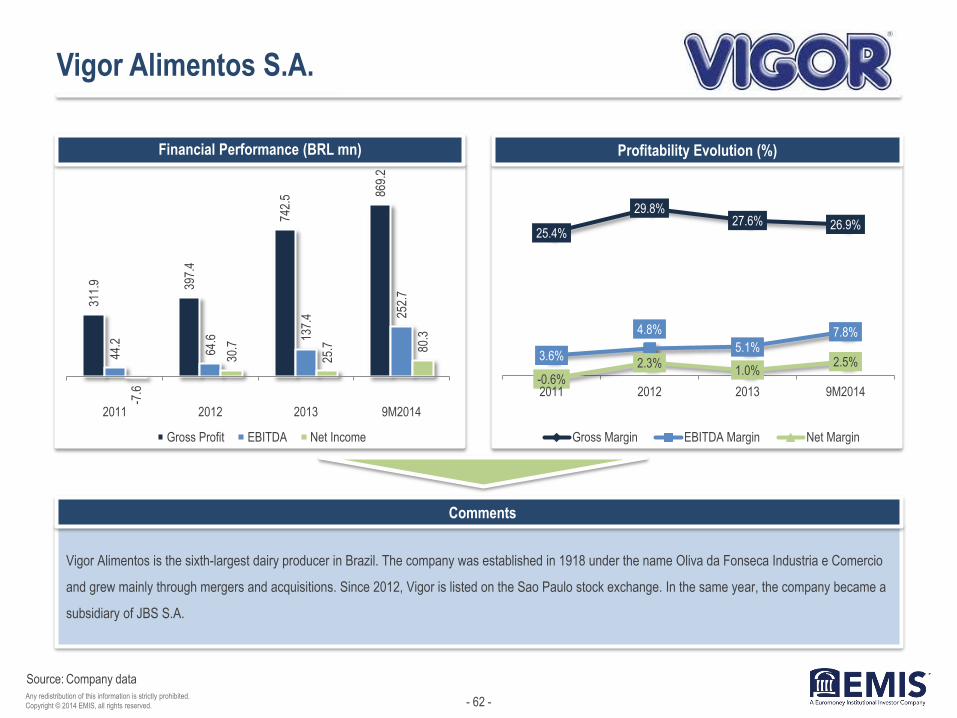

Vigor Alimentos is the sixth-largest dairy producer in Brazil. The company was established in 1918 under the name Oliva da Fonseca Industria e Comercio

and grew mainly through mergers and acquisitions. Since 2012, Vigor is listed on the Sao Paulo stock exchange. In the same year, the company became a

subsidiary of JBS S.A.

Financial Performance (BRL mn) Profitability Evolution (%)

Company data

311.

9 397.

4

742.

5 869.

2

44.2

64.6

137.

4 252.

7

-7.6

30.7

25.7

80.3

2011 2012 2013 9M2014

Gross Profit EBITDA Net Income

25.4%

29.8% 27.6% 26.9%

3.6%

4.8%

5.1% 7.8%

-0.6%

2.3% 1.0%

2.5%

2011 2012 2013 9M2014

Gross Margin EBITDA Margin Net Margin

- 63 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Vigor Alimentos S.A. (cont'd)

Sales Segmentation by Product 2013 (%)

Comments

Revenue Segmentation by Product (BRL mn)

Company data

Dairy Products 31.9%

Spreads 21.9%

UHT Milk 23.6%

Powder Milk 13.7%

Others 8.9%

666.9 751.6

1,108.6 1,109.3

341.0 400.4

474.4 498.8

129.1 98.9

285.9 316.5

729.4

1,241.7

92.6 83.0

94.9

69.5

1,229.6 1,333.9

2,693.2

3,235.8

2011 2012 2013 9M2014

Dairy Products Spreads UHT Milk Powder Milk Others

In the beginning of 2013, Vigor announced the acquisition of its

competitor Itambe Alimentos S.A. for BRL 410mn.

Through the deal Vigor increased its presence in the Minas Gerais and

Rio de Janeiro states. The target company has five production plants and

ten distribution centres.

The other 50% of Itambe are controlled by Central Cooperative of Rural

Producers of Minas Gerais (CCPR).

Also in 2013, Vigor announced the incorporation of Laticinios MB. The

acquisition of the company was made in 2012 and increased Vigor's

presence on the parmesan cheese market in Brazil.

- 64 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Contact:

Corporate Headquarters

Nestor House

Playhouse Yard

London EC4V 5EX

UK

Voice: +44 207 779 8471

Fax: +44 207 779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

U.S.

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No.

III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organisations, and others.