Fomc 20020626 Material

50

Appendix 1: Materials used by Mr. Kos June 25-26, 2002 130 of 179

-

Upload

fraser-federal-reserve-archive -

Category

Documents

-

view

212 -

download

0

Transcript of Fomc 20020626 Material

Appendix 1: Materials used by Mr. Kos

June 25-26, 2002 130 of 179

1.52

2.53

3.54

4.55

5.56

6.5

Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-041.522.533.544.555.566.5

-43 bps

4.5

4.8

5.1

5.4

5.7

3/1 3/11 3/21 3/31 4/10 4/20 4/30 5/10 5/20 5/30 6/9 6/194.5

4.8

5.1

5.4

5.7

Rates Implied by Eurodollar Futures CurveComparison of March 19, May 6, & June 24, 2002

Page 1

PercentPercent

Source: Bloomberg

March 19, 2002May 6, 2002

-60 bps-70 bps-74 bps

-65ps

-52 bps -45 bps-42 bps

-43 bps

2.6

2.9

3.2

3.5

3.8

3/1 3/11 3/21 3/31 4/10 4/20 4/30 5/10 5/20 5/30 6/9 6/192.6

2.9

3.2

3.5

3.8

10 -Year Treasury YieldMarch 1, 2002 - June 24, 2002

PercentPercent

2 -Year Treasury YieldMarch 1, 2002 - June 24, 2002

FOMC3/19

FOMC3/19

Source: BloombergSource: Bloomberg

PercentFOMC

5/7FOMC

5/7

June 24, 2002

-39ps

28

30

32

34

36

38

40

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/2128

30

32

34

36

38

40

Eurodollar Deposit Futures Implied Volatility (December contract)March 1, 2002 to June 24, 2002 PercentPercent

Source: Bloomberg

June 25-26, 2002 131 of 179

88

90

92

94

96

98

100

102

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/2188

90

92

94

96

98

100

102

Page 2

1.31 4.80 4.92 4.95 5.01 5.09 5.17 5.34 5.40 6.00 6.510

1

2

3

4

5

6

7

Japan U.S. Germany U.K. France Spain Italy Canada Sweden Australia NewZealand

Global 10-yr. Government Bond YieldsAs of June 24, 2002 PercentPercent

Source: Bloomberg

Source: Bloomberg

6

8

10

12

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/216

8

10

12

1- month Euro-Dollar and Dollar-Yen Exchange Rate Option Implied VolatilityMarch 1, 2002 to June 24, 2002 PercentPercent

Source: Bloomberg

Euro-dollar

Dollar-yen

FOMC3/19

FOMC5/7

Index3/1/2002=100

Index3/1/2002=100

U.S. Dollar Versus Selected Foreign CurrenciesMarch 1, 2002 - June 24, 2002

Swiss Franc

Euro

British Pound

Canadian Dollar

Australian Dollar

Yen

June 25-26, 2002 132 of 179

78

82

86

90

94

98

102

106

110

3/1 3/11 3/21 3/31 4/10 4/20 4/30 5/10 5/20 5/30 6/9 6/1978

82

86

90

94

98

102

106

110

Domestic EquitiesMarch 1, 2002 - June 24, 2002

Page 3

80

85

90

95

100

105

110

115

3/1 3/11 3/21 3/31 4/10 4/20 4/30 5/10 5/20 5/30 6/9 6/1980

85

90

95

100

105

110

115

International EquitiesMarch 1, 2002 - June 24, 2002

18

20

22

24

26

28

30

32

34

3/1 3/11 3/21 3/31 4/10 4/20 4/30 5/10 5/20 5/30 6/9 6/1918

20

22

24

26

28

30

32

34

S&P 100 Volatility Index (VIX)March 1, 2002 - June 24, 2002 PercentPercent

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Index3/1/02=100

Index3/1/02=100

Index3/1/02=100

Index3/1/02=100

FOMC3/19

FOMC5/7

Dow S&P 500

Nasdaq

FOMC3/19

FOMC5/7Bolsa

Swiss Market Index German DAX

FTSE

FOMC5/7

FOMC3/19

Nikkei

June 25-26, 2002 133 of 179

Page 4

Domestic Credit Spreads to Comparable TreasuriesMarch 1, 2002 to June 24, 2002

40

50

60

70

80

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/2140

50

60

70

80

100

120

140

160

180

200

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/21100

120

140

160

180

200Basis pointsBasis points Basis points

Source: Bloomberg Source: Bloomberg

10-Year Fannie Mae Benchmark

10-Year US Interest Rate Swaps

A-1 Industrial Corporate

30-yr. Fannie Mae Current Coupon MBS

400

700

1000

1300

1600

3/1 3/15 3/29 4/12 4/26 5/10 5/24 6/7 6/21400

700

1000

1300

1600

U.S. Corporate High Yield, EMBI+ and the Brazilian Sub-ComponentMarch 1, 2002 to June 24, 2002 Basis pointsBasis points

Source: Bloomberg Merrill Lynch High Yield Spread

Brazilian Sub-component of the JP MorganEMBI+ Sovereign Spread

JP Morgan EMBI+ Sovereign Spread

4/23/02 WCOMdowngrade to

Baa2

5/29/02ATT

downgradeto Baa2

5/9/02WCOMdowngrade toHigh Yield

June 25-26, 2002 134 of 179

$ Billions

0

10

20

30

40

50

60

70

80

1996 1997 1998 1999 2000 2001 20020

10

20

30

40

50

60

70

80Net Portfolio Expansion Purchases to Offset Redemptions

$ Billions

CurrentForecast

570

580

590

600

610

620

630

640

650

12/1 1/1 2/1 3/1 4/1 5/1 6/1 7/1 8/1 9/1 10/1 11/1 12/1570

580

590

600

610

620

630

640

650

Currency Component of M1 (excludes vault cash) Seasonally AdjustedDecember 2001 - December 2002

Page 5

$ Billions$ Billions

Total Outright Purchases and Net Soma Expansion1996 - 2002

Actuals

Current Estimates (10% growth throughSeptember, 8% growth through December)

Estimates as of the May FOMC meeting(9% growth over forecast period)

June 25-26, 2002 135 of 179

Appendix 2: Materials used by Mr. Rolnick

June 25-26, 2002 136 of 179

June 25-26, 2002 137 of 179

June 25-26, 2002 138 of 179

June 25-26, 2002 139 of 179

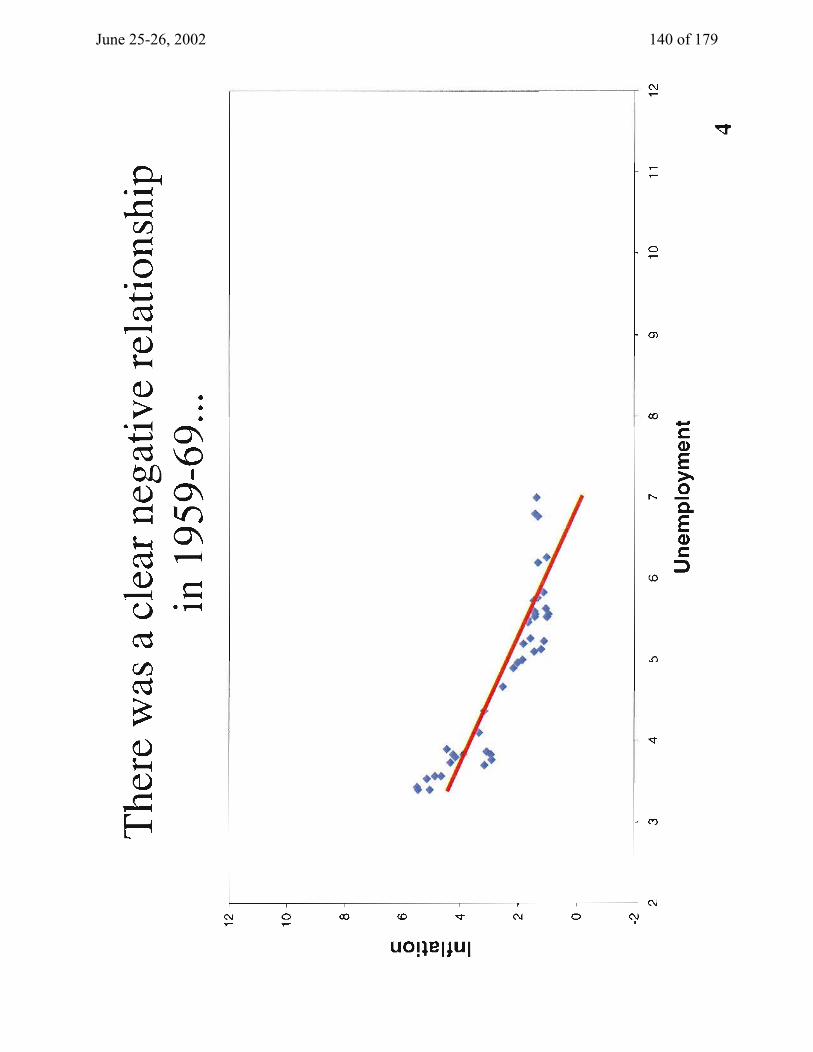

June 25-26, 2002 140 of 179

June 25-26, 2002 141 of 179

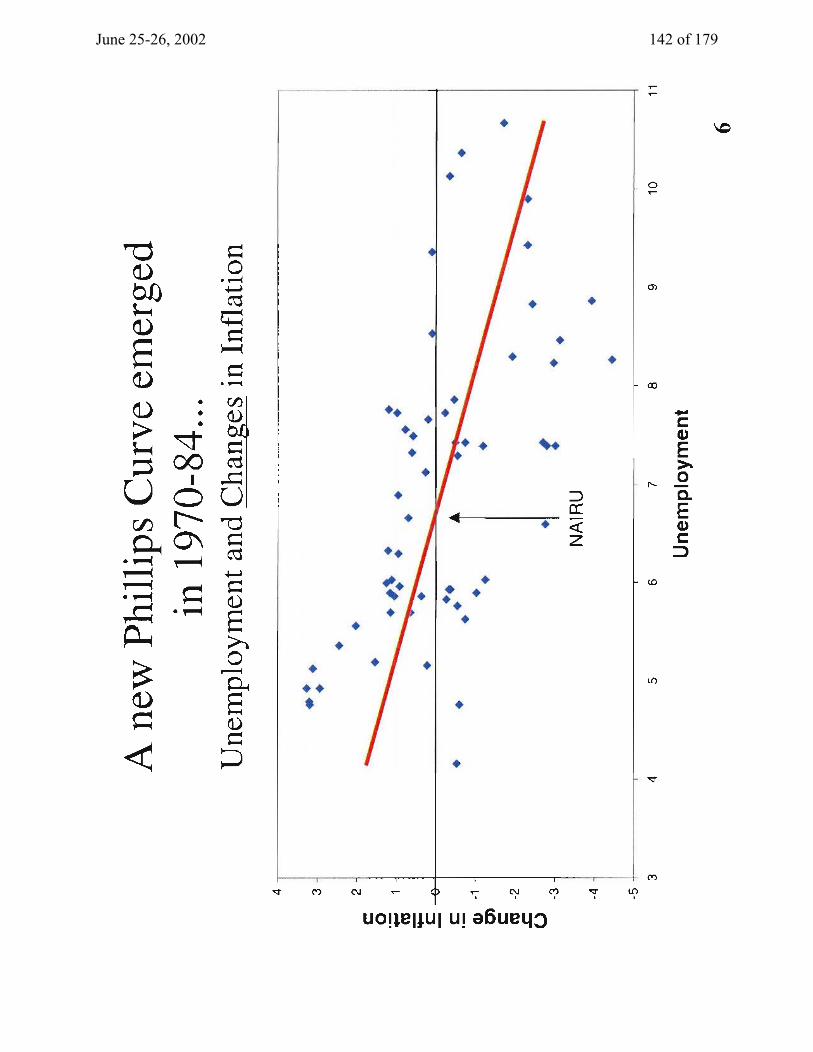

June 25-26, 2002 142 of 179

June 25-26, 2002 143 of 179

June 25-26, 2002 144 of 179

June 25-26, 2002 145 of 179

June 25-26, 2002 146 of 179

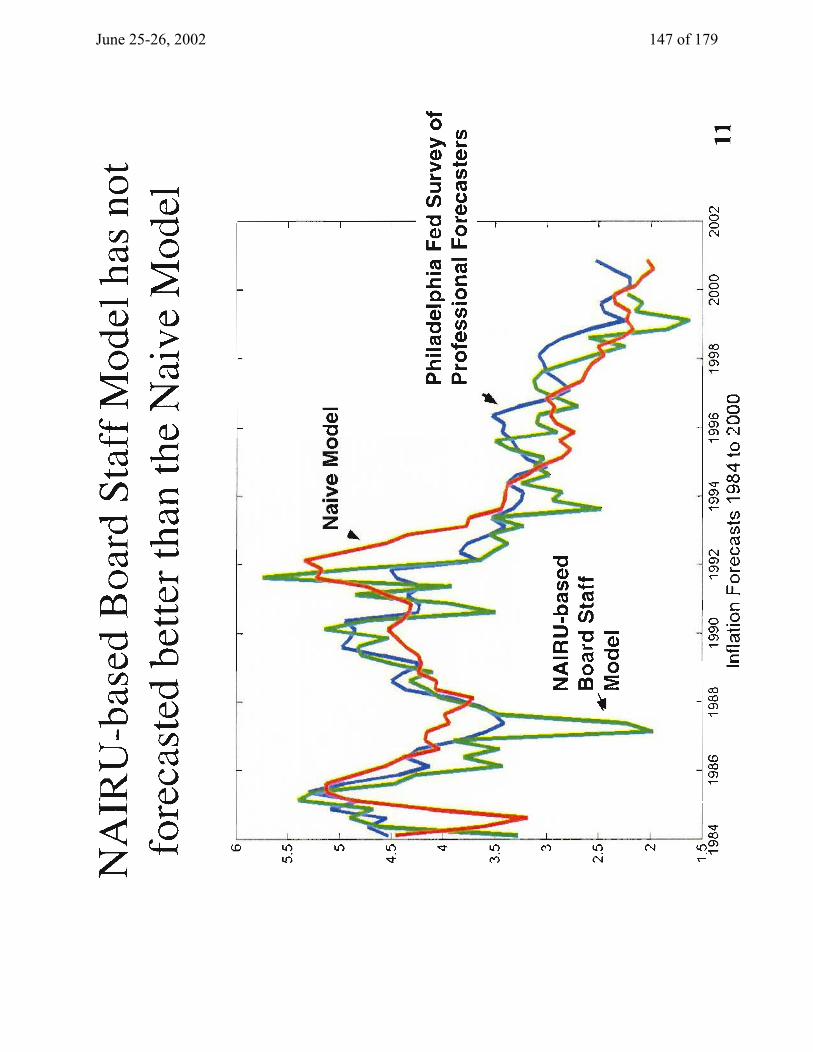

June 25-26, 2002 147 of 179

June 25-26, 2002 148 of 179

June 25-26, 2002 149 of 179

June 25-26, 2002 150 of 179

June 25-26, 2002 151 of 179

June 25-26, 2002 152 of 179

June 25-26, 2002 153 of 179

Appendix 3: Materials used by Mr. Roberts and Mr. Lebow

June 25-26, 2002 154 of 179

Material for

Board Staff Presentation on Explaining Low Inflation Since the Mid-1990s

Division of Research and Statistics

June 25, 2002

June 25-26, 2002 155 of 179

June 25-26, 2002 156 of 179

Exhibit 2

The FRB/US Model of Inflation Dynamics

• Bt = $ Bt-1 + (1-$) Bte - ( (Ut - Ut

n) + relative price shocks + unit labor costs

B = rate of price inflation

B e = expected rate of price inflation

U = unemployment rate

U n = natural rate of unemployment

$, ( = coefficients

• B e reflects knowledge of the structure of the economy, including the conduct ofmonetary policy.

• How do our factors fit in this model?

< Changes in the conduct of monetary policy alter the influence of U on B e.

< Changes in labor productivity growth affect inflation through unit labor costs.

< Labor market developments shift U n.

• Movements of (U - U n) explain about 20 percent of the variation of year-to-yearchanges in inflation.

June 25-26, 2002 157 of 179

June 25-26, 2002 158 of 179

June 25-26, 2002 159 of 179

June 25-26, 2002 160 of 179

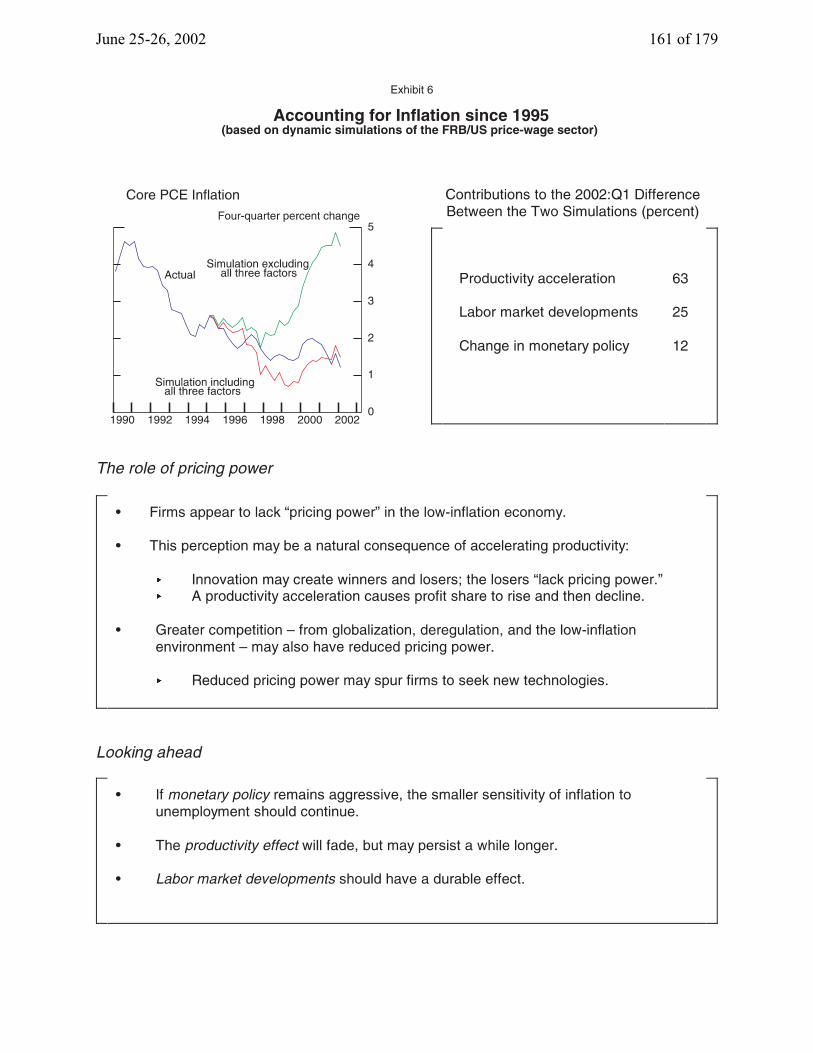

June 25-26, 2002 161 of 179

Appendix 4: Materials used by Mr. Stockton, Mr. Oliner, and Ms. Johnson

June 25-26, 2002 162 of 179

June 25-26, 2002 163 of 179June 25-26, 2002 163 of 179

June 25-26, 2002 164 of 179

June 25-26, 2002 165 of 179

June 25-26, 2002 166 of 179

June 25-26, 2002 167 of 179

June 25-26, 2002 168 of 179

June 25-26, 2002 169 of 179

June 25-26, 2002 170 of 179

June 25-26, 2002 171 of 179

June 25-26, 2002 172 of 179

June 25-26, 2002 173 of 179

June 25-26, 2002 174 of 179

June 25-26, 2002 175 of 179

June 25-26, 2002 176 of 179

June 25-26, 2002 177 of 179

June 25-26, 2002 178 of 179

June 25-26, 2002 179 of 179