Focus Deal oF the Week InDustRy Q&a Selectively sellingNew York 660 Madison Avenue, New York, NY...

21

Asia’s Private Equity News Source avcj.com September 10 2013 Volume 26 Number 34 FOCUS DEAL OF THE WEEK Selectively selling Asia makes its - small - mark on a difficult global secondaries market Page 7 Enter the litigators Financiers offer PE returns via the courts Page 10 The kids are all right Wolseley sells childcare business to Navis Page 17 Data f ile Page 19 AVCJ RESEARCH INDUSTRY Q&A China fund-of-funds struggle for direction Page 14 DEAL OF THE WEEK FOCUS Jupiter Capital’s Indika Hettiarachchi Page 18 PE investosr exit China payments firm to Ping An Page 17 Trade buyers target China internet assets Page 3 CHAMP Private Equity, CVCI, Hamilton Lane, Headland, NewQuest, OTPP, Quadria, Sequoia Page 4 EDITOR’S VIEWPOINT NEWS

Transcript of Focus Deal oF the Week InDustRy Q&a Selectively sellingNew York 660 Madison Avenue, New York, NY...

Asia’s Private Equity News Source avcj.com September 10 2013 Volume 26 Number 34

Focus Deal oF the Week

Selectively sellingAsia makes its - small - mark on a difficult global secondaries market Page 7

Enter the litigators Financiers offer PE returns via the courts Page 10

The kids are all rightWolseley sells childcare business to Navis Page 17

Data f ile Page 19

aVcJ ReseaRch

InDustRy Q&a

China fund-of-funds struggle for direction

Page 14

Deal oF the Week

Focus

Jupiter Capital’s Indika Hettiarachchi

Page 18

PE investosr exit China payments firm to Ping An

Page 17

Trade buyers target China internet assets

Page 3

CHAMP Private Equity, CVCI, Hamilton Lane, Headland, NewQuest, OTPP, Quadria, Sequoia

Page 4

eDItoR’s VIeWpoInt

neWs

Anything is possible...

There are many barriers to liquidity in private equity: complexity,

transaction size, deadlines, disparate assets, confidentiality, alignment,

tax, shareholder sensitivities – the list goes on.

But with creativity, experience and determination ... anything is possible.

Contact: [email protected] solutions for private equity investors worldwide

Hong Kong20 Pedder Street

Hong Kong

London33 Cavendish Square

London

New York950 Third Avenue

New York

www.collercapital.com

European SecondariesDeal of the Year –

Lloyds Banking Group

Secondaries Firm ofthe Year for the

8th consecutive year

Number 34 | Volume 26 | September 10 2013 | avcj.com 3

eDItoR’s [email protected]

We have groWn accustomed to China’s incumbent internet giants engaging in M&A. Since 2010, the BATS – Baidu, Alibaba Group, Tencent Holdings and Sina – have deployed around $6.5 billion (and that’s just disclosed transactions), eight times the amount spent in the preceding eight years.

Financial institutions make an interesting addition to the mix. Last week an affiliate of Ping An Insurance Group acquired SmartPay, one of the country’s leading mobile payment providers. The investment facilitated the exit of Lunar Capital, RRE Ventures and Icon.

From SmartPay’s perspective, the buyer could have been a domestic e-commerce platform, some of which might like to own one of the channels customers use to pay for products. Ping An, however, wanted to slot SmartPay into its own electronic payments offering, scale up the business and create a viable challenger to market leader Alipay, part of the Alibaba empire.

The BATS are pursuing acquisitions for a combination of financial and strategic reasons. They are under pressure from shareholders to deploy capital and diversify their portfolios and have sufficient resources to achieve this through inorganic rather than organic expansion.

Baidu, for example, built its search engine business on PCs but is now responding to growth in smart phone usage by targeting

mobile platforms. Hence its acquisitions of 91 Wireless, a mobile app store and game operator, and iQiyi, which is an online video platform popular with mobile users.

China’s financial services companies are in a similar position. They didn’t emerge online but have invested in creating a presence there, and now they must do the same with mobile.

Competition between financial services providers and internet companies is unlikely to be as intense as that between the internet companies themselves. First, financial services in China are still highly regulated and profits are to a large extent dictated by government-set product prices. Second, they are not trying to develop broader platforms at the expense of one another. And third, in the most part they are targeting different kinds of assets.

But for a start-up with a technology that is applicable e-commerce – online payment platforms, customer verification software, or anything that facilitates the transition from bricks and mortar to mobile – the universe of trade buyers is bigger than one might think.

Tim BurroughsManaging EditorAsian Venture Capital Journal

Battle of the strategics

Managing Editor Tim Burroughs (852) 3411 4909

Staff Writers Andrew Woodman (852) 3411 4852 Mirzaan Jamwal (852) 3411 4821

Winnie Liu (852) 3411 4907

Creative Director Dicky Tang Designers

Catherine Chau, Edith Leung, Mansfield Hor, Tony Chow

Senior Research Manager Helen Lee

Research Manager Alfred Lam

Research Associates Herbert Yum, Isas Chu, Jason Chong, Kaho Mak

Circulation Manager Sally Yip

Circulation Administrator Prudence Lau

Manager, Delegate Sales Pauline Chen

Senior Marketing Manager Rebecca Yuen

Director, Business Development Darryl Mag

Manager, Business Development Anil Nathani, Samuel Lau

Sales Coordinator Debbie Koo

Conference Managers Jonathon Cohen, Sarah Doyle, Zachary Reff,

Conference Administrator Amelie Poon

Conference Coordinator Fiona Keung, Jovial Chung

Publishing Director Allen Lee

Managing Director Jonathon Whiteley

The Publisher reserves all rights herein. Reproduction in whole or in part is permitted only with the written consent of

AVCJ Group Limited. ISSN 1817-1648 Copyright © 2013

Incisive Media Unit 1401 Devon House, Taikoo Place

979 King’s Road, Quarry Bay,Hong Kong

T. (852) 3411-4900F. (852) 3411-4999E. [email protected]

URL. avcj.com

Beijing Representative officeNo.1-2-(2)-B-A554, 1st Building,

No.66 Nanshatan,Chaoyang District, Beijing,People’s Republic of China

T. (86) 10 5869 6203F. (86) 10 5869 6205 E. [email protected]

Anything is possible...

There are many barriers to liquidity in private equity: complexity,

transaction size, deadlines, disparate assets, confidentiality, alignment,

tax, shareholder sensitivities – the list goes on.

But with creativity, experience and determination ... anything is possible.

Contact: [email protected] solutions for private equity investors worldwide

Hong Kong20 Pedder Street

Hong Kong

London33 Cavendish Square

London

New York950 Third Avenue

New York

www.collercapital.com

European SecondariesDeal of the Year –

Lloyds Banking Group

Secondaries Firm ofthe Year for the

8th consecutive year

M&A activity by Baidu, Alibaba, Tencent and Sina

Source: AVCJ Research Note: Does not include take-private of Alibaba.com/Yahoo buyback; or itself as a target

5,000

4,000

3,000

2,000

1,000

0

20

15

10

5

0

US$

mill

ion

Dea

ls

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013YTD

Baidu Alibaba Tencent Sina Total deal value (US$m)

avcj.com | September 10 2013 | Volume 26 | Number 344

GLOBAL

Hamilton Lane closes third fund at $900mHamilton Lane held a final close of $900 million on its Hamilton Lane Secondary Fund III, surpassing the original target of $650 million. The LP base includes public and corporate pension funds, family offices and high-net-worth investors, sovereign wealth funds, endowments and foundations, and insurance companies.

ASIA PACIFIC

OTPP loses head of Asia fund investmentsAlison Nankivell has left her role as head of Asian fund investments at Ontario Teachers’ Pension Plan for a job with Business Development Bank of Canada. The change comes as OTPP prepares for the formal launch of its Hong Kong office.

AUSTRALASIA

BlueChilli targets $10m for angel fundAustralian venture firm BlueChilli is looking to raise a $10 million angel fund for early-stage tech investments. The vehicle has raised $2.2 million to date. Individuals can invest a minimum of $100,000, paid in at an annual rate of $20,000 over five years. Artesian Venture Partners will manage the fund.

CHAMP, Headland seek Miclyn buyoutCHAMP Private Equity and Headland Capital Partners have offered to buy the 24.8% of Miclyn Express Offshore (MEO) they do not own for around A$150 million ($137 million). The firms are offering to pay A$2.20 per share, which matches what they paid back in April for an additional 8% stake. MEO charters service vessels to the offshore oil and gas industry across Southeast Asia, Australia and the Middle East.

AVCAL CEO Katherine Woodthorpe resignsKatherine Woodthorpe, CEO of the Australian Private Equity and Venture Capital Association (AVCAL), has resigned. Having spent seven years in the role, Woodthorpe announced she would

be stepping down on October 31 in order to “pursue fresh challenges.”

GREATER CHINA

Sequoia invests $10m in personal finance siteSequoia Capital has committed a total of $10 million across two rounds of funding for Feidee.com, a Chinese personal finance management website with over 60 million registered users. The company completed a Series A round in December and the second round came last month. It also operates another site called

Cardniu.com, which is a mobile app to manage credit card expenditure.

Morgan Stanley part exits Sihuan PharmaMorgan Stanley Private Equity Asia (MSPEA) will reduce its stake in Hong Kong-listed Sihuan Pharmaceutical Holdings from 7.17% to 5.24% via a block trade agreement. Based on current market prices, MSPEA’s remaining holding is worth HK$1.4 billion ($180 million). The PE firm took a 10% stake in Sihuan in 2009.

China Fortune Link to set up Qinghai VC fundChina Fortune Link Fund Management has rolled out a RMB100 million ($16.3 million) venture capital fund to invest in Qinghai, a province located in China’s far northwest. The firm hopes to partner with the local government to launch VC funds to support potential start-ups in the region. It previously set up a RMB1 billion VC fund targeting Ningxia Hui Autonomous Region.

Temasek, DCM back $60m round for China travel siteTemasek Holdings and existing backer DCM have invested in a $60 million Series D round of funding for Tuniu.com, a Chinese online travel tour provider. The proceeds will be used to optimize its online products and staff hiring.In the first half of this year, Tuniu offered over 40 thousand tours to more than 3 million visitors.

CFIUS approves Shuanghui acquisition The Committee on Foreign Investment in the United States (CFIUS) has cleared the way for PE-backed Chinese pork producer Shuanghui International to buy US counterpart Smithfield Foods, overcoming one of the biggest hurdles to the $4.7 billion deal. Approval from Smithfield’s shareholders is still required. This is expected at a meeting on September 24, after which the transaction will formally close.

NORTH ASIA

Rakuten acquires VC-backed video site VikiJapanese e-commerce giant Rakuten has acquired Viki, a VC-backed global video streaming platform with social TV and subtitling capability.The financial details of the transaction were

Citigroup sells CVCI to Rohatyn GroupCitigroup is selling its $4.3 billion PE unit, Citi Venture Capital International (CVCI), to emerging markets investment firm The Rohatyn Group (TRG) for an undisclosed sum. The deal will see TRG’s footprint expand to 18 offices worldwide with more than $7 billion in total assets under management. Of this, around $6 billion is in private equity.

The transaction, which is expected to close in the fourth quarter, is the latest deal to help TRG broaden its Asia presence. In 2012, it acquired a 60% stake in Singapore-based mid-market infrastructure PE firm CapAsia, while in 2011 is bought 50% of PE real estate investor Arch Capital.

Founded in 2001, CVCI is part of Citi’s alternative asset management platform Citi Capital Advisors. It operates exclusively in emerging markets and currently oversees five funds with $4.3 billion in equity investments and committed capital. The sales reflects Citi’s decision to shed its private equity and hedge funds to comply with the Volcker Rule - part of the 2010 Dodd-Frank financial reform legislation that restrict banks’ holdings of alternative investments.

neWs

New York 660 Madison Avenue, New York, NY 10065 212 754 0411 Boston 111 Huntington Avenue, Suite 3020, Boston, MA 02199 617 247 7010 Menlo Park 3000 Sand Hill Road, 1-220, Menlo Park, CA 94025 650 561 9600

London 42 Berkeley Square, London W1J 5AW 44 20 7318 0888 Hong Kong 15/F York House, The Landmark, 15 Queen's Road Central, Central, Hong Kong 852 3987 1600

[email protected] www.lexingtonpartners.com

June 2013

Lexington Co-Investment Partners III, L.P.

THIS PARTNERSHIP HAS BEEN ESTABLISHED EXCLUSIVELY

TO MAKE EQUITY CO-INVESTMENTS IN TRANSACTIONS

LED BY PRIVATE EQUITY SPONSORS GLOBALLY.

$1,575,000,000

avcj.com | September 10 2013 | Volume 26 | Number 346

not disclosed. Investors in Viki include Charles River Ventures, Omidyar Network, Andreessen Horowitz, Greylock Partners and Neoteny Labs, among others.

Future Venture Capital raises $5m fundJapan’s Future Venture Capital has raised a JPY500 million ($5 million) venture fund, Ehime Venture Fund 2013, which is backed by regional lender Ehime Bank with a JPY475 million commitment. It will focus on making investments in unlisted high growth technology companies in Ehime prefecture in Western Japan, with a view to taking them public.

Nissay Capital leads $1.5m round in WelSelfNissay Capital has a led a JPY150 million ($1.5 million) round of investment in WelSelf, the Tokyo-based start-up behind online skils marketplace Coconala. Other investors include internet marketing companies Opt and Adways, and the CEO of cosmetics site iStyle. Coconala allows users to trade knowledge, skills and experience from one another.

SOUTH ASIA

Patnis set up incubator for big data start-upsThe co-founders of Nirvana Venture Advisors, Arihant and Amit Patni, have set up Hive Technologies to invest $200,000 to $2 million in Indian big data start-ups. Hive will back 4-5 companies every year over the next two years, with an exit horizon of 8-10 years. The focus is on ventures with expertise in telecom, fraud detection, social media and customer relationship management.

StanChart raises stake in Fortis HealthcareStandard Chartered Private Equity has invested a further INR370.3 million ($5.7 million) to buy preferential shares in India’s Fortis Healthcare. It brings SCPE’s total investment into the company to approximately INR2.5 billion. Fortis said the deal concluded its fundraising initiatives for the year, which have aggregated to INR10.4 billion.

Matrix commits $6m to Meditrina HospitalsMatrix Partners India has invested INR400 million

($6 million) in Meditrina Hospitals for a significant minority stake. Meditrina currently operates four centers focused on cardiology in the state of Kerala. The proceeds will be used to expand its footprint by setting up 20 specialty inside hospital units in second tier cities in India.

Motilal Oswal PE closes $155m fundMotilal Oswal Private Equity (MOPE) has closed its growth capital India Business Excellence Fund II (IBEF-II) at $155 million (INR10 billion). The fund

was launched in July 2011, and has raised $105 million from international investors and $50 million from domestics. It will invest in 12-15 mid-market companies, with the preferred themes of domestic consumption, financial services, healthcare and niche manufacturing and infra services.

SOUTHEAST ASIA

Lombard closes fourth Asia fund at $350m hard capLombard Investments has closed its fourth Asia fund at the hard cap for institutional commitments of $350 million after 18 months in the market. It will make growth-oriented investments in companies formed and operated in Southeast Asia. LPs include the International Finance Corporation (IFC), which agreed to contribute $25 million.

Traveloka gets Series A round from SamwersGlobal Founders Capital (GFC) a VC firm co-founded by Rocket Internet’s Samwer brothers, has made its first Asia investment - committing an undisclosed sum to Indonesian flight search engine Traveloka. Launched in September 2012, Traveloka started as an airline ticket search engine for mostly domestic flights but now also processes ticket bookings.

Quadria reaches first close on healthcare fundQuadria Capital has reached a first close of $107 million on its second fund, which invests in mid-size healthcare companies in South and Southeast Asia. Only 30% of the capital will be deployed in India. It has attracted commitments from development finance institutions, investment institutions, corporates and family offices globally, some of which have considerable healthcare experience.

Malaysia’s Ekuinas to back five local PE managersMalaysian government-backed PE investor Ekuinas will make LP commitments to funds raised by five local PE firms – Tael Partners, RM Capital Partners, Tuas Capital Partners and CMS Opus Private Equity will receive MYR240 million ($72.2 million) in seed capital. The fifth GP is Asiasons, selected as a replacement manager for the first tranche of this capital outsourcing program.

NewQuest tries to buyout China HydroelectricNewQuest Capital Partners has made a take-private offer to US-listed China Hydroelectric that values the company at just over $160 million. The secondary specialist GP already owns 49.83% of China Hydroelectric and holds options and warrants that, if exercised, would increase its stake to 56.8%. CPI Ballpark Investments, a NewQuest affiliate, has offered to buy all outstanding American Depository Shares (ADS) at $2.97 apiece.

Last year, an investor group led by NewQuest instigated the removal of five of China Hydroelectric’s seven directors, citing strategic and operational issues at the company and the

apparent lack of credibility and accountability on the board. They were replaced by four directors nominated by the investor group. In addition to NewQuest, which spun out from Bank of America Merrill Lynch in 2011, the group comprised Swiss Re, Tsing Capital and Aqua Resources, as well as two family offices, Abrax and IWU International.

China Hydroelectric was set up in 2006 to acquire and operate small hydroelectric power projects of less than 50 megawatts in capacity. It posted revenues of $85.4 million in 2012, up 56% year-on-year, which saw its net loss narrow to $1.1 million from $55.3 million. The company had a working capital deficiency of approximately $81 million.

neWs

Number 34 | Volume 26 | September 10 2013 | avcj.com 7

coVeR [email protected]

the rupee is currently trading at around INR65 to the dollar. It has slumped more than 20% since May, driven by international investors pulling their money out of India. For an LP in an India-focused private equity fund, that committed capital in US dollars, it makes for grim reading. Those that went in when the market was at its peak in 2006-2008 were getting INR40 on the dollar. Even if the fund portfolio has doubled in local currency terms, with talk of the rupee entering INR70 territory and beyond, the LP could still be looking at a US dollar return closer to 1x.

Are these investors looking to cut their losses

and trade out their positions at a discount on the secondary market, or is there a sense that the situation can’t get any worse?

“Net asset value (NAV) is down by 50% in US dollar terms so performance is much worse and distributions are paling in comparison to what many people expected – but at the same time capital calls are cheaper if you are investing,” says Juan Delgado-Moreira, managing director at Hamilton Lane. “In the first half of the game you don’t worry too much; that comes in the second half. Most secondary deals normally happen in years 4-7. There will be more rebalancing but it hasn’t happened yet.”

Other market participants say the wheel is already turning, and not just on India. Although economists have revised their China growth projections upwards on the back of recent encouraging indicators, GDP expansion has

slowed in nine of the last 10 quarters. Indonesia, meanwhile, saw growth slip below 6% last quarter for the first time since 2010, adding to concerns about slowing investment, accelerating inflation and a weakening currency.

There may be optimism regarding these countries’ long-term prospects, but investors are calculating the opportunity cost of their exposure.

“We are seeing more Asian funds in global portfolio sales,” says Hiro Mizuno, a partner at Coller Capital. “Right after Lehman there were so many secondary transactions but quite a few

sellers opted to hold on to their Asian assets because they expected more outperformance. Now sentiment has changed. There is no justification for holding on to Asian funds.”

Still small fryAnother explanation is simply that the market is maturing. Asia saw a huge amount of fundraising during the vintage preceding the global financial crisis; many of these vehicles are now fully invested and LPs are considering their options. In addition to the pan-regional funds, there are now more country-specific vehicles, with China, India and a touch of Southeast Asia joining Japan and Australia on the block.

Even so, the region still makes barely a ripple in the secondaries market globally. Alex Lee, a partner at Axiom Asia, estimates it is no more than 5-10% of worldwide deal flow.

According to Cogent Partners, global secondaries volume dropped off in the first half of 2013, with approximately $7 billion transacted – the lowest level in four years. In both 2011 and 2012, the full-year total came to $25 billion. Meanwhile, prices were rising. The average first round high bid for all funds was 84% of NAV, an increase of four percentage points on the second half of 2012.

“With NAVs rising and secondary buyers actively seeking to deploy more than $35 billion of dry powder, current market conditions have been nearly ideal for potential sellers,” the Cogent report concluded. “The question therefore remains how long will this seller-favorable window remain open?”

The answer rests on two factors: public markets and secondary fund dry powder.

First, the upswing in public markets – after treading water for much of 2012, the Dow Jones Industrial Average Index is up more than 16% year-to-date – was a disincentive for many prospective sellers. Having seen better distributions from portfolio GPs in the last 6-12 months and hopeful that NAVs would improve still further, they decided to bide their time.

“It created a situation where people felt far less pressure to do something,” says Philip Tsai, a managing director at UBS. “With the lag in reporting as well, people decided to wait one more quarter and see if GPs write up their portfolios even further.”

Cogent found that the drop in deal volume is due to reduced activity on the part of public pension funds and financial institutions specifically, groups that can typically be relied upon to execute a few transactions of $1 billion or more. These two categories of investor accounted for approximately 25% of sellers in the first half of 2013, down from nearly 50% in the previous six-month period.

According to Coller’s Mizuno, financial institutions have lost their urge to sell because most have now been through a couple of secondary transactions. While still carrying significant PE positions, they now know how quickly they can offload them when required.

Adam Howarth, a managing director with Partners Group, adds that financial institutions are delaying on sales because the regulations

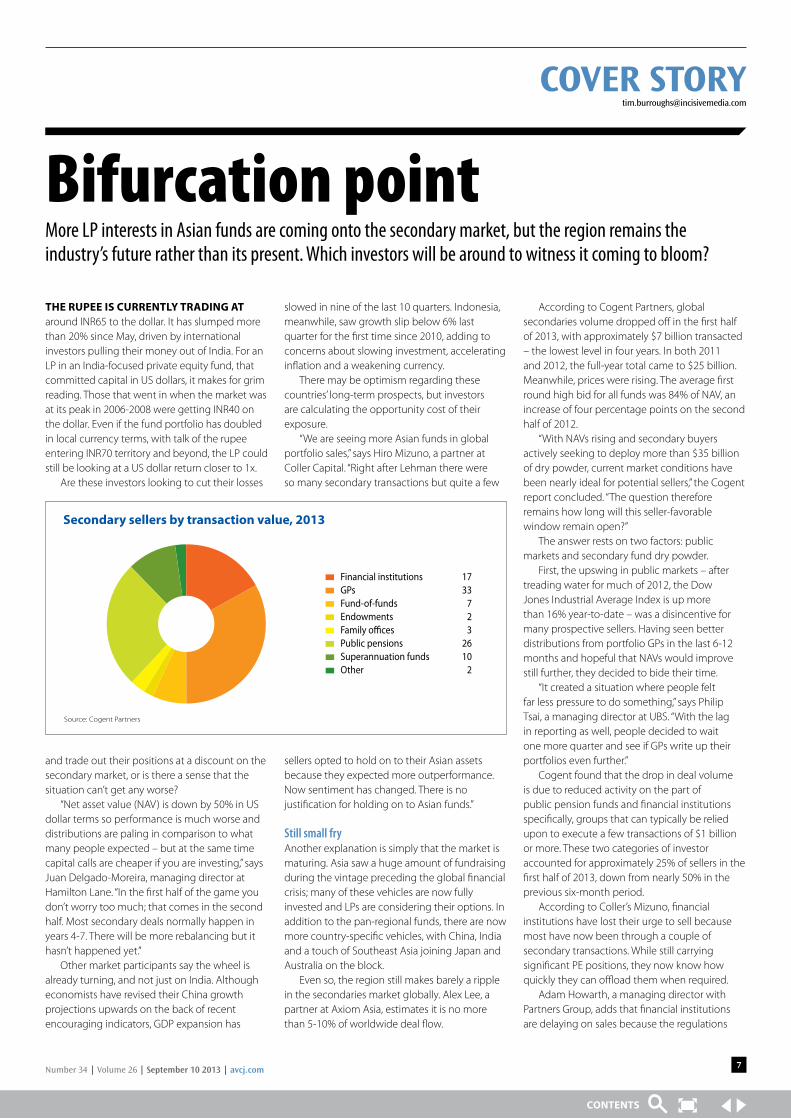

Bifurcation pointMore LP interests in Asian funds are coming onto the secondary market, but the region remains the industry’s future rather than its present. Which investors will be around to witness it coming to bloom?

Financial institutions 17GPs 33Fund-of-funds 7Endowments 2Family o�ces 3Public pensions 26Superannuation funds 10Other 2

Secondary sellers by transaction value, 2013

Source: Cogent Partners

KV

Asi

A C

Api

tAl

Fun

d i

�ailand

Singapore

Malaysia

Cambodia

Vietnam

Laos

Philippines

Indonesia

Brunei

Myanmar

us$262,988,000To make significant equity investments in quality mid-sized companies in Southeast AsiaJuly 2013

The undersigned acted as exclusive global fundraising adviser

The following appears as a matter of record only

Number 34 | Volume 26 | September 10 2013 | avcj.com 9

requiring them to divest – Basel III and the Volcker Rule, which impose stricter capitalization levels and limit balance sheet exposure to alternative assets, respectively – have yet to be put into a final timeline.

However, the general consensus is that activity has picked up in the last 2-3 months. Tsai of UBS is predicting full-year secondary deal volume to reach $16-18 billion, while Cogent thinks $20 billion is within reach. “Investors don’t necessarily want to push their luck – they’ve had a good run and may want to take chips off the table for interests they deem non-core, taking advantage of relatively strong pricing,” says Tsai.

Dry powder debateThe second factor, dry powder held by secondary investors, is more complicated and asks questions of managers’ differing approaches to the market.

Since the beginning of 2013, HarbourVest Partners, Adams Street Partners, StepStone, LGT Capital Partners and Deutsche Bank have all closed secondary vehicles on or above target. Last week Hamilton Lane joined the club. Of the big beasts, Coller and Axa Private Equity raised funds of $5.5 billion and $8 billion, respectively, last year, while Lexington Partners will reportedly return to market this year, seeking $8 billion.

UBS put the amount of dry powder in the secondaries market at nearly $42 billion at the start of 2013; Cogent’s projection is $35 billion. These estimates only include dedicated secondary buyers, so there could be more capital earmarked for the space from opportunistic investors with generalist funds.

Dominik Woessner, a director with Cogent, notes that secondary demand exceeded supply during the first half of the year, which contributed to the increase in transaction pricing. However, he claims not to be unduly worried by the current capital overhang. Even if dry powder levels reach $40 billion this year, a transaction volume of $20 billion would be sufficient to maintain a capital overhang of 2x, which has been fairly common over the past few years.

Coller’s Mizuno is even more effusive, declaring that 2012-2013 will be a golden vintage for secondaries because the funds raised ahead of the global financial crisis – when more than one third of the PE funds ever raised globally drew capital – are coming to market. “This is my third fund with Coller,” he says. “After we raised the first two funds, I asked who we should be approaching. Now it’s obvious; all the banks have a lot of private equity on their balance sheets.”

Fortune has not favored all industry participants, though. According to market sources, a deal is already in place that will see StepStone acquire Greenpark Capital in some way, shape or form, after the latter struggled to

meet its fundraising target. The future of Paul Capital is also said to be uncertain.

This may be evidence of an industry becoming increasingly bifurcated, with large players at one end of the spectrum who feature in all the auctions and smaller, more specialized practitioners at the other. It is also increasingly competitive. The likes of HarbourVest, Adams Street, Hamilton Lane, Partners Group and LGT offer combinations of primary fund-of-funds, co-investment and secondaries as they seek to meet the needs of a more sophisticated LP base.

In a number of cases, LPs have the option of cutting out the third-party manager entirely as intermediaries approach them with secondary opportunities – although their ability to respond is a function of internal resources.

“The portion of managers in the secondary market by dollars who are also primary managers

is increasing,” says Hamilton Lane’s Delgado-Moreira. “If you go back to the 2008-2009 vintage, that is when a lot of the fund-of-funds starting raising secondary vehicles of $1 billion or more.”

A primary business represents a competitive advantage: a manager has access to more data, enabling him to respond quicker to opportunities; and GPs may prefer to deal with an investor that could come in on their next fundraise.

Partners Group claims that its existing GP knowledge and relationships in Asia are already delivering secondary positions at attractive prices. The firm monitors 30 funds in Asia every quarter and, based on its analysis of the underlying assets, bought an LP interest in one of these vehicles. “Subsequently we saw the same fund in a portfolio come to market through an advisor and we were told it cleared at a premium to where we purchased it,” says Howarth.

The impact of this information advantage is contested by secondary specialists that have built their businesses without a primaries arm, but it potentially offers an edge in a market some say is badly in need of differentiation. As one industry source puts it, secondaries have become so well established and funds so large that it is difficult to replicate the returns seen 10 years ago.

In this context, a smaller practitioner with access to proprietary deal flow might be able to generate the returns investors are looking for. But how far is a firm willing to go in order to get it?

The theory posited by several market watchers is that Greenpark and Paul are victims of a general perception that, for all the benefits secondaries bring in terms of eliminating blind pool risk and ameliorating the J-curve effect, it is difficult to outperform the median and mean. And in trying to bridge this expectations gap, they shifted strategy.

“People have tried to stretch themselves to create an edge, and then got caught a little bit,” says UBS’ Tsai.

For Greenpark, this edge included an emerging markets angle. The firm teamed up with International Finance Corporation (IFC) to create a $500 million fund that would give it access to IFC’s 180 portfolio GPs, positioning it to get the first call whenever an LP was looking to exit. Greenpark said it expected to see in excess of $3 billion in emerging markets secondaries

in 2012; and because the fund sizes tend to be smaller there would be less intermediation and less competition for deals.

AVCJ understands that the agreement between IFC and Greenpark has lapsed.

Niche opportunitiesThere is still room for niche approaches in the secondaries market - as Axiom’s Lee observes, “you don’t have to be a $5 billion fund to be competitive” - but it is difficult to find space beyond the reach of intermediaries and in the current fundraising environment LPs are unforgiving. Furthermore, the industry appears to be in the midst of a broader consolidation. The Blackstone Group’s recent acquisition of Credit Suisse Strategic Partners suggests there are willing buyers among PE firms with aspirations to become multi-strategy asset managers.

As for Asia’s prospects, it may be case of soon, but not quite yet. Although assets are coming to market, and there is evidence to suggest more will follow, it is a trickle not a torrent.

“We are working on a handful of emerging markets deals right now,” says Jason Sambanju, managing director at Paul Capital. “It’s not just banks that have private equity side pockets; plenty of hedge funds and corporations have them too. If you look at the behavior of Asian corporates in recent years, a lot of them are starting PE-like businesses.”

coVeR [email protected]

“After we raised the first two funds, I asked who we should be approaching. Now it’s obvious; all the banks have a lot of private equity on their balance sheets” – Hiro Mizuno

avcj.com | September 10 2013 | Volume 26 | Number 3410

the battle betWeen nkosana makate and his former employers at South African mobile giant Vodacom is a modern tale of David and Goliath. Known as the “Please Call Me” case, the dispute involves a cell phone service – which Makate claims to have invented – that allows pre-pay users who have run out of credit to send a free text message to a friend requesting a call back.

Makate says came up with the idea back in 2000 while working for Vodacom and was promised a share of the profits. Not a cent has been paid. Vodacom, meanwhile, has made millions from the idea. Normally this case – and many others like it – would struggle to see the light of day, but thanks to litigation financiers who were will to stump up the capital needed, David is able to take on Goliath.

In this instance the investor was Commercial Intelligence (CI) Funds Group, currently South Africa’s biggest litigation financier, which put up the money in return for a share of the eventual winnings. An outcome is expected this month.

Eye on AsiaCI has been in the business for six years, offering litigation financing through private equity-style funds raised from third-party investors. The firm sees increasing opportunities coming out of Asia. Of its latest vehicle, which has a target of $150 million, nearly 65% will be committed to the region.

“Litigation financing has moved on a lot over the last 10 years,” says Michael Shone, a managing partner at CI.”The only place it hasn’t moved on is in emerging markets.”

CI, which also commits around 20% of its capital to distressed debt, is not the only litigation financier interested in Asia. Australia is already home to a handful of industry participants who have been tapping the domestic market, while Hong Kong and Singapore have also attracted investors, including CI, seeking opportunities in the international arbitration space.

So what exactly is drawing litigation funders to Asia and how do the promised returns compare to conventional private equity?

The idea that a law firm could fund clients’ claims from its own balance sheet in return for a percentage of the proceeds on a contingency fee basis is well established, especially in the US.

However, the practice of bringing in third-party investors to put up the capital is still very much in its infancy.

Australia has widely been credited as the birthplace of litigation financing since the industry was legitimized in 1995. The first litigation financier to set up the in country was IMF Group, which listed on the Australian Securities Exchange in 2001. The Sydney-based firm – still the domestic market leader – focuses on funding litigation claims with a minimum value of A$5 million ($4.6 million) and arbitration claims with a minimum value of A$10 million.

“A cause of action is like any other piece of property,” says Hugh McLernon, managing

director at IMF in Perth. “It’s yours and you are entitled to do what you want with it, whether you sell it, assign it or burn it. That is basically the situation we have in Australia.”

In Australia, the US and the UK, litigation financing has flourished as a result of the liberalization of the rules surrounded third-party financing. In UK and Australia at least, the practice was once restricted by an English common-law prohibition against “champerty” and “maintenance,” which prevents outside investors from meddling in lawsuits or taking cuts from judgments.

Out of bounds?While the restriction has since been removed in these two countries – in 1967 for the UK and 1995 for Australia – similar common law prohibitions remain in many Asian jurisdictions rendering most litigation cases out of bounds for potential investors.

However, there are two areas where exceptions can be made: insolvency cases and international arbitration. The latter is particularly attractive because of the large sums involved

and also the fact that litigation financiers can concentrate their energies on Asia’s two major jurisdictions for international arbitration: Singapore and Hong Kong.

“The reason the rules around international arbitration are somewhat more relaxed is because it tends to be disengaged from local laws when it comes to funding,” says Denis Brock, a dispute resolutions partner at King & Wood Mallesons in Hong Kong. “There is no clear authority that says you can have funding in international arbitration.”

Insolvent companies, meanwhile, are by definition in need of funding, so it is no surprise that in countries like the UK the assignment of

a cause of action to a third party would not run afoul of prohibitions against champerty and maintenance.

In Hong Kong it has been less clear-cut, although two recent cases have shown that the jurisdiction is becoming more open to litigation funding in insolvency cases.

The first is that of Akai Holdings vs. Ernst & Young in 2009. Akai was a Hong Kong-listed electronics manufacturer which had gone into liquidation in 2004. Liquidators launched an action in the Hong Kong High Court against the Ernst & Young, claiming damages for alleged negligence and breach of duty in auditing Akai’s accounts from 1997 to 1999. They argued this negligence led to the company’s eventual collapse.

The case was significant in that the liquidators are reported to have obtained court approval for the litigation funding from a third party investor – however the identity of the fund remained anonymous.

“Akai is what caught people’s attention,” says CI’s shone. “You had a big liquidation and a horrendously expensive case against a Big Four

The justice leagueLitigation financiers are increasingly looking for opportunities in Asia, many making their investments out of private equity-style funds. But do they bring the same returns?

“A cause of action is like any other piece of property, it’s yours and you are entitled to do what you want with it whether you sell it, assign it or burn it. That is basically the situation we have in Australia” – Hugh McLernon

accounting firm. That’s when people realized there were big opportunities in Asia.”

The second, and perhaps more landmark ruling in terms of opening up the Hong Kong market, was that of the insolvency of Cyberworks Audio Video Technology. Briscoe & Wong, one of the firm’s liquidators, sought sanction to enter into an agreement with litigation funder Remedy Asia, so that it could pursue litigation against various parties in a bid to recover losses.

Cut of the profitsWhen successful in a case, litigation funders can take anything between 30-60% of a client’s financial reward. With potential claims amounting to hundreds of millions, return cans be very lucrative.

“The basic figure we are coming out with is that for every dollar we invest, we get three dollars back,” says IMF’s Mclernon. “That is over an average of 2.2 years for each case – so it is a tick under a 100% gross return, and from what we can tell that is scalable.”

While there is no data readily available on returns for litigation fund investors, industry participants are expecting similarly high returns as IMF’s McLernon. London-listed litigation financier Juridica, for example – which has $200 million in assets under management – recently

reported a total IRR of 81.97% across all the recoveries in 2012.

But can the same returns be expected in Asia? CI’s Shone thinks they can, although he cautions

that the nature of the risk requires a sophisticated investor. There is no guarantee that every case will be won – and when one is lost, the fund investor bears the cost.

“It is relatively high-risk strategy where everything depends on your case selection, your management and cost control,” he says. “There also a lot of factors beyond your control.” CI counts institutional investors and large family office among its LPs.

Given the risks involved, legal experience within team is essential; indeed, many litigation funders come from a legal background rather

than an investment one. IMF’s McLernon argues that a strong team can ameliorate the risk. “That is our arbitrage,” he says. “It is our view of the risk compared to other people’s view of the risk. If we

settle eight out of 10 cases, and win half of those that go to court – that is nine out of 10 cases won – how many other business have that kind of certainty?”

While there are few Asia-focused litigation funds to speak of, anecdotal evidence suggests would-be LPs are interested. Teras Group, a litigation financier based in

Singapore, focuses on funding international cases involving Asian claimants that are litigated in US or UK courts. While the firm is currently privately financed it has claims to have received numerous approaches from prospective investors asking about a third-party vehicle.

“There is more interest in the region and more activity and that is a trend that will only continue,” says Steven Goodman, Teras’ founder. “A lot of people like the space and they like the proposition and the experience we have here. They often ask if we will take outside investment but we are just not ready yet.”

Sponsored by

AVCJ Private Equity & Venture Capital Awards – AsiaNominations open until 30 September. Act now!

Held in conjunction with the AVCJ Forum and now in their 13th year, the AVCJ Awards have become the highest distinction that

can be achieved in private equity in Asia, and a showcase for first-class innovation, ingenuity and performance.

Tell us who you think deserves recognition.Submissions for nominations are open now until 30 September, 2013.

Visit www.avcjforum.com/nominations and fill out the form.

For any enquiries, please e-mail [email protected]

AssociAte your brAnd with excellence: If you would like to be associated with recognising and rewarding excellence within the Asian private equity industry, award sponsorship opportunities are available.

For more information, please contact Samuel Lau on +852 3411 4963 or [email protected]

•FirmoftheYear•PrivateEquityProfessionaloftheYear•VentureCapitalProfessionaloftheYear•PrivateEquityDealoftheYear•VentureCapitalDealoftheYear

•PrivateEquityExitoftheYear•FundraisingoftheYear•OperationalValueAddAward•AVCJSpecialAchievementAward

The Awards categories

Recognising excellence in AsiAn PRivAte equity

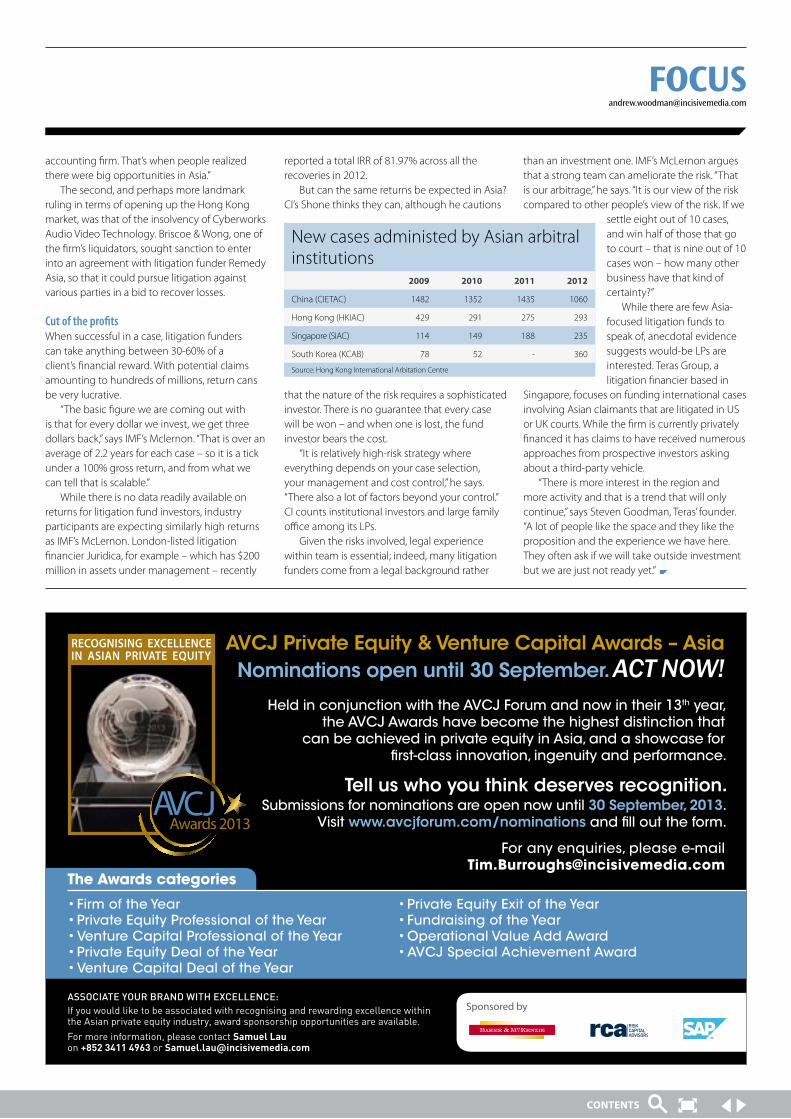

New cases administed by Asian arbitral institutions

2009 2010 2011 2012

China (CIETAC) 1482 1352 1435 1060

Hong Kong (HKIAC) 429 291 275 293

Singapore (SIAC) 114 149 188 235

South Korea (KCAB) 78 52 - 360

Source: Hong Kong International Arbitation Centre

avcjforum.com

12-14 November 2013 Four Seasons Hotel, Hong Kong

Book your place

by 27 September and save us$300

26th AnnuAl

Registration: pauline chen T: +852 3411 4936 E: [email protected]

Contact us

Senior LP speakers already confirmed include:

Soren Thinggaard HansenHead of Private EquityINDUSTRIENS PENSION

Steve ByromHead of Private EquityFUTURE FUND

Suyi KimManaging Director, Head of Private Equity Asia, CANADA PENSION PlAN INvESTMENT BOARD

Pak-Seng LaiManaging Director & Head of AsiaAUDA

D. Brooks ZugSenior Managing Director & FounderHARBOURvEST PARTNERS, llC

Risto AutioDirector, Private Equity vARMA MUTUAl PENSION INSURANCE COMPANy

Volkert DoeksenChairman & Chief Executive OfficerAlPINvEST PARTNERS

Juan Delgado-MoreiraManaging Director and Head of InternationalHAMIlTON lANE

Thomas KubrExecutive ChairmanCAPITAl DyNAMICS

Nicole Musiccovice PresidentONTARIO TEACHERS’ PENSION PlAN

Richard HallManaging Director, Private Markets, TEACHER RETIREMENT SySTEM OF TExAS

Thomas Kleinvice PresidentDEG

Fritz BeckerCEO & Managing DirectorHARAlD QUANDT HOlDING GMBH

Jeremy CollerExecutive Chairman & CIOCOllER CAPITAl

Jay ParkManaging DirectorBlACKROCK PRIvATE EQUITy PARTNERS

Jim Pittmanvice President, Private EquityPSP INvESTMENTS

David NieuwendijkSenior Investment Officer Private EquityFMO

Sherry LinManaging PartnerMOUSSE PARTNERS

save us$300 before 27 september.Register now at avcjforum.com

and many more…

avcjforum.com

12-14 November 2013 Four Seasons Hotel, Hong Kong

Book your place

by 27 September and save us$300

26th AnnuAl

Registration: pauline chen T: +852 3411 4936 E: [email protected]

Contact us

Senior LP speakers already confirmed include:

Soren Thinggaard HansenHead of Private EquityINDUSTRIENS PENSION

Steve ByromHead of Private EquityFUTURE FUND

Suyi KimManaging Director, Head of Private Equity Asia, CANADA PENSION PlAN INvESTMENT BOARD

Pak-Seng LaiManaging Director & Head of AsiaAUDA

D. Brooks ZugSenior Managing Director & FounderHARBOURvEST PARTNERS, llC

Risto AutioDirector, Private Equity vARMA MUTUAl PENSION INSURANCE COMPANy

Volkert DoeksenChairman & Chief Executive OfficerAlPINvEST PARTNERS

Juan Delgado-MoreiraManaging Director and Head of InternationalHAMIlTON lANE

Thomas KubrExecutive ChairmanCAPITAl DyNAMICS

Nicole Musiccovice PresidentONTARIO TEACHERS’ PENSION PlAN

Richard HallManaging Director, Private Markets, TEACHER RETIREMENT SySTEM OF TExAS

Thomas Kleinvice PresidentDEG

Fritz BeckerCEO & Managing DirectorHARAlD QUANDT HOlDING GMBH

Jeremy CollerExecutive Chairman & CIOCOllER CAPITAl

Jay ParkManaging DirectorBlACKROCK PRIvATE EQUITy PARTNERS

Jim Pittmanvice President, Private EquityPSP INvESTMENTS

David NieuwendijkSenior Investment Officer Private EquityFMO

Sherry LinManaging PartnerMOUSSE PARTNERS

save us$300 before 27 september.Register now at avcjforum.com

and many more…

avcjforum.com

Register now at avcjforum.com

Sponsorship: Darryl Mag T: +852 3411 4919 E: [email protected]

Contact us

Lead sponsors Asia series sponsor

Co-sponsors

SOLICITORS AND INTERNATIONAL LAWYERS

Legal sponsors Knowledge partner VC summit legal sponsorVC summit sponsors

PE leaders’ summit sponsors Awards sponsors

Exhibitors Official broadcast partner Communications partner

avcj.com | September 10 2013 | Volume 26 | Number 3414

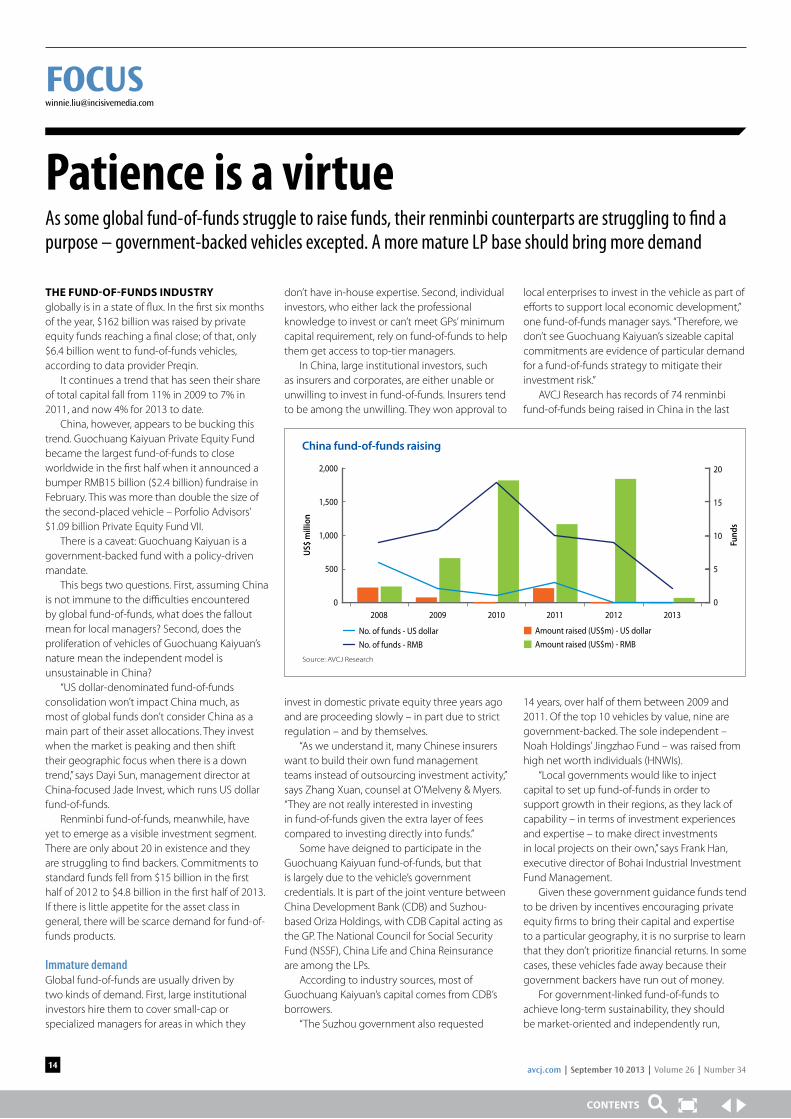

the fund-of-funds industry globally is in a state of flux. In the first six months of the year, $162 billion was raised by private equity funds reaching a final close; of that, only $6.4 billion went to fund-of-funds vehicles, according to data provider Preqin.

It continues a trend that has seen their share of total capital fall from 11% in 2009 to 7% in 2011, and now 4% for 2013 to date.

China, however, appears to be bucking this trend. Guochuang Kaiyuan Private Equity Fund became the largest fund-of-funds to close worldwide in the first half when it announced a bumper RMB15 billion ($2.4 billion) fundraise in February. This was more than double the size of the second-placed vehicle – Porfolio Advisors’ $1.09 billion Private Equity Fund VII.

There is a caveat: Guochuang Kaiyuan is a government-backed fund with a policy-driven mandate.

This begs two questions. First, assuming China is not immune to the difficulties encountered by global fund-of-funds, what does the fallout mean for local managers? Second, does the proliferation of vehicles of Guochuang Kaiyuan’s nature mean the independent model is unsustainable in China?

“US dollar-denominated fund-of-funds consolidation won’t impact China much, as most of global funds don’t consider China as a main part of their asset allocations. They invest when the market is peaking and then shift their geographic focus when there is a down trend,” says Dayi Sun, management director at China-focused Jade Invest, which runs US dollar fund-of-funds.

Renminbi fund-of-funds, meanwhile, have yet to emerge as a visible investment segment. There are only about 20 in existence and they are struggling to find backers. Commitments to standard funds fell from $15 billion in the first half of 2012 to $4.8 billion in the first half of 2013. If there is little appetite for the asset class in general, there will be scarce demand for fund-of-funds products.

Immature demandGlobal fund-of-funds are usually driven by two kinds of demand. First, large institutional investors hire them to cover small-cap or specialized managers for areas in which they

don’t have in-house expertise. Second, individual investors, who either lack the professional knowledge to invest or can’t meet GPs’ minimum capital requirement, rely on fund-of-funds to help them get access to top-tier managers.

In China, large institutional investors, such as insurers and corporates, are either unable or unwilling to invest in fund-of-funds. Insurers tend to be among the unwilling. They won approval to

invest in domestic private equity three years ago and are proceeding slowly – in part due to strict regulation – and by themselves.

“As we understand it, many Chinese insurers want to build their own fund management teams instead of outsourcing investment activity,” says Zhang Xuan, counsel at O’Melveny & Myers. “They are not really interested in investing in fund-of-funds given the extra layer of fees compared to investing directly into funds.”

Some have deigned to participate in the Guochuang Kaiyuan fund-of-funds, but that is largely due to the vehicle’s government credentials. It is part of the joint venture between China Development Bank (CDB) and Suzhou-based Oriza Holdings, with CDB Capital acting as the GP. The National Council for Social Security Fund (NSSF), China Life and China Reinsurance are among the LPs.

According to industry sources, most of Guochuang Kaiyuan’s capital comes from CDB’s borrowers.

“The Suzhou government also requested

local enterprises to invest in the vehicle as part of efforts to support local economic development,” one fund-of-funds manager says. “Therefore, we don’t see Guochuang Kaiyuan’s sizeable capital commitments are evidence of particular demand for a fund-of-funds strategy to mitigate their investment risk.”

AVCJ Research has records of 74 renminbi fund-of-funds being raised in China in the last

14 years, over half of them between 2009 and 2011. Of the top 10 vehicles by value, nine are government-backed. The sole independent – Noah Holdings’ Jingzhao Fund – was raised from high net worth individuals (HNWIs).

“Local governments would like to inject capital to set up fund-of-funds in order to support growth in their regions, as they lack of capability – in terms of investment experiences and expertise – to make direct investments in local projects on their own,” says Frank Han, executive director of Bohai Industrial Investment Fund Management.

Given these government guidance funds tend to be driven by incentives encouraging private equity firms to bring their capital and expertise to a particular geography, it is no surprise to learn that they don’t prioritize financial returns. In some cases, these vehicles fade away because their government backers have run out of money.

For government-linked fund-of-funds to achieve long-term sustainability, they should be market-oriented and independently run,

Patience is a virtueAs some global fund-of-funds struggle to raise funds, their renminbi counterparts are struggling to find a purpose – government-backed vehicles excepted. A more mature LP base should bring more demand

China fund-of-funds raising

Source: AVCJ Research

2,000

1,500

1,000

500

0

20

15

10

5

0

US$

mill

ion

Fund

s

No. of funds - RMBNo. of funds - US dollar

2008 2009 2010 2011 2012 2013

Amount raised (US$m) - RMB Amount raised (US$m) - US dollar

says Chun Zeng, a partner at Gopher Asset Management, the private equity arm of New York-listed Noah Holdings.

Gopher Asset Management started a fund-of-funds business three years ago, leveraging parent company Noah’s HNWI network. This network was cultivated through the fi rm’s placement agent business, which distributes fi xed income products and private equity funds. It has assisted the likes of CDH Investments, Sequoia Capital and SAIF Partners in their fundraising eff orts.

With domestic private equity fi rms facing a period of painful consolidation due to the challenging fundraising environment, Gopher sees opportunities arising in the secondaries market. PE players that want to tap investors for new funds must return capital – a bridge too far for managers that invested with a view to an IPO exit but now fi nd the public markets closed.

In May, Gopher reached a fi rst close of RMB500 million on its debut secondaries fund.

The fi rm also plans to enter the US dollar fund space, following managers that made their names with renminbi vehicles and now want to target more sophisticated off shore investors. Several years down the line, these managers are also likely to start pursuing cross-border transactions.

“Later when local GPs are familiar with

overseas markets, we will allocate assets to invest in managers operating overseas,” Zeng adds. “We foresee enormous change for China’s PE industry, including fund managers focusing more on early-stage investments rather than pre-IPO deals, diff erent exit routes and increased specialization. We want to have the fl exibility to launch new products in line with these changes.”

Two’s companyPartnering with foreign fund-of-funds is another way for renminbi managers to get more exposure to global markets. In April, Swiss-based Capital Dynamics joined forces with China-focused Diligence Capital, agreeing to adopt its partner’s name when conducting activities relating to China, while Diligence Capital operates under the English brand name Capital Dynamics China.

“We have established a very tight cooperative arrangement and we defi nitely plan to off er our clients – whether Chinese or international – a fully integrated investment solution. It should be to the degree that people know there are two separate corporate entities, but with one product in the future,” Thomas Kubr, Capital Dynamics’ executive chairman, told AVCJ earlier this year.

Other industry players are concerned that such strategic partnerships won’t last long, citing a misalignment of interests. While Capital

Dynamics chose a local partner to access the Chinese market, Diligence Capital’s objective is to raise US dollar funds. What happens to this dual currency cooperation as the renminbi moves towards convertibility remains to be seen.

“In 2-3 years, the current model of US dollar funds will disappear. The renminbi will become an international currency – more transferrable, exchangeable and liquid – so there will be no need to have renminbi and US dollar vehicles running in a parallel,” says Bruno Raschle, executive chairman of Adveq Group.

This evolution is expected to coincide with a maturing of China’s LP base, which may ultimately provide succor to the renminbi fund-of-funds. For now, those that are able to outsource their investments don’t want to, but the institutional participants in PE should be very diff erent in several years compared to today.

Some LPs might adopt a passive approach because they don’t have the resources to engage with managers directly; others may simply appreciate the diversifi cation fund-of-funds bring to their investment exposure.

“For example, we expect Chinese insurers’ appetite for fund-of-funds to increase as they realize the advantages it brings in risk mitigation, and after they have tried to make investments themselves,” Jade Invest’s Sun says.

Wider reach to everyone in your organisation

avcj.com site licence allows everyone in your organisation to have instant access to in-depth analysis, real-time news and information on private equity in Asia and beyond. Sign up for an avcj.com site licence now and empower your team with critical information and data to soar above your competitors in Asian private equity.

How does it work?

We will arrange online access for your employees to avcj.com, either with individual passwords or by general access through IP address recognition.

How much does it cost

That depends on how much access you want, but we can customise cost-effective packages to all firms, regardless of size. For more information, contact Sally Yip at +(852) 3411 4921 or email [email protected].

avcj.com

ExprEssion of intErEst (“Eoi”)forEign partnEr sElEction for a nEw

sub-saharan privatE Equity fund

Please send Expression of Interest letters by October 28th deadline, 2013 by email to:[email protected],

Tel: +234-703-470-4697

today, sub-saharan africa represents the last and perhaps one of the world’s most attractive emerging market private equity frontier regions.

our client is the investment banking arm of one of sub-saharan africa’s largest, oldest and most prestigious diversified publicly traded financial service institutions. in 2012,it reported audited assets in excess of $20bn,earnings of approximately $500m+, and a return on average shareholders’ funds of 18.8%.

over the past decade (2003-2013), our client has operated a small-cap private equity and principal investing business but now intends to raise a separate, significant and sizeable new private equity fund (the “new africa fund”). the new africa fund will focus on larger investments in sub-saharan africa thereby capitalizing on the many attractive and diverse private equity opportunities in this high growth region.

Expressions of interest [“Eoi”] are now sought from highly successful and proven existing private Equity firms operating internationally (prior emerging market pE experience is essential) to partner with our client in the new africa fund. upon submission of an Eoi as a co-fund manager, your firm, if pre-qualified, will receive a formal request for proposal (“rfp”) due for submission by december 2nd, 2013. Final partner selection is expected to occur by March, 2014.

the international pE partner selected should expect to fully co-manage all aspects of the new africa fund with our client including: 1) providing a leadership role with our client in international fund raising and support on africa wide fund raising efforts, 2) developing the new africa fund’s investment strategy and sector/country focus, 3) the lp engagement process (preparing 3rd party presentation materials, road show, etc) and 4) negotiations and achieving financial closing(s) for the new africa fund.

your expression of interest letter must include the following to avoid disqualification:1. full registered name of your current fund2. Key person contact details (email, phone & physical address)3. total fund assets under Management [auM]4. name and address to where to send the formal rfp (contact name, fund name, e-mail and physical address only)5. your fund’s website address

only successfully selected responses to this Eoi will be notified by e-mail to your designated contact by not later than october 31st, 2013.

Summary Indicative Timetable:• Expression of Interest submission deadline: October

28th, 2013• Successful EOI responses notified, October 31st, 2013• RFP & Term sheet circulated Nov. 1st, 2013• Management presentation& one-on-one meetings,

november 14th & 15th, 2013• RFP submission deadline, Dec. 2nd, 2013

• Successful RFP submissions notified Dec. 10th, 2013• One-on-One pre-negotiations/Term Sheet review

dec. 12th – 15th, 2013• One-on-One negotiations commence January

20th, 2014• Conclude negotiations & partner selection

March 31st, 2014

Number 34 | Volume 26 | September 10 2013 | avcj.com 17

ping an insurance group has taken the fight to Alibaba Group once before. In 2010 it bought an 80% stake in online grocery retailer Yihaodian and helped build the business into one of China’s leading B2C e-commerce players, finding space in the corner of a market increasingly dominated by Alibaba’s Tmall and Jingdong’s JD.com. Ping An sold majority control to Wal-Mart last year.

SmartPay, the group’s most recent acquisition, sets the scene for a challenge to Alipay, Alibaba’s market-leading third-party payment platform. Offering clear synergies with Ping An’s core financial services business – it has bank and asset management interests as well as being China’s second-largest life insurer – SmartPay is unlikely to be exited as quickly as Yihaodian.

Indeed, the group is expected to make other investments in the space, as it aggressively pushes into electronic services. Ping An’s mobile integrated terminal (MITs) system already allows

insurance policies to be sold, underwritten and paid for in just one client meeting. More than RMB70 billion ($11.4 billion) in premiums have been processed through MITs since 2011.

“Payments is a huge opportunity, especially for merchants with their own sales force and transactions,” an industry source told AVCJ.

The SmartPay acquisition facilitated the exit of Lunar Capital and co-investors RRE Ventures and Icon, based in the US and Sweden, respectively. The company was created in 2003 as a spin-out from

Linktone, a wireless value-added service provider co-founded by principals at Lunar Capital that went public on NASDAQ in 2004. It was one of a handful of tech-related assets in the China-focused private equity firm’s debut fund.

RRE Ventures’ early involvement derives from its financial services experience. The US-based firm’s managing partner, Jim Robinson, is a well known investor in the payments field while his

father and co-founder, who is also called Jim Robinson, was previously chairman and CEO of American Express.

A sale to a financial institution or a merchant – such as an e-commerce platform – was always likely for SmartPay. A number of independent third-party payment platforms in China have struggled recently with the rise of Alipay and domestic banks aggressively entering the market.

SmartPay is understood to process nearly RMB10 billion per year and is reportedly profitable, although it remains a fraction of Alipay’s size because it focuses on payments transacted via mobile phones. Alipay is more broadly exposed to online payment, receiving transaction fees from Tmall and Alibaba.com.

As early movers in the payment space, SmartPay and Alipay are the only industry participants that can boast a full set of licenses, enabling them to run payment services, operate online, and perform a custodian and processing role. This is a significant issue, now that third-party payment is subject to closer regulatory scrutiny and approvals are not easily obtained.

australian politicians have long debated ways to enlarge the country’s tax base as they prepare for the economic ramifications of a spiraling dependency ratio. By 2050 there will be just 2.7 people of working age for each person aged 65 and over, compared to five at present.

While not a solution on its own, getting mothers back to work earlier after they have children certainly helps. This explains why childcare featured prominently in the recent federal election, with Prime Minister elect Tony Abbot promising to honor existing programs and also introduce paid maternity leave.

The combination of demographics and strong political support played into Navis Capital Partners’ investment thesis when it agreed to pay A$120 million ($110 million) for childcare services provider Guardian Early Learning Group. The seller, Wolseley Private Equity, has secured a 2.3x money multiple and a 40% IRR on an investment made two-and-a-half years ago.

“We have been looking at education in all its forms for quite some time. It is driven by demographics that are predictable and

understandable,” said Philip Latham, an Australia-based partner with Navis. “In Australia there is far more demand for childcare services than supply right now. Occupancy levels are in the high 80s and for this business they are in the mid 90s.”

Guardian is the second-largest operator of private childcare services in Australia, providing education and care for more than 5,700 children daily from a network of 69 centers. Navis wants the company to double in size during its ownership period through greenfield investments and acquiring existing providers. The market leader is domestically-listed G8 Education, which has more than 160 centers.

The average number of hours an Australian child spends in care services per week is 23.8, up from 23 in 2004. For long day care, the average has jumped to 27.5 hours from 26.6. Nearly half of all 3-5 year-olds – Guardian’s primary target market – were using childcare services as of 2011.

Wolseley helped the company scale up

in what remains a highly fragmented market, particularly among operators with 10 centers or less. In the last two-and-a-half years Guardian has acquired 21 facilities and increased its employee headcount from 720 to 1,700, while compound

annual revenue growth increased 46% and profit tripled.

The PE firm chose to exit beccause it had invested as much as it could to Guardian and more was required to take it to the next level. Company management is participating in the Navis deal and will hold approximately 10% of the equity.

As a pan-regional PE firm, all of Navis’ investments in Australia have included an element of cross-border expansion. Guardian has yet to consider this strategy but Latham said it is likely to be studied at some point. He sees potential for taking the corporate business into places like Singapore and Hong Kong, but warns that local regulatory conditions often present challenges.

Deal oF the [email protected]

SmartPay joins Ping An’s e-payment push

Navis in Australia demographics play

Mobile: Pay as you go

ExprEssion of intErEst (“Eoi”)forEign partnEr sElEction for a nEw

sub-saharan privatE Equity fund

Please send Expression of Interest letters by October 28th deadline, 2013 by email to:[email protected],

Tel: +234-703-470-4697

today, sub-saharan africa represents the last and perhaps one of the world’s most attractive emerging market private equity frontier regions.

our client is the investment banking arm of one of sub-saharan africa’s largest, oldest and most prestigious diversified publicly traded financial service institutions. in 2012,it reported audited assets in excess of $20bn,earnings of approximately $500m+, and a return on average shareholders’ funds of 18.8%.

over the past decade (2003-2013), our client has operated a small-cap private equity and principal investing business but now intends to raise a separate, significant and sizeable new private equity fund (the “new africa fund”). the new africa fund will focus on larger investments in sub-saharan africa thereby capitalizing on the many attractive and diverse private equity opportunities in this high growth region.

Expressions of interest [“Eoi”] are now sought from highly successful and proven existing private Equity firms operating internationally (prior emerging market pE experience is essential) to partner with our client in the new africa fund. upon submission of an Eoi as a co-fund manager, your firm, if pre-qualified, will receive a formal request for proposal (“rfp”) due for submission by december 2nd, 2013. Final partner selection is expected to occur by March, 2014.

the international pE partner selected should expect to fully co-manage all aspects of the new africa fund with our client including: 1) providing a leadership role with our client in international fund raising and support on africa wide fund raising efforts, 2) developing the new africa fund’s investment strategy and sector/country focus, 3) the lp engagement process (preparing 3rd party presentation materials, road show, etc) and 4) negotiations and achieving financial closing(s) for the new africa fund.

your expression of interest letter must include the following to avoid disqualification:1. full registered name of your current fund2. Key person contact details (email, phone & physical address)3. total fund assets under Management [auM]4. name and address to where to send the formal rfp (contact name, fund name, e-mail and physical address only)5. your fund’s website address

only successfully selected responses to this Eoi will be notified by e-mail to your designated contact by not later than october 31st, 2013.

Summary Indicative Timetable:• Expression of Interest submission deadline: October

28th, 2013• Successful EOI responses notified, October 31st, 2013• RFP & Term sheet circulated Nov. 1st, 2013• Management presentation& one-on-one meetings,

november 14th & 15th, 2013• RFP submission deadline, Dec. 2nd, 2013

• Successful RFP submissions notified Dec. 10th, 2013• One-on-One pre-negotiations/Term Sheet review

dec. 12th – 15th, 2013• One-on-One negotiations commence January

20th, 2014• Conclude negotiations & partner selection

March 31st, 2014

Childcare: Growth market

avcj.com | September 10 2013 | Volume 26 | Number 3418

InDustRy Q&a | INDIKA [email protected]

Q: In 2009 Leopard Capital and Calamander Capital failed to raise a Sri Lanka fund. Is there more LP interest now?

A: I think there is good level of LP interest. LPs are experiencing low returns in South Asia regional funds, realizing there are vast differences between each country in the region, and so they are now looking for direct country exposure. Also, many investors with large Asia allocations are finding it tough to increase investments in China or India because these markets are slowing. So they are looking at smaller growth markets like Sri Lanka. We have a lot of interest from global funds-of-funds as well as from a couple of development finance institutions (DFIs). Many of them are looking at the country for the first time.

Q: How does Sri Lanka compare with other emerging markets?

A: Sri Lanka offers good opportunities but due to the small size of the economy these are not $100 million deals – they are in the $5-10 million range. I think it is important to distinguish Sri Lanka from India. Sri Lanka has never achieved its fair share of attention or investment due to the India factor – it is considered an extension of India or part of a South Asian regional allocation, which India ends up absorbing disproportionately large chunks of. Investors should look at South Asian countries individually because they have different growth drivers and business environments. The Sri Lankan economy is not linked to the domestic market, but it includes exports and services such as tourism. Also, compared to

other emerging markets, PE is an excellent way to get broader equity market exposure here. The small size of the stock market means that transactions of around $1 million often have to be negotiated off market – like a PE deal. So Sri Lanka is a good for secondary PIPE deals.

Q: What is the outlook for the Sri Lankan economy?

A: Last year growth slowed to 6.4% from two years of 8%. This year I think we will hit 6-7%. In terms of contributors to GDP growth, for the next few years, the bulk will come from infrastructure development and the reconstruction of former war zones. The construction sector will contribute significantly, as will transport and industrial ventures. In addition, steady growth in export and tourism is expected.

Q: Why have you chosen to focus on small and medium-sized enterprises (SMEs) for Jupiter Capital’s debut fund?

A: That’s where the growth is going to come from. During the last 30 years the level of entrepreneurship has been low so the larger companies have become too big and too diversified. As a result, some have lost their competitiveness or core expertise. SMEs are more flexible and able to achieve higher growth, plus exiting them is not as challenging. The domestic market is not big enough to give high returns so we’re looking at companies whose growth is linked to exports or overseas expansion. We will also focus on companies which are targeting local market, but will be very selective. The typical deal size

will be $2-8 million and we plan to do about 15 deals.

Q: But according to the Sri Lanka Chamber of Small and Medium Industries, 25% of local SMEs have gone bankrupt over the last 2-3 years…

A: The debt level of Sri Lankan companies is much higher than elsewhere in the region. When a company is growing it needs quick money and banks have been very aggressive in their lending practices. As a result, companies are over-leveraged and all their cash is used to pay off debts. We expect defaults to grow in the coming quarters. A lot of mid-sized companies lack capital for expansion and modernization, so they open to equity deals but they don’t have many funding options. There

are some equity investors, but they are linked to other business groups. Companies are not comfortable with the perceived conflicts of interest.

Q: What is the competition for deals like?

A: In smaller markets like Sri Lanka developing proprietary deal flow is a challenge. There are no local independent PE managers, but there are many investment firms linked to financial institutions, diversified business groups and family offices. There were two foreign PE firms here, LR Global and Aureos Capital [now part of The Abraaj Group], but they have closed down. Other than those, Actis and DFIs such as International Finance Corporation (IFC), German Investment Corporation (DEG) and the Netherlands’ FMO are active here.

Q: What kind of returns can investors expect?

A: We are targeting a minimum 100% return in three years, or about 23% IRR. We’ve increased the target size of the fund from $50 million to $100 million – with the option of closing at $75 million – after investors said $50 million was too small for them to consider. We’ve also broadened the fund strategy to include secondary and PIPE deals.

Q: What is the exit strategy?A: We have seen both public

market exits as well as trade sales. I personally prefer IPOs because it helps to develop the capital markets, but usually trade sales give much higher returns as large companies buy into emerging companies or SMEs to find growth.

Overlooked, underinvested Indika Hettiarachchi, director at Sri Lanka-based Jupiter Capital Partners, outlines why India’s economic troubles could help other South Asian countries get a bigger share of investment in the region

“Sri Lanka has never achieved its fair share of attention or investment due to the India factor”

Number 34 | Volume 26 | September 10 2013 | avcj.com 19

PRIvATE EQUITY DATA FILE | aVcJ [email protected]

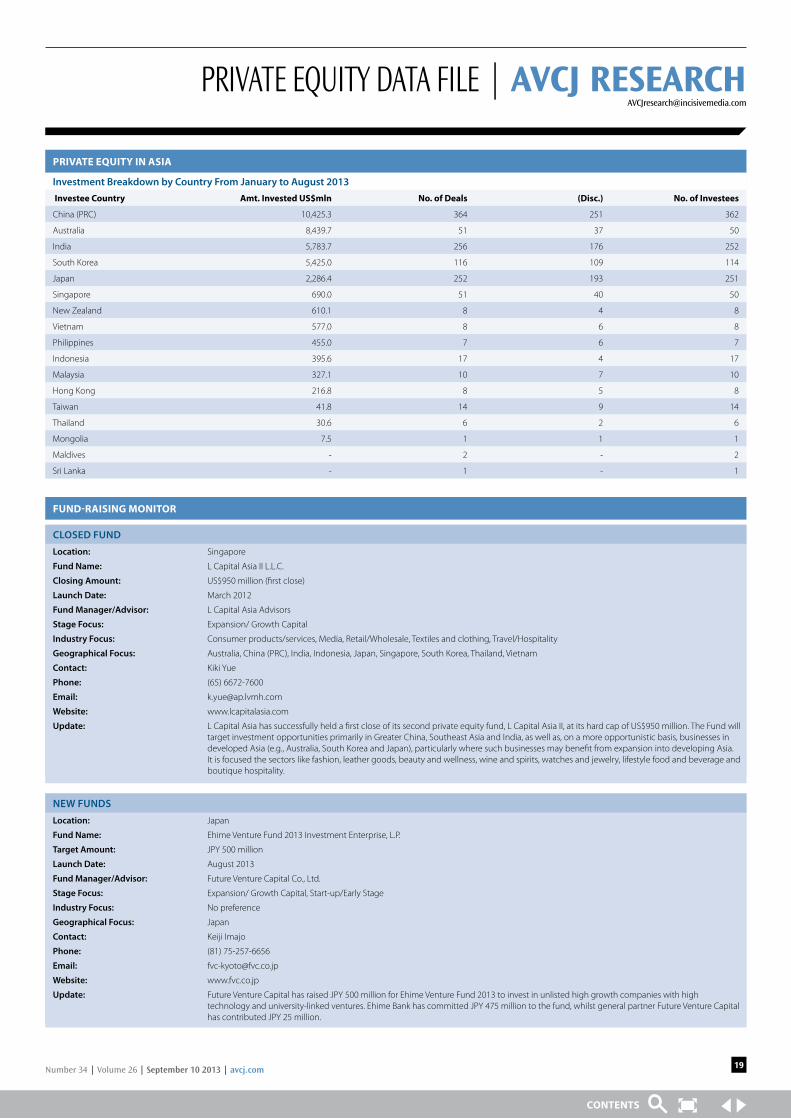

private equity in asia

Investment Breakdown by Country From January to August 2013 investee country amt. invested us$mln no. of deals (disc.) no. of investees

China (PRC) 10,425.3 364 251 362

Australia 8,439.7 51 37 50

India 5,783.7 256 176 252

South Korea 5,425.0 116 109 114

Japan 2,286.4 252 193 251

Singapore 690.0 51 40 50

New Zealand 610.1 8 4 8

Vietnam 577.0 8 6 8

Philippines 455.0 7 6 7

Indonesia 395.6 17 4 17

Malaysia 327.1 10 7 10

Hong Kong 216.8 8 5 8

Taiwan 41.8 14 9 14

Thailand 30.6 6 2 6

Mongolia 7.5 1 1 1

Maldives - 2 - 2

Sri Lanka - 1 - 1

CLoSEd Fund

Location: Singapore

Fund name: L Capital Asia II L.L.C.

Closing Amount: US$950 million (first close)

Launch date: March 2012

Fund Manager/Advisor: L Capital Asia Advisors

Stage Focus: Expansion/ Growth Capital

Industry Focus: Consumer products/services, Media, Retail/Wholesale, Textiles and clothing, Travel/Hospitality

Geographical Focus: Australia, China (PRC), India, Indonesia, Japan, Singapore, South Korea, Thailand, Vietnam

Contact: Kiki Yue

Phone: (65) 6672-7600

Email: [email protected]

Website: www.lcapitalasia.com

update: L Capital Asia has successfully held a first close of its second private equity fund, L Capital Asia II, at its hard cap of US$950 million. The Fund will target investment opportunities primarily in Greater China, Southeast Asia and India, as well as, on a more opportunistic basis, businesses in developed Asia (e.g., Australia, South Korea and Japan), particularly where such businesses may benefit from expansion into developing Asia. It is focused the sectors like fashion, leather goods, beauty and wellness, wine and spirits, watches and jewelry, lifestyle food and beverage and boutique hospitality.

nEW FundS

Location: Japan

Fund name: Ehime Venture Fund 2013 Investment Enterprise, L.P.

Target Amount: JPY 500 million

Launch date: August 2013

Fund Manager/Advisor: Future Venture Capital Co., Ltd.

Stage Focus: Expansion/ Growth Capital, Start-up/Early Stage

Industry Focus: No preference

Geographical Focus: Japan

Contact: Keiji Imajo

Phone: (81) 75-257-6656

Email: [email protected]

Website: www.fvc.co.jp

update: Future Venture Capital has raised JPY 500 million for Ehime Venture Fund 2013 to invest in unlisted high growth companies with high technology and university-linked ventures. Ehime Bank has committed JPY 475 million to the fund, whilst general partner Future Venture Capital has contributed JPY 25 million.

fund-raising monitor

TiE Investors’ Forum12 September, 9:30am - 5:00pm, Happy Valley Race Course

What is the Hong Kong investment ecosystem like for start-ups? What can Hong Kong learn about Silicon Valley’s investment environment? How do we

select the right investment? What are startups in HK doing now?