Fm balance sheet ratios

17

n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n financial ratios CAPITAL RATIOS FOR BALANCE SHEET

-

Upload

jenny-jose -

Category

Economy & Finance

-

view

70 -

download

0

Transcript of Fm balance sheet ratios

n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n

financial ratiosCAPITAL RATIOS FOR BALANCE SHEET

Current Assets -convertible to cash within a year Current Liabilities - payable within a year Ideally higher ratio indicates more liquid of the firms ability to current obligations in time and vice versa

2:1

Current ratioCurrent assets

Current liabilities• Cash in hand, bank • Sundry debtors • Bills receivable • Marketable securities (short term) • Short term investments • Inventories:

• raw materials • work in progress • finished goods

• Sundry creditors • Bills payable • Bank overdraft (short term) • Short term Advances • Income tax payable • Unpaid or unclaimed dividend

Current ratioADVANTAGES • Current ratio helps to measure the liquidity of a firm. • It represents general picture of the adequacy of the working capital position of a company. • It indicates liquidity of a company. • It represents a margin of safety, i.e., cushion of protection against current creditors. • It helps to measure the short-term financial position of a company or short-term solvency of a firm.

DISADVANTAGES • Current ratios cannot be appropriate to all business it depends on many other factors. • Window' dressing is another problem of current ratio, for example, overvaluation of closing stock. • It is a crude measure of a firm's liquidity only on the basis Of quantity and not quality of current assets.

Current ratio

Liquid ratioQuick assets

Current liabilitiesCURRENT ASSETS - STOCK - PREPAID EXPENSES

..or Quick/Acid test Ratio indicates short term solvency of company because only quick assets are related to current liabilities • Ideally i.e for every rupee of current liabilities there is a

rupee of quick assets • its an improvement over current ratio • indicates short term debt paying capacity of company • it is a better indicator of liquidity than current ratio • it emphasises qualitative aspect

1:1

Absolute liquid assets Current liabilities

CASH + BANK + MARKETABLE SECURITIES

• The reason of computing absolute liquid ratio is to eliminate accounts receivables from the list of liquid assets because there may be some doubt about their quick collection.

• This ratio is useful only when used in conjunction with current ratio and quick ratio.

• Ideally 0.5:1

Absolute liquid ratio

Absolute liquid ratio

Absolute liquid ratio

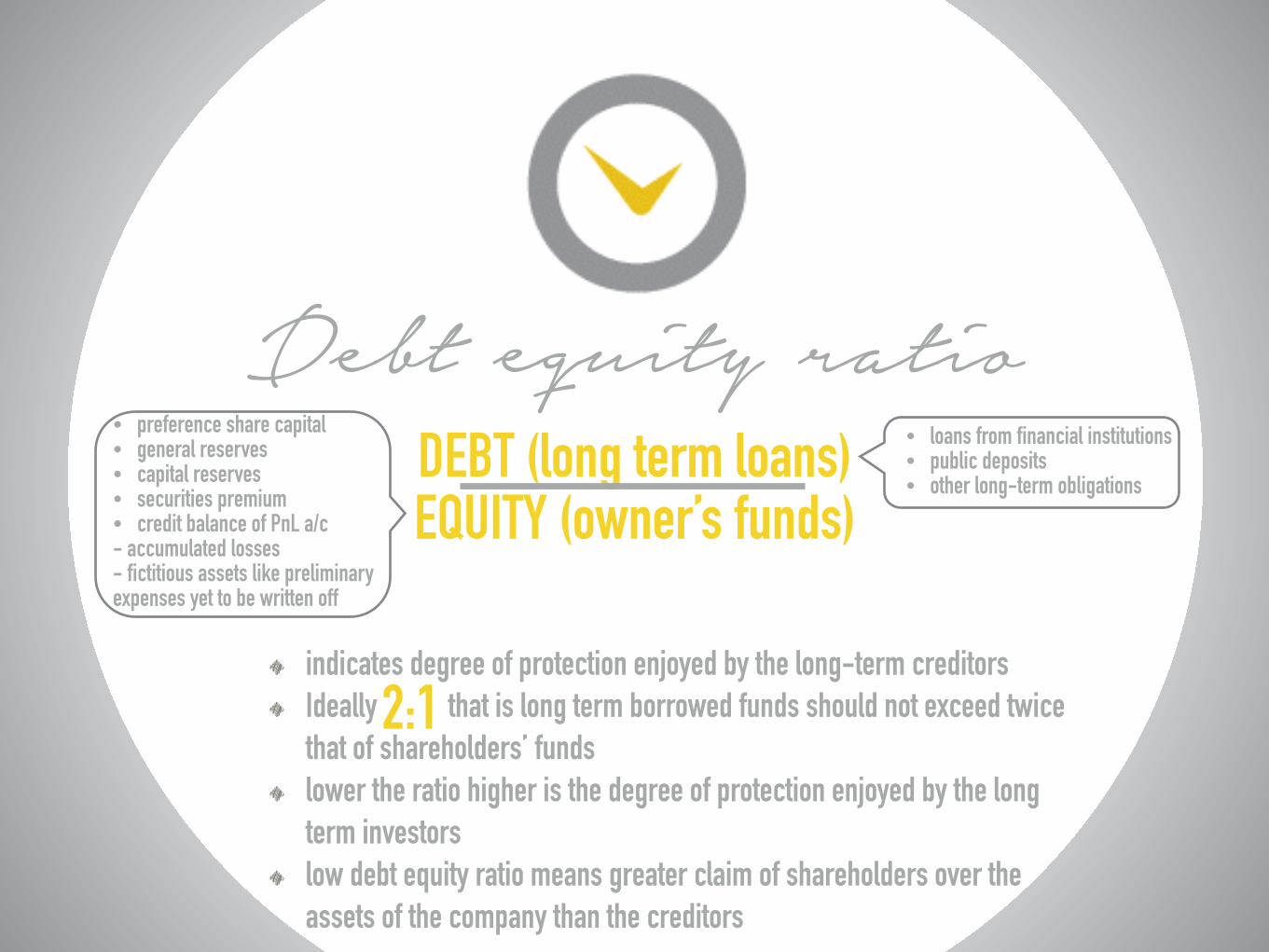

indicates degree of protection enjoyed by the long-term creditors Ideally that is long term borrowed funds should not exceed twice that of shareholders’ funds lower the ratio higher is the degree of protection enjoyed by the long term investors low debt equity ratio means greater claim of shareholders over the assets of the company than the creditors

2:1

Debt equity ratioDEBT (long term loans) EQUITY (owner’s funds)

• preference share capital • general reserves • capital reserves • securities premium • credit balance of PnL a/c - accumulated losses - fictitious assets like preliminary expenses yet to be written off

• loans from financial institutions • public deposits • other long-term obligations

Debt equity ratioDEBT (long term loans) EQUITY (owner’s funds)

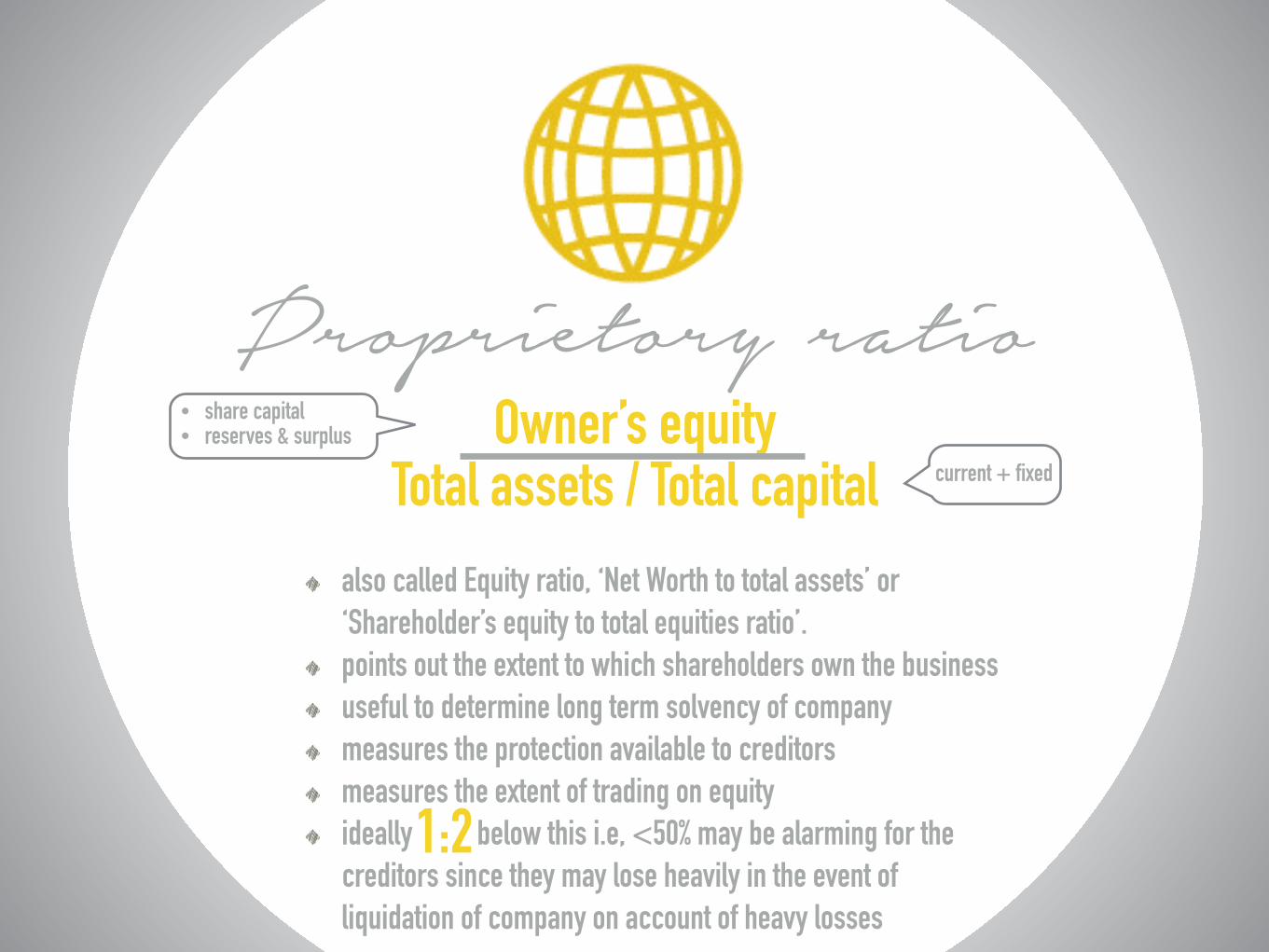

also called Equity ratio, ‘Net Worth to total assets’ or ‘Shareholder’s equity to total equities ratio’. points out the extent to which shareholders own the business useful to determine long term solvency of company measures the protection available to creditors measures the extent of trading on equity ideally below this i.e, <50% may be alarming for the creditors since they may lose heavily in the event of liquidation of company on account of heavy losses

1:2

Proprietory ratioOwner’s equity

Total assets / Total capital• share capital • reserves & surplus

current + fixed

also known as Leverage Ratio measures company’s ability f using debt for the benefit of shareholders expresses the relationship between equity shareholder’s funds and fixed interest/dividend bearing securities such as debentures, bonds and preference share capital when company is said to be low geared i.e, capital carrying a fixed rate of interest and dividend is in lesser proportion to equity share capital and vice versa

Capital gearing ratioPaid up amt of preference share capital + debentures + bonds

paid up amt of equity share capital + reserves & surplus

<1

Capital gearing ratio

indicates company’s operation efficiency measures how well a company is able to generate cash using working capital at its current inventory level low value of 1 or less of this ratio means company has high liquidity of current asset higher value means that a company is carrying too much inventory and is not favorable for management because excessive inventories can place heavy burden on the cash resources of the company

Capital inventory to working capital ratio

INVENTORY WORKING CAPITAL

• The increase in the ratio means that trading is slack or mechanization has been used.

• A decline in the ratio means that debtors and stocks are increased too much or fixed assets are more intensively used.

• If current assets increase with the corresponding increase in profit, it will show that the business is expanding

Current assets Fixed assets

• Cash in hand, bank • Sundry debtors • Bills receivable • Marketable securities (short term) • Short term investments • Inventories:

• raw materials • work in progress • finished goods

• machinery • buildings • plant • vehicles

Current assets to fixed assets ratio

n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n n

thank youJAYMEET——AMAYA——MUBASHSHIR——JILL——JENNY

Assets - proprietorship ratio

- -