FJJ Cornelissen - Dutch, German, and English Housing Bubbles in the 21th Century

52

DUTCH, GERMAN, AND ENGLISH HOUSING BUBBLES IN THE 21TH CENTURY AN EMPIRICAL INVESTIGATION OF EXPLOSIVE BEHAVIOR IN HOUSING MARKETS IN ORDER TO DETECT AND DATE- STAMP HOUSING BUBBLES F.J.J. Cornelissen, LL.M. Master thesis Financial Economics Radboud University Nijmegen Supervisor: S.C. Füllbrunn, PhD

-

Upload

frank-cornelissen -

Category

Documents

-

view

27 -

download

2

description

This study tries to determine whether housing bubbles existed in three European housing markets (the Dutch, German, and English) several years prior to, during, and directly after the recent global financial crisis. Furthermore, it aims to detect exactly when any bubbles in these markets started and ended. In order to achieve these goals, this study uses empirical methods, recently developed by Phillips, Wu, and Yu (2011) and Phillips, Shi, and Yu (2012), that look at explosive behavior in house prices by applying sophisticated unit root tests. These yielded some interesting results. While many bubbles were found in the Dutch housing market, the most surprising results was that a bubble existed between April 2011 to September 2013. Conversely, the German housing market was stable prior to and during the crisis but has developed a bubble since the third quarter of 2012. The English housing market exhibited a bubble between June 2006 and January 2008 but, surprisingly, showed no signs of bubbles since. As this study will argue, the empirical methods used to pinpoint the start and ending of bubbles can also be used as a real-time monitoring instrument to detect housing bubbles as they form, providing policy makers with a valuable early warning system.

Transcript of FJJ Cornelissen - Dutch, German, and English Housing Bubbles in the 21th Century

DUTCH, GERMAN, AND ENGLISH HOUSING

BUBBLES IN THE 21TH CENTURY

AN EMPIRICAL INVESTIGATION OF EXPLOSIVE BEHAVIOR IN HOUSING MARKETS IN

ORDER TO DETECT AND DATE-STAMP HOUSING BUBBLES

F.J.J. Cornelissen, LL.M.

Master thesis Financial Economics

Radboud University Nijmegen

Supervisor: S.C. Füllbrunn, PhD

i

ABSTRACT This study tries to determine whether housing bubbles existed in three European housing

markets (the Dutch, German, and English) several years prior to, during, and directly after the

recent global financial crisis. Furthermore, it aims to detect exactly when any bubbles in these

markets started and ended. In order to achieve these goals, this study uses empirical methods,

recently developed by Phillips, Wu, and Yu (2011) and Phillips, Shi, and Yu (2012), that look at

explosive behavior in house prices by applying sophisticated unit root tests. These yielded some

interesting results. While many bubbles were found in the Dutch housing market, the most

surprising results was that a bubble existed between April 2011 to September 2013. Conversely,

the German housing market was stable prior to and during the crisis but has developed a bubble

since the third quarter of 2012. The English housing market exhibited a bubble between June

2006 and January 2008 but, surprisingly, showed no signs of bubbles since. As this study will

argue, the empirical methods used to pinpoint the start and ending of bubbles can also be used

as a real-time monitoring instrument to detect housing bubbles as they form, providing policy

makers with a valuable early warning system.

Keywords: housing market bubbles, house prices, rent, right-tailed unit root tests,

Augmented Dickey-Fuller tests, date-stamping bubbles, real-time monitoring,

early warning system.

ii

CONTENTS

Abstract ................................................................................................................................................................................... i

Contents ................................................................................................................................................................................. ii

1. Introduction ................................................................................................................................................................ 1

1.1 Bubbles in European housing markets .................................................................................................. 1

2. Literature review ...................................................................................................................................................... 3

2.1 An overview of alleged bubbles ................................................................................................................ 3

2.1.1 Dutch bubbles ......................................................................................................................................... 3

2.1.2 German bubbles ..................................................................................................................................... 4

2.1.3 English bubbles ...................................................................................................................................... 6

2.2 Potential effects of housing market bubbles ....................................................................................... 6

2.3 Defining a bubble ............................................................................................................................................ 7

2.4 Fundamental value ......................................................................................................................................... 8

2.4.1 Income ....................................................................................................................................................... 9

2.4.2 Inflation, demographics, interest.................................................................................................... 9

2.4.3 Rent .......................................................................................................................................................... 10

2.5 Rational bubble theory .............................................................................................................................. 11

2.5.1 Fundamental value ............................................................................................................................ 11

2.5.2 Rational bubbles ................................................................................................................................. 13

2.6 Irrationality and bubbles .......................................................................................................................... 14

2.7 Research questions ..................................................................................................................................... 15

3. Research Method ................................................................................................................................................... 17

3.1 Statistical method: finding evidence of a bubble ............................................................................ 17

3.1.1 Variance bounds test ........................................................................................................................ 17

3.1.2 Explosive autoregressive behavior ............................................................................................. 17

3.1.3 Forward recursive autoregressive test ..................................................................................... 19

3.2 A method of date-stamping bubbles .................................................................................................... 21

3.2.1 A bubble within the sample ........................................................................................................... 21

3.2.2 Date-stamping multiple bubbles ................................................................................................. 22

3.3 Real-time monitoring ................................................................................................................................. 24

3.4 Data .................................................................................................................................................................... 25

4. Empirical testing and results ............................................................................................................................ 27

4.1 Empirical testing for bubble presence ................................................................................................ 27

4.1.1 -tests ............................................................................................................................................ 27

4.1.2 Forward recursive -test ....................................................................................................... 28

iii

4.2 Date stamping ............................................................................................................................................... 29

4.2.1 Forward recursive -test ....................................................................................................... 29

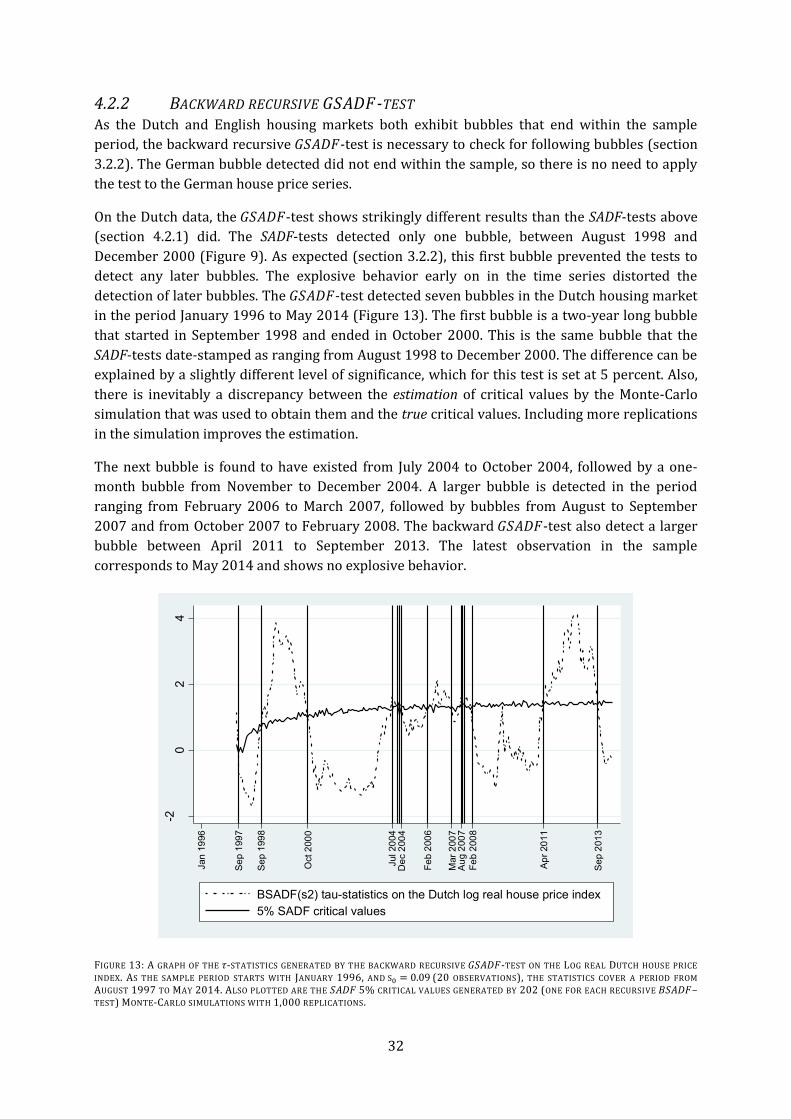

4.2.2 Backward recursive -test ................................................................................................. 32

4.3 Real-time monitoring ................................................................................................................................. 34

5. Discussion ................................................................................................................................................................. 36

6. Conclusion ................................................................................................................................................................ 39

Bibliography ...................................................................................................................................................................... 40

Appendix A: Bubble forms ........................................................................................................................................... 45

Appendix B: Time series’ graphs ....................................................................................................................... 46

1

1. INTRODUCTION

1.1 BUBBLES IN EUROPEAN HOUSING MARKETS In recent years, price developments on European housing markets have been topic of hot debate.

News articles often report on house price bubbles, whose existence is normally regarded as a

fact of common knowledge. On August 30, 2014, The Economist stated: ‘House prices in Europe

are losing touch with reality again’. Furthermore, it concludes that of twenty-three property

markets tested, nine are overvalued by at least 25%, six of which are European. Overvaluation is

defined as a positive deviation from a price-ratio’s historic average.

On the Dutch housing market specifically, the Financial Times reported on August 25, 2013, ‘that

the Dutch housing market is deflating, as prices were too high’. On the downgrading of the

Netherlands’ credit rating by Standard & Poor’s, The Economist declared at November 29, 2013:

‘[t]he chief culprit, everyone agrees, is a massive housing bubble early in the last decade’. Der

Spiegel at March 20, 2013: ‘The Netherlands is still one of the most competitive countries in the

European Union, but now that the real estate bubble has burst, it threatens to take down the

entire economy with it.’1 Figure 1 shows that house prices did indeed steeply rise from the

second half of the 1990s and started falling in 2008.

This thesis aims to investigate what many news articles so casually assume: did housing market

bubbles exist in Europe in the last decade and when did they occur? It will apply modern

econometric research methods to find answers to these questions. In order to get a

comprehensive result, while being able to apply several methods, this thesis necessarily focuses

on three countries in the 2000s and 2010s: the Netherlands, England, and Germany. These

countries are chosen partly because of the availability of data on their housing markets. Also, as

we will see below, there was at one point consensus among economists about the presence of a

bubble for the Dutch, English and German housing markets. Therefore, the results of this

research are also an assessment of methods used and opinions given by economists on these

markets. That assessment may add to the relevance of this thesis.

The importance of detecting housing market bubbles stands in sharp contrast to the inability of

economists to agree on whether particular bubbles exist (section 2.1). Therefore, this thesis

aims to add some clarity to theoretical and methodological issues concerning bubble tests, and

to establish if and when bubbles existed on the Dutch, German, and English housing markets. To

this end, other literature on the definition and nature of housing bubbles will be discussed next.

Then, the theoretical and methodological framework of this study are outlined, empirical tests

are performed.

This study detects housing bubbles by comparing house price movements to movements in rent.

It asserts that the fundamental value of houses depends on rents. Explosive behavior of house

prices constitutes a bubble if it is not caused by a simultaneous explosiveness of rents. Using

several right-tailed unit root tests to determine whether either house prices or rents behave

explosively, this study will determine if bubbles exist in housing markets and, if so, when they

1 Translation of this originally German article obtained from: http://www.spiegel.de/international/europe/economic-crisis-hits-the-netherlands-a-891919.html, retrieved at April 25, 2014.

2

started and ended (if at all). Also, a new way to monitor housing markets in real time is

proposed.

It is also important to note what this thesis does not aim to do. It does not explain why or how

bubbles occur. It will not give any policy advice, other than advice on how to better detect

market bubbles. If a bubble is detected, this thesis will not explain what its consequences would

be, or whether a ‘soft landing’ is possible or desirable.

3

2. LITERATURE REVIEW

2.1 AN OVERVIEW OF ALLEGED BUBBLES

2.1.1 DUTCH BUBBLES When looking at a visual representation of Dutch housing prices (Figure 1), one could easily

assume that a bubble occurred, and that it reached its height in 2008. While the alleged bubble

in the Dutch housing market apparently formed and subsequently collapsed, consensus in

economic literature was lacking. As late as 2010 there was and had been no housing market

bubble according to many economists despite many disturbing signs (Knibbe, 2010, pp. 106-

107). Real house prices had already fallen by 8% in two years’ time, while they had risen

between 1986 and 2007 by about 150% (Knibbe, 2010, p. 106).

FIGURE 1: DUTCH HOUSE PRICE INDEX (2010=100), CONTAINING 221 MONTHLY OBSERVATIONS, FROM JANUARY 1996 TO MAY 2014. DATA

SOURCE: STATLINE, STATISTICS NETHERLANDS (MORE INFORMATION IN SECTION 3.4).

Many researchers use an error correction model (ECM) to determine whether house prices are

overvalued. Such a model consists of two (main) equations, representing a long-term

equilibrium and short-term price adjustments. In the long run, the level of house prices is

modeled to depend on one or more fundamental variables (level of income, rent etc., section

2.4). However, in the short run, the change in house prices depends on changes in fundamentals,

previous house price changes and the deviation of actual house prices from their long-term

equilibrium.

Using such a model, Francke (2010, p. 17) asserts that Dutch house prices were not overvalued

as of 2009. The CPB Netherlands Bureau for Economic Policy Analysis estimated a 10 percent

overvaluation of house prices in 2003 (2005, p. 29) that shrunk to approximately 0 percent in

2007 (2008, p. 7). According to the OECD, there was a 20.4 percent house prices overvaluation

in 2004 (2005, p. 136).

At the same time, the IMF found a gap of 30 percent between actual and fundamental house

prices that cumulated between 1997 and 2007 (2008, p. 113), contradicting the CPB’s

40

60

80

100

120

Dutc

h h

ouse

price

ind

ex

Jan 1996 Sep 1999 May 2003 Jan 2007 Sep 2010 May 2014

4

assessment. In 2009 however, the International Monetary Fund (2009, p. 10) states that ‘[t]he

housing market (…) does not appear out of kilt (…)’. Similarly, in 2011 IMF’s Executive Director

for the Netherlands concludes that ‘house prices seem to be in line with fundamentals’

(International Monetary Fund, 2011).

Dreger and Kholodilin (2013, p. 13) investigated large samples of housing market data on 12

OECD countries and detected no bubbles on the Dutch housing market between the third

quarter of 1978 to the last quarter of 2009. This finding contradicts the assessments mentioned

above by the CPB, the OECD, and the IMF.

In its 2014 edition of the Economic Survey, the OECD (2014, p. 11) asserted that Dutch house

price-to-rent and house price-to-income ratios are still above their long-term averages in the

last quarter of 2013 (by 5% and 20%) and warns that house prices could therefore continue to

fall. There is and has been no agreement among economists whether the Dutch housing market

experienced one or more bubbles in the last two decennia and when they occurred.

2.1.2 GERMAN BUBBLES Unlike the Dutch housing market, the German housing market seemed a clear-cut case for most

of the 2000s. German real house prices had been quite stable since 1999. According to Kofner

(2014), this stability is due to the tenure structure of the German housing market, which is

relatively unique for a developed country. In 2012, only 53.3 percent of Germany’s population

lives in owner-occupied houses. 2 The academic consensus seems to have been that no

overvaluation of German house prices had existed. There are few publications on house prices

during this stable period. This is probably due to a publication bias: few people are willing to

publish articles or reports on stationary markets and the absence of a bubble. IMF Staff reports

do not explicitly tell German authorities not to worry about housing price developments. Also,

researchers will often only try to detect a bubble if they hypothesized it is really there. Dreger

and Kholodilin (2013, p. 13) did look for housing market bubbles in Germany but found none in

a period from 1995 to 2009.

In recent years, however, German house prices have been increasing (Figure 2) and this increase

raises the question whether a bubble is forming. The Bundesbank, having a reputation for

conservatism, suggests in its Monthly Report in October 2013 that lax monetary policy by the

European Central Bank may lead to an inflation of house prices. The report estimates an

overvaluation of house prices of 5 to 10 percent in urban areas and even 20 percent in

particularly attractive cities but found no substantial overvaluation in the German property

market as a whole (Bundesbank, 2013, pp. 13, 28).

Thus far, German economists seem to agree with their national bank. Just et al. (2013, p. 35)

found no ‘Blasenbildung’ in the German property market and Feld et al. (2014, p. 3) state: ‘Von

Überhitzung derzeit keine Spur.‘ Chen and Funke (2013, pp. 12-13) also found no bubble up until

the last quarter of 2012. Tschekassin (2014) even points out that two important indicators, the

price-to-rent ratio and the price-to-income ratio, were still below their long-term averages in the

last quarter of 2013. The OECD (2014, p. 12) agrees that with the Bundesbank that although

some local overvaluation may exist, there is no bubble in the housing market as a whole. The

IMF (2014, pp. 25-26) also agrees with the assessment of the Bundesbank and the OECD, but it

2 Eurostat 2012, http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=ilc_lvho02&lang=en. Retrieved September 11, 2014. For Switzerland, this number is even lower: 43.8%.

5

advises German authorities to carefully monitor the housing market in the near future (p. 36):

‘While concerns about a housing bubble are premature, preparations against it are not.’

FIGURE 2: GERMAN HOUSE PRICE INDEX (2010=100), CONTAINING 55 QUARTERLY OBSERVATIONS, FROM 2000Q1 TO 2013Q3. DATA

SOURCE: DESTATIS, GERMAN FEDERAL STATISTICS OFFICE (MORE INFORMATION IN SECTION 3.4).

In short, no-one believes a bubble was present on the German housing market in recent years,

even though prices have risen (Figure 2). However, the increased house prices did prompt the

IMF to advice German authorities to closely monitor further developments.

FIGURE 3: ENGLISH HOUSE PRICE INDEX (2010=100), CONTAINING 113 MONTHLY OBSERVATIONS, FROM JANUARY 2005 TO MAY 2014. DATA SOURCE: OFFICE OF NATIONAL STATISTICS (MORE INFORMATION IN SECTION 3.4).

95

100

105

110

Germ

an h

ouse

price

ind

ex

2000Q1 2002Q2 2004Q3 2006Q4 2009Q1 2011Q2 2013Q3

80

90

100

110

120

En

glis

h h

ou

se p

rice in

de

x

Jan 2005 Nov 2006 Oct 2008 Aug 2010 Jul 2012 May 2014

6

2.1.3 ENGLISH BUBBLES Economists did find bubbles in an English housing market that has undergone large shifts in

house prices in recent years (Figure 3). Fry (2009) found that bubbles comprised 30 to 40

percent of English house prices between 2002 and 2007. And Dreger and Kholodilin (2013, p.

13) detected a bubble in the aggregate UK housing market in roughly the same period (2002Q2

to 2007Q2). An analysis ordered by the European Commission concluded that late in 2008,

prices were (much) higher than any fundamentals could justify (Kuenzel & Bjørnbak, 2008).

Recently, the IMF (2014, p. 26) stated that the United Kingdom, including England, is at (high)

risk of experiencing a sharp reduction in house prices. It also notes that house prices are

increasing rapidly. The IMF does not use the terms ‘bubble’ or ‘overvaluation’, but it strongly

seems that this is exactly what it has found and is warning for. Along the same lines, the

Governer of the Bank of England stated during a hearing of the Treasury Committee of the House

of Commons that the housing market contains great risks to the UK economy, especially because

house prices are ‘biased upwards’ (Treasury Committee, 2014), which seems to be a euphemism

for a bubble.

On the English and UK housing markets, a general consensus exists that a bubble existed up until

2007 or 2008 (at least) and that the recent increase in house prices also indicates a bubble.

2.2 POTENTIAL EFFECTS OF HOUSING MARKET BUBBLES ‘Prior to the global recession of 2008-2009 and the associated disruptions in financial markets, asset price

bubbles were often considered as a sideshow to macroeconomic fluctuations. The global recession demonstrated

painfully that this dominant pre-crisis presumption was dangerously wrong.’ (Chen & Funke, 2013, p. 2)

The importance of detecting bubbles in the housing market cannot be overstated. The deflation

or implosion of such bubbles has large adverse effects both on the macroeconomic scale and at

the level of households (Baker, 2002, p. 12). These separate types of impact are shortly

addressed here.

When there is a housing bubble, people will want to invest more in houses because they expect

prices to rise even further. They will buy larger or more houses than they would otherwise do.

The bubble also spurs consumption in two ways. First, there is a direct effect: larger and more

houses need more furniture, carpets and other household items. Secondly, the wealth effect of

the housing bubble affects consumption indirectly. As people see their wealth accumulating

because of the rising value of their houses, they are likely to feel less need to save for the future.

Higher house prices also enable house-owning families to borrow more as they can use their

home equity to secure loans. This money is spend on consumption. Case et al. (2005, p. 1249)

found ‘strong evidence that variations in housing market wealth have important effects upon

consumption’ and concluded that the housing market appears to be more important than the

stock market in influencing consumption.

Large though the effects of a collapsing housing bubble on the macroeconomic scale may be, for

individual households, the impact can be even more severe. As the home is often a family’s most

important asset, a sudden decline in its value greatly affects the household’s wealth. As long as it

does not sell the house, and does not immediately need the wealth represented by the house, no

problems may occur. However, if people planned to liquefy their wealth by selling or

remortgaging in order to finance their retirement, their retirement income will be much lower.

Furthermore, if people are forced to move because of a divorce or because of their jobs, they

7

may be left with large debts as their mortgage loan is larger than the market price of their house.

If this effect prevents people to be able to move for new jobs, it also leads to inefficient job

markets and possibly to more unemployment.

Reinhart and Rogoff (2008) investigated a selection of 18 financial crises in different countries

and found that a large rise in housing prices almost always preceded a crisis. The housing

market may therefore be a contributing factor in a certain state of the economy that leads to a

crisis. This relation is also described by Kindleberger and Aliber (2005, p. 117). Even if no such

causal relationship exists, housing prices may serve as an early warning of an approaching

financial crisis.

Local government income depends heavily on house prices, because of real property tax.3 A

collapsing housing market bubble could significantly affect the income of Dutch and German

municipalities, and England’s districts.

2.3 DEFINING A BUBBLE There is no one answer to what a bubble in asset prices is exactly. Kindleberger and Aliber

(2005, p. 29) give a very broad definition and state that a bubble is ‘an upward price movement

over an extended period of fifteen to forty months that then explodes’. The esteemed economist

Robert J. Shiller, who together with Fama and Hansen received a Nobel Prize in 2013 ‘for their

empirical analysis of asset prices’ states:

‘I define a speculative bubble as a situation in which news of price increases spurs investor enthusiasm, which

spreads by psychological contagion from person to person, in the process amplifying stories that might justify

the price increases and bringing in a larger and larger class of investors, who, despite doubts about the real

value of an investment, are drawn to it partly through envy of others’ successes and partly through a gambler’s

excitement.’ (Shiller, 2005, p. 2)

Regrettably, both widely used definitions are not suited to this thesis. Kindleberger and Aliber’s

encompasses more than what is an asset price bubble. When market agents expectations on

future cash flows arising from an asset rise, than the price of that particular asset should also

rise. A sudden negative change in expectations then could adversely and instantly affect the

price of that asset. For example, the unexpected discovery of large quantities of easily mineable

gold would undoubtedly cause a large drop in gold prices. This does not mean that rising gold

prices prior to the drop constitute a bubble. In this case, the “explosion” of the price movement is

caused by fundamentals. The definition given by Shiller on the other hand, describes a

psychological process that is hardly testable at the housing market scale. More importantly, his

definition seems to preclude the possibility that agents investing in bubble markets might do so

rationally. They may invest when they expect the bubble to expand even more.

An empirically testable and conceptually sound definition of an asset price bubble can be

deduced from the following statement by Joseph E. Stiglitz:

‘[I]f the reason that the price is high today is only because investors believe that the selling price will be high

tomorrow – when ‘fundamental’ factors do not seem to justify such a price – then a bubble exists.’ (Stiglitz,

1990, p. 13)

3 In the Netherlands, municipalities collect Onroerendezaakbelasting pursuant to the Wet waardering onroerende zaken. The Grundsteuergesetz delegates power to German municipalities to collect Grundsteuer. In England, districts collect Council Tax in carrying out the Local Government Finance Act 1992.

8

Lind (2009, p. 81) notes that this definition does not cover the whole bubble episode and only

refers to price increases, and rejects Stiglitz’ definition. I will stick to Stiglitz’ bubble description

but suggest adding a phrase to include the period between a bubble’s collapse and the return to

fundamental value:

‘(…) then a bubble exists until the price returns to a level that is justified by those fundamentals.’

A bubble thus exists if, for a significant period of time, the price of an asset exceeds its

fundamental value. The price is not justified by its fundamentals, and the difference between

market price and fundamental value is a bubble. Some economists even allow for negative

bubbles (Siegel, 2003, p. 14). As asset price bubble can exist solely because of the belief that,

regardless of the fundamental value, an existing overvaluation will endure. This is commonly

referred to as a rational bubble. The theory of rational bubbles is central to this thesis and will

be discussed formally in section 2.5.

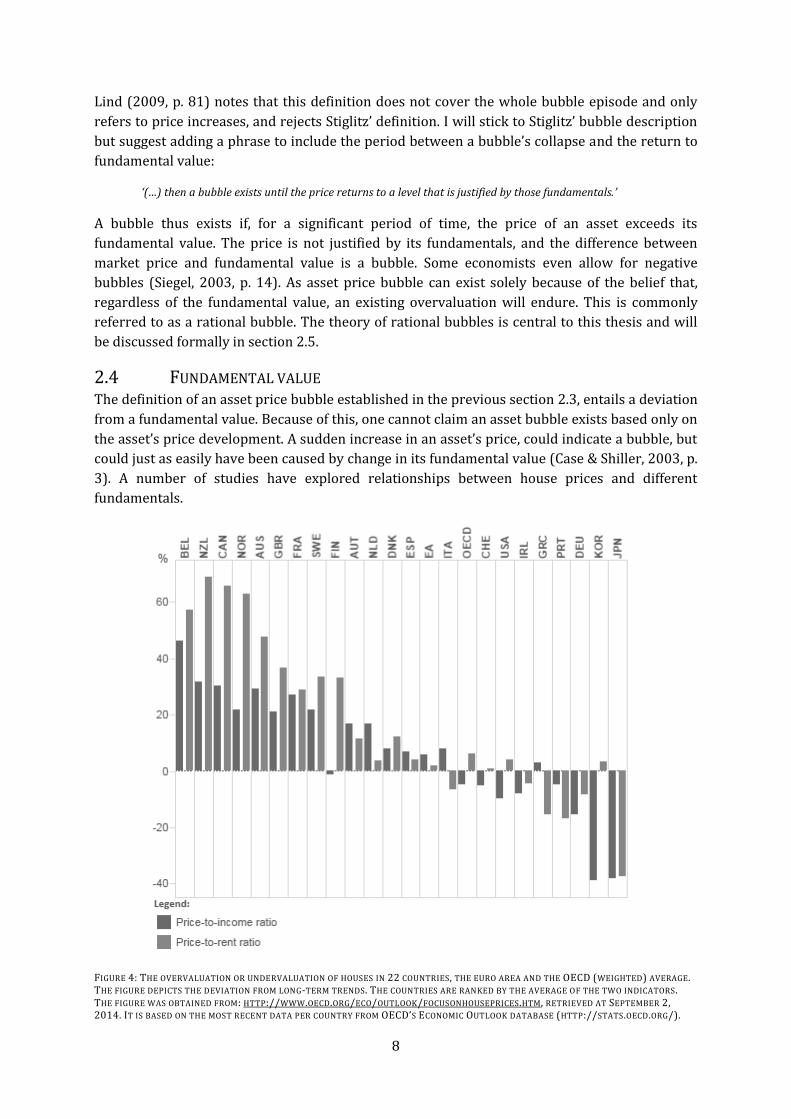

2.4 FUNDAMENTAL VALUE The definition of an asset price bubble established in the previous section 2.3, entails a deviation

from a fundamental value. Because of this, one cannot claim an asset bubble exists based only on

the asset’s price development. A sudden increase in an asset’s price, could indicate a bubble, but

could just as easily have been caused by change in its fundamental value (Case & Shiller, 2003, p.

3). A number of studies have explored relationships between house prices and different

fundamentals.

FIGURE 4: THE OVERVALUATION OR UNDERVALUATION OF HOUSES IN 22 COUNTRIES, THE EURO AREA AND THE OECD (WEIGHTED) AVERAGE. THE FIGURE DEPICTS THE DEVIATION FROM LONG-TERM TRENDS. THE COUNTRIES ARE RANKED BY THE AVERAGE OF THE TWO INDICATORS. THE FIGURE WAS OBTAINED FROM: HTTP://WWW.OECD.ORG/ECO/OUTLOOK/FOCUSONHOUSEPRICES.HTM, RETRIEVED AT SEPTEMBER 2, 2014. IT IS BASED ON THE MOST RECENT DATA PER COUNTRY FROM OECD’S ECONOMIC OUTLOOK DATABASE (HTTP://STATS.OECD.ORG/).

9

2.4.1 INCOME In studies of residential property bubbles, a common fundamental is the per capita disposable

income. The price-to-income ratio, also referred to as the affordability ratio, is a measure of

whether or not a house is within reach of the average buyer. In theory, if the ratio is too high,

buying a house is no longer attainable for prospective buyers, demand will drop and therefore

house prices decrease. In this way, the ratio is always expected to return to a long-term

(fundamental) average (Girouard, Kennedy, Noord, & André, 2006, p. 16). Figure 4 depicts the

deviation of the price-to-income ratios to long-term equilibria. According to the price-income

relationship and this method, Dutch house prices are overvalued, as are house prices in Great-

Britain and – probably – England. German house prices on the other hand are undervalued.

There is some criticism in literature on using the price-to-income ratio to look for bubbles.

Girouard et al. note a serious flaw in the measurement: the disposable income is an average of a

whole population, while buyers and sellers on the housing market have higher-than-average

incomes (2006, p. 16). Another objection is raised by Gallin (2003). He found no evidence in US

housing market data that there is a significant relationship between the level of house prices and

the level of disposable income and asserts that many tests for bubbles based on this relationship

may be inappropriate. Furthermore, André notes that tests based on the price-to-income ratio

cannot exclude that a higher ratio is caused by a higher (long-term) equilibrium (2010, p. 11).

2.4.2 INFLATION, DEMOGRAPHICS, INTEREST Brunnermeier and Julliard (2006) looked at the relationship between house prices and inflation

and found that potential home buyers base their decision to purchase a house not on the real

interest rate, but on the nominal interest rate. They attribute the influence of inflation to money

illusion, due to the fact that households compare monthly rental payments to nominal mortgage

payments.

Other fundamentals are financing conditions, such as the availability of mortgage loans, and

demographic development (André, 2010, p. 27). As populations grow, demand for homes

increases. Furthermore, household size has generally diminished over time in OECD countries,

due to larger numbers of single-parent families, and an ageing population that is increasingly

autonomous (Heyer, Le Bayon, Péléraux, & Timbeau, 2005, p. 16). These and other demand-

increasing factors affect house price level especially because of rigidities in the housing markets’

supply adjustment (André, 2010, p. 27).

It is virtually uncontested that a significant relationship between the interest rates and house

price movements exists (McQuinn & O'Reilly, 2008). Low interest rates open up the housing

markets for more households (and allow existing homeowners to be able to purchase larger

houses) as a result of cheaper mortgage loans. Also, opportunity costs for owning a house are

lower. Furthermore, a lower (nominal) interest rate, positively affects demand as it decreases

borrowing restraints for households (André, 2010, p. 19) As a result, a decrease in interest rates

stimulates demand for residential property and therefore house prices should rise. Case and

Shiller (2003, p. 312) however, found that in several US housing markets in the 1990s, house

prices did not significantly respond to changes in interest rates. They contribute this finding to

simultaneity: low interest rates stimulate the housing market, but low interest rates may be

caused by monetary easing as a response to a weak economy and housing market.

10

Shiller (2007) also mentions the construction cost of new houses as an important fundamental

that is significantly related to house prices.

2.4.3 RENT Many researches testing for housing bubbles focus on the relationship between prices and rent,

e.g.: Ambrose et al. (2013), Yiu & Lu (2012), Shi (2007), Hwang-Smith & Smith (2006), and Chan

et al. (2001). The price-to-rent ratio can be seen as the cost of owning versus renting a house

(Girouard, Kennedy, Noord, & André, 2006, p. 19). The relationship between house prices and

rent can also be interpreted as between an investment and the cash flows it generates. The

fundamental value as the present value of future cash flows is explained in detail in section 2.5.1.

Gallin studied US housing market data from 1970 to 2003 and found that a significant

relationship between rent and house prices exists (2004). The OECD found that, according to the

price-to-rent ratios, Dutch house prices are (slightly) overvalued, British house prices are

overvalued by nearly 40 percent, and German house prices are undervalued (Figure 4).

Glaeser and Gyourko (2007, pp. 17-22) argue that there is little arbitrage between owning and

renting on the housing market. First of all, the abstract notion of consumable housing units does

not exist in real life: rental property is very different from owner-occupied property. On average,

rental homes are units in buildings that house multiple households (e.g., apartments), while

owner-occupied homes are often detached houses. Furthermore, both types of homes are

located in different parts of metropolitan areas and have different quality neighborhoods. Also,

renters and owners are different types of people. Knibbe (2010, p. 109) makes the point that not

all households are able to choose between renting and buying as low income groups often do not

have access to the mortgage market. Many households therefore do not have (or make) a real

choice between renting and owning.

In spite of the observation that there is only limited arbitrage between owning and renting, this

thesis will use the price-rent relationship to model the housing markets. First of all, the link

between house prices and rent is conceptually clear (section 2.5.1). Because both rent and house

prices are housing market variables, many other fundamentals discussed here affect them

symmetrically (Brunnermeier & Julliard, 2006, p. 9) (Ambrose, Eichholtz, & Lindenthal, 2013, p.

16). For example, higher disposable incomes are likely to positively affect both rents and

housing prices. Similarly, on a 30 percent increase in US real house prices between 1995 and

2002, Baker states:

‘The fact that rents had risen by less than 10 percent in real terms should have provided more evidence to

support the view that the country was experiencing a housing bubble. If there were fundamental factors driving

the run-up in house sale prices they should be having a comparable effect on rents.’ (Baker, 2008, p. 74)

Furthermore, even though there may be limited arbitrage between owning and renting, a house

can also be viewed as an investment that requires certain future cash flows (rental income) to

justify its price (section 2.5.1). Much literature on asset price bubbles refers (primarily) to stock

market bubbles. The fundamental value is always determined by the present value model,

whereby the sum of discounted expected future dividends from that stock constitutes its

fundamental value. For the housing market, the fundamental value of houses is similarly

determined by their strand of expected future cash flows. Instead of dividends, houses generate

rental income. As Hwang-Smith and Smith (2006, p. 8) argue, the implicit cash flow from an

owner-occupied house, are the rental payments that would have to be made if the house were

rental property. The fundamental value and market value of a house are perhaps unclear for

11

market agents. Real property markets are characterized by infrequent, privately negotiated

deals in which whole, unique assets are traded. In this type of market, it is difficult to know at

any given time the precise market value of any given real estate asset (Geltner, Miller, Clayton, &

Eichholtz, 2007, p. 272). In these aspects, the real estate market differs from stock markets.

Every listed share always has a clear market price, as shares, unlike houses, are homogeneous

goods that are traded frequently and publicly. House prices have been shown to be somewhat

forecastable (Case & Shiller, 1989), which is probably due to the fact that entering and exiting

the housing market is costly (Shiller, 2005, p. 14).

2.5 RATIONAL BUBBLE THEORY

2.5.1 FUNDAMENTAL VALUE As mentioned in section 2.4, this paper explores the relationship between actual house prices as

opposed to fundamental house prices, determined by rent. The fundamental value of houses is

expressed mathematically according to the present value model, as demonstrated by Homm and

Breitung (2012, pp. 200-201) for stocks. By definition, the following standard no-arbitrage

condition must be true for the rate of return on any asset:

Equation 1

,

where is the rate of return on holding the asset at time , denotes the asset price at time

and is the return (pecuniary or otherwise) on the asset at time .4

As Brancaccio (2005, p. 27) notes, Equation 1 is only an accounting definition. In order to

produce the final present value model equation, three assumptions have to be made that can be

represented schematically (Figure 5).

FIGURE 5: THREE ASSUMPTIONS OF THE PRESENT VALUE MODEL.

4 This timing assumption is a convention in finance literature. Holding a stock gives a claim to next period’s dividend but not to this period’s dividend. By contrast, Blanchard and Watson (1982), who for the first time described mathematically how rational bubbles can exist, do not adhere to this convention and

assert that

.

Present Value Model

Constant expected return on asset R

ASSUMPTION I

Constant intertemporal preferences and risk

neutrality

ASSUMPTION II At any given time, all agents have the same information

and have rational expectations

ASSUMPTION III Transversality condition

12

Assumption I (A-I) means that market agents’ preferences about consumption, savings and

wealth allocation do not vary in time. Following Blanchard and Watson (1982, p. 2) this also

means that market agents are risk neutral. The second assumption (A-II) includes the strong-

form Efficient Market Hypothesis (EMH): all agents have the same information set, so there is no

insider or private information. Furthermore, A-II states that agents have rational expectations

and do not forget any information so that , where is the information set available to

agents at time .

Though the real return on an asset is not necessarily equal to the expected return, all

information available is shared by all agents and is included in their expectations. The deviation

of real return from the expected return is therefore random, and the expected return is equal to

the risk-free rate, as agents are risk neutral and do not require a risk premium. Expressed

mathematically:

Equation 2 ( ) , and, combining Equation 1 and Equation 2:

Equation 3 ( )

( ).

where is the risk-free rate. Following Phillips et al. (2011, p. 205), I assume that the risk-free

rate is strictly positive: . The price of an asset depends on its expected future price and

returns discounted at the discount factor ( ) .

As Blanchard and Watson (1982, p. 2) explain, some assumptions are inessential to the model

and could be relaxed at the cost of notational complexity. This includes the assumption of a

constant discount factor (and risk-free rate) which is common in empirical bubble literature

(Engsted & Nielsen, 2012). Phillips et al. (2011, p. 204) explain that the discount rate could also

be stationary and time-varying but that would complicate the analysis of the rational bubble

explained further on. Inessential are also the assumptions that there are no constraints on short

selling and agents are risk neutral. In reference to Figure 5, A-I is not an essential assumption of

the present value model, but helps keep it simple. However, the strong information assumption

is essential and central to the model. The model assumes strong-form market efficiency, as

Roberts famously called it (Campbell, Lo, & MacKinlay, 1997, p. 22).

Given Equation 3, the asset price at time can now be stated:

Equation 4 ( )

( ).

Inserting Equation 4 in Equation 3, the price at time is:

Equation 5 ( ( ) )

( ).

Solving Equation 3 by further forward iteration shows that:

Equation 6 ∑

( ) ( ),

where

is the fundamental value of the asset that, being a strictly positive constant, depends

solely on the market’s expectation on all future returns on the asset given the information

currently available to it. Equation 6 implicitly follows the Law of Iterated Expectations, meaning

13

that if , one cannot predict at time , when available information is restricted to the set

, what the forecast error one would make having (Campbell, Lo, & MacKinlay, 1997, p. 23).

The fundamental value therefore only depends upon information that is currently available.

Equation 6 is only a unique solution to Equation 3 when the transversality condition (A-III)

holds (Blanchard & Watson, 1982, p. 7):

Equation 7 .

( ) / , so that

Equation 8

.

Equation 7 means that the present value of the asset price at an infinitely far away future period,

is zero. This value of the asset depends on expected returns from that future date onward

(Equation 6). The transversality condition therefore requires cash flows to grow at a lower rate

than .

In short, if the three main assumptions depicted in Figure 5 hold, an asset’s actual price

represents its fundamental value.

2.5.2 RATIONAL BUBBLES For a long time economists took any deviations of actual prices from goods’ fundamental values,

when observed, as evidence of irrationality. Blanchard and Watson (1982, p. 1) asserted for the

first time that this is a non sequitur as the argument precluded the possibility of a rational

bubble. This is a bubble rational agents would buy in to in order to sell the asset in the future

when it is (rationally) expected to be at least equally overvalued.

In order for a bubble to form in this present value framework, no irrationality need be

introduced. Markets can still be efficient and market agents still carry rational expectations (A-

II). For a bubble to be able to exist, relaxing A-III suffices.

Without the transversality condition of Equation 7, is not the only price that solves equation

(1). A bubble component can be introduced. Consider for example a process ( ) with the

property

Equation 9 ( ) ( ) .

Evidently, adding the bubble component to the fundamental asset price

results in another

solution to Equation 3:

Equation 10 , where ,

so that there can be no negative bubble. When agents can freely dispose of an asset, rationality

implies that cannot be negative (Blanchard & Watson, 1982, p. 7). Applying the Law of

Iterated Expectations to Equation 9, the expected bubble component at a future time can be

described as

Equation 11 ( ) ( ) .

If is negative at any time, it would grow at a rate of each period and as , ( )

, implying a negative asset price somewhere in the future (Homm & Breitung, 2012, p. 201).

14

It must then be true as Phillips et al. (2011, p. 205) point out, that ( ) , so the bubble is

a submartingale and explosive in behavior.

If there was no bubble, would equal

. If there is a bubble however, it must be expected to

grow at a rate of at least . This means that future asset prices are expected to grow at a rate

(Equation 7). This makes intuitive sense: no-one would be willing to buy an overpriced

asset if he did not believe that it would remain overpriced. Furthermore, the added investment

in the overpricing should at least be expected to grow at a rate for which it could either be

borrowed or could generate income elsewhere. If investors believe that overpriced assets will

increase at least at rate , and subsequently invest in property, the actual asset prices will indeed

rise and complete the loop of a self-fulfilling prophecy (Homm & Breitung, 2012, p. 201). The

model thus shows the workings of the ‘Greater Fool Theory’: the last buyer is always (rationally)

counting on the greater fool to sell the asset to (Kindleberger & Aliber, 2005, p. 13).

The rate at which the bubble component grows, should not exceed however, as Equation 9

shows. If ( )

, then investments would grow to profit from a return higher than

inflating the bubble component until Equation 9 holds again. The bubble ( ) is commonly

referred to as ‘rational’ because, as shown here, it is entirely consistent with A-II: agents have

rational expectations (Campbell, Lo, & MacKinlay, 1997, p. 258).

While conforming to Equation 9 and Equation 11, the actual bubble process may take several

forms. Some of these are discussed in detail in Appendix B: Time series’ graphs. It is important

to note that while rational bubble theory explains how a rational bubble can exist, it does not

explain how it emerges. It just assumes that a (strictly positive) bubble component is always

present (Equation 10).

2.6 IRRATIONALITY AND BUBBLES Traditionally, heterodox definitions of market bubble are quite colorful, like the one given by

behavioral economist Shiller (2005, p. 2), quoted in section 2.3. Kindleberger and Aliber (2005,

p. 39) use words like ‘speculative mania’, and ‘something close to mass hysteria’ to describe a

financial bubble.5

Heterodox economists view stock market bubbles as a result of overenthusiastic investors.

Especially when the market is in Minsky’s (1972, p. 102) words ‘euphoric’, these agents tend to

overestimate future dividends and therefore are willing to pay more for the stock than they

should. In other words, the agents behave irrationally (Brancaccio, 2005, p. 32).

In the (neoclassical) present value model, irrational investor behavior can be interpreted as a

rejection of the rational expectations and efficient market hypothesis, A-II. For a long time, a

deviation from fundamentals was defined as irrationality, until rational bubble theory was

developed. In the previous section, this reasoning was already exposed as a non sequitur

argument. Regrettably, it still pervades a part of the economic literature, and much of popular

literature (LeRoy, 2004, p. 785). For example, Hall draws this conclusion:

5 One could argue that behavioral finance, as practiced by Nobel Prize laureate Shiller, is not heterodox (anymore). For simplicity’s sake, I will adhere to the convention of calling all fields of economics ‘heterodox’ that are not neoclassical.

15

‘I reject market irrationality in favor of the hypothesis that the financial claims on firms command values

approximately equal to the discounted future returns.’ (Hall, 2001, p. 1)

In this thesis, I will focus on rational bubble theory for several reasons. There is no testable

model of a relation between agents’ irrationality and financial bubble. As the objective is to

determine whether there are or have been any bubbles in housing markets, the theory must be

testable. For the moment, heterodox economics is at best able to explain why and how a bubble

develops, but cannot tell from historic data if a bubble existed in a particular period. Behavioral

finance literature in particular explores the development of psychological characteristics only in

general terms and does not compare market agents’ behavior at the beginning of a boom and at

the moment the market crashes. Therefore, it cannot explain the formation and collapse of

bubbles directly (Komáromi, 2006, p. 20). According to Blanchard, ‘old’ (heterodox) theorists

use only ‘anecdotal methodology’ (Brancaccio, 2005, p. 34).

In contrast, bubble tests based on the rational bubble model have been proven to detect bubbles

that experience shows to have been bubbles. Examples of bubbles detected by methodology

based on rational bubble theory are the 1990s NASDAQ bubble (Phillips, Wu, & Yu, 2011), the

late 1990s and early 2000s dot-com bubble in the S&P500 (Phillips, Shi, & Yu, 2012), and the

residential property market bubble in Hong Kong in the 1990s (Chan, Lee, & Woo, 2001) and the

2000s (Yiu & Lu, 2012). As Friedman (Friedman, 1966, p. 15) argued, the ‘realism’ of an

assumption is not relevant. The sole criterion on which to judge an assumption is whether the

theory works, which it does if it yields sufficiently accurate predictions. This means that using

the rational bubble theory to describe market bubbles does not require one to believe the

bubble was actually caused by rational agents and rational behavior. Even if purely rational

bubbles may seem unlikely, we can still learn from studying them (Campbell, Lo, & MacKinlay,

1997, p. 206). Behavioral finance and other disciplines may still explain why the market acted

the way it did when a ‘rational’ bubble is found. This point is best explained by the following

quote of historic economists Kindleberger and Aliber.

‘Rationality is thus an a priori assumption about the way the world should work rather than a description of the

way the world has actually worked. The assumption that investors are rational in the long run is a useful

hypothesis because it illuminates understanding of changes in prices in different markets; in the terminology of

Karl Popper, it is a ‘pregnant’ hypothesis. Hence it is useful to assume that investors are rational in the long run

and to analyze economic issues on the basis of this assumption.’ (Kindleberger & Aliber, 2005, p. 40)

2.7 RESEARCH QUESTIONS This thesis will focus on these main research questions, that will be answered for the Dutch,

German and English housing markets. First, it wil answer the question:

1. Is there any evidence for bubbles in the housing markets in the 21th century?

If the hypotheses that bubbles were and are present, are supported by empirical evidence, this

thesis will also investigate when these bubbles started and when the bubbles ended, if they

ended at all. This is captured by the following research questions:

2. If bubbles exist, when did they start and when did the bubbles end (if at all)?

Answering this question will require identifying the exact periods that markets were in bubble

territory. Next, the problem is faced of detecting a bubble while it is forming. Methods of

detecting overheating of markets in an early stage can be of great importance to policy makers.

16

This goes for housing markets especially, considering the great potential impact of bubbles as

explained in section 2.2. Therefore, I pose this research questions:

3. Is it possible to have an early warning system for housing market bubbles and

crashes?

4. If such an early warning system is conceivable, what does it say on the current

price movement in the Dutch, German, and English housing markets?

17

3. RESEARCH METHOD The theoretical framework that is described in section 2.5, can be tested in several ways. First,

the method for establishing whether or not there was a bubble must be determined. Assuming a

bubble will indeed be found, a separate method is needed to assess when it started and ended.

Finally, a real-time monitoring method will be discussed to investigate if the housing market

bubble could have been detected while it was forming.

3.1 STATISTICAL METHOD: FINDING EVIDENCE OF A BUBBLE

3.1.1 VARIANCE BOUNDS TEST The first methods used to discover bubbles, were the variance bounds tests developed by Shiller

(1981) and by LeRoy and Porter (1981). These tests, explained in more detail by Gürkaynak

(2008, pp. 170-173), are based on the assertion that the variance of the ex post rational price of

an asset (based on actual income) must in absence of a bubble be larger than the variance of the

actual price at the time (based on expected future income). This is true because an

unforecastable, mean zero error term is added to the expected incomes in equation (6) to form

actual incomes, giving this new equation:

Equation 12 ∑

( ) * ,( ) -+ ∑

( ) ,

Where is the return on the asset in period , is the error term, is the actual asset

price and represents the ex post rational price under the hypothesis that no bubble exists (i.e.,

). As the variance of can be determined by the (strictly positive) variances ( ) of

and ∑

( ) , it must be true that

Equation 13 ( ) ( ).

Shiller (1981) found that for American stock prices and dividends between 1871 and 1979, the

variance of the actual real stock price was much larger than the variance of the ex post rational

price. He used this deviation from theory to criticize the present value model. Others, however,

attributed this high and unexplained volatility to asset price bubbles (Gürkaynak, 2008, p. 171).

Using a variance bounds test for bubble detection in this way has since been rejected in

economic literature. It offers no structure on the bubble component, can offer no more than an

indication of bubbles and even such an indication could be ruled out by other reasonable factors

(Yiu & Lu, 2012, p. 1).

3.1.2 EXPLOSIVE AUTOREGRESSIVE BEHAVIOR As Gürkaynak states on the perceived failure of the aforementioned variance bounds tests:

‘[i]t is clear from the discussion of the variance bounds tests that testing for the validity of the standard model

and bubbles are related but different endeavours. For a ‘test of bubbles’, a bubble should at least be in the set of

alternatives when the test rejects the standard model.’ (Gürkaynak, 2008, p. 173)

In other words, variance bounds tests do not investigate a positive bubble theory. However,

these bubbles also have theoretical properties that can be included in the model as to improve

its accuracy and power. Furthermore, the variance bounds test only tests whether actual data

conform to a presupposed model. Significant deviations from this model are then ascribed to

bubbles. This method therefore precludes the possibility that there are fundamentals that are

18

observed by market agents but not by the researcher. He thus risks ‘finding’ a bubble in a data

set, where the ‘excess variance’ in his time series is actually caused by changes in unobserved

fundamentals (Hamilton & Whiteman, 1985, p. 354).

Diba and Grossman (1988a), aware of this problem, included unobserved fundamentals in their

model. To the standard definition of the fundamental price in the Present Value Model (Equation

6), they added a variable , that has the property of being stationary. This variable represents

all variables other than rental income that may influence the asset prices. For the housing

market, these fundamental influences could be changes in tax-laws and money demand

disturbances. The new fundamental price equation now reads:

Equation 14 ∑

( ) ,( ) -.

By adding variable , Diba and Grossman (1988a) mainly show that by looking for explosive

behavior instead of comparing price levels to the fundamental’s levels, other fundamentals do

not distort bubble detection as long as these other fundamentals do not behave explosively. In

this way, the empirical method used in this thesis is more robust than many error correction

models (ECM, section 2.1.1) that rely on long-term average ratio of price levels to fundamentals’

levels to determine an asset’s fundamental value. Furthermore, even if an unobserved

fundamental should behave explosively, that would only affect the detection of bubbles if this

fundamental affects the relationship between rent and house prices. Many fundamentals other

than rent, however, are expected to affect both house prices and rent symmetrically (section

2.4.3) (Brunnermeier & Julliard, 2006, p. 9).

In the absence of bubbles, if rental incomes ( ) are stationary in levels, house prices will be

equal to market fundamentals and should also be stationary in levels; if rental incomes are

stationary in th differences, house prices should be stationary in th differences (Gürkaynak,

2008, p. 177). On the other hand, a bubble is an explosive process that is self-sustaining

(Equation 11) and Diba and Grossman (1988a) show that the bubble component is non-

stationary regardless how many differences are taken. A clear method for testing for bubbles

now presents itself. Assuming that, at least in behavior, series of expected fundamentals equal

the real ex post fundamentals, and that is stationary the following is true.

1 If house prices are stationary when differenced the same number of times required

to make the rental incomes stationary, no bubble exists.

2 If house prices are non-stationary while at the same differences-level rental incomes

are stationary, this must be due to the existence of a bubble.

3 If both the house price series and the rental incomes series are non-stationary, but

both time series are co-integrated, the fundamental relation between rent and house

price is still present so it must be concluded that there is no bubble.

Not long after this apparent break-through method was developed, Evans (1991) showed it had

one serious practical flaw: the test gave false negative outcomes when confronted with

periodically collapsing bubbles. When the chance of a bubble collapsing is larger, over a long

period of time, the asset price series may not be significantly distinguishable from a random

walk or from being stationary. In other words, when one or more bubbles start and end within a

sample, this method runs the risk of a type II error, i.e. not rejecting a false H0-hypothesis.

19

3.1.3 FORWARD RECURSIVE AUTOREGRESSIVE TEST Since Evans’ critique, methods have been developed to mitigate the flaws of this model, while

maintaining the assertion that stationarity and cointegration properties of the time series of the

asset price and its fundamentals can be used to test for a bubble. Homm and Breitung (2012)

tested several sophisticated methods in this area for their power of detection by confronting

them with simulated and real time series with bubbles. They concluded that ‘the Phillips, Wu,

and Yu (2011) test is much more robust against multiple breaks than all other tests.’ For this

reason, this test has also been adopted by Kivedal (2012). As independent research convincingly

shows the test developed by Phillips, Wu, and Yu (2011) to be the most robust, I will also adopt

their methodology (with a few modifications).

When a bubble occurs in the housing market, the house prices will behave explosively. Actual

house prices include a bubble component (Equation 10) that is explosive in nature by definition

(Equation 11). Phillips, Wu and Yu (2011) propose using a right-tailed unit root test to test this

explosive behavior. This test will therefore first be conducted on time series of house prices in

the Netherlands, Germany, and England. If such behavior is observed, it must first be excluded

that the fundamental variable (i.e. rent, section 2.4.3) is explosive and is the explosive behavior

of the price series. The same right-tailed unit root test is therefore applied to that time series. If

the tests show that house prices behave explosively while the rent series is either stationary or

an I(1) series (the right-tailed test does not distinguish between the two), a bubble exists.

To escape the ‘pitfall’ mentioned by Evans (1991), a forward recursive test is used. This means

that tests are first applied to a small time interval or window of the entire sample and are

consecutively performed on a growing interval of the sample. In this way, a collapsing bubble

that inflates again within the whole sample, is still detected. For each time series (house prices

and rental income), the method applies the Augmented Dickey-Fuller ( ) test. This means the

following autoregressive specification is estimated by least squares:

Equation 15 ∑ (

),

( ) ∑ (

)

where is the dependent variable, representing either the logarithmic real house price series

( ( )) or the logarithmic real rental income series ( ( )). denotes that the error terms

are normally and independently distributed. Furthermore, denotes the lag parameter. For

every test performed, an optimal number of lags must be included. This optimum is determined

by the Bayesian Information Criterion (BIC) that Schwarz (1978) developed with a maximum of

12. Note that the regression model includes a constant but no trend. The model thus assumes

that the time series exhibit a non-zero constant and no trend. After visual inspection of the

series, the model may have to be adapted to better fit the particular series tested. As it is not

economically plausible that either house prices or rents would fluctuate or wander around zero,

the model should include a constant. House prices of rents series could exhibit trend, however. If

that is the case, the trending series should be tested according to the following model that

includes a trend variable ( ) (Hill, Griffiths, & Lim, 2011, p. 487):

Equation 16 ∑ (

)

( ) ∑ (

).

20

To detect explosive behavior, the hypothesis of a random walk model (H0: ) is tested

against the alternative hypothesis of an explosive root (H1: ) for each time series.

In forward recursive regressions, the model (Equation 15) is estimated repeatedly, implying a

sequence of -tests for different windows of the sample data (Figure 6). Here, is used to

describe an interval within the dataset relative to the size of the entire dataset and can therefore

be any value from 0 to 1. This process of repeated regressions starts with the smallest time

interval of the entire sample that is just large enough so that a regression is still possible: . The

(chronological) starting point of any window is referred to as and the end point is called .

and are numbers that represent the size of the time interval that starts at 0, relative to the

entire sample, at which the window starts. In a forward recursive regression sequence, the

starting point ( ) is fixed at 0. The end point is therefore equal to the window [ ] and takes

the following values in the sequence of tests: , -. After a test on the smallest interval has

been performed, subsequent tests add one observation each time until the entire sample is used,

and .

FIGURE 6: SCHEMATIC DEPICTION OF -WINDOWS IN THE -TEST, WHERE FOR THE ENTIRE SAMPLE: , , -, AND

= .

The -test τ-statistic6 generated by each test can be expressed formally:

Equation 17 ∫

(∫

) ,

where is a standard Brownian motion. The test statistic used to test whether or not there is a

bubble, is denoted as:

Equation 18

[ ]

[ ]∫

(∫

) .

This test statistic is the supremum of the series of generated -statistics for varying values of

and shall henceforth be referred to as . In this instance, the supremum of the series is

equal to its maximum. The highest test result from the repeated process ( ) must therefore

be tested against the right-tail critical values that are specific to the test, the sample size and the

tested autoregressive model. If it is larger than these values, the underlying time series is

explosive and the alternative hypothesis ( ) is confirmed.

6 The Augmented Dickey-Fuller test generates a (tau) statistic instead of a ‘normal’ -statistic. If the -hypothesis is true, is a random walk and has the property that variance increases with the sample size. The usual -statistic is altered by this increasing variance and is therefore called the -statistic (Hill, Griffiths, & Lim, 2011, p. 485).

21

From running these forward recursive -tests on the time series for house prices and rent,

four combined scenarios are possible:

Scenario I for the house price series and for the rent series;

Scenario II for the house price series and for the rent series;

Scenario III for the house price series and for the rent series;

Scenario IV for the house price series and for the rent series.

The results are interpreted as follows. Scenario I states that both time series are non-explosive

and confirms that there is no bubble in the housing market. Scenario IV implies that there is a

bubble. The explosive behavior in the house price series is not caused by the rent series, and is

not caused by unobserved fundamentals as they are assumed to be stationary (section 3.1.2).

The second scenario (Scenario II) should not occur within the theoretical framework

(specifically, Equation 6) of this thesis. The fundamental part of the house price series is

determined by the rental income series, so explosive behavior in the latter series should also

make the first series behave explosively. Therefore, this scenario is very unlikely. However, if the

scenario is found to be true, there is much reason to reconsider the theory and the research

method used. Scenario III is inconclusive: both series are explosive, so explosive behavior of the

house price series is at least partially caused by explosive behavior of the rent series. Logically,

this does not preclude the possibility that the bubble component of the house price (see

Equation 10) causes further explosive behavior and a bubble exists. Therefore, other methods

must be used to investigate this. It is possible to check for cointegration, as Diba and Grossman

(1988b) did, but in a forward recursive way to avoid the pitfall noted by Evans (1991).

Cointegration is then interpreted as establishing that the explosive behavior of the house price

series is exclusively caused by the rental incomes, and there is no room for a bubble. It is also

possible to compose a time series of the log real price-rent differential. This method is used by

Phillips, Shi, and Yu (2012) and by Yiu and Lu (2012). If this ratio is explosive, there is a bubble.

3.2 A METHOD OF DATE-STAMPING BUBBLES

3.2.1 A BUBBLE WITHIN THE SAMPLE The method laid out so far cannot date stamp any bubble found. It cannot tell when the bubble

began, and when it deflated so that no bubble remained. Phillips, Wu, and Yu (2011) suggest

using the strand of -statistics of the time series that has been established to contain a

bubble. When they are tested against the right-tail critical values of the asymptotic distribution

of the Augmented Dickey-Fuller -statistic, the starting and end date (if the bubble has ended)

can be determined. The bubbles is said to have started on the date when the -statistic is

first equal to or larger than the critical value. The bubble collapses on the date when the -

statistics is again (for the first time after the starting date) smaller than the critical value.

According to the rational bubble theory, the collapse of a bubble, or the market crash coincides

with an immediate return to fundamental value. The reason is that a bubble needs to ‘feed’ on its

own explosiveness as Equation 11, Equation A.1, and Equation A.2 show. Market agents will only

buy into a bubble if it is expected to grow at rate (section 2.5.2). Thus, the bubble’s collapse

puts an end to any overvaluation.

22

The start and ending of a bubble can be represented mathematically:

Equation 19 { ( )} ,

{ ( )} ,

where is the window representing the bubble’s starting date and is the window

representing the end date of the bubble. is the infimum or (in this case) smallest value of

[ ] or , - for which the condition stated in the brackets is true. The condition states

that the -statistic is equal to or larger than its asymptotic critical value with significance

level . Phillips et al. (2011) assert that this significance level should approach zero

asymptotically as in order to prevent a type I error (i.e. rejection of a true H0-hypothesis).

Therefore, following them, I will make the significance level dependent upon according to the

formula (Phillips, Wu, & Yu, 2011, pp. 207-208):

Equation 20

( ( ))

.

3.2.2 DATE-STAMPING MULTIPLE BUBBLES Using a strand of -statistics to date stamp bubbles, has a serious flaw. The method cannot

accurately detect and date stamp multiple bubbles within the sample, as Phillips et al. (2012)

show. This makes intuitive sense. The start of a bubble is defined as the moment the time series

is found to significantly behave explosively. Explosive behavior is tested by recursive

Augmented Dickey-Fuller tests and each added observation is assessed in the light of all

previous observations. A second bubble in the sample is harder to detect as the detection of

explosive behavior at that time is distorted by the first bubble. Note that this problem is not

present when a sample’s first bubble has not ended at the end of the dataset. For each housing

market that exhibits a bubble that collapses within the sample, an additional method is

necessary to check for possible following bubbles.

Phillips et al. (2012) assert such a method, which they have named the generalized sup ADF test

( ). Where the -test performs repeated tests on expanding samples that have a fixed

starting point (0) and an increasing end ( , -), the -test also varies the starting

point. For each starting point between 0 and , it performs a complete -test (Figure

7). As with the -test, the starting point is referred to as As the minimum window size

must be observed, the starting points of -tests within the -test range from 0 to

( ). The end points ( ) for each -test are in the range , -. Therefore, for

the entire -test, the end points range from to 1. Note that, as explained in section 3.1.3,

the starting and end ‘points’ are actually the size of the time interval between 0 and the

observation at which the test window starts or ends. The -test generates a sequence of

-statistics and every -statistic is the supremum of a strand of -statistics. Of all

-statistics generated by the -test, the -statistic is the supremum, or the

statistic with the maximum value. This statistic is expressed formally:

Equation 21

, -

, -

, -

, -

∫

(∫

) .

Because the -test has a moving starting point that can ‘pass over’ the first bubble, a

second bubble can be detected just as easily as the first.

23

FIGURE 7: SCHEMATIC DEPICTION OF -WINDOWS IN THE NORMAL -TEST, WHERE FOR THE ENTIRE SAMPLE: , -,

, -.

In order to accurately date stamp one or more bubbles within a sample, Phillips et al. (2012)

suggest applying the -test in reverse order. Instead of performing a sequence of -

tests, they run backward sup ADF ( ) tests. For each -test performed within this

test, is fixed and , -. The -test is performed for each value of , is also

executed in reverse order, performing backward -tests ( ( )) for each

⌈ ⌉. The sequence of sample windows that ( )-tests are conducted within a

-test, is depicted schematically in Figure 8.

Analogous to Equation 19, starting and ending dates for a (first) bubble are denoted:

Equation 22 , -{ ( ) ( )} ,

, -{ ( ) ( )}

where is the sample size representing the bubble’s starting date and is the sample size

representing the end date of the bubble. is the infimum or (in this case) smallest value of

[ ] and , - for which the condition stated in the brackets is true. So, the bubble’s

start is set on the chronologically first date that has a corresponding -statistic that is

greater than the critical value for its . When that statistic further on in time becomes smaller

than the sequence of critical values, the corresponding date is identified as the end of the bubble.

The critical values ( ) for the -statistics cannot be generated by a convenient

formula, like the critical values ( ) for the recursive -test (section 3.2.1). Instead,

they are generated by successive Monte-Carlo simulations for every value of ( , -). For

this purpose, the level of significance ( ) is set at 5 percent. Admittedly, this level of

significance is rather arbitrary, and the level chosen should depend on weighing the risk of a

Type I error (higher at a lower level of significance) and the risk of a Type II error (higher at a

higher level of significance). When making policy decisions, not detecting an emerging bubble

(Type II) might be more harmful than a ‘false alarm’ and a (lower) significance level of 10

percent may be more appropriate.

24

FIGURE 8: SCHEMATIC DEPICTION OF -WINDOWS IN THE -TEST, WHERE FOR THE ENTIRE SAMPLE: , -, , -,

AND .

In short, two methods will be used in this thesis to date-stamp housing bubbles. First, the -

test is applied to each house price series (Figure 6). If this test finds a bubble that starts within

the sample but does not end, the bubble detection is complete. If, however, an ‘complete’ bubble

is detected with the -test that has a beginning and an ending, further testing is necessary.