FIXED ASSETS MANAGEMENT POLICY MARCH 2015 -...

25

1 UNIVERSITY OF NAIROBI FIXED ASSETS MANAGEMENT POLICY MARCH 2015

Transcript of FIXED ASSETS MANAGEMENT POLICY MARCH 2015 -...

1

UNIVERSITY OF NAIROBI

FIXED ASSETS MANAGEMENT

POLICY

MARCH 2015

2

VISION

A world-class university committed to scholarly excellence MISSION To provide quality university education and training and to embody the aspirations of the Kenyan people and the global community through the creation, preservation, integration, transmission and utilization of knowledge CORE VALUES

Freedom of thought and expression;

Innovativeness and creativity; Good governance and integrity; Team spirit and teamwork; Professionalism; Quality customer service;

Responsible citizenship; National cohesion and inclusiveness.

3

Foreword

The University of Nairobi is the premier institution of higher learning in the country.

Having been established as the Royal Technical College in 1956, the institution morphed

into the Royal College, Nairobi in 1963, then a constituent college of the University of

East Africa. It eventually became the University of Nairobi in 1970, and for more than a

decade was the only University in Kenya.

Within the duration of its existence, the University has acquired assets in various forms,

some fixed and others moveable. Though they have largely been properly taken care of

and well kept, records of the assets have been kept in an ad hoc manner. A register of

the assets has also been kept but this has not been guided by any policy.

It is therefore important that the University prepares a policy to guide the management

of its assets, targeting mainly the fixed assets. The main purpose of the policy is to

track the cost of the assets, how they are maintained, the depreciation levels and how

they can be disposed.

In particular, the assets management policy will guide in recording and capitalization of

the assets, the methods of depreciation and impairment of the assets, timing for

valuations and revaluations and procedures for retirement, write off and disposal of the

same.

Whereas the core business of managing this process and implementing the assets

management policy will fall in the Finance and Estates Departments, all units of the

University have a responsibility to ensure there is proper management and utilization of

the assets under their care. This includes keeping an updated inventory of the assets

and their current state.

I therefore call upon all Unit heads to familiarize themselves with the contents of this

policy and ensure its proper implementation in all the Units across the university.

Peter M. F. Mbithi, EBS,PhD Vice Chancellor & Professor of Veterinary Surgery

4

Preface

The University has a significant investment in fixed assets such as land, buildings and

equipment, which are used to carry out its core mandate of teaching, learning and

research. Though these assets have been properly taken care of and well kept, the

records of the assets have been kept in an ad hoc manner. The University

administration therefore found it prudent to develop a policy to guide in the

management of the fixed assets register.

The Vice Chancellor therefore appointed a Fixed Asset Register Automation committee

with the following mandate: to identify and tag the University’s moveable assets;

valuation of the identified assets; coding, processing and activating the assets module

in Financial Information Management System (FIMS); and ultimately develop the

University of Nairobi fixed asset management policy.

The purpose of this policy is to ensure that the University’s fixed assets are acquired,

safeguarded, accounted for, controlled and disposed of in accordance with the Laws of

Kenya, International Financial Standards and Generally Accepted Accounting Principles.

This Policy is designed to ensure a uniform understanding of capitalization of the

University’s fixed assets and the efficient management of the fixed assets register.

The Policy addresses among others the following issues related to fixed assets:

definition, categorization, additions, tagging, disposal or transfer, depreciation,

inventory and capital budgeting of fixed assets.

In discharging its mandate the committee held several meetings and consultations with

various stakeholders. In this regard, the Committee wishes to thank the Vice-Chancellor

and the University Management Board for their support and guidance in preparing this

Policy document. The committee also wishes to thank the management of Kenya Ports

Authority, Kenya Airways and Kenya Power Limited for the support in the preparation of

this Policy document.

Peter K. Busienei Deputy Finance Officer (G) & Chairman, Fixed Assets Register Automation Committee

5

TABLE OF CONTENTS

Foreword ...................................................................................................................................................... 3

Preface ......................................................................................................................................................... 4

Abbreviations ............................................................................................................................................... 7

Definition of Terms ..................................................................................................................................... 8

Rationale ...................................................................................................................................................... 9

1.0 Introduction ........................................................................................................................................ 10

1.1 Preamble ..................................................................................................................................... 10

1.2 Policy Statement ........................................................................................................................ 10

1.3 Policy Objectives ........................................................................................................................ 11

2.0 Responsibility for Asset Management ............................................................................................ 11

3.0 Classification of Fixed Assets and Codes ....................................................................................... 13

3.1 Assets Categorization ................................................................................................................ 13

3.2 Asset Coding ............................................................................................................................... 14

4.0 Capitalization ...................................................................................................................................... 15

4.1 Capitalization Procedure ........................................................................................................... 15

4.2 Capitalization Guiding Principles .............................................................................................. 15

5.0 Asset Valuation and Revaluation ..................................................................................................... 16

5.1 Valuation of Assets .................................................................................................................... 17

5.2 Revaluation of Assets ................................................................................................................ 17

6.0 Donated Assets .................................................................................................................................. 18

7.0 Capital Budget .................................................................................................................................... 18

8.0 Asset Tagging .................................................................................................................................... 18

9.0 Depreciation ....................................................................................................................................... 19

9.1 Depreciation Rates ..................................................................................................................... 19

6

9.2 Posting of Depreciation ............................................................................................................. 19

10.0 Inventory of Fixed Assets .............................................................................................................. 20

11.0 Movement of Fixed Assets between the Units ............................................................................ 20

12.0 Disposal of Fixed Assets ................................................................................................................. 20

12.1 Asset Impairment .................................................................................................................... 20

12.2 Asset Disposal .......................................................................................................................... 20

13.0 Monitoring and Evaluation ............................................................................................................. 21

14.0 Review and Revision of the Policy ................................................................................................ 21

MEMBERSHIP ............................................................................................................................................ 22

APPENDIX I................................................................................................................................................ 23

APPENDIX II .............................................................................................................................................. 24

APPENDIX III............................................................................................................................................. 25

7

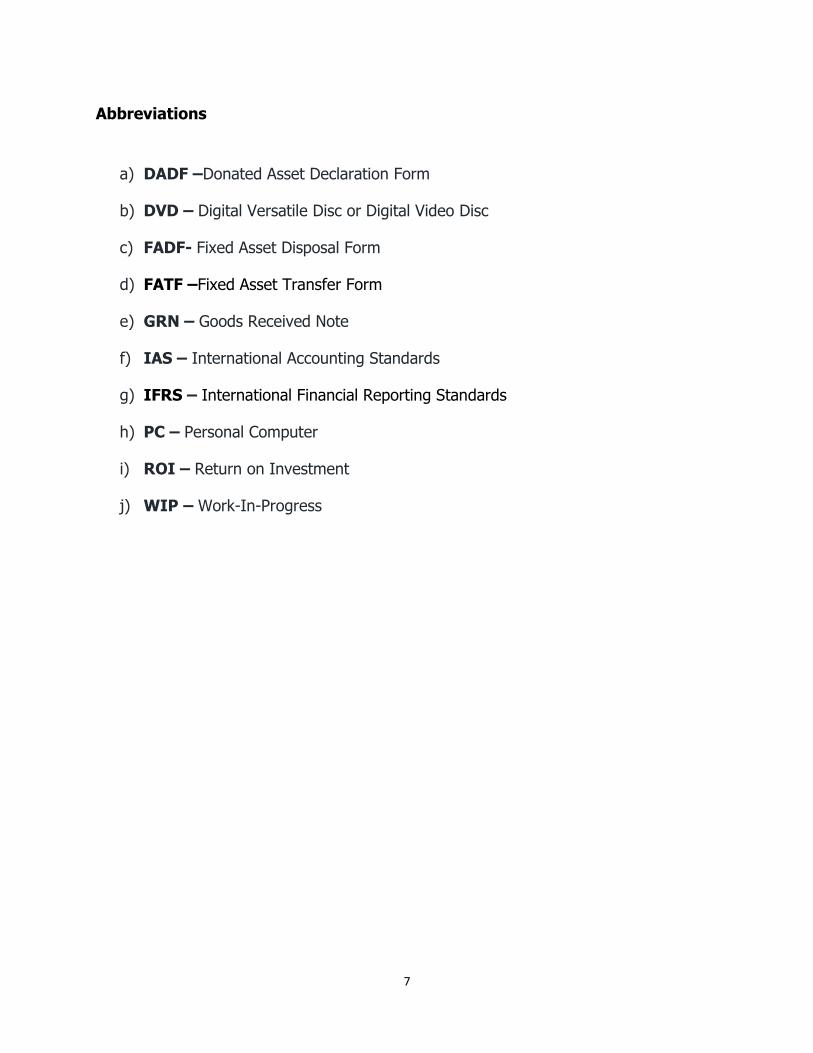

Abbreviations

a) DADF –Donated Asset Declaration Form

b) DVD – Digital Versatile Disc or Digital Video Disc

c) FADF- Fixed Asset Disposal Form

d) FATF –Fixed Asset Transfer Form

e) GRN – Goods Received Note

f) IAS – International Accounting Standards

g) IFRS – International Financial Reporting Standards

h) PC – Personal Computer

i) ROI – Return on Investment

j) WIP – Work-In-Progress

8

Definition of Terms

a) Asset: this is an economic resource owned by an entity that generates benefits or service which will flow to the entity and whose costs of fair value can be measured reliably

b) Fixed Asset/Capital Asset: All assets which cannot easily be converted into cash and which are usually held for a long period of time, including land, buildings, equipment and furniture

c) Coding: is generating and assigning a number to an asset for identification and classification.

d) Tagging: is the process of numbering and labeling fixed assets and allow the

tracking of their movement from location to location.

e) Asset Impairment: is an abrupt decrease of the fair value of an asset due to physical damage, significant changes in economic, market or legal environment, obsoleteness, or idleness of the asset.

f) Capitalization: is the recognition of expenditure of an Asset in the Financial Asset Register

g) Depreciation: this is a non-cash expense that reduces the value of an asset as a result of wear and tear, age or obsolescence

h) Disposal: It is the sale, transfer of ownership or destruction of surplus or obsolete assets

i) Revaluation: the upward or downward adjustment of the net book value of a fixed asset to account for major changes in the fair market value of the asset.

9

Rationale

The University of Nairobi has gone through tremendous changes over the years in the management of its affairs. It is also evident that the University is moving away from conventional systems of management towards embracing modern management techniques, including results-based performance and quality management systems.

The University’s Vision is anchored on world class excellence in service delivery. To

support this Vision, there is need for effective management of the University fixed

assets. This provides the rationale for developing and implementing a comprehensive

fixed assets management policy.

This policy is designed to support the University’s business as spelt out in the 2013-

2018 Strategic Plan, Statutes as well as other policy documents and guidelines. One

of the strategic objectives in the University’s Strategic Plan is “to manage the

University efficiently”. This policy will assist the University in achieving this strategic

objective.

The Finance and Estates departments in the University are charged with the

responsibility of ensuring that the fixed assets register is managed effectively and

used prudently. These assets include land, equipment, ICT resources, furniture,

motor vehicles, physical facilities, plant and machinery.

This policy defines methods and procedures for recording, acquiring, movement,

classification, tagging, capitalization, revaluation, depreciation, retirement and

disposal of fixed assets. It has been developed in compliance with International

Financial Standards to ensure that the University assets are managed prudently and

accounted for.

10

1.0 Introduction

1.1 Preamble

Except to the extent to which the context may otherwise require, this policy shall be construed in accordance with the following provisions:

a) This policy shall apply to fixed assets acquired with funding originating

from the University, the government or other external sources, and by gift or loan.

b) Any word or expression denoting any gender shall include both genders;

c) Words denoting the singular only may also include the plural, and vice

versa, where the context requires;

d) This policy shall apply only in respect of management of the University's fixed assets specifically land, buildings, plant, equipment, furniture, software, goodwill and other assets of an enduring nature which are owned and controlled by the University;

e) Where the term asset is used in this policy, it refers to fixed asset whose economic benefit to the University exceeds one year.

1.2 Policy Statement

The purpose of this policy is to define the guidelines, regulations and procedures governing the control and reporting of fixed assets. This includes accountability over the assets, meeting financial reporting needs, and generating asset management information.

It is intended to assist the University in implementing and maintaining an effective fixed assets control program. The implementation of an effective and accurate process for tracking fixed assets is necessary for several reasons:

a) The University requires to track asset cost, depreciation and disposal.

Assets to be depreciated will be categorized and assigned a depreciation life.

b) The University also uses asset records for insurance purposes. In the event of a loss, it is necessary to have an accurate record of the University assets to ensure comprehensive insurance coverage.

c) Most importantly, it is for accountability reason. It is important to have a policy that helps to account for the use of University funds.

11

1.3 Policy Objectives

This document undertakes to describe standard policies required for recording new and existing assets, changes in assets and the methodology of record keeping. Moreover, it is intended to provide procedures to assist the University in safeguarding, accounting for and disposal of assets.

The objectives of this policy are to ensure that:

a) Procedures for recording and capitalization of fixed assets have been

established; b) Methods of depreciation, impairment, diminution and amortization of

fixed assets have been established; c) Timings for revaluations and accounting in respect of the fixed assets

have been determined and documented; d) Procedures for write off and disposal of fixed assets have been

established; and e) The University assets are accounted for in compliance with international

Financial Standards.

2.0 Responsibility for Asset Management

The responsibilities of various key offices in the enforcement of this policy

are as follows:

2.1 Vice Chancellor

The Vice Chancellor shall have overall responsibility for oversight, monitoring, implementation and enforcement of this policy and related regulations or procedures.

2.2 College Principals

College Principals shall be responsible for familiarizing themselves with and sensitizing staff within their Colleges on this Policy. They will also ensure that:

Current inventory of all fixed assets within the College is properly maintained;

They notify the Estates Manager and the Finance Officer whenever fixed assets are acquired, transferred, donated, impaired, stolen, lost or otherwise disposed;

Identify and report to the Estates Manager and Finance Officer any surplus assets which are useable but need not be in their college, or which is beyond economic repair and needs to be disposed of; and

12

Assets under their custody are secured, handled with care and used for official University business only.

2.3 Heads of Department/Units

Heads of Units in Central Administration and SWA shall be responsible for familiarizing themselves with and sensitizing staff within their Units on this Policy. They will also ensure that:

Current inventory of all fixed assets within their Units are properly maintained;

They notify the Estates Manager and the Finance Officer whenever fixed assets are acquired, transferred, donated, impaired, stolen, lost or otherwise disposed;

Identify and report to the Estates Manager and Finance Officer any surplus assets which are useable but need not be in their Units, or which is beyond economic repair and needs to be disposed of; and

Assets under their custody are secured, handled with care and used for official University business only.

2.4 Estates Manager

The Estates Manager shall be responsible for custody, management and control of assets in the University.

2.5 Finance Officer

The Finance Officer shall be responsible for coordinating asset audits and physical inventories with the Estates Manager as well as recording capital asset acquisitions, transfers and disposals. Where necessary, the Finance Officer shall evaluate, review or adapt the policy or the implementation of the policy, in order to improve assets management and comply with changes in the financial reporting standards.

2.6 Senior Accountant (Capital Section)

The Senior Accountant Capital Section shall familiarize himself with this Policy and also ensure that:

Current inventory of all fixed assets within the University are properly maintained;

Changes are effected and notify the Estates Manager and the Finance Officer whenever there are changes in the fixed assets register; and

Assets in the University are secured.

13

3.0 Classification of Fixed Assets and Codes

3.1 Assets Categorization

Fixed assets shall be classified as follows:

NO

CATEGORY SUB CATEGORY

ITEM ID CODE ITEM

SUB-CODE

SUB-ITEM

1 001 Land 010 Lease Hold 001-010

020 Free Hold 001-020

2 002 Buildings

010 Office Blocks 002-010

020 Lecture Theatres 002-020

030 Laboratories 002-030

040 Workshops 002-040

050 Hostels 002-050

060 Residential Houses 002-060

070 Others 002-070

3 003 Furniture & Fittings

010 Chairs 003-010

020 Sofa Sets 003-020

030 Tables 003-030

040 Desks 003-040

050 Beds 003-050

060 Mattresses 003-060

070 Cabinets/Bookshelves 003-070

080 Counters 003-080

090 Others 003-090

4 004 Plant & Equipment

010 Fixed Machines 004-010

020 Movable Machines 004-020

030 Trailers 004-030

040 Safes 004-040

050 Fridges/ Freezers 004-050

060 Water Dispensers 004-060

070 Cold Rooms 004-070

080 Water Pumps 004-080

090 Air Conditioners 004-090

100 Irrigation Equipment 004-100

110 Water Tanks 004-110

120 Cookers 004-120

130 Telephone Equipment 004-130

140 Others 004-140

14

NO

CATEGORY SUB CATEGORY

ITEM ID CODE ITEM

SUB-CODE

SUB-ITEM

5 005 Motor Vehicles

010 Buses 005-010

020 Lorries 005-020

030 Pick-Ups 005-030

040 Tractors 005-040

050 Motor Boats 005-050

060 Ambulances 005-060

070 Vans 005-070

080 Cars 005-080

090 Motor Cycles 005-090

100 Water Bowsers 005-100

110 Others 005-110

6

006 Computers and ICT Infrastructure

010 Desktop Computers 006-010

020 Laptops 006-020

030 Servers 006-030

040 Printers 006-040

050 Scanners 006-050

060 Copiers 006-060

070 Projectors 006-070

080 Network Cabling 006-080

090 TVS 006-090

100 Others 006-100

7 007 Academic Attire

010 Gowns 007-010

020 Hoods 007-020

030 Caps 007-030

8

008 Intangible Assets

010 ICT Software / Databases 008-010

020 Patents 008-020

030 Copy Rights 008-030

040 Trademarks 008-040

050 Licenses 008-050

3.2 Asset Coding

The code/tag shall be segmented as follows:

a) Segment 1- Shall take 3 characters identifying the institution i.e

UON

b) Segment 2- Shall take 7 characters as follows:

15

i. 2 Characters to identify the College/Central administration/

SWA.

ii. 3 Characters to identify Central departments/ faculty/ school

/ institute / centre.

iii. 2 Characters to identify unit/ teaching departments/ section.

c) Segment 3- Shall take 3 characters identifying the cost centre.

d) Segments 4- Shall take 6 characters

i. 3 characters for main category

ii. 3 characters for sub-category

e) Segment 5- shall take 4 characters identifying the item.

Example:

A printer in FIMS Office Finance department shall be coded and tagged as

follows:

CODE: UON/07-010-30/020/006-040/0554

TAG: UON/CAD-FIN-FIMS/006-040/0554

Where 0554 is the printer number, which is auto generated.

4.0 Capitalization

4.1 Capitalization Procedure

a) This procedure involves establishing criteria and/or threshold(s) for

classifying an item as a fixed asset.

b) Appropriate capitalization thresholds for fixed assets are to be

determined by the University using reasonable and consistent

rationale.

c) The University primarily acquires assets either as complete units ready

for use (direct acquisition) such as vehicles, computers, equipment

and projectors or through project expenditure for assets like buildings

and roads (indirect acquisition).

4.2 Capitalization Guiding Principles

The capitalization thresholds shall be as follows:

16

a) Land, buildings and motor vehicles shall be capitalized regardless of

the cost.

b) Asset additions, enhancement, repair, replacement or expansion

expenditures that enhance or extend the useful economic life of the

assets shall be capitalized.

c) Work in progress costs shall be closed out and capitalized into the

appropriate assets classification when a project is complete,

acceptable and placed into use.

d) Expenditure incurred in acquiring Information Technology equipment

e.g. laptops, notebooks, desktop computers, servers, printers shall be

capitalized. Where there is additional expenditure to improve/upgrade

existing equipment, the expenditure shall be capitalized.

e) Furniture and equipment acquired with a value of more than KSh. 10,000.00 and expected lifespan of five years shall be capitalized. However equipment of a household nature e.g microwaves, fridges, hotplates, utensils acquired for use in administrative offices will not be capitalized

f) Assets whose value is below KSh. 10,000 are expensed in the fiscal year of purchase and are not capitalized.

g) When assets are capitalized, the University shall assign an asset number and arrange for the asset to be tagged with the asset number for control purposes.

h) Costs incurred to keep a fixed asset in its normal operating condition that does not extend the original useful life of the asset or increase the asset’s future service potential are not capitalized. These costs are expensed as repairs or maintenance.

5.0 Asset Valuation and Revaluation

The responsibility to undertake valuation and revaluation of assets lies with the Finance Officer and the Estates Manager.

The objectives of valuation are:

i) To ascertain fair values of fixed assets for accounting purposes for sale, disposition or other purposes;

ii) To facilitate reconciliation of the fixed asset register and the physical inventory of assets

iii) Establish replacement costs for purposes of insurance and general replacement of assets

17

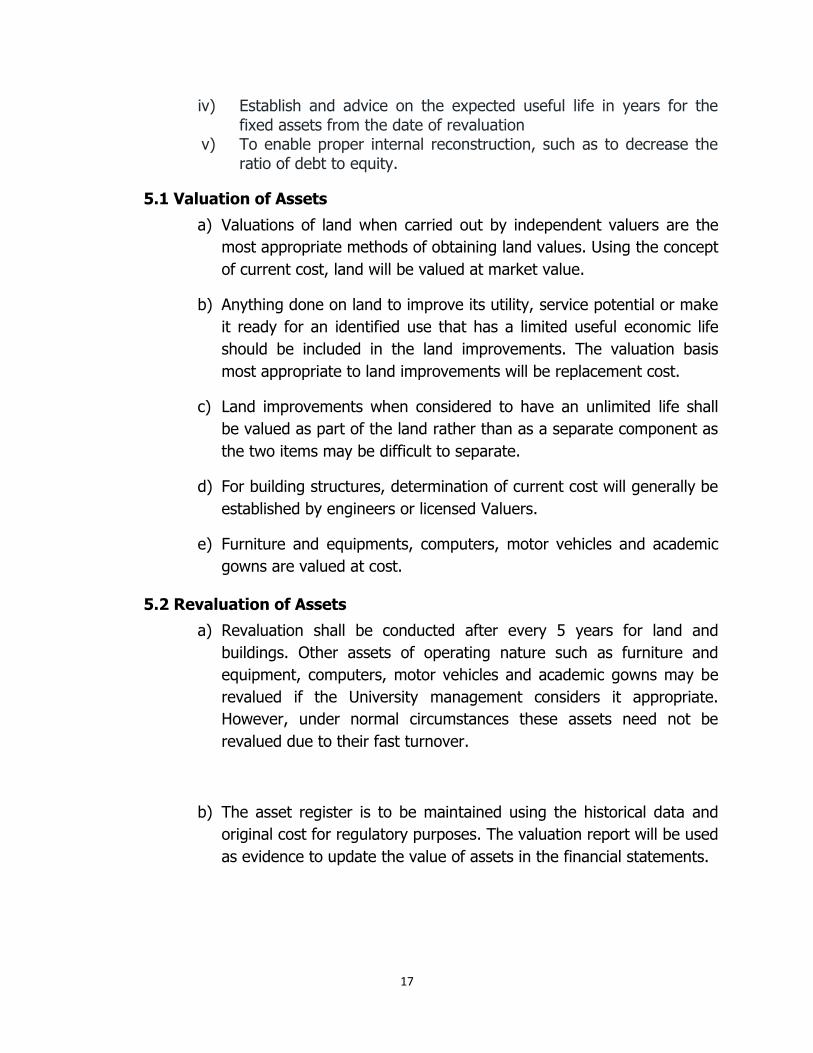

iv) Establish and advice on the expected useful life in years for the fixed assets from the date of revaluation

v) To enable proper internal reconstruction, such as to decrease the ratio of debt to equity.

5.1 Valuation of Assets

a) Valuations of land when carried out by independent valuers are the

most appropriate methods of obtaining land values. Using the concept

of current cost, land will be valued at market value.

b) Anything done on land to improve its utility, service potential or make

it ready for an identified use that has a limited useful economic life

should be included in the land improvements. The valuation basis

most appropriate to land improvements will be replacement cost.

c) Land improvements when considered to have an unlimited life shall

be valued as part of the land rather than as a separate component as

the two items may be difficult to separate.

d) For building structures, determination of current cost will generally be

established by engineers or licensed Valuers.

e) Furniture and equipments, computers, motor vehicles and academic

gowns are valued at cost.

5.2 Revaluation of Assets

a) Revaluation shall be conducted after every 5 years for land and

buildings. Other assets of operating nature such as furniture and

equipment, computers, motor vehicles and academic gowns may be

revalued if the University management considers it appropriate.

However, under normal circumstances these assets need not be

revalued due to their fast turnover.

b) The asset register is to be maintained using the historical data and

original cost for regulatory purposes. The valuation report will be used

as evidence to update the value of assets in the financial statements.

18

6.0 Donated Assets

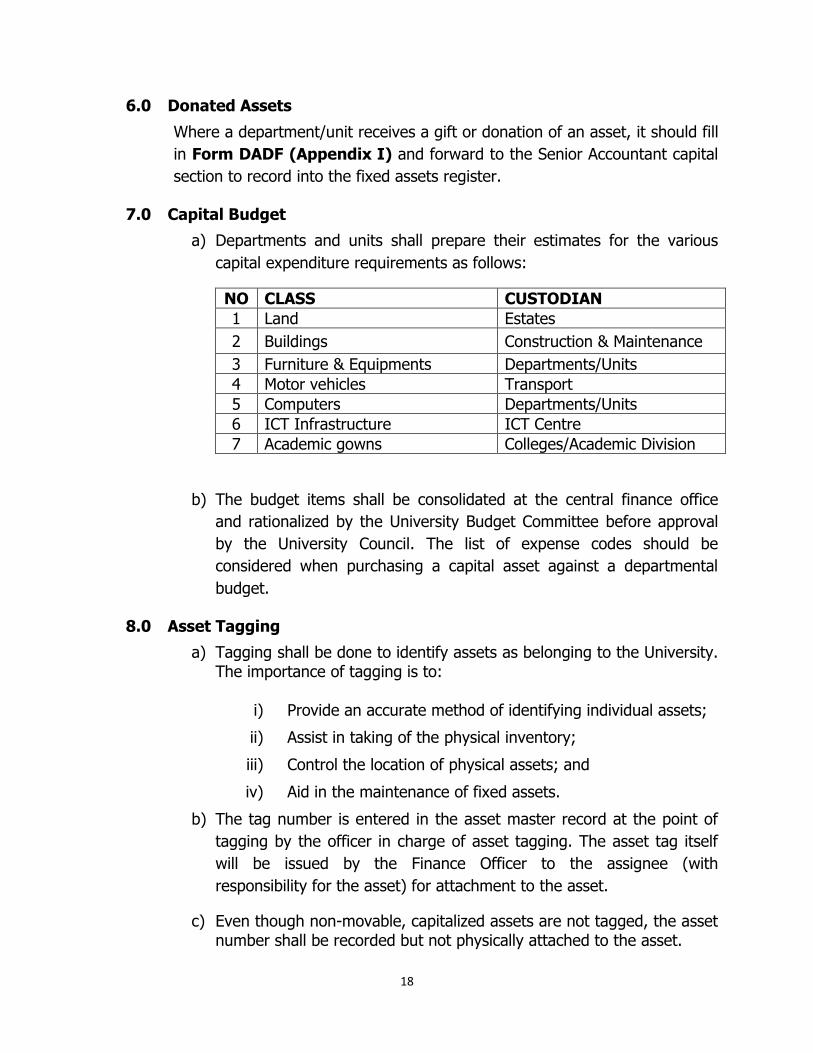

Where a department/unit receives a gift or donation of an asset, it should fill

in Form DADF (Appendix I) and forward to the Senior Accountant capital

section to record into the fixed assets register.

7.0 Capital Budget

a) Departments and units shall prepare their estimates for the various

capital expenditure requirements as follows:

NO CLASS CUSTODIAN

1 Land Estates

2 Buildings Construction & Maintenance

3 Furniture & Equipments Departments/Units

4 Motor vehicles Transport

5 Computers Departments/Units

6 ICT Infrastructure ICT Centre

7 Academic gowns Colleges/Academic Division

b) The budget items shall be consolidated at the central finance office

and rationalized by the University Budget Committee before approval

by the University Council. The list of expense codes should be

considered when purchasing a capital asset against a departmental

budget.

8.0 Asset Tagging

a) Tagging shall be done to identify assets as belonging to the University. The importance of tagging is to:

i) Provide an accurate method of identifying individual assets;

ii) Assist in taking of the physical inventory;

iii) Control the location of physical assets; and

iv) Aid in the maintenance of fixed assets.

b) The tag number is entered in the asset master record at the point of

tagging by the officer in charge of asset tagging. The asset tag itself

will be issued by the Finance Officer to the assignee (with

responsibility for the asset) for attachment to the asset.

c) Even though non-movable, capitalized assets are not tagged, the asset number shall be recorded but not physically attached to the asset.

19

d) Any asset whose cost exceeds KSh 10,000 and has a life greater than

one year should be tagged.

e) Furniture and equipment including health and fitness machines with a replacement cost above KSh. 10,000 must be tagged. This includes but is not limited to:

i) Furniture ii) Computers and Laptops iii) Audio Visual Equipment

f) Other special assets to be tagged regardless of their value include

assets such as overhead projectors, printers, televisions, DVD players, video cameras, digital cameras, fax machine, PCs, monitors, laptop computers, tablets and any asset that may be easily stolen.

g) The tags should be consistently placed in the same location on each similar asset type. The tags should be placed, if possible where they can be:

i) Easily accessible

ii) Easily identifiable without disturbing the operation of the asset.

9.0 Depreciation

Depreciation is charged on a straight line basis calculated at cost or valuation of an asset over its useful economic life. Depreciation is charged in full during the year of acquisition and nil during the year of disposal.

9.1 Depreciation Rates

The annual rates of depreciation for each class of assets are as follows:

NO CLASS RATE

1 Land NIL

2 Buildings 2%

3 Furniture & Equipments 10%

4 Motor vehicles 20%

5 Computers & ICT Infrastructures 20%

6 Academic gowns 5%

9.2 Posting of Depreciation

20

a) Depreciation shall be calculated monthly and charged to the income statement.

b) The depreciation shall be effective from 1st day of the subsequent

month, following the date of capitalization.

10.0 Inventory of Fixed Assets

a) A register of fixed assets shall be maintained by the Finance Officer.

b) Title deeds, leases and contracts relating to land and buildings shall be

maintained by the Estates Manager.

c) The Estates Manager and the Finance Officer shall annually conduct an

inventory inspection of all fixed assets of the University.

11.0 Movement of Fixed Assets between the Units

When an asset is transferred to another Unit, the transferring Unit together

with the receiving Unit shall fill in Form FATF (Appendix II) and forward to

the Senior Accountant Capital Section to record into the fixed assets register.

12.0 Disposal of Fixed Assets

12.1 Asset Impairment

a) A capital asset will be considered to be impaired when its service utility has permanently declined significantly. Events or changes that may lead to impairment include: physical damage, stalling of construction projects, obsolescence, technological, legal or environmental changes.

b) An asset shall be declared impaired by the User as defined in section 7.0 above.

c) The responsibility to record the impairment of assets and reversals of

impairment losses lies with the Finance Officer.

d) For the purposes of financial statements and in compliance with International Financial Standards, impairment of assets shall be recognized at the end of the Financial Year.

12.2 Asset Disposal

a) The University shall dispose fixed assets that are in surplus, not in working condition, obsolete or dismantled.

21

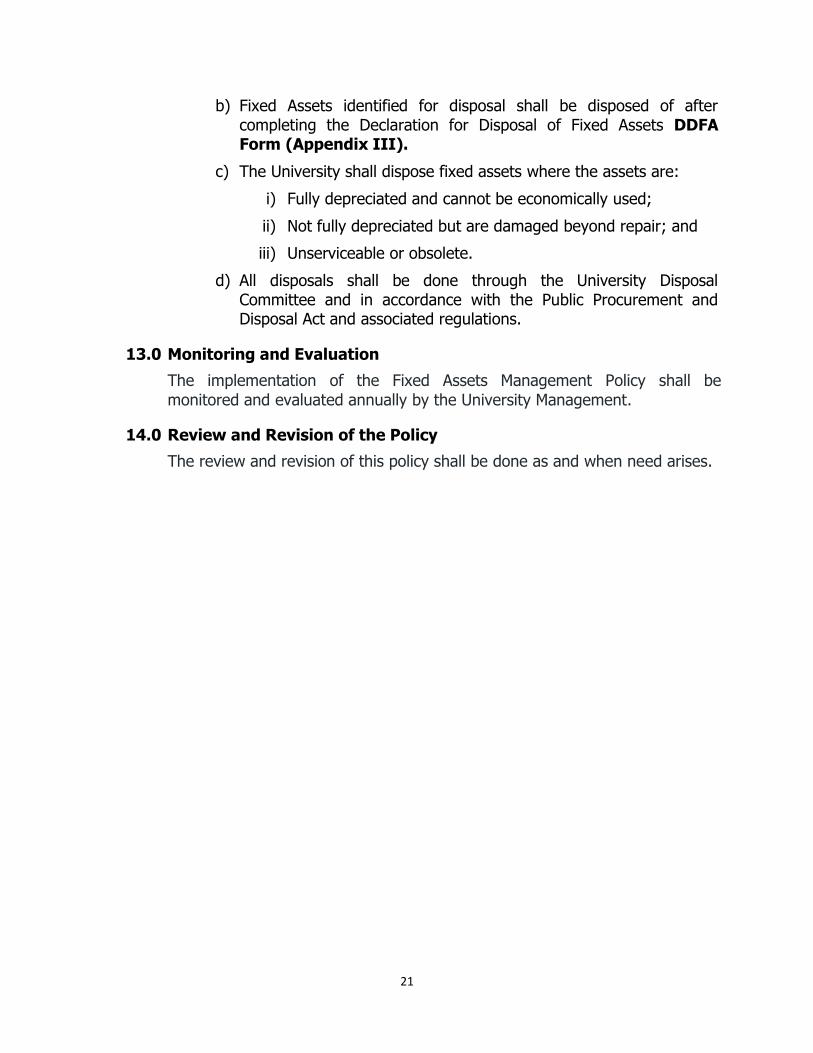

b) Fixed Assets identified for disposal shall be disposed of after completing the Declaration for Disposal of Fixed Assets DDFA Form (Appendix III).

c) The University shall dispose fixed assets where the assets are:

i) Fully depreciated and cannot be economically used;

ii) Not fully depreciated but are damaged beyond repair; and

iii) Unserviceable or obsolete.

d) All disposals shall be done through the University Disposal Committee and in accordance with the Public Procurement and Disposal Act and associated regulations.

13.0 Monitoring and Evaluation

The implementation of the Fixed Assets Management Policy shall be

monitored and evaluated annually by the University Management.

14.0 Review and Revision of the Policy

The review and revision of this policy shall be done as and when need arises.

22

MEMBERSHIP

The following were the members of the Fixed Assets Register Committee:

1. Mr. Peter K. Busienei - Chairman

2. Mr. Ibrahim Otieno - Member

3. Mr. David C. Gichuru - Member

4. Mrs. Damaris M. Kavoi - Member

5. Mrs. Lucy W. Gachara - Member

6. Mr. Peter M. Muturi - Co-opted Member

7. Mr. Leonard M. Musyoka - Co-opted Member

8. Ms. Esther W. Ndung’u - Co-opted Member

9. Mr. Stanley M. Mwangi - Secretary

23

APPENDIX I

FORM DADF

UNIVERSITY OF NAIROBI

DONATED ASSET DECLARATION FORM

This form is used to add donated assets to the fixed assets register.

College: __________________________________________________

Faculty/School/Institute/Centre: ________________________________

Department/Unit: ____________________________________________

ASSET INFORMATION

Description: _________________________ Date of Donation: _________________

Make/Model: ________________________ Manufacturer: ____________________

Serial No: ___________________________ Part No/Vehicle Reg.: ______________

Asset Type: _________________________ Tag No: _________________________

Prepared by: ________________________ Date: ____________________

Checked by: _________________________ Date: ____________________

Please forward this form to Finance Department within a month. A copy of the form will be returned to you with a Permanent Tag Number.

24

APPENDIX II

FORM FATF

UNIVERSITY OF NAIROBI

FIXED ASSETS TRANSFER FORM

This form is used for transfer of fixed assets

From: To:

College: ____________________________ College: ____________________________

Faculty/School: ______________________ Faculty/School: ______________________

Department/Unit: _____________________ Department/Unit: _____________________

Reason for Transfer:

_________________________________________________________________________

_________________________________________________________________________

ASSET INFORMATION

Description: _________________________ Date of Purchase: _____________________

Make/Model: ________________________ Manufacturer: ________________________

Serial No: ___________________________Part No/Vehicle Reg.: __________________

Asset Type: _________________________ Tag No: _____________________________

Prepared by: ________________________ Date: ____________________

Accepted by: _________________________ Date: ____________________

Please forward this form to Procurement Department within a month.

25

APPENDIX III

FORM DDFA

UNIVERSITY OF NAIROBI

DECLARATION FOR DISPOSAL OF FIXED ASSETS FORM

This form is used to declare fixed assets for disposal

College: __________________________________________________

Faculty/School/Institute/Centre: ________________________________

Department/Unit: ____________________________________________

Reason for Disposal: (Please tick)

Obsolescence [ ] Unserviceable [ ] Damaged [ ] Surplus [ ] Other: ___________

ASSET INFORMATION

Description: _________________________ Date of Purchase: _____________________

Make/Model: ________________________ Manufacturer: ________________________

Serial No: ___________________________ Part No/Vehicle Reg.: __________________

Asset Type: _________________________ Tag No: _____________________________

Prepared by: ________________________ Date: ____________________

Authorized by: _________________________ Date: ____________________

Please forward this form to Procurement Department within a month.