FISD-03-B

110

Bangalore 8/28/2014 1

-

Upload

kanchan-sharma -

Category

Documents

-

view

5 -

download

0

description

FIS

Transcript of FISD-03-B

Bangalore

8/28/2014 1

8/28/2014 2

Bond Markets: Advanced Perspectives Part-03B

8/28/2014 3

8/28/2014 4

Borrowers issue bonds in the international market to raise medium to long term funds. Borrowers MNCs,

governments, financial institutions.

High Net Worth (HNW) investors use these markets for risk diversification

International Bond Market

Eurobond segment

Foreign bond segment

5

8/28/2014 6

Bonds denominated in one or more

currencies other than the local currency

E.g. Bonds issued in currencies other than the

Yen, which are sold in Japan

The issuer may be a Japanese or a foreign entity

7

Sony is issuing bonds in

Japan:

Issuer = Japanese company

Principal = $10 billion

Currency of issue = USD

Currency of Japan = Yen

IBM is issuing bonds in

Japan:

Issuer = American company

Principal = $10 billion

Currency of issue = USD

Currency of Japan = Yen

8

Bonds are issued in the currency of the

country in which they are sold

But by an agency from a foreign country

9

Sony is issuing bonds in

Japan:

Issuer = Japanese company

Principal = 100 billion

Currency of issue = Yen

Currency of Japan = Yen

IBM is issuing bonds in

Japan:

Issuer = American company

Principal = 100 billion

Currency of issue = Yen

Currency of Japan = Yen

10

Foreign Bond Not a Foreign Bond

Foreign bonds have nicknames

U.S. Yankee bonds

Japan Samurai bonds

U.K. Bulldog bonds

Australia Kangaroo bonds

Spain → Matador Bonds

11

Eurobond market provides a lower yield, yet has grown faster than the foreign bond market:

1. These bonds are not subject to the regulations of the country in whose currency they are issued

E.g. to issue US dollar bonds in Japan permission is not required from U.S. authorities

2. They can be brought to the market quickly and with less disclosure

Important characteristic when an issuer wants to take advantage of favorable market conditions

12

3. They are issued in ‘bearer’ form and offer

favorable tax status by assuring anonymity

The name and address of the holder are not

mentioned on the bond certificates.

In practice this has facilitated tax evasion

and tax avoidance

4. Interest paid on such bonds is not subject to

withholding taxes a.k.a. TDS in India

13

Top quality borrowers Any global currency Bearer bonds Not regulated by sovereign governments No withholding taxes Annual coupons for fixed rate bonds Semi-annual/quarterly coupons for Floating-rate

notes Listed on London/Luxembourg Unsecured Bullet principal repayment Book-entry settlement via

Euroclear/Clearstream

8/28/2014 14

Euro straights pay fixed annual coupons on a 30/360 basis

US bonds pay semi-annually If the US yield is r% per annum and the

Eurobond yield is y% per annum (1+y) = (1 + r/2)2

y = r (1 + r/4) r = 2[(1+y)1/2 – 1]

8/28/2014 15

Many eurobonds have attached warrants Debt warrants allow holders to buy additional

debt at a fixed price These are interest rate call options They appeal to investors who expect rate

declines They allow holders to buy additional bonds with

the same maturity at lower coupons

8/28/2014 16

Some bonds have currency and commodity warrants Currency warrants permit holders to exchange

one currency for another at a preset rate It protects the holder against a depreciation in

the currency in which cash flows are denominated

Commodity warrants allow holders to buy a commodity at a fixed price

8/28/2014 17

Dual currency bonds pay interest in one currency and principal in another They are a portfolio of an annuity in one

currency and a ZCB in another Exchange rate may be specified at the time of

issuance Otherwise it will be the prevailing rate at the

time of payment Streaker bonds are ZCBs Global bonds are a hybrid of Eurobonds and

foreign bonds World Bank placed 10 year USD notes in the US

and other markets simultaneously

8/28/2014 18

In a falling interest rate environment Investors prefer fixed rate bonds Issuers prefer FRNs

In a rising interest rate environment Investors prefer FRNs Issuers prefer fixed rate bonds

8/28/2014 19

Perpetual FRNs have no maturity date Collared floaters have a cap and a floor The floor is usually set higher than the

prevailing interest rate To attract investors

8/28/2014 20

Yields on FRNs are usually not quoted as absolute values

Rather they are quoted as a spread in relation to a benchmark such as LIBOR or LIBID

Example LIBOR + 40 b.p.

8/28/2014 21

If a T-Bond is issued on one of the standard semi-annual dates it will pay a full coupon every 6 months

Otherwise the first coupon may be more or less than the subsequent full coupons Such bonds are said to have an odd first coupon

8/28/2014 22

If the first coupon is less than a full coupon It is termed as a Short First Coupon

If the first coupon is more than a full coupon It is termed as a Long First Coupon

Short first coupons typically occur when the usual issue date falls on a weekend/holiday And consequently the bond is issued on the

subsequent first business day

8/28/2014 23

Odd first coupons pose computational issues from the standpoint of Accrued Interest Cash flows YTM

These issues however do not exist after the first coupon Remaining coupons are full coupons Payable on the scheduled semi-annual days

8/28/2014 24

There is a 9.5% 2 year T-note The scheduled issue date is April 30, 20XX The actual issue date is May 2, 20XX Because 30 April is a Saturday

The coupon dates are 30 April and 31 October

T-notes entail the use of the Actual/Actual day-count convention April 30 to October 31 is 184 days May 2 to October 31 is 182 days

Thus the first coupon is 4.75% x 182/184 = 4.6984%

8/28/2014 25

There are two issues while calculating the AI for a settlement date falling in the first coupon period The first coupon is not a FULL coupon The maximum accrual period is shorter than 6

months

8/28/2014 26

Assume that the settlement date is 15 June The number of days since the issue date is 44 The actual length of the coupon period is 182

Thus the AI is 4.6984 x 44/182 = 1.1359%

8/28/2014 27

The fraction of a period that is remaining is computed as follows. The numerator is the number of days from the

settlement date to the next coupon date In this case it is 138

The denominator is the number of days from the semi-annual scheduled issue date and the next coupon date In this case it will be 184

8/28/2014 28

We will use the standard bond pricing equation with two differences The magnitude of the first coupon will be less

than the magnitude of subsequent coupons The beginning of the interval for calculating the

fractional first period predates the actual issue date

In the standard pricing equation it will be the actual issue date

8/28/2014 29

Let us assume that the YTM is 8% per annum. The fractional first period is 138/184 = 0.75

Assume that the face value is 1,000 The first coupon will be 0.046984 x 1,000 =

46.984 Subsequent coupons will be 47.50

On October 31 there will be 3 full coupons and the face value remaining The PV is 1020.8132 The coupon received on that day is 46.984

8/28/2014 30

The dirty price is (1020.8132 + 46.984)/(1.04)0.75 = 1036.8448

The accrued interest is $ 11.359 The clean price is 1025.4858

8/28/2014 31

A bond is issued on September 30 20XX It matures on 15 November 20XX+10 The scheduled coupon dates are May 15 and

November 15 The first semi-annual coupon date is 15

November 20XX In this case no interest is payable on that date The first coupon will be paid on 20XX + 1

The coupon rate is 9.5% per annum

8/28/2014 32

For the interval from 15 November 20XX to 15 May 20XX+1 a full coupon will be paid This amounts to 4.75% in this case

In addition a partial coupon is payable for the period 30 September to 15 November 15 May 20XX to 15 November 20XX is 184 30 September to 15 November is 46 days 46/184 = 0.25 0.25 x 4.75 = 1.1875

Thus the total first coupon = 4.75 + 1.1875 = 5.9375%

8/28/2014 33

There are two separate parts to the time between the issue date and the first coupon date There is a short period from the issue date till

the first semi-annual anniversary date And a long period from the first semi-annual

anniversary date to the second semi-annual anniversary date Which is the date on which the actual coupon is paid

We need to distinguish between these two periods while computing accrued interest

8/28/2014 34

Assume that the settlement date is 23 October 20XX

Accrued interest is computed using the partial coupon component of the first coupon

30 September till 23 October is 23 days. 30 September till 15 November is 46 days Accrued interest = (23/46) x 1.1875 =

0.59375%

8/28/2014 35

Assume the settlement date is 15 January 20XX+1

15 November till 15 May is 181 days 15 November till 15 January is 61 days Accrued interest as on 15 January 20XX+1 = 1.1875% + (61/181) x 4.75% = 2.7883%

8/28/2014 36

The price yield computation depends on whether the valuation date lies In the short period preceding the first coupon

payment Or in the long period preceding the first coupon

In the first case the first cash flow will be received more than six months later

In the second case it will be received less than six months later

8/28/2014 37

Assume the valuation date is 23 October 20XX

The first semi-annual anniversary date is 15 November 20XX

May 15 till November 15 is 184 days. 23 October till 15 November is 23 days Thus the first coupon will be paid after 1+

23/184 = 1.125 periods

8/28/2014 38

On 15 May 20XX+1, a bond with a face value of $1,000 will pay a coupon of 5.9375% or $59.375

On this date there will be 19 coupons left and a terminal face value of $1,000 Each of these coupons will be $47.50

The present value of cash flows on this date is 59.375 + 47.50xPVIFA(0.04,19) + 1000PVIF(.04,19) = 59.375 + 1,098.5045 = $1,157.8795

8/28/2014 39

The present value on 23 October is 1157.8795/(1.04)1.125 = $1107.9008 This is the dirty price The clean price is 1107.9008 –

0.0059375x1000 = 1101.9633

8/28/2014 40

Assume that we are on 15 January 20XX+1 The fractional period till the first coupon is

120/181 = 0.6630 The PV of all cash flows on 15 May 20XX+1 is

$1,157.8795 The PV on 15 JAN is 1157.8795/(1.04)0.663

= 1128.1589 This is the dirty price The clean price is 1128.1589 – 0.027883 x 1,000 =

1,100.2759

8/28/2014 41

Assume we are on 1 FEB 2014 Settlement will happen on 2 FEB 2014 A T-note maturing on 15 NOV 2023 is trading

at 97-08 The coupon is 5.40% The dirty price is 97 + (8/32) + 2.7 x 79/181 = 98.4285

8/28/2014 42

On 15 FEB 2014 the Treasury will reopen the issue

The trader can borrow on a collateralized basis at 3.50% per annum.

Amount borrowed = 98.4285 Amount repayable = 98.4285 x [1 + 0.035 x

13/360] = 98.5529 To breakeven the newly issued security must

be sold for this amount

8/28/2014 43

Accrued interest on 15 FEB = 2.7 x 92/181 = 1.3724

Clean price corresponding to 98.5529 is 98.5529 - 1.3724 = 97.1805

YTM corresponding to the price on FEB 1 is 5.7705

The YTM corresponding to the price on 15 FEB is 5.7812

Thus the break-even on the roll is 578.12-577.05 = 1.07 basis points

8/28/2014 44

There are two types of issues P-Linkers and C-Linkers

In the case of P-Linkers The coupon rate is fixed The principal is linked to changes in an Index like

the CPI Such bonds are usually issued by governments

TIPS (Treasury Inflation-Protected Securities) are an example

8/28/2014 45

C-Linkers are like floating rate bonds The principal is fixed The coupons are variable and are linked to the

CPI They are usually issued by commercial banks and

insurance companies

8/28/2014 46

Face value = $100 Coupon rate = 5% Payment frequency = annual Maturity = 5 years

8/28/2014 47

Time CPI INF.Rate Adj.Prin Nominal Cash Flow

Real Value

0 100 100.00 -100.000 -100.000

1 108 8% 108.00 5.400 5.00

2 117.5 8.7963% 117.50 5.875 5.00

3 112.50 -4.2553% 112.50 5.625 5.00

4 120 6.6667% 120.00 6.000 5.00

5 130 8.3333% 130.00 136.500 105.00

Average 6.5082% IRR 10.6814% 5.00%

8/28/2014 48

If the previous issue were to be a C-Linker the coupon every period will be the announced rate plus the rate of inflation

In this case the announced rate is 5% So if the rate of inflation is 3% The actual coupon paid will be 8%

8/28/2014 49

Time CPI INF.Rate Coupon Rate

Nominal Cash Flow

Real Value

0 100 -100.000 -100.000

1 108 8% 13.0000% 13.0000 12.0370

2 117.5 8.7963% 13.7963% 13.7963 11.7415

3 112.50 -4.2553% 0.7447% 0.7447 0.6620

4 120 6.6667% 11.6667% 11.6667 9.7223

5 130 8.3333% 13.3333% 113.3333 87.1795

Average 6.5082% IRR 10.5630 4.7423%

8/28/2014 50

Cash flows on the C-Linker are more – front loaded- as compared to the P-Linker

Compensation for inflation on the C-Linker is paid on realization It is mostly deferred till maturity on the P-Linker

8/28/2014 51

This is used for bonds which have a sinking fund provision.

A firm has issued bonds with a total face value of $200 MM

The bonds have 5 years to maturity. Coupons are paid on an annual basis at a rate

of 6% per annum The company will redeem a fraction of the

issue every year as per the following schedule

8/28/2014 52

YEAR (t) Proportion Redeemed (w)

Redemption Price (P)

1 0.10 102.00

2 0.15 101.50

3 0.20 101.00

4 0.20 100.50

5 0.35 100.00

8/28/2014 53

The average life is defined as: Σ(w x P x t) ÷ Σ (w x P) The numerator is 0.10x102x1 + 0.15 x101.50x2 + 0.20x101x3 +

0.20x100.50x4 + 0.35x100x5 = 356.65 The denominator is 0.10x102 + 0.15 x101.50 + 0.20x101 +

0.20x100.50 + 0.35x100 = 100.725 The average life is 356.65 ÷ 100.725 = 3.5408

years

8/28/2014 54

The yield to average life is computed under the assumption That the bond matures at the time corresponding

to the average life And that the cash flow at that time is the

average redemption price

Assume that the prevailing market price is 98.25

8/28/2014 55

8/28/2014 56

Where N -1 is the number of coupons received at regular intervals prior to the time corresponding to the average life M is the average redemption price N* is the time corresponding to the average life Yal is the yield to average life

In our illustration N-1 = 3 N* = 3.5408 M = 100.725 P = 98.25 The solution is 7.4892% The YTM is 6.4202%

8/28/2014 57

The bond is trading at a discount The redemption schedule has the effect of

reducing the time interval over which the capital gain arises Thus the yield gets pushed up

8/28/2014 58

In this measure we consider the present value of the redemption price instead of the price itself This accounts for the fact that the redemption

prices are received at different points in time

8/28/2014 59

8/28/2014 60

The formula for the equivalent life is given by:

In this case the present values are defined using the yield to equivalent life

Hence we need to compute the yield to equivalent life before we can compute the equivalent life

8/28/2014 61

8/28/2014 62

The yield to equivalent life is defined as:

Where N is the number of remaining coupon periods wi is the proportion redeemed at time i Pi is the redemption price corresponding to time i yel is the yield to equivalent life

In our example: N = 5 C = 6 P = 98.25 The yield to equivalent life comes to 8.9471% The YTM is 6.4202% The equivalent life is 3.3782 years The equivalent life will always be shorter

than the average life since in the former, earlier cash flows get greater weight

8/28/2014 63

The yield to equivalent life is higher than the yield to average life

8/28/2014 64

When a corporation decides to issue bonds it must submit the required documents to the regulator For authorization to borrow

The authorization per se need not be recorded in the books of account However it is usually disclosed in the footnotes

The footnote will mention the number and value of bonds authorized.

As well as the interest rate, the interest payment dates, and the life of the bond

Assume that Alpha corporation issues a JD-15 bond on 15 June 2014

The face value is $1,000 and the coupon is 8% per annum payable semi-annually

Assume that 1,000 bonds are issued at par and that the maturity is 4 years.

Debit Amount Amount Credit

Cash 1,000,000 1,000,000 Bonds Payable

Cash which is an asset will be debited by 1,000,000 as there is an inflow Bonds payable will be credited with 1,000,000 as there is a liability

On 15 December 2014 there will be an interest payable In this case 1,000,000 x 0.08/2 = 40,000

Bond interest expenses will be debited by 40,000

If the amount is immediately paid out then cash will be credited with 40,000

If the amount is not paid out immediately Interest Payable will be credited with 40,000

Consider the same bond. The coupon is 8%, however the YTM at the

time of issue is 8.50% The issue price will be 983.34 The total inflow from 1,000 bonds is 983,340 Cash will be debited with 983,340 Bonds payable will be credited with 1,000,000 Unamortized bond discount will be debited with

16,660

Unamortized bond discount is a contra-liability account

The balance in this account is deducted from the face value to arrive at the present value

It will be amortized or written off during the life of the bonds

Consider the same data Assume the YTM at the time of issue is 7.50% The issue price per bond will be 1017.01 The total inflow will be 1,017,010 It will be reflected in the books as follows Cash will be debited with 1,017,010 Bonds payable will be credited with 1,000,000 Unamortized bond premium will be credited with

17,010

Issue costs for a bond issue can be significant These have benefits for the entire life of the

bond Consequently they need to be spread out

The net result of incurring such costs will be To reduce the proceeds from an issue at par To increase the discount for an issue below par To decrease the premium for an issue above par

Thus such expenses can be amortized over the life of the bond by way of amortizing the discount/premium

The discount should be amortized over the life of the issue

Thus the discount will gradually decline over time and the carrying value will steadily increase The carrying value is the Face Value – Unamortized Discount

At maturity the carrying value will be equal to the face value And the unamortized discount will be zero

If a bond is issued at a discount the effective interest paid by the issuer is greater than the coupon rate

This is because the effective interest paid is the sum of the coupons plus the discount The company does not receive the full face value

at the time of issue Yet it must pay back the face value at maturity

Thus the discount must be added to the total interest payments to arrive at the effective interest

In our case the total coupon payment is 40,000 x 8 = 320,000

The discount = 16,660 Thus the total interest cost is 336,660

The discount is allocated over the life of the bond as an increase in the interest paid

Thus the interest expense for a period will exceed the actual interest by the amount of the amortized discount

This process of allocation is called the Amortization of Bond Discount

It equalizes amortization of the discount for each interest period.

Our bond pays interest on June-15 and December-15 every year for 4 years

Thus there are total of 8 coupon periods The amortized bond discount per period = 336,660/8 = 42,082.50 Cash interest paid = 40,000 per period Interest Expense per period = 42,082.50

Debit Bond Interest Expense with 42,082.50 Credit Cash with 40,000 Credit unamortized bond discount with

2,082.50

The debit balance of unamortized bond discount is reduced by 2,082.50 every period

Thus the carrying value of the bonds increases by this amount every period

Similar entries will be made every six months At maturity the unamortized bond discount

will have a zero balance The carrying value will be 1,000,000 Exactly what is owed to the bondholders

The method has certain weaknesses When amortizing a discount the carrying

value goes up every period but the interest expense is constant Thus the rate of interest falls over time

Obviously if a premium were to be amortized The rate of interest will rise over time

In this method a constant interest rate is applied to the carrying value of the bond at the beginning of the period

This rate is the YTM prevailing at the time of issue

The amount amortized each period is the difference between the interest computed using the YTM and the actual interest paid

Let us consider the data we have for the discount bond.

The issue proceeds were 983,340 and the YTM was 8.50%

The discount is 16,660 and the initial carrying value is 983,340

The interest expense for the first quarter will be 983,340 x 0.085/2 = 41,791.95

The actual interest paid is 40,000 Thus the amortized discount is 41,791.95 –

40,000 = 1,791.95 The unamortized bond discount at the end of

the period is 16,660 – 1,791.95 This will decrease every period The carrying value will increase every period Thus the amortized discount will steadily

increase

So the entries at the end of the first period will be:

Debit Interest Expense by 41,791.95 Credit cash with 40,000 Credit Unamortized Bond Discount by

1,791.95

PERIOD Beginning Carrying Value

Interest Expense

Coupon Amortized Discount

Unamorti-zed Bond Discount

Ending Carrying Value

0 16,660 983,340

1 983,340 41791.95 40,000 1,791.95 14,868 985,132

2 985132 41868.11 40,000 1,868.11 13000 987,000

3 987000 41947.50 40,000 1947.50 11052 988948

4 988948 42030.27 40,000 2030.27 9022 990978

5 990978 42116.56 40,000 2116.56 6906 993094

6 993094 42206.51 40,000 2206.51 4699 995301

7 995301 42300.29 40,000 2300.29 2399 997601

8 997601 42398.05 40,000 2398.05 1 999,999

The carrying value gradually increases and approaches the face value at maturity

The interest expense is a fixed percentage of the carrying value Consequently it increases every period Since the coupon payments are constant the

amortized discount steadily increases

Let us consider the situation where the coupon is 8% per annum and the YTM is 7.50%

The initial inflow was 1,017,010 Thus there is an unamortized bond premium

of 17,010 Like a discount, the premium needs to be

amortized over the life of the bonds

The premium represents an amount that the bondholders will not receive at maturity

It is an advance reduction of the total interest paid over the life of the bond.

The total coupon = 40,000 x 8 = 320,000 The bond premium is 17,010 Thus the total interest cost is 302,990 Now let us consider amortization of the

premium

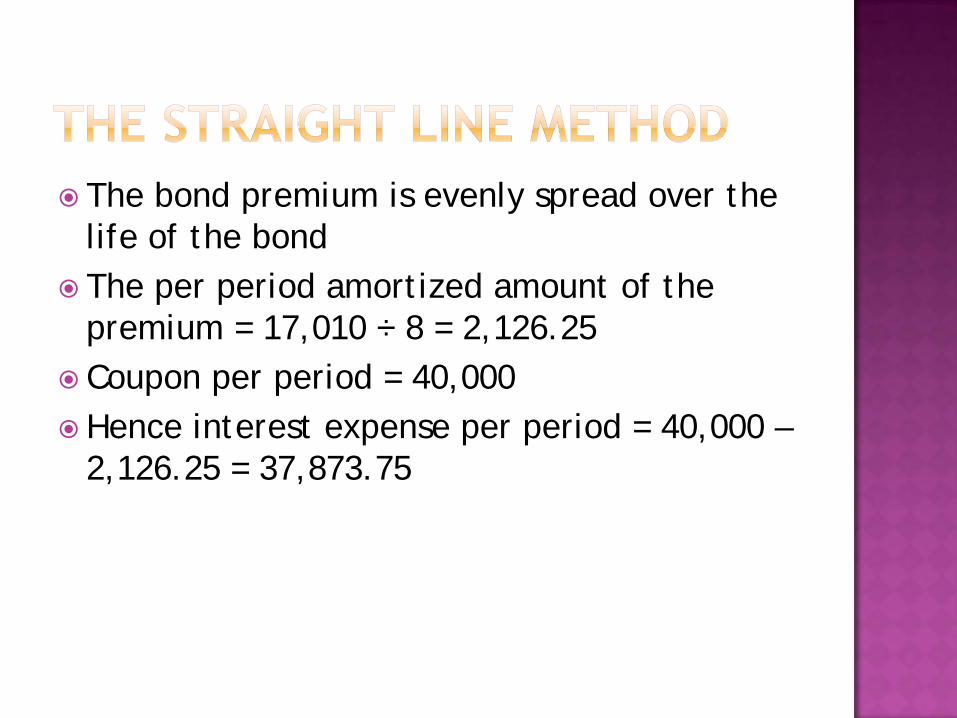

The bond premium is evenly spread over the life of the bond

The per period amortized amount of the premium = 17,010 ÷ 8 = 2,126.25

Coupon per period = 40,000 Hence interest expense per period = 40,000 –

2,126.25 = 37,873.75

Debit Interest Expense with 37,873.75 Credit cash with 40,000 Debit unamortized bond premium with

2126.25

The interest expense is less than what bondholders receive

The difference is debited to the Unamortized Bond Premium

This lowers the credit balance for the unamortized bond premium

It also reduces the carrying value of the bond by the same amount

Similar entries will be made every six months When the bond matures the balance in the

unamortized bond premium account will be zero

The carrying value will be equal to the face value

In this case the initial YTM is applied to the carrying value at the outset.

Since the carrying value will steadily decline so will the interest expense

The unamortized bond premium declines gradually and approaches zero

The amount of premium amortized in a period is equal to the coupon minus the interest expense Since the expense is gradually declining the

amount amortized will steadily increase

TIME Beginning Carrying Value

Interest Expense

Coupon Amortized Premium

Unamorti-zed Premium

Ending Carrying Value

0 17,010 1,017,010

1 1,017,010 38137.88 40000 1862.13 15,148 1,015,148

2 1,015,148 38068.05 40000 1931.96 13,216 1,013,216

3 1,013,216 37995.60 40000 2004.40 11,212 1,011,212

4 1,011,212 37920.43 40000 2079.57 9,132 1,009,132

5 1,009,132 37842.45 40000 2157.55 6,974 1,006,974

6 1,006,974 37761.54 40000 2238.46 4,736 1,004,736

7 1,004,736 37677.60 40000 2322.40 2,414 1,002,414

8 1,002,414 37590.51 40000 2409.49 4 1,000,004

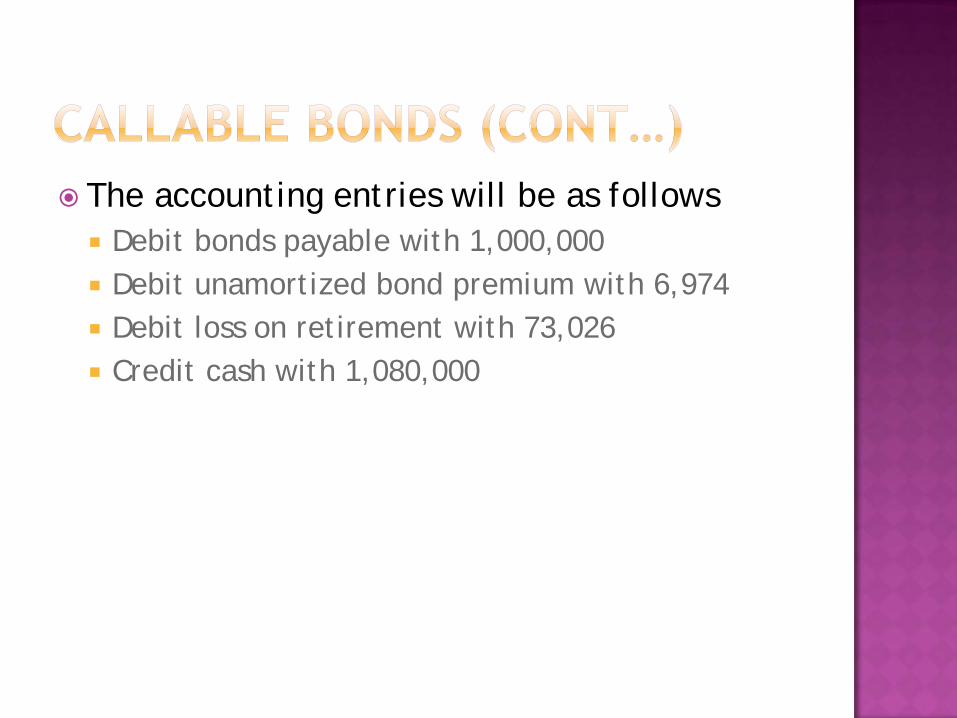

Consider the bond that was issued at a premium

Assume that the bonds can be recalled at 1,080 - Face value plus one year’s coupon

Let us assume that the bond is recalled after 5 coupon periods The unamortized premium will be 6,974

The accounting entries will be as follows Debit bonds payable with 1,000,000 Debit unamortized bond premium with 6,974 Debit loss on retirement with 73,026 Credit cash with 1,080,000

Sometimes a rise in interest rates may cause the market price of the bond to fall way below the face value

In such cases the issuer may enter the market and buy back bonds

In this case a gain will be realized for the difference between the repurchase price and the carrying value

Assume that the bond which was issued at a premium is bought back after 5 coupon periods at 950

The entries will be as follows Debit bonds payable with 1,000,000 Debit unamortized bond premium with 6,974 Credit cash with 950,000 Credit gain on retirement of bonds with

56,974

If a bond holder decides to convert the company will record the common stock issued at the carrying cost of the bonds

The bond liability and the unamortized premium or discount are written off

Thus there is no recorded gain or loss

Let us consider the case of the bond issued at a premium

After 5 periods the carrying value is 1,006,974

Let us assume that bond holders convert to 40 shares with a par value of 20 each.

The entries will be as follows Debit bonds payable by 1,000,000 Debit unamortized bond premium by 6,974

Credit common stock with 800,000 Credit additional paid in capital with 206,974

Bonds are often issued at a date corresponding to a coupon date

At times however they may be issued between two semi-annual coupon dates

In these cases they usually collect from the investors the interest that would have accrued for the partial period And payout the interest for the entire period on

the next coupon date

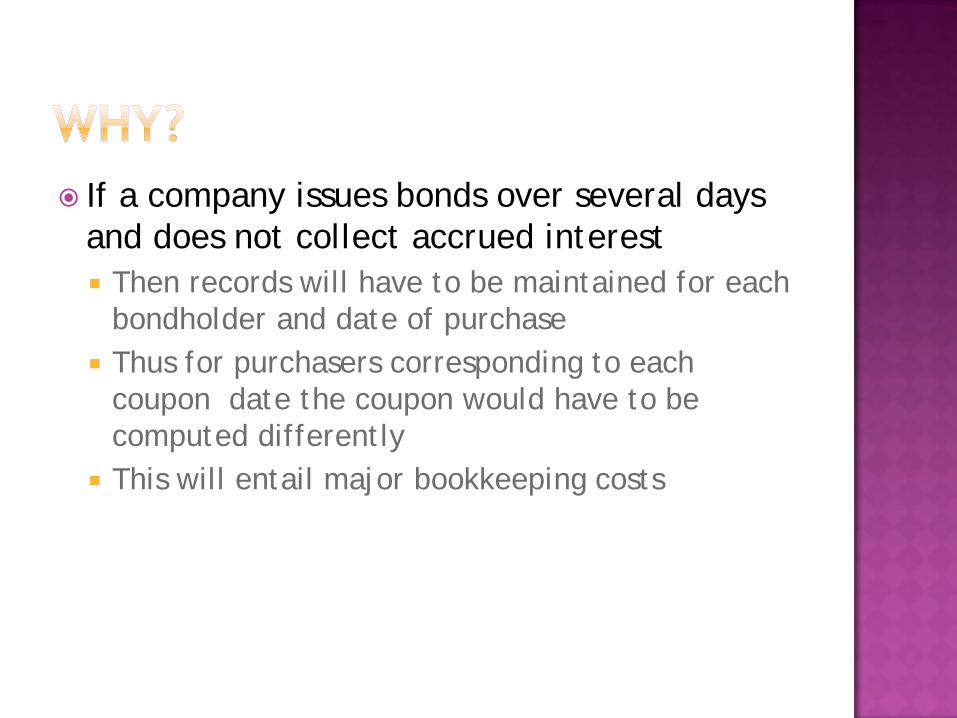

If a company issues bonds over several days and does not collect accrued interest Then records will have to be maintained for each

bondholder and date of purchase Thus for purchasers corresponding to each

coupon date the coupon would have to be computed differently

This will entail major bookkeeping costs

Assume that a bond with a face value of 1,000 and a coupon of 8% payable semi-annually is issued 1 ½ months after the corresponding semi-annual coupon date

The accrued interest will be 10 Thus for each bond 1,010 will be collected

which would amount to 1,010,000 in all

This would be accounted for as follows Debit cash with 1,010,000 Credit Interest Expense with 10,000 Credit bonds payable with 1,000,000 On the next coupon date the following

entries will be made Debit bond interest expense with 40,000 Credit cash with 40,000

The semi-annual coupon dates will usually not correspond with the ending date for the financial year

Thus there is a need to accrue interest from the last coupon date to the end of the year

Also any discount or premium must be amortized for the partial period

Consider the bonds that were issued at a premium on June 15, 2014 at a premium

The next coupon would be paid on 15 December 2014

Thus on 31 March 2015, we need to provide for Accrued interest for 3 ½ months or 7/12 of a

period And for 7/12 of the amortized premium

corresponding to the second coupon period which is 1931.96

Thus the following entries would be passed on 31 March 2015 Debit interest expense with 22,206.35 Debit unamortized bond premium with 1,126.98 Credit interest payable with 23,333,33

On June-15 2015 the following entries will be passed Debit bond interest expense with 15,861.70 Debit unamortized premium with 804.98 Debit bond interest payable with 16,666.67 Credit cash with 40,000