FISD-02-A

115

Bangalore 8/28/2014 1

-

Upload

kanchan-sharma -

Category

Documents

-

view

221 -

download

0

Transcript of FISD-02-A

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 1115

Bangalore

8282014 1

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 2115

8282014 2

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 3115

Part-02ABond amp Bond Markets An Introduction

8282014 3

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 4115

What is debtIt is a financial claim

Who issues it

The borrower of fundsFor whom it is a liability

Who holds itThe lender of funds

For whom it is an asset

8282014 4

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 5115

Difference between debt and equityDebt does not confer ownership rightsIt is merely an IOU

A promise to pay interest at periodic intervalsAnd to repay the principal at a pre-specified maturitydate

8282014 5

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 6115

It usually has a finite life spanPerpetual debt is rare

The interest payments are contractualobligations

Borrowers are required to make payments irrespectiveof their financial performance

8282014 6

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 7115

Interest payments to be made before anydividends for equity holders

In the event of liquidationThe claims of debt holders must be settled firstOnly then can equity holders be paid

8282014 7

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 8115

Bonds and debentures are termed as FixedIncome Securities

Once the rate of interest is set at the onset ofthe period for which it is due

It is not a function of the profitability of the firmFailure to pay the promised interest willtantamount to default

8282014 8

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 9115

Bonds may be secured or unsecuredUnsecured debt securities are termed asDebentures in the USUnsecured means no specific assets have beenearmarked as collateralSecured debt requires the firm to earmarkspecific assets as collateralSecured debt holders enjoy priority from thestandpoint of payments

8282014 9

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 10115

Debt securities may be negotiable or non-negotiable

Negotiable securities can be traded in thesecondary market

Can be endorsed by one party in favor of anotherExamples of non-negotiable debt securities

National savings certificatesConventional Time or Fixed deposits

8282014 10

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 11115

The most basic form of a bond is called thePlain Vanilla version

8282014 11

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 12115

This is true for all securities not just for bondsMore complicated versions are said to have`Bells and Whistlesrsquo attached

8282014 12

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 13115

These bonds are slightly differentThe interest rate does not remain fixedIt varies each period based on the reference rate

Short-term reference rate ndash maturity lt 1 yearFloating rate bonds

Longer-term reference rateVariable or adjustable rate bonds

8282014 13

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 14115

Convertible bonds can be converted to sharesof stockCallable bonds can be prematurely retired by

the issuerPutable bonds can be prematurelysurrendered by the holders

8282014 14

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 15115

It is the principal valueAmount payable by the borrower to the lastholder at maturityAmount on which the periodic interest paymentsare calculatedAKA as

Par ValueRedemption Value Maturity ValuePrincipal Value

8282014 15

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 16115

It is the time remaining in the life of thebond

The length of time for which interest has to bepaid as promisedThe the length of time after which the face valuewill be repaidAKA as

MaturityTermTenor

8282014 16

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 171158282014 17

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 18115

The periodic interest payment that has to bemade by the borrower

The coupon rate multiplied by the face valuegives the rupeedollar value of the coupon

8282014 18

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 19115

Most bonds pays coupons on a semi-annual basisTrue in UKUSAustraliaJapanIn European and Eurobond markets annualpayments are the norm

8282014 19

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 20115

In earlier days bonds were accompanied by abooklet of post-dated coupons

Each coupon could be detached and redeemedon the corresponding coupon payment date

Even today bearer bonds come with couponsThe bearer certificate number is mentioned onthe coupon

8282014 20

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 21115

Bond with a face value of $1000The coupon rate is 8 per annum paid semi-annually

So the bond holder will receive1000 x 008

___ = $40 every six months2

8282014 21

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 22115

The rate of return if an investor buys thebond at the prevailing price and holds ittill maturity

In order to get the YTM two conditionsmust be satisfied

The bond must be held till maturity All coupon payments received before maturitymust be reinvested at the YTM

8282014 22

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 23115

At any point in time the YTM may beGreater thanLess than or

Equal to the Coupon RateYTM is the IRR of a bond

8282014 23

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 24115

Bonds involve pure cash flowsSo only ONE REAL POSITIVE YTM

Solution to a Non-Linear equation

Solved iteratively

8282014 24

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 25115

A holder gets a stream of contractuallypromised payments

The value of the bond is the value of this stream

of cash flowsCash flows arising at different points in timecannot be addedCash flows have to be discounted

8282014 25

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 26115

It is a chicken and egg storyIf we know the yield that is required we canquote a priceOnce we acquire the asset at a certain price we

can work out the corresponding yield

8282014 26

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 27115

A bond will pay identical coupons everyperiodAnd will repay the face value at maturity

The periodic cash flows constitutean annuity The terminal face value is a lump

sum payment

8282014 27

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 28115

Bond pays a semi-annual coupon of $C2and has a face value of $MAssume there are N coupons left

And that we are standing on a coupondate

We are assuming that the next coupon is exactlysix months away

The required annual yield is yImplies that the semi-annual yield is y2

8282014 28

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 29115

The present value of the coupon stream is

8282014 29

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 30115

The present value of the face value is

8282014 30

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 31115

So the price of the bond is

8282014 31

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 32115

IBM has issued a bond with a face value of$1000The coupon is 8 per year to be paid on July

15 and January 15 every yearToday is 15 July 2013 and that the bondmatures on 15 January 2033The required yield is 10 per annum

8282014 32

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 33115

JJ ndash 0115FA ndash 0115MS ndash 0115

AO ndash 0115MN ndash 0115JD ndash 0115

8282014 33

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 34115

8282014 34

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 35115

In the example the price is less than theface value

Such a bond is called a Discount Bond

It is trading at a discount from the face valueThe reason is that

The yield is greater than the coupon

8282014 35

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 36115

If the yield were to equal the couponThe bond would sell at PARSuch bonds are called PAR Bonds

If the yield is less than the couponThe price will exceed the face valueSuch bonds are called Premium Bonds

8282014 36

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 37115

As we move from one coupon date to thenext if the YTM were to remain constant

Par bonds would continue to trade at PARPremium bonds will steadily decline in priceDiscount bonds will steadily increase in price

This is called the Pull to Par EffectAt maturity ndash ALL BONDS WILL TRADE AT PAR

8282014 37

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 38115

As we approach maturity the number ofcoupons reduces

The contribution of coupons to price reducesThe contribution of the PV of the face valueincreases

For premium bonds the first effect dominatesThus the price steadily declines

For discount bonds the second effectdominatesThus the price steadily increases

8282014 38

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 39115

A plain vanilla or Bullet Bond pays the entireface value at maturity in a lump sumAmortizing bonds pay the principal in

installmentsThe first payment occurs before maturityThe last payment is made at maturity

8282014 39

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 40115

Consider a 5 year amortizing bond with aface value of $1000 and an annual coupon of8

The annual cash flows are depicted below

8282014 40

Time Cash Flow

1 802 803 3304 3105 540

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 41115

The first two cash flows represent interest ona principal of $1000The third cash flow is interest on $1000 plus

a principal payment of $250The outstanding principal is $750The fourth cash flow is interest on $750 plusa principal payment of $250

The outstanding principal is $500The final cash flow is interest on $500 plusthe remaining principal of $500

8282014 41

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 42115

Some companies issue such bonds becausethe assets being funded have a similar cashflow profile

Second the coupon on such a bond may belower than that of a bullet bondIn the case of a bullet bond the entire principalis due at a single point in timeThere is greater default risk

8282014 42

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 43115

8282014 43

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 44115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 45115

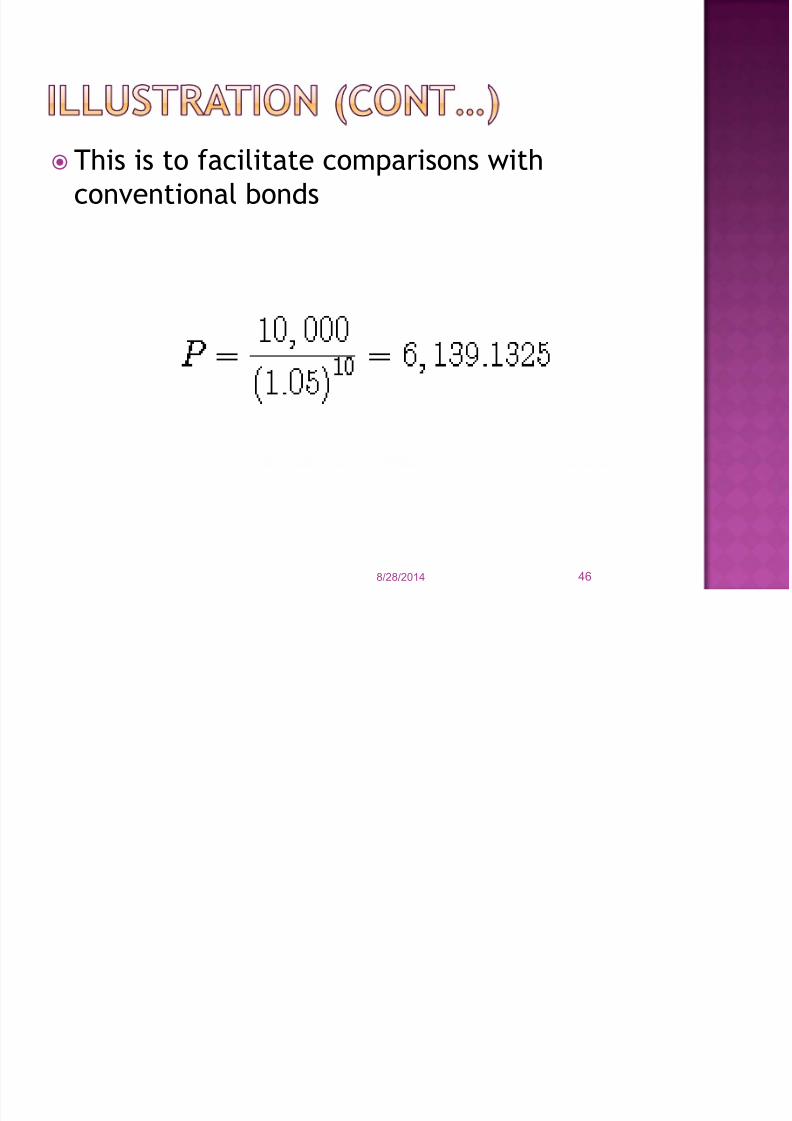

Microsoft is issuing zeroes with 5 years tomaturity and a face value of $10000

The required yield is 10 per annumWhat should be the price

Price is the PV of the face valueIn practice we discount on a semi-annual basis

8282014 45

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 46115

This is to facilitate comparisons withconventional bonds

8282014 46

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 47115

A zero coupon bond can never sell at apremium

It will always trade at a discount prior tomaturityAt maturity it will trade at par

8282014 47

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 48115

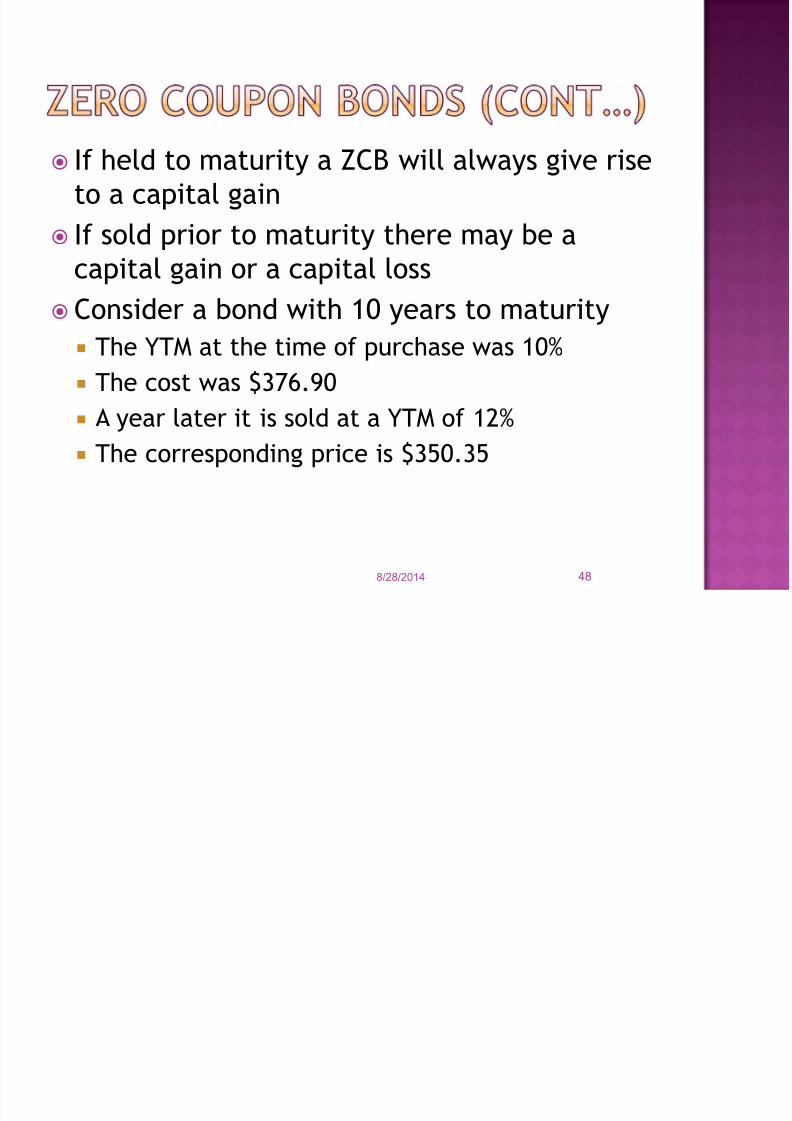

If held to maturity a ZCB will always give riseto a capital gainIf sold prior to maturity there may be a

capital gain or a capital lossConsider a bond with 10 years to maturityThe YTM at the time of purchase was 10The cost was $37690

A year later it is sold at a YTM of 12The corresponding price is $35035

8282014 48

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 49115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 50115

A newly established issuerOr an issuer with a relatively virgin productor service

Or a restructured company due to a mergeror following a bankruptcyWill be perceived as more riskyInvestors will demand a high coupon

Such firms are unlikely to have high earningsRevenues will peak only after theproductservice is established

8282014 50

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 51115

They can ill afford high couponsThey may consider a step-up coupon bond

Where the coupon increases as the bond ages

Assume a company can issue a plain vanillaat a coupon of 8 with a maturity of 5 yearsInstead it may opt for a bond

With a coupon of 6 for the first three years

And a coupon of 10 for the last two yearsThis is a Deferred Interest Security

Provides the issuer with breathing room in theearlier years

8282014 51

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 52115

These pay coupons in the form of additionalsecurities and not cash

This offers the issuer time to prepare for cashoutlays

They are used as Mezzanine FinanceThey rank between senior debt and equity in thecapital structureInvestors take more risk as compared to buyersof regular bonds ndash but get higher returnsIssuers can conserve cash in earlier years when itis at a premium

8282014 52

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 53115

8282014 53

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 54115

Fully backed by the federal government ofthe issuing nationConsequently they are virtually devoid ofcredit risk or the risk of defaultThe yield on such securities is a benchmarkfor setting rates on other kinds of debt

8282014 54

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 55115

Treasury securities are issuedTo finance expenses in excess of currentrevenuesTo pay interest on debt accumulated in earlieryears due to deficits in those yearsTo repay past debt issues that are currentlymaturing

The US Treasuries marketIs the largest bond market in the worldIs the most liquid bond market in the world

8282014 55

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 56115

The Treasury issues three categories ofmarketable securities

T-bills are discount securitiesThey are zero coupon securitiesT-notes and T-bonds are sold at face value andpay interest periodically

8282014 56

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 57115

T-bills are issued with a original time tomaturity of one year or less

They are Money market instrumentsThey have maturities of either 1 3 6 or 12months at the time of issue

8282014 57

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 58115

T-notes and T-bonds have a time to maturityexceeding one year at the time of issue

They are capital market instrumentsT-notes have maturities ranging from 1-10 yearsT-bonds have an original maturity in excess of 10years extending up to 30 years

8282014 58

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 59115

An issue may be followed later by a furtherissue

With the same remaining time to maturity andthe same couponThe issuance of further tranches is termed as aRe-opening

8282014 59

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 60115

Six months ago a 10-year note was issuedwith a coupon of 8 per annumToday if a note with 9 frac12 years to maturityand a coupon of 8 issued it will add to thepool that is already trading in the marketThus it is a re-opening of an existing issue

8282014 60

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 61115

Who is a primary dealerA PD is a dealer who is authorized to dealdirectly with the Central Bank of the countryIn the US a PD is a bank or securities broker-dealer that directly deals with the FRBNY

Importance of FRBNYIn India a PD deals directly with the RBI

8282014 61

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 62115

8282014 62

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 63115

The Treasury sells bills notes and bonds byway of a competitive auction process

Most of the treasury securities are bought byprimary dealers

Individual investors submit non-competitive bidsand participate on a much smaller scale

8282014 63

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 64115

Bids may beCompetitive

Indicate price amp quantity or yield amp quantityNon-competitive

Indicate only quantity

Small investors and individualsgenerally submit non-competitive bids

A non-competitive bidder may not bid for more than$5MM worth of securities in a bill or bond auction

8282014 64

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 65115

Primary dealers bid for their accounts andon behalf of their clientsThey usually submit large competitive

bidsBids indicate the maximum price that the bidderis prepared to pay if it is a price based auctionOr the minimum yield that the bidder is

prepared to accept if it is a yield based auction

8282014 65

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 66115

The Treasury will net out the totalamount of non-competitive bids

The balance will be allocated to competitivebidders

There are two ways in which securitiescan be allotted

The multiple priceyield auction mechanism

French AuctionsThe uniform priceyield auction mechanism

Dutch Auctions

8282014 66

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 67115

Assume that the Treasury is offering 25billion dollars worth of T-bonds

2 billion dollars worth of non-competitive bidshave been receivedSo 23 billion dollars worth of bonds are availableto be offered to the competitive bidders

8282014 67

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 68115

There are six competitive bidders who havesubmitted the following yields

The bids have been arranged in ascending orderof yieldIn a price based auction the bids would havebeen arranged in descending order of price

8282014 68

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 69115

Bidder Bid Yield Bid Amount

Aggregate Amount

Alpha 5370 30 bn 30 bnBeta 5372 50 bn 80 bn

Gamma 5373 40 bn 12 bn

Delta 5375 80 bn 20 bnCharlie 5375 120 bn 32 bn

Tango 5380 30 bn 35 bn8282014 69

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 70115

The aggregate demand equals the amount onoffer at a yield of 5375A multiple yield auction will lead to thefollowing allocation

Alpha will get 3 bn at a yield of 5370Beta will get 5 bn at 5372Gamma will get 4 bn at 5373

8282014 70

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 71115

At a yield of 5375 we have only 11 bn left toallocateThere is a demand of 20 bn at this yield

8 bn from Delta and 12 bn from CharlieThus we will allocate 1120 = 55 to eachbidder at this yield

There will be pro-rata allocation

055 of 8 bn or 440 bn will go to Delta055 of 12 bn or 66 bn will go to Charlie

8282014 71

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 72115

The highest accepted yield is called the StopYield or High Yield

In this case it is 5375The ratio of bids received to the amountawarded is known as the bid to cover ratio

The higher the ratio the stronger is the auction

8282014 72

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 73115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 74115

Those who bid more than 5375 will getnothing and are said to be shutout of theauctionSince 1999 the US Treasury has beenconducting only uniform yield auctions

8282014 74

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 75115

WI stands for ndash When As and If IssuedThe when issued market is a market forforward trading of a bond

Which has been announced but not yet issuedTrades take place from the date ofannouncement until the actual issue date

Helps bidders to gauge the marketrsquos interestbefore the actual auction

8282014 75

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 76115

WI trading has ramifications for the biddingstrategies of market participantsTraders can take both long and shortpositions

Settlement is scheduled for the issue date

8282014 76

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 77115

It has a bearing on the outcome of theauction

It affects the strategy used by a bidder becauseit has an impact on his prior positionBidders who are long in the WI market enter theauction with a Long PositionThose who are short in the WI market enter theauction with a short position

8282014 77

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 78115

The WI market helps in price discoveryIt provides important information on

The strength of demand for the securityAnd on the disparity of biddersrsquo views

This help potential bidders to formulate theirstrategiesAt times a dealer may believe that he hasvery important private information

If so he may not participate in the WI market andwill directly enter the auction with bids based onhis knowledge

8282014 78

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 79115

On or before the date of the auction theissues trade on a yield basis

The actual price can be established only afterthe coupon is set

Starting with the day after the auctionSecurities are quoted on a price basis becausethe coupon is known

8282014 79

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 80115

In a coupon roll a dealer will purchase themost recently issued security from a clientAnd simultaneously sell the same amount ofthe recently announced new security

The first leg with settle on the following dayThe second leg is a forward contract

8282014 80

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 81115

There can be a Reverse RollThe dealer will sell the most recent issue fornext day settlementAnd buy the newly announced security forforward settlement

The forward leg in a RollReverse Roll is a WItrade

It will settle on the new issue settlement date

8282014 81

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 82115

The roll is the spread between the yield onthe new security and that on the outstandingissue in the same maturity segmentA GIVE in the Roll means that

The WI security provides a higher yield than theoutstanding issue

A Take in the Roll means thatThe WI security provides a lower yield

8282014 82

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 83115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 84115

On March 17 20XX the Treasury announcedthe auction of a 2-year note

The auction was scheduled for March 24The settlement date was March 31

Trading of the roll began as soon as the issuewas announcedA Give of 5 bp means that the dealer proposes tobuy the current issue at the prevailing yieldAnd sell the new issue at a yield that is 5 bpmoreA Take of 5 bp means that the dealer proposes tosell the new issue at a yield that is 5bp lower

8282014 84

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 85115

The roll achieves the followingHe acquires the outstanding issue for next daysettlementHe sells the to be issued security with the samepar value for forward delivery on 31 March

The customer is rolling over the investmentfrom the current issue to the new issue

This extends the maturity of the investment byone month

8282014 85

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 86115

The client can invest the funds received tillthe new issue settlesHowever he loses the accrued interest thathe would have earned had he held on to theissue

8282014 86

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 87115

The Treasury per se does not issue zerocoupon securitiesBut zero coupon securities can be created

which are backed by conventional bondsTake a large quantity of a T-note or bond andseparate all the cash flows from each otherSell the entitlement to each cash flowseparately

8282014 87

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 88115

Take the case of a two-year T-noteIt can be separated into five zero couponsecurities maturing after

6 months12 months18 months24 months

8282014 88

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 89115

Earlier investment banks used to buy bondsfrom the Treasury and separate the cashflows

Each cash flow was then sold separately as a zerocoupon bondSuch issues are called trademarks

8282014 89

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 90115

The issue of trademarks has now ceasedBecause investment banks can now createsuch instruments

In concert with the Treasury itselfThese ZCBs are known as STRIPS ndash

Separate Trading of Registered Interest andPrincipal of Securities

These are not issued or sold by the Treasury

The market is made by investment banks

8282014 90

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 91115

What is the motivation to create suchproductsIn practice arbitrage is possible when a

coupon security is purchased at a priceThat is lower than what could be obtained byselling each cash flow separately

8282014 91

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 92115

Coupon stripping reflects a case of financialengineering

Creating a risk-return profile that is nototherwise available

An investment bank would buy a largequantity of a Treasury security

The securities would be placed with an SPV

8282014 92

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 93115

The SPV is a single-purpose dedicated trustIt has the powers to own the bonds andcollect payments

It cannot sell or lend the bondsIt cannot write options on the bondsOr use them as collateral for borrowing

The SPV is empowered to issue zero coupon

bondsWhere each security represents the ownership ofa single cash flow from the mother bond

8282014 93

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 94115

Assume that 100MM USD of 15 year bondswith a coupon of 8 are placed with the SPV

The SPV can issue 6M 12M 18M extending up to14 frac12 year zeroes with a total face value of 4MM

USD eachAnd 15 year zeroes with a total face value of104MM

8282014 94

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 95115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 96115

8282014 96

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 97115

The Treasury launched this program in 1985to facilitate the stripping of designatedsecurities

All new T-bonds and notes with a maturity of 10years or more are eligibleThe zeroes created in the process are directobligations of the US government

8282014 97

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 98115

The mechanism is as followsA dealer who owns a bond or note can ask theFRB where it is held

To replace it with an equivalent set of STRIPS

representing each payment as a separate securityEach of these securities can be traded independentlyof others

8282014 98

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 99115

In 1987 the Treasury started to allow dealersto reverse the process

This is called STRIPS RECONSTUTUTION If a dealer owns STRIPS representing all thecoupon and principal payments of a bond

The FED can on request convert these holdings into asingle position in the corresponding bond

8282014 99

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 100115

Each coupon and principal cash flow from aTreasury security is assigned a CUSIP

The mother bond is also assigned a CUSIPThe stripped coupons are known as C-STRIPSThe stripped principal is known as P-STRIPSSupply of a C-STRIP increases over time

because a C-STRIP maturing on a day like 15 FEB

2020 will have the same CUSIP irrespective ofwhich mother bond it has come fromThe original coupon rate is irrelevant

8282014 100

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 101115

P-STRIPS always correspond to the originalsecurityThey have a unique CUSIPTheir supply is fixed at the time of issuanceIn practice the prices of long-dated P-STRIPSare a bit higher than those of C-STRIPS withthe same maturity date

One reason is that P-STRIPS are more liquid due

to greater availabilityA $100 face value bond with a coupon of 8 willgenerate C-STRIPS with a face value of $4 but P-STRIPS with a face value of $100

8282014 101

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 102115

Another reason why P-STRIPS are in higherdemand is that they allow reconstitutionactivities more easily

Assume that the sum of the STRIPS is cheaper than

the mother bondIf a dealer already has the P-STRIPS only the C-STRIPSneed to be acquiredHowever if he owns some of the C-STRIPS he needs toacquire the P-STRIPS and the remaining C-STRIPSThe facility to reconstitute when profitable is pricedinto the P-STRIPSNote Buy and hold investors will prefer C-STRIPSsince they are priced lower and give a higher yield

8282014 102

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 103115

For Plain Vanilla bonds the specifiedcoupon rate is valid for the life of thebond

In the case of Floaters the rate is reset atthe beginning of every periodThe rate will vary directly with thebenchmark

8282014 103

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 104115

The rate on a Floater is specified as LIBOR+ 50 bp

The spread is positiveIf it were specified as LIBOR ndash 30bp

The spread will be negativeIf LIBOR rises the rate will increasewhereas if LIBOR falls it will decrease

8282014 104

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 105115

In the case of a default risk-free floater theprice will reset to par on a coupon date

It may sell at a premium or discount betweencoupon dates

Consider a floater with a coupon = 5-year T-Bond rate

Assume there are two periods left to maturity

8282014 105

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 106115

8282014 106

The price at the end of the first coupon period willbe given by

cT-1 is the coupon one period before maturityyT-1 is the YTM one period before maturity

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 107115

On a coupon reset date the YTM = couponBecause we have assumed there is no default riskAny change in the required yield as reflected inthe prevailing YTM

Will also be reflected in the coupon being setIf coupon = yield the bond should sell at par

Thus P T-1 = M

8282014 107

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 108115

8282014 108

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 109115

Once again at T-2 c T-2 = yT-2 and P T-2 = MThis logic can be applied to a bond with anytime remaining till maturityHowever between two coupon dates theprice may not be equal to par

Consider the valuation at T-2+k

8282014 109

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 110115

8282014 110

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 111115

Although c T-2 was set at T-2 and is equal toyT-2

yT-2+k is determined at T-2+k and will reflect theyield prevailing at that time

Thus yT-2+k need not equal c T-2 and may behigher or lower

Hence between two coupon dates a floater maysell at a premium or discount

8282014 111

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 112115

Now consider a floater characterized bydefault risk

The risk premium required by the market neednot be constant over time

Assume that at the time of issue YTM = 5-year T-note rate + 75bp

The coupon would have been set equal to thisrate and the bond would have been issued at par

8282014 112

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 113115

Six months hence the issue may be perceivedas more risky

YTM = 5-year T-note rate + 95 bpThe coupon will however be set equal to theprevailing 5-year rate + 75 bpIf so the issue will not reset to par at the nextcoupon date

8282014 113

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 114115

Floaters may come with a CAP or a FLOOR orBOTH

The CAP is a maximum coupon rateProtects issuers against rising rates

The FLOOR is a minimum coupon rateProtects investors against falling rates

When there is a spread over LIBORThere is a natural floorLIBOR cannot be less than zero

8282014 114

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 115115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 2115

8282014 2

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 3115

Part-02ABond amp Bond Markets An Introduction

8282014 3

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 4115

What is debtIt is a financial claim

Who issues it

The borrower of fundsFor whom it is a liability

Who holds itThe lender of funds

For whom it is an asset

8282014 4

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 5115

Difference between debt and equityDebt does not confer ownership rightsIt is merely an IOU

A promise to pay interest at periodic intervalsAnd to repay the principal at a pre-specified maturitydate

8282014 5

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 6115

It usually has a finite life spanPerpetual debt is rare

The interest payments are contractualobligations

Borrowers are required to make payments irrespectiveof their financial performance

8282014 6

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 7115

Interest payments to be made before anydividends for equity holders

In the event of liquidationThe claims of debt holders must be settled firstOnly then can equity holders be paid

8282014 7

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 8115

Bonds and debentures are termed as FixedIncome Securities

Once the rate of interest is set at the onset ofthe period for which it is due

It is not a function of the profitability of the firmFailure to pay the promised interest willtantamount to default

8282014 8

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 9115

Bonds may be secured or unsecuredUnsecured debt securities are termed asDebentures in the USUnsecured means no specific assets have beenearmarked as collateralSecured debt requires the firm to earmarkspecific assets as collateralSecured debt holders enjoy priority from thestandpoint of payments

8282014 9

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 10115

Debt securities may be negotiable or non-negotiable

Negotiable securities can be traded in thesecondary market

Can be endorsed by one party in favor of anotherExamples of non-negotiable debt securities

National savings certificatesConventional Time or Fixed deposits

8282014 10

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 11115

The most basic form of a bond is called thePlain Vanilla version

8282014 11

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 12115

This is true for all securities not just for bondsMore complicated versions are said to have`Bells and Whistlesrsquo attached

8282014 12

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 13115

These bonds are slightly differentThe interest rate does not remain fixedIt varies each period based on the reference rate

Short-term reference rate ndash maturity lt 1 yearFloating rate bonds

Longer-term reference rateVariable or adjustable rate bonds

8282014 13

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 14115

Convertible bonds can be converted to sharesof stockCallable bonds can be prematurely retired by

the issuerPutable bonds can be prematurelysurrendered by the holders

8282014 14

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 15115

It is the principal valueAmount payable by the borrower to the lastholder at maturityAmount on which the periodic interest paymentsare calculatedAKA as

Par ValueRedemption Value Maturity ValuePrincipal Value

8282014 15

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 16115

It is the time remaining in the life of thebond

The length of time for which interest has to bepaid as promisedThe the length of time after which the face valuewill be repaidAKA as

MaturityTermTenor

8282014 16

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 171158282014 17

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 18115

The periodic interest payment that has to bemade by the borrower

The coupon rate multiplied by the face valuegives the rupeedollar value of the coupon

8282014 18

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 19115

Most bonds pays coupons on a semi-annual basisTrue in UKUSAustraliaJapanIn European and Eurobond markets annualpayments are the norm

8282014 19

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 20115

In earlier days bonds were accompanied by abooklet of post-dated coupons

Each coupon could be detached and redeemedon the corresponding coupon payment date

Even today bearer bonds come with couponsThe bearer certificate number is mentioned onthe coupon

8282014 20

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 21115

Bond with a face value of $1000The coupon rate is 8 per annum paid semi-annually

So the bond holder will receive1000 x 008

___ = $40 every six months2

8282014 21

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 22115

The rate of return if an investor buys thebond at the prevailing price and holds ittill maturity

In order to get the YTM two conditionsmust be satisfied

The bond must be held till maturity All coupon payments received before maturitymust be reinvested at the YTM

8282014 22

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 23115

At any point in time the YTM may beGreater thanLess than or

Equal to the Coupon RateYTM is the IRR of a bond

8282014 23

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 24115

Bonds involve pure cash flowsSo only ONE REAL POSITIVE YTM

Solution to a Non-Linear equation

Solved iteratively

8282014 24

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 25115

A holder gets a stream of contractuallypromised payments

The value of the bond is the value of this stream

of cash flowsCash flows arising at different points in timecannot be addedCash flows have to be discounted

8282014 25

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 26115

It is a chicken and egg storyIf we know the yield that is required we canquote a priceOnce we acquire the asset at a certain price we

can work out the corresponding yield

8282014 26

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 27115

A bond will pay identical coupons everyperiodAnd will repay the face value at maturity

The periodic cash flows constitutean annuity The terminal face value is a lump

sum payment

8282014 27

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 28115

Bond pays a semi-annual coupon of $C2and has a face value of $MAssume there are N coupons left

And that we are standing on a coupondate

We are assuming that the next coupon is exactlysix months away

The required annual yield is yImplies that the semi-annual yield is y2

8282014 28

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 29115

The present value of the coupon stream is

8282014 29

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 30115

The present value of the face value is

8282014 30

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 31115

So the price of the bond is

8282014 31

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 32115

IBM has issued a bond with a face value of$1000The coupon is 8 per year to be paid on July

15 and January 15 every yearToday is 15 July 2013 and that the bondmatures on 15 January 2033The required yield is 10 per annum

8282014 32

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 33115

JJ ndash 0115FA ndash 0115MS ndash 0115

AO ndash 0115MN ndash 0115JD ndash 0115

8282014 33

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 34115

8282014 34

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 35115

In the example the price is less than theface value

Such a bond is called a Discount Bond

It is trading at a discount from the face valueThe reason is that

The yield is greater than the coupon

8282014 35

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 36115

If the yield were to equal the couponThe bond would sell at PARSuch bonds are called PAR Bonds

If the yield is less than the couponThe price will exceed the face valueSuch bonds are called Premium Bonds

8282014 36

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 37115

As we move from one coupon date to thenext if the YTM were to remain constant

Par bonds would continue to trade at PARPremium bonds will steadily decline in priceDiscount bonds will steadily increase in price

This is called the Pull to Par EffectAt maturity ndash ALL BONDS WILL TRADE AT PAR

8282014 37

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 38115

As we approach maturity the number ofcoupons reduces

The contribution of coupons to price reducesThe contribution of the PV of the face valueincreases

For premium bonds the first effect dominatesThus the price steadily declines

For discount bonds the second effectdominatesThus the price steadily increases

8282014 38

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 39115

A plain vanilla or Bullet Bond pays the entireface value at maturity in a lump sumAmortizing bonds pay the principal in

installmentsThe first payment occurs before maturityThe last payment is made at maturity

8282014 39

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 40115

Consider a 5 year amortizing bond with aface value of $1000 and an annual coupon of8

The annual cash flows are depicted below

8282014 40

Time Cash Flow

1 802 803 3304 3105 540

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 41115

The first two cash flows represent interest ona principal of $1000The third cash flow is interest on $1000 plus

a principal payment of $250The outstanding principal is $750The fourth cash flow is interest on $750 plusa principal payment of $250

The outstanding principal is $500The final cash flow is interest on $500 plusthe remaining principal of $500

8282014 41

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 42115

Some companies issue such bonds becausethe assets being funded have a similar cashflow profile

Second the coupon on such a bond may belower than that of a bullet bondIn the case of a bullet bond the entire principalis due at a single point in timeThere is greater default risk

8282014 42

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 43115

8282014 43

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 44115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 45115

Microsoft is issuing zeroes with 5 years tomaturity and a face value of $10000

The required yield is 10 per annumWhat should be the price

Price is the PV of the face valueIn practice we discount on a semi-annual basis

8282014 45

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 46115

This is to facilitate comparisons withconventional bonds

8282014 46

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 47115

A zero coupon bond can never sell at apremium

It will always trade at a discount prior tomaturityAt maturity it will trade at par

8282014 47

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 48115

If held to maturity a ZCB will always give riseto a capital gainIf sold prior to maturity there may be a

capital gain or a capital lossConsider a bond with 10 years to maturityThe YTM at the time of purchase was 10The cost was $37690

A year later it is sold at a YTM of 12The corresponding price is $35035

8282014 48

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 49115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 50115

A newly established issuerOr an issuer with a relatively virgin productor service

Or a restructured company due to a mergeror following a bankruptcyWill be perceived as more riskyInvestors will demand a high coupon

Such firms are unlikely to have high earningsRevenues will peak only after theproductservice is established

8282014 50

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 51115

They can ill afford high couponsThey may consider a step-up coupon bond

Where the coupon increases as the bond ages

Assume a company can issue a plain vanillaat a coupon of 8 with a maturity of 5 yearsInstead it may opt for a bond

With a coupon of 6 for the first three years

And a coupon of 10 for the last two yearsThis is a Deferred Interest Security

Provides the issuer with breathing room in theearlier years

8282014 51

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 52115

These pay coupons in the form of additionalsecurities and not cash

This offers the issuer time to prepare for cashoutlays

They are used as Mezzanine FinanceThey rank between senior debt and equity in thecapital structureInvestors take more risk as compared to buyersof regular bonds ndash but get higher returnsIssuers can conserve cash in earlier years when itis at a premium

8282014 52

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 53115

8282014 53

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 54115

Fully backed by the federal government ofthe issuing nationConsequently they are virtually devoid ofcredit risk or the risk of defaultThe yield on such securities is a benchmarkfor setting rates on other kinds of debt

8282014 54

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 55115

Treasury securities are issuedTo finance expenses in excess of currentrevenuesTo pay interest on debt accumulated in earlieryears due to deficits in those yearsTo repay past debt issues that are currentlymaturing

The US Treasuries marketIs the largest bond market in the worldIs the most liquid bond market in the world

8282014 55

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 56115

The Treasury issues three categories ofmarketable securities

T-bills are discount securitiesThey are zero coupon securitiesT-notes and T-bonds are sold at face value andpay interest periodically

8282014 56

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 57115

T-bills are issued with a original time tomaturity of one year or less

They are Money market instrumentsThey have maturities of either 1 3 6 or 12months at the time of issue

8282014 57

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 58115

T-notes and T-bonds have a time to maturityexceeding one year at the time of issue

They are capital market instrumentsT-notes have maturities ranging from 1-10 yearsT-bonds have an original maturity in excess of 10years extending up to 30 years

8282014 58

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 59115

An issue may be followed later by a furtherissue

With the same remaining time to maturity andthe same couponThe issuance of further tranches is termed as aRe-opening

8282014 59

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 60115

Six months ago a 10-year note was issuedwith a coupon of 8 per annumToday if a note with 9 frac12 years to maturityand a coupon of 8 issued it will add to thepool that is already trading in the marketThus it is a re-opening of an existing issue

8282014 60

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 61115

Who is a primary dealerA PD is a dealer who is authorized to dealdirectly with the Central Bank of the countryIn the US a PD is a bank or securities broker-dealer that directly deals with the FRBNY

Importance of FRBNYIn India a PD deals directly with the RBI

8282014 61

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 62115

8282014 62

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 63115

The Treasury sells bills notes and bonds byway of a competitive auction process

Most of the treasury securities are bought byprimary dealers

Individual investors submit non-competitive bidsand participate on a much smaller scale

8282014 63

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 64115

Bids may beCompetitive

Indicate price amp quantity or yield amp quantityNon-competitive

Indicate only quantity

Small investors and individualsgenerally submit non-competitive bids

A non-competitive bidder may not bid for more than$5MM worth of securities in a bill or bond auction

8282014 64

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 65115

Primary dealers bid for their accounts andon behalf of their clientsThey usually submit large competitive

bidsBids indicate the maximum price that the bidderis prepared to pay if it is a price based auctionOr the minimum yield that the bidder is

prepared to accept if it is a yield based auction

8282014 65

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 66115

The Treasury will net out the totalamount of non-competitive bids

The balance will be allocated to competitivebidders

There are two ways in which securitiescan be allotted

The multiple priceyield auction mechanism

French AuctionsThe uniform priceyield auction mechanism

Dutch Auctions

8282014 66

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 67115

Assume that the Treasury is offering 25billion dollars worth of T-bonds

2 billion dollars worth of non-competitive bidshave been receivedSo 23 billion dollars worth of bonds are availableto be offered to the competitive bidders

8282014 67

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 68115

There are six competitive bidders who havesubmitted the following yields

The bids have been arranged in ascending orderof yieldIn a price based auction the bids would havebeen arranged in descending order of price

8282014 68

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 69115

Bidder Bid Yield Bid Amount

Aggregate Amount

Alpha 5370 30 bn 30 bnBeta 5372 50 bn 80 bn

Gamma 5373 40 bn 12 bn

Delta 5375 80 bn 20 bnCharlie 5375 120 bn 32 bn

Tango 5380 30 bn 35 bn8282014 69

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 70115

The aggregate demand equals the amount onoffer at a yield of 5375A multiple yield auction will lead to thefollowing allocation

Alpha will get 3 bn at a yield of 5370Beta will get 5 bn at 5372Gamma will get 4 bn at 5373

8282014 70

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 71115

At a yield of 5375 we have only 11 bn left toallocateThere is a demand of 20 bn at this yield

8 bn from Delta and 12 bn from CharlieThus we will allocate 1120 = 55 to eachbidder at this yield

There will be pro-rata allocation

055 of 8 bn or 440 bn will go to Delta055 of 12 bn or 66 bn will go to Charlie

8282014 71

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 72115

The highest accepted yield is called the StopYield or High Yield

In this case it is 5375The ratio of bids received to the amountawarded is known as the bid to cover ratio

The higher the ratio the stronger is the auction

8282014 72

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 73115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 74115

Those who bid more than 5375 will getnothing and are said to be shutout of theauctionSince 1999 the US Treasury has beenconducting only uniform yield auctions

8282014 74

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 75115

WI stands for ndash When As and If IssuedThe when issued market is a market forforward trading of a bond

Which has been announced but not yet issuedTrades take place from the date ofannouncement until the actual issue date

Helps bidders to gauge the marketrsquos interestbefore the actual auction

8282014 75

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 76115

WI trading has ramifications for the biddingstrategies of market participantsTraders can take both long and shortpositions

Settlement is scheduled for the issue date

8282014 76

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 77115

It has a bearing on the outcome of theauction

It affects the strategy used by a bidder becauseit has an impact on his prior positionBidders who are long in the WI market enter theauction with a Long PositionThose who are short in the WI market enter theauction with a short position

8282014 77

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 78115

The WI market helps in price discoveryIt provides important information on

The strength of demand for the securityAnd on the disparity of biddersrsquo views

This help potential bidders to formulate theirstrategiesAt times a dealer may believe that he hasvery important private information

If so he may not participate in the WI market andwill directly enter the auction with bids based onhis knowledge

8282014 78

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 79115

On or before the date of the auction theissues trade on a yield basis

The actual price can be established only afterthe coupon is set

Starting with the day after the auctionSecurities are quoted on a price basis becausethe coupon is known

8282014 79

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 80115

In a coupon roll a dealer will purchase themost recently issued security from a clientAnd simultaneously sell the same amount ofthe recently announced new security

The first leg with settle on the following dayThe second leg is a forward contract

8282014 80

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 81115

There can be a Reverse RollThe dealer will sell the most recent issue fornext day settlementAnd buy the newly announced security forforward settlement

The forward leg in a RollReverse Roll is a WItrade

It will settle on the new issue settlement date

8282014 81

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 82115

The roll is the spread between the yield onthe new security and that on the outstandingissue in the same maturity segmentA GIVE in the Roll means that

The WI security provides a higher yield than theoutstanding issue

A Take in the Roll means thatThe WI security provides a lower yield

8282014 82

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 83115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 84115

On March 17 20XX the Treasury announcedthe auction of a 2-year note

The auction was scheduled for March 24The settlement date was March 31

Trading of the roll began as soon as the issuewas announcedA Give of 5 bp means that the dealer proposes tobuy the current issue at the prevailing yieldAnd sell the new issue at a yield that is 5 bpmoreA Take of 5 bp means that the dealer proposes tosell the new issue at a yield that is 5bp lower

8282014 84

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 85115

The roll achieves the followingHe acquires the outstanding issue for next daysettlementHe sells the to be issued security with the samepar value for forward delivery on 31 March

The customer is rolling over the investmentfrom the current issue to the new issue

This extends the maturity of the investment byone month

8282014 85

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 86115

The client can invest the funds received tillthe new issue settlesHowever he loses the accrued interest thathe would have earned had he held on to theissue

8282014 86

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 87115

The Treasury per se does not issue zerocoupon securitiesBut zero coupon securities can be created

which are backed by conventional bondsTake a large quantity of a T-note or bond andseparate all the cash flows from each otherSell the entitlement to each cash flowseparately

8282014 87

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 88115

Take the case of a two-year T-noteIt can be separated into five zero couponsecurities maturing after

6 months12 months18 months24 months

8282014 88

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 89115

Earlier investment banks used to buy bondsfrom the Treasury and separate the cashflows

Each cash flow was then sold separately as a zerocoupon bondSuch issues are called trademarks

8282014 89

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 90115

The issue of trademarks has now ceasedBecause investment banks can now createsuch instruments

In concert with the Treasury itselfThese ZCBs are known as STRIPS ndash

Separate Trading of Registered Interest andPrincipal of Securities

These are not issued or sold by the Treasury

The market is made by investment banks

8282014 90

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 91115

What is the motivation to create suchproductsIn practice arbitrage is possible when a

coupon security is purchased at a priceThat is lower than what could be obtained byselling each cash flow separately

8282014 91

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 92115

Coupon stripping reflects a case of financialengineering

Creating a risk-return profile that is nototherwise available

An investment bank would buy a largequantity of a Treasury security

The securities would be placed with an SPV

8282014 92

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 93115

The SPV is a single-purpose dedicated trustIt has the powers to own the bonds andcollect payments

It cannot sell or lend the bondsIt cannot write options on the bondsOr use them as collateral for borrowing

The SPV is empowered to issue zero coupon

bondsWhere each security represents the ownership ofa single cash flow from the mother bond

8282014 93

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 94115

Assume that 100MM USD of 15 year bondswith a coupon of 8 are placed with the SPV

The SPV can issue 6M 12M 18M extending up to14 frac12 year zeroes with a total face value of 4MM

USD eachAnd 15 year zeroes with a total face value of104MM

8282014 94

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 95115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 96115

8282014 96

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 97115

The Treasury launched this program in 1985to facilitate the stripping of designatedsecurities

All new T-bonds and notes with a maturity of 10years or more are eligibleThe zeroes created in the process are directobligations of the US government

8282014 97

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 98115

The mechanism is as followsA dealer who owns a bond or note can ask theFRB where it is held

To replace it with an equivalent set of STRIPS

representing each payment as a separate securityEach of these securities can be traded independentlyof others

8282014 98

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 99115

In 1987 the Treasury started to allow dealersto reverse the process

This is called STRIPS RECONSTUTUTION If a dealer owns STRIPS representing all thecoupon and principal payments of a bond

The FED can on request convert these holdings into asingle position in the corresponding bond

8282014 99

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 100115

Each coupon and principal cash flow from aTreasury security is assigned a CUSIP

The mother bond is also assigned a CUSIPThe stripped coupons are known as C-STRIPSThe stripped principal is known as P-STRIPSSupply of a C-STRIP increases over time

because a C-STRIP maturing on a day like 15 FEB

2020 will have the same CUSIP irrespective ofwhich mother bond it has come fromThe original coupon rate is irrelevant

8282014 100

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 101115

P-STRIPS always correspond to the originalsecurityThey have a unique CUSIPTheir supply is fixed at the time of issuanceIn practice the prices of long-dated P-STRIPSare a bit higher than those of C-STRIPS withthe same maturity date

One reason is that P-STRIPS are more liquid due

to greater availabilityA $100 face value bond with a coupon of 8 willgenerate C-STRIPS with a face value of $4 but P-STRIPS with a face value of $100

8282014 101

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 102115

Another reason why P-STRIPS are in higherdemand is that they allow reconstitutionactivities more easily

Assume that the sum of the STRIPS is cheaper than

the mother bondIf a dealer already has the P-STRIPS only the C-STRIPSneed to be acquiredHowever if he owns some of the C-STRIPS he needs toacquire the P-STRIPS and the remaining C-STRIPSThe facility to reconstitute when profitable is pricedinto the P-STRIPSNote Buy and hold investors will prefer C-STRIPSsince they are priced lower and give a higher yield

8282014 102

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 103115

For Plain Vanilla bonds the specifiedcoupon rate is valid for the life of thebond

In the case of Floaters the rate is reset atthe beginning of every periodThe rate will vary directly with thebenchmark

8282014 103

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 104115

The rate on a Floater is specified as LIBOR+ 50 bp

The spread is positiveIf it were specified as LIBOR ndash 30bp

The spread will be negativeIf LIBOR rises the rate will increasewhereas if LIBOR falls it will decrease

8282014 104

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 105115

In the case of a default risk-free floater theprice will reset to par on a coupon date

It may sell at a premium or discount betweencoupon dates

Consider a floater with a coupon = 5-year T-Bond rate

Assume there are two periods left to maturity

8282014 105

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 106115

8282014 106

The price at the end of the first coupon period willbe given by

cT-1 is the coupon one period before maturityyT-1 is the YTM one period before maturity

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 107115

On a coupon reset date the YTM = couponBecause we have assumed there is no default riskAny change in the required yield as reflected inthe prevailing YTM

Will also be reflected in the coupon being setIf coupon = yield the bond should sell at par

Thus P T-1 = M

8282014 107

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 108115

8282014 108

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 109115

Once again at T-2 c T-2 = yT-2 and P T-2 = MThis logic can be applied to a bond with anytime remaining till maturityHowever between two coupon dates theprice may not be equal to par

Consider the valuation at T-2+k

8282014 109

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 110115

8282014 110

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 111115

Although c T-2 was set at T-2 and is equal toyT-2

yT-2+k is determined at T-2+k and will reflect theyield prevailing at that time

Thus yT-2+k need not equal c T-2 and may behigher or lower

Hence between two coupon dates a floater maysell at a premium or discount

8282014 111

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 112115

Now consider a floater characterized bydefault risk

The risk premium required by the market neednot be constant over time

Assume that at the time of issue YTM = 5-year T-note rate + 75bp

The coupon would have been set equal to thisrate and the bond would have been issued at par

8282014 112

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 113115

Six months hence the issue may be perceivedas more risky

YTM = 5-year T-note rate + 95 bpThe coupon will however be set equal to theprevailing 5-year rate + 75 bpIf so the issue will not reset to par at the nextcoupon date

8282014 113

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 114115

Floaters may come with a CAP or a FLOOR orBOTH

The CAP is a maximum coupon rateProtects issuers against rising rates

The FLOOR is a minimum coupon rateProtects investors against falling rates

When there is a spread over LIBORThere is a natural floorLIBOR cannot be less than zero

8282014 114

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 115115

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 3115

Part-02ABond amp Bond Markets An Introduction

8282014 3

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 4115

What is debtIt is a financial claim

Who issues it

The borrower of fundsFor whom it is a liability

Who holds itThe lender of funds

For whom it is an asset

8282014 4

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 5115

Difference between debt and equityDebt does not confer ownership rightsIt is merely an IOU

A promise to pay interest at periodic intervalsAnd to repay the principal at a pre-specified maturitydate

8282014 5

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 6115

It usually has a finite life spanPerpetual debt is rare

The interest payments are contractualobligations

Borrowers are required to make payments irrespectiveof their financial performance

8282014 6

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 7115

Interest payments to be made before anydividends for equity holders

In the event of liquidationThe claims of debt holders must be settled firstOnly then can equity holders be paid

8282014 7

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 8115

Bonds and debentures are termed as FixedIncome Securities

Once the rate of interest is set at the onset ofthe period for which it is due

It is not a function of the profitability of the firmFailure to pay the promised interest willtantamount to default

8282014 8

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 9115

Bonds may be secured or unsecuredUnsecured debt securities are termed asDebentures in the USUnsecured means no specific assets have beenearmarked as collateralSecured debt requires the firm to earmarkspecific assets as collateralSecured debt holders enjoy priority from thestandpoint of payments

8282014 9

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 10115

Debt securities may be negotiable or non-negotiable

Negotiable securities can be traded in thesecondary market

Can be endorsed by one party in favor of anotherExamples of non-negotiable debt securities

National savings certificatesConventional Time or Fixed deposits

8282014 10

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 11115

The most basic form of a bond is called thePlain Vanilla version

8282014 11

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 12115

This is true for all securities not just for bondsMore complicated versions are said to have`Bells and Whistlesrsquo attached

8282014 12

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 13115

These bonds are slightly differentThe interest rate does not remain fixedIt varies each period based on the reference rate

Short-term reference rate ndash maturity lt 1 yearFloating rate bonds

Longer-term reference rateVariable or adjustable rate bonds

8282014 13

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 14115

Convertible bonds can be converted to sharesof stockCallable bonds can be prematurely retired by

the issuerPutable bonds can be prematurelysurrendered by the holders

8282014 14

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 15115

It is the principal valueAmount payable by the borrower to the lastholder at maturityAmount on which the periodic interest paymentsare calculatedAKA as

Par ValueRedemption Value Maturity ValuePrincipal Value

8282014 15

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 16115

It is the time remaining in the life of thebond

The length of time for which interest has to bepaid as promisedThe the length of time after which the face valuewill be repaidAKA as

MaturityTermTenor

8282014 16

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 171158282014 17

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 18115

The periodic interest payment that has to bemade by the borrower

The coupon rate multiplied by the face valuegives the rupeedollar value of the coupon

8282014 18

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 19115

Most bonds pays coupons on a semi-annual basisTrue in UKUSAustraliaJapanIn European and Eurobond markets annualpayments are the norm

8282014 19

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 20115

In earlier days bonds were accompanied by abooklet of post-dated coupons

Each coupon could be detached and redeemedon the corresponding coupon payment date

Even today bearer bonds come with couponsThe bearer certificate number is mentioned onthe coupon

8282014 20

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 21115

Bond with a face value of $1000The coupon rate is 8 per annum paid semi-annually

So the bond holder will receive1000 x 008

___ = $40 every six months2

8282014 21

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 22115

The rate of return if an investor buys thebond at the prevailing price and holds ittill maturity

In order to get the YTM two conditionsmust be satisfied

The bond must be held till maturity All coupon payments received before maturitymust be reinvested at the YTM

8282014 22

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 23115

At any point in time the YTM may beGreater thanLess than or

Equal to the Coupon RateYTM is the IRR of a bond

8282014 23

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 24115

Bonds involve pure cash flowsSo only ONE REAL POSITIVE YTM

Solution to a Non-Linear equation

Solved iteratively

8282014 24

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 25115

A holder gets a stream of contractuallypromised payments

The value of the bond is the value of this stream

of cash flowsCash flows arising at different points in timecannot be addedCash flows have to be discounted

8282014 25

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 26115

It is a chicken and egg storyIf we know the yield that is required we canquote a priceOnce we acquire the asset at a certain price we

can work out the corresponding yield

8282014 26

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 27115

A bond will pay identical coupons everyperiodAnd will repay the face value at maturity

The periodic cash flows constitutean annuity The terminal face value is a lump

sum payment

8282014 27

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 28115

Bond pays a semi-annual coupon of $C2and has a face value of $MAssume there are N coupons left

And that we are standing on a coupondate

We are assuming that the next coupon is exactlysix months away

The required annual yield is yImplies that the semi-annual yield is y2

8282014 28

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 29115

The present value of the coupon stream is

8282014 29

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 30115

The present value of the face value is

8282014 30

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 31115

So the price of the bond is

8282014 31

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 32115

IBM has issued a bond with a face value of$1000The coupon is 8 per year to be paid on July

15 and January 15 every yearToday is 15 July 2013 and that the bondmatures on 15 January 2033The required yield is 10 per annum

8282014 32

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 33115

JJ ndash 0115FA ndash 0115MS ndash 0115

AO ndash 0115MN ndash 0115JD ndash 0115

8282014 33

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 34115

8282014 34

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 35115

In the example the price is less than theface value

Such a bond is called a Discount Bond

It is trading at a discount from the face valueThe reason is that

The yield is greater than the coupon

8282014 35

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 36115

If the yield were to equal the couponThe bond would sell at PARSuch bonds are called PAR Bonds

If the yield is less than the couponThe price will exceed the face valueSuch bonds are called Premium Bonds

8282014 36

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 37115

As we move from one coupon date to thenext if the YTM were to remain constant

Par bonds would continue to trade at PARPremium bonds will steadily decline in priceDiscount bonds will steadily increase in price

This is called the Pull to Par EffectAt maturity ndash ALL BONDS WILL TRADE AT PAR

8282014 37

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 38115

As we approach maturity the number ofcoupons reduces

The contribution of coupons to price reducesThe contribution of the PV of the face valueincreases

For premium bonds the first effect dominatesThus the price steadily declines

For discount bonds the second effectdominatesThus the price steadily increases

8282014 38

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 39115

A plain vanilla or Bullet Bond pays the entireface value at maturity in a lump sumAmortizing bonds pay the principal in

installmentsThe first payment occurs before maturityThe last payment is made at maturity

8282014 39

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 40115

Consider a 5 year amortizing bond with aface value of $1000 and an annual coupon of8

The annual cash flows are depicted below

8282014 40

Time Cash Flow

1 802 803 3304 3105 540

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 41115

The first two cash flows represent interest ona principal of $1000The third cash flow is interest on $1000 plus

a principal payment of $250The outstanding principal is $750The fourth cash flow is interest on $750 plusa principal payment of $250

The outstanding principal is $500The final cash flow is interest on $500 plusthe remaining principal of $500

8282014 41

8112019 FISD-02-A

httpslidepdfcomreaderfullfisd-02-a 42115