Fiscal Impact Analysis: New Methods, New Data and Best Practices

53

Fiscal Impact Analysis: New Methods, New Data and Best Practices NJ-APA Conference, New Brunswick Fiscal Impact Analysis New Methods, New Data and Best Practices Speakers Steven L. Nelson, AICP, Econsult Solutions, Inc. Peter Angelides, AICP, Ph.D., Econsult Solutions, Inc. Charles Heydt, AICP, Dresdner Robin Sidney Wong, Ph.D., Community Data Analytics American Planning Association The New Jersey Chapter Conference January 26, 2017 New Brunswick

-

Upload

econsult-solutions -

Category

Economy & Finance

-

view

246 -

download

2

Transcript of Fiscal Impact Analysis: New Methods, New Data and Best Practices

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Fiscal Impact Analysis New Methods, New Data and Best

Practices

Speakers

Steven L. Nelson, AICP, Econsult Solutions, Inc.

Peter Angelides, AICP, Ph.D., Econsult Solutions, Inc.

Charles Heydt, AICP, Dresdner Robin

Sidney Wong, Ph.D., Community Data Analytics

American Planning Association The New Jersey Chapter Conference

January 26, 2017 New Brunswick

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Introduction

• Fiscal Impact Analysis Methods and

Issues

• Demographic Multipliers in New

Jersey

• Reverse Fiscal Impact Analysis

• Discussions

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Fiscal Impact Analysis

Methods and Issues

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Why Do We Care about Development Impacts?

• Fiscal

• Economic

• School

• Traffic

• Environment

• Social

• Political

• Others

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Fiscal Benefits

• Property tax revenues

• Local wage tax revenues

• Sales tax revenues

• Other levies

• User charges, fees and fines

• Increment of property values / tax base

expansion

• Others

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Fiscal Costs

• School expenditures

• Government operating expenses

• Capital improvement costs

• Traffic improvement expenditures

• Debt financing

• Others

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Fiscal Impact Analysis

“[a] projection of the direct, current,

public costs, and revenues

associated with residential or

nonresidential growth to the local

jurisdiction(s) in which this growth is

taking place.”

Page 1,

Burchell, Robert W. and David

Listokin, 1978.

The Fiscal Impact Handbook Source: http://www.transactionpub.com/title/The-Complete-Illustrated-Book-of-Development-Definitions-978-1-4128-5504-4.html

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

“Is growth good or bad for my

for community?” • It depends…

• Development generates a host of new costs for

a municipality.

• Also generates new revenues.

• It is important that municipalities determine if

the new revenues offset the associated costs.

• FIA can help elected officials make fiscally sound land use decisions.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

The Uses of FIA

• Planning Applications of FIA include: – Land use policies

– Rezonings

– Annexations/Acquisitions

– Redevelopment

• Budget and Finance Applications – Capital improvement programming

– Revenue forecasting

– Fiscal planning

– Level of service changes

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Methods of Fiscal Impact

Analysis • There are number of standard approaches to

choose from.

• For revenues, determine local assessment approach or industry standard.

• For costs, the two most common include: – The Average Cost approach

– The Marginal Cost approach

• The distinction between the two is fundamental to FIA.

• They may result in dramatically different estimates of the fiscal impacts.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

The Hybrid Cost Approach

• Combines the Average Cost approach with

a case study analysis.

• The Average Cost approach is used to

calculate per-capita costs and revenues.

• The case studies are used to identify areas of

capacity constraints.

– This helps bring in the benefits of the Marginal

Approach.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Steps of Fiscal Impact Analysis

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

FIA Steps

• Step 1: Estimate the number of

residents and/or employees

– Total population

– School-Age Children

Based on the type of housing units

– PUMS data provides the most up-to-date

information

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

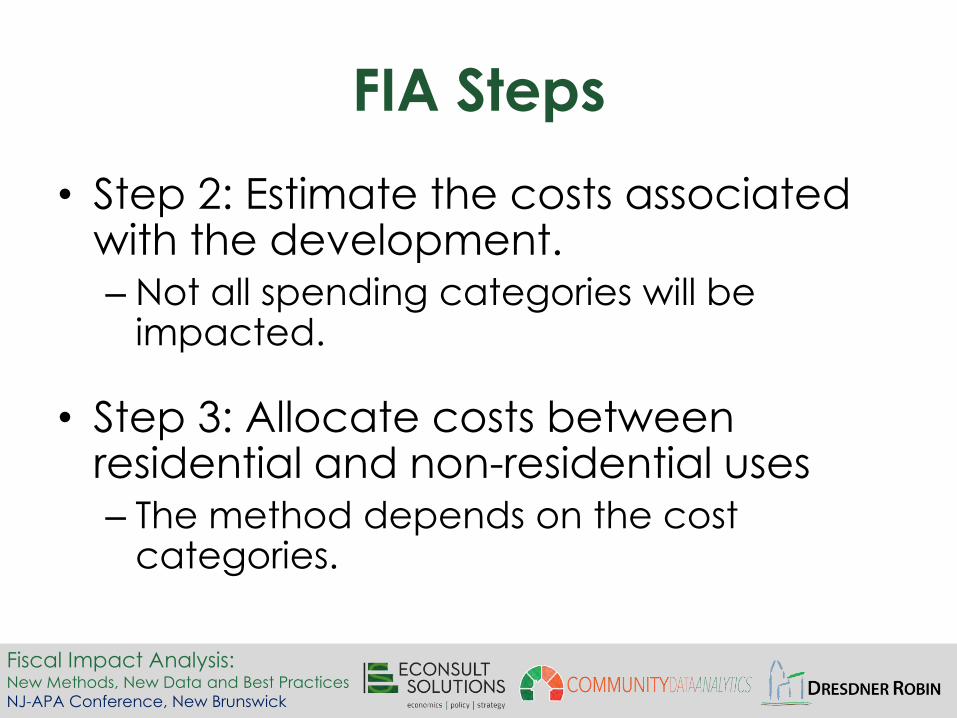

FIA Steps

• Step 2: Estimate the costs associated with the development. – Not all spending categories will be

impacted.

• Step 3: Allocate costs between residential and non-residential uses – The method depends on the cost

categories.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

FIA Steps

• Step 4: Derive per-capita, per-student,

per-employee expenditure estimates

• Step 5: Sum Total Costs

– Operating costs vs. capital costs

– Use case studies and interviews to

understand potential capital costs

• Step 6: Assess need for new capacity

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

FIA Steps

• Step 7: Estimate the revenues

associated with the project.

– Property tax vs. other revenues

• Step 8: Allocate other revenue to land

uses

– Estimate per-capita and per-employee

revenues

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

FIA Steps

• Step 9: Sum Total Revenues

– Property taxes

– Other revenues

– One-time revenue

• Step 10: Calculate the Net-fiscal

impacts

– Revenues - costs

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Potential Issues

• Property Tax Abatements – Could pose an issue for the period where

any taxes are abated.

• As if first “fully” occupied.

• The outputs are only as good as the inputs.

• Critical data for estimating impacts.

• Link between revenues and taxes.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

• Local Data – Office of Budget/Finance – Tax Assessor

– Clerk’s Office

• State Data – Department of Consumer Affairs

– Department of Education

– Department of Labor and Workforce Development

– Department of Treasury

• Federal Data – Census

– American Community Survey - PUMS

General Data Resources

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Estimate Impacts

With a focus on

Demographic Multipliers

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Per household

Demographic Multipliers Occupants • Household Size

• Age Breakdown

Housing Types

• Structure Types

• Number of Bedrooms

• Rental or Owned

• Year Structure Built

• Other attributes

School

• School-Age Children

• Public School Attendees

Traffic

• Number of Cars Available

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Traditional Demographic

Multiplier

• Developed at Rutgers by Professors Robert

Burchell and David Listokin in the 1980s.

• State level data (except 3 sub-state regions

for NJ)

• The last series is based on 2000 Census PUMS,

i.e. information in the 1990s.

• Sample of occupied units built between

1990 and 2000.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Possible Data Sources

• Census (Summary 1 File)

• American Community Survey

• American Housing Survey

• Customized Survey

• Administrative Records

• Public Use Microdata Sample

X

X

X

X

X

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Public Use Microdata Sample

Viable, robust and workable

but not so easy to use

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Public Use Microdata Sample

(PUMS)

• ACS raw data: Un-tabulated records about individuals,

households, and housing units.

• Released every year, sample size:1% per year.

• 1-year, 3-year, and 5-year samples.

• 2011-2015 5-year PUMS just released on January 19,

2017.

• Geographic Areas: Region, Division, State, and

PUMA.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Public Use Microdata Areas

(PUMA)

• A PUMA represents at least 100,000 residents, but

can be up to 200,000

• Size depends on population density.

• Revised after each decennial census.

• 73 PUMAs in New Jersey, their 2010 population total

is 8.8 million persons (100% coverage)

• 8 PUMAs in Bergen County, 2 in Jersey City, 2 in

Newark City.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

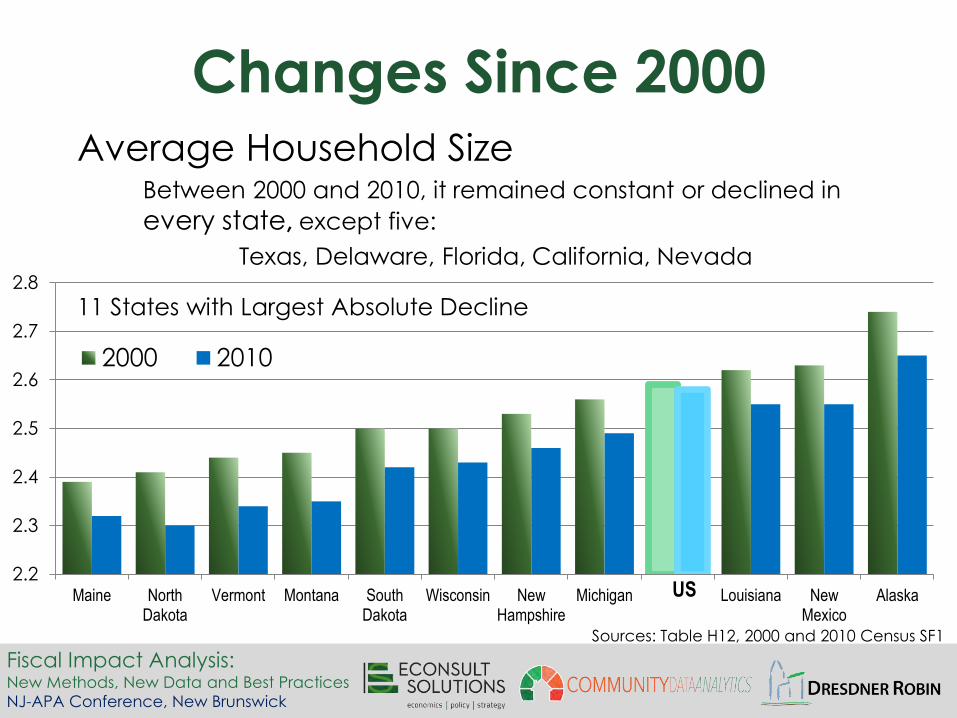

Changes Since 2000 Average Household Size

Between 2000 and 2010, it remained constant or declined in

every state, except five:

Texas, Delaware, Florida, California, Nevada

2.2

2.3

2.4

2.5

2.6

2.7

2.8

Maine NorthDakota

Vermont Montana SouthDakota

Wisconsin NewHampshire

Michigan US Louisiana NewMexico

Alaska

2000 2010

US

11 States with Largest Absolute Decline

Sources: Table H12, 2000 and 2010 Census SF1

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Current Demographic Multipliers

and Planning Ratios

Changes since 2000

Local Variations

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

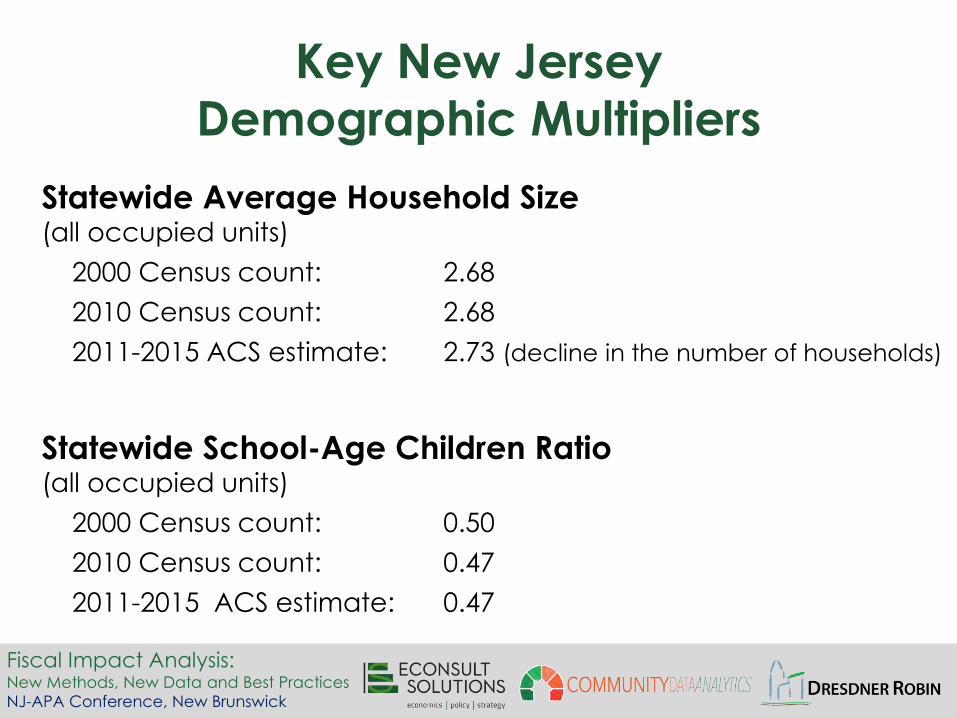

Key New Jersey

Demographic Multipliers

Statewide Average Household Size (all occupied units)

2000 Census count: 2.68

2010 Census count: 2.68

2011-2015 ACS estimate: 2.73 (decline in the number of households)

Statewide School-Age Children Ratio (all occupied units)

2000 Census count: 0.50

2010 Census count: 0.47

2011-2015 ACS estimate: 0.47

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

0.0

0.5

1.0 2000 20142-Bedroom Units

School-Age Children Ratio New Jersey State Level, New Units Sample,

Sources: Community Data Analytics (2017), based on 2000 Census and 2010-2014 5-Year ACS-PUMS Fannie Mae Foundation (2006), Residential Demographic Multipliers, New Jersey Table 2

0.0

0.5

1.0

1.5

SF

Attached

SF

Detached

MF2-4 MF5+ MF5+

Owned

MF5+

Rented

All Owned All Rented

3-Bedroom Units

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Improved New Residents Sample

2014 New Jersey State Level

Scatterplot, 0 to 4 Bedroom Units • New units sample is a subset of

new residents sample.

• New units sample size

fluctuates – housing market.

• New units sample is less reliable.

• New residents sample reflects

long-term effects.

• New residents sample has

slightly larger value except for

units with 5 or more bedrooms.

1

2

3

4

5

1 2 3 4 5

Ne

w U

nits

Sa

mp

le

New Residents Sample Source: Community Data Analytics (2017),

based on 2010-2014 5-Year ACS-PUMS

Pearson R = 0.988

N = 72

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Selected PUMAs in New Jersey

• Geography: From different parts of the state

• Counties: 17 PUMAs from 13 counties

• Development density: City, suburb/exurb, shore, rural

• These 17 PUMAs represent a population of 2 million

(2010), or 23% of NJ population.

• Population ranges from 100,700 (Plainfield City) to

188,400 (East Orange City)

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

New Brunswick

New Jersey

North

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

New Jersey

South

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

PUMA Level, New Residents Sample

New Jersey Local Variations: School-Age Children

Occupied Units, all Bedroom Size

Source: Community Data Analytics (2017), based on 2010-2014 5-Year ACS-PUMS

0

0.2

0.4

0.6

0.8

101 304 306 601 701 901 906 1003 1103 1205 1302 1404 1700 2002 2301 2303 2500 NJ

Owned Rented

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

0.0

0.5

1.0

PUMA Level, New Residents Sample

New Jersey Local Variations: School-Age Children

Source: Community Data Analytics (2017), based on 2010-2014 5-Year ACS-PUMS

All 2-Bedroom Multifamily Units

0.0

0.5

1.0

101 304 306 601 701 901 906 1003 1103 1205 1302 1404 1700 2002 2301 2303 2500 NJ

3-Bedroom Single Family Detached Units

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse Fiscal Impact Analysis

Innovative tool in property buy-outs

and acquisition proposals

Disaster prone areas

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse Fiscal Impact Analysis

• Reverse FIA is tool for decision-makers

• Hazard mitigation strategy analysis

• Targeted tool for targeted audience

• Focus on fiscal impacts (excludes public

safety/health considerations)

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

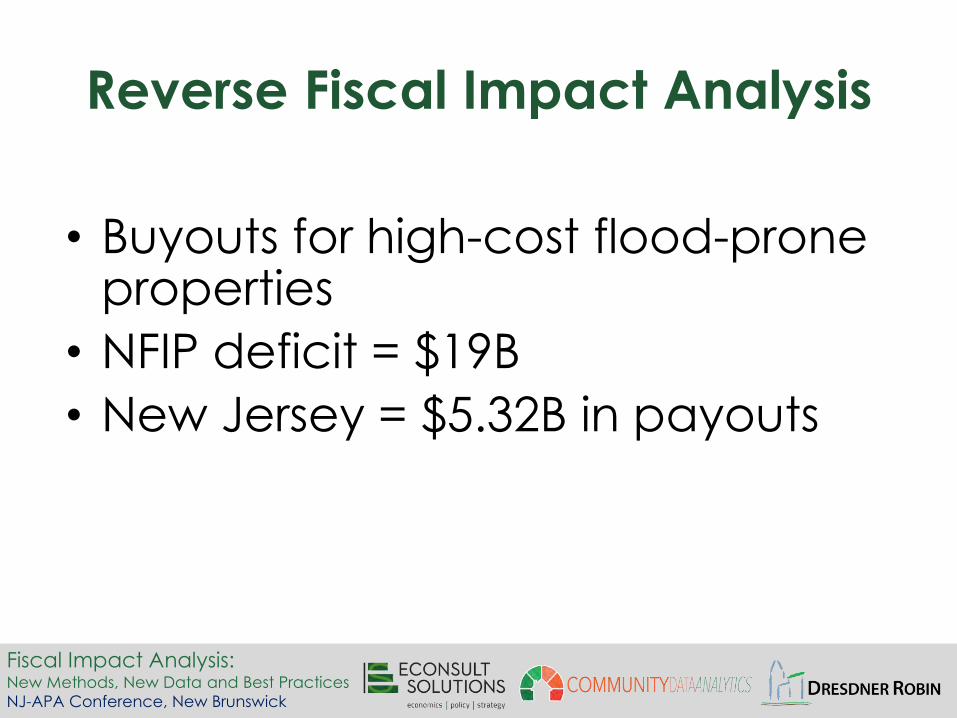

Reverse Fiscal Impact Analysis

• Buyouts for high-cost flood-prone properties

• NFIP deficit = $19B

• New Jersey = $5.32B in payouts

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse FIA Framework

• FIA estimates new construction & development

• Reverse FIA estimates loss of development &

“de-construction.”

• Uses real data

• Reduced population = reduced demand for

services

• Typically uses avg. cost method

• Does not include “induced impacts.”

• Does not include acquisition & demo costs.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse FIA Framework

Traditional

• Revenue (taxes, fees,

non-local)

• Costs (municipal

services, education,

debt service)

Reverse FIA

• Costs (revenue lost

from taxes, fees, etc.)

• Revenue (cost savings

from lower demand for

services)

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse Fiscal Impact

Methodology 1. Determine geographic area.

2. Identify & quantify type of properties & values.

3. Estimate existing costs by type of property, number of

residents, workers, school children.

4. Estimate losses of residents, workers, school kids.

5. Estimate total revenue loss.

6. Estimate cost savings.

7. Apply sensitivity analysis.

8. Final impact estimate(s).

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Simplified Example of Reverse FIA 1. Geographic Area:

– 11 properties;

• 10 residential, 1 non-residential

2. Identify & Quantify Values and Population:

– Assessed value = $1,5000,000;

• $1,000,000 for residential, $500,000 for non-residential.

– 30 residents, 2 school kids, 5 workers

3. Estimate Existing Costs:

– $900/resident, $100/worker, $13000/child

4. Project Losses

– Residents, school kids, workers

– Revenue to municipality and school district

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Simplified Example (cont’d)

5. Revenue lost

• Municipal revenue loss:

10 homes x $100,000 + 1 non-residential property x $500,000 x 0.005

(municipal tax rate)

= $5,000 + $2,500 = $7,500

• School District revenue loss:

10 homes x $100,000 + 1 commercial property x $500,000 x 0.01

(school tax rate)

= $5,000 + $10,000 = $15,000

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Simplified Example (cont’d)

6. Estimate Cost Savings

• Municipal:

30 persons x $900 + 5 workers x $100 = $27,000

+ $500 = $27,500

• School District:

2 children x $13000 x .5 (share of budget from

local tax) = $13,000

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Simplified Example (cont’d) 7. Sensitivity Analysis

• Muni: $27,500 (cost savings) - $7,500 (lost revenue) =

$20,000 potential savings

If muni can save 50% of potential cost savings = $6,250

If muni can save 10% of potential savings = -$4,750

• School District: $13,000 (cost savings) - $15,000 (lost revenue) =

-$2,000 potential cost

If School District can save 50% of potential savings = -$6,500

If School District can save 10% of cost savings = - $14,700

• Interview key staff

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Sea Bright Borough

• 198 residential units, 21

commercial properties,

municipal impact only.

• $85,000 (savings) (50% of

savings realized)

• -$208,000 (cost) (25% of

savings realized)

2050 Sea Level Rise

Examples of Reverse FIA

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Examples of Reverse FIA

• 100 to 500 residential

properties, municipal

and primary school

impact only.

• Municipal impact:

- $70,000 to -$515,000

(cost)

• Primary School District

impact:

- $37,000 to - $363,000

(cost)

Mystic Island

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

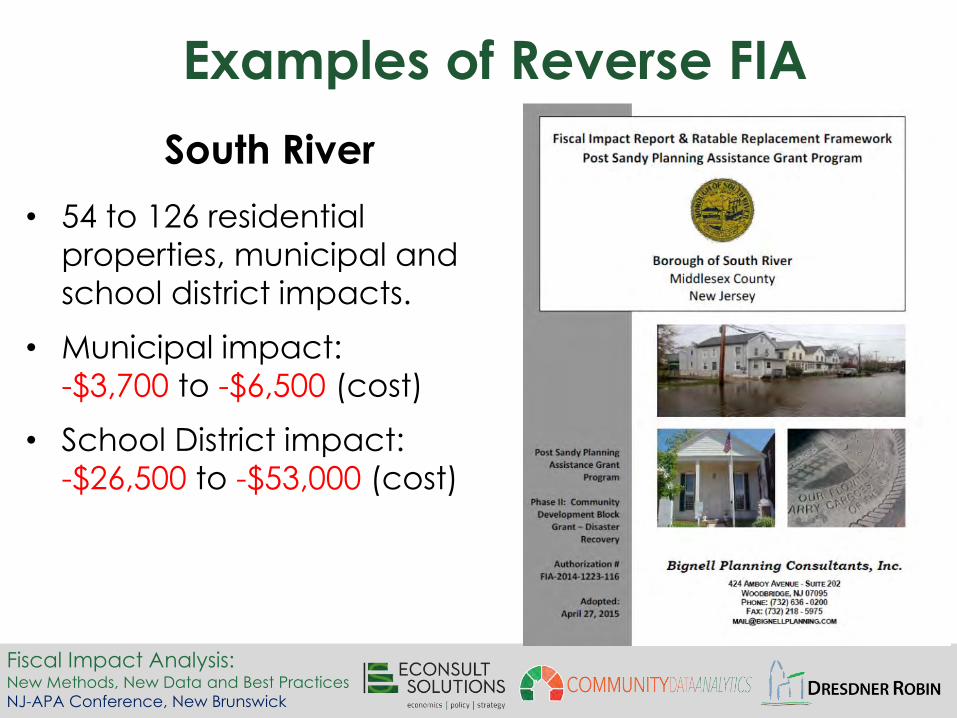

Examples of Reverse FIA

South River

• 54 to 126 residential

properties, municipal and

school district impacts.

• Municipal impact:

-$3,700 to -$6,500 (cost)

• School District impact:

-$26,500 to -$53,000 (cost)

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

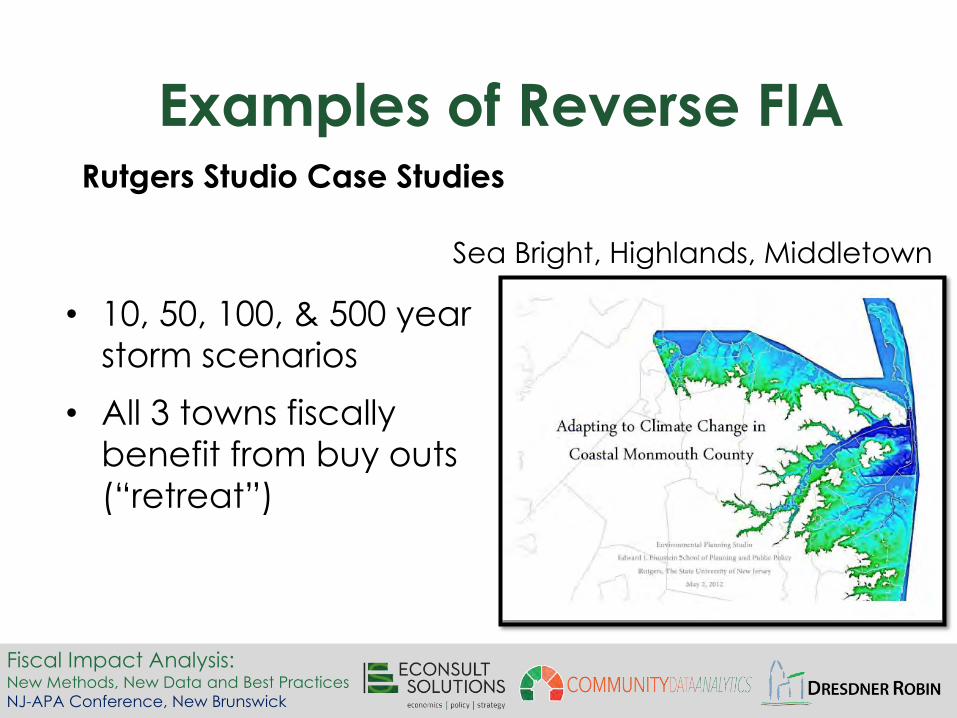

Examples of Reverse FIA

• 10, 50, 100, & 500 year storm scenarios

• All 3 towns fiscally

benefit from buy outs (“retreat”)

Rutgers Studio Case Studies

Sea Bright, Highlands, Middletown

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Reverse Fiscal Impact Analysis

Conclusions

• Part of larger analysis of mitigation strategies

• Very limited number of examples, varied results.

• South River example probably overestimates

municipal cost impact.

• Characteristics of different towns result in

significant differences in results.

• School district impacts not fully analyzed

• Need to perform more analyses.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

SESSION CONCLUSIONS

• Fiscal Impact Analysis remains an important

tool.

• Hybrid cost approach should be used.

• Current and geographically specific

demographic multipliers & planning ratios from

PUMS should be used.

• FIA can be used to evaluate property buy-outs

and acquisition proposals.

Fiscal Impact Analysis: New Methods, New Data and Best Practices

NJ-APA Conference, New Brunswick

Discussion