FIRST-HALF REPORT - Kering · 1 2015 First-Half Report ... 2015 Sport & Lifestyle Luxury 95% 4,132m...

74

FIRST-HALF REPORT 2015

Transcript of FIRST-HALF REPORT - Kering · 1 2015 First-Half Report ... 2015 Sport & Lifestyle Luxury 95% 4,132m...

FIRST-HALF

REPORT

2015

Table of contents

1 2015 First-Half Report – Kering

Chapter 1

Kering in the first half of 2015 – Key figures 3

Chapter 2

Financial information for first-half 2015 6

1. Activity report 6

2. Condensed consolidated interim financial statements 38

3. Statutory Auditors’ review report 69

4. Statement by the persons responsible for the interim financial report 70

This is a free translation into English of the 2015 First-Half report issued in French and is provided solely for the convenience of the English speaking users.

Kering in the first half of 2015 – Key figures 1

3 2015 First-Half Report – Kering

Kering in the first half of 2015

Key figures

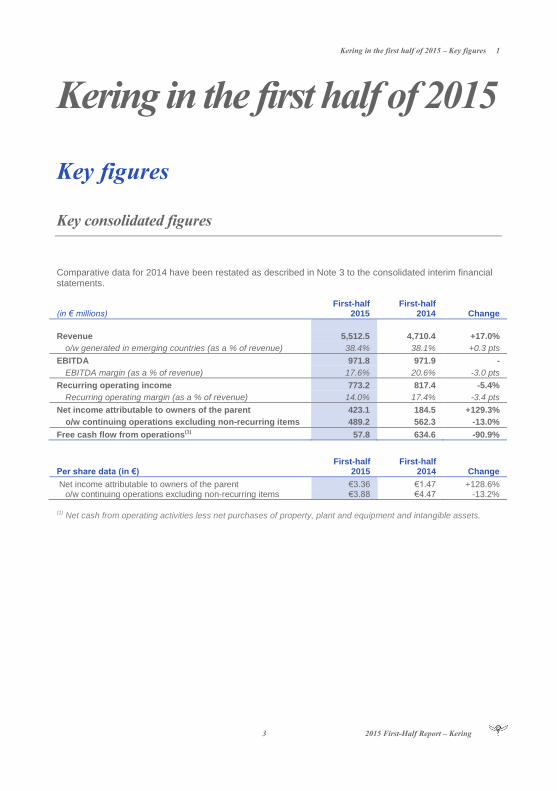

Key consolidated figures

Comparative data for 2014 have been restated as described in Note 3 to the consolidated interim financial statements.

(in € millions) First-half

2015 First-half

2014 Change

Revenue 5,512.5 4,710.4 +17.0%

o/w generated in emerging countries (as a % of revenue) 38.4% 38.1% +0.3 pts

EBITDA 971.8 971.9 -

EBITDA margin (as a % of revenue) 17.6% 20.6% -3.0 pts

Recurring operating income 773.2 817.4 -5.4%

Recurring operating margin (as a % of revenue) 14.0% 17.4% -3.4 pts

Net income attributable to owners of the parent 423.1 184.5 +129.3%

o/w continuing operations excluding non-recurring items 489.2 562.3 -13.0%

Free cash flow from operations(1) 57.8 634.6 -90.9%

Per share data (in €) First-half

2015 First-half

2014 Change

Net income attributable to owners of the parent €3.36 €1.47 +128.6% o/w continuing operations excluding non-recurring items €3.88 €4.47 -13.2%

(1) Net cash from operating activities less net purchases of property, plant and equipment and intangible assets.

1 Kering in the first half of 2015 – Key figures

2015 First-Half Report – Kering 4

Breakdown of revenue by Division

Breakdown of revenue by region

* EEMEA: Eastern Europe, Middle East and Africa

Sport & Lifestyle

32%

Luxury 68%

First-half 2014

Sport & Lifestyle

32%

Luxury 68%

First-half 2015

Western Europe 32%

North America

Asia-Pacific 26%

EEMEA* 8%

South America 4%

Japan 9%

21%

First-half 2014

North America

Asia-Pacific 27%

EEMEA* 7%

South America 4%

Japan

23%

First-half 2015

Western Europe 30%

Japan Japan 9%

Kering in the first half of 2015 – Key figures 1

5 2015 First-Half Report – Kering

Breakdown of recurring operating income by Division*

* Excluding the Corporate segment.

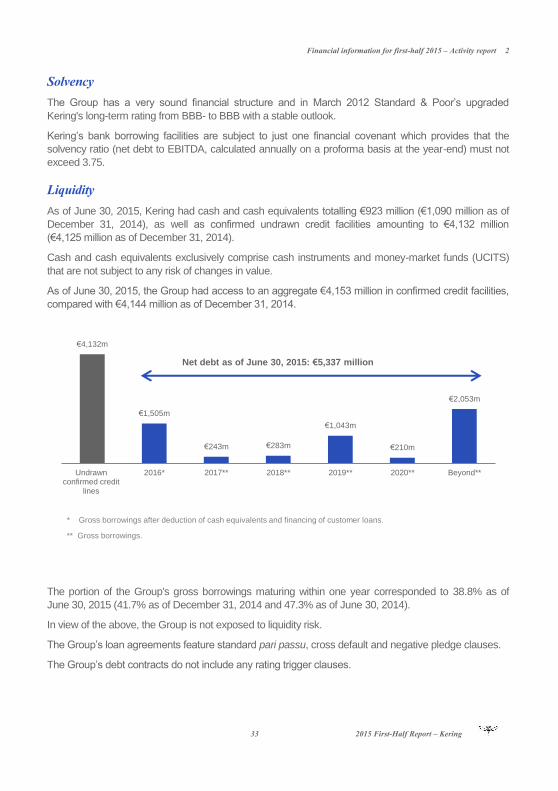

Maturity schedule of net debt

First-half 2014

Sport & Lifestyle

8%

Luxury 92%

First-half 2015

Sport & Lifestyle

5%

Luxury 95%

€4,132m

€1,505m

€243m €283m

€1,043m

€210m

€2,053m

Undrawnconfirmed credit

lines

2016* 2017** 2018** 2019** 2020** Beyond**

* Gross borrowings after deduction of cash equivalents and financing of customer loans. ** Gross borrowings.

Net debt as of June 30, 2015: €5,337m

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 6

Financial information for first-half 2015

1. Activity report

Foreword – Definitions

IFRS 5 – Non-current assets held for sale and discontinued operations

In accordance with IFRS 5 – Non-current Assets Held for Sale and Discontinued Operations, the Group

has presented certain activities as “Non-current assets held for sale and discontinued operations”. The

net income or loss from these activities is shown on a separate line of the income statement, “Net

income (loss) from discontinued operations”, and is restated in the statement of cash flows and income

statement for all reported periods.

Assets and liabilities relating to assets held for sale are presented on separate lines in the Group’s

statement of financial position, without restatement for previous periods. Assets and liabilities relating to

discontinued operations are not presented on separate lines in the Group’s statement of financial

position.

As stated in Note 10 to the condensed consolidated interim financial statements, Sergio Rossi and the

Redcats group are classified as “Non-current assets held for sale and discontinued operations”.

Definition of “reported” and “comparable” revenue

The Group’s “reported” revenue corresponds to published revenue. The Group also uses "comparable"

data to measure organic growth. “Comparable” revenue is 2014 revenue restated for the impact of

changes in Group structure in 2014 or 2015, and for translation differences relating to foreign

subsidiaries’ revenue in 2014.

Definition of recurring operating income

The Group's total operating income includes all revenues and expenses directly related to Group

activities, whether these revenues and expenses are recurring or arise from non-recurring decisions or

transactions.

"Other non-recurring operating income and expenses" consists of unusual items, notably as concerns

the nature or frequency, that could distort the assessment of Group entities’ economic performance.

Other non-recurring operating income and expenses include impairment of goodwill and other intangible

assets, gains or losses on disposals of non-current assets, restructuring costs and costs relating to

employee adaptation measures.

Financial information for first-half 2015 – Activity report 2

7 2015 First-Half Report – Kering

Consequently, Kering monitors its operating performance using “Recurring operating income”, defined

as the difference between total operating income and other non-recurring operating income and

expenses (see Note 6 to the condensed consolidated interim financial statements).

Recurring operating income is an intermediate line item intended to facilitate the understanding of the

entity's operating performance and which can be used as a way to estimate recurring performance. This

indicator is presented in a manner that is consistent and stable over the long-term in order to ensure the

continuity and relevance of financial information.

Recurring operating income at comparable exchange rates for 2014 takes into account the currency

impact on revenue and Group acquisitions, the effective portion of currency hedges and the impact of

changes in exchange rates on the translation of the recurring operating income of consolidated entities

located outside the eurozone.

Definition of EBITDA

The Group uses EBITDA to monitor its operating performance. This financial indicator corresponds to

recurring operating income plus net charges to depreciation, amortisation and provisions on non-current

operating assets recognised in recurring operating income.

EBITDA at comparable exchange rates is defined using the same principles as for recurring operating

income at comparable exchange rates.

Definition of free cash flow from operations and available cash flow

The Group also uses an intermediate line item, “Free cash flow from operations”, to monitor its financial

performance. This financial indicator measures net operating cash flow less net operating investments

(defined as purchases and sales of property, plant and equipment and intangible assets).

"Available cash flow" corresponds to free cash flow from operations plus interest and dividends received

less interest paid and equivalent.

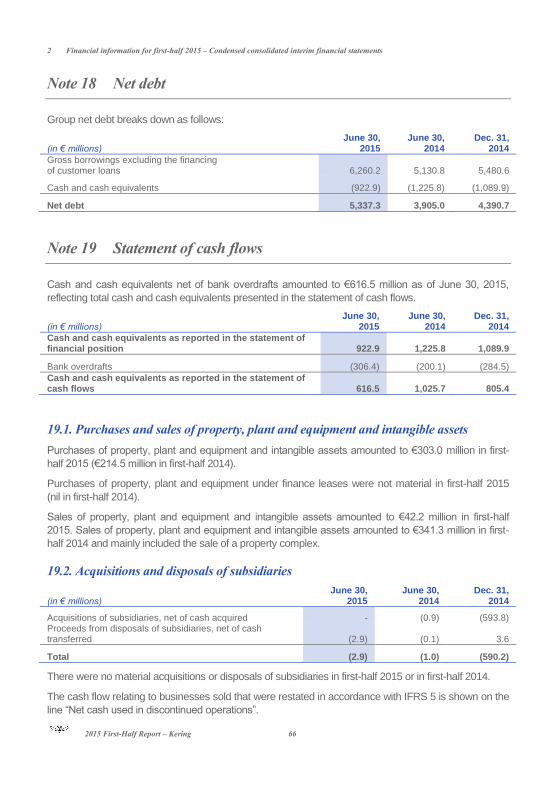

Definition of net debt

As defined by CNC recommendation No. 2009-R-03 of July 2, 2009, net debt comprises gross

borrowings, including accrued interest, less net cash.

Net debt includes fair value hedging instruments recorded in the statement of financial position relating

to bank borrowings and bonds whose interest rate risk is fully or partly hedged as part of a fair value

relationship (see Note 18 to the condensed consolidated interim financial statements).

The financing of customer loans by fully-consolidated consumer credit businesses is presented in

borrowings. Group net debt excludes the financing of customer loans by consumer credit businesses.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 8

Highlights of first-half 2015

Change in management and creative responsibility at Gucci

On January 21, 2015, Marco Bizzarri – Gucci's President and CEO who succeeded Patrizio di Marco

on January 1, 2015 – announced that Alessandro Michele had been appointed as the brand's new

Creative Director following the departure of his predecessor Frida Giannini.

Alessandro Michele has been given total creative responsibility for all of Gucci's collections and its

brand image. The first collection fully designed by Alessandro Michele was the 2016 Cruise collection,

which was unveiled in New York on June 4, 2015 and will be available in stores as from the end of the

third quarter of 2015.

Finalisation of the partnership with Safilo and launch of Kering Eyewear

In 2014, Kering announced its plan to invest in a dedicated entity specialised in luxury, high-end and

sport Eyewear, managed by a skilled team of experienced professionals under the direction of Roberto

Vedovotto. This innovative management model for the Group's Eyewear business will allow it to

leverage the full potential of its brands in this category.

As part of this strategic move, Kering and Safilo agreed to further their partnership and jointly intend to

terminate the current Gucci licence agreement two years in advance, i.e., by December 31, 2016, which

will result in total compensation of €90 million to be paid to Safilo. On January 12, 2015, Kering

announced that it had signed a partnership agreement with Safilo covering the development,

manufacture and supply of Gucci Eyewear products. The agreement will be effective as of fourth-

quarter 2015 in order to ensure a seamless transition for Gucci's Eyewear business.

On March 18, 2015, Kering announced the appointment of Roberto Vedovotto, CEO of Kering

Eyewear, as a new member of its Executive Committee. Kering Eyewear was officially launched on

June 30, 2015 when its first collection, "Collezione Uno" was presented at the Palazzo Grassi in Venice.

The overall €90 million in compensation due to Safilo has been recognised as an intangible asset in the

financial statements at June 30, 2015 and will be amortised as from January 1, 2017. The

compensation will be paid in three equal instalments, with the first payment on January 12, 2015 and

the following two in December 2016 and September 2018.

Other highlights

On January 15, 2015, Kering sold the assets of Movitex to the group's management team, after

recapitalising it in accordance with the preliminary agreement signed on December 3, 2014.

On March 20, 2015, Kering issued a €500 million, 0.875% fixed-rate bond maturing in seven years. Also

during the first half of 2015, Kering carried out two issues of notes in foreign currency – a

USD 150 million issue in March 2015 of five-year floating-rate notes, and a USD 150 million issue in

June 2015 of six-year fixed-rate notes with an annual coupon of 2.887%.

On March 25, 2015 Kering bought out the non-controlling interests in Sowind Group in accordance with

the shareholder agreements signed in June 2011. This acquisition did not have a material impact on the

Group's interim financial statements.

On June 30, 2015, PUMA announced that it had sold the intellectual property rights (including

trademark rights) of its subsidiary, Tretorn Group, to US-based Authentic Brands Group, LLC (ABG).

Tretorn – which is based in Helsingborg in Sweden and makes sport and leisure products – was

acquired by PUMA in 2002. This sale is in line with PUMA's strategy of refocusing on its core

businesses.

Financial information for first-half 2015 – Activity report 2

9 2015 First-Half Report – Kering

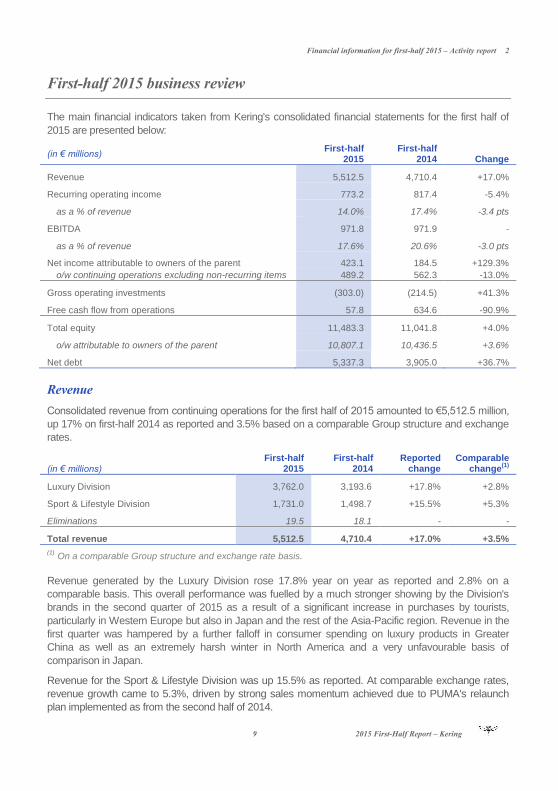

First-half 2015 business review

The main financial indicators taken from Kering's consolidated financial statements for the first half of

2015 are presented below:

(in € millions) First-half

2015 First-half

2014 Change

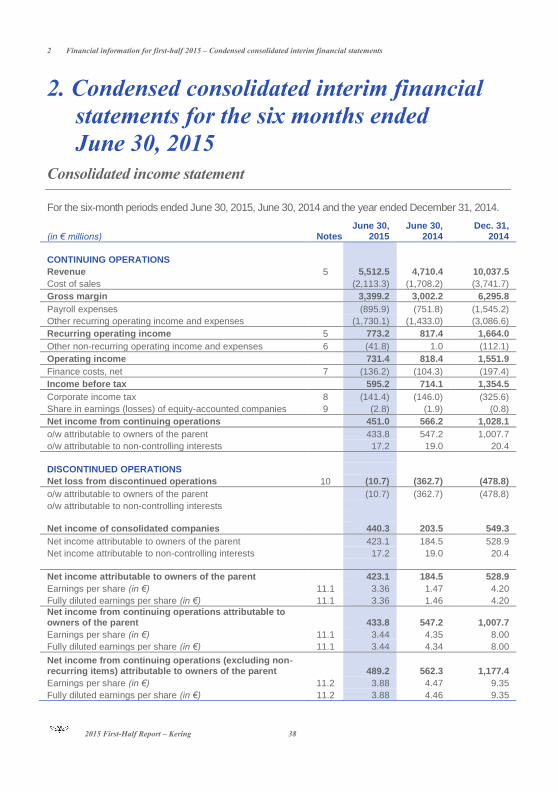

Revenue 5,512.5 4,710.4 +17.0%

Recurring operating income 773.2 817.4 -5.4%

as a % of revenue 14.0% 17.4% -3.4 pts

EBITDA 971.8 971.9 -

as a % of revenue 17.6% 20.6% -3.0 pts

Net income attributable to owners of the parent 423.1 184.5 +129.3%

o/w continuing operations excluding non-recurring items 489.2 562.3 -13.0%

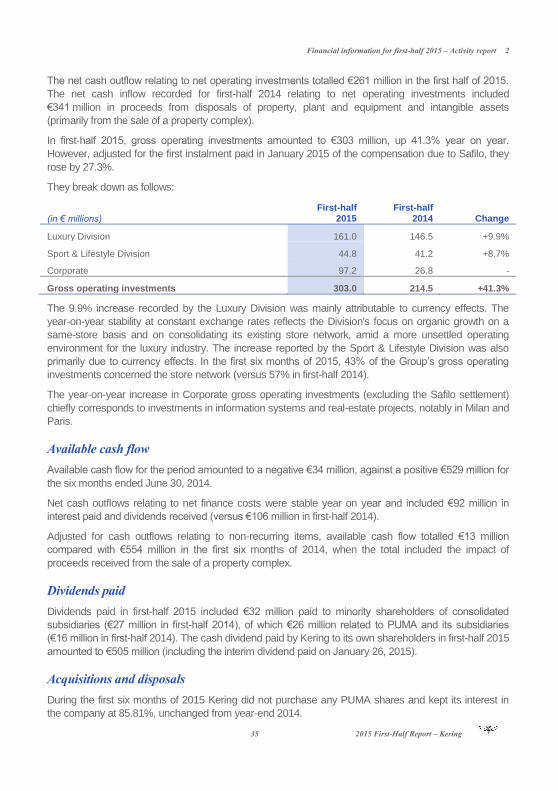

Gross operating investments (303.0) (214.5) +41.3%

Free cash flow from operations 57.8 634.6 -90.9%

Total equity 11,483.3 11,041.8 +4.0%

o/w attributable to owners of the parent 10,807.1 10,436.5 +3.6%

Net debt 5,337.3 3,905.0 +36.7%

Revenue

Consolidated revenue from continuing operations for the first half of 2015 amounted to €5,512.5 million,

up 17% on first-half 2014 as reported and 3.5% based on a comparable Group structure and exchange

rates.

(in € millions)

First-half 2015

First-half 2014

Reported change

Comparable change

(1)

Luxury Division 3,762.0 3,193.6 +17.8% +2.8%

Sport & Lifestyle Division 1,731.0 1,498.7 +15.5% +5.3%

Eliminations 19.5 18.1 - -

Total revenue 5,512.5 4,710.4 +17.0% +3.5%

(1) On a comparable Group structure and exchange rate basis.

Revenue generated by the Luxury Division rose 17.8% year on year as reported and 2.8% on a

comparable basis. This overall performance was fuelled by a much stronger showing by the Division's

brands in the second quarter of 2015 as a result of a significant increase in purchases by tourists,

particularly in Western Europe but also in Japan and the rest of the Asia-Pacific region. Revenue in the

first quarter was hampered by a further falloff in consumer spending on luxury products in Greater

China as well as an extremely harsh winter in North America and a very unfavourable basis of

comparison in Japan.

Revenue for the Sport & Lifestyle Division was up 15.5% as reported. At comparable exchange rates,

revenue growth came to 5.3%, driven by strong sales momentum achieved due to PUMA's relaunch

plan implemented as from the second half of 2014.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 10

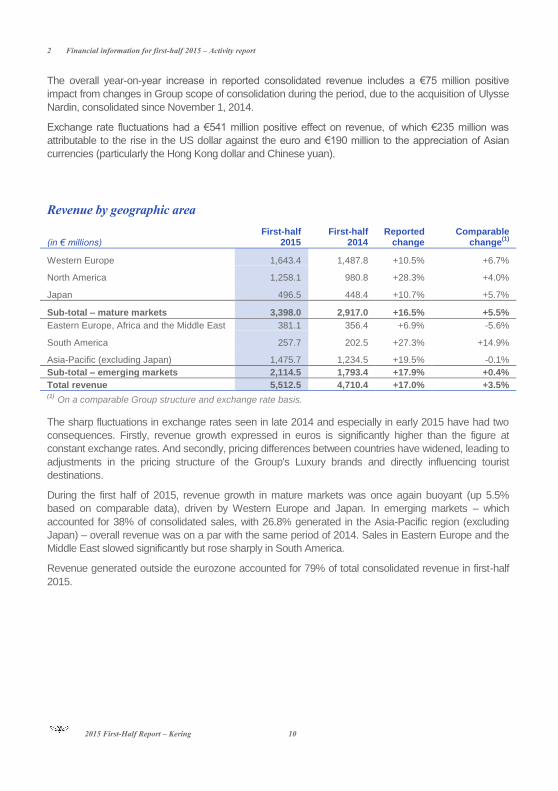

The overall year-on-year increase in reported consolidated revenue includes a €75 million positive

impact from changes in Group scope of consolidation during the period, due to the acquisition of Ulysse

Nardin, consolidated since November 1, 2014.

Exchange rate fluctuations had a €541 million positive effect on revenue, of which €235 million was

attributable to the rise in the US dollar against the euro and €190 million to the appreciation of Asian

currencies (particularly the Hong Kong dollar and Chinese yuan).

Revenue by geographic area

(in € millions)

First-half 2015

First-half 2014

Reported change

Comparable change

(1)

Western Europe 1,643.4 1,487.8 +10.5% +6.7%

North America 1,258.1 980.8 +28.3% +4.0%

Japan 496.5 448.4 +10.7% +5.7%

Sub-total – mature markets 3,398.0 2,917.0 +16.5% +5.5%

Eastern Europe, Africa and the Middle East 381.1 356.4 +6.9% -5.6%

South America 257.7 202.5 +27.3% +14.9%

Asia-Pacific (excluding Japan) 1,475.7 1,234.5 +19.5% -0.1%

Sub-total – emerging markets 2,114.5 1,793.4 +17.9% +0.4%

Total revenue 5,512.5 4,710.4 +17.0% +3.5% (1) On a comparable Group structure and exchange rate basis.

The sharp fluctuations in exchange rates seen in late 2014 and especially in early 2015 have had two

consequences. Firstly, revenue growth expressed in euros is significantly higher than the figure at

constant exchange rates. And secondly, pricing differences between countries have widened, leading to

adjustments in the pricing structure of the Group's Luxury brands and directly influencing tourist

destinations.

During the first half of 2015, revenue growth in mature markets was once again buoyant (up 5.5%

based on comparable data), driven by Western Europe and Japan. In emerging markets – which

accounted for 38% of consolidated sales, with 26.8% generated in the Asia-Pacific region (excluding

Japan) – overall revenue was on a par with the same period of 2014. Sales in Eastern Europe and the

Middle East slowed significantly but rose sharply in South America.

Revenue generated outside the eurozone accounted for 79% of total consolidated revenue in first-half

2015.

Financial information for first-half 2015 – Activity report 2

11 2015 First-Half Report – Kering

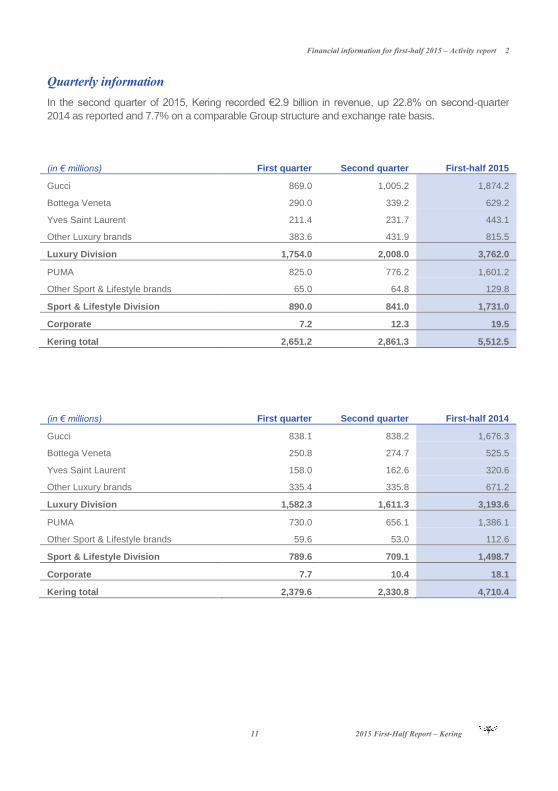

Quarterly information

In the second quarter of 2015, Kering recorded €2.9 billion in revenue, up 22.8% on second-quarter

2014 as reported and 7.7% on a comparable Group structure and exchange rate basis.

(in € millions) First quarter Second quarter First-half 2015

Gucci 869.0 1,005.2 1,874.2

Bottega Veneta 290.0 339.2 629.2

Yves Saint Laurent 211.4 231.7 443.1

Other Luxury brands 383.6 431.9 815.5

Luxury Division 1,754.0 2,008.0 3,762.0

PUMA 825.0 776.2 1,601.2

Other Sport & Lifestyle brands 65.0 64.8 129.8

Sport & Lifestyle Division 890.0 841.0 1,731.0

Corporate 7.2 12.3 19.5

Kering total 2,651.2 2,861.3 5,512.5

(in € millions) First quarter Second quarter First-half 2014

Gucci 838.1 838.2 1,676.3

Bottega Veneta 250.8 274.7 525.5

Yves Saint Laurent 158.0 162.6 320.6

Other Luxury brands 335.4 335.8 671.2

Luxury Division 1,582.3 1,611.3 3,193.6

PUMA 730.0 656.1 1,386.1

Other Sport & Lifestyle brands 59.6 53.0 112.6

Sport & Lifestyle Division 789.6 709.1 1,498.7

Corporate 7.7 10.4 18.1

Kering total 2,379.6 2,330.8 4,710.4

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 12

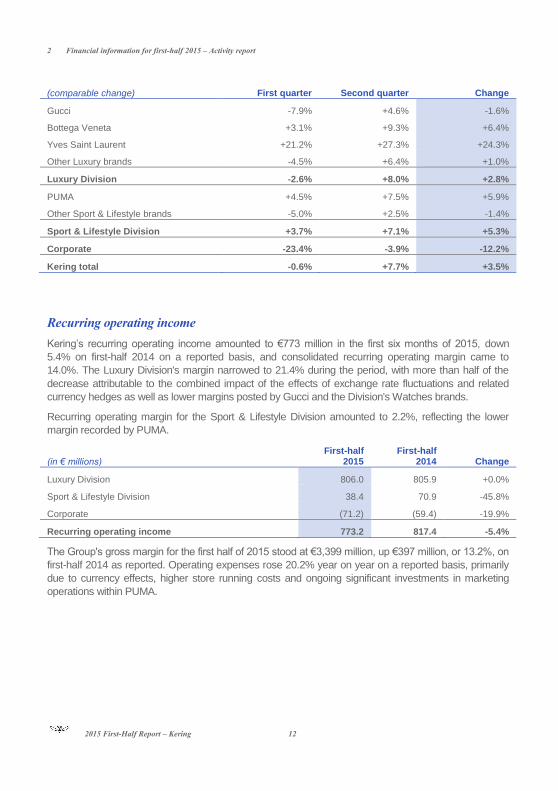

(comparable change) First quarter Second quarter Change

Gucci -7.9% +4.6% -1.6%

Bottega Veneta +3.1% +9.3% +6.4%

Yves Saint Laurent +21.2% +27.3% +24.3%

Other Luxury brands -4.5% +6.4% +1.0%

Luxury Division -2.6% +8.0% +2.8%

PUMA +4.5% +7.5% +5.9%

Other Sport & Lifestyle brands -5.0% +2.5% -1.4%

Sport & Lifestyle Division +3.7% +7.1% +5.3%

Corporate -23.4% -3.9% -12.2%

Kering total -0.6% +7.7% +3.5%

Recurring operating income

Kering’s recurring operating income amounted to €773 million in the first six months of 2015, down

5.4% on first-half 2014 on a reported basis, and consolidated recurring operating margin came to

14.0%. The Luxury Division's margin narrowed to 21.4% during the period, with more than half of the

decrease attributable to the combined impact of the effects of exchange rate fluctuations and related

currency hedges as well as lower margins posted by Gucci and the Division's Watches brands.

Recurring operating margin for the Sport & Lifestyle Division amounted to 2.2%, reflecting the lower

margin recorded by PUMA.

(in € millions)

First-half 2015

First-half 2014 Change

Luxury Division 806.0 805.9 +0.0%

Sport & Lifestyle Division 38.4 70.9 -45.8%

Corporate (71.2) (59.4) -19.9%

Recurring operating income 773.2 817.4 -5.4%

The Group's gross margin for the first half of 2015 stood at €3,399 million, up €397 million, or 13.2%, on

first-half 2014 as reported. Operating expenses rose 20.2% year on year on a reported basis, primarily

due to currency effects, higher store running costs and ongoing significant investments in marketing

operations within PUMA.

Financial information for first-half 2015 – Activity report 2

13 2015 First-Half Report – Kering

EBITDA

Consolidated EBITDA came to €972 million, on a par with the first-half 2014 figure as reported, and the

EBITDA margin narrowed by 3 points on a reported basis to 17.6%.

(in € millions)

First-half 2015

First-half 2014 Change

Luxury Division 960.7 925.4 +3.8%

Sport & Lifestyle Division 70.1 96.8 -27.6%

Corporate (59.0) (50.3) -17.3%

EBITDA 971.8 971.9 -

Other non-recurring operating income and expenses

Other non-recurring operating income and expenses consist of unusual items that could distort the

assessment of each brand's financial performance.

Other non-recurring operating income and expenses represented a net expense of €42 million in the six

months to June 30, 2015 and primarily included restructuring costs, asset impairment losses for Luxury

activities – particularly Gucci inventory write-downs in line with the brand's current period of transition –

and disposal gains, chiefly relating to the sale of the Tretorn brand and the capital gain arising on the

sale of a property complex.

In first-half 2014, this item represented a net gain of €1 million and primarily included (i) a net gain on

the disposal of a property complex and (ii) asset impairment losses, including €183 million charged

against the "Other Sport & Lifestyle brands" goodwill.

Further details on this item are provided in Note 6 to the consolidated interim financial statements.

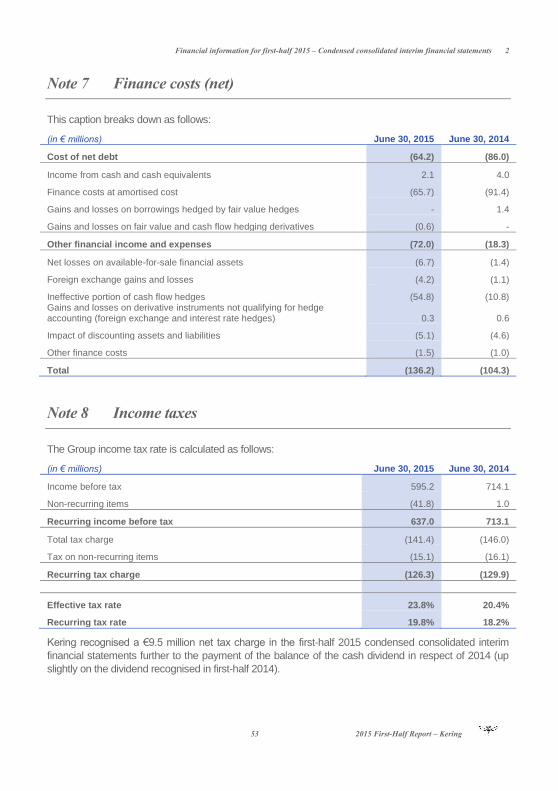

Net finance costs

The Group’s net finance costs can be analysed as follows:

(in € millions)

First-half 2015

First-half 2014 Change

Cost of net debt (64.2) (86.0) -25.3%

Other financial income and expenses (72.0) (18.3) -

Finance costs, net (136.2) (104.3) +30.6%

The Group’s cost of net debt in first-half 2015 was 25% lower than in the same period of 2014, coming

in at just over €64 million.

Average outstanding net debt increased by 32% year on year, chiefly due to currency effects and

changes in Group structure (notably the recapitalisations of La Redoute, Relais Colis and Movitex).

However, this negative effect was partly offset by a decrease in Kering's average cost of borrowing,

particularly thanks to much lower interest rates on the Group's bond debt.

"Other financial income and expenses" represented a net expense that was €54 million higher than in

first-half 2014, mainly due to the application of IAS 39, and notably the adverse impact of the ineffective

portion of cash flow hedges.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 14

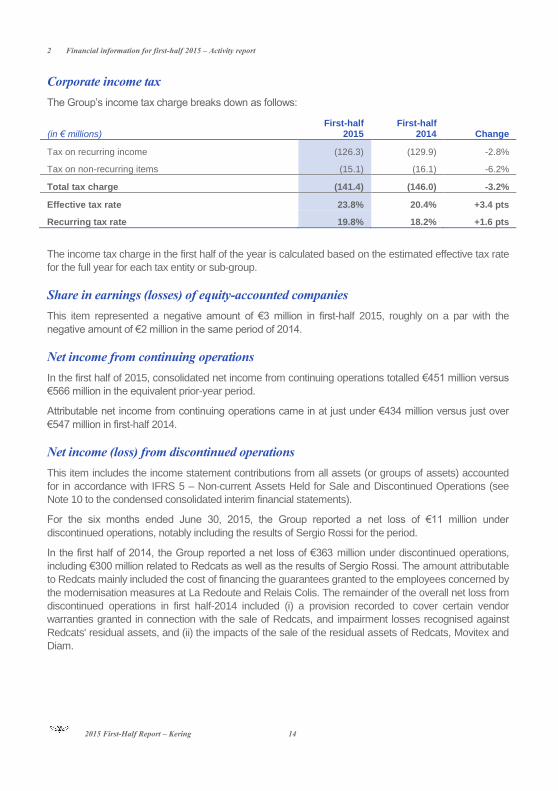

Corporate income tax

The Group’s income tax charge breaks down as follows:

(in € millions)

First-half 2015

First-half 2014 Change

Tax on recurring income (126.3) (129.9) -2.8%

Tax on non-recurring items (15.1) (16.1) -6.2%

Total tax charge (141.4) (146.0) -3.2%

Effective tax rate 23.8% 20.4% +3.4 pts

Recurring tax rate 19.8% 18.2% +1.6 pts

The income tax charge in the first half of the year is calculated based on the estimated effective tax rate

for the full year for each tax entity or sub-group.

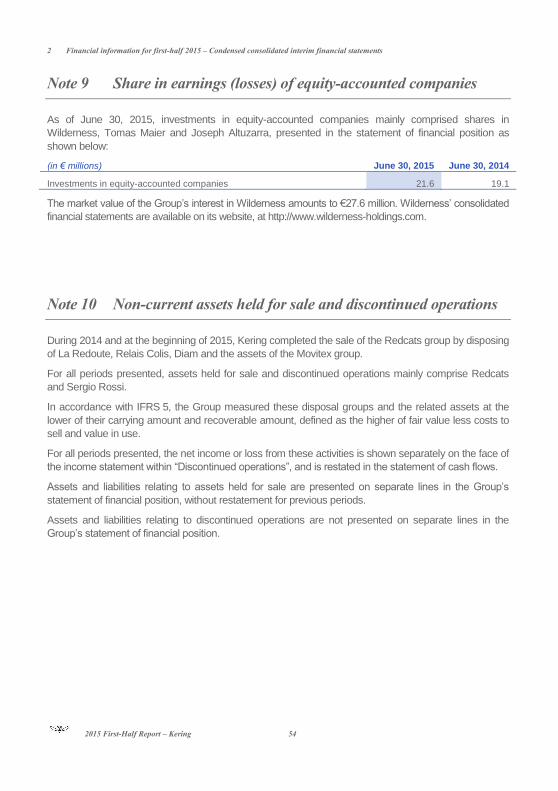

Share in earnings (losses) of equity-accounted companies

This item represented a negative amount of €3 million in first-half 2015, roughly on a par with the

negative amount of €2 million in the same period of 2014.

Net income from continuing operations

In the first half of 2015, consolidated net income from continuing operations totalled €451 million versus

€566 million in the equivalent prior-year period.

Attributable net income from continuing operations came in at just under €434 million versus just over

€547 million in first-half 2014.

Net income (loss) from discontinued operations

This item includes the income statement contributions from all assets (or groups of assets) accounted

for in accordance with IFRS 5 – Non-current Assets Held for Sale and Discontinued Operations (see

Note 10 to the condensed consolidated interim financial statements).

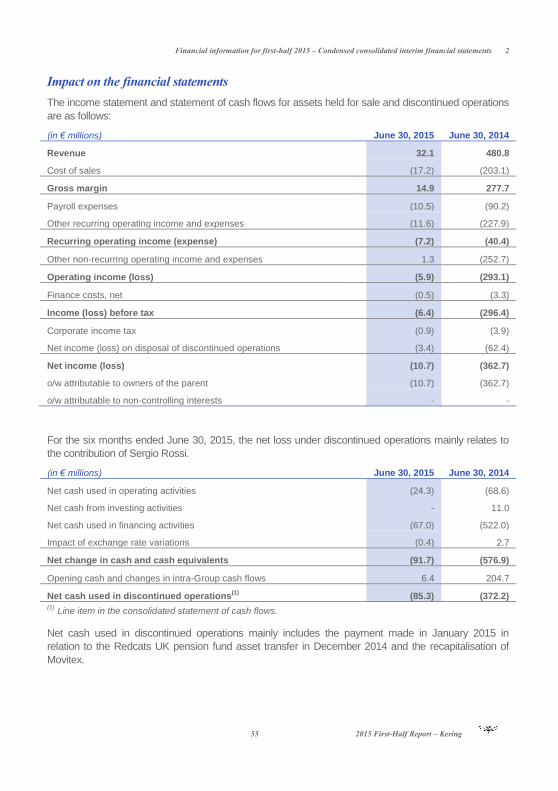

For the six months ended June 30, 2015, the Group reported a net loss of €11 million under

discontinued operations, notably including the results of Sergio Rossi for the period.

In the first half of 2014, the Group reported a net loss of €363 million under discontinued operations,

including €300 million related to Redcats as well as the results of Sergio Rossi. The amount attributable

to Redcats mainly included the cost of financing the guarantees granted to the employees concerned by

the modernisation measures at La Redoute and Relais Colis. The remainder of the overall net loss from

discontinued operations in first half-2014 included (i) a provision recorded to cover certain vendor

warranties granted in connection with the sale of Redcats, and impairment losses recognised against

Redcats' residual assets, and (ii) the impacts of the sale of the residual assets of Redcats, Movitex and

Diam.

Financial information for first-half 2015 – Activity report 2

15 2015 First-Half Report – Kering

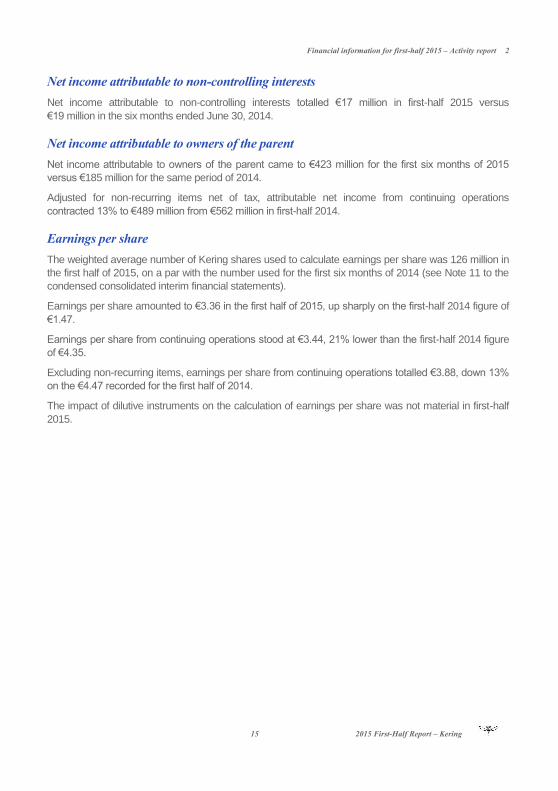

Net income attributable to non-controlling interests

Net income attributable to non-controlling interests totalled €17 million in first-half 2015 versus

€19 million in the six months ended June 30, 2014.

Net income attributable to owners of the parent

Net income attributable to owners of the parent came to €423 million for the first six months of 2015

versus €185 million for the same period of 2014.

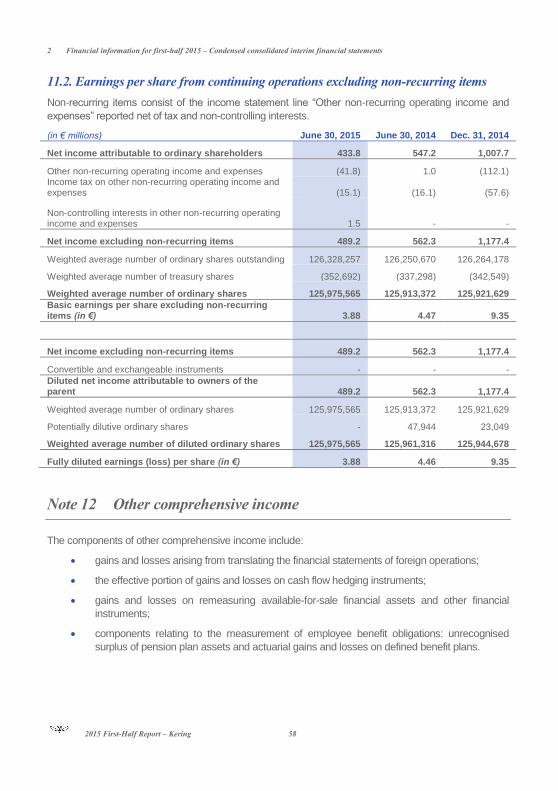

Adjusted for non-recurring items net of tax, attributable net income from continuing operations

contracted 13% to €489 million from €562 million in first-half 2014.

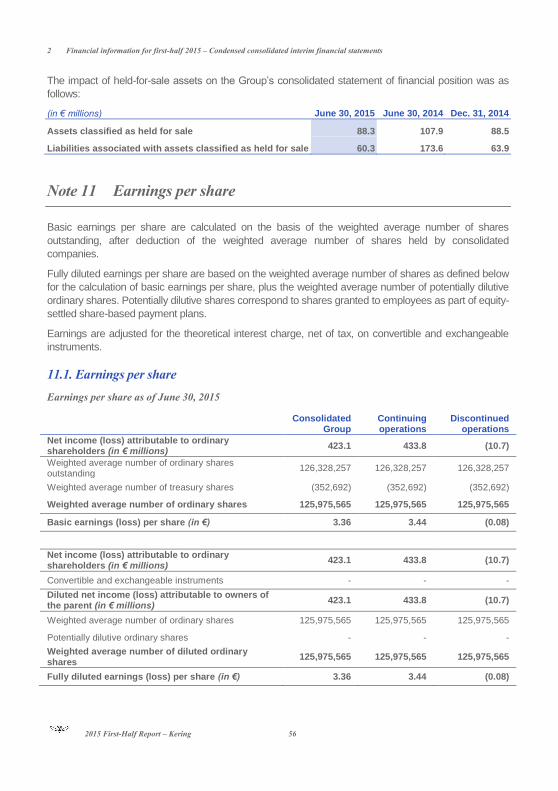

Earnings per share

The weighted average number of Kering shares used to calculate earnings per share was 126 million in

the first half of 2015, on a par with the number used for the first six months of 2014 (see Note 11 to the

condensed consolidated interim financial statements).

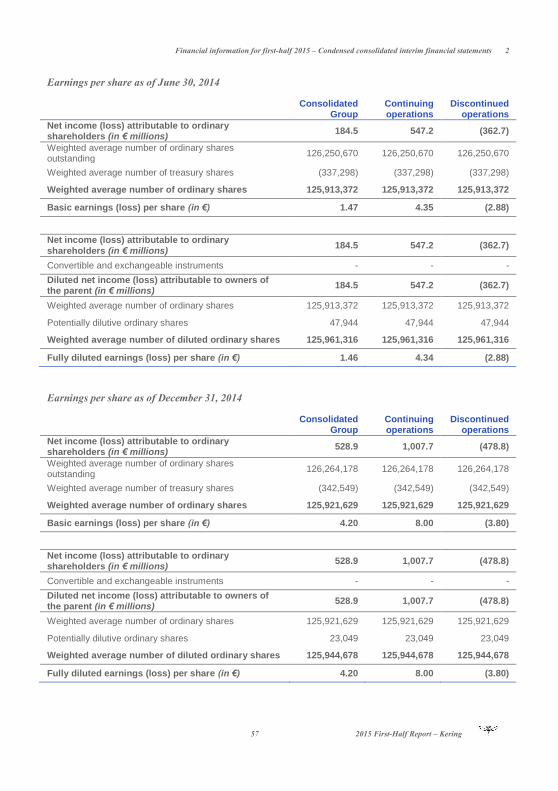

Earnings per share amounted to €3.36 in the first half of 2015, up sharply on the first-half 2014 figure of

€1.47.

Earnings per share from continuing operations stood at €3.44, 21% lower than the first-half 2014 figure

of €4.35.

Excluding non-recurring items, earnings per share from continuing operations totalled €3.88, down 13%

on the €4.47 recorded for the first half of 2014.

The impact of dilutive instruments on the calculation of earnings per share was not material in first-half

2015.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 16

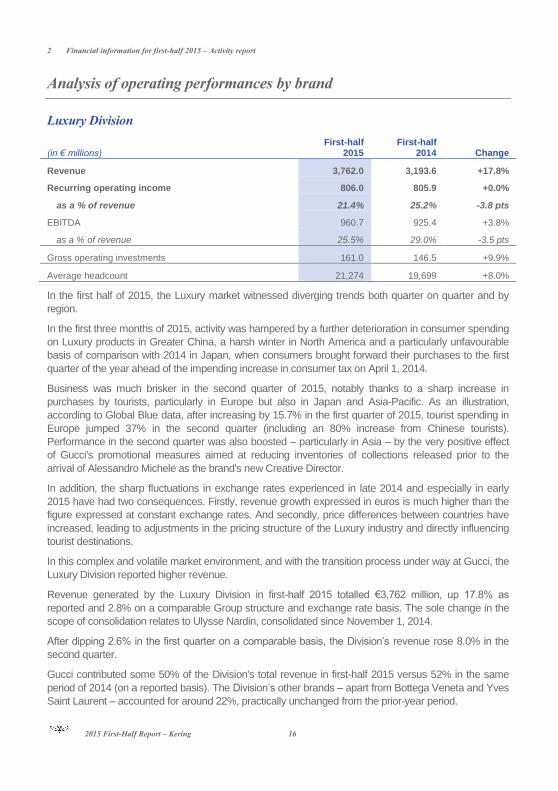

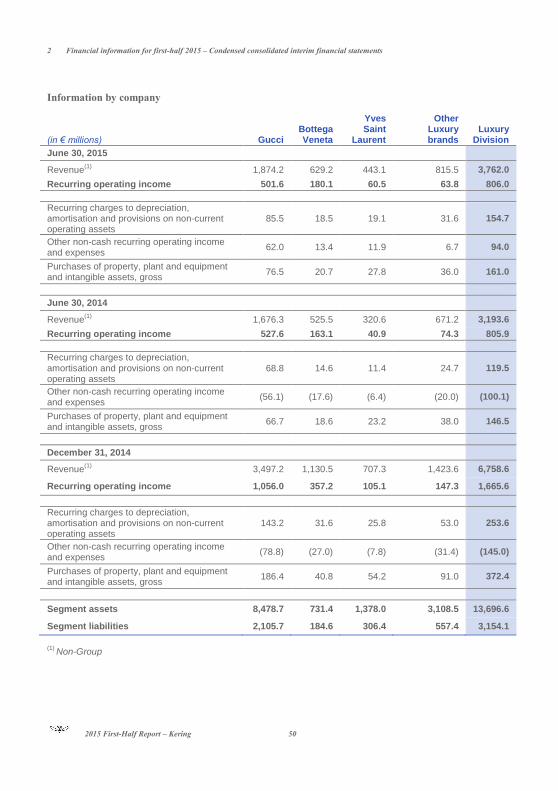

Analysis of operating performances by brand

Luxury Division

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 3,762.0 3,193.6 +17.8%

Recurring operating income 806.0 805.9 +0.0%

as a % of revenue 21.4% 25.2% -3.8 pts

EBITDA 960.7 925.4 +3.8%

as a % of revenue 25.5% 29.0% -3.5 pts

Gross operating investments 161.0 146.5 +9.9%

Average headcount 21,274 19,699 +8.0%

In the first half of 2015, the Luxury market witnessed diverging trends both quarter on quarter and by

region.

In the first three months of 2015, activity was hampered by a further deterioration in consumer spending

on Luxury products in Greater China, a harsh winter in North America and a particularly unfavourable

basis of comparison with 2014 in Japan, when consumers brought forward their purchases to the first

quarter of the year ahead of the impending increase in consumer tax on April 1, 2014.

Business was much brisker in the second quarter of 2015, notably thanks to a sharp increase in

purchases by tourists, particularly in Europe but also in Japan and Asia-Pacific. As an illustration,

according to Global Blue data, after increasing by 15.7% in the first quarter of 2015, tourist spending in

Europe jumped 37% in the second quarter (including an 80% increase from Chinese tourists).

Performance in the second quarter was also boosted – particularly in Asia – by the very positive effect

of Gucci's promotional measures aimed at reducing inventories of collections released prior to the

arrival of Alessandro Michele as the brand's new Creative Director.

In addition, the sharp fluctuations in exchange rates experienced in late 2014 and especially in early

2015 have had two consequences. Firstly, revenue growth expressed in euros is much higher than the

figure expressed at constant exchange rates. And secondly, price differences between countries have

increased, leading to adjustments in the pricing structure of the Luxury industry and directly influencing

tourist destinations.

In this complex and volatile market environment, and with the transition process under way at Gucci, the

Luxury Division reported higher revenue.

Revenue generated by the Luxury Division in first-half 2015 totalled €3,762 million, up 17.8% as

reported and 2.8% on a comparable Group structure and exchange rate basis. The sole change in the

scope of consolidation relates to Ulysse Nardin, consolidated since November 1, 2014.

After dipping 2.6% in the first quarter on a comparable basis, the Division’s revenue rose 8.0% in the

second quarter.

Gucci contributed some 50% of the Division's total revenue in first-half 2015 versus 52% in the same

period of 2014 (on a reported basis). The Division’s other brands – apart from Bottega Veneta and Yves

Saint Laurent – accounted for around 22%, practically unchanged from the prior-year period.

Financial information for first-half 2015 – Activity report 2

17 2015 First-Half Report – Kering

Retail sales in directly-operated stores and online rose 7.0% year on year (on a comparable basis) and

represented 71.5% of the Division's total revenue in first-half 2015 compared with 69.0% in the first six

months of 2014. This year-on-year increase reflects the strategy implemented by all of the Division's

brands to control their distribution more effectively and reinforce their exclusivity; it also reflects

measures taken to prudently manage the expansion of the directly-operated store network.

Wholesale sales were 7.3% lower than in first-half 2014 on a comparable basis, with the decrease

primarily attributable to Gucci. In view of the transition process under way within Gucci in terms of both

its creative vision and its organisational structure, the brand launched a new phase in a plan to

streamline the wholesale distribution network by drastically reducing exposure to multi-brand distributors

in Europe.

By product category, the Division's overall revenue is becoming increasingly balanced, reflecting the

complementarity of the brands in the portfolio, with the contributions of Leather Goods, Ready-to-Wear

and Shoes representing 54.2%, 15.7% and 12.1%, respectively. Watches and Jewellery sales

accounted for 9.7% of revenue. Apart from Watches – which were adversely affected by a lacklustre

market and the sharp appreciation of the Swiss franc – revenue was up in each of the Division's main

product categories.

Growth was highest in the Division's traditional, more mature markets, coming in at 7.3% on a

comparable basis overall and 13.4% for the directly-operated store network.

Western Europe (which made up 31.0% of the Division's revenue) posted a strong 9.5% increase,

driven by robust sales in eurozone countries (up 17.6%). These figures were achieved thanks to both

the sharp increase in tourist numbers in Europe – which began in the first quarter of 2015 and has

accelerated since – and steadily rising sales to local customers.

In North America (which contributed 20.1% of the Division's sales), revenue climbed 4.0% year on year,

fuelled by 6.0% growth in the second quarter following on from a less buoyant first three months when

performance was weighed down by bad weather conditions. The rise of the US dollar against many of

the world's other major currencies had an overall adverse impact on sales to tourists, however.

Revenue in Japan advanced 7.4% during first-half 2015, driven by increased tourism from Mainland

China and robust sales to the local clientele.

The Luxury Division's sales in emerging markets (which represented 39.1% of its total revenue) edged

back 3.5% on a comparable basis, with performance hampered by unfavourable market conditions in

Greater China and continued economic and political tension in Eastern Europe which had an indirect

effect on the spending of Russian tourists in Turkey and the Middle East.

In the Asia-Pacific region (excluding Japan), revenue declined 2.3% in first-half 2015, as an upturn in

spending by Chinese customers in certain countries within the region – such as South Korea, Taiwan

and Australia – did not offset the sales contraction in Hong Kong and Macao. Year-on-year revenue in

Mainland China remained stable.

Sales also decreased in the Division's other emerging markets, except for Latin America, which saw its

revenue jump.

The Luxury Division's recurring operating income amounted to €806 million for first-half 2015, stable

from first-half 2014.

Recurring operating margin came in at 21.4%, down 380 basis points as reported. More than half of this

decrease was due to the combined effects of exchange rate fluctuations and currency hedges, which

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 18

had a massive dilutive impact in the period. The remainder of the decline was attributable to the

contraction in recurring operating income posted by Gucci and weaker performance in Watches.

EBITDA rose 3.8% in first-half 2015 to €961 million, and the EBITDA margin stood at 25.5%. The year-

on-year change in EBITDA was more favourable than for EBIT, reflecting the growing weight of

depreciation and amortisation within operating income (up 29.5% on first-half 2014) as a result of the

Division’s capital expenditure strategy implemented over the past several years.

The Luxury Division's gross operating investments totalled €161 million for first-half 2015, 9.9% higher

than in the same period of 2014. The increase primarily stemmed from currency effects, as gross

operating investments at constant exchange rates were relatively stable compared with first-half 2014.

This reflects the Division’s focus on organic growth on a same-store basis and consolidating the

network of existing stores, while taking into consideration the more unsettled operating context for the

Luxury industry. At the same time, measures previously undertaken to reallocate capital expenditure

were pursued during the period, with a pronounced increase in the amount of financing assigned to

store refurbishments, extensions and relocations, particularly for Gucci.

As of June 30, 2015, the Luxury Division had a network of 1,201 directly-operated stores, including 745

(62%) in mature markets and 456 in emerging markets. Net store additions during the period totalled 15

(representing a 1.3% increase compared with December 31, 2014).

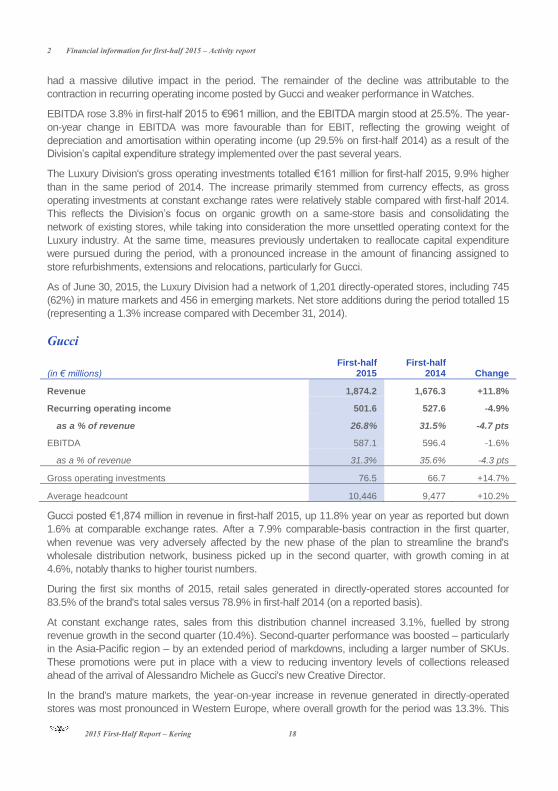

Gucci

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 1,874.2 1,676.3 +11.8%

Recurring operating income 501.6 527.6 -4.9%

as a % of revenue 26.8% 31.5% -4.7 pts

EBITDA 587.1 596.4 -1.6%

as a % of revenue 31.3% 35.6% -4.3 pts

Gross operating investments 76.5 66.7 +14.7%

Average headcount 10,446 9,477 +10.2%

Gucci posted €1,874 million in revenue in first-half 2015, up 11.8% year on year as reported but down

1.6% at comparable exchange rates. After a 7.9% comparable-basis contraction in the first quarter,

when revenue was very adversely affected by the new phase of the plan to streamline the brand's

wholesale distribution network, business picked up in the second quarter, with growth coming in at

4.6%, notably thanks to higher tourist numbers.

During the first six months of 2015, retail sales generated in directly-operated stores accounted for

83.5% of the brand's total sales versus 78.9% in first-half 2014 (on a reported basis).

At constant exchange rates, sales from this distribution channel increased 3.1%, fuelled by strong

revenue growth in the second quarter (10.4%). Second-quarter performance was boosted – particularly

in the Asia-Pacific region – by an extended period of markdowns, including a larger number of SKUs.

These promotions were put in place with a view to reducing inventory levels of collections released

ahead of the arrival of Alessandro Michele as Gucci's new Creative Director.

In the brand's mature markets, the year-on-year increase in revenue generated in directly-operated

stores was most pronounced in Western Europe, where overall growth for the period was 13.3%. This

Financial information for first-half 2015 – Activity report 2

19 2015 First-Half Report – Kering

region saw a solid revenue rise of 6.3% on a comparable basis in the first quarter followed by a 19.8%

jump in the second, driven by high tourist numbers, particularly Chinese and American, as well as by

very positive trends in the domestic market which demonstrate the brand's enhanced customer appeal.

In North America, Gucci reported 5.8% comparable-basis revenue growth despite lower sales to tourists

due to the appreciation of the US dollar against many of the world's other major currencies.

In Japan, where the Gucci brand is well established and its repositioning has been completed, sales in

directly-operated stores were up 2.1% year on year on a comparable basis, with a 19.0% bounce in the

second quarter, powered by an increase in sales to tourists.

In emerging markets (which accounted for 46.8% of the brand's sales in directly-operated stores versus

47.2% in first-half 2014, as reported), sales moved back 1.8% on a comparable exchange rate basis,

primarily as a result of a 3.6% contraction in the Asia-Pacific region. This downward trend in Asia-Pacific

(excluding Japan) was entirely due to the ongoing decline in consumer spending in Hong Kong and

Macao, as sales in Mainland China were up year on year and South Korea and Australia reported a

very solid sales performance in line with the rise in tourist numbers. The brand's revenue in other

emerging markets was higher than in first-half 2014 overall despite flat sales in the Middle East.

By product category, Gucci's performance in directly-operated stores was similar to 2014 for Leather

Goods. Handbag sales in directly-operated stores were up significantly, but weaker performances were

seen once again for small leather goods and luggage – two categories that were partially revisited in

connection with Gucci’s strategy to render the brand more exclusive and as a result of the arrival of the

new Creative Director.

Leather Goods represented 57.8% of Gucci's total revenue during the period.

The brand's other main product categories (Shoes and Ready-to-Wear) also delivered growth in the first

six months of 2015, spurred by the upswing in sales of Women's Ready-to-Wear lines, which started to

be felt in 2014 and continued into the first half of 2015. Shoes and Ready-to-Wear represented 25.9%

of Gucci's total revenue during the period.

Wholesale sales dropped by 20.9% on a comparable basis in the first half of 2015, reflecting the new

phase in the plan to drastically streamline this distribution channel, particularly in the multi-brand

distributors segment. All product categories were affected by the additional reduction in volumes

distributed by wholesalers.

Overall, Gucci's performance in the first six months of 2015 was largely based on sales of collections

presented in 2014 and does not fully reflect the measures and initiatives put in place by Marco Bizzarri

since he joined the brand as its new President and CEO at the beginning of the year. The first collection

fully designed by Alessandro Michele – which was highly acclaimed when presented in New York in

June 2015 – was the 2016 Cruise collection, which will be available in stores as from the end of the third

quarter of 2015.

Gucci's recurring operating income for first-half 2015 came in at just under €502 million, down 4.9%

year on year as reported. The brand's recurring operating margin narrowed by 470 basis points to

26.8%. More than half of this decrease was due to the dilutive impact of currency hedges during the

period and the remainder was attributable to an increase in operating expenses, which primarily derived

from higher store running costs.

Gross margin was also down year on year on a reported basis but stable at constant exchange rates.

EBITDA amounted to €587 million in first-half 2015 and the EBITDA margin remained very high, at

31.3% of revenue.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 20

As of June 30, 2015, Gucci operated 512 stores, including 211 in emerging markets. A net seven stores

were added during the period, including two in South Africa previously operated by a third party that

have been brought under direct management.

Gucci's gross operating investments amounted to €77 million in first-half 2015, up 14.7% on the same

period of 2014. This increase was due to differences in the phasing of investments compared to last

year, and to currency effects on investments outside the eurozone.

Bottega Veneta

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 629.2 525.5 +19.7%

Recurring operating income 180.1 163.1 +10.4%

as a % of revenue 28.6% 31.0% -2.4 pts

EBITDA 198.6 177.7 +11.8%

as a % of revenue 31.6% 33.8% -2.2 pts

Gross operating investments 20.7 18.6 +11.3%

Average headcount 3,350 3,146 +6.5%

Bottega Veneta posted revenue of €629 million in first-half 2015, up 19.7% as reported and 6.4% at

comparable exchange rates. The brand's growth rate was higher in the second quarter, at 9.3% on a

comparable basis.

With a view to preserving its high-end positioning and exclusivity, Bottega Veneta's preferred distribution

channel is its directly-operated stores, and in the first six months of 2015 this distribution channel

accounted for 83.0% of the brand's total sales. Year-on-year revenue growth for directly-operated stores

amounted to 7.2% overall on a comparable basis. First-quarter growth was somewhat subdued, coming

in at just 1.9% based on comparable data, as it was weighed down by unfavourable market conditions

in the Asia-Pacific region as well as by widening price differences between geographic areas due to the

weakening of the euro against many of the world’s other major currencies. However, thanks to

corrective measures put in place by Bottega Veneta to effectively manage pricing differences, combined

with the sharp rise in tourist numbers in the main travel destinations, the brand's sales performance in

its directly-operated stores was far more robust in the second quarter, with revenue up 12.2% on a

comparable basis.

Sales generated in the wholesale network increased 2.4% in first-half 2015. However, this overall figure

masks contrasted trends: during the period Bottega Veneta focused on a small number of strategic

markets – such as North America, South Korea and the Middle East – where sales trends were very

strong, with growth hovering around or exceeding 10%.

Leather Goods once again formed the brand's core business, representing 88.4% of Bottega Veneta's

total sales during the six-month period and recording very solid year-on-year growth of 8.3%. This

strong performance demonstrates the success of the strategy underlying the brand's offering, which is

based on a controlled combination of iconic pieces, new seasonal designs and new leather goods

models whose design and pricing structure have been reviewed in order to more closely take into

account customers' expectations.

Financial information for first-half 2015 – Activity report 2

21 2015 First-Half Report – Kering

Unlike previous periods, Bottega Veneta's sales growth in first-half 2015 was very unevenly balanced

between its traditional and emerging markets, which recorded a 15.8% revenue rise and a 3.9%

contraction, respectively (at comparable exchange rates).

The Asia-Pacific region (excluding Japan) once again accounted for over 90% of Bottega Veneta's

business in emerging markets. Sales in this region dropped 4.3% year on year, weighed down by the

lacklustre Luxury goods market in Greater China during the period, despite the very positive trends

seen in South Korea, Taiwan and Australia, where purchases by Chinese tourists increased

significantly.

In Western Europe – which represents 28.4% of the brand's total revenue – sales surged 25.3% on a

comparable basis, driven by extremely high tourist numbers.

In Japan – which made up 15.0% of total sales – revenue advanced 13.0% at constant exchange rates,

powered by ongoing growth trends in the domestic market and high levels of purchases by Chinese

customers.

Sales in North America increased 2.1% overall on a comparable basis, reflecting the combined impact

of continued growth in revenue generated with department stores and a decrease in the number of

tourists due to the strengthening of the US dollar.

Bottega Veneta posted recurring operating income of €180 million for the six months ended

June 30, 2015, up 10.4% year on year. Recurring operating margin came in at 28.6%, down 240 basis

points as reported. However, adjusted for the currency effect and the impact of currency hedges,

profitability was roughly unchanged compared to the first half of 2014.

EBITDA climbed almost 12% to just under €199 million. This represents a higher rise than for recurring

operating income, due to an increase in depreciation and amortisation expenses resulting from the

brand's investments in recent years.

Bottega Veneta's network of directly-operated stores totalled 240 units as of June 30, 2015, including

100 in emerging markets. There were four net store additions during the first half.

Bottega Veneta's gross operating investments totalled nearly €21 million compared with €19 million in

first-half 2014. This slight year-on-year increase includes the automatic impact of currency effects on

investments outside the eurozone.

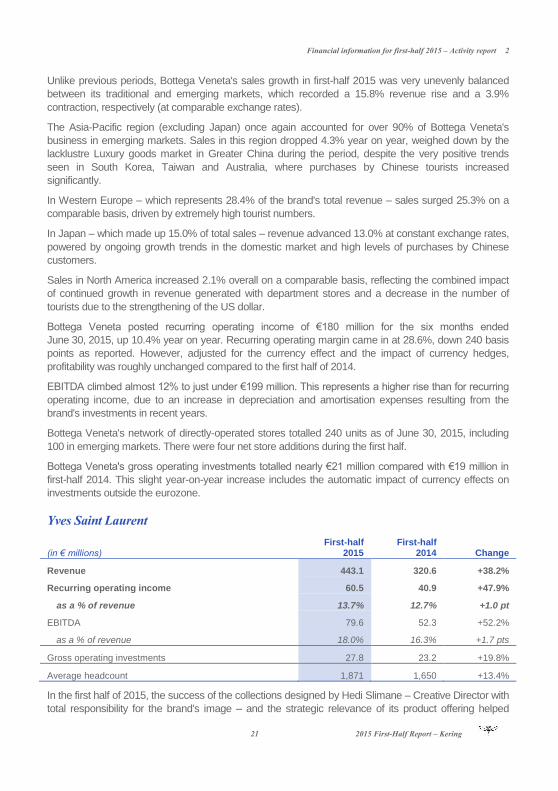

Yves Saint Laurent

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 443.1 320.6 +38.2%

Recurring operating income 60.5 40.9 +47.9%

as a % of revenue 13.7% 12.7% +1.0 pt

EBITDA 79.6 52.3 +52.2%

as a % of revenue 18.0% 16.3% +1.7 pts

Gross operating investments 27.8 23.2 +19.8%

Average headcount 1,871 1,650 +13.4%

In the first half of 2015, the success of the collections designed by Hedi Slimane – Creative Director with

total responsibility for the brand's image – and the strategic relevance of its product offering helped

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 22

further strengthen Yves Saint Laurent's brand appeal. This appeal – which was given an additional

boost by continued investments in the brand's stores and a 360° communication strategy – resulted in

very robust growth for Yves Saint Laurent during the period.

Yves Saint Laurent's revenue totalled €443 million for first-half 2015, a year-on-year surge of 38.2% as

reported and 24.3% based on comparable exchange rates. As for the Group's other Luxury brands, the

pace of growth accelerated in the second quarter, reaching 27.3% based on comparable data versus

21.2% in the first.

The investments undertaken for the directly-operated store network since 2012 have enabled

Yves Saint Laurent to increase the portion of sales generated through this exclusive distribution

channel, which accounted for around 64% of the brand’s total sales in first-half 2015. Revenue from

retail sales in directly-operated stores advanced by 25.7% during the period, driven by a sharp increase

in same-store sales.

Wholesale sales were up 21.9% based on comparable data, illustrating independent distributor

appreciation of the brand as a major growth driver for their business. This distribution channel also

remains strategically important for Yves Saint Laurent as it represents a perfect fit with its retail channel.

Following on from the upswing in the last quarter of 2014, revenue from royalties rose by 21.5% in the

first six months of 2015, compared with a relatively weak performance in first-half 2014.

All of Yves Saint Laurent's main product categories registered very strong sales growth during the

period.

The brand's Leather Goods offering continues to prove highly attractive, particularly as the price

structure has been partially revisited to reflect changes in exchange rates and market conditions in

certain regions. Sales posted by this category climbed by 22.6%.

Revenue from Ready-to-Wear sales jumped by 26.8% at constant exchange rates and this category

once again occupied an essential place in the brand's product offering, with well-balanced sales of

Women's and Men's collections.

Yves Saint Laurent notched up revenue increases across all of its geographic regions in the first six

months of 2015.

In emerging markets – which contributed 29.5% of the brand's total revenue for the period – sales grew

10.7%. The economic climate in Hong Kong and Mainland China weighed on the brand's performance

in Greater China, although revenue nonetheless climbed by 7.1% in this region based on comparable

data. Business was buoyant in other Asia-Pacific countries as well as in Latin America, but was less

brisk in the Middle East and Eastern Europe.

Sales in Yves Saint Laurent's traditional markets soared by 31.1% on a comparable basis, reflecting the

brand's renewed appeal both with local customers and with tourists from emerging markets. Revenue

growth reached extremely high levels across all of these regions, coming in at 34.2% in Japan, where

the brand was in remarkably high demand, 32.9% in North America, and 29.3% in Western Europe.

Yves Saint Laurent ended the first half of 2015 with recurring operating income of €61 million, versus

around €41 million in the corresponding prior-year period, representing a year-on-year increase of

47.9%. Recurring operating margin reached 13.7%, up by 100 basis points as reported. This rise was

even higher after stripping out the impacts of fluctuations in exchange rates and currency hedges. It was

led by a further increase in gross margin (excluding currency hedges) and a better absorption of fixed

costs, and was achieved despite the brand-development costs incurred to expand the store network

and implement an active brand marketing policy.

Financial information for first-half 2015 – Activity report 2

23 2015 First-Half Report – Kering

Given the growing weight of depreciation and amortisation, EBITDA rose at a faster pace than recurring

operating income, coming in at €80 million. The EBITDA margin was 18.0%, up 170 basis points on

first-half 2014.

As of June 30, 2015, the Yves Saint Laurent brand directly operated 132 stores, including 56 in

emerging markets. There were only four net store additions during the period, as operating investments

were focused more on extending, relocating and refurbishing existing stores.

Overall, the brand's gross operating investments came to nearly €28 million, representing a €5 million

increase on first-half 2014.

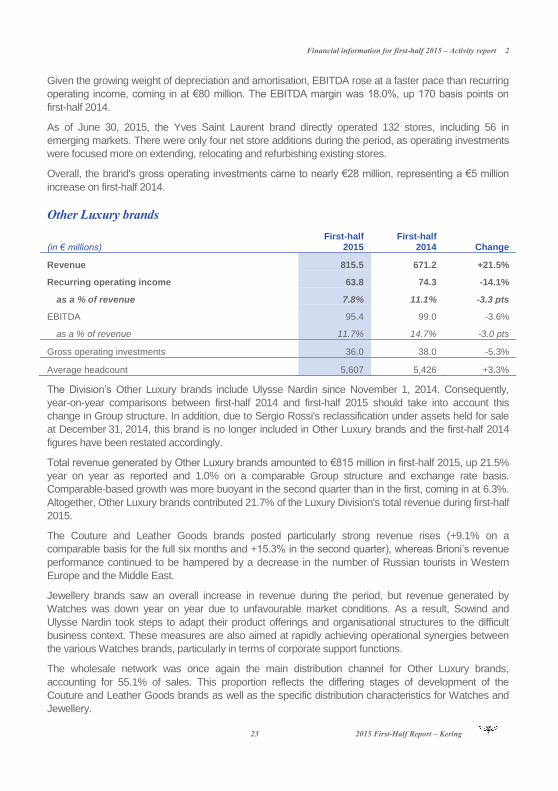

Other Luxury brands

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 815.5 671.2 +21.5%

Recurring operating income 63.8 74.3 -14.1%

as a % of revenue 7.8% 11.1% -3.3 pts

EBITDA 95.4 99.0 -3.6%

as a % of revenue 11.7% 14.7% -3.0 pts

Gross operating investments 36.0 38.0 -5.3%

Average headcount 5,607 5,426 +3.3%

The Division’s Other Luxury brands include Ulysse Nardin since November 1, 2014. Consequently,

year-on-year comparisons between first-half 2014 and first-half 2015 should take into account this

change in Group structure. In addition, due to Sergio Rossi's reclassification under assets held for sale

at December 31, 2014, this brand is no longer included in Other Luxury brands and the first-half 2014

figures have been restated accordingly.

Total revenue generated by Other Luxury brands amounted to €815 million in first-half 2015, up 21.5%

year on year as reported and 1.0% on a comparable Group structure and exchange rate basis.

Comparable-based growth was more buoyant in the second quarter than in the first, coming in at 6.3%.

Altogether, Other Luxury brands contributed 21.7% of the Luxury Division's total revenue during first-half

2015.

The Couture and Leather Goods brands posted particularly strong revenue rises (+9.1% on a

comparable basis for the full six months and +15.3% in the second quarter), whereas Brioni’s revenue

performance continued to be hampered by a decrease in the number of Russian tourists in Western

Europe and the Middle East.

Jewellery brands saw an overall increase in revenue during the period, but revenue generated by

Watches was down year on year due to unfavourable market conditions. As a result, Sowind and

Ulysse Nardin took steps to adapt their product offerings and organisational structures to the difficult

business context. These measures are also aimed at rapidly achieving operational synergies between

the various Watches brands, particularly in terms of corporate support functions.

The wholesale network was once again the main distribution channel for Other Luxury brands,

accounting for 55.1% of sales. This proportion reflects the differing stages of development of the

Couture and Leather Goods brands as well as the specific distribution characteristics for Watches and

Jewellery.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 24

Sales generated in the wholesale network decreased 6.4% year on year on a comparable basis. A

contraction in wholesale sales of Watches, particularly in emerging markets, offset positive revenue

trends for the Couture, Leather Goods and Jewellery brands. In addition, due to the volatility of some of

the markets in which they operate, wholesalers remained generally prudent in the first half of 2015 in

terms of volumes purchased.

Conversely, retail sales in directly-operated stores advanced 13.1% based on comparable data. This

performance was led by the Couture and Leather Goods brands as a result of the successful, controlled

expansion of their exclusive distribution networks. Retails sales in directly-operated stores rose a brisk

8.0% in the first three months of the year and an even sharper 18.0% in the second quarter, boosted by

high tourist numbers.

Ready-to-Wear remained the best-selling product category, making up 30.9% of total Other Luxury

brands revenue, and reported year-on-year sales growth. Watches and Jewellery represented the

second largest revenue generator, accounting for 28.6% of the total, but this category saw contrasting

trends during the period between its two different segments (year-on-year growth for Jewellery and a

contraction for Watches). Leather Goods and Shoes posted the highest year-on-year increase in

revenue among Other Luxury brands for the six months ended June 30, 2015.

Revenue generated in mature markets rose 5.2% on a comparable basis in first-half 2015, whereas

business in emerging markets contracted by 8.9%.

This reflects the fact that the performance of some brands (particularly Brioni and Ulysse Nardin) was

weighed down by weak demand in Eastern Europe and the Middle East, as well as in Hong Kong in the

case of Watches. Sales of other brands continued their upward trend in the Asia-Pacific region,

however, with growth coming in at 2.6%, led by the strong performance of the Couture and Leather

Goods brands, whose revenue in the region advanced 16.1% on a comparable basis thanks to their

increasing appeal and renown in key Asian countries.

In mature markets – which accounted for 73.1% of total sales – Japan and Western Europe were once

again the main growth drivers, powered by an upswing in domestic consumer spending and a sharp

rise in tourism.

Recurring operating income for Other Luxury brands retreated 14.1% to €64 million in first-half 2015,

and recurring operating margin narrowed by 330 basis points to 7.8%, partly due to the adverse impact

of currency hedges. These overall figures also reflect the decrease in profitability reported by the

Watches brands, which suffered a steep drop in gross margin due to the sharp rise in the Swiss franc

and continued unsettled market conditions.

EBITDA came in at just over €95 million, down by a more contained 3.6% on first-half 2014 as reported.

The network of directly-operated stores owned by the Other Luxury brands totalled 317 units as of

June 30, 2015, unchanged from December 31, 2014. There were 16 store openings during the period,

offset by 16 closures. As of June 30, 2015, the network comprised 228 stores in mature markets and 89 in

emerging markets, including 58 in Greater China.

Despite a negative currency effect arising from the translation of foreign currency-denominated capital

expenditures, gross operating investments decreased year on year to €36 million. As in 2014, this

reflects the brands' highly selective and disciplined investment strategies.

Financial information for first-half 2015 – Activity report 2

25 2015 First-Half Report – Kering

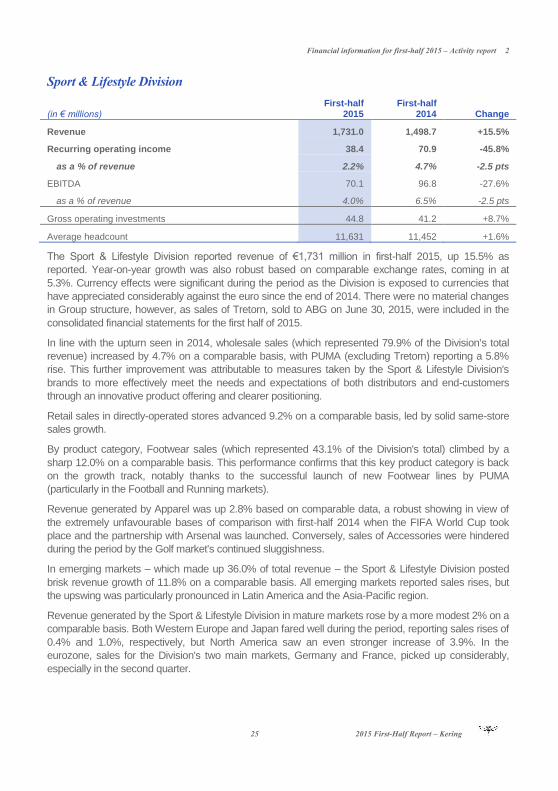

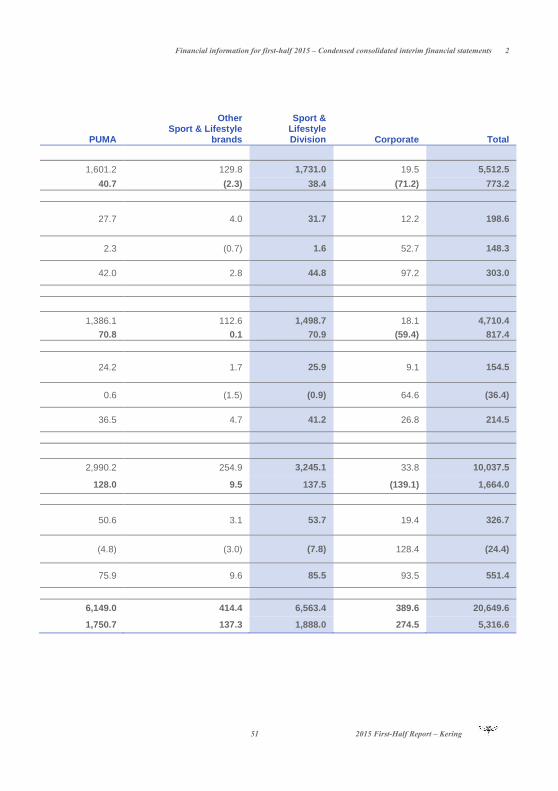

Sport & Lifestyle Division

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 1,731.0 1,498.7 +15.5%

Recurring operating income 38.4 70.9 -45.8%

as a % of revenue 2.2% 4.7% -2.5 pts

EBITDA 70.1 96.8 -27.6%

as a % of revenue 4.0% 6.5% -2.5 pts

Gross operating investments 44.8 41.2 +8.7%

Average headcount 11,631 11,452 +1.6%

The Sport & Lifestyle Division reported revenue of €1,731 million in first-half 2015, up 15.5% as

reported. Year-on-year growth was also robust based on comparable exchange rates, coming in at

5.3%. Currency effects were significant during the period as the Division is exposed to currencies that

have appreciated considerably against the euro since the end of 2014. There were no material changes

in Group structure, however, as sales of Tretorn, sold to ABG on June 30, 2015, were included in the

consolidated financial statements for the first half of 2015.

In line with the upturn seen in 2014, wholesale sales (which represented 79.9% of the Division's total

revenue) increased by 4.7% on a comparable basis, with PUMA (excluding Tretorn) reporting a 5.8%

rise. This further improvement was attributable to measures taken by the Sport & Lifestyle Division's

brands to more effectively meet the needs and expectations of both distributors and end-customers

through an innovative product offering and clearer positioning.

Retail sales in directly-operated stores advanced 9.2% on a comparable basis, led by solid same-store

sales growth.

By product category, Footwear sales (which represented 43.1% of the Division's total) climbed by a

sharp 12.0% on a comparable basis. This performance confirms that this key product category is back

on the growth track, notably thanks to the successful launch of new Footwear lines by PUMA

(particularly in the Football and Running markets).

Revenue generated by Apparel was up 2.8% based on comparable data, a robust showing in view of

the extremely unfavourable bases of comparison with first-half 2014 when the FIFA World Cup took

place and the partnership with Arsenal was launched. Conversely, sales of Accessories were hindered

during the period by the Golf market's continued sluggishness.

In emerging markets – which made up 36.0% of total revenue – the Sport & Lifestyle Division posted

brisk revenue growth of 11.8% on a comparable basis. All emerging markets reported sales rises, but

the upswing was particularly pronounced in Latin America and the Asia-Pacific region.

Revenue generated by the Sport & Lifestyle Division in mature markets rose by a more modest 2% on a

comparable basis. Both Western Europe and Japan fared well during the period, reporting sales rises of

0.4% and 1.0%, respectively, but North America saw an even stronger increase of 3.9%. In the

eurozone, sales for the Division's two main markets, Germany and France, picked up considerably,

especially in the second quarter.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 26

The Sport & Lifestyle Division ended the first half of 2015 with recurring operating income of €38 million,

compared with €71 million in the same period of 2014, and the recurring operating margin narrowed by

250 basis points to 2.2%. This fall in profitability mainly reflects the lower margin recorded by PUMA,

primarily due to higher cost of goods sold in light of the brand's significant exposure to the US dollar, as

well as to an expected increase in marketing and communications costs during the period.

EBITDA totalled around €70 million, representing a year-on-year decrease of 27.6%.

Gross operating investments were contained at €45 million in the first six months of 2015, with the year-

on-year rise primarily stemming from currency effects.

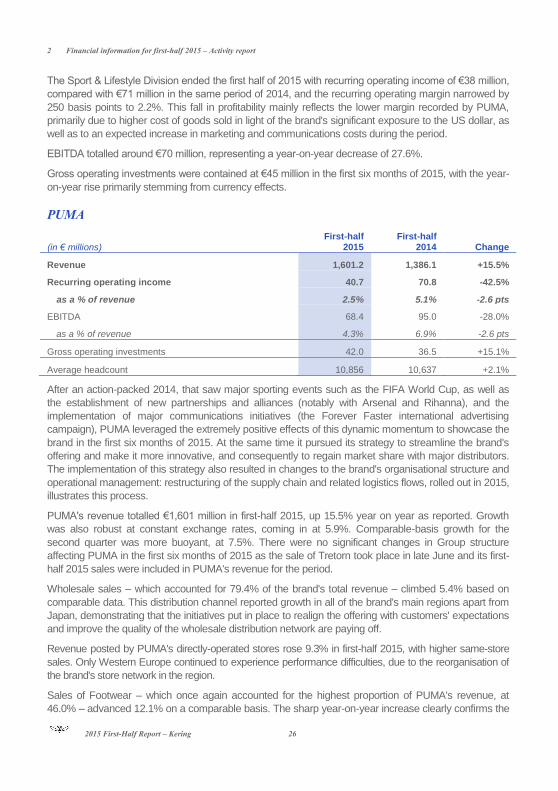

PUMA

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 1,601.2 1,386.1 +15.5%

Recurring operating income 40.7 70.8 -42.5%

as a % of revenue 2.5% 5.1% -2.6 pts

EBITDA 68.4 95.0 -28.0%

as a % of revenue 4.3% 6.9% -2.6 pts

Gross operating investments 42.0 36.5 +15.1%

Average headcount 10,856 10,637 +2.1%

After an action-packed 2014, that saw major sporting events such as the FIFA World Cup, as well as

the establishment of new partnerships and alliances (notably with Arsenal and Rihanna), and the

implementation of major communications initiatives (the Forever Faster international advertising

campaign), PUMA leveraged the extremely positive effects of this dynamic momentum to showcase the

brand in the first six months of 2015. At the same time it pursued its strategy to streamline the brand's

offering and make it more innovative, and consequently to regain market share with major distributors.

The implementation of this strategy also resulted in changes to the brand's organisational structure and

operational management: restructuring of the supply chain and related logistics flows, rolled out in 2015,

illustrates this process.

PUMA's revenue totalled €1,601 million in first-half 2015, up 15.5% year on year as reported. Growth

was also robust at constant exchange rates, coming in at 5.9%. Comparable-basis growth for the

second quarter was more buoyant, at 7.5%. There were no significant changes in Group structure

affecting PUMA in the first six months of 2015 as the sale of Tretorn took place in late June and its first-

half 2015 sales were included in PUMA's revenue for the period.

Wholesale sales – which accounted for 79.4% of the brand's total revenue – climbed 5.4% based on

comparable data. This distribution channel reported growth in all of the brand's main regions apart from

Japan, demonstrating that the initiatives put in place to realign the offering with customers' expectations

and improve the quality of the wholesale distribution network are paying off.

Revenue posted by PUMA's directly-operated stores rose 9.3% in first-half 2015, with higher same-store

sales. Only Western Europe continued to experience performance difficulties, due to the reorganisation of

the brand's store network in the region.

Sales of Footwear – which once again accounted for the highest proportion of PUMA's revenue, at

46.0% – advanced 12.1% on a comparable basis. The sharp year-on-year increase clearly confirms the

Financial information for first-half 2015 – Activity report 2

27 2015 First-Half Report – Kering

brand's recovery in this key product category following the initial signs of a turnaround in the third

quarter of 2014. This improved performance was driven by the launch of new product ranges in the

Running, Training and Football categories, which proved very popular both with distributors and end-

customers. One of the most emblematic recent launches was Ignite – a running shoe available in

performance as well as lifestyle versions.

Apparel sales (33.9% of PUMA's total revenue for first-half 2015) climbed 3.0% on a comparable basis.

Growth for this category was once again very solid in all of the brand's regions, except for Europe due to

an extremely unfavourable base of comparison in first-half 2014 due to sales of replica football jerseys

during the FIFA World Cup.

Emerging markets made up 37.8% of PUMA's first-half 2015 revenue, versus 35.9% for the same

period of 2014 as reported. Sales in these markets advanced 12.0% on a comparable basis. PUMA's

revenue in Mainland China surged by 20.6%, reflecting the successful measures launched in 2013 to

reorganise the brand's distribution in the country. Sales trends were also extremely positive in the

brand's other major emerging markets, especially Latin America, India and Turkey.

In Western Europe, revenue edged up 0.6% based on comparable data, led by a more marked sales

recovery in eurozone countries, particularly Germany and France.

In North America, sales growth was once again brisk, up 5.3% on a comparable basis. The Footwear

category posted the highest year-on-year revenue rise in this region, a very encouraging sign.

In Japan, the brand returned to growth (up 1.0% on a comparable basis) despite ongoing tough

conditions in the Golf accessories market.

PUMA's contribution to the Group's recurring operating income amounted to €41 million in the first six

months of 2015 and the brand's recurring operating margin decreased by 260 basis points to 2.5%.

EBITDA contracted year on year to €68 million.

The €30 million decrease in recurring operating income in absolute terms chiefly stemmed from an

increase in operating expenses – primarily communication and marketing costs incurred as part of

PUMA's announced brand investment plan.

The lower recurring operating margin was partly attributable to adverse currency effects as the rise in

the US dollar pushed up supply costs and the brand’s currency hedges and targeted price increases

were not sufficient to offset the resulting negative impact on gross margin. Consequently, PUMA’s gross

margin narrowed by 100 basis points as reported, but at constant exchange rates it improved slightly

year on year. The decline in recurring operating margin was also due to higher marketing and

communication costs as a percentage of revenue.

As of June 30, 2015 PUMA's directly-operated retail network included 620 stores, down four from

December 31, 2014.

Gross operating investments amounted to €42 million, up 15.1% on first-half 2014, reflecting the

combined impact of the conversion into euros of investments undertaken outside the eurozone and the

brand's continuing measures to overhaul its supply chain and information systems.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 28

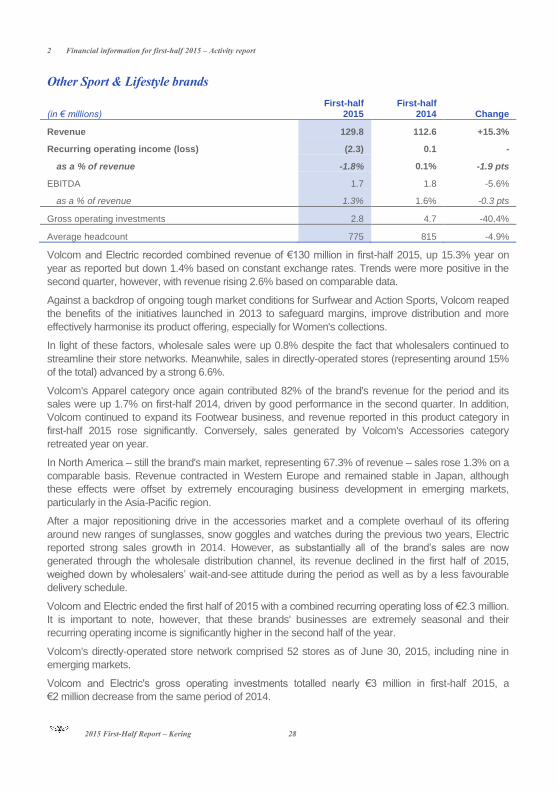

Other Sport & Lifestyle brands

(in € millions)

First-half 2015

First-half 2014 Change

Revenue 129.8 112.6 +15.3%

Recurring operating income (loss) (2.3) 0.1 -

as a % of revenue -1.8% 0.1% -1.9 pts

EBITDA 1.7 1.8 -5.6%

as a % of revenue 1.3% 1.6% -0.3 pts

Gross operating investments 2.8 4.7 -40.4%

Average headcount 775 815 -4.9%

Volcom and Electric recorded combined revenue of €130 million in first-half 2015, up 15.3% year on

year as reported but down 1.4% based on constant exchange rates. Trends were more positive in the

second quarter, however, with revenue rising 2.6% based on comparable data.

Against a backdrop of ongoing tough market conditions for Surfwear and Action Sports, Volcom reaped

the benefits of the initiatives launched in 2013 to safeguard margins, improve distribution and more

effectively harmonise its product offering, especially for Women's collections.

In light of these factors, wholesale sales were up 0.8% despite the fact that wholesalers continued to

streamline their store networks. Meanwhile, sales in directly-operated stores (representing around 15%

of the total) advanced by a strong 6.6%.

Volcom's Apparel category once again contributed 82% of the brand's revenue for the period and its

sales were up 1.7% on first-half 2014, driven by good performance in the second quarter. In addition,

Volcom continued to expand its Footwear business, and revenue reported in this product category in

first-half 2015 rose significantly. Conversely, sales generated by Volcom's Accessories category

retreated year on year.

In North America – still the brand's main market, representing 67.3% of revenue – sales rose 1.3% on a

comparable basis. Revenue contracted in Western Europe and remained stable in Japan, although

these effects were offset by extremely encouraging business development in emerging markets,

particularly in the Asia-Pacific region.

After a major repositioning drive in the accessories market and a complete overhaul of its offering

around new ranges of sunglasses, snow goggles and watches during the previous two years, Electric

reported strong sales growth in 2014. However, as substantially all of the brand’s sales are now

generated through the wholesale distribution channel, its revenue declined in the first half of 2015,

weighed down by wholesalers’ wait-and-see attitude during the period as well as by a less favourable

delivery schedule.

Volcom and Electric ended the first half of 2015 with a combined recurring operating loss of €2.3 million.

It is important to note, however, that these brands' businesses are extremely seasonal and their

recurring operating income is significantly higher in the second half of the year.

Volcom's directly-operated store network comprised 52 stores as of June 30, 2015, including nine in

emerging markets.

Volcom and Electric's gross operating investments totalled nearly €3 million in first-half 2015, a

€2 million decrease from the same period of 2014.

Financial information for first-half 2015 – Activity report 2

29 2015 First-Half Report – Kering

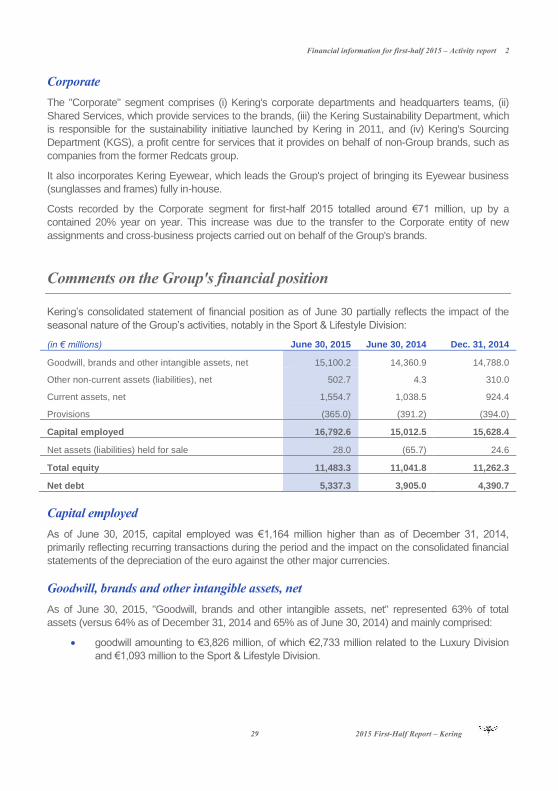

Corporate

The "Corporate" segment comprises (i) Kering's corporate departments and headquarters teams, (ii)

Shared Services, which provide services to the brands, (iii) the Kering Sustainability Department, which

is responsible for the sustainability initiative launched by Kering in 2011, and (iv) Kering's Sourcing

Department (KGS), a profit centre for services that it provides on behalf of non-Group brands, such as

companies from the former Redcats group.

It also incorporates Kering Eyewear, which leads the Group's project of bringing its Eyewear business

(sunglasses and frames) fully in-house.

Costs recorded by the Corporate segment for first-half 2015 totalled around €71 million, up by a

contained 20% year on year. This increase was due to the transfer to the Corporate entity of new

assignments and cross-business projects carried out on behalf of the Group's brands.

Comments on the Group's financial position

Kering’s consolidated statement of financial position as of June 30 partially reflects the impact of the

seasonal nature of the Group’s activities, notably in the Sport & Lifestyle Division:

(in € millions) June 30, 2015 June 30, 2014 Dec. 31, 2014

Goodwill, brands and other intangible assets, net 15,100.2 14,360.9 14,788.0

Other non-current assets (liabilities), net 502.7 4.3 310.0

Current assets, net 1,554.7 1,038.5 924.4

Provisions (365.0) (391.2) (394.0)

Capital employed 16,792.6 15,012.5 15,628.4

Net assets (liabilities) held for sale 28.0 (65.7) 24.6

Total equity 11,483.3 11,041.8 11,262.3

Net debt 5,337.3 3,905.0 4,390.7

Capital employed

As of June 30, 2015, capital employed was €1,164 million higher than as of December 31, 2014,

primarily reflecting recurring transactions during the period and the impact on the consolidated financial

statements of the depreciation of the euro against the other major currencies.

Goodwill, brands and other intangible assets, net

As of June 30, 2015, "Goodwill, brands and other intangible assets, net" represented 63% of total

assets (versus 64% as of December 31, 2014 and 65% as of June 30, 2014) and mainly comprised:

goodwill amounting to €3,826 million, of which €2,733 million related to the Luxury Division

and €1,093 million to the Sport & Lifestyle Division.

2 Financial information for first-half 2015 – Activity report

2015 First-Half Report – Kering 30

brands valued at €10,880 million, of which €6,960 million for the Luxury Division and

€3,920 million for the Sport & Lifestyle Division. The increase in this item between

December 31, 2014 and June 30, 2015 was primarily attributable to the amount recognised

for the Ulysse Nardin brand as part of the provisional purchase price allocation process.

Net of deferred tax liabilities relating to brands (which are recorded under "Other non-current assets

(liabilities), net", as shown below), this item came to €12,348 million as of June 30, 2015.

Other non-current assets, net

(in € millions) June 30, 2015 June 30, 2014 Dec. 31, 2014

Property, plant and equipment, net 2,003.1 1,683.4 1,887.2

Net deferred tax liabilities (2,035.2) (2,036.1) (2,033.8)

Investments in equity-accounted companies 21.6 19.1 23.2

Non-current financial assets, net 455.1 302.2 397.2

Other 58.1 35.7 36.2

Other non-current assets, net 502.7 4.3 310.0

"Property, plant and equipment, net" rose in first-half 2015 due to the impact of changes in Group

structure (notably the first-time consolidation of Ulysse Nardin as of November 1, 2014), recurring

transactions (acquisitions/disposals and depreciation), and exchange rate fluctuations.

Deferred tax liabilities chiefly relate to brands recognised on business combinations, notably Gucci and

PUMA.

As of June 30, 2015, investments in equity-accounted companies comprised shares in Tomas Maier,

Joseph Altuzarra and Wilderness.

Current assets, net

As of June 30, 2015, net current assets totalled €1,555 million, versus €1,038 million as of

June 30, 2014 and €924 million as of December 31, 2014. This item breaks down as follows:

(in € millions) June 30, 2015 June 30, 2014 Dec. 31, 2014

Inventories 2,474.0 2,079.7 2,234.7

Trade receivables 1,115.2 988.2 1,030.0

Trade payables (1,051.1) (929.8) (982.8)

Current tax receivables/payables (181.5) (271.5) (139.5)

Other current assets and liabilities (801.9) (828.1) (1,218.0)

Current assets, net 1,554.7 1,038.5 924.4

As of June 30, 2015, Kering's net current assets were €630 million higher than at December 31, 2014.

After stripping out the impact of fluctuations in exchange rates and changes in Group structure, changes

in working capital requirement led to a cash outflow of €428 million.

Financial information for first-half 2015 – Activity report 2

31 2015 First-Half Report – Kering

Changes in inventories (adjusted for the impact of fluctuations in exchange rates and changes in Group

structure) resulted in a cash outflow of €253 million during the first half of 2015. The increase in

inventories during the period reflects (i) changes in the Luxury Division's sales volumes and (ii) higher

volumes of purchases by PUMA in order to maintain sales levels and – to a lesser extent – phasing of

inventory build-up.

Excluding the impact of fluctuations in exchange rates and changes in Group structure, the increase in

trade receivables during first-half 2015 led to a €46 million cash outflow. However this impact was partly