Fintech 2016 Edinburgh

242

Welcome To

-

Upload

ray-bugg -

Category

Technology

-

view

129 -

download

1

Transcript of Fintech 2016 Edinburgh

Welcome To

Ray BuggScot-Tech

@scot_tech#ftscot

#scotdata

Our Next Event - 8th Dec 2016

Theo PriestleyConference Chair

@tprstly#ftscot

Yafei TianCiti Group

@tyafei#ftscot

See Appendix A-1 for Analyst Certification, Important Disclosures and non-US research analyst disclosures

Citi Research is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be

aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Certain products (not inconsistent with the author’s published research) are available only on Citi's portals.

This presentation was approved for distribution on 3 October 2016; the disclosures in Appendix A1 are current as of the same date.

.

DIGITAL DISRUPTION

03 October 2016

Yafei Tian

Citi Banks Research

+44 (0) 20 7986 4100

How FinTech is Forcing Banking to a Tipping Point

8

Who Has a Phone?

Source: Citi Research

9

A Long Time Ago

1990

10

Did you Guess Correctly?

1%

11

Leap Frog

Source: Citi Research

Disruption Risks

12

13

Follow the Money

Private Investment in Global FinTech Companies ($bn)

“Silicon Valley is coming. There are hundreds of start-ups

with a lot of brains and money working on various

alternatives to traditional banking.” - Jamie Dimon

FinTech investments have grown exponentially: $19bn in

2015 was up two-thirds from $12bn in 2014. By client

segment, Consumer and SME are the focus (73%). By

product, Marketplace/P2P lending (46%) and Payments

(23%) dominate FinTech dollars invested.

B2C dominates due to changing consumer behaviour, the

smartphone revolution and lower switching costs. Future

investment into B2B could grow.

Source: Citi and CB Insights; Includes first round and subsequent private investments.

0

5

10

15

20

2010 2011 2012 2013 2014 2015

14

Follow the Money

Capital Deployed in Private FinTech Companies By Segment

Capital Deployed in Private FinTech Companies By Business Area

Source: CBInsights, KPMG, Crunch Base and Citi Research; Based on c120 private companies from CBInsights FinTech Periodic table Dec 2014; KPMG’s top 50 most prominent FinTech innovators Dec 2015; Valuation based on Crunch Base Total Equity Funding for private companies and exit value for acquired companies

Personal & SME73%

Asset Management & Wealth10%

Insurance10%

Investment Banking4%

Large Corporate3%

Digital Currency3%

Equity crowdfunding2%

Institutional Tools3%

Lending46%

Money Transfer3%

Payment23%

Savings & Wealth10%

Insurance10%

15

Different is Better than Cheaper

For FinTech Competitive Edge, Different and Capital Light is Key

Not all FinTech new entrants will have a sustainable

competitive advantage. Many FinTech companies may be

better or lower cost than banks rather than different.

Companies that are different rather than having a lower

cost to serve are more likely to maintain their competitive

edge for longer.

Different does not need to be technologically different. It

can be a different target market (iZettle) or a new business

model (Credit Karma or Funding Circle).

A lower cost business model can – for a period of time – be

a form of a differentiation. But lower cost models may get

copied faster by competitors and incumbents.

Banks’ have a natural advantage in capital intensive

products. Most plain vanilla retail and corporate banking is

capital intensive and relatively low cost.

Activities that are capital light (credit scoring, payments,

P2P lending as an agent not principal) are more likely to be

disrupted by new digital business models

Source: Citi Research

Marketplace Lending (Funding Circle)

PoS/ Card Acceptance (iZettle)

Payments (Klarna)

Credit Scoring (Credit Karma)

Lending Platforms (Kabbage)

Corporate Lending

Wholesale Banking

Mortgage Lending

Robo Advisors (NutMeg)

DifferentCheaper

Cap

ital L

ight

Cap

ital I

nten

sive

16

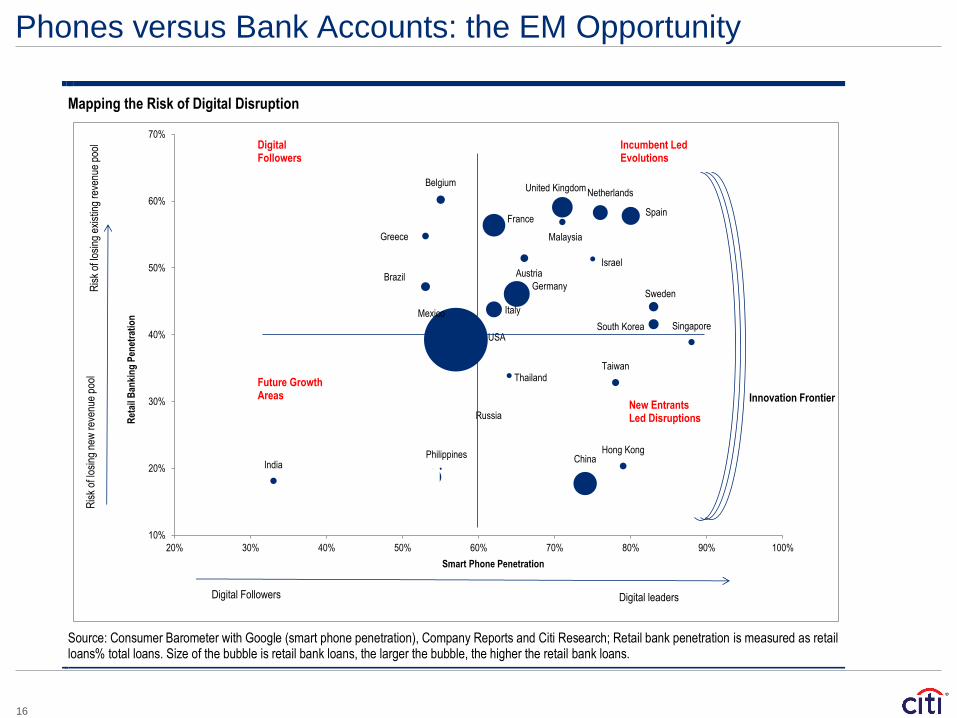

Phones versus Bank Accounts: the EM Opportunity

Mapping the Risk of Digital Disruption

Underdeveloped banking systems. Emerging markets

such as China, India and Philippines have a large

unbanked/underbanked population. Consumer banking is

often underdeveloped in many emerging markets.

High level of smart phone penetration. Some countries

such as China and Malaysia have smart phone penetration

on par with DM counterparts. Others may have fewer smart

phones but a lot of mobile phones eg India, Africa.

Dominant position of technology or telecom giants. Ant

Financial (owner of Alipay) benefits from Alibaba’s e-

commerce ecosystem. Mobile Money’s success in Kenya

is a result of Safaricom’s dominant market share (~70%).

Pragmatic regulatory environment. China had limited

regulation around online payment and P2P lending until

recently. Kenya’s regulatory environment was conducive to

the success of M-Pesa over the past decade.

Policy Matters. Government policy can foster a positive

environment for FinTech growth. See India government’s

J.A.M initiative (Jan Dhan – financial inclusion, Aadhaar –

National Identity Card and Mobile).

Source: Consumer Barometer with Google (smart phone penetration), Company Reports and Citi Research; Retail bank penetration is measured as retail loans% total loans. Size of the bubble is retail bank loans, the larger the bubble, the higher the retail bank loans.

BelgiumNetherlands

Austria

France

Germany

Greece

Spain

Israel

Italy

Sweden

Russia

United Kingdom

USA

Brazil

Mexico

Japan

China

South Korea

Hong Kong

India

Singapore

Malaysia

Philippines

TaiwanThailand

10%

20%

30%

40%

50%

60%

70%

20% 30% 40% 50% 60% 70% 80% 90% 100%

Ret

ail B

anki

ng

Pen

etra

tio

n

Smart Phone Penetration

Innovation Frontier

Ris

k of

losi

ng e

xist

ing

reve

nue

pool

Ris

k of

losi

ng n

ew r

even

ue p

ool

Digital leadersDigital Followers

New Entrants Led Disruptions

Incumbent LedEvolutions

Future GrowthAreas

DigitalFollowers

17

At the Tipping Point in the West, Past the Tipping Point in China

Sub 1% of North America Consumer Banking Revenues are on New Digital Business Model

US (or European) consumer banking is at the early stages

of the disruption cycle. Currently only c1% of North

American consumer banking revenues have migrated to

new digital business models but this could accelerate.

China, led by tech giants such as Alibaba and Tencent, is

well past the tipping point. China’s e-commerce system is

the largest in the world (40% of GMV, 2015). Alipay’s total

payment value in 2015 was over 3x PayPal in 2015.

For Chinese banks, earnings lost to FinTech innovators

may be only a small part of the existing profit pool, but it is

an opportunity lost to a big and growing market segment.

Source: Citi Digital Strategy

18

At the Tipping Point in the West, Past the Tipping Point in China

Global Ecommerce Mainly Comes From China & US 2015

Alipay TPV bigger than Paypal 2015 ($bn)

Source: eMarketer, Citi Research; Based on Gross Merchandise Value (GMV) Source: Company Reports and Citi Research; Alipay TPV 2015 is estimated based on discloser in 2014 adjusted for growth in Alibaba’s GMV.

Global $1.7tr

China $0.67tr (40%)

US $0.34tr (20%)

Alibaba $0.45tr (26%)

931

282

0

200

400

600

800

1000

AliPay PayPal

AliPay3.3x

PayPal

19

BATs Provide a Roadmap for GAFA

GAFA vs BAT

BATs are ahead of GAFAs when it comes to expanding to financial

services (higher market share).

Due to early entrance. Alipay and Tenpay were created over a decade

ago. Google was the first to venture into payments among GAFAs in

2011, seven years after Alipay.

Finance is strategically important for the BATs. In a country with a

relatively underdeveloped consumer banking system, payment is now

seen as core to their online to offline (O2O) strategy.

GAFAs operate in an existing well developed consumer payments

system and financial services are not as strategically important as it is

for BATs.

Amazon is more likely to be a major player in financial services due to

its focus on e-commerce.

Android Pay and Apple Pay are part of Google and Apple’s broader

strategy to further enhance customer stickiness to their OS ecosystem.

Payment Leaders in the west include PayPal, Buy rated, due to

exposure to rapidly growing online payment; Visa and Master Card,

both Buy Rated, because of solid market position, trend of cash to

electronic payments.

Western Union, Sell rated, is most at risk due to potential pressure on

remittance volumes and margin from increased FinTech competition.

Number of Users 2015

Business Model

Finance Products Volume

Google Around 200m monthly unique users

data monetisation

* Google Wallet (2011)

* Android Pay (2015)

Around 20m devices have Google wallet installed in the US; 1-2m active users in the US

Apple 800m (iTunes) data, software and hardware

* ApplePay (2014) * Around 24m Apple Pay compatible devices in the US; Around 4m users have used it at least once and 1-2m active users in the US

*< 2% transactions at top US retailers

Facebook 1,550m data monetisation

* Messenger Payments (2015) -

Amazon 304m eCommerce * Amazon Lending (2012): Loan to sellers

* Amazon Payments (2007): Online payment

* Globally more than 23 million customers (<10% of customers) have used the Pay with Amazon service since 2013.

* Payment volume from Pay with Amazon increased 150% year-over-year in 2015;

Number of Users 2015

Business Model

Finance Products Volume

Baidu 590m data monetisation

* Baidu Wallet (2014)

* Baidu Finance (2013): Including consumer credit, marketplace lending, wealth and so on

45m Baidu Wallet users

< 2% of third party payment (online + offline) market share

Alibaba 407m (number of active buyers over LTM)

eCommerce * Alipay (2004)

* Yu'e Bao (2013)

* Mybank (2015)

* Zhima Credit (2015)

* 33% third party transactions (online + offline) market share

* Around RMB 17tr ($2.6tr) transactions in 2015

Tencent 697m (WeChat) data monetisation

* Tenpay (2005)

* WeBank (2015): online/mobile bank

* Wilidai (2015): consumer credit

* 10% third party transactions (online + offline) market share

* Around RMB 5tr ($0.8tr) transactions in 2015

Source: Citi Research

20

BATs Provide a Roadmap for GAFA

Banking’s Uber Moment

21

22

Diminishing Return of Physical Assets

Commercial Bank Branches Per 100k Adults By Region

“The number of branches and people may decline by as much as 50% over the

next years" - Antony Jenkins, the former CEO of Barclays

Northern Europe has already done a lot — Nordic and Dutch banks have cut total

branch levels by around 50% from recent peak levels.

The US banks on average appear to be about 5 years behind European banks

who are in turn about a decade behind the Nordic banks.

“Over the past one year, US banks have started to cut back, as they have realized

that interest rates are unlikely to increase any time soon… some banks in the US

will more than halve their branches over the next 5 years” - Citi GPS Report:

Digital Disruption March 2016

Source: WorldBank, Citi Research

-

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2018 2020 … 2025

Euro area United StatesEast Asia & Pacific (all income levels) Latin America & Caribbean (all income levels)Nordics

Forecasts

-33%

-45%

-50%

We Are At the Tipping Point of FTE Reduction

FTE in European banks is down 11% since 2008 crisis and down 5% for US banks

(2% per annum).

We see another ~30% reduction in staff next decade with a 3% decline per year

– Driven by automation: Branches and associated staff costs make up about

65% of the total retail cost base of a larger bank and a lot of these costs can be

removed via automation.

– Focus on Return in a Low Growth & Low Rate Environment: For countries

that have gone through a more severe financial crisis and consolidation FTE

reduction ranges between 3%-5% per year.

Source: ECB, United States Bureau of Labor Statistics, Citi Research Estimates

2.933.26

2.572.89

1.80 1.82

-

1

2

3

4

US Europe

Mill

ion

s

Peak 2015 2025

-40% -45%

23

People: Automation Tipping Point

Mill

ions

24

People: Automation Tipping Point

FTE Reduction 2014 vs 2008

Source: ECB, Sweden Banker’s Association , United States Bureau of Labor Statistics, Citi Research

-40%

-30%

-20%

-10%

0%

Latv

ia

Gre

ece

Den

mar

k

Irel

and

Spa

in

Est

onia

Rom

ania

Lith

uani

a

Net

herla

nds

UK

Fin

land

Bel

gium

Por

tuga

l

Slo

veni

a

Cyp

rus

EU

28

Italy

Hun

gary

Slo

vaki

a

Pol

and

Aus

tria

Ger

man

y

Fra

nce

Sw

eden US

So What Are the Challenges and Opportunities?

25

26

The Competitive Threat

China is the Silicon Valley of FinTech

EM Banks as Low PE Businesses?

DM Banks and FinTech: Co-opetition

DM: Watch Amazon ....

27

A FinTech Bubble?

“Over 100,000

Downloads”

Citi GPS: Global Perspectives and Solutions:

DIGITAL DISRUPTION: How FinTech is Forcing Banking to a Tipping Point

https://www.citivelocity.com/citigps/ReportSeries.action?recordId=51

28

Appendix A-1

Analyst Certification

The research analysts primarily responsible for the preparation and content of this research report are either (i) designated by “AC” in the author block or (ii) listed in bold alongside content which is attributable to that analyst. If multiple AC analysts are designated in the author block, each analyst is certifying with respect to the entire research report other than (a) content attributable to another AC certifying analyst listed in bold alongside the content and (b) views expressed solely with respect to a specific issuer which are attributable to another AC certifying analyst identified in the price charts or rating history tables for that issuer shown below. Each of these analysts certify, with respect to the sections of the report for which they are responsible: (1) that the views expressed therein accurately reflect their personal views about each issuer and security referenced and were prepared in an independent manner, including with respect to Citigroup Global Markets Inc. and its affiliates; and (2) no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in this report.

IMPORTANT DISCLOSURES

Disclosure for investors in the Republic of Turkey: Under Capital Markets Law of Turkey (Law No: 6362), the investment information, comments and advices given herein are not part of investment advisory activity. Investment advisory services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences. Whereas the comments and advices included herein are of general nature. Therefore, they may not fit to your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations. Furthermore, Citi Research is a division of Citigroup Global Markets Inc. (the “Firm”), which does and seeks to do business with companies and/or trades on securities covered in this research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report.

Analysts’ compensation is determined by Citi Research management and Citigroup’s senior management and is based upon activities and services intended to benefit the investor clients of Citigroup Global Markets Inc. and its affiliates (the “Firm”). Compensation is not linked to specific transactions or recommendations. Like all Firm employees, analysts receive compensation that is impacted by overall Firm profitability which includes investment banking, sales and trading, and principal trading revenues. One factor in equity research analyst compensation is arranging corporate access events between institutional clients and the management teams of covered companies. Typically, company management is more likely to participate when the analyst has a positive view of the company.

For securities recommended in the Product in which the Firm is not a market maker, the Firm is a liquidity provider in the issuers' financial instruments and may act as principal in connection with such transactions. The Firm is a regular issuer of traded financial instruments linked to securities that may have been recommended in the Product. The Firm regularly trades in the securities of the issuer(s) discussed in the Product. The Firm may engage in securities transactions in a manner inconsistent with the Product and, with respect to securities covered by the Product, will buy or sell from customers on a principal basis.

For important disclosures (including copies of historical disclosures) regarding the companies that are the subject of this Citi Research product ("the Product"), please contact Citi Research, 388 Greenwich Street, 28th Floor, New York, NY, 10013, Attention: Legal/Compliance [E6WYB6412478]. In addition, the same important disclosures, with the exception of the Valuation and Risk assessments and historical disclosures, are contained on the Firm's disclosure website at https://www.citivelocity.com/cvr/eppublic/citi_research_disclosures. Valuation and Risk assessments can be found in the text of the most recent research note/report regarding the subject company. Pursuant to the Market Abuse Regulation a history of all Citi Research recommendations published during the preceding 12-month period can be

29

accessed via Citi Velocity (https://www.citivelocity.com/cv2) or your standard distribution portal. Historical disclosures (for up to the past three years) will be provided upon request.

Citi Research Equity Ratings Distribution 12 Month Rating Data current as of 30 Sep 2016 Buy Hold Sell

Citi Research Global Fundamental Coverage 47% 39% 14% % of companies in each rating category that are investment banking clients 66% 61% 60%

Guide to Citi Research Fundamental Research Investment Ratings: Citi Research stock recommendations include an investment rating and an optional risk rating to highlight high risk stocks. Risk rating takes into account both price volatility and fundamental criteria. Stocks will either have no risk rating or a High risk rating assigned. Investment Ratings: Citi Research investment ratings are Buy, Neutral and Sell. Our ratings are a function of analyst expectations of expected total return ("ETR") and risk. ETR is the sum of the forecast price appreciation (or depreciation) plus the dividend yield for a stock within the next 12 months. The Investment rating definitions are: Buy (1) ETR of 15% or more or 25% or more for High risk stocks; and Sell (3) for negative ETR. Any covered stock not assigned a Buy or a Sell is a Neutral (2). For stocks rated Neutral (2), if an analyst believes that there are insufficient valuation drivers and/or investment catalysts to derive a positive or negative investment view, they may elect with the approval of Citi Research management not to assign a target price and, thus, not derive an ETR. Analysts may place covered stocks "Under Review" in response to exceptional circumstances (e.g. lack of information critical to the analyst's thesis) affecting the company and / or trading in the company's securities (e.g. trading suspension). As soon as practically possible, the analyst will publish a note re-establishing a rating and investment thesis. To satisfy regulatory requirements, we correspond Under Review and Neutral to Hold in our ratings distribution table for our 12-month fundamental rating system. However, we reiterate that we do not consider Under Review to be a recommendation. Investment ratings are determined by the ranges described above at the time of initiation of coverage, a change in investment and/or risk rating, or a change in target price (subject to limited management discretion). At other times, the expected total returns may fall outside of these ranges because of market price movements and/or other short-term volatility or trading patterns. Such interim deviations from specified ranges will be permitted but will become subject to review by Research Management. Your decision to buy or sell a security should be based upon your personal investment objectives and should be made only after evaluating the stock's expected performance and risk.

Prior to May 1, 2014 Citi Research may have also assigned a three-month relative call (or rating) to a stock to highlight expected out-performance (most preferred) or under-performance (least preferred) versus the geographic and industry sector over a 3 month period. The relative call may have highlighted a specific near-term catalyst or event impacting the company or the market that was anticipated to have a short-term price impact on the equity securities of the company. Absent any specific catalyst the analyst(s) may have indicated the most and least preferred stocks in the universe of stocks under consideration, explaining the basis for this short-term view. This three-month view may have been different from and did not affect a stock's fundamental equity rating, which reflected a longer-term total absolute return expectation.

NON-US RESEARCH ANALYST DISCLOSURES Non-US research analysts who have prepared this report (i.e., all research analysts listed below other than those identified as employed by Citigroup Global Markets Inc.) are not registered/qualified as research analysts with FINRA. Such research analysts may not be associated persons of the member organization and therefore may not be subject to the FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. The legal entities employing the authors of this report are listed below:

Citigroup Global Markets Ltd Yafei Tian, CFA

OTHER DISCLOSURES

Any price(s) of instruments quoted are as of the prior day’s market close on the primary market for the instrument unless otherwise stated.

30

European regulations require that where a recommendation differs from any of the author’s previous recommendations concerning the same financial instrument or issuer that has been published during the preceding 12-month period that the change(s) and the date of that previous recommendation are indicated. For fundamental coverage please refer to the price chart or rating change history within this disclosure appendix or the issuer disclosure summary at https://www.citivelocity.com/cvr/eppublic/citi_research_disclosures.

European regulations require that a firm must establish, implement and make available a policy for managing conflicts of interest arising as a result of publication or distribution of investment research. The policy applicable to Citi Research's Products can be found at https://www.citivelocity.com/cvr/eppublic/citi_research_disclosures.

The proportion of all Citi Research fundamental research recommendations that were the equivalent to “Buy”,”Hold”,”Sell” at the end of each quarter over the prior 12 months (with the % of these that were at the time investment banking clients shown in brackets) is as follows: Q2 2016 Buy 31% (45%), Hold 45% (40%), Sell 24% (38%); Q1 2016 Buy 31% (46%), Hold 45% (40%), Sell 24% (39%); Q4 2015 Buy 31% (45%), Hold 45% (39%), Sell 24% (40%); Q3 2015 Buy 32% (47%), Hold 44% (40%), Sell 24% (36%).

Citigroup Global Markets India Private Limited and/or its affiliates may have, from time to time, actual or beneficial ownership of 1% or more in the debt securities of the subject issuer.

Citi Research generally disseminates its research to the Firm’s global institutional and retail clients via both proprietary (e.g., Citi Velocity and Citi Personal Wealth Management) and non-proprietary electronic distribution platforms. Certain research may be disseminated only via the Firm’s proprietary distribution platforms; however such research will not contain changes to earnings forecasts, target price, investment or risk rating or investment thesis or be otherwise inconsistent with the author’s previously published research. Certain research is made available only to institutional investors to satisfy regulatory requirements. Individual Citi Research analysts may also opt to circulate published research to one or more clients by email; such email distribution is discretionary and is done only after the research has been disseminated. The level and types of services provided by Citi Research analysts to clients may vary depending on various factors such as the client’s individual preferences as to the frequency and manner of receiving communications from analysts, the client’s risk profile and investment focus and perspective (e.g. market-wide, sector specific, long term, short-term etc.), the size and scope of the overall client relationship with the Firm and legal and regulatory constraints.

Pursuant to Comissão de Valores Mobiliários Rule 483, Citi is required to disclose whether a Citi related company or business has a commercial relationship with the subject company. Considering that Citi operates multiple businesses in more than 100 countries around the world, it is likely that Citi has a commercial relationship with the subject company.

Securities recommended, offered, or sold by the Firm: (i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution (including Citibank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested. The Product is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in the Product must take into account existing public information on such security or any registered prospectus. Although information has been obtained from and is based upon sources that the Firm believes to be reliable, we do not guarantee its accuracy and it may be incomplete and condensed. Note, however, that the Firm has taken all reasonable steps to determine the accuracy and completeness of the disclosures made in the Important Disclosures section of the Product. The Firm's research department has received assistance from the subject company(ies) referred to in this Product including, but not limited to, discussions with management of the subject company(ies). Firm policy prohibits research analysts from sending draft research to subject companies. However, it should be presumed that the author of the Product has had discussions with the subject company to ensure factual accuracy prior to publication. All opinions, projections and estimates constitute the judgment of the author as of the date of the Product and these, plus any other information contained in the Product, are subject to change without notice. Prices and availability of financial instruments also are subject to change without notice. Notwithstanding other departments within the Firm advising the companies discussed in this Product, information obtained in such role is not used in the preparation of the Product. Although Citi Research does not set a predetermined frequency for publication, if the Product is a fundamental equity or credit research report, it is the intention of Citi Research to provide research coverage of the covered issuers, including in response to news affecting the issuer. For non-fundamental research reports, Citi Research may not provide regular updates to the views, recommendations and facts included in the reports. Notwithstanding that Citi Research maintains coverage on, makes recommendations concerning or discusses issuers, Citi Research may be periodically restricted from referencing certain issuers due to legal or policy reasons. Citi Research may provide different

31

research products and services to different classes of customers (for example, based upon long-term or short-term investment horizons) that may lead to differing conclusions or recommendations that could impact the price of a security contrary to the recommendations in the alternative research product, provided that each is consistent with the rating system for each respective product.

Investing in non-U.S. securities, including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of the U.S. Securities and Exchange Commission. There may be limited information available on foreign securities. Foreign companies are generally not subject to uniform audit and reporting standards, practices and requirements comparable to those in the U.S. Securities of some foreign companies may be less liquid and their prices more volatile than securities of comparable U.S. companies. In addition, exchange rate movements may have an adverse effect on the value of an investment in a foreign stock and its corresponding dividend payment for U.S. investors. Net dividends to ADR investors are estimated, using withholding tax rates conventions, deemed accurate, but investors are urged to consult their tax advisor for exact dividend computations. Investors who have received the Product from the Firm may be prohibited in certain states or other jurisdictions from purchasing securities mentioned in the Product from the Firm. Please ask your Financial Consultant for additional details. Citigroup Global Markets Inc. takes responsibility for the Product in the United States. Any orders by US investors resulting from the information contained in the Product may be placed only through Citigroup Global Markets Inc.

Important Disclosures for Bell Potter Customers: Bell Potter is making this Product available to its clients pursuant to an agreement with Citigroup Global Markets Australia Pty Limited. Neither Citigroup Global Markets Australia Pty Limited nor any of its affiliates has made any determination as to the suitability of the information provided herein and clients should consult with their Bell Potter financial advisor before making any investment decision.

The Citigroup legal entity that takes responsibility for the production of the Product is the legal entity which the first named author is employed by. The Product is made available in Australia through Citigroup Global Markets Australia Pty Limited. (ABN 64 003 114 832 and AFSL No. 240992), participant of the ASX Group and regulated by the Australian Securities & Investments Commission. Citigroup Centre, 2 Park Street, Sydney, NSW 2000. Citigroup Global Markets Australia Pty Limited is not an Authorised Deposit-Taking Institution under the Banking Act 1959, nor is it regulated by the Australian Prudential Regulation Authority. The Product is made available in Australia to Private Banking wholesale clients through Citigroup Pty Limited (ABN 88 004 325 080 and AFSL 238098). Citigroup Pty Limited provides all financial product advice to Australian Private Banking wholesale clients through bankers and relationship managers. If there is any doubt about the suitability of investments held in Citigroup Private Bank accounts, investors should contact the Citigroup Private Bank in Australia. Citigroup companies may compensate affiliates and their representatives for providing products and services to clients. The Product is made available in Brazil by Citigroup Global Markets Brasil - CCTVM SA, which is regulated by CVM - Comissão de Valores Mobiliários ("CVM"), BACEN - Brazilian Central Bank, APIMEC - Associação dos Analistas e Profissionais de Investimento do Mercado de Capitais and ANBIMA – Associação Brasileira das Entidades dos Mercados Financeiro e de Capitais. Av. Paulista, 1111 - 14º andar(parte) - CEP: 01311920 - São Paulo - SP. If the Product is being made available in certain provinces of Canada by Citigroup Global Markets (Canada) Inc. ("CGM Canada"), CGM Canada has approved the Product. Citigroup Place, 123 Front Street West, Suite 1100, Toronto, Ontario M5J 2M3. This product is available in Chile through Banchile Corredores de Bolsa S.A., an indirect subsidiary of Citigroup Inc., which is regulated by the Superintendencia de Valores y Seguros. Agustinas 975, piso 2, Santiago, Chile. The Product is distributed in Germany by Citigroup Global Markets Deutschland AG ("CGMD"), which is regulated by Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin). CGMD, Reuterweg 16, 60323 Frankfurt am Main. Research which relates to "securities" (as defined in the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong)) is issued in Hong Kong by, or on behalf of, Citigroup Global Markets Asia Limited which takes full responsibility for its content. Citigroup Global Markets Asia Ltd. is regulated by Hong Kong Securities and Futures Commission. If the Research is made available through Citibank, N.A., Hong Kong Branch, for its clients in Citi Private Bank, it is made available by Citibank N.A., Citibank Tower, Citibank Plaza, 3 Garden Road, Hong Kong. Citibank N.A. is regulated by the Hong Kong Monetary Authority. Please contact your Private Banker in Citibank N.A., Hong Kong, Branch if you have any queries on or any matters arising from or in connection with this document. The Product is made available in India by Citigroup Global Markets India Private Limited (CGM), which is regulated by the Securities and Exchange Board of India (SEBI), as a Research Analyst (SEBI Registration No. INH000000438). CGM is also actively involved in the business of merchant banking, stock brokerage, and depository participant, in India, and is registered with SEBI in this regard. CGM’s registered office is at 1202, 12th Floor, FIFC, G Block, Bandra Kurla Complex, Bandra East, Mumbai – 400051. CGM’s Corporate Identity Number is U99999MH2000PTC126657, and its contact details are: Tel:+9102261759999 Fax:+9102261759961. The Product is made available in Indonesia through PT Citigroup Securities Indonesia. 5/F, Citibank Tower, Bapindo Plaza, Jl.

32

Jend. Sudirman Kav. 54-55, Jakarta 12190. Neither this Product nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesian residents except in compliance with applicable capital market laws and regulations. This Product is not an offer of securities in Indonesia. The securities referred to in this Product have not been registered with the Capital Market and Financial Institutions Supervisory Agency (BAPEPAM-LK) pursuant to relevant capital market laws and regulations, and may not be offered or sold within the territory of the Republic of Indonesia or to Indonesian citizens through a public offering or in circumstances which constitute an offer within the meaning of the Indonesian capital market laws and regulations. The Product is made available in Israel through Citibank NA, regulated by the Bank of Israel and the Israeli Securities Authority. Citibank, N.A, Platinum Building, 21 Ha'arba'ah St, Tel Aviv, Israel. The Product is made available in Italy by Citigroup Global Markets Limited, which is authorised by the PRA and regulated by the FCA and the PRA. Via dei Mercanti, 12, Milan, 20121, Italy. The Product is made available in Japan by Citigroup Global Markets Japan Inc. ("CGMJ"), which is regulated by Financial Services Agency, Securities and Exchange Surveillance Commission, Japan Securities Dealers Association, Tokyo Stock Exchange and Osaka Securities Exchange. Shin-Marunouchi Building, 1-5-1 Marunouchi, Chiyoda-ku, Tokyo 100-6520 Japan. If the Product was distributed by SMBC Nikko Securities Inc. it is being so distributed under license. In the event that an error is found in an CGMJ research report, a revised version will be posted on the Firm's Citi Velocity website. If you have questions regarding Citi Velocity, please call (81 3) 6270-3019 for help. The Product is made available in Korea by Citigroup Global Markets Korea Securities Ltd., which is regulated by the Financial Services Commission, the Financial Supervisory Service and the Korea Financial Investment Association (KOFIA). Citibank Building, 39 Da-dong, Jung-gu, Seoul 100-180, Korea. KOFIA makes available registration information of research analysts on its website. Please visit the following website if you wish to find KOFIA registration information on research analysts of Citigroup Global Markets Korea Securities Ltd. http://dis.kofia.or.kr/websquare/index.jsp?w2xPath=/wq/fundMgr/DISFundMgrAnalystList.xml&divisionId=MDIS03002002000000&serviceId=SDIS03002002000. The Product is made available in Korea by Citibank Korea Inc., which is regulated by the Financial Services Commission and the Financial Supervisory Service. Address is Citibank Building, 39 Da-dong, Jung-gu, Seoul 100-180, Korea. The Product is made available in Malaysia by Citigroup Global Markets Malaysia Sdn Bhd (Company No. 460819-D) (“CGMM”) to its clients and CGMM takes responsibility for its contents. CGMM is regulated by the Securities Commission of Malaysia. Please contact CGMM at Level 43 Menara Citibank, 165 Jalan Ampang, 50450 Kuala Lumpur, Malaysia in respect of any matters arising from, or in connection with, the Product. The Product is made available in Mexico by Acciones y Valores Banamex, S.A. De C. V., Casa de Bolsa, Integrante del Grupo Financiero Banamex ("Accival") which is a wholly owned subsidiary of Citigroup Inc. and is regulated by Comision Nacional Bancaria y de Valores. Reforma 398, Col. Juarez, 06600 Mexico, D.F. In New Zealand the Product is made available to ‘wholesale clients’ only as defined by s5C(1) of the Financial Advisers Act 2008 (‘FAA’) through Citigroup Global Markets Australia Pty Ltd (ABN 64 003 114 832 and AFSL No. 240992), an overseas financial adviser as defined by the FAA, participant of the ASX Group and regulated by the Australian Securities & Investments Commission. Citigroup Centre, 2 Park Street, Sydney, NSW 2000. The Product is made available in Pakistan by Citibank N.A. Pakistan branch, which is regulated by the State Bank of Pakistan and Securities Exchange Commission, Pakistan. AWT Plaza, 1.1. Chundrigar Road, P.O. Box 4889, Karachi-74200. The Product is made available in the Philippines through Citicorp Financial Services and Insurance Brokerage Philippines, Inc., which is regulated by the Philippines Securities and Exchange Commission. 20th Floor Citibank Square Bldg. The Product is made available in the Philippines through Citibank NA Philippines branch, Citibank Tower, 8741 Paseo De Roxas, Makati City, Manila. Citibank NA Philippines NA is regulated by The Bangko Sentral ng Pilipinas. The Product is made available in Poland by Dom Maklerski Banku Handlowego SA an indirect subsidiary of Citigroup Inc., which is regulated by Komisja Nadzoru Finansowego. Dom Maklerski Banku Handlowego S.A. ul.Senatorska 16, 00-923 Warszawa. The Product is made available in the Russian Federation through ZAO Citibank, which is licensed to carry out banking activities in the Russian Federation in accordance with the general banking license issued by the Central Bank of the Russian Federation and brokerage activities in accordance with the license issued by the Federal Service for Financial Markets. Neither the Product nor any information contained in the Product shall be considered as advertising the securities mentioned in this report within the territory of the Russian Federation or outside the Russian Federation. The Product does not constitute an appraisal within the meaning of the Federal Law of the Russian Federation of 29 July 1998 No. 135-FZ (as amended) On Appraisal Activities in the Russian Federation. 8-10 Gasheka Street, 125047 Moscow. The Product is made available in Singapore through Citigroup Global Markets Singapore Pte. Ltd. (“CGMSPL”), a capital markets services license holder, and regulated by Monetary Authority of Singapore. Please contact CGMSPL at 8 Marina View, 21st Floor Asia Square Tower 1, Singapore 018960, in respect of any matters arising from, or in connection with, the analysis of this document. This report is intended for recipients who are accredited, expert and institutional investors as defined under the Securities and Futures Act (Cap. 289). The Product is made available by The Citigroup Private Bank in Singapore through Citibank, N.A., Singapore Branch, a licensed bank in Singapore that is regulated by Monetary Authority of Singapore. Please contact your Private Banker in Citibank N.A., Singapore Branch if you have any queries on or any matters arising from or in connection with this document. This report is intended for recipients who are

33

accredited, expert and institutional investors as defined under the Securities and Futures Act (Cap. 289). This report is distributed in Singapore by Citibank Singapore Ltd ("CSL") to selected Citigold/Citigold Private Clients. CSL provides no independent research or analysis of the substance or in preparation of this report. Please contact your Citigold//Citigold Private Client Relationship Manager in CSL if you have any queries on or any matters arising from or in connection with this report. This report is intended for recipients who are accredited investors as defined under the Securities and Futures Act (Cap. 289). Citigroup Global Markets (Pty) Ltd. is incorporated in the Republic of South Africa (company registration number 2000/025866/07) and its registered office is at 145 West Street, Sandton, 2196, Saxonwold. Citigroup Global Markets (Pty) Ltd. is regulated by JSE Securities Exchange South Africa, South African Reserve Bank and the Financial Services Board. The investments and services contained herein are not available to private customers in South Africa. The Product is made available in the Republic of China through Citigroup Global Markets Taiwan Securities Company Ltd. ("CGMTS"), 14 and 15F, No. 1, Songzhi Road, Taipei 110, Taiwan and/or through Citibank Securities (Taiwan) Company Limited ("CSTL"), 14 and 15F, No. 1, Songzhi Road, Taipei 110, Taiwan, subject to the respective license scope of each entity and the applicable laws and regulations in the Republic of China. CGMTS and CSTL are both regulated by the Securities and Futures Bureau of the Financial Supervisory Commission of Taiwan, the Republic of China. No portion of the Product may be reproduced or quoted in the Republic of China by the press or any third parties [without the written authorization of CGMTS and CSTL]. If the Product covers securities which are not allowed to be offered or traded in the Republic of China, neither the Product nor any information contained in the Product shall be considered as advertising the securities or making recommendation of the securities in the Republic of China. The Product is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security or financial products. Any decision to purchase securities or financial products mentioned in the Product must take into account existing public information on such security or the financial products or any registered prospectus. The Product is made available in Thailand through Citicorp Securities (Thailand) Ltd., which is regulated by the Securities and Exchange Commission of Thailand. 399 Interchange 21 Building, 18th Floor, Sukhumvit Road, Klongtoey Nua, Wattana ,Bangkok 10110, Thailand. The Product is made available in Turkey through Citibank AS which is regulated by Capital Markets Board. Tekfen Tower, Eski Buyukdere Caddesi # 209 Kat 2B, 23294 Levent, Istanbul, Turkey. In the U.A.E, these materials (the "Materials") are communicated by Citigroup Global Markets Limited, DIFC branch ("CGML"), an entity registered in the Dubai International Financial Center ("DIFC") and licensed and regulated by the Dubai Financial Services Authority ("DFSA") to Professional Clients and Market Counterparties only and should not be relied upon or distributed to Retail Clients. A distribution of the different Citi Research ratings distribution, in percentage terms for Investments in each sector covered is made available on request. Financial products and/or services to which the Materials relate will only be made available to Professional Clients and Market Counterparties. The Product is made available in United Kingdom by Citigroup Global Markets Limited, which is authorised by the Prudential Regulation Authority (“PRA”) and regulated by the Financial Conduct Authority (“FCA”) and the PRA. This material may relate to investments or services of a person outside of the UK or to other matters which are not authorised by the PRA nor regulated by the FCA and the PRA and further details as to where this may be the case are available upon request in respect of this material. Citigroup Centre, Canada Square, Canary Wharf, London, E14 5LB. The Product is made available in United States by Citigroup Global Markets Inc, which is a member of FINRA and registered with the US Securities and Exchange Commission. 388 Greenwich Street, New York, NY 10013. Unless specified to the contrary, within EU Member States, the Product is made available by Citigroup Global Markets Limited, which is authorised by the PRA and regulated by the FCA and the PRA. The Product is not to be construed as providing investment services in any jurisdiction where the provision of such services would not be permitted. Subject to the nature and contents of the Product, the investments described therein are subject to fluctuations in price and/or value and investors may get back less than originally invested. Certain high-volatility investments can be subject to sudden and large falls in value that could equal or exceed the amount invested. Certain investments contained in the Product may have tax implications for private customers whereby levels and basis of taxation may be subject to change. If in doubt, investors should seek advice from a tax adviser. The Product does not purport to identify the nature of the specific market or other risks associated with a particular transaction. Advice in the Product is general and should not be construed as personal advice given it has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Accordingly, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to their objectives, financial situation and needs. Prior to acquiring any financial product, it is the client's responsibility to obtain the relevant offer document for the product and consider it before making a decision as to whether to purchase the product. Citi Research product may source data from dataCentral. dataCentral is a Citi Research proprietary database, which includes the Firm’s estimates, data from company reports and feeds from Thomson Reuters. The printed and printable version of the research report may not include all the information (e.g., certain financial summary information and comparable company data) that is linked to the online version available on the Firm's proprietary electronic distribution platforms.

34

© 2016 Citigroup Global Markets Inc. Citi Research is a division of Citigroup Global Markets Inc. Citi and Citi with Arc Design are trademarks and service marks of Citigroup Inc. and its affiliates and are used and registered throughout the world. All rights reserved. The research data in this report is not intended to be used for the purpose of (a) determining the price or amounts due in respect of one or more financial products or instruments and/or (b) measuring or comparing the performance of a financial product or a portfolio of financial instruments, and any such use is strictly prohibited without the prior written consent of Citi Research. Any unauthorized use, duplication, redistribution or disclosure of this report (the “Product”), including, but not limited to, redistribution of the Product by electronic mail, posting of the Product on a website or page, and/or providing to a third party a link to the Product, is prohibited by law and will result in prosecution. The information contained in the Product is intended solely for the recipient and may not be further distributed by the recipient to any third party. Where included in this report, MSCI sourced information is the exclusive property of Morgan Stanley Capital International Inc. (MSCI). Without prior written permission of MSCI, this information and any other MSCI intellectual property may not be reproduced, redisseminated or used to create any financial products, including any indices. This information is provided on an "as is" basis. The user assumes the entire risk of any use made of this information. MSCI, its affiliates and any third party involved in, or related to, computing or compiling the information hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. MSCI, Morgan Stanley Capital International and the MSCI indexes are services marks of MSCI and its affiliates. The Firm accepts no liability whatsoever for the actions of third parties. The Product may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the Product refers to website material of the Firm, the Firm has not reviewed the linked site. Equally, except to the extent to which the Product refers to website material of the Firm, the Firm takes no responsibility for, and makes no representations or warranties whatsoever as to, the data and information contained therein. Such address or hyperlink (including addresses or hyperlinks to website material of the Firm) is provided solely for your convenience and information and the content of the linked site does not in any way form part of this document. Accessing such website or following such link through the Product or the website of the Firm shall be at your own risk and the Firm shall have no liability arising out of, or in connection with, any such referenced website.

ADDITIONAL INFORMATION IS AVAILABLE UPON REQUEST

Nick HungerfordNutmeg

@nickhungerford#ftscot

36Confidential -- 2016 Nutmeg Saving & Investment Limited

A mission to democratise finance

Nick HungerfordNutmeg co-founder

Fintech 2016 - Edinburgh

37Confidential -- 2016 Nutmeg Saving & Investment Limited

The financial sector has a trust problem

38Confidential -- 2016 Nutmeg Saving & Investment Limited

It also has a tech problem

Source: KPMG report on UK challenger banks, May 2016

Complex IT

Complex

products

Costly real

estate

Legacy

compliance

Manual

operating

models

39Confidential -- 2016 Nutmeg Saving & Investment Limited

And more broadly, while interest rates are low, society has a savings problem…

40Confidential -- 2016 Nutmeg Saving & Investment Limited

…so the old ways of saving – pension, house, bank deposits – are no longer working.

41Confidential -- 2016 Nutmeg Saving & Investment Limited

FinTech meets an urgent social need

DIY

IFA

Wealth managers

House & pensionW

ealth

Ways to save and invest

Exclusion / complexity

Bank

42Confidential -- 2016 Nutmeg Saving & Investment Limited

The Scots are saving pretty well!UK

% who feel confident they are “on track” to achieve desired income in retirement

30% 43%

% saving more than £500/month for retirement 11% 18%

Average pension pot size £34k £48k

Target income in retirement £27k £29k

% worried about impact of Brexit on pension 30% 37%

43Confidential -- 2016 Nutmeg Saving & Investment Limited

It’s not just tech change that is required

Established firms Nutmeg / other FinTechs

IT / tech stack Legacy, paper-based, few APIs APIs used throughout the business, cloud-based, proprietary purpose-built systems

Reporting Paper via direct mail, charges for ad hoc statements Online-first, live or daily reports

Transparency Many complex fee schedules, lack of reporting on total fees paid One simple management fee and no exit fees.A running total of fees paid on the dashboard

On boarding Paper-based 100% online-only for 80%+ of customers

Performance Net of fees - rarely if ever calculated for the customer Transparently presented and consistently top-quartile among UK wealth managers

Financial insight and advice

Delivered via humans, charged by hour, charges opaque Financial planning tools delivered online, as part of the Nutmeg service

44Confidential -- 2016 Nutmeg Saving & Investment Limited

Disaggregation of a bank

Foreign exchange

Payday

Payments

Banking

Personal credit

Investing and wealth management

Mortgages

Business lending

Disruption is yesterdays word: now it’s the norm

SalaryFinance

45Confidential -- 2016 Nutmeg Saving & Investment Limited

Where might all this lead?

• Tech firms moving into finance • Virtual reality pensions

• “Emotional surveillance” –tech to stop emotions upsetting investment strategies

• Wealth managers moving into concierge / family office services to protect HNW market share

• AI / chatbot advisors

46Confidential -- 2016 Nutmeg Saving & Investment Limited

Regulators have helped so far… and they need help

• Project Innovate

• Advice Unit

• Regulatory Sandbox

Pension Dashboard

FinTech Panel

Professional services hub for FinTech

FinTech bridges with priority global markets

New Bank Unit

BoE Open Forum

47Confidential -- 2016 Nutmeg Saving & Investment Limited

And together can do more…

• Government can speed up change

• Require electronic ISA and pension transfers (i.e. no paper forms) • Impose maximum ISA and pension transfer times• Introduce higher transparency standards on performance and fees

• Regulators can be more flexible

• Allow us to speak in language people understand – “money at risk” not “capital at risk”

• Allow wealth managers to rely on the due diligence of banks

• The tax system can channel capital to entrepreneurs

• Enterprise Investment Scheme (EIS) for university lecturers and students: Prof-EIS

48Confidential -- 2016 Nutmeg Saving & Investment Limited

So in conclusion

• Established firms in finance lack trust, have tech legacies, and struggle to balance profit and social responsibility (no VC money!)

• This creates an opportunity: help people to improve their finances –winning trust by doing so

• Regulators are keen, and have eyes on the future

• But policymakers can do more to help FinTechs grow and keep innovating

• The societal necessity is too great for us to slow down!

Bharat BhushanIBM

@_bharat_#ftscot

50

51© 2016 IBM Corporation |

Innovation Timeline: 1900 - 2008

1900 20081950

Automobile

Safety Razor

Transatlantic Flight

Aeroplane

Tape Recorder

Tabloid Newspaper

Vacuum Cleaner

Cornflakes

Nylon

Instant Coffee

Helicopter

Plastics

Bra

Traffic Lights

Assembly Lines

Hydrofoil

E=MC2

Sonar

Spin Dryer

Band Aid

Television

Lego

Jet Engine

Chocolate Chip Biscuit

Hearing Aid

Sliced Bread

Microwave Oven

Ballpoint Pen

Velcro

Photocopier

Jet Airliner

Nuclear Fission

Electronic Computer

Credit Card

DNA

Tupperware

Frisbee

Polaroid Camera

Colour TV

Silicon Chip

Superglue

Nuclear Power

Radial Tyres

The Pill

Plate Tectonics

Heart Transplants

Satellites

Hovercraft

Jacuzzi

Cassette Tape

Carbon Dating

Computer Mouse

Artificial Heart

Source: http://www.nowandnext.com

Radar

Pocket Calculator

Floppy Disk

Dot Matrix Printer

Moon Landing

Walkman

VCRSpace Station

IVF

Fax Machine

Gore-tex

IBM PC

Cell Phone

Space Shuttle

Compact Disk

Camcorder

eBay

MySpace

Yahoo

Amazon

Skype

YouTube

Netscape

GPS

Apple Mac

CD-ROM

Disposable Camera

Post-it Notes

Home Computing

3-D Gaming

Flickr

Penicillin

Laser

Cats Eyes

Parking MetersAtom Bomb

ATMInternet

Games Console

Starbucks

Barcodes

Word Processor

Astroturf

52© 2016 IBM Corporation |

The Greatest Innovations Of All Time?

Airplane

Car

Bicycle

iPod

SKY +

Helicopter

Mobile Phone

Cats Eyes

Sliced Bread

Some Contenders …

53© 2016 IBM Corporation |

Innovations that never took off

A snow screen for the face !! The family bicycle !! The one-wheel motorcycle !!

54

© 2016 IBM Corporation

1. Augmenting products to generate data

2. Digitising Assets

3. Combining Data Within and Across Industries

4. Trading Data

5. Codifying a Distinctive Service Capability

5 Patterns of Innovation

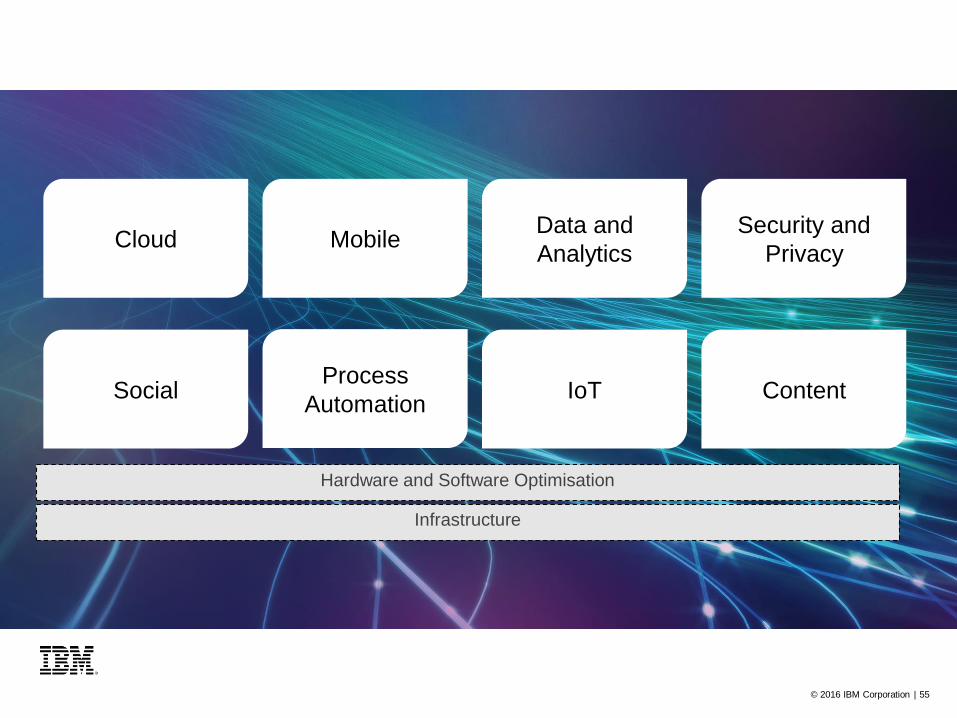

55© 2016 IBM Corporation |

Cloud MobileData and

Analytics

Security and

Privacy

SocialProcess

AutomationIoT Content

Hardware and Software Optimisation

Infrastructure

56© 2016 IBM Corporation |

Cognitive Era

57© 2016 IBM Corporation |

Digital and Cognitive Era

User Centric

Value Centric

Collaborative

Speed and Agility

Scale

Secure

Transparent

58© 2016 IBM Corporation |

Source: June 2015 World Economic Forum, The Future of Financial Services

6 Core Functions of

Financial ServicesThe World Economic Forum developed

the first consolidated taxonomy for

disruptive innovation in financial services

around 6 core functions that comprise

financial services:

Transactions / Payments

Deposits & Lending

Investment / Wealth Management

Insurance

Capital Raising

Market Provisioning

1

© 2015 IBM Corporation |

2 11 Clusters of Disruptionclusters were identified that were exerting

pressure on traditional business models

Disruptors are deploying better customer propositions in lower-cost models

1.Data Intensive

2.Platform / Ecosystem

3.Capital Light

59

Barclays SponsorsEuropeROW

60

61

62

63

64

Convert center screen resolution to 1920 x 782 @ 140dpi (13.714 x 5.586)

$4.8 Trillion Market by 2025

Source: Ovum: Digital Economy 2025: Core Scenario

65

66

© 2016 IBM Corporation

Ecosystems – Its all about customers needs

Speed

Bankingreal time booking,

payments, loans, …

Aggregation of traditional assets and new P2P

and

social banking products

ConvenienceMoney transfer, deposits, currency

transactions via twitter, mobile number,

Open Architecture: natively adaptable to

innovations e.g. Virtual

currencies like Bitcoin, open

protocols like Ripple, …

Open APIprovides powerful and easy to

understand, to setup and to use

interface to access all fidorOS

functions

Alternative Assetse.g. Travel loyalty miles, precious

metals

The Fidor Plusmulti-language, multi-currency, multi

jurisdiction, multi-CBS, white-label

fidorOS

67© 2016 IBM Corporation |

fOS is API based,

Modular and Free of

Legacy

“Cloud native” bank built

on a cloud ecosystem of

financial product providers

Built it’s own API centric

core bank platform

Social is used exclusively

for acquisition, retention,

cross sell, R&D

Fidor has a community

of 500k+ users and 100k

“KYC” customers

CASE STUDY: Fidor Bank operating environment allows for a substantially lower cost structure

IT cost per user: -

$200

Traditional

Bank

$3 $15

Customer acquisitions costs: -

€7

Traditional

Bank

<€1

68

69

100% of relevant softwareavailable on the cloud

70

From idea to prototype in minutes

CREATE new cognitive, mobile

and IoT capabilities in the cloud

71

Creative disruption

Digital businesses move six times faster

72

What will you build?

Bob FergusonFCA

@TheFCA#ftscot

74

Bob Ferguson, Head of Project InnovateScot-Tech Fintech Conference 11 October 2016

Promoting Innovation through a collaborative approach to regulation

FCA: Project Innovate

75

• Launched in October 2014

• Promote FCA’s competition objective by:

Providing direct support to innovative businesses

Policy and process improvement

• While balancing opportunities and risk

Project Innovate: Aims

Aims

• “Innovation-friendly” regulatory system – policy and process improvement, balanced approach to opportunity and risk

• Help for innovative businesses to learn how to live with regulation, and to achieve market entry as smoothly as possible – fintech start-ups, pure tech players, large firms

Not

• A deregulatory initiative

• A soft option for innovative businesses

• An initiative just aimed at start-ups

76

How and with whom we collaborate

• Direct support for innovative businesses

• Regulatory sandbox

• Themed weeks

• Fintech ecosystem representative bodies

• Overseas regulators

77

Direct Support

• Provides one-to-one interaction with the regulator for innovative businesses

• Advice on regulatory implications of business concepts

• Advice on how to prepare an application for authorisation – but Hub does not make

authorisation decisions

• An “end-to-end” regulatory experience

• Service is confined to regulatory matters

78

Statistics: September 2016

Total number of requests for help – 608

Help given – 312

Firms authorised or awaiting decision – 42

Informal steers – 86

Eligibility criteria

• Genuine innovation?

• Consumer benefit?

• Research done?

• Need for support?

79

Regulatory Sandbox

80

• Created as a safe space to test new ideas with real customers without incurring disproportionate regulatory consequences

• Aimed at helping firms test the viability of an idea on a small scale, reducing product development time/cost

• An experiment for all parties involved, including the FCA

• Consumer safeguards built in to each pilot

• First cohort of firms due to begin live testing very shortly

• 69 applications received and 24 chosen to develop towards testing

• We have seen partnerships between start-ups and incumbents

• Second round of applications due to open in November

Contact

https://www.the-fca.org.uk/firms/project-innovate-innovation-hub

Phone: +44 (0)20 7066 4488

Email: [email protected]

81

#ftscot

Questions & Discussion

#ftscot

Morning BreakoutsPlease check rear

of badge

Fintech 2016Scot-Tech

Edinburgh

Yvonne Dunn, Partner

Luke Scanlon

Head of Fintech Propositions

11 October 2016

Overview

Todays aim…

• Engaging with

regulators

• Blockchain and

DLT – beyond the

hype

• The future of

robo advice

• Digital

currencies in

their own right

Engaging with regulators

• Project Innovate

• Regulatory Sandbox

• Challenger Bank Unit

• Robo Advice

• International co-operation

FCA and

Fintech

Distributed ledgers

88

Distributed

ledger activity

• 2,500+ patents

• 90+ businesses

• 90+ central banks

• Digital IDs

• Smart contracts

• Regulatory reporting

• Privacy issues

• Governance

• Cyber, fraud, money

laundering

Regulatory

concerns

Robo Advice

Background and

drivers…

• Perception of an “advice

gap”

• Robo advice to plug the

gap

• Threats and opportunities

• Different concepts across banking,

securities and insurance

• Advice vs guidance

What is

“advice”?

• Consumer

• Provider

Risks and

issues

Digital currencies

95

• Definitional challenges

• Policy priorities of

different jurisdictions

• Consumer protection

• Taxation

• Anti-money laundering

The future

of money?

The way forward

…• Fourth Money

Laundering Directive

(MLD4)

• Second Electronic

Money Directive

• Payment Accounts

Directive

• Payment Services

Directive (2)

• HM Treasury's views

• Cyber

• Collaboration

• Alternative finance

• Open data

Quick

update

Pinsent Masons LLP is a limited liability partnership registered in England & Wales (registered number: OC333653) authorised and regulated by the

Solicitors Regulation Authority, and by the appropriate regulatory body in the other jurisdictions in which it operates. The word ‘partner’, used in

relation to the LLP, refers to a member of the LLP or an employee or consultant of the LLP or any affiliated firm of equivalent standing. A list of the

members of the LLP, and of those non-members who are designated as partners, is displayed at the LLP’s registered office: 30 Crown Place,

London EC2A 4ES, United Kingdom. We use 'Pinsent Masons' to refer to Pinsent Masons LLP, its subsidiaries and any affiliates which it or its

partners operate as separate businesses for regulatory or other reasons. Reference to 'Pinsent Masons' is to Pinsent Masons LLP and/or one or

more of those subsidiaries or affiliates as the context requires. © Pinsent Masons LLP 2014

For a full list of our locations around the globe please visit our websites:

www.pinsentmasons.com www.Out-Law.com

Precision Search

Precision Search

• Reduce the time and effort finding information - Learn how valuable Precision Search can be

• How to “Know what you don’t know” by Discovering Value in your Unstructured Data

• The Golden Rules for Unstructured Data Analysis that you need to know!

Welcome

Our mission …

To help any individual, business user or organisation who is at a loss with navigating and using their electronic documents and data

Why do we have this mission …

Back Office costs are too high

Risks of making a mistake are too high

Adoption of modern technologies outside of Advance Analytics, Risk Profiling and Social Monitoring is too low

IT change is considered as too expensive

Do you …

…have large amounts of documents or data which you need to be able to review and search accurately in multiple sources?

…need to answer detailed questions on demand?

…want to reduce your search time for specific documents and improve the quality of discovery?

…require easy access to all your information?

Independent Analysis …Challenges within Fintech

How do we gain value …

WHOLEDOCUMENT

S

DOCUMENTS

BY SECTION

CONTENT BY

PARAGRAH

A SINGLE SENTENCE

• Big Data service focussed on unstructured data

• We use the inherent textual structure of your documents and data content to

enable precise and accurate searches – capturing the Digital DNA of your data

• Scalable from single and small numbers of project documents to corporate shared

drives containing millions of documents

Reduce the Time and Effort Spent Searching

Why is SEARCH important?

50% Indexed

>25% time

$48,000 per weekOr $2.5m per year

Precision Searching …

Precision Searching …Material Breach

Precision Searching …

Know what you don’t know

Discovery Techniques …

• Content Categorisation

• Topic highlighting

• Entity highlighting

• Content Summarisation

• Sentiment Analysis

• Word Clouds – Heat Maps

Discovery – What is the reality …

NDA’s Contracts NDA’s Contracts

Pharma

Food Oil & Gas

Retail

A

A

Template

Customer

A VariationsNDA’s

A

A

Template

Customer

AVariationsContract’

s

The Golden Rules for Unstructured Data Analysis that you need to know

Analysis

• Redact Sensitive

Information

• Keep it simple

• Put the power into the

hands of all applicable

users – not just the select

few

• Use precise search tools,

else you are wasting time!

Come and see us on our

stand for a FREE trial

Directive (EU) 2015/2366 on payment services in the internal market -12/1/2016

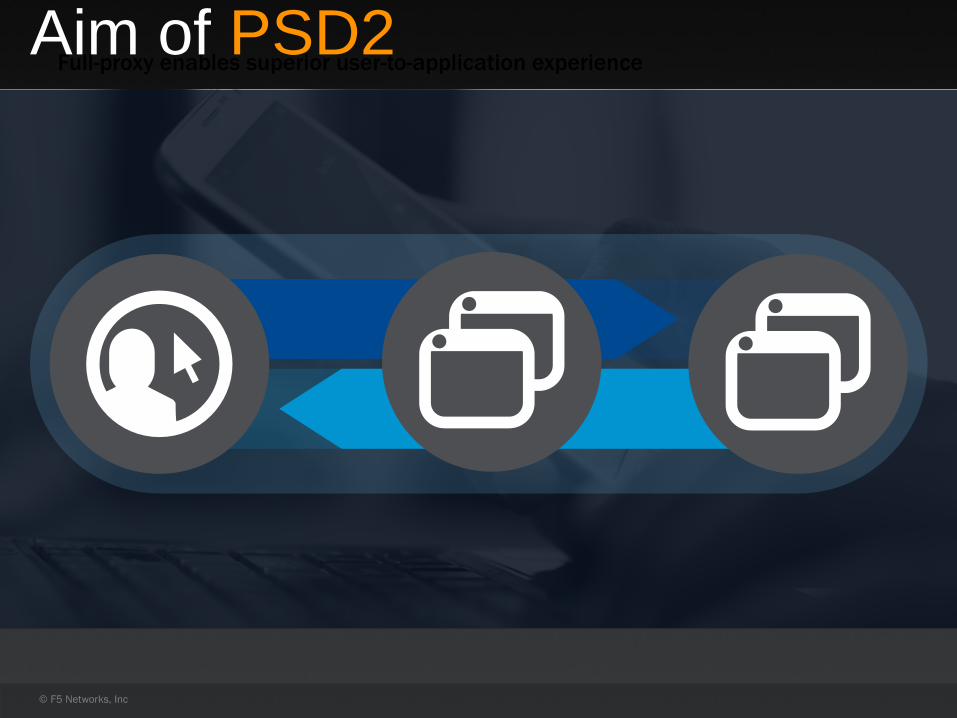

PSD2

Full-proxy enables superior user-to-application experience

End Users

Account info

Aim of PSD2

Still to confirm Regulatory Technical Standards

Short timeframes

Strong Customer Authentication - SCA

XS2A – Access to account rules

4

3

2

1

122

PSD2 key points

Write your own?

API security?

Other alternatives?

Open API?

TO API OR NOT API?

OPEN API?

DATA STANDARD

RULES BY WHICH DATA

ARE DESCRIBED AND RECORDED

API STANDARD

SPECIFICATIONS THAT INFORM THE DESIGN,

DEVELOPMENT AND

MAINTENANCE OF AN OPEN API

SECURITY STANDARD

SECURITY ASPECTS OF THE API STANDARD

Open Banking Standard

A set of specifications and rules addressing the data, technical and security aspects in an open API environment,

supported by a Governence Model

https://uk.openbankproject.com

GDPR

SECURITY CONSIDERATIONS.

Authentication

Malware / Social Engineering

Scale

DDOS

http://blog.smartbear.com/readyapi/api-security-testing-how-to-hack-an-api-and-get-away-with-it-part-1-of-3/

DYRE - ZEUS

Internet of things

Al kazeem cyber fighters

API PROTECTION

JSON/AJAX -

XML

GWT

L7 DDOS

© F5 Networks, Inc 127

Attack vectors – IOT v API v PSD2

IoT PlatformMQTT

MQTT

HTTP

Gatewa

y

Gateway

MQTT

HTTP

MQTT

HTTP

Customers

DDoS

Attack

HTTP

What’s the problem

• Protocol heterogeneity

• Weak cryptography

• Complex Authentication

• Tricky Authorization

• Siloed Security

• Global scalability

https://f5.com/about-us/news/articles/mirai-the-iot-bot-that-took-down-krebs-and-launched-a-tbps-ddos-attack-on-ovh-21937

Market opportunity

New channels

Must get the security right

Must comply

Risk v Reward

Thank you.

COMMERCIAL IN CONFIDENCE © Copyright 2016 Fujitsu Limited

Passwords – Do Not Resuscitate

David Cameron

Business Development Director – Digital Financial Services

1 COMMERCIAL IN CONFIDENCE

Bill Gates – But what was the year?

“Traditional password-

based security is

headed for extinction,

because it cannot meet

the challenge of

keeping critical

information secure.”

2004 RSA Conference -

Copenhagen

2 COMMERCIAL IN CONFIDENCE

Lazy Passwords

ID as currency: put these in order of ‘value’

3

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

ID as currency: put these in order of ‘value’

Driving Licence

Open market value approx. £15-30

4

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

Debit/Current Account

approx. £4

Credit Card £ 0.60

The Challenge

41%of all

Fraud in

the UK is

IDFraud

5

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

The Challenge

80%of account

opening

and ID theft

fraud is

committed

on line.

6

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

The Challenge

52%increas

e in

fraud

for the

under

30’s

7

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

The current baseline is Password based

authentication…

8

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

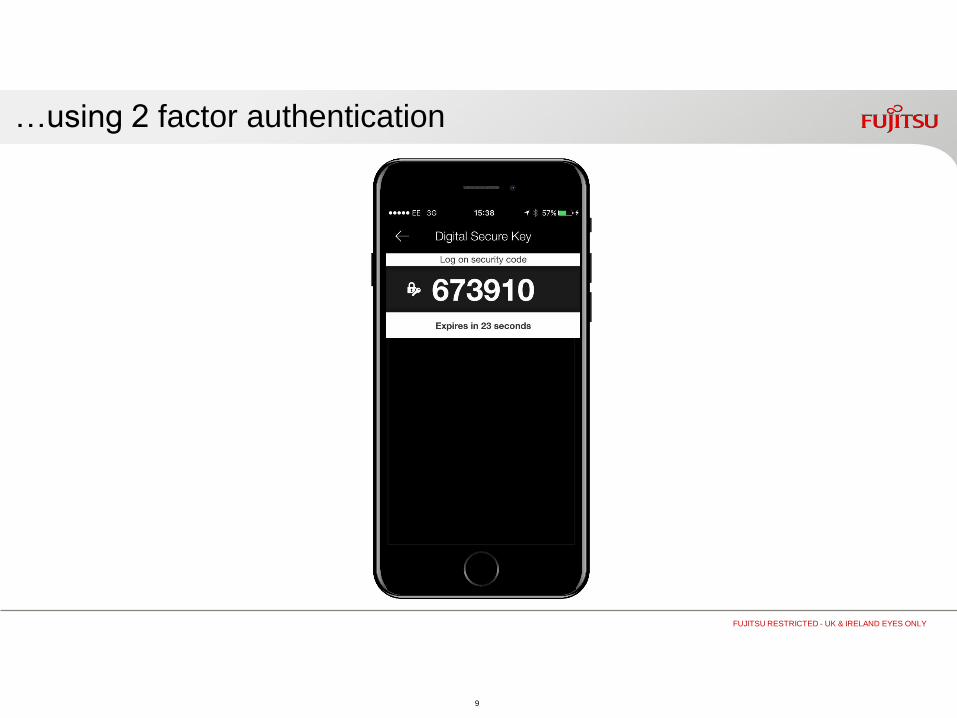

…using 2 factor authentication

9

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

…however this is negated by Smartphones

10

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

…and passwords are becoming ever more

complex

11

FUJITSU RESTRICTED - UK & IRELAND EYES ONLY

So lets use biometrics !

12 COMMERCIAL IN CONFIDENCE

But there is a problem…

13 COMMERCIAL IN CONFIDENCE

How do you verify identity at enrollment?

ID Document

3rd party data check

LivelinessCheck

Biometrics

Facial and or Voice

Know your Device Check

Geolocation check

14 COMMERCIAL IN CONFIDENCE

Click in Slideshow mode to access video

15 COMMERCIAL IN CONFIDENCE

Current approach in the market

ID Document

3rd party data check

LivelinessCheck

Biometrics

Facial and or Voice

Know your Device Check

Geolocation check

16 COMMERCIAL IN CONFIDENCE

17 COMMERCIAL IN CONFIDENCE

Risk based transaction authorisation

So far so good but how do you make it work?

18 COMMERCIAL IN CONFIDENCE

Passwords – Do Not Resucitate

19 COMMERCIAL IN CONFIDENCE

Do not resuscitate does not mean do not treat!

Don’t rely on biometrics alone

for Identity and Verification

Do maximise alternative

identification technologies

20 COMMERCIAL IN CONFIDENCE

Do not resuscitate does not mean do not treat!

21 COMMERCIAL IN CONFIDENCE

Don’t push all your customers

through a standard process

Do trust 3rd party data sets to

remove friction and provide insight

Do not resuscitate does not mean do not treat!

Don’t try to do everything yourself!

22 COMMERCIAL IN CONFIDENCE

Questions

Q&A

23 COMMERCIAL IN CONFIDENCE

#ftscot

Welcome Back

Dave BirchConsult Hyperion

@dgwbirch#ftscot

www.chyp.comPlease Copy and Distribute157

Who will make money?

A discussion about the future of

digital currency

Dave Birch

@dgwbirch

Fintech 2106

Edinburgh

October 2016

www.chyp.comPlease Copy and Distribute

David G.W. Birch

Director of Innovation at Consult Hyperion

Visiting Professor, University of Surrey Business School

An internationally-recognised thought leader in digital identity and digital money;

Named one of the global top 15 favourite sources of business information (Wired magazine);

In the London FinTech top 10 most influential commentators (City A.M.);

One of the top ten Twitter accounts followed by innovators, along with Bill Gates and Richard Branson (PR Daily);

One of the top ten most influential voices in banking (Financial Brand);

Named one of the “Fintech Titans” (NextBank);

Ranked Europe’s most influential commentator on emerging payments (Total Payments magazine).

158

www.chyp.comPlease Copy and Distribute

Agenda

159

What is digital currency?

Who might issue digital currency?

Who do I think will issue digital currency?

www.chyp.comPlease Copy and Distribute

Currency and Digital Currency

160

Let’s agree on the terminology

And then we can move on

www.chyp.comPlease Copy and Distribute

Dumb Money and Smart Money

161

www.chyp.comPlease Copy and Distribute

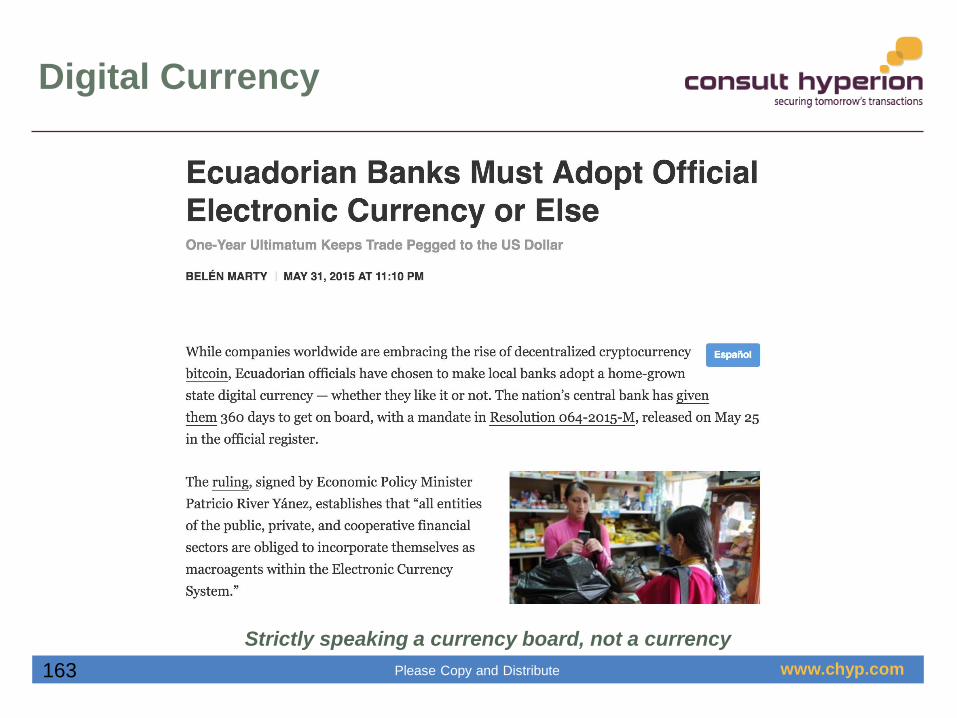

Virtual Currency

162