Findings of the MEFMI Study on Contingent Liabilities Liabilities... · Findings of the MEFMI Study...

26

Findings of the MEFMI Study on Contingent Liabilities Debt Management Stakeholders’ Forum 3 rd –4 th June 2015 Manila, Philippines

Transcript of Findings of the MEFMI Study on Contingent Liabilities Liabilities... · Findings of the MEFMI Study...

Findings of the MEFMI Study on Contingent Liabilities

Debt Management Stakeholders’ Forum

3rd – 4th June 2015

Manila, Philippines

Outline• Introduction

• Objectives of the Study

• Scope of the Study

• Methodology

• Findings

o Legal and institutional framework

o Data compilation, recording, reporting and

dissemination methodologies

o Magnitude of contingent liabilities

• Challenges

• Recommendations and Way forward

Introduction• Contingent liabilities have become a bigger fiscal risk to govts. Key

reasons for this include:

o The transformation of the role of the state from a supplier of

goods and services to a facilitator through, for instance,

extending guarantees to the public and private sector, thus

creating contingent liabilities.

o Economic and financial crises e.g. the recent global crisis which

resulted in govts bailing out their economies through guarantees

and off-budget commitments.

o Adoption of public private partnerships (PPPs).

o The absence of fully funded pension schemes (pay-as-you go),

thereby making future pension payments be contingent

liabilities.

• These have changed the nature of the financial burden of the fiscal

authorities to include increasing obligations arising from CLs.

Regional Context• The same trend of having significant CLs is replicated in

all countries in the MEFMI region.

• Unfortunately, while all countries in the region could be

having significant amounts of CLs, the amounts are not

clearly known and in some countries not well documented.

• Where the amounts are known, it is not very clear how

governments plan to deal with such liabilities.

• This situation therefore prompted MEFMI to collaborate

with the OECD to undertake a study on contingent

liabilities in the region.

Objectives of the Study

• To assess govt approaches in managing the CLs;

• To determine the stock of CLs by quantifying both

explicit and implicit CLs;

• Assess the legal and institutional arrangements for

managing CLs in the region

• Come up with a sound framework for recording,

monitoring and managing the risks arising from the CLs.

Scope and Methodology• Covered 12 MEFMI member countries: Botswana, Kenya,

Lesotho, Malawi, Mozambique, Namibia, Rwanda,

Swaziland, Uganda, Zambia and Zimbabwe.

• Preceded by pilot study in Zambia in the first half of 2013.

Tanzania conducted its study in 2014.

• Entailed field surveys using a structured questionnaire to

collect data.

• Questionnaires administered by practitioners mainly in the

Ministries of Finance or Central Banks.

• Each practitioner analysed the data and prepared country

report.

Country Responses

• The study was successfully completed for 9 countries:

Kenya, Lesotho, Malawi, Mozambique, Namibia, Rwanda,

Tanzania, Uganda and Zambia. The rest were unable to

submit the complete set of information required

• The individual countries’ findings are being consolidated for

the region - summarizing the findings, challenges and

proposed way forward.

PRELIMINARY FINDINGS

Legal Framework

Institutional Arrangements

Measurement, Budgeting and Reporting

The magnitude of CLs

Findings on Legal Framework• Almost all countries have legislation on CLs particularly those arising

from state guarantees. These authorize the Minister responsible for

Finance to issue guarantees.

• In a few countries (e.g. Uganda, Zambia) the national constitutions

have articles authorizing guarantees.

• Some countries require authorization by Parliament (Uganda), others

Cabinet (Lesotho, Malawi) or both e.g. Lesotho where the purpose

and amount requires Cabinet approval (on recommendation of the

Minister) and the terms of each loan guarantee are reported to

National Assembly for approval.

• Some have guarantee limits on outstanding balance (Mozambique).

• Some have annual fee charged on guarantees, or risk premium and all

costs incurred by the Government in the process (Lesotho &

Mozambique), fixed rate of 2% p.a.(Namibia &Zambia).

Other Findings on Legal Framework• Most countries have adopted PPPs with laws to support these:

o Many countries have enacted laws on PPPs e.g. Zambia (2009),

Malawi (2010), Tanzania (2010), Mozambique (2011), and Kenya (2013).

o But, there are a few countries implementing PPPs without

explicit legal backing e.g. Lesotho and Rwanda

• Almost all countries practice on-lending to SOEs implementing

infrastructure projects deemed of national interest – though without

adequate legal backing in all countries.

o In some countries, on-lending agreements attract a margin above the

original agreement rate to cover expenses including bank

charges/commissions (Mozambique & Namibia).

• To complement the legal framework, some countries have

developed detailed policies and guidelines on issuance and

management of contingent liabilities e.g. Malawi, Namibia

Institutional Arrangements for CLs• In most countries, guarantees are handled within Ministries of

Finance – though many departments within are involved

o Uganda has established a Unit in MoF to manage contingent liabilities.

• The debt mgt committees are also involved in the process

especially in the analysis of guarantees before issuance.

• In some countries the PPP Acts established committees/units to

foresee PPPs e.g. Kenya, Malawi, Mozambique, etc

• In Kenya for instance the Act establishes the PPP Facilitation

Fund which among others is expected to cater for contingent

liabilities arising from PPP activities.

• Generally, active mgt of CLs is limited. CLs are dealt with on an ad

hoc basis. In addition, there are weak institutional frameworks for

managing CLs.

Measurement of CLs• Information on contingent liabilities is collected through

audited financial reports.

o SOEs and private companies regularly (by semester) provide

financial balance sheets along with details of the amount of

guaranteed loans they have outstanding.

o However, analysis is not detailed unless there is a special need to

do so for a particular entity

• There are data challenges for other types of CLs,

particularly on implicit liabilities including those arising

from litigation.

• In other countries, there are no formalised structures for

collecting information on CL in general. The available data

on CLs are mainly estimates.

Measurement of CLs

• A few countries compile guarantees data (explicit

guarantees) in the same manner as other debt instruments,

o E.g. Lesotho records CLs in CS-DRMS in the same way as other

loans.

• Explicit guarantees are recorded on face value at the time

the guarantee is issued and does not require further

quantifications.

Budgeting for CLs• In some cases, the Ministry of Finance makes budget provision

for likely defaults, particularly on loan guarantees

o The amounts are projected based on the repayment schedule and the

historical performance of the affected entity

• In other cases, there is no clear disclosure of all implicit CLs;

however, a minimal amount of contingency is budgeted for

under the Ministry of Finance e.g. Namibia, Zambia

• In general, there are no reserve funds to cater for contingent

liabilities.

o The PPP law in Kenya provides for the creation of PPP Facilitation

Fund (PPPFF) which is expected to provide a source of liquidity to

meet any contingent liabilities arising from a PPP project.

Reporting of CLs

• In general, there are no specific laws on reporting of

contingent liabilities. Reporting is mainly guided by

organic laws for public institutions to report on contingent

liabilities through financial statements.

• Some institutions report on the existing CLs through their

publications such as Central Bank Reports.

• In general, debt management reports do not provide

comprehensive coverage of contingent liabilities apart

from government guarantees.

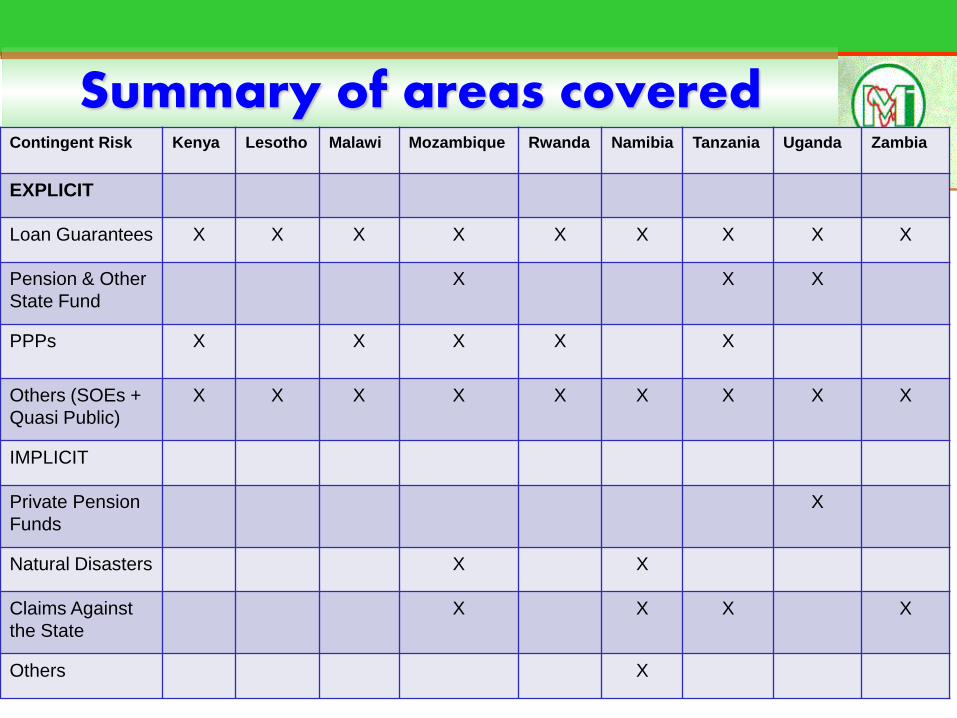

Summary of areas coveredContingent Risk Kenya Lesotho Malawi Mozambique Rwanda Namibia Tanzania Uganda Zambia

EXPLICIT

Loan Guarantees X X X X X X X X X

Pension & Other

State Fund

X X X

PPPs X X X X X

Others (SOEs +

Quasi Public)

X X X X X X X X X

IMPLICIT

Private Pension

Funds

X

Natural Disasters X X

Claims Against

the State

X X X X

Others X

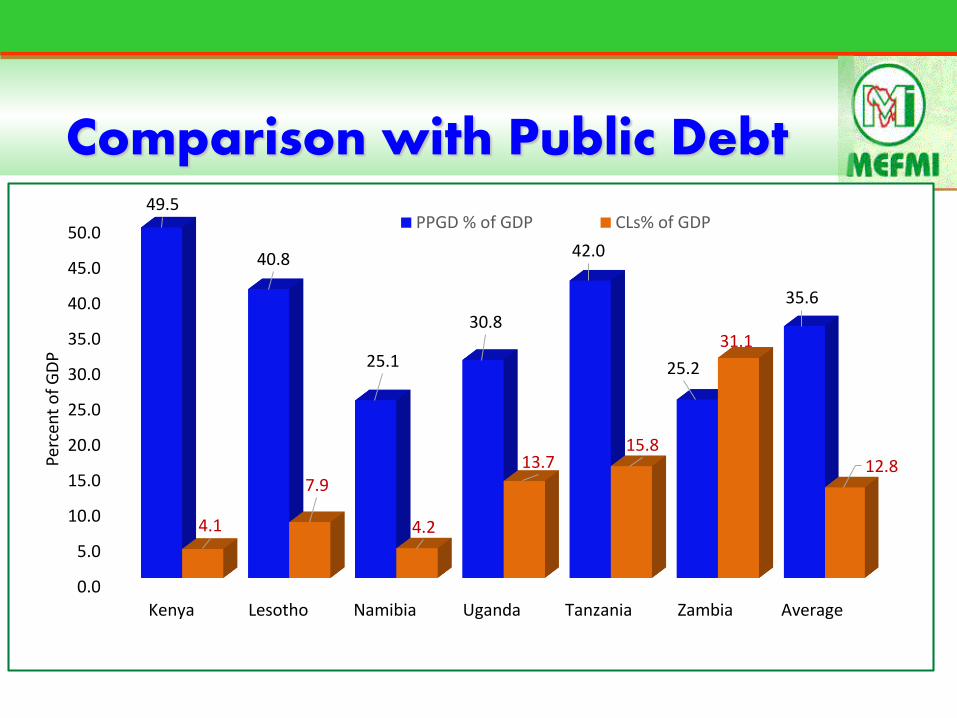

Magnitude Of CLs

Total PPG Debt Contingent Liabilities CL/PPG

Country Period

Nominal

(US$ m) % GDP

Nominal

(US$ m) %GDP %

Kenya Jun-12 19,265.55 49.5% 1,606.97 4.1% 8.3%

Lesotho Sep-13 910.50 40.8% 176.20 7.9% 19.3%

Namibia Mar-13 3,473.9 25.1% 585.5 4.2% 16.9%

Uganda Jun-13 6,402.9 30.8% 2,845.0 13.7% 44.4%

Tanzania Jun-14 15,367.0 42.0% 5,778.2 15.8% 37.6%

Zambia Dec-10 4,032.0 25.2% 4,967.0 31.1% 123.2%

Total/Average

49,451.8 36.5% 15,958.9 12.8% 41.6%

Comparison with Public Debt

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Kenya Lesotho Namibia Uganda Tanzania Zambia Average

49.5

40.8

25.1

30.8

42.0

25.2

35.6

4.1

7.9

4.2

13.715.8

31.1

12.8Perc

ent

of

GD

P

PPGD % of GDP CLs% of GDP

CLs as % of Total Public Debt

8.3

19.3

44.437.6

123.2

16.9

46.6

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Kenya Lesotho Uganda Tanzania Zambia Namibia Average

Perc

ent

The most

accurate??

We think so

Cost of CLs vs Domestic revenue• Budget provision/payment and gov’t assumption of

implicit CLs remains relatively low:o Kenya paid Ksh 961.3 million (About US$11 million, 0.12% of domestic

revenue) in 2011/12. In the last 21 years, Kenya has paid a cumulative Ksh

22,109 million (about US$253 million)

o Lesotho assumed M 205.5 million (US$20.6 million, 1.7% of domestic

revenue) of implicit contingent liabilities in 2012/13

o Namibia assumed implicit contingent liabilities amounting to N$420.5

millions (US$42.3 million, 2% of domestic revenue) as at end of 2012/13

o Zambia allocated ZMK 44.588 million (0.14% of the total budget, around

0.03% of the expected GDP) in 2013

o Uganda - PV of Implicit Contingent Liabilities is about 205% domestic

revenue and 16.5% of GDP.

Challenges• Inadequate legal coverage of all categories of CLs – in most cases

it is limited to some aspects of explicit contingent liabilities i.e.

loan guarantees.

• Absence or weak institutional framework for active

management/monitoring of CLs. Emphasis has been on central

government debt hence:

o Absence of centralized and comprehensive databases on CLs.

o Limited assessment & management of fiscal exposure to risks related

to CLs

o Inadequate integration of CLs in the management of public debt

• Most of the legislation in the surveyed countries do not give

guidance as to the criteria to be used in issuing guarantees and the

limits or guidance on terms and conditions of the guarantee.

Challenges• While collecting data on contingent liabilities the following challenges

were faced in almost all countries:

o Lack of transparency in SOEs financial operations – resulting in

implicit contingent liabilities without adequate provisions in the

govt. annual budgets.

o There is no formal requirement for reporting of contingent

liabilities in most countries (Except for Uganda where the law

requires that loan guarantees are reported in the “Loans, Grants

and Guarantees Report”) This, however, has not been done in practice and payments disclosure is not explicitly required

The legislation lacks requirement for statutory preliminary analysis and risk assessment before issuing

guarantees

Challenges• Where limits of guarantees are in place:

o They lack limits for each guarantee and concentration of risk

( i.e. sectoral spread of guarantees) and terms.

o No mention on the regularity and basis of fixing the limits

• PPPs are taken in isolation of public debt, yet they entail fiscal

obligations under certain events • On-lending is not covered in most of the countries’ legislation

Recommendations & Way Forward• Review of legislation to include all forms of CLs and procedures for

managing/monitoring them – countries require technical assistance

• The need to take CLs as an integral part of public debt management.

Need to have centralized analysis, issuance, monitoring and regular

reporting of CLs

o Need to include contingent liabilities in public Debt Sustainability Analysis

• Govts need to make provisions for CLs in their annual budgets –

Namibia for example is already providing for natural disasters and

claims on state.

• Need to emphasize use of CS-DRMS or DMFAS. This can be done

with regular flow of information (including transactions) from SOEs

to debt management offices.

• Institutional reforms and capacity building for debt managers

towards active management of contingent liabilities.

Namibia

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

(In Namibian dollar million, end period)

(i) Total outstanding guarantees 3767.6 3413.3 3029.0 2634.9 2012.7 1730.3 2471.6

of which

(a) Domestic guarantees 1760.9 1229.8 1070.0 1211.4 1072.2 944.0 1329.4

(b) External gurantees 2006.7 2183.5 1959.0 1423.5 940.5 786.3 1142.2

(ii) Realised cost to government 116.5 0 255 218.1 11.4 260 131.6

(Ratios as per cent of)

(iii) Key Indicators

Total guarantees to GDP 6.7 5.3 4.1 3.4 2.4 1.8 2.2

Total guarantees to Revenue 24.1 16.4 12.8 10.9 8.9 5.8 6.7Default ratio (Default payments/

Outstanding guarantees)3.1 0.0 8.4 8.3 0.6 15.0 5.3

(iv) Composition

Domestic Total guarantees 46.7 36.0 35.3 46.0 53.3 54.6 53.8

External to Total guarantees 53.3 64.0 64.7 54.0 46.7 45.4 46.2

Fiscal Years 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13(est)

In millions N$ dollar, unless otherwise stated

Claims against the state 13.3 11.2 13.1 18.3 19.4 22.6 25.1

Contingency Provision 112.7 179.8 268.9 222.2 372.8 234.7 395.5

Total Implicit Guarantees 126.1 191.1 281.9 240.5 392.2 257.3 420.5

Outstanding Explicit Contingent Liabilities

Materialised Implicit Contingent Liabilities

Namibia

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

(In N$ millions, end of period) unless otherwise stated

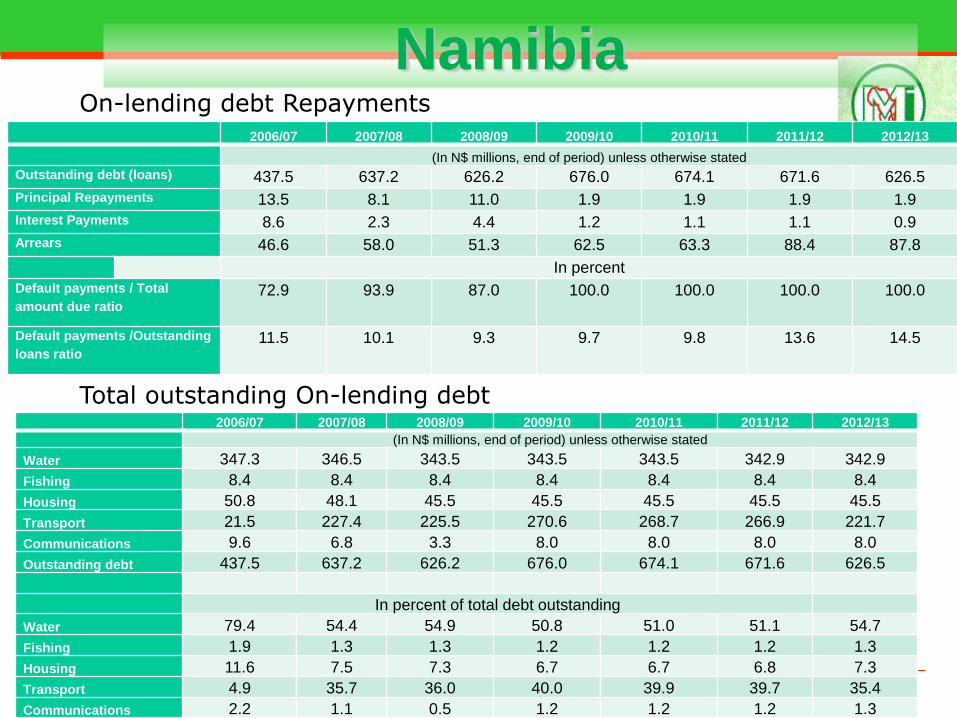

Outstanding debt (loans) 437.5 637.2 626.2 676.0 674.1 671.6 626.5

Principal Repayments 13.5 8.1 11.0 1.9 1.9 1.9 1.9

Interest Payments 8.6 2.3 4.4 1.2 1.1 1.1 0.9

Arrears 46.6 58.0 51.3 62.5 63.3 88.4 87.8

In percent

Default payments / Total

amount due ratio72.9 93.9 87.0 100.0 100.0 100.0 100.0

Default payments /Outstanding

loans ratio11.5 10.1 9.3 9.7 9.8 13.6 14.5

On-lending debt Repayments

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

(In N$ millions, end of period) unless otherwise stated

Water 347.3 346.5 343.5 343.5 343.5 342.9 342.9

Fishing 8.4 8.4 8.4 8.4 8.4 8.4 8.4

Housing 50.8 48.1 45.5 45.5 45.5 45.5 45.5

Transport 21.5 227.4 225.5 270.6 268.7 266.9 221.7

Communications 9.6 6.8 3.3 8.0 8.0 8.0 8.0

Outstanding debt 437.5 637.2 626.2 676.0 674.1 671.6 626.5

In percent of total debt outstanding

Water 79.4 54.4 54.9 50.8 51.0 51.1 54.7

Fishing 1.9 1.3 1.3 1.2 1.2 1.2 1.3

Housing 11.6 7.5 7.3 6.7 6.7 6.8 7.3

Transport 4.9 35.7 36.0 40.0 39.9 39.7 35.4

Communications 2.2 1.1 0.5 1.2 1.2 1.2 1.3

Total outstanding On-lending debt