Financing for Real Estate Investors in 2016

36

-

Upload

marshallreddick -

Category

Real Estate

-

view

250 -

download

1

Transcript of Financing for Real Estate Investors in 2016

Reed Hazard – Amerifirst Financial

Branch Manager – Senior Mortgage Planner/ NMLS # 291490

• Specializes in Purchase and refinance loans for Investment property and Primary residence (1-4 units)

• Licensed Continuing Education Instructor/ PSRE (Performance School of Real Estate)

• 12 years of experience with Marshall Reddick

• Seasoned real estate investor

• Purchased 1st property at age 19

• Worked with over 500 Marshall Reddick members just like you.

• Federally and State licensed to lend in CA, TX and AZ. – Branch licensed in IN and TN

Brett Gilliland – Amerifirst Financial

Sales Manager – Senior Mortgage Planner/ NMLS # 857828

• Specialize in Purchase and refinance loans for Investment property and Primary residence (1-4 units)

• Licensed Continuing Education Instructor/ PSRE (Performance School of Real Estate)

• USC Graduate - 1998

• Purchased 1st property 13 years ago

• Federally and State licensed to lend in CA, TX, AZ, IN, TN, WA and ID.

• Board of Directors – Joyful Foundation

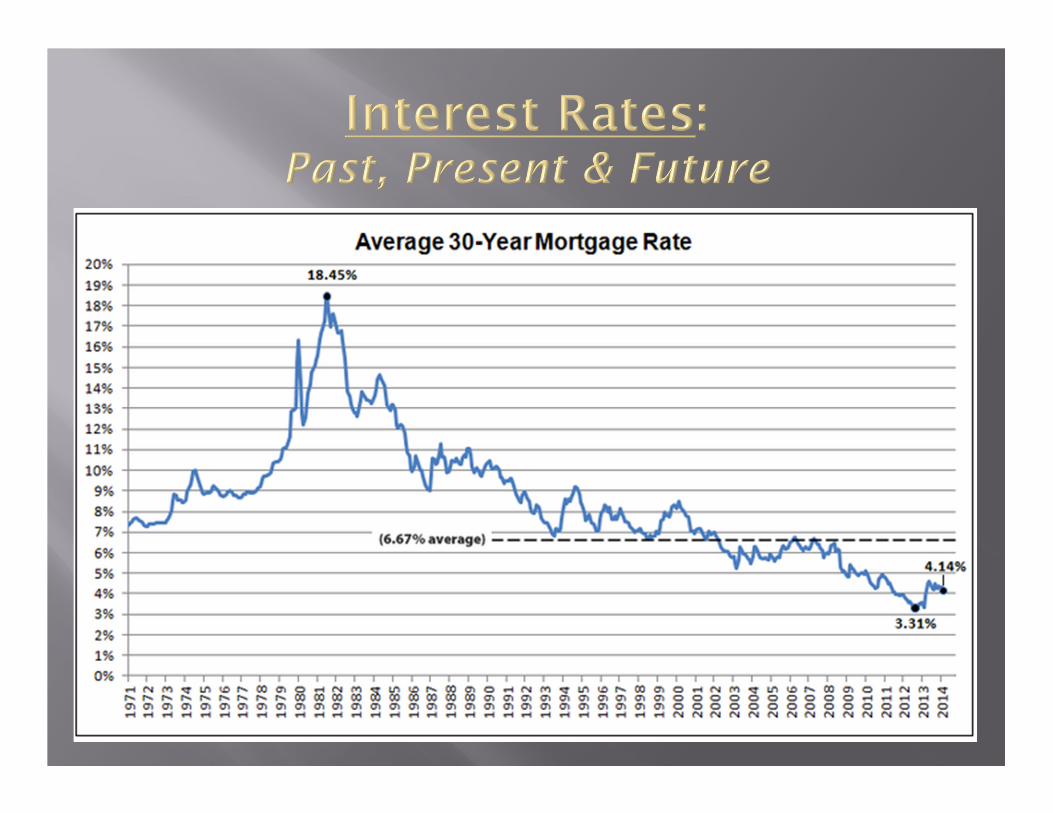

� Fed Fund rate (overnight rate at which banks and institutions have money leant to them from the federal reserve) was raised on December 16th for the first time in over a decade.

� Fed offers no set dates for their next rates hikes but on 1-27-16 keeps rates unchanged but does not take potential rate hikes off the table in 2016

� Fed is closely monitoring inflation and employment as their key driver for when to raise rates next

� What has happened to rates since the first rate hike in December?

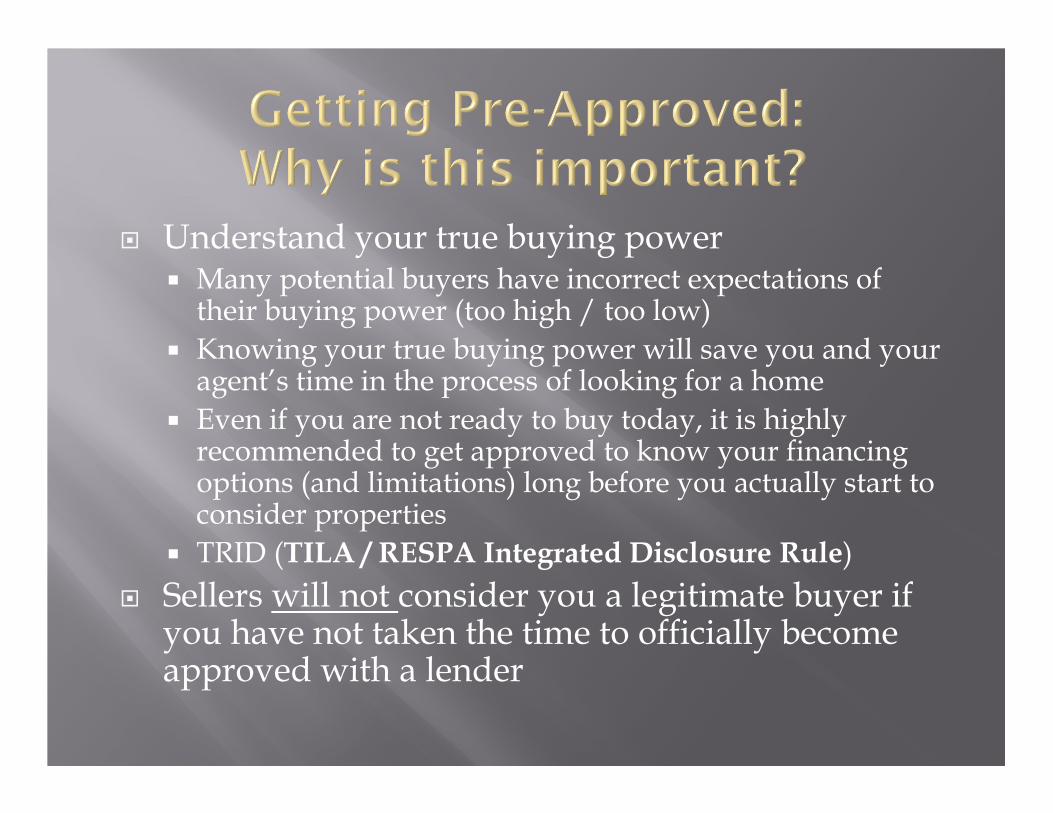

� Understand your true buying power� Many potential buyers have incorrect expectations of

their buying power (too high / too low)

� Knowing your true buying power will save you and your agent’s time in the process of looking for a home

� Even if you are not ready to buy today, it is highly recommended to get approved to know your financing options (and limitations) long before you actually start to consider properties

� TRID (TILA / RESPA Integrated Disclosure Rule)

� Sellers will not consider you a legitimate buyer if you have not taken the time to officially become approved with a lender

� The five required tasks in the approval process 1. Application taken

2. Credit Report Pulled and Reviewed

3. Automated Underwriting System (AUS) completed

4. Supporting documents have been received and reviewed

5. Underwriter confirms overall accuracy and has issued official underwritten conditional loan approval

� This would represent a “Conditional Loan Approval Letter”

� Reality check: until an underwriter has issued a conditional loan approval, you have nothing of value

Unfortunately, most pre-approval letters have only completed the following steps:� Application taken

� Credit Report Pulled and Reviewed

� Automated Underwriting System

Even worse, many pre-approved letters are issued with only the following:�Application taken

Protect yourself by getting pre-approved the right way, by the right lender

How to calculate your debt to income ratio?

DEBT Divided into Gross (before tax) monthly income = Debt to income ratio

Debts include the following: Minimum payments on Credit cards, Auto loans, mortgages including property taxes and insurance, student loans, any other loan on credit.

Debts that do not count against DTI ratios include the following: Auto/Health insurance, cell phone and utilities (including cable), loans to family and friends that are not recorded, business loans.

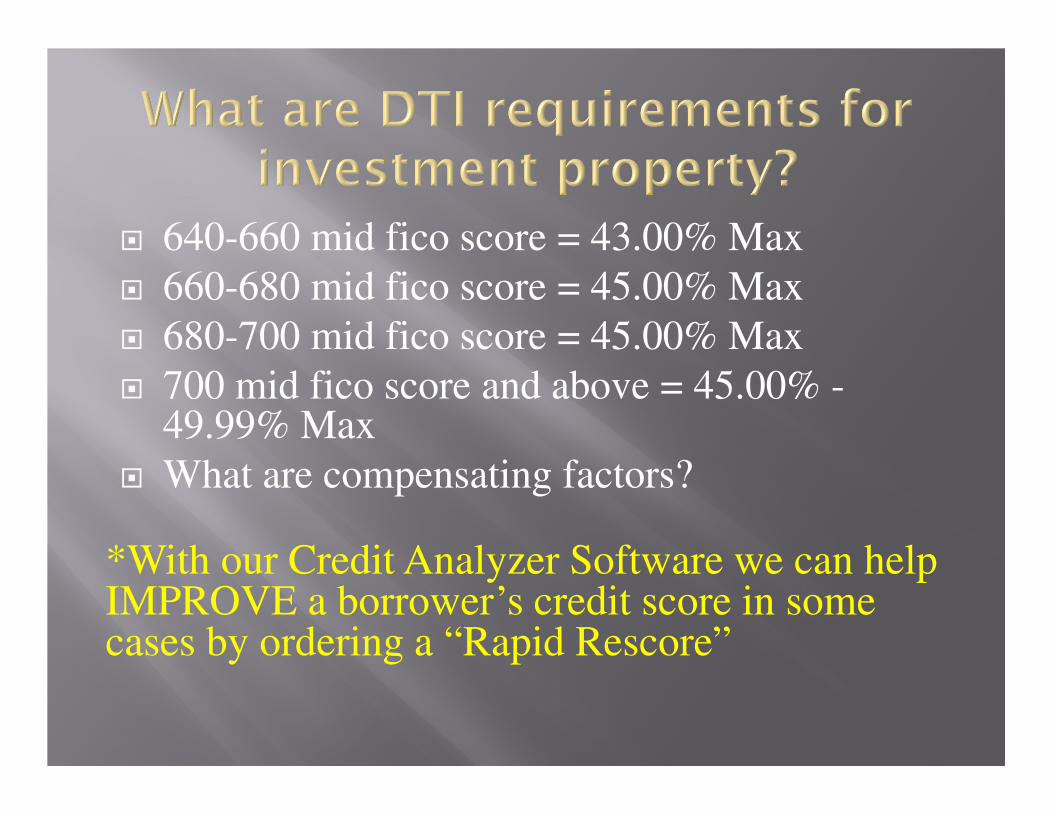

� 640-660 mid fico score = 43.00% Max

� 660-680 mid fico score = 45.00% Max

� 680-700 mid fico score = 45.00% Max

� 700 mid fico score and above = 45.00% -49.99% Max

� What are compensating factors?

*With our Credit Analyzer Software we can help IMPROVE a borrower’s credit score in some cases by ordering a “Rapid Rescore”

� Borrowers with 4 or less properties financed:

� 1 Unit - 80% financed (20% down) - 640 Fico

� 2-4 Units - 75% financed (25% down) – 640 Fico

� Borrowers with 5 to 10 properties financed:

� 1 Unit - 75% financed (25% down) - 720 Fico

� 2-4 Units - 70% financed (30% down) – 720 Fico

� Must have a mid fico score of 700 to get properties 5 and 6, must have a 720 for properties 7-10.

� Must have 6 months PITI in reserve for each property

� Rental income can be used to offset subject monthly payment at 75.00% of projected monthly rents.

� Max debt to income ratio of 45.00%

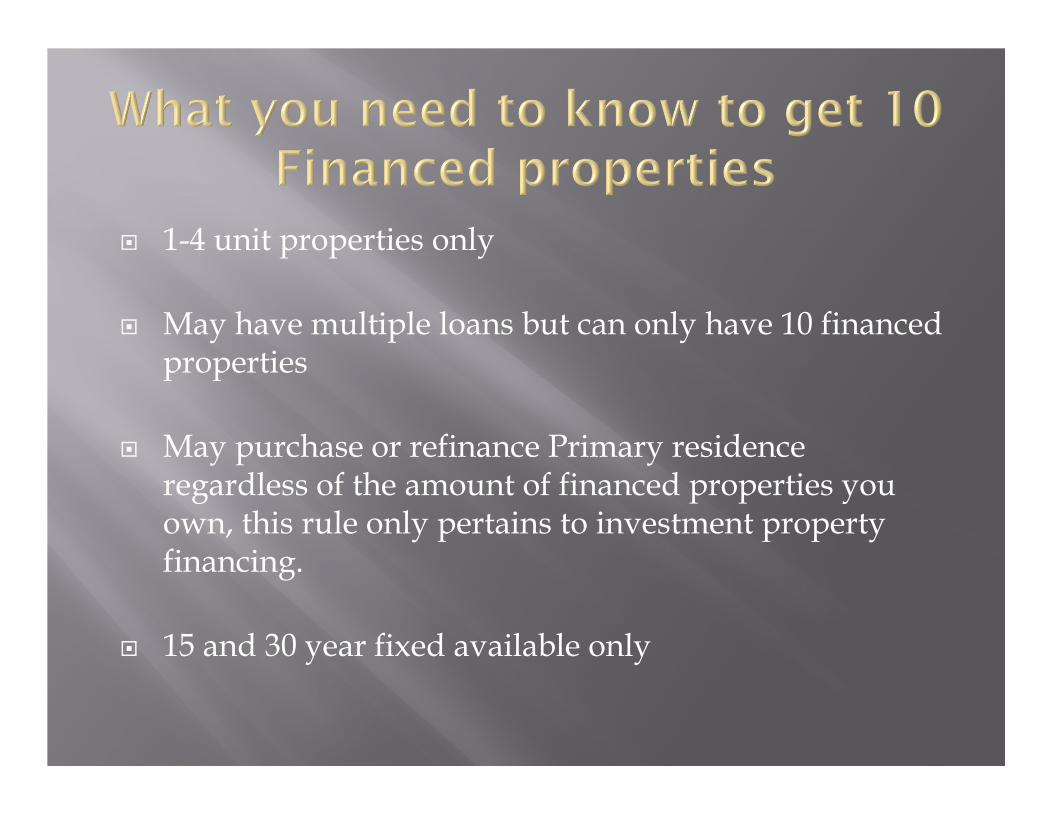

� 1-4 unit properties only

� May have multiple loans but can only have 10 financed properties

� May purchase or refinance Primary residence regardless of the amount of financed properties you own, this rule only pertains to investment property financing.

� 15 and 30 year fixed available only

� Does subject rental income count towards my debt to income ratios? � Yes, we can use 75.00% of the gross rental income to

qualify

� How do you factor the rental amount if the home is not pre-leased? � A Form 442 is ordered with your appraisal which

will verify local market rents. The underwriter will use average rents to calculate 75.00% towards your debt ratios. Most of these properties pay for themselves or even lower your DTI ratios

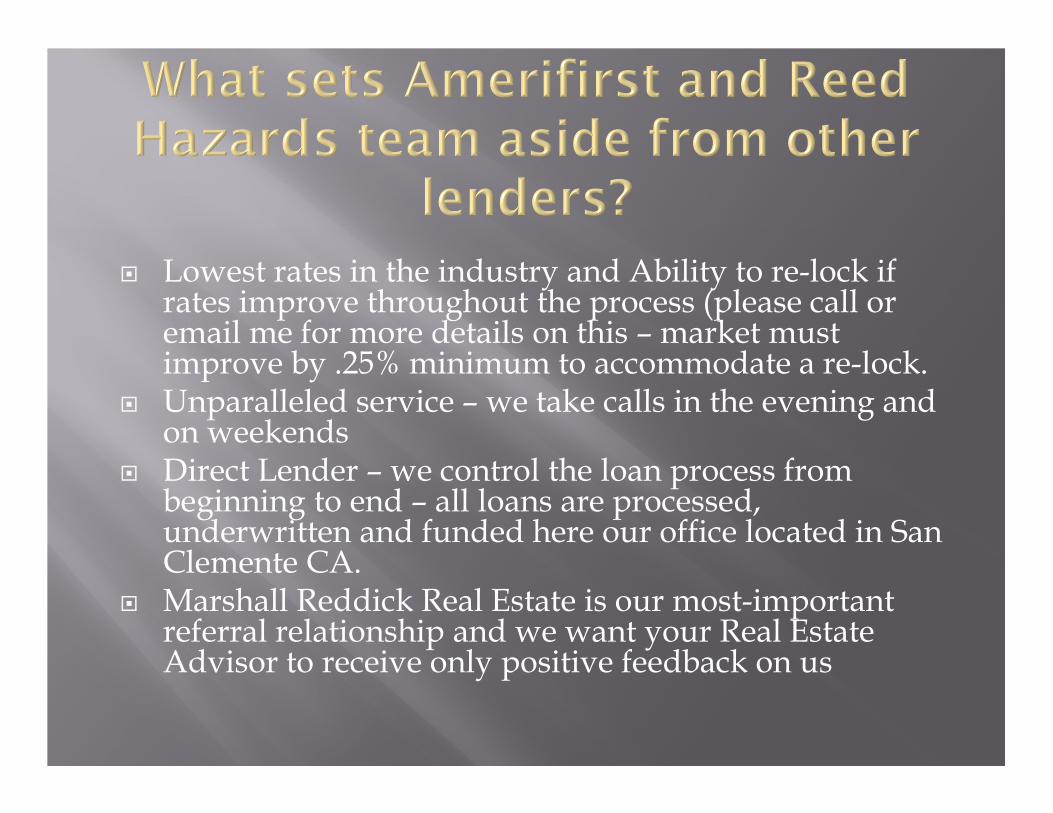

� Lowest rates in the industry and Ability to re-lock if rates improve throughout the process (please call or email me for more details on this – market must improve by .25% minimum to accommodate a re-lock.

� Unparalleled service – we take calls in the evening and on weekends

� Direct Lender – we control the loan process from beginning to end – all loans are processed, underwritten and funded here our office located in San Clemente CA.

� Marshall Reddick Real Estate is our most-important referral relationship and we want your Real Estate Advisor to receive only positive feedback on us

Appraisal credit at closing for All Marshall Reddick Buyers!

� Offer only valid through AmerfiFirstRodriguez/Hazard Office

� Redeemable at closing

� One coupon per transaction

Reed Hazard

Branch Manager

Cell: 949-973-5226

101 South El Camino Real, San Clemente CA. 92672

Email: [email protected]

Website: www.reedhazard.com

• Long Beach State University� Finance, Real Estate & Law

• 13 Years w/Marshall Reddick

• Rental Property Owner

• Private Real Estate Lender

• Real Estate Broker

Patrick PruntyController

Marshall Reddick Real Estate

BRE 01949337 - NMLS 1205733

Lend or Borrow!

I can help you when Reed or your bank can’t.

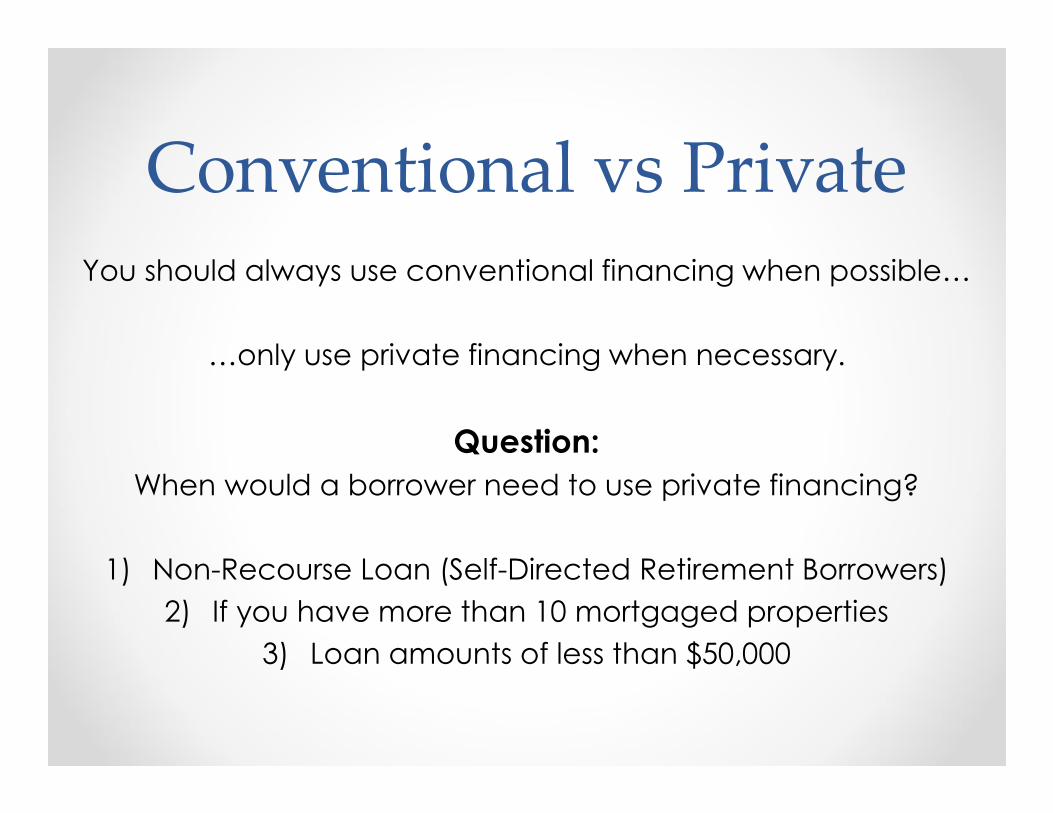

Conventional vs PrivateYou should always use conventional financing when possible…

…only use private financing when necessary.

Question:

When would a borrower need to use private financing?

1) Non-Recourse Loan (Self-Directed Retirement Borrowers)

2) If you have more than 10 mortgaged properties

3) Loan amounts of less than $50,000

Buy & Hold

Asset Based Lending

We qualify the property not the borrower

your down payment or your equity is all that is required.

Available for both:

Purchase Money Loans

or

Refinance/Cash-Out

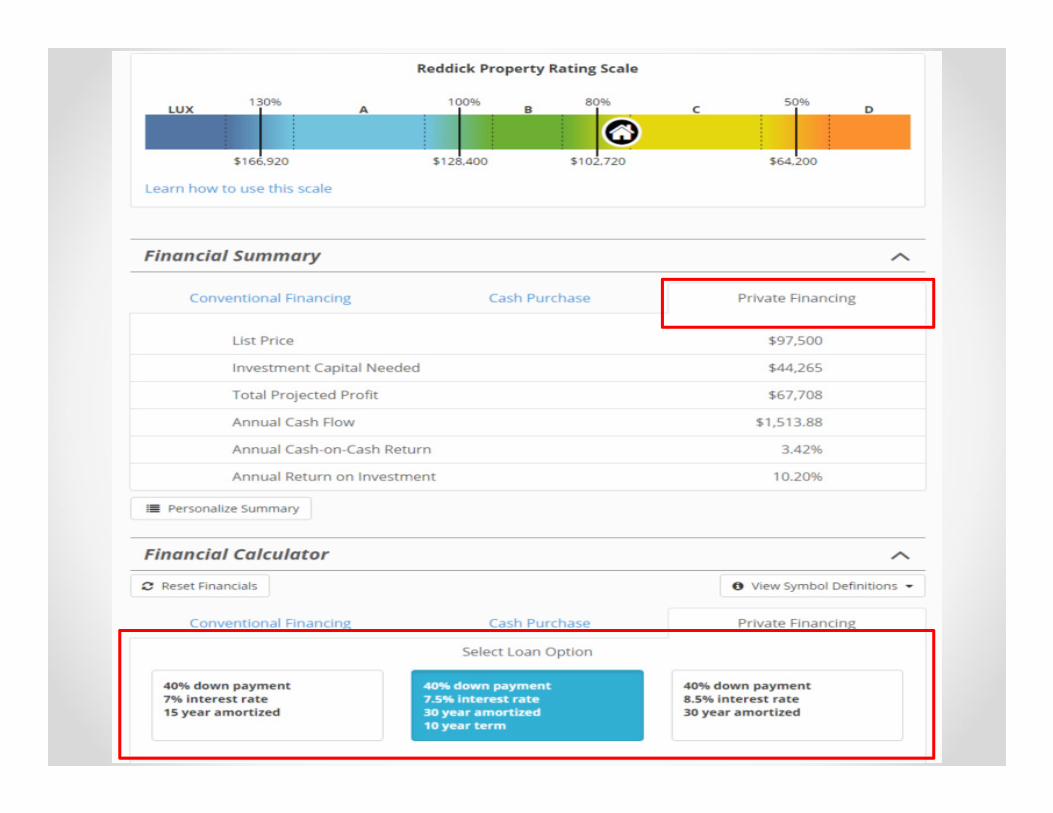

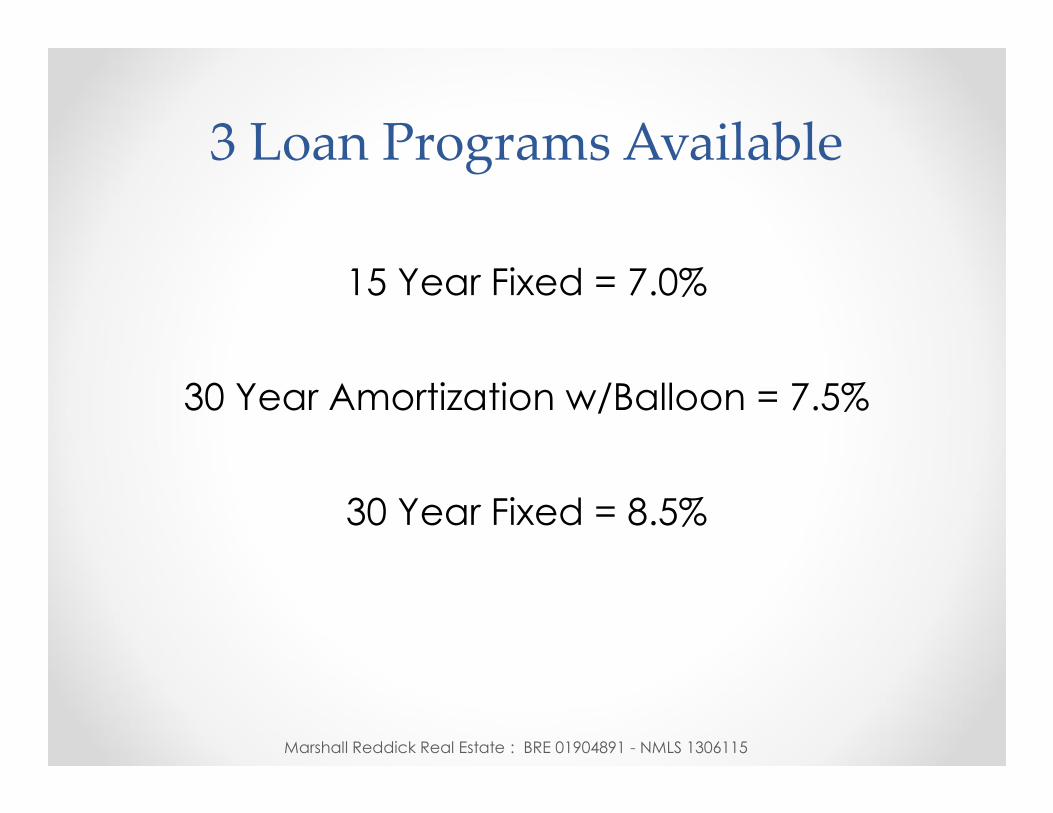

3 Loan Programs Available

15 Year Fixed = 7.0%

30 Year Amortization w/Balloon = 7.5%

30 Year Fixed = 8.5%

Marshall Reddick Real Estate : BRE 01904891 - NMLS 1306115

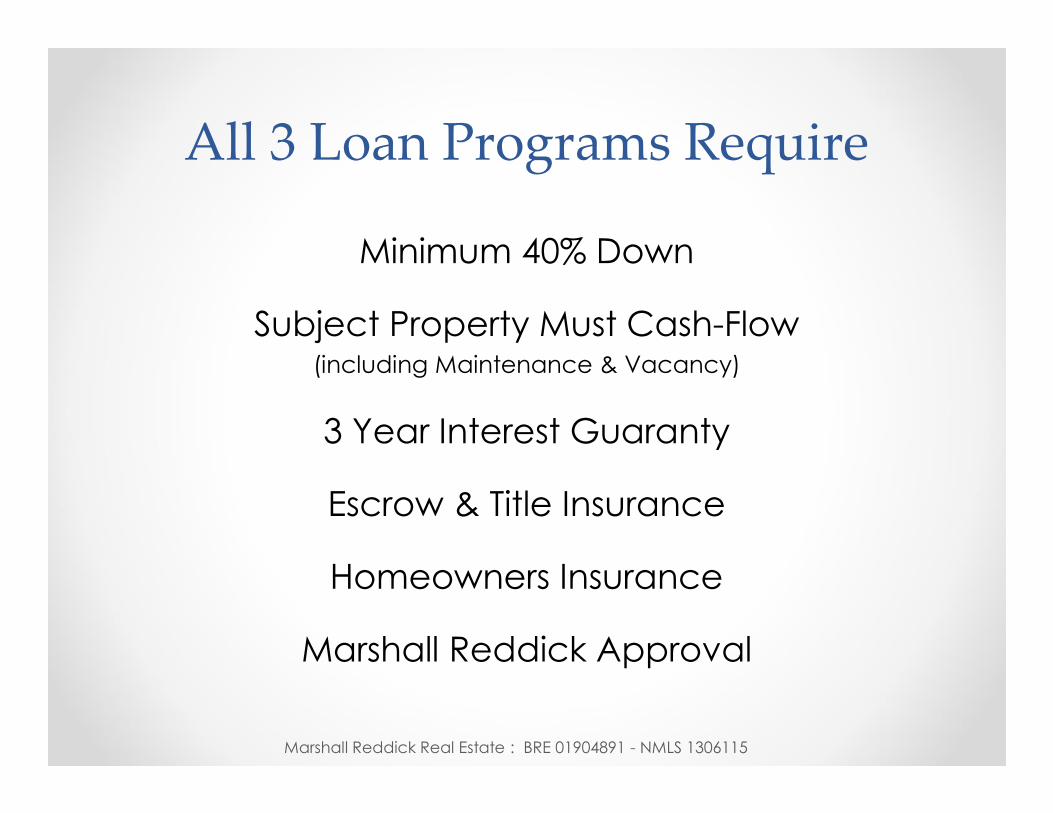

All 3 Loan Programs Require

Minimum 40% Down

Subject Property Must Cash-Flow (including Maintenance & Vacancy)

3 Year Interest Guaranty

Escrow & Title Insurance

Homeowners Insurance

Marshall Reddick Approval

Marshall Reddick Real Estate : BRE 01904891 - NMLS 1306115

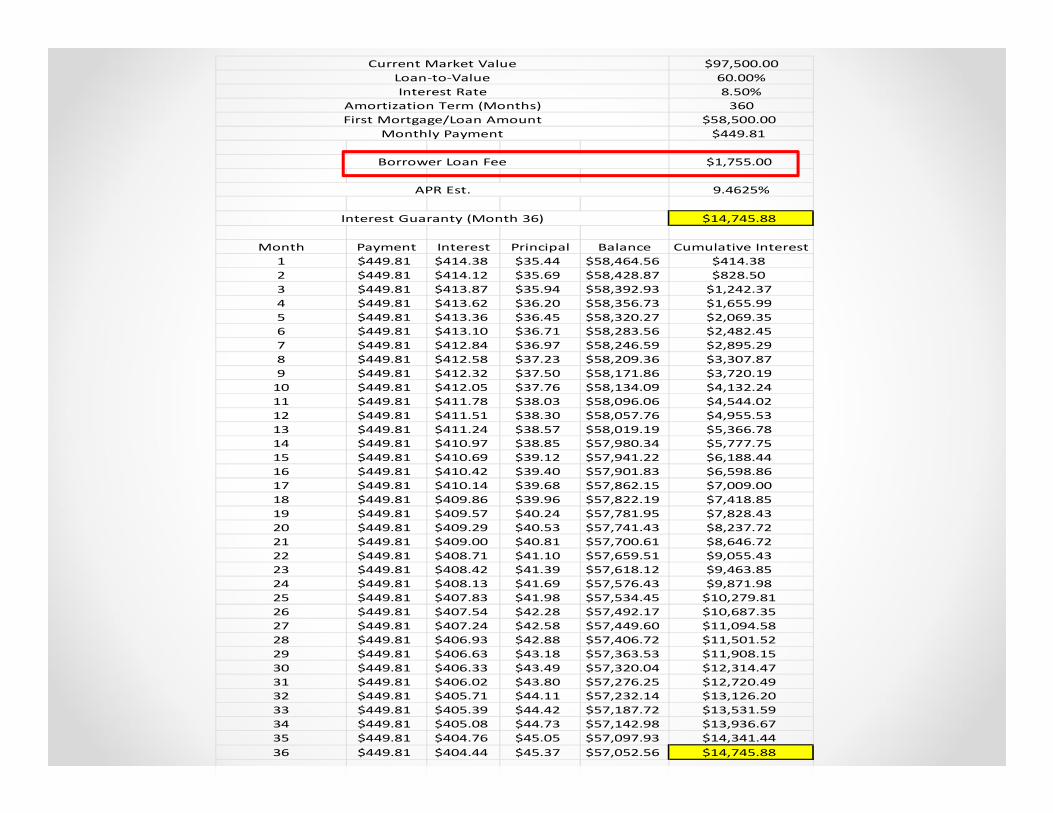

Asset Based Private Lending Programs

The payments, Rates, APR and Interest Guaranty above are based on a loan amount of $60,000 and 7% closing costs.

Question:

What does Marshall Reddick charge to do a private loan?

3 Points (3% of the loan amount)

Marshall Reddick Real Estate : BRE 01904891 - NMLS 1306115

$97,500.00

60.00%

8.50%

360

$58,500.00

$449.81

Borrower Loan Fee $1,755.00

9.4625%

$14,745.88

Month Payment Interest Principal Balance Cumulative Interest

1 $449.81 $414.38 $35.44 $58,464.56 $414.38

2 $449.81 $414.12 $35.69 $58,428.87 $828.50

3 $449.81 $413.87 $35.94 $58,392.93 $1,242.37

4 $449.81 $413.62 $36.20 $58,356.73 $1,655.99

5 $449.81 $413.36 $36.45 $58,320.27 $2,069.35

6 $449.81 $413.10 $36.71 $58,283.56 $2,482.45

7 $449.81 $412.84 $36.97 $58,246.59 $2,895.29

8 $449.81 $412.58 $37.23 $58,209.36 $3,307.87

9 $449.81 $412.32 $37.50 $58,171.86 $3,720.19

10 $449.81 $412.05 $37.76 $58,134.09 $4,132.24

11 $449.81 $411.78 $38.03 $58,096.06 $4,544.02

12 $449.81 $411.51 $38.30 $58,057.76 $4,955.53

13 $449.81 $411.24 $38.57 $58,019.19 $5,366.78

14 $449.81 $410.97 $38.85 $57,980.34 $5,777.75

15 $449.81 $410.69 $39.12 $57,941.22 $6,188.44

16 $449.81 $410.42 $39.40 $57,901.83 $6,598.86

17 $449.81 $410.14 $39.68 $57,862.15 $7,009.00

18 $449.81 $409.86 $39.96 $57,822.19 $7,418.85

19 $449.81 $409.57 $40.24 $57,781.95 $7,828.43

20 $449.81 $409.29 $40.53 $57,741.43 $8,237.72

21 $449.81 $409.00 $40.81 $57,700.61 $8,646.72

22 $449.81 $408.71 $41.10 $57,659.51 $9,055.43

23 $449.81 $408.42 $41.39 $57,618.12 $9,463.85

24 $449.81 $408.13 $41.69 $57,576.43 $9,871.98

25 $449.81 $407.83 $41.98 $57,534.45 $10,279.81

26 $449.81 $407.54 $42.28 $57,492.17 $10,687.35

27 $449.81 $407.24 $42.58 $57,449.60 $11,094.58

28 $449.81 $406.93 $42.88 $57,406.72 $11,501.52

29 $449.81 $406.63 $43.18 $57,363.53 $11,908.15

30 $449.81 $406.33 $43.49 $57,320.04 $12,314.47

31 $449.81 $406.02 $43.80 $57,276.25 $12,720.49

32 $449.81 $405.71 $44.11 $57,232.14 $13,126.20

33 $449.81 $405.39 $44.42 $57,187.72 $13,531.59

34 $449.81 $405.08 $44.73 $57,142.98 $13,936.67

35 $449.81 $404.76 $45.05 $57,097.93 $14,341.44

36 $449.81 $404.44 $45.37 $57,052.56 $14,745.88

First Mortgage/Loan Amount

Monthly Payment

APR Est.

Interest Guaranty (Month 36)

Current Market Value

Loan-to-Value

Interest Rate

Amortization Term (Months)

Talk to your real estate advisor.

Use the website to run cash-flow and return analysis.

Complete an application & obtain a pre-approval letter.

Getting Started