Financial System and Monetary Policy Transmission ... · PDF fileFinancial System and Monetary...

22

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception Miranda S. Goeltom Acting Governor, Bank Indonesia Bank Indonesia’s 7th International Seminar “Global Financial Tsunami: What can we do?” Bali, 13 June 2009

Transcript of Financial System and Monetary Policy Transmission ... · PDF fileFinancial System and Monetary...

Financial System and Monetary Policy Transmission Mechanism:How to Address the Increasing Risk Perception

Miranda S. GoeltomActing Governor, Bank Indonesia

Bank Indonesia’s 7th International Seminar “Global Financial Tsunami: What can we do?”

Bali, 13 June 2009

Scope of the Paper 2

1. Introduction

2. Behavioural Change in the Financial System

3. The Monetary Policy Transmission Mechanism: the Role of Risk Perception

4. Financial System and Monetary Policy in Indonesia4. Financial System and Monetary Policy in Indonesia

5. Policy Implication: General View

6. Conclusion

1. Salient Aspect Arise in Global Financial Crises. ..

� Rapid and deep propagation of th he impact of the c urrent financial crisis

– The considerable change of global economic environment compared to the brazen confidence of the 1990s

– The rapidly changing financial system coupled with its innovative development as the main engine

� Increasing the complexity of monetary policy managem ent

3

� Reorientation of the central bank policy ...

– not only expands the scope of existing policy, but also

– enables a shift in policy paradigm to adjust to the changes in the economic environment

Factors contributing the change in global financial system ... 4

Real Interet Rate

� Three factors precipitate shifts in the global fina ncial system:1. innovative development of information and technology2. deregulation of supporting financial systems3. conducive global macroeconomic conditions, including low real interest rate

� The shifts in the global financial system have not been independent from the financial system characteristics .... that tend t o be pro-cyclical

Source: IMF

2. Behavioral Changes in the Global Financial Syste m

Risk Management

� The preferrence to hedge and diversify risk, as well as transfer risk to other financial institutions more rapidly

� The ability to manage risk relates to the decline in liquidity risk along with more liquid financial institutions

� The ability to manage risk is developing in line with the rise in financial product innovation that can accommodate risk diversification such as credit derivative products

Changes Features

� The ability to accumulate and distribute funds increased rapidly

5

Operational Activity

- Due to the fact that the capacity of financial institutions to expand their businesses is less constraint from using available funds

� Differs entirely from the old characteristics of financial institutions where fund distribution was highly influenced by the actual funds available

Improved the ability of the financial institutions to separate the two primary functions of bank: the origination and holding of c redit risk

Pattern of Financial Institution Integration

Horizontal Integration

� Integration between the stock and bonds markets� Facilitated greater capital mobility between countries

Type of Integration Features

6

The change also occurred in the type of financial i nstitution integration ...

Vertical

� Integration between the role and the function of financial institutions

� Involved a blurring of the boundaries of the financial services Vertical Integration

� Involved a blurring of the boundaries of the financial services offered by each type of financial institution

� Products offered by banks, insurance companies, the money market and the capital market shared similar characteristics and were often difficult to differentiate

DiagonalIntegration

� Integration between the financial and commodity markets � In line with financial product innovation involving activities in the

commodity market� The value of commodity derivatives has skyrocketed in the last

10 years, from USD400 billion in 1998 to USD9 trillion at the end of 2007 (Jenkison et al, 2008)

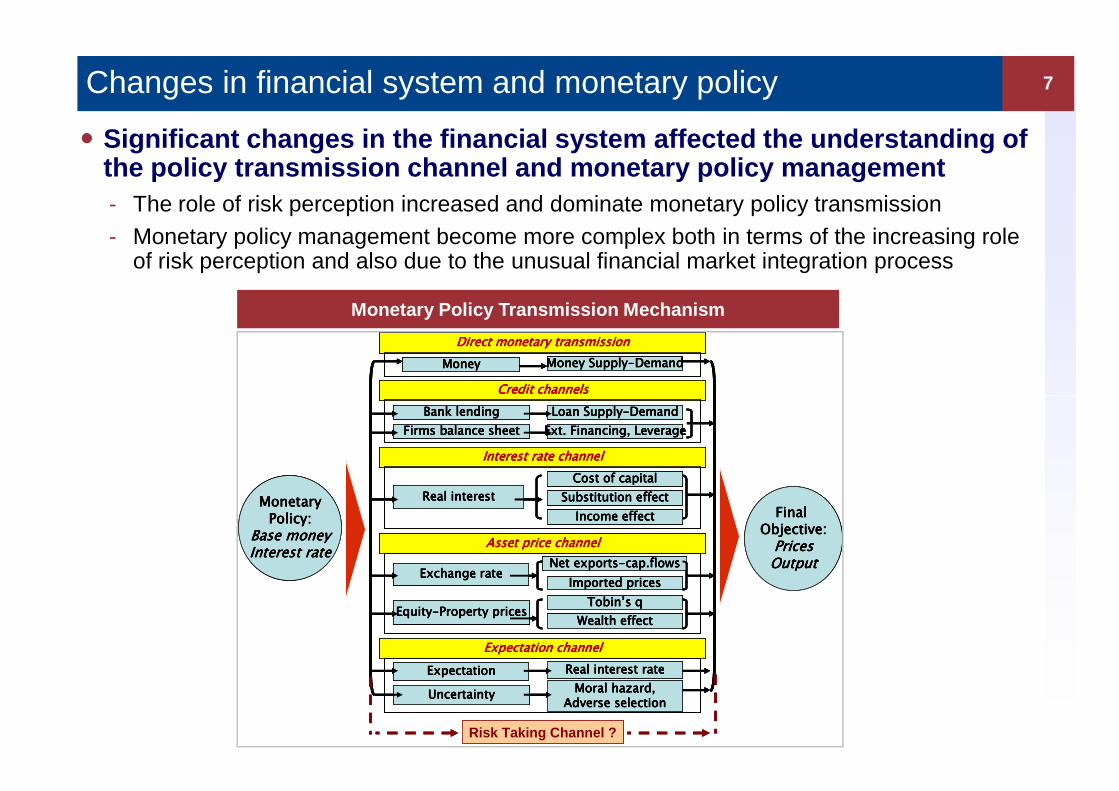

Changes in financial system and monetary policy

Monetary Policy Transmission Mechanism

� Significant changes in the financial system affecte d the understanding of the policy transmission channel and monetary policy management- The role of risk perception increased and dominate monetary policy transmission- Monetary policy management become more complex both in terms of the increasing role

of risk perception and also due to the unusual financial market integration process

7

Direct monetary transmissionDirect monetary transmissionDirect monetary transmissionDirect monetary transmission

MoneyMoneyMoneyMoney

Credit channelsCredit channelsCredit channelsCredit channels

Money SupplyMoney SupplyMoney SupplyMoney Supply----DemandDemandDemandDemand

Direct monetary transmissionDirect monetary transmissionDirect monetary transmissionDirect monetary transmission

MoneyMoneyMoneyMoney

Credit channelsCredit channelsCredit channelsCredit channels

Money SupplyMoney SupplyMoney SupplyMoney Supply----DemandDemandDemandDemand

Direct monetary transmissionDirect monetary transmissionDirect monetary transmissionDirect monetary transmission

MoneyMoneyMoneyMoney

Credit channelsCredit channelsCredit channelsCredit channels

Money SupplyMoney SupplyMoney SupplyMoney Supply----DemandDemandDemandDemand

MonetaryMonetaryMonetaryMonetaryPolicy:Policy:Policy:Policy:

Base moneyBase moneyBase moneyBase moneyInterest rateInterest rateInterest rateInterest rate

Final Final Final Final Objective:Objective:Objective:Objective:PricesPricesPricesPricesOutputOutputOutputOutput

Interest rate channelInterest rate channelInterest rate channelInterest rate channel

Real interestReal interestReal interestReal interest

Cost of capitalCost of capitalCost of capitalCost of capital

Substitution effectSubstitution effectSubstitution effectSubstitution effect

Income effectIncome effectIncome effectIncome effect

Asset price channelAsset price channelAsset price channelAsset price channel

Exchange rateExchange rateExchange rateExchange rateNet exportsNet exportsNet exportsNet exports----cap.flowscap.flowscap.flowscap.flows

TobinTobinTobinTobin’’’’s qs qs qs q

Wealth effectWealth effectWealth effectWealth effect

Credit channelsCredit channelsCredit channelsCredit channels

Bank lendingBank lendingBank lendingBank lending Loan SupplyLoan SupplyLoan SupplyLoan Supply----DemandDemandDemandDemand

Ext. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageFirms balance sheetFirms balance sheetFirms balance sheetFirms balance sheet

Imported pricesImported pricesImported pricesImported prices

EquityEquityEquityEquity----Property pricesProperty pricesProperty pricesProperty prices

Expectation channelExpectation channelExpectation channelExpectation channel

ExpectationExpectationExpectationExpectation Real interest rateReal interest rateReal interest rateReal interest rate

Moral hazard,Moral hazard,Moral hazard,Moral hazard,Adverse selectionAdverse selectionAdverse selectionAdverse selection

UncertaintyUncertaintyUncertaintyUncertainty

Risk Taking Channel ?

MonetaryMonetaryMonetaryMonetaryPolicy:Policy:Policy:Policy:

Base moneyBase moneyBase moneyBase moneyInterest rateInterest rateInterest rateInterest rate

Final Final Final Final Objective:Objective:Objective:Objective:PricesPricesPricesPricesOutputOutputOutputOutput

Interest rate channelInterest rate channelInterest rate channelInterest rate channel

Real interestReal interestReal interestReal interest

Cost of capitalCost of capitalCost of capitalCost of capital

Substitution effectSubstitution effectSubstitution effectSubstitution effect

Income effectIncome effectIncome effectIncome effect

Asset price channelAsset price channelAsset price channelAsset price channel

Exchange rateExchange rateExchange rateExchange rateNet exportsNet exportsNet exportsNet exports----cap.flowscap.flowscap.flowscap.flows

TobinTobinTobinTobin’’’’s qs qs qs q

Wealth effectWealth effectWealth effectWealth effect

Credit channelsCredit channelsCredit channelsCredit channels

Bank lendingBank lendingBank lendingBank lending Loan SupplyLoan SupplyLoan SupplyLoan Supply----DemandDemandDemandDemand

Ext. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageFirms balance sheetFirms balance sheetFirms balance sheetFirms balance sheet

Imported pricesImported pricesImported pricesImported prices

EquityEquityEquityEquity----Property pricesProperty pricesProperty pricesProperty prices

Expectation channelExpectation channelExpectation channelExpectation channel

ExpectationExpectationExpectationExpectation Real interest rateReal interest rateReal interest rateReal interest rate

Moral hazard,Moral hazard,Moral hazard,Moral hazard,Adverse selectionAdverse selectionAdverse selectionAdverse selection

UncertaintyUncertaintyUncertaintyUncertainty

MonetaryMonetaryMonetaryMonetaryPolicy:Policy:Policy:Policy:

Base moneyBase moneyBase moneyBase moneyInterest rateInterest rateInterest rateInterest rate

Final Final Final Final Objective:Objective:Objective:Objective:PricesPricesPricesPricesOutputOutputOutputOutput

Interest rate channelInterest rate channelInterest rate channelInterest rate channel

Real interestReal interestReal interestReal interest

Cost of capitalCost of capitalCost of capitalCost of capital

Substitution effectSubstitution effectSubstitution effectSubstitution effect

Income effectIncome effectIncome effectIncome effect

Asset price channelAsset price channelAsset price channelAsset price channel

Exchange rateExchange rateExchange rateExchange rateNet exportsNet exportsNet exportsNet exports----cap.flowscap.flowscap.flowscap.flows

TobinTobinTobinTobin’’’’s qs qs qs q

Wealth effectWealth effectWealth effectWealth effect

Credit channelsCredit channelsCredit channelsCredit channels

Bank lendingBank lendingBank lendingBank lending Loan SupplyLoan SupplyLoan SupplyLoan Supply----DemandDemandDemandDemand

Ext. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageExt. Financing, LeverageFirms balance sheetFirms balance sheetFirms balance sheetFirms balance sheet

Imported pricesImported pricesImported pricesImported prices

EquityEquityEquityEquity----Property pricesProperty pricesProperty pricesProperty prices

Expectation channelExpectation channelExpectation channelExpectation channel

ExpectationExpectationExpectationExpectation Real interest rateReal interest rateReal interest rateReal interest rate

Moral hazard,Moral hazard,Moral hazard,Moral hazard,Adverse selectionAdverse selectionAdverse selectionAdverse selection

UncertaintyUncertaintyUncertaintyUncertainty

Risk Taking Channel ?

3. Risk Perception and Monetary Transmission Mechan ism 8

� Borio and Zhu (2008) called “the risk-taking channe l” ....

Risk Taking Channel in Monetary Policy Transmission Mechanism

Source: Borio and Zhu (2008)

� Three mechanisms of risk-taking channel (Borio and Zhu, 2008) : 1. Relates to valuation factors, income and cash flows2. The correlation between the interest rate & the nominal rates of return 3. Positive effect of transparency from central banks

� Empirical studies support the argument the role of a risk-taking channel

– Loannidou et al, (2007) show in Bolivia that banks tend to take more risk when monetary policy is loose

– Amato (2005) showed monetary policy stance affects the pricing of credit risk and influences credit approval patterns by financial institutions

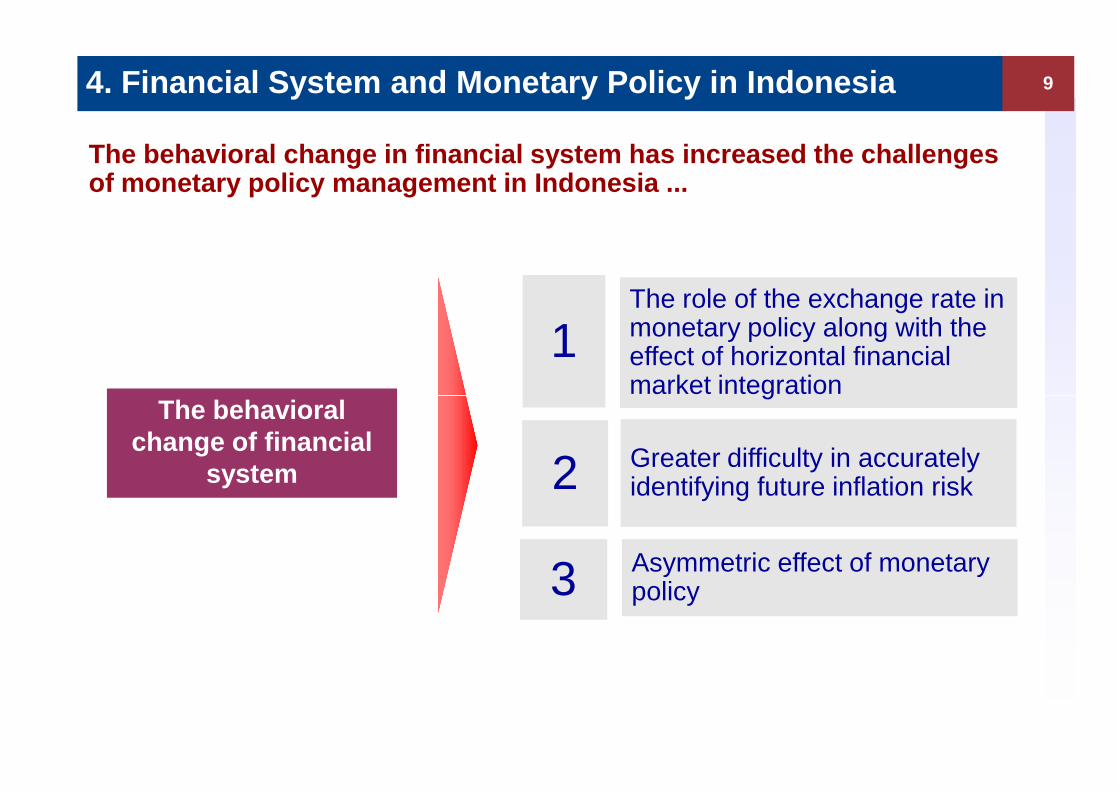

4. Financial System and Monetary Policy in Indonesi a

The role of the exchange rate in monetary policy along with the effect of horizontal financial market integration

The behavioral

9

The behavioral change in financial system has incre ased the challenges of monetary policy management in Indonesia ...

1market integration

The behavioral change of financial

systemGreater difficulty in accurately identifying future inflation risk 2

Asymmetric effect of monetary policy3

The exchange rate tends to move exogenously and amp lifies shocks in the economy ...

� The dynamics of rupiah exchange rate highly affected by the financial account

� The strong influence of the financial account is primarily attributable to the increasing trend of capital flows in the form of investment portfolio compared to the form of FDI

� The role of capital flows increased due to low perception of risk for investment in Indonesia and other emerging markets as reflected by the relatively low Emerging Market Global Bond Index (EMBIG) and Indonesia’s Credit Default Swap (CDS)

The role of exchange rate .... 10

Current Account and Financial Account: INDONESIA

(12)

(7)

(2)

3

8

13

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Current

Account

Foreign Portfolio

Investment (net)

Foreign Direct

Investment (net)

$ billion

Annualized

quarterly data

EMBIG and CDS Indonesia

Source: Bank Indonesia and Bloomberg

100

300

500

700

900

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09

100

300

500

700

900

1100

1300

1500EMBI Global CDS Indonesia (RHS)

bpsbps

Two different period of loosening monetary policy stance

Diamond Diagram

Accuracy to identify future inflation risk ...

� Due to increasing financial market innovation and in tegration with the commodity market ...

� The effects of loosening monetary policy to future inflation risk becoming hidden– Inflation was relatively low despite the loose monetary policy stance– However, the capital and commodity markets expanded indicating a bubble

11

16Suku bungaInterest Rate

(Monthly Decreasing, bps)16Suku bungaInterest Rate

(Monthly Decreasing, bps)

0

4

8

12

Inflasi inti

IHSG

REER

Aug 95 - Jul 97

May 06 - May 07

125,81 115,54

17,7

39,07

7,376,07

=

29,8

8,7

Core Inflation

(%)

JCI

0

4

8

12

Inflasi inti

IHSG

REER

Aug 95 - Jul 97

May 06 - May 07

125,81 115,54

17,7

39,07

7,376,07

=

29,8

8,7

Core Inflation

(%)

JCI

� 1996-1997 (period of undeveloped financial innovation): core inflation was relatively high

� 2005-2007 (period of developed financial market): core inflationary pressure was not excessively high at around 6%

� However, the stock index witnessed strong rallies and imply to price bubbles

� Was driven by substantial foreign capital inflows triggered by lower risk perception.

The asymmetric effect of monetary policy

� Related to the influence of financial system behavi or that tended to be pro-cyclical coupled with the presence of the risk-taking channe l

� Asymmetry in the sensitivity between the BI Rate an d lending rate, as well as between credit rate and demand for credit (Goeltom et al., 2009)

– Lending rate during an expansionary economic cycle-both working capital credit and investment credit - is less sensitive in response to a hike in the BI Rate

– Credit demand during an expansionary economic cycle is greater than contractionaryeconomic cycle

12

The Asymmetric Monetary Policy Transmission Mechani sm

Variable Credit Interest Rate-Working Capital

Credit Interest Rate-Investment

Demand for Credit

BI Rate 0.104 0.058

Credit Interest Rate - - -0.076

Interest Rate Response in the Expansionary Cycle

-0.012 -0.006 0.037

Source: Goeltom et. al (2009)

Risk perception and bank response

� Asymmetry was also clearly evident during the curre nt crisis period when loosening monetary policy by Bank Indonesia was res ponded slowly by the banks

� The bank slow response corresponded to the risk per ception ...

– Increasing business risk: the slow response was attributable to the high perception of business risk during the crisis period, which was offset by the high interest rate

– Increasing legal risk:

13

%

Interest Rate Dynamic� Bankers from state-owned banks (BUMN) felt exposed

Source: Bank Indonesia

4

8

12

16

20

24

00 01 02 03 04 05 06 07 08

BI RateDeposit Rate 1 Month

Credit-InvestmentCredit-Working Capital

%banks (BUMN) felt exposed to legal risk in the event of non-performing loans

� ... may consider that a loss originating from a BUMN bank as a national loss

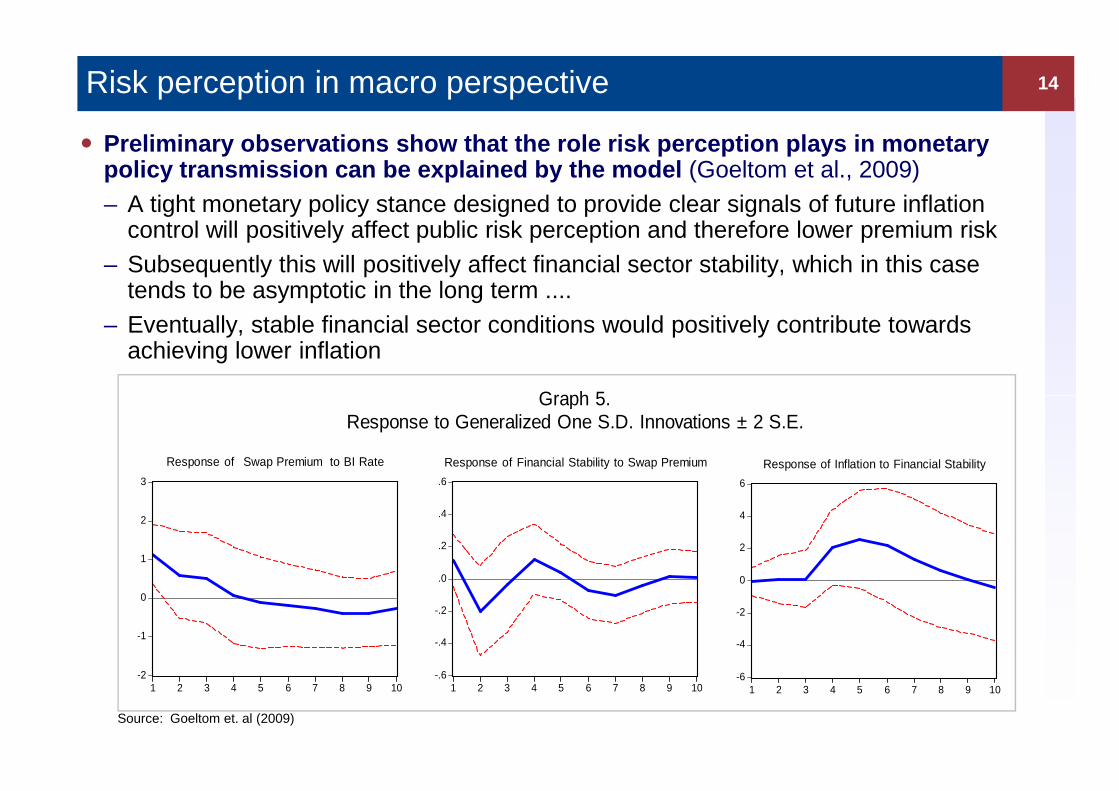

Risk perception in macro perspective

� Preliminary observations show that the role risk pe rception plays in monetary policy transmission can be explained by the model (Goeltom et al., 2009)– A tight monetary policy stance designed to provide clear signals of future inflation

control will positively affect public risk perception and therefore lower premium risk – Subsequently this will positively affect financial sector stability, which in this case

tends to be asymptotic in the long term ....– Eventually, stable financial sector conditions would positively contribute towards

achieving lower inflation

14

Graph 5.

-2

-1

0

1

2

3

1 2 3 4 5 6 7 8 9 10

Response of Swap Premium to BI Rate

-.6

-.4

-.2

.0

.2

.4

.6

1 2 3 4 5 6 7 8 9 10

Response of Financial Stability to Swap Premium

-6

-4

-2

0

2

4

6

1 2 3 4 5 6 7 8 9 10

Response of Inflation to Financial Stability

Graph 5.Response to Generalized One S.D. Innovations ± 2 S.E.

Source: Goeltom et. al (2009)

5. Policy Implications: General View

The achievement of macroeconomic stability, which n ot only relates to price stability but also interacts with financial s tability

15

� Price stability in support of macroeconomic stabili ty must be complemented with stability in the financial systemwith stability in the financial system

– Partial policy that only features price stability or financial stability will result in sub-optimal macroeconomic management in the mid-long term

� Requirement for integrated policy encompassing mone tary policy, banking policy and the policies taken by other authorities

Policy Implications: Monetary Policy

MP formulation should consider more the dynamics of financial system

16

� Monetary policy needs to redefine the meaning of pr ice stability as the overarching goal of monetary policy– Price stability should not only relate to inflation risk but also a

decomposition of balanced weighting of inflation risk and risk from financial system stability

� Monetary policy should extend a forward -looking horizon regarding

1

...in the future, monetary policy should be more fl exible

� Monetary policy should extend a forward -looking horizon regarding price stability risk– Price stability risk can remain hidden due to its temporary absorption

in the rapidly expanding financial and commodity market

2

Monetary policy should be more flexible ...

� Combining old and new ideas to accommodate the role of financial system stability in policy formulation

� Considers the role of financial system stability ca n also relate to the role of the exchange rate

– Bending monetary policy rule to consider the exchange rate should be reinforced

� Opens the possibility of reusing the ‘quantity appr oach’ in the monetary policy framework

17

policy framework

– When the economy is in recessionary cycle coupled by a very high perception of risk can hinder the transmission of monetary policy through interest rate channel

Monetary policy should be more flexible: Indonesia case ...

Striking a balance between three strategic aspects . ...� monetary stability� strengthening financial system stability � aligning stimuli to maintain economic growth momentum

� Feasibility of financial sector stability in anchori ng the effect of monetary policy towards the real sector and prices

- Re-affirms its role as a nominal anchor of monetary policy ?

� The lack of merit the assumption holds on the limit ed role the exchange rate

18

� The lack of merit the assumption holds on the limit ed role the exchange rate implies the need for flexibility in implementing ITF in Indonesia

– There is justification for taking the role of exchange rate into account during the implementation of ITF based monetary policy in Indonesia (Goeltom, 2008)

– ‘The bending rule’ also enables a more optimal countercyclical policy response

� Cautious easing monetary policy response– Seven time gradually decrease of BI rate in the last six months (from 9.5% in Dec

‘08 to 7.0%) .... limited room for further decrease ....– BI should explore different avenues with a different perspective, or beyond the

conventional wisdom of monetary policy� However, ... should be mindful of the provisions governing the Central Bank Act

Policy Implications: Banking Policy

Banking system regulations are aimed at managing fi nancial system behavior that is pro-cyclical towards the economic cycle ...

19

� A couple of important elements under the principle o f tighter regulations should economic expansion occur , vice versa (Leijonhufvud, 2009)

– To impose a reserve requirement on banks and financial institutions that hold public funds, including money market funds

– To increase capital deposits for all players in the financial market as a whole by emphasizing core capital (Tier 1) availability emphasizing core capital (Tier 1) availability

� Regulations is complemented by a wider view of the banking system as a whole

– When responding to pressures stemming from a crisis, the actions of individual banks can precipitate a rise in systemic risk

– Bank response, which individually may be optimal, collectively may weaken the banking system (fallacy of composition phenomenon)

� Financial intermediaries should return to basics

– A clear separation between the role of commercial banks and investment banks should be reaffirmed, monitored and regulated by the relevant authorities

Banking policy: Indonesia case

Directed towards safeguarding the bank intermediati on function

• Continues to institute a variety of policies that s trengthen bank resilience in order to support financial system stability

� Under the auspices of both the Basel II framework as well as Indonesian Banking Architecture

• The Financial Stability Wing also actively reinforc es its two main functions:

� Financial supervision: development of the Payment System and clearing of securities which are closely correlated and carry very high systemic risk.

20

securities which are closely correlated and carry very high systemic risk.

� Supervision of systemic banks: in line with counter-cyclical measures, the current buzzword is “capital strengthening”, especially Tier-1 capital, so that banks are able to maintain an adequate first-line of defense against shocks in the financial sector

6. Conclusion

� Central banks should be more flexible and creative . ..– Policy flexibility is crucial in the short term so that the policy response instituted

does not undermine the actions taken to maintain macroeconomic stability

– Policy guidelines must be adjusted to anticipate risk that may arise and could disrupt macroeconomic stability

� Future policy must be integrated from all authoriti es and strongly supported by political will ...

21

– Comprehensive crisis resolution requires complete information and a broad authoritative scope

– Can only be obtained if all authorities and officials maintain strong relationships to eliminate the problems of coordination

22

Thank you...