Financial Supply Chain Why do you need to know? June 2011 Benjamin Lam.

14

Financial Supply Chain Why do you need to know? June 2011 Benjamin Lam

-

Upload

grant-cameron -

Category

Documents

-

view

216 -

download

0

Transcript of Financial Supply Chain Why do you need to know? June 2011 Benjamin Lam.

Financial Supply ChainWhy do you need to know?

June 2011Benjamin Lam

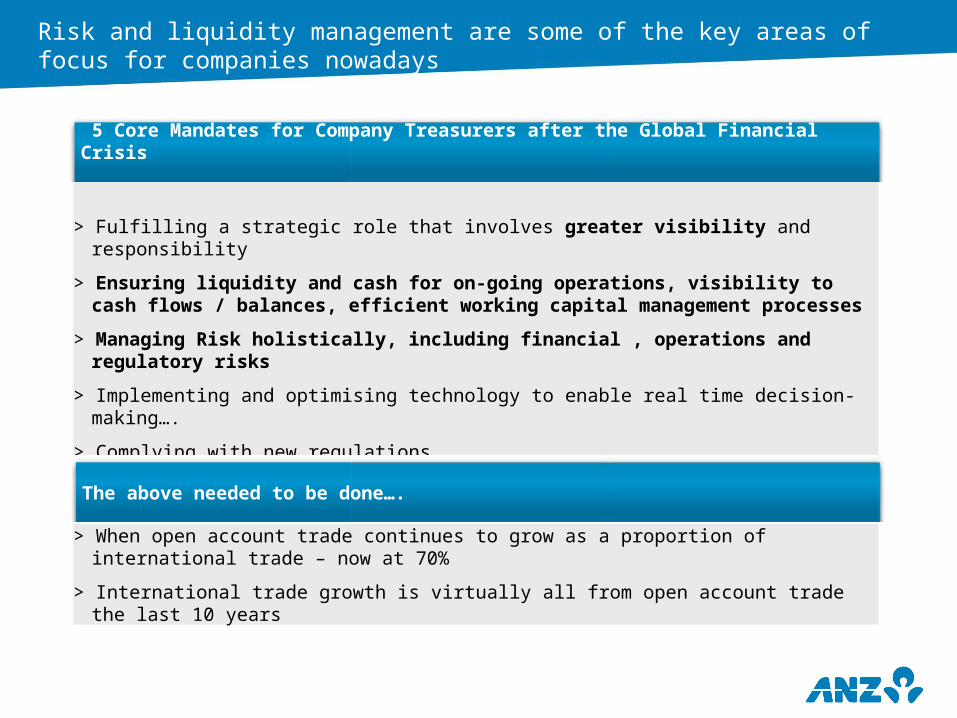

Risk and liquidity management are some of the key areas of focus for companies nowadays

> Fulfilling a strategic role that involves greater visibility and responsibility

> Ensuring liquidity and cash for on-going operations, visibility to cash flows / balances, efficient working capital management processes

> Managing Risk holistically, including financial , operations and regulatory risks

> Implementing and optimising technology to enable real time decision-making….

> Complying with new regulations

Source: Serving the new Corporate Treasurer by Oliver Wyman

5 Core Mandates for Company Treasurers after the Global Financial Crisis

The above needed to be done….

> When open account trade continues to grow as a proportion of international trade – now at 70%

> International trade growth is virtually all from open account trade the last 10 years

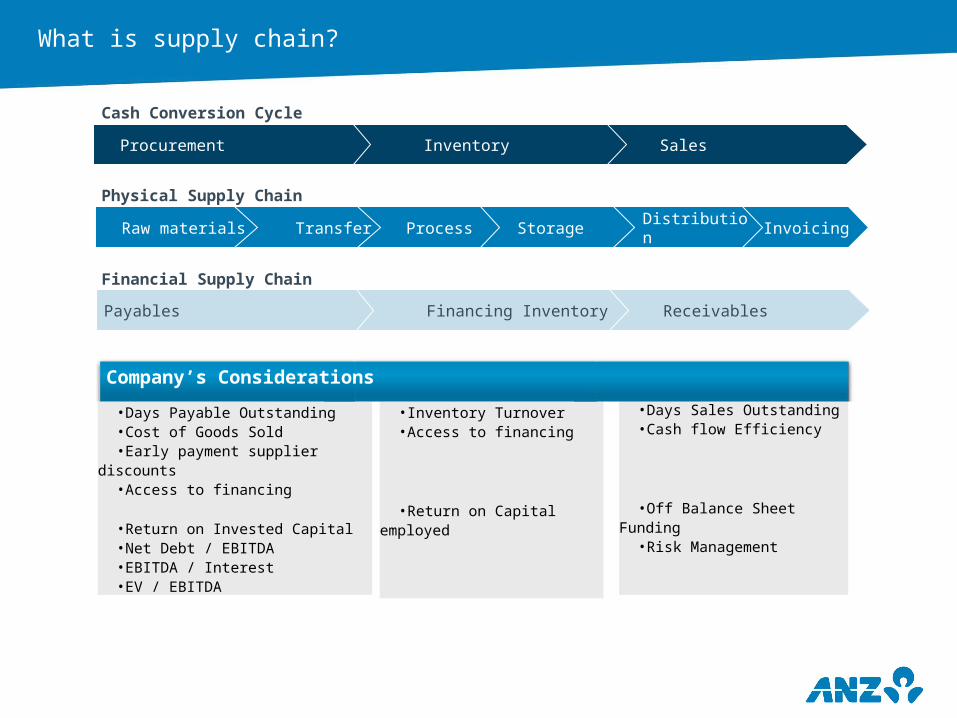

What is supply chain?

Cash Conversion Cycle

Physical Supply Chain

Financial Supply Chain

Sales Inventory Procurement

InvoicingDistribution Storage Process Transfer Raw materials

Receivables Financing InventoryPayables

•Days Payable Outstanding•Cost of Goods Sold •Early payment supplier discounts•Access to financing

•Return on Invested Capital•Net Debt / EBITDA•EBITDA / Interest•EV / EBITDA

•Inventory Turnover•Access to financing

•Return on Capital employed

•Days Sales Outstanding•Cash flow Efficiency

•Off Balance Sheet Funding•Risk Management

Company’s Considerations

Why Supply Chain?

>Optimising the efficiency of a company’s end to end supply chain, both physical and financial is essential for working capital needs

>Supply chain management has the potential to improve the three key drivers of financial performance – growth, profitability and capital utilisation

Costs

Working Capital Efficiency Reduces Days Sales Outstanding and accelerates the cash conversion cycle through readily accessible liquidity; or more sales with unchanged DSOs

Reduces financing cost by leveraging on the Buyer’s credit strength; secured long-term supply; reduce purchasing cost

Improved liquidity allows suppliers to allocate funds to other use including capital expenditure or investment opportunities

Subject to auditor’s confirmation, potential to minimise impact on the basis of “true sale” of the receivables to ANZ

With the assignment of receivables, there is an opportunity to transfer the buyer’s default/payment risk to the bank

RF provides an alternative source of funding by leveraging off the credit profile of their Buyers, with minimal impact to existing bank relationships (for without recourse structure)

Cash Flow

Risk

Balance Sheet Impact

Access to Credit

Financing supply chain – bank’s approach

>A supply chain event can be issuing of invoice; maturity of payment terms; delivery of goods and etc

>The solution can be provision of financing, guaranteeing payment to you or on your behalf, or both

>The solution can be provided based on your company’s strengths or those of your buyers

A bank’s approach is to ensure that the financial supply chain is designed to match the physical supply chain; financing and/or risk management is triggered by selected events in the chain

FINANCIAL SUPPLY CHAIN

PHYSICAL SUPPLY CHAIN

MANUFACTURERS/ SERVICES

> Process

Your supplier

> Payment>Sales Storage Process

> Payment>Sales

Funds Transfer

Accounts Receivable Financing Inventory

FundsTransfer

Raw materials

Raw materials

Accounts Payable

> Payment>SalesStorage

Your company

Your customer

$

$

Labour I.P. Networks

An example – receivables solutions

Immediate Payment

1. Buyer and seller have a sales contractual relationship

2. Seller to enter a Receivables Purchase Agreement (‘RPA”) with a bank which is comfortable with the buyer’s financial position and the seller’s ability to produce and deliver goods.

3. Seller delivers goods to the buyer and issues invoice (or against PO issued by buyer with invoice to be issued later)

4. ANZ makes payment to the seller (funded structure) or guaranteeing payment upon payment maturity (unfunded structure)

5. On due date of the receivable, the buyer makes payment for the invoiced goods to the bank (for unfunded structures, this payment is forwarded by ANZ to the seller).

How does it work?

Is this Cash?

1. Commercial disputes

2. Money ‘wrongly received’ or ‘deducted’

Delivery of Goods

Deferred Payment

SellerBUYERS

Bank

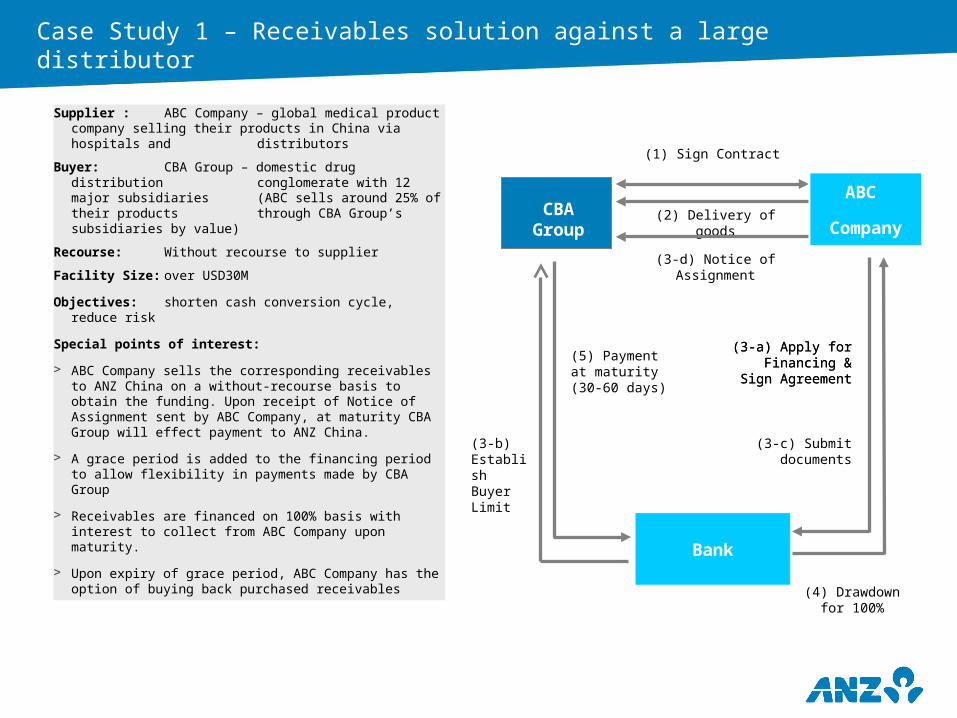

Case Study 1 – Receivables solution against a large distributor

Supplier : ABC Company – global medical product company selling their products in China

via hospitals and distributors

Buyer: CBA Group – domestic drug distribution conglomerate with 12 major subsidiaries (ABC sells around 25% of their products through CBA Group’s subsidiaries by

value)

Recourse: Without recourse to supplier

Facility Size: over USD30M

Objectives: shorten cash conversion cycle, reduce risk

Special points of interest:

ABC Company sells the corresponding receivables to ANZ China on a without-recourse basis to obtain the funding. Upon receipt of Notice of Assignment sent by ABC Company, at maturity CBA Group will effect payment to ANZ China.

A grace period is added to the financing period to allow flexibility in payments made by CBA Group

Receivables are financed on 100% basis with interest to collect from ABC Company upon maturity.

Upon expiry of grace period, ABC Company has the option of buying back purchased receivables

ABC

CompanyCBA

Group(2) Delivery of goods

(3-a) Apply for Financing & Sign

Agreement

(4) Drawdown for 100%

(5) Payment at maturity (30-60 days)

(1) Sign Contract

(3-d) Notice of Assignment

(3-b) Establish Buyer Limit

(3-a) Apply for Financing & Sign

Agreement

(3-c) Submit documents

Bank

Case Study 2 – Application of receivables solution in IT industry

Supplier: XYZ Technology – global IT equipment supplier outside China

Buyer: DDD Company - key national IT product distributors in China

Facility Size: Over USD50M

Objectives: offload a portion of supplier’s risk against the buyer to stay within its own internal credit limit irrespective of expected sales growth through the buyer.

Special points of interest:

> XYZ’s local company is responsible for delivery of goods to DDD while payments is made by DDD to XYZ’s regional billing centre

> XYZ will not seek to sell receivables to bank unless its internal credit limit against the buyer is exceeded

> Long grace period included in the structure to allow DDD flexibility in making payments to XYZ

> Assignment of receivables (hence risk) will not happen until DDD defaults on payment

>IBM WTC >DCT

>IBM HK

>ANZ

XYZ >DDD

XYZ

Regional

>1. Order

>2. Ship & invoice

3. A/R Assignment and intra company

settlement

5. Payments by remittance to XYZ

Regional

Bank

4. Master Risk Participation

>Agreement

7. If DCT defaults, A/R assignment to ANZ

8. Bank claim on

receivables

against DCT

6. Settlement

Case Study 3 – Receivables solution with traditional trade tool

Supplier: AAA Trading Company – trading company of surface mount technology (SMT)

machines in Asia

Buyer: HH Electronics – leading electronic product manufacturer

Facility Size: over USD40M

Objective: obtain finance leveraging on the buyer’s strengths to settle own import of product under letter of credits

Key points of interest:

> A receivables solution combining a letter of credit operation for AAA’s purchase of end products

- LC is issued to ultimate supplier upon AAA’s signing of contract with HH

- finance (upto its cost of purchase) is provided to AAA to allow its settlement of the LC outstanding

> Quality and reputation of the ultimate supplier is also key to the success of the solution

HH Electro

nics

4. Shipment of goods

(7)

Paym

ent a

t

mat

ur

ity

Supplier

1.

Order

AAA Trading

3. L/C

issued5. Drawdown for 85% invoice

2. Order (L/C)

6. LC

Settlement

bank

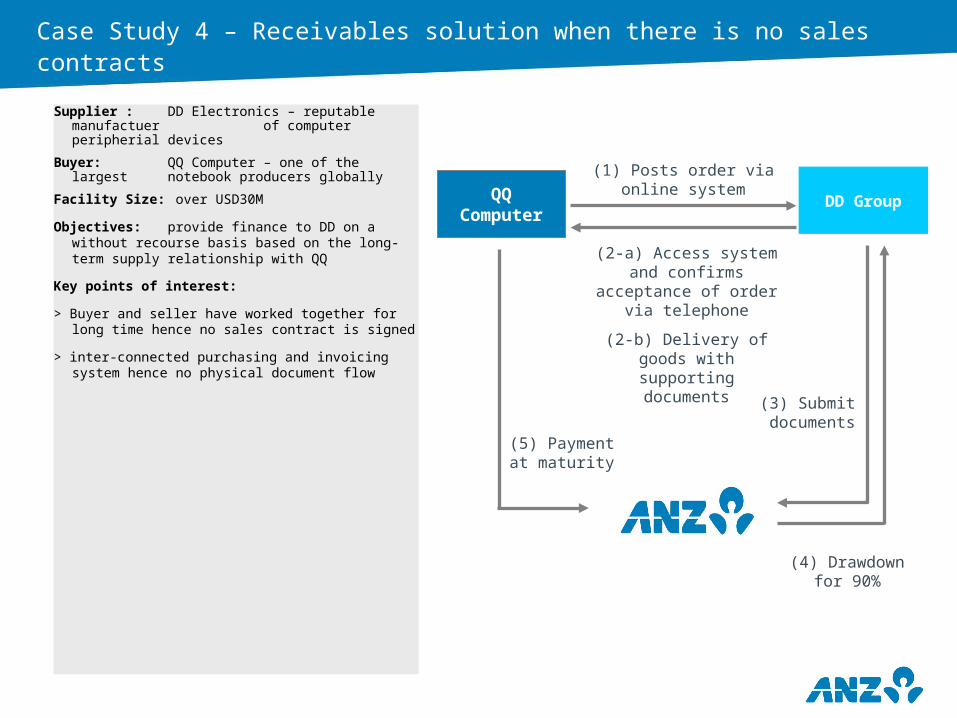

Case Study 4 – Receivables solution when there is no sales contracts

Supplier : DD Electronics – reputable manufactuer of computer peripherial devices

Buyer: QQ Computer – one of the largest notebook producers globally

Facility Size: over USD30M

Objectives: provide finance to DD on a without recourse basis based on the long-term supply relationship with QQ

Key points of interest:

> Buyer and seller have worked together for long time hence no sales contract is signed

> inter-connected purchasing and invoicing system hence no physical document flow

DD GroupQQ Compute

r

(2-a) Access system and confirms

acceptance of order via telephone

(2-b) Delivery of goods with supporting

documents

(3) Submit documents

(4) Drawdown for

90%

(5) Payment at maturity

(1) Posts order via online system

How do I get started?

> Look at your company’s balance sheet and profit & loss account

—Do you find your receivables / payables too large and want to trim it down or maintain it while sales grows?

—Do you find your gross profit margin under pressure and want to improve / maintain?

—Do you find your finance cost a bit and want to reduce it?

—Select those largest, most critical payables and receivables as a start by understanding the credit terms and settlement arrangements

> Talk to your purchasing departments

—Review purchase contracts with key suppliers and discuss the purchasing process

—Establish purchasing objectives: better purchase price? secure long-term supply? reduce payment pressure?

—Ask them to talk to the suppliers

> Talk to your sales departments

—Review sales contracts with key buyers and discuss the sales process

—Establish sales objectives: grow sales by better credit terms? Control exposure to key buyers while sales are growing?

—Understand the settlement record of your key buyers and their financial strengths?

—Ask them to talk to their buyers if they are willing to allow your assignment of receivables to bank

Just to re-cap….

>The physical supply chain of your company is also an important source for you to extract values

>Financial supply chain is not just about financing, it is also about balance sheet and risk management

>A supply chain solution is not an off-the-shelf product offered by banks. It is developed highly dependent on your company’s physical supply chain

>A capable bank should pay attention to your company’s physical supply chain in order to develop a solution that suits you

>Developing a supply chain solution requires the involvements of various departments within your company and it takes time; start from your largest or most critical receivables / payables, ie suppliers / buyers and get them prepared to talk to your bank

Benjamin Lam

Head of Trade and Supply Chain China

T. +86 21 6169 6308 E. [email protected]

Yen Poon

Head of Business Development

Trade and Supply Chain China

T. +86 21 6169 6123 E. [email protected]

Contacts

DISCLAIMER AND CONFIDENTIALITY

> This communication is issued on the basis that it is only for the information of the particular person to whom it is provided. This communication may not be reproduced, distributed or published by any recipient for any purpose. Nothing in this communication constitutes a representation that any product or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. This communication does not take into account your personal needs and financial circumstances. Under no circumstances is this communication to be used or considered as an offer to sell, or a solicitation of an offer to buy. The recipient should seek its own financial, legal credit, tax and other relevant advice and should independently verify the accuracy of the information contained in this communication .

> The author makes no representation as to its accuracy or completeness and the information should not be relied upon as such. All opinions and estimates herein reflect the author’s judgement on the date of this document and are subject to change without notice. ANZ, their affiliated companies, their respective directors, officers, and employees disclaim any responsibility, and shall not be liable, for any loss, damage, claim, liability, proceedings, cost or expense (“Liability”) arising directly or indirectly (and whether in tort (including negligence), contract, equity or otherwise) out of or in connection with the contents of and/or any omissions from this communication except where a Liability is made non-excludable by applicable law.

> If this communication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of this publication, which may arise as a result of electronic transmission.

> Please refer to the relevant product terms and conditions for full information relating to the products and services mentioned in this communication.

![[Lam cha, lam me] Cach dong vien con](https://static.fdocuments.net/doc/165x107/558cf3e1d8b42a7c0f8b4602/lam-cha-lam-me-cach-dong-vien-con.jpg)

![PROSEMINAR: MODELLBASIERTE ......Symposium on Software Testing and Analysis (ISSTA '11). ACM, New York, NY, USA, 320-330.] [V. Benjamin Livshits and Monica S. Lam. 2005. Finding security](https://static.fdocuments.net/doc/165x107/602056be5c80ce1e903d2c5a/proseminar-modellbasierte-symposium-on-software-testing-and-analysis-issta.jpg)