Financial Stability in the Insurance SectorFinancial .../media/internet/content/dateien... ·...

44

Financial Stability in the Insurance Sector Financial Stability in the Insurance Sector Prof. Dr. Hato Schmeiser [email protected] July 2009

Transcript of Financial Stability in the Insurance SectorFinancial .../media/internet/content/dateien... ·...

Financial Stability in the Insurance SectorFinancial Stability in the Insurance Sector

Prof. Dr. Hato Schmeiser [email protected]

July 2009

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 2

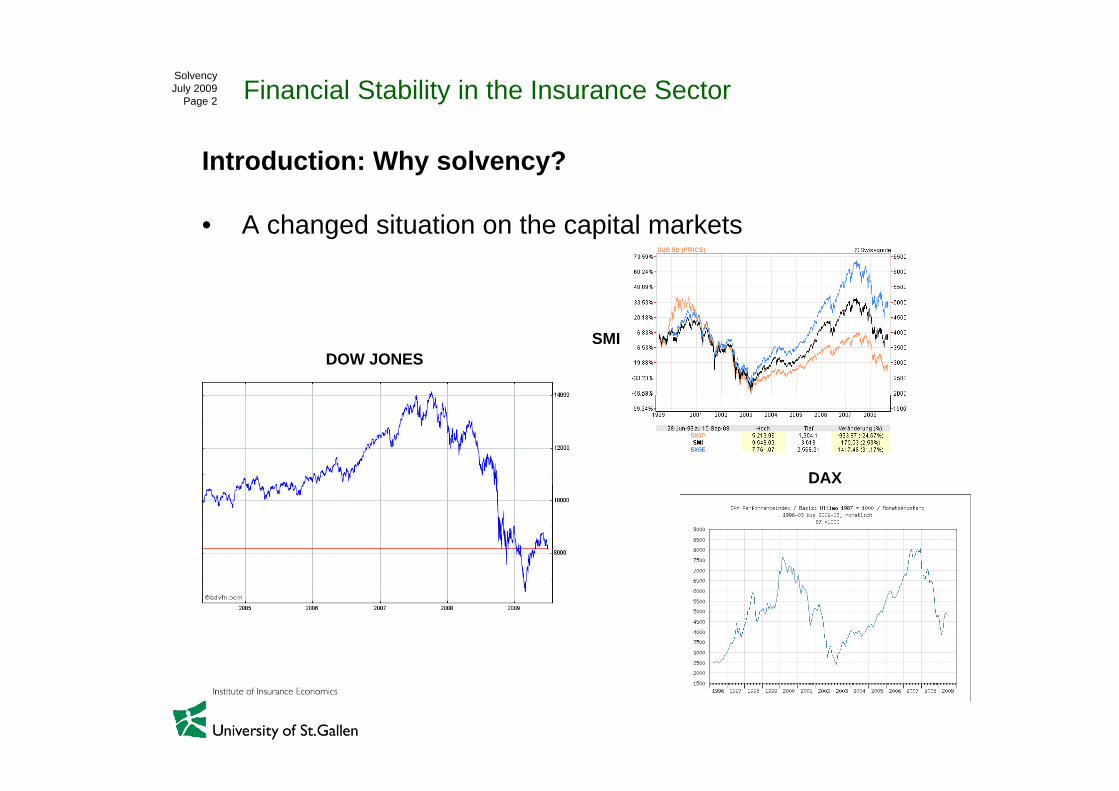

Introduction: Why solvency?

A h d it ti th it l k t• A changed situation on the capital markets

DOW JONESSMI

DAX

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 3

• Low interest rates (e.g., CH, Germany)

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 4

• A changed policyholder's value proposition

- Lower loyalty to present insurer

- Increased price sensitivityp y

- Better informed customers

- Intensified competition with stronger consumer advertising

New distribution channels (internet platform other financial ser- New distribution channels (internet platform, other financial ser-vice providers, etc.)

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 5

Financial crises and Insurance

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 6

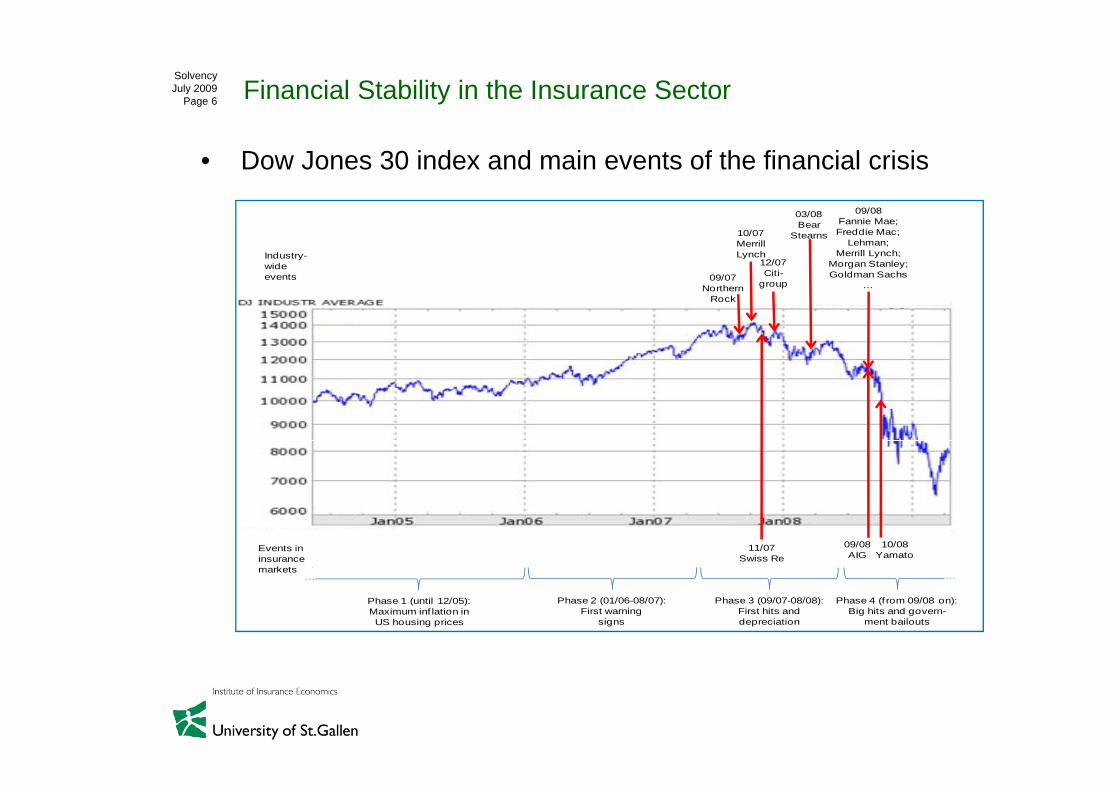

• Dow Jones 30 index and main events of the financial crisis

09/0803/08Fannie Mae; Freddie Mac;

Lehman;Merrill Lynch;

Morgan Stanley; Goldman Sachs

…

Industry-wideevents

10/07MerrillLynch

12/07Citi-

group09/07

Northern Rock

03/08Bear

Stearns

09/08AIG

11/07Swiss Re

10/08Yamato

Events ininsurancemarkets

Phase 3 (09/07-08/08): First hits anddepreciation

Phase 4 (f rom 09/08 on): Big hits and govern-

ment bailouts

Phase 2 (01/06-08/07): First warning

signs

Phase 1 (until 12/05): Maximum inf lation in US housing prices

……

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 7

• Estimates by IMF

- Losses from current market turmoil estimated to around1'405 Billion USD

- Depreciations in the banking sector of worldwide 700 BillionUSD

- Necessary capital for the banking system in the next years:675 Billion USD675 Billion USD

- Worldwide losses of insurance companies are estimated to150 Billion USD (realized and non-realized losses)

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 8

• Reasons

- Propensity to consume and global financing policy of theU.S.?

- Intransparent cross-linked capital markets?

- Incentive structures in corporations led by managers?

- Stochastic models and their interpretation?Stochastic models and their interpretation?….

S f- Search for "culprit"

Financial Stability in the Insurance SectorSolvencyJuly 2009

Page 9

• Model risk

- Stochastic models are all about probabilities

Typically only the pure randomness is modeled- Typically only the pure randomness is modeled

- Stochastic phenomena stay stochastic (with or without risk mo-deling)

- Using similar models (IFRS Solvency II etc ) forces systemicUsing similar models (IFRS, Solvency II etc.) forces systemicrisk within the market

"All models are wrong, some models are useful"George E. Box, born 1919

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 10

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 11

• Crises in the insurance industry

- AIG

September 16th 2008: Liquidity crisisSeptember 16th 2008: Liquidity crisiswith a downgrade of its credit rating

Sh i h d f ll 95% tShare price had fallen over 95% to1.25 USD on September 16th 2008

Federal Reserve Bank: First rescue package of 85 Billion USD(up to now: 182 Billion USD)

Largest government bailout of a private company in U.S. history

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 12

• Crises in the insurance industry

AIG- AIG

Report of nearly 62 Billion USD loss in the fourth quarter of2008 (largest quarterly loss in corporate history)

Corporate loss in 2008:palmost 100 Billion USD

March 2009: AIG announcedMarch 2009: AIG announcedpay outs of 165 Million USDin executive bonuses(bonuses for the entire(bonuses for the entirecompany could reach morethan 1 Billion USD)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 13

• Crises in the insurance industry

- Mannheimer Lebensversicherung

Highly stock oriented

DAX merely accounted 2‘200 points in 2003 (now: 5‘000)

Hidden liabilities

At the end: Absorption of the company by the Protektor AGAt the end: Absorption of the company by the Protektor-AG(safety institution financed by German life insurers)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 14

• Crises in the insurance industry (continued):

- Equitable Life

England´s oldest life insurer (founded 1762)

Too high annuity guarantees had been promised to policyhol-ders

In addition: Guarantees have been insufficiently hedged

( ff )In December 2002, the business line was closed ("run-off")

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 15

• Solvency regulation has a special importance in the insurancesector:

I l f i l d t " i " f thInsolvency of an insurance company can lead to "ruin" of thepolicyholder

Safety level of the insurance company directly influences theproduct qualityp q y

Willingness to pay reacts extremely sensitive to variations ofthe safety level of the insurance company

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 16

• Why solvency regulations?

"Risk incentive problem"

- Starting point: Current EU and CH regulations (update isStarting point: Current EU and CH regulations (update iscalled "Solvency I") unsatisfactory for deriving minimum equitycapital requirement

• Example Solvency I (P/L Insurer)

Minimum Capital Requirements (MCR): 23% / 26% * Net-Claims ("loss index")

MCR < current equity capital (based on balance sheet)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 17

Solvency – An overview

Source: Eling Schmeiser Schmit RMIR 2007Source: Eling, Schmeiser, Schmit, RMIR 2007

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 18

Solvency II – Objectives and current development status

• Objectives of Solvency II• Objectives of Solvency II

Development of solvency standards which are applicable in allt i d EU l i f i titi ithi th icountries under EU law; aim: fair competition within the insur-

ance market

Risk-oriented determination of the minimum equity capital re-quirement

Improvement of risk management in insurance companies

Inclusion of qualitative aspects in the supervision processInclusion of qualitative aspects in the supervision process

Creation of incentives to develop internal risk models

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 19

• Solvency II time table

- 2003: End of "discussion stage"

- 2004-2011: Development of a detailed supervisory system- 2004-2011: Development of a detailed supervisory systeminfluencing:

Equity capital requirements- Equity capital requirements- Capital investment policy- Product policy

R i li- Reinsurance policy- Underwriting policy of the insurer

- 2012 (?): Completion of the legislative procedure

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 20

• Following Basel II: "three-pillar structure"

- First pillar: equity capital requirement, capital investment,assessment of claim reserves

- "Two level approach":

1 Definition of an absolute minimum capital (based on1. Definition of an absolute minimum capital (based on"Solvency I")

2 Definition of a target capital by means of a

MCR = Minimum Capital Requirements

2. Definition of a target capital by means of a

standard approach or by means of an

internal risk model SCR = Solvency Capital Requirements (Target Capital)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 21

• Standard approach

- The standard approach is meant to adequately display therisk situation of the majority of insurance companies

- The approach must be applicable independent of companysize or legal structure

- In the meantime, various design options for a standard modelhave been tested:

Practicability of calculationsAssessment of possible effects on balance sheetEvaluation of the applicability of the different models discusEvaluation of the applicability of the different models discus-sed so far by the participants of the field test

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 22

• Internal solvency models

- Standard approach can be substituted by internal models

- Alternative of a partial substitution is presently discussedAlternative of a partial substitution is presently discussed

- Accreditation by supervisory authority necessary

- Sustainable internal risk model fulfills many wishes for insur-ance companies:

External solvency verificationInternal risk and profit controlC SCorporate governance regulation in Switzerland…

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 23

• Supposed capital requirements depending on the modelingapproachpp

Graduated intervention by the supervision

Solvency Capital Requirement SCR

Minimum Capital Requirement

MCR

Internal risk modelInternal risk model

Standard approach

Amount of equity capitalAmount of equity capital

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 24

• Summary

1st pillar

Two-level approach

2nd pillar

Control by the

3rd pillar

Market discipline

• Minimum Capital

• Solvency capital

supervision

• Accreditation• Market transparency

• DisclosureSolvency capital

- Internal models:Lower

i t ?

• Review processDisclosure

- In principle:requirements?

- Impulses for the risk management of the insurance

- Organizational consequences?

product rating

- Problematicof the insurance company? - Reregulation?

Problematicincentive effects?

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 25

Workshop (4 groups, 10 minutes)

• Financial Stability and Insurance

What are the main reasons leading to the- What are the main reasons leading to thecurrent financial crisis?

Wh t l t b l d f th- What are lessons to be learned from thefinancial crisis?

- In which way can or should (solvency) regulation help to in-crease the stability and credibility of the insurance business?

- Why are insurance companies on average less effected by thecurrent financial crisis compared to the banking industry?

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 26

Swiss Solvency Test (SST)

• Time table:

2003: Start of the SST project2004: Field test with 10 insurance companies2005: Field test with 45 insurance companies2006: Commencement of the new supervisory provision

(Solvency I persists)(Solvency I persists)2006: Mandatory field test (Exceptions: SME)2008: Application of the SST in all insurance companies2011: Capital requirements have to be met

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 27

• Application area of the SST

Insurance companies based in Switzerland in case they areunder the control of the FINMA (CH regulator)

To apply to life / non-life / reinsurance

• Time horizon: 1 year• Time horizon: 1 year

• Models differ for life / non-life / health insurance

• Deduction of SCR plus SST report

• MCR is provided by the Solvency I rules whereas SCR >• MCR is provided by the Solvency I rules, whereas SCR >MCR

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 28

• Principle-based supervision

- 14 principles describe the objectives of the supervision andgive basic definitions

- Regulatory authority provides standard models

- Companies shall (or must) employ individually customizedinternal models to determine the particular Solvency Capitalinternal models to determine the particular Solvency CapitalRequirement SCR

- Reinsurers have to utilize internal risk models

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 29

• Basis

- Combination of factor model and scenario model

- Basic quantities:

RBC0 ("risk-bearing capital", actual size t = 0) and SCR0 ( g p , )

- Requirement: RBC0 > SCR

- SCR results from the modeling of the RBC (in one year) as adistribution function and by specification of a risk measure(Tail Value at Risk)(Tail-Value-at-Risk)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 30

Market Consistent Data

Standard Models or Internal Models

Mix of predefined and company

specific scenarios

ScenariosMarket RiskCredit Risk

N lif

Market Value AssetsRisk Models Valuation Models

B t E ti tNonlife Best Estimate Liabilities

MVM

O t t f l ti l d l (Di t ib ti )

LifeHealth

Aggregation Method

Output of analytical models (Distribution)

RBC, SCR and SST Report

Source: FINMA

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 31

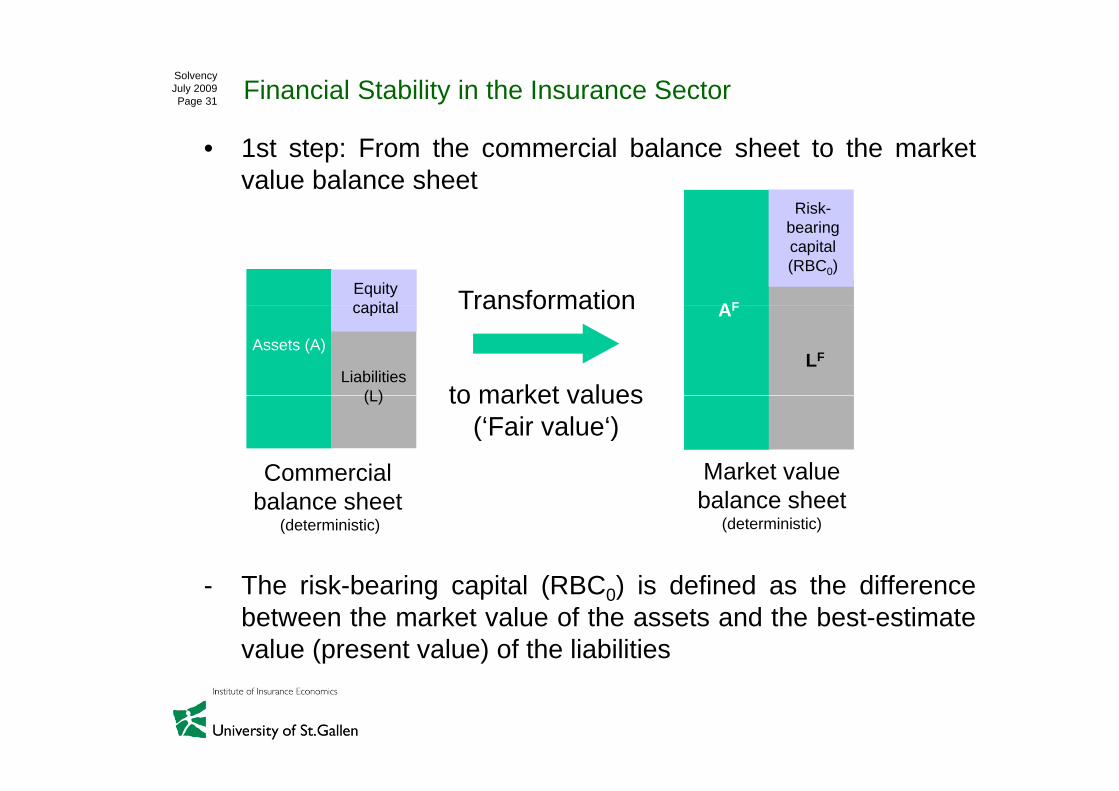

• 1st step: From the commercial balance sheet to the marketvalue balance sheet

Risk-

TransformationEquity capital AF

bearing capital (RBC0)

Transformation

to market values

Assets (A)

capital

Liabilities (L)

AF

LF

to market values(‘Fair value‘)

Commercial Market value

(L)

( C ) f ff

balance sheet(deterministic)

balance sheet(deterministic)

- The risk-bearing capital (RBC0) is defined as the differencebetween the market value of the assets and the best-estimatevalue (present value) of the liabilities

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 32

• 2nd step: From the presence view to the future

based on expected values

AF

RBC0

TransformationE(A1

F )

E(RBC1 )

A

LF to a future view

E(A1 )

E(L1F )

Market value balance sheet

Market value balance sheetbalance sheet

todaybalance sheet

in one year (deterministic)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 33

• 3rd step: From the deterministic to the stochastic future view

~

A1F

~

RBC1RBC1

A1F

~

~~

L1F

~~L1

F

Market value balance sheet

Aggregated variation of RBCbalance sheet

in one year (stochastic)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 34

Distribution RBC in t = 1

• 4th step: Comparison of RBC with SCR

RBC~

RBC in t 1

MB

A1F

~

RBC1

A1F

~TVAR

L1F

~~L1

F

Market value balance sheet in one year

(stochastic)

Aggregated variation of RBC

TVAR Ri k "T il V l t Ri k" b d di t ib ti f th RBC i t 1 (1% l l)TVAR = Risk measure "Tail-Value-at-Risk" based on distribution of the RBC in t = 1 (1% level)MB = Minimum amount (run-off costs in case of an insolvency)SCR = TVAR + MB

RBC0 > SCR Requirement0 q

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 35

1 1 01

1= −

+F FX RBC RBC

r

= F FRBC A L1 1 1= −RBC A L

( )1% 1 1TVAR E X X VaRα α= = − ≤

( ) ( ){ }1 inf : 1%F x F xα α− = ≥ =

1%SCR TVAR MBα== +

eory

For formula lovers: The SST at a glance

VaR1%

0 0 0F F FRBC A L SCR= − >.

The

VaR1%

TVAR ( )f x

RBC1Expected value

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 36

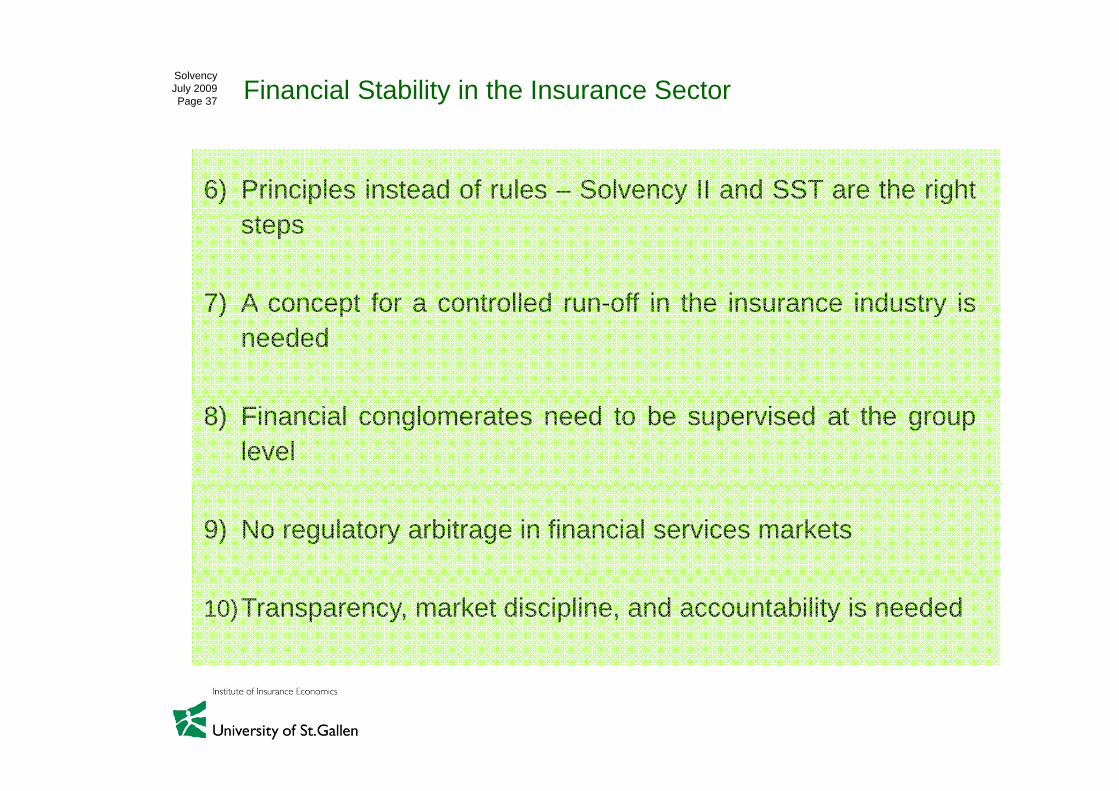

Insurance and the credit crisis: Ten Consequences for RiskManagement and Supervisiong p

1) We need to strengthen risk management and supervision

2) We need to take care of model risk and non-linearities

3) We need easy to use and understandable risk management

4) Right incentives are needed

5) T k f th l f tf li th Ri k t5) Take care of the lessons from portfolio theory – Risk, return,and diversification

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 37

6) Principles instead of rules – Solvency II and SST are the righttsteps

7) A concept for a controlled run-off in the insurance industry is7) A concept for a controlled run-off in the insurance industry isneeded

8) Financial conglomerates need to be supervised at the grouplevel

9) No regulatory arbitrage in financial services markets

10)Transparency, market discipline, and accountability is needed

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 38

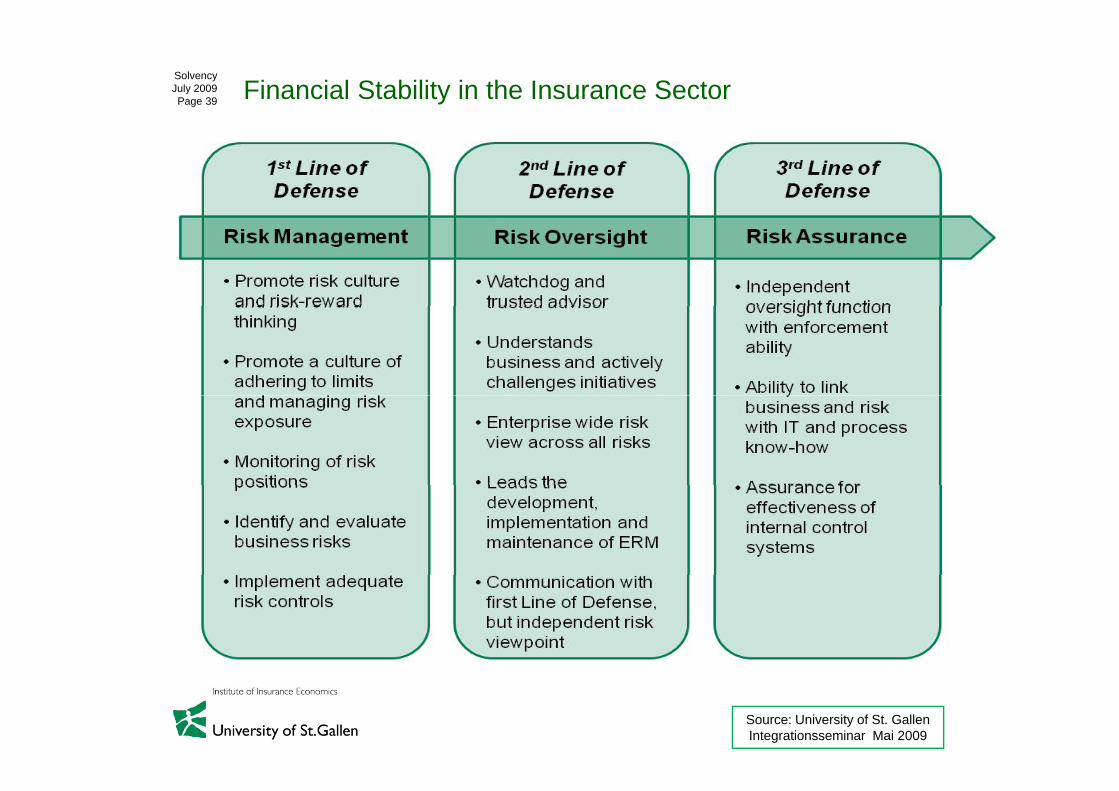

Enterprise Risk Management ERM

Source: University of St. GallenIntegrationsseminar Mai 2009

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 39

Enterprise Risk Management

Source: University of St. GallenIntegrationsseminar Mai 2009

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 40

• Complex system within the ERM

C it l i k t f i t t (CRTI ) b t t- Capital risk transfer instruments (CRTIs) between parent com-panies and subsidiaries (AIG had 4.000 subsidiaries!)

Fungible capital

Intra-group retrocession, contingent capital issued and received, etc.

Parent Company

Fungible capital

Legal Entity 2Legal Entity 1

Parent CompanyMarket Value Margin

- New rules for group supervision in the EU (Solvency II) andCH (Group SST)

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 41

• Consequence: Growing relevance of enterprise risk manage-ment, in particular in insurance groups

- Prevention of a mere "silo risk management"

- Recording and valuation of group-internal finance and risktransfer

- Establishment of transparency, particularly in complex riskstructures

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 42

Conclusion

• Solvency situation of the insurer represents significant qualitycharacteristic for the product “insurance”

• In the future, financial situation will become more transparentand thus an important competitive factorp p

• Current credit crisis demands a review of traditional risk ma-nagement toolsnagement tools

Thank you very much for your attention

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 43

Financial Stability in the Insurance SectorSolvencyJuly 2009Page 44

• Kontakt

Prof. Dr. Hato SchmeiserU i ität St G llUniversität St. Gallen Kirchlistrasse 2 CH - 9010 St. Gallen Telefon: +41 (0)71 243 40 [email protected]