Financial Services & Insurance: The Long March Insurance Information Institute December 2001 If...

87

Financial Services & Insurance: The Long March Insurance Information Institute December 2001 If you’d like a copy of this presentation, I will be happy to e-mail it to you Robert P. Hartwig, Ph.D. Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

-

Upload

neil-thomas -

Category

Documents

-

view

213 -

download

0

Transcript of Financial Services & Insurance: The Long March Insurance Information Institute December 2001 If...

Financial Services & Insurance: The Long March

Insurance Information InstituteDecember 2001

If you’d like a copy of this presentation, I will be happy to e-mail it to you

Robert P. Hartwig, Ph.D. Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Presentation Outline• Financial Services—What’s Happening Today?

• Who’s the Competition?

• Why Bother Getting into Financial Services?

• What’s Hot?

• Lessons from Banks’ Experience with Insurance

• Does the Internet Make a Difference?

• Your Bread & Butter: Investing, Estate & Retirement Planning

• The Economy

• Q&A

CONVERGENCE CREATES OPTIONS & OPPORTUNITIES FOR BANKS AND INSURERS

% Non-Life Insurers Planning to Widen Fin’l. Services Operations

17.2%

58.1%

8.6%4.5%

8.6%13.6%

28.3%

16.7%13.1%

26.3%

0%

10%

20%

30%

40%

50%

60%

70%

InsuranceServices

Insurance Alliances withBank/AssetManagers

Ownership ofBanks/AssetManagers

FinancialServices

Conglomerate

Today

2005

Source: EIU/Pricewaterhouse Coopers; December 2000.

Is moreConglomeration

in store?

Applications for Thrift Charters, by Industry

Telecom1%

Retail5%Insurance

53%

Trade Group5%

Mfg.8%

Misc.10%

SecuritiesBroker/Dealers

18%

January 1, 1997 – May 1, 2001 (220 Applications)

Source: Office of Thrift Supervision

World’s Largest Financial Services Firms, 2000

*EstimateSource: Fortune

$129.9

$111.8

$92.8

$71.2 $71.0

$0

$20

$40

$60

$80

$100

$120

$140

General Electric Citigroup AXA ING Group Allianz

$ Millions

Top 10 Bank Holding Companies (2000, $ Billions)

Source: Board of Governors of the Federal Reserve; Insurance Information Institute.

$953.4

$712.7$625.5

$289.8 $272.4 $245.9 $216.5 $202.1 $165.2 $164.7

$0

$250

$500

$750

$1,000 $ Billions

Number of Bank Holding Cos. Formed Since GLB, (by FRB District)*

*As of Aug. 10, 2001.; GLB signed into law Nov. 1999.Source: Board of Governors of the Federal Reserve; Insurance Information Institute.

13

44

26

49

29

85

68

4437

89

42 42

$0

$20

$40

$60

$80

$100

Dallas district holding companies have smallest asset base of all 12 districts!!

Financial Assets by Sector

1990 vs. 2000 ($Billions)

608

2,644

1,351

556

6,406 6,492

3,139

1,217880

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Mutual Funds* CommercialBanks

Life Insurers Securities Non-LifeInsurers

1990 2000

*Includes closed-end funds.Source: Federal Reserve, Insurance Information Institute

The Mating Dance

Wave of the Future?

Know Thy Enemy

Top 10 P/C Insurers: TX & US(2000)

Texas NWP US NWPState Farm $3,125.1 State Farm $33.3Allstate 1,997.8 Allstate 21.6Farmers 1,956.6 Zurich/Farmers 16.8AIG 817.5 AIG 12.2USAA 776.9 Berk. Hathaway 10.4Travelers 695.4 Travelers/Citi 9.9Progressive 532.6 Nationwide 9.5Continental 441.5 Liberty 8.7Liberty 403.8 C N A 8.1Hartford 401.9 Hartford 6.9

Top 10 Life/Health Insurance Groups & Cos., (2000, US Market)

*EstimateSource: Insurance Services Office, Insurance Information Institute.

$30.6

$24.0 $23.5 $23.0

$18.6 $18.2 $17.5 $17.0 $15.6 $14.4

$0

$5

$10

$15

$20

$25

$30

$35

Met

Life ING

AIG

Aegon

USA

Hartfo

rd L

ife

Nation

wide

CIGNA

Pruden

tial

Princip

al L

ife

New Y

ork L

ife

$ Billions

Top 10 Global Life Insurance Companies, (2000)

Source: Fortune, Insurance Information Institute.

$92.8

$71.2 $68.1$61.5

$53.3$46.4 $43.1

$38.1 $37.5$31.9

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100 $ Billions

Top 10 Writers of Annuities, 2000

*EstimateSource: Insurance Services Office, Insurance Information Institute.

$9.5

$7.1 $6.7 $6.5$5.9 $5.4 $5.3 $5.3 $4.9 $4.9

$0

$2

$4

$6

$8

$10

Hartfo

rd L

ife

Amer

ican G

ener

al

Citigr

oup

Aegon

USA

GE Fin

ancia

l

Met

Life

Nation

wide

TIAA G

roup

ING

Gro

up

Amer

ican E

xpre

ss

$ Billions

Top 10 Securities Firms’ Revenue (2000)

Source: Fortune, Insurance Information Institute.

$45.4 $44.9

$33.0

$26.4

$10.3$7.1

$2.8 $2.3 $2.0 $1.7$0

$10

$20

$30

$40

$50 $ Billions

Top 10 Mutual Fund Cos. (Assets, 2000)

Source: Investment Company Institute, Insurance Information Institute.

$818.8

$574.3

$368.5

$242.6$191.7 $177.0 $176.6 $172.2 $171.7 $166.0

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900 $ Billions

Why Bother Getting into Financial Services?

0%

5%

10%

15%

20%

25%

US P/C Insurers All US Industries LifeDiversified Finl. Comm. Banks

ROE: Financial Services Industry Segments, 1987–2000*

* 2000 figures are estimates.Source: Insurance Information Institute

-2%

0%

2%

4%

6%

8%

10%

12%

14%

P/C Life

Source: A.M. Best, Insurance Information Institute

Growth in Premiums Written: P/C vs. Life/Annuity

*2000 est.; 2001 forecast from III Groundhog Survey

Life Growth Outpaces P/C

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

ROE Non-Life Cost of Capital

ROE vs. Cost of Capital: US Non-Life 1991 – 2000

Source: The Geneva Association, Insurance Information Institute.

Ranks of the “Best of Breed” are Thin

1999 Return on Equity (Profitability)

1.0%

2.8%

3.1%

5.5%

6.5%

7.4%

15.4%

0% 5% 10% 15% 20%

Fortune 500

PP Auto

US All P/C Lines

Workers Comp

Homeowners

Comm Multi Peril

Comm Auto

Source: NAIC, Insurance Information Institute

1999

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

ROE Life Cost of Capital

ROE vs. Cost of Capital: US Life Insurance 1992 – 2000

Source: The Geneva Association, Insurance Information Institute.

Ranks of the “Best of Breed” are thin among stock life insurers too, though not quite so bad.

Competition—Still Intense: Number of Insurers: 1970-2000

1095 1059

15751702

2406 2430 2485 2480 2455

1802 17461958

2261 2195

17151563

0

500

1,000

1,500

2,000

2,500

3,000

1970 1975 1980 1985 1990 1995 1998 1999 2000

Property/Casualty

Life/Health

Sources: P/C: A.M. Best; L/H: NAIC.

Impact of Recession on P/C Premiums and Profitability (1970-1999)

8.1%

5.4%

-2.7%

0.2%

3.9% 3.8%2.7%

4.1%

8.8%

4.7%

7.0%

8.9%9.4%

11.3%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Inflation (CPI) NWP Growth(unadj.)

Real NWPGrowth

ROE--P/CInsurers*

ROE--AllIndustries*

ROE--Banks* ROE--DiversifiedFinancial*

Recession Years (1970; 74-75; 80-82; 90-91)

Non-Recession Years (all other years, 1970-1999)

*GAAP return on equity, adjusted for inflation; Bank data 1952-99; Div. Fin. 1987-99Source: Insurance Information Institute

Source: New York Times Magazine, August 12, 2001

Source: New York Times Magazine, August 12, 2001

Source: New York Daily News, September 10, 2001

Financial Services Reform: The Reality so Far

• GLB: Signed by President Clinton Nov. 12, 1999• M&As: Little activity between banks and insurers.

Overall M&A activity ($ & #) down significantlyPartnerships popular (Travelers/Citi model not followed)Acquisition of agencies somewhat popular

• Impediments:Low ROEs (esp. on P/C side, but also Life)Regulatory uncertainties (fed vs. state regulation; privacy)Extraordinary economic/financial uncertainty

• Organic Growth:Many insurers have formed banks Has appeal for banks and insurers (e.g. State Farm)

• No federal chartering of insurers—yet

What’s Hot?

Value of Shares Traded, 1990- 2000 ($ Trillions)

Source:Securities Industry Association, Insurance Information Institute

1.3

1.5

1.8 2.3

2.5 3.1 4.

1 5.8 7.

3 9.0

11.1

0.5

0.7

0.9 1.4

1.5 2.

4 3.3 4.

5 5.8

11.0

20.4

0

5

10

15

20

25

90 91 92 93 94 95 96 97 98 99 00

NYSE NASDAQ

Number of Mutual Funds, 1985- 2000*

*Total also includes hybrid and money market funds.Source: Investment Company Institute, Insurance Information Institute

5791,100

2,140

4,395

382 4041,046

2,2101,527

3,081

5,728

8,171

0

3,000

6,000

9,000

1985 1990 1995 2000

Equity Bond Total

Principal Categories of Revenue Growth for Life Insurers

13.6%

18.5%

23.6%

24.1%

48.1%

72.0%

0% 20% 40% 60% 80%

Indiv. Annuities

All Lines

Ordinary Life

Indiv. A&H

Group A&H

Group Life

G ro u p L i f e

Source: AM Best

Percent Change from 1995 - 2000

Fixed Annuity Sales, Distribution Channel (2000)

Source: LIMRA.

1995

Stockbrocker10.0%

Banks21.0%Direct Resp.

1.0%Other3.0%

Ind. Agents38.0%

Career Agents27.0%

2000

Stockbrocker6.0%

Banks29.0%

Direct Resp.1.0%Other

4.0%

Ind. Agents47.0%

Career Agents13.0%

Variable Annuity Sales, Distribution Channel (2000)

Source: LIMRA.

1995

Stockbrocker30.0%

Banks7.0%

Direct Resp.14.0%

Other5.0%

Ind. Agents12.0%

Career Agents32.0%

2000

Stockbrocker41.0%

Banks10.0%

Direct Resp.8.0%Other

5.0%

Ind. Agents11.0%

Career Agents25.0%

Annuities: Too Many Eggs in One Basket?

“C N A To Cut Staff 11%; Charges To Be Taken”

--Wall Street Journal, December 6, 2001

Will cut 1,850 jobs (600 at Chicago HQ)

Discontinue variable life and annuity business

Take charge up to $174 million (2/3 for restructuring)

Reduce number of offices from 169 to 68

What are the Banks Doing?

Bank Distribution Channels for P/C Insurance

4.3%

15.4%

17.4%

21.7%

27.7%

0% 5% 10% 15% 20% 25% 30%

Agents in Banks

Direct Mail

Telemarketing

Bank/platform empl

Securities/Inv Grp

Source: American Bankers Insurance Association, Insurance Information Institute

2000

1998 Bank Insurance Premiums

Other1%

Annuities$19.6 billion

63%

Life$1.5 billion

5%

Personal$2.9 billion

9%

Commercial$4.0 billion

13%

Credit$2.9 billion

9%

Total = $31.1 Billion

1999 Bank Insurance Premiums

Other$0.3 billion

1%

Indiv. Life$0.7 billion

2%

Annuities$24.2 billion

66%

Indiv. Health/Dis$1.1 billion

3%

Personal$3.1 billion

8%

Commercial$4.4 billion

12%

Credit$2.9 billion

8%

Total = $36.7 Billion

Source: American Bankers Insurance Association, Insurance Information Institute.

2000 Bank Insurance Premiums

Annuities$31.0 billion

66%

Indiv. Health/Dis$2.1 billion

3%

Personal$3.7 billion

8%

Commercial$5.4 billion

12%

Credit$2.7 billion

8%

Total = $44.9 Billion

Annuity Sales through Banks, 2000

3.7 4.1 3.9 4.1

3.94.4

4.0 3.7

$7.8$7.9

$8.5

$7.6B

$0

$3

$6

$9

1Q 2Q 3Q 4Q

($ in billions)

Fixed Variable

Source: Kenneth Kehrer & Associates/American Banker

Bank Sales of Mutual Funds

$19.2

$33.0

$41.0

$46.3 $45.5

$40.0

$0

$10

$20

$30

$40

$50

1995 1996 1997 1998 1999 2000

$ Billions

Source: Kenneth Kehrer Associates, Insurance Information Institute.

WHY MOST BANKS FAIL AT SELLING INSURANCE

Bankers Hours?Image Problem

Why Most Banks Fail in Insurance

• Short-Term Thinking

Stick with it

• Failure to Think Strategically

Need to focus on customers’ insurance needs

• Putting a Banker in Charge

Specialized expertise important

Source: American Banker, January 19, 2001.

Why Most Banks Fail in Insurance (cont’d)

• Neglecting Cultural Issues

Europeans successful at cultural integration

• Ignoring Commercial Market

Especially middle market

What Can We Expect?

• More Partnerships

• Major Insurers Focus on Organic Growth

• Europeans:

Dominant, Aggressive, Experienced

• CEOs Focused and Distracted by Other Issues

Profits, disasters, economy

• Many Banks/Insurers struggling with “core issues”

Does the Internet Make a Difference?

Shifting Distribution Channels: Property/Casualty Insurers

Source: Datamonitor

20031998

Direct Response

10.0%Banks8.1%

Interne t7.3%

Other2.5%

Independent Agents23.3%

Captive Agents48.8%

Direct Response

9.8%Banks2.8%

Interne t0.9%

Other3.0%

Independent Agents27.0%

Captive Agents56.5%

Projected Online Sales of Auto, Home & Term Life Insurance

0

500

1000

1500

2000

2500

3000

3500

Auto Home Term Life

1998

1999

2000

2001

2002

2003

Source: Forrester Research

$ Millions

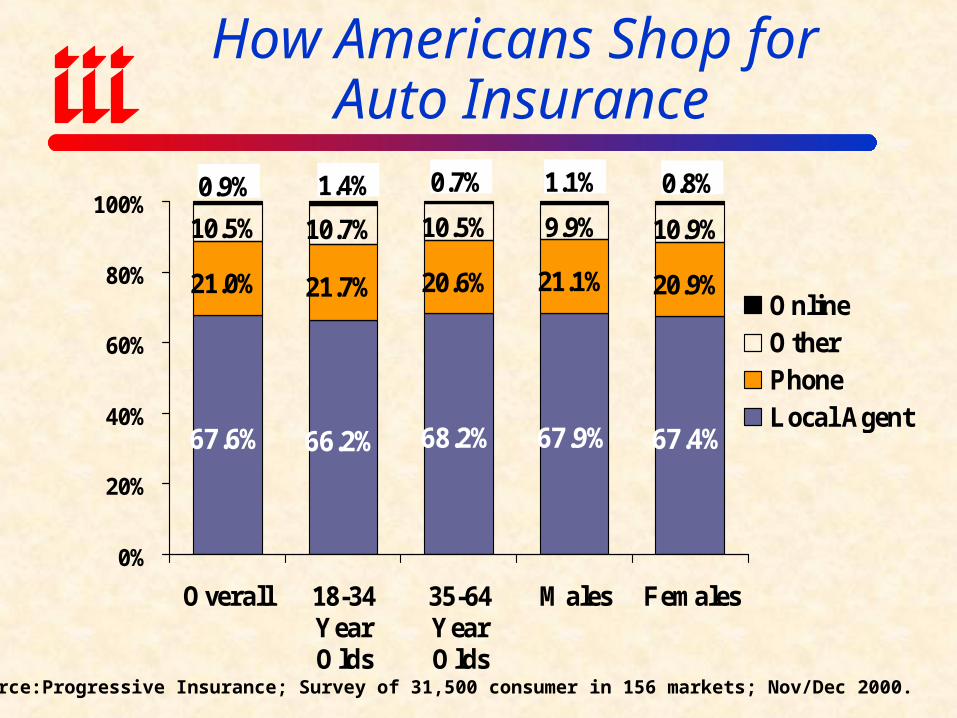

How Americans Shop for Auto Insurance

67.6% 66.2% 68.2% 67.9% 67.4%

21.0% 21.7% 20.6% 21.1% 20.9%

10.5% 10.7% 10.5% 9.9% 10.9%

0.8%1.1%0.7%1.4%0.9%

0%

20%

40%

60%

80%

100%

Overall 18-34YearOlds

35-64YearOlds

Males Females

OnlineOtherPhoneLocal Agent

Source:Progressive Insurance; Survey of 31,500 consumer in 156 markets; Nov/Dec 2000.

Interest in 1-Stop Shopping Concept

61%

74%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Single-Source Supermarket Either Option

Source: Bank Administration Institute,; Cambridge Group; as of February 2000.

High interest in use online financial services online

% On-Line Customers Conducting Selected Transactions

1%2%

4% 4%

8%

10%11%

12%13%

0%2%4%6%8%

10%12%14%

Source: Bank Administration Institute,; Cambridge Group; as of February 2000.

Use of financial services online lags expectations

6-Month Change in Number of E-Distribution Start-Ups

0

10

20

30

40

50Aug. 2000

Feb. 2001

Source: Conning

Distribution Channels Continue to Proliferate

Customer InsurerAgent Broker

Mail Telephone

Bank

Internet Dealerships Payroll Plans

Stock Exchanges

Online Auctions

????

Insurers: Tangled in the Web?

Leading Insurers Selling Life Ins. Through Banks

Source: Kenneth Kehrer Associates, Insurance Information Institute.

$50.

9

$27.

1

$20.

8

$8.7

$31.

1

$12.

3

$16.

1

$39.

5

$17.

1

$6.1

$56.

8

$47.

7

$36.

4

$35.

1

$28.

7

$24.

7

$20.

9

$20.

2

$17.

8

$10.

0

$0

$10

$20

$30

$40

$50

$60

1999 2000

$ Millions

Employment in Banking Sector, 1991- 2000

Source: Bureau of Labor Statistics, Insurance Information Institute.

1,5291,466 1,430

382276 253

135 156 194

0

200

400

600

800

1,000

1,200

1,400

1,600

1991 1995 2000

(Thousands)

Investing

Investing: Rewards but Many Pitfalls

• Agent often has inside track on major life events (banks don’t)

• Appropriate advice: Assessing the customer’s needs

90 year olds don’t need annuities (it’s happened)

• Bad advice can ruin a relationship and cost you the customer’s p/c and life business

too

• Decision on what to push can’t be entirely commission-driven

E.g., tech funds pushed aggressively until tech bubble burst

Better of with dollar cost averaging, but commission not as good

• Knowledge Gap: LT market performance, stocks v. bonds, interest rates, FX, GDP,

CPI, M&A

• Impact of economy on performance

-30%

-20%

-10%

0%

10%

20%

30%

40%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

Large Company Stocks*As of December 5, 2001.Source: Ibbotson Associates, Insurance Information Institute

Total Returns for Large Company Stocks: 1970-2001

2001*

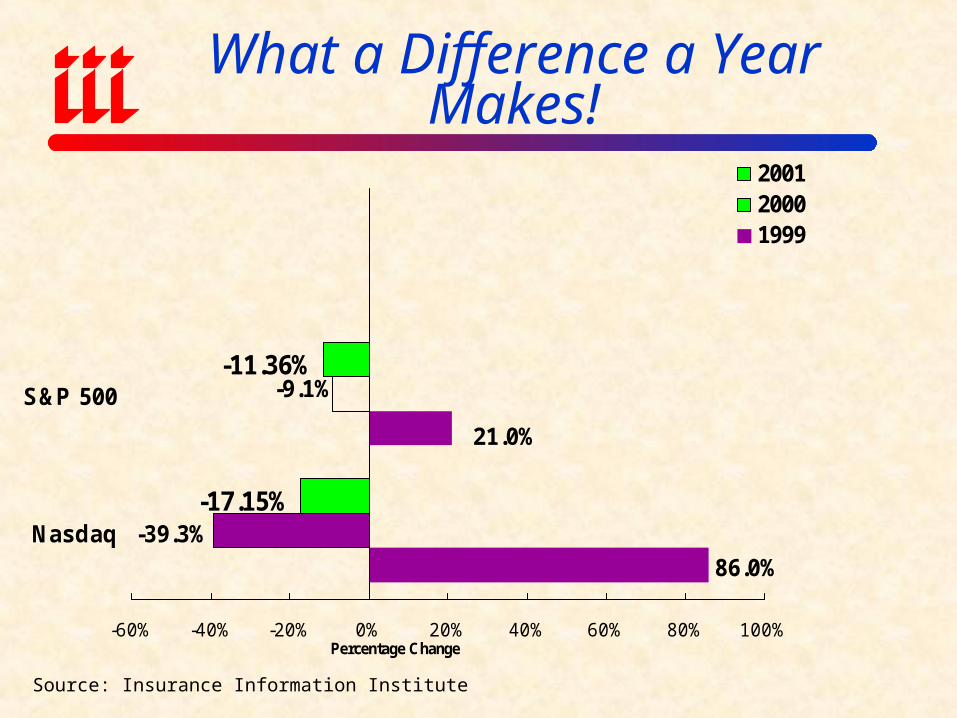

What a Difference a Year Makes!

86.0%

-17.15%

-11.36%

21.0%

-39.3%

-9.1%

-60% -40% -20% 0% 20% 40% 60% 80% 100%

Nasdaq

S&P 500

Percentage Change

200120001999

Source: Insurance Information Institute

Security Broker & Dealer Employment, 1991- 2000

Source: Bureau of Labor Statistics, Insurance Information Institute.

315 334359

393 400 417446

481505

548

0

100

200

300

400

500

600

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

(Thousands)

Texas: Income, 2000

$39,642$42,148

$27,722 $28,451

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

Median Household Per Capita

Texas US

Texas: Race Distribution 2000

Asian3%

Native Hawiaan

0%

Other12%

Two or More2%

American Indian

1%

African American

11%White71%

6.67 Million (32%) residents of Texas identify themselves as Latino or Hispanic (of any race)

75%

12%

1%

4%

0%6%2%

Texas PopulationU.S. Population

Source: U.S. Census Bureau

Retirement

Retirement Planning

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

401(k) 457 Traditional &Roth IRA

SEP-IRA TraditionalKeough

Maximum contribution

To

Be

Det

erm

ined

To

Be

Det

erm

ined

‘01 ‘02 ‘06 ‘01 ‘02 ‘06 ‘01 ‘02 ‘06 ‘01 ‘02 ‘06 ‘01 ‘02 ‘06

Source: National Bureau of Economic Research

IRA Market Shares

Source: Investment Company Institute.

20001995

Banks/Thrifts20.0%

Life Insurers7.0%

Broker/ Dealers35.0%

Mutual Funds38.0%

Banks/Thrifts9.0%Life Insurers

9.0%

Broker/ Dealers35.0%

Mutual Funds45.0%

Retirement Benefit Asset Mix (2000)

Source: Investment Company Institute.

Private Defined

Benefits Plans

Other10.0%

Cash, e tc.7.0%

Mutual Funds6.0%

Broker/ Dealers35.0%

Equitie s49.0%

Private Defined

Contribution PlansOther20.0%

Cash, e tc.5.0%

Mutual Funds28.0%

Broker/ Dealers35.0%

Equitie s39.0%

Estate Planning

Texas: Age Distribution, 2000

Under 2032%

20 to 3423%

35 to 5428%

55 to 7413%

74 and older4%

Texas Population: 20,851,820

28%

20%31%

15%

6%

U.S. Population: 276 MillionNov 2001 projections

Source: U.S. Census Bureau

TX has a significantly younger population than the US as a whole.

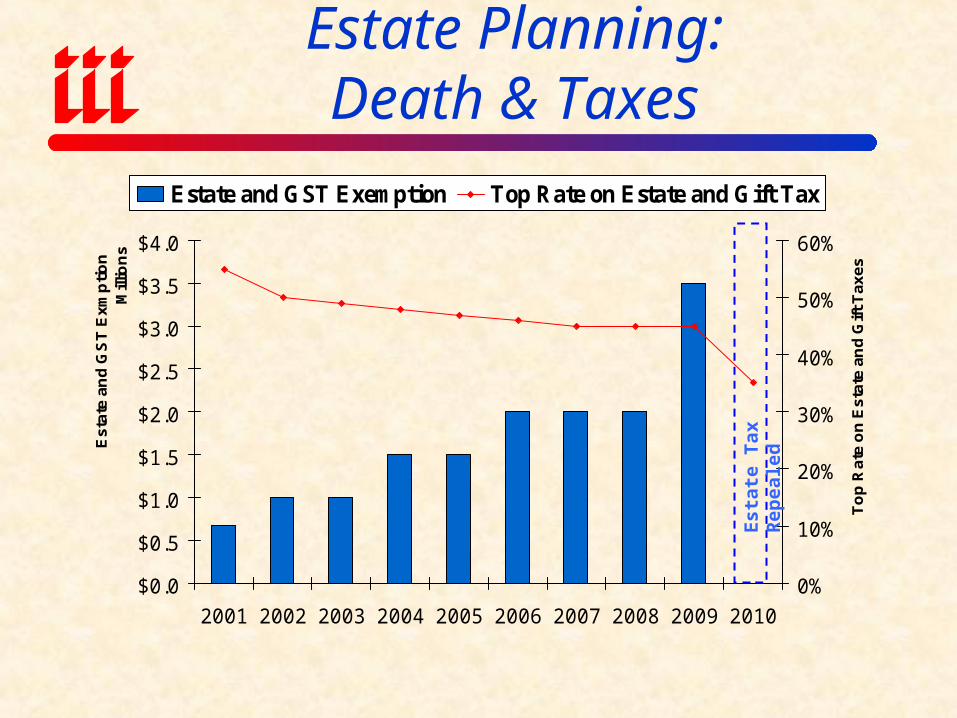

Estate Planning:Death & Taxes

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Es

tate

an

d G

ST

Ex

mp

tio

nM

illio

ns

0%

10%

20%

30%

40%

50%

60%

To

p R

ate

on

Es

tate

an

d G

ift

Ta

xe

s

Estate and GST Exemption Top Rate on Estate and Gift Tax

Est

ate

Tax

Rep

eale

d

It’s the Economy, Stupid!

Post World War II Recessionary Cycles

Previous Peak Trough Contraction in Months

February ‘45 October ‘45 8

November ’48 October ‘49 11

July ’53 May ’54 10

August ’57 April ‘58 8

April ’60 February ’61 10

December ’69 November ‘70 11

November ’73 March ’75 16

January ’80 July ’80 6

July ’81 November ’82 16

July ’90 March ’91 8

March ’01 - ? - ?Source: National Bureau of Economic Research

4.4%

3.5%

2.5%

5.7%

8.3%

4.8%5.6%

2.2%

1.0% 1.3%0.7%

-0.4%

-1.5%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Real GDP Growth

Source: US Department of Commerce; Insurance Information Institute.*Estimate.

Economy is experiencing negative G-forces after several quarters of unsustainably high

real growth

In March 2001 we entered our first recession since 1990/91

-2

0

2

4

6

8

10

12

14

Per

cen

t

CPI - All Items (1982-84=100)

Change in Consumer Price Index

*EstimateSource: Bureau of Labor Statistics

Texas:Personal Bankruptcies

44,8

78

58,0

60

69,2

55

69,0

61

62,3

95

59,5

39

73,1

12

86,0

15

79,2

71

74,6

02

75,4

04

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Unemployment Rate (%)

5.6

6.8

7.56.9

6.15.6

5.44.9

4.54.2 4.0

5.4

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

90 91 92 93 94 95 96 97 98 99 00 Oct'01

Source: US Bureau of Labor Statistics; Insurance Information Institute.

Unemployment Is Up

Unemployment rate of 5.8% is

forecast for 2002.

Texas: Unemployment Rate

4.2

4.0

4.8

4.7

6.3

6.1

5.9

5.7

5.5

5.3 5.5

5.3

3

4

4

5

5

6

6

7

2000 2001 2002 2003 2004 2005

Texas USA

Estimates made before Enron debacle.

Texas: Change in Employment

3.1%

2.2%

2.1%

0.4% 0.5%

-0.3

%

2.7%

2.1% 2.

4%

1.9%

1.8%

1.2%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2000 2001 2002 2003 2004 2005

Texas USA

Consumer Confidence: Nov. ’01 vs. Nov. ‘00

Source: Conference Board

PACIFIC

-43.7%

GREAT PLAINS

-27.0%

SW. CENTRAL

-29.8%

ROCKY MOUNTAIN

–32.9%

SE. CENTRAL

-41.0%

S. ATLANTIC

-38.9%

MID ATLANTIC

-33.7%

NEW ENGLAND

-39.0%

US: -38.0%

70,4

18 83,1

03

82,1

80

99,8

31

101

,848

108

,613

107

,319

91,1

22

89,7

02

82,7

47

79,8

97

0

20000

40000

60000

80000

100000

120000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Texas: Single-Family Housing Permits

42,0

57 53,3

59

57,2

95

99,4

83

82,2

90

72,8

53

118,

297

84,1

53

74,0

17

71,0

14

67,9

68

0

20,000

40,000

60,000

80,000

100,000

120,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Texas: Mortgage Originations

1,12

7,30

0

1,16

6,40

0

1,14

4,00

0

1,21

2,70

0

1,28

5,20

0

1,41

3,00

0

1,39

6,30

0

1,36

2,10

0

1,37

1,60

0

1,35

0,00

0

1,36

1,10

0

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Texas: New Vehicle Registrations

Insurance Information Institute On-Line

If you would like a copy of this presentation, please give me your business card with e-mail address or