Financial Roadshow 2007 Credit Management (August) By: John Cotterell.

20

Financial Roadshow 2007 Credit Management (August) By: John Cotterell

-

Upload

melvyn-hodge -

Category

Documents

-

view

218 -

download

0

Transcript of Financial Roadshow 2007 Credit Management (August) By: John Cotterell.

Financial Roadshow 2007

Credit Management

(August)

By: John Cotterell

RMIT University Slide 2

The Team• John Cotterell – Manager

• Amarjit Kaur – ARG Liason/TPC’s

• Chintha Ranwala – Student Accounts

• Paul Hamilton – Trade Debtors

• Lee Murphy – Trade Liason/Support

• Varun Khanna – Student Accounts

• TBC – DCA Accounts

RMIT University Slide 3

Areas of Responsibility• Student Debtors (2)

• Trade Debtors (1)

• TPC & ARG Support (1)

• DCA Accounts (1)

• Investigations & Reports (1)

RMIT University Slide 4

Student Debtors• Contacts – Surname (A-L) – 51771

Surname (M-Z) – 52231

Email- [email protected]

RMIT University Slide 5

Trade Debtors• Contacts – Collections/Disputes – 51734

Credit Checks/Reports – 52778

Email – [email protected]

RMIT University Slide 6

ARG Liason/TPC’s• Contacts – All Enquiries – 53649

Email – [email protected]

RMIT University Slide 7

DCA Accounts• Contacts – All Enquiries – 52231

Email – [email protected]

External Agents – Dun & Bradstreet

Citibureau ( NCML)

* DCA – Debt Collection Agencies

RMIT University Slide 8

Functions of Credit Department• Assessment of Credit Risk – Good Credit processes will strive to accept all business, but they must

continuously assess and monitor in place to control high risk customers.

• Establishment of Credit Terms & Limits – Terms (Days) and Limits should take into account the risk. The Limits can not simply be the value of the invoice, post sales.

Monitoring & Control of Debt – This includes ensuring;

* Agreed Terms & Credit Limits are being adhered to and appropriate – ( Annual Reviews to be put in place).

* All High Risk Debtors are kept under tight control. * Major customers must also be watched carefully as they account for a high proportion of the ledger and

therefore cashflow.

• Collection of Payment – Collections to be made solely by the credit management department, in a manner that creates optimum cashflow whilst ensuring continuity of good business.

RMIT University Slide 9

Creating Invoices

• To save time and possibly avoid frustrations , it always pays to check FD33 Display Credit Management before starting to create an invoice.

RMIT University Slide 10

Credit Used

RMIT University Slide 11

Credit Limit Confirmation

RMIT University Slide 12

Account Blocked ( See Tick)

RMIT University Slide 13

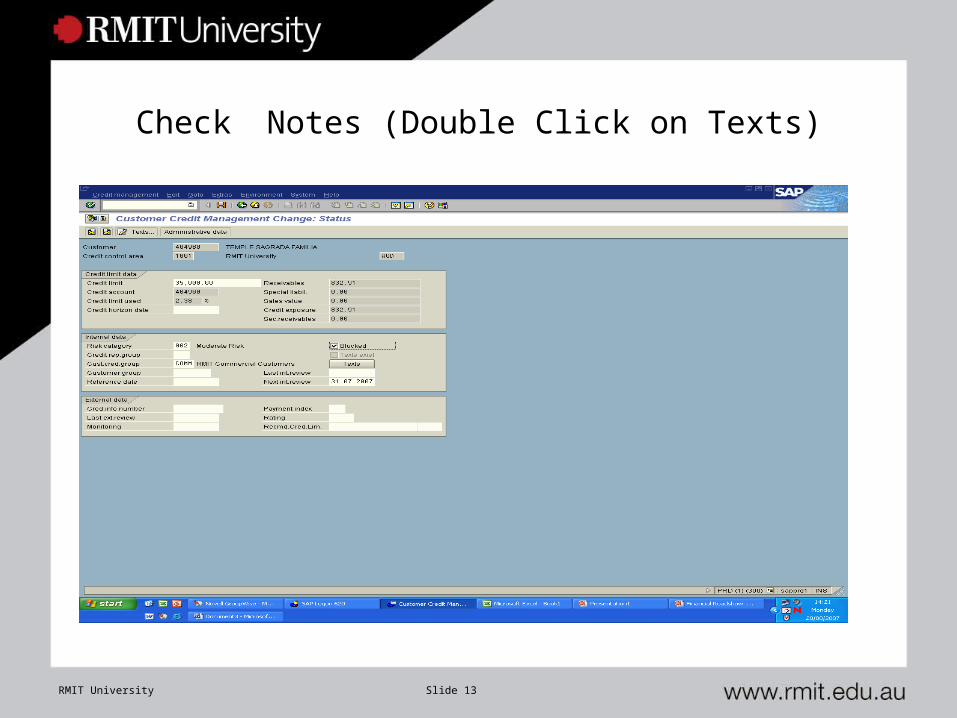

Check Notes (Double Click on Texts)

RMIT University Slide 14

How we can help?This process of checking account status briefly prior to invoice raising will

hopefully prevent invoices being half raised before matters surrounding credit limits come to light at your level. Then by bringing specific issues to our attention will assist Credit Management in assessing the credit limit and amending as appropriate as soon as possible.

RMIT University Slide 15

Credit Limits• Credit Limits across all segments are under review. In the policy currently

under review it is our intent to set high fixed value credit limits for our non commercial customers. (I.E. Accounts starting 5*** & 6****).

• This will hopefully allow freer and smoother invoicing within confirmed contractual arrangements.

• A suggestion would be to give all 5** accounts a set credit limit of $50,000 ( unless sighted contracts advise otherwise), and all 6**** accounts a set credit limit of $1,000,000 (unless sighted contracts advise otherwise).

• Of course Credit Management will still , through a detailed and confirmed dunning process, monitor days overdue and act accordingly within revised policy

RMIT University Slide 16

Calculating a Credit LimitWhilst checks still need to be made to confirm the correct credit limit for an

account, a simple calculation to assist the Credit Department is to request twice the monthly invoice value.

This allows an invoice to be raised in the second month, whilst the one from the previous month still sits within terms or has recently fallen outside terms.

Of course if this went on into the 3rd month, the dunning process may well have blocked this account until payments or any issues have been resolved.

This more accurate guide will again make invoice raising quicker and smoother whilst the limit is accurate and customer remains within agreed terms.

RMIT University Slide 17

Disputing Invoices• Moving forward departmental contacts are likely to be removed from

invoices, to assist in prompter payment receipts and logging of disputes.

• The logic is that once an invoice is sent out , the first department that need to be aware of any payment/dispute is accounts receivable and the invoice will be redesigned to reflect that.

• Once this has been approved in design, a copy will be sent out for viewing.

• Prompt payment receipt and processing , and timely logging of disputes, will update accounts and block invoices so that the most up to date and accurate presentation of an account is made.

RMIT University Slide 18

• Once a dispute has been logged and invoice blocked, the dispute will immediately be passed out to school/portfolio for investigation.

• Any payment disputes will initially be investigated by the Credit Management department.

RMIT University Slide 19

Payments• As mentioned with disputes, the design of the invoice is under

review to advise of more accurate and timely payments.• This will hopefully be achieved , by making the invoice clear in

remittance details ( customer no.) , and also payment methods and addresses.

• The sending of cheques to other areas of the university needs to be discouraged, and the use of cash books is to be significantly decreased over the coming months. The removal of this and directing to automated areas, will allow credit card details to be processed and checked immediately.

RMIT University Slide 20

Collections• Whilst there may be frustration in payment delays, please do not

contact customers directly over outstanding accounts. It may appear helpful, yet debt collection is now a legal minefield and by acting outside legislation and guidelines you may put yourself under severe risk of financial penalty.

• All staff are currently undergoing formal training re the ASIC Debtor Guidelines and National Privacy Act, and along with our established external agents, all proper steps will be made to recover outstanding debt.

• Feel free to contact me directly, if you have any concerns re the

above.