Financial Recovery Following a Disaster. 2 Purpose The Financial Recovery Process Restoring...

27

Financial Recovery Following a Disaster

-

Upload

brendan-simmons -

Category

Documents

-

view

217 -

download

1

Transcript of Financial Recovery Following a Disaster. 2 Purpose The Financial Recovery Process Restoring...

Financial Recovery Following a Disaster

2

Purpose

The Financial Recovery ProcessRestoring stabilityPlanning for the futureQuestions and answers

3

Who is FPA?

Membership organization for the financial planning community

FPA volunteers provide free planning advice to help individuals and their families recover from natural disasters

4

Recovery Priorities

Make Sure You and Your Family are OK Register With FEMA, Red Cross, etc. Secure Housing Get Access to Cash Check on Your Job Launch Your Financial Recovery

5

Steps Toward Financial Recovery

1. Re-establish address, bank accounts

2. Determine all available income sources

3. Address your debts

4. Prepare a realistic spending plan

5. Review tax considerations

6. Avoid common mistakes

7. Set goals and create a plan for the future

8. FOLLOW THROUGH WITH THE PLAN!!

6

Step 1: Address & Bank Accts.

Mailing address is required for evacuees to register with FEMA and aid agencies

Change of addresshttps://moversguide.usps.com

Bank account is required to receive aid and hold fundsNew account may be needed if old bank

incapacitated

7

Step 2: Identify Income Sources

a) Federal, State and Red Cross Programs

b) Insurance Claims/Proceeds

c) Job-Related Benefits

d) Life Insurance Policies

e) Retirement Plans

f) Other Sources

8

Step 2: Identify Income Sources a) Federal, State and Red Cross

Immediate FEMA and Red Cross emergency financial aid

Medium term State unemployment benefits Federal Disaster Unemployment Assistance State food stamp programs

Long Term FEMA Individuals & Household Programs grants SBA Real Property and Personal Property

Disaster Loans (for individuals/families) SBA Physical Disaster and Economic Injury

Loans (for businesses)

9

Step 2: Identify Income Sources a) Register to get financial help

FEMA – http://www.FEMA.gov 1-800-621-FEMA (3362)

Red Cross – http://www.redcross.org1-866-438-4636 (AL, FL, LA and MS)1-800-975-7585 (all other states)

Louisiana 2-1-1 Get Connected/Get Information

NOLA Ready- http://new.nola.gov/ready

10

Step 2: Identify Income Sources b) Insurance Claims

Contact your insurer ASAP Report how, when, & where damage

occurred Document all damaged property –

(take photos, gather receipts, etc.) Prepare an ongoing inventory list –

(inventory needed for taxes as well) Ask for living expense reimbursement

11

Step 2: Identify Income Sources b) Sample Inventory Form

HOME INVENTORY Description Brand/Model Serial Number Where and

when boughtPrice paid Replacement /

appraised val.Receipt kept?

LIVING ROOM / DEN

Television

VCR/DVD player

Carpet/rugs

Curtains/shades, etc.

Sofas

Cushions

Chairs

Coffee table

End tables

Desk

Bookcases

Books

12

Step 2: Identify Income Sources b) Flood Insurance

Flood damage usually NOT covered by homeowner’s or renter’s insurance

Flood is water that covers the groundEven if it starts out as rainEven if it’s driven by hurricane winds

Government-backed flood insurance may be available in flood-prone areas

13

Step 2: Identify Income Sources

c) Job-Related Benefits

Paycheck Advance Paid Time Off Advance Donated Paid Time Off Family & Medical Leave Act

If caring for injured family memberhttp://www.dol.gov & (866) 487-9243

14

Step 2: Identify Income Sources

d) Life Insurance Policies

Tap Cash Values of Permanent Insurance Whole, Universal, Variable, etc.

Loans Must pay interest Reduces death benefit No taxes, no penalties Policy may lapse if loan is too large

Withdrawals Reduces death benefit No taxes or penalties up to premiums paid

15

Step 2: Identify Income Sources

e) Retirement Plans

Borrowing or withdrawing from retirement plans should be a LAST RESORT May trigger income tax and penalties May seriously disrupt long-term retirement plans

Loans from 401(k) & Profit Sharing Plans: Amount – 50% of available balance Repayment options – 5-10 years to repay

Hardship Withdrawals from IRA & 401(k): 10% penalty unless used for approved costs Income tax must be paid on amount withdrawn

16

Step 2: Identify Income Sources

f) Other Sources to Consider

Family & Friends Agree now on terms to avoid future disputes

Local Organizations Churches and volunteer organizations like the Lions Club

Veteran Organizations Credit Cards

BEWARE of interest and fees!! BE CAREFUL not to overload on debt!!

17

Step 3: Address Debt Obligations

Notify mortgage company Most offer 90-day grace period in disaster zones

Notify credit card company Request a grace period Be careful if your credit history is not great

Contact other creditors Negotiate payments on services you are not

using: utilities, Internet, telephone and cable

18

Step 4: Create a Spending Plan

Take control of spending by creating a realistic spending plan

List all sources of income

List everything you spend, divided by:Spending on things you NEEDSpending on things you WANT

19

Step 4: Create a Spending Plan

Sample Expense Tracking Chart

Spending Plan Month Ending:________________________________

Expense Type Week 1 Week 2 Week 3 Week 4 Week 5

Weekly Total by Expense

Type

Monthly Planned

Spending

Difference Plus or Minus

Rent

Food - Grocery Shopping

Savings

Phone

Transportation

Medical Expenses

Laundry/ Dry Cleaning

Clothing

Personal Products

Debt Repayment

Personal Care/Hair

Education / Training Exp.

Church / Charity Dona.

Other Misc

TOTAL EXPENSES

20

Step 4: Create a Spending Plan

What Are Needs and Wants?

Income Needs Wants

Salary Housing Entertainment

Pension, Soc. Sec. Food Eating out

Savings Utilities New clothes

Govt. grant or loan Transportation Toys/electronics

Unemployment Insurance Gifts

21

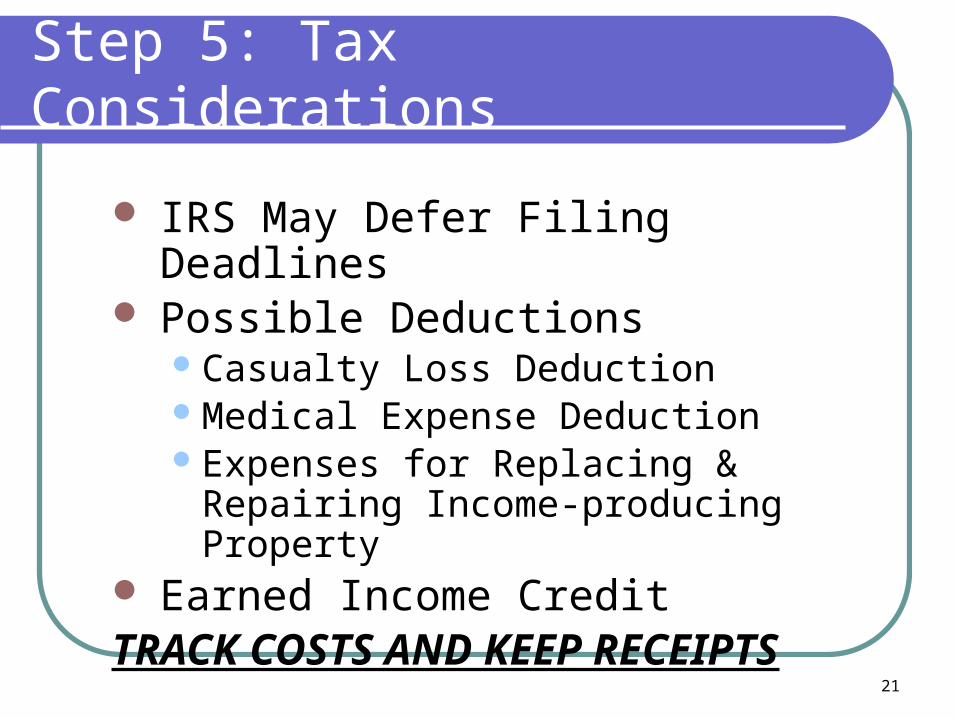

Step 5: Tax Considerations

IRS May Defer Filing Deadlines Possible Deductions

Casualty Loss DeductionMedical Expense DeductionExpenses for Replacing & Repairing

Income-producing Property Earned Income CreditTRACK COSTS AND KEEP RECEIPTS

22

Step 5: Tax Considerations

Getting Professional Tax Help Taxes Are Complex – Consult a

Professional Free help may be available

VITA – Volunteer Income Tax Assistance Program 1 800.829.1040

TCE – Tax Counseling for the Elderly 1 800.829.1040

AARP Tax Aid Program Email: [email protected] 1 888.227.7669

23

Step 6: Be Careful of These!!!

Credit Card Cash Advances Payday Advance Loans Zero Down, Zero Interest Offers Reverse Mortgages Misspending funds received from FEMA

WATCH OUT FOR SCAMS AND PREDATORS

24

Step 6: Be Careful of These!!!

Dealing with Contractors

Disaster zones attract predators Demand proof of licenses, permits, etc. Get contracts and costs in writing Pay periodically as work progresses Make sure work meets building codes Don’t make final payment until you’re

satisfied with the work

25

Step 7: Plan for the Future

Decide on life goals and determine the financial steps needed to reach them

Revise your income and spending plan to achieve steps toward your goals

Choose investments and insurance matched to your goals

Create an emergency fund

26

Step 8: Follow Through

Implement the Plan Monitor and Maintain the Plan on a

Regular Basis Make Adjustments As Your Situation

Changes

A PLAN THAT IS NOTIMPLEMENTED IS WORTHLESS!!

27

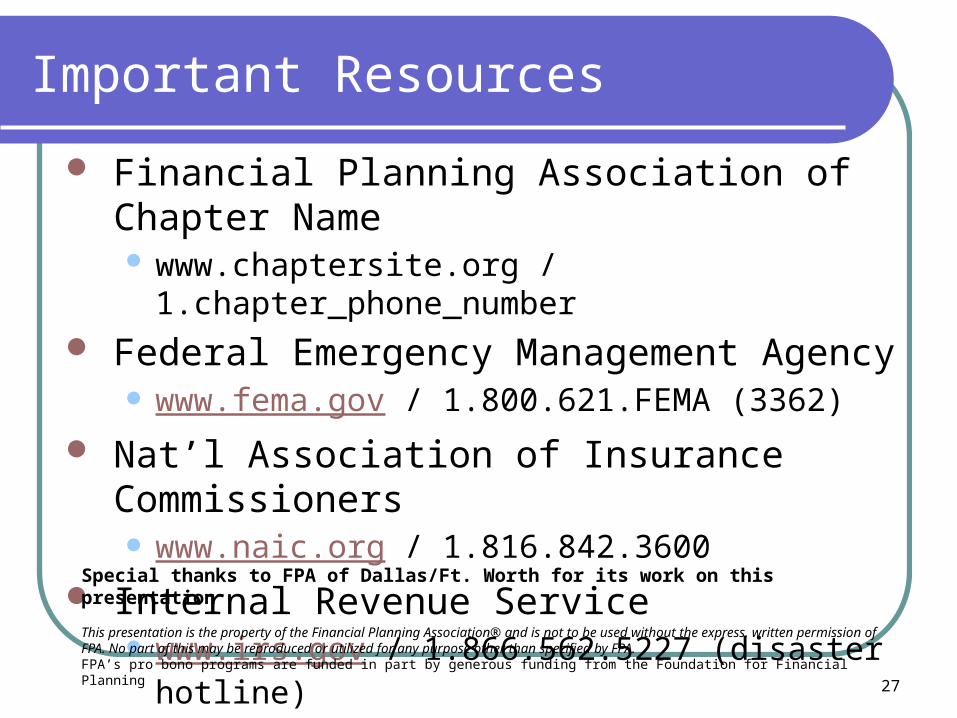

Important Resources

Financial Planning Association of Chapter Name www.chaptersite.org / 1.chapter_phone_number

Federal Emergency Management Agency www.fema.gov / 1.800.621.FEMA (3362)

Nat’l Association of Insurance Commissioners www.naic.org / 1.816.842.3600

Internal Revenue Service www.irs.gov / 1.866.562.5227 (disaster hotline)

Special thanks to FPA of Dallas/Ft. Worth for its work on this presentation

This presentation is the property of the Financial Planning Association® and is not to be used without the express, written permission of FPA. No part of this may be reproduced or utilized for any purpose other than specified by FPA.FPA’s pro bono programs are funded in part by generous funding from the Foundation for Financial Planning