Financial R 2015

82

Comprehensive Annual Financial Report for the year ended September 30, 2015 2015 F INANCIAL R EPORT

Transcript of Financial R 2015

Comprehensive Annual Financial Report for the year ended September 30, 2015

2015Financial RepoRt

Aub

urn U

nive

rsity

201

5

2

This page is intentionally left blank.

Aub

urn U

nive

rsity

201

5

3

INTRODUCTORY SECTION

PRESIDENT’S LETTER .......................................................................................................................................................6

FINANCIAL SECTION

INDEPENDENT AUDITOR’S REPORT ................................................................................................................................8

MANAGEMENT’S DISCUSSION AND ANALYSIS .............................................................................................................12

AUBURN UNIVERSITY FINANCIAL STATEMENTS

STATEMENTS OF NET POSITION ....................................................................................................................................22

STATEMENTS OF REVENUES, EXPENSES AND CHANGES IN NET POSITION ..........................................................23

STATEMENTS OF CASH FLOWS......................................................................................................................................24

COMPONENT UNITS’ FINANCIAL STATEMENTS

AUBURN UNIVERSITY FOUNDATION AND AUBURN ALUMNI ASSOCIATION ..............................................................26

TIGERS UNLIMITED FOUNDATION ..................................................................................................................................28

AUBURN RESEARCH AND TECHNOLOGY FOUNDATION .............................................................................................30

NOTES TO FINANCIAL STATEMENTS ....................................................................................................................................32

DIVISIONAL FINANCIAL STATEMENTS (UNAUDITED)

AUBURN UNIVERSITY MAIN CAMPUS ............................................................................................................................66

AUBURN UNIVERSITY AT MONTGOMERY ......................................................................................................................68

ALABAMA AGRICULTURAL EXPERIMENT STATION ......................................................................................................70

ALABAMA COOPERATIVE EXTENSION SYSTEM ...........................................................................................................72

REQUIRED SUPPLEMENTAL INFORMATION ........................................................................................................................75

AUBURN UNIVERSITY BOARD OF TRUSTEES .....................................................................................................................81

TABLE OF CONTENTS

2015Financial RepoRt

Aub

urn U

nive

rsity

201

5

4

Aub

urn U

nive

rsity

201

5

5

intRoductoRy Section

2015Financial RepoRt

Aub

urn U

nive

rsity

201

5

6

January 20, 2016

Dear Members of the Auburn Community and Alabama Citizens:

It’s a good time to be an Auburn Tiger. Here are a few highlights: Top ranking

The Business Journals examined universities across the country to determine who offers the best educational experience. Auburn came out on top in the state based on such criteria as retention and graduation rates, reputation, admissions, and housing.

Leader in global skills & engagement Auburn is fast becoming a thought leader in global engagement. In addition to augmenting

opportunities for study abroad and international skills development, in the past year we’ve held two standing-room-only forums where government and military leaders have addressed current world issues. Learn more at #AUWorldAffairs.

Record number of prestigious scholarships Auburn helps students reach their fullest potential, and for some that means competing for

prestigious scholarships to further their intellectual development. In just one example, four spring graduates won Fulbright Scholarships, bringing the total to a record 14 in the past six years. Fulbright is the flagship international exchange program, and these students serve as excellent ambassadors for Auburn and the U.S.

First UAS flight school Unmanned aerial systems offer tremendous economic potential in fields as diverse as

agriculture and construction. Auburn is one of the nation’s oldest aviation programs, and it’s now the youngest UAS flight school after earning the federal government’s first certification to train commercial drone pilots.

This report summarizes our financial position and activity for the fiscal year ending September 30, 2015. We invite you to learn more at www.auburn.edu.

O F F I C E O F T H E P R E S I D E N T

Sincerely,

Jay Gogue President

Aub

urn U

nive

rsity

201

5

7

Financial Section

2015Financial RepoRt

Aub

urn U

nive

rsity

201

5

8

PricewaterhouseCoopers LLP, 569 Brookwood Village, Suite 851, Birmingham, AL 35209 T: (205) 414 4000, F: (205) 414 4001, www.pwc.com/us

Independent Auditor's Report

To the Board of Trustees of Auburn University:

We have audited the accompanying financial statements of Auburn University (the “University”), a component unit of the State of Alabama, as of and for the years ended September 30, 2015 and 2014, and the related notes to the financial statements, which consist of the statements of net position and the related statements of revenues, expenses and changes in net position and statements of cash flows of Auburn University and the statements of financial position and of activities and changes in net assets of the University’s discretely presented component units. We have audited the statements of financial position and of activities and changes in net assets, for Auburn Research and Technology Foundation (“ARTF”), one of the University’s discreetly presented component units, as of and for the year ended September 30, 2015 and 2014.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express opinions on the financial statements based on our audits. We did not audit the financial statements of Auburn Alumni Association (the “Association”) and Auburn University Foundation (the “Foundation”), two of the University’s discretely presented component units, as of and for the years ended September 30, 2015 and 2014. We did not audit the financial statements of Tigers Unlimited Foundation (“TUF”), one of the University’s discretely presented component units, as of and for the years ended June 30, 2015 and 2014. Those statements were audited by other auditors whose reports have been furnished to us, and our opinion, insofar as it relates to the amounts included for the above mentioned discretely presented component units of the University, is based solely on the reports of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the University’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the University’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the

Aub

urn U

nive

rsity

201

5

9

2

overall presentation of the financial statements. We believe that the audit evidence we haveobtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, based on our audits and the reports of the other auditors, the financial statements referred to above present fairly, in all material respects, the financial position of the University andits discretely presented component units at September 30, 2015 and 2014, or at June 30, 2015 and 2014, as applicable, and the changes in financial position and, where applicable, cash flows thereof for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Emphasis of Matter

As discussed in Note 1 and 11 to the basic financial statements, in the year ended September 30, 2015, the University adopted new accounting guidance related to the manner in which it accounts for pensions. As described within the notes to the financial statements, the University adopted Governmental Accounting Standards Board (“GASB”) Statement No. 68, Accounting and Financial Reporting for Pensions, an Amendment of GASB Statement No. 27, and GASB Statement No. 71,Pension Transition for Contributions Made Subsequent to the Measurement Date, an amendmentof GASB Statement No. 68, effective October 1, 2014. Our opinion is not modified with respect to this matter.

Other Matters

The accompanying management's discussion and analysis and the required supplemental information for the year ended September 30, 2015 on pages 12 through 21 and 75 through 80, respectively, are required by accounting principles generally accepted in the United States of America to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in the appropriate operational, economic, or historical context. We applied certain limited proceduresto the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about themethods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

The University has omitted the management's discussion and analysis for the year ended September 30, 2014 that accounting principles generally accepted in the United States of America require to be presented to supplement the basic financial statements. Such missing information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in the appropriate operational, economic, or historical context. Our opinions on the basic financial statements are not affected by this missing information.

Aub

urn U

nive

rsity

201

5

10

3

Our audits were conducted for the purpose of forming opinions on the financial statements that collectively comprise the University’s basic financial statements. The introductory information on pages 5 to 6 and the supplemental divisional financial statements on pages 66 to 73 are presented for purposes of additional analysis and are not a required part of the basic financial statements.Such information has not been subjected to the auditing procedures applied in the audit of the basic financial statements by us or other auditors, and accordingly, we express no opinion nor provide any assurance on them.

January 20, 2016

Aub

urn U

nive

rsity

201

5

11

This page is intentionally left blank.

Aub

urn U

nive

rsity

201

5

12

The following discussion and analysis provides an overview of the financial position and activities of Auburn University (the University) for the year ended September 30, 2015, with a comparison to the year ended September 30, 2014. This discussion has been prepared by management and should be read in conjunction with the financial statements and the notes thereto, which follow this section. The financial statements, footnotes, and this discussion are the responsibility of University management.

The University is a land-grant institution with two campuses, Auburn (main campus) and Montgomery (AUM). Main campus is classified by the Carnegie Foundation as “Doctoral/Research-Extensive,” while AUM is classified as “Master’s I.” Fall 2015 enrollment totaled 32,206 students at main campus and AUM. The University offers a diverse range of degree programs in 12 colleges and schools and has 5,406 full-time employees, including 1,397 faculty members, who contribute to the University’s mission of serving the citizens of the State of Alabama through its instructional, research, and outreach programs.

Using the Annual ReportThe University’s financial statements are prepared in accordance with Governmental Accounting Standards Board (GASB) principles, which establish standards for external financial reporting for public colleges and universities. The financial report includes three financial statements: the Statement of Net Position; the Statement of Revenues, Expenses, and Changes in Net Position; and the Statement of Cash Flows. All references to “2015,” “2014,” or another year refer to the fiscal year ended September 30, unless otherwise noted.

The University’s financial statements are summarized as follows:

The Statement of Net Position presents entity-wide assets, deferred outflows of resources, liabilities, deferred inflows of resources, and net position (assets and deferred outflows of resources minus liabilities and deferred inflows of resources) on the last day of the fiscal year. Distinctions are made in current and noncurrent assets and liabilities. Net position is segregated into unrestricted, restricted (expendable and nonexpendable), and net investment in capital assets. The University’s net position is one indicator of the University’s financial health. From the data presented, readers of the Statement of Net Position have the information to determine the assets available to continue the operations of the University. They may also determine how much the University owes vendors, investors, and lending institutions. Finally, the Statement of Net Position outlines the net resources available to the University.

The Statement of Revenues, Expenses and Changes in Net Position presents the revenues earned and expenses incurred during the year. Activities are reported as either operating or nonoperating. Governmental accounting standards require state appropriations, gifts, and investment earnings to be classified as nonoperating revenues. As a result, the University will typically realize a significant operating loss. The utilization of capital assets is reflected in the Statement of Revenues, Expenses and Changes in Net Position as depreciation expense, which reflects the amortization of the cost of an asset over its expected useful life.

The Statement of Cash Flows reports the major sources and uses of cash and reveals further information for assessing the University’s ability to meet financial obligations as they become due. Inflows and outflows of cash are summarized by operating, noncapital financing, capital and related financing, and investing activities.

In addition to the University’s financial statements, related component unit Statements of Financial Position and Statements of Activities and Changes in Net Assets have been included in this annual report.

GASB Statement No. 39, Determining Whether Certain Organizations Are Component Units-an amendment of GASB Statement No. 14, provides criteria for determining which related organizations should be reported as component units based on the nature and significance of their relationship with the primary government, which is the University. GASB Statement No. 39 also clarifies financial reporting requirements for those organizations as amendments to GASB Statement No. 14, The Financial Reporting Entity. The University also evaluated GASB Statement No. 61, The Financial Reporting Entity: Omnibus-an amendment of GASB Statements No. 14 and No. 34 to ensure proper disclosure. The component units report financial results under principles prescribed by the Financial Accounting Standards Board (FASB) and are subject to standards under the Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles and present net assets in three classes: unrestricted, temporarily restricted, and permanently restricted. The four component units of the University reported herein are as follows:

(1) Auburn University Foundation (AUF) - AUF was organized on February 9, 1960, and is the fundraising foundation for the University. As of September 30, 2015, AUF holds endowments and distributes earnings from those endowments to the University. AUF is incorporated as a legally separate, tax-exempt nonprofit organization established to solicit individual and corporate donations for the direct benefit of the University. The Auburn University Real Estate Foundation, Inc. (AUREFI) has been consolidated into AUF’s financial statements.

(2) Auburn Alumni Association (the Association) - The Association is a nonprofit corporation organized on April 14, 1945, which was created to promote mutually beneficial relationships between the University and its alumni, to encourage loyalty among alumni, and to undertake various other actions for the benefit of the University, its alumni, and the State of Alabama. Membership is comprised of alumni, friends, and students of the University. The Association provides monetary support to the University in the form of faculty awards and student scholarships.

(3) Tigers Unlimited Foundation (TUF) - TUF is a legally separate nonprofit organization incorporated in December 2002, which began operations on April 21, 2004. TUF was organized exclusively for charitable purposes, pursuant to Sections 501(a) and 501(c)(3) of the Internal Revenue Code to support athletic fundraising and athletic programs. TUF has a June 30 fiscal year end. TUF provides economic resources to the University for athletic scholarships, athletic building maintenance or new construction, and for athletic department programs.

(4) Auburn Research and Technology Foundation (ARTF) - ARTF was organized on August 24, 2004, as a separate nonprofit organization to develop and operate the Auburn Research Park and to assist the University with the attraction, development, and commercialization of technology. The vision of ARTF is to establish an entrepreneurial atmosphere for businesses to foster economic diversification and vitality of the local community, state, and region.

During the year, the University implemented GASB Statement No. 68, Accounting and Financial Reporting for Pensions and GASB Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date. GASB Statement No. 68 revises existing standards for employer financial statements and requires the recognition of a liability equal to the net pension obligation for pension plans provided by the University to its employees. The net pension obligation is measured as the total pension liability, less the amount of the pension plan’s fiduciary net position. The total pension liability is determined based upon

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Aub

urn U

nive

rsity

201

5

13

Financial Highlights Statement of Net PositionA summary of assets, deferred outflows of resources, liabilities, deferred inflows of resources, and net position as of September 30, 2015 and 2014, is as follows:

2015 2014

AssetsCurrent assets $ 236,697,624 $ 301,408,817 Capital assets 1,560,193,650 1,550,144,298 Other noncurrent assets 995,824,011 861,390,142 Total assets 2,792,715,285 2,712,943,257

Deferred Outflows of Resources 80,183,723 14,442,185

LiabilitiesCurrent liabilities 345,166,861 333,782,202 Noncurrent liabilities 1,309,624,581 751,013,602 Total liabilities 1,654,791,442 1,084,795,804

Deferred Inflows of Resources 39,513,489 435,203

Net PositionNet investment in capital assets 855,698,812 821,520,355 Restricted-nonexpendable 28,537,859 28,176,521 Restricted-expendable 177,483,201 162,165,880 Unrestricted 116,874,205 630,291,679 Total net position $ 1,178,594,077 $ 1,642,154,435

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

term maturities. The University saw increases in capital assets, net of depreciation, shown as “Investment in plant, net” on the Statement of Net Position, of $10.0 million from 2014 to 2015. Capital assets generally represent the historical cost of land, land improvements, buildings, construction in progress, infrastructure, equipment, library books, art and collectibles, software system implementation, and livestock, less applicable accumulated depreciation, with buildings comprising approximately 76.8% of the total net capital asset value. The increase, offset by disposal activity, depreciation, and transfers, was the result of $86.8 million of new additions to property, plant, and equipment, net of construction in progress transfers. The University expended $69.5 million in new construction during fiscal year 2015.

The following building construction projects totaling $37.5 million were either completed and placed into service or additional work was performed on a previously completed project during the current fiscal year:

Jordan Hare Stadium New Score and Video Board System $ 13.2 million Cambridge Apartments $ 5.2 million East Glenn Administrative Support Facility $ 3.4 million Bailey Small Animal Teaching Hospital $ 2.6 million Dudley Envelope and Windows $ 2.0 million South Donahue Residence Halls $ 1.5 million Lowder East Hall Courtyard Student Lounge $ 1.3 million War Hawk Residence Hall $ 1.3 millionPathological Waste Incinerator and Building Improvements $ 1.2 million Jordan Hare Stadium Power System Improvement $ 1.1 million Other Small Projects $ 4.7 million

The University’s AssetsCurrent assets consist of cash and cash equivalents, operating investments (those investments that are expected to be liquidated during the course of normal operations), net accounts receivable (primarily amounts due from the federal and state governments and other agencies as reimbursements for sponsored programs), net student accounts receivable (including amounts due from third parties on behalf of the students), current portion of loans receivable, accrued interest receivable, inventories, and prepaid expenses. The University’s current assets decreased $64.7 million from 2014 to 2015. Of this decrease, cash and cash equivalents and operating investments decreased by $78.4 million. During the year, the University decreased the amount of deposits on hold with banks based on revised federal bank regulations. These funds were invested in longer term maturities. Accounts receivable (including loans receivable and interest receivable) increased $8.7 million. The majority of the accounts receivable increase was due to increased spending prior to year end on federal, state and other sponsored projects, which generated receivables. Student accounts receivable increased $3.9 million, which was due to the tuition increase approved by the Board of Trustees and changes in enrollment and scholarship strategies. The remaining changes were due to increases in inventories and prepaid expenses of $1.1 million.

The University’s long-term investments, shown in other noncurrent assets, increased by $134.5 million from 2014 to 2015. As discussed above, this was due partially to changes in federal bank regulations as well as investing the University’s increases in net position in longer

discounting projected benefit payments based on the benefit terms and legal agreements existing at the pension plan’s fiscal year end. Projected benefit payments are required to be discounted using a single rate that reflects the expected rate of return on investments, to the extent that plan assets are available to pay benefits, and a tax-exempt, high-quality municipal bond rate when plan assets are not available. This Statement requires that most changes in the net pension liability be included in pension expense in the period of the change. GASB Statement No. 71 is a clarification to GASB Statement No. 68 requiring recognition of a beginning deferred outflow of resources for its pension contributions, if any, made subsequent to the measurement date of the beginning

net pension liability. These statements also enhance accountability and transparency through revised note disclosures and required supplementary information (RSI). September 30, 2014 amounts have not been restated to reflect the impact of GASB Statement No. 68 because the information is not available to calculate the impact on pension expense for the fiscal year ending September 30, 2014. In accordance with the Statement, the University has reported a net pension liability (net of deferred outflows of resources) in the amount of $558,573,898 as a change in accounting principle adjustment to unrestricted net position as of October 1, 2014.

Aub

urn U

nive

rsity

201

5

14

The University’s Deferred Inflows of ResourcesDeferred inflows of resources are an acquisition of net assets that are applicable to a future reporting period. The University engages in certain voluntary nonexchange transactions (grants). Grant funds received for which all eligibility requirements have been met, other than time requirements, are presented as deferred inflows of resources in accordance with GASB Statements No. 63 and No. 65. In 2015, the University implemented GASB Statement No. 68 which required the reporting of deferred inflows of resources relating to the accounting and reporting of pensions.

The University's deferred inflows of resources had an increase of $39.1 million from 2014 to 2015. This increase was the result of the accounting and reporting of pension activity, in accordance with GASB Statement No. 68 (see Note 11).

The University’s Net Position The three major net position categories are discussed below:

Net investment in capital assets represents the University’s capital assets, net of accumulated depreciation and outstanding principal balances of debt as well as any deferred inflows or outflows of resources, attributable to the acquisition, construction, or improvement of those assets. Net investment in capital assets increased 4.2% from 2014 to 2015. This increase was due to capitalization of assets as previously described and payments made on outstanding debt.

Restricted (nonexpendable and expendable) net position:

Restricted-nonexpendable net position is subject to external restrictions governing its use and consists of the University’s permanent endowment funds. This net position increased 1.3% from 2014 to 2015. This increase was the result of additional gifts to permanently endowed funds as well as investment earnings that were added back to current permanent endowments.

Restricted-expendable net position is also subject to external restrictions governing its use. Items of this nature include gifts, contracts, and grants restricted by federal, state, local governments, or private sources for purposes as determined by donors and/or external entities that have placed time or purpose restrictions on the use of the assets. Restricted funds functioning as endowments, restricted funds available for student loans, and funds restricted for construction purposes are also included in this category. Restricted-expendable net position increased 9.4% from 2014 to 2015. This majority of the increase was due to additional gift receipts in fiscal year 2015.

Unrestricted net position is the third major class of net position, and it is not subject to externally imposed stipulations; however, the majority of the University’s unrestricted net position has been internally designated for various mission-related purposes. This category includes funds for general operations of the University, auxiliary operations (including athletics, housing, and the bookstores), unrestricted quasi-endowments, and capital projects. Unrestricted net position decreased 81.5% from 2014 to 2015. The decrease in unrestricted net position was due to the implementation of GASB Statement No. 68. Otherwise, the University would have shown an increase in unrestricted net position of $45.2 million.

The University’s Deferred Outflows of ResourcesDeferred outflows of resources are a consumption of net assets that are applicable to a future reporting period. In 2010, 2012, 2014, and 2015, the University defeased certain outstanding bonds. These refundings resulted in losses (the difference between the acquisition price of the new debt and the net carrying amount of the old debt). In accordance with GASB Statements No. 63 and No. 65, these losses are presented as deferred outflows of resources. In 2015, the University implemented GASB Statement No. 68 which required the reporting of deferred outflows of resources relating to the accounting and reporting of pensions.

Deferred outflows of resources increased $65.7 million, which is made up of loss on refunding of bonds and pension activity. During the year, the University partially defeased certain bonds and issued 2015A and 2015B General Fee Bonds. The losses on refunding of these defeasances, which totaled $15.7 million, were amortized with prior years’ losses. The amortized amount of $3.2 million netted with the current year losses to account for $12.5 million of the increase. The loss on refunding is amortized over the life of the old or new bonds, whichever is shorter. The University is amortizing over the life of the defeased bonds (see Note 8). In addition, deferred outflows of resources increased $53.2 million relating to pension activity in accordance with the implementation of GASB Statement No. 68 (see Note 11).

The University’s LiabilitiesCurrent liabilities consist of accounts payable, accrued salaries and wages, the current portion of compensation-related liabilities, accrued interest payable, other accrued liabilities, student and other deposits (including Perkins and Health Professions loan liability), unearned revenues, and the current portion of noncurrent liabilities. Current liabilities increased $11.4 million from 2014 to 2015. While the University accrued $3.0 million less in payables at year end, unearned revenues increased $15.2 million. Unearned revenue is comprised of tuition, room and board revenue that relates to fiscal year 2016, contracts and grants funding received prior to expenditure as well as athletic revenue related to games played subsequent to September 30. For Fall 2015, the Board of Trustees approved approximately a 2.5% and 3.2% tuition increase for main campus and AUM, respectively. Sixty percent of fall tuition is reported as unearned revenue due to the fiscal year end of September 30. The remaining changes were due to a decrease in the pollution remediation liability of $2.9 million, which was determined to be due subsequent to fiscal year 2016 and an increase of $1.4 million in the University's current portion of long term liabilities. This increase was the result of the University’s debt repayment strategies. Bonds issued in 2012 were structured to begin principal repayments in 2016, aligning payments with generation of corresponding pledged revenue.

Noncurrent liabilities include principal amounts due on University bonds payable, accrued compensated absences and other compensation-related liabilities that are payable beyond September 30, 2016. Noncurrent liabilities increased $558.6 million from 2014 to 2015. The majority of the increase was due to the implementation of GASB Statement No. 68 which requires the recognition of a liability equal to the net pension obligation for pension plans provided by the University to its employees. Based on actuarial data, the University’s pension obligation was $570.4 million. An additional $1.8 million was accrued for the University's post-employment medical plan, in accordance with GASB Statement No. 45. These increases were offset with debt payments and amortization of bond premium and discounts in the amount of $16.3 million. The remaining increase was due to the University’s pollution remediation liability, which did not change significantly in total from 2014; however, it is now determined it will be due subsequent to fiscal year 2016.

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Aub

urn U

nive

rsity

201

5

15

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Statement of Revenues, Expenses and Changes in Net Position Changes in total net position are the result of activity presented in the Statement of Revenues, Expenses and Changes in Net Position. The purpose of this statement is to present operating and nonoperating

2015 2014

Operating revenues $ 718,514,949 $ 663,909,152 Operating expenses 949,522,278 928,297,437 Operating loss (231,007,329) (264,388,285)

Net nonoperating revenues and other changes in net position 326,020,869 329,276,547

Increase in net position 95,013,540 64,888,262

Net position - beginning of year 1,642,154,435 1,577,266,173 Cumulative effect of change in accounting principle (558,573,898)

Net position, October 1, 2014, as restated 1,083,580,537

Net position - end of year $ 1,178,594,077 $ 1,642,154,435

The 2015 Statement of Revenues, Expenses, and Changes in Net Position reflects an increase in net position at the end of the year of $95.0 million. Operating revenues increased 8.2% from 2014 to 2015. The majority of this increase is attributable to the increase in student tuition and fee revenue, net of discounts. The $29.7 million tuition and fee increase over 2014 was the result of the Board-approved increase in tuition for both main campus and AUM and changes to the University's enrollment and scholarship strategies. The University also saw increases in other operating revenue of $6.8 million. The majority of the increase was due to revenue recognized on a fixed price contract, of which the revenue was previously deferred. The University saw a net increase in federal appropriations, federal, state, and nongovernmental contract and grant revenues of $2.9 million, which was primarily the result of an increase in spending of federal grant funds appropriated and awarded for research. Auxiliary revenue increased $12.9 million. The majority of this increase was due to increased athletic ticket sales, radio and television revenues. In addition, the University saw increases in housing revenue at main campus and at AUM.

Operating expenses increased $21.2 million from 2014 to 2015. Multiple factors contributed to this net increase. Compensation and benefit costs increased 3.5%. This was the result of Board-approved salary increases and one-time supplement payments. Scholarship and fellowship

revenues, operating and nonoperating expenses, other revenues, expenses, gains, losses, and changes in net position.A condensed statement is provided below:

expense decreased $1.9 million, while other supplies and services expenses had a modest increase of $2.0 million. Depreciation expense increased 3.5% in 2015. This increase was the result of recording depreciation beginning in fiscal year 2015 on projects completed in 2014. The biggest addition in fiscal year 2014 was the Bailey Small Animal Teaching Hospital.

Net nonoperating revenues and other changes in net position decreased $3.3 million from 2014 to 2015. The University’s net investment income decreased from $38.8 million in fiscal year 2014 to $27.4 million in fiscal year 2015. During fiscal year 2015, there were several factors that contributed to this decrease. The University experienced one-year losses of (4.0)%, compared to one-year returns of 10.8% in 2014; this caused a decrease in unrealized gains/losses of $7.2 million. During fiscal year 2014, the University recognized a gain of approximately $5.0 million which did not occur in fiscal year 2015. Therefore, the realized gain/losses on investments decreased $4.0 million. In addition, the University’s interest expense increased $3.2 million. These changes were offset by an increase in appropriations from the State of Alabama of $2.5 million, additional revenue recognized on Pell grants awarded to students in fiscal year 2015 of $0.5 million or 2.6%, and an increase in gifts and capital gifts and grants of $8.3 million.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

2011 2012 2013 2014 2015b* 2015a*

Am

ou

nt

in M

illio

ns

Fiscal Year

TOTAL NET POSITION

Unrestricted

Restricted Expendable

Restricted Nonexpendable

Net Investment of Capital Assets

$1,435

$1, 737

$1,518 $1,577 $1,642

$1,179

*Note: For illustrative purposes only, 2015* is the net position excluding the cumulative effect of the adoption of GASB Statement No. 68, which reduced the University’s October 1, 2014 net position by $558,573,898. 2015 is the net position including the adoption of GASB Statement No. 68.

TOTAL NET POSITION

Am

ount

in M

illio

ns

Fiscal Year

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

2011 2012 2013 2014 2015b* 2015a*

Am

ou

nt

in M

illio

ns

Fiscal Year

TOTAL NET POSITION

Unrestricted

Restricted Expendable

Restricted Nonexpendable

Net Investment of Capital Assets

$1,435

$1, 737

$1,518 $1,577 $1,642

$1,179

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

2011 2012 2013 2014 2015b* 2015a*

Am

ou

nt

in M

illio

ns

Fiscal Year

TOTAL NET POSITION

Unrestricted

Restricted Expendable

Restricted Nonexpendable

Net Investment of Capital Assets

$1,435

$1, 737

$1,518 $1,577 $1,642

$1,179

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

2011 2012 2013 2014 2015b* 2015a*

Am

ou

nt

in M

illio

ns

Fiscal Year

TOTAL NET POSITION

Unrestricted

Restricted Expendable

Restricted Nonexpendable

Net Investment of Capital Assets

$1,435

$1, 737

$1,518 $1,577 $1,642

$1,179

Aub

urn U

nive

rsity

201

5

16

OPERATING EXPENSES BY NATURAL CLASSIFICATIONFor the year ended September 30, 2015

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

OPERATING EXPENSES BY FUNCTIONFor the year ended September 30, 2015

OPERATING REVENUES SUPPORTING CORE ACTIVITIESFor the year ended September 30, 2015

Instruction 27%

Research 10%

Public Service 11%

Academic Support 6%

Library 1%

Student Services 4%

Institutional Support 8%

Operations & Maintenance 8%

Scholarships & Fellowships

4% Auxiliaries 13%

Depreciation 8%

OPERATING EXPENSES BY FUNCTION For the year ended September 30, 2015

Compensation & Benefits 63%

Other Supplies & Services 24% Depreciation

8%

Utilities 3%

Scholarships & Fellowships

2%

OPERATING EXPENSES BY NATURAL CLASSIFICATION For the year ended September 30, 2015

Other Operating Revenue 4%

Sales & Services 6%

Grants & Contracts 14%

Federal Appropriations 2%

Student Tuition & Fees, 55%

Auxiliaries, net 19%

OPERATING REVENUES SUPPORTING CORE ACTIVITIES For the year ended September 30, 2015

Other Operating Revenue 3%

Sales & Services 6%

Grants & Contracts 15%

Federal Appropriations 2%

Student Tuition & Fees, Net 55%

Auxiliaries, Net 19%

OPERATING REVENUES SUPPORTING CORE ACTIVITIES For the year ended September 30, 2014

Other Operating Revenue 3%

Sales & Services 6%

Grants & Contracts 15%

Federal Appropriations 2%

Student Tuition & Fees, Net 55%

Auxiliaries, Net 19%

OPERATING REVENUES SUPPORTING CORE ACTIVITIES For the year ended September 30, 2014

Other Operating Revenue 3%

Sales & Services 6%

Grants & Contracts 15%

Federal Appropriations 2%

Student Tuition & Fees, Net 55%

Auxiliaries, Net 19%

OPERATING REVENUES SUPPORTING CORE ACTIVITIES For the year ended September 30, 2014

Aub

urn U

nive

rsity

201

5

17

Net cash used in operating activities decreased from 2014 to 2015 by 6.5%. The majority of this decrease was the result of additional cash provided from tuition and fees of $28.0 million, auxiliary enterprises of $23.3 million, other operating revenues of $7.0 million, and federal appropriations of $1.6 million. These increases in cash were offset by payments for employee compensation and benefits of an additional $21.9 million, as a result of Board-approved salary increases and one-time supplement payments, and additional payments to suppliers of $11.0 million. Although the University received fewer funds from grants and contracts of $19.3 million, payments for utilities and scholarship & fellowships decreased $1.5 million and $1.2 million, respectively.

Net cash provided by noncapital financing activities increased $11.8 million. This was primarily due to additional gifts of $7.7 million and additional allocation of state appropriations of $2.5 million over the allocation in fiscal year 2014. The remaining increase of $1.6 million was the difference between direct and other loan receipts and disbursements in fiscal year 2015.

The University saw an increase in net cash used in capital and related financing activities of $1.8 million. During fiscal year 2015, the University received $2.1 million less than in fiscal year 2014 related to capital gifts and grants. The University completed several projects funded by bond issuances, which caused funds expended related to those issuances to decrease by $10.4 million. During the fiscal year, the University partially refunded two bond issuances causing a net increase in cash flows provided by capital and related financing activity of $8.8 million. In contrast, payments for interest expense increased $13.9 million. This increase was a direct result of the completion of the previously mentioned construction projects. In prior years, some payments relating to interest expense were capitalized. These same costs are now shown as interest expense. In addition, the University increased the principal payments on debt by $5.3 million. This increase was the result of the University’s debt repayment strategies. Bonds issued in 2012 were structured to begin principal repayments in 2016, aligning payments with generation of corresponding pledged revenue.

Net cash used in investing activities increased by $149.6 million. Although the University received an additional $237.5 million from the proceeds from the sale and maturities of investments, the University utilized $388.6 million in the purchasing of new investments. The remaining increase of $1.5 million was attributable to investment income receipts. Economic factors that will affect the futureWhile the University is impacted by the general economic conditions, management believes the University will continue its high level of excellence in service to students, sponsors, the State of Alabama, and

Statement of Cash FlowsThe Statement of Cash Flows presents information about changes in the University’s cash position using the direct method of reporting sources and uses of cash. The direct method reports all major gross cash inflows and outflows, differentiating these activities into operating activities; noncapital financing, such as nonexchange grants and

contributions; capital and related financing, including bond proceeds from debt issued to purchase or construct buildings; and investing activities. Operating activity uses of cash significantly exceed operating activity sources of cash due to classification of state appropriations and gifts as noncapital financing activities.

The University’s cash flows are summarized below:

2015 2014

Net cash provided by (used in): Operating activities $ (156,592,736) $ (167,488,580) Noncapital financing activities 313,173,218 301,397,720 Capital and related financing activities (127,591,944) (125,797,480) Investing activities (91,707,514) 57,846,593

Net (decrease) increase in cash (62,718,976) 65,958,253 Cash and cash equivalents - beginning of year 137,388,965 71,430,712

Cash and cash equivalents - end of year $ 74,669,989 $ 137,388,965

other constituents. The University’s strong financial position and internal planning processes provide the University some protection against funding reductions and adverse economic conditions. Nonetheless, future reductions in state support must be anticipated and managed carefully to maintain excellence. Neither external nor internal efforts to mitigate the impact, however, are intended to eliminate the effects of future proration or decrease in state funding. As a labor intensive organization, the University faces competitive pressures related to attracting and retaining faculty and staff. The rising cost of health care remains a concern, particularly in light of the post-retirement health care benefits offered to retirees.

The University continues to address aging facilities with significant new construction, as well as modernization and renovation of existing facilities. Although funding of these projects through gifts, federal and state funds, and deferred maintenance budget allocations continues, the costs of operating the new and renovated facilities will continue to place additional resource demands on the operating budget of the institution.

The University continues to take steps to enhance student recruitment, both in marketing efforts and in providing additional scholarship funding. Applications, acceptances, and retention are monitored closely to assess the potential impact of general economic conditions on future enrollment. Management is cautiously optimistic that demand will remain strong.

The University will continue to employ its long-term investment strategy to maximize total returns at an appropriate level of risk, while utilizing a spending rate policy to insulate the University’s operations from temporary market volatility. Preservation of capital is regarded as the highest priority in the investing of the cash pool. Diversification through asset allocation is utilized as a fundamental risk strategy for endowed funds.

Cautionary note regarding forward-looking statements Certain information provided by the University, including written, as outlined above, or oral statements made by its representatives, may contain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, which address activities, events, or developments that the University expects or anticipates will or may occur in the future, contain forward-looking information.

In reviewing such information, it should be kept in mind that actual results may differ materially from those projected or suggested in such forward looking information. This forward-looking information is based upon various factors and was derived using various assumptions.

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Aub

urn U

nive

rsity

201

5

18

UNDERGRADUATE TUITION FOR THE ACADEMIC YEAR2011-12 2012-13 2013-14 2014-15 2015-16

Auburn Main Campus/Auburn University at Montgomery

Full Time Students: In-State $8,698/$7,580 $9,446/$8,115 $9,852/$8,750 $10,200/$9,080 $10,424/$9,350

Out-of-State $23,290/$21,440 $25,190/$23,115 $26,364/$24,950 $27,384/$19,640 $28,040/$20,210

FALL STUDENT ENROLLMENT2011 2012 2013 2014 2015

Auburn Main Campus andAuburn University at Montgomery

Undergraduate and Professional 24,849 24,400 24,133 25,006 26,043

Graduate 5,925 5,723 5,827 5,963 6,163

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

DEGREES AWARDED FOR THE ACADEMIC YEAR2010-11 2011-12 2012-13 2013-14 2014-15

Auburn Main Campus andAuburn University at Montgomery

Bachelor 4,800 4,833 4,834 5,090 5,115

Advanced 1,809 1,922 1,835 1,869 1,905

506 498 499 498

485

437

467 471 473 453

316 310 294 294

317

109 112 111 130 125

11 7 9 16 17

0

100

200

300

400

500

600

FALL 2011 FALL 2012 FALL 2013 FALL 2014 FALL 2015

Nu

mb

er o

f F

acu

lty

Term

AUBURN UNIVERSITY MAIN CAMPUS AND AUBURN UNIVERSITY AT MONTGOMERY

FULL-TIME FACULTY BY RANK

Professor Associate Professor Assistant Professor Instructor Visiting

AUBURN UNIVERSITY MAIN CAMPUS AND AUBURN UNIVERSITY AT MONTGOMERYFULL-TIME FACULTY BY RANK

Aub

urn U

nive

rsity

201

5

19

AUBURN UNIVERSITY MAIN CAMPUS FRESHMENENROLLMENT BY ALABAMA COUNTIES

SUMMER/FALL TERMS 2015

SOURCES OF ENTERING FRESHMEN BY STATEMAIN CAMPUS SUMMER/FALL TERMS 2015

AUBURN UNIVERSITY MAIN CAMPUS TOTAL STUDENT CREDIT HOURS BY COLLEGE/SCHOOL 2014-15

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

80,410

64,282

81,999

74,960

60,261

26,832

26,106

20,616

21,498

17,789

16,484

11,964

4,823

115,929

83,774

1,236

369

0 50,000 100,000 150,000 200,000 250,000

Liberal Arts

Sciences & Mathematics

Business

Engineering

Education

Human Sciences

Architecture, Design & Construction

Pharmacy

Veterinary Medicine

Agriculture

Other

Nursing

Forestry & Wildlife Sciences

Number of Credit Hours

College/School

AUBURN UNIVERSITY MAIN CAMPUS TOTAL STUDENT CREDIT HOURS BY COLLEGE/SCHOOL 2014-15

Other Courses

Core Courses

Alabama 59%

Georgia 14%

Florida 6%

Tennessee 3%

Texas 3%

North Carolina 2%

Other Locations 13%

Sources of Entering Freshmen by State Main Campus Summer/Fall Terms 2015

Jefferson 18%

Madison 15%

Shelby 11%

Lee 9%

Montgomery 5%

Mobile 5%

Baldwin 5%

Other 32%

Auburn University Main Campus Freshmen Enrollment by Alabama Counties

Summer/Fall Terms 2015

Aub

urn U

nive

rsity

201

5

20

AUBURN UNIVERSITYFIVE YEAR HIGHLIGHTS (MILLIONS OF DOLLARS)FOR THE FISCAL YEARS ENDED SEPTEMBER 30

2011 2012 2013 2014 2015

Revenues by Source Tuition and fees $ 294.7 $ 323.1 $ 349.2 $ 365.9 $ 395.6 Federal appropriations 38.8* 11.8 13.0 12.9 14.3 State appropriations 235.7 247.8 238.6 243.0 245.5 Grants and contracts, net 136.6 134.5 121.1 118.4 120.5 Gifts 32.3 36.6 35.4 36.6 43.9 Capital gifts and grants 48.2 17.2 28.2 3.8 4.8 Sales and services, investments and other income, net of interest expense

58.8 72.8 60.7 89.2 83.6

Sales and services of auxiliary enterprises 106.2 101.5 104.8 123.4 136.3 Total Revenues by Source $ 951.3 $ 945.3 $ 951.0 $ 993.2 $ 1,044.5

Expenditures by Function Instruction $ 230.4 $ 239.5 $ 242.6 $ 249.0 $ 254.6 Research 102.8 102.6 97.4 99.2 97.3 Public service 106.0 107.4 104.7 102.5 106.7 Academic support 38.8 38.8 43.7 53.3 55.4 Library 8.3 10.1 8.3 9.7 9.0 Student services 23.6 24.9 27.6 30.2 33.0 Institutional support 74.1 73.3 70.0 70.5 78.5 Operation and maintenance 77.8 66.3 84.5 78.8 78.8 Scholarships and fellowships 33.7 35.0 39.5 40.2 39.3 Auxiliary enterprises 102.5 99.1 106.9 123.1 122.6 Depreciation 53.8 61.1 66.1 71.8 74.3

Total Expenditures by Function $ 851.8 $ 858.1 $ 891.3 $ 928.3 $ 949.5

Expenditures by Natural Classification Compensation & benefits $ 536.6 $ 539.2 $ 558.0 $ 578.2 $ 598.4 Scholarships & fellowships 17.3 18.4 21.6 22.7 20.7 Utilities 23.3 23.2 22.8 26.0 24.5 Other supplies and services 220.8 216.2 222.8 229.6 231.6 Depreciation 53.8 61.1 66.1 71.8 74.3

Total Expenditures by Natural Classification $ 851.8 $ 858.1 $ 891.3 $ 928.3 $ 949.5

*Includes appropriation from The American Recovery and Reinvestment Act of 2009.

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Aub

urn U

nive

rsity

201

5

21

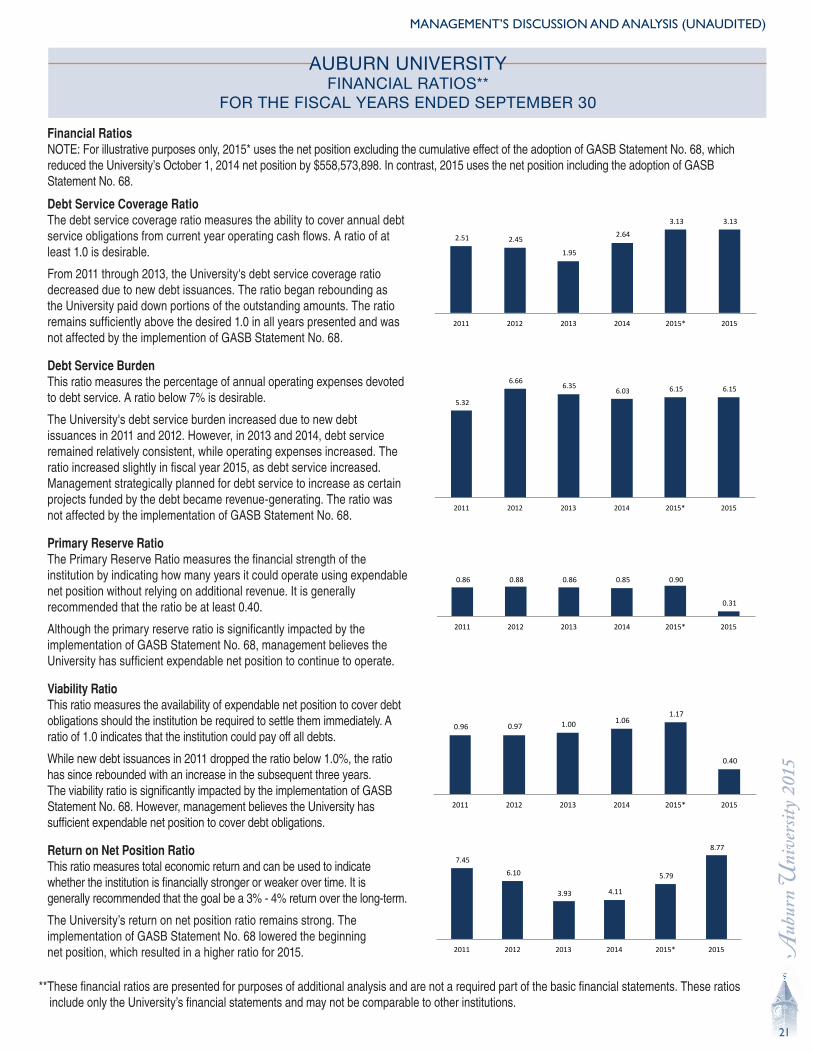

AUBURN UNIVERSITYFINANCIAL RATIOS**

FOR THE FISCAL YEARS ENDED SEPTEMBER 30

Debt Service Coverage Ratio The debt service coverage ratio measures the ability to cover annual debt service obligations from current year operating cash flows. A ratio of at least 1.0 is desirable.

From 2011 through 2013, the University's debt service coverage ratio decreased due to new debt issuances. The ratio began rebounding as the University paid down portions of the outstanding amounts. The ratio remains sufficiently above the desired 1.0 in all years presented and was not affected by the implemention of GASB Statement No. 68.

Debt Service Burden This ratio measures the percentage of annual operating expenses devoted to debt service. A ratio below 7% is desirable.

The University's debt service burden increased due to new debt issuances in 2011 and 2012. However, in 2013 and 2014, debt service remained relatively consistent, while operating expenses increased. The ratio increased slightly in fiscal year 2015, as debt service increased. Management strategically planned for debt service to increase as certain projects funded by the debt became revenue-generating. The ratio was not affected by the implementation of GASB Statement No. 68.

Primary Reserve Ratio The Primary Reserve Ratio measures the financial strength of the institution by indicating how many years it could operate using expendable net position without relying on additional revenue. It is generally recommended that the ratio be at least 0.40.

Although the primary reserve ratio is significantly impacted by the implementation of GASB Statement No. 68, management believes the University has sufficient expendable net position to continue to operate.

Viability Ratio This ratio measures the availability of expendable net position to cover debt obligations should the institution be required to settle them immediately. A ratio of 1.0 indicates that the institution could pay off all debts.

While new debt issuances in 2011 dropped the ratio below 1.0%, the ratio has since rebounded with an increase in the subsequent three years. The viability ratio is significantly impacted by the implementation of GASB Statement No. 68. However, management believes the University has sufficient expendable net position to cover debt obligations.

Return on Net Position Ratio This ratio measures total economic return and can be used to indicate whether the institution is financially stronger or weaker over time. It is generally recommended that the goal be a 3% - 4% return over the long-term.

The University’s return on net position ratio remains strong. The implementation of GASB Statement No. 68 lowered the beginning net position, which resulted in a higher ratio for 2015.

Financial Ratios NOTE: For illustrative purposes only, 2015* uses the net position excluding the cumulative effect of the adoption of GASB Statement No. 68, which reduced the University’s October 1, 2014 net position by $558,573,898. In contrast, 2015 uses the net position including the adoption of GASB Statement No. 68.

**These financial ratios are presented for purposes of additional analysis and are not a required part of the basic financial statements. These ratios include only the University’s financial statements and may not be comparable to other institutions.

2.51 2.45

1.95

2.64

3.13 3.13

2011 2012 2013 2014 2015* 2015

5.32

6.66 6.35

6.03 6.15 6.15

2011 2012 2013 2014 2015* 2015

0.86 0.88 0.86 0.85 0.90

0.31

2011 2012 2013 2014 2015* 2015

0.96 0.97 1.00 1.06 1.17

0.40

2011 2012 2013 2014 2015* 2015

7.45

6.10

3.93 4.11

5.79

8.77

2011 2012 2013 2014 2015* 2015

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

Aub

urn U

nive

rsity

201

5

22

AUBURN UNIVERSITYSTATEMENTS OF NET POSITIONSEPTEMBER 30, 2015 AND 2014

2015 2014ASSETS Current assets Cash and cash equivalents $ 74,669,989 $ 137,388,965 Operating investments 29,488,110 45,171,928 Accounts receivable, net 45,263,204 37,295,056 Student accounts receivable, net 41,267,044 37,346,662 Loans receivable, net 2,969,077 2,555,991 Accrued interest receivable 2,138,158 1,814,348 Inventories 4,861,123 4,599,906 Prepaid expenses 36,040,919 35,235,961 Total current assets 236,697,624 301,408,817

Noncurrent assets Investments 978,782,993 844,273,591 Loans receivable, net 17,041,018 17,116,551 Investment in plant, net 1,560,193,650 1,550,144,298 Total noncurrent assets 2,556,017,661 2,411,534,440 Total assets 2,792,715,285 2,712,943,257

DEFERRED OUTFLOWS OF RESOURCES Loss on refunding of bonds 26,953,797 14,442,185 Pension 53,229,926 - Total deferred outflows 80,183,723 14,442,185

LIABILITIES Current liabilities Accounts payable 52,709,497 55,670,506 Accrued salaries and wages 3,501,872 3,025,472 Accrued compensated absences 19,023,576 18,347,365 Accrued interest payable 11,677,978 12,298,575 Other accrued liabilities 5,449,261 8,344,327 Student deposits 2,866,239 3,068,492 Deposits held in custody 20,133,089 19,900,249 Unearned revenues 199,551,845 184,309,364 Noncurrent liabilities-current portion 30,253,504 28,817,852 Total current liabilities 345,166,861 333,782,202

Noncurrent liabilities Bonds and notes payable 699,839,916 716,188,582 Pension and OPEB 588,439,539 16,232,518 Other noncurrent liabilities 21,345,126 18,592,502 Total noncurrent liabilities 1,309,624,581 751,013,602 Total liabilities 1,654,791,442 1,084,795,804

DEFERRED INFLOWS OF RESOURCES Nonexchange transactions 206,159 435,203 Pension 39,307,330 - Total deferred inflows 39,513,489 435,203

NET POSITION Net investment in capital assets 855,698,812 821,520,355 Restricted Nonexpendable 28,537,859 28,176,521 Expendable: Scholarships, research, instruction, other 167,933,215 151,931,724 Loans 5,171,064 5,013,550 Capital projects 4,378,922 5,220,606 Unrestricted 116,874,205 630,291,679 Total net position $ 1,178,594,077 $ 1,642,154,435

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

23

AUBURN UNIVERSITYSTATEMENTS OF REVENUES, EXPENSES AND CHANGES IN NET POSITION

FOR THE YEARS ENDED SEPTEMBER 30, 2015 AND 2014

2015 2014OPERATING REVENUES Tuition & fees, net of scholarship allowances of $104,855,468 and $107,695,483, respectively $ 395,612,498 $ 365,946,812 Federal appropriations 14,304,014 12,888,064 Federal grants & contracts, net 65,197,789 65,480,729 State & local grants & contracts, net 18,137,344 16,025,884 Nongovernmental grants & contracts, net 14,533,400 14,871,312 Sales & services of educational departments 44,393,576 42,072,042 Auxiliary revenue, net of scholarship allowances of $8,113,771 and $7,041,111, respectively 136,309,769 123,401,308 Other operating revenues 30,026,559 23,223,001 Total operating revenues 718,514,949 663,909,152

OPERATING EXPENSES Compensation & benefits 598,404,935 578,242,854 Scholarships & fellowships 20,739,919 22,651,077 Utilities 24,520,336 26,003,836 Other supplies & services 231,559,648 229,604,057 Depreciation 74,297,440 71,795,613 Total operating expenses 949,522,278 928,297,437

Operating loss (231,007,329) (264,388,285)

NONOPERATING REVENUES (EXPENSES) State appropriations 245,502,175 242,982,031 Gifts 43,862,924 36,622,346 Grants 22,620,365 22,037,644 Net investment income 27,441,880 38,843,549 Interest expense on capital debt (18,597,132) (15,435,498) Nonoperating revenues, net 320,830,212 325,050,072

Income before other changes in net position 89,822,883 60,661,787

OTHER CHANGES IN NET POSITION Capital appropriations - 16,585 Capital gifts & grants 4,829,319 3,729,932 Additions to permanent endowments 361,338 479,958 Net increase in net position 95,013,540 64,888,262

Net position - beginning of year 1,642,154,435 1,577,266,173 Cumulative effect of accounting change (558,573,898)Net position October 1, 2014, as restated 1,083,580,537Net position - end of year $ 1,178,594,077 $ 1,642,154,435

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

24

AUBURN UNIVERSITYSTATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED SEPTEMBER 30, 2015 AND 2014

2015 2014CASH FLOWS FROM OPERATING ACTIVITIES Tuition & fees $ 401,863,262 $ 373,885,655 Federal appropriations 13,398,839 11,822,841 Grants & contracts 88,102,237 107,445,031 Sales & services of educational departments 42,390,578 41,765,348 Auxiliary revenue 144,934,497 119,881,121 Other operating revenues 30,698,728 23,686,105 Payments to suppliers (234,889,869) (222,067,887) Payments for utilities (24,520,336) (26,003,836) Payments for employee compensation & benefits (596,775,639) (574,905,901) Payments for scholarships & fellowships (21,286,355) (22,507,092) Student loans issued (3,872,655) (3,397,962) Student loans collected 3,363,977 2,907,997 Net cash used in operating activities (156,592,736) (167,488,580)

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES State appropriations 245,502,175 242,982,031 Gifts and grants for other than capital purposes 66,738,081 59,170,269 Direct and other loan receipts 198,010,171 177,467,924 Direct and other loan disbursements (197,077,209) (178,222,504) Net cash provided by noncapital financing activities 313,173,218 301,397,720

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES Proceeds from advanced refunding of debt, net of issuance cost 171,240,220 75,346,556 Capital appropriations - 16,585 Capital grants & gifts received 2,544,239 4,611,200 Purchases of capital assets (82,628,205) (93,052,995) Proceeds received from sale of capital assets 308,735 81,250 Principal paid on debt & capital leases (24,863,361) (19,596,314) Interest paid on debt & capital leases (39,373,572) (25,503,762) Payment to escrow on advanced refunding of debt (154,820,000) (67,700,000) Net cash used in capital and related financing activities (127,591,944) (125,797,480)

CASH FLOWS FROM INVESTING ACTIVITIES Proceeds from sales and maturities of investments and reinvestments 600,620,269 363,116,309 Investment income 20,924,830 19,419,490 Purchases of investments (713,252,613) (324,689,206) Net cash (used in) provided by investing activities (91,707,514) 57,846,593

Net (decrease) increase in cash and cash equivalents (62,718,976) 65,958,253

Cash and cash equivalents - beginning of year 137,388,965 71,430,712

Cash and cash equivalents - end of year $ 74,669,989 $ 137,388,965

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

25

AUBURN UNIVERSITYSTATEMENTS OF CASH FLOWS (CONTINUED)

FOR THE YEARS ENDED SEPTEMBER 30, 2015 AND 2014

2015 2014RECONCILIATION OF OPERATING LOSS TO NET CASH USED IN OPERATING ACTIVITIES:

Operating loss $ (231,007,329) $ (264,388,285) Adjustments to reconcile operating loss to net cash used in operating activities: Depreciation and amortization 74,297,440 71,795,613 Reserve for recovery of loans receivable 171,125 224,464 Loss on sale of capital assets 2,160,182 1,894,750 Changes in assets and liabilities: Accounts receivable (8,326,852) 6,747,315 Student accounts receivable (3,920,382) (2,986,486) Inventories (261,217) (82,414) Unearned revenues 15,242,481 10,445,588 Accounts payable (4,400,835) 4,791,721 Prepaid expenses (804,958) 17,492 Accrued salaries, wages and compensated absences 1,152,611 1,203,266 Student deposits and deposits held in custody (902,375) 24,548 Loans to students (508,678) (489,965) Other accrued liabilities (2,895,066) 644,363 Nonexchange transactions (229,044) 88,209 Pension obligation (2,062,054) - Other noncurrent liabilities 5,702,215 2,581,241 Net cash used in operating activities $ (156,592,736) $ (167,488,580)

SUPPLEMENTAL NONCASH ACTIVITIES INFORMATION

Capital assets acquired with a liability at year-end $ 4,674,497 $ 3,234,671 Gifts of capital assets 2,750,330 2,385,618 Capitalized interest 12,535,730 18,485,556

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

26

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF FINANCIAL POSITION

SEPTEMBER 30, 2015 AND 2014

Auburn University Foundation Auburn Alumni Association2015 2014 2015 2014

ASSETS Cash and cash equivalents $ 10,226,894 $ 3,349,824 $ 20,729 $ 72,071 Investments 421,516,863 418,046,081 4,357,167 4,776,518 Investment in Auburn University Foundation Securities Pool - - 8,210,325 8,989,525 Accrued interest receivable 107,808 79,593 17,423 20,431 Contributions receivable, net 105,082,407 68,585,013 297,820 357,720 Other assets 27,773 6,467 - 34 Investment in real estate 3,200,304 4,074,251 674,799 674,799 Cash surrender value of life insurance 5,588,166 5,082,046 - - Beneficial interest in outside trusts 5,205,119 5,405,637 - - Property and equipment, net 189,941 218,706 1,885,632 1,943,453 Prepaid items - - 270 5,025 Due from Auburn University 545,454 260,860 - - Due from Auburn University Foundation - - 379 - Due from Auburn Alumni Association 639,500 - - - Total assets $ 552,330,229 $ 505,108,478 $ 15,464,544 $ 16,839,576

LIABILITIES Accounts payable and accrued liabilities $ 500,357 $ 423,320 $ 63,839 $ 102,396 Annuities payable 9,424,128 8,637,277 - - Due to Auburn University 109,533 168,834 75,559 - Due to Auburn University Foundation - - 641,043 452,369 Due to Auburn Alumni Association 8,210,325 8,989,525 - - Due to Tigers Unlimited Foundation 8,047,688 8,606,643 - - Deferred revenue 94,151 1,126 8,476,549 8,391,185 Total liabilities 26,386,182 26,826,725 9,256,990 8,945,950

NET ASSETS Unrestricted 19,619,387 23,015,641 6,207,554 7,893,626 Temporarily restricted 144,144,939 123,459,727 - - Permanently restricted 362,179,721 331,806,385 - - Total net assets 525,944,047 478,281,753 6,207,554 7,893,626 Total liabilities and net assets $ 552,330,229 $ 505,108,478 $ 15,464,544 $ 16,839,576

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

27

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

FOR THE YEARS ENDED SEPTEMBER 30, 2015 AND 2014

Auburn University Foundation Auburn Alumni Association2015 2014 2015 2014

REVENUES AND OTHER SUPPORT Public support - contributions $ 108,542,846 $ 65,670,616 $ 1,578,527 $ 2,374,133 Investment income 1,768,469 2,511,539 369,014 352,191 Other revenues 2,345,413 2,037,897 897,123 881,262 Total operating revenues 112,656,728 70,220,052 2,844,664 3,607,586

EXPENSES AND LOSSES Program services Contributions to and support for Auburn University 36,885,661 31,503,530 - - Other program services 3,264,551 3,403,546 2,140,300 1,778,184 Total program services 40,150,212 34,907,076 2,140,300 1,778,184

Support services General and administrative 1,675,940 1,505,924 1,466,443 1,439,651 Fund raising 3,291,330 2,890,611 202,302 259,264 Total support services 4,967,270 4,396,535 1,668,745 1,698,915 Total expenses 45,117,482 39,303,611 3,809,045 3,477,099

Unrealized losses (gains) on investments 23,590,805 (17,822,794) 721,691 (568,822) Realized gains on investments (5,481,835) (16,003,747) - - Change in valuation of split-interest agreements 1,742,862 (1,602,085) - - Impairment in real estate 25,120 23,234 - - Total expenses, (gains) and losses 64,994,434 3,898,219 4,530,736 2,908,277

*Change in net assets 47,662,294 66,321,833 (1,686,072) 699,309

Net assets - beginning of year 478,281,753 411,959,920 7,893,626 7,194,317

Net assets - end of year $ 525,944,047 $ 478,281,753 $ 6,207,554 $ 7,893,626

*Change in net assets Unrestricted $ (3,396,254) $ 2,491,520 $ (1,686,072) $ 699,309 Temporarily restricted 20,685,212 29,700,243 - - Permanently restricted 30,373,336 34,130,070 - - Total change in net assets $ 47,662,294 $ 66,321,833 $ (1,686,072) $ 699,309

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

28

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF FINANCIAL POSITION

JUNE 30, 2015 AND 2014

Tigers Unlimited FoundationTigers Unlimited FoundationTigers Unlimited Foundation Tigers Unlimited Foundation2015 2014

ASSETS

Cash and cash equivalents $ 1,412,961 $ 756,174 Investments 39,440,159 36,013,989 Investment in Auburn University Foundation Securities Pool 8,542,039 8,629,832 Due from Auburn University 36,800 - Accrued interest receivable 105,043 95,311 Contributions receivable, net 10,833,485 10,726,457 Other receivables 412,063 614,125 Other assets 195,459 175,967 Property and equipment, net 17,617 91,129 Total assets $ 60,995,626 $ 57,102,984

LIABILITIES Accounts payable and accrued liabilities $ 462,449 $ 665,088 Contracts payable, net 5,467,368 6,719,759 Deferred revenue 2,379,824 1,872,870 Due to Auburn University 5,693,143 2,943,300 Due to Auburn University Foundation 165,000 - Total liabilities 14,167,784 12,201,017

NET ASSETS Unrestricted 23,614,005 22,862,847 Temporarily restricted 16,060,965 14,919,083 Permanently restricted 7,152,872 7,120,037 Total net assets 46,827,842 44,901,967 Total liabilities and net assets $ 60,995,626 $ 57,102,984

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

29

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

FOR THE YEARS ENDED JUNE 30, 2015 AND 2014

Tigers Unlimited FoundationTigers Unlimited FoundationTigers Unlimited Foundation Tigers Unlimited Foundation2015 2014

REVENUES AND OTHER SUPPORT Public support - contributions $ 40,117,708 $ 37,870,989 Investment income 765,225 714,044 Other revenues 6,080,997 5,823,499 Total operating revenues 46,963,930 44,408,532

EXPENSES AND LOSSES Program services Contributions to and support for Auburn University 16,756,982 17,217,019 Other program services 17,644,565 17,531,732 Total program services 34,401,547 34,748,751

Support services General and administrative 1,645,433 1,235,573 Fund raising 8,064,233 7,847,297 Total support services 9,709,666 9,082,870 Total expenses 44,111,213 43,831,621

Unrealized gains on investments, net (109,901) (1,319,406) Realized losses on investments, net 641 228 Loss on write-off of contribution receivable 1,036,102 1,969,702 Total expenses, (gains) and losses 45,038,055 44,482,145

*Change in net assets 1,925,875 (73,613)

Net assets - beginning of year 44,901,967 44,975,580

Net assets - end of year $ 46,827,842 $ 44,901,967

*Change in net assets Unrestricted $ 751,158 $ (151,084) Temporarily restricted 1,141,882 (70,480) Permanently restricted 32,835 147,951 Total change in net assets $ 1,925,875 $ (73,613)

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

30

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF FINANCIAL POSITION

SEPTEMBER 30, 2015 AND 2014

Tigers Unlimited FoundationTigers Unlimited FoundationAuburn Research and Technology Foundation2015 2014

ASSETS

Cash and cash equivalents $ 898,777 $ 731,782 Deposits 40,836 42,143 Other assets 22,051 26,886 Accounts receivable 788,789 349,836 Contributions receivable, net 1,015,948 1,070,336 Property and equipment, net 8,242,346 8,549,672 Total assets $ 11,008,747 $ 10,770,655

LIABILITIES Accounts payable $ 134,590 $ 68,353 Deferred revenue 201,375 184,955 Deposits held in custody 40,836 42,143 Interest payable 34,972 36,478 Loan payable to Auburn University 841,305 877,548 Other payable to Auburn University 225,705 110,102 Total liabilities 1,478,783 1,319,579

NET ASSETS Unrestricted 8,513,975 8,380,699 Temporarily restricted 1,015,989 1,070,377 Total net assets 9,529,964 9,451,076 Total liabilities and net assets $ 11,008,747 $ 10,770,655

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

31

AUBURN UNIVERSITY COMPONENT UNITSSTATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

FOR THE YEARS ENDED SEPTEMBER 30, 2015 AND 2014

Auburn Research and Technology Foundation2015 2014

REVENUES AND OTHER SUPPORT Rental income $ 1,044,682 $ 982,030 Interest income 20,855 - Other contracts 536,735 266,654 Contributions 27,639 24,702 Total operating revenues 1,629,911 1,273,386

EXPENSES Support services General and administrative 1,133,438 838,562 Amortization 65,026 65,026 Depreciation 316,769 317,894 Interest 35,790 37,328 Total support services 1,551,023 1,258,810 Total expenses 1,551,023 1,258,810

*Change in net assets 78,888 14,576

Net assets - beginning of year 9,451,076 9,436,500

Net assets - end of year $ 9,529,964 $ 9,451,076

*Change in net assets Unrestricted $ 133,276 $ 71,683 Temporarily restricted (54,388) (57,107) Total change in net assets $ 78,888 $ 14,576

See accompanying notes to financial statements.

Aub

urn U

nive

rsity

201

5

32

NOTES TO FINANCIAL STATEMENTS (1) NATURE OF OPERATIONSAuburn University (the University) is a land grant university originally chartered on February 1, 1856, as the East Alabama Male College. The Federal Land Grant Act of 1862, by which the University was established as a land grant university, donated public lands to several states and territories with the intent that the states would use these properties for the benefit of agriculture and the mechanical arts. Several pertinent laws dictate specific purposes for which the land may be used. In 1960, the Alabama State Legislature officially changed the name to Auburn University. The University has two campuses, Auburn and Montgomery, with a combined enrollment of 32,206 students for Fall semester 2015. The University serves the State of Alabama, the nation and international business communities through instruction of students and the advancement of research and outreach programs. By statutory laws of the State of Alabama, the University is governed by the Board of Trustees (the Board) who are appointed by the Governor of Alabama, a committee consisting of two trustees and two Alumni Association board members and approved by the Alabama State Senate.

The accompanying financial statements of the University have been prepared in accordance with accounting principles generally accepted in the United States of America, as prescribed by the Governmental Accounting Standards Board (GASB). The accompanying financial statements include the following four divisions of the University:

Auburn University Main CampusAuburn University at MontgomeryAlabama Agricultural Experiment StationAlabama Cooperative Extension System

The University, a publicly supported, state funded institution, is a component unit of the State of Alabama and is included in the Comprehensive Annual Financial Report of the State. However, the University is considered a separate reporting entity for financial statement purposes.

The University, as a public corporation and instrumentality of the State of Alabama, is exempt from federal income taxes under Section 115 of the Internal Revenue Code. Certain transactions may be taxable as unrelated business income under Internal Revenue Code Sections 511 to 514.

Contributions intended for the University’s benefit are primarily received through the University’s component units and are deductible by donors as provided under Section 170 of the Internal Revenue Code, consistent with the provisions under Section 501(c)(3) and corresponding state law.

Component UnitsThe University adheres to GASB Statement No. 39, Determining Whether Certain Organizations Are Component Units-an amendment of GASB Statement No. 14. This statement clarifies GASB Statement No. 14, The Financial Reporting Entity, which provides criteria for determining whether such organizations for which a government is not financially accountable should be reported as component units. In accordance with GASB Statement No. 61, The Financial Reporting Entity: Omnibus –an Amendment of GASB Statements No. 14 and No. 34, the University has included statements for Auburn University Foundation, Auburn Alumni Association, Tigers Unlimited Foundation and Auburn Research and Technology Foundation in these financial statements, as exclusion