![RUSSELL INVESTMENTS? - SIIA...By the time you read this sentence, Russell Investments may be no more. 1NaW]ZMIL\PQ[QV6W^MUJMZ :][[MTT_QTTTQSMTaZMUIQV_PI\Q\[W{KQITJQWOZIXPaKTIQU[Q\\W](https://static.fdocuments.net/doc/165x107/5fa1020ebceb0c53e64c4f04/russell-investments-by-the-time-you-read-this-sentence-russell-investments.jpg)

Financial Professional outlook - Russell Investments

27

Financial Professional Outlook THE QUEST FOR A SUSTAINABLE ADVISORY BUSINESS: How advisors are adapting their businesses to address regulatory, industry and competitive pressures in 2016. Q1 2016 TRACKING THE OPINIONS, CONVERSATIONS AND MARKET SENTIMENT OF U.S. FINANCIAL ADVISORS SINCE 2010.

Transcript of Financial Professional outlook - Russell Investments

Financial Professional OutlookTHE QUEST FOR A SUSTAINABLE ADVISORY BUSINESS: How advisors are adapting their businesses to address regulatory, industry and competitive pressures in 2016.

Q1 2016

TRACKING THE OPINIONS, CONVERSATIONS AND MARKETSENTIMENT OF U.S. FINANCIAL ADVISORS SINCE 2010.

The latest Financial Professional Outlook (FPO) survey was fi elded from February 5, 2016 to February 19, 2016. During that time we heard from 258 fi nancial advisors working for 228 investment fi rms nationwide. › In this survey, we asked important questions about issues and topics

that concern fi nancial professionals the most.

› We also provide key data insights on what advisors are thinking now and our perspective on these challenges and potential solutions.

p / 2Russell Investments // Financial Professional Outlook

In this Q1 2016 edition of the FPO, we explored how advisors are addressing key challenges in an environment that is heavily impacted by:› Increasing market volatility.

› The proposed Department of Labor (DOL) Fiduciary Standard.

› Changing demographics of investors.

› A low return and rising interest rate environment.

All of the above are impacting advisors’ overall business sustainability and manageability in the long-term.

Q1 2016The quest for a sustainable advisory business: How advisors are adapting their businesses to address regulatory, industry and competitive pressures in 2016.

p / 3Russell Investments // Financial Professional Outlook

How are advisors and their clients feeling about market shifts and regulatory changes?

p / 4Russell Investments // Financial Professional Outlook

Volatility and uncertainty weigh on market sentiment again.› In each edition of the Financial Professional Outlook survey (FPO),

we ask advisors how optimistic or pessimistic they feel about the performance of the capital markets over the next three years. We also ask advisors to assess how they think their clients feel about the markets over that time period.

› According to surveyed advisors, the percentage of investors who feel pessimistic about the markets over the next three years rose from 22% to 29% over the past quarter, and 55% of them still continue to feel uncertain.

p / 5Russell Investments // Financial Professional Outlook

MARKET SENTIMENT INDEX—INVESTORS

Throughout the life of the survey, the largest percentage of advisors answering this question have always said clients are “uncertain,” and this continues in the latest survey.RUSSELL INVESTMENTS’ PERSPECTIVE:

› We think investors are likely reacting to trends such as market volatility, falling commodity prices and divergent global markets.

› Investors may also be swayed by the recency bias2 of the low returns in 2015 and the volatile markets experienced so far in 2016.

0-100 +100

UNCERTAINSLIGHTLYPESSIMISTIC

SLIGHTLYOPTIMISTIC

EXTREMELYOPTIMISTIC

EXTREMELYPESSIMISTIC

3-MONTH TRENDMOVING NEGATIVE

-13

INVESTOR

In general, how optimistic or pessimistic are your clients about capital markets over the next three years?How are investors feeling?

Investor Sentiment Index1 dropped into negative territory.

1 The Sentiment Index provides a point-in-time measurement of advisor and investor sentiment about capital markets over the next three years. The Sentiment Index takes into account both those who are optimistic and those who are pessimistic, and is calculated in this way: Sentiment Index = (% of group that is optimistic) – (% of group that is pessimistic).

2 Recency bias is the tendency to think that trends and patterns we observe in the recent past will continue in the future.

ON A -100 to +100 POINT RANGE

Investor sentiment since 1Q14

0

16 13

3

-13

1Q14 2Q14 3Q14 2Q15 4Q15 1Q16

15

p / 6Russell Investments // Financial Professional Outlook

MARKET SENTIMENT INDEX—ADVISORS

› Contrary to the pessimism about the markets that advisors observe in their clients, 67% of advisors who responded to our Q1 survey are more optimistic about the capital markets over the next three years.

RUSSELL INVESTMENTS’ PERSPECTIVE:

› Advisors are not adversely reacting to the recent volatility and are still closely watching the markets, which is a good sign. They are likely prepared for continuing volatility through 2016—and they don’t necessarily see this as a red fl ag, but more of an opportunity.

0-100 +100

UNCERTAINSLIGHTLYPESSIMISTIC

SLIGHTLYOPTIMISTIC

EXTREMELYOPTIMISTIC

EXTREMELYPESSIMISTIC

3-MONTH TRENDMOVING POSITIVE

51

ADVISOR

In general, how optimistic or pessimistic are you about capital markets over the next three years?How are advisors feeling?

What keeps the Advisor Sentiment Index positive when the Investor Sentiment Index is negative?

ON A -100 to +100 POINT RANGE

81

Advisor sentiment since 1Q14

71 69

54

45 51

1Q14 2Q14 3Q14 2Q15 4Q15 1Q16

p / 7Russell Investments // Financial Professional Outlook

› In the case of sentiment, our research has shown a persistent gap between advisors’ optimism about capital markets over the next three years and their clients’ continuing uncertainty and pessimism.

RUSSELL INVESTMENTS’ PERSPECTIVE:

› According to our 2Q 2016 Global Market Outlook report, we expect volatility to be a headline throughout 2016—which may lead investors to remain uncertain about the equity markets. However, we’re not forecasting a sustained bear market—provided the U.S. does not fall into recession. We think equity growth is likely to be in the low single digits, along with a gradual rise in long-term interest rates.

0-100 +100

UNCERTAINSLIGHTLYPESSIMISTIC

SLIGHTLYOPTIMISTIC

EXTREMELYOPTIMISTIC

EXTREMELYPESSIMISTIC

3-MONTH TRENDMOVING NEGATIVE

3-MONTH TRENDMOVING POSITIVE

-13 51

INVESTOR ADVISOR

In general, how optimistic or pessimistic are you and your clients about capital markets over the next three years?How do advisors and investors compare this quarter?

p / 8Russell Investments // Financial Professional Outlook

› The two Sentiment Indexes over the past quarter show advisors' optimism and investors' pessimism are both increasing and the gap in their outlook continues to widen.

› The real questions we all have to ask are—what will the two Sentiment Indexes look like a quarter from now, and what will advisors do (or be required to do) as a result?

0Investor

Advisor

SENTIMENT INDEX

Pessimistic

Optimistic

-40

-20

1200

600

80

60

40

20

11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2

2011 2012 2013 2014 2015 ‘16‘10

RUSSELL 1000® INDEX

Scal

e of

-100

to

+100

Performance over the years

Time to address investor uncertainty.

p / 9Russell Investments // Financial Professional Outlook

How will current advisor practices and preferences hold up as markets, regulation (DOL) and politics rock the client boat?

p / 10Russell Investments // Financial Professional Outlook

› In this challenging environment, we recommend that advisors review their current capacity, the positions/CUSIPs they are overseeing and their overall client manageability, to help improve effi ciencies and client engagement. We were curious about what advisors are thinking now in terms of their current capacity and how many clients they think they can manage in the future.

Manageability and sustainability are key to long-term success in today’s changing advisory landscape.

p / 11Russell Investments // Financial Professional Outlook

0

5

10

15

20

25

30

35

0-75 76-100 101-150 151-200 201+

33%

25%

11%

16%13%

17%

9%

18%

34%

24%

ACTUAL MANAGEABLE

% o

f ac

tual

and

man

agea

ble

clie

nts

Number of clients per advisor

› We asked the question, “What is the actual number of clients you have today versus what you think is a manageable amount?” Interestingly, one-third of advisors said they manage 0-75 and 201+ clients, and about one-fourth of them think that’s a manageable amount.

ACTUAL AND MANAGEABLE CLIENT HOUSEHOLDS

p / 12Russell Investments // Financial Professional Outlook

› We asked the question, “What is the actual number of products or positions (CUSIPs) you are overseeing today versus what you think is a manageable amount?”

› Seventy-seven percent of advisors said they are following up to 250 CUSIPs and half of them are following 100 or fewer.

› One possible conclusion is that advisors naturally seek a level of book size (and by extension client engagement) with which they are comfortable. The inverse could also be true. The way advisors choose to manage money and service clients constrains the number and/or type of client they can serve.

0

10

20

30

40

50

60

0-100 101-250 251-400 401-600 601+

52% 51%

25%30%

10% 9%5% 3%

8% 7%

ACTUAL MANAGEABLE

% o

f ac

tual

and

man

agea

ble

CU

SIP

s/po

siti

ons

Amount of CUSIPs per advisor

ACTUAL AND MANAGEABLE CUSIPs FOLLOWED

p / 13Russell Investments // Financial Professional Outlook

What are advisors and investors talking about, and why is there a huge gap? › Advisors see stress and strain in the capital markets, likely because

of the alarmist political narrative in this electoral season.

› Unsurprisingly, market volatility is top-of-mind for most investors. Clients obviously want to talk about what advisors think of as “context” (volatility, global events, and portfolio performance)—and what it means to their fi nancial security.

Be prepared. Investors want to talk about volatility.

p / 14Russell Investments // Financial Professional Outlook

› Top investor-initiated conversation topics are market volatility (62%) followed by portfolio performance (56%) and global events (41%). Market volatility conversations are likely being spurred by investors due to the recent volatility in January and February 2016.

Nov-11 Nov-12 Nov-13 Oct-14 Oct-15 Feb-16

Market Volatility 63% 45% 42% 47% 58% 62%

Portfolio Performance 44% 21% 28% 29% 50% 56%

Global Events 44% 25% 19% 27% 36% 41%

Running Out Of Money 29% 30% 24% 26% 25% 24%

Rising Interest Rates 18% 25% 15%

Concerns with Govt Policy 53% 55% 56% 29% 24% 27%

Portfolio Rebalancing 14% 10% 12% 8% 22% 17%

0%

10%

20%

30%

40%

50%

60%

70%

Nov-11 Nov-12 Nov-13 Oct-14 Oct-15 16-Feb

Portfolio Performance 30% 27% 32% 32% 42% 45%

Portfolio Rebalancing 49% 27% 40% 43% 38% 43%

Global Events 44% 21% 14% 9% 37% 38%

Rising Interest Rates 21% 34% 17%

Market Volatility 29% 15% 17% 27% 31% 38%

0%

10%

20%

30%

40%

50%

60%

How often are investors bringing up these topics? INVESTOR-INITIATED CONVERSATION TOPICS: TRENDS

p / 15Russell Investments // Financial Professional Outlook

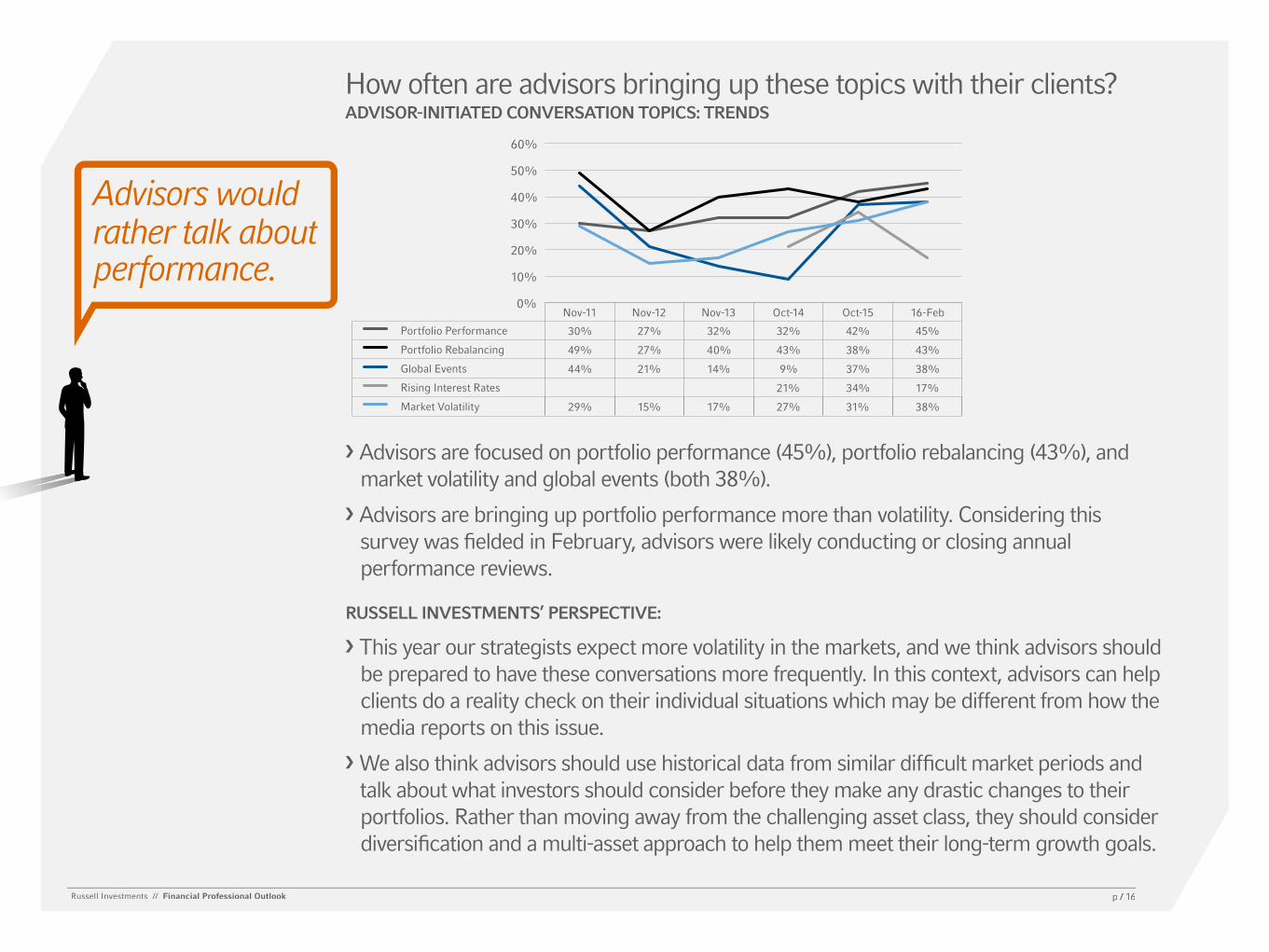

How often are advisors bringing up these topics with their clients?ADVISOR-INITIATED CONVERSATION TOPICS: TRENDS

Nov-11 Nov-12 Nov-13 Oct-14 Oct-15 Feb-16

Market Volatility 63% 45% 42% 47% 58% 62%

Portfolio Performance 44% 21% 28% 29% 50% 56%

Global Events 44% 25% 19% 27% 36% 41%

Running Out Of Money 29% 30% 24% 26% 25% 24%

Rising Interest Rates 18% 25% 15%

Concerns with Govt Policy 53% 55% 56% 29% 24% 27%

Portfolio Rebalancing 14% 10% 12% 8% 22% 17%

0%

10%

20%

30%

40%

50%

60%

70%

Nov-11 Nov-12 Nov-13 Oct-14 Oct-15 16-Feb

Portfolio Performance 30% 27% 32% 32% 42% 45%

Portfolio Rebalancing 49% 27% 40% 43% 38% 43%

Global Events 44% 21% 14% 9% 37% 38%

Rising Interest Rates 21% 34% 17%

Market Volatility 29% 15% 17% 27% 31% 38%

0%

10%

20%

30%

40%

50%

60%

› Advisors are focused on portfolio performance (45%), portfolio rebalancing (43%), and market volatility and global events (both 38%).

› Advisors are bringing up portfolio performance more than volatility. Considering this survey was fi elded in February, advisors were likely conducting or closing annual performance reviews.

RUSSELL INVESTMENTS’ PERSPECTIVE:

› This year our strategists expect more volatility in the markets, and we think advisors should be prepared to have these conversations more frequently. In this context, advisors can help clients do a reality check on their individual situations which may be different from how the media reports on this issue.

› We also think advisors should use historical data from similar diffi cult market periods and talk about what investors should consider before they make any drastic changes to their portfolios. Rather than moving away from the challenging asset class, they should consider diversifi cation and a multi-asset approach to help them meet their long-term growth goals.

p / 16Russell Investments // Financial Professional Outlook

What’s notable is the relative gap between the topics favored by investors and their advisors on some topics (and the similarity on others).

Investors seem much less interested in talking about rebalancing than advisors do.

38%

45%

38%

19%

17%

43%

62%

56%

41%

27%

24%

17%

Advisor Investor

PORTFOLIO PERFORMANCE

GLOBAL EVENTS

CONCERNS WITH GOVERNMENT POLICY

RUNNING OUT OF MONEY IN RETIREMENT

PORTFOLIO REBALANCING / SHIFTING THEIR

PORTFOLIO'S ASSET ALLOCATION

MARKET VOLATILITY

When thinking about conversations you’ve had with your clients over the past three months, which of the following have been the most common topics of conversations?

WHAT ADVISORS AND INVESTORS ARE TALKING ABOUT.

p / 17Russell Investments // Financial Professional Outlook

What are advisors doing differently to navigate through market volatility, while trying to grow their businesses and maintain competitive advantage?

p / 18Russell Investments // Financial Professional Outlook

What are you doing differently to navigate through the market volatility?

4%

10%

15%

16%

22%

77%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Nothing

Other

Reviewing number of client relationships

Shifting staffing resources to focus on client services

Consolidating products within lineup

Increasing frequency of client contact

Advisors navigate volatility with more client contacts.

› Seventy-seven percent of advisors are increasing the frequency of client contact in response to market volatility and other changing trends, followed by 22% who are consolidating products within their lineup.

› Only 15% said they are reviewing client relationships, and almost an equal percentage said they are shifting resources to focus on client services.

› Advisors are clearly paying attention to the market noise, as well as to the longer-term economic and social signals, telling them their world is changing.

p / 19Russell Investments // Financial Professional Outlook

› The highest percentage (72%) of advisors said market volatility is a key factor contributing to changes in how they manage their business in 2016, followed by aging client base (40%), and the proposed DOL Fiduciary Standard (34%). Rising interest rates (28%) was rated fourth as a key factor in this regard.

RUSSELL INVESTMENTS’ PERSPECTIVE:

› While DOL and market volatility are two immediate issues facing the advisory business, key longer-term challenges included in the exhibit above are substantially changing the way advisors do business.

Several factors are changing the way advisors do business.

What factors are contributing in how you manage your businesses?

6%

8%

19%

20%

28%

34%

40%

72%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Other

Competition from robo-advisors

Succession planning for my practice

Managing the transfer of multi-generational wealth

Rising interest rates

Proposed DOL Fiduciary Standard

Aging client base

Market volatility

% of advisor respondents

p / 20Russell Investments // Financial Professional Outlook

What are your strategies to maintain competitive advantage and enhance growth?

12%

18%

28%

32%

38%

43%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Identify successor

Target millennials

Invest in technology

Re-engineer client service model

Transition client accounts to advisory solutions

Develop my COI relationships

% of advisor respondentsAdvisor growth is focused on Centers of Infl uence (COIs)

RUSSELL INVESTMENTS’ PERSPECTIVE:

› Given the increasing average age of the fi nancial advisor, the relatively low level of importance to “identify a successor” stands out.

› Advisors often underestimate the time and attention required to effectively identify, onboard, and transition a successful successor.

The largest percentage (43%) of advisors say they are developing their Center of Infl uence (COI) relationships (accountants, lawyers, tax planners, etc.) while 38% are transitioning client accounts to advisory solutions, where appropriate, followed by re-engineering their client service model (32%), and making investments in technology (28%).

p / 21Russell Investments // Financial Professional Outlook

Are advisors in the blind spot when it comes to potential impacts of DOL?› The Department of Labor’s (DOL) Fiduciary Standard proposal has

the potential to change how advisors are running their businesses with the introduction of a new fi duciary “best interest” standard. It will likely impact all brokers and advisors, giving advice on retirement accounts and receiving compensation for it.

› The question we asked was a simple one: “To what degree do you see the DOL proposal impacting your business if it passes?”

› Sixty-one percent of advisors expect slight or no impact from the proposed DOL Fiduciary Standard and only 21% expect a signifi cant impact.

Potential impact of proposed DOL Fiduciary Standard

21%

35%

26%

18%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Significant impact Slight impact No impact Uncertain% of advisor respondents

Do most advisors have a DOL blind spot?

p / 22Russell Investments // Financial Professional Outlook

› Indeed, the actions advisors were considering as of the early days of 2016 before the proposed rule came through seem to refl ect a combination of unfamiliarity with the proposed rule, an uncertainty about what to do (and this could be a function of where they work), or a “I’ll start making moves once I know what game we’re playing” point of view.

RUSSELL INVESTMENTS’ PERSPECTIVE:

› The DOL proposal has the potential to signifi cantly impact fi nancial advisors and all aspects of their business operation.

› Advisors who embrace the necessary changes as a result of the fi nal DOL proposal are likely to achieve the greatest degree of success in a post-DOL world. Many of the DOL-critical implementation principles are rooted in best practices that top advisors have been deploying to maintain their competitive edge. Workfl ow documentation and product inventory control serve as key examples.

p / 23Russell Investments // Financial Professional Outlook

Isn’t it time to take action and look at the big picture?Actions considered to prepare for proposed DOL rule

7%

5%

12%

13%

17%

18%

20%

24%

49%

0% 10% 20% 30% 40% 50%

Other

Team with another advisor

Disengage certain clients

Redesign my service model

Re-evaluate households with small balances

Re-evaluate investment proposition and solutions

Re-evaluate core investment propositionstrategies and financial products used

No changes until rule is finalized

Review and update compliance andrecord keeping

Advisors are not planning to make any changes until the rule is fi nalized.

› 49% of advisors are not making any changes until the rule is fi nalized and are likely underestimating the impact of the proposed rule.

› Russell Investments has been advocating strategies to help build a sustainable practice for more than 18 years. Many of these strategies refl ect what we perceive as the necessary response to not only address the DOL rule at the forefront, but also address larger competitive pressures that advisors are facing.

p / 24Russell Investments // Financial Professional Outlook

What does Russell Investments think advisors should do? We believe there are four pillars of a sustainable advisory business:1. Manageable number of client households

2. Product inventory control

3. Documentation and implementation of key processes

4. Optimized client experiences, including client portfolios

Successfully managing these four pillars in your business not only helps you go on the ‘defense’ with the DOL proposal, but also on the ‘offense’ by helping you deliver lasting, high-quality client relationships—the holy grail of advisor success. Clients who feel valued and well served tend to become valuable advocates.

p / 25Russell Investments // Financial Professional Outlook

Our biggest data sets in this survey were Independent Financial Advisors and National Broker Dealers. Type of Company

19%

10%

2%

2%

14%

21%

31%

,0% .5% 10% 15% 20% 25% 30% 35%

No answer

Other

National or Regional Bank

Insurance or Mutual

Regional Broker Dealer

National Broker Dealer or Wirehouse

Independent Financial Advisor

Sample size for Insurance/Mutual and Banks is too small for analysis. No detail is available for the other category.

p / 26Russell Investments // Financial Professional Outlook

About the Financial Professional Outlook (FPO)

Russell Investments conducted the Financial Professional Outlook survey between February 5 and February 19. The survey was sent to a broad group of U.S. fi nancial advisors. Having a fi nancial relationship with Russell was not part of the criteria for being included in the survey. The sample size of 258 is suffi cient to provide 95% confi dence that the results will be within plus or minus 6.2%. In other words, if we repeated this survey 100 times we would expect to fi nd similar results in 95 of the 100 trials.

General Disclosures Russell Financial Professional Outlook is a product of Russell Investments, produced independently of Russell’s investment and manager research services.

The views in this Annual Market Outlook are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

The information contained herein has been obtained from sources that we believe to be reliable, but its accuracy and completeness cannot be guaranteed. The information, analysis and opinions expressed herein result from surveys of persons outside Russell Investments and may not represent the opinion of Russell Investments, its affi liates or subsidiaries. This report is provided for general information only and is not intended to provide specifi c advice or recommendations for any individual or entity. This is not an offer, solicitation or recommendation to purchase any security or the services of any organization.

Russell 1000® Index: Measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 92% of the U.S. market. Performance quoted represents past performance and should not be viewed as a representation of future results.

Diversifi cation does not assure a profi t and does not protect against loss in declining markets.

Keep in mind, like all investing, that multi-asset investing does not assure a profi t or protect against loss.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an ‘as is’ basis without warranty.

The Russell logo is a trademark and service mark of Russell Investments. This material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group.

Russell Financial Services, Inc., member FINRA, part of Russell Investments.

Copyright © Russell Investments 2015. All rights reserved.

First used March 2016.

RFS-17055

p / 27Russell Investments // Financial Professional Outlook