Financial Position Unit 1. Assets = Liabilities + Owner’s Equity The Basic Accounting Equation...

18

Financial Position Unit 1

-

Upload

allan-page -

Category

Documents

-

view

219 -

download

0

Transcript of Financial Position Unit 1. Assets = Liabilities + Owner’s Equity The Basic Accounting Equation...

Financial Position

Unit

1

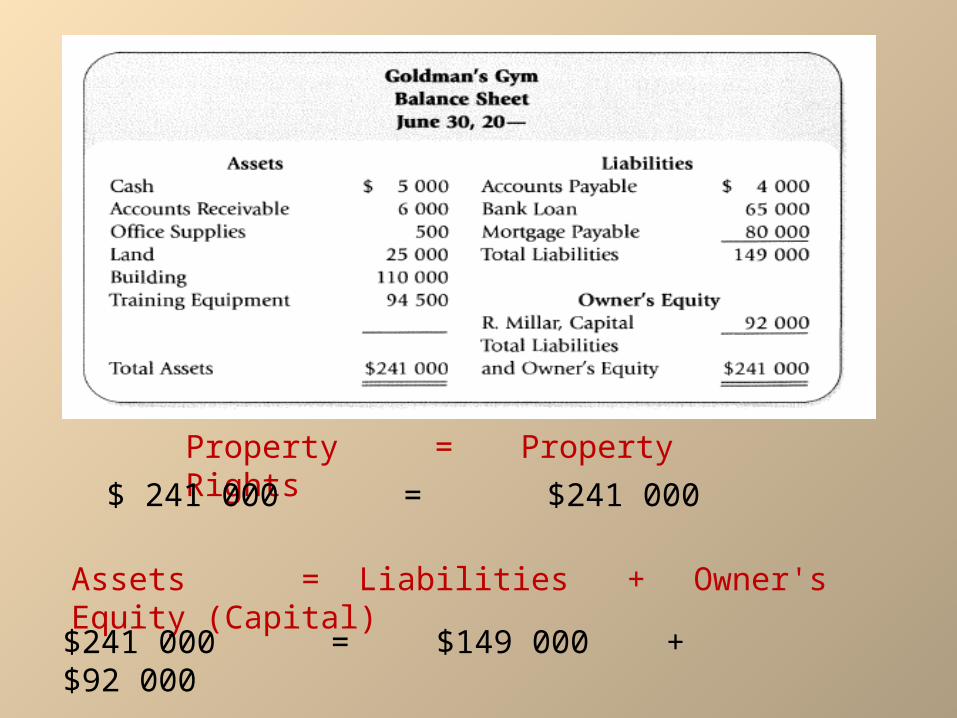

Assets = Liabilities + Owner’s Equity

The Basic Accounting Equation

PropertyProperty Property RightsProperty Rights=

also referred to as the Balance Sheet Equation

It is also known as a Statement Of Financial Position

The Balance Sheet is a financial statement which shows the amount and nature of business assets, liabilities, and owner's equity (capital) as of a specific point in time.

It show a companies financial position in terms of Assets, Liabilities and Equity.

From the Transaction analysis sheet or balance sheet equation we can create a Balance Sheet and or work backwards

The Balance Sheet

Property = Property Rights

Assets = Liabilities + Owner's Equity (Capital)

$ 241 000 = $241 000

$241 000 = $149 000 + $92 000

Step 1: Prepare Statement Heading

Step 2: List Assets

Types of Assets

Cash-Monetary items that are available to meet current obligations of the business. It includes bank deposits, currency & coins, checks, money orders, and traveler's checks.

Accounts Receivable-Business claims against the property of a customer arising from the sale of goods and/or services on account.

Notes Receivable-Formal written promises given by customers or others to pay definite sums of money to the business at specified times.

Inventory-Expenditures for items held for resale in the normal course of a business's operations.

Office Supplies-Expenditures for maintaining a supply of on hand supplies such as typewriter, copier, and computer paper, pens, pencils, and special forms.

Land-Expenditures for parcels of the earth. It includes building sites, yards, and parking areas.

Buildings-Expenditures for structures erected on land and used for the conduct of business.

Equipment-Expenditures for physical goods used in a business, such as machinery or furniture. Equipment is used in a business during the production of income.

Furniture-includes items needed in a business office such as tables, desks, chairs, and cabinets

Step 3: List Liabilities

Types Of Liabilities

Accounts Payable-Creditor's claims against the business's property arising from the business's purchase of goods and/or services on account.

Notes Payable-Formal written promises to pay definite sums of money owed at specified times.

Mortgage Payable-Notes payable which are secured by a lien on land, buildings, equipment, or other property of the borrower (your company).

Step 4: Show Owner’s Equity

Facts to Remember

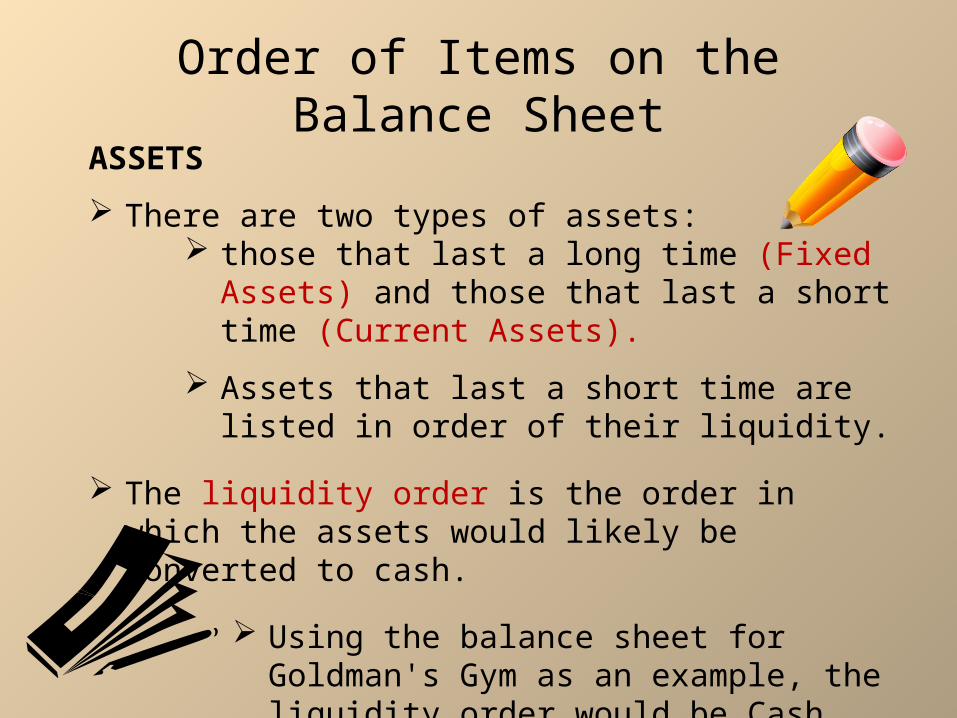

Order of Items on the Balance SheetASSETS

There are two types of assets: those that last a long time (Fixed Assets) and those

that last a short time (Current Assets).

Assets that last a short time are listed in order of their liquidity.

The liquidity order is the order in which the assets would likely be converted to cash.

Using the balance sheet for Goldman's Gym as an example, the liquidity order would be Cash, Accounts Receivable, and Office Supplies.

Next come assets that last a long time and are used for a long time to operate the business.

Examples include Land, Building, and Training Equipment.

They are listed in order of their useful life to the business, with the longest lasting listed first.

Liabilities are listed according to when they must be paid in full, from shortest (Current Liabilities) to longest term (Long Term Liabilities).

The payment due date is known as the maturity date.

Liabilities

Common Recording Practices

They are described and illustrated below:

1. When ruled accounting paper is used, dollar signs, commas, spaces, and decimals are not used.

2. A single line indicates addition or subtraction.

3. A double line indicates final totals.

4. When ruled accounting forms are not used, dollar signs, spaces or commas, and decimals are used.

5. Dollar signs are placed in alignment before the first figure in a column and beside final column totals when accounting forms are not used.

6. Abbreviations are not used on financial statements unless the official name of the company contains an abbreviation.

For example, Lumonics Inc. does contain a short

form (Inc.) in its official name and should be written as Lumonics Inc. Goldcorp Investments Limited should not be written in short form since the company uses Limited, not Ltd., as part of its official name.

7. Accounting records must be neat and legible. They are used by many people and are kept for a long period of time. They are either printed, keyed, or written in ink Care must be taken to write numbers and words clearly and legibly.