Financial Planning in a Healthcare Reform Environment...

29

Financial Planning in a Healthcare Reform Environment – Organizing all the Moving Parts Organizing all the Moving Parts January 10, 2012 Dave Frank, Partner Brian Kerby, Director

Transcript of Financial Planning in a Healthcare Reform Environment...

Financial Planning in a Healthcare Reform Environment –Organizing all the Moving PartsOrganizing all the Moving PartsJanuary 10, 2012

Dave Frank, PartnerBrian Kerby, Director

The Unique Alternative to the Big Four®

Learning ObjectivesFinancial planning in today’s healthcare reform environment entails many moving parts and considerations. This webinar will focus on key components of financial planning and annual budgeting with focus on items of risk in today’s environment. Session objectives will include: Understand healthcare reform and market consolidation potential impacts on Understand healthcare reform and market consolidation potential impacts on

financial planning and budgeting; Understand key financial planning variables and current trends/issues impacting

these variables;these variables; Develop an understanding of accounting and financial reporting changes

impacting financial planning; Overall objective: better financial planning for the next 3-5 years in light of j p g y g

market consolidation and healthcare reform.

© 2012 Crowe Horwath LLP 2Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Polling Question #1 Which enterprising healthcare organization and/or investor category best describes your Which enterprising healthcare organization and/or investor category best describes your

organization:1. Hospitals and Health Systems2. Physician Groups or Other Ancillary Provider (ASC, Lab, etc)3 H H lth3. Home Health4. Rehabilitation5. Behavioral Health6. Long-term Care, Hospice and Senior Living 7. Other.

© 2012 Crowe Horwath LLP 3Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Rapidly Changing Times: A Summary and Perspective

Healthcare ReformHealthcare Reform The Patient Protection and Affordable Care Act (passed on March 23, 2010) has

produced many short-term impacts through cuts in reimbursement rates, modifications to required healthcare benefits offered by employers, and similar q y p y ,cost focused endeavors.

This noted, a significant portion of the Act is still undefined related to specifics that will be implemented during the next 10 years.

This lack of specificity has not stopped the nation’s healthcare providers from anticipating and preparing for a rapidly changing healthcare delivery system.

There is broad-based consensus that the fundamental drivers of long-term viability such as volume per unit reimbursement quality cost access to capitalviability such as volume, per unit reimbursement, quality, cost, access to capital, tax-exemption, and other are all “in motion” with or without healthcare reform in its current form.

© 2012 Crowe Horwath LLP 4Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Rapidly Changing Times: A Summary and Perspective

State and Federal Budget DeficitsState and Federal Budget Deficits The deterioration in the U.S. economic outlook that began in 2008 had

substantial consequences and impacts on the thinking of today’s leaders. While business activity and capital markets have showed continued improvement from y p plows achieved three years ago, the underlying change in sentiment and outlook has been gradual at many organizations.

A growing concern in 2010 and continuing in 2011 is healthcare reform funding t ti l l l d ifi ll b d t d fi it t t t l l Mat a national level and, more specifically, budget deficits at a state level. Many

states are forecasting multi-billion dollar deficits, with changes in federal funding and state deficits expected to impact healthcare in many ways including: Decreased reimbursement rates through budget neutral or other adjustments;Decreased reimbursement rates through budget neutral or other adjustments; Prolonged payment cycles (particularly at the state level); Potential new taxes on healthcare services as historically excluded healthcare services

may be viewed as new options to fund/offset state budget issues;

© 2012 Crowe Horwath LLP 5Audit | Tax | Advisory | Risk | Performance

Increased fees and taxes on healthcare licenses, registrations and other.

The Unique Alternative to the Big Four®

M&A wave is already picking up steam within Crowe’s client base nationally

Rapidly Changing Times: A Summary and PerspectiveM&A wave is already picking up steam within Crowe s client base nationally… St. Vincent Health acquires 300+ physicians in past year

Catholic Healthcare Partners divesting Knoxville and Scranton hospitalsg p

Catholic Health Initiatives merging Kentucky facilities with Jewish Hospital & St. Mary’s Healthcare and University of Louisville

Norton Healthcare establishes ACO for commercially-insured patients in partnership with Humana

Community Health System bidding for Tenet

© 2012 Crowe Horwath LLP 6Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

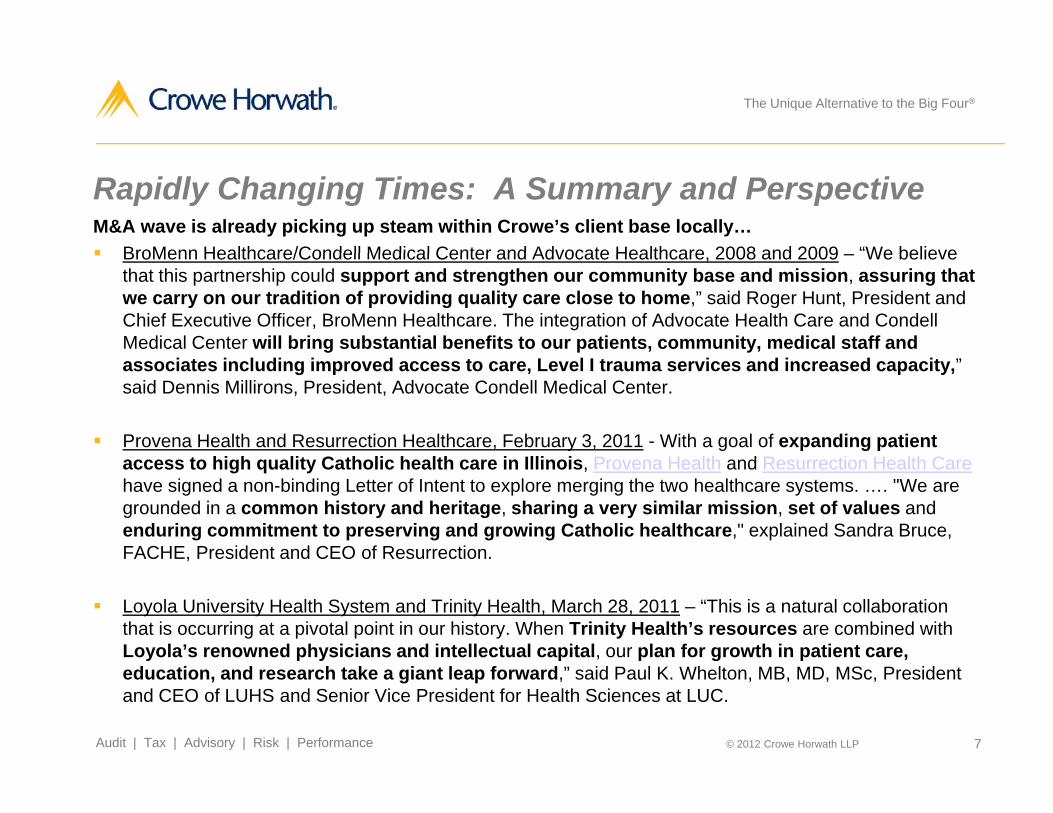

Rapidly Changing Times: A Summary and PerspectiveM&A wave is already picking up steam within Crowe’s client base locally… BroMenn Healthcare/Condell Medical Center and Advocate Healthcare 2008 and 2009 “We believe BroMenn Healthcare/Condell Medical Center and Advocate Healthcare, 2008 and 2009 – We believe

that this partnership could support and strengthen our community base and mission, assuring that we carry on our tradition of providing quality care close to home,” said Roger Hunt, President and Chief Executive Officer, BroMenn Healthcare. The integration of Advocate Health Care and Condell Medical Center will bring substantial benefits to our patients, community, medical staff and associates including improved access to care, Level I trauma services and increased capacity,” said Dennis Millirons, President, Advocate Condell Medical Center.

Provena Health and Resurrection Healthcare, February 3, 2011 - With a goal of expanding patient t hi h lit C th li h lth i Illi i P H lth d R ti H lth Caccess to high quality Catholic health care in Illinois, Provena Health and Resurrection Health Care

have signed a non-binding Letter of Intent to explore merging the two healthcare systems. …. "We are grounded in a common history and heritage, sharing a very similar mission, set of values and enduring commitment to preserving and growing Catholic healthcare," explained Sandra Bruce, FACHE, President and CEO of Resurrection.,

Loyola University Health System and Trinity Health, March 28, 2011 – “This is a natural collaboration that is occurring at a pivotal point in our history. When Trinity Health’s resources are combined with Loyola’s renowned physicians and intellectual capital, our plan for growth in patient care,

© 2012 Crowe Horwath LLP 7Audit | Tax | Advisory | Risk | Performance

education, and research take a giant leap forward,” said Paul K. Whelton, MB, MD, MSc, President and CEO of LUHS and Senior Vice President for Health Sciences at LUC.

The Unique Alternative to the Big Four®

Rapidly Changing Times: A Summary and PerspectiveM&A wave is already picking up steam within Crowe’s client base locally… Delnor Community Health System and Central DuPage Health March 31 2011 “Today we have Delnor Community Health System and Central DuPage Health, March 31, 2011 – Today, we have

created a new health system with greater scale to provide patients with even higher quality care, access to a greater number of specialists, a broader range of clinical capabilities and a more integrated approach to health care,” said C. William Pollard, Chairman of the CDH board of directors.

Metropolitan Chicago Healthcare Council To Develop Nation's Largest Metro Health Information Exchange To Improve Quality Of Care And Cost Efficiencies, April 25, 2011 - "MCHC is charting a new course with the MetroChicago HIE," said Mary Anne Kelly, Vice President of MCHC. "The HIE will be one of the largest in the country and will allow our region's healthcare market to improve efficiency by

ti t k h h lth i f ti fl ith th ti t tt h i i dcreating a network where health information flows with the patient, no matter where care is received. The reaction from local hospitals has been overwhelmingly positive. Seventy percent of hospitals in the Chicago metro area have already become founding members of the HIE, which is a testament to area healthcare organizations' stalwart commitment to improving quality and patient safety.“

Alexian Brothers Health system and Ascension Health, April 27, 2011 – said Mark A. Frey, Executive Vice President of Alexian Brothers Health System, "This partnership is a sign of Alexian Brothers Health System's commitment to ensure that everyone in the communities we serve will continue to receive the highest level of care for the long term and strengthen Catholic healthcare in the Chicago

© 2012 Crowe Horwath LLP 8Audit | Tax | Advisory | Risk | Performance

metropolitan region."

The Unique Alternative to the Big Four®

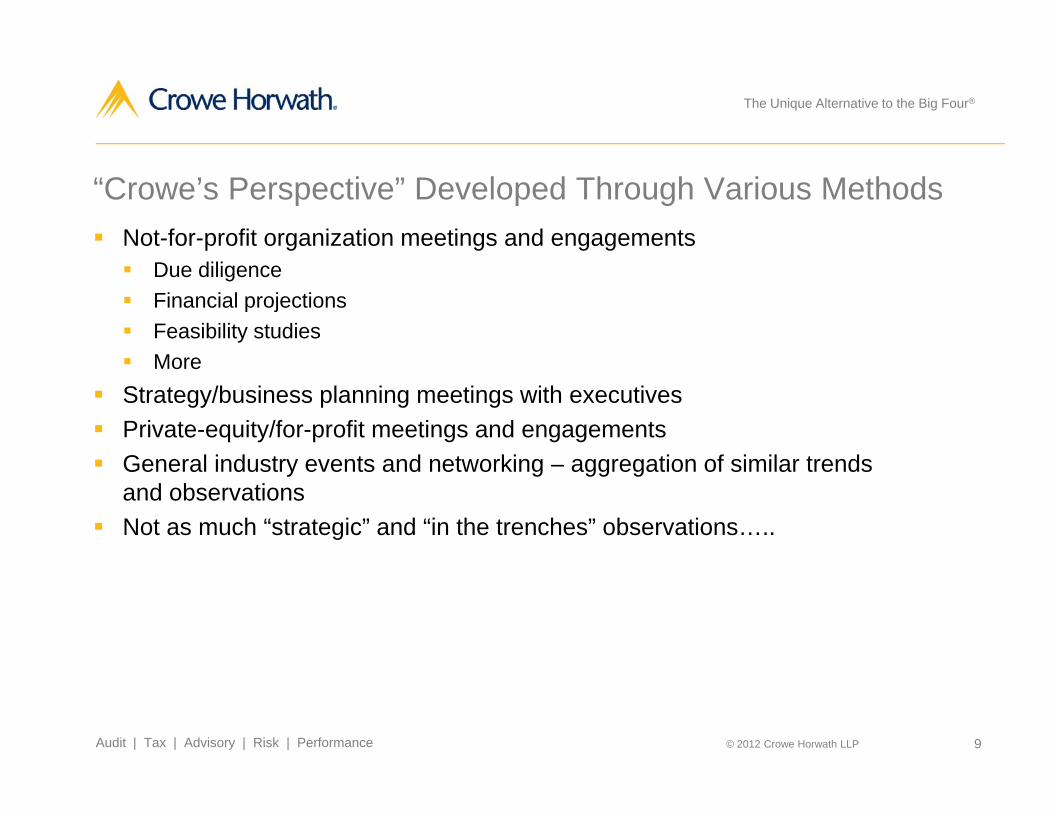

“Crowe’s Perspective” Developed Through Various Methods Not-for-profit organization meetings and engagements Due diligence Financial projections Feasibility studies

M More Strategy/business planning meetings with executives Private-equity/for-profit meetings and engagements

G l i d t t d t ki ti f i il t d General industry events and networking – aggregation of similar trends and observations

Not as much “strategic” and “in the trenches” observations…..

© 2012 Crowe Horwath LLP 9Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

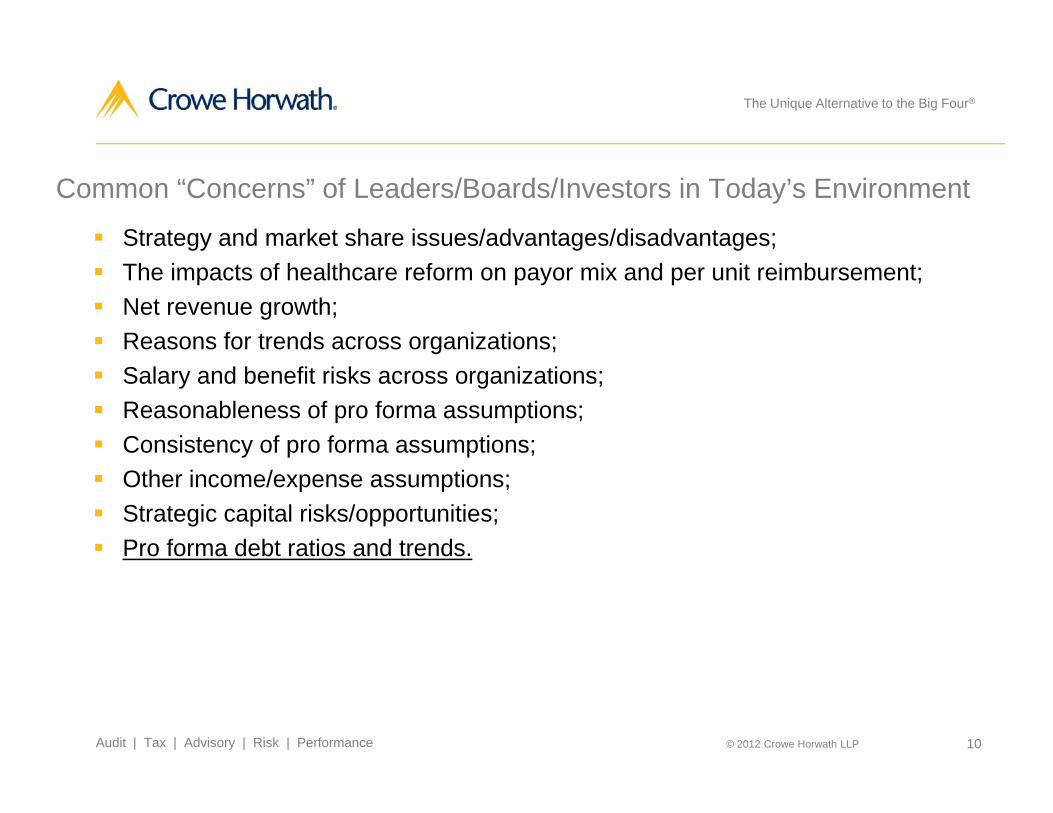

Common “Concerns” of Leaders/Boards/Investors in Today’s Environment

Strategy and market share issues/advantages/disadvantages; The impacts of healthcare reform on payor mix and per unit reimbursement; Net revenue growth; Reasons for trends across organizations; Salary and benefit risks across organizations; Reasonableness of pro forma assumptions; Consistency of pro forma assumptions; Other income/expense assumptions; Strategic capital risks/opportunities; Pro forma debt ratios and trends.

© 2012 Crowe Horwath LLP 10Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

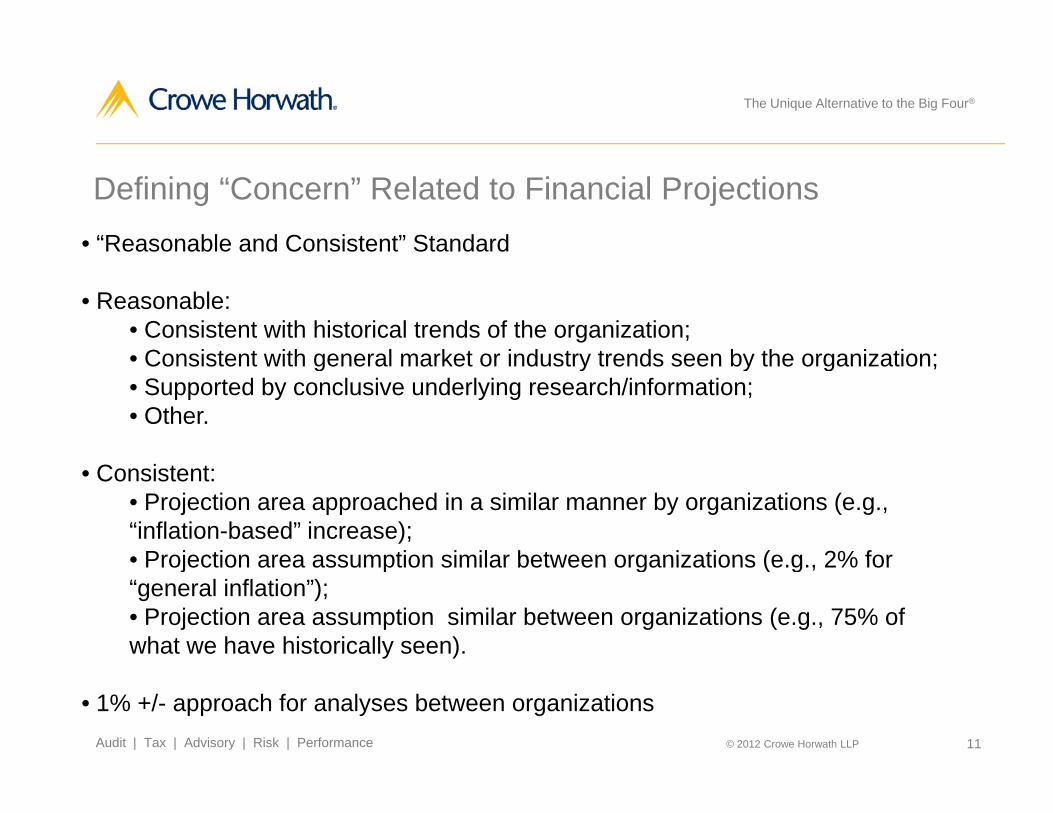

Defining “Concern” Related to Financial Projections• “Reasonable and Consistent” Standard

• Reasonable:• Consistent with historical trends of the organization;• Consistent with general market or industry trends seen by the organization;• Consistent with general market or industry trends seen by the organization;• Supported by conclusive underlying research/information;• Other.

• Consistent:• Projection area approached in a similar manner by organizations (e.g., “inflation-based” increase);• Projection area assumption similar between organizations (e g 2% for• Projection area assumption similar between organizations (e.g., 2% for “general inflation”);• Projection area assumption similar between organizations (e.g., 75% of what we have historically seen).

© 2012 Crowe Horwath LLP 11Audit | Tax | Advisory | Risk | Performance

• 1% +/- approach for analyses between organizations

The Unique Alternative to the Big Four®

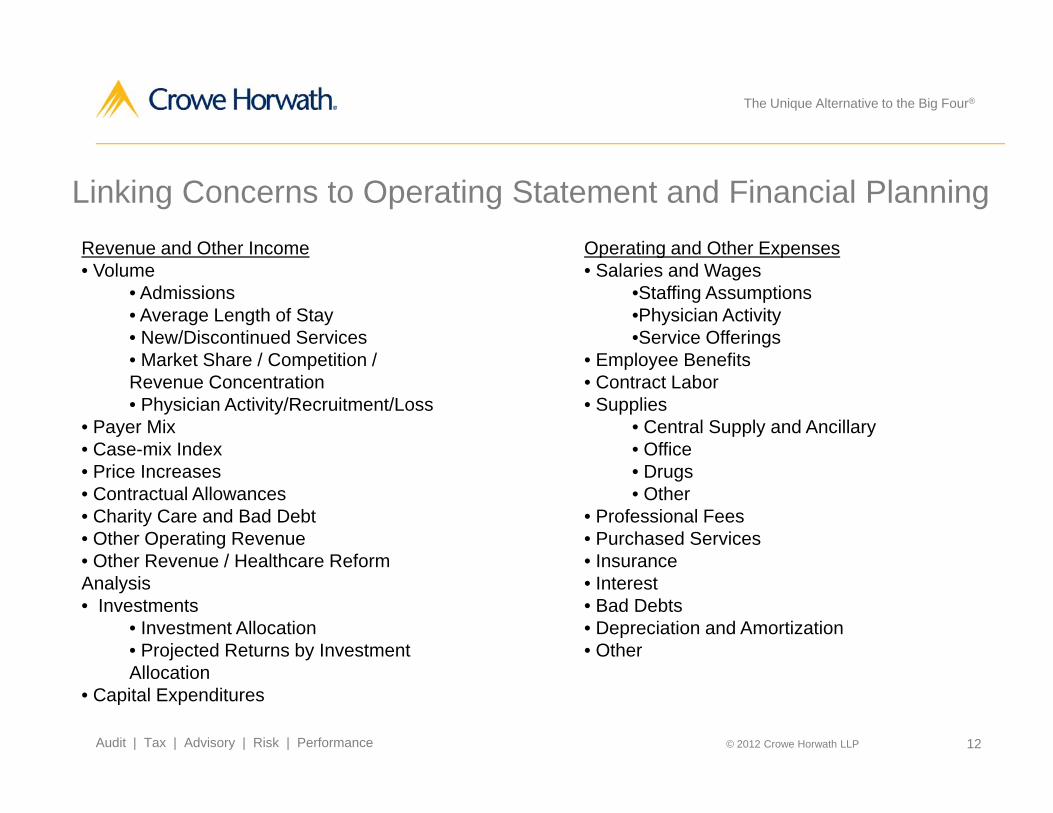

Linking Concerns to Operating Statement and Financial PlanningRevenue and Other Income Operating and Other ExpensesRevenue and Other Income• Volume

• Admissions • Average Length of Stay• New/Discontinued Services

M k t Sh / C titi /

Operating and Other Expenses• Salaries and Wages

•Staffing Assumptions•Physician Activity•Service Offerings

E l B fit• Market Share / Competition / Revenue Concentration• Physician Activity/Recruitment/Loss

• Payer Mix• Case-mix Index

• Employee Benefits• Contract Labor• Supplies

• Central Supply and Ancillary• Office

• Price Increases• Contractual Allowances• Charity Care and Bad Debt• Other Operating Revenue• Other Revenue / Healthcare Reform

• Drugs• Other

• Professional Fees• Purchased Services• Insurance• Other Revenue / Healthcare Reform

Analysis• Investments

• Investment Allocation• Projected Returns by Investment

• Insurance• Interest • Bad Debts• Depreciation and Amortization• Other

© 2012 Crowe Horwath LLP 12Audit | Tax | Advisory | Risk | Performance

Allocation• Capital Expenditures

The Unique Alternative to the Big Four®

Linking Concerns to Operating Statement and Financial Planning

A f C id tiArea of Financial

Consideration Items in a

Planning / Budgeting

Consolidating HealthcareBudgeting Healthcare

Reform Environment

© 2012 Crowe Horwath LLP 13Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

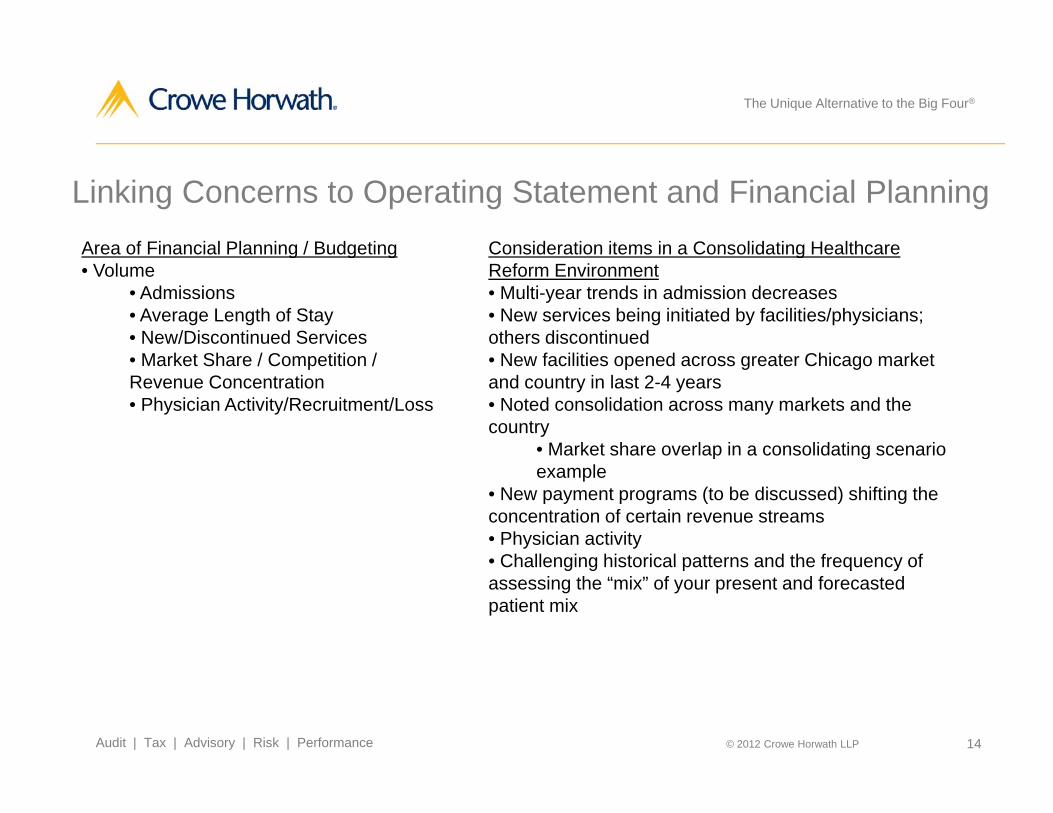

Linking Concerns to Operating Statement and Financial PlanningArea of Financial Planning / Budgeting Consideration items in a Consolidating HealthcareArea of Financial Planning / Budgeting• Volume

• Admissions • Average Length of Stay• New/Discontinued Services

M k t Sh / C titi /

Consideration items in a Consolidating Healthcare Reform Environment• Multi-year trends in admission decreases• New services being initiated by facilities/physicians; others discontinued

N f iliti d t Chi k t• Market Share / Competition / Revenue Concentration• Physician Activity/Recruitment/Loss

• New facilities opened across greater Chicago market and country in last 2-4 years• Noted consolidation across many markets and the country

• Market share overlap in a consolidating scenario p gexample

• New payment programs (to be discussed) shifting the concentration of certain revenue streams• Physician activity• Challenging historical patterns and the frequency of• Challenging historical patterns and the frequency of assessing the “mix” of your present and forecasted patient mix

© 2012 Crowe Horwath LLP 14Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

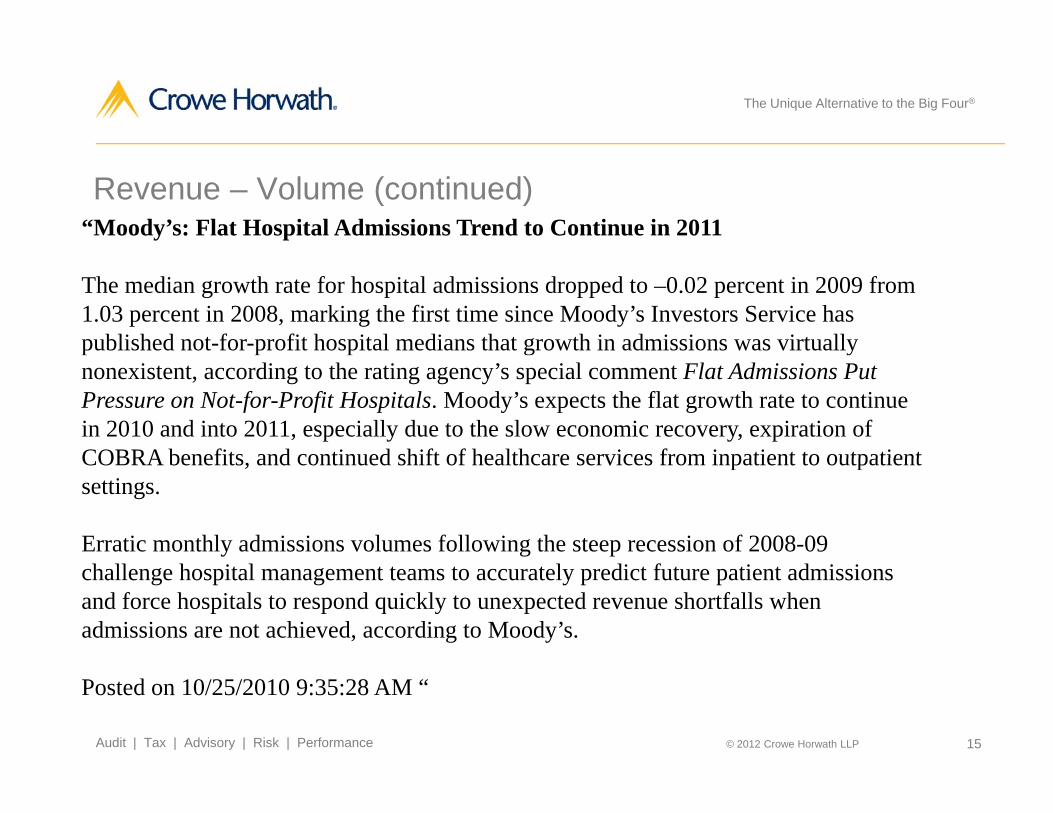

Revenue – Volume (continued)“Moody’s: Flat Hospital Admissions Trend to Continue in 2011

The median growth rate for hospital admissions dropped to –0.02 percent in 2009 from 1.03 percent in 2008, marking the first time since Moody’s Investors Service has published not-for-profit hospital medians that growth in admissions was virtually nonexistent, according to the rating agency’s special comment Flat Admissions Put Pressure on Not-for-Profit Hospitals. Moody’s expects the flat growth rate to continue in 2010 and into 2011, especially due to the slow economic recovery, expiration of COBRA benefits and continued shift of healthcare services from inpatient to outpatientCOBRA benefits, and continued shift of healthcare services from inpatient to outpatient settings.

Erratic monthly admissions volumes following the steep recession of 2008-09 challenge hospital management teams to accurately predict future patient admissions and force hospitals to respond quickly to unexpected revenue shortfalls when admissions are not achieved, according to Moody’s.

© 2012 Crowe Horwath LLP 15Audit | Tax | Advisory | Risk | Performance

Posted on 10/25/2010 9:35:28 AM “

The Unique Alternative to the Big Four®

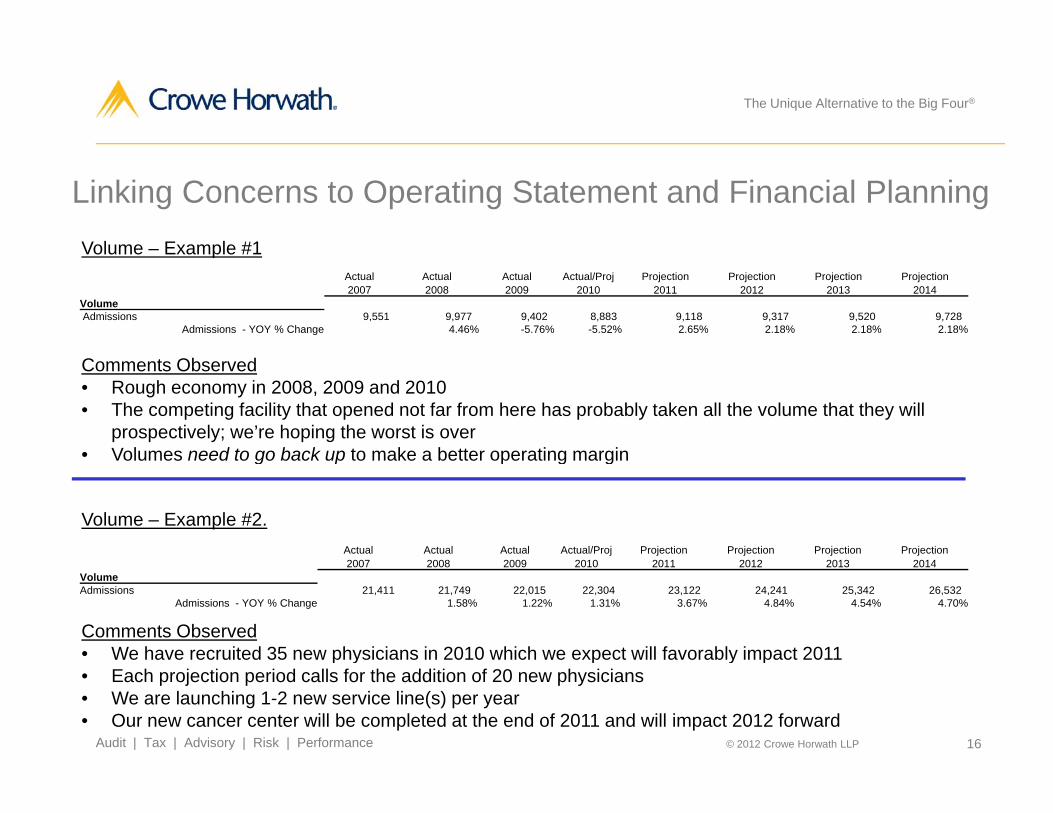

Linking Concerns to Operating Statement and Financial PlanningVolume – Example #1Volume Example #1

Actual Actual Actual Actual/Proj Projection Projection Projection Projection2007 2008 2009 2010 2011 2012 2013 2014

VolumeAdmissions 9,551 9,977 9,402 8,883 9,118 9,317 9,520 9,728

Admissions - YOY % Change 4.46% -5.76% -5.52% 2.65% 2.18% 2.18% 2.18%

Comments Observed• Rough economy in 2008, 2009 and 2010• The competing facility that opened not far from here has probably taken all the volume that they will

prospectively; we’re hoping the worst is over• Volumes need to go back up to make a better operating margin

Volume – Example #2.

Volumes need to go back up to make a better operating margin

Actual Actual Actual Actual/Proj Projection Projection Projection Projection2007 2008 2009 2010 2011 2012 2013 20142007 2008 2009 2010 2011 2012 2013 2014

VolumeAdmissions 21,411 21,749 22,015 22,304 23,122 24,241 25,342 26,532

Admissions - YOY % Change 1.58% 1.22% 1.31% 3.67% 4.84% 4.54% 4.70%

Comments Observed• We have recruited 35 new physicians in 2010 which we expect will favorably impact 2011

© 2012 Crowe Horwath LLP 16Audit | Tax | Advisory | Risk | Performance

p y p y p• Each projection period calls for the addition of 20 new physicians• We are launching 1-2 new service line(s) per year• Our new cancer center will be completed at the end of 2011 and will impact 2012 forward

The Unique Alternative to the Big Four®

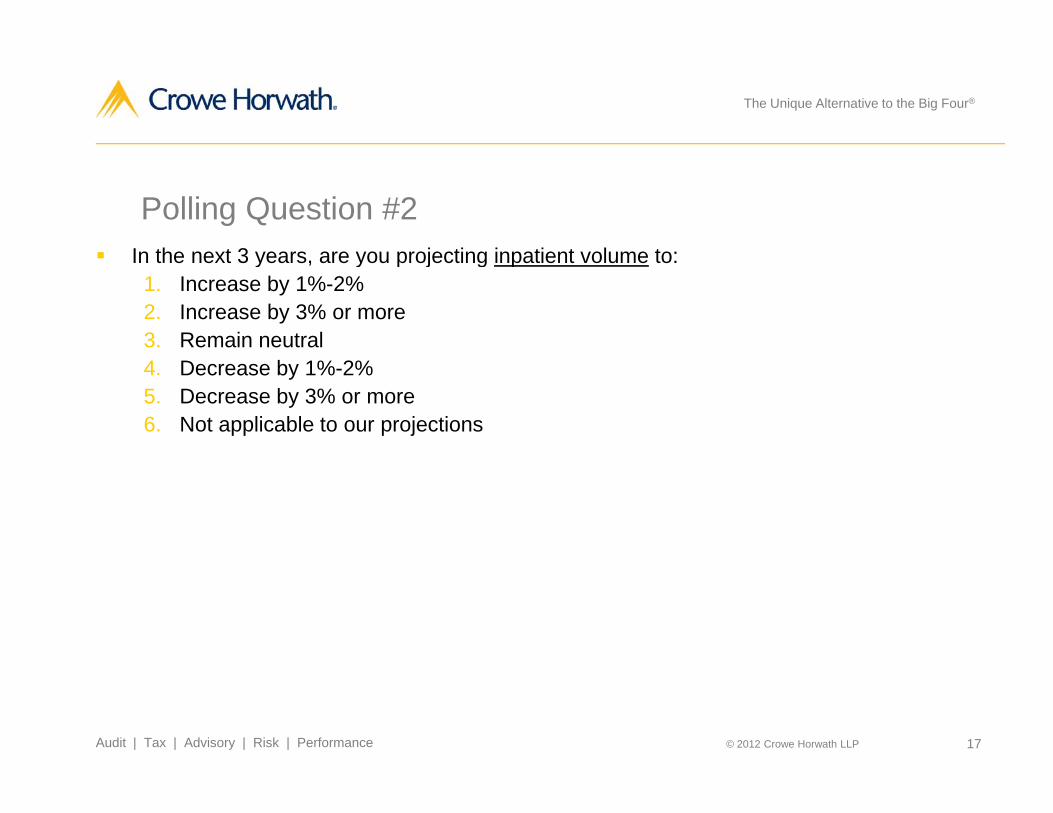

Polling Question #2 In the next 3 years are you projecting inpatient volume to: In the next 3 years, are you projecting inpatient volume to:

1. Increase by 1%-2%2. Increase by 3% or more3. Remain neutral4. Decrease by 1%-2%5. Decrease by 3% or more6. Not applicable to our projections

© 2012 Crowe Horwath LLP 17Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

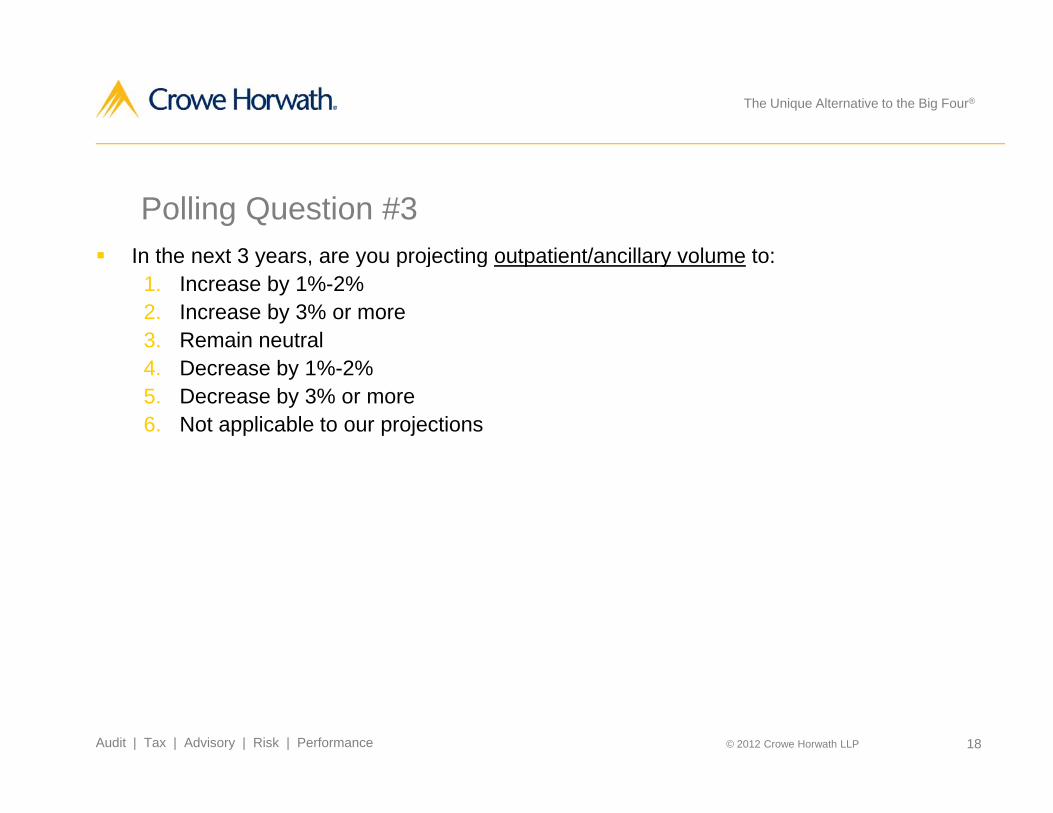

Polling Question #3 In the next 3 years are you projecting outpatient/ancillary volume to: In the next 3 years, are you projecting outpatient/ancillary volume to:

1. Increase by 1%-2%2. Increase by 3% or more3. Remain neutral4. Decrease by 1%-2%5. Decrease by 3% or more6. Not applicable to our projections

© 2012 Crowe Horwath LLP 18Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

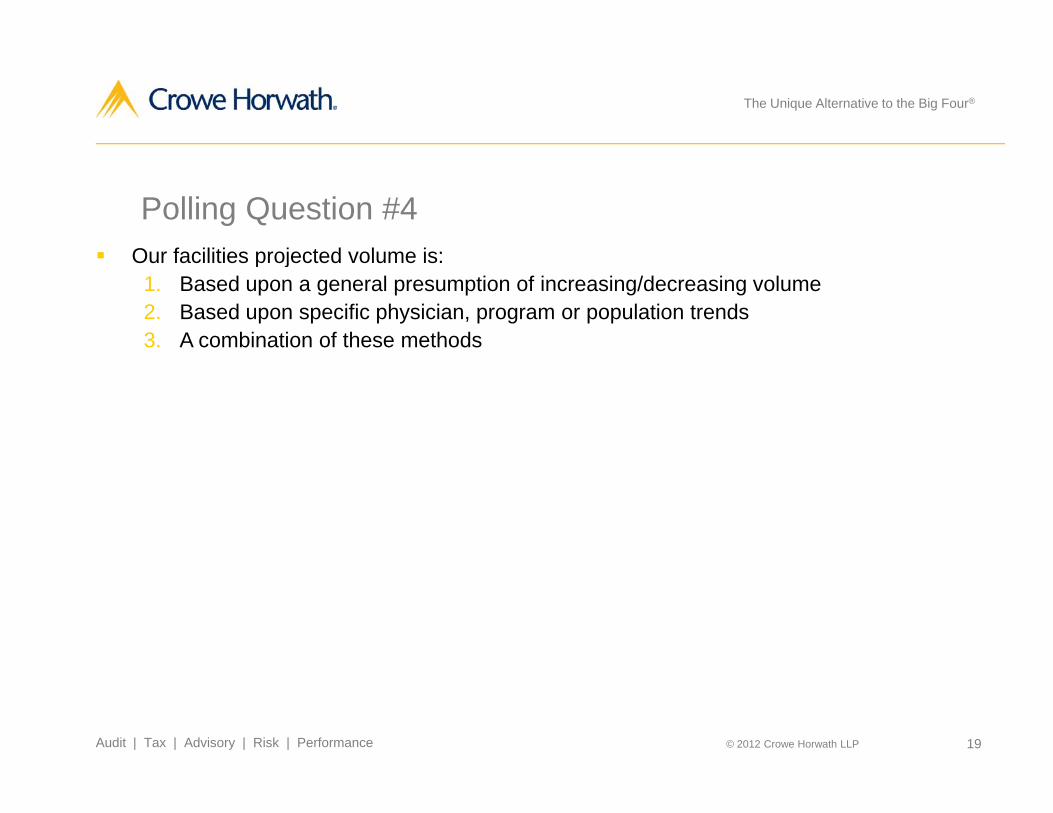

Polling Question #4 Our facilities projected volume is: Our facilities projected volume is:

1. Based upon a general presumption of increasing/decreasing volume2. Based upon specific physician, program or population trends3. A combination of these methods

© 2012 Crowe Horwath LLP 19Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

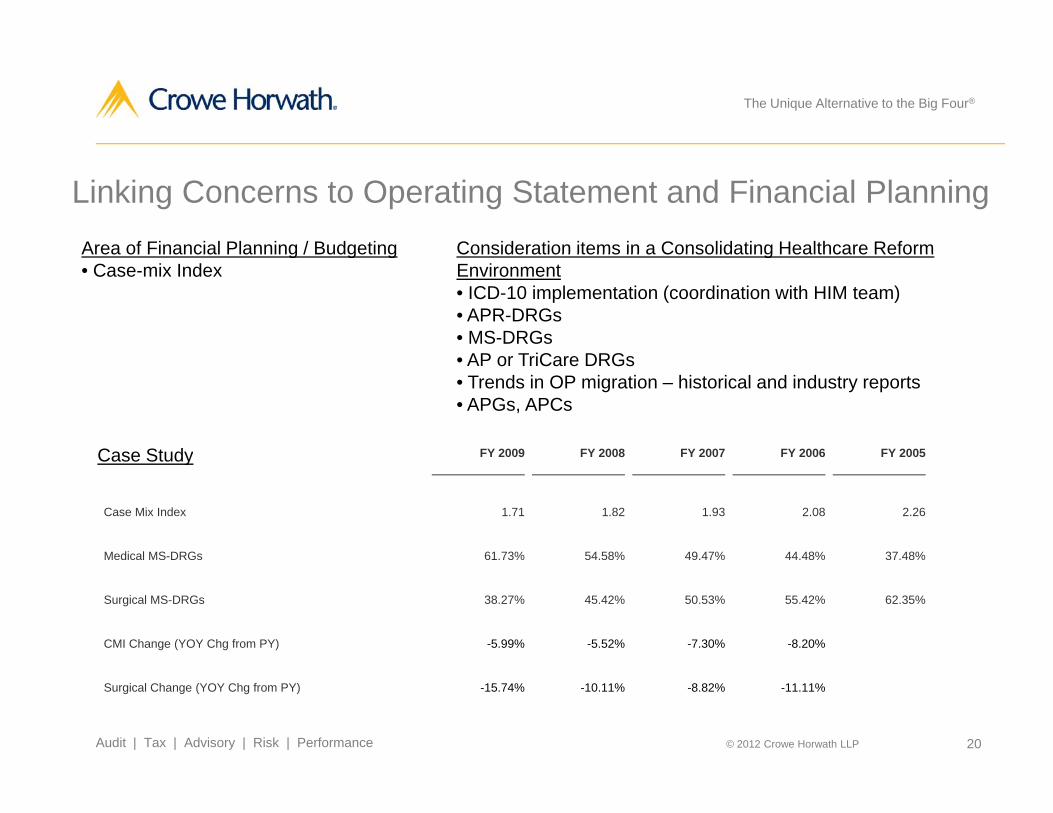

Linking Concerns to Operating Statement and Financial PlanningArea of Financial Planning / Budgeting Consideration items in a Consolidating Healthcare ReformArea of Financial Planning / Budgeting• Case-mix Index

Consideration items in a Consolidating Healthcare Reform Environment• ICD-10 implementation (coordination with HIM team)• APR-DRGs• MS-DRGs

AP T iC DRG• AP or TriCare DRGs• Trends in OP migration – historical and industry reports• APGs, APCs

FY 2009 FY 2008 FY 2007 FY 2006 FY 2005Case Study

Case Mix Index 1.71 1.82 1.93 2.08 2.26

Medical MS-DRGs 61.73% 54.58% 49.47% 44.48% 37.48%

Case Study

Surgical MS-DRGs 38.27% 45.42% 50.53% 55.42% 62.35%

CMI Change (YOY Chg from PY) -5.99% -5.52% -7.30% -8.20%

© 2012 Crowe Horwath LLP 20Audit | Tax | Advisory | Risk | Performance

Surgical Change (YOY Chg from PY) -15.74% -10.11% -8.82% -11.11%

The Unique Alternative to the Big Four®

Polling Question #5 Will ICD 10 APR DRGs: Will ICD-10, APR-DRGs:

1. Positively impact your case-mix index/patient acuity2. Negatively impact your case-mix index/patient acuity3. Have not yet determine what, if any, impact will occur

© 2012 Crowe Horwath LLP 21Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

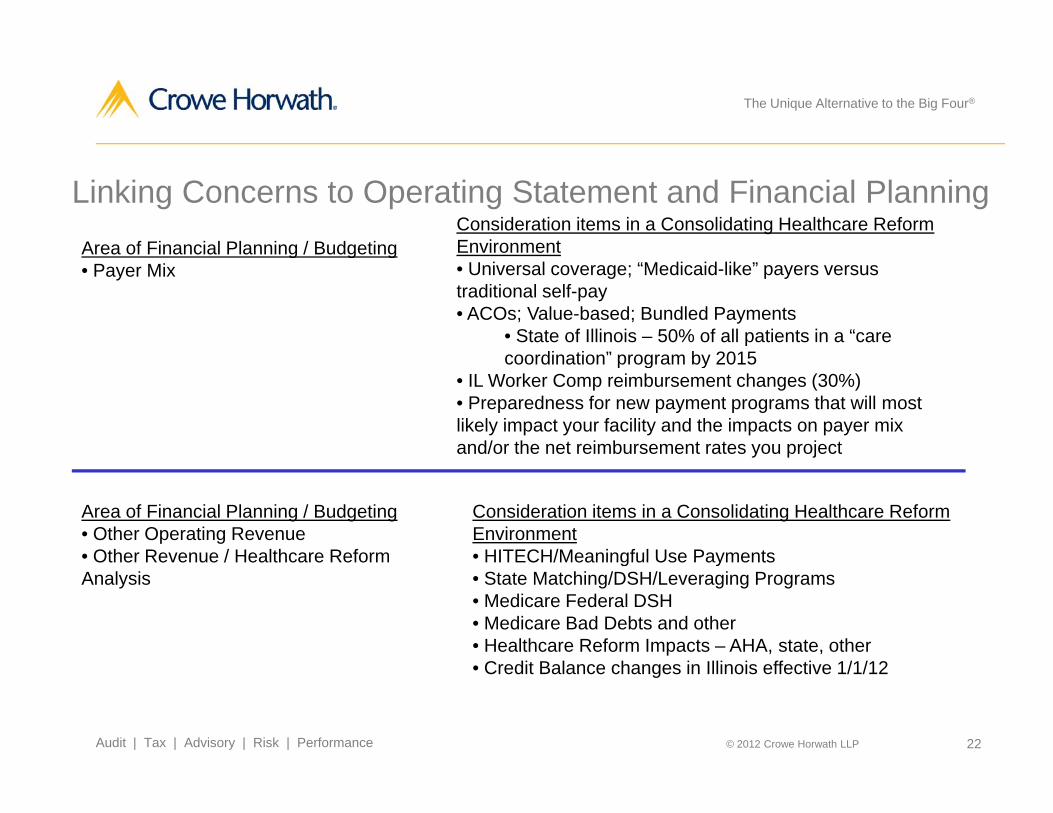

Linking Concerns to Operating Statement and Financial PlanningArea of Financial Planning / Budgeting

Consideration items in a Consolidating Healthcare Reform EnvironmentArea of Financial Planning / Budgeting

• Payer Mix • Universal coverage; “Medicaid-like” payers versus traditional self-pay• ACOs; Value-based; Bundled Payments

• State of Illinois – 50% of all patients in a “care coordination” program by 2015coordination program by 2015

• IL Worker Comp reimbursement changes (30%)• Preparedness for new payment programs that will most likely impact your facility and the impacts on payer mix and/or the net reimbursement rates you project

Area of Financial Planning / Budgeting• Other Operating Revenue• Other Revenue / Healthcare Reform

Consideration items in a Consolidating Healthcare Reform Environment• HITECH/Meaningful Use PaymentsOther Revenue / Healthcare Reform

AnalysisHITECH/Meaningful Use Payments

• State Matching/DSH/Leveraging Programs• Medicare Federal DSH• Medicare Bad Debts and other• Healthcare Reform Impacts – AHA, state, other

C dit B l h i Illi i ff ti 1/1/12

© 2012 Crowe Horwath LLP 22Audit | Tax | Advisory | Risk | Performance

• Credit Balance changes in Illinois effective 1/1/12

The Unique Alternative to the Big Four®

Polling Question #6 Our organization have factored ACO Value based and/or bundled payment impacts in a Our organization have factored ACO, Value-based, and/or bundled payment impacts in a

healthcare reform environment into financial projections:1. Yes2. No

© 2012 Crowe Horwath LLP 23Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

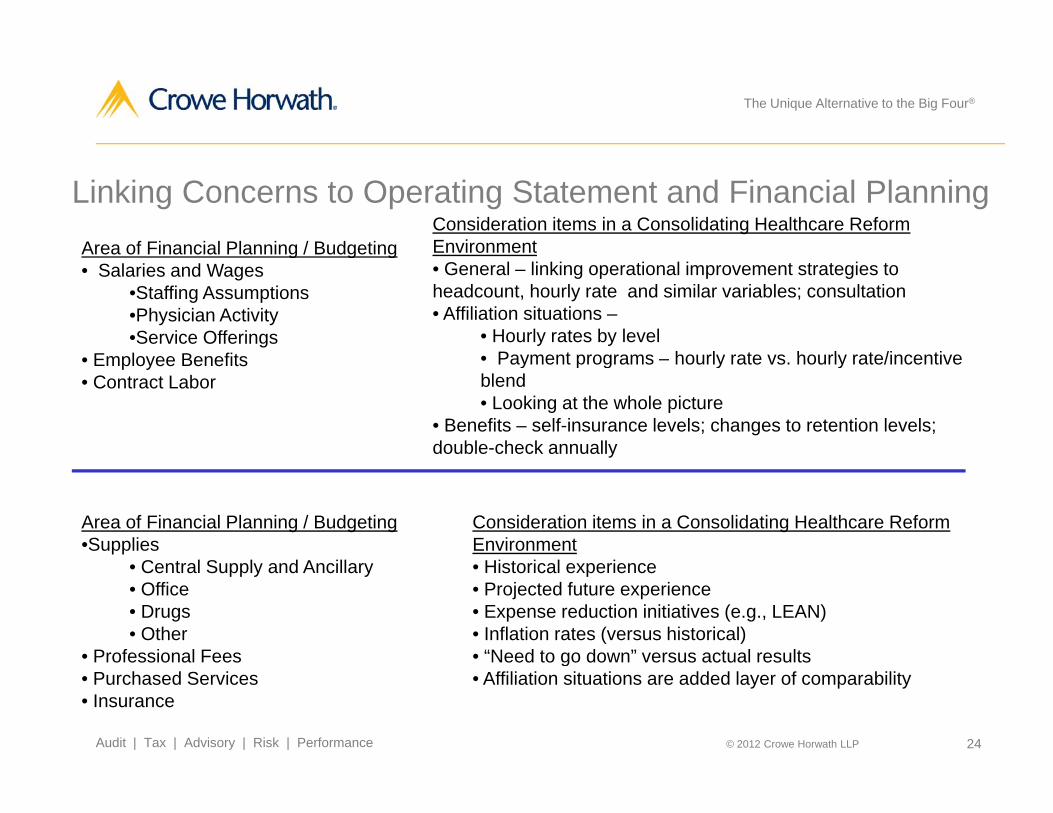

Linking Concerns to Operating Statement and Financial PlanningArea of Financial Planning / Budgeting

Consideration items in a Consolidating Healthcare Reform EnvironmentArea of Financial Planning / Budgeting

• Salaries and Wages•Staffing Assumptions•Physician Activity•Service Offerings

E l B fit

• General – linking operational improvement strategies to headcount, hourly rate and similar variables; consultation• Affiliation situations –

• Hourly rates by levelPayment programs hourly rate vs hourly rate/incentive• Employee Benefits

• Contract Labor• Payment programs – hourly rate vs. hourly rate/incentive blend• Looking at the whole picture

• Benefits – self-insurance levels; changes to retention levels; double-check annually

Area of Financial Planning / Budgeting•Supplies

C t l S l d A ill

Consideration items in a Consolidating Healthcare Reform Environment

Hi t i l i• Central Supply and Ancillary• Office• Drugs• Other

• Professional Fees

• Historical experience• Projected future experience• Expense reduction initiatives (e.g., LEAN)• Inflation rates (versus historical)• “Need to go down” versus actual results

© 2012 Crowe Horwath LLP 24Audit | Tax | Advisory | Risk | Performance

• Purchased Services• Insurance

g• Affiliation situations are added layer of comparability

The Unique Alternative to the Big Four®

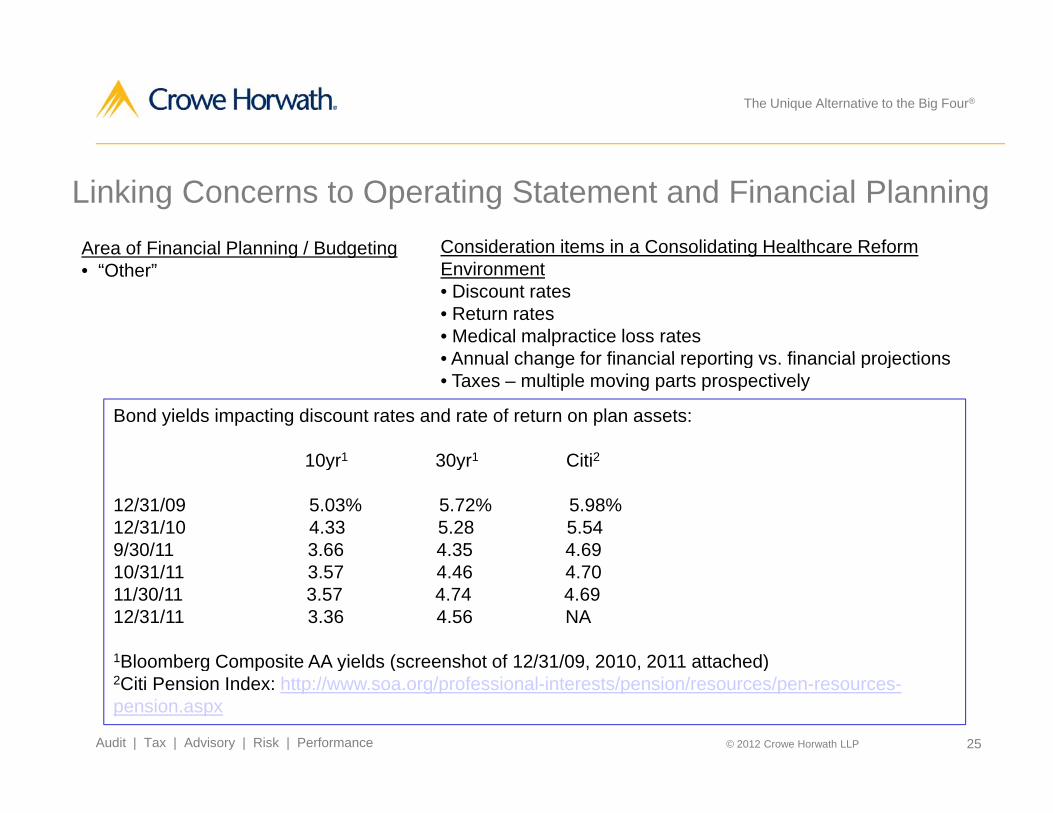

Linking Concerns to Operating Statement and Financial PlanningArea of Financial Planning / Budgeting Consideration items in a Consolidating Healthcare Reform Area of Financial Planning / Budgeting• “Other”

Co s de at o te s a Co so dat g ea t ca e e oEnvironment• Discount rates• Return rates• Medical malpractice loss rates

Annual change for financial reporting vs financial projections• Annual change for financial reporting vs. financial projections• Taxes – multiple moving parts prospectively

Bond yields impacting discount rates and rate of return on plan assets:

10yr1 30yr1 Citi210yr1 30yr1 Citi2

12/31/09 5.03% 5.72% 5.98%12/31/10 4.33 5.28 5.549/30/11 3.66 4.35 4.6910/31/11 3.57 4.46 4.7011/30/11 3.57 4.74 4.6912/31/11 3.36 4.56 NA

1Bloomberg Composite AA yields (screenshot of 12/31/09 2010 2011 attached)

© 2012 Crowe Horwath LLP 25Audit | Tax | Advisory | Risk | Performance

Bloomberg Composite AA yields (screenshot of 12/31/09, 2010, 2011 attached)2Citi Pension Index: http://www.soa.org/professional-interests/pension/resources/pen-resources-pension.aspx

The Unique Alternative to the Big Four®

Linking Concerns to Operating Statement and Financial Planning

Area of Financial Planning / Budgeting Consideration items in a Consolidating Healthcare ReformArea of Financial Planning / Budgeting• Investments

• Investment Allocation• Projected Returns by Investment Allocation

Consideration items in a Consolidating Healthcare Reform Environment• Historical experience• Projected future experience• Investment advisor guidance

• Capital Expendituresg

• For certain organizations, large projection versus actual results could significantly impact benchmark ratios and operations/capital spending• Affiliation situations are added layer of comparability

• Investment strategies between organizations• Investment strategies between organizations• Expected rates of return for similar asset classes

© 2012 Crowe Horwath LLP 26Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Accounting and Financial Reporting Snapshot HITECH/Meaningful Use – HFMA Whitepaper very helpful in explaining the grant accounting

th d l i ti th dmethodology versus gain contingency method ASU 2010-23, Health Care Entities: Measuring Charity Care for Disclosure ASU 2010-24, Health Care Entities: Presentation of Insurance Claims and Related Insurance

Recoveries ASU N 2011 07 H lth C E titi P t ti d Di l f P ti t S i R ASU No 2011-07 Health Care Entities: Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts and the Allowance For Doubtful accounts

ASU No 2011-08, Intangibles – Goodwill and Other Leases

ASU N 2010 20 R i bl (T i 310) Di l b t th C dit Q lit f Fi i ASU No. 2010-20, Receivables (Topic 310): Disclosures about the Credit Quality of Financing Receivables and the Allowance for Credit Losses

ASU No. 2010-06, Fair Value Measurements and Disclosures (Topic 820) : Improving Disclosures about Fair Value Measurements

AICPA Audit and Accounting Guide Health Care Entities AICPA Audit and Accounting Guide – Health Care Entities ASC 360: Impairment or Disposal of Long-Lived Intangible Assets Beginning look at these changes pre-recorded on 10/13/11 at:

http://www.crowehorwath.com/ContentDetails.aspx?id=3135&terms=healthcare%20accounting Refreshed look at these changes on 1/19/12 at: http://www crowehorwath com/event

© 2012 Crowe Horwath LLP 27Audit | Tax | Advisory | Risk | Performance

Refreshed look at these changes on 1/19/12 at: http://www.crowehorwath.com/event-detail.aspx?id=3793

The Unique Alternative to the Big Four®

Takeaways and comments from recent experiences……Line by line financial statement planning: What are key drivers What have they been historically What are we projecting in the future Does healthcare reform impact this line item Does recent industry activity impact our views Are outside macro trends like discount rates appropriately considered in our

models Do recent accounting and financial reporting changes impact our planning If affiliating or contemplating affiliation – how do we compare on key variables

and visions for the future Are projections reasonable and consistent in a consolidating healthcare reform

environment

© 2012 Crowe Horwath LLP 28Audit | Tax | Advisory | Risk | Performance

The Unique Alternative to the Big Four®

Contact information

Dave Frank, PartnerDave Frank, PartnerOffice: (630) 586-5237Email: [email protected]

Brian Kerby, DirectorOffice: (312) 857-7368Email: brian kerby@crowehorwath comEmail: [email protected]

Crowe Horwath LLP is an independent member of Crowe Horwath International, a Swiss verein. Each member firm of Crowe Horwath International is a separate

© 2012 Crowe Horwath LLP 29Audit | Tax | Advisory | Risk | Performance

and independent legal entity. Crowe Horwath LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. This material is for informational purposes only and should not be construed as financial or legal advice. Please seek guidance specific to your organization from qualified advisers in your jurisdiction. © 2012 Crowe Horwath LLP