Financial inclusion in Uganfa - COMCEC · FINANCIAL INCLUSION IN UGANDA ... Forex bureaus, Mobile...

40

FINANCIAL INCLUSION IN UGANDA A Presentation During the 2nd Meeting of the COMCEC Financial Cooperation Working Group, March 27th, 2014, at Crowne Plaza 0Hotel, in Ankara, Republic of Turkey By Kasenge Lawrence Economist, Microfinance Department, Ministry Of Finance, Planning And Economic Development, UGANDA

-

Upload

truongdiep -

Category

Documents

-

view

215 -

download

2

Transcript of Financial inclusion in Uganfa - COMCEC · FINANCIAL INCLUSION IN UGANDA ... Forex bureaus, Mobile...

FINANCIAL INCLUSION IN UGANDA A Presentation During the 2nd Meeting of the COMCEC Financial Cooperation Working Group, March 27th, 2014, at Crowne Plaza 0Hotel, in Ankara, Republic of Turkey

By Kasenge Lawrence Economist, Microfinance Department, Ministry Of Finance,

Planning And Economic Development, UGANDA

Outline of presentation

• Background

• Classification of Financial institutions

• FINANCIAL INCLUSION IN UGANDA-Key Findings of FINSCOPE Survey

• Financial Access Strands

• Challenges and Barriers to financial Inclusion

• Way Forward

Background Since 2006, the Uganda’s financial sector has experienced

positive changes, remarkably; in the increase of commercial banks (24 banks with over 400 branches), SACCOS and MFIS and informal financial institutions (VSLAs, ASCAs and ROSCAs) 20 insurance companies licensed and regulated by IRA In particular since 2009, there has been a dramatic increase in the

use of mobile money services

Government efforts to strengthen financial inclusion since 2001 With the above developments, there is need to explore the

extent to which these developments have translated into more financial inclusion of the adult population.

In Uganda this has been monitored through FinScope surveys since 2006, repeated every after three years

Financial Inclusion- Definition & Measurement Issues Financial inclusion means access to

basic financial services from reliable service providers in day to day life.

Financial Inclusion- Definition & Measurement Issues With no widely adopted uniform definition, financial inclusion is

reckoned in Uganda as access to financial services from:

a) Officially regulated and supervised entities

Banks and MDI institutions licensed by Bank of Uganda Insurance companies supervised by Insurance Regulatory

Authority, Capital market institutions like investment banks, merchant

banks, stock exchanges supervised by the Securities and Exchange Commission (SEC).

a) Official entities themselves

Post offices offering savings; Money transfer and insurance services; Mobile banking

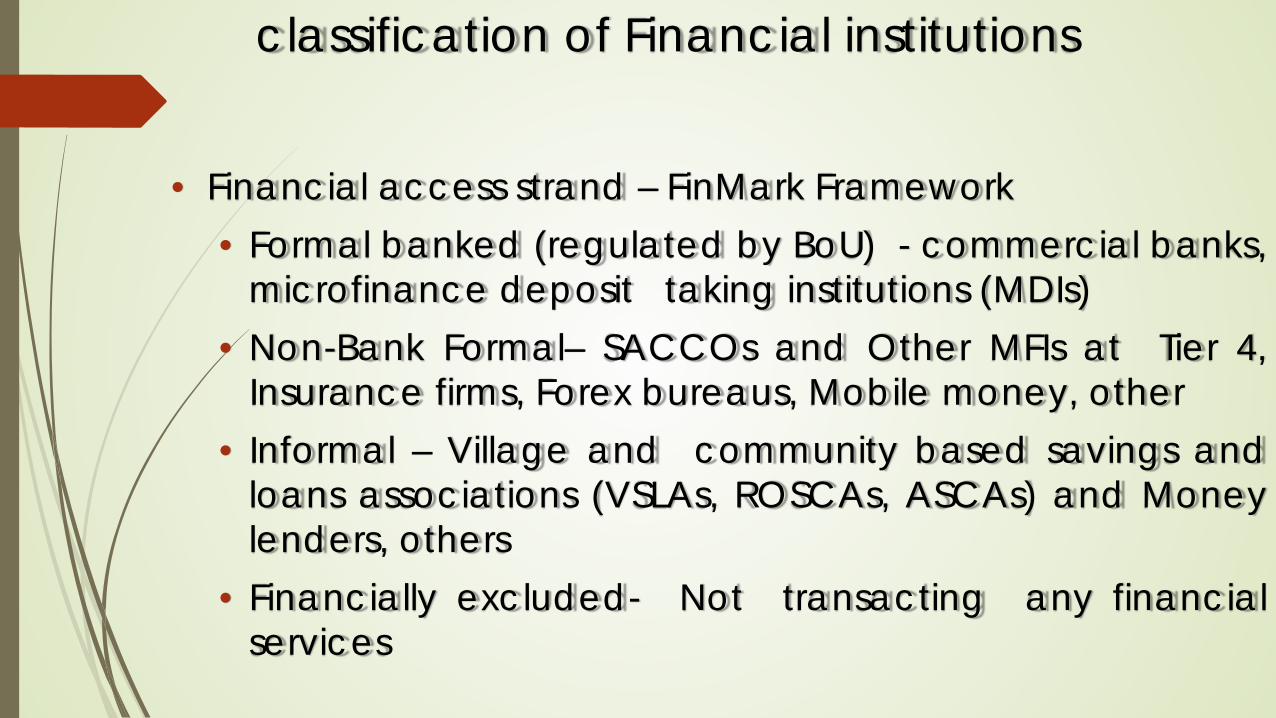

classification of Financial institutions

• Financial access strand – FinMark Framework

• Formal banked (regulated by BoU) - commercial banks, microfinance deposit taking institutions (MDIs)

• Non-Bank Formal– SACCOs and Other MFIs at Tier 4, Insurance firms, Forex bureaus, Mobile money, other

• Informal – Village and community based savings and loans associations (VSLAs, ROSCAs, ASCAs) and Money lenders, others

• Financially excluded- Not transacting any financial services

FINANCIAL INCLUSION IN UGANDA FINSCOPE 3 SURVEY 2013

Overall usage of financial services, % 2013 2009

30

60

20

21

28

Excluded

Informal

Non-bank formal

Formal bank

Formal

15

74

52

20

54

Excluded

Informal

Non-bank formal

Formal bank

Formal

Formal Product penetration Formal product penetration means products and services that are transacted through formal financial institutions (formal banked and non-bank formal) These include (operating a savings account, fixed deposit

account, joint account, current account, ATM card/Debit card, credit card, investment account, other)

The common ones are operating a savings account and ATM card/Debit card

Overall 20 percent of Adult Ugandans have accounts with formal financial institutions

SACCOs next to commercial banks seem to be picking up in providing account holding

Operating an account with formal financial institutions, % 74

8 5 5 7

1

50

5 5

21

8 11

Commercial bank MDIs Creditinstitutions

SACCOs MFIs Others

2009 2013

Product penetration…ctd

Who is likely to operate an account?

Urban residents

especially Kampala

Well to do households

Males Those in paid employment

Those wit higher

education

The main accounts operated are savings followed by ATM card/Debit, which are operated by more than 10 percent of the urban population

The most common

transactions with different banking points are deposit and withdraws by about 33 percent of the adult population in 2013

SAVINGS AND INVESTMENTS

Figure 6: Savings and investment strand, %

18

24

16

23

15

36

16

33

21

19

4

4

6

7

4

4

5

11

4

6

28

28

46

40

34

12

47

28

28

43

19

17

26

25

17

22

26

22

18

25

31

27

7

5

30

25

6

5

29

6

Female

Male

Female

Male

Rural

Urban

Rural

Urban

Uganda

Uganda

2009

2013

2009

2013

2009

2013

Formal Bank Formal Other Informal Home/Secret Place Excluded

Reasons for savings, %

7

9

11

13

22

33

41

67

Agricultural inputs

Business

Land

Safety

Livestock

Education

Emergency

Basic needs

Investment mechanisms, %

10

23

24

39

41

53

Investment in financialinstitution

Produce to sell later

Investing in business

Investment through informalinstitution

Livestock

Farm land

CREDIT & BORROWING

Overall access to credit % 2013

65

13

23

12

35

Unserved

Friends

Informal

Formal

All credit

2009

55

15

34

5

44

Unserved

Friends

Informal

Formal

All credit

7

10

13

14

15

20

Asset acquistion

Agricultural production

Business

Daily expenses

Emergencies

Education

Uses of credit from all sources, %

6

8

15

29

54

Farm equipment

Buy agricultural land

Buy livestock

Farm labour

Agricultural inputs

Reasons for accessing agricultural credit, %

Remittances and Transfers

Overall access to remittances & transfers, % 2013

26

41

55

Informal

Formal

Any remittances

2009

22

11

30

Informal

Formal

Any remittances

Insurance and Risk Management

Risks encountered in the last 12 months 2013,%

10

15

15

18

21

26

48

Death of livestock

Crop/livstock disease

Theft

Price fluctuations

Death of family member/relative

Drought

Ill-health of family member

Overall usage of insurance, % 2013

43

2

45

Informal

Formal

Any insurance

2009

21

3

23

Informal

Formal

Any insurance

Risk management mechanisms in 2013, %

8

13

15

18

18

Borrow from informal institution

Reduce consumption

Sale assets

Seek for donations

Borrow from friends/family

Mobile Money Services

Mobile Money Services in 2013

56

34

77

Currently using

Registered user

Knowledge about mobile money

Knowledge & use, %

33

46

54

56

Cash deposits

Send money

Receive money

Cash withdrawal

What transactions done, %

Challenges to financial inclusion

Challenges to Financial Inclusion: Bank accounts, %

47

22 18 17

Do not haveincome

Cost of operatingaccount

Do not understandhow it works

Do not have a job

Challenges to savings and investments, %

44 47

3

Do not have money toinvest

Do not have adequateinformation on savings

Lost money in investmentbefore

Challenges to credit & borrowing, %

31

14 13

9

Fear of debts Loans are tooexpensive

Lack of security I do not think I amcredit worthy

Challenges to informal insurance in 2013, %

43 40 39

29

22 19

Members do notpay contributions

Members keeppulling out

Death occurred tomembers

Dishonesty bymembers causing

financial loss

Pooradministration

Loss of moneythrough theft or

fraud from aCommittee

member

%

Challenges to formal insurance in 2013, % 55

17 17

10 6

Does not knowhow it works

Never thoughtabout it

Lack knowledgeon how

Does not knowwhere to go

Do not want it

Barriers to using mobile money services 2013, %

26

19

11 9

6

No cell phone No money tosend/receive

No sim card Not enoughinformation

Not though aboutit

Challenges from the supply side

the transaction costs that the bankers incur, poor communication, lack of infrastructure, language barriers, low literacy levels poor technology High costs of providing services

Challenges from the supply side cont’d

Few branches or service outlets of banks and other formal financial institutions in rural areas;

Small sized transactions with the poor which is seen as un-remunerative and unattractive by the financial institutions;

Quite difficult to have a One-Size-Fits-All financial inclusion policy and regulations for the different players

Absence of sufficient data on institutions especially on microfinance institutions

Lack of a definitive present address of rural migrants in urban areas.

Challenges on the supply side cont’d

• Legislative Requirements – The legislative environment may hinder establishment

of financial inclusion policies Capital adequacy requirements, audited balance sheets, size of business, threshold category based on number of members

and professionalism – They aim at financial sustainability but are a constraint

to inclusion

WAY FORWARD-How to address challenges

“Cooperation”. policy makers can work together in - engineering solutions, - creating a financial inclusion enabling environment, - designing regulation and infrastructure, - monitoring progress and assessing policy achievement.

WAY FORWARD-How to address challenges cont’d • Build bridges and collaborations between

Government institutions concerning policy on financial inclusion.

• Cooperation across departments within the same level of Government.

• Ensure inter-sectoral collaboration for communities that are to play an active role in the policy-making process.

• Build financial literacy so that people have realistic expectations and understand their rights

WAY FORWARD-How to address challenges cont’d

Information Technology: a major breakthrough Lower borrowing costs made possible by IT based

remote delivery and recovery of loans can enable many currently excluded individuals to borrow for new output activities.

Some public utilities are already collecting utility bills from users through mobile phone based arrangements.

Cost saving IT based remote delivery arrangements are possible for numerous government payments like social safety net allowances, pension payments, and so on.

Concluding Remarks There may never be an occasion to call the tasks of

financial inclusion and poverty eradication over and done with.

In conclusion, we should deeply keep in mind that financial inclusion combats poverty by: unblocking advancement opportunities for the

disadvantaged poor; fostering social inclusion; Promoting inclusive socioeconomic growth.

Many thanks