Financial Constraint, Margins of FDI and Aggregate ...literature. (Muuls 2008, Berman and Hericourt...

25

Bond Finance, Margins of FDI and Aggregate Industry Productivity 1 Jiarui ZHANG Lei HOU 2 Department of Economics Department of Economics University of Munich, Germany University of Munich, Germany and Jilin University of China AUTHORS INFORMATION 1. Jiarui ZHANG, PhD candidate at Department of Economics, University of Munich, Germany. Research Interest: Monetary Policy, Real Business Cycles, Corporate Financial Structure, Soft Budget Constraint. Address: Schackstrasse 4, D-80539, Munich, Germany. Tel.0049-89-21803113 email: [email protected]. 2. Lei HOU, PhD candidate at School of Economics, Jilin University, P.R.China and Department of Economics, University of Munich, Germany. Research Interest: International Trade, Multinational Corporations. Address: Room 219, Ludwigstrasse 28, D-80539, Munich, Germany. Tel.0049-89-21806286 email: [email protected], [email protected]. ABSTRACT: In this paper, we introduce bond issuing as another external financing source besides bank credit in heterogeneous firms setup and investigate the impact of financial constraints on firms’ margins of Foreign Direct Investment (henceforth FDI). We show that, facing a bank credit supply shock (negative shock, e.g.), FDI firms of different productivities react in different ways. Some less productive firms will be forced to exit the foreign market. These firms have no more incentive to issue bond to finance their foreign production so that their total bond issuing will decrease (complementary effect of bank credit and bond issuing). In contrast, some very productive firms will maintain FDI, and they will issue bond as the alternative finance to compensate the decrease of bank credit (substitution effect). As for the impact on margins of FDI, on one hand, less credit availability leads to higher cutoff productivity for FDI and lower expected profit, consequently firms are less likely to do FDI(extensive margin); on the other hand, less credit access does not necessarily result in contraction in affiliate sales. Firms could reallocate available funds, including internal funds and funds from issued bond to keep production unaffected (intensive margin). Furthermore, we examine the aggregate industry outcome in general equilibrium. We find that firms’ foreign expansions cause selection effect across heterogeneous firms through the adjustment in bond market and labor market, and bring aggregate productivity gains. Our model shows that whether worse credit conditions intensify or weaken the productivity gains is ambiguous, which relies on the overall outcome of complementary effect and substitution effect. JEL: F21, F23, F36, G11, G21 KEYWORDS: bond market, financial constraint, heterogeneous firm, productivity, intensive margin of FDI, extensive margin of FDI 1 For helpful comments and discussions, we thank Prof. Dr. Dalia Marin, Prof. Dr. Monika Schnitzer, Prof. Dr. Gerhard Illing, Prof. Dr. Carsten Eckel, Prof. Dr. Gianmarco I.P. Ottaviano, Dr. Alexander Tarasov and all the participants of International Economics Workshop, Macro Seminar and IO & Finance Seminar at University of Munich, and also the participants of CES 2010 annual conference at Xiamen. Jiarui Zhang gratefully acknowledge funding under China Scholarship Council. Lei Hou gratefully acknowledge funding under Bavarian Elite Aid Act (Bayerischen Eliteförderungsgesetz, BayEFG) program. All errors and inconsistencies are our own. 2 Corresponding author. Fax: 0049-89-21806227. Email: [email protected], [email protected].

Transcript of Financial Constraint, Margins of FDI and Aggregate ...literature. (Muuls 2008, Berman and Hericourt...

Bond Finance, Margins of FDI and Aggregate Industry Productivity1

Jiarui ZHANG Lei HOU2

Department of Economics Department of Economics

University of Munich, Germany University of Munich, Germany and Jilin University of China

AUTHORS INFORMATION 1. Jiarui ZHANG, PhD candidate at Department of Economics, University of Munich, Germany. Research Interest: Monetary Policy, Real Business Cycles, Corporate Financial Structure, Soft Budget Constraint. Address: Schackstrasse 4, D-80539, Munich, Germany. Tel.0049-89-21803113 email: [email protected]. 2. Lei HOU, PhD candidate at School of Economics, Jilin University, P.R.China and Department of Economics, University of Munich, Germany. Research Interest: International Trade, Multinational Corporations. Address: Room 219, Ludwigstrasse 28, D-80539, Munich, Germany. Tel.0049-89-21806286 email: [email protected], [email protected].

ABSTRACT: In this paper, we introduce bond issuing as another external financing source besides bank credit in heterogeneous firms setup and investigate the impact of financial constraints on firms’ margins of Foreign Direct Investment (henceforth FDI). We show that, facing a bank credit supply shock (negative shock, e.g.), FDI firms of different productivities react in different ways. Some less productive firms will be forced to exit the foreign market. These firms have no more incentive to issue bond to finance their foreign production so that their total bond issuing will decrease (complementary effect of bank credit and bond issuing). In contrast, some very productive firms will maintain FDI, and they will issue bond as the alternative finance to compensate the decrease of bank credit (substitution effect). As for the impact on margins of FDI, on one hand, less credit availability leads to higher cutoff productivity for FDI and lower expected profit, consequently firms are less likely to do FDI(extensive margin); on the other hand, less credit access does not necessarily result in contraction in affiliate sales. Firms could reallocate available funds, including internal funds and funds from issued bond to keep production unaffected (intensive margin). Furthermore, we examine the aggregate industry outcome in general equilibrium. We find that firms’ foreign expansions cause selection effect across heterogeneous firms through the adjustment in bond market and labor market, and bring aggregate productivity gains. Our model shows that whether worse credit conditions intensify or weaken the productivity gains is ambiguous, which relies on the overall outcome of complementary effect and substitution effect. JEL: F21, F23, F36, G11, G21 KEYWORDS: bond market, financial constraint, heterogeneous firm, productivity, intensive margin of FDI, extensive margin of FDI

1 For helpful comments and discussions, we thank Prof. Dr. Dalia Marin, Prof. Dr. Monika Schnitzer, Prof. Dr. Gerhard Illing, Prof. Dr. Carsten Eckel, Prof. Dr. Gianmarco I.P. Ottaviano, Dr. Alexander Tarasov and all the participants of International Economics Workshop, Macro Seminar and IO & Finance Seminar at University of Munich, and also the participants of CES 2010 annual conference at Xiamen. Jiarui Zhang gratefully acknowledge funding under China Scholarship Council. Lei Hou gratefully acknowledge funding under Bavarian Elite Aid Act (Bayerischen Eliteförderungsgesetz, BayEFG) program. All errors and inconsistencies are our own. 2 Corresponding author. Fax: 0049-89-21806227. Email: [email protected], [email protected].

1. INTRODUCTION

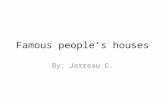

Facing the same shock, firms of different productivity may react differently. For example, during the current financial crisis, some firms cut sales while some firms expand the injection of working capital. When bank credit suddenly becomes tight, some “less able” firms give up their foreign market while some “very able” firms find alternative finance to keep their multinational status (see evidence below). This paper aims to model this observation. Since Melitz (2003) and Helpman et al. (2004), it is widely believed and empirically supported (somehow) that firm’s productivity is a key determinant for its internationalization. Manova (2007) introduces export‐oriented bank credit and takes credit constraint as another important determinant for firms’ export. She argues that the ability to export also depend on the level of financial development and credit availability. Only those firms who are more productive as well as less credit constrained export. The impact of financial factors on firms’ internationalization is confirmed by a new body of empirical literature. (Muuls 2008, Berman and Hericourt 2008, Li and Yu 2009, Buch et al. 2009, Jarreau and Poncet 2010). The recent financial crisis and simultaneous drawdown in export and FDI also prove the potential link between financial situation and firms’ decision making. Overall, both export and FDI decline as a result of credit crunch, which is consistent with literature predictions. However, if we look carefully at the firm level activities, we find that a fraction of firms reallocate more internal fund to finance working capital and their sales keep unchanged or even expand, especially in domestic‐oriented or non‐tradable sectors ,3 4 (World Bank Financial Crisis Survey 2010, 2010 Survey on Current Conditions and Intention of Outbound Investment by Chinese Enterprises. See figure 1). This means facing a credit supply shock, firms of different productivities react in different ways.

Percent of firms with sales increase (2009/2008) by country

14.8

9.2

5.4

4.9

6.1

14.1

0 2 4 6 8 10 12 14

Turkey

Romania

Lithuanian

Latvia

Hungary

Bulgaria

Figure 1: firms that benefit from crisis Figure 2: corporate bond spreads

3 This observation may be considered as the reallocation effect in Melitz(2003), but that reallocation effect tells the story that when a economy shifts from autarky to openness, each firm in home country faces a new segmented market and therefore it wants to expand. The more productive firms can actually do this because expansion incurs additional fixed cost. When those firms expand in a segmented market, the total labor demand will be higher in open economy, which pushes the real wage up. Facing higher production cost, the less productive firms have to cut sales or even exit. Our observation differs from the above reallocation in principle because the shock in the observation does not come from the product market but capital market and we will focus more on reallocation of working capital instead of product market share. . 4 Another branch of literature on pro-competitive effect sheds light on reallocation effect. For example, Melitz and Ottaviano (2008) build a model with endogenous markup: when some firms go to bankruptcy or contract sales, other firms can take advantage of it and expand the market share. This is essentially also the product market reasoning. The question we address here based on those observations is that when those firms aim to expand, where do they get additional finance, given that the bank credit has been tight? This motivates our second external finance source: corporate bond.

- 1 -

For those expanding firms, we address the question that where do they get the finance, given that the bank credit has been tight? One problem of the existing literatures is that borrowing from bank is the only external finance source. When bank credit is tight, all firms have nothing to do but cut sales. However, in reality, firms have other financing sources, such as issuing bond, stock or obtaining special financial support from trade partners or government etc that are substitutions of loan. When there is a credit crunch, some less productive firms will stop producing while some very productive firms will go to other external finance (even if it is more expensive) to maintain their sales. During the current crisis, under limited internal resources and tighter credit constraints, firms resort to issuing bond to finance production, which bid up the bond return rate dramatically. (World Investment Report 2009, see figure 2). Manova (2008) examines the impact of equity market liberalization on export composition, which implies other external financing source besides bank credit also matters. Based on these facts, we motivate a bond market and reexamine firms’ production and internationalization decision. Our main purposes are to examine how firms react differently when there is a credit supply shock and what the aggregate outcome will be with bond market as the channel for working capital reallocation among heterogeneous firms. Specifically, we are trying to answer the following questions: how do firms allocate internal and external funds to different investment projects? How do the two external financing sources, i.e. bank credit as the indirect financing and bond issuing as the direct financing, interact each other and influence firms’ financial status? What is the effect of financial constraint on firms’ internationalization? Furthermore, what is the impact of a credit supply shock on bond market and hence on aggregate productivity? We do that by adopting Melitz’s (2003) setup, using Dixit‐Stiglitz differentiated goods and heterogeneous firms for the case of FDI. Our model derives the standard result that financial constraint affect firm’s internationalization while differs from existing literature at several major respects. In the first place, we model the facts that firms have limited internal fund. Because of the limited internal fund, costly raising external finance for working capital is considered and the financing cost becomes one component of production cost, which will be reflected in product price. More importantly, under limited internal funds, firms’ various investment projects are related to each other. This setup then models firms’ decisions of domestic production, external financing and FDI inseparably (as argued by Buch et al, 2009, Li et al, 2010). It differs from previous literature which assumes that when there is another segmented market (e.g. when economy opens), firms can costlessly raise fund to serve that market. In the second place, this paper tries firstly proposing a perfect bond market in which firms can either issue or buy bonds. This proposition has realistic counterpart as we motivated above and plays an important role in the economy: (1) with the existence of a bond market, firms’ outside option for production is not zero but a safe bond holding return. Firms of very low productivities would rather invest their entire internal fund on buying bond. In contrast, a firm who is very productive but does not have enough internal funds for production can issue bond. Since the bond market is perfect, all bonds are the same and share the same return rate which is determined by bond market clearing condition. A single firm is a price taker in the bond market. (2) when bank credit is tight, some less productive firms are forced to exit from doing FDI whereas the most productive firms will increase bond issuing as an

- 2 -

alternative finance to stay in FDI due to the high profit. Therefore, the bond market can be “more competitive” and the bond return rate will increase. This is what we observe during the financial crisis. (3) the adjustment of bond return rate may induce Melitz‐type selection effect through bond market and influence welfare of the economy. In the third place, we analyze bond issuing and borrowing from bank in the following aspects. For simplicity, we assume the bank loan is only going‐abroad oriented and it requires no external finance premium, i.e., borrowing for domestic production is not possible but borrowing for FDI has no cost. We focus on how much a firm can borrow against certain collateral (we call it credit multiplier) and how this possible amount of borrowing affects firms’ FDI decision. In comparison, the bond return rate is positive which reflects the cost of raising capital, or the premium of external finance over internal finance. Both credit multiplier and bond rate reflect financial constraints. Based on this setting, we examine how the two types of external finance interact and co‐determine the extensive margin and intensive margin of FDI (which are defined by Buch et al. 2009, as the decision to enter a foreign market for the first time and the decision on the volume of foreign affiliates’ sales respectively). We further derive the general equilibrium to investigate whether better credit condition (financial development) intensifies the welfare brought by FDI in home country. Last but not least, we assume that FDI incurs additional fixed cost and it is uncertain in a sense that some cost reveals only when a firm sets foot on the foreign land. FDI is successful if and only if the additional fixed cost turned out to be fully covered. Ex ante, an FDI firm might prepare some fund (possibly from internal fund, bond market or borrowing from bank) such that the firm expects a probability of FDI’s success. The cost of keeping this fund is the opportunity cost bond return, while the benefit is the likelihood of earning FDI’s profit. Therefore, the firm tradeoffs the cost and the benefit and endogenously determines the probability of success for FDI. Using this framework, we are able to derive the results obtained by Melitz (2003) and some financial constraint literature mentioned above: there are two productivity cutoffs, one for domestic production and one for FDI. The FDI cutoff productivity is higher than domestic production cutoff but the difference can be very small taking financial factors into account, as it is observed by Buch et al (2009) that average productivity of FDI firms is not significantly higher than non‐FDI firms (German firm data). Firms are partitioned by these two cutoffs: those whose productivities are lower than domestic production cutoff do not produce but invest all internal fund in holding bond; those whose productivities are between domestic cutoff and FDI cutoff produce but only serve home market, whether they buy bond or issue bond depends on how much internal fund they have and their revealed productivities; those whose productivities are higher than FDI cutoff will become multinationals. The more productive a firm is, the more working capital it needs. In addition, we provide explicit expressions to show that firms’ financial situation affects their internationalization. In our setting, the parameters that reflect financial constraints, i.e. credit multiplier and bond return rate, enter prices of varieties and the cutoff productivity for FDI, meaning both margins of FDI depend on the financial constraints. Looser financial constraints (larger credit multiplier or lower bond rate) make the cutoff productivity for FDI lower in a sense that more firms are able to go abroad (extensive margin of FDI). The prices of FDI goods will also be lower, meaning the affiliate sales will increase (intensive margin of FDI).

- 3 -

Going beyond the above results, our setting allows us to add some new insights to financial constraint literatures. We study why firms behave differently facing an exogenous credit shock, taking credit crunch as an example. When there is credit crunch, firms adjust their investment portfolio and financing structures, which induces two opposite outcome in bond market. For less productive firms, tighter bank credit hinders them from doing FDI and therefore these firms have less incentive to issue bond. It means less credit availability leads to less bond issuing and lower bond rate. We call this complementary effect between bank credit and bond issuing. In comparison, for those very productive firms, FDI is still profitable even with higher financing cost. Under tighter bank credit, they use money from issued bond to substitute bank credit and stay in FDI, which bids up the bond rate. This is called substitution effect. Overall, the two effects induce a reallocation effect of working capital towards more productive firms through bond market. Furthermore, as bond rate works as a financial cost in our model, the increase of bond rate will trigger a Melitz‐type selection effect and bring aggregate productivity gains. Apparently, the bank credit availability could affect the bond rate (the aggregate result of complementary and substitution effect), but the direction depends on the distribution of firms’ productivities. Our paper contributes to the growing literatures on financial constraint and firms’ internationalization. A large literature has confirmed the role of financial factor on firm’s production and internationalization. (Beck 2002, Beck2003, Beck et al. 2005b, Manova2007, Muuls 2008, Berman and Hericourt 2008, Li and Yu 2009, Buch et al. 2009, Arndt et al. 2009). Manova(2007) introduces financial constraint into Melitz(2003) and argues that the existence of financial constraint will intensify the negative effect of low productivity on firms’ export. Her empirical findings at industry level are consistent with the theoretical predictions. Following Manova(2007), Jarreau and Poncet(2010) sets up specific indicators for Chinese financial system efficiency and investigate the interaction of financial system efficiency and the trade structure in China. They confirm the persistence of credit constraints in China and find that the distortions of financial system hamper export growth and result in unbalanced impact on trade structure. They also point out that the inflow of foreign investment acts as a substitute to domestic credit and helps to relax the credit constraints. Muuls(2008), Berman and Hericourt(2008), Li and Yu(2009) examine the impact of financial constraint on firms’ export with firm‐level data. Muuls(2008) and Berman and Hericourt(2008) emphasize the interaction of productivity and credit constraint firms face. Only those firms with both high productivity and low credit constraint are able to export. Muuls(2008) further show that credit constraints restrict the number of export destinations whereas the average export volumes across destinations keep unaffected. Li and Yu(2009) model firm‐specific financial constraint as a function of its productivity. They show that more productive and therefore less financially constrained firms are more likely to do export. They introduce initial wealth and trade credit as substitutes for traditional external credit from banks and also show their impacts on export. Compared to export, researches on the impact of financial constraint on FDI are less. Buch et al.(2009) develops a model with both real and financial factors and provide empirical evidence with German multinationals data. They show that the financial barrier limit firms’ FDI, which is more severe for larger firms. The parent‐level financial constraint matters more for extensive margin of FDI whereas affiliate‐level financial constraint matters more for intensive margin. Arndt et al.(2009) analyzes potential constraints over firms’ internationalization, including both export and FDI. The evidence from

- 4 -

German firm‐level data shows the positive relationship between firm size, productivity and firm’s internationalization. Compared to financial constraint, the constraint from labor market matters more. This paper differs from previous literature in the following aspects. Firstly, we model firms’ international activities (FDI here) inseparably with domestic activities. By doing so, we could explain how firms redistribute available funds between domestic and foreign investments as a reaction to financial shock. Secondly, in comparison to the general prediction of overall shrink in international activities when there is a bad credit shock in previous literatures, we find the firms who are exceptions: these firms resort to other source of finance. This paper is organized as follows: section 2 presents the model and discusses our propositions, both in closed economy case and open economy case. Section 3 gives the general equilibrium and examines the aggregate outcome. Section 4 concludes.

2. MODEL

Consider a world with two countries. We call one country as home (domestic country) and the other as host (foreign country).There is a continuum of firms, indexed by i, producing differentiated varieties in each country. Firm i is born with initial internal fund Ni. Ni is a random number from a common distribution Γ( Ni). To know its productivity, the firm must pay an entry cost of fe, then it draws a productivity ϕi from a common distribution g(ϕ) (Melitz 2003). With the knowledge of its own productivity, the firm faces three potential investment choices: (1) holds bond Bi; (2) invests domestic production, i.e. produces and sells a distinct product ω in the home country and the output is denoted by qiD; (3) does FDI, i.e. produces and sells ω in host country and the output is denoted by qiF. Note that the subscript D denotes variables for domestic production whereas F for foreign production. This applies to the whole paper. There is a perfect bond market where firms can either buy or issue bonds (Bi could be either positive or negative). Upon a draw of very low productivity, producing is not as profitable as buying bond. The firm therefore invests all its internal fund on bond holdings to get a safe return. Upon a draw of high productivity, on the contrary, the firm will produce. If its internal fund is not enough to pay labor which is the only input for production, the firm will issue bond to raise working capital. There is no fixed cost for the firm to invest in bond market. In contrast, if the firm engages in production, no matter domestic production or FDI, it must pay a fixed overhead cost f to setup the factory. In addition, there is an extra fixed cost CF for FDI. All kinds of fixed cost are measured in labor unit while the sunk cost of entry fe. is in money unit. 2.1 CLOSED ECONOMY This subsection provides the closed economy case as a bench mark in which firms only serve domestic market. 2.1.1 DEMAND The utility function of a representative consumer is

- 5 -

( ) 11 −

Ω∈

−

⎥⎦⎤

⎢⎣⎡= ∫

εε

ωεε

ωω dqU

where the set Ω represents the mass of available varieties and ε denotes the elasticity of substitution between any two varieties. Define the aggregate good Q ≡U with aggregate price

( )[ ] εω

ε ωω −Ω∈

−∫= 11

1 dpP

and solve the EMP (Expenditure Minimization Problem) of the consumer, we have the demand function for every variety ω.

( ) ( ) Qp

Pqε

ωω ⎟⎟

⎠

⎞⎜⎜⎝

⎛= (1)

2.1.2 PRODUCTION Each firm i produces a distinct variety ω and its output for domestic market is denoted as qiD. Labor is the only input. Define the cost function for producing qiD as:

fq

li

iDiD +=

ϕ (2)

where f >0 is the fixed cost for production measured in labor units, which is the same for any single firm. ϕi is the firm‐specific productivity. Domestic nominal wage is denoted as wD. Assume that labor must be prepaid. 2.1.3 BOND MARKET Assume bond market is perfect in a sense that it is competitive and there is no information asymmetry, and the equilibrium bond rate is r. Firms can invest their internal funds in buying bond and get a return rate of 1+r. Those firms whose domestic production is confined by limited internal fund can also issue bond in bond market at the rate of 1+r. In general equilibrium setting, bond return rate r is determined by the condition that there is no aggregate net demand of bond. For a single firm, however, r can be viewed as given. The perfect bond market setting is simple as a starting point for our model but can of course be extended. 2.1.4 FIRMS’ OPTIMAL DECISION In closed economy, firm i allocates its own internal fund between bond holding Bi and domestic production qiD (if it produces) and maximizes the total profit from the investment portfolio. Firm i solves

iiD Bp ,max iiDDiDiDiD rBlwqp +−=π

eiiiDD fNBlw −≤+s.t. ; (1); (2)

where piD is product price in home country. We have:

( rwpi

DiD +

−= 1

1 ϕεε ) (3)

( )( ) Q

rwP

qD

iiD

ε

εϕε

⎥⎦

⎤⎢⎣

⎡+

−=

11

(4)

- 6 -

( )( ) fQ

rwPl

DiiD +⎥

⎦

⎤⎢⎣

⎡+

−= −

εε

εεϕ

111 (5)

Bond holdings can be calculated from budget constraint.

( )( ) ⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

+⎥⎦

⎤⎢⎣

⎡+

−−−= − fQ

rwPwfNB

DiDeii

εε

εεϕ

111 (6)

Here in our setting, the derived price piD consists of three parts: marginal cost wD/ϕi, markup ε/(ε−1) and an additional part 1+r. Compared to the price derived in previous literature (marginal cost times markup), here 1+r as a reflection of financial cost of raising capital enters the price. As r>0 (meaning the positive premium of external finance), the price is higher than the one under standard markup pricing rule without resource constraints. We can understand this in two ways: if the firm does not have enough fund for production, it issues bond with a cost of 1+r; on the other hand, even if the firm has abundant fund, 1+r is still its outside option, or opportunity cost of producing. Nevertheless, if all the firms have unlimited fund, in our setting, bond return rate will be driven to 0 due to unlimited demand of bond purchasing. In this case, the price is the same as the traditional one. All in all, the higher price charged in this model is due to limited internal fund, and hence the positive external finance premium. Proposition 1: (pricing with limited internal fund) Both financial cost (bond rate r) and real cost (wage rate wD and firm-specific productivity ϕi,,) compose product price. Other things equal, the higher r, higher wD or lower ϕi, the higher price, lower output, lower labor demand and less bond finance. More initial internal fund the firm has, production keeps unaffected at its optimal level while bond issuing decreases (or bond holding increases). Firm i’s allocation of its own internal fund (after pays the entry cost for productivity draw) between production and bond purchasing depends on the relative profit of the two investment options. Higher wage or bond rate or lower productivity pushes up unit cost of a variety and erodes profit from production, therefore the firm allocates more fund towards bonds. As for the effect of internal fund Ni on output, it only works through aggregation. Since market capacity is fixed, when firm i achieves its optimal supply, with the increase of internal fund, the firm has no incentive to change its supply, so long as the bond return rate does not change. However, if “a lot of” firms have more internal funds at hand (firms of measure larger than 0), as they spend the extra money on bond holding, the bond return rate will decline (the outcome in general equilibrium). Other things equal, the supply of each variety will increase. 2.1.5 CUTOFF PRODUCTIVITY FOR DOMESTIC PRODUCTION For the existence of bond market, firms could always get safe return from bond holding, while the profit from domestic production depends on firm’s productivity. The less productive the firm is, the less profit it gets from production, then the less incentive for it to produce. In other words, productivity acts as a real factor which characterizes firm’s ability to enter product market. Only those firms whose productivities are above a certain cutoff level will produce. To solve this cutoff productivity for production, we need to compare the profit in section 2.1.4, which is made under the assumption that the firm does produce for domestic market, with the profit when the firm does not produce but invest all its internal fund in bond market. The firm will produce if and only if the former is greater than the latter, therefore the cutoff productivity for domestic production ϕ*iD is

- 7 -

determined by equation (7) below:

( )eiiiDDiDiD fNrrBlwqp −=+− (7)

Using (3), (4), (5) and binding budget constraint, we have

( ) ( )( )

11

*

111 −

⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

⎥⎦

⎤⎢⎣

⎡−+−

=εε

εεεϕ

Prw

Qf D

iD (8)

Proposition 2: (productivity cutoff for domestic production) Under financial constraint, the productivity cutoff for domestic production ϕ*iD.is lower in a country with lower fixed production cost f, lower labor wage wD or lower bond financing cost r. f and wD measure the real cost and r measures the financial cost of production. Intuitively, the above increasing relationship means higher cost (either real or financial cost) requires higher productivity for firms to engage in production. The shape of the increasing relationship depends on ε. For example, when ε is less than 2, the cutoff productivity is convex in f while when ε is lager than 2, it is concave in f. As for the impact of firm’s internal fund, it only works through bond market in aggregation. From proposition 1, firms’ bond holding is increasing with internal fund. More aggregate internal fund could pull down the bond rate and result in a lower cutoff productivity. However, in partial equilibrium, bond rate is exogenous for single firm. Therefore, internal fund is not directly related to firm‐level cutoff productivity. 2.2 OPEN ECONOMY In this subsection, we consider the case of open economy in the sense that firms are interested in producing domestically as well as expanding to foreign country by the means of FDI. We introduce going‐abroad‐ oriented bank credit and reconsider above firm’s investment portfolio decision. The cutoff productivity for a firm to become a multinational is also derived. Moreover, the question that how firms choose different financing when going abroad is discussed. 2.2.1 DEMAND For simplicity and without loss of generality, we assume the aggregate price index and aggregate goods index at the host country are the same as those at home country, and are denoted again as P and Q respectively. We impose further the assumption that when the economy shifts from autarky to openness, P and Q will not change. In other words, the new variety coming in as the result of openness will not affect the aggregate indices. The demand function for each variety in host country is given by:

QpPqiF

iF

ε

⎟⎟⎠

⎞⎜⎜⎝

⎛= (9)

2.2.2 PRODUCTION Assume firm i ‘s productivity spills over to foreign affiliate and it produces in foreign country with the same marginal cost as in home country while it has to shoulder an extra fixed cost CF to do FDI. This foreign expansion induced fixed cost includes the expenses for building up foreign affiliates and distribution channels, collecting information about foreign market and foreign regulations etc. Regardless of the form of such a cost, it is independent of firm’s output and must be paid before the

- 8 -

firm’s revenue in foreign market is fulfilled. As mentioned in section 1, CF is assumed to be uncertain for the firm at the moment when a firm arranges its investment portfolio. The distribution of CF is common knowledge and FDI decision is made based on firm’s expectation for CF. CF is revealed when the firm sets foot on the foreign land. FDI is successful (hence FDI profit received) only if CF is fully covered. In open economy, the domestic production function is still given by (2), while production function for FDI is given as:

Fi

iFiF Cf

ql ++=

ϕ (10)

where qiF, liF are respectively output and labor input in foreign country. Here assume the extra fixed cost CF follows a concave distribution f(CF) with support [0, ∞]. The f(CF) has the cumulative distribution F(CF). 2.2.3 GOING‐ABROAD ORIENTED LOAN AND PROBABILITY OF FDI’S SUCCESS To cover CF, the firm can get finance from banks. Assume that a going‐abroad oriented bank loan is available for all FDI firms. Such loan is aiming to release firms financial constraint due to the substantial upfront costs of FDI and therefore assumed to be used only to shoulder CF 5 Collateral is required to obtain the bank loan in a way that firm i pledges a fraction τ,τ ∈(0,1], of the overhead fixed cost f as collateral to obtain external finance. τ is an industry‐specific parameter. The firm can borrow μτf, where μ is the multiplier over the collateral. Here we use μ to measure the availability of external credit. For simplicity, we assume μ is country‐specific and reflects the financial development of a country. The higher μ, the better access to external credit and the better financial development at country level. We assume further there is no cost of borrowing as bankers are competitive and have no access to the bond market. Moreover, the firm may feel that the borrowing is “not enough” to cover CF, therefore it might have incentive to keep some other fund, together with the borrowing, to pay the extra fixed cost. Here in our model, the firms are allowed to endogenously determine how much fund, both external fund and internal fund, to be prepared. Besides the borrowing μτf, a firm may want to keep an additional fund A, either from bond market issued or from internal fund, to cover CF. Therefore, before CF is revealed, the firm has A+μτf prepared. Hence, the probability of FDI’s success is Prob(CF ≤ A+μτf), which is F(A+μτf) and it is endogenized. As we shall see, for FDI firms, the more productive the firm is, the larger A is kept, the more likely that FDI is successful. 2.2.4 FIRMS’ OPTIMAL DECISION Firm i maximizes the expected total profit from bond holding, domestic production and FDI.

( ) ( ){ }iiiFFiFiFiDDiDiDi rBfAFlwqplwqpEE ++−+−= μτπ ][iiiFiD BApp ,,,

max

( ) eiiiFiFFiDD fNBAClwlw −≤++−+s.t. ; (1); (2); (9); (10);

Note that the profit from FDI is multiplied by the probability of its success. Also note that in the budget constraint, CF is covered by A and μτf. Denote the expected value of CF as C, we have:

5 By this assumption, we make the results of open economy case comparable to closed economy and we could focus on the effect of bank loan on firms’ financing strategy and FDI decisions,.

- 9 -

( rw

pi

DiD +

−= 1

1 ϕεε ) (11)

( )⎟⎟⎠

⎞⎜⎜⎝

⎛+

+−

=fAF

rwpii

FiF μτϕε

ε 11

(12)

( ) iiFFiDDeii AClwlwfNB −−−−−= (13)

and Ai is determined by:

( ) ( ) rfAflwqp iiFFiFiF =+− μτ (14)

Since we have assumed the concavity of F(CF), equation (11)‐(14) characterizes the optimal choice of an FDI firm. We can compare the prices at home country and host country by comparing (11) and (12), noticing that F(A+μτf)≤1. The price for domestic market has the same expression as that in closed economy benchmark (see section 2.1.4). This means firms do not change their pricing strategy for home market when they start FDI business. Nevertheless, the actual value of the domestic price may be different. When the economy shifts from autarky to openness, firms of high productivity adjust investment portfolios: purchase less bond (or issue more bond) and start FDI. The adjustment, as will be discussed more in aggregation in section 3, induces a tougher competition in bond market and drives the bond return rate up. Hence, the actual price in home market under open economy setting will be higher than in closed economy though they share the same mathematical expression. Meanwhile, proposition 2 tells that the cutoff productivity for domestic producing is increasing in r. As a result of increased bond return rate (higher financial cost for producing firms), therefore, a Melitz‐type selection effect will take place through bond market. Least productive firms (those whose productivities are lower than the increased domestic producing cutoff) are crowed out of production and become purely bond holders. Firm i’ choice of A is given by (14). It is an implicit solution. The simulation results are provided in Appendix B (where proposition 3 to 6 are simulated). We have the following proposition: Proposition 3: (reserve fund for FDI) When a firm faces financial constraint, the more productive the firm is (higher ϕi), the more fund Ai it keeps to guarantee the likelihood of success of FDI project. The reserve fund for FDI Ai is higher in a country with less credit access (lower μ), lower production fixed cost f or lower bond financing cost r. Proposition 3 says that if a firm can maintain FDI, its reserve for extra fixed cost CF depends on many parameters: if credit multiplier μ is lower, meaning the firm can borrow less or it is more credit constrained, it will increase Ai as the alternative source to cover CF. Actually, for those productive firms, it is optimal to hold Prob(CF ≤ A+μτf) when bank credit is tight. This finding supplements Manova and many of her followers’ argument that when bank credit is tight, firms are left helpless but reduce the outward investment. In our model, however, firms can resort to alternative finance.

- 10 -

Note that borrowing from bank has no cost but Ai has cost of (1+r), because Ai is raised either from internal fund or from bond market. If bond return rate is higher, it is more attractive to buy bond rather than producing, hence the firm will cut Ai. As for the role of fixed cost f, it works in two ways. On one hand, f is a real cost of FDI. The higher the cost is, the less incentive for firms to do FDI, and hence less reserve fund firms keep for FDI project. On the other hand, f could be used as collateral: firms can get more bank loans against a larger f, so they could reduce the amount of reserve fund. An important finding is that if the firm is more productive, it will increase Ai, because producing is more profitable with higher productivity. Therefore, the firm has incentive to increase the probability of FDI’s success. We have the corollary that more productive firm has higher probability of success abroad. The probability is chosen by the firm itself. This result differs from the existing literature where probability of success is assumed to be exogenous (e.g. Buch et. al, 2009), or the probability of firms’ default on financial contract is exogenous (e.g. Manova, 2007). Some paper does assume that more productive firms have higher probability of success (Li and Yu, 2009), but such relationship is ex ante given without micro foundation. In our model, however, firms choose how much to “invest” to increase the probability of success. Proposition 4: (intensive margin of FDI) The more productive a firm is (higher ϕi), the larger is its affiliate sale. The sale is also larger if the wage cost wF is lower or the bond financing cost r is lower. If a firm can maintain FDI after credit crunch6 (decrease in credit multiplier μ.),it raises working capital from issuing bond and keeps its affiliate sale unaffected. The first three arguments are easy to be verified through (12). The last argument about the credit multiplier μ, needs some intuition. In partial equilibrium environment, when bank credit suddenly becomes tight, like the time when the financial crisis started, we do observe that many multinational firms fail to continue their business abroad and they have to go back. However, we also observe that some multinational firms who successfully stay abroad does not significantly cut their sales; instead, they raise more capital from bond market to substitute bank credit in order to keep their working capital. In our model, when μ decreases such that the firm can borrow less, if it can maintain FDI, it will increase A (proposition 3) to keep the probability of FDI’s success. Therefore, as the bond return rate will not be affected in partial equilibrium, the affiliate sale qiF will not be affected as well. In general equilibrium environment, nevertheless, the increase of A (transfer money from bond market to A) bids up the bond return rate, and the firm will increase the price of the affiliate sale, leading to lower supply. 2.2.5 CUTOFF PRODUCTIVITY FOR FDI Following the argument in section 2.1.5, the cutoff productivity for FDI is derived by equalizing the profit calculated in section 2.2.4 and the profit in section 2.1.4, i.e., the firm will do FDI if and only if its profit is higher than that if the firm only serves the domestic market. Equation (15) represents this:

( ) ( ) iDiDDiDiDiFiFFiFiFiDDiDiD rBlwqprBfAFlwqplwqp +−=++−+− μτ (15)

6 We will discuss the condition for firms to maintain FDI in section 2.2.5.

- 11 -

where BiF comes from (13) and BiD comes from (6). The LHS of (15) is the profit when the firm does FDI while the RHS is the profit when the firm only produces for domestic market (as well as holding bond). We have the expression of the cutoff productivity for FDI (F denotes F(A+μτf)):

( ) ( )( ) ( )

11

* /11

/11 −

⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

⎟⎟⎠

⎞⎜⎜⎝

⎛++

+⎥⎦

⎤⎢⎣

⎡−+−

=εε

εεεϕ

frFwrAFC

PFrw

Qf FF

iF (16)

Comparing (16) to (8), and knowing that F(A+μτf)≤1, we immediately conclude that ϕ*iF>ϕ*iD. The two cutoffs equal if and only if C=0. When C =0, the firm will not keep any A because it is not necessary and A is costly. In this case, meanwhile, the probability of a successful FDI is 1. In proposition 5, we examine the determinants on both cutoff productivity ϕ*iF and expected profit of FDI. Lower cutoff means more firms are able to do FDI whereas higher expected profit means firms are more willing to do FDI. Both ability and willingness contribute to the extensive margin of FDI. Proposition 5: (extensive margin of FDI) productivity cutoff for FDI ϕ*iF is lower when firms face better access to credit (higher credit multiplier μ), lower bond financing cost r, lower production fixed cost (either fixed cost f or expected extra fixed cost C) and lower labor wage wF. The expected profit of doing FDI is larger under higher μ.. When μ is higher, the cutoff productivity for FDI is lower, meaning it is more possible to go abroad (note that all firms draw their productivities ex ante, a lower cutoff productivity means more likely to be a multinational). At the same time, the expected profit is higher, meaning firms are more willing to become multinationals if they can be. Therefore, firms are more likely to do FDI in a country with better credit condition. The real factors cost, such as labor wage and fixed cost, impede firms going out. Proposition 6: (cutoff gap)The gap between productivity cutoff for FDI and cutoff for domestic production (ϕ*

iF

−ϕ*iD) is lower facing lower bond rate r, larger credit multiplier μ, and lower expected fixed cost C.

Proposition 2 and 5 tell that when external finance is cheaper, i.e., if firms can issue bond with lower return rate committed, both cutoff productivities for FDI and domestic production will decrease. Proposition 6 further shows that FDI cutoff decreases faster such that difference between the two cutoffs is smaller. Actually, if r=0, firms can raise as much capital as possible without incurring any cost. In this case,

( ) 11

** /1/ −+= εϕϕ fCiDiF (17)

On the other hand, when the firms can get more borrowing, i.e., μ is higher, domestic cutoff does not change while FDI cutoff decreases. Intuitively, in reality, firms engaging in foreign expansion are more likely to incur financial stress for the existence of extra fixed cost. That is why FDI requires a higher productivity (ϕ*iF > ϕ*iD). Proposition 6 says that better credit condition (higher μ) or less bond financing cost (lower r) can reduce such a requirement for productivity. Financial factors, besides the real factors, do have impact on firms’ going abroad ability. This proposition can explain the evidence that the average productivity of German FDI firms is not significantly higher than non‐FDI firms (see Buch et al 2009).

- 12 -

2.2.6 COMPLEMENTARY EFFECT AND SUBSTITUTION EFFECT Now we are ready to propose our explanation of the observations in the introduction of the paper. When bank credit suddenly becomes tight, i.e., μ suddenly decreases, we know from proposition 5 that ϕ*iF will be higher, this means some firms (the relatively less productive FDI firms whose productivities are between the “old” and “new” ϕ*iF) will be forced to exit from FDI. These firms transfer their money back home and buy more bond7 (or equivalently issue less bond). We find that in this case less bank credit induces less bond issuing, which we call the complementary effect of bond issuing and bank credit. In contrast, however, although ϕ*iF is higher, there are firms who are productive enough to remain doing FDI. From proposition 3 we know that these firms will increase A to secure the probability of success. Because of the shrink of available credit and limited internal fund, they issue more bond as substitution for reduced bank credit and keep the working capital for foreign production unchanged. For the existence of bond financing, the firms do not necessarily experience production contraction facing credit tightness. This phenomenon exists in the data, and we call it the substitution effect of bond issuing and bank credit. Figure 3 gives an intuitive explanation of the complementary effect and substitution effect. We know that only those firms whose productivities are higher than the cutoff productivity for FDI will reserve fund A (the start value of A is 0). The more productive the firm is, the more it reserves. When μ decreases to μ’, the cutoff increases from ϕ*iF (μ) to ϕ*iF (μ’). The firms with productivities in between exit from FDI and hence do not reserve A any more. While those firms with productivity higher than ϕ*iF (μ’) will maintain in FDI and raise more A from issued bond.

ϕ

A

ϕ*iF (μ) ϕ*iF (μ’)

μ’<μ

Complementary Substitution

0

Figure 3: complementary effect and substitution effect

3. AGGREGATION

To complete the model, we derive the general equilibrium results, with which we give more insights into adjustment in bond market and its impact on aggregate industry productivity. In the present model, since bond market is assumed perfect and competitive, any single firm is a price taker with the bond return rate. The rate is determined by equalizing aggregate supply and demand of bond. As we discussed above, facing a credit supply shock, firms will adjust bond supply or demand and firms with

7 In the present model, firms’ market power is constant. These firms will not expand their domestic production when they withdraw capital from FDI but only invest in bond market.

- 13 -

different productivities behave differently, In this part, we further examine what the overall result is in bond market and to which direction the bond rate will go. Firms compete in both labor market and bond market in our setting. Selection effect exists in both markets, which will bring aggregate industry productivity change 3.1 DEFINITION OF GENERAL EQUILIBRIUM In an open economy, a stationary general equilibrium is defined as: (1) a mass of M firms produce for domestic markets. A mass of MF firms do FDI. Total measure of prospective firms is normalized to 1, and MF ⊆ M, 1−M firms only holds bond; (2) there is an aggregate cutoff productivity for domestic production which is determined by “zero cutoff profit” condition and “free entry” condition; (3) there is an aggregate cutoff productivity for FDI which is determined by comparing total profit of whether to do FDI or not; (4) product market clears such that the consumers’ demand is met by firms’ supply; (5) labor market clears to determine the wage (we assume the inelastic supply of labor); (6) bond market clears in a sense that no aggregate net demand of bond, where bond rate r is determined; Following the argument in Melitz (2003), prospective firms of measure 1 are waiting to enter our model. To enter, they have to pay fe from their initial internal fund to draw their own productivities from a common distribution g(ϕ). g(ϕ) is Pareto distribution with CDF G(ϕ) (following Helpman et al., 2004). Firms with high productivity produce (and choose whether FDI or not) whereas those with low productivity hold bonds only. All firms face a constant probability δ (among all productivities and all times) of forced exit. The forced exit firms can pay fe to draw new productivity again. As for the industry equilibrium considered in our model, it is the steady state equilibrium in a sense that the forced exit (producing) firms are as many as new entrants (for producing) each period. The derivation of the general equilibrium is given in Appendix C. Under the heterogeneous firms setup, to show aggregate results conveniently, we need a “representative” firm. The “representative” firm’s productivity is the weighted average productivity of all the firms, where the weight is the market share. In open economy, we also find a “representative” FDI firms. All aggregators such as aggregate price index, aggregate goods etc. can be expressed as functions of this representative firm’s productivity. The aggregate cutoff productivity for domestic production is calculated by “Zero Cutoff Profit (ZCP)” condition and Free Entry (FE) condition. ZCP condition means the representative firm is indifferent in producing or not. Note that, for the existence of bond market, FE condition in our model means the firm’s net present value (NPV) if entering product market is the same as the NPV if investing all its internal funds in bonds after it pays fe to draw productivity. The bond return rate and labor wage are determined by bond market clearing condition and labor market clearing condition respectively. 3.2 AGGREGATE OUTCOME OF COMPLEMENTARY EFFECT AND SUBSTITUTION EFFECT From the discussion above, we know that facing tighter credit condition, complementary effect means firms withdraw money from FDI and purchase more bonds whereas substitution effect means firms issue more bonds to finance FDI. In general equilibrium, the complementary effect and substitution effect influence the bond rate in two opposite directions. The overall outcome depends on which effect dominates. The evidence that spreads in corporate bonds soared dramatically during the current crisis (World Investment Report 2009) implies far more firms belong to the substitution effect type.

- 14 -

3.3 SELECTION EFFECT IN BOND MARKET AND AGGREGATE INDUSTY PRODUCTIVITY In aggregation, adjustments of bond return rate and labor wage have impact on all producing firms, either FDI or non‐FDI firms. If the bond return rate is bid up, the cutoff productivity for domestic producing ϕ*

iD will also increase and some less productive firms will be forced to exit the product market, which brings aggregate industry productivity gains. Section 3.2 argues that a credit supply shock can influence the bond return rate, hence further the aggregate productivity gains. But whether change of credit conditions will intensity or weaken such gains also relies on the relative importance of the above complementary effect and substitution effect. There are two implications from this analysis. First, policy aiming at influencing international activities could also have effect on domestic firms. Remember that even if μ is designed for going‐abroad oriented loan, a shock on μ will be conducted to non‐FDI firms through competition in bond market. Second, tighter credit condition is not always bad. Every story has two sides. Looser credit condition is sunshine for all kinds of firms. Financial stress, on the other hand, shuffles the deck and washes out less productive firms. The survivals are more productive ones.

4. CONCLUSION

A growing literature emphasizes the link between financial constraint and firms’ internationalization. This paper identifies the impact of financial constraint on firms’ FDI decision based on a model which introduce bond issuing as another external financing source besides bank credit into Melitz (2003) framework and discuss the allocation of limited available funds, both internal and external funds, among domestic production, FDI and bonds. We find that bank credit and bond issuing interplay and co‐determine firms’ FDI decision. When suffering from credit crunch, FDI firms respond differently. The most productive firms stay in FDI and issue more bonds to compensate the decreased credit (substitution effect: issuing bonds acts as a substitute of bank credit) while the less productive FDI firms drop from FDI and redistribute more funds in domestic activities (complementary effect: less credit hinders firms from doing FDI and therefore firms have less incentive to issue bond). We conclude that for the interaction of bank credit and bond issuing, how financial constraints affect FDI depends on firms’ productivities. We further find that the bond return rate derived in general equilibrium works as a cost and the increase of bond rate induced by FDI could trigger a Melitz‐type selection effect through bond market and bring aggregate productivity gains. The model in this paper starts with a setup of constant elasticity of substitution between varieties. We expect that embedding the insights into endogenous markup setting may explain better why some firms contract whereas others expand production during financial crisis, and bring more fruitful results. Moreover, we assume a perfect bond market in this paper and bonds issued by heterogeneous firms share the same bond return rate. Another interesting direction for further research is to relax the assumption and extend the model into an incomplete bond market. Allowing firms to issue firm‐specific bonds is more realistic and may exert different effect on margins of FDI.

- 15 -

REFERENCES

1. Aghion, P., Angeletos, G.‐M., Banerjee, A. and K. Manova (2005). ʺVolatility and Growth: Credit

Constraints and Productivity‐Enhancing Investmentʺ, Harvard University mimeo.

2. Aitken, B. J. and A. E. Harrison (1999). ʺDo Domestic Firms Benefit from Direct Foreign Investment?

Evidence from Venezuelaʺ, American Economic Review 89(3), pp.605‐618.

3. Antras, P., and E. Helpman (2004). ʺGlobal Sourcingʺ, Journal of Political Economy, 112(3), pp. 552‐580.

4. Arndt, C., C. Buch and A. Mattes (2009). ʺBarriers to Internationalization: Firm‐level Evidence from

Germanyʺ, IAW Discussion Paper 52.

5. Beck, T. (2002). ʺFinancial Development and International Trade. Is There a Link?ʺ Journal of

International Economics 57(1), pp.107‐131.

6. Beck, T. (2003). ʺFinancial Dependence and International Tradeʺ, Review of International Economics 11(2),

pp.296‐316.

7. Beck, T., Demirgüç‐Kunt, A., Laeven L. and R. Levine (2005a). ʺFinance, Firm Size, and Growth.ʺ,

NBER Working Paper 10983.

8. Beck, T., Demirgüç‐Kunt, A. and V. Maksimovic (2005b). ʺFinancial and Legal Constraints to Firm

Growth: Does Size Matter?ʺ, Journal of Finance 60(1), pp.137‐177.

9. Becker, B. and D. Greenberg (2005). ʺFinancial Development and International Tradeʺ, University of

Illinois at Urbana‐Champaign mimeo.

10. Berman, N. and J. Hericourt (2008). ʺFinancial Factors and the Margins of Trade: Evidence from

Cross‐Country Firm‐Level Dataʺ, Universite Paris CES Working Paper.

11.Bitzer, J. and H. Görg(2005). ʺThe Impact of FDI on Industry Performanceʺ, Leverhulme Centre

Research paper 2005/09.

12. Boyreau‐Debray, G. and S.‐J. Wei(2005). ʺPitfalls of a State‐dominated Financial System: The Case of

China ʺ, NBER Working Paper 11214.

13. Buch, C., I. Kesternich, A. Lipponer and M. Schnitzer (2009). ʺFinancial Constraints and the Margins

of FDIʺ, GESY Discussion Paper No.272.

14. Buch, C., I. Kesternich, A. Lipponer and M. Schnitzer (2010). ʺExport versus FDI Revisited: Does

Finance Matter? ʺ, Deutsche Bundesbank Discussion Paper No.03/2010.

15. Chaney, T. (2005). ʺLiquidity Constrained Exportersʺ, University of Chicago mimeo.

16. Swenson, D.(2008).ʺMultinations and the Creation of Chinese Trade Linkagesʺ, Canadian Journal of

Economics 41(2), pp596‐618.

17. Greenaway, D., Guariglia, A. and R. Kneller (2007). ʺFinancial Factors and Exporting Decisionsʺ,

Journal of International Economics 73(2), pp.377‐395.

18. Helpman, E., M.J. Melitz and S.R. Yeaple (2004). ʺExport versus FDI with Heterogeneous Firms ʺ,

American Economic Review 94 (1), pp.300‐316.

19. Helpman, E., M.J. Melitz and Y. Rubinstein (2008). ʺEstimating Trade Flows: Trading Partners and

Trading Volumes ʺ, The Quarterly Journal of Economics 123 (2), pp.441‐487.

20. Hericourt, J. and S. Poncet (2009). ʺFDI and Credit Constraints: Firm‐level Evidence from Chinaʺ,

Economic Systems 33(1), pp. 1‐21.

- 16 -

21. Jarreau, J. and S. Poncet (2010). ʺFinancial Development and the Structure of China’s Tradeʺ, CES

2010 Annual Conference Paper.

22. Javorcik, B. S. (2004) . ʺDoes Foreign Direct Investment Increase the Productivity of Domestic Firms?

In Search of Spillovers through Backward Linkagesʺ, American Economic Review, 94(3), pp 605‐627.

23. Li, J., L.Hou and J. Zhang (2010). ʺCapital Endowment, Credit Constraint and Foreign Direct

Investmentʺ, University of Munich Working Paper.

24. Li, Z. and M. Yu(2009). ʺExports, Productivity, and Credit Constraints: A Firm‐level Empirical

Investigation for Chinaʺ, NBER‐CCER Conference Paper.

25. Manova, K. (2007). ʺCredit Constraints, Heterogeneous Firms, and International Tradeʺ, Standford

University Working Paper.

26. Manova, K.(2008). ʺCredit Constraints, Equity Market Liberalizations, and International Tradeʺ,

Journal of International Economics 76(1), pp.33‐47.

27. Melitz, M. (2003). ʺThe Impact of Trade on Intra‐industry Reallocations and Aggregate Industry

Productivityʺ, Econometrica 71(6), pp. 1695‐1725.

28. Muuls, M. (2008). ʺExporters and Credit Constraints: A Firm‐level Approachʺ, National Bank of

Belgium Working Paper No.139.

29. Olley, S. and A. Pakes (1996). ʺThe Dynamics of Productivity in the Telecommunications Equipment

Industryʺ, Econometrica 64(6), pp. 1263‐1297.

30. Poncet, S., W. Steingress and H. Vandenbussche(2009). ʺFinancial Constraints in China: Firm‐level

Evidenceʺ, UCL Discussion Paper 35.

- 17 -

APPENDIX A: DERIVE OF THE PARTIAL EQUILIBRIUM AND FDI’S CUTOFF

We give the open economy case, because the closed economy case is similar and easier. A firm

( ) ( ) rBfAFlwqplwqp FFFFDDDD ++−+− μτBApp FD ,,,

max

( ) QpPq DDε/=s.t. ( ) eFFDD fNBAClwlw −≤++−+ , , , ( ) QpPq FF

ε/=

fql DD += ϕ/ Cfql FF ++= ϕ/,

Note that the distribution F(.) is concave, therefore the first order conditions with respect to pD, pF, A and B of the above problem give the solution (11), (12), (13) and (14). The sales and labor demand can be calculated from the constraints. The cutoff productivity for FDI is determined by the equation:

( ) ( ) iDiDDiDiDiFiFFiFiFiDDiDiD rBlwqprBfAFlwqplwqp +−=++−+− μτ

Substitute BiF and BiD respectively by (13) and (6), we have:

( ) ( ) ( )ClrwrAfAFlwqp FFiFFiFiF −+=+− μτ

Use the expressions of (11), (12) and the corresponding expressions from the constraints, we have:

( ) ( ) rfrwrAFCfFrF +Θ+=

⎭⎬⎫

⎩⎨⎧ +−Θ−Θ

−+ −−− 111 /

1/1 εεε ϕϕϕ

εε

( )( ) Q

FrwP

F

ε

εε

⎟⎟⎠

⎞⎜⎜⎝

⎛+−

=Θ/1

1 ( )fAF μτ+ and denotes F . After derivation we have where

( ) ( )( ) ( )

11

* /11

/11 −

⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

⎟⎟⎠

⎞⎜⎜⎝

⎛++

+⎥⎦

⎤⎢⎣

⎡−+−

=εε

εεεϕ

frFwrAFC

PFrw

Qf FF

iF (A.1)

Note that the expression has a variable A, so it is not the final result. The cutoff productivity is determined by the system of equations of (A.1) and (14). The (A.1) is the result that facilitates our comparison of FDI cutoff productivity and domestic production cutoff productivity.

- 18 -

APPENDIX B: SIMULATIONS OF PROPOSITIONS

Proposition 1 and 2 are straightforward, so we only provide the simulation results for proposition 3, 4, 5 and 6. Distribution of the fixed cost for FDI: as we have assumed a concave distribution of CF, we take the Pareto distribution as our example for simulations. Assume CF follows the distribution of the form:

( ) ( )k

F xbxCxF ⎟⎠⎞

⎜⎝⎛−=≤= 1Pr (B.1)

where b and k are parameters of the distribution and x has the support of [b,∞]. The probability density function of CF is therefore given by

( )k

k

k

xb

xk

xkbxf ⎟

⎠⎞

⎜⎝⎛== +1 (B.2)

And the expectation of CF is E[CF]=kb/(k-1). By equations (9), (10), (12) and (14), we have the following equation to solve Ai:

( )( ) ( )( )r

fAbr

fAbr

fAb

fAkQP

wk

ik

i

k

iii

F =⎟⎟

⎠

⎞

⎜⎜

⎝

⎛

⎟⎟⎠

⎞⎜⎜⎝

⎛

+−+

−−⎟

⎟⎠

⎞⎜⎜⎝

⎛

+−+⎟⎟

⎠

⎞⎜⎜⎝

⎛++−

−1

/1111

/11

1 μτεε

μτμτμτϕεε ε

(B.3) To solve the cutoff productivity for FDI, we have the equation (16). However, the unknown variable A is also in the expression. Moreover, the A of a firm in (16) takes the value at the productivity of the FDI cutoff. Therefore, we have the simultaneous equations:

( ) ( )( ) ( )

11

* /11

/11 −

∗

∗∗∗

⎪⎭

⎪⎬⎫

⎪⎩

⎪⎨⎧

⎟⎟⎠

⎞⎜⎜⎝

⎛+

++⎥

⎦

⎤⎢⎣

⎡−+−

=εε

εεεϕ

frFwrACF

PFrw

Qf FF

iF (B.4)

( )( ) ( )( )r

fAbr

fAbr

fAb

fAkQP

wkk

k

iF

F =⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

⎟⎟⎠

⎞⎜⎜⎝

⎛

+−+

−−⎟

⎟⎠

⎞⎜⎜⎝

⎛

+−+⎟⎟

⎠

⎞⎜⎜⎝

⎛++−

−

∗∗∗∗∗

1

/1111

/11

1 μτεε

μτμτμτϕεε ε

(B.5) where A* is chosen by a firm whose productivity is the cutoff productivity of FDI and F* is the probability of success of the firm. The cutoff productivity is determined by solving (B.4) and (B.5) simultaneously. The parameters for simulation are given as follows (these are the basic setup, for each proposition and static comparative analysis, we vary one of the parameters and keep the rest constant):

10=Q 10=f2=ε , , , , 1== FD ww 05.0=r 10=P , 5.0=iϕ , 4.1=μ , , , 10=ef 500=N ,

. 3== kbProposition 3: we vary μ from 1.2 to 1.7, other parameters unchanged, and get the upper left chart in figure B.1; then we set μ as 1.4 again and vary r from 0.05 to 0.15, ceteris paribus, and get the upper right chart in figure B.1; then reset the parameters back to the basic setup and we vary f from 8 to 13, ceteris paribus, and get the lower left chart in figure B.1; finally we vary the productivity ϕ from 0.3 to 0.8, other things set at the basic, and get the lower right chart in figure B.1. The vertical axes are A in the four

- 19 -

charts.

15.8

16.4

17

17.6

18.2

18.8

1.2 1.3 1.4 1.5 1.6 1.7

12.4

13.7

15

16.3

17.6

A A

11.1μ r

0.05 0.07 0.09 0.11 0.13 0.15

15.3

16.1

16.9

17.7

- 20 -

18.5

19.3

8 9 10 11 12 13

15.6

16.9

18.2

20.8

19.5 A A

14.3

0.3 0.4 0.5 0.6 0.7 0.8f ϕ

Figure B.1 the comparative static relationship between A and respectively μ, r, f and ϕ.

15

Proposition 4: to see how do both real cost and financial cost affect the intensive margin of FDI, we simulate the proposition 4 in figure B.2. The vertical axes of all the charts are qiF.

49

50.9

52.8

54.7

56.6

44.3

55.1

65.9

76.7

87.5

qiF qiF

47.1 33.5 r wF 0.05 0.07 0.09 0.11 0.13 0. 0.8 0.9 1 1.1 1.2 1.3

40

46

52

58

64

70

1.2 1.3 1.4 1.5 1.6 1.7

143.2 qiF qiF

20.7

45.2

69.7

94.2

118.7

0.3 0.4 0.5 0.6 0.7 0.8

ϕ μ

Figure B.2 the comparative static relationship between qiF and respectively r, wF, ϕ and μ.

Proposition 5 tells that how the cutoff productivity for FDI is affected by parameters, which are simulated in figure B.3. The vertical axes are ϕ*iF.

0.06307

0.06319

0.06331

0.06343

0.06355

0.06367

1.2 1.3 1.4 1.5 1.6 1.7

- 21 -

0.063

0.0656

0.0682

0.0708

0.0734

0.076

0

ϕ*iF ϕ*iF

μ r .05 0.07 0.09 0.11 0.13 0.15

0.055

0.0594

0.0638

0.0682

0.0726

0.077

8 9 10 11 12 130.04

0.054

0.068

0.082

0.096

0.11

0.8 0.9 1 1.1 1.2 1.3

ϕ*iF ϕ*iF

f wF

Figure B.3 the comparative static relationship between ϕ*iF and respectively μ, r, f and wF.

Figure B.4 depicts the relationship between the profit and the credit multiplier (the upper left one), and it also depicts the proposition 6. The vertical axis of the upper left one is profit while those of the rest charts are ϕ*iF − ϕ*iD.

235.96

235.995

236.03

236.065

236.1

1.2 1.3 1.4 1.5 1.6 1.7

0.022 π ϕ*iF−ϕ*iD

0.0192

0.0199

0.0206

0.0213

0.05 0.07 0.09 0.11 0.13 0.15

μ r

0.0188

0.0189

0.01905

0.0192

0.01935

0.0195

1.2 1.3 1.4 1.5 1.6 1.7

0.01892 μ E[C]

0.01904

0.01916

0.0194

2 2.2 2.4 2.6 2.8 3

0.01928 ϕ*iF−ϕ*iD ϕ*iF−ϕ*iD

Figure B.4 the comparative static relationship between π and μ, and ϕ*iF−ϕ*iD and respectively r, μ and E[C].

APPENDIX C: SKETCH OF THE GENERAL EQUILIBRIUM

In the open economy, firms’ problem is introduced in section 2.2.4, and equations (11), (12), (13) and (14) give the firms’ strategies. Note that each firm’s strategy can be identified by its own productivity, hence we have the strategy of a firm with productivity ϕ :

( ) ( rw

p DD +

−= 1

1 ϕεεϕ ) (C.1)

( ) ( )( )⎟⎟⎠⎞

⎜⎜⎝

⎛+

+−

=fAF

rwp FF μτϕϕε

εϕ 11

(C.2)

( ) ( ) ( )( ) ( )ϕϕϕϕ AClwlwfNB FFDDe −−−−−= (C.3)

and A is determined by:

( ) ( ) ( )( ) ( )( ) rfAflwqp FFFF =+− μτϕϕϕϕ (C.4)

( ) ( ) ( )ϕϕϕ DDD qpr = ( ) ( ) ( )ϕϕϕ FFF qpr =Denote , , we have the profit of a firm:

( ) ( ) ( ) ( ) ( )[ ] ( ) ( )( ) ( )[ ]ϕϕϕϕϕϕϕϕπ AClwlwfNrFlwrlwr FFDDeFFFDDD −−−−−+−+−= , or

( ) ( ) ( ) ( ) ( )( ) ( ][1 ϕεϕ

εϕ

ϕπ ACfNrCfrFwrFfwrreF

FD

D −+−+++−⋅

++−= )

( )( ) ϕ

ϕϕϕ ~~ =

D

D

pp ( )

( )

ε

ϕϕ

ϕϕ

⎟⎟⎠

⎞⎜⎜⎝

⎛= ~~

D

D

qq ( )

( )

1

~~

−

⎟⎟⎠

⎞⎜⎜⎝

⎛=

ε

ϕϕ

ϕϕ

D

D

rr∗≥∀ Dϕϕϕ ~, ∗≥∀ FF ϕϕϕ ~,, we have , , ; and , Because:

( )( )

( ) ( )( )( ) ( )( )rFF

rFFpp

F

FF

FF

F

++

=ϕϕϕϕϕϕ

ϕϕ

~~~

~( )( )

( ) ( )( )( ) ( )( )

ε

ϕϕϕϕϕϕ

ϕϕ

⎟⎟⎠

⎞⎜⎜⎝

⎛++

=rFF

rFFqq

FF

F

FF

F~~

~~

( )( )

( ) ( )( )( ) ( )( )

1

~~~

~

−

⎟⎟⎠

⎞⎜⎜⎝

⎛++

=ε

ϕϕϕϕϕϕ

ϕϕ

rFFrFF

rr

FF

F

FF

F, , , where

( FF )ϕ~ ( )( )fAF F μτϕ +~ denotes , and are cutoff productivities for domestic production and

FDI, respectively. Define

∗Dϕ

∗Fϕ

( ) 11

0

1~ −∞ − ⎟⎠⎞⎜

⎝⎛= ∫

εε ϕϕϕϕ du ( ) ( )( )∗−

=DG

guϕϕϕ

1( ) 0=ϕu, where if and ∗≥ Dϕϕ

if . Therefore ϕ~∗< Dϕϕ is the weighted average productivity of all producing firms (including FDI

firms). Define ( ) 11

0

1~ −∞ − ⎟⎠⎞⎜

⎝⎛= ∫

εε ϕϕϕϕ duFF ( ) ( )( )∗−

=F

F Ggu

ϕϕϕ

1( ) 0=ϕFu, where if and ∗≥ Fϕϕ if

. Therefore Fϕ~∗< Fϕϕ is the weighted average productivity of all FDI firms.

The expected average profit of a firm before it draws its productivity is given by:

( ) ( )( ) ( )FF

D

FD G

Gϕπ

ϕϕ

ϕππ ~11~

∗

∗

−−

+=

- 22 -

( ) ( ) ( ) ][1~~

eDD

D fNrfwrr−++−=

εϕ

ϕπwhere is the profit from domestic market (product and

bond), ( ) ( ) ( ) ( )( )( ) ( ]~[~ )~~~

FFFFFF

FF ACrCfrFwrFϕϕ

εϕϕ

ϕπ −+++−⋅

= is the profit from FDI,

( )( )∗

∗

−−

D

F

GGϕϕ

11

is the probability of being able to do FDI. Therefore, we have the following two “zero cutoff

profit” conditions:

( ) ][ eDD fNr −=∗ϕπ ZCP 1

( ) 0=∗FF ϕπ ZCP 2

The ZCP 1 says the domestic profit at domestic cutoff productivity is the same as purely holding bond; the ZCP 2 says the FDI profit at the FDI cutoff productivity is 0. Hence we have:

( ) ( ) fwrr DDD εϕ +=∗ 1 ZCP 1’

( ) ( ) ( )( )( ) ( ) ( )][ ∗∗

∗∗

∗ −−++= FF

FFF

FF ACrF

CfrFwF

r ϕϕεϕ

ϕεϕ ZCP 2’

( )( )

( ) ( )( )( ) ( )( )

1

~~~

~

−

⎟⎟⎠

⎞⎜⎜⎝

⎛++

=ε

ϕϕϕϕϕϕ

ϕϕ

rFFrFF

rr

FF

F

FF

F( )( )

1

~~

−

⎟⎟⎠

⎞⎜⎜⎝

⎛=

ε

ϕϕ

ϕϕ

D

D

rr and Use at the respective cutoff productivity level,

we have

( ) ( ) ( )( )

( )( )

( ) ( )( )( ) ( )( ) ×⎟⎟

⎠

⎞⎜⎜⎝

⎛++

−−

+−+⎟⎟

⎠

⎞

⎜⎜

⎝

⎛−⎟⎟

⎠

⎞⎜⎜⎝

⎛+=

−

∗∗

∗

∗∗

∗−

∗

11

~~~~

11

1~

1εε

ϕϕϕϕϕϕ

ϕϕ

ϕϕ

ϕϕπ

rFFrFF

FF

GG

fNrfwrFFF

FFF

F

F

D

Fe

DD

( )( )( )( ) ( )( )( )( )CfrFwrCrCCfrFw FFFF ++−+−++∗ ϕϕ ~ (C.5)

( ) ( )fFF F μτϕ =∗( ) 0=∗FAϕwhere , and

( ) ( ) ( )∗∗∗ = FFFFFF qpr ϕϕϕMoreover, by ZCP 1’ and ZCP 2’, and use the definition that and

( ) ( ) ( )∗∗∗ = DDDDDD qpr ϕϕϕ , we know a relationship between and : ∗Fϕ

∗Dϕ

( )( ) ( )( )( )( ) rCCfrFw

fFwrww

Fr

FF

FD

D

F

FF

D

−+++

=⎟⎟⎠

⎞⎜⎜⎝

⎛⎟⎟⎠

⎞⎜⎜⎝

⎛+ ∗

∗−

∗∗

∗

ϕϕ

ϕϕϕ

ε1

11

(C.6)

ϕ~Fϕ~We now know that is a function of , therefore ∗

Fϕ∗Dϕ and are functions of as well. ∗

Dϕ

Because each firm faces a constant probability δ of forced exit, and the ex ante expected profit if the firm

produce is ( )( )δπϕ ∗− DG1π , therefore the value of the firm is given by: . The firm wants to produce if

and only if the net value of producing is as much as holding bond (outside option). This is defined as the

- 23 -

( )( ) [ ]e

eeD f

fNrfG −

−=−− ∗

δδπϕ1free entry condition: , or:

[ ]( )( )∗−−

=D

e

GfNrϕ

π1

(C.7)

Note that (C.5) and (C.7) intersect only once and determine an equilibrium . ∗Dϕ

To calculate the equilibrium bond return rate and labor wage, we impose another two market clear conditions. Bond market clears means there is no net demand of bond:

( ) ( ) 00

=∫∞

ϕϕϕ dgB (C.8)

( ) efNB −=ϕ ( ) ( )ϕϕ DDe lwfNB −−=where if ; ∗< Dϕϕ if ; and ∗∗ <≤ FD ϕϕϕ

( ) ( ) ( )( ) ( )ϕϕϕϕ AClwlwfNB FFDDe −−−−−= if . ϕϕ ≤∗F

Labor market clears means:

( ) ( ) Ldgl =∫∞

0ϕϕϕ (C.9)

( ) 0=ϕl ( ) ( )ϕϕ Dll = ( ) ( ) ( )ϕϕϕ FD lll +=where if ; ∗< Dϕϕ if ; ∗∗ <≤ FD ϕϕϕ if . ϕϕ ≤∗F

The rest of the equilibrium is to determine the aggregate index, such as P, Q, and the mass of producing firms M. The price index P has its definition:

( ) ( ) ( ) ε

ϕ

ε ϕϕϕ −∞ − ⎟⎠⎞⎜

⎝⎛ += ∫ ∗

11

1 duMMpP TFD

(C.10)

( )∗−= DGM ϕ1 ( )∗−= FF GM ϕ1where is the mass of producing firms and is the mass of FDI firms,

( )ϕTu is the productivity distribution of all the available varieties, because in an open economy, there

are domestic goods as well as foreign goods so that the price index must be consist of domestic firms and foreign firms who come to do FDI at domestic country. The aggregate goods Q is determined by

PLwQ D= (C.11)

We therefore have all the general equilibrium conditions and we have assumed pareto distribution of both productivity and extra fixed cost of doing FDI.

- 24 -