Financial Accounting Standards Board’s (FASB) … · ©2014 CliftonLarsonAllen LLP ©2014...

56

©2014 CliftonLarsonAllen LLP CLAconnect.com Financial Accounting Standards Board’s (FASB) Organization and Purpose April 6, 2016 Presentation for the National Association of Federal Credit Unions

-

Upload

hoangkhuong -

Category

Documents

-

view

219 -

download

2

Transcript of Financial Accounting Standards Board’s (FASB) … · ©2014 CliftonLarsonAllen LLP ©2014...

©20

14 C

lifto

nLar

sonA

llen

LLP

©20

14 C

lifto

nLar

sonA

llen

LLP

CLAconnect.com

Financial Accounting Standards Board’s (FASB) Organization and Purpose

April 6, 2016

Presentation for the National Association of Federal Credit Unions

©20

14 C

lifto

nLar

sonA

llen

LLP

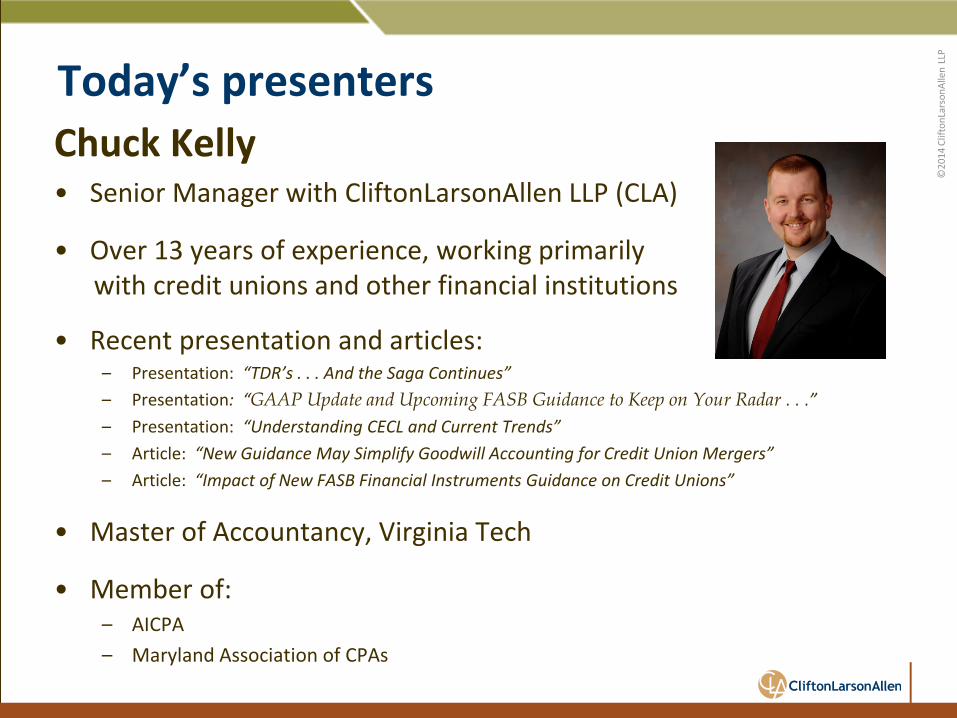

Chuck Kelly • Senior Manager with CliftonLarsonAllen LLP (CLA)

• Over 13 years of experience, working primarily with credit unions and other financial institutions

• Recent presentation and articles: – Presentation: “TDR’s . . . And the Saga Continues” – Presentation: “GAAP Update and Upcoming FASB Guidance to Keep on Your Radar . . .” – Presentation: “Understanding CECL and Current Trends” – Article: “New Guidance May Simplify Goodwill Accounting for Credit Union Mergers” – Article: “Impact of New FASB Financial Instruments Guidance on Credit Unions”

• Master of Accountancy, Virginia Tech

• Member of: – AICPA – Maryland Association of CPAs

Today’s presenters

©20

14 C

lifto

nLar

sonA

llen

LLP

Today’s presenters

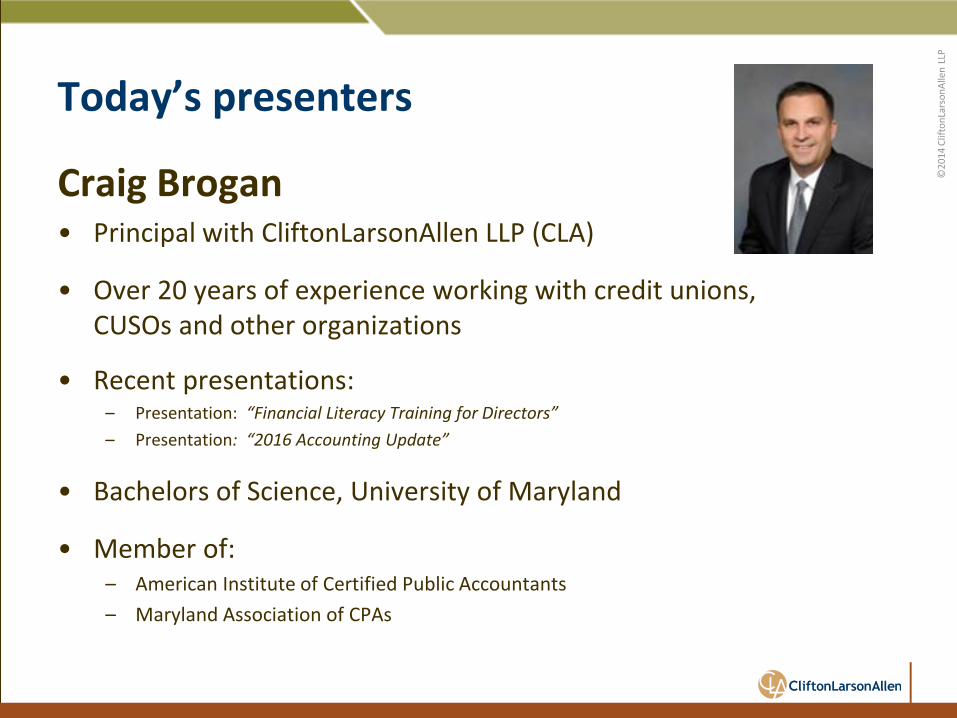

Craig Brogan • Principal with CliftonLarsonAllen LLP (CLA)

• Over 20 years of experience working with credit unions, CUSOs and other organizations

• Recent presentations: – Presentation: “Financial Literacy Training for Directors” – Presentation: “2016 Accounting Update”

• Bachelors of Science, University of Maryland

• Member of: – American Institute of Certified Public Accountants – Maryland Association of CPAs

©20

14 C

lifto

nLar

sonA

llen

LLP

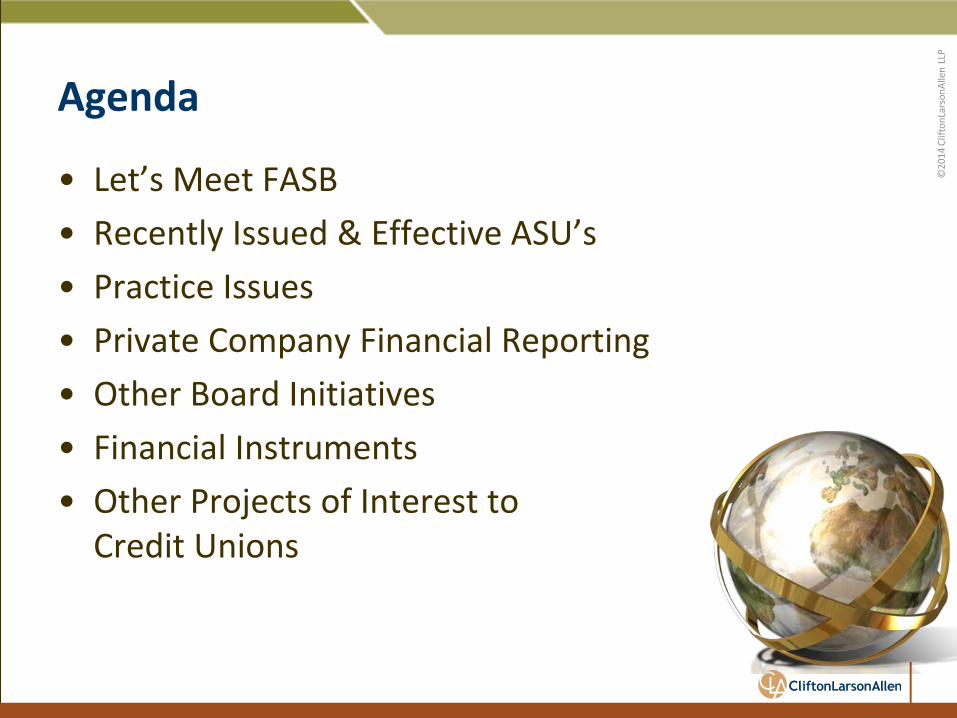

Agenda

• Let’s Meet FASB • Recently Issued & Effective ASU’s • Practice Issues • Private Company Financial Reporting • Other Board Initiatives • Financial Instruments • Other Projects of Interest to

Credit Unions

©20

14 C

lifto

nLar

sonA

llen

LLP

History of FASB

• FASB established in 1973 by the Financial Accounting Foundation (FAF)

• First standard was also issued in 1973 • Designated organization for establishing standards of financial

accounting for nongovernmental entities • Standards are officially recognized by the SEC and AICPA • 1991 - FASB participated in an international conference on

global accounting standards • 2009 – FASB Accounting Standards Codification is created

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

• Financial Accounting Standards Board (FASB) • Seven Member Board • Oversight provided by the Financial Accounting

Foundation (FAF) • Norwalk, CT

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

• Russell G. Golden, Chairman

• From 2008 to September 2010, he was Technical Director of the FASB, overseeing FASB staff work on accounting standards and technical application and implementation activities.

• He also chaired the FASB’s Emerging Issues Task Force (EITF). • He was initially appointed to the FASB in 2010, after serving for six

years on the FASB staff. Mr. Golden’s term as chairman extends to June 30, 2017, when he will be eligible for appointment to an additional term of three years.

• Before joining the FASB staff, Mr. Golden was a partner at Deloitte & Touche LLP in the National Office Accounting Services department.

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

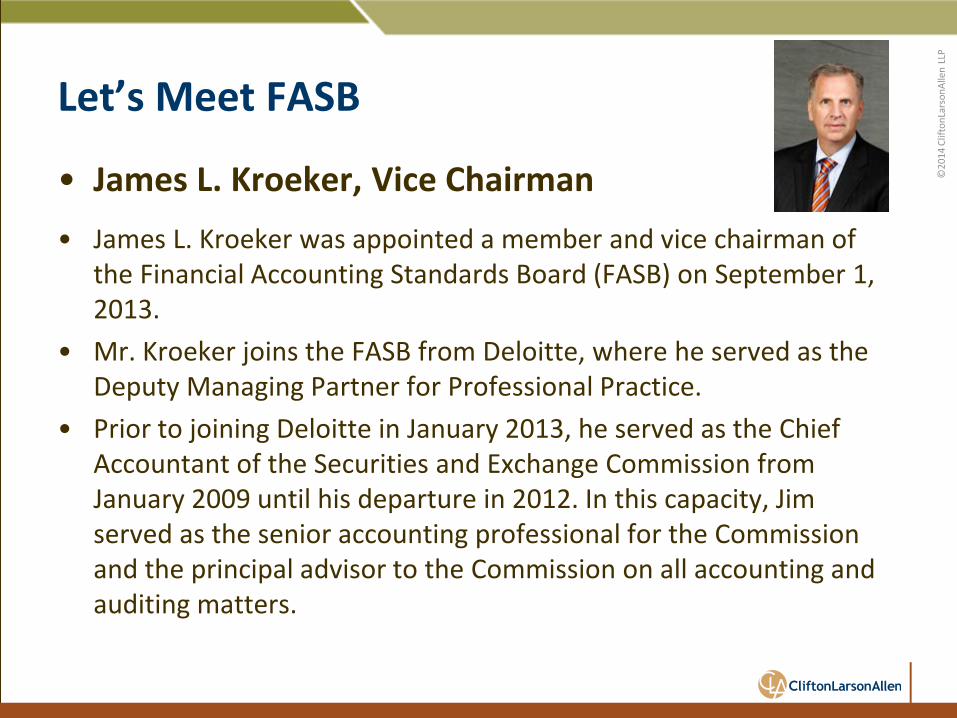

• James L. Kroeker, Vice Chairman

• James L. Kroeker was appointed a member and vice chairman of the Financial Accounting Standards Board (FASB) on September 1, 2013.

• Mr. Kroeker joins the FASB from Deloitte, where he served as the Deputy Managing Partner for Professional Practice.

• Prior to joining Deloitte in January 2013, he served as the Chief Accountant of the Securities and Exchange Commission from January 2009 until his departure in 2012. In this capacity, Jim served as the senior accounting professional for the Commission and the principal advisor to the Commission on all accounting and auditing matters.

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

• Marc A. Siegel, Board Member

• Marc A. Siegel was appointed to the Financial Accounting Standards Board (FASB) in 2008, reappointed to a second five-year term in 2013.

• A recognized expert in forensic accounting, Mr. Siegel has 20 years of experience in diverse and global industries that include technology, media, telecommunications, healthcare, retail, and insurance.

• Prior to his appointment to the FASB, he led the Accounting Research and Analysis team at the RiskMetrics Group in Rockville, Maryland.

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

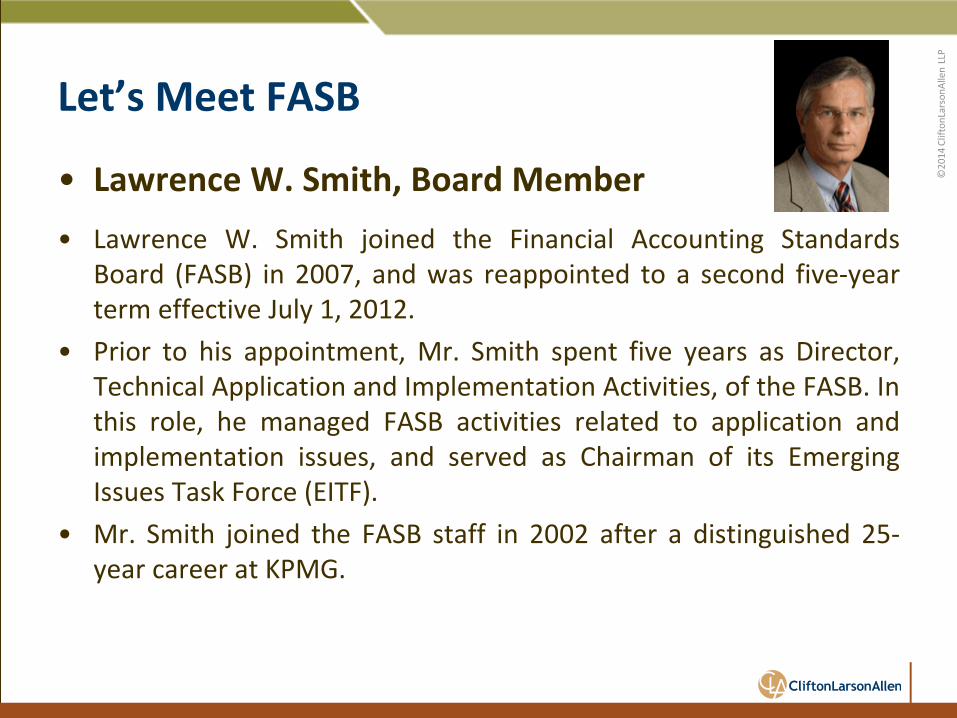

• Lawrence W. Smith, Board Member

• Lawrence W. Smith joined the Financial Accounting Standards Board (FASB) in 2007, and was reappointed to a second five-year term effective July 1, 2012.

• Prior to his appointment, Mr. Smith spent five years as Director, Technical Application and Implementation Activities, of the FASB. In this role, he managed FASB activities related to application and implementation issues, and served as Chairman of its Emerging Issues Task Force (EITF).

• Mr. Smith joined the FASB staff in 2002 after a distinguished 25-year career at KPMG.

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

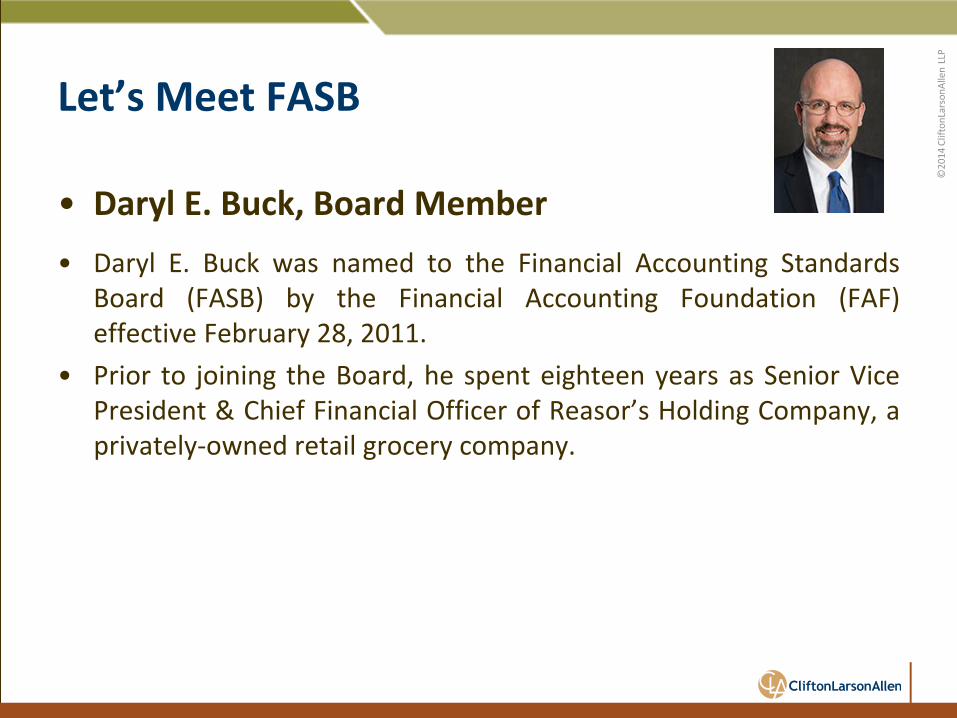

• Daryl E. Buck, Board Member

• Daryl E. Buck was named to the Financial Accounting Standards Board (FASB) by the Financial Accounting Foundation (FAF) effective February 28, 2011.

• Prior to joining the Board, he spent eighteen years as Senior Vice President & Chief Financial Officer of Reasor’s Holding Company, a privately-owned retail grocery company.

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

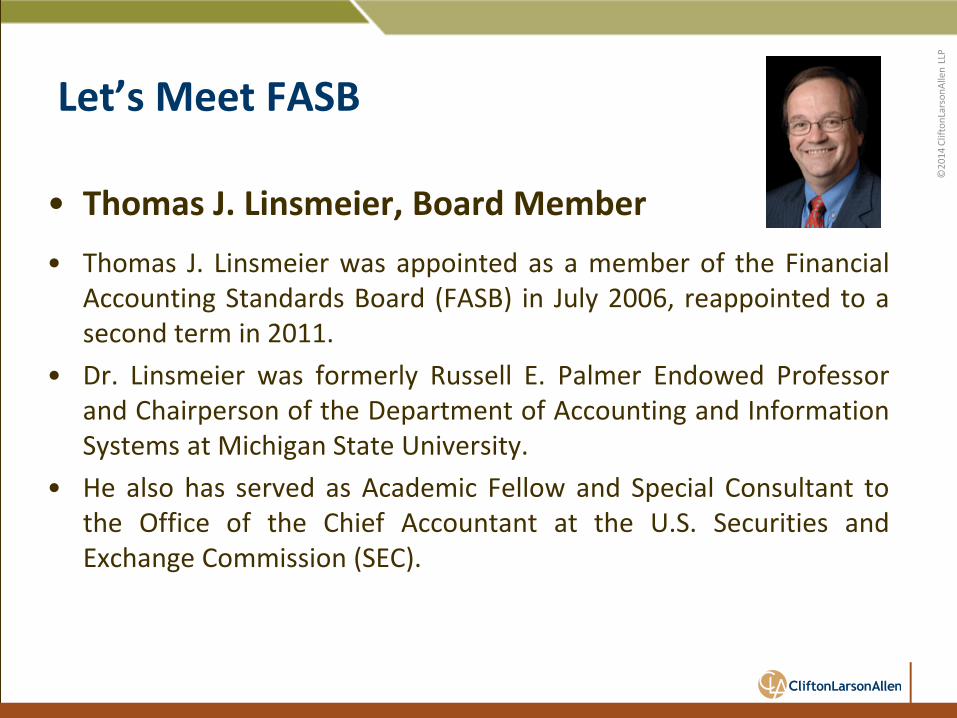

• Thomas J. Linsmeier, Board Member

• Thomas J. Linsmeier was appointed as a member of the Financial Accounting Standards Board (FASB) in July 2006, reappointed to a second term in 2011.

• Dr. Linsmeier was formerly Russell E. Palmer Endowed Professor and Chairperson of the Department of Accounting and Information Systems at Michigan State University.

• He also has served as Academic Fellow and Special Consultant to the Office of the Chief Accountant at the U.S. Securities and Exchange Commission (SEC).

©20

14 C

lifto

nLar

sonA

llen

LLP

Let’s Meet FASB

• R. Harold Schroeder, Board Member

• R. Harold “Hal” Schroeder joined the FASB in February 2011, reappointed to a second term in 2015.

• Mr. Schroeder is a CPA who brings over 30 years of diverse experience in investing and financial reporting to the FASB.

• Most notably, he brings a strong investor perspective to the FASB, with more than 15 years of experience working with all facets of the investment community.

• Prior to joining the Board, Mr. Schroeder was a partner at Carlson Capital, L.P., a Dallas-based money manager with assets under management of over $6 billion.

©20

14 C

lifto

nLar

sonA

llen

LLP

What Does FASB Produce?

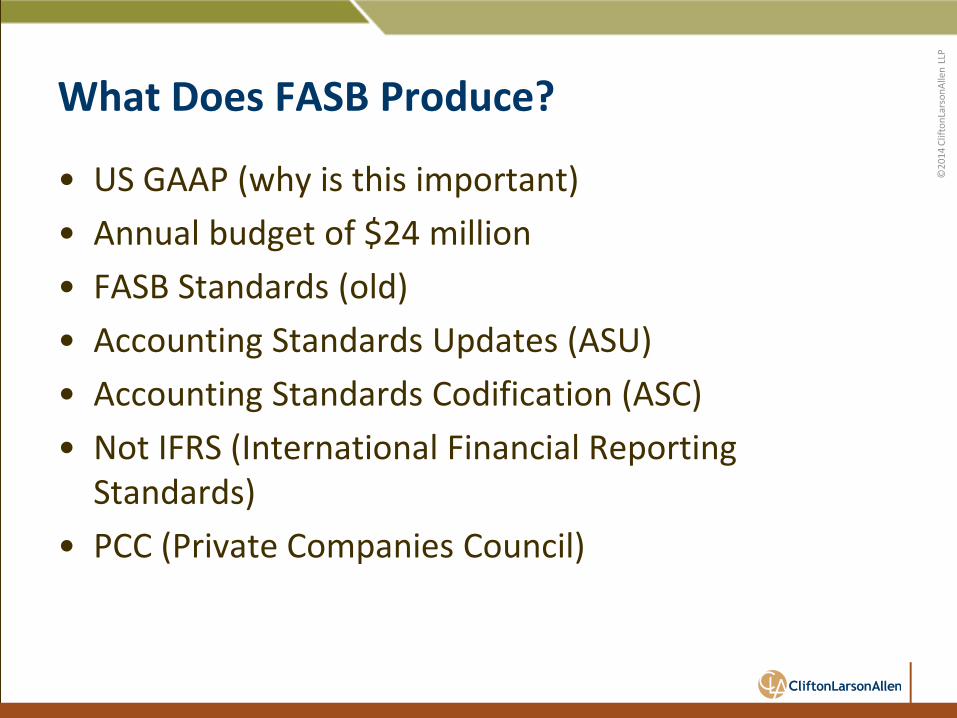

• US GAAP (why is this important) • Annual budget of $24 million • FASB Standards (old) • Accounting Standards Updates (ASU) • Accounting Standards Codification (ASC) • Not IFRS (International Financial Reporting

Standards) • PCC (Private Companies Council)

©20

14 C

lifto

nLar

sonA

llen

LLP

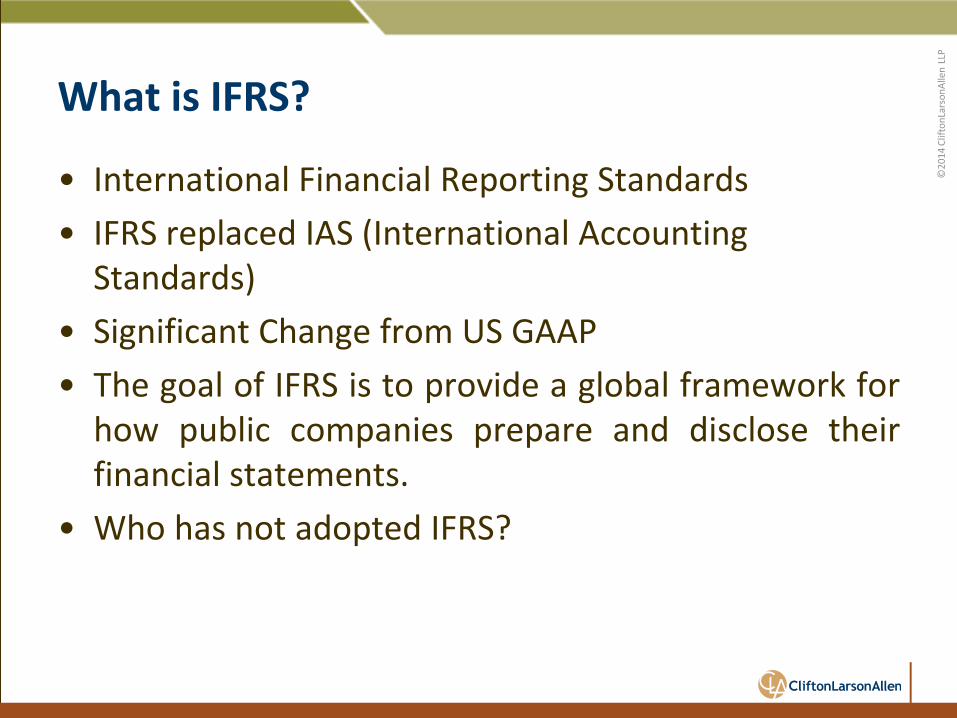

What is IFRS?

• International Financial Reporting Standards • IFRS replaced IAS (International Accounting

Standards) • Significant Change from US GAAP • The goal of IFRS is to provide a global framework for

how public companies prepare and disclose their financial statements.

• Who has not adopted IFRS?

©20

14 C

lifto

nLar

sonA

llen

LLP

Who has not adopted IFRS? • There are only 10 out of 140 jurisdictions that neither permit,

not require IFRS for any domestic publicly accountable entities, including: – United States

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt • Guinea-Bissau

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt • Guinea-Bissau • Macau

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt • Guinea-Bissau • Macau • Vietnam

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt • Guinea-Bissau • Macau • Vietnam • Thailand (in the process of adopting IFRS in full)

©20

14 C

lifto

nLar

sonA

llen

LLP Who Does Not Require or Permit IFRS for

Domestic Public Entities? • United States • Nigeria • Bolivia • China • Egypt • Guinea-Bissau • Macau • Vietnam • Thailand (in the process of adopting IFRS in full) • Indonesia (in the process of convergence)

©20

14 C

lifto

nLar

sonA

llen

LLP

Differences Between GAAP and IFRS

• GAAP is rule-based, whereas IFRS is principle-based • Inventory - LIFO vs FIFO • Intangibles – Future Economic Benefit? • Write downs

Presenter

Presentation Notes

With a principle based framework there is the potential for different interpretations of similar transactions, which could lead to extensive disclosures in the financial statements. Although, the standards setting board in a principle-based system can clarify areas that are unclear. This could lead to fewer exceptions than a rules-based system. By no means an exhaustive list of differences, but: Intangibles�The treatment of acquired intangible assets helps illustrate why IFRS is considered more "principles based." Acquired intangible assets under U.S. GAAP are recognized at fair value, while under IFRS, it is only recognized if the asset will have a future economic benefit and has measured reliability. Intangible assets are things like R&D and advertising costs. Inventory — Under IFRS, LIFO cannot be used, but GAAP, companies have the choice between LIFO and FIFO. Write Downs�Under IFRS, if an asset is written down, the write down can be reversed in future periods if specific criteria are met. Under U.S. GAAP, once an asset has been written down, any reversal is prohibited. �

©20

14 C

lifto

nLar

sonA

llen

LLP

What does FASB issue?

• Pre 2008 – Statements of Financial Reporting Standards (FASB Standards) FAS 91, FAS 115

• Post 2008 – ASU (Accounting Standards Updates)

• Post 2008 – ASC (Accounting Standards Codification)

©20

14 C

lifto

nLar

sonA

llen

LLP Pre 2008 – Statements of Financial

Reporting Standards • Statements of Standards on Financial Reporting • Issued sequentially • Remained stand alone authoritative guidance • Messy – amendments • Two libraries –As originally Issued, As amended,

Current Text

©20

14 C

lifto

nLar

sonA

llen

LLP

Standard Codification 2008

• All FASB standards moved into: Accounting Standards Codification (ASC)

• All new standards issued as Accounting Standards Updates (ASU)

• Accounting Standards Updates will not be amended (rather, changes would be included in future ASU’s)

©20

14 C

lifto

nLar

sonA

llen

LLP

True or False: As of December 31, 2015, U.S. generally accepted accounting

principles merged with international financial reporting standards.

Polling Question

©20

14 C

lifto

nLar

sonA

llen

LLP

FASB Standards 1-168 (old)

• Intro

• Standard of Financial Accounting and Reporting

• Effective date and transition

• Appendix

©20

14 C

lifto

nLar

sonA

llen

LLP

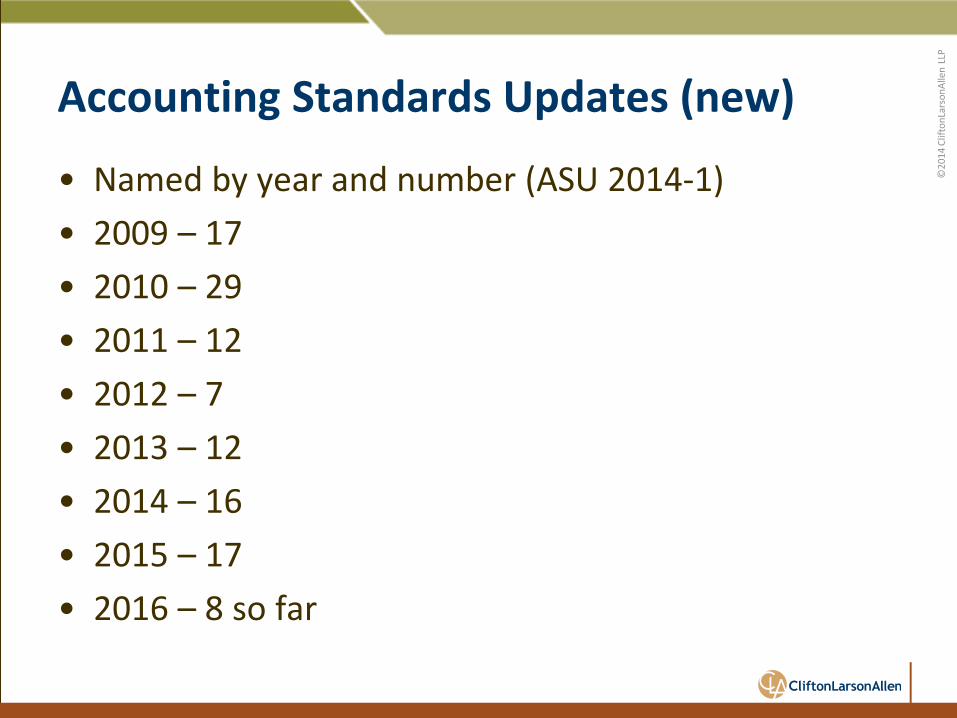

Accounting Standards Updates (new)

• Named by year and number (ASU 2014-1) • 2009 – 17 • 2010 – 29 • 2011 – 12 • 2012 – 7 • 2013 – 12 • 2014 – 16 • 2015 – 17 • 2016 – 8 so far

©20

14 C

lifto

nLar

sonA

llen

LLP

Accounting Standards Update - Format

• Why is the FASB issuing this ASU?

• Who is affected by this ASU?

• What are the main provisions?

• How do the main provisions differ from current GAAP?

• When will it be effective

• How do the provisions compare with IFRS?

©20

14 C

lifto

nLar

sonA

llen

LLP

Evolution of New Accounting Standards Updates

• Key Principle – FASB will only issue standards when the expected

benefits of a change justify the perceived costs of that change.

– For this reason, accounting standard updates are subjected to a Cost-Benefit Analysis.

– So how is this accomplished?

©20

14 C

lifto

nLar

sonA

llen

LLP Evolution of New Accounting Standards Updates

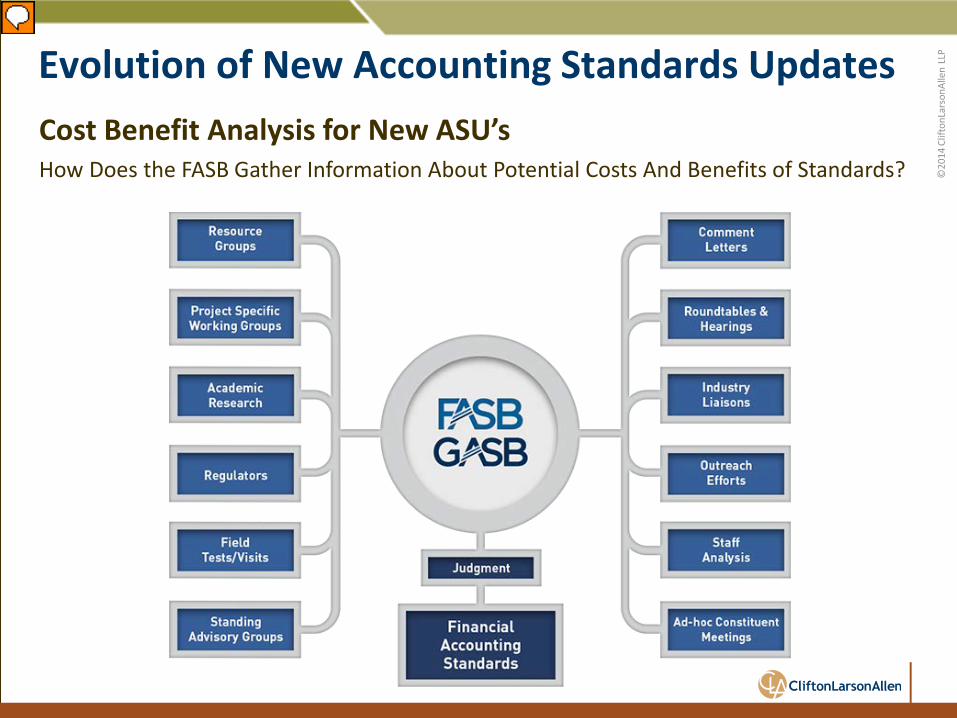

Cost Benefit Analysis for New ASU’s

How Does the FASB Gather Information About Potential Costs And Benefits of Standards?

Presenter

Presentation Notes

An independent standard-setting process is critical to producing high-quality accounting standards, because it relies on the collective judgment of experts, and it is informed by the input of all interested parties through a thorough and deliberative process. The FASB sets accounting standards through processes that are open and allow for extensive input from all stakeholders. These stakeholders represent a broad range of capital market participants, including investors, analysts, donors to nonprofit organizations, financial statement preparers, auditors, academics, and other interested parties.��Throughout the stages of a project, the FASB’s procedures, which are called “due process,” are specifically designed to generate feedback about costs and benefits of a proposed new standard. Stakeholders are asked about the most faithful way to portray a transaction or economic phenomenon, as well as the most cost-effective ways to implement any changes. Before being implemented, every proposal is exposed for public commentary and discussed with numerous informed stakeholders. Technical decisions by the Board are made in public meetings after careful consideration of the input from stakeholders.

©20

14 C

lifto

nLar

sonA

llen

LLP

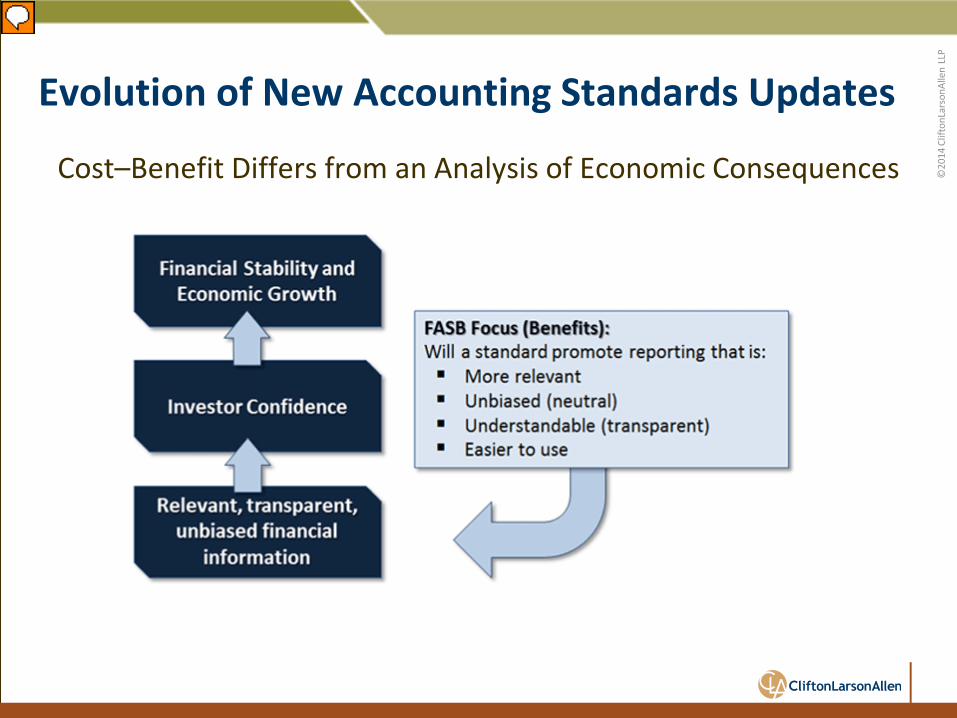

Cost–Benefit Differs from an Analysis of Economic Consequences

Evolution of New Accounting Standards Updates

Presenter

Presentation Notes

The economic consequences of a new financial reporting standard are separate and distinct from an analysis of costs and benefits relating to the adoption of a new standard. The role of financial reporting is not to deter-mine or influence what capital allocation decisions should be made or what actions should be taken by management. Rather, the role of financial reporting is to promote decisions that are well-informed and to provide investors information they need to make those decisions. The FASB’s objective in developing accounting standards is to show a complete and unbiased picture of a company’s financial position and performance. Better information (which could be favorable or unfavorable for a particular organization) is expected to change capital allocation decisions, but the Board does not try to influence the outcome of those decisions.�

©20

14 C

lifto

nLar

sonA

llen

LLP

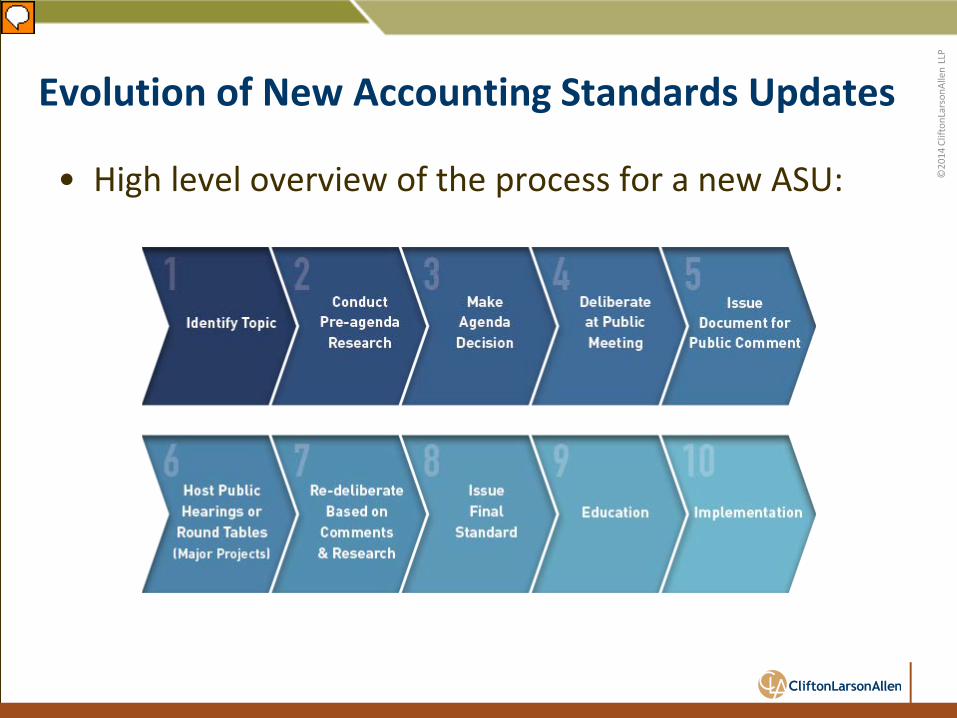

• High level overview of the process for a new ASU:

Evolution of New Accounting Standards Updates

Presenter

Presentation Notes

The Board identifies financial reporting issues based on requests/recommendations from stakeholders or through other means. The FASB decides whether to add a project to the technical agenda based on a staff-prepared analysis of the issues. The Board deliberates at one or more public meetings the various reporting issues identified and analyzed by the staff. The Board issues an Exposure Draft to solicit broad stakeholder input. (In some projects, the Board may issue a Discussion Paper to obtain input in the early stages of a project.) The Board holds a public roundtable meeting on the Exposure Draft, if necessary. The staff analyzes comment letters, public roundtable discussion, and all other information obtained through due process activities. The Board redeliberates the proposed provisions, carefully considering the stakeholder input received, at one or more public meetings. The Board issues an Accounting Standards Update describing amendments to the Accounting Standards Codification.

©20

14 C

lifto

nLar

sonA

llen

LLP

Accounting Standards Codification • General Principals

– 105 Generally Accepted Accounting Principles

• Presentation – 205 Presentation of Financial Statements – 210 Balance Sheet – 215 Statement of Shareholder Equity – 220 Comprehensive Income – 225 Income Statement – 230 Statement of Cash Flows – 235 Notes to Financial Statements – 250 Accounting Changes and Error Corrections – 255 Changing Prices – 260 Earnings Per Share

©20

14 C

lifto

nLar

sonA

llen

LLP

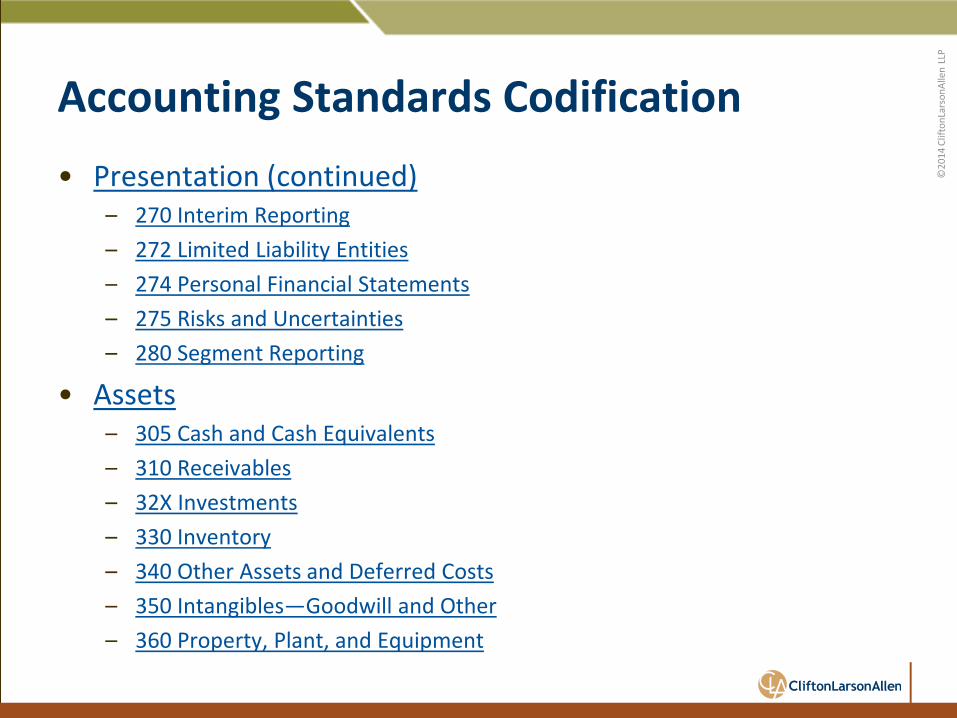

Accounting Standards Codification • Presentation (continued)

– 270 Interim Reporting – 272 Limited Liability Entities – 274 Personal Financial Statements – 275 Risks and Uncertainties – 280 Segment Reporting

• Assets – 305 Cash and Cash Equivalents – 310 Receivables – 32X Investments – 330 Inventory – 340 Other Assets and Deferred Costs – 350 Intangibles—Goodwill and Other – 360 Property, Plant, and Equipment

©20

14 C

lifto

nLar

sonA

llen

LLP

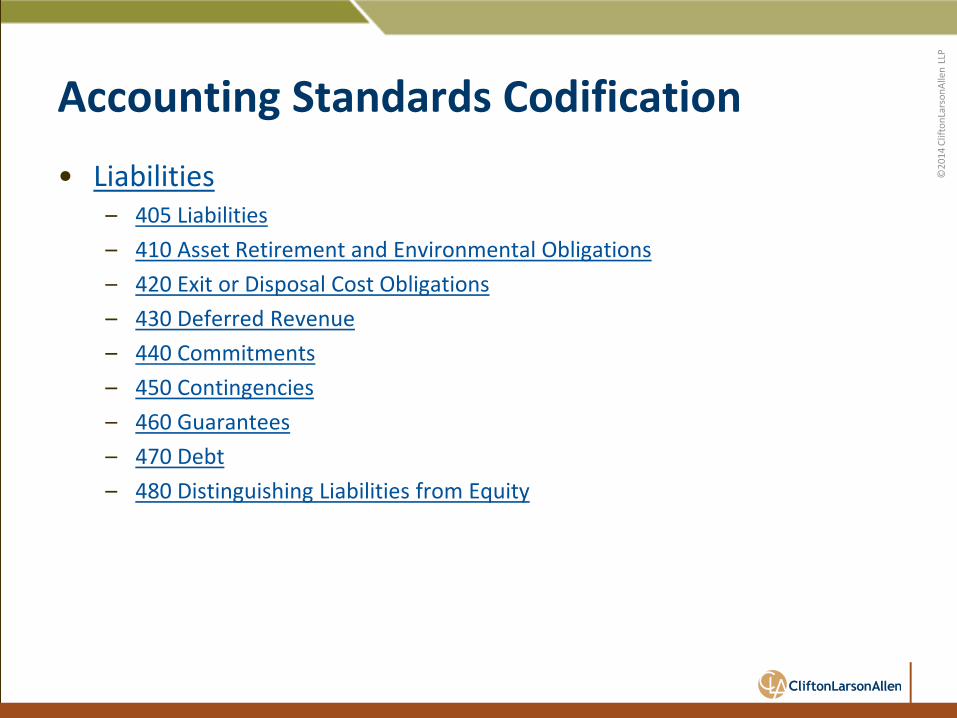

Accounting Standards Codification • Liabilities

– 405 Liabilities – 410 Asset Retirement and Environmental Obligations – 420 Exit or Disposal Cost Obligations – 430 Deferred Revenue – 440 Commitments – 450 Contingencies – 460 Guarantees – 470 Debt – 480 Distinguishing Liabilities from Equity

©20

14 C

lifto

nLar

sonA

llen

LLP

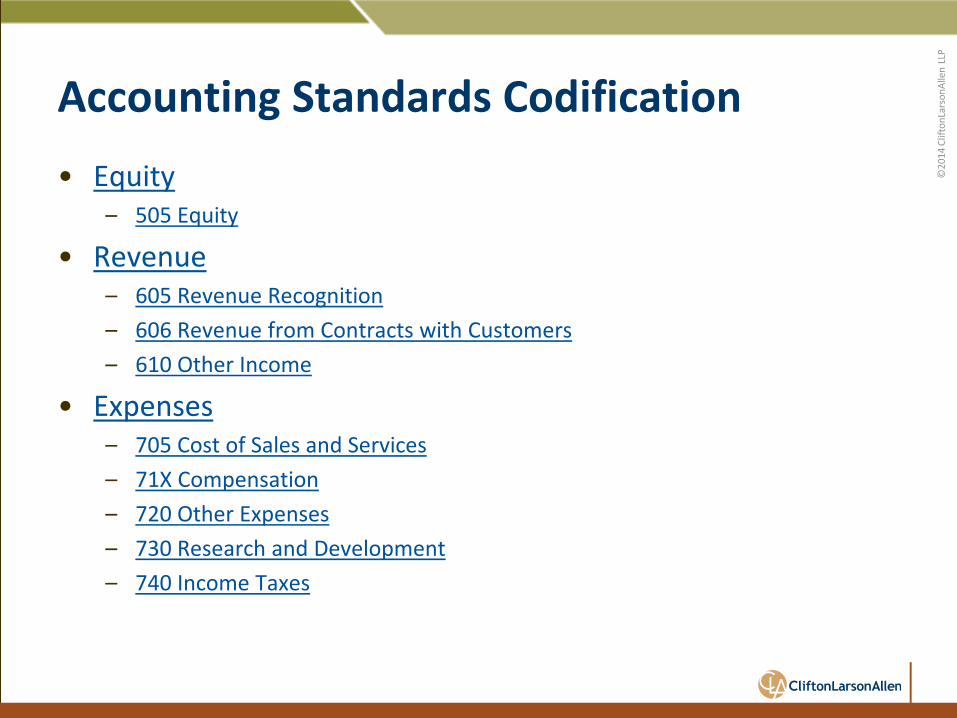

Accounting Standards Codification • Equity

– 505 Equity

• Revenue – 605 Revenue Recognition – 606 Revenue from Contracts with Customers – 610 Other Income

• Expenses – 705 Cost of Sales and Services – 71X Compensation – 720 Other Expenses – 730 Research and Development – 740 Income Taxes

©20

14 C

lifto

nLar

sonA

llen

LLP

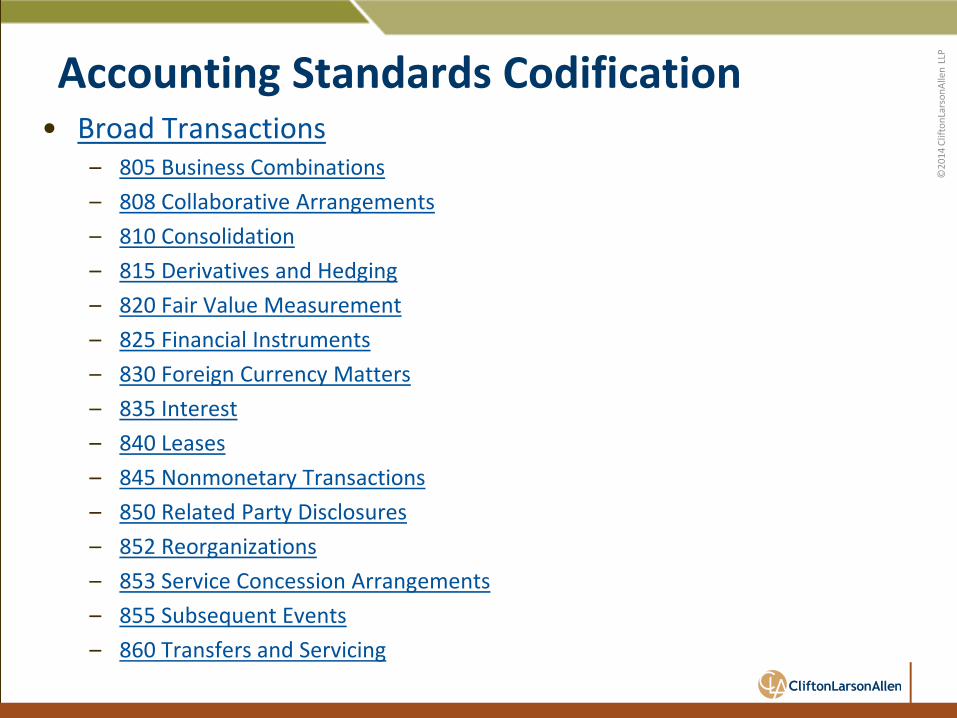

Accounting Standards Codification • Broad Transactions

– 805 Business Combinations – 808 Collaborative Arrangements – 810 Consolidation – 815 Derivatives and Hedging – 820 Fair Value Measurement – 825 Financial Instruments – 830 Foreign Currency Matters – 835 Interest – 840 Leases – 845 Nonmonetary Transactions – 850 Related Party Disclosures – 852 Reorganizations – 853 Service Concession Arrangements – 855 Subsequent Events – 860 Transfers and Servicing

©20

14 C

lifto

nLar

sonA

llen

LLP

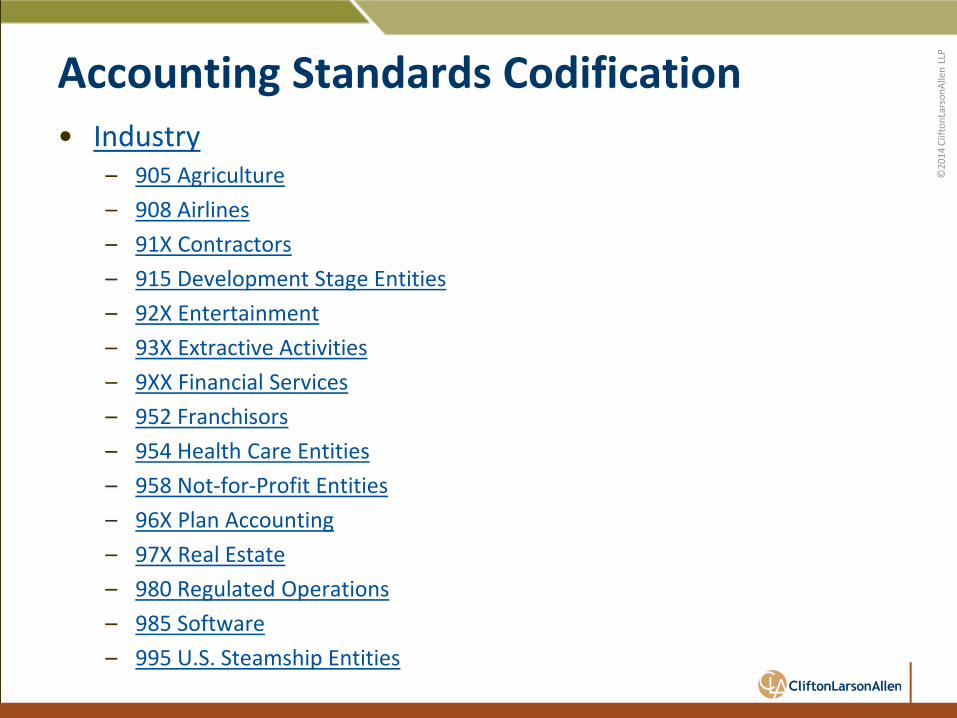

Accounting Standards Codification • Industry

– 905 Agriculture – 908 Airlines – 91X Contractors – 915 Development Stage Entities – 92X Entertainment – 93X Extractive Activities – 9XX Financial Services – 952 Franchisors – 954 Health Care Entities – 958 Not-for-Profit Entities – 96X Plan Accounting – 97X Real Estate – 980 Regulated Operations – 985 Software – 995 U.S. Steamship Entities

©20

14 C

lifto

nLar

sonA

llen

LLP

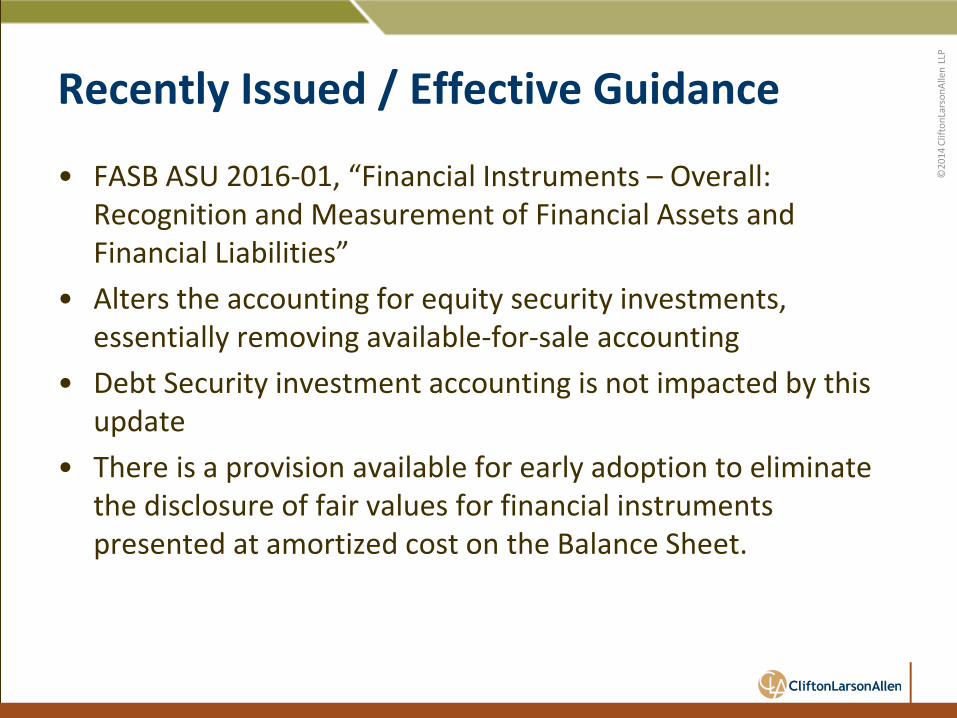

Recently Issued / Effective Guidance

• FASB ASU 2016-01, “Financial Instruments – Overall: Recognition and Measurement of Financial Assets and Financial Liabilities”

• Alters the accounting for equity security investments, essentially removing available-for-sale accounting

• Debt Security investment accounting is not impacted by this update

• There is a provision available for early adoption to eliminate the disclosure of fair values for financial instruments presented at amortized cost on the Balance Sheet.

©20

14 C

lifto

nLar

sonA

llen

LLP

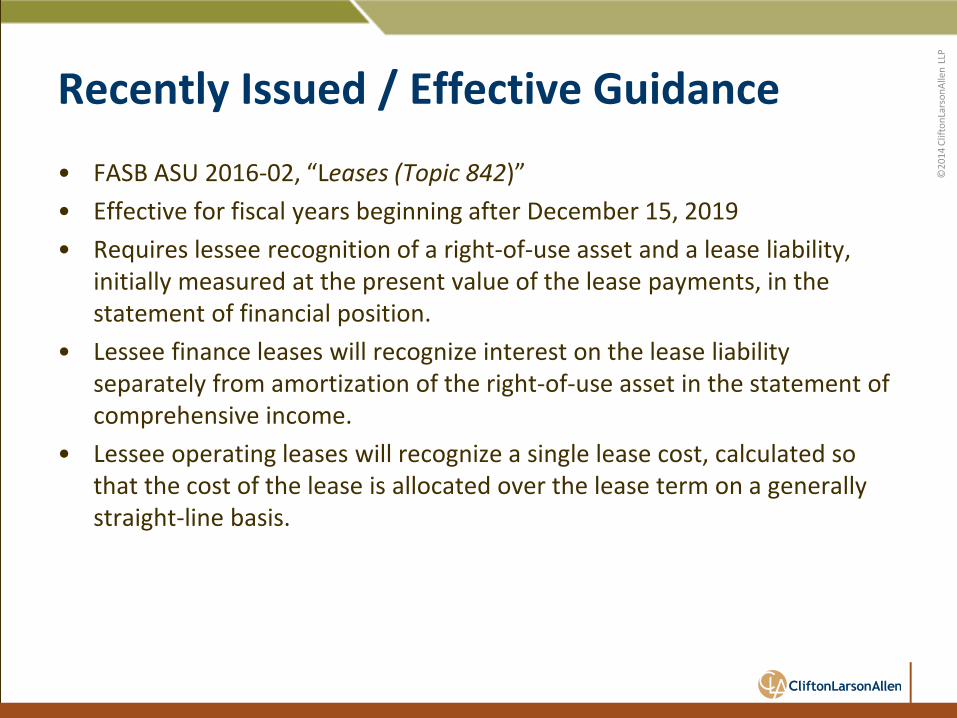

Recently Issued / Effective Guidance

• FASB ASU 2016-02, “Leases (Topic 842)” • Effective for fiscal years beginning after December 15, 2019 • Requires lessee recognition of a right-of-use asset and a lease liability,

initially measured at the present value of the lease payments, in the statement of financial position.

• Lessee finance leases will recognize interest on the lease liability separately from amortization of the right-of-use asset in the statement of comprehensive income.

• Lessee operating leases will recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term on a generally straight-line basis.

©20

14 C

lifto

nLar

sonA

llen

LLP

Recently Issued / Effective Guidance

• ASU No. 2014-14, “Receivables—Troubled Debt Restructurings by Creditors (Subtopic 310-40), Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure”

• The amendments clarify when an in-substance repossession or foreclosure occurs, and require disclosure of both the amount of foreclosed residential real estate property held by a creditor and the recorded investment in consumer mortgage loans collateralized by residential real estate property that are in the process of foreclosure according to local requirements of the applicable jurisdiction.

©20

14 C

lifto

nLar

sonA

llen

LLP

Current Projects and Expected Updates

• Current Expected Credit Loss model – expected Q2 2016

• Simplification of Equity Method Accounting – initial deliberations

©20

14 C

lifto

nLar

sonA

llen

LLP

Polling Question

• What best describes your plan of preparation (or for the majority of credit unions you audit or regulate) for the forthcoming standard credit losses? a) Followed the issue closely and prepared an estimate of

the impact on the institution b) Are aware of the issue and plan to begin preparation in

2016 when a final standard is issued c) Will deal with it when our accounting firm gives us some

guidance d) Who is the CECL guy and how is he involved?

©20

14 C

lifto

nLar

sonA

llen

LLP

Private Company Council (PCC)

• The PCC is an advisory body for FASB on private company matters

• PCC recommends alternative accounting treatments for private companies

• Private Company Financial Reporting – Private company framework – Definition of a Public Business Entity (ASU 2013-12) – Goodwill Amortization (ASU 2014-02) – Interest Rate Swaps (ASU 2014-03) – Variable Interest Entities (VIEs) in Leasing Arrangements

(ASU 2014-07)

©20

14 C

lifto

nLar

sonA

llen

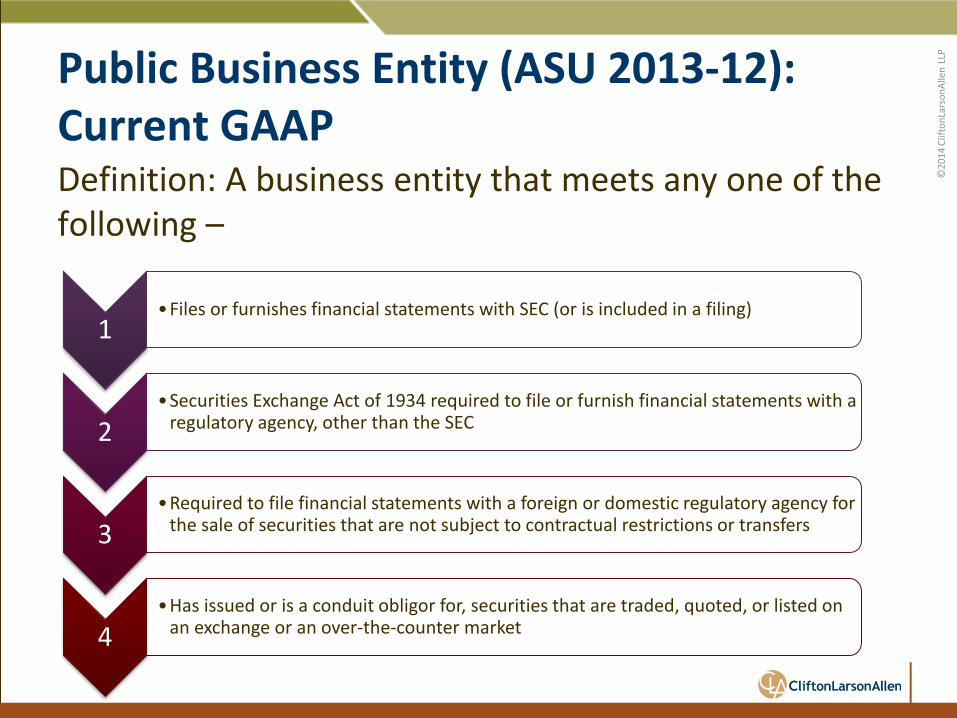

LLP Public Business Entity (ASU 2013-12):

Current GAAP Definition: A business entity that meets any one of the following –

1 •Files or furnishes financial statements with SEC (or is included in a filing)

2 •Securities Exchange Act of 1934 required to file or furnish financial statements with a

regulatory agency, other than the SEC

3 •Required to file financial statements with a foreign or domestic regulatory agency for

the sale of securities that are not subject to contractual restrictions or transfers

4 •Has issued or is a conduit obligor for, securities that are traded, quoted, or listed on

an exchange or an over-the-counter market

©20

14 C

lifto

nLar

sonA

llen

LLP

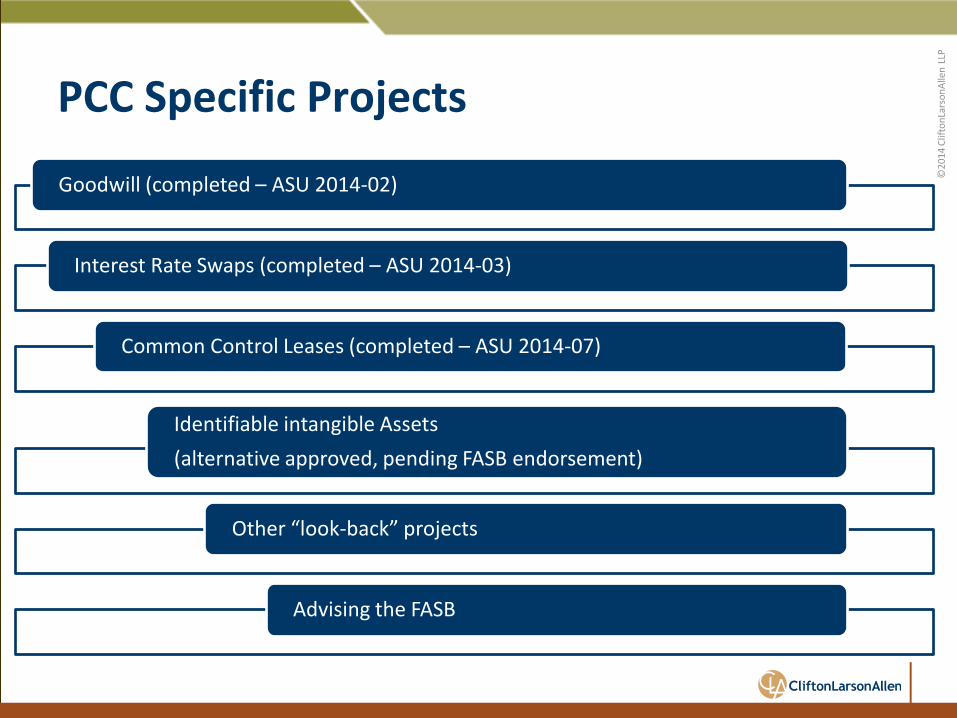

PCC Specific Projects

Goodwill (completed – ASU 2014-02)

Interest Rate Swaps (completed – ASU 2014-03)

Common Control Leases (completed – ASU 2014-07)

Identifiable intangible Assets (alternative approved, pending FASB endorsement)

Other “look-back” projects

Advising the FASB

©20

14 C

lifto

nLar

sonA

llen

LLP

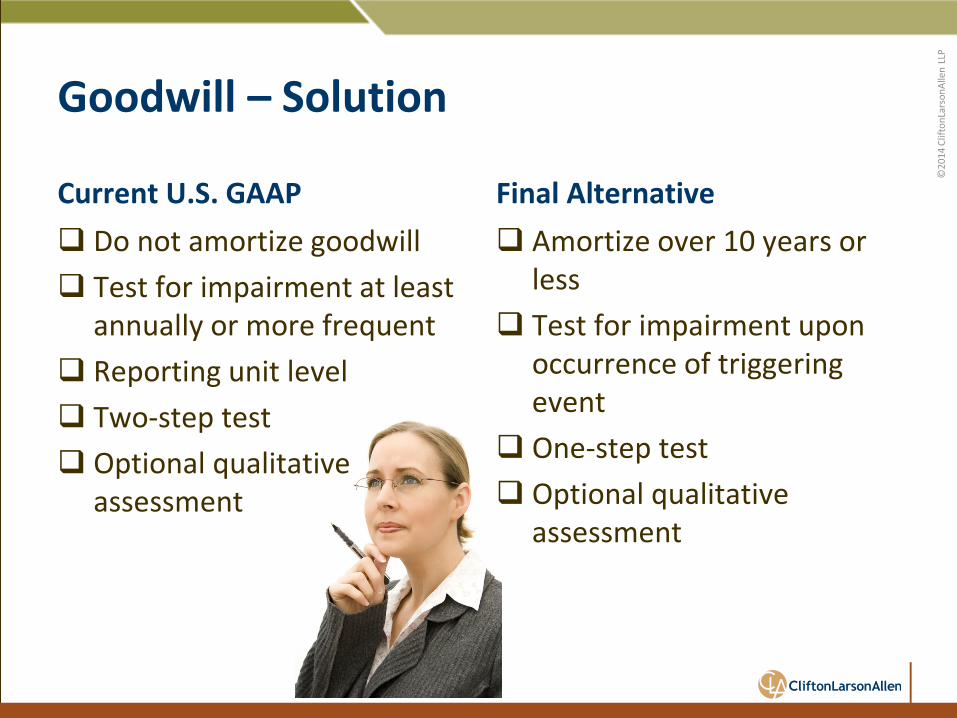

Current U.S. GAAP Do not amortize goodwill Test for impairment at least

annually or more frequent Reporting unit level Two-step test Optional qualitative

assessment

Final Alternative Amortize over 10 years or

less Test for impairment upon

occurrence of triggering event

One-step test Optional qualitative

assessment

Goodwill – Solution

©20

14 C

lifto

nLar

sonA

llen

LLP

Goodwill – Benefits of Alternative

• Significant cost savings for many private companies that carry goodwill on their balance sheet

• Amortization reduces likelihood of impairments, private companies will test goodwill for impairment less frequently

©20

14 C

lifto

nLar

sonA

llen

LLP

PCC Advising on FASB Projects

• Revenue recognition • Going concern • Reporting discontinued operations • Leases • Accounting for financial instruments • Government assistance disclosures • Pushdown accounting (AITF) • Simplification initiative • Disclosure framework: Disclosure reviews

©20

14 C

lifto

nLar

sonA

llen

LLP

True or False: Credit Unions are categorized as Not-for-Profits according to

Generally Accepted Accounting Principles.

Polling Question

©20

14 C

lifto

nLar

sonA

llen

LLP

56

©20

14 C

lifto

nLar

sonA

llen

LLP

CLAconnect.com

twitter.com/ CLAconnect

facebook.com/ cliftonlarsonallen

linkedin.com/company/ cliftonlarsonallen

Craig Brogan, CPA Principal (301) 902-8566 [email protected] Chuck Kelly, CPA Senior Manager (410) 308-8076 [email protected]